MCI (P) 137/11/2012 Ref No: RM2013_0021 1 of 15

Regional Market Focus

Phillip Securities Research Pte Ltd

30 January 2013

Singapore

SMRT Corporation – Results (Derrick Heng) Recommendation: Sell Previous close: S$1.675 Fair value: S$1.41

Sharp fall in profits a surprise.

Staff cost rose to an all time high.

Lower than expected share of rail CAPEX is the only positive development.

Maintain Sell with revised target price of S$1.41.

Thailand

MCOT – Company Preview Recommendation: TRADING BUY Previous close: Bt 47 Fair value: Bt50.75

We expect 4QCY12 net profit to jump 244.60% y-y to Bt456mn, comparing to an extra low base a year ago due to flood impact.

CY12 earnings are expected to see slight improvement and we expect a 2HCY12 dividend of Bt1.14/share.

We project CY13 net profit at Bt2,051mn as MCOT will benefit from the recent ad rate hikes and an increased ratio of in-house production TV program. We rate the stock a ‘TRADING BUY’ with a target price of Bt50.75/share.

Hong Kong

China Molybdenum(3993.HK) – Slight Improvement in Operation

Recommendation: Neutral Previous close: HKD 3.55 Fair value: HKD 3.95

The price rebound in molybdenum and wolfram would benefit the operation results of China Molybdenum. The urbanization process has been bringing the steel price up, the market demand of products is another positive factor to the company.

China Molybdenum will devote fund to the industry chain construction of wolfram. With the growth of self-sufficiency rate in raw materials, the leading position of China Molybdenum will be consolidated.

Most financial indicators have been improving and are not affected by revenue decline. Overall, the financial stability of China Molybdenum is reliable.

The EPS of 2011FY is CNY 0.23, we estimate that the performance in the 4th quarter is hard to improve, so the EPS in the 2012FY and 2013FY are CNY 0.22 and 0.27, the target price in next 6 months is HKD 3.95 under 12x P/E, the rating is Neutral.

Regional Market Focus

30 January 2013

2 of 15

Strategy Views

- Country Strategy: S’pore, 26 Dec / China & HK, 28 Jan / Thai, 19 Dec - Global Macro, Asset Strategy: 24 Jan, Update / 4 Jan / US, 21 Dec / ASEAN, 5 Dec

Morning Commentary

- STI: -0.43% to 3259.8 - JCI: +0.50% to 4439 - HSCEI: -0.18% to 12077.9 - Nikkei 225: +0.39 to 10866.7

- SET: +0.46% to 1478.8 - KLCI: +0.01 to 1637.3 - Hang Seng: -0.07% to 23655.2 - S&P500: +0.51% to 1507.8

SINGTEL UPDATE: By Ken Ang, Financials & Telco Analyst

SingTel (Neutral, TP: $3.06) announced the sale of its entire 30% stake in Warid Telecom (Private) Ltd, purchased in Sep 2007 for S$1.17 billion, for a consideration of US$150 million in cash, and right to receive 7.5% share of net proceeds from any future divestment. We view this divestment positively, as it reduces further losses and commitments, including guarantees of approximately US$90 million. As at Sep 2012, SingTel had received a guarantee call amounting to US$30.3 million which was not met due to on-going discussions. We note that Warid has performed poorly, registering negative post-tax contributions every quarter since its acquisition, due to a depreciating Pakistani rupee and poor performance. The number of mobile subscribers has also been declining in recent quarters. We expect SingTel to re-invest the cash consideration into its existing business MARKET OUTLOOK: By Joshua Tan, Hd of Research

China A shares, CSI300, yesterday exited the classic definition of a bear market having put in a 20% gain since its 4q12 low. The A share market is in some sense playing catchup with the HSCEI and Hang Seng which have been rallying since June last year.

For the STI, yesterday we retreated nearly half a percent, in line with our heads up comment on Tuesday morning that as the index has been on strong 7 day advance, “…yesterday’s (Monday’s) inverted hammer close may indicate the market may soon be in the mood to profit take, its very hard to tell at the moment but just take note.” We view profit taking as short term and are OW Singapore for the year.

Singapore authorities has also released a white paper indicating a target population of 6.9m from the current 5.3m, making the urgency for infrastructure and housing more acute. The paper is likely to set off another wave of construction. Our top pick beneficiary is Pan United (see Equity Strategist note below), eminent ready mixed concrete supplier in Singapore with largest market share (30%).

In ASEAN, the KLCI managed to grind out another tiny gain, building on its rebound off the 200dma, this suggests that it will rebound higher still. But our opinion is that this is a quick trade (beware dead cat bounce) as the run-up to election may induce volatility as investors speculate the result. Thailand’s SET continues its beautiful uptrend.

US markets reversed previous day’s stall to charge higher. There is not much in terms of resistance to now shoot for the 2007 closing high of 1561.8. Earnings and economic data, on the whole, continue to suggest an improving economy led by a manufacturing rebound.

As usual we finish off with our market outlook for the year: we continue to believe that this is a year for stocks and maintain OW on CN, HK, SG, TH and PH, while MW on the US, MY and ID. Investors looking to invest in the first 4 markets should check out our Country Strategy reports, else invest/trade them thru ETFs/PhillipCFDs listed in the Asset Strategy reports (see Sector/Strategy Reports section). Equity Strategists: - Hd of China Research: China Life Insurance (2628.HK), China Lumena New Material (67.HK) - Hd of HK Research: AIA (1299.HK) and HSBC (5.HK) - SG Equity Strategist (Derrick Heng): For 1Q2013, we believe that cyclical stocks in the Industrials space could do well in the near term: SIA (Buy, TP: S$13.40), Keppel Corp. (Accumulate, TP: S$12.38) & NOL (Accumulate, TP: S$1.36). Top picks for the year are Pan United (Buy, TP: S$0.88), SIAEC (Buy, TP: S$5.00) & Capitaland (Accumulate, TP: S$3.97). Pan United is a dominant supplier to the construction industry in Singapore and we expect the company to perform well given the strong pipeline of infrastructure work over the next few years. Although current price (S$0.97) has overshot our TP, and may experience short term profit taking, we look forward to 4q12 results to reassess our TP. SIAEC is a key beneficiary of the aviation growth story in the region and offers excellent dividend yields. Capitaland would be a beneficiary of the stabilisation of property prices and bottoming out of economic conditions in China. MACRO DATA In US, consumer confidence declined to 58.6 in Jan, the weakest level since Nov 2011, from a revised 66.7 in Dec, much lower than the market expected 64. Another report shows that property values rose by 5.5% y-y in Nov, the biggest gain since Aug 2006, after advancing 4.2% y-y in Oct.

In Australia, business confidence rebounded by the most in more than a decade. The confidence index for Dec rose sharply to 3 from -9, indicating a reverse of sentiment from pessimistic to optimistic. Reserve Bank of Australia Governor Glenn Stevens and his board cut the benchmark rate to 3 percent last month, matching the level reached from April-October 2009 that was the lowest since 1960, as the economy struggles under a sustained high currency.

In India, the central bank lowered the benchmark interest rate for the first time since April, from 8% to 7.75%, and cut the cash reserve ratio from 4.25% to 4%. The central bank cut the inflation forecast to 6.8% and said there’s space, “albeit limited,” to support a faltering economy.

Regional Market Focus

30 January 2013

3 of 15

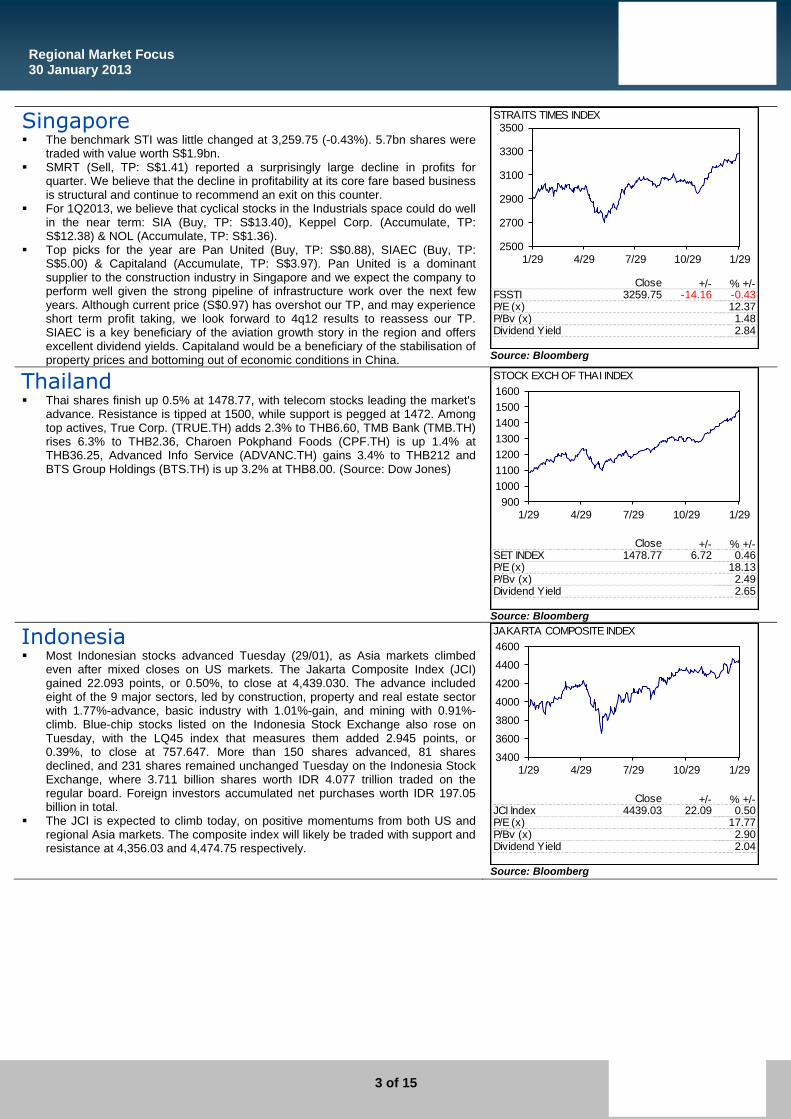

Singapore The benchmark STI was little changed at 3,259.75 (-0.43%). 5.7bn shares were

traded with value worth S$1.9bn. SMRT (Sell, TP: S$1.41) reported a surprisingly large decline in profits for

quarter. We believe that the decline in profitability at its core fare based business is structural and continue to recommend an exit on this counter.

For 1Q2013, we believe that cyclical stocks in the Industrials space could do well in the near term: SIA (Buy, TP: S$13.40), Keppel Corp. (Accumulate, TP: S$12.38) & NOL (Accumulate, TP: S$1.36).

Top picks for the year are Pan United (Buy, TP: S$0.88), SIAEC (Buy, TP: S$5.00) & Capitaland (Accumulate, TP: S$3.97). Pan United is a dominant supplier to the construction industry in Singapore and we expect the company to perform well given the strong pipeline of infrastructure work over the next few years. Although current price (S$0.97) has overshot our TP, and may experience short term profit taking, we look forward to 4q12 results to reassess our TP. SIAEC is a key beneficiary of the aviation growth story in the region and offers excellent dividend yields. Capitaland would be a beneficiary of the stabilisation of property prices and bottoming out of economic conditions in China.

Close +/- % +/-FSSTI 3259.75 -14.16 -0.43P/E (x) 12.37P/Bv (x) 1.48

2.84Dividend Yield

STRAITS TIMES INDEX

2500

2700

2900

3100

3300

3500

1/29 4/29 7/29 10/29 1/29

Source: Bloomberg

Thailand Thai shares finish up 0.5% at 1478.77, with telecom stocks leading the market's

advance. Resistance is tipped at 1500, while support is pegged at 1472. Among top actives, True Corp. (TRUE.TH) adds 2.3% to THB6.60, TMB Bank (TMB.TH) rises 6.3% to THB2.36, Charoen Pokphand Foods (CPF.TH) is up 1.4% at THB36.25, Advanced Info Service (ADVANC.TH) gains 3.4% to THB212 and BTS Group Holdings (BTS.TH) is up 3.2% at THB8.00. (Source: Dow Jones)

Close +/- % +/-SET INDEX 1478.77 6.72 0.46P/E (x) 18.13P/Bv (x) 2.49

2.65Dividend Yield

STOCK EXCH OF THAI INDEX

900

1000

1100

1200

1300

1400

1500

1600

1/29 4/29 7/29 10/29 1/29

Source: Bloomberg

Indonesia

Most Indonesian stocks advanced Tuesday (29/01), as Asia markets climbed even after mixed closes on US markets. The Jakarta Composite Index (JCI) gained 22.093 points, or 0.50%, to close at 4,439.030. The advance included eight of the 9 major sectors, led by construction, property and real estate sector with 1.77%-advance, basic industry with 1.01%-gain, and mining with 0.91%-climb. Blue-chip stocks listed on the Indonesia Stock Exchange also rose on Tuesday, with the LQ45 index that measures them added 2.945 points, or 0.39%, to close at 757.647. More than 150 shares advanced, 81 shares declined, and 231 shares remained unchanged Tuesday on the Indonesia Stock Exchange, where 3.711 billion shares worth IDR 4.077 trillion traded on the regular board. Foreign investors accumulated net purchases worth IDR 197.05 billion in total.

The JCI is expected to climb today, on positive momentums from both US and regional Asia markets. The composite index will likely be traded with support and resistance at 4,356.03 and 4,474.75 respectively.

Close +/- % +/-JCI Index 4439.03 22.09 0.50P/E (x) 17.77P/Bv (x) 2.90

2.04Dividend Yield

JAKARTA COMPOSITE INDEX

3400

3600

3800

4000

4200

4400

4600

1/29 4/29 7/29 10/29 1/29

Source: Bloomberg

Regional Market Focus

30 January 2013

4 of 15

Sri Lanka The Colombo bourse concluded on a negative note for the second consecutive

trading day, resulting both indices to retain at negative closures, this was mainly due to the prevalent selling pressure which was visible throughout the day. The benchmark ASPI Index lost heavy 54.34 points or 0.93% and closed at 5,800.75 recording its lowest value after 8 successive trading days and the S&P SL20 Index stood at 3,185.76 dipping 8.96 points or 0.28%. The market capitalization as at the day’s closure was LKR 2.23Tn recording a year to date gain of 2.8%.

The turnover for the day was hoisted at LKR 1.35Bn with heavy crossings; which was an increase of 77.85% compared to the previous trading day. Bank Finance & Insurance (LKR758.3Mn) and Diversified Holdings (LKR444.9Mn) stood out as the best performers under the sectorial review. Shares totaling up to 28.1Mn changed hands during the day; this was an increase of 72.36% compared to the previous trading day. The foreigners were bullish for the second consecutive trading day resulting a net foreign inflow of LKR 830.6Mn while, recording a year to date net foreign inflow of LKR 399.2Mn; Furthermore, the Inflow recorded during the day was the highest inflow recorded for the year. The USD closed the day at a quoted price of LKR 128.78/-.

Close +/- % +/-CSEALL Index 5800.75 -54.34 -0.93P/E (x) 12.38P/Bv (x) 1.77

2.57

Dividend Yield

SRI LANKA COLOMBO ALL SH

4500

4700

4900

5100

5300

5500

5700

5900

6100

1/29 4/29 7/29 10/29 1/29

Source: Bloomberg

Australia

On Tuesday the Australian stocks posted the longest streak of daily gains in more than eight years as three cuts in interest rates boosted lenders’ profit margins and signs of recovery in China’s economy buoyed BHP Billiton Ltd. The benchmark S&P/ASX200 index rose 53.8 points or 1.11 per cent to 4,889.0 - its highest close since April 2011.

Today, the Australian market looks set to open flat following a mixed performance on Wall Street ahead of consumer confidence and housing data and in anticipation of a US Federal Reserve monetary policy meeting.

On the economic news front for Wednesday, the Australian Property Institute is scheduled to release its residential property outlook for 2013 and in equities news, the second Hastie Group creditors meeting, expected to go for two days, is due to begin in Melbourne, Sydney, Perth and Adelaide. Legal firm Jones Day is to host a seminar in Sydney on Australia's foreign anti-bribery legislation and its relevance to the resource sector, while Wesfarmers is expected to release its second quarter sales results.

Close +/- % +/-S&P/ASX 200 INDEX 4888.30 -0.68 -0.01P/E (x) 18.84P/Bv (x) 1.94

5.76

STANDARD & POORS/ ASX 200 INDEX

Dividend Yield

3800

4000

4200

4400

4600

4800

5000

1/29 4/29 7/29 10/29 1/29

Source: Bloomberg

Hong Kong

Local stocks swung between gain and loss. The HSI and HSCEI lost 16 points and 22 points to 23655 and 12077 respectively. Market volume was 75.660 billion, rising 12.2% dod.

Investors lost trading direction before the end of January, we believe the market is going to consolidate, as some of the technical indicators is showing that the HSI is overbuying. We suggest for investors to stand on sideline and wait for a clear trading signal.

Technically, the HSI is expected to gain a support from 23300 level, major resistance will be 23800 level.

Close +/- % +/-HSI INDEX 23655.17 -16.71 -0.07P/E (x) 12.13P/Bv (x) 1.58

2.99Dividend Yield

HANG SENG INDEX

17000

18000

19000

20000

21000

22000

23000

24000

25000

1/29 4/29 7/29 10/29 1/29

Source: Bloomberg

Regional Market Focus

30 January 2013

5 of 15

Market News

US Confidence among US consumers declined more than forecast in January, reaching the lowest level in more than a year as higher

payroll taxes took a bigger bite out of Americans' paychecks. The Conference Board's index decreased to 58.6, the weakest since November 2011, from a revised 66.7 in December, figures from the New York-based private research group showed yesterday. The drop in confidence coincides with a 2 percentage-point increase in the payroll tax used to fund Social Security, a hurdle for consumers after a projected pick-up in spending in the fourth quarter. Americans' outlooks for employment prospects and their incomes also deteriorated this month, yesterday's figures showed. (Source: BT Online)

Singapore Singapore is putting a new economic roadmap in place, one that will see a gentler but more sustainable pace of growth than before. At

the same time, it will also start growing its workforce far more slowly than it has been doing so for the past three decades. The new approach was revealed as the government released its White Paper on Population yesterday. It is estimated that Singapore's population could grow an estimated 30 per cent from the current 5.3 million to reach 6.5-6.9 million by 2030. But going forward, moderation will be the key for the economy. No longer will growth targets be set at 5-6 per cent a year. Instead, it is estimated that GDP could grow at 3-5 per cent a year between now and 2020. Beyond that, from 2020 to 2030, growth could be an even more modest 2-3 per cent a year, the paper estimates. (Source: BT Online)

Enough land has been set aside for 700,000 more homes here by 2030 - more than half the 1.2 million households currently - to cater to

a growing population. This is part of a plan to provide good and affordable housing for Singaporeans detailed in the Population White Paper yesterday, as the population may reach 6.9 million by then. Of the 700,000 homes that can be built, about 200,000 are already under construction. Of the remaining half a million houses, many will be in new towns, such as Tengah, Tampines North and Bidadari. There will also be new homes built in mature estates where land is available. (Source: BT Online)

Markets love volatility and currency movements have been triggered by "Abenomics" - Japanese Prime Minister Shinzo Abe's aggressive

strategy of talking the yen down to boost exports and get the country out of its two decades long deflation. On average, volumes are up 20 per cent in daily FX (foreign exchange) trading activity so far this year compared with the same period a year ago, said Mr Oruche. FX players love volatile markets because of the potential for significant profits. Many are comfortable dealing with multiple currencies. (Source: BT Online)

Hong Kong

Chinese incomes rose faster in the countryside than in cities for a third straight year in 2012 as migrant workers boosted their pay and the government strengthened the social safety net. Rural per-capita net income advanced 10.7 percent, compared with 9.6 percent for urbandwellers, partly on the rise in migrant laborers and their wages, the National Bureau of Statistics said Jan. 18. Rural residents’ income from benefits payments rose 21.9 percent, almost double the urban pace, as the government boosted its budget for health-care handouts. (Source: Bloomberg)

Taiwan will double the limit on mainland Chinese institutions’ securities investments in its market as the cross-strait economic

relationship deepens. Maximum inbound investment from China will be increased to $1 billion from $500 million, according to Huang Tien-mu, Taiwan’s securities regulator. He spoke after a meeting yesterday between Guo Shuqing, chairman of the China Securities Regulatory Commission, and Taiwan’s top market regulator, Chen Yuh-chang, in Taipei. (Source: Bloomberg)

Hong Kong banks’ loans in neighboring Shenzhen’s Qianhai district may jump in the next three to five years as companies registered in

the zone start operating, according to Wing Lung Bank Ltd. The bank is among the first 15 Hong Kong lenders to Qianhai companies, which agreed to borrow a total of about 2 billion yuan ($321 million), the city government said Jan. 28. Banks will probably price the loans, mainly for construction and development, at 4 percent to 4.5 percent, Henry Huang, assistant general manager of the Hong Kong-based unit of China Merchants Bank Co. (3968), said in a briefing yesterday. (Source: Bloomberg)

Thailand Thailand’s baht rose for a second day on optimism the nation’s improving economy and relatively high bond yields will draw overseas

capital. The currency appreciated 2.7 percent this month, the best exchange-rate performance in Asia, as international investors poured more than $4 billion into local stocks and sovereign bonds, official data show. The Bank of Thailand raised its 2013 growth forecast on Jan. 18 to 4.9 percent from an October estimate of 4.6 percent. Benchmark 10-year government notes pay 3.71 percent in Thailand, compared with 2 percent in the U.S. and 0.77 percent in Japan. (Source: Bloomberg)

Indonesia The government estimates investment will provide the greatest contribution to economic growth this year by 3.1-3.2percent of the 6.6-6.8

percent economic growth rate. Coordinating Minister for Economic Affair, said investment rate remains high in 2013 because Indonesia is still an investment destination. He added to encourage investment the government will rely on infrastructure programs and improving investment climate, administrative, and labor. To develop investment climate, the government will improve national logistics system and the special economic zone. (Source: Indonesia Finance Today)

Regional Market Focus

30 January 2013

6 of 15

The price hike of basic needs – particularly foodstuffs – was due to the effects of weather and inundation in parts of Indonesia. The bad weather has boosted inflation in January 2013 to top over one percent. Governor of Bank Indonesia said the high inflation was caused by disruption in the flow of goods distribution, resulting in prices increasing. He said expected inflation in January 2013 has exceeded Bank Indonesia’s projections in the beginning of this year, prior to the flooding in the Greater Jakarta area and parts of Indonesia. In early 2013, Bank Indonesia estimated inflation in January 2013 would be 0.9 percent, but after the inundation the figure is expected to reach 1.1 percent. (Source: Indonesia Finance Today)

Cement consumption in Indonesia is expected to reach 62 million tonnes this year, up 10 percent from 55 million tonnes in 2012,

according to a senior official from the Ministry of Industry.The Ministry of Industry`s director for downstream chemical industry. Domestic consumption of cement increased by 14.5 percent last year, compared with 48 million tonnes in 2011. Even in Indonesia`s eastern regions, the demand increased by about 54 percent, far higher than other regions of the country, In keeping with the Master Plan for Acceleration and Expansion of Indonesia`s Economic Development (MP3EI), increasing the number of factories is part of the effort to support the MP3EI projects by meeting the domestic demand for cement. (Source: Antara News)

Sri Lanka Sri Lanka will get two loans from the Hungarian Export – Import Bank to finance the rehabilitation of Labugama and Kalatuwawa Water

Treatment Plants. The Hungarian Bank will provide over 34 million Euro’s to finance the rehabilitation work of the above mentioned two tanks. The loan to rehabilitate the Labugama plant will run up to Euro 16.71 million, while the Kalatuwawa plant will receive a funding support of Euro 17.38 million. (Source: Dailymirror.lk)

Australia Australian stocks posted the longest streak of daily gains in more than eight years as three cuts in interest rates boosted lenders’ profit

margins and signs of recovery in China’s economy buoyed BHP Billiton Ltd. The benchmark S&P/ASX 200 (AS51) Index yesterday rose for a ninth day, the longest run since December 2004. Lenders from Westpac Banking Corp. (WBC) to National Australia Bank Ltd. (NAB) accounted for the largest proportion of the increase as home sales climbed and business confidence grew. BHP, the world’s largest mining company, paced gains among mining companies as China’s manufacturing, economic growth and industrial production exceeded estimates. The measure climbed 0.3 percent at 11:26 a.m. in Sydney today. Investors are moving into equities as the Reserve Bank of Australia undertakes the most aggressive interest-rate cuts among advanced economies, sapping the allure of bonds as yields decline. The S&P/ASX 200’s forecast dividend yield of 4.5 is the highest among the world’s 10 largest equity markets, according to data compiled by Bloomberg. (Source: Bloomberg)

