SYNOPSIS OF Ph.D. THESIS ENTITLED

RISK MANAGEMENT IN LIFE INSURANCE WITH EMPHASIS ON LIFE INSURANCE FRAUD

SUBMITTED TO

KADI SARVA VISHWAVIDYALAYA,

GANDHINAGAR, GUJARAT, INDIA

FOR THE DEGREE OF

DOCTOR OF PHILOSOPHY (Ph.D)

IN

MANAGEMENT

BY

DHARA CHUDGAR

UNDER THE SUPERVISION OF

DR. ANJANI KUMAR ASTHANA

Institute of Cooperative Management, Bhopal

JUNE, 2015

SYNOPSIS OF Ph.D. THESIS ENTITLED

RISK MANAGEMENT IN LIFE INSURANCE WITH EMPHASIS ON LIFE INSURANCE FRAUD

SUBMITTED TO : KADI SARVA VISHWAVIDYALAYA, GANDHINAGAR, GUJARAT, INDIA.

: MANAGEMENT

: FINANCE

: DHARA JITENDRA CHUDGAR

: DR. ANJANI KUMAR ASTHANA

: 11E0342

FACULTY

SUBJECT

RESEARCH STUDENT

RESEARCH GUIDE

REGISTRATION NO.

DATE OF REGISTRATION : 04/10/2011

SIGN OF GUIDE

SIGN OF STUDENT

DR. ANJANI KUMAR ASTHANA

RESEARCH SUPERVISOR

DHARA JITENDRA CHUDGAR

RESEARCH STUDENT

1

Contents

1 Introduction .............................................................................................................................................. 3

1.1 Research Background ........................................................................................................................ 3

1.2 Research Problem .............................................................................................................................. 4

1.3 Purpose of the study .......................................................................................................................... 4

1.4 Objectives .......................................................................................................................................... 5

2 Literature review ...................................................................................................................................... 6

2.1 Industry overview .............................................................................................................................. 6

2.2 Risk Management .............................................................................................................................. 6

2.3 Life Insurance fraud .......................................................................................................................... 7

2.3.1 Life Insurance fraud – Defined.............................................................................................. 7 2.3.2 Types of fraud........................................................................................................................ 9

2.4 Impact of fraud............................................................................................................................ 10

2.4.1 Economical impact of fraud ................................................................................................ 10

2.4.2 Fraud Detection and Prevention .......................................................................................... 11 2.4.3 Customer’s perception for fraud .......................................................................................... 13

3 Research Gap ...................................................................................................................................... 14

4 Research Methodology ........................................................................................................................... 15

4.1 Research Design: ........................................................................................................................ 15

4.2 Sampling Frame............................................................................................................................... 15

4.2.1 Sampling Technique ................................................................................................................. 15 4.2.2 Sample size ............................................................................................................................... 15

4.2.3 Sample selection procedure ...................................................................................................... 15 4.3 Data Collection Tools ................................................................................................................. 16

4.4 Mode of data collection .............................................................................................................. 16

4.5 Method for data analysis ............................................................................................................. 16

5 Data Analysis..................................................................................................................................... 17

5.1 Types of Fraud ................................................................................................................................. 19

5.2 Typical fraud categories .................................................................................................................. 19

5.2.1 Proposal Stage: Fraud ............................................................................................................... 21

5.2.2 Claims Stage: Fraud ................................................................................................................. 24 5.3 Control on Life Insurance fraud ...................................................................................................... 25

5.3.1 Discussion and Analysis ........................................................................................................... 25 5.3.2 Review existing fraud control mechanism ............................................................................... 26

5.4 Customer’s perception ..................................................................................................................... 29

5.4.1 Four drivers that contribute to fraudulent activity. ................................................................... 30 5.4.2 Four Expressions : Tolerance level of customers for life insurance fraud ............................... 31 5.4.3 Attitudes towards Industry ....................................................................................................... 32

5.4.4 Reasons for life insurance fraud ............................................................................................... 33

2

5.4.5 Ways insurance companies should prevent fraud .................................................................... 34

5.4.6 Punishments for life insurance fraud ........................................................................................ 34

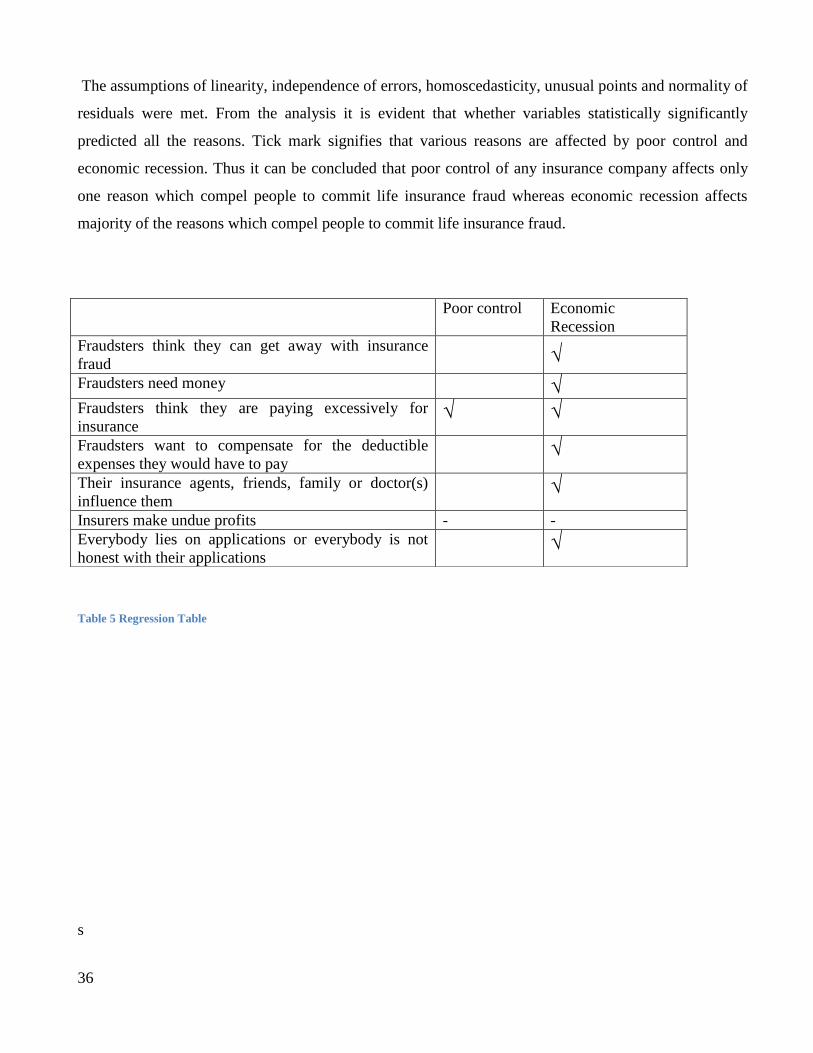

5.4.7 Factors affecting various reasons ........................................................................................ 35 6 Findings ................................................................................................................................................. 37

7 Suggestions ............................................................................................................................................ 42

8 Limitations ............................................................................................................................................. 44

9 Conclusion ............................................................................................................................................. 45

10 Further scope of Research ................................................................................................................... 47

References ................................................................................................................................................. 48

3

1 Introduction

1.1 Research Background

Risk Management has been acquiring monumental importance, especially over the last few years,

globally. Apart from the conventional areas that one has in mind with regard to risk management, there

is just no end to the challenges that emerge afresh from hitherto unknown areas. It is this dynamic nature

of business that puts an additional onus on risk management being thoroughly comprehensive. The

corporate world has been gearing itself up for these new challenges; and their risk management

strategies have been demonstrating the adoption of a wider coverage of business activity. As a natural

corollary, the risk management strategies of insurers would also need to take a fresh look at how they

are geared up for eventualities.

Risk Management is the process of measuring or assessing risk and then developing strategies to

manage the risk (George, 2003; Harringtion and Niehaus, 2004). Risk in life insurance could be

associated with sales, underwriting, medical network, claims, operations and finance. Risk management

is needed because of increasing instances of fraud, to have a framework in place to battle risk and fraud

issues, enhances company image, acts as a deterrent to frauds by its very existence and acts as a safety

net for the Organization.

There are various types of risks involved in life insurance which are discussed later; however the study

focuses on fraud risk. Instances of life insurance fraud are increasing since few years and therefore there

is a need to curtail life insurance fraud.

India is one of the fastest growing economies and so is the case with the country’s insurance sector. The

significant role that fraud plays negatively affects the insurance sector is often under-reported or

discounted. There is a general consensus in the market that fraud cases have been significantly

increasing. Frauds increase the cost of insurance, resulting in insurers losing to their competitors, and at

the same time, the policyholders end up paying higher premiums. As India’s insurance industry matures,

fraud risk management is going to be a major concern for insurers and business leaders. Insurers will

need to continuously reassess their processes and policies to manage and mitigate the risk of fraud. (Bali

et al., 2010)

The amounts involved in insurance fraud have certainly increased as insurance made its transition into

modern consumer society. The industry has been a problem of increasing prevalence and of sizeable

4

proportions. Insurers who have long passed the cost of fraud onto their policyholders in the form of

increased premium rates, as well as other stakeholders such as legislators, prosecutors, judges and

consumer interest groups, have started to realize that the fraud problem can no longer be ignored.

(Dedene, G., & Viaene, S., 2004).

Insurance fraud is relatively simple to commit, easy to get away with, and seemingly considered ‘fair

game’—and even legitimate—by a significant minority of the population. But it is illegal, costs the

insurance companies millions of pounds, and is by no means ‘victimless’. (Gill 2001)

1.2 Research Problem

Insurance fraud is one of the most serious problems facing insurers, insurance consumers and regulators.

Its existence not only increases the cost of insurance, but also threatens the financial strength of insurers

and negatively affects the availability of insurance. Insurance fraud encompasses a wide range of illicit

practices and illegal acts involving intentional deception or misrepresentation. The industry has

witnessed an increase in the number of fraud cases in the last couple of years. Organizations are

realizing that frauds are driving up the overall costs of insurers and premiums for policyholders, which

may threaten their viability and also have a bearing on their profitability. Hence, companies need a more

vigorous fraud management framework. Larger insurers, which spend more on the investigation and

settlement of claims and on medical exam and inspection fees, are better at detecting fraud. (Bali et al.,

2010)

1.3 Purpose of the study

The purpose of the study is to explore the magnitude of the problem including the industry’s and

regulatory authority’s responses in tackling the menace in India. As mentioned in the literature review

increase in life insurance fraud is hindering the revenues of insurance companies which in turn affect the

growth of the industry and in turn to the economy as whole. The competition is good at the sales level in

the Insurance Industry but insurers need to be united to fight the frauds. The main purpose of this study

is to analyze various types of life insurance frauds, assess the risks associated with these frauds and

finally frame an ideal risk management strategy to curtail or minimize the frauds associated with life

insurance. The existing literature on life insurance fraud is used to explore the fraud risk management

and internal control system of various organizations.

5

1.4 Objectives

1) To identify different types of frauds in life insurance

2) To review existing fraud control mechanism in life insurance in India

i) To analyze that fraud risk exposure faced by insurance companies and areas that need more

stringent anti-fraud regulations are independent of each other

ii) To check the most widely used mechanism by the companies to discover life insurance fraud

iii) To check the most widely used mechanism to condense life insurance fraud

iv) To study whether the source of receiving insurance and insurer complaints are identical

3) Suggest preventive and fraud control measures with the help of research data analysis

i)To study whether there is significant correlation between the characteristics for committing insurer

fraud scheme and insurance fraud scheme

ii) To analyse the parameters which help in implementing effective fraud control policy

iii) To understand the most demanding ways insurance companies should use to prevent life

insurance fraud from customers perspective

iv) To rate a series of possible consequences or punishments for fraud from customers

perspective.

4) Perception of fraud by customers in the market

i) To measure customer’s tolerance level for life insurance fraud. Four groups will be divided

i.e. Pragmatists, Traditionalists, Moralists and Columnists. Which groups of people are

highest?

ii) To rate the overall experience towards life insurance. Whether the same is negative, positive

or neutral.

iii) To know the perception of people with regard to understand the capability of insurance

companies in identifying or preventing life insurance fraud

5) To identify the drivers that contribute to fraudulent activity (life insurance fraud)

i) To identify various reasons which compel people to commit life insurance fraud

ii) To check whether poor control and economic recession have significant effect on various

reasons which compel people to commit life insurance fraud

6

2 Literature review

2.1 Industry overview

As per the annual report of IRDA, Indian Insurance in the global scenario, the share of life insurance

business in total premium was 56.2 per cent. However, the share of life insurance business for India was

very high at 79.6 per cent while the share of non-life insurance business was small at 20.4 per cent. In

life insurance business, India is ranked 11th among the 88 countries, for which data is published by

Swiss Re. India’s share in global life insurance market was 2.00 per cent during 2013. However, during

2013, the life insurance premium in India declined by 0.5 per cent (inflation adjusted) when global life

insurance premium increased by 0.7 per cent.

At the end of March 2014, there are 53 insurance companies operating in India; of which 24 are in the

life insurance business and 28 are in non-life insurance business. In addition, GIC is the sole national

reinsurer. Of the 53 companies presently in operation, eight are in the public sector - two are specialized

insurers, namely ECGC and AIC, one in life insurance namely LIC, four in non-life insurance and one in

reinsurance. The remaining forty five companies are in the private sector.

Life insurance industry recorded a premium income of `3,14,283 crore during 2013-14 as against

`2,87,202 crore in the previous financial year, registering a growth of 9.43 per cent (0.05 per cent growth

in previous year). While private sector insurers posted 1.35 per cent decline (6.87 per cent decline in

previous year) in their premium income, LIC recorded 13.48 per cent growth (2.92 per cent growth in

previous year). While renewal premium accounted for 61.72 per cent (62.62 per cent in 2012-13) of the

total premium received by the life insurers, first year premium contributed the remaining 38.28 per cent

(37.38 per cent in 2012-13). During 2013-14, the growth in renewal premium was 7.85 per cent (3.88

per cent in 2012-13). First year premium registered a growth of 12.07 per cent in comparison to a

decline of 5.78 per cent during 2012-13.

Overall, the industry witnessed a 7.50 per cent decline (0.01 per cent decline in 2012-13) in the number

of new policies issued.

2.2 Risk Management

Risk management is viewed as a corner stone of good corporate governance and therefore results in

better service delivery, more efficient and effective use of scarce resources and better project

management (Collier et al., 2007). It has to do with identification, analysis and control of such risks that

threaten resources, assets, personnel and the earning capacity of a company.

7

According to Dorfman (2007), risk management is the logical development and implementation of a

plan to deal with potential losses. It is important for an organization to put in place risk management

programs so as to manage its exposure to risks as well as protect its assets. The essence is to prepare

ahead of time on how to control and finance losses before they occur. Dorfman continues to say that risk

management is a strategy of pre-loss planning for pre-loss resources.

Risk management is: “a process of understanding and managing the risks that the entity is inevitably

subject to in attempting to achieve its corporate objectives. For management purposes, risks are usually

divided into categories such as operational, financial, legal compliance, information and personnel. One

example of an integrated solution to risk management is enterprise risk management” (CIMA, 2005).

The Institute of Risk Management also provided a more detailed definition of risk management as: the

processes by which organizations methodologically address the risks to their activities with the goal of

achieving sustained benefit within each activity and across the portfolio of all activities (IRM et al.,

2002).

Risk management is an integral part of an organisation’s strategic management. Enterprise Risk

management forays into an efficient Corporate Governance as a tool to measure the exposure of

uncertainties and to design sensible mitigation plans.

COSO’s Enterprise Risk Management defined Enterprise risk management is a process, effected by an

entity’s board of directors, management and other personnel, applied in strategy setting and across the

enterprise, designed to identify potential events that may affect the entity, and manage risk to be within

its risk appetite, to provide reasonable assurance regarding the achievement of entity objectives

2.3 Life Insurance fraud

Practically all of the literature regarding insurer fraud is in the insurance trade press. Only in the trade

press can one find stories detailing various types of insurer fraud and describing specific legal cases.

2.3.1 Life Insurance fraud – Defined

Richard A. Derrig, V. Z. (2002) explained that the term “fraud” carried the connotation that the activity

was illegal and, hence, that prosecution and conviction were potential outcomes of a specific fraud.

Accepting that premise allows us to adopt the legal definition of fraud in the insurance context and to

examine the experience of dealing with insurance fraud in terms of property-liability insurance lines.

Specifically, ten years of data on referrals and disposals of incidents of suspected fraud as processed by

the Insurance Fraud Bureau of Massachusetts to provide estimates of the distribution of types of people

who perpetrate a variety of insurance frauds were examined.

8

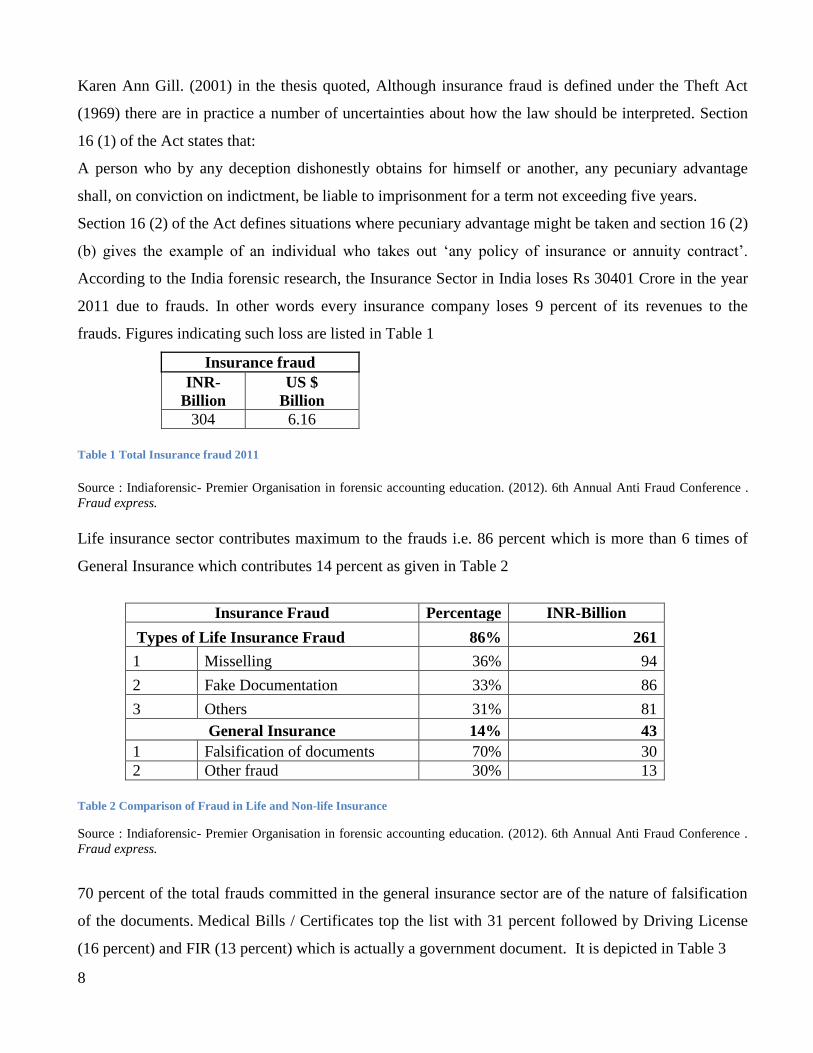

Karen Ann Gill. (2001) in the thesis quoted, Although insurance fraud is defined under the Theft Act

