Sales Tax Audits in the Era

of Digital Documentation Preparing for a Computer-Based Review Involving Electronic Invoices, Bills of Lading, Etc.

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Please refer to the instructions emailed to the registrant for the dial-in information.

Attendees can still view the presentation slides online. If you have any questions, please

contact Customer Service at 1-800-926-7926 ext. 10.

THURSDAY, JANUARY 31, 2013

Presenting a live 110-minute teleconference with interactive Q&A

Mark L. Stone, Managing Partner, Sales Tax Defense LLC, Deer Park, N.Y.

Adam Rupp, Manager, Ryan, Philadelphia

Andrew Sabol, Property Tax Administrator, Tax Technology Services LLC, Raleigh, N.C.

For this program, attendees must listen to the audio over the telephone.

Tips for Optimal Quality

Sound Quality

Call in on the telephone by dialing 1-866-873-1442 and enter your PIN when

prompted.

If you have any difficulties during the call, press *0 for assistance. You may also

send us a chat or e-mail [email protected] immediately so we can address

the problem.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

Continuing Education Credits

Attendees must stay on the line throughout the program, including the Q & A

session, in order to qualify for full continuing education credits. Strafford is

required to monitor attendance.

Record verification codes presented throughout the seminar. If you have not

printed out the “Official Record of Attendance”, please print it now. (see

“Handouts” tab in “Conference Materials” box on left-hand side of your computer

screen). To earn Continuing Education credits, you must write down the

verification codes in the corresponding spaces found on the Official Record of

Attendance form.

Please refer to the instructions emailed to the registrant for additional

information. If you have any questions, please contact Customer Service

at 1-800-926-7926 ext. 10.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides and the Official Record of Attendance for today's program.

• Double-click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Sales Tax Audits in the Era of Digital Documentation Seminar

Mark Stone, Sales Tax Defense LLC

Jan. 31, 2013

Andrew Sabol, Tax Technology Services LLC

Adam Rupp, Ryan

Today’s Program

Introduction

[Andrew Sabol]

Examples Of State Electronic Audit Rules

[Andrew Sabol]

Practical Issues For Corporate Taxpayers

[Mark Stone]

Planning For And Managing An E-Audit, As The Taxpayer

[Mark Stone]

Client Experiences With Electronic Sales Tax Audits

[Adam Rupp]

Slide 8 – Slide 17

Slide 38 – Slide 39

Slide 40 – Slide 43

Slide 18 – Slide 27

Slide 28 – Slide 37

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

7

INTRODUCTION

Andrew Sabol, Tax Technology Services LLC

Audit Sampling

All states that impose sales and use tax provide for some type of sampling of data in performance of audits.

Authority for sampling varies between statutory and administrative.

Revenue laws in most states give the tax agency the authority to base an assessment on the best information available.

9

Audit Sampling (Cont.)

Approximately half the states enter into written agreements establishing the applicable sample methodology; however, not all agreements are binding.

Sampling is most frequently used for sales and for purchases of expense items; all fixed assets for an audit period may be reviewed.

10

Manual Audits

Prior to the widespread use of computers, the most typical sampling method was some form of block sample.

An auditor undertook a physical review of all the sales/purchases within a selected period (usually several months) and projected a percentage of error for the entire audit period.

Block sampling procedures are typically less formalized.

11

Slide Intentionally Left Blank

Manual Audits (Cont.)

There is less likely to be documentation establishing sample size and population prior to the audit.

For larger audits, an auditor was usually required to visit a company’s location and might be on-site for an extended period of time.

A taxpayer might have to address issues such as finding work space for the auditor, providing access to records, providing access to personnel, and providing equipment to access electronically stored information.

13

Electronic Audits

Company and tax agency usually agree on the elements of sample prior to the examination.

Statistical sampling is commonly used.

Data is initially transmitted remotely or via storage media to the tax agency.

The auditor may still make an on-site visit to review operations, and might have to visit a company location to access the documents agreed to be reviewed once the data is processed.

14

Electronic Audits (Cont.)

If back-up documentation is digitized, the tax agency may allow electronic transmission of this data, further reducing the presence of agency personnel.

States generally will have personnel dedicated to administering computer-assisted audits. These personnel are usually responsible for processing data and do not take part in the taxation review.

15

Advantages

Statistical sampling is a more reliable and objective measure than block sampling of establishing tax liability.

Quicker completion of audits benefit a company and the tax agency.

A tax agency official spends less time at a company’s location.

16

Advantages (Cont.)

A written agreement is evidence, if an appeal occurs.

A company still retains the ability to object to an assessment, although it may not be able to dispute agreed-upon sampling parameters.

17

EXAMPLES OF STATE ELECTRONIC AUDIT RULES

Andrew Sabol, Tax Technology Services LLC

State-Specific: California

California publishes an audit manual that has a chapter (13) devoted to computer-assisted audits.

A company is encouraged to interact with audit staff in the development of the sampling plan.

An auditor is to take into account underpayments and overpayments.

Form BOE-472, Audit Sampling Plan, is used to document the sampling plan and set the audit criteria.

19

Slide Intentionally Left Blank

State-Specific: Texas

Texas publishes a brochure with information for conducting computer-assisted audits, and a sampling manual.

Two programs in place: CAMS-Mainframe and CAMS-PC.

CAMS-Mainframe is a traditional electronic program for large numbers or records, when data is transmitted or sent to the agency.

21

State-Specific: Texas (Cont.)

CAMS-PC is a program installed on an auditor’s computer and that allows the auditor to run the program. It is designed for smaller numbers of records.

Included in the records used are the following: General ledger detail files, purchasing data files, sales invoice detail files and vendor/customer master files.

22

State-Specific: Illinois

Illinois publishes Publication 107, Electronic Records and Computer Assisted Auditing.

The revenue agency will review a company’s electronic records to evaluate eligibility for an electronic audit.

Agency may conduct a system integrity audit to attain an acceptable level of confidence in the EDI process.

23

State-Specific: Illinois (Cont.)

The revenue agency and taxpayer will conduct a conference to establish an audit plan. The agency then will conduct a computer system review, and there will be an overview of the sampling guidelines and techniques.

24

State-Specific: Massachusetts

Massachusetts publishes a Guide to Computer Assisted Audit Techniques.

The revenue agency uses a computer audit questionnaire to gather information needed to conduct the audit.

Agency uses storage media and secure e-mail to transmit data.

25

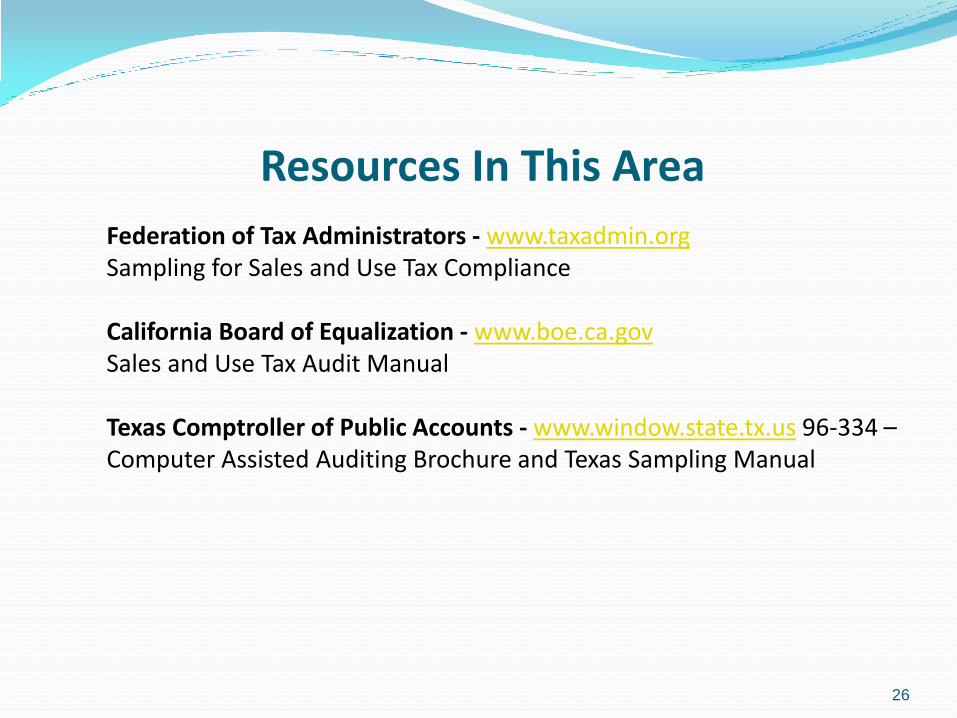

Federation of Tax Administrators - www.taxadmin.org Sampling for Sales and Use Tax Compliance California Board of Equalization - www.boe.ca.gov Sales and Use Tax Audit Manual Texas Comptroller of Public Accounts - www.window.state.tx.us 96-334 – Computer Assisted Auditing Brochure and Texas Sampling Manual

Resources In This Area

26

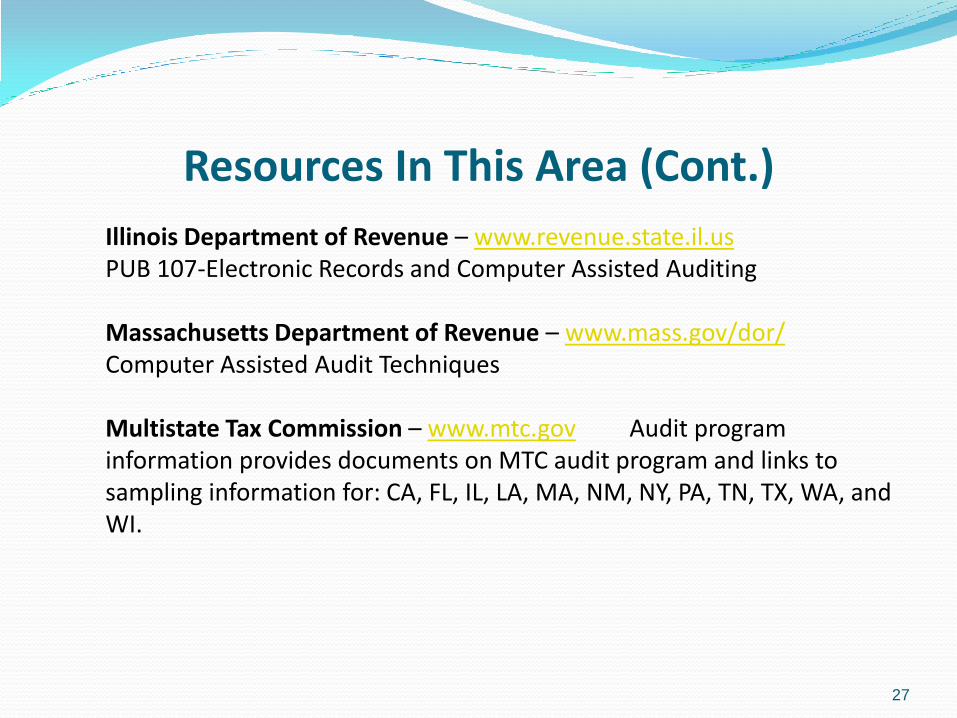

Resources In This Area (Cont.)

Illinois Department of Revenue – www.revenue.state.il.us PUB 107-Electronic Records and Computer Assisted Auditing Massachusetts Department of Revenue – www.mass.gov/dor/ Computer Assisted Audit Techniques Multistate Tax Commission – www.mtc.gov Audit program information provides documents on MTC audit program and links to sampling information for: CA, FL, IL, LA, MA, NM, NY, PA, TN, TX, WA, and WI.

27

PRACTICAL ISSUES FOR CORPORATE TAXPAYERS

Mark Stone, Sales Tax Defense LLC

Acceptable Digital Formats

I. What format should my records be in?

A. Do I need to keep hard copies as well as electronic

records?

B. Types of records that I need to keep

1. Purchase records

2. Miscellaneous records

3. Informational records

4. Other documents

29

Slide Intentionally Left Blank

Data Integrity Tests

I. How do I ensure that my data are safe?

A. Data back-up options

1. Remote back-up to a server or hard drive

2. Use a back-up service via the cloud, such as IBM

SmartCloud

B. Benefits of backing up data

1. Data is stored in multiple locations, preventing loss due

to theft or natural disasters.

2. Data can be accessed from any Internet-connected

computer.

3. The data automatically are backed up; there is nothing

extra you would need to do,

31

Records Confidentiality And Access Provisions

I. What is being done to protect my information?

A. Are there laws that ensure the privacy of my data?

B. Federal audit

C. IRS rules regarding privacy

II. State audits

A. State laws regarding privacy

B. Who has access to my records?

32

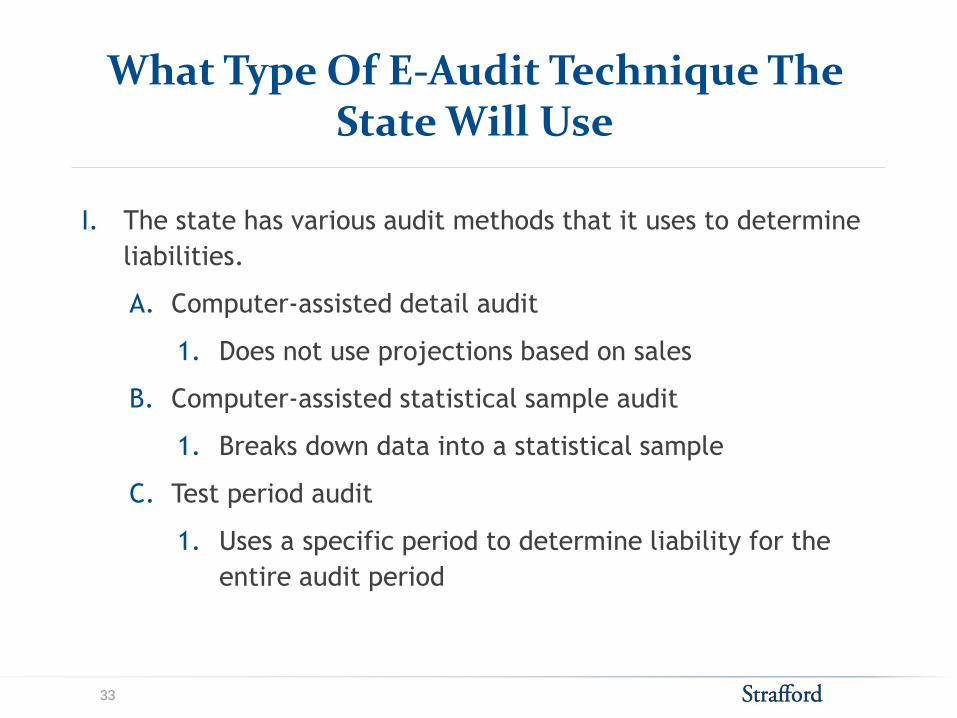

What Type Of E-Audit Technique The State Will Use

I. The state has various audit methods that it uses to determine

liabilities.

A. Computer-assisted detail audit

1. Does not use projections based on sales

B. Computer-assisted statistical sample audit

1. Breaks down data into a statistical sample

C. Test period audit

1. Uses a specific period to determine liability for the

entire audit period

33

Detail Audit Vs. Statistical Sample Vs. Test Period Audit

A. Computer-assisted detail audit

1. Examines all records for the audit period

2. Information needed for the detailed audit

3. Advantages and disadvantages to this type of audit

B. Computer-assisted statistical sample audit

1. This audit method is generally used for audits of expense purchases,

but may be used for capital assets or other areas.

2. Uses a random sample of transactions to determine liability

3. Advantages and disadvantages to this type of audit

C. Test period audit

1. Uses a specific period within the audit to determine liability for

entire audit

2. Advantages and disadvantages to this type of audit

34

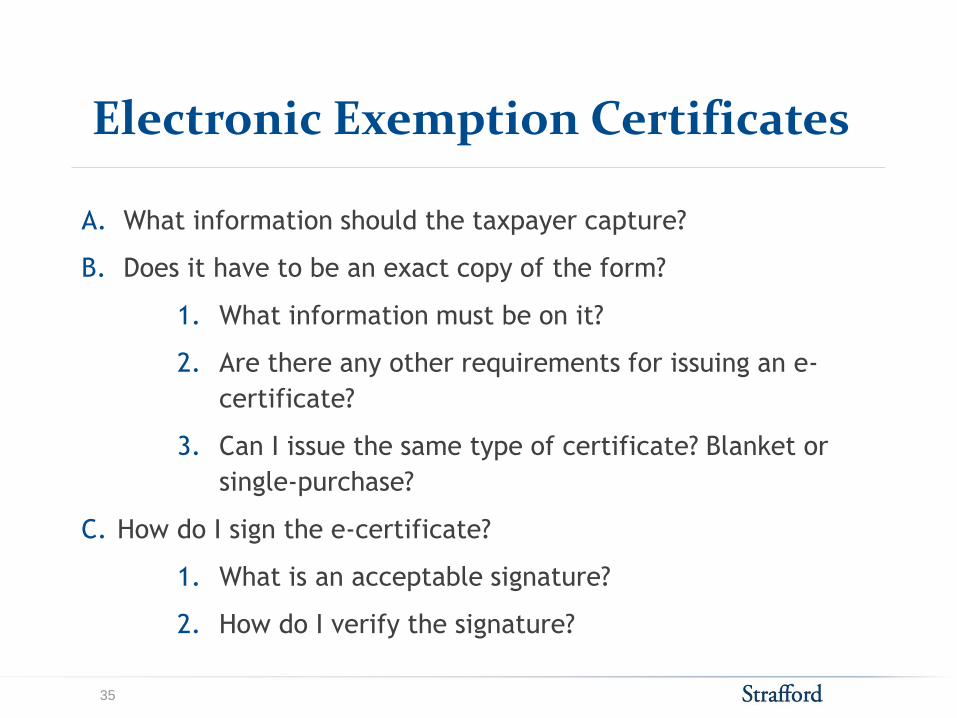

Electronic Exemption Certificates

A. What information should the taxpayer capture?

B. Does it have to be an exact copy of the form?

1. What information must be on it?

2. Are there any other requirements for issuing an e-

certificate?

3. Can I issue the same type of certificate? Blanket or

single-purchase?