Regional Market Focus

30 January 2013

7 of 15

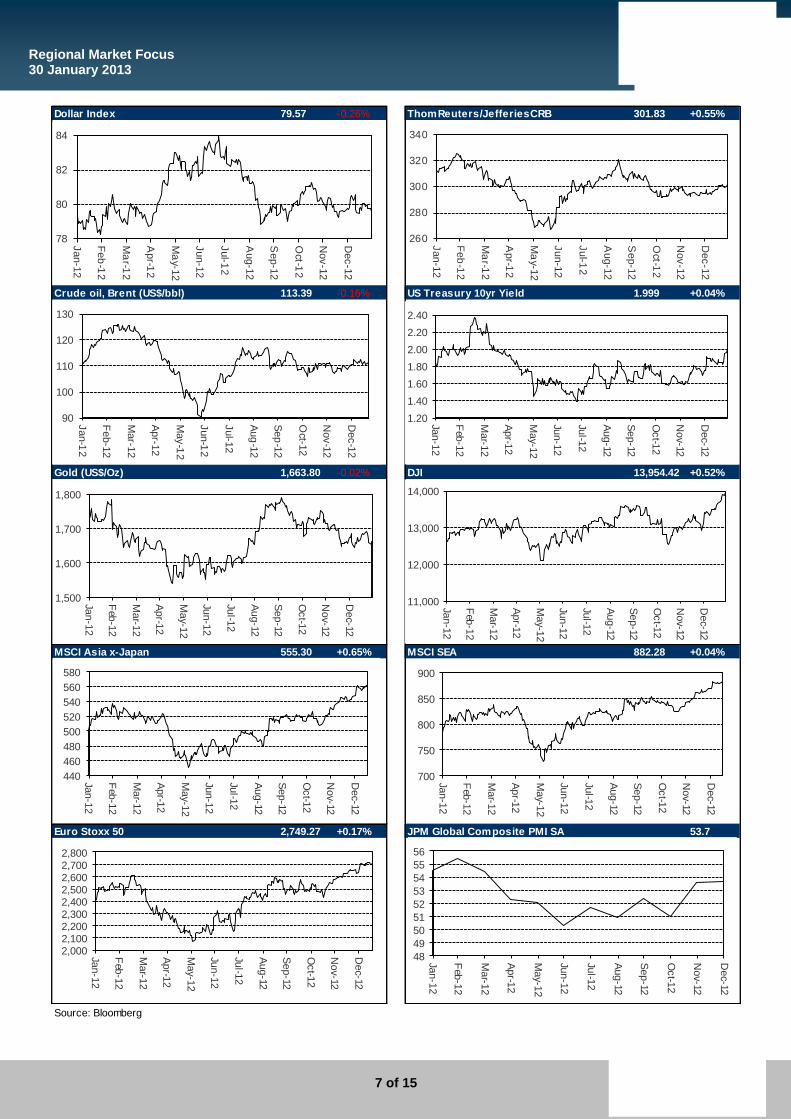

79.57 -0.26% 301.83 +0.55%

113.39 -0.16% 1.999 +0.04%

1,663.80 -0.02% 13,954.42 +0.52%

555.30 +0.65% MSCI SEA 882.28 +0.04%

2,749.27 +0.17% 53.7

Source: Bloomberg

MSCI Asia x-Japan

JPM Global Composite PMI SA

ThomReuters/JefferiesCRB

DJI

Crude oil, Brent (US$/bbl) US Treasury 10yr Yield

Euro Stoxx 50

Dollar Index

Gold (US$/Oz)

1.20

1.40

1.60

1.80

2.00

2.20

2.40

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Aug-12

Sep-12

Oct-1

2

Nov-12

Dec-12

700

750

800

850

900

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Aug-12

Sep-12

Oct-1

2

Nov-12

Dec-12

11,000

12,000

13,000

14,000

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Aug-12

Sep-12

Oct-1

2

Nov-12

Dec-12

2,0002,1002,2002,3002,4002,5002,6002,7002,800

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Aug-12

Sep-12

Oct-1

2

Nov-12

Dec-12

48

49

50

51

52

53

54

55

56

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Aug-12

Sep-12

Oct-1

2

Nov-12

Dec-12

1,500

1,600

1,700

1,800

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Aug-12

Sep-12

Oct-1

2

Nov-12

Dec-12

78

80

82

84

Jan-1

2

Feb

-12

Ma

r-12

Apr-1

2

Ma

y-12

Jun-1

2

Jul-1

2

Aug-1

2

Sep-1

2

Oct-1

2

Nov-1

2

Dec-1

2

260

280

300

320

340

Jan-1

2

Feb

-12

Ma

r-12

Apr-1

2

Ma

y-12

Jun-1

2

Jul-1

2

Aug-1

2

Sep-1

2

Oct-1

2

Nov-1

2

Dec-1

2

90

100

110

120

130

Jan-1

2

Feb-1

2

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Aug

-12

Sep

-12

Oct-1

2

Nov-1

2

Dec-1

2

440

460

480

500

520

540

560

580

Jan-1

2

Feb

-12

Mar-1

2

Apr-1

2

May-1

2

Jun-1

2

Jul-1

2

Aug-12

Sep-12

Oct-1

2

Nov-12

Dec-12

Regional Market Focus

30 January 2013

8 of 15

Valuations of Major Regional Markets

14.7 1.48

13.6 2.49

11.5 1.58

14.1 2.90

14.8 1.95

Source: Bloomberg

Jakarta Stock Exchange Composite Index, P/B (X)

Straits Times Index, Forward P/E (X)

Hang Seng Index, Forward P/E (X)

Straits Times Index, P/B (X)

Stock Exchange of Thailand, Forward P/E (X) Stock Exchange of Thailand, P/B (X)

Jakarta Stock Exchange Composite Index,

Hang Seng Index, P/B (X)

S&P/ASX 200 Index, Forward P/E (X) S&P/ASX 200 Index, P/B (X)