(1969) there are in practice a number of uncertainties about how the law should be interpreted. Section

16 (1) of the Act states that:

A person who by any deception dishonestly obtains for himself or another, any pecuniary advantage

shall, on conviction on indictment, be liable to imprisonment for a term not exceeding five years.

Section 16 (2) of the Act defines situations where pecuniary advantage might be taken and section 16 (2)

(b) gives the example of an individual who takes out ‘any policy of insurance or annuity contract’.

According to the India forensic research, the Insurance Sector in India loses Rs 30401 Crore in the year

2011 due to frauds. In other words every insurance company loses 9 percent of its revenues to the

frauds. Figures indicating such loss are listed in Table 1

Insurance fraud

INR-

Billion

US $

Billion

304 6.16

Table 1 Total Insurance fraud 2011

Source : Indiaforensic- Premier Organisation in forensic accounting education. (2012). 6th Annual Anti Fraud Conference .

Fraud express.

Life insurance sector contributes maximum to the frauds i.e. 86 percent which is more than 6 times of

General Insurance which contributes 14 percent as given in Table 2

Insurance Fraud Percentage INR-Billion

Types of Life Insurance Fraud 86% 261

1 Misselling 36% 94

2 Fake Documentation 33% 86

3 Others 31% 81

General Insurance 14% 43

1 Falsification of documents 70% 30

2 Other fraud 30% 13

Table 2 Comparison of Fraud in Life and Non-life Insurance

Source : Indiaforensic- Premier Organisation in forensic accounting education. (2012). 6th Annual Anti Fraud Conference .

Fraud express.

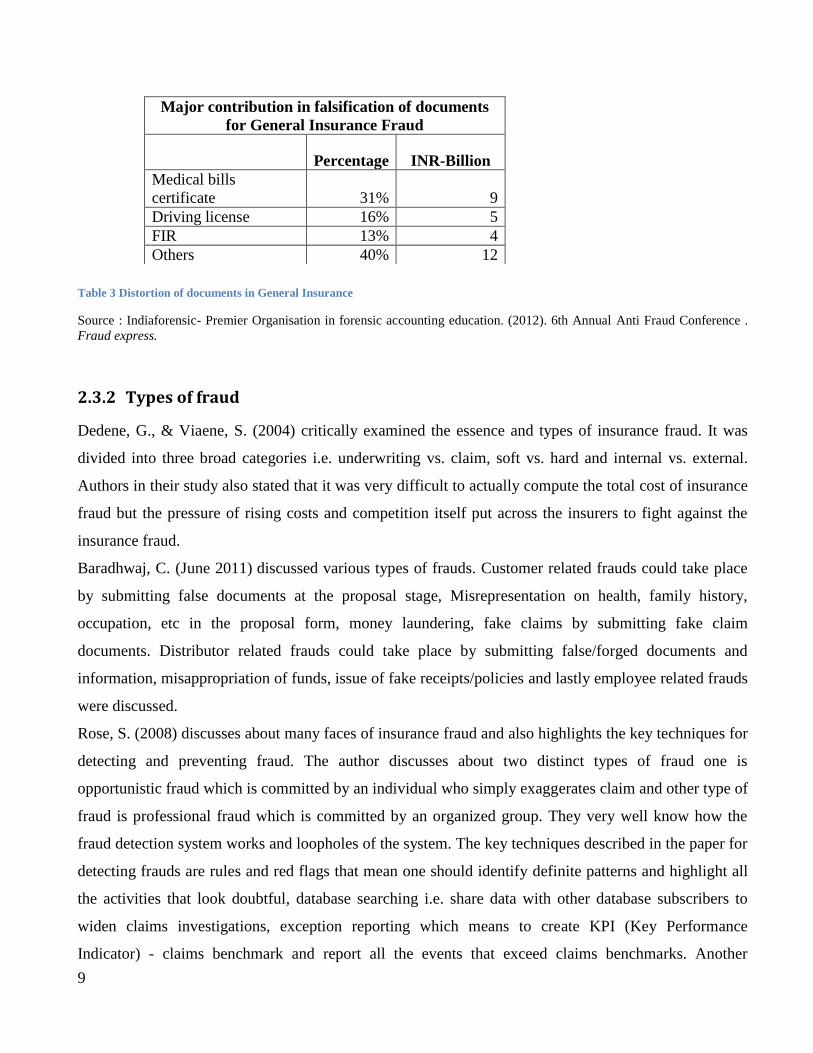

70 percent of the total frauds committed in the general insurance sector are of the nature of falsification

of the documents. Medical Bills / Certificates top the list with 31 percent followed by Driving License

(16 percent) and FIR (13 percent) which is actually a government document. It is depicted in Table 3

9

Table 3 Distortion of documents in General Insurance

Source : Indiaforensic- Premier Organisation in forensic accounting education. (2012). 6th Annual Anti Fraud Conference .

Fraud express.

2.3.2 Types of fraud

Dedene, G., & Viaene, S. (2004) critically examined the essence and types of insurance fraud. It was

divided into three broad categories i.e. underwriting vs. claim, soft vs. hard and internal vs. external.

Authors in their study also stated that it was very difficult to actually compute the total cost of insurance

fraud but the pressure of rising costs and competition itself put across the insurers to fight against the

insurance fraud.

Baradhwaj, C. (June 2011) discussed various types of frauds. Customer related frauds could take place

by submitting false documents at the proposal stage, Misrepresentation on health, family history,

occupation, etc in the proposal form, money laundering, fake claims by submitting fake claim

documents. Distributor related frauds could take place by submitting false/forged documents and

information, misappropriation of funds, issue of fake receipts/policies and lastly employee related frauds

were discussed.

Rose, S. (2008) discusses about many faces of insurance fraud and also highlights the key techniques for

detecting and preventing fraud. The author discusses about two distinct types of fraud one is

opportunistic fraud which is committed by an individual who simply exaggerates claim and other type of

fraud is professional fraud which is committed by an organized group. They very well know how the

fraud detection system works and loopholes of the system. The key techniques described in the paper for

detecting frauds are rules and red flags that mean one should identify definite patterns and highlight all

the activities that look doubtful, database searching i.e. share data with other database subscribers to

widen claims investigations, exception reporting which means to create KPI (Key Performance

Indicator) - claims benchmark and report all the events that exceed claims benchmarks. Another

Major contribution in falsification of documents

for General Insurance Fraud

Percentage INR-Billion

Medical bills

certificate 31% 9

Driving license 16% 5

FIR 13% 4

Others 40% 12

10

technique explained in the paper is predictive modeling which means to use data mining tools to build

models to produce fraud prosperity scores.

2.4 Impact of fraud

2.4.1 Economical impact of fraud

Dixon, M. (2007) clarified that effects of fraud on the industry in the USA has caused an overwhelming

endorsement of the exchange of information not only between insurance companies but with

Governmental and other organizations. If companies in the UK fail to follow their lead, this will no

doubt result in an escalation of problems of insurance fraud in this country.

Anonymous. (2011) stated that over the last 10 years, the Indian insurance industry has grown at a

compounded annual growth rate of around 20 percent. However, with the exponential growth in the

industry, there has also been an increased incidence of frauds. Insurance fraud encompasses a wide

range of illicit practices and illegal acts involving intentional deception or misrepresentation. The

industry has witnessed an increase in the number of fraud cases in the last one year. Organizations are

waking up to the fact that frauds are driving up the overall costs of insurers and premiums for

policyholders, which may threaten their viability and also have a bearing on their profitability. Hence,

companies need a more vigorous fraud management framework. Although this survey focuses on retail

insurance, frauds related to commercial insurance claims and third-party claims are also on the rise. The

sophistication of fraudsters in the area of commercial insurance claims and third-party claims makes it

all the more difficult for organizations to detect and control fraud in time.

Gupta, A., & Venugopal, R. (July 2011) revealed the fact that In USA, the cost of insurance frauds was

more than 100 billion USD in the year 2003 working out to 950 USD per family. In 2001, 73percent of

the US Property & Commercial insurers rated fraud as a serious problem - 4.6 on a scale of 5. In U.K.

the fraud is in excess of four million pounds per week. The yearly figures are one billion pounds. In

Canada, it is 1.3 billion Can Dollars. Survey done by India forensic revealed the fact that the insurance

industry is losing close to 15000 Crores rupees every year! That is almost 9percent of revenues of an

insurance company. This clearly indicates the seriousness of the problem According to a PwCSurvey,

more than a third of Indian companies do nothing about the frauds. 32 percent of the fraudsters (internal)

are simply warned/ transferred /reprimanded. 28 percent are dismissed. 60 percent are criminally

charged/civil action taken. Mostly the fraudster is a person who has a long standing relationship with the

11

victim company. 31 percent are Agent-hackers, 19 percent are external suppliers, 15 percent top and

middle management; and 8 percent are customers.

2.4.2 Fraud Detection and Prevention

Aart, C. V., & Tamma, V. (2008) presented two business templates which can help to decrease risk and

costs in the insurance market. Risks can be decreased by having agents gather evidence for (possible)

fraud chains. At this moment fraud detection is still performed manually and therefore a time consuming

and imprecise process. When using fraud detection agents, every damage report can be investigated on a

large scale looking for black listed drivers, stolen cars and known types of fraud.

Colquit, L. L., & Hoytt, R. E. (1997) evaluated the reasons given by insurers for resisting fraudulent

claims. The author also investigated specific characteristics such as claims, demographic, economic and

insurer that were related to the nature and level of life insurance fraud. Also larger insurers and insurers

that spend more on the investigation, settlement of claims, medical exam and inspection fees were

considered to be better fraud detectors. Findings suggest that frauds were higher in the states where

unemployment was high and where public attitude’s to accept the fraud was higher.

Holmes, S. A., Todd, J. D., Welch, S. T., Welch, O. J., & Holmes, S. A. (1999) concluded that insurance

industry was more careful than other industries with regard to internal control systems in order to reduce

the effect of fraud. Auditors of insurance industry could detect only customer fraud and not even a single

case of insurer fraud was detected by them. Insurer fraud was detected either through suspicion or

through internal or outside complaint. The schemes used by insurer fraud perpetrators were simpler,

affecting fewer accounts and involving fewer violations of internal control mechanisms, than those of

other industries. Insurers were also more likely to act against their employees for fraud compared to

other industries. Internal whistle-blowing in other organizations compared to insurance industry was

strong. Significant differences were observed in the formal fraud investigation in case of insurance

industry compared to financial and other industries. Insurers rely on outside examination where as

financial and other industries rely on internal investigation. Insurer and other financial institution wanted

criminal prosecution of their employees compared to other industries.

Derrig, R. A. (2002) revealed that the fundamental problem for insurers coping with both fraud and

systemic abuse was to devise a mechanism that efficiently sorts claims into categories that require the

acquisition of additional information at a cost. Measurement, detection, and deterrence of fraud were

advanced through statistical models, intelligent technologies were applied to informative databases to

12

provide for efficient claim sorts, and strategic analysis was applied to property-liability and health

insurance situations.

Boyer, M. M. (2007) contributed to the crime and punishment debate by looking at the impact of

prevention and punishment in an insurance fraud context. More to the point, the author developed a

theoretical approach in which stiffer penalties and increased prevention could have no impact on the

amount of fraud when the proportion of criminal elements in society was too high. The principal–agent

model which the author presented introduced agents that could be of two possible types that differ only

with respect to the propensity to commit fraud: Truths never do whereas Dares have no moral objection

to it. If the proportion of Dares was large enough, then the amount of fraud and the number of agents

found to have committed fraud was independent of their exact proportion. Finally, investment in

prevention would be useless if the proportion of Dares was large enough because then investing in

prevention becomes a waste of resources. This last result holds when the proportion of Dares was large.

When their proportion was small, investing in prevention reduced fraud.

Bali, S., Singh, A., Parekh, A., Indge, R., & Torpey, D. (2010) revealed the findings that there have been

increased incidences of fraud over the last one year. Fraud risk exposure from claims or surrender was a

major concern area for industry players. They have emphasized the need for increased anti-fraud

regulations in the area of claims management. According to the survey report, there were various types

of insurance frauds, which occurred in all the areas of insurance, e.g., as claims and surrenders, fake

documentation, misselling, collusion between parties, etc. Today, when India’s insurance industry is

working toward reducing costs, one of its main focus areas to control or reduce costs is by proactively

arresting fraud, which can be achieved through an effective fraud risk assessment (FRA) program i.e.

Effective policy holder and vendor due diligence process, Effective claims validation, Mystery

shopping, i.e., gathering market intelligence relating to tied and corporate agents, brokers, etc., Channel

reviews pertaining to tied agency, bancassurance and tele calling, Contract compliance reviews

including review of advertising expenses, intellectual property (IP) compliance, etc., Effective fraud

analytics and electronic dashboards.

BRAMLET, C. (2012) revealed the fact that going after fraud simply doesn’t fall on the shoulders of

SIU alone. There must be a companywide commitment and training throughout all layers of the

corporation. Staff must be apprised of proper data-mining techniques, and the insurer must be willing to

cultivate a system-wide awareness of fraud at all levels of the company and programs for identifying and

disseminating clues to the special investigative unit (SIU).

13

Swaby, G. (2011) finds that the current state of the law allows for the insurer to claim damages from an

insured when a fraudulent claim is made to recover the cost of any investigations. Second the insurer can

refuse to meet a claim that is tainted by fraud. Third the insurer can have the right to avoid the policy

obligations upon the discovery of a fraud, but subject to some limitations. Fourth there is a need for the

insured to be protected against an insurer’s unjustified allegations of fraud.

2.4.3 Customer’s perception for fraud

Coalition against insurance fraud. (1997) conducted a study which was designed on understanding the

customer's perception on unethical behavior and suggested various measures to curtail insurance fraud

such as-proper scrutiny of applications, proper investigation of claims and rejecting false claims or

application

Tennyson, S. (2002) examined whether consumers’ level of experience with insurance was related to

their attitudes toward insurance fraud. Such a relationship could arise because inexperienced consumers

may have misperceptions about insurance contracts and institutional rules, which could result in

accepting attitudes towards actions that are in fact fraudulent. Survey data shows that respondents who

owned more types of insurance and those who had recent insurance claiming experience were less likely

to find insurance fraud to be acceptable.

Michael Costonis, J. B. (2010) conducted an insurance consumer fraud survey. Insurance consumer

attitudes and behaviors toward fraud greatly influence insurance companies’ claims volumes and cost.

Results from the Accenture Insurance Consumer Fraud Survey 2010 point to four overall key findings

that contribute to the slowdown of claims performance: • Poor control was more likely to encourage

fraud. • Claims filing frequency and fraud increase in a difficult economy. • Fraudsters believe they can

get away with it. • Consumers expect insurers to continue their investments to prevent fraud. Based on

the survey results, Accenture believes that insurers can drive high performance through claims by taking

a hybrid approach to addressing fraud. In a hybrid approach, a carrier has a two-fold aim to: 1. Provide

better service on the policy and claim sides for a more positive, consistent customer experience that

builds customer loyalty and dissuades potential individual insurance fraud, and engage analytics tools to

more sharply focus on, detect and tackle organized fraud. Insurers should strive for better customer

service on the whole as a way to reduce potentially fraudulent individual behavior, given that survey

respondents were clear in suggesting that individual customers may be less inclined to commit fraud if

they believe a carrier has their best interest in mind and aims to restore them to their pre-claim situation.

Examples of customer service improvements include: Ensuring that non-claims personnel are adequately

14

trained on the claims process to advice customers properly during sales and service transactions. • Doing

a better job of setting policyholder expectations of what happens when a claim is filed, and then •

Meeting those expectations during claim fulfillment. • Demonstrating care and concern for the insured in

a more consistent manner.

Miyazaki, A. D. (2009) conducted an experimental study which showed that higher deductible amounts

result in stronger perceptions that insurance claim padding is fair to the insurance company, weaker

perceptions that the behavior is unethical, and higher proposed claim award amounts. The study also

shows, however, that the deductible amount effects are attenuated for consumers who display higher

ethical standards as reflected by their scores on the consumer ethics scale. The study also shows,

however, that the deductible amount effects are attenuated for consumers who display higher ethical

standards as reflected by their scores on the consumer ethics scale. Implications are discussed with

respect to the insurance industry, deviant consumer behavior, and general business ethics theory.

3 Research Gap

There have been a number of valuable studies of insurance fraud (Gupta, A., & Venugopal, R.

(2011), Lesch, Dedene, G., & Viaene, S. (2004) all of which present evidence of insurance

fraud on the entire industry in general. However, none of these studies considers only life

insurance.

While there has been some research on fraudulent activities related to claims (Rose, S. (2008),

Swaby, G. (2011), Miyazaki, A. D. (2009)), where in the focus is only on claims fraud and little

has been written about all the fraudulent activities.

There are several papers which focus on measures to curtail insurance fraud (Dixon, M. I.

(1996), Holmes, et al. (1999) but little focus is on what should be the fraud control mechanism

for life insurance fraud or how to curtail fraud. Which are the characteristics for committing for

insurance and insurer fraud, whether it is same for both and what should be the punishments to

the perpetrators for life insurance fraud and drivers that contribute to fraudulent activity?

There are several papers which focus on risk management (George, E. (2003) in insurance but

hardly any paper talk about the fraud risk, how to do fraud risk assessment and the risk

management

15

4 Research Methodology

4.1 Research Design:

Exploratory Research: This comprises of secondary data analysis as well as primary. Primary data

comprise of qualitative research – expert interview and advice was taken. These experts comprised of

manager and above cadre (risk profile) from life insurance companies as well as investigating agencies

which were 6 in number and also 4 academicians’ interview were taken. Questionnaire was circulated

via email to industry experts and proof checking of the content of the questionnaire was done and the

questions were modified as per the expert’s advice. This helped us to gather information such as actual

practices followed by them to review fraud and the measures taken by them to control it.

Descriptive Research: Two surveys i.e. employees and consumer survey was conducted in order to study

the customer’s perception and practices followed by the life insurance companies. This helped us to

know how a customer would rate their company as well as agent, personal experience of the consumer

with fraud, curtailing and punishing fraud. Detail description is given below.

4.2 Sampling Frame

4.2.1 Sampling Technique

Survey 1 - Method of sampling used was judgmental and convenience. Survey 2 - method of sampling was

convenience.

4.2.2 Sample size

Survey 1 – 50 industry experts.

Survey 2 - Total 500 respondents.

4.2.3 Sample selection procedure

Survey 1 - Total seven life insurance companies (LIC, Reliance, Bajaj, ICICI, Kotak, Aviva and Birla )

were selected on the basis of status of grievances reported for the year 2010-11 in the annual report of

IRDA. Three departments were taken i.e. risk/audit and compliance, claims and operation working in

Ahmedabad, Mumbai, Delhi and Chennai.

16

Survey 2 – Respondents were selected and mostly walk in customers in the insurance companies and

banks were taken.

4.3 Data Collection Tools

The secondary data was collected from various online database, journals and books available in the

library. Primary data was collected through survey by administering questionnaire. Personal as well as

telephonic interview were taken of experts. Telephonic mode was selected in order to meet wider

geographic reach. Online as well as personal survey was taken. Online was again selected in order to

meet wider geographic reach.

4.4 Mode of data collection

Data pertaining to research has been collected with the help of questionnaire

4.5 Method for data analysis

Statistical tool i.e. SPSS is used in order to analyse the data. Various statistical tests were used i.e.

frequency distribution, cross tab, chi-square test, one sample independent t test, two sample independent

t test, correlation and regression were applied.

17

5 Data Analysis

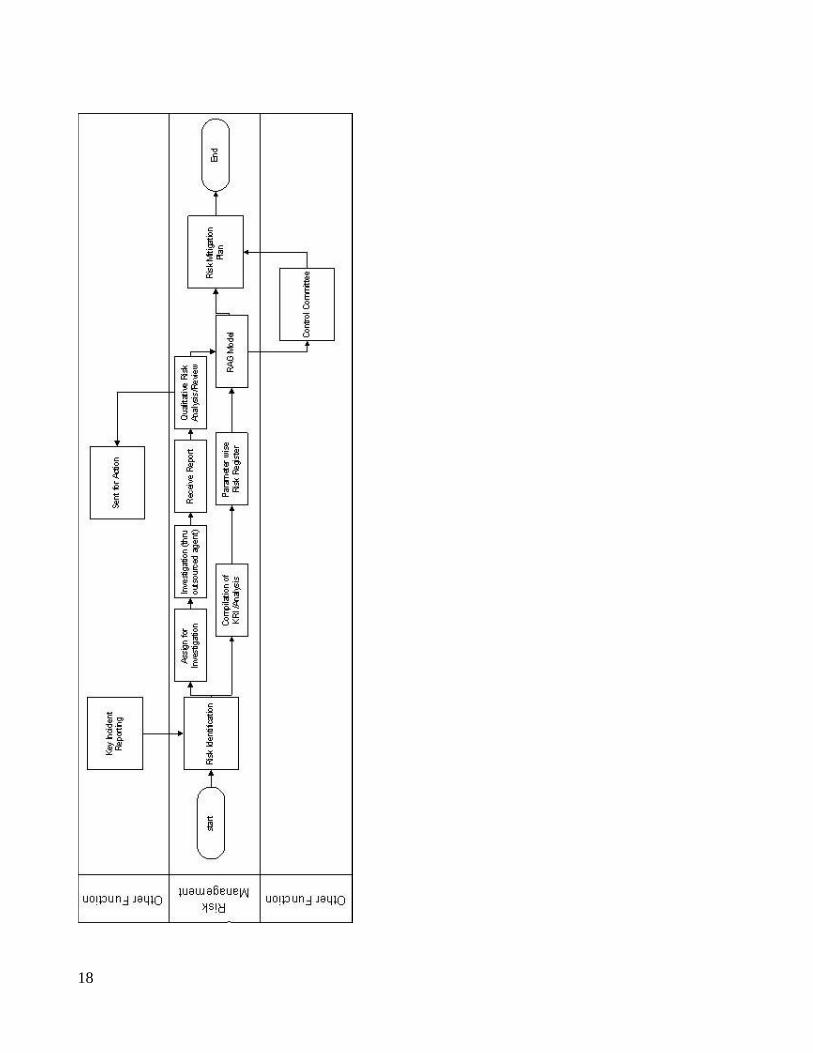

This chapter discusses about the analysis done i.e secondary and primary. First the secondary data

analysis is discussed. Brief description about risk management process:

The risk management process starts with key incident reporting which means receipt of Case/ Issue

/Incident. The process starts with receiving request from Referee Unit for Investigation. Referee unit

will be one who will refer the case. It can be operations team while processing the application, claims

team while processing the claims, risk team while conducting the branch audit, doctor audit, mystery

shopping or complaints. Further step of the process is to assign the case for investigation to the risk

consultant. Investigation is then conducted with the help of outsourced team. Risk consultant will then

receive the report and will give final recommendation on the basis of report. Side by side it is also

forwarded to control committee to plan risk mitigation and present it to control committee. Risk

management process which is explained above is inferred from the below mentioned diagram. This

process map was made after meeting various industry experts during the visit to company.

18

19

5.1 Types of Fraud

Thus from the literature review available and experience the types of fraud can be broadly divided as

follows:

Internal Fraud: Internal frauds are those perpetrated against a company or its policyholders by agents,

managers, executives, or other employees.

External Fraud: External frauds are directed against the company by individual or entities as diverse as

medical providers, policy holders, beneficiaries, vendors and career criminals.

An internal fraud often involves theft of proprietary information, improper relationships with vendors or

consultants involving conflicts of interest, diversion of policyholder or company funds by employees,

use of confidential information for investment purposes, intentional misrepresentation by agents to

prospective customers about the characteristics or future performance of company products and any

other unethical activity that might put the business interest at risk. External fraud can involve such

schemes as fraudulent automobile, life, health or disability claims, the use of tax-advantaged insurance

products for concealing the origins of illicit funds, or the negotiation of counterfeit checks. Internal

frauds are those perpetrated against a company or its policyholders by agents, managers, executives, or

other employees.

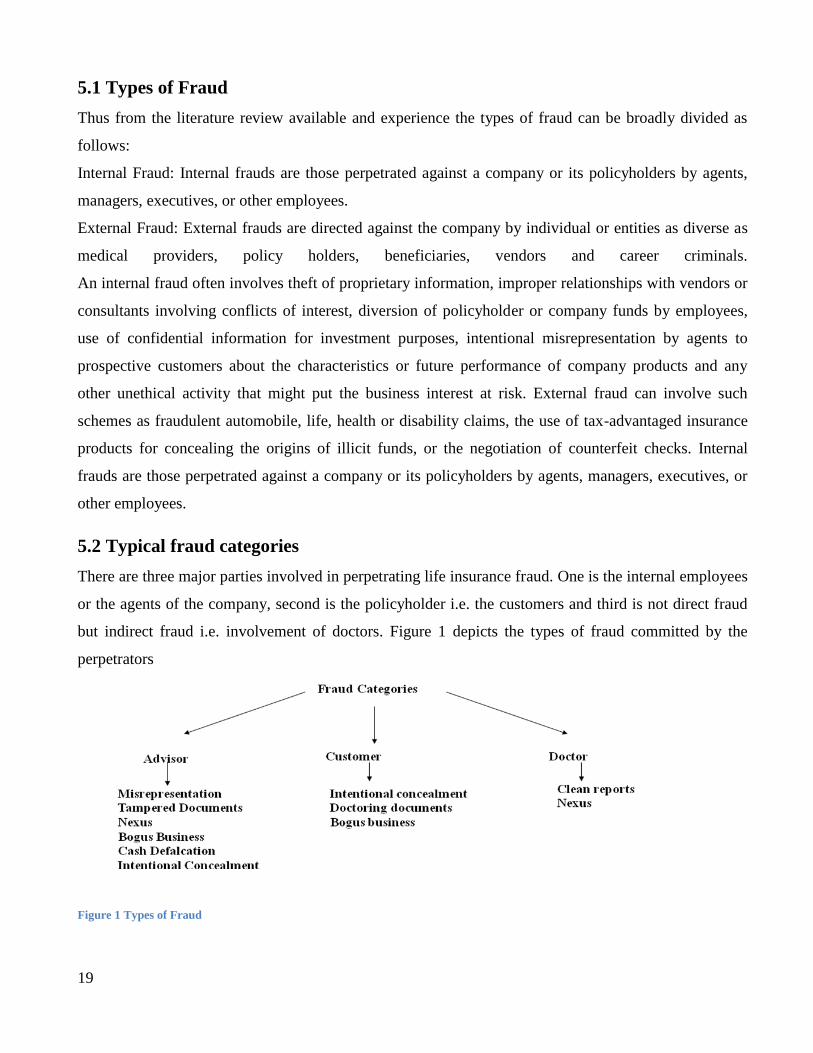

5.2 Typical fraud categories

There are three major parties involved in perpetrating life insurance fraud. One is the internal employees

or the agents of the company, second is the policyholder i.e. the customers and third is not direct fraud

but indirect fraud i.e. involvement of doctors. Figure 1 depicts the types of fraud committed by the

perpetrators

Figure 1 Types of Fraud

20

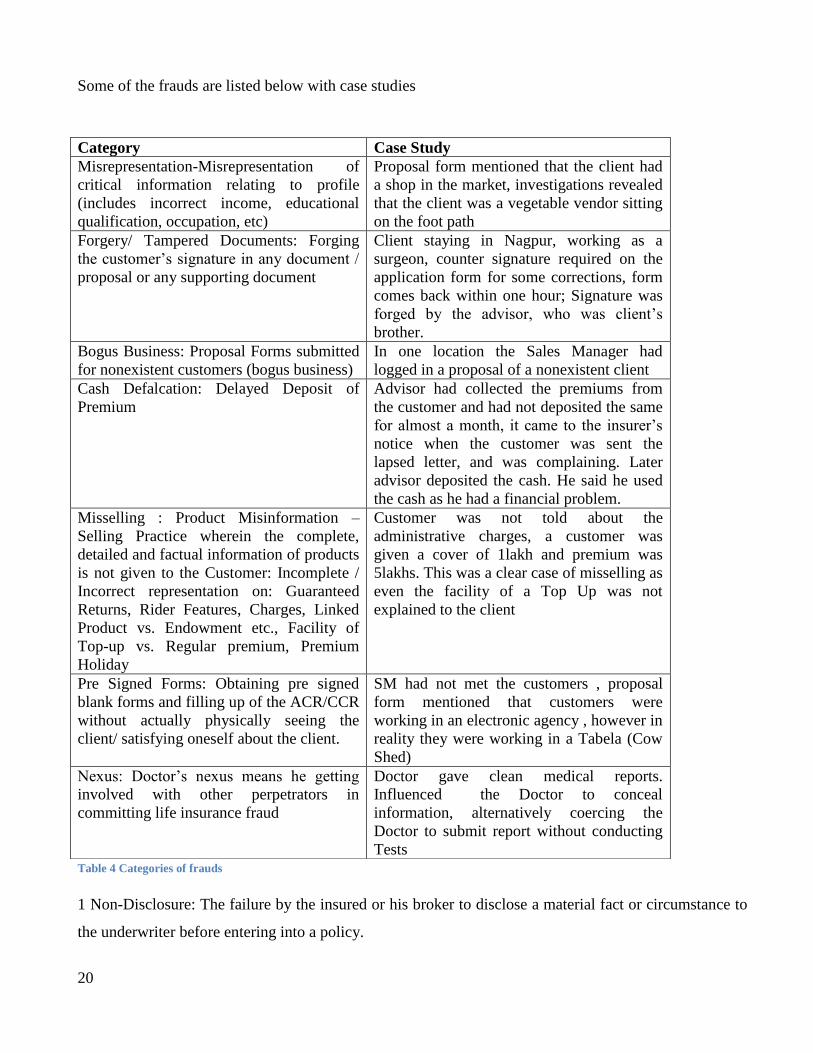

Some of the frauds are listed below with case studies

Table 4 Categories of frauds

1 Non-Disclosure: The failure by the insured or his broker to disclose a material fact or circumstance to

the underwriter before entering into a policy.

Category Case Study

Misrepresentation-Misrepresentation of

critical information relating to profile

(includes incorrect income, educational

qualification, occupation, etc)

Proposal form mentioned that the client had

a shop in the market, investigations revealed

that the client was a vegetable vendor sitting

on the foot path

Forgery/ Tampered Documents: Forging

the customer’s signature in any document /

proposal or any supporting document

Client staying in Nagpur, working as a

surgeon, counter signature required on the

application form for some corrections, form

comes back within one hour; Signature was

forged by the advisor, who was client’s

brother.

Bogus Business: Proposal Forms submitted

for nonexistent customers (bogus business)

In one location the Sales Manager had

logged in a proposal of a nonexistent client

Cash Defalcation: Delayed Deposit of

Premium

Advisor had collected the premiums from

the customer and had not deposited the same

for almost a month, it came to the insurer’s

notice when the customer was sent the

lapsed letter, and was complaining. Later

advisor deposited the cash. He said he used

the cash as he had a financial problem.

Misselling : Product Misinformation –

Selling Practice wherein the complete,

detailed and factual information of products

is not given to the Customer: Incomplete /

Incorrect representation on: Guaranteed

Returns, Rider Features, Charges, Linked

Product vs. Endowment etc., Facility of

Top-up vs. Regular premium, Premium

Holiday

Customer was not told about the

administrative charges, a customer was

given a cover of 1lakh and premium was

5lakhs. This was a clear case of misselling as

even the facility of a Top Up was not

explained to the client

Pre Signed Forms: Obtaining pre signed

blank forms and filling up of the ACR/CCR

without actually physically seeing the

client/ satisfying oneself about the client.

SM had not met the customers , proposal

form mentioned that customers were

working in an electronic agency , however in

reality they were working in a Tabela (Cow

Shed)

Nexus: Doctor’s nexus means he getting

involved with other perpetrators in

committing life insurance fraud

Doctor gave clean medical reports.

Influenced the Doctor to conceal

information, alternatively coercing the

Doctor to submit report without conducting

Tests

21

2 Misrepresentation: A ‘misrepresentation’ is a false statement of fact made by one party to another

party and has the effect of inducing that party into the contract. For example, under certain

circumstances, false statements or promises made by a seller of goods regarding the quality or nature

of the product that the seller has may constitute misrepresentation.

3 Mis-selling: The ethically questionable practice of a salesperson misrepresenting or misleading an

investor about the characteristics of a product or service. In an effort to make a sale to a potential

customer, a financial products salesperson could leave out certain information or describe a financial

product as something the investor urgently needs, even though sound financial judgment would

come to the opposite conclusion.

A good example of misselling can be seen in the life insurance industry. Consider an investor who

has a large amount of savings and investments but no dependent children and a deceased spouse.

This investor would arguably have little need for whole life insurance and, therefore, an insurance

salesperson describing the product as something the investor urgently needed to protect his or

her assets in the event of death could be considered a case of misselling.

4 Cheque dishonor: Where any cheque drawn by a person on an account maintained by him with a

banker for payment of any amount of money to another person from out of that account for the

discharge, in whole or in part, of any debt or other liability, is returned by the bank unpaid, either

because of the amount of money standing to the credit of that account is insufficient to honor the

cheque or that it exceeds the amount arranged to be paid from that account by an agreement made

with that bank.

5 Paying premium for customers – rebating: Giving a premium reduction or another financial

advantage not stated in the policy as an inducement to purchase the policy. The offer of sharing

commissions with the applicant is an inducement that is not part of the insurance policy and,

therefore, is considered rebating. Rebates include not only cash but also personal services and items

of value. Rebating is considered a violation of the Unfair Trade Practices Acts in most states.

5.2.1 Proposal Stage: Fraud

This chapter reports the research findings on fraud at the proposal stage. It looks at the two main factors

which facilitate fraud: first, the system of selling through unaccountable agents, who put sales above all

other considerations; and second, the features of policies which expose them to fraud. While these

22

factors are discussed separately, in reality they overlap. Three case studies are discussed, focusing on the

three types of insurance fraud by customers most common at this stage.

Deficiencies of current methods of sale:

As previously noted, most insurance is sold through agents, and this can lead to two main problems:

first, insurers have little control over the type of person they are insuring; and second, they have little

control over the types of policies that are sold.

Insurers admit that often banks or building societies take total control of policies, from issue through to

the claim or renewal process. Because of this insurers rely on their agents to detect fraud at the proposal

stage. But agents are encouraged by large commissions to sell insurance, and it is not necessarily in their

interests to expose fraudulent intent. If they identify a prospective fraudster at the proposal stage, and

refuse to insure him/her, they lose a sale and the commission on that sale. The commissions that agents

receive for the sale of insurance policies are often a very important source of income. Reports in the

insurance press suggest those travel agents’ and tour operators’ profit margins on the policies they sell

are between 30 and 60 per cent (Wheal 1997). It has even been suggested that travel agents obtain

bigger mark-ups on insurance, to compensate for their low margins on holiday sales (Wheal 1997). In

this way insurers are actively motivating their agents to sell policies, but there is no incentive to prevent

fraud.

Agents sometimes sell insurance as a secondary product, in the form of a standard package. As a result,

applicants may have little choice as to the type of insurance they purchase, and the outcome may be that

their policies are unsuitable or provide inadequate cover. If a policy is not suitable, and a loss occurs,

some policyholders are likely to lie on their claims form and misrepresent the circumstances of the loss

in order to ensure that the insurer pays out on the claim. In order to understand the life insurance fraud at

the proposal stage four case studies were studied. These case studies were shared by one of the life

insurance company. Out of four case studies one case study is explained in detail below:

Case Study 1

A proposal form was signed on 9/2/2006 was submitted at the branch on 14/2/2006. It reached

underwriter's desk on 16/2/2006 and policy was issued on 20/2/2006. The policy was dispatched to the

customer and was returned undelivered to HO. Hence it was resent to branch to be personally handed

over to the customer. By that time, branch was intimated about the death of Life Assured. Life Assured

died on 24/2/2006, just 4 days after RCD. Entire set of medical reports was submitted to the company at

23

the time of claim, which brought to light distressing facts. Life Assured was under treatment from as

early as 27/12/2004 and she was tested HIV positive on 31/1/2005.

As per the proposal form she was keeping good health. Same was confirmed by the confidential report

given by Advisor who knows LA for 7 years. The report was also countersigned by the SM. With Height

159 cms and weight 65 kgs, as mentioned in the proposal form, BMI was standard. But, the medical

reports presented an altogether different picture regarding Life Assured's weight. On 4/2/2006, she was

weighing 37 kgs and on 9/2/2006, the day she signed proposal form, her weight was 36 kgs, making

BMI as non standard. Moreover, the day the proposal form was signed i.e. 9/2/2006; Life Assured was

under treatment in hospital.

Being a clear case of misrepresentation and non disclosure of material facts, the claim was repudiated

and as a goodwill gesture fund value was paid to claimant. Learning from the case study was to make

sure that discreet enquiries are made about the proposer before a policy is issued, so as to ensure fair

selection of lives. In this case advisor knew LA for seven years and she was under treatment on the day

proposal form was signed. Whenever, a countersign is done by SM, it is the responsibility of SM to

reconfirm the facts relating to health, age and occupation directly with the customer at least through a

telephonic call. Not long ago, executives believed that a hallmark of the well-run enterprise was its

ability to actively avoid risk while pursuing objectives devoid of danger.

Risks emerge from a potent mix of factors, including regulatory compliance, competitive pressure,

environmental impacts, security and privacy concerns, business continuity, strategic planning, reporting

protocols, operational processes, sustainability, and more. Companies of differing sizes, industries, and

geographies will face a varied and unique arrangement of risk factors.

Risk management, as currently practiced, is often a one-time, internally disruptive event. Despite fancy

analytical capability and dedicated professionals, many companies deploy a risk management system

that is more theoretical than practical, based on anecdotal rather than empirical evidence, and one that is

fragmented across jurisdictions, industries, and frameworks. The result is less risk management and

more risk recognition. It's a good start but only a start.

Developing a Risk Strategy with reference to this case study is as under :

Risk intelligence, on the other hand, requires a real time, ongoing process capable of engaging external

risks and opportunities to fulfill stated company objectives within accepted risk-taking parameters. To

attain this state requires, first, executives who actually understand the nature of risk and, second, a well

defined strategy to guide an organization's risk management program.

24

Strategic risk management is not merely identifying risks, nor is it listing objectives to be achieved in

dealing with identified risk. Both the identification and the elucidation are necessary-but not sufficient-

to complete the optimum risk management program.

Strategy is key. An effective strategy will include the following procedures to deal with the full

spectrum of risk defined above:

Risk assessment should begin by identifying a company's most basic strategic assumptions

followed by questioning their veracity.

Understand the difference between unrewarded and rewarded risk and allocate resources

accordingly. For example, compliance with regulatory requirements is necessary but won't result

in a reward. Acquiring a competitor might.

Focus on finite effects instead of infinite causes. Understand critical assets and dependencies and

plan for their independent functioning when necessary.

Test organizational resilience under different scenarios. Improve flexibility to deal with

uncertainties.

Harmonize (ensure risk managers all speak the same language), synchronize (coordinate across

institutional boundaries), and rationalize (eliminate duplication of effort) existing risk

management functions to drive down the cost of good risk management.

Effective strategic risk management should enable companies to state unequivocally and document

clearly the organization's risk exposure. Most importantly, with an appropriate risk strategy in place, the

decision to accept risk exposure will be informed, deliberate, and justified.

5.2.2 Claims Stage: Fraud

This chapter summarizes the research findings on fraud at the claims stage. The present chapter focuses

on four main facilitators of insurance fraud, i.e. the factors which make fraud possible. These include:

the difficulty of proving that a fraud has occurred; the involvement of people willing to help fraudsters;

the awareness that insurers do not investigate some cases of suspected fraud, as they find it quicker and

cheaper to pay out on a claim; and the process of ‘fast tracking’, which leaves insurers little time to look

for fraud. In order to understand claims stage fraud total three case studies were studied, out of which

one is listed below. These case studies were shared by one of the life insurance company.

25

Case Study 2

The proposal amounted for 150K and the age of the insured was 42 years. The term plan was taken for

25 yrs. Occupation was driver and annual income was 75K. Family history was good. BMI was normal

and personal health detail was good. Age proof was standard. The LA was known to the advisor for last

1 year. The underwriting decision was to accept at ordinary rate and policy was issued on 27/01/03. LA

died on 31/01/2003 and the cause of death submitted in claim form was heart attack.

Investigation was first done by SM that LA visited one of the neighbor states about light treatment for

some time. Detail investigation revealed that LA was suffering from Cancer for last one year and

undergoing treatment at Cancer Institute. On 27/01/03 also he went for treatment to the Hospital.

Decision taken was claim to be repudiated and action was to be taken against Advisor.

Whatever the type of case, we have to begin with the basics, carefully building from there. Every

investigation is a detailed and systematic examination to uncover the facts and determine the truth.

Every investigation follows a set process starting from collecting evidence and information, ascertaining

conclusions and acting on them.

5.3 Control on Life Insurance fraud

This chapter focuses on the primary survey done with the industry experts. The assessment was done in two

phases. The first phase involved selection of variables, selection of scale of measurement and designing

questionnaire, testing and piloting of the questionnaire. The second phase involved online and telephonic survey

based on the questionnaire, cross checking, data entry, data analysis and preparation of final report. A set of

variables were selected on the basis of literature review and discussion with the risk personnel of different life

insurance companies. The sampling profile displays 32 percent of the valid responses falls in risk profile. 28

percent fall in operations profile and 20 percent fall in both claims and audit or compliance.

5.3.1 Discussion and Analysis

Data obtained from the questionnaires were tested using nonparametric means. The Chi square test of

independence was used to measure the independence of two variables. Independent Sample T test was

used to measure the significant differences between two variables. Multiple responses set in SPSS were

created to group different variables into one. Correlation was also used. Cross tabulation and frequency

distribution were also used.

26

5.3.2 Review existing fraud control mechanism

5.3.2.1 Research Hypothesis

H1o: Fraud risk exposure faced by insurance companies and areas that need more stringent anti fraud regulation

are independent of each other

Life insurance fraud arises because of four major types of risk : Operational Risk is defined as the risk of loss

resulting from inadequate or failed internal processes, people and systems or from external events, Insurance Risk

refers generally to the uncertainty about the ultimate amount of net cash flows from premiums, commissions,

claims and claims-settlement expenses emanating from a cession of contractually defined liabilities (Actuarial and

Underwriting Risk) and the timing of the receipt and payment of those cash flows, Legal and Reputational Risk

refers generally to the risk resulting from institution’s failure to enact appropriate policies, procedures, or controls

to ensure it conforms to laws, regulations, contractual arrangements, and other legally binding agreements and

requirements and Financial Risk refers generally to the risk resulting from having inadequate definition of

accounting policies, material misstatement and cash defalcation. We wanted to check whether four key areas of

risk exposure and the areas that needs more stringent anti fraud regulation are independent of each other. These

four areas are operational risk, financial risk, legal and reputational risk and insurance risk. Respondents were

asked two separate questions and requested to give ranking from one to four. Options for both questions were

common. To check the hypothesis non-parametric test i.e. chi-square test of independence was applied at

significance level of 0.05. Results depicted p value equal to 0.000 which is less than 0.05 and therefore null

hypothesis is rejected. This means that key areas of risk exposure and the areas that need more stringent anti fraud

regulation are dependent on each other.

5.3.2.2 Mechanism used by life insurance companies to discover life insurance fraud

It is very much important for any life insurance company to have a proper mechanism to discover life insurance

fraud. It is found with the help of survey that 33 percent of the respondents indicated that fraud risk assessment

framework consisting of a dedicated risk department and internal audit both are the mostly used mechanism to

discover fraud. It is followed by whistleblower policy i.e. 28 percent and 5 percent of the respondents expressed

that external audit is used as a mechanism. None of the respondents have told that external database search is used

to discover life insurance fraud.

H2o: The selection mechanism used for discovering life insurance fraud is independent of the individual profile

There are various mechanisms which are used by the life insurance companies to discover life insurance fraud.

