US Benefits ORACLEflex Enrollment Guide 2013 This guide contains highlights of the 2013 benefit options available through Oracle’s US employee benefits program. They are not complete descriptions of the benefits. Oracle may terminate, withdraw or modify any benefits described in this guide, in whole or in part, at any time. The descriptions of the benefits are not guarantees of current or future employment or benefits. We make every effort to ensure the accuracy of the information in this guide. If there is any conflict between this guide and official Plan Documents, the official documents will govern. For full provisions of the benefit plans described in this guide, consult the documentation specific to the plan. You can find our plan documentation on the Oracle US Benefits Website.

2 | P a g e Rev 06.14.13 cnt1509275

Introduction ................................................................................................. 6

ORACLEflex Benefits .................................................................................. 7

Your ORACLEflex Choices ....................................................................................................................... 7

Your ORACLEflex Effective Date .............................................................................................................. 7

Your ORACLEflex End Date ..................................................................................................................... 7

Your ORACLEflex Credits ......................................................................................................................... 7

Your Annual Benefits Compensation ......................................................................................................... 8

Core Coverage (Minimum Protection Requirements) ............................................................................... 8

Declining Coverage ................................................................................................................................... 9

Who’s Eligible ............................................................................................................................................ 9

How to Enroll ............................................................................................ 11

Online Enrollment System ....................................................................................................................... 11

New Hires/Newly Eligible ........................................................................................................................ 11

Annual US Benefits Open Enrollment ....................................................... 13

Make Your Open Enrollment Elections ................................................................................................... 13

Special Election Consideration for Health Care Reimbursement Account Participants .......................... 14

Qualified Status Change Events ............................................................... 14

Qualified Status Change – Effective Date ............................................................................................... 14

Qualified Status Change – Making Benefit Elections .............................................................................. 15

Beneficiary Designation ............................................................................ 15

Medical Plans ........................................................................................... 15

Eligibility – Geographic Service Area ...................................................................................................... 15

United Healthcare (UHC) Plans .............................................................................................................. 16

UHC Health and Wellness Resources .................................................................................................... 17

Premium Choice Plus PPO Plan ............................................................................................................. 17

3 | P a g e Rev 06.14.13 cnt1509275

Medium Choice Plus PPO Plan .............................................................................................................. 17

Premium and Medium Out-of-Area Plans ............................................................................................... 18

HSA Medical Plan ................................................................................................................................... 18

Exclusive Provider Organization (EPO) Choice Plan ............................................................................. 18

HPHC Passport Plan ............................................................................................................................... 18

UHC’s Preferred Prescription Drug List (PDL) ........................................................................................ 19

Mail Order Program (Maintenance Medications) .................................................................................... 20

Specialty Medications .............................................................................................................................. 20

Health Maintenance Organizations (HMOs) ........................................................................................... 20

HealthNet HMO ....................................................................................................................................... 21

Kaiser Permanente HMO ........................................................................................................................ 21

Group Health Cooperative (GHC) Washington ....................................................................................... 22

Medical Plan Selection Considerations ................................................................................................... 22

Mental Health Benefits .............................................................................. 22

Employee Assistance Program ............................................................................................................... 22

Mental Health and Substance Abuse Benefits ........................................................................................ 23

Live and Work Well ................................................................................................................................. 23

Dental Plans ............................................................................................. 23

Network and Non-Network Dentists ........................................................................................................ 24

Comprehensive Dental Plan: Pre-Treatment Estimates ......................................................................... 24

Dental Plan Selection Considerations ..................................................................................................... 25

Vision Plans .............................................................................................. 25

Network and Non-Network Eye Care Professionals ............................................................................... 25

Calendar Year Benefits Eligibility ............................................................................................................ 25

How to Use VSP ..................................................................................................................................... 26

Vision Plan Selection Considerations ..................................................................................................... 26

Disability Insurance ................................................................................... 26

4 | P a g e Rev 06.14.13 cnt1509275

Short Term Disability (STD) Insurance .................................................................................................... 26

Long Term Disability (LTD) Insurance ..................................................................................................... 27

Long Term Disability (LTD): Pre-Tax vs. After-Tax Coverage ................................................................. 27

Long Term Disability (LTD) Selection Considerations ............................................................................. 28

Life Insurance ........................................................................................... 28

Employee Pre-Tax Life Insurance ........................................................................................................... 28

After-Tax Life Insurance .......................................................................................................................... 29

After-Tax Life Insurance Coverage for You ............................................................................................. 29

Life Insurance Coverage for Your Spouse/Domestic Partner ................................................................. 29

Life Insurance Coverage for Your Children ............................................................................................. 29

Changing Your Life Insurance – Annual Open Enrollment ...................................................................... 30

Changing Your Life Insurance – Qualified Status Change ...................................................................... 30

Life Insurance and AD&D Selection Considerations ............................................................................... 30

Accidental Death and Dismemberment (AD&D) Insurance ....................... 31

Changing Your AD&D Insurance – Annual Open Enrollment .................................................................. 31

Health and Dependent Care Reimbursement Accounts ............................ 31

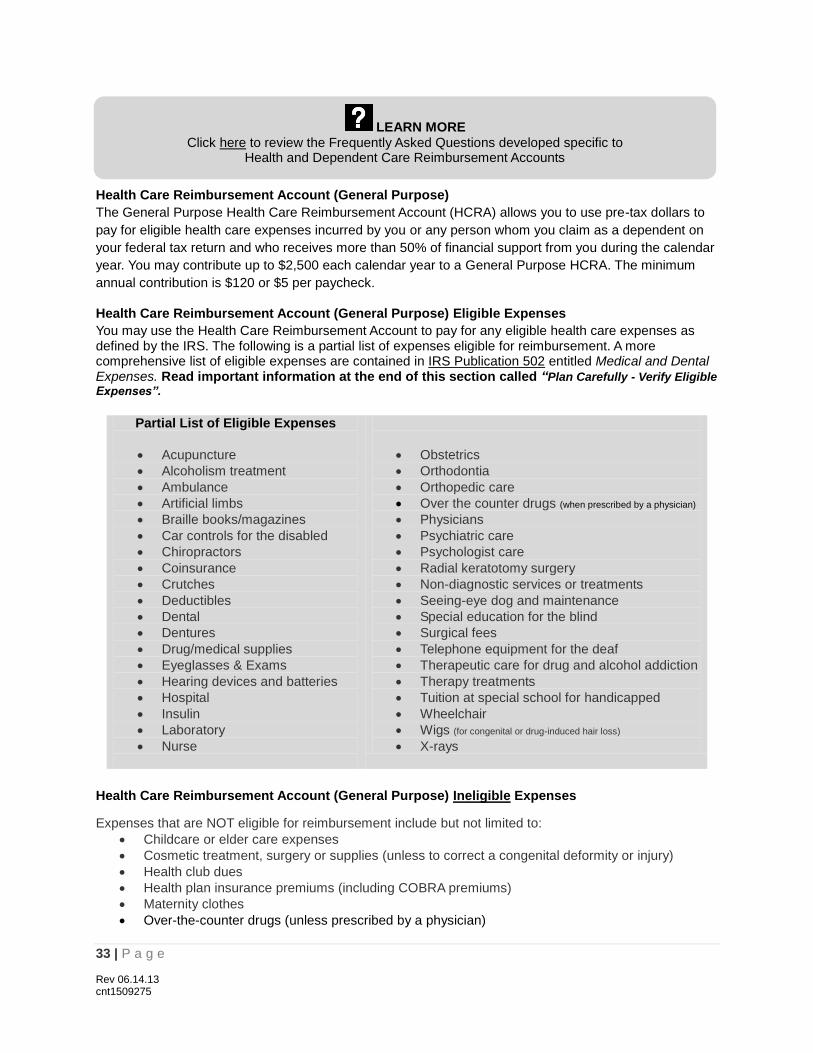

Health Care Reimbursement Account (General Purpose) ...................................................................... 33

Health Care Reimbursement Account (General Purpose) Eligible Expenses ........................................ 33

Health Care Reimbursement Account (General Purpose) Ineligible Expenses ...................................... 33

Health Care Reimbursement Account (Limited Purpose) ....................................................................... 34

Health Care Reimbursement Account Enrollment Considerations ......................................................... 34

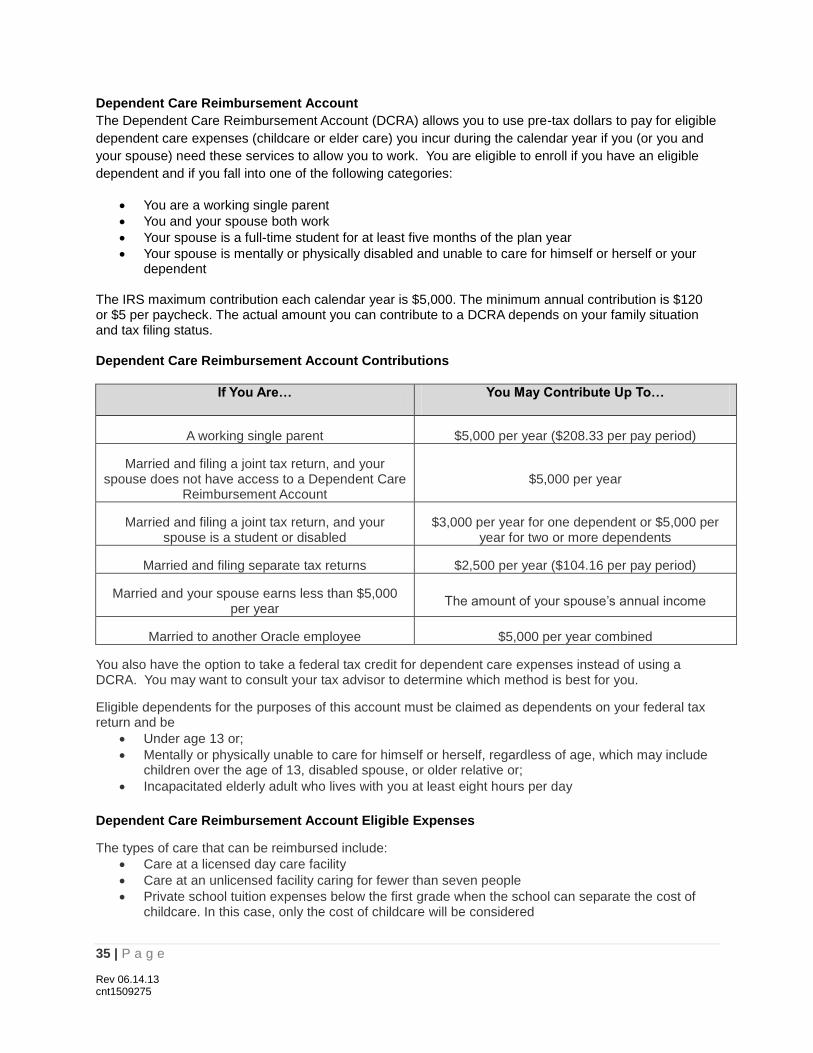

Dependent Care Reimbursement Account ............................................................................................. 35

Dependent Care Reimbursement Account Eligible Expenses ................................................................ 35

Dependent Care Reimbursement Account Ineligible Expenses ............................................................. 36

Dependent Care Reimbursement Account Enrollment Considerations .................................................. 36

Group Legal Plans .................................................................................... 36

Financial Planning .................................................................................... 37

5 | P a g e Rev 06.14.13 cnt1509275

Long Term Care Insurance........................................................................ 39

Personal Insurance (Auto / Home / Renters) ............................................. 39

Health Care Reform .................................................................................. 39

Maximize Your Benefits ............................................................................. 40

6 | P a g e Rev 06.14.13 cnt1509275

2013 Benefits Enrollment Guide

Introduction

This enrollment guide provides information for employees enrolling in ORACLEflex for the first time and

during the annual Open Enrollment period. This guide is an excellent reference tool to assist you in

making your enrollment decisions. The enrollment criteria may differ between new hire/newly eligible and

Open Enrollment elections and these differences are marked in the document where applicable.

Additional resources to assist in your decision making process includes:

Oracle Benefits Website: Located at www.oraclebenefits.com, this is your best source for benefits

and enrollment information. From this website, you can find direct links to program information on all

Oracle benefit plan offerings. Visit “The Basics” to view general information available outside of the

Oracle firewall. For confidentiality purposes the detailed plan information requires you to log into the

Oracle network to access them. Visit “Full Website and Details” to access the entire site.

Top Picks: The Oracle US Benefits Website is a great place to find information but you may not have

the time to review each and every page or even know where to begin. To help you navigate quickly

and efficiently to key information we’ve pulled together our “Top Picks” to help you enroll.

This Enrollment Guide

Comparison Charts (medical, dental, vision)

Prices and Credits

Vendor Contacts

Family Status Change

Summary Plan Description (SPD)

HSA Medical Plan Resource Center

What’s New: Accessible on the Oracle US Benefits Website this important document highlights key

information about the annual Open Enrollment period including deadlines, enrollment instructions,

information resources, and new plan and prices changes.

Plan Comparison Charts: Side-by-side review of the key features of the medical, dental, and vision

plans. Use these helpful charts to learn more about the benefits that best meet the needs of you and

your family. You can access the information by visiting the Oracle US Benefits Website and selecting

"The Basics”

Summary Benefits Coverage (SBC): There is an individual Summary Benefits Coverage or SBC for

each Oracle medical plan offering and are designed to provide an overview of key plan features and

benefit coverage such as co-pays and coinsurance. You can use the SBCs to view benefits, make

comparisons between the different medical plans, and view cost scenario examples. You can access

the information by visiting the Oracle US Benefits Website and selecting "The Basics”. They are also

available in the online enrollment tool.

HSA Medical Plan Resource Center: This Oracle sponsored website provides information, tools,

tutorials, and FAQs regarding the HSA Medical Plan. You can access the information by visiting the

HSA Medical Plan Resource Center.

7 | P a g e Rev 06.14.13 cnt1509275

NEW HIRES

Flex credits and deductions for new hires/newly eligible

employees will be retroactive to your eligibility date (e.g. hire

date) and adjusted on your paycheck.

ORACLEflex Benefits

Your ORACLEflex Choices

As an Oracle employee – you are eligible to enroll in the following benefit program choices. This enrollment guide contains additional information about each of the programs.

Medical

Employee Assistance Program (EAP)l

Mental Health & Substance Abuse

Dental

Vision

Long Term Disability (LTD) Insurance

Life/Accidental Death & Dismemberment (AD&D) Insurance

Health (General and Limited Purpose) & Dependent Care Reimbursement Accounts

Group Financial and Legal Services

Long Term Care (LTC) Insurance

Personal Auto/Home/Renters Insurance

Your ORACLEflex Effective Date

Newly Eligible/New Hires Annual Benefits Open Enrollment

All benefits are effective on your eligibility date (e.g.

new hire date). This means you will be retroactively

enrolled in the plans you select. Retroactive payroll

deductions may apply.

Open Enrollment is held each fall. All elections are

effective on January 1 following the enrollment

period

Your ORACLEflex End Date

Your benefits end effective midnight of the day you lose eligibility (e.g. termination date). In the event of

an employee’s death, medical, dental, and vision benefits for covered family members will automatically

continue for an additional 30 days. Eligible dependents may elect COBRA to continue coverage beyond

this 30 day period.

Your ORACLEflex Credits

ORACLEflex allows you to choose the benefit plans and coverage

levels that are right for you and your family. Each pay period,

Oracle provides a specified amount of ORACLEflex credits to

purchase your benefits. Full-time regular employees working 30

hours or more per week receive full flex credits. All regular part-

time employees working an average of 20–29 hours per week

receive 50% of the full-time employee ORACLEflex credits.

Your take-home pay will be affected by the benefit elections that

you make. If the benefits you choose cost less than the amount of

your ORACLEflex credits, the difference will be applied to your paycheck as taxable income. If the

benefits you choose cost more than the amount of your ORACLEflex credits, you pay the difference

through pre-tax or after-tax payroll deductions, depending on the benefit plan. The chart below provides

basic information about your ORACLEflex credits. Login to the ORACLEflex Enrollment System to view

the prices and flex credits applicable to you each pay period.

8 | P a g e Rev 06.14.13 cnt1509275

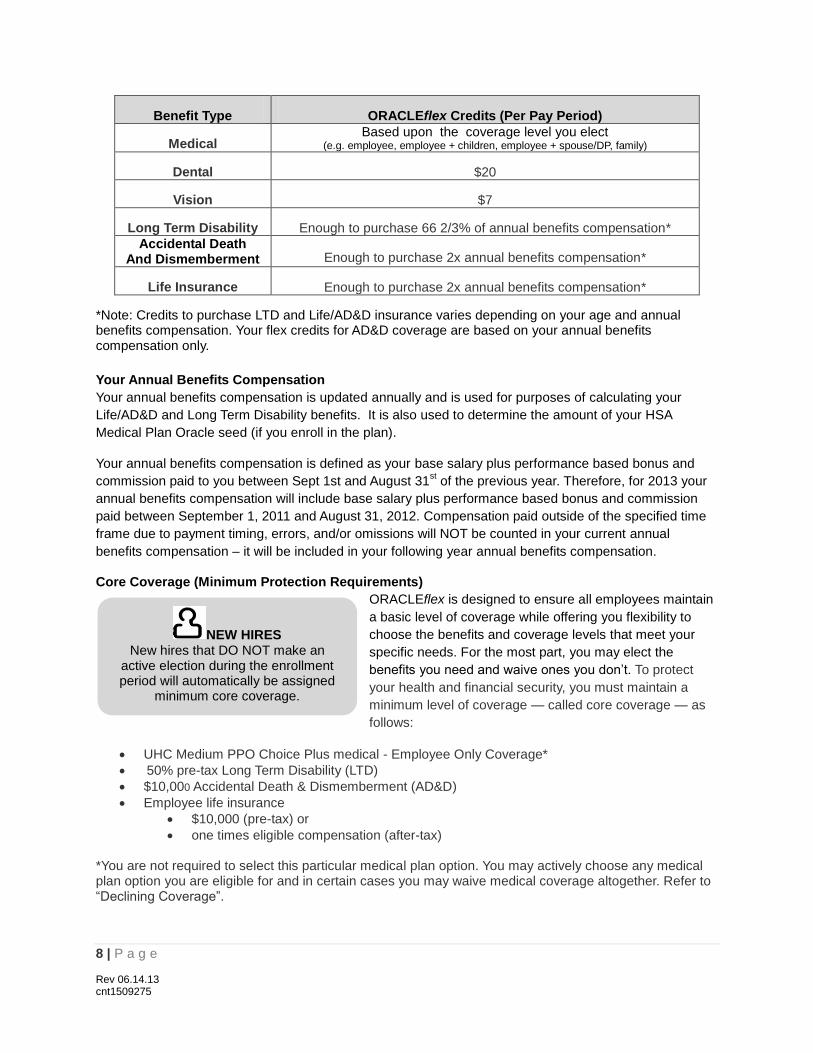

NEW HIRES

New hires that DO NOT make an active election during the enrollment period will automatically be assigned

minimum core coverage.

Benefit Type ORACLEflex Credits (Per Pay Period)

Medical Based upon the coverage level you elect

(e.g. employee, employee + children, employee + spouse/DP, family)

Dental $20

Vision $7

Long Term Disability Enough to purchase 66 2/3% of annual benefits compensation*

Accidental Death And Dismemberment Enough to purchase 2x annual benefits compensation*

Life Insurance Enough to purchase 2x annual benefits compensation*

*Note: Credits to purchase LTD and Life/AD&D insurance varies depending on your age and annual benefits compensation. Your flex credits for AD&D coverage are based on your annual benefits compensation only.

Your Annual Benefits Compensation

Your annual benefits compensation is updated annually and is used for purposes of calculating your

Life/AD&D and Long Term Disability benefits. It is also used to determine the amount of your HSA

Medical Plan Oracle seed (if you enroll in the plan).

Your annual benefits compensation is defined as your base salary plus performance based bonus and

commission paid to you between Sept 1st and August 31st of the previous year. Therefore, for 2013 your

annual benefits compensation will include base salary plus performance based bonus and commission

paid between September 1, 2011 and August 31, 2012. Compensation paid outside of the specified time

frame due to payment timing, errors, and/or omissions will NOT be counted in your current annual

benefits compensation – it will be included in your following year annual benefits compensation.

Core Coverage (Minimum Protection Requirements)

ORACLEflex is designed to ensure all employees maintain

a basic level of coverage while offering you flexibility to

choose the benefits and coverage levels that meet your

specific needs. For the most part, you may elect the

benefits you need and waive ones you don’t. To protect

your health and financial security, you must maintain a

minimum level of coverage — called core coverage — as

follows:

UHC Medium PPO Choice Plus medical - Employee Only Coverage*

50% pre-tax Long Term Disability (LTD)

$10,000 Accidental Death & Dismemberment (AD&D)

Employee life insurance

$10,000 (pre-tax) or

one times eligible compensation (after-tax) *You are not required to select this particular medical plan option. You may actively choose any medical plan option you are eligible for and in certain cases you may waive medical coverage altogether. Refer to “Declining Coverage”.

9 | P a g e Rev 06.14.13 cnt1509275

Minimum core coverage does NOT include:

Coverage for eligible dependents

Dental

Vision

Long Term Care

Group Legal

Financial Services

Declining Coverage

You may decline medical coverage provided you can verify coverage from another source, such as your

spouse/domestic partner’s medical plan. If you choose to decline medical coverage, you will receive a

minimal per pay period waive credit that will offset your total benefits cost. Dental and vision coverage are

not included in core coverage and you are not required to enroll in these plans. If you waive dental or

vision coverage you receive a minimal per pay period credit.

Who’s Eligible

Employees and Dependents

Employees

All regular full-time employees on the Oracle U.S. payroll working 30 hours or more per week and regular

part-time employees working at an average of 20–29 hours per week are eligible to enroll in ORACLEflex

plans. Independent contractors and/or "leased employees" engaged by a staff leasing company are not

eligible for ORACLEflex benefits.

Dependents Your spouse or domestic partner and your children are eligible to enroll in certain ORACLEflex benefits.

The list below provides general information. It is recommended that you review the “Eligibility” section of

the Summary Plan Description for complete details.

Your spouse/domestic partner includes:

Your spouse recognized under federal law

Your qualified same or opposite sex domestic partner

Your children include:

Your natural and/or adopted children

Your children placed with you for adoption

Your domestic partner’s children

Your stepchildren

Your children for whom you are the legal guardian and a federal tax dependent

Your children for whom you are required to provide coverage as the result of a Qualified Medical Child Support Order

10 | P a g e Rev 06.14.13 cnt1509275

LEARN MORE For more information regarding Domestic Partner coverage visit the Oracle US Benefits Website

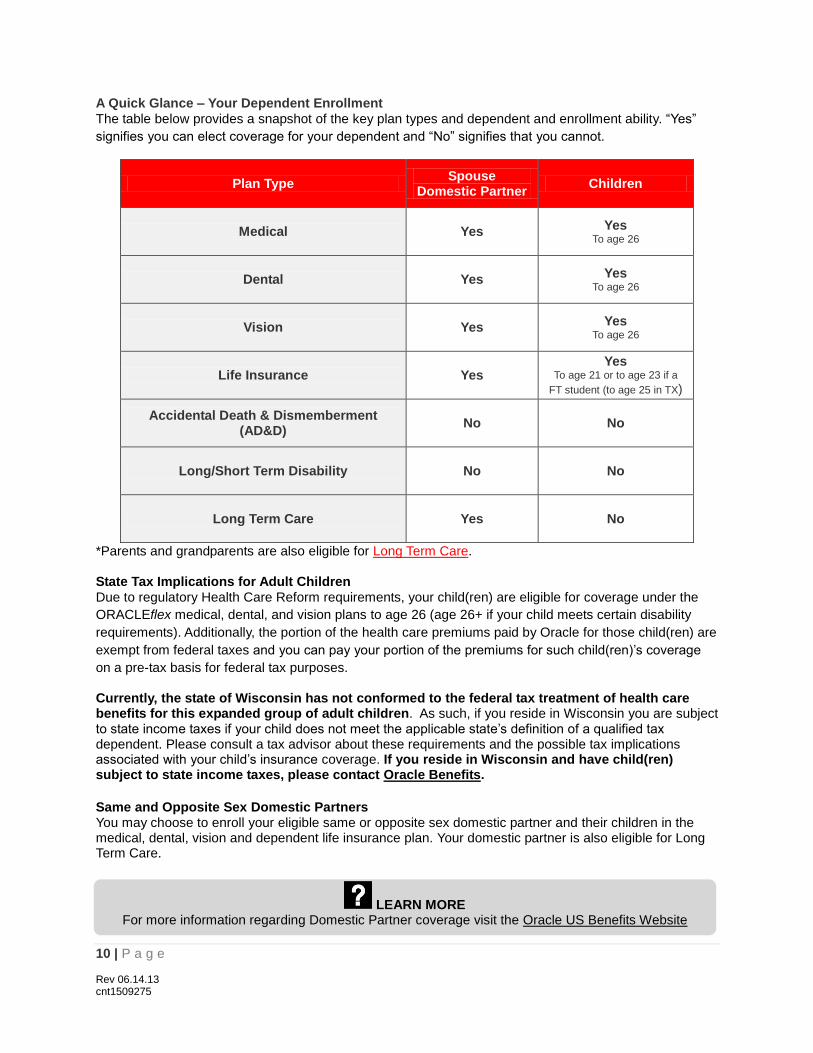

A Quick Glance – Your Dependent Enrollment

The table below provides a snapshot of the key plan types and dependent and enrollment ability. “Yes”

signifies you can elect coverage for your dependent and “No” signifies that you cannot.

Plan Type Spouse

Domestic Partner Children

Medical Yes Yes

To age 26

Dental Yes Yes

To age 26

Vision Yes Yes

To age 26

Life Insurance Yes Yes

To age 21 or to age 23 if a

FT student (to age 25 in TX)

Accidental Death & Dismemberment (AD&D)

No No

Long/Short Term Disability No No

Long Term Care Yes No

*Parents and grandparents are also eligible for Long Term Care.

State Tax Implications for Adult Children

Due to regulatory Health Care Reform requirements, your child(ren) are eligible for coverage under the

ORACLEflex medical, dental, and vision plans to age 26 (age 26+ if your child meets certain disability

requirements). Additionally, the portion of the health care premiums paid by Oracle for those child(ren) are

exempt from federal taxes and you can pay your portion of the premiums for such child(ren)’s coverage

on a pre-tax basis for federal tax purposes.

Currently, the state of Wisconsin has not conformed to the federal tax treatment of health care benefits for this expanded group of adult children. As such, if you reside in Wisconsin you are subject to state income taxes if your child does not meet the applicable state’s definition of a qualified tax dependent. Please consult a tax advisor about these requirements and the possible tax implications associated with your child’s insurance coverage. If you reside in Wisconsin and have child(ren) subject to state income taxes, please contact Oracle Benefits.

Same and Opposite Sex Domestic Partners You may choose to enroll your eligible same or opposite sex domestic partner and their children in the medical, dental, vision and dependent life insurance plan. Your domestic partner is also eligible for Long Term Care.

11 | P a g e Rev 06.14.13 cnt1509275

Employees Who Enroll a Same Sex Domestic Partner

Under ORACLEflex benefits, same sex-spouses who are legally married under state law and partners

who have entered into a valid civil union under state law are treated as an eligible domestic partner.

Applicable benefits and state law protections will be offered to same-sex spouses, civil union partners and

certain state registered domestic partners in the same manner as a spouse. Any special tax treatment

remains the responsibility of the employee and should be addressed when filing your state income tax

return.

Note: Certain portions of ORACLEflex benefits are governed by federal law and do not provide the same

provisions for domestic partners as they do for a legal spouse. In these cases, the federal treatment of

domestic partners is not treated in the same manner as spousal benefits.

California Employees Who Enroll a Same Sex Domestic Partner (CA Only):

Assembly Bill 25 (AB 25) provides the right to receive employer provided health coverage for a domestic

partnership without additional state income taxation. Federal tax still applies. Application of this law

requires registration of the domestic partnership with the State of California. AB 25 may also extend to

opposite-sex domestic partners if one or both partners are over age 62 and one or both partners meet

specified eligibility criteria under the Social Security Act. Any special tax treatment remains the

responsibility of the employee and should be addressed when filing your state income tax return.

When You and Spouse/Domestic Partner Are Oracle Employees If both you and your spouse/domestic partner are employed by Oracle, you may not have “double

coverage” under the ORACLEflex medical, dental and vision plans. This means you may not be covered

as both an Oracle employee and as a dependent of another Oracle employee for these plans. In addition,

you and your spouse/domestic partner may not cover the same child as a dependent for any benefit.

However, you may both elect spouse/domestic partner after-tax life insurance for one another. If one or

both of you choose to “double cover” under the employee and spouse/domestic partner life insurance

options, the combined maximum amount of life insurance coverage you may purchase is $2,050,000.

Rehires

If you leave Oracle and are rehired within 30 days, the benefits you were enrolled in on your termination

date will automatically be reinstated. If you are rehired after 30 days, you must re-enroll for benefits.

Please be advised that if you are a rehire and previously enrolled in the UHC POS Choice Plus plan, it is

no longer an enrollment option for you. Additionally, if you have been on a leave of absence where you

were ineligible for benefits for more than 30 days, you will not be able to re-elect this plan upon your

return to active status.

How to Enroll

Online Enrollment System

Enrolling in ORACLEflex benefits is simple and easy to do. And, the system is accessible outside of

Oracle’s firewall giving you the flexibility to enroll anywhere with internet connection. When accessing

from outside of the Oracle firewall you will be required to login using your Oracle OCS - Single-Sign-On

(SSO) Username and Password. In addition to enrolling in benefits - you may also add or make changes

to your dependents and designate or modify your life insurance, accidental death & dismemberment, and

401(k) plan beneficiaries.

New Hires/Newly Eligible

Newly eligible employees will receive an email approximately one week after your eligibility date (e.g. your

hire date) and a letter will be sent via US mail to your home address approximately two weeks after your

12 | P a g e Rev 06.14.13 cnt1509275

NEW HIRES Avoid Late Enrollment: You are considered a late enrollee if you do not enroll by your specified

deadline. Late enrollees are automatically assigned the minimum core benefit coverage. Core coverage does NOT cover your eligible dependents - nor does it include dental, and vision.

eligibility date. The enrollment email and letter provide you with important information and instructions -

including your enrollment deadline.

Upon receipt of either one of these communications, you can access the ORACLEflex Enrollment System

and make your elections. You can make changes to your enrollment up to your deadline. If you don’t

enroll by the specified deadline, you will automatically be enrolled in the required minimum core benefits.

Refer to the “Core Coverage” section of this document.

System Access

There is a slight delay in your ability to access the enrollment system. If your hire date is a Monday or

Tuesday you will generally be able to make your elections on Wednesday. If your hire date is Wednesday,

Thursday, or Friday you will generally be able to make your elections on the following Monday. You will

be notified via email when you are able to make your elections.

Enrollment Instructions To make your US Benefits elections, visit the ORACLEflex Enrollment System. You may access the

enrollment system in or outside of the Oracle firewall. When accessing from outside of the Oracle firewall

you will be required to login using your Oracle OCS - Single-Sign-On (SSO) Username and Password.

Follow the online instructions to make your benefit elections

You can enter and exit the enrollment application, as many times as needed, up until your election deadline. At that point, your elections are binding

When you have completed your elections, please review your summary of elections for accuracy and keep a copy for your records

The benefits shown on your election summary will remain in effect for the plan year unless you experience a qualified family status change.

Your ORACLEflex Personal Summary Your ORACLEflex Personal Summary is a confirmation of the benefit plans you are electing for the new

plan year. To view your Personal Summary, login to the ORACLEflex Enrollment System and click on any

underlined plan to review or make changes to your elections. Initially, your Personal Summary will reflect

the required core coverage benefits. However, once you make your active elections, your Personal

Summary will reflect your selected coverage.

Your ORACLEflex Personalized Confirmation Statement

After you submit your election, you will receive an e-mail confirming your elections have been recorded.

Upon receipt of this email you can view your Confirmation Statement online. Please review this statement

carefully for accuracy and make any corrections prior to the enrollment date deadline listed in your e-mail.

If you do not make your corrections prior to your deadline, the benefits and enrolled dependent(s)

reflected on your Confirmation Statement will remain in place through the year unless you have a

qualifying status change. Refer to the Oracle US Benefits website “Family Status Change” to learn more

about qualifying events.

13 | P a g e Rev 06.14.13 cnt1509275

Annual US Benefits Open Enrollment

2013 Open Enrollment Period: October 29 – November 20, 2012 Important: The Open Enrollment end date has been extended from November 16 to November 20. Take advantage of your annual opportunity to review your benefit options and make changes if needed. Be sure to review the “What’s New” document which includes plan and price changes for 2013. This important read can be found on the Oracle US Benefits Website.

The following actions must be completed on or before the deadline - November 20.

Review your benefits

Add/change your current benefit plan elections

Add/cancel coverage for yourself and eligible dependents

Enroll or make changes to your Health/Dependent Care Reimbursement Accounts

Review and update your dependent information and beneficiary designations as needed Note: Dependents removed from coverage during the annual Open Enrollment period is not an IRS qualifying COBRA event and are NOT eligible for COBRA benefits continuation.

Make Your Open Enrollment Elections

Access the ORACLEflex Enrollment System to review, enroll, and/or make changes to your benefits. Any

plan and/or premium changes become effective January 1, 2013 and remain in effect for the entire year.

Your next opportunity to make changes to your benefits is the next annual Open Enrollment period or if

you have a qualifying status change event. For more information about how to enroll - refer to the “How to

Enroll” section of this document.

IMPORTANT

Health and Dependent Care Reimbursement Accounts Automatic Re-Enrollment Health Care and Dependent Care Reimbursement elections will automatically roll-over into 2013, unless you make an election to discontinue, change your contribution amount, or currently have a Health Care Reimbursement Account election greater than $2,500.

Partial Year Election If you enrolled mid-year, your partial year election will carry over and will apply to the entire 2013 calendar year. If you participated in only a portion of the year, you may want to adjust your election accordingly.

Health Care Reimbursement Account – NEW REDUCED MAXIMUM ($2,500) Effective January 1, 2013 Health Care Reform laws require employers to REDUCE the maximum Healthcare Reimbursement Account contribution from $5,000 to $2,500. The Limited Purpose Healthcare and Dependent Care Reimbursement Account maximum amounts will not change.

Plan accordingly and take the appropriate action during Open Enrollment. For more information, refer to section in this document “Special Election Consideration for Health Care

Reimbursement Account Participants”

14 | P a g e Rev 06.14.13 cnt1509275

Newborns/Newly Adopted Children Coverage is NOT Automatic

You must add your new dependent(s) to your coverage and make any other benefit changes within the established timeframes. Your new child(ren) are NOT automatically enrolled for you.

Special Election Consideration for Health Care Reimbursement Account Participants

If you do not make any changes, all current elections will automatically roll forward into 2013 including

Health/Dependent Care Reimbursement Accounts, unless your current Health Care Reimbursement

Account contribution election is greater than $2,500.

If your current Health Care Reimbursement Account election is greater than $2,500 you should

reduce your election for 2013. If you do not take action during the Open Enrollment period – your

current election will automatically drop to the new maximum of $2,500.

If your current Health Care Reimbursement Account election is equal to or less than $2,500 your

current election will continue in 2013 unless you make a change during the Open Enrollment period.

Qualified Status Change Events

You may be eligible to make changes to benefit elections during the plan year due to a qualifying status change. In general, qualifying status changes include the following:

Your marriage or divorce

Birth or adoption

Children placed with you for adoption

Loss of dependent status

Change of your spouse/domestic partner’s coverage

Spouse/domestic partner's Open Enrollment

Beginning/ending of domestic partnership

Qualified Status Change – Effective Date

The event date and the effective date of coverage are not always the same. For the most part, qualifying

status changes will be effective the day you complete your online status change enrollment, not the date

the event occurred. If you want your new election to be effective on the date of your qualifying status

change, you must submit the change on the qualifying status change event date or contact Oracle

Benefits for assistance prior to the event date.

There are certain qualifying event changes where benefits are retroactive to the event date provided you

make your benefit changes within 62 days (30 days for Kaiser and HealthNet) of the change. Events

include:

Birth or adoption

Ineligible dependents (e.g. divorce, over-aged dependent children)

LEARN MORE

To learn more about qualifying status changes, eligible benefit changes, change effective dates, and

notification requirements defined by the Internal Revenue Service visit the Oracle US Benefits Website

15 | P a g e Rev 06.14.13 cnt1509275

Qualified Status Change – Making Benefit Elections

Submit your benefit elections by accessing the ORACLEflex Enrollment System. You must make your

changes within 62 days of the status change (30 days for Kaiser and HealthNet). You can make benefit

changes that are directly related to your status change. For example, if you adopt a child, you may add

the child to your current medical plan, but you may not drop your spouse’s medical coverage at that time.

Upon successful submission of your new benefit elections, the online enrollment application will provide

immediate confirmation of the elections you made. If applicable, new medical ID cards will be mailed to

your home address approximately 10 – 15 business days following your election. ID cards are not

required for dental or vision coverage.

Beneficiary Designation

Access the ORACLEflex Enrollment System at anytime to designate, review, or update your life

insurance, accidental death & dismemberment insurance, and 401(k) plan beneficiary information. If you

enrolled in the UHC HSA Medical Plan you must make your Health Savings Account beneficiary

designation directly with the OptumHealth Bank. You may access the form from the OptumHealth Bank

website.

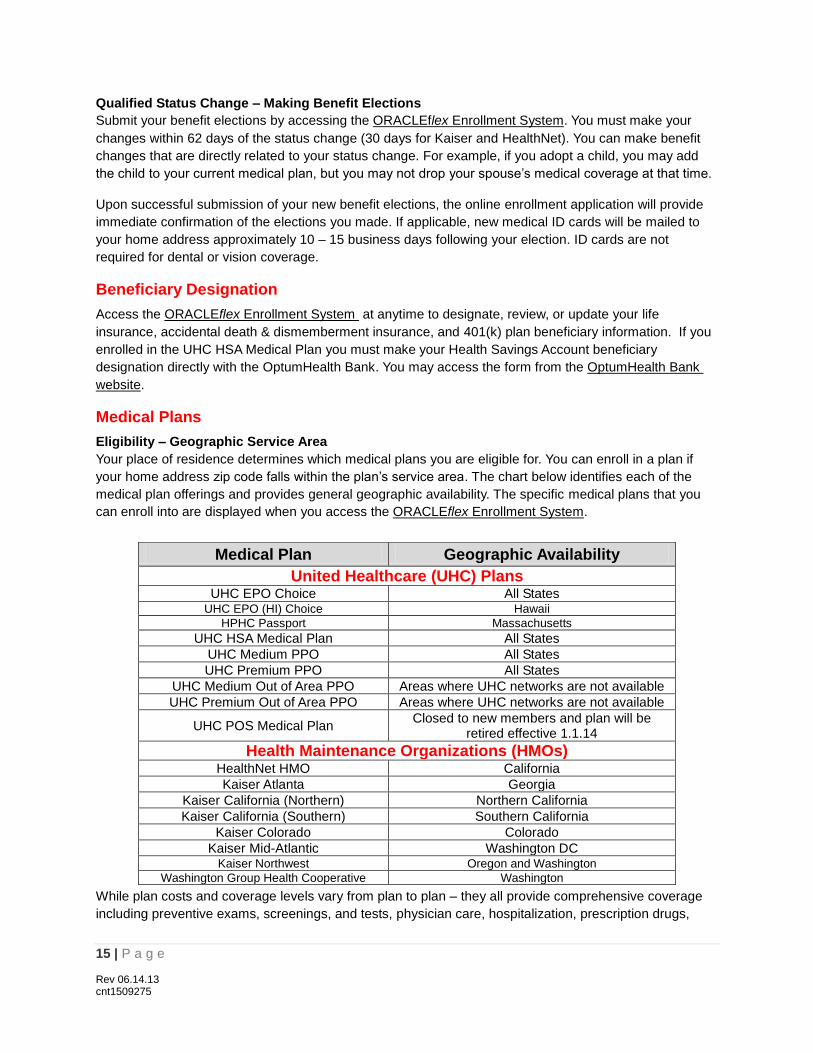

Medical Plans

Eligibility – Geographic Service Area

Your place of residence determines which medical plans you are eligible for. You can enroll in a plan if

your home address zip code falls within the plan’s service area. The chart below identifies each of the

medical plan offerings and provides general geographic availability. The specific medical plans that you

can enroll into are displayed when you access the ORACLEflex Enrollment System.

While plan costs and coverage levels vary from plan to plan – they all provide comprehensive coverage

including preventive exams, screenings, and tests, physician care, hospitalization, prescription drugs,

Medical Plan Geographic Availability

United Healthcare (UHC) Plans UHC EPO Choice All States

UHC EPO (HI) Choice Hawaii HPHC Passport Massachusetts

UHC HSA Medical Plan All States

UHC Medium PPO All States

UHC Premium PPO All States

UHC Medium Out of Area PPO Areas where UHC networks are not available

UHC Premium Out of Area PPO Areas where UHC networks are not available

UHC POS Medical Plan Closed to new members and plan will be

retired effective 1.1.14

Health Maintenance Organizations (HMOs) HealthNet HMO California

Kaiser Atlanta Georgia

Kaiser California (Northern) Northern California

Kaiser California (Southern) Southern California

Kaiser Colorado Colorado

Kaiser Mid-Atlantic Washington DC Kaiser Northwest Oregon and Washington

Washington Group Health Cooperative Washington

16 | P a g e Rev 06.14.13 cnt1509275

Usual, Reasonable & Customary

When you obtain routine care outside

of your insurance company’s network,

the eligible expense for your benefit is

a portion of the usual, reasonable, and

customary (UCR) charges.

UCR charges are determined by

looking at the fees for medical services

and supplies across the nation and

determining whether your provider’s

fees are in line with those of other

providers in your area. Non-network

services that exceed UCR are not

covered under the UHC plans and you

are required to pay any amount above

UCR.

If your provider’s fees exceed UCR

your Explanation of Benefits (EOB) will

show an amount you must pay over

what the plan pays for services. Any

excess amount you pay does not count

toward your annual deductible or out-

of-pocket maximum. However, these

expenses may qualify for the Health

Care Reimbursement Account (HCRA)

and Health Savings Account (HSA) if

you are an enrolled participant.

You are NOT responsible for charges

in excess of eligible expenses when

you receive covered services within

the network.

emergency care, and mental health/substance abuse intervention. Medical ID cards for all plans are

mailed to your home address approximately 10 – 15 business days after you submit your election.

United Healthcare (UHC) Plans

ORACLEflex offers you a choice of United Healthcare (UHC) medical plans including Choice Plus

Preferred Provider Options (PPOs), a Choice Exclusive Provider Organization (EPO) plan and a Choice

Plus High Deductible Health Plan (HDHP).

The UHC plans are self-insured – which means Oracle pays UHC an administrative fee to pay for things

such as access to provider network, claims processing, customer service, and participation in care

management programs, systems, and tools. Additionally – Oracle pays for ALL of the claims incurred by

you and your family.

All UHC plans utilize the same large nationwide network and

you are encouraged to use network providers whenever

possible. For the most part the provider attrition rate is low

and the network continues to grow. You are encouraged to

verify the network status of your provider before seeking care.

Most of the UHC plans allow you to see any licensed

physician or health care facility – while a few require that you

see only network providers (except in an emergency).

Medical claims for eligible services are discounted as a result

of negotiated contract agreements between the providers and

UHC. This results in lower cost to Oracle and to you. Network

providers will also handle claim submission and any required

authorizations for you (such as hospitalization).

If you obtain care from a non-network provider you will be

responsible for a deductible and the plans will cover a

percentage of the usual, reasonable, and customary (UCR)

charges. UCR charges are generally more than UHC’s

negotiated rates and any expenses exceeding UCR charges

are your responsibility. When you use non-network providers,

you may need to file claim forms and manage authorizations

(if required) to avoid a penalty.

Each of the UHC plans includes a safety net against

catastrophic injury or illness that may result in high cost

claims. The plans’ calendar year out-of-pocket maximum

varies between plans - however each limit the amount you will

be required to pay each year. Should you reach your annual

out-of-pocket maximum the plans will pay 100% of eligible

expenses for the rest of the year.

Eligible services are the same in all UHC plans – however the

plan coverage and your out-of-pocket cost varies by plan. To

review and compare plan features including co-pays,

17 | P a g e Rev 06.14.13 cnt1509275

DID YOU KNOW Wellness and Prevention Starts with You

ALL Oracle sponsored medical plans cover eligible preventive care services at 100% if received by

network providers. UHC members can visit www.uhcpreventivecare.com for more information about

preventive care services and guidelines. The HMO websites offer similar information.

UHC Medical Plan members have access to a variety of health and wellness resources including preventive care, 24/7 nurseline services, chronic condition, and family planning support. For more

information access the UHC Health & Wellness Resource Guide

deductibles, coinsurance, and out-of pocket maximums you are encouraged to review the Medical

Comparison Chart.

When you enroll in a UHC Plan, prescription drug coverage is included. Your medical ID card also serves

as your prescription drug ID card. For Tier 1 drugs you are responsible to pay the applicable co-pay. Tier

2 and Tier 3 drugs are subject to coinsurance. A minimum and maximum applies which means there is a

minimum amount you will be required to pay – and a maximum amount which limits your financial risk if

you require costly medications. Although coinsurance applies to Tier 2 and Tier 3 medications -

prescription drug coverage DOES NOT require a deductible (The exception is the HSA Medical Plan –

this plan requires you meet the plan deductible before coinsurance applies). For cost savings and

convenience, you may also choose to use the mail-order program for maintenance prescriptions. Review

the Medical Comparison Chart to view prescription drug coverage details.

UHC Health and Wellness Resources

There are a variety of programs and support services to improve the health of you and your family

members. These free services are included automatically when you enroll in one of the UHC plans.

Services and programs include a 24/7 Nurseline, Employee Assistance Program, Healthy Pregnancy, and

dedicated nurse advocates to help manage complex and chronic conditions. An information brochure that

contains ALL of the programs is available in both electronic and pdf format. You may not need any of the

services today – however it is always recommended that you remain informed about the programs

available. Digital Format / PDF Format

Choice Plus Preferred Provider Options (PPOs)

Premium Choice Plus PPO Plan

The rich coverage of the UHC Premium Choice Plus PPO Plan makes this plan attractive. However, due

to the high plan value it is also has the highest per pay period premium of the UHC plans. Network

physician’s office visits are covered at 100% after you pay the applicable co-pay and, most other network

services are also covered at 100% after you pay the annual deductible. The majority of network services

do not require you to meet a deductible – however a deductible is applied to a few services including in-

patient facility and non-preventive laboratory. If you receive care from non-network providers, the plan

pays 80% of UCR charges after you pay the annual deductible. This plan has the richest non-network

coverage.

Medium Choice Plus PPO Plan

The UHC Medium Choice Plus PPO Plan is the most popular UHC option. Its’ comprehensive coverage

and moderate per pay period premium is adequate for most people. This plan is most cost effective when

care is received by network providers. However – it does provide a basic level of non-network coverage.

The plan covers network physician’s office visits at 100% after you pay the applicable co-pay. Most other

network provider services are covered at 90% after you pay the annual deductible. If you receive care

from non-network providers, the plan pays 70% of UCR charges after you pay the annual deductible.

18 | P a g e Rev 06.14.13 cnt1509275

Health Savings Account (HSA) - Eligibility Requirements

In addition to being enrolled in an IRS qualified HDHP -there are specific eligibility requirements to open

and contribute to a Health Savings Account. Be sure you validate your eligibility by reviewing the criteria

available on the HSA Medical Plan Resource Center

.

Premium and Medium Out-of-Area Plans

If you live outside of UHC’s Choice and Choice Plus service areas, you’re eligible to enroll in the Premium

or Medium Out-of-Area Plans. Because you do not have access to network physicians and facilities – the

plan pays 80% of UCR charges after you pay the annual deductible for all services (except prescription

drugs). There are no gaps in the pharmacy network – therefore prescription drug coverage is accessed in

the same manner as the other UHC plans described in this document.

HSA Medical Plan

The UHC HSA Medical plan is an IRS qualified High Deductible Health Plan (HDHP). All services (except

for eligible preventive care services, which are covered at 100% no deductible) are subject to the plan

deductible and coinsurance. If you receive care from a network provider, the plan pays 90% of UCR

charges after you pay the annual deductible. If you receive care from non-network providers, the plan

pays 70% of UCR charges after you pay the annual deductible. In this plan, all prescriptions (regardless

of Tier) are also subject to the plan deductible and coinsurance. For more information about the HSA

Medical Plan visit the HSA Medical Plan Resource Center.

Aggregate Deductible and Out-of-Pocket Maximum

Unlike the other UHC plans – the annual deductible and out-of-pocket maximum rules are different in this

plan. In the other UHC plans, an individual within a family moves to benefits (coinsurance) once he/she

satisfies the individual deductible. Likewise, an individual within a family isn’t responsible for additional

eligible expenses in the plan year once he/she satisfies the individual OOP maximum.

In the UHC HSA Medical Plan, the plan deductible and out-of-pocket maximum are aggregated. This

means the family deductible must be met before coinsurance applies even if one family member meets

the individual deductible. The same applies to the OOP maximum. The dependent OOP maximum must

be met even if one family member reaches the individual OOP maximum.

Exclusive Provider Organization (EPO) Choice Plan

The Exclusive Provider Organization (EPO) Choice Plan requires you to use EPO Choice physicians and

providers to receive benefits. Non-network benefits are NOT covered except in an emergency,

acupuncture, or ABA Therapy for autism. Most services are covered at 100% after you pay the applicable

co-pay. For the majority of services this plan does not require you to meet a deductible – however a

deductible is applied to a few services including in-patient facility and non-preventive laboratory.

HPHC Passport Plan

UnitedHealthcare’s Harvard Pilgrim Passport Plan (HPHC) network is available to most employees who live in Massachusetts, Maine, New Hampshire and the cities in Vermont and New York that border Massachusetts or New Hampshire. If you enroll in the HPHC Passport Plan you must use the HPHC network. When you are traveling outside of the designated network area you have the flexibility to access the broader UHC Choice network. Non-network benefits are NOT covered except in an emergency. Most services are covered at 100% after you pay the applicable co-pay.

19 | P a g e Rev 06.14.13 cnt1509275

HMO Drug Lists

HMO plans have their own list of prescription

drugs. If you are enrolled in Kaiser or

HealthNet contact your HMO directly to obtain

the list of drugs covered under the plan.

If you have eligible dependents living outside of the HPHC service area, they are eligible for coverage

provided they utilize the UHC Choice network. Any care obtained outside the HPHC network or UHC

Choice network, except in an emergency, are NOT covered.

United Healthcare (UHC) Health Statements

Each month that UHC processes at least one claim for you or a covered dependent, you will receive a

Health Statement in the mail. Health Statements make it easy for you to manage your family’s medical

costs by providing claims information in an easy-to-understand format and terms. If you prefer not to

receive printed statements go to www.myuhc.com and opt out. You can choose to receive email alerts

when a new statement is generated and monitor and track activity online.

Managing Your Prescription Costs

Prescription drugs are the fastest-growing segment of health care expenses. Drug costs are increasing at

double-digit rates and are outpacing costs for hospital and physician services. Two of the most effective

ways for you to help manage these costs are:

Use lower cost medications when available and appropriate for your condition. Medicines prescribed in the UHC plans fall into one of three drug tiers. You will pay more or less depending on which tier your medication falls in.

Save time and money. Consider purchasing maintenance drugs (those you take on a regular basis for conditions such as asthma or diabetes) using the mail order feature of your prescription benefit. The UHC plans and HMOs all offer mail order programs.

UHC’s Preferred Prescription Drug List (PDL)

A Preferred Drug List (PDL) is a formal list that classifies prescribed medications into different tiers. The

list includes generic, brand name, and compound prescription medications approved by the FDA. When

you choose a medication you and your physician should consult the PDL to help you obtain the most out

value from your benefit. You may obtain the most current tier information on the Oracle US Benefits

Website, www.myuhc.com or calling the UHC member phone number noted on the back of your ID card.

Tier changes generally occur each January and July. You will need to check periodically to be sure you

have the most up-to-date list and print it out and bring it with you when you visit the physician.

UHC’s Prescription Drug Tiers Three Tiers: The UHC medical plan prescription drugs

are categorized into three individual tiers. Each tier has

an associated cost (co-pay or coinsurance). This is the

amount you will pay when you fill a prescription. There

are three tiers – tier 1 is the lowest cost option, tier 2 is

mid-range, and tier 3 is the highest cost option. If you are

currently taking a medication that falls in tier 2 or 3 – you

may want to ask your physician if there is an appropriate medication classified in a lower cost tier.

Compound medications are those with one or more ingredients that are prepared at the pharmacy

location. These types of medications are almost always classified as tier 3 and a lower tier option is not

available. Generally you will find that most generic medications are classified in tier 1 however that may

not always be the case.

Classification Decisions

The UHC PDL Management Committee is responsible for making tier placement decisions. This

committee is made up of senior level UHC physicians and business leaders. The goal of this committee is

20 | P a g e Rev 06.14.13 cnt1509275

to help ensure access to a wide range of medications and at the same time help control costs. Decisions

are made based as new drugs are released and clinical guidelines are updated. Tier changes generally

occur two times per calendar year (January 1 and July 1) and if your current medication(s) move to a

different tier it will result in you paying a lower or higher amount for your medication.

Mail Order Program (Maintenance Medications)

The mail order program is ideal for people who use maintenance medications – such as medicines for

cholesterol and high blood pressure. Using the mail order program saves you money and is also

convenient. You receive a higher quantity of medications at a lower cost and prescriptions are mailed

directly to your home which saves you a trip to the retail pharmacy. When you begin the mail order

program it’s recommended that you obtain two prescriptions from your physician. If you are required to

being your medication immediately – you can obtain your first fill at your local retail pharmacy. The other

prescription can be used to start the mail order program.

Specialty Medications

Specialty medications are critical to improving the health and lives of individuals with complex, serious, or

rare conditions. They are the most expensive medications being used today - usually costing more than

$250 per prescription. These types of prescriptions are typically not available at retail pharmacies and

require additional clinical support for better health outcomes. The majority of medications are not

classified in this special category.

For the small percentage of employees and family members who do require specialty medications, the

program is designed to make them accessible, affordable, and provide you with additional customer

service and clinical support. Therefore, UHC medical plan members are required to use a participating

specialty pharmacy to receive network coverage for all specialty medications. Specialty medications are

dispensed in a 30-day supply only. This is due to the expense and complexity of these medications and

allows physicians to assess the drug’s effectiveness to prevent waste of these very costly medications.

To locate a participating specialty pharmacy visit www.uhcspecialtyrx.com or call the Specialty Pharmacy

Referral Line at 866-429-8177. Representatives are available 24/7 and will answer any questions you

may have about the program and transfer you directly to a participating network specialty pharmacy

based on your medication(s). If you choose to fill your prescription at a non-network pharmacy, you will

be required to pay a higher amount.

Health Maintenance Organizations (HMOs)

ORACLEflex offers you a choice of HealthNet and Kaiser Permanente (Kaiser) HMOs. The HMOs are

available in certain geographic areas only. For more information about service areas – refer to “Eligibility –

Geographic Service Area” section of this document. Additionally, when login to the ORACLEflex

Enrollment System , only the medical plans you are eligible for will be displayed.

The Oracle sponsored HMOs are fully insured – which means Oracle pays HealthNet and Kaiser a

monthly premium for administration and to pay for all claims.

LEARN MORE For more detailed information about Specialty Medications visit

www.uhcspecialtyrx.com or call 1-866-429-8177

21 | P a g e Rev 06.14.13 cnt1509275

HMOs are managed care plans that require you to use network physicians and facilities. Non-network

benefits are NOT covered except in an emergency. Overall, HMO’s require you to pay a higher per pay

period premium – however services are 100% after the applicable co-pay. As a result, your out-of-pocket

costs for eligible services are predictable and relatively low. Each plan offers similar benefits – but

services and coverage levels vary by plan. To review and compare plan features including eligible

services and co-pays, you are encouraged to review the Medical Comparison Chart.

When you enroll in a HMO prescription drug coverage is included. Your medical ID card also serves as

your prescription drug ID card. There are two categories of prescription drugs – generic, and brand name.

You receive your prescription drugs through the HMO’s pharmacy network and non-network prescriptions

are NOT covered. Each drug category is covered at 100% after you pay the applicable co-pay. For cost

savings and convenience, the HMOs offer a mail-order program for maintenance prescriptions. Review

the Medical Comparison Chart to view prescription drug coverage.

Each of the HMO plans includes a safety net against catastrophic injury or illness. The plans’ calendar

year out-of-pocket maximum varies between plans - however each limit the amount you will be required to

pay each year. Should you reach your annual out-of-pocket maximum the plans will pay 100% of eligible

expenses for the rest of the year.

HealthNet HMO

(Available in California) HealthNet is available to most Oracle employees living in California. If you enroll in HealthNet, you must

choose a Primary Care Physician (PCP) for yourself and enrolled dependents. Your PCP belongs to a

HealthNet affiliated medical group and he/she is responsible for coordinating all of your medical care -

including referring you to specialists, hospitals, and other services within the medical group.

When you enroll for the first time you will be required to designate your selected PCP by entering his/her

10-digit identification number in the ORACLEflex Enrollment System You should visit the HealthNet

website to select a PCP and write down his/her ID number prior to enrolling in ORACLEflex benefits. You

are able to select the same or different PCP for each enrolled family member. Any PCP changes that

occur after your initial enrollment should be handled directly with HealthNet.

The HealthNet HMO requires you to use network physicians and providers to receive benefits. Services

are covered at 100% after you pay the applicable co-pay and there are no deductibles or claim forms to

file. Non-network benefits are NOT covered except in an emergency.

Kaiser Permanente HMO

(Available in California, Colorado, Georgia, Washington DC, Oregon, and Washington) Kaiser Permanente (Kaiser) is available to Oracle employees in certain states across the country. If you

enroll in Kaiser, you receive your care by Kaiser physicians and facilities. Services are covered at 100%

after you pay the applicable co-pay and there are no deductibles or claim forms to file. You must use

Kaiser physicians and facilities to receive benefits. Non-network benefits are NOT covered except in an

emergency.

LEARN MORE To review and compare medical plan features visit the Medical Comparison Chart.

22 | P a g e Rev 06.14.13 cnt1509275

Employee Assistance Program

Help is Always Available 866-728-8413

www.livenadworkwell.com (enter access code 228485)

Group Health Cooperative (GHC) Washington

An affiliate of Kaiser Permanente

GHC is available to most employees living in Washington. If you enroll in the GHC plan, you receive care

through GHC physicians and facilities. The GHC Plan covers services at 100% after you pay the

applicable co-pay and there are no deductibles or claim forms to file. You must use GHC physicians and

facilities to receive benefits. Non-network benefits are NOT covered except in an emergency.

Medical Plan Selection Considerations

It’s up to you to think about what’s important to you, cost, provider choice and convenience, then decide

and select the medical option that is best for you. Consider the following:

Are your current physicians and facilities in the plan network? You’ll receive higher benefits for

visiting a network physician or facility. And, in some plans benefits are not covered when you use

non-network providers.

How often do you usually require medical care during the year? Some plans make sense if you

have a known condition that requires recurring medical care or have a longstanding relationship

with a non-network provider. Others may be more cost-efficient with lower monthly costs if you

only need routine care during the year.

What are the out-of-pocket costs associated with each plan? Depending on the plan, you may be

required to pay a co-pay for most services while other plans require an annual deductible before

the plan starts paying benefits. And – check out the out-of-pocket maximum which is your

financial safety net in the event of unexpected catastrophic injury or illness.

If you’re choosing between the UHC medical plans, be reminded that the preferred provider network of physicians, facilities, and pharmacies are the same for all plans.

Mental Health Benefits

Your medical plans cover more than just physical care — they also provide assistance when you need counseling to help with emotional and personal wellness.

Employee Assistance Program

The Employee Assistance Program (EAP) provides confidential, personal assessment and referral

services for you and your family members. Enrollment in the EAP is automatic and free of charge to you

and your eligible dependents - even if you are not covered by an Oracle medical plan. United Behavioral

Health (UBH) administers the EAP. You may call UBH 24 hours a day, seven days a week by calling 866-

728-8413. The EAP is available to help with a variety of concerns including:

Stress

Depression

Job Worries

Legal & Financial Concerns

Family & Marital Problems

Alcohol & Chemical Dependency

When you call UBH, a specialist will ask you a few questions to help identify the nature of your issue and

the appropriate resources to address it. The specialist will work with you to find the appropriate clinician

and to satisfy your gender, language, and cultural preferences. The EAP provides 100% coverage for up

23 | P a g e Rev 06.14.13 cnt1509275

Mental Health / Substance Abuse

UHC medical plan members must call 1.866.728.8413

for referral assistance and to preauthorize treatments

to six (6) in person visits per concern per year with an EAP counselor for each family member. Mental

health outpatient care beyond six (6) visits is managed through Mental Health and Substance Abuse

benefits described in this document.

Mental Health and Substance Abuse Benefits

Care beyond the six free EAP visits

If you enroll in a UHC medical plan, your mental health and

substance abuse coverage will be provided through UHC

and its subsidiary United Behavioral Health (UBH). If you

enroll in an HMO, mental health outpatient care is managed

through the HMO – contact your HMO for more information.

UHC medical plan participants are required to pre-authorize

any mental health and substance abuse outpatient and

inpatient treatment. The UBH network includes a wide range of professionals — psychiatrists,

psychologists, masters-level social workers, and marriage and family counselors — as well as hospitals

and alcohol and substance abuse treatment centers. This applies to both network and non-network

facilities. Please call UBH to pre-authorize services.

When you access care through the UBH mental health network you receive a higher level of benefits than

if you obtain care outside the network. Your benefits vary depending on which plan you’re in and whether

you obtain authorization from UBH. Review the Medical Comparison Chart to view mental

health/substance abuse coverage.

Live and Work Well

Live and Work Well is an interactive website that provides access to benefits and tools to help enhance

your work, health, and life. You may access this online resource center at www.liveandworkwell.com (use

Oracle’s access code 228485). Key features of the website allow you to:

Submit online service requests

Check your benefits information

Search for network clinicians

Participate in interactive and customizable self-improvement programs

Access information and resources related to hundreds of everyday work and life topics such as o Balancing work and personal life o Locating child care and elder care resources o Parenting o Adoption o Selecting schools

Dental Plans

ORACLEflex offers you a choice of two dental plans administered by MetLife:

Preventive Plan: This plan covers preventive care ONLY. This includes services such as routine

exams/x-rays and cleanings. Services such as fillings, oral surgery, implants, dentures, orthodontia,

and periodontal care are NOT covered.

Comprehensive Plan: This plan covers the full spectrum of dental care needs including preventive, basic, major, and orthodontia care for adults and children.

24 | P a g e Rev 06.14.13 cnt1509275

LEARN MORE Check out what you could save on network and non-network fees.

Visit www.metlife.com/mybenefits and try the Dental Procedure Fee Tool, search for network dentists, view your claims online, and more!

For more detailed information on coverage levels and services provided by each of the dental plans, refer

to the Dental Plan Comparison Chart.

Network and Non-Network Dentists

Both plans allow you to use any licensed dentist. You can choose a dentist from MetLife’s preferred

provider network or any dentist outside of the network. When you obtain services from a network or non-

network dentist, the plan applies the same deductible and coinsurance. However, when you visit a

network dentist your out-of-pocket costs are usually lower. That’s because network providers have

agreed to accept negotiated/discounted fees for dental services. The negotiated fees are usually 15% to

45% less than the average dental fees in the same community. This can help you lower your out-of-

pocket costs and stretch your annual dental benefit maximum..

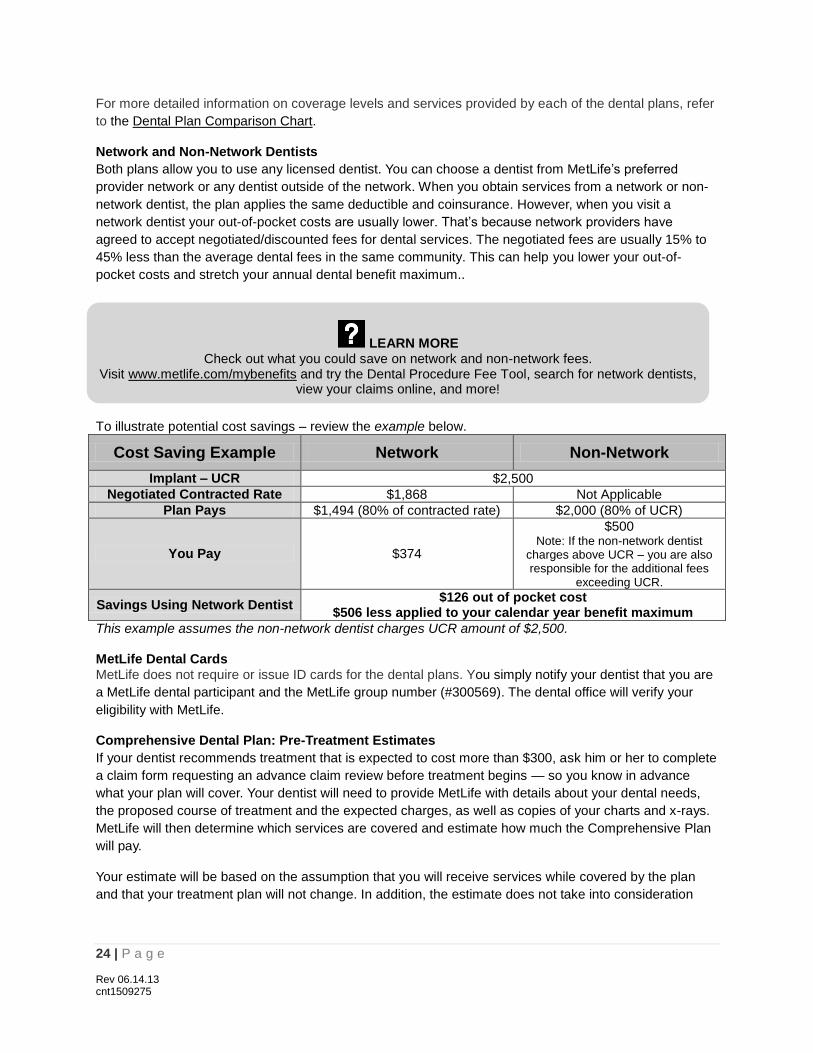

To illustrate potential cost savings – review the example below.

Cost Saving Example Network Non-Network

Implant – UCR $2,500

Negotiated Contracted Rate $1,868 Not Applicable

Plan Pays $1,494 (80% of contracted rate) $2,000 (80% of UCR)

You Pay $374

$500 Note: If the non-network dentist

charges above UCR – you are also responsible for the additional fees

exceeding UCR.

Savings Using Network Dentist $126 out of pocket cost

$506 less applied to your calendar year benefit maximum

This example assumes the non-network dentist charges UCR amount of $2,500. MetLife Dental Cards

MetLife does not require or issue ID cards for the dental plans. You simply notify your dentist that you are

a MetLife dental participant and the MetLife group number (#300569). The dental office will verify your

eligibility with MetLife.

Comprehensive Dental Plan: Pre-Treatment Estimates

If your dentist recommends treatment that is expected to cost more than $300, ask him or her to complete

a claim form requesting an advance claim review before treatment begins — so you know in advance

what your plan will cover. Your dentist will need to provide MetLife with details about your dental needs,

the proposed course of treatment and the expected charges, as well as copies of your charts and x-rays.

MetLife will then determine which services are covered and estimate how much the Comprehensive Plan

will pay.

Your estimate will be based on the assumption that you will receive services while covered by the plan

and that your treatment plan will not change. In addition, the estimate does not take into consideration

25 | P a g e Rev 06.14.13 cnt1509275

deductibles or calendar year maximums as there is no way to determine, when the actual claim comes in,

how much of the deductible and calendar year maximum will be met.

Dental Plan Selection Considerations

It’s up to you to think about what’s important to you, cost, provider choice and convenience, then decide

and select the dental option that is best for you. Consider the following:

How often do you usually require dental care during the year? Is your dental care usually limited

to preventive exams, x-ray, and cleanings? Or – do you tend to require additional services such

as fillings?

Do you or your children require orthodontia services?

Are you comfortable paying the Preventive Plan’s lower premium and assume full financial risk

should you need non-preventive services.

Most dental services are eligible Health Care Reimbursement Account and Health Savings

Account (HSA) expenses.

Vision Plans

ORACLEflex offers you a choice of two vision plans, both administered by Vision Service Plan (VSP).

Vision Plan I

Annual Eye Exam

One benefit allowance for lenses or contacts every calendar year

One frame allowance every calendar year. Vision Plan II

Annual Eye Exam

Two benefit allowances for lenses or contacts every calendar year

Two frame allowances every calendar year.

Higher contact lens dollar allowance than Vision I Plan For detailed information on coverage levels and services provided by each of the vision plans, refer to the

Vision Plan Comparison Chart. You may also visit www.vsp.com to search for network physicians, review

plan benefits and allowances, read eye care articles, and more!

Network and Non-Network Eye Care Professionals

You can choose a physician from VSP’s provider network or any provider outside of the network. Benefits

for services performed by VSP network providers are covered at a higher rate and generally, you incur

less out-of-pocket cost for services performed by network providers. The plan pays up to specified dollar

amounts for non-network services. Access the Vision Plan Comparison Chart to view the non-network

allowances.

Calendar Year Benefits Eligibility

Your eligibility for vision benefits is based on the calendar year (January through December) and the

number of benefit allowances provided under the plan in which you are enrolled.

26 | P a g e Rev 06.14.13 cnt1509275

Examples:

Vision Plan 1: You elect Vision Plan I effective January 1, 2013. This plan provides one frame

allowance each year and you obtain frames in June 2013. You will be eligible for another set of

frames in January 2014.

Vision Plan II: You elect Vision Plan II effective January 1, 2013. This plan provides two frame

allowances each year and you obtain frames in June 2013 and another set of frames in

December 2013. You will be eligible for another set of frames in January 2014.

How to Use VSP

VSP makes it very easy to access care. Simply select a VSP physician and contact the physician to

schedule an appointment. VSP physicians will verify your eligibility, your benefit allowances, and process

any necessary forms. Approval from VSP must be obtained prior to services or the coverage will be

considered out of network. If you receive services from a non-VSP physician, you must first pay the bill in

full and then send your itemized receipt to VSP for reimbursement (paid up to limited allowance only).

VSP Vision Cards

VSP does not require or issue ID cards for the vision plans. You simply notify your physician that you are

a VSP participant and the VSP group number (#12-134446). The provider’s office will verify your eligibility

with VSP.

Vision Plan Selection Considerations

It’s up to you to think about what’s important to you, cost, provider choice and convenience, then decide

and select the vision option that is best for you. Consider the following:

How often do you need to replace your glasses or contact lenses? Do you or your dependents wear glasses or contact lenses? Will you need new ones in 2013?

Have you noticed any changes in your vision?

Do you expect you or any of your dependents will need glasses for the first time?

Even if you do not require corrective lenses – an annual eye examination is a good preventive measure. Medical conditions, such as certain cancers and diabetes, can be identified through a non-invasive eye exam. Medical plans generally cover vision screenings – which is not as comprehensive as a professional exam.

Disability Insurance

Short Term Disability (STD) Insurance

Eligible employees are automatically enrolled in short-term disability insurance at no cost. Employees

who work in California are automatically enrolled in Oracle’s Voluntary Plan - voluntary disability

insurance (VDI), which is a self insured plan as part of a legal alternative in lieu of applying for state

disability insurance. Employees will contribute into the Voluntary Plan through payroll deductions.

Employees may receive VDI benefits up to 365 days of an approved disability. For employees who work

outside of California will receive salary continuation up to 90 days of an approved disability, integrated

with statutory benefits where applicable. Employees that remain disabled greater than 90 days are

eligible to apply for Long Term Disability benefits.

27 | P a g e Rev 06.14.13 cnt1509275

Pre-Tax or After-Tax Premiums

Paying for your LTD premiums on a pre-

tax basis will result in taxable LTD

benefits. Your LTD benefits will NOT be

taxed if you pay your premium after-tax.

Long Term Disability (LTD) Insurance

Long-Term Disability (LTD) insurance provides income protection if you become totally disabled and

cannot work. You may be eligible for monthly LTD benefits after three months of continuous disability. LTD

picks up where STD ends such that you do not have a gap in your income stream. LTD is a core benefit

— you are required to purchase a minimum amount of LTD insurance coverage for yourself. For more

information - refer to the “Core Coverage” section of this document.

Generally, you are considered totally disabled if, as a result of injury or illness, you cannot perform the

material duties of your occupation in the first 24 months. After the first 24 months, you are considered

totally disabled if you cannot perform the duties of any occupation for which you are reasonably qualified

by education, training or experience, due to the same injury or illness. Your dependent spouse/domestic

partner or child(ren) are not eligible for LTD coverage.

ORACLEflex offers you two levels of LTD coverage: