Qatar Business Optimism Survey Q2 2010

Presented by Presented by Dun & Bradstreet South Asia Middle East Ltd.Dun & Bradstreet South Asia Middle East Ltd.Qatar Financial Centre (QFC) Authority Qatar Financial Centre (QFC) Authority

• The D&B Business Optimism Index is recognized world over as an

indicator which ascertains the pulse of the business community

• Provides insight into the short-term outlook of business units on

sales, profit growth, investment, etc.

• Provides analysis of major trends, outlook and issues concerning

the business units

Business Optimism Index

• Sample of business units representing Qatar’s economy was selected

• 500 business owners and senior executives across different industry

sectors were surveyed

• Survey conducted during March 2010 for the 2nd quarter of 2010

• Respondents are asked questions about their expectations on relevant

business parameters

• Survey also captures respondent feedback on current business

conditions

Survey

Composite Business Index

• The Composite Business Index is calculated separately for the hydrocarbon and non hydrocarbon sector

• For the non hydrocarbon sector, the Composite Index captures the weighted aggregate behavior of five individual indices

• For the hydrocarbon sector, the Index takes into account the weighted aggregate behavior of three individual indices

40.3

37.4

40.1

43.2 44.0

48.1 48.2

52.053.2

54.2

51.753.1 53.2 53.6

30.0

35.0

40.0

45.0

50.0

55.0

60.0

Jan-

09

Feb-

09

Mar-0

9

Ap

r-09

May-

…

Jun-

09

Jul-0

9

Aug-

09

Sep-

09

Oct-0

9

No

v-09

Dec-

09

Jan-

10

Feb-

10

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

2008 2009 2010 2011

World Advanced Economies

Emerging and developing economies Middle East

World Economic Outlook

• Global economy expected to grow 3.9% in 2010, emerging economies to expand 6.0%

• US economy registered 5.6% growth in Q4 2009, fastest since third quarter of 2003

• Global composite PMI indicates continued expansion of manufacturing and services

industry activity

Real GDP Growth Global composite manufacturing & services PMI

Source: IMF Source: JP Morgan and market economics

0

5

10

15

20

25

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2007 2008 2009 2010

Crude oil and ref ined petroleum products exports LNG and related exports

Current account Central Bank reserves, net

Real GDP Growth (% Change - RHS)