10

12

14

16

18

Dec-0

9

Fe

b-1

0

Ap

r-10

Ju

n-1

0

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Ju

n-1

1

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Ju

n-1

2

Au

g-1

2

Oct-1

2

Dec-1

2

1.0

1.2

1.4

1.6

1.8

2.0

Dec-0

9

Fe

b-1

0

Ap

r-10

Ju

n-1

0

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Ju

n-1

1

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Ju

n-1

2

Au

g-1

2

Oct-1

2

Dec-1

2

1.0

1.5

2.0

2.5

Dec-0

9

Fe

b-1

0

Ap

r-10

Ju

n-1

0

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Ju

n-1

1

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Ju

n-1

2

Au

g-1

2

Oct-1

2

Dec-1

2

8

10

12

14

16

Dec-0

9

Fe

b-1

0

Ap

r-10

Ju

n-1

0

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Ju

n-1

1

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Ju

n-1

2

Au

g-1

2

Oct-1

2

Dec-1

2

1.01.21.41.61.82.02.2

Dec-0

9

Fe

b-1

0

Ap

r-10

Ju

n-1

0

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Ju

n-1

1

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Ju

n-1

2

Au

g-1

2

Oct-1

2

Dec-1

2

8

10

12

14

16

Dec-0

9

Fe

b-1

0

Ap

r-10

Ju

n-1

0

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Ju

n-1

1

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Ju

n-1

2

Au

g-1

2

Oct-1

2

Dec-1

2

2.22.42.62.83.03.23.43.6

Dec-0

9

Fe

b-1

0

Ap

r-10

Ju

n-1

0

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Ju

n-1

1

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Ju

n-1

2

Au

g-1

2

Oct-1

2

Dec-1

2

10

12

14

16

18

20

Dec-0

9

Fe

b-1

0

Ap

r-10

Ju

n-1

0

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Ju

n-1

1

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Ju

n-1

2

Au

g-1

2

Oct-1

2

Dec-1

2

1.4

1.6

1.8

2.0

2.2

Dec-0

9

Fe

b-1

0

Ap

r-10

Ju

n-1

0

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Ju

n-1

1

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Ju

n-1

2

Au

g-1

2

Oct-1

2

Dec-1

2

8

10

12

14

16

18

Dec-0

9

Fe

b-1

0

Ap

r-10

Ju

n-1

0

Au

g-1

0

Oct-1

0

Dec-1

0

Fe

b-1

1

Ap

r-11

Ju

n-1

1

Au

g-1

1

Oct-1

1

Dec-1

1

Fe

b-1

2

Ap

r-12

Ju

n-1

2

Au

g-1

2

Oct-1

2

Dec-1

2

Regional Market Focus

30 January 2013

9 of 15

Source: Bloomberg

World Index

JCI 0.50% 4,439.03

HSI -0.07% 23,655.17

KLCI 0.01% 1,637.34

NIKKEI 0.39% 10,866.72

KOSPI 0.84% 1,955.96

SET 0.46% 1,478.77

SHCOMP 0.53% 2,358.98

SENSEX -0.56% 19,990.90

ASX 1.11% 4,888.98

FTSE 100 0.71% 6,339.19

DOW 0.52% 13,954.42

S&P 500 0.51% 1,507.84

NASDAQ -0.02% 3,153.66 COLOMBO -0.93% 5,800.75

STI -0.43% 3,259.75

Regional Market Focus

30 January 2013

10 of 15

Date Statistic For Survey Prior Date Statistic For Survey Prior

1/30/2013 MBA Mortgage Applications 25-Jan -- 7.00% 1/31/2013 Unemployment Rate (sa) 4Q P 2.00% 1.90%

1/30/2013 ADP Employment Change Jan 165K 215K 1/31/2013 Credit Card Bad Debts Dec -- 20.0M

1/30/2013 GDP QoQ (Annualized) 4Q A 1.10% 3.10% 1/31/2013 Credit Card Billings Dec -- 3412.9M

1/30/2013 Personal Consumption 4Q A 2.10% 1.60% 1/31/2013 Bank Loans & Advances (YoY) Dec -- 15.90%

1/30/2013 GDP Price Index 4Q A 1.50% 2.70% 1/31/2013 M1 Money Supply (YoY) Dec -- 5.30%

1/30/2013 Core PCE QoQ 4Q A 1.00% 1.10% 1/31/2013 M2 Money Supply (YoY) Dec -- 6.20%

1/31/2013 FOMC Rate Decision 30-Jan 0.25% 0.25% 2/4/2013 Electronics Sector Index Jan -- 46.6

1/31/2013 Challenger Job Cuts YoY Jan -- -22.10% 2/4/2013 Purchasing Managers Index Jan -- 48.6

1/31/2013 Employment Cost Index 4Q 0.50% 0.40% 2/6/2013 Automobile COE Open Bid Cat A 6-Feb -- 91010

1/31/2013 Personal Income Dec 0.80% 0.60% 2/6/2013 Automobile COE Open Bid Cat B 6-Feb -- 95501

1/31/2013 Personal Spending Dec 0.30% 0.40% 2/6/2013 Automobile COE Open Bid Cat E 6-Feb -- 97889

1/31/2013 PCE Deflator (MoM) Dec 0.00% -0.20% 2/7/2013 Foreign Reserves Jan -- $259.31B

1/31/2013 PCE Deflator (YoY) Dec 1.40% 1.40% 10-22 FEB GDP (annualized) (QoQ) 4Q F -- 1.80%

1/31/2013 PCE Core (MoM) Dec 0.10% 0.00% 10-22 FEB GDP (YoY) 4Q F -- 1.10%

1/31/2013 PCE Core (YoY) Dec 1.40% 1.50% 2/15/2013 Retail Sales Ex Auto (YoY) Dec -- 2.00%

Date Statistic For Survey Prior Date Statistic For Survey Prior

29-31 JAN Total Car Sales Dec -- 148243 1/30/2013 Money Supply M3 - in HK$ (YoY) Dec -- 10.90%

1/31/2013 Total Exports in US$ Million Dec -- $19332M 1/30/2013 Money Supply M2 - in HK$ (YoY) Dec -- 11.00%

1/31/2013 Total Exports YOY% Dec -- 27.10% 1/30/2013 Money Supply M1 - in HK$ (YoY) Dec -- 15.30%

1/31/2013 Total Imports in US$ Million Dec -- $18705M 1/31/2013 Govt Mthly Budget Surp/Def HK$ Dec -- 24.8B

1/31/2013 Total Imports YOY% Dec -- 24.10% 1/31/2013 Retail Sales - Value (YoY) Dec -- 9.50%

1/31/2013 Total Trade Balance Dec -- $627M 1/31/2013 Retail Sales - Volume (YoY) Dec -- 8.10%

1/31/2013 Overall Balance in US$ Million Dec -- $1203M 2/5/2013 Purchasing Managers Index Jan -- 51.7

1/31/2013 Current Account Balance (USD) Dec -$945M $392M 2/7/2013 Foreign Currency Reserves Jan -- $317.3B

1/31/2013 Business Sentiment Index Dec -- 52 2/19/2013 Composite Interest Rate Jan -- 0.32%

2/1/2013 Foreign Reserves 25-Jan -- $182.0B 2/21/2013 Unemployment Rate SA Jan -- 3.30%

2/1/2013 Forw ard Contracts 25-Jan -- $23.0B 2/22/2013 CPI - Composite Index (YoY) Jan -- 3.70%

2/1/2013 Consumer Price Index (YoY) Jan 3.50% 3.63% 2/25/2013 Exports YoY% Jan -- --

2/1/2013 Consumer Price Index NSA (MoM) Jan -- 0.39% 2/25/2013 Imports YoY% Jan -- --

2/1/2013 Core CPI (YoY) Jan 1.65% 1.78% 2/25/2013 Trade Balance Jan -- --

2/7/2013 Consumer Confidence Economic Jan -- 70.6 2/27/2013 Annual GDP 2012 -- --

Source: BloombergSource: Bloomberg

Source: Bloomberg

Thailand Hong Kong

Source: Bloomberg

US Singapore

Economic Announcement

Regional Market Focus

30 January 2013

11 of 15

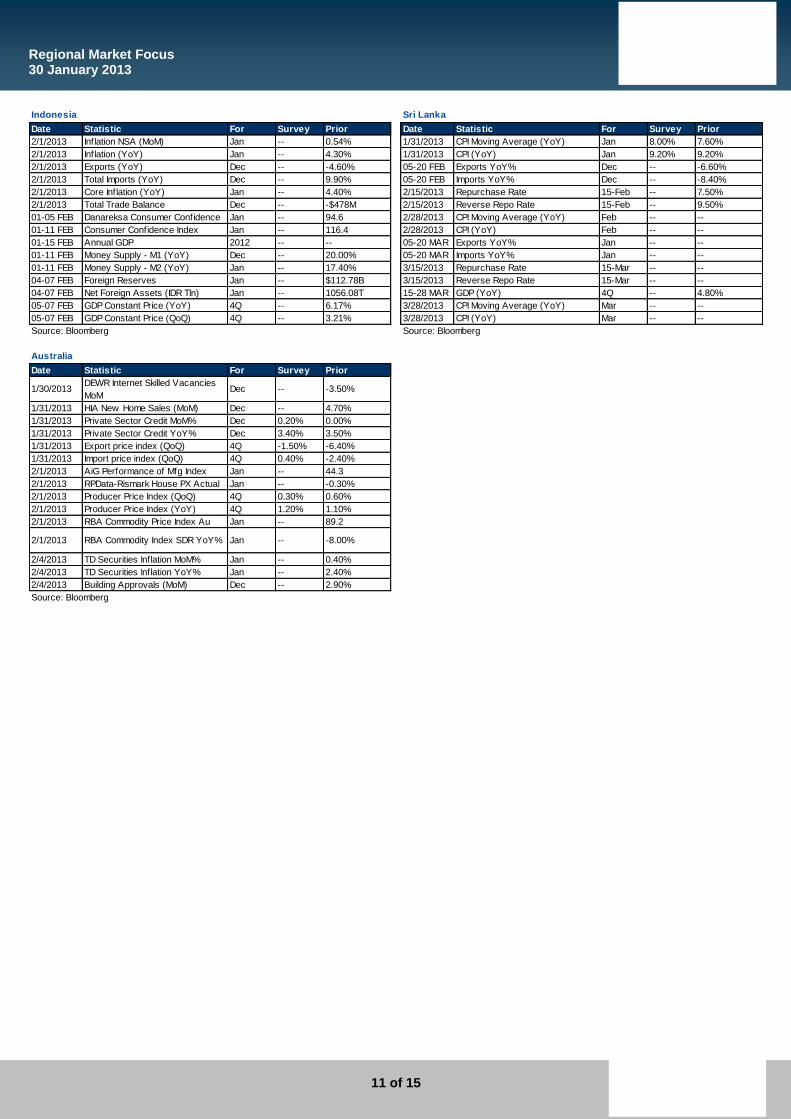

Date Statistic For Survey Prior Date Statistic For Survey Prior

2/1/2013 Inflation NSA (MoM) Jan -- 0.54% 1/31/2013 CPI Moving Average (YoY) Jan 8.00% 7.60%

2/1/2013 Inflation (YoY) Jan -- 4.30% 1/31/2013 CPI (YoY) Jan 9.20% 9.20%

2/1/2013 Exports (YoY) Dec -- -4.60% 05-20 FEB Exports YoY% Dec -- -6.60%

2/1/2013 Total Imports (YoY) Dec -- 9.90% 05-20 FEB Imports YoY% Dec -- -8.40%

2/1/2013 Core Inflation (YoY) Jan -- 4.40% 2/15/2013 Repurchase Rate 15-Feb -- 7.50%

2/1/2013 Total Trade Balance Dec -- -$478M 2/15/2013 Reverse Repo Rate 15-Feb -- 9.50%

01-05 FEB Danareksa Consumer Confidence Jan -- 94.6 2/28/2013 CPI Moving Average (YoY) Feb -- --

01-11 FEB Consumer Confidence Index Jan -- 116.4 2/28/2013 CPI (YoY) Feb -- --

01-15 FEB Annual GDP 2012 -- -- 05-20 MAR Exports YoY% Jan -- --

01-11 FEB Money Supply - M1 (YoY) Dec -- 20.00% 05-20 MAR Imports YoY% Jan -- --

01-11 FEB Money Supply - M2 (YoY) Jan -- 17.40% 3/15/2013 Repurchase Rate 15-Mar -- --

04-07 FEB Foreign Reserves Jan -- $112.78B 3/15/2013 Reverse Repo Rate 15-Mar -- --

04-07 FEB Net Foreign Assets (IDR Tln) Jan -- 1056.08T 15-28 MAR GDP (YoY) 4Q -- 4.80%

