MOZAMBIQUE- LOCAL TAXATION UNDER FISCAL

STRESS- WHAT OPTIONS, WHAT IMPLICATIONS?

BERNHARD WEIMER

5TH INTERNATIONAL WORKSHOP ON DOMESTIC REVENUE MOBILISATION FOR

IMPLEMENTING THE 2030 AGENDA:

THE ROLE OF SUBNATIONAL TAXATION

GDI / DIE, BONN, 13-14 SEPTEMBER, 2016

POLITICAL ECONOMYStructure

• Extractive, export oriented economy

• High poverty rates

• predominant foundational party since Independence (1975)

• Neopatrimonial-clientilist system with rent seeking national and local elites

• monopolistic, inefficient SOEs

• Limited Access Order (LAO), - > periodic conflicts, conflictual political settlement

Current Crisis

• Low intensity war, partial agreement (2014) failing, ongoing peace negotiations, incl on autonomous provinces

• Unfavourable global economic environment and markets

• Unsustainable public debt caused by surge of illicit Non concessional credits ( 2,3 bln USD) Risk of defaulting

• Budget support (500 million USD ; 2016) and IMF standby credit (286 million USD) frozen

• Budget deficit increase (approx. 500 Million USD, 2016))

• Decline of FOREX reserves , Decline of FDI

• Dramatic devaluation of currency (50% of value since 2014) , rising inflation

• Decline of growth rate , from 8% (2013) to 4% (2016)

• Closure of businesses, increasing unemployment

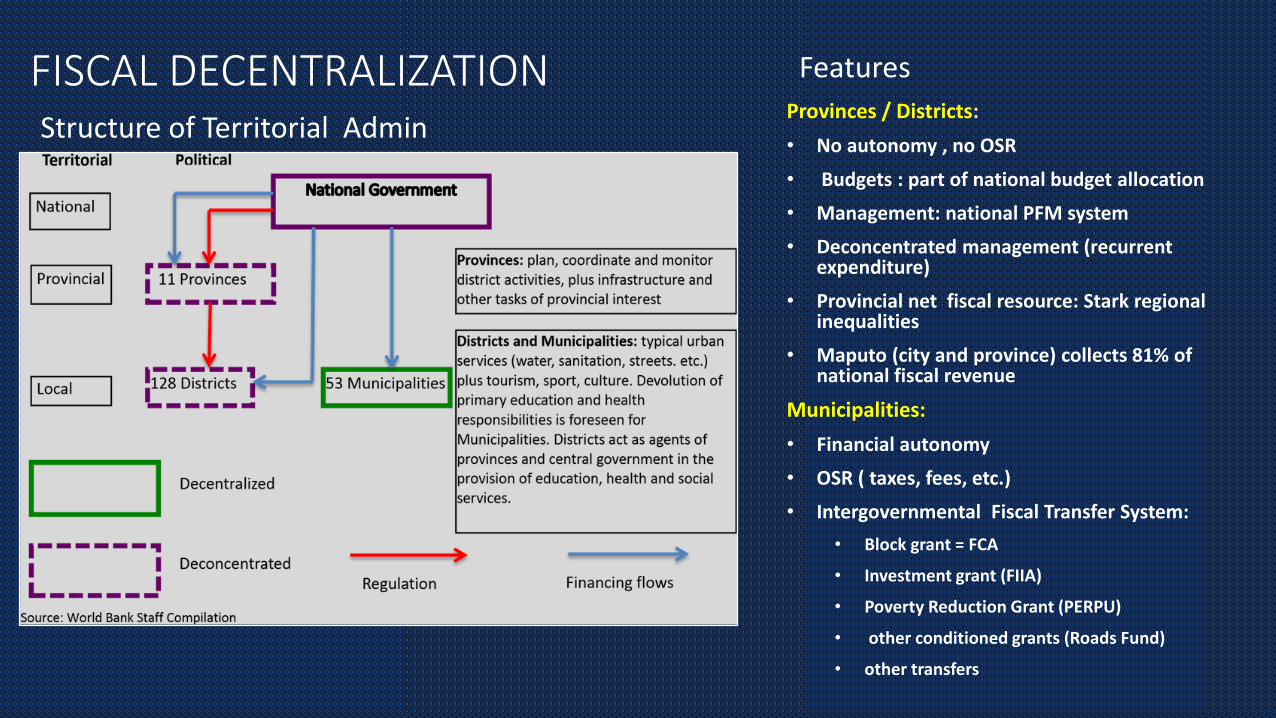

FISCAL DECENTRALIZATION Structure of Territorial Admin

Features

Provinces / Districts:

• No autonomy , no OSR

• Budgets : part of national budget allocation

• Management: national PFM system

• Deconcentrated management (recurrent expenditure)

• Provincial net fiscal resource: Stark regional inequalities

• Maputo (city and province) collects 81% of national fiscal revenue

Municipalities:

• Financial autonomy

• OSR ( taxes, fees, etc.)

• Intergovernmental Fiscal Transfer System:

• Block grant = FCA

• Investment grant (FIIA)

• Poverty Reduction Grant (PERPU)

• other conditioned grants (Roads Fund)

• other transfers

TOTAL EXPENDITURE BY LEVEL OF PUBLIC ADMINISTRATION, 2008 AND 2014 (IN %)

63

.3

31

.4

4.2

1.1

63

.4

21

14

.7

1.6

CENTRAL PROVINCIAL DISTRICT MUNICIPAL

% O

F TO

TAL

EXP

END

ITU

RE

LEVEL OF PUBLIC ADMINISTRATION

2008 2014

Source: author , based on Govt Data

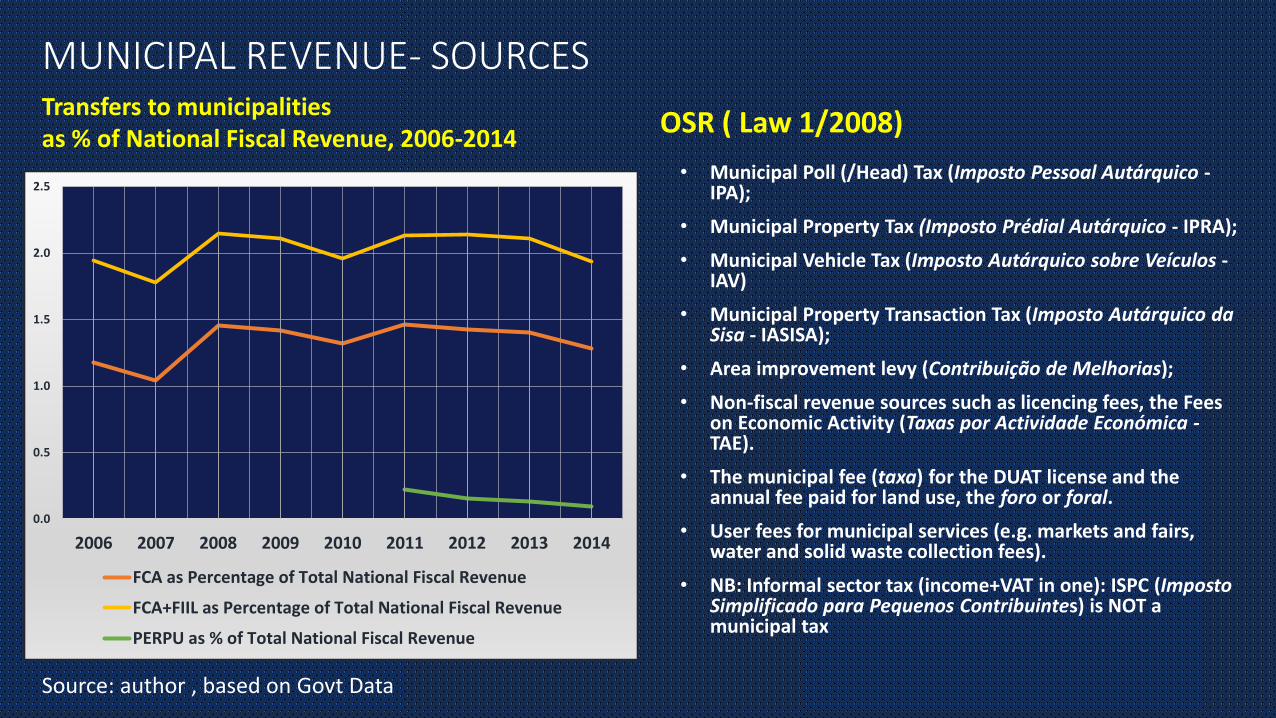

MUNICIPAL REVENUE- SOURCESTransfers to municipalities as % of National Fiscal Revenue, 2006-2014

OSR ( Law 1/2008)

• Municipal Poll (/Head) Tax (Imposto Pessoal Autárquico -IPA);

• Municipal Property Tax (Imposto Prédial Autárquico - IPRA);

• Municipal Vehicle Tax (Imposto Autárquico sobre Veículos -IAV)

• Municipal Property Transaction Tax (Imposto Autárquico da Sisa - IASISA);

• Area improvement levy (Contribuição de Melhorias);

• Non-fiscal revenue sources such as licencing fees, the Fees on Economic Activity (Taxas por Actividade Económica -TAE).

• The municipal fee (taxa) for the DUAT license and the annual fee paid for land use, the foro or foral.

• User fees for municipal services (e.g. markets and fairs, water and solid waste collection fees).

• NB: Informal sector tax (income+VAT in one): ISPC (Imposto Simplificado para Pequenos Contribuintes) is NOT a municipal tax

0.0

0.5

1.0

1.5

2.0

2.5

2006 2007 2008 2009 2010 2011 2012 2013 2014

FCA as Percentage of Total National Fiscal Revenue

FCA+FIIL as Percentage of Total National Fiscal Revenue

PERPU as % of Total National Fiscal Revenue

Source: author , based on Govt Data

DIAGNOSTIC ASSESSMENTMUNICIPAL REVENUE- AVERAGE OSR POTENTIAL, 2009 (SAMPLE 6 MUNICIPALITIES)

8%1% 5%

47%

22%

36%49%

92%99% 95%

53.0%

77.9%

64.2%51.3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Potencial

Esforço (ET)

Sources: Boex et al 2011; Weimer, 2012

Assessment criteria:

• Coverage ratio• Application ratio• Compliance ratio

Source: Boex et al. 2011; Kelly, 200o