Economy of Qatar

• Qatar’s real GDP is expected to

expand by 18.1% in 2010

• Continued government support

and increased hydrocarbon

revenues to boost the economy

• Central Bank’s net reserves

estimated at US$ 19.3 bn (2009),

up from US$ 9.8 bn in 2008

Qatar Economic Indicators

740

750

760

770

780

790

800

810

820

Q209 Q309 Q409 2009 Dec-09 Jan-10 Feb-10

Average Oil Production

Source: IMF

Source: OPEC

% C

han

ge

Composite Business Optimism Indices

6966

34

7

2128

24 27

0

10

20

30

40

50

60

70

80

Q308 Q408 Q109 Q209 Q309 Q409 Q110 Q210

95

70

-37

-6 -5

25 2812

-60

-40

-20

0

20

40

60

80

100

120

Q308 Q408 Q109 Q209 Q309 Q409 Q110 Q210

Non Hydrocarbon Sector Hydrocarbon Sector

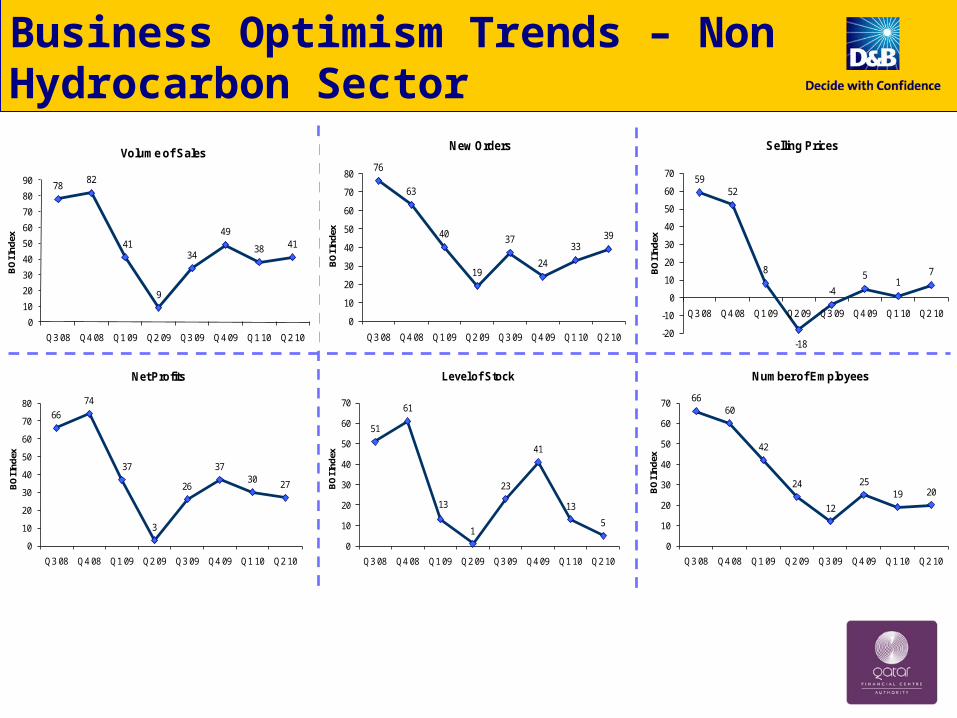

• Business optimism in the non hydrocarbon sector has stabilized in last two quarters

• Drop in selling price optimism becomes a drag on the hydrocarbon sector outlook

Business Optimism Trends – Non Hydrocarbon Sector

76

63

40

19

37

24

3339

0

10

20

30

40

50

60

70

80

Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10B

OI I

ndex

New Orders

5952

8

-18

-4

51

7

-20

-10

0

10

20

30

40

50

60

70

Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10

BO

I Ind

ex

Selling Prices

66

74

37

3

26

3730 27

0

10

20

30

40

50

60

70

80

Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10

BO

I In

dex

Net Profits

51

61

13

1

23

41

13

5

0

10

20

30

40

50

60

70

Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10

BO

I Ind

ex

Level of Stock

6660

42

24

12

2519 20

0

10

20

30

40

50

60

70

Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10

BO

I In

dex

Number of Employees

7882

41

9

34

49

38 41

0

10

20

30

40

50

60

70

80

90

Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10

BO

I In

dex

Volume of Sales

30

35

40

45

50

55

60

Feb-07

Apr-07

Jun-07

Aug-07

Oct-

07

Dec-07

Feb-08

Apr-08

Jun-08

Aug-08

Oct-

08

Dec-08

Feb-09

Apr-09

Jun-09

Aug-09

Oct-

09

Dec-09

Feb-10

63

47

15

50

11

4544

14

1

3220

3338

50

9

32

19 20

54

41

6

39

104

0

10

20

30

40

50

60

70

Volume of Sales

New Orders Level of Selling Prices

Net Profits Number of Employees

Level of Stock

Inde

x

Q3 2009 Q4 2009 Q1 2010 Q2 2010

Manufacturing Sector

• Global manufacturing activity suffers a slight dip, February reading at 56.5 as compared

to 58.4 in the previous month

• Qatar manufacturing sector optimism mixed as volume of sales parameter improves but

new orders decline

Global Manufacturing Purchasing Managers’ Index

Source: JP Morgan and market economics

BOI - Manufacturing Sector GDP

8.3%

19 21

-19

14

4 4

71

38

16

59

40

58

27 30

-7

33

169

26

43

5

2024

8

-30

-20

-10

0

10

20

30

40

50

60

70

80

Volume of Sales

New Orders Level of Selling Prices

Net Profits Number of Employees

Level of Stock

Ind

ex

Q3 2009 Q4 2009 Q1 2010 Q2 2010

GDP

4.9%

Construction Sector

• Global construction sector currently driven by infrastructure spending as commercial

property undergoes correction

• Demand outlook for Qatar’s construction sector shows signs of improvement with increasing

optimism on new orders

• Profitability levels are expected to stay muted due to higher raw material costs

BOI – Construction Sector

13

31

-9

-3

-76

43

3

15

28

16

35

2420

-5

20 19

8

33 33

-5

10

27

5

-20

-10

0

10

20

30

40

50

Volume of Sales

New Orders Level of Selling Prices

Net Profits Number of Employees

Level of Stock

Ind

ex

Q3 2009 Q4 2009 Q1 2010 Q2 2010

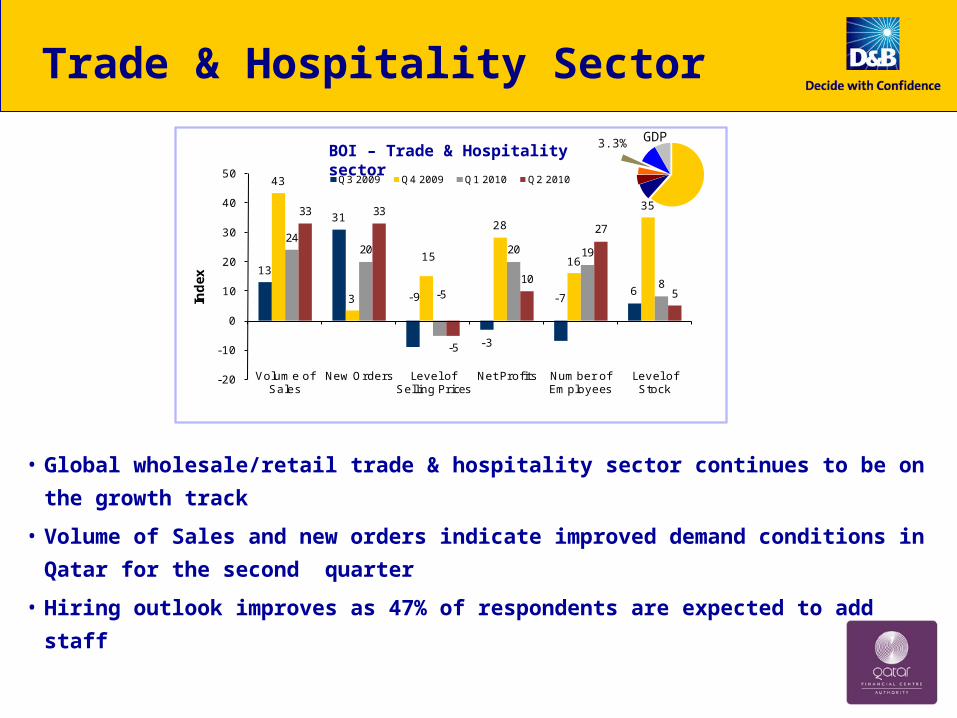

Trade & Hospitality Sector

• Global wholesale/retail trade & hospitality sector continues to be on the growth track

• Volume of Sales and new orders indicate improved demand conditions in Qatar for the

second quarter

• Hiring outlook improves as 47% of respondents are expected to add staff

BOI – Trade & Hospitality sectorGDP3.3%

24

45

0

2522

31

-12 -5

232826

35

-16 3

15

31

23

38

20

-20

-10

0

10

20

30

40

50

Volume of Sales

New Orders Level of Selling Prices

Net Profits Number of Employees

Ind

ex

Q3 2009 Q4 2009 Q1 2010 Q2 2010

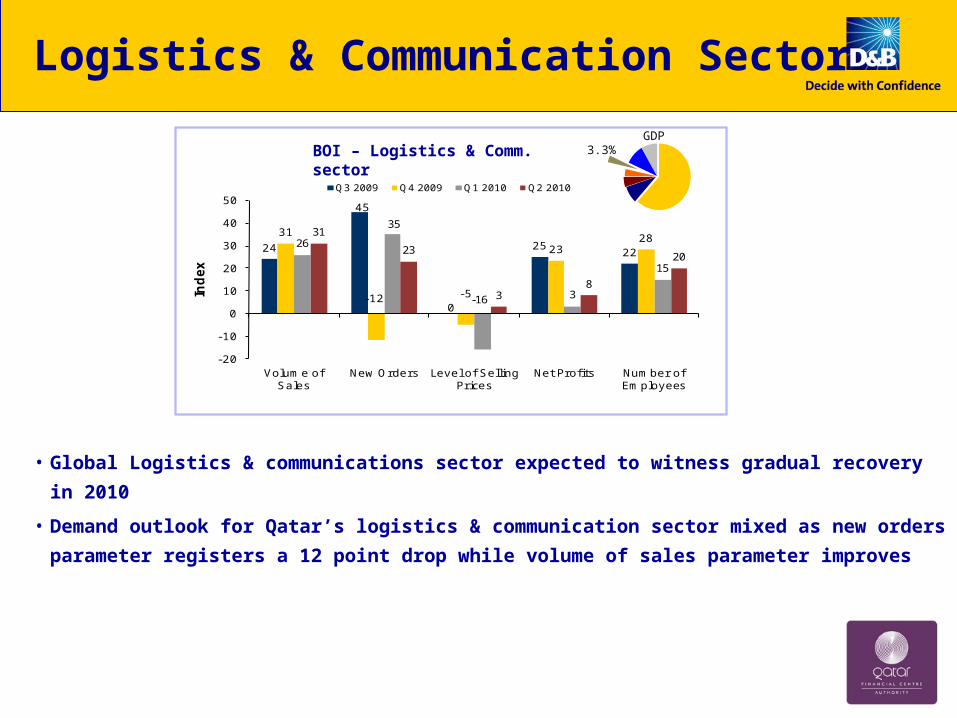

Logistics & Communication Sector

• Global Logistics & communications sector expected to witness gradual recovery in 2010

