Thailand’s Financial and Banking Systems

By Plearnpit Satsanguan

and Sukanda Lewis

Faculty of Economics Thammasat University

1

Thailand’s Financial and Banking Systems

1. Introduction

Thailand’s financial system, which is dominated by the banking sector,

remained robust in 2008 despite the economic slowdown due to the global financial

crisis which began in the summer of 2007.

The performances of Thai authorities in managing its money and banking

affairs in 1960s and 1970s were impressive, partly due to successful development and

diversification of its financial institutions. “However, economic imbalances in the

early 1980s and the rising tendency of government intervention put the financial

sector under stress, thus reducing its efficiency in resource mobilization and

allocation (U.S. Library of Congress).” During the 1980s and early 1990s the Thai

financial institutions particularly under the supervision of the Bank of Thailand, the

Central Bank, had been under the process of financial liberalization that includes

deregulation of international capital flows, a movement toward a more flexible

exchange rate system, and financial innovation. In order to reach the ambitious goal

of turning Bangkok to be a regional financial center, the Bangkok International

Banking Facilities, BIBFs, was established in 1993 which eventually led to the East

Asian Financial Crisis in 1997.

The purpose of this paper is to explore the development of Thailand’s

financial and banking systems. The current situations of Thailand’s financial and

banking systems are also discussed. In addition, the paper covers the recent financial

reforms and the weaknesses in the financial sector as well.

This paper is organized as follows. Section 2 describes the overview of Thailand’s

Financial and Banking Sector. Section 3 summarizes the recent financial sector

reform. Section 4 outlines various policy measures toward financial liberalization

between the late 1980s and the early 1990s. Section 5 addresses the current

weaknesses in the Thai Financial Sector.

2. Overview of the Thai Financial System

Thailand’s financial system can be classified into four major constituents,

namely: i) commercial banks; ii) capital markets (including both the stock and bond

markets); iii) government-owned specialized financial institutions (SFIs); and iv) non-

2

bank financial intermediaries comprising finance companies, credit foncier

companies, life insurance companies, and various co-operatives (Disyatat and

Nakornthab, 2003: 3).

2.1 Commercial Banks

Table 1, which provides some salient features of these four constituents as of

end-2002 and end-2008, indicates that commercial banks are the oldest financial

institutions and dominate the Thai financial system, accounting for 56 percent of total

financial sector assets (excluding capital markets) at the end of 2008. As of March

2009, there were 14 domestic banks, 16 foreign bank branches, 3 retail banks and one

subsidiary.

Commercial banks in Thailand are allowed to undertake universal banking.

Banks can offer a wide range of financial services in both traditional and investment

banking. Between 2004 and 2008, the local banks were focused primarily on

commercial banking, with interest income accounting for about 80 percent of total

income. Currently, banks turn from traditional corporate banking to retail banking and

SME businesses because they offered better diversification and enhance profit. Facing

with intense competition in the banking sector, “banks implemented competitive

strategy including modernizing their services, expanding their networks, and

differentiating themselves by offering more financial products such as short-term bills

of exchange (B/E), special deposits, and cross-selling of products such as by acting as

broker for life insurance and selling of mutual fund products (Bank of Thailand,

Supervision Report 2007: 13).”

Before the financial crisis in 1997, Thailand’s financial system can be

described as ‘bank-based’, with commercial banks dominating the landscape.

However, after the crisis, the role of the banking sector becomes less prominent, as

shown in Table 2. As of 2008, the banking sector still had the largest share of the

whole financial system. However, the stock market and the bond market have more

important presence.

Changing Financial Landscape

The structure of the Thai financial sector has changed significantly since the

financial crisis. Before the crisis, the financial sector consisted of a large number of

3

financial institutions, and was heavily dominated by finance and securities companies.

Of the total 176 financial institutions under the supervision of the Bank of Thailand,

there were 91 finance and securities companies.

Due to closures and mergers of many finance and securities companies after

the crisis, this landscape changed. As of December 31, 2003, there were only 18

finance and securities companies left operating. Figure 1 shows the changing

composition of the financial institutions under the supervision of the Bank of Thailand

from 1997 to 2003 and 2009. Since 2003, the change in financial landscape has

continued.

4

Table 1: Major Constituents of Thailand’s Financial System

Constituent First Est.

No. Total assets/values ( Bt b)

Share of Total Financial institution Assets (%)

2002 2008 2002 2008 2002 2008

1. Commercial banks

Domestic banks 1906 13 18 5,780 8,774 59.4 56.2 Foreign bank branch 1888 18 16 686 1,274 7.0 8.2

2. Capital markets

SET market capitalization 1975 N.A. N.A. 1,986 3,568 N.A. N.A. Public bonds Outstanding 1933 N.A. N.A. 1,757 4,002 N.A. N.A. Corporate bonds Outstanding 1992 N.A. N.A. 543 1,002 N.A. N.A. Securities companies 1953 39 43 51 146 0.5 0.9 Mutual fund companies 1975 14 22 467 1,525 4.8 9.8

3. Specialized Financial Institutions (SFIs)

Government Savings Bank 1913 1 1 600 772 1 6.2 4.9

BAAC 1966 1 1 396 631 4.1 4.0

Government Housing Bank 1953 1 1 362 647 2 3.7 4.1

IFCT 3 1959 1 N.A. 210 N.A. 2.2 N.A.

Export-Import Bank 1993 1 1 48 60 0.5 0.4

SME Bank (formerly SIFC) 1992 1 1 13 49 4 0.1 0.3

Secondary Mortgage Corp. 1997 1 1 2 5 5 0.02 0.01

4. Non-bank financial intermediaries

Finance companies 1969 19 4 254 45 2.6 0.3 Credit Foncier companies 1969 6 3 6 1 0.1 0.0 Life insurance companies 1929 26 25 360 818 6 3.7 5.2

Agricultural cooperatives 1916 4,073 4,343 67 96 7 0.7 0.6

Non-agricultural cooperatives 1937 2,333 3,329 437 781 8 4.5 5.0

Source: BOT; DOI; SET; TBDC 1, 2, 5 Statistics at the end of Quarter3/2008

3 IFCT merged with The Thai Military Bank Public Company Ltd. since 1 September 2004.

4, 6, 7’8 Statistics at the end of the year 2007

5

Table 2: Shares of the Thai Financial System (%)

1996 2002 2008 Bank Loans 61.05 51.78 41.54

Equities (SET market capitalization)

32.38 22.35 28.19

Domestic Bonds (par value) Source: The Thai Bond Market Association

6.57 25.87 30.27

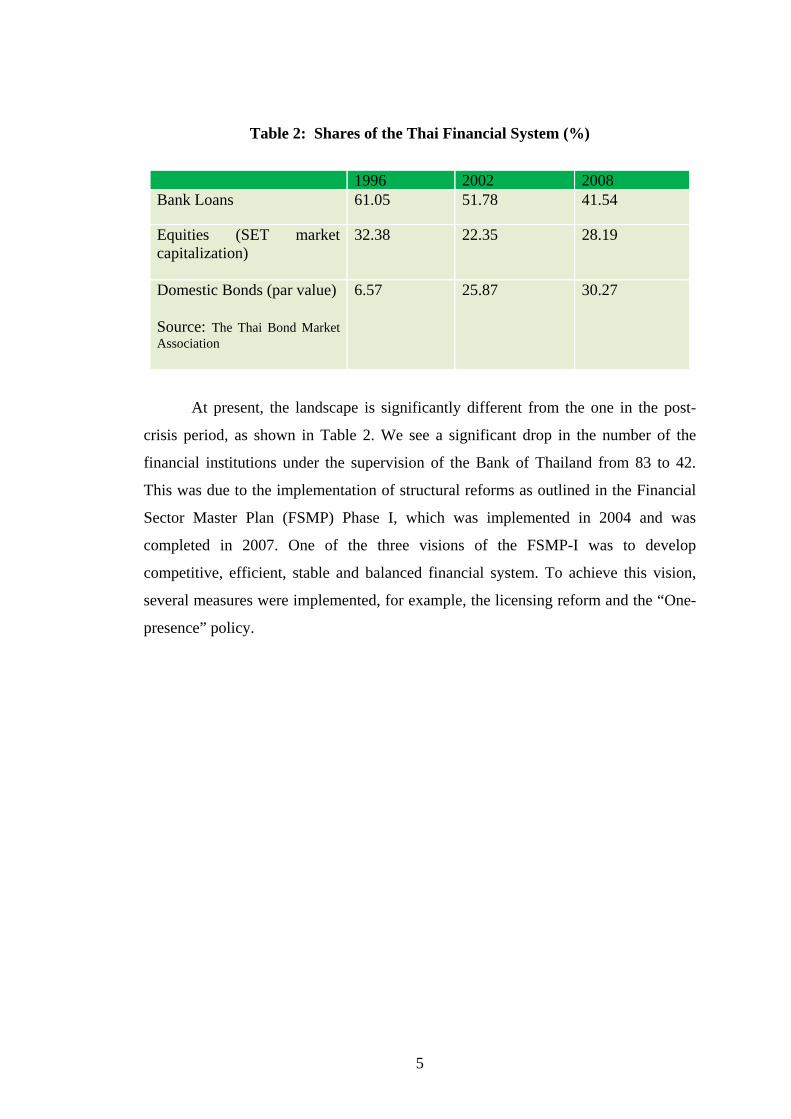

At present, the landscape is significantly different from the one in the post-

crisis period, as shown in Table 2. We see a significant drop in the number of the

financial institutions under the supervision of the Bank of Thailand from 83 to 42.

This was due to the implementation of structural reforms as outlined in the Financial

Sector Master Plan (FSMP) Phase I, which was implemented in 2004 and was

completed in 2007. One of the three visions of the FSMP-I was to develop

competitive, efficient, stable and balanced financial system. To achieve this vision,

several measures were implemented, for example, the licensing reform and the “One-

presence” policy.

6

Figure 1: Structural Changes in Financial Institutions under the Supervision of the Bank of Thailand

Source: Bank of Thailand

According to the Bank of Thailand (BOT)’s Supervision Report 2006, types of

licensing for domestic deposit-taking financial institutions were reduced from six

types- commercial bank, foreign bank branch, International Banking Facilities,

restricted bank, finance company and credit foncier company - to four types -

commercial bank, retail bank, foreign bank branch and subsidiary of a foreign bank.

In addition, the “One-presence” policy requires that individual financial

conglomerates are allowed to have only one deposit-taking financial institution in

their group.

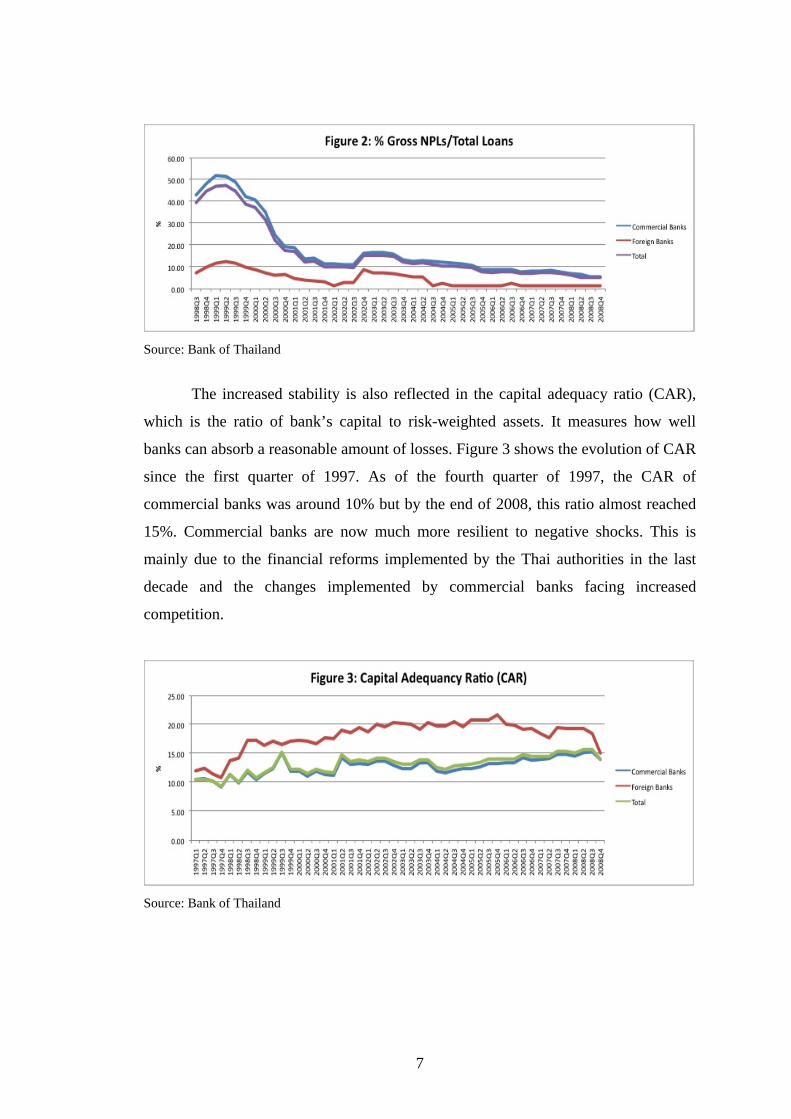

Improved Stability

Since the financial crisis, there has been improvement in the stability of Thai

commercial banks. The ratio of gross non-performing loans (NPLs) to total loans has

been decreasing steadily. As shown in Figure 2, the ratio of gross NPLs to total loans

of commercial banks reached its peak of 50% around the first quarter of 1999, and has

been declining gradually. By the fourth quarter of 2008, they were only around 8% of

total loans. The ratio of NPLs to total loans of foreign banks has been low throughout

the period.

7

Source: Bank of Thailand

The increased stability is also reflected in the capital adequacy ratio (CAR),

which is the ratio of bank’s capital to risk-weighted assets. It measures how well

banks can absorb a reasonable amount of losses. Figure 3 shows the evolution of CAR

since the first quarter of 1997. As of the fourth quarter of 1997, the CAR of

commercial banks was around 10% but by the end of 2008, this ratio almost reached

15%. Commercial banks are now much more resilient to negative shocks. This is

mainly due to the financial reforms implemented by the Thai authorities in the last

decade and the changes implemented by commercial banks facing increased

competition.

Source: Bank of Thailand

8

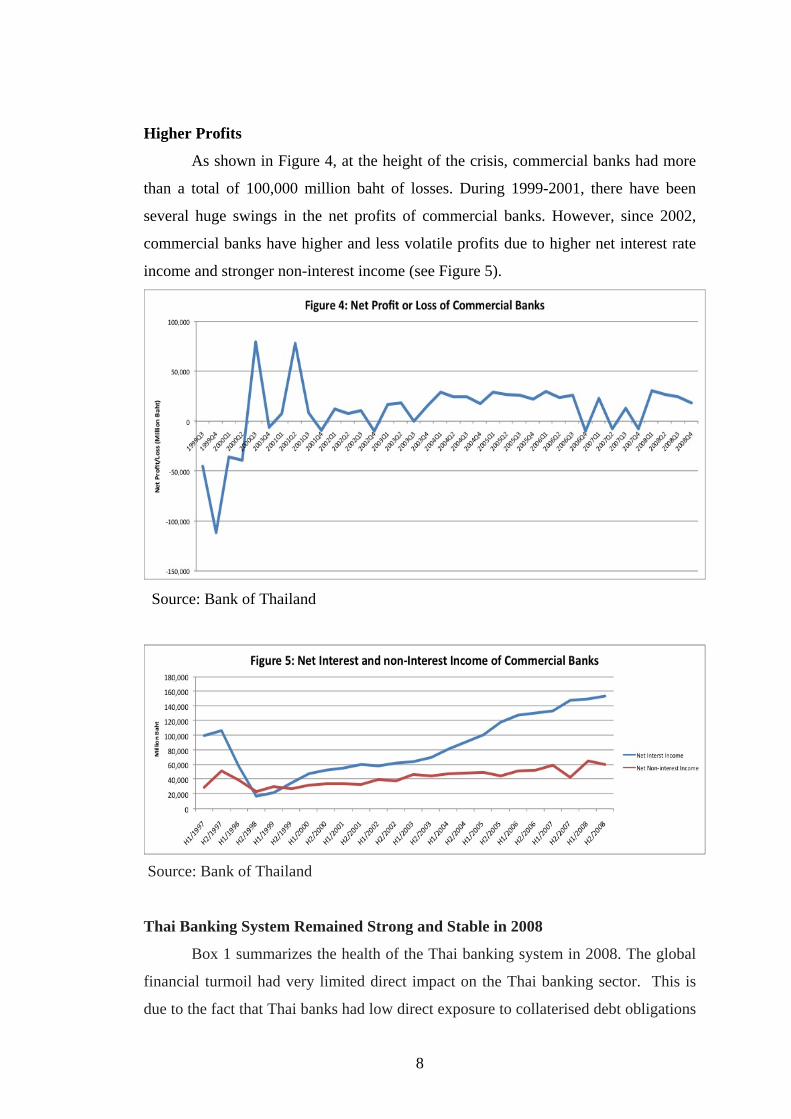

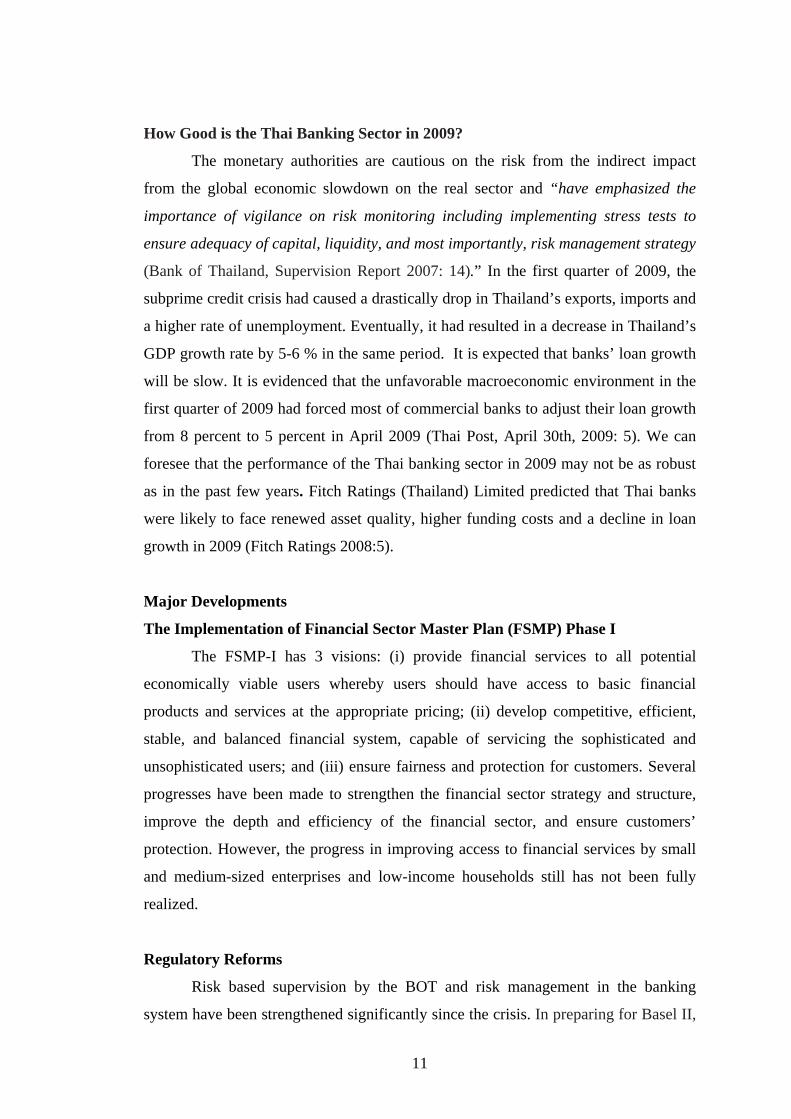

Higher Profits

As shown in Figure 4, at the height of the crisis, commercial banks had more

than a total of 100,000 million baht of losses. During 1999-2001, there have been

several huge swings in the net profits of commercial banks. However, since 2002,

commercial banks have higher and less volatile profits due to higher net interest rate

income and stronger non-interest income (see Figure 5).

Source: Bank of Thailand

Source: Bank of Thailand

Thai Banking System Remained Strong and Stable in 2008

Box 1 summarizes the health of the Thai banking system in 2008. The global

financial turmoil had very limited direct impact on the Thai banking sector. This is

due to the fact that Thai banks had low direct exposure to collaterised debt obligations

9

(CDOs) and other problem assets. As of September 2008, exposure to CDOs was 0.02

percent of total assets (Bank of Thailand, Supervision Report 2007: 38). Moreover,

Thai banks are relying on local deposits as main source of funds. Table 3 confirms

that the local commercial banks had been in solid positions between 2004 and 2008.

Box 1

Thailand’s Banking System Performance in the Year 2008

The banking system recorded a net profit of 99 billion bahts in 2008, up from the previous year when the strengthened NPL provisioning rule, in line with International Accounting Standard No.39, was completed. The strengthened provision helps to ensure that banks have adequate cushion against future risk. Return on asset (ROA) stood at 1% in 2008, while the ratio of capital to risk asset (or the BIS ratio) stood at 14.2% as of December 2008, when the strengthened capital requirement under Basel II became effective. (The ratio as of September was 15.7%, when under the Basel I standards).

Loan growth accelerated in the first nine months but decelerated in the fourth quarter in line with the economic conditions. Overall, loan expanded by 11.4% for the year, up from the 4.7% growth recorded in 2007. Corporate loan (constituting 75.3% of total loan) and consumer loan rose at 10.5% and 14%, respectively. In contrast, deposit growth which fell in the first nine months of the year, accelerated in the fourth quarter, growing by 8.6% for the year, due to increased emphasis on mobilisation of deposit which constitutes core funding for liquidity enhancement, aided by low rate of return of risky assets in line with the downturn in the global stock market. Commercial banks also increased their fund mobilization via borrowing in the form of Bill of Exchange (B/E) which grew by 9.2%. With the convergence of deposit and loan growths, liquidity of the banking system improved, with the ratio of loan to deposit plus B/E easing to 88.3%.

Gross non-performing loans (gross NPLs) amounted to 397 billion bahts – a 56 billion bahts decrease from the end of 2007. The NPL per total loan ratio decreased with gross NPL and net NPL ratios standing at 5.3% and 2.9%, respectively. The decline in NPL resulted from loan repayment, debt restructuring, writing-off, and close monitoring of asset quality to prevent new NPL. The NPL ratio for both consumer and corporate loans decreased. However, there remains pressure on asset quality as indicated by the increase in special mentioned loan (i.e. loans which are past due by over 1 month but not exceeding 3 months), resulting from current global financial crisis which caused the slowdown in domestic and global economy, weighted down on loan repayment ability, thus commercial banks should remain vigilant and closely monitor their asset quality.

Source: Bank of Thailand News

10

Table 3: Domestic Bank's Selected Financial Soundness Indicators

Q4/2004 Q4/2005 Q4/2006 Q4/2007 p Q4/2008 p

Capital Adequacy Ratio (%)

Capital funds/Risk assets 11.94 13.22 13.59 14.80 13.92

Tier 1 Capital/Risk assets 8.71 9.94 10.70 11.86 10.74

Asset Quality (%)

Non - performing loan/Loans 11.94 9.06 8.07 7.86 5.65

Loans/Deposits 87.64 83.15 87.74 92.97 102.65

Liquidity/Deposits and Borrowings n. a. 18.19 16.69 19.57 24.22

Off-balance-sheet Transactions/Assets 43.19 70.48 84.44 128.25 126.77

Loan Classifications (% of Total Loans)

Production 26.14 25.23 25.22 24.52 22.02 Wholesale, Retail Sale and Repair of Motor Vehicles, Motorcycles, Personal and Household goods 18.05 17.34 17.19 16.56 14.44

Financial Intermediation 11.84 11.03 9.82 9.35 17.57

Personal Consumption 16.60 19.02 21.67 23.84 22.62

Profitability (%) Net interest income and dividend/Average net assets (Per year) (NIM) 2.55 2.85 3.16 3.29 3.36

Net profit (loss)/Average net assets (Per year) (ROA) 1.25 1.36 0.77 0.12 1.00

Non-interest income/Total income 25.31 20.98 17.93 16.51 18.48 Source : Bank of Thailand

11

How Good is the Thai Banking Sector in 2009?

The monetary authorities are cautious on the risk from the indirect impact

from the global economic slowdown on the real sector and “have emphasized the

importance of vigilance on risk monitoring including implementing stress tests to

ensure adequacy of capital, liquidity, and most importantly, risk management strategy

(Bank of Thailand, Supervision Report 2007: 14).” In the first quarter of 2009, the

subprime credit crisis had caused a drastically drop in Thailand’s exports, imports and

a higher rate of unemployment. Eventually, it had resulted in a decrease in Thailand’s

GDP growth rate by 5-6 % in the same period. It is expected that banks’ loan growth

will be slow. It is evidenced that the unfavorable macroeconomic environment in the

first quarter of 2009 had forced most of commercial banks to adjust their loan growth

from 8 percent to 5 percent in April 2009 (Thai Post, April 30th, 2009: 5). We can

foresee that the performance of the Thai banking sector in 2009 may not be as robust

as in the past few years. Fitch Ratings (Thailand) Limited predicted that Thai banks

were likely to face renewed asset quality, higher funding costs and a decline in loan

growth in 2009 (Fitch Ratings 2008:5).

Major Developments

The Implementation of Financial Sector Master Plan (FSMP) Phase I

The FSMP-I has 3 visions: (i) provide financial services to all potential

economically viable users whereby users should have access to basic financial

products and services at the appropriate pricing; (ii) develop competitive, efficient,

stable, and balanced financial system, capable of servicing the sophisticated and

unsophisticated users; and (iii) ensure fairness and protection for customers. Several

progresses have been made to strengthen the financial sector strategy and structure,

improve the depth and efficiency of the financial sector, and ensure customers’

protection. However, the progress in improving access to financial services by small

and medium-sized enterprises and low-income households still has not been fully

realized.

Regulatory Reforms

Risk based supervision by the BOT and risk management in the banking

system have been strengthened significantly since the crisis. In preparing for Basel II,

12

the BOT has developed a range of risk management systems and a set of prudential

guidelines to enhance banks’ risk management practices. Furthermore, the BOT has

continuously conducted risk based examination and supervision focusing on strategic

risk, credit risk, market risk, liquidity risk, and operational risk of commercial banks.

The BOT also implements consolidated supervision for commercial banks. So far,

banks have undertaken organizational restructuring to enhance effective risk

management, internal control, and corporate governance, as well as improving risk

management tools.

2.2 Capital Markets

The equity and bond markets make up the second most important constituent

of the Thai financial system.

The Stock Market Thailand’s equity market, the Securities Exchange of Thailand (SET), was

established in 1975. It operates under the legal framework laid down in the Securities

and Exchange Act, B.E. 2535 (1992). It main operations include securities listing,

supervision of listed companies and information disclosure, trading, market

surveillance and member supervision, information dissemination and investor

education (www.set.or.th).

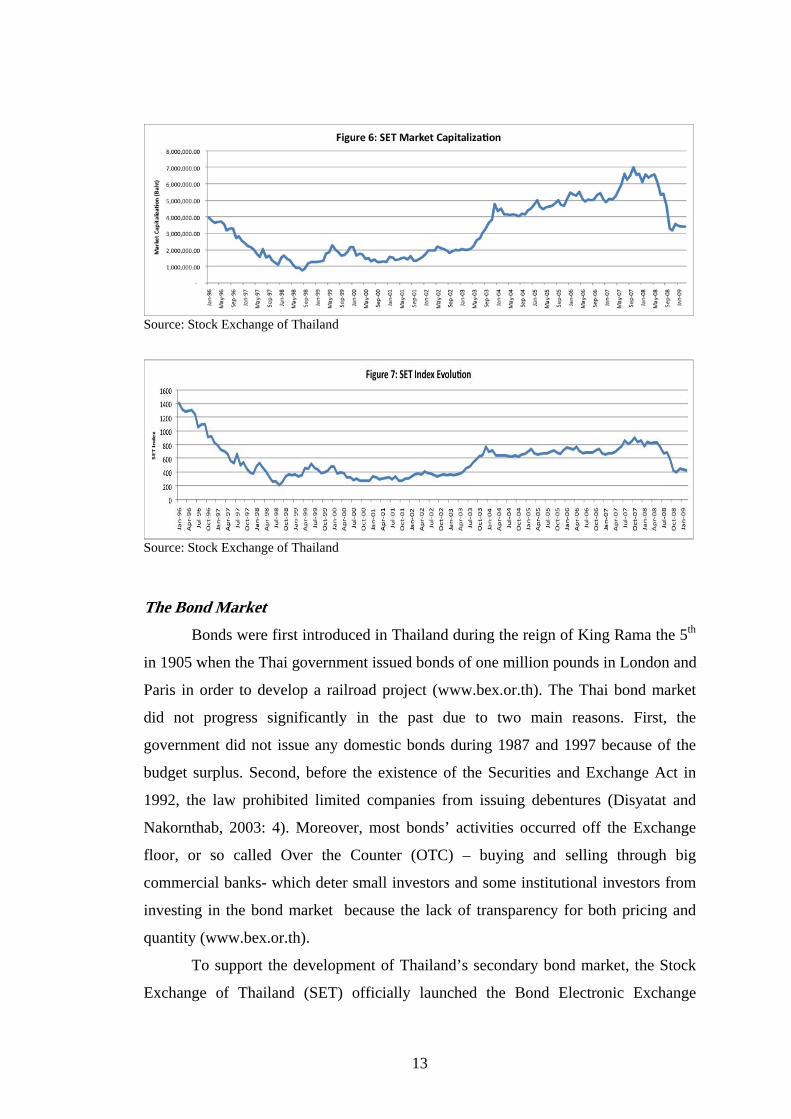

By the end of 1993 SET market capitalization had reached 105 percent of GDP

(Disyatat and Nakornthab, 2003: 4). Figure 6 shows the SET market capitalization

from 1996-2009. The market capitalization faced a major reduction due to the stock

index decline in 2008. As of January 2009, the market capitalization is around USD

100 billion. Figure 7 shows the SET index evolution from 1996 to 2009. The (SET)

was badly affected by the 1997 crisis. The SET Index had experienced sharp declines

since 1996. Before the crisis, the SET Index was over 1200 points. In the middle of

1998, at the height of the crisis, the index dropped to around 200 points. During the

period between 1999 and 2003, the SET index stabilized at around 400 points. Due to

better prospects in the economy, in December 2003, the SET index reached 772

points. The market stabilized at that level for a few years then fell back to 400 points

in November 2008 due to the financial crisis in the United States and negative

domestic factors such as the economic downturn and political turmoil in Thailand.

13

Source: Stock Exchange of Thailand

Source: Stock Exchange of Thailand The Bond Market

Bonds were first introduced in Thailand during the reign of King Rama the 5th

in 1905 when the Thai government issued bonds of one million pounds in London and

Paris in order to develop a railroad project (www.bex.or.th). The Thai bond market

did not progress significantly in the past due to two main reasons. First, the

government did not issue any domestic bonds during 1987 and 1997 because of the

budget surplus. Second, before the existence of the Securities and Exchange Act in

1992, the law prohibited limited companies from issuing debentures (Disyatat and

Nakornthab, 2003: 4). Moreover, most bonds’ activities occurred off the Exchange

floor, or so called Over the Counter (OTC) – buying and selling through big

commercial banks- which deter small investors and some institutional investors from

investing in the bond market because the lack of transparency for both pricing and

quantity (www.bex.or.th).

To support the development of Thailand’s secondary bond market, the Stock

Exchange of Thailand (SET) officially launched the Bond Electronic Exchange

14

(BEX) on November 26th, 2003. The SET committee allowed both government bonds

and corporate issues to be traded in its Exchange. Since the crisis, the size of the

domestic bond market has grown substantially mainly driven by the growth of the

government securities. Figure 8 shows the relative size of the government securities

and the corporate bonds according to the outstanding value. The Thai domestic bond

market is clearly dominated by the government securities. Figure 9 shows the

combination of new issuances of government securities, i.e. Treasury bills, state

agency bonds1, state-owned enterprise bonds, and government bonds. Since 2004, the

new issuance of state agency bonds has increased tremendously.

Source: The Thai Bond Market Association

Source: The Thai Bond Market Association

Before the financial crisis, the market for corporate bonds was virtually

nonexistent. In the first quarter of 1997, the issuance of debt from the corporate sector

amounted to only 3,709 million baht and remained at a very low level for several 1 State agency bonds consist of BOT bonds, Financial Institution Development Fund (FIDF) bonds and Property Loans Management Organization (PLMO) bonds.

15

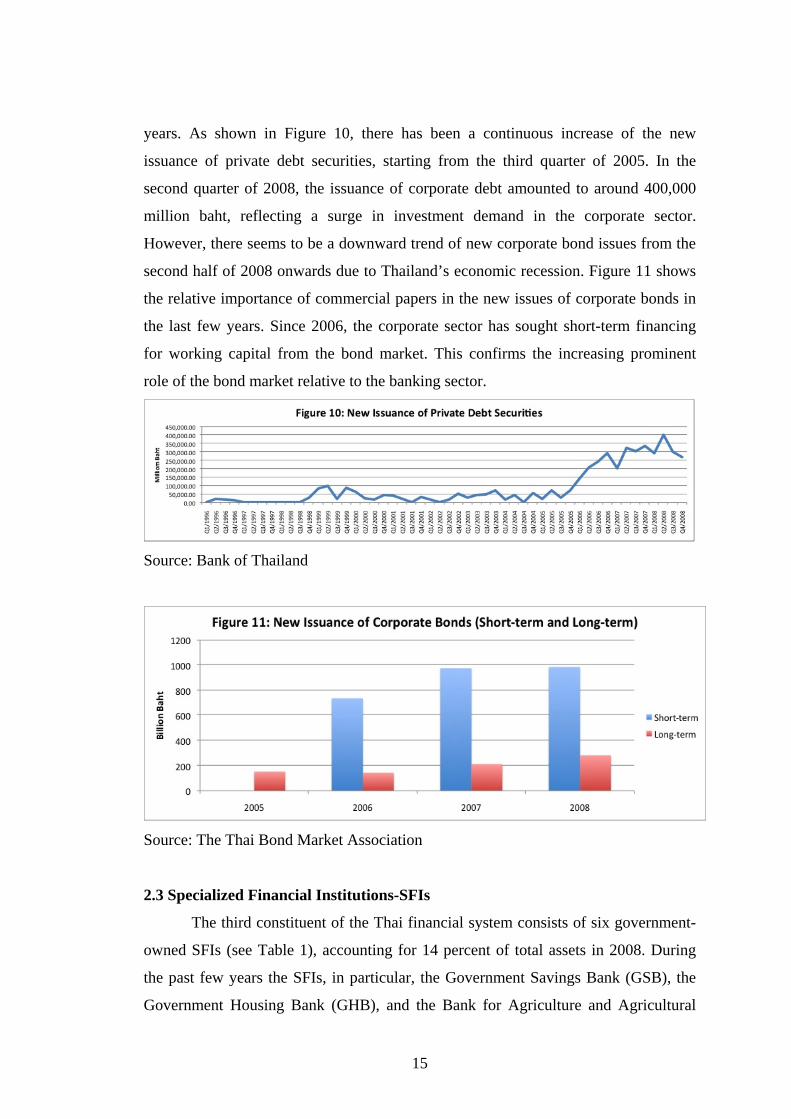

years. As shown in Figure 10, there has been a continuous increase of the new

issuance of private debt securities, starting from the third quarter of 2005. In the

second quarter of 2008, the issuance of corporate debt amounted to around 400,000

million baht, reflecting a surge in investment demand in the corporate sector.

However, there seems to be a downward trend of new corporate bond issues from the

second half of 2008 onwards due to Thailand’s economic recession. Figure 11 shows

the relative importance of commercial papers in the new issues of corporate bonds in

the last few years. Since 2006, the corporate sector has sought short-term financing

for working capital from the bond market. This confirms the increasing prominent

role of the bond market relative to the banking sector.

Source: Bank of Thailand

Source: The Thai Bond Market Association

2.3 Specialized Financial Institutions-SFIs

The third constituent of the Thai financial system consists of six government-

owned SFIs (see Table 1), accounting for 14 percent of total assets in 2008. During

the past few years the SFIs, in particular, the Government Savings Bank (GSB), the

Government Housing Bank (GHB), and the Bank for Agriculture and Agricultural

16

Co-operatives (BAAC), had a more prominent role. This is due to the fact that SFIs

had been actively used by the Thaksin government to carry out the “populist” policies

in extending loans to the underserved segments of the population such as the poor and

small and medium sized enterprises (SMEs).

In Thailand, “SFIs serve as a government’s arm for the economic and social

development as well as certain policy implementation agencies in order to provide

financial assistance to specific sectors of the economy. With the range of services

provided such as housing credits, credits to SMEs, export-import credits or micro-

credits, SFIs are able to reach various types of customers, particularly low-income

groups who are unable to access the service of commercial financial institutions

(Menkhoff and Suwanaporn 2006:7).

The BAAC, established in 1966, has been the main source of credit for

farmers. It was upgraded to be the rural bank in order to provide loans beyond the

agricultural sector.

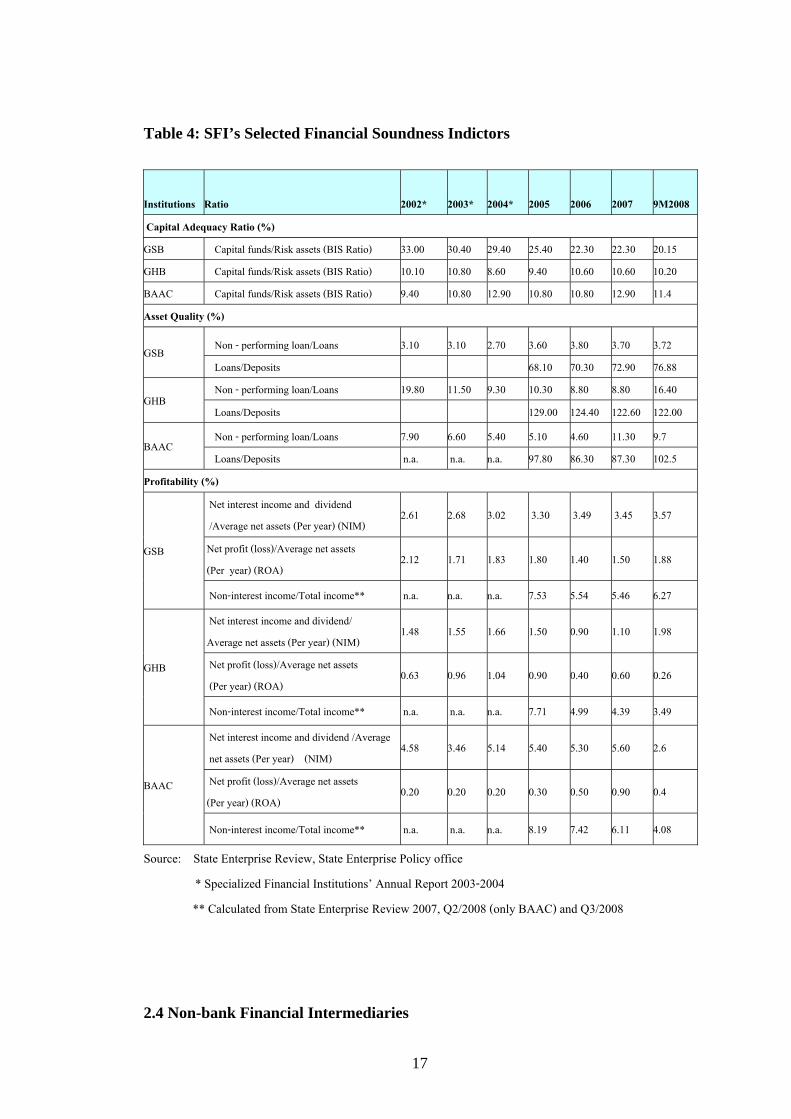

Table 4 presents some financial indicators for the three most important SFIs.

It demonstrates that all of these SFIs maintained Capital Adequacy Ratio-CAR at the

level higher than regulatory requirement. GSB had the highest CAR of 20.15 % in the

third quarter of 2008. Even though ROAs of these SFIs were lower in the third quarter

of 2008, the quality of capital of these SFIs remained strong. For asset quality,

measured by the ratio of NPLs to total loans, only GSB had done a good job. Its

NPLs/Loans ratio was the lowest at 3.72 % in the third quarter of 2008 and lower than

that of local commercial banks. BAAC had made a lot of improvement in its asset

quality in 2008. Its NPLs/Loans was 9.70 % in the third quarter of 2008 which was a

lot lower than in 2007 which stood at 11.30 %. GHB had the worst asset quality. Its

NPLs/Loans was 16.40% in the third quarter of 2008 which was double that of 2007

since GHB had to comply with the “populist” policy implemented by the Thaksin

Government in extending loans to build houses for the poor. It is not surprising for

GHB to have higher NPLs/Loans ratio since its loan/deposit ratio of GHB was so

high. It was 122 % in the third quarter of 2008 while those of BAAC and GSB were

102 % and 76.8 % respectively in the same period. Only GSB had higher return on

assets (ROA) in third quarter of 2008 than that in 2007 whereas ROAs for BAAC and

GHB in the third quarter of 2008 were about half of that in 2007.

17

Table 4: SFI’s Selected Financial Soundness Indictors

Institutions Ratio 2002* 2003* 2004* 2005 2006 2007 9M2008

Capital Adequacy Ratio (%) GSB Capital funds/Risk assets (BIS Ratio) 33.00 30.40 29.40 25.40 22.30 22.30 20.15 GHB Capital funds/Risk assets (BIS Ratio) 10.10 10.80 8.60 9.40 10.60 10.60 10.20 BAAC Capital funds/Risk assets (BIS Ratio) 9.40 10.80 12.90 10.80 10.80 12.90 11.4

Asset Quality (%)

GSB Non - performing loan/Loans 3.10 3.10 2.70 3.60 3.80 3.70 3.72 Loans/Deposits 68.10 70.30 72.90 76.88

GHB Non - performing loan/Loans 19.80 11.50 9.30 10.30 8.80 8.80 16.40

Loans/Deposits 129.00 124.40 122.60 122.00

BAAC Non - performing loan/Loans 7.90 6.60 5.40 5.10 4.60 11.30 9.7 Loans/Deposits n.a. n.a. n.a. 97.80 86.30 87.30 102.5

Profitability (%)

GSB

Net interest income and dividend /Average net assets (Per year) (NIM)

2.61 2.68 3.02 3.30 3.49 3.45 3.57

Net profit (loss)/Average net assets (Per year) (ROA)

2.12 1.71 1.83 1.80 1.40 1.50 1.88

Non-interest income/Total income** n.a. n.a. n.a. 7.53 5.54 5.46 6.27

GHB

Net interest income and dividend/ Average net assets (Per year) (NIM)

1.48 1.55 1.66 1.50 0.90 1.10 1.98

Net profit (loss)/Average net assets (Per year) (ROA)

0.63 0.96 1.04 0.90 0.40 0.60 0.26

Non-interest income/Total income** n.a. n.a. n.a. 7.71 4.99 4.39 3.49

BAAC

Net interest income and dividend /Average net assets (Per year) (NIM)

4.58 3.46 5.14 5.40 5.30 5.60 2.6

Net profit (loss)/Average net assets (Per year) (ROA)

0.20 0.20 0.20 0.30 0.50 0.90 0.4

Non-interest income/Total income** n.a. n.a. n.a. 8.19 7.42 6.11 4.08

Source: State Enterprise Review, State Enterprise Policy office * Specialized Financial Institutions’ Annual Report 2003-2004

** Calculated from State Enterprise Review 2007, Q2/2008 (only BAAC) and Q3/2008

2.4 Non-bank Financial Intermediaries

18

Non-bank Financial Intermediaries are the final constituent of the Thai

financial system, accounting for 11 percent of total Thai financial sector assets in

2008. Life insurance companies play the most important role in this constituent,

accounting for 5.2 percent of total assets whereas the significance of finance

companies is negligible, accounting for only 0.3 percent of total assets as of 2008.

Insurance Industry

The Thai insurance market had been closed for decades until the government

liberalized it in the late 1990s. This has resulted in about 100 insurance companies

operating in the market. In 2009, there are 25 life insurers, 72 non-life insurers and 2

reinsurance companies.

The Thai life insurance industry starts with the establishment of a foreign

company, American Life Assurance, AIA, in 1931. Eleven years later the first Thai

insurance company, Thai Life Insurance, was established (Karim and Jhantasana

2005: 21).

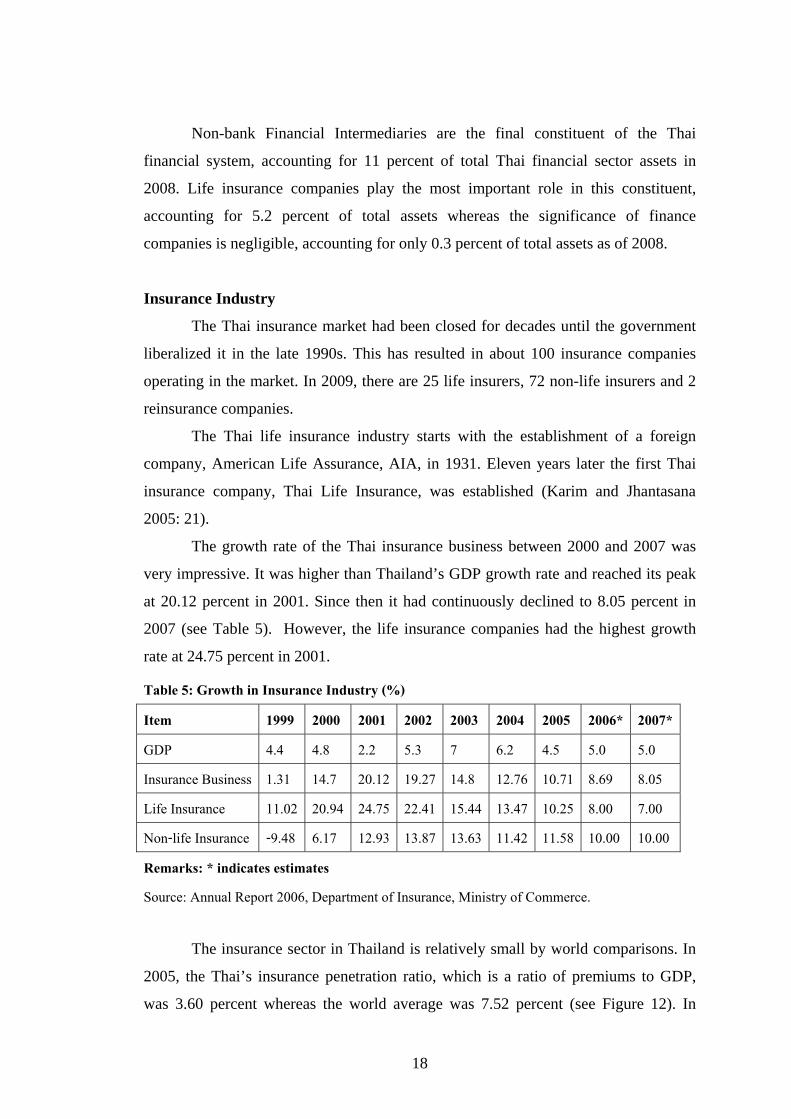

The growth rate of the Thai insurance business between 2000 and 2007 was

very impressive. It was higher than Thailand’s GDP growth rate and reached its peak

at 20.12 percent in 2001. Since then it had continuously declined to 8.05 percent in

2007 (see Table 5). However, the life insurance companies had the highest growth

rate at 24.75 percent in 2001.

Table 5: Growth in Insurance Industry (%)

Item 1999 2000 2001 2002 2003 2004 2005 2006* 2007* GDP 4.4 4.8 2.2 5.3 7 6.2 4.5 5.0 5.0 Insurance Business 1.31 14.7 20.12 19.27 14.8 12.76 10.71 8.69 8.05 Life Insurance 11.02 20.94 24.75 22.41 15.44 13.47 10.25 8.00 7.00 Non-life Insurance -9.48 6.17 12.93 13.87 13.63 11.42 11.58 10.00 10.00 Remarks: * indicates estimates Source: Annual Report 2006, Department of Insurance, Ministry of Commerce.

The insurance sector in Thailand is relatively small by world comparisons. In

2005, the Thai’s insurance penetration ratio, which is a ratio of premiums to GDP,

was 3.60 percent whereas the world average was 7.52 percent (see Figure 12). In

19

2003, only fifteen percent of population holds life insurance policies with a premium

of about 3 billion dollars (Karim and Jhantasana 2005: 22).

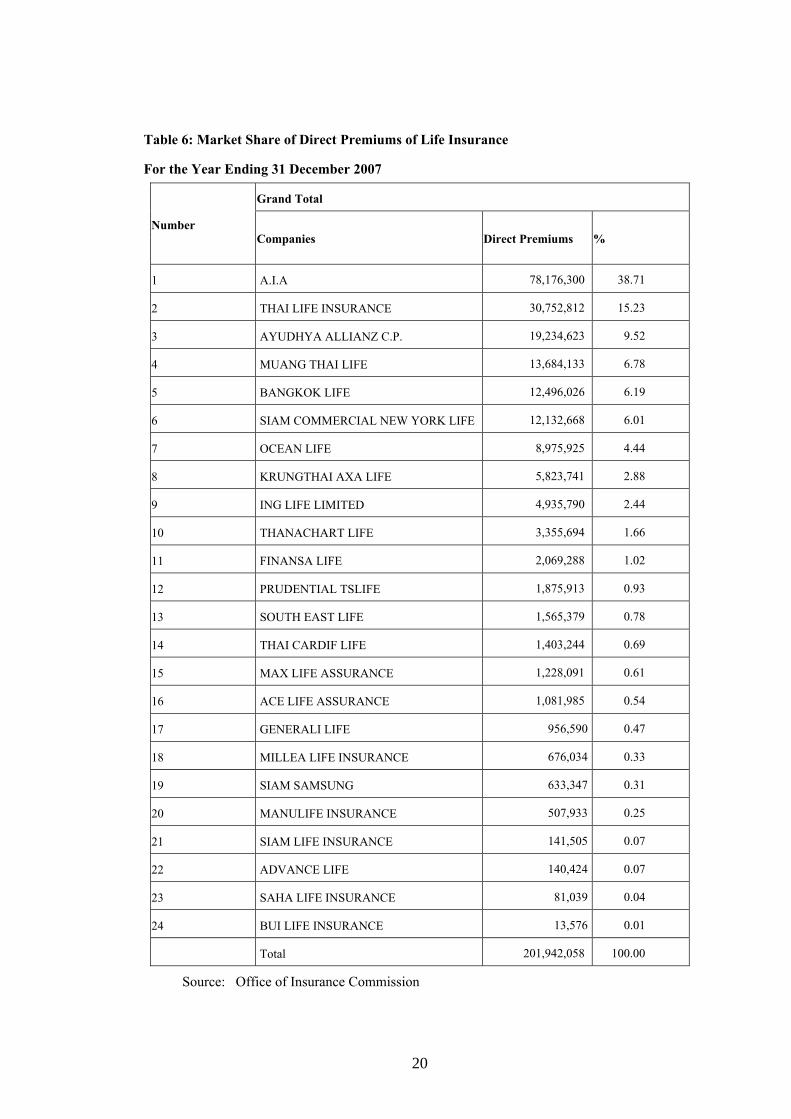

The Thai life insurance industry is heavily concentrated with the five largest

insurers control 51 percent of the market share in 2007 (see Table 6). The market is

dominated by AIA, a foreign branch, which holds 38.71 percent of the market while

the largest local company, Thai Life Insurance, has a market share of 15.23 percent.

In order to reform and strengthen the insurance industry, the Commission for

Regulation and Promotion of Insurance Business Act 2007 established a new industry

regulator, which is widely known as the Insurance Commission, to replace the

previous one which was housed under the Ministry of Commerce. The new regulator

is shifted to be under the supervision of the Ministry of Finance which is more

suitable than the Ministry of Commerce in overseeing the insurance industry.

Figure 12: Insurance Penetration (premiums in % of GDP in 2005)

Source: Annual Report 2006, Department of Insurance, Ministry of Commerce

Currently, new insurance products offered include voluntary motor insurance

policy type 4, non-performing loan insurance, weather index insurance, unit-linked

insurance, high-rise building insurance and universal life insurance (Annual Report on

Insurance Business 2006, Office of Insurance Commission: 1).

Table 7 presents profit and loss statements of life insurance companies in Thailand for

20

Table 6: Market Share of Direct Premiums of Life Insurance For the Year Ending 31 December 2007

Number

Grand Total

Companies Direct Premiums %

1 A.I.A 78,176,300 38.71

2 THAI LIFE INSURANCE 30,752,812 15.23

3 AYUDHYA ALLIANZ C.P. 19,234,623 9.52

4 MUANG THAI LIFE 13,684,133 6.78

5 BANGKOK LIFE 12,496,026 6.19

6 SIAM COMMERCIAL NEW YORK LIFE 12,132,668 6.01

7 OCEAN LIFE 8,975,925 4.44

8 KRUNGTHAI AXA LIFE 5,823,741 2.88

9 ING LIFE LIMITED 4,935,790 2.44

10 THANACHART LIFE 3,355,694 1.66

11 FINANSA LIFE 2,069,288 1.02

12 PRUDENTIAL TSLIFE 1,875,913 0.93

13 SOUTH EAST LIFE 1,565,379 0.78

14 THAI CARDIF LIFE 1,403,244 0.69

15 MAX LIFE ASSURANCE 1,228,091 0.61

16 ACE LIFE ASSURANCE 1,081,985 0.54

17 GENERALI LIFE 956,590 0.47

18 MILLEA LIFE INSURANCE 676,034 0.33

19 SIAM SAMSUNG 633,347 0.31

20 MANULIFE INSURANCE 507,933 0.25

21 SIAM LIFE INSURANCE 141,505 0.07

22 ADVANCE LIFE 140,424 0.07

23 SAHA LIFE INSURANCE 81,039 0.04

24 BUI LIFE INSURANCE 13,576 0.01

Total 201,942,058 100.00

Source: Office of Insurance Commission

21

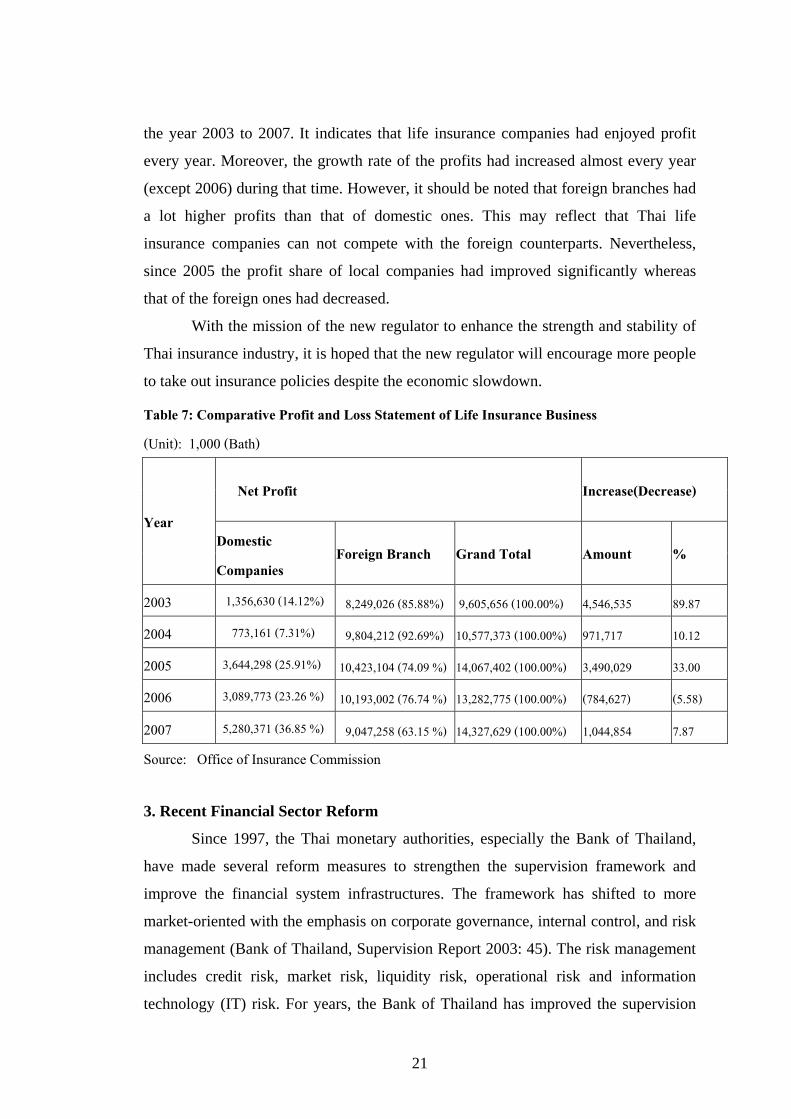

the year 2003 to 2007. It indicates that life insurance companies had enjoyed profit

every year. Moreover, the growth rate of the profits had increased almost every year

(except 2006) during that time. However, it should be noted that foreign branches had

a lot higher profits than that of domestic ones. This may reflect that Thai life

insurance companies can not compete with the foreign counterparts. Nevertheless,

since 2005 the profit share of local companies had improved significantly whereas

that of the foreign ones had decreased.

With the mission of the new regulator to enhance the strength and stability of

Thai insurance industry, it is hoped that the new regulator will encourage more people

to take out insurance policies despite the economic slowdown.

Table 7: Comparative Profit and Loss Statement of Life Insurance Business (Unit): 1,000 (Bath)

Year

Net Profit Increase(Decrease)

Domestic Companies

Foreign Branch Grand Total Amount %

2003 1,356,630 (14.12%) 8,249,026 (85.88%) 9,605,656 (100.00%) 4,546,535 89.87

2004 773,161 (7.31%) 9,804,212 (92.69%) 10,577,373 (100.00%) 971,717 10.12

2005 3,644,298 (25.91%) 10,423,104 (74.09 %) 14,067,402 (100.00%) 3,490,029 33.00

2006 3,089,773 (23.26 %) 10,193,002 (76.74 %) 13,282,775 (100.00%) (784,627) (5.58)

2007 5,280,371 (36.85 %) 9,047,258 (63.15 %) 14,327,629 (100.00%) 1,044,854 7.87

Source: Office of Insurance Commission 3. Recent Financial Sector Reform

Since 1997, the Thai monetary authorities, especially the Bank of Thailand,

have made several reform measures to strengthen the supervision framework and

improve the financial system infrastructures. The framework has shifted to more

market-oriented with the emphasis on corporate governance, internal control, and risk

management (Bank of Thailand, Supervision Report 2003: 45). The risk management

includes credit risk, market risk, liquidity risk, operational risk and information

technology (IT) risk. For years, the Bank of Thailand has improved the supervision

22

framework in line with international standards. This has contributed to the improved

risk management and resiliency of the banking system. In addition, the Bank of

Thailand has introduced various prudential policies and supervision guidelines related

to risk management in order to strengthen financial institutions, increasing

competition and protecting consumers.

In 2007, three new important laws which are necessary for effective banking

supervision were enacted, namely, the Amended Bank of Thailand Act B.E. 2551, the

Financial Institution Business Act B.E. 2551 (FIBA) (replacing the Commercial

Banking Act B.E. 2505 and the Act on the Undertaking of Finance Business,

Securities Business and Credit Foncier Business 2522) and the Deposit Protection

Agency Act B.E. 2552 (DPA)(replacing the blanket deposit guarantee scheme

implemented right after the 1997 Financial Crisis).

The amended BOT Act “stipulates the independence, transparency and

accountability of the bank of Thailand, as well as expanded the Bank of Thailand’s

capacity to manage assets and conduct monetary policy more efficiently (Bank of

Thailand, Supervision Report 2007:36).” Moreover, the law specifies explicitly the

term, and the process for appointing and dismissing the Governor.

The objective of the FIBA is to strengthen supervisory framework of the

financial institution system by clearly separating the role and responsibility between

the Ministry of Finance and the Bank of Thailand. The Bank of Thailand is

empowered to supervise and close financial institutions whereas the Ministry of

Finance is empowered to grant and revoke license. Moreover, the Bank of Thailand is

offered additional power to “conduct consolidated supervision over financial

conglomerates, implement prudential regulation to comply with the Basel Core

Principles, and oversee consumer protection (Bank of Thailand, Supervision Report

2007:36)”.

The DPA Act “is responsible for providing compensation to depositors when

a financial institution’s license is revoked and acting as a liquidator for such an

institution (Bank of Thailand, Supervision Report 2007: 37)”. It will take five years to

eventually reduce maximum coverage to one million baht per depositor per financial

institution. However, due to the Global Financial Turmoil, the DPA Act has been

revised in 2008 (see Table 1, Appendix I).

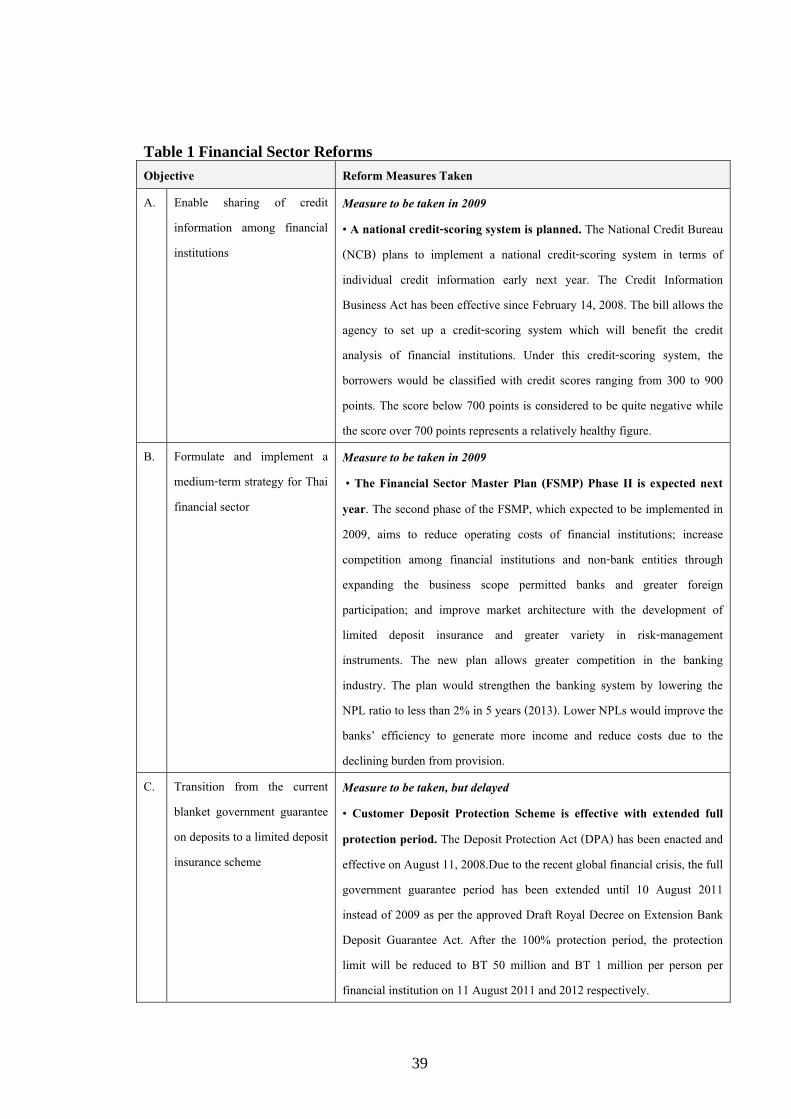

23

(Table 1, Appendix I summarizes the reform measures in the Thai Financial Sector

taken in 2008 and 2009.)

4. Financial Deregulation and Liberalization

Unlike many East Asian newly industrialized economies (NIEs) which

embarked on their financial liberalization programs in the early 1980s, Thailand

began its financial liberalization in the late 1980s and accelerated in the early 1990s

(Zhang 2002: 1). Changes in the international environments, for instance, trade in

services were included in the Uruguay Round. Pressures from developed countries

and the International Monetary Fund (IMF) were the main factors that accelerated the

Thai monetary authorities to liberalize the financial sector. In addition, the

government’s desire to become the financial regional center was an additional factor

that prompted the pace of the financial liberalization in Thailand.

The financial sector reform policy in the late 1980s was formulated in a

regional context because the fundamental changes in the political and economic

landscape of Indochina over the 1980’s were taken into account (Zhang 2003: 105).

The Bank of Thailand had launched the first long-term financial reform plan (1990-

1992) with an ambitious goal to turn Bangkok into a regional financial center

replacing the one in Hong Kong and Singapore (Nidhiprabha 2003: 40). The purpose

of the financial sector reform was to “ensure an efficient allocation of resources and

greater flexibility in the economy’s adjustment to changes and to the increasingly

competitive environment” (the Bank of Thailand Annual Report 1992).

The Bank of Thailand implemented 4 major policies on financial deregulation

and liberalization. They were as follows:

3.1 Interest rate liberalization.

3.2 Foreign exchange liberalization.

3.3 Relaxation in financial institutions’ portfolio management, and

3.4 Expansion in the scope of the operation of financial institutions (the

Bank of Thailand Annual Report 1992).

4.1 Interest rate liberalization

Prior to interest rate liberalization, financial institutions under the supervision

of the Bank of Thailand which are commercial banks, finance companies and credit

24

fonciers were constrained by ceilings on interest rates and on the expansion of credit.

This had caused the distortion in the financial markets and hindered efficient

allocation of resources in the financial sector.

These ceilings served as binding constraint on interest rate movement in an

upward direction only (Wibulswasdi 1986: 30). The monopolistic power in the

commercial banking sector, due to the high degree of concentration of the ownership,

led to cartel-like organization in which commercial banks collectively, through the co-

ordination of the Thai Bankers’ Association (TBA), set lending interest rates at any

level below official ceilings (Wibulswasdi 1986: 30; Zhang 2003: 108). But for the

deposit rate, there was a certain degree of downward rigidity as commercial banks

were reluctant to offer interest rates lower than official ceiling rates (Wibulswasdi

1986: 30).

In order to turn Bangkok to be the regional financial centre, interest rate

liberalization is required. Ceilings of various interest rates of the aforementioned

financial institutions were gradually removed. It took 3 years for the Bank of Thailand

to accomplish this task, starting with the abolition of ceiling on commercial banks’

time deposit rates with maturity exceeding 1 year in June 1989. The rationale behind

this was aimed at creating a more flexible interest rate system and encouraging

longer-term savings as well (Wibulswasdi 1995: 2). The next two and a half more

years, ceilings on commercial banks’ savings deposits were abolished in January

1992. And finally, in June1992 ceilings on all remaining interest rates including

ceilings on deposits at finance and credit foncier companies were removed.

25

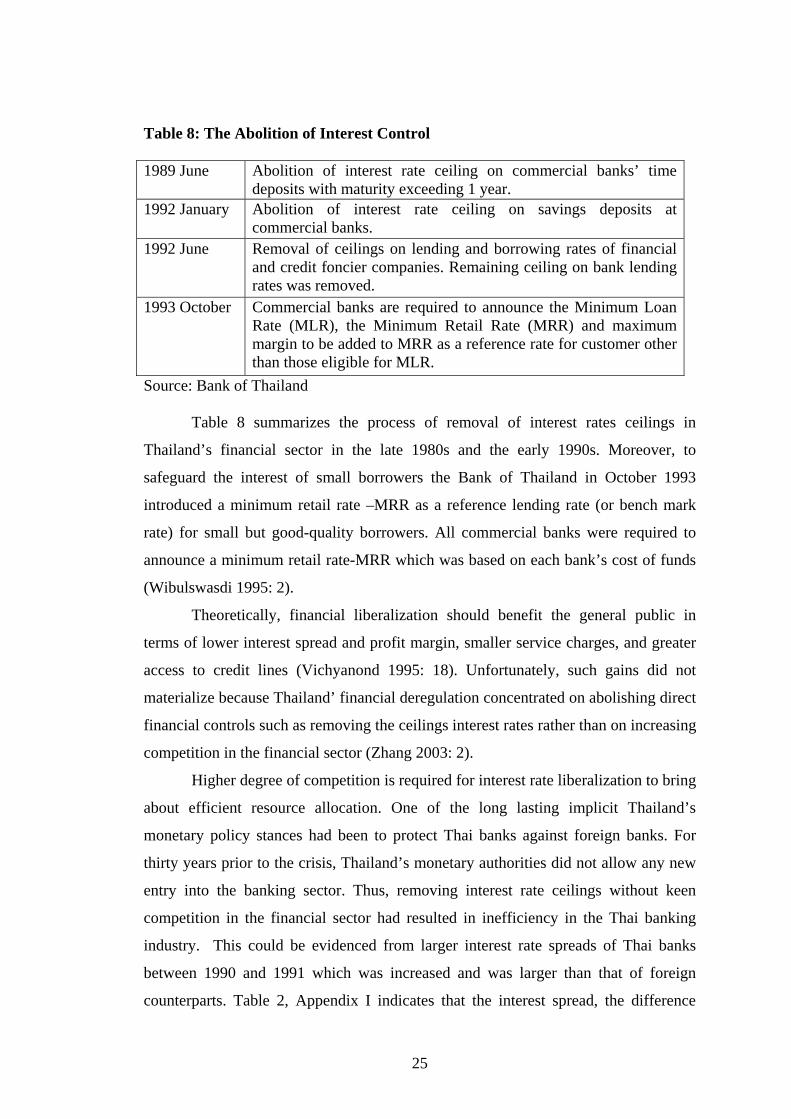

Table 8: The Abolition of Interest Control 1989 June Abolition of interest rate ceiling on commercial banks’ time

deposits with maturity exceeding 1 year. 1992 January Abolition of interest rate ceiling on savings deposits at

commercial banks. 1992 June Removal of ceilings on lending and borrowing rates of financial

and credit foncier companies. Remaining ceiling on bank lending rates was removed.

1993 October Commercial banks are required to announce the Minimum Loan Rate (MLR), the Minimum Retail Rate (MRR) and maximum margin to be added to MRR as a reference rate for customer other than those eligible for MLR.

Source: Bank of Thailand

Table 8 summarizes the process of removal of interest rates ceilings in

Thailand’s financial sector in the late 1980s and the early 1990s. Moreover, to

safeguard the interest of small borrowers the Bank of Thailand in October 1993

introduced a minimum retail rate –MRR as a reference lending rate (or bench mark

rate) for small but good-quality borrowers. All commercial banks were required to

announce a minimum retail rate-MRR which was based on each bank’s cost of funds

(Wibulswasdi 1995: 2).

Theoretically, financial liberalization should benefit the general public in

terms of lower interest spread and profit margin, smaller service charges, and greater

access to credit lines (Vichyanond 1995: 18). Unfortunately, such gains did not

materialize because Thailand’ financial deregulation concentrated on abolishing direct

financial controls such as removing the ceilings interest rates rather than on increasing

competition in the financial sector (Zhang 2003: 2).

Higher degree of competition is required for interest rate liberalization to bring

about efficient resource allocation. One of the long lasting implicit Thailand’s

monetary policy stances had been to protect Thai banks against foreign banks. For

thirty years prior to the crisis, Thailand’s monetary authorities did not allow any new

entry into the banking sector. Thus, removing interest rate ceilings without keen

competition in the financial sector had resulted in inefficiency in the Thai banking

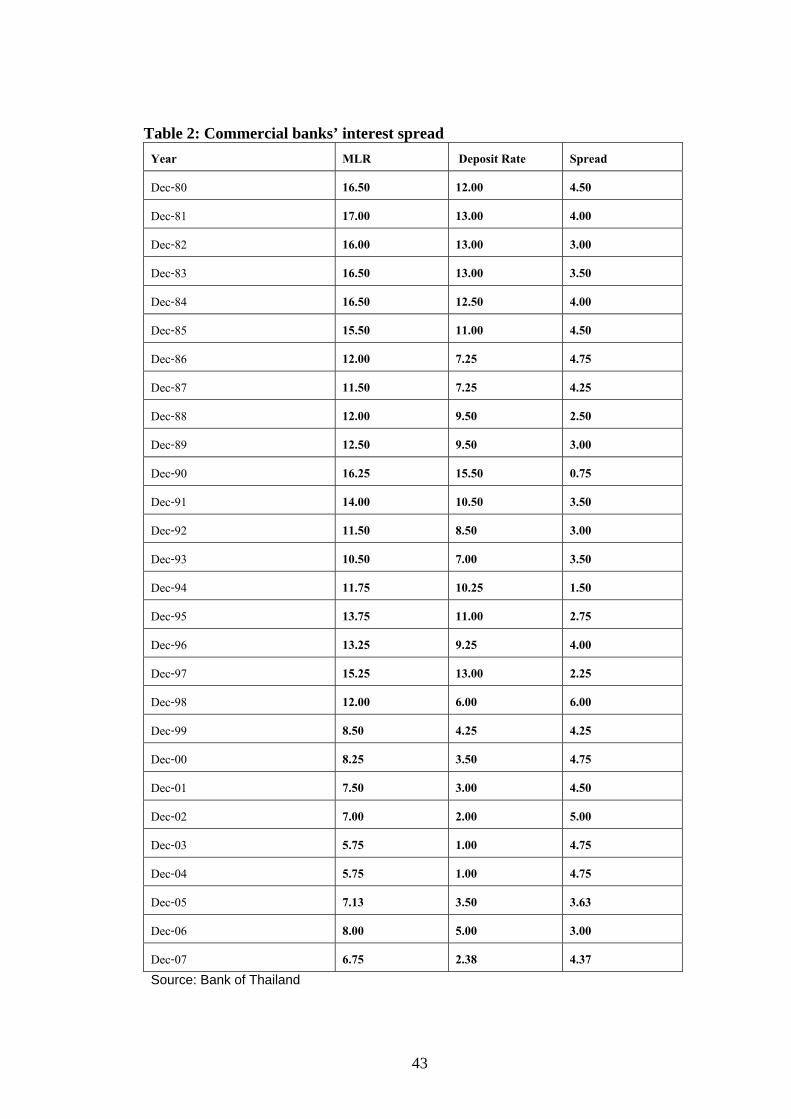

industry. This could be evidenced from larger interest rate spreads of Thai banks

between 1990 and 1991 which was increased and was larger than that of foreign

counterparts. Table 2, Appendix I indicates that the interest spread, the difference

26

between minimum lending rate and 12-month time deposit rate, after the Asian

Financial Crisis were larger than that before the crisis.

Prior to 1992 large banks acted as price leaders in setting up bank interest rates

and small banks followed suit. Nidhiprabha demonstrated that after interest rate

liberalization such practices are changed. The interest rate liberalization allows each

bank to set its own interest rates according to its cost structure and own market niche

and in some cases small banks became price leaders (Nidhiprabha 2003: 29).

Currently, domestic interest rates particularly money market rates-inter-bank

rates- are more volatile because they are sensitive to movements in the world interest

rates especially the US Federal Funds rate.

4.2 Foreign Exchange Liberalization

Thailand like most emerging economies relaxed the restrictions on capital

controls in the 1990s. Thai monetary authorities thought that the turn of the 1990

decade was the right time to start foreign exchange liberalization since Thailand’s

external conditions then were relatively stable. The international reserves were high –

equivalent to 5 months of imports; low debt-service ratio which was 10 percent

compared to 20 per cent in the first half of 1980s. Moreover, “The country’s practice

of exchange control was, in practice, in conformity with Article VIII requirements for

many years; i.e., there were no restrictions on payments for current account

transactions and no discriminatory currency arrangements or multiple currency

practices” (Wibulswasdi 1992: 34). Thus, as a first sign or first stage of financial

liberalization, Thailand in May 1990 accepted the obligations under the Article VIII

of the IMF’s Articles of agreement which lifted all controls on all foreign-exchange

transactions on the current account. Many observers pointed that this marked the

beginning of the series of financial liberalization measures and the origins of the 1997

Asian Financial Crisis.

Commercial banks were allowed to (i) process customers’ applications for the

purchase of foreign exchanges for trade-related transactions without prior approval

from the Bank of Thailand and (ii) approve outward transfer of foreign exchange in

small amounts not exceeding $US 500,000 for remittance of loans, sale of securities,

or liquidation of companies. Funds for Overseas trip were limit to $US 20,000 per trip

(Wibulswasdi 1992: 34).

27

The Bank of Thailand announced the second stage of foreign exchange control

deregulation on April 1, 1991 allowing private businesses and the general public more

flexibility in purchasing and selling foreign exchanges. Residents were permitted to

open foreign currency accounts if the funds originated from abroad. However, the

acquisition of real estate and investment in the stock market abroad were still required

the Bank of Thailand’s approval. On May 1992, further exchange rate liberalization

measures were pursued; prior approval from the Bank of Thailand was not required

for exporters to use foreign exchange receipts to repay foreign debts. Nonresidents

were permitted to open foreign currency accounts (Nidhiprabha 2003: 31).

“In February 1994, more investment or lending abroad was allowed and more baht

notes were permitted to be carried into neighboring countries. In general, there were

fewer constraints on commercial banks’ portfolio management by the mid 1990s

(Institute for International Monetary Affairs 2006: 20).

Bangkok International Banking Facilities (BIBFs)

The second milestone in opening up of the Thai financial system was the

gradual opening of the capital account through the launching of the Bangkok

International Banking Facilities (BIBFs) in 1993 (Siamwalla 2000: 3).

The Bangkok International Banking Facilities (BIBFs) provided three types of

services: (1) banking to nonresidents in foreign currencies and Baht (“out-out”

transactions),(2)banking to domestic residents in foreign currency only (“out-in”

transactions), and (3) international financial and investment banking services. The

BIBF units must mobilize fund from overseas and extend credits only in foreign

currencies (Financial Institutions in Thailand 1998:50).

To enable BIBFs to compete with financial institutions in other financial

centers various tax privileges were granted: the corporate income tax was reduced

from 30 to 10 percent; exemptions were provided for the sales tax and stamp duties;

and the withholding tax rate on interest payments was reduced from 15 to 10 percent

for “out-in” transactions (Annual Economic Report 1993, Bank of Thailand: 54).

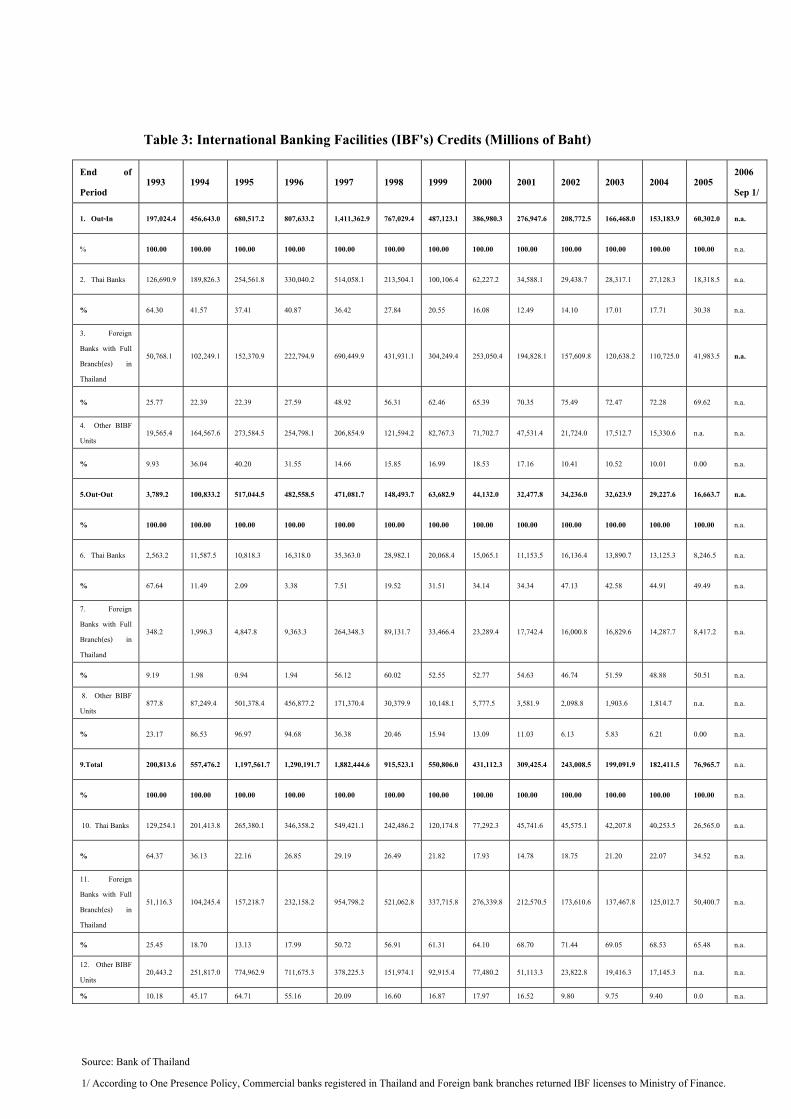

Financial liberalization through BIBFs induced a flood of capital inflows into

Thailand, especially into its banking sector in the period 1990-96. The BIBF’s credits

reached its peak in 1997 at 1,882 billion Baht or about 40 per cent of GDP compared

with 1,290 billion Baht in 1996. However, the BIBF’s credits had been decreasing

28

since 1998 but it was still at high levels. In 2005 this figure drastically dropped to 76

billion Baht (see Table 3.3). Since September 2006 according to “One Presence

Policy” under the Financial Sector Master Plan (FSMP) the BIBF operations were

abolished. Commercial banks registered in Thailand and foreign bank branches had to

return IBF licenses to the Ministry of Finance.

Four years after the Bank of Thailand had launched the BIBFs, Thai banks

were the major players in “out-in” business (except year 1995) due to strong customer

base; whereas foreign banks BIBF units with no branches in Thailand dominated the

“out-out” business. But after the 1997 Asian Financial Crisis foreign banks with Full

Branches in Thailand had become the major players in both “out-in” and “out-out”

businesses.

The Bank of Thailand hoped that the BIBF lending would concentrate on the

“out-out” activities –fund raised abroad and lent to the Indochina countries- rather

than on the “out-in” business. But it turned out that the size of the “out-in” lending

was about 80 % of the total BIBF lending between 1993 to 2005 (see Table 3

Appendix 1) This was attributed to the relatively high interest rates in Thailand. The

“out-in” capital flows led to excessive credit expansion to private sectors. This fuelled

investment spending in the non-traded goods sector, speculation, and current account

deficits. Speculative and imprudent lending from BIBFs inflated several “bubble

sectors” especially in the stock markets and the real estate sector.

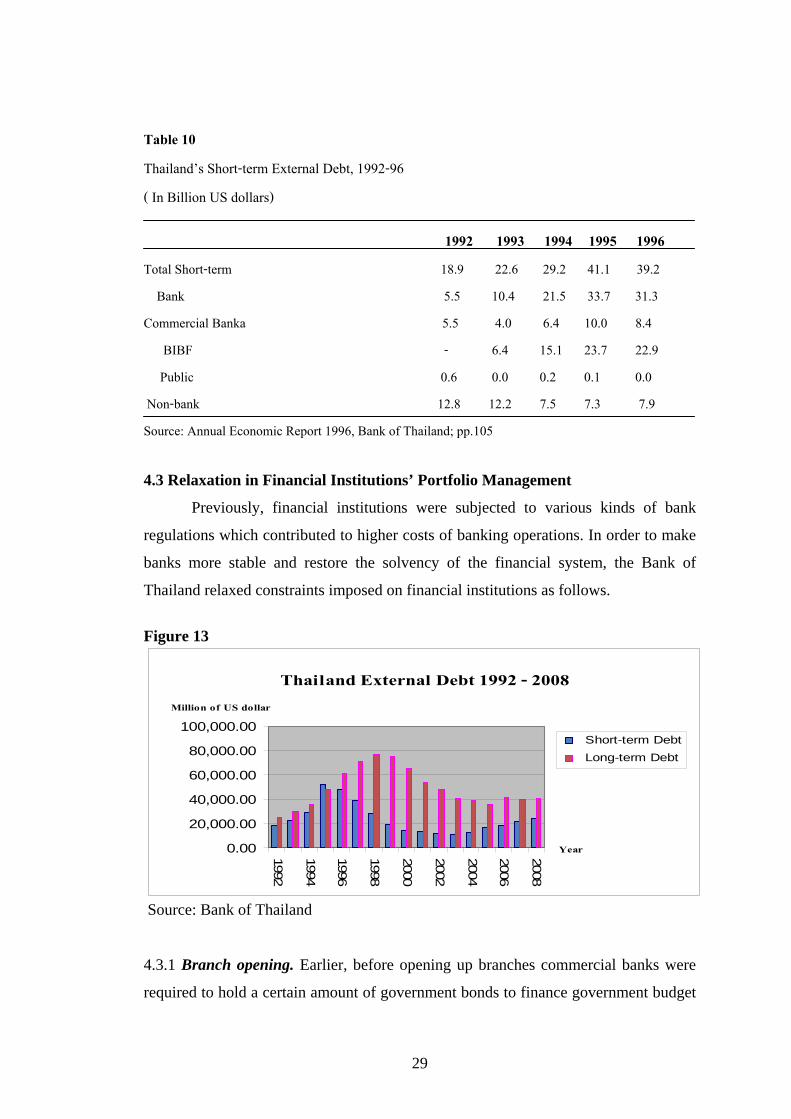

The BIBFs operations were the main cause of the rapid increase in Thailand’s

external debt particularly the short-term ones. The debt-to-GDP ratio rose from 39.2

percent in 1992 to 48.7 percent in 1996 (Annual Economic Report 1996. The Bank of

Thailand: 104). Table 10 and Figure 13 indicate that Thailand’s short-term external

debt had increased between 1992 and 1995 and BIBFs were the main factor

responsible for such increase especially for banks.

The monetary authority believed that the establishment of the BIBF was the

first step in the process of promoting Thailand as a financial center of the region

(Annual Economic Report 1998, The Bank of Thailand: 58). But it turned out that

BIBF had contributed to the East Asian Financial Crisis.

29

Table 10 Thailand’s Short-term External Debt, 1992-96 ( In Billion US dollars)

1992 1993 1994 1995 1996 Total Short-term 18.9 22.6 29.2 41.1 39.2 Bank 5.5 10.4 21.5 33.7 31.3 Commercial Banka 5.5 4.0 6.4 10.0 8.4 BIBF - 6.4 15.1 23.7 22.9 Public 0.6 0.0 0.2 0.1 0.0 Non-bank 12.8 12.2 7.5 7.3 7.9 Source: Annual Economic Report 1996, Bank of Thailand; pp.105 4.3 Relaxation in Financial Institutions’ Portfolio Management

Previously, financial institutions were subjected to various kinds of bank

regulations which contributed to higher costs of banking operations. In order to make

banks more stable and restore the solvency of the financial system, the Bank of

Thailand relaxed constraints imposed on financial institutions as follows.

Figure 13

Thailand External Debt 1992 - 2008

0.00

20,000.00

40,000.00

60,000.00

80,000.00

100,000.00

1992

1994

1996

1998

2000

2002

2004

2006

2008

Year

Million of US dollar

Short-term Debt Long-term Debt

Source: Bank of Thailand 4.3.1 Branch opening. Earlier, before opening up branches commercial banks were

required to hold a certain amount of government bonds to finance government budget

30

deficits. Starting in November 1990 the Bank of Thailand lowered the ratio of bond

holding requirement from 16 percent of total deposits to 9.5 percent. Then the ratios

had been decreased to 8 percent in September 1991, 7 percent in February 1992, 6.5

percent in October 1992, 5.5 percent in February 1993 and nil in May 1993

(Vichyanond 1995).

4.3.2 Rural credit requirement. Previously, commercial banks had an obligation to

allocate no less than 20 percent of their deposits to the agricultural sector.

Commercial banks found it difficult to comply with this regulation since the definition

of the “agricultural credit” was too narrow. Thus in 1987, 1991, and 1992 the Bank of

Thailand changed the name of the “agricultural credit” to the “rural credit” and

modified the loan to cover more related occupations which included regional small-

scale industries, wholesale trading of agricultural produces, regional industrial estate,

farmers’ secondary occupations and the exportation of farm products (Vichyanond

1995). The rationale behind this modification was to support the rural development

strategy implemented then (Wibulswasdi 1987).

4.3.3 Reserve requirement. In June 1991, the Bank of Thailand required financial

institutions to maintain a liquidity ratio in place of the reserve requirement ratio. This

allowed commercial banks to substitute other securities for government bonds and

manage their assets more efficiently. Commercial banks are now required to hold

liquid assets at no less than 6 per cent of total deposits.

4.3.4 Capital adequacy ratio. On the first of January 1993, the Bank of Thailand

modified the regulations on capital adequacy ratio in order to comply with the

guidelines of the Bank for International Settlements (BIS). Commercial banks’ capital

funds are divided into first tier and second tier. First tier capital comprised paid-up

capital, legal reserves; reserves appropriated from net profits and retained earning.

While the second tier capital funds are 50 percent of the revaluation of buildings and

land, hybrid debt instruments and subordinated term debts (the Bank of Thailand

Annual Report 1992: 109).

31

Thai commercial banks were required to maintain a minimum capital ratio of 7

percent of total assets and contingent liabilities (off-balance-sheet items); within with

at least 5 percent must be first tier capital. By the end of 1994, these two ratios were

adjusted upward to 9 percent and 5.5 percent respectively (Vichyanond 1995).

Branches of commercial banks incorporated abroad or foreign banks were required to

maintain capital funds in Thailand as well and the adequacy ratio was 6.25 percent of

total assets and contingent liabilities. Thai commercial banks are now required to hold

8.5 percent of the capital adequacy ratio.

4.4 Expansion in the Scope of the Operation of Financial Institutions

To promote greater competition in the supply of financial services the Bank of

Thailand allowed financial institutions to undertake new related businesses. Effective

14 March 1992, commercial banks were permitted to carry out three new types of

business namely, underwriting government’s and state enterprises’ debt instruments,

providing economic, financial and information services, and providing financial

advisory services in mergers, acquisition and take-over cases. In June 1992, additional

businesses were added for commercial banks to operate including managing, issuing,

underwriting and trading of debt instruments. Nevertheless, approval from the Bank

of Thailand was required. Other businesses, requiring no prior approval from the

Bank of Thailand, were agents for the sale of mutual funds, secured debentures

holders’ representatives, mutual fund supervisors, and securities registrar. However,

approval from the Securities and Exchange commission-SEC was required for the last

three businesses (the Bank of Thailand Annual Report 1992:106).

For finance companies and finance and securities companies, new services

offered to them to operate were leasing services, acting as selling agents for public

debt instruments, arrangers, underwriters, and dealers for debt instruments and act as

mutual fund supervisors (the Bank of Thailand Annual Report 1992: 51).

5. Weaknesses in the Thai Financial and Banking Systems

Even though the Thai financial system has gone through various reforms

within the last decade, there are underlying weaknesses which have still to be

addressed. Some of the weaknesses are discussed below.

32

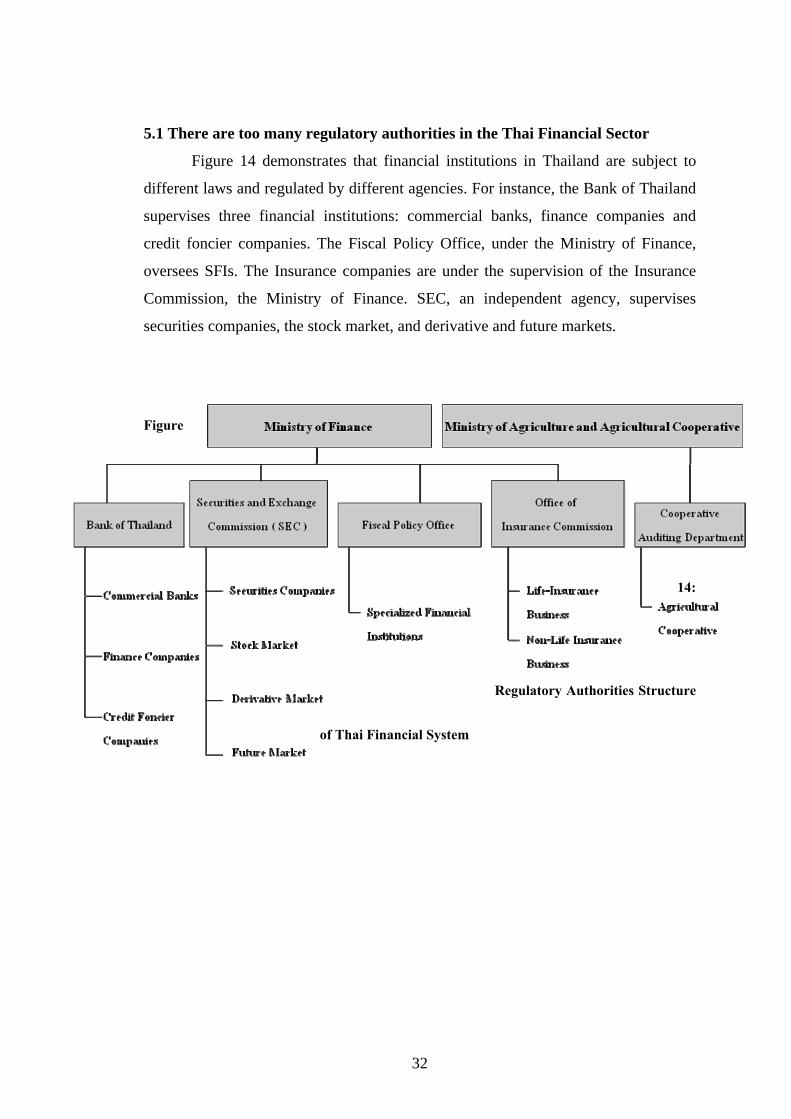

5.1 There are too many regulatory authorities in the Thai Financial Sector

Figure 14 demonstrates that financial institutions in Thailand are subject to

different laws and regulated by different agencies. For instance, the Bank of Thailand

supervises three financial institutions: commercial banks, finance companies and

credit foncier companies. The Fiscal Policy Office, under the Ministry of Finance,

oversees SFIs. The Insurance companies are under the supervision of the Insurance

Commission, the Ministry of Finance. SEC, an independent agency, supervises

securities companies, the stock market, and derivative and future markets.

Figure

14:

Regulatory Authorities Structure

of Thai Financial System

33

The current institutional structure of regulatory and supervisory agencies in

the Thai financial sector as mentioned above has resulted in sub-optimal, less

efficient, costly and cause inconsistencies in supervising and regulations among

various monetary regulators. The blurring business line between different types of

financial institutions calls for a convergence of regulation and supervisory practices.

A question that arises is whether Thailand needs a single financial authority

like the one in Singapore, namely, the Monetary Authority of Singapore-MAS.

During the Thaksin Administration, the Ministry of Finance floated the idea that a

new monetary authority should be set up to oversee all financial institutions. The

financial institutions under the supervision of the Bank of Thailand should be

transferred to the new authority and the Bank of Thailand should be solely responsible

for the monetary policy. Of course, this idea is opposed by the Bank of Thailand. We

think that it is timely to raise this question and seriously debate it in order to improve

the overall supervision of the financial sector for the benefit of the majority of the

people.

5.2 The Thai financial sector operates inefficiently

Chansarn (2005) had studied to investigate the efficiency in the Thai financial

sector after the financial crisis (1998-2004) using the total factor productivity (TFP)

growth. He found that “the efficiency in the Thai financial sector, the commercial

bank sector, and the finance and securities company sector was diminishing over the

period of 1998-2004, while the efficiency in the insurance company sector remained

unchanged over the same period. However, the sharp decrease in efficiency in these

three sectors occurred only over the period of 1998-1999, while the efficiency was

decreasing very slightly over the period of 1999-2004 (Chansarn 2005).

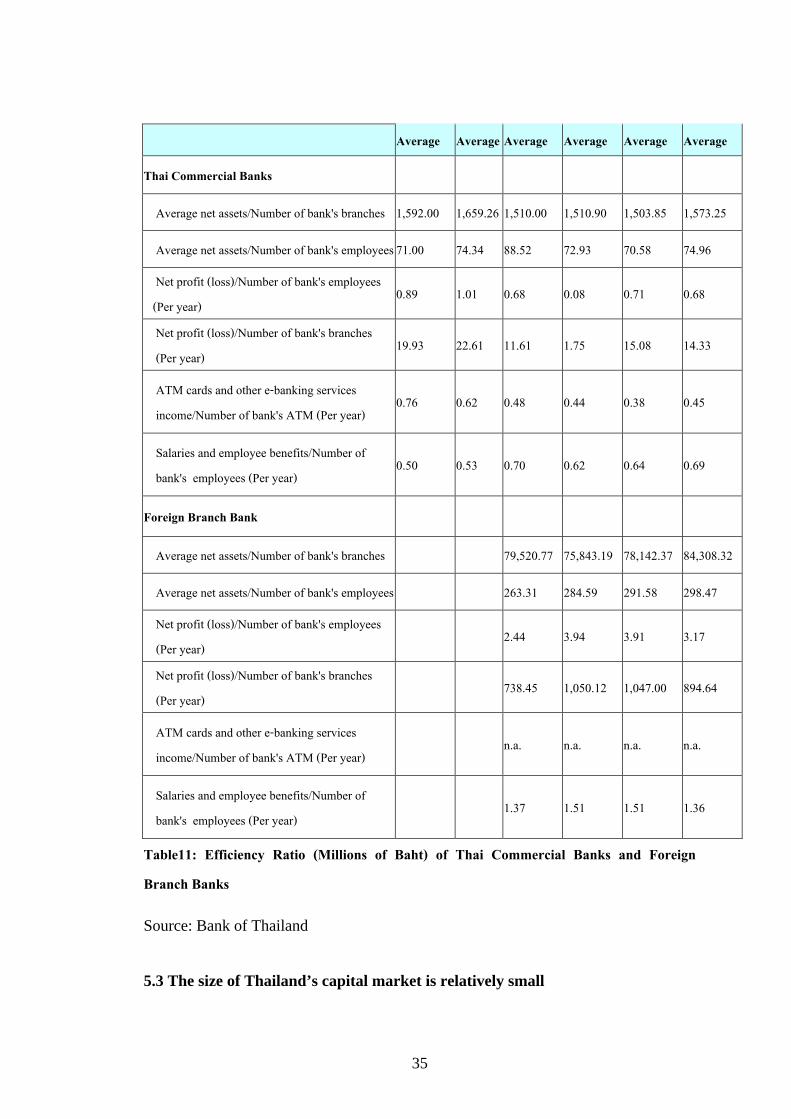

Table 11 confirms that even though the operating environment of the banking

sector in Thailand has undergone major changes in recent years, Thai banks still can

not compete with foreign counterparts. Thai commercial banks operate less efficient

than foreign banks. With a unit of bank resource, foreign branch banks can operate at

a higher profit. For in stance, a Thai commercial banks’ employee could make net

profit only 0.68 million baht in the first quarter of 2009 whereas that of the foreign

branch bank was 298.47 million baht in the same period. This reflects that Thai

34

financial institutions can not compete with foreign counterparts. The reason is that

foreign branch banks have skill advantages in sales and marketing, product

innovation, and risk management as well as access to cheaper source of funds.

Foreign financial institutions, particularly commercial banks, should be

allowed to play more important role in the Thai financial sector. During the past three

decades, the Thai monetary authorities were reluctant to encourage foreign

participation in the market. There had been an implicit policy of the Bank of Thailand

that protected Thai banks over foreign counterparts which had led to incompetence of

Thai banks before the 1997 Financial Crisis. “Foreign penetration has had positive

effects on Thailand on the sense that they promoted market competition and improved

the operational efficiency of banking. In addition, foreign acquisition of Thai domestic

banks introduced advanced skills and technology helping upgrade the business

operations of banks (Okuda and Rungsomboon, 2006)”. Fortunately, one of the

objectives of the Financial Sector Master Plan (FSMP) Phase II is to increase

competition within the financial sector through offering greater foreign participation.

It remains to be seen whether this will be materialized.

Financial Ratio Q4/2004 Q4/2005 Q4/2006 Q4/2007 p Q4/2008 p Q1/2009 p

35

Table11: Efficiency Ratio (Millions of Baht) of Thai Commercial Banks and Foreign Branch Banks Source: Bank of Thailand 5.3 The size of Thailand’s capital market is relatively small

Average Average Average Average Average Average

Thai Commercial Banks

Average net assets/Number of bank's branches 1,592.00 1,659.26 1,510.00 1,510.90 1,503.85 1,573.25

Average net assets/Number of bank's employees 71.00 74.34 88.52 72.93 70.58 74.96

Net profit (loss)/Number of bank's employees (Per year)

0.89 1.01 0.68 0.08 0.71 0.68

Net profit (loss)/Number of bank's branches (Per year)

19.93 22.61 11.61 1.75 15.08 14.33

ATM cards and other e-banking services income/Number of bank's ATM (Per year)

0.76 0.62 0.48 0.44 0.38 0.45

Salaries and employee benefits/Number of bank's employees (Per year)

0.50 0.53 0.70 0.62 0.64 0.69

Foreign Branch Bank

Average net assets/Number of bank's branches 79,520.77 75,843.19 78,142.37 84,308.32

Average net assets/Number of bank's employees 263.31 284.59 291.58 298.47

Net profit (loss)/Number of bank's employees (Per year)

2.44 3.94 3.91 3.17

Net profit (loss)/Number of bank's branches (Per year)

738.45 1,050.12 1,047.00 894.64

ATM cards and other e-banking services income/Number of bank's ATM (Per year)

n.a. n.a. n.a. n.a.

Salaries and employee benefits/Number of bank's employees (Per year)

1.37 1.51 1.51 1.36

36

Even though the SET has been operated for over 30 years, the Thai equity

market still has a limited number of listed firms and thin trading volume. As of

December 2008, there were 488 listed companies in the SET, 52 companies in Market

for Alternative Investment (MAI) and 4 companies in the BEX. Moreover, the

number of people engaging in the capital market is negligible compared with other

countries. As of 2005 only 0.42 percent of Thai population invested in the stock

market whereas that of Taiwan and Japan were 57 % and 27 % respectively (Invest

Company Institute; SEC; SET). In 2006, there were 478, 585 client accounts with

securities companies and only 25 % were active accounts (SET). Out of the total

client accounts, .032 % or 15,562 accounts belonged to foreign clients, of which 18

percent was active accounts (Thailand Securities Depository Co., Ltd. (TSD)).

Some financial analysts believe that the Thai Stock Market still lack good

governance and transparency. It seems that the SEC and the SET tend to favor large

investors. Some investors are skeptical that illegal practices such as an insider trading

still persist. It is impossible to raise funds in the stock market without the protection

of small investors (Okuda 2007). The corporate governance mechanisms should be

improved to prevent large investors from exploiting small investors.

5.4 Steps need to be taken to develop an inclusive financial system

One of the visions of FSMP is to provide financial services to all economically

viable users. In Thailand there are many savings groups providing basic lending and

deposit services to members. However, most of them still lack management and

liquidity support. Before they can obtain liquidity from financial institutions, these

savings groups have to be strong and well run. Injecting money to weak groups will

destroy credit discipline. In addition, the Village Fund Initiative also has flaws due to

inappropriate incentives and weak organization. How can we encourage financial

institutions to provide services to the poor? Can microfinance be the answer? To

accomplish this vision, more concrete efforts need to be taken.

References

37

Bank of Thailand. Annual Economic Report, Bangkok.various issues. ______________. Quarterly Bulletin, Bangkok, various issues. ______________. Financial Institutions and Markets in Thailand (1998),Bangkok. ______________. Supervision Report, Bangkok, Various issues. Chansarn, S. “The efficiency in Thai financial sector after the financial crisis,” BU Academic Review. Volume 6 Number 2 (July- December 2007). Department of Insurance. Annual Report on Insurance Business. Bangkok. Various issues. Disyatat, P. and D. Nakornthab. “The Changing Nature of Financial Structure in Thailand and Implications for Policy,” Bank of Thailand Discussion Paper (2003): 1- 34. Fitch Ratings (Thailand) Limited. “Impact of Global Financial Crisis and Political Turmoil on Thai Banks,” 22 October 2008. Insurance Commission. Annual Report on Insurance Business. Bangkok. Various issues. Karim, M. and C. Jhantasana. “Cost Efficiency and Profitability in Thailand Life Insurance Industry: A Stochastic Cost Frontier Approach,” International Journal of Applied Econometrics and Quantitative Studies. Vol. 2-4 (2005). Menkhoff, L. and C. Suwanaporn. “10 Years after the Crisis: Thailand’s Financial System Reform,” Discussion Paper 356 (January 2007) : 1-25. Nidhiprabha, B. “Premature Liberalization and economic crisis in Thailand,” In Financial Liberalization and the Economic Crisis in Asia. Edited by Chung H.Lee, 27-46. London and New York, RoutledgeCurzon, 2003 . Okuda H. Comment on “Ten Years After the Financial Crisis in Thailand: what Has Been Learned or Not Learned” Asian Economic Policy Review 2(1) (2007):100-118. Okuda H., Rungsomboon S. Comparative cost study of foreign and Thai domestic banks 1990-2002: Estimating cost functions of the Thai banking industry. Journal of Asian Economics 17 (4) (2006): 714-737. Siamwalla, A. “Picking Up the Pieces: Bank and Corporate Restructuring in Post-1997 Thailand”, Paper Presented at the Sub regional Seminar on Financial and Corporate Sectors Restructuring in East and South-East Asia, Seoul, Korea, 30May-1June 2001. ________________.“Anatomy of the Thai Economic Crisis” In Thailand Beyond the Crisis Edited by Peter Warr, 66-104. London, RoutledgeCurzon, 2005.

38

U.S. Library of Congress Vichyanond, P. “The Evolution of Thailand’s Financial System: Future Trends” TDRI Quarterly Review.Vol.10 No. 3 (September 1995): 16-20. Vanikkul, K. “Thailand Experience of Banking and Financial Sector Reform After the Crisis,” Bank of Thailand, 2007. Wibulswasdi C. and O. Tanvanich. “Liberalization of the Foreign Exchange Market: Thailand’s Experience.” Bank of Thailand Quarterly Bulletin. Vol. 32 No.4 (1992): 25-37. Wibulswasdi C. “The Formulation and Implementation of the Monetary Policy: The Thai Monetary Experience during 1983-1984.” Bank of Thailand Quarterly Bulletin. Vol.26 No.3, (1986): 27-44. ___________ .“Thai Experience in Economic Management during 1980-87.” Bank of Thailand Quarterly Bulletin. Vol.27 No. 3 (1987): 31-46. ____________. “Strengthening the Domestic Financial System.” Paper on Policy Analysis and Assessment, Economic Research Department, Bank of Thailand (1995): 1-12. Zhang, X. The Changing Politics of Finance in Korea and Thailand: From deregulation to debacle. London: Routledge, 2003. Appendix I

39

Table 1 Financial Sector Reforms Objective Reform Measures Taken

A. Enable sharing of credit information among financial institutions

Measure to be taken in 2009 • A national credit-scoring system is planned. The National Credit Bureau (NCB) plans to implement a national credit-scoring system in terms of individual credit information early next year. The Credit Information Business Act has been effective since February 14, 2008. The bill allows the agency to set up a credit-scoring system which will benefit the credit analysis of financial institutions. Under this credit-scoring system, the borrowers would be classified with credit scores ranging from 300 to 900 points. The score below 700 points is considered to be quite negative while the score over 700 points represents a relatively healthy figure.

B. Formulate and implement a medium-term strategy for Thai financial sector

Measure to be taken in 2009 • The Financial Sector Master Plan (FSMP) Phase II is expected next year. The second phase of the FSMP, which expected to be implemented in 2009, aims to reduce operating costs of financial institutions; increase competition among financial institutions and non-bank entities through expanding the business scope permitted banks and greater foreign participation; and improve market architecture with the development of limited deposit insurance and greater variety in risk-management instruments. The new plan allows greater competition in the banking industry. The plan would strengthen the banking system by lowering the NPL ratio to less than 2% in 5 years (2013). Lower NPLs would improve the banks’ efficiency to generate more income and reduce costs due to the declining burden from provision.

C. Transition from the current blanket government guarantee on deposits to a limited deposit insurance scheme

Measure to be taken, but delayed • Customer Deposit Protection Scheme is effective with extended full protection period. The Deposit Protection Act (DPA) has been enacted and effective on August 11, 2008.Due to the recent global financial crisis, the full government guarantee period has been extended until 10 August 2011 instead of 2009 as per the approved Draft Royal Decree on Extension Bank Deposit Guarantee Act. After the 100% protection period, the protection limit will be reduced to BT 50 million and BT 1 million per person per financial institution on 11 August 2011 and 2012 respectively.

40

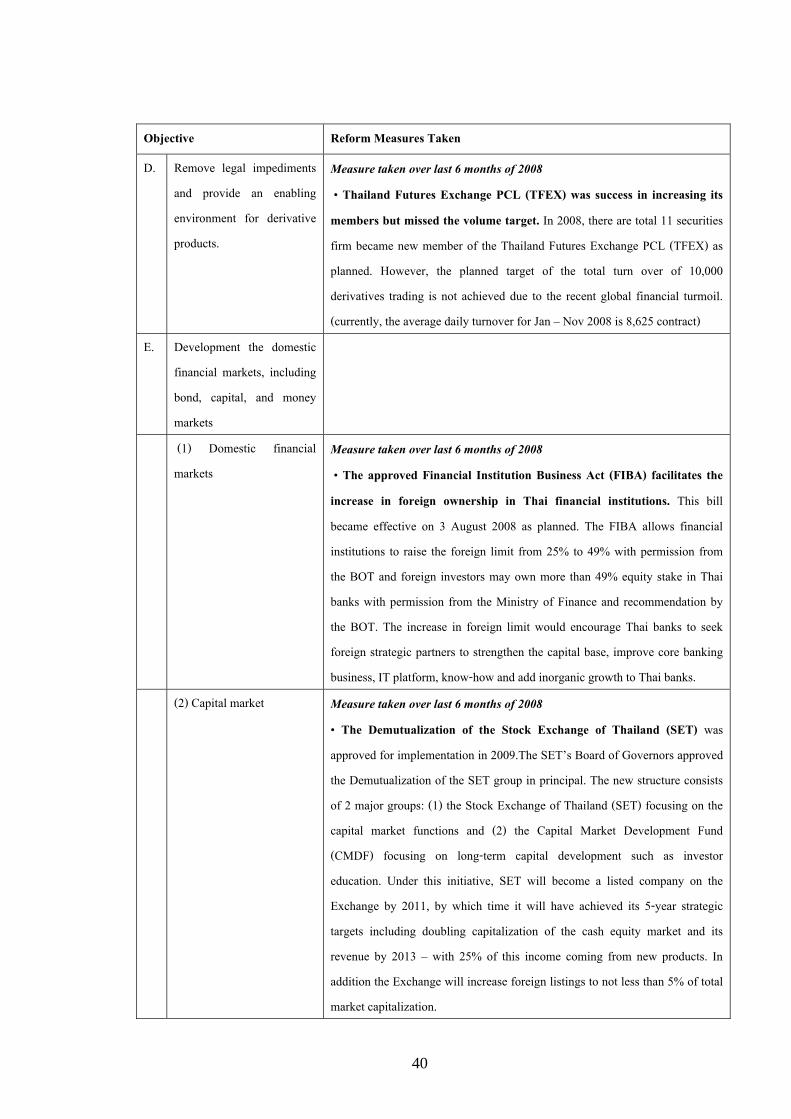

Objective Reform Measures Taken

D. Remove legal impediments and provide an enabling environment for derivative products.

Measure taken over last 6 months of 2008 • Thailand Futures Exchange PCL (TFEX) was success in increasing its members but missed the volume target. In 2008, there are total 11 securities firm became new member of the Thailand Futures Exchange PCL (TFEX) as planned. However, the planned target of the total turn over of 10,000 derivatives trading is not achieved due to the recent global financial turmoil. (currently, the average daily turnover for Jan – Nov 2008 is 8,625 contract)

E. Development the domestic financial markets, including bond, capital, and money markets

(1) Domestic financial markets

Measure taken over last 6 months of 2008 • The approved Financial Institution Business Act (FIBA) facilitates the increase in foreign ownership in Thai financial institutions. This bill became effective on 3 August 2008 as planned. The FIBA allows financial institutions to raise the foreign limit from 25% to 49% with permission from the BOT and foreign investors may own more than 49% equity stake in Thai banks with permission from the Ministry of Finance and recommendation by the BOT. The increase in foreign limit would encourage Thai banks to seek foreign strategic partners to strengthen the capital base, improve core banking business, IT platform, know-how and add inorganic growth to Thai banks.

(2) Capital market Measure taken over last 6 months of 2008 • The Demutualization of the Stock Exchange of Thailand (SET) was approved for implementation in 2009.The SET’s Board of Governors approved the Demutualization of the SET group in principal. The new structure consists of 2 major groups: (1) the Stock Exchange of Thailand (SET) focusing on the capital market functions and (2) the Capital Market Development Fund (CMDF) focusing on long-term capital development such as investor education. Under this initiative, SET will become a listed company on the Exchange by 2011, by which time it will have achieved its 5-year strategic targets including doubling capitalization of the cash equity market and its revenue by 2013 – with 25% of this income coming from new products. In addition the Exchange will increase foreign listings to not less than 5% of total market capitalization.

41

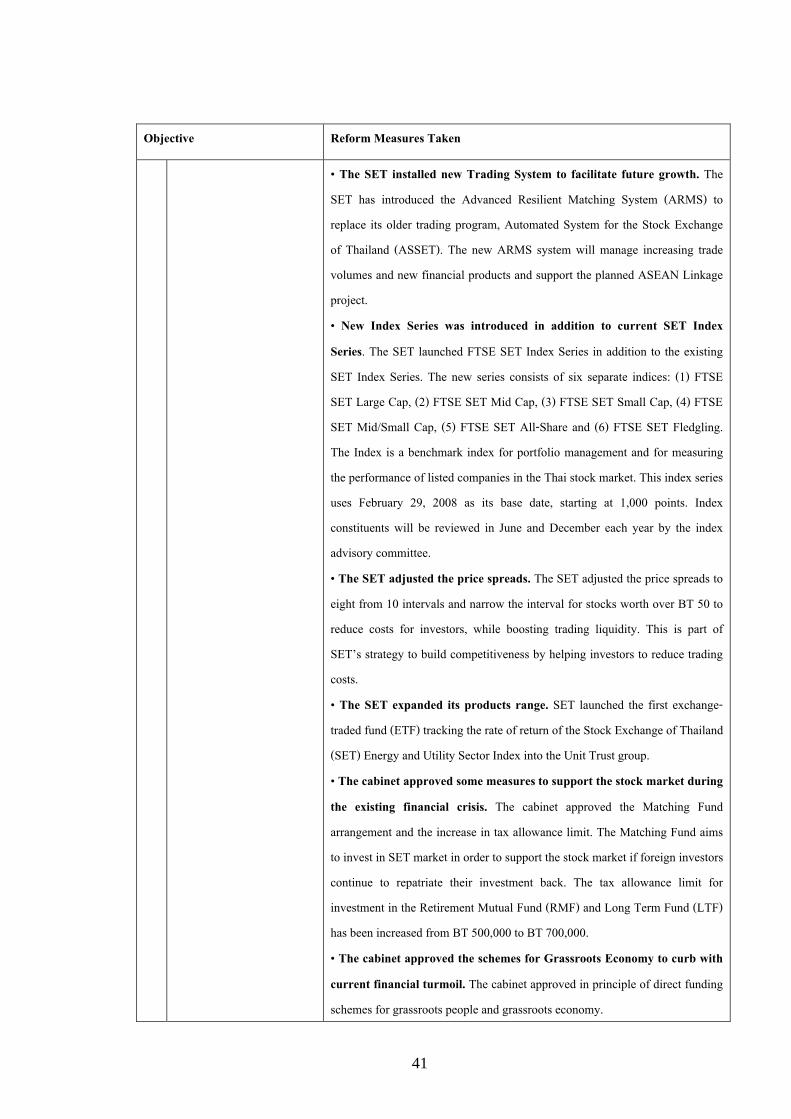

Objective Reform Measures Taken

• The SET installed new Trading System to facilitate future growth. The SET has introduced the Advanced Resilient Matching System (ARMS) to replace its older trading program, Automated System for the Stock Exchange of Thailand (ASSET). The new ARMS system will manage increasing trade volumes and new financial products and support the planned ASEAN Linkage project. • New Index Series was introduced in addition to current SET Index Series. The SET launched FTSE SET Index Series in addition to the existing SET Index Series. The new series consists of six separate indices: (1) FTSE SET Large Cap, (2) FTSE SET Mid Cap, (3) FTSE SET Small Cap, (4) FTSE SET Mid/Small Cap, (5) FTSE SET All-Share and (6) FTSE SET Fledgling. The Index is a benchmark index for portfolio management and for measuring the performance of listed companies in the Thai stock market. This index series uses February 29, 2008 as its base date, starting at 1,000 points. Index constituents will be reviewed in June and December each year by the index advisory committee. • The SET adjusted the price spreads. The SET adjusted the price spreads to eight from 10 intervals and narrow the interval for stocks worth over BT 50 to reduce costs for investors, while boosting trading liquidity. This is part of SET’s strategy to build competitiveness by helping investors to reduce trading costs. • The SET expanded its products range. SET launched the first exchange-traded fund (ETF) tracking the rate of return of the Stock Exchange of Thailand (SET) Energy and Utility Sector Index into the Unit Trust group. • The cabinet approved some measures to support the stock market during the existing financial crisis. The cabinet approved the Matching Fund arrangement and the increase in tax allowance limit. The Matching Fund aims to invest in SET market in order to support the stock market if foreign investors continue to repatriate their investment back. The tax allowance limit for investment in the Retirement Mutual Fund (RMF) and Long Term Fund (LTF) has been increased from BT 500,000 to BT 700,000. • The cabinet approved the schemes for Grassroots Economy to curb with current financial turmoil. The cabinet approved in principle of direct funding schemes for grassroots people and grassroots economy.

42

Objective Reform Measures Taken

(3) Bond market Measure taken over last 6 months of 2008 • The SET has approved the reduction in the transaction costs of the Bond Trading. The SET terminated the listing fee for bonds to promote bond listing on the local market. In addition, the SET also extended the waiver of trading fees for bond of 0.005% on trading value in order to boost bond trade and lower costs.

Source: Anantavrasilpa Ratchada, Thailand Economic Monitor December 2008 World Bank Office - Bangkok

43

Table 2: Commercial banks’ interest spread Year MLR Deposit Rate Spread

Dec-80 16.50 12.00 4.50

Dec-81 17.00 13.00 4.00

Dec-82 16.00 13.00 3.00

Dec-83 16.50 13.00 3.50

Dec-84 16.50 12.50 4.00

Dec-85 15.50 11.00 4.50

Dec-86 12.00 7.25 4.75

Dec-87 11.50 7.25 4.25

Dec-88 12.00 9.50 2.50

Dec-89 12.50 9.50 3.00

Dec-90 16.25 15.50 0.75

Dec-91 14.00 10.50 3.50

Dec-92 11.50 8.50 3.00

Dec-93 10.50 7.00 3.50

Dec-94 11.75 10.25 1.50

Dec-95 13.75 11.00 2.75

Dec-96 13.25 9.25 4.00

Dec-97 15.25 13.00 2.25

Dec-98 12.00 6.00 6.00

Dec-99 8.50 4.25 4.25

Dec-00 8.25 3.50 4.75

Dec-01 7.50 3.00 4.50

Dec-02 7.00 2.00 5.00

Dec-03 5.75 1.00 4.75

Dec-04 5.75 1.00 4.75

Dec-05 7.13 3.50 3.63

Dec-06 8.00 5.00 3.00

Dec-07 6.75 2.38 4.37 Source: Bank of Thailand

44

Table 3: International Banking Facilities (IBF's) Credits (Millions of Baht)

End of Period

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 Sep 1/

1. Out-In 197,024.4 456,643.0 680,517.2 807,633.2 1,411,362.9 767,029.4 487,123.1 386,980.3 276,947.6 208,772.5 166,468.0 153,183.9 60,302.0 n.a.