05-07 FEB GDP Constant Price (YoY) 4Q -- 6.17% 3/28/2013 CPI Moving Average (YoY) Mar -- --

05-07 FEB GDP Constant Price (QoQ) 4Q -- 3.21% 3/28/2013 CPI (YoY) Mar -- --

Date Statistic For Survey Prior

1/30/2013DEWR Internet Skilled Vacancies

MoMDec -- -3.50%

1/31/2013 HIA New Home Sales (MoM) Dec -- 4.70%

1/31/2013 Private Sector Credit MoM% Dec 0.20% 0.00%

1/31/2013 Private Sector Credit YoY% Dec 3.40% 3.50%

1/31/2013 Export price index (QoQ) 4Q -1.50% -6.40%

1/31/2013 Import price index (QoQ) 4Q 0.40% -2.40%

2/1/2013 AiG Performance of Mfg Index Jan -- 44.3

2/1/2013 RPData-Rismark House PX Actual Jan -- -0.30%

2/1/2013 Producer Price Index (QoQ) 4Q 0.30% 0.60%

2/1/2013 Producer Price Index (YoY) 4Q 1.20% 1.10%

2/1/2013 RBA Commodity Price Index Au Jan -- 89.2

2/1/2013 RBA Commodity Index SDR YoY% Jan -- -8.00%

2/4/2013 TD Securities Inflation MoM% Jan -- 0.40%

2/4/2013 TD Securities Inflation YoY% Jan -- 2.40%

2/4/2013 Building Approvals (MoM) Dec -- 2.90%

Source: Bloomberg

Source: Bloomberg

Indonesia

Australia

Sri Lanka

Source: Bloomberg

PHILLIP RESEARCH STOCK SELECTION SYSTEMS

BUY >15% upside from the current price

HOLD Trade within ± 15% from the current price

SELL >15% downside from the current price

We do not base our recommendations entirely on the above quantitative return bands. We consider qualitative factors

like (but not limited to) a stock's risk reward profile, market sentiment, recent rate of share price appreciation, presence or

absence of stock price catalysts, and speculative undertones surrounding the stock, before making our final

recommendation

GENERAL DISCLAIMER

This publication is prepared by Phillip Securities (Hong Kong) Ltd (“Phillip Securities”). By receiving or reading this

publication, you agree to be bound by the terms and limitations set out below.

This publication shall not be reproduced in whole or in part, distributed or published by you for any purpose. Phillip

Securities shall not be liable for any direct or consequential loss arising from any use of material contained in this

publication.

The information contained in this publication has been obtained from public sources which Phillip Securities has no reason

to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”)

contained in this publication are based on such information and are expressions of belief only. Phillip Securities has not

verified this information and no representation or warranty, express or implied, is made that such information or Research

is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in this

publication is subject to change, and Phillip Securities shall not have any responsibility to maintain the information or

Research made available or to supply any corrections, updates or releases in connection therewith. In no event will Phillip

Securities be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of

the information or Research made available, even if it has been advised of the possibility of such damages.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this material are as of the date

indicated and are subject to change at any time without prior notice.

This material is intended for general circulation only and does not take into account the specific investment objectives,

financial situation or particular needs of any particular person. The products mentioned in this material may not be suitable

for all investors and a person receiving or reading this material should seek advice from a financial adviser regarding the

suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of

that person, before making a commitment to invest in any of such products.

This publication should not be relied upon as authoritative without further being subject to the recipient’s own independent

verification and exercise of judgment. The fact that this publication has been made available constitutes neither a

recommendation to enter into a particular transaction nor a representation that any product described in this material is

suitable or appropriate for the recipient. Recipients should be aware that many of the products which may be described in

this publication involve significant risks and may not be suitable for all investors, and that any decision to enter into

transactions involving such products should not be made unless all such risks are understood and an independent

determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein

with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks.

Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of a security. Any decision to

purchase securities mentioned in this research should take into account existing public information, including any

registered prospectus in respect of such security.

Disclosure of Interest

Analyst Disclosure: Neither the analyst(s) preparing this report nor his associate has any financial interest in or serves as

an officer of the listed corporation covered in this report.

Firm’s Disclosure: Phillip Securities does not have any investment banking relationship with the listed corporation covered

in this report nor any financial interest of 1% or more of the market capitalization in the listed corporation. In addition, no

executive staff of Phillip Securities serves as an officer of the listed corporation.

Phillip Securities (HK)Phillip Securities (HK)Phillip Securities (HK)Phillip Securities (HK) Ltd Ltd Ltd Ltd

2

Availability

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or

entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the

applicable law or regulation or which would subject Phillip Securities to any registration or licensing or other requirement,

or penalty for contravention of such requirements within such jurisdiction.

© 2011 Phillip Securities (Hong Kong) Limited

Phillip Capital – Regional Member Companies

SINGAPORE

Phillip Securities Pte Ltd

Raffles City Tower 250, North Bridge Road #06-00

Singapore 179101 Tel : (65) 6533 6001 Fax : (65) 6535 6631

Website : www.poems.com.sg

MALAYSIA

Phillip Capital Management Sdn Bhd

B-2-6 Megan Avenue II 12 Jln Yap Kwan Seng 50450 Kuala Lumpur Tel : (603) 2166 8099 Fax : (603) 2166 5099

Website : www.poems.com.my

HONG KONG

Phillip Securities (HK) Ltd

11-12/F United Centre 95 Queensway, Hong Kong

Tel : (852) 2277 6600 Fax : (852) 2868 5307

Website : www.poems.com.hk

THAILAND

Phillip Securities (Thailand) Public Co Ltd

15/F, Vorawat Building 849 Silom Road

Bangkok Thailand 10500 Tel : (622) 635 7100 Fax : (622) 635 1616

Website : www.poems.in.th

JAPAN

The Naruse Securities Co Ltd

4-2, Nihonbashi Kabutocho Chuo Ku, Tokyo Japan 103-0026

Tel : (81) 03-3666-2101 Fax : (81) 03-3664-0141

Website : www.naruse-sec.co.jp

UNITED KINGDOM King & Shaxson Ltd

6th Floor, Candlewick House

120 Cannon Street London EC4N 6AS

Tel : (44) 207 426 5950 Fax : (44) 207 626 1757

Website : www.kingandshaxson.com