• Demand outlook for Qatar’s logistics & communication sector mixed as new orders

parameter registers a 12 point drop while volume of sales parameter improves

BOI – Logistics & Comm. sectorGDP

3.3%

38.6

41.543.7 43.2

47.4 46.5

50.552.6 53.0

50.351.8 51.2

52.6

30

35

40

45

50

55

Feb

-09

Mar

-09

Apr

-09

May

-09

Jun

-09

Jul-

09

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan

-10

Feb

-10

33 35

-10

2521

50 50

4

37

22

55

26

10

41

24

4743

13

38

24

-20

-10

0

10

20

30

40

50

60

Volume of Sales

New Orders Level of Selling Prices

Net Profits Number of Employees

Inde

x

Q3 2009 Q4 2009 Q1 2009 Q2 2010

Finance and Business Services Sector

• The Global Services PMI reading suggests continued expansion of business activity

• Half of the respondents in Qatar’s Financial and Business Services sector expect to get new

orders in Q2 2010

• Sector outlook with regards to Net Profit and Number of Employees shows signs of stabilization

BOI – Finance & Business Services sectorGDP9.9%

Source: JP Morgan and market economics

Global Services Purchasing Managers’ Index

38.641.5 41.4

45.850.2

55.8

69.6

64.6

71.467.2

72.776.3

74.076.0

73.077.2

30.0

40.0

50.0

60.0

70.0

80.0

Dec

-08

Jan

-09

Feb

-09

Mar

-09

Apr

-09

May

-09

Jun

-09

Jul-

09

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan

-10

Feb

-10

Mar

-10

-20

-10

0

10

20

30

40

50

Q2 09 Q3 09 Q4 09 Q1 10 Q2 10

Ind

ex

Level of Selling Prices Net Prof its New Employees

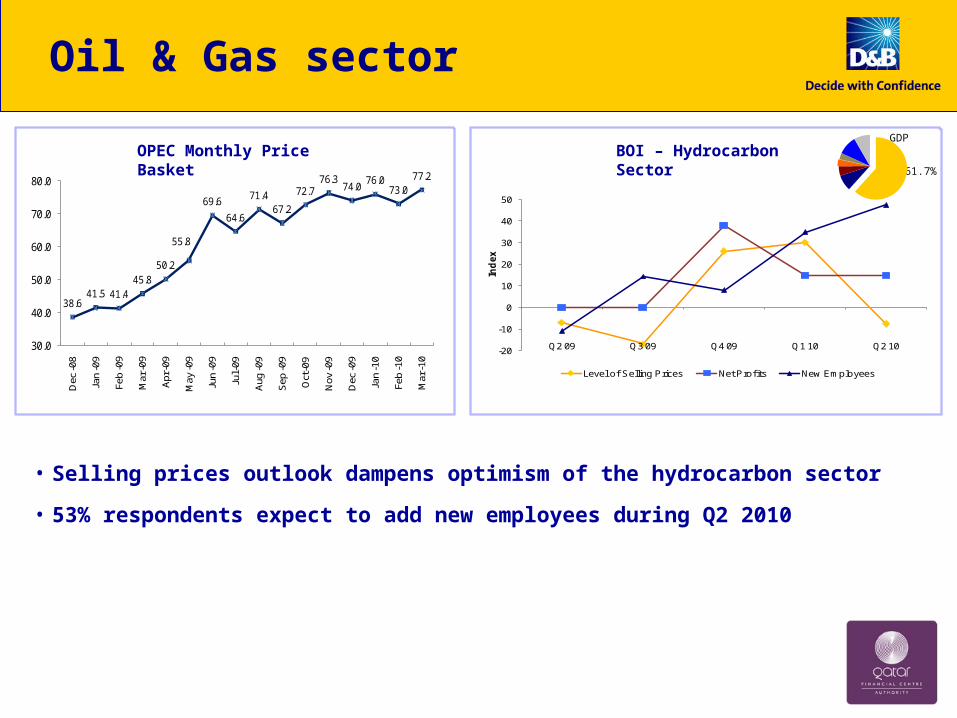

Oil & Gas sector

• Selling prices outlook dampens optimism of the hydrocarbon sector

• 53% respondents expect to add new employees during Q2 2010

GDP

61.7%

BOI – Hydrocarbon SectorOPEC Monthly Price Basket

Other Key Highlights

•Raw materials cost continues to be a major concern for the manufacturing sector •37% of the non hydrocarbon respondents expect borrowing conditions to improve during the quarter

•One third of companies in the non hydrocarbon sector plan to invest in business expansion

•60% of companies in the hydrocarbon sector expect to face project delays

Conclusion

• Business Optimism levels in Qatar’s non hydrocarbon sector improve slightly in Q2 2010

• Improvement in volume of sales and new orders indicates stable demand outlook for the non hydrocarbon sector

• Qatar’s trade and hospitality sector expect better demand conditions in the second quarter

• Despite turbulence witnessed in the international financial markets during the last quarter, optimism levels in finance & business services sector registers a minor improvement

THANK YOU THANK YOU