C. How do I sign the e-certificate?

1. What is an acceptable signature?

2. How do I verify the signature?

35

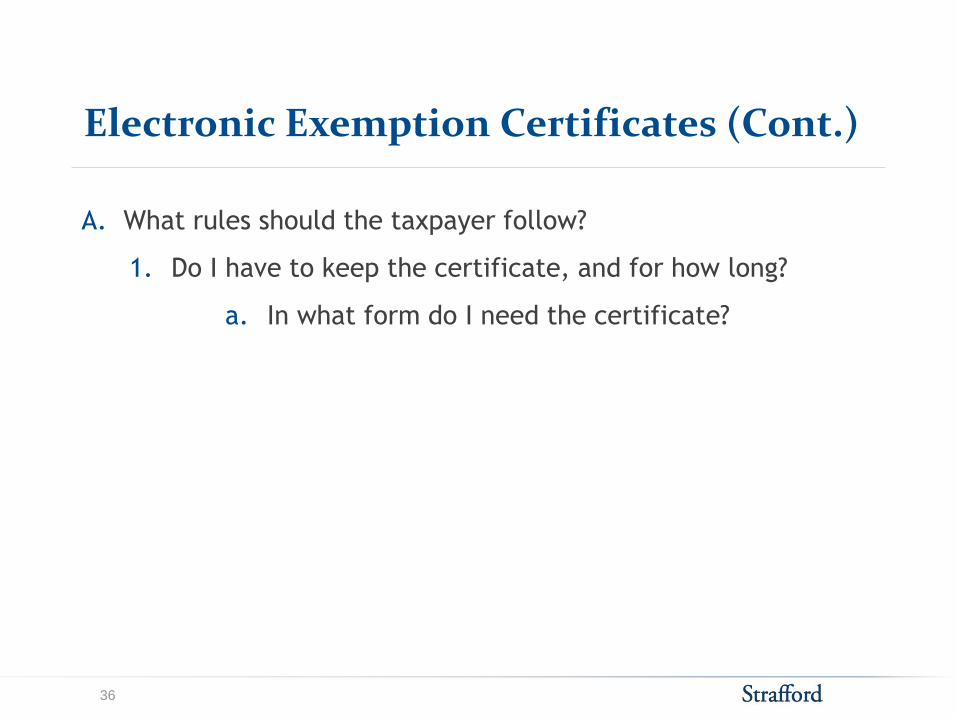

Electronic Exemption Certificates (Cont.)

A. What rules should the taxpayer follow?

1. Do I have to keep the certificate, and for how long?

a. In what form do I need the certificate?

36

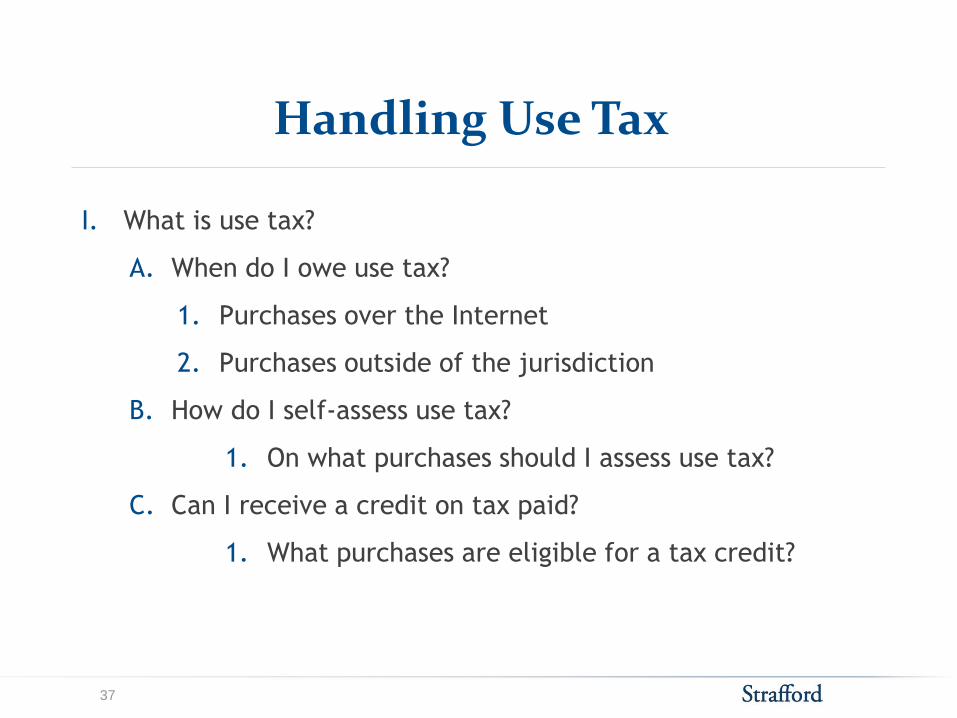

Handling Use Tax

I. What is use tax?

A. When do I owe use tax?

1. Purchases over the Internet

2. Purchases outside of the jurisdiction

B. How do I self-assess use tax?

1. On what purchases should I assess use tax?

C. Can I receive a credit on tax paid?

1. What purchases are eligible for a tax credit?

37

PREPARING FOR AND MANAGING AN E-AUDIT, AS THE TAXPAYER

Mark Stone, Sales Tax Defense LLC

A Review Of Issues To Anticipate In Audit Planning

I. What if I am missing records?

A. Incomplete or invalid exemption certificates

1. Can I go back and get the correct form?

B. Bank deposits in excess of sales

1. Comparing income tax returns to sales and use tax

returns

C. Responsible person assessment

1. What makes someone a responsible person for the

business?

D. Penalties and interest

1. Can penalties be abated?

39

CLIENT EXPERIENCES WITH ELECTRONIC SALES TAX AUDITS

Adam Rupp, Ryan

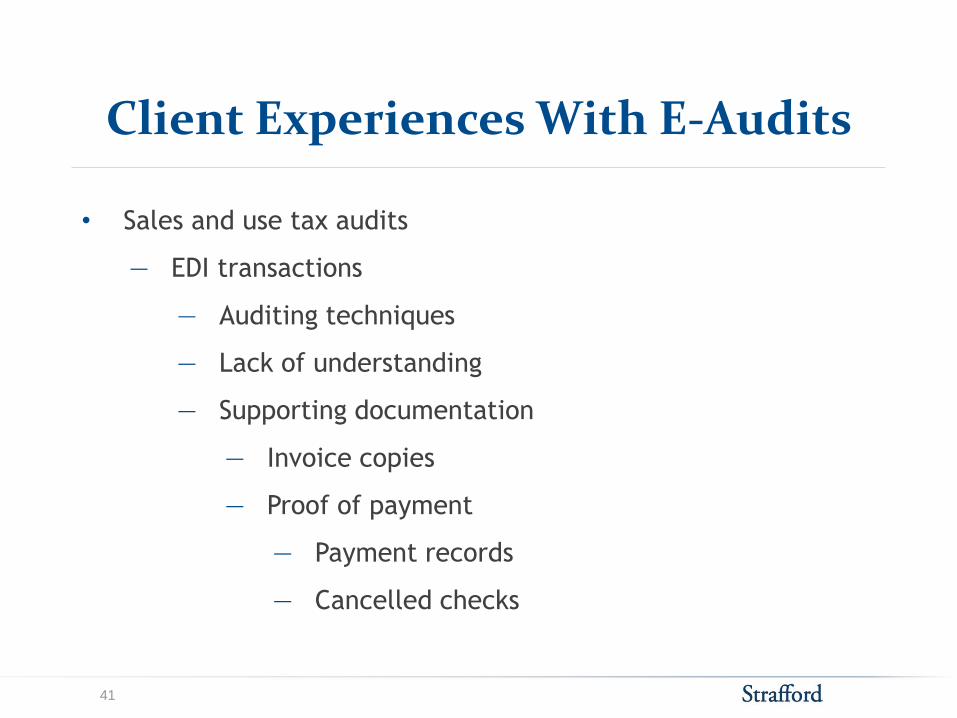

Client Experiences With E-Audits

• Sales and use tax audits

― EDI transactions

― Auditing techniques

― Lack of understanding

― Supporting documentation

― Invoice copies

― Proof of payment

― Payment records

― Cancelled checks

41

Slide Intentionally Left Blank

Client Experiences With E-Audits (Cont.)

• Sales and use tax audits (Cont.)

― Specific state experiences

― Michigan

― Missouri

― Florida

43