San Jose, Costa Rica, 18 septiembre, 2013

Alejandro Alvarez de la Campa

Global Product Leader STCR

Secured Transactions and Collateral

Registries Program

Access to Finance, IFC

1. Definition of Secured Transactions

2. Why are Secured Transactions Important?

Why are they important in Latin America and

the Caribbean?

4. IFC’s Approach to Secured Transactions

Reform

5. Global Portfolio and Impact in Reforming

Jurisdictions

6. Reform challenges and lessons learned

OUTLINE

1. Definition of

Secured

Transactions

Legal and institutional framework to facilitate the use of movable property as collateral for both business and consumer credit

Bank Accounts Inventory and raw goods

Vehicles Industrial and agricultural

equipment Durable consumer

goods Agricultural products (crops,

livestock, fish farm)

Intellectual Property

rights

Accounts receivable

Secured Transactions Systems

2. Why are Secured Transactions

Important? Why are they important

in Latin America and the

Caribbean?

SME Finance Gap

6

SME FINANCE GAP IN LATIN AMERICA & CARIBBEAN

Source: McKinsey & Co. Global Financial Inclusion Practice

Between US$ 125-155 Billion

SME Finance Gap: value of collateral (in %)

needed for a loan in Latin America and Caribbean

Collateral Gap

Source: World Bank Enterprise Surveys

Mismatch between assets owned by companies and

collateral required

44%

34%

22%

Vehicles/machinery/equipmentAccounts Receivable

Land / Real Estate

73%

27%

Land / Real Estate Movable property

Capital Stock of Firms Collateral Taken by FIs

•BENEFITS OF A SOLID SECURED TRANSACTIONS SYSTEM

9

• Promotes Credit Diversification

• Increases Market Competition

• Reduces the Cost of Credit

• Increases Access to Credit Reducing the Risk of Credit - Underserved

MSMEs & women entrepreneurs

- Promotes risk management, prudent lending

-

- Better interest rates - Move from informal to formal financing

- Cost savings for businesses

- Credit risk diversification: immovable and movable

- Sector diversification in the portfolio

- Development of industries (factoring and leasing)

- NBFIs

Benefits of a solid Secured Transactions System

Variable Effect

Access to finance 8 percentage points

Access to a loan 7 percentage points

% of working capital

financed by banks

10 percentage points

Interest rates 3 percentage points

Loan maturity 6 months

10

Study also provides evidence that the impact of the introduction of movable

registries on firms’ access to finance is larger among smaller firms, who also

report a reduction in subjective, perception-based measure of finance

obstacles.

Evidence/results from first study that provides

empirical evidence about the impact of

collateral registries on:

Why are financial institutions not willing to take movable

property as collateral?

Restrictions on types of

assets

Lack of clear creditor

priority

Enforcement issues

Lack adequate legal

framework

Lack registry of

security interests in

movables

Dysfunctional Registry/

No Registry

Lack of publicity

No transparency

No experience with this

type of financing

Do not have staff with

necessary skills

Lack know how on

movable asset

lending

Not their type of

business

No competition in the

lending markets

Revenue from other

sources (TB)

Lack interest

3. How does IFC

implement this

work?

13

INTERNATIONAL ACCEPTED STANDARDS

UNCITRAL Registry Guide and Legislative

Guide on Secured Transactions

World Bank Principles on Insolvency and

Creditors Rights

IFC Guide on Secured Transactions and

Collateral Registries

OAS Model Law

LEGAL STANDARDS FOR AN EFFECTIVE SECURED

TRANSACTIONS SYSTEM

14

Effective Secured

Transactions System

Broad scope

Creation

Publicity / registration

Priority

Enforcement

KEY FEATURES OF A MODERN

COLLATERAL REGISTRY

1. Centralized on-line

2. For all types of security interests

in movables

3. Registration by creditors

4. Notice based registry (no

documentation)

5. Public search available to all

6. Reasonable flat fees

7. Limited role of registrar in

verification

8. Security and data back up

9. No cash payments

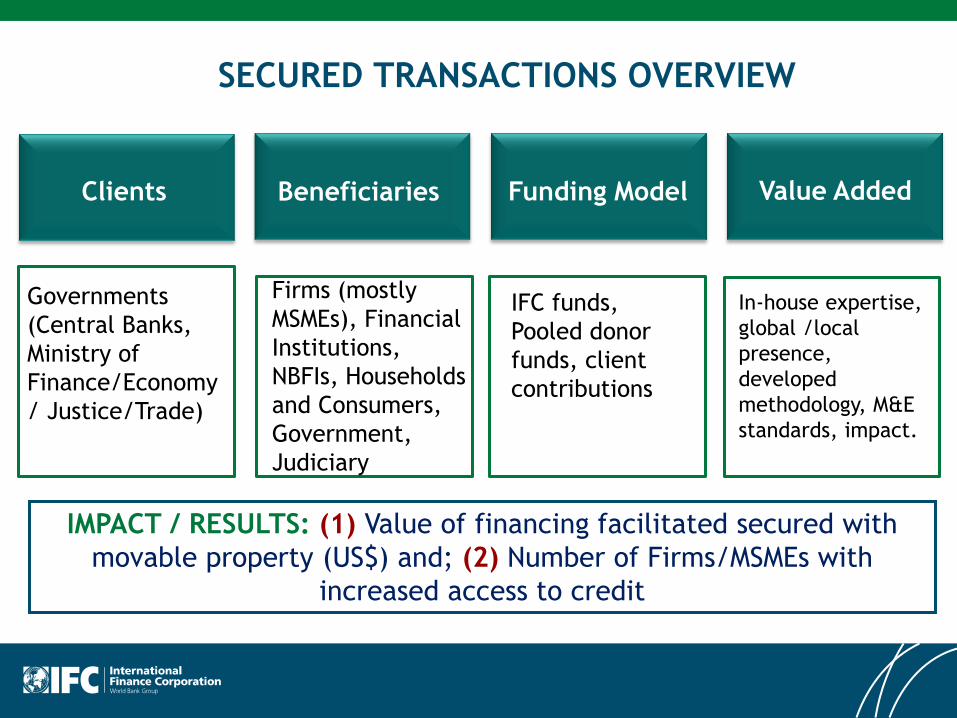

IMPACT / RESULTS: (1) Value of financing facilitated secured with

movable property (US$) and; (2) Number of Firms/MSMEs with

increased access to credit

Clients

Governments

(Central Banks,

Ministry of

Finance/Economy

/ Justice/Trade)

Beneficiaries

Firms (mostly

MSMEs), Financial

Institutions,

NBFIs, Households

and Consumers,

Government,

Judiciary

Funding Model

IFC funds,

Pooled donor

funds, client

contributions

Value Added

In-house expertise,

global /local

presence,

developed

methodology, M&E

standards, impact.

SECURED TRANSACTIONS OVERVIEW

• Building the Capacity of

Stakeholders

• Monitoring Impact & Communications

• Creation of Electronic Registry

• Legal and Regulatory Framework

1. Create Committee

2. Draft new Secured Transactions Law

3. Raise awareness

4. Submit Law to Parliament

5. Draft registry regulations

1. Determine Government Agency to host registry

2. Develop technical specifications

3. Hardware & software procurement

4.Training/awareness

5. Launching of registry

1. Training and awareness raising stakeholders (public & private stakeholders), including law and registry

2. Training on movable asset financing for Financial Institutions

1. Develop monitoring & evaluation plan including baseline information

2. Conduct periodic monitoring of impact through registry indicators & surveys

3. Communications

1 2

4 3

BUSINESS AND DELIVERY MODEL

Toolkits Impact evaluation

Network Building

Publications

Program Highlights- Knowledge Management

Knowledge Sharing

Surveys

Factsheets Events – Peer

learning

4. Global

Portfolio and

Results

20

AFRICA

Ghana

Liberia

Malawi

Rwanda

Zambia

MENA

AMF

Afghanistan

Jordan

Lebanon

UAE

West Bank &

Gaza

EAST ASIA & PACIFIC

Cambodia

China

Lao PDR

Mongolia

Philippines

Vietnam

SOUTH ASIA

India

Bangladesh

Sri Lanka

ECA

Azerbaijan

Belarus

Uzbekistan

LAC

Colombia

Costa Rica

Haiti

Pipeline Nigeria, Sierra Leone, Indonesia, Egypt, Morocco, Tajikistan, etc

CURRENT REGIONAL PORTFOLIO

CHINA VIETNAM GHANA

IMPACT OF SECURED TRANSACTIONS REFORMS IN

AFRICA AND EAST ASIA

GHANA

Ghana video:

http://www.youtube.com/watch?v=5c84WF02_IY

Impact of Secured Transaction Reform

in East Asia

- Law reform (2007) and new centralized online registry for

accounts receivables and leasing (2008)

- Project has led to more than US$ 3.5 trillion in financing secured

with receivables, mostly to SMEs (around 60% of the loans)

- More than 70,000 SMEs have received loans

- Project has led to the development of the factoring and leasing

industries

China

Impact of Secured Transaction Reform in

East Asia

- Law reform and new centralized online registry for movable

assets launched in March 2012.

- After 1 year of operation of the new registry, 103,000 new loans for

a value of $600 million have been registered and 212,000 searches

conducted

- It is estimated that around 54,000 SMEs have received loans

VIETNAM

24

5. Reform challenges

and lessons learned

Partner with a strong institution with strong political clout.

Build consensus among stakeholders. Takes time 1

Public and private commitment is critical: government counterpart

commitment and a dynamic and supportive financial sector 2

Local ownership is key: client monetary or in-kind contributions;

local software solutions and IT support strengthen client ownership

and sustainability 3

LESSONS LEARNED

Position reforms as a “transformation of the credit market”. 4

Sustain effort with a professional team over time merging local

knowledge with global subject-matter expertise. 5

Alejandro Alvarez de la Campa

Global Product Leader, IFC Secured Transactions

THANK YOU