They are having a fraud risk assessment framework i.e. a dedicated risk department, whistleblower policy,

conducting external audits, conducting internal audits and external database search. Hypothesis addresses whether

27

the selection of these mechanisms are independent of the individual profile of the respondents. Profile consists of

personnel from risk, audit/compliance, claims and operations department. Chi square test of independence was

used at significance level of 0.05. P value computed is 0.140 which is more than 0.05 and therefore null

hypothesis is not rejected. Hence we can conclude that the selection for mechanism used for discovering life

insurance fraud is independent of the individual profile.

H3o: The selection methods used by life insurance companies to condense life insurance fraud is independent of

the individual profile

There are various methods used by life insurance companies to condense life insurance fraud which are

screening, sampling, mathematical tools, psychometric tests and investigation on suspicion. Hypothesis

addresses whether the selection for methods used by life insurance companies to condense life insurance

fraud is independent of the individual profile. Chi square test of independence was used at significance

level of 0.05. P value computed is 0.001 which is less than 0.05 and therefore null hypothesis is rejected.

Hence we can conclude that the selection for methods used by life insurance companies to condense life

insurance fraud is dependent on the individual profile.

5.3.2.3 Insurance complaints

There are two major types of life insurance frauds one is Insurer fraud which means an internal fraud i.e. that

committed by agents or employees and second is Insurance fraud which means a fraud perpetrated by

policyholders. Majority of insurer and insurance fraud are depicted from the complaints or grievances received.

These complaints can be received from inside the organization or outside the organization. 88 percent of insurer

complaints are received from inside the organization and 12 percent outside the organization similarly

88 percent of insurance complaints are received from outside the organization and 12 percent from

inside the organization.

5.3.2.4 Preventive and fraud control measures

5.3.2.4.1 Characteristics for committing fraud

There were seven characteristics identified for committing insurance fraud and insurer fraud. We wanted to check

whether there is any correlation between the characteristics for committing insurer fraud and insurance fraud.

H4o: There is no significant correlation between the characteristics for committing insurer fraud scheme and

insurance fraud scheme

28

We have checked the assumptions for correlation that both the variables are in interval scale, there is

linear relationship which was observed with the help of scatter diagram, data was normally distributed

and there were no significant outliers. A Pearson product-moment correlation was run to determine the

relationship between characteristics for committing insurer fraud and insurance fraud. There were in

total seven characteristics identified for committing insurer and insurance fraud. The data showed no

violation of normality, linearity assumption except for 1, 2 and 6th characteristics. Hence these were

excluded and the remaining four characteristics were Perpetrator takes advantage of lax organizational

attitude, Exploitation due to lack of separation of duties, Exploitation due to untrained personnel and

Exploitation due to failure to conduct periodic checks. There was a strong, positive correlation for

exploitation due to lack of separation of duties for insurer and insurance fraud (r = 0.662, n = 50, p <

.0005). Thus it can be concluded that out of seven different characteristics for committing insurer fraud

and insurance fraud there is significant positive correlation in three characteristics. This also confers that

different characteristics are adopted for committing insurer and insurance fraud. Taking advantage of

lax organizational attitude, exploitation due to lack of separation of duties and failure to conduct

periodic checks all this leads to lack of internal control system. Since there is a significant correlation in

the characteristics for these three, it can be concluded that lack of internal control leads to both insurer

and insurance fraud.

If there are vital differences or similarities, however, information of those differences or similarities

could be particularly helpful to insurer-fraud avoidance and detection units in achieving their missions.

Regarding characteristics of schemes, we would expect employees to develop, through their daily

activities, an understanding of company internal controls and to become familiar with any weaknesses

inherent in their execution.

Internal controls are policies and procedures designed to protect assets from damage or theft and to

prevent concealment of fraudulent activity through modification of the information system that tracks

assets and transactions. Examples of good control mechanisms would include separation of duties so

that one employee cannot have both the custody of cash and authorize its removal from the company;

protection of documents from alteration or destruction so that the validity of transactions can be

ascertained; and periodically taking an inventory of both assets and the documents that vouch for

transactions to make sure neither has been removed during the period to conceal a fraud. Employees,

through their knowledge and ongoing relationship with the company, would tend to be in a position to

use multiple schemes to perpetrate a fraud. In contrast, multiple schemes should be somewhat less

prevalent where fraud-detection processes are in greatest use e.g., insurance fraud. Finally, regarding

29

methods of detection and investigation, it can be expected claims examinations to be the major vehicle

whereby insurance fraud is detected and investigated, because this form of fraudulent activity is

considered the primary target for insurers. Consequently, employee fraud most likely will be detected

and investigated by alternative methods.

5.3.2.4.2 Parameters for an effective Fraud control Policy

As discussed above, it is vital for any life insurance company to have an effective fraud control policy

but the question is what will help the insurer in implementing an effective fraud control policy. The

results of the survey are given below:

23 percent of the respondents indicated that management involvement and awareness and training

workshop will help in implementing an effective fraud control policy equally. 22 percent of the

respondents expressed that stringent action on fraud identified will help to implement such policy. 14

percent feel enabling employees to report and deal with life insurance fraud will help. 10 percent of the

respondents feel that walk the talk will help. 10 percent of the respondents feel that all of the parameters

listed will help in implementing an effective fraud control policy.

5.4 Customer’s perception

This chapter focuses on the perception of customer with regard to life insurance fraud. Customer survey

was conducted to know their perception with regard to life insurance fraud. Direct survey as well as

online Survey was conducted for the same using the website esurveyspro.com. Data collection for the

same is done and data analysis is under process. The collected data was edited, coded, tabulated,

grouped and organized according to the requirement of the study and then it was entered into SPSS

(statistical package for social sciences) for analysis.

This study was conducted to gain insight on why public tolerance of insurance fraud seems to be

increasing. Both qualitative and quantitative research was used to attempt to understand how public

attitudes about fraud are formed and what factors influence them. Among the areas explored in the

survey include opinions about insurance fraud and insurance providers. The frequency distribution

displays 45 percent female and 55 percent male respondents.

30

5.4.1 Four drivers that contribute to fraudulent activity.

After conducting the survey it was observed and found that broadly there are four drivers which

contribute to the fraudulent activity in life insurance fraud. 1) Poor control (Internal control of the

company) 2) Difficult economy 3) Fraudster’s attitude( I can get away with it) and 4) Consumer’s

attitude (Fraud is unacceptable).

The respondents were asked to what degree they agree that poor control from an insurance company

might make a person more likely to commit fraud against that company. The respondents were asked to

what degree they agree that poor control is likely to contribute to life insurance fraud and it was

observed that more than half that is 55 percent of the respondents believe that poor control is responsible

for driving insurance fraud.

Further creating a market atmosphere conducive to fraud is the current slow economy. Consumers agree

that people are more likely to commit insurance fraud during economic downturns. 61 percent of the

respondents agree that in difficult economy that is during recession there are more chances of

committing life insurance frauds.

More than 55 percent of respondents believe insurance fraud occurs because people believe they can get

away with it and that they need money. This clearly describes the fraudster’s attitude for driving up the

insurance fraud.

Around 70 percent of the respondents have shown the likelyhood to report a case for life insurance

fraud

It is evident from the analysis that around 80 percent of the respondents feel that insurance companies

are capable of detecting fraud. But amongst those it is clear that 52 percent of them think that insurance

companies are only somewhat capable, which is concern. There are 20 percent of the respondents who

still feel that insurers are not capable of detecting life insurance fraud. Fraud can be perpetrated in many

ways. Therefore, an insurer should adopt a holistic approach to adequately identify, measure, control and

monitor fraud risk. For an insurance organization, its fraud management strategy should form part of its

business strategy and be consistent with its overall mission and objectives. Detection of insurance fraud

should be in two steps: The first is to proactively identify suspicious claims or surrender that has a high

possibility of being fraudulent. This can be done by conducting data analysis using various forensic tools

or by putting in place an effective fraud risk assessment framework. Additionally, insurance companies

can provide their stakeholders with a fraud reporting mechanism and second is regardless of the mode

31

of implementing step one, the next step should be to investigate these fraud claims or surrender and

conduct further analysis.s

5.4.2 Four Expressions : Tolerance level of customers for life insurance fraud

All the respondents were grouped into one of the subgroups depending on their levels of tolerance and

certain perceptions of why people commit insurance fraud. For the purposes of this study, the subgroups

are identified as Pragmatists, Traditionalist, Moralists and Columnist.

The Pragmatists have a low tolerance for insurance fraud but realize it occurs. They may feel some

behaviors are justified depending on the circumstances; they don t advocate strong punishment. This

group represents 16 percent of the survey s respondents.

The Traditionalists are fairly tolerant of insurance fraud, largely because they believe many people do it,

making it more acceptable. For that reason, they tend to believe in more moderate forms of punishment.

This group makes up 27 percent of the survey s respondents.

The Moralists have the least tolerance of insurance fraud. They believe there s no excuse for this

behavior and are the most willing to punish perpetrators severely. This is the largest group of

respondents 47 percent of the surveyed population.

The Columnists have the highest tolerance for fraud and tend to blame the insurance industry for people

s behaviors because they believe insurers don t conduct business fairly. They want little or no

punishment for perpetrators. This group represents 10 percent of the survey s respondents.

For analyzing the hypothesis, Pearson Chi-Square is the most common test for significance of the

relationships between categorical variables. The Chi-Square test is not appropriate if any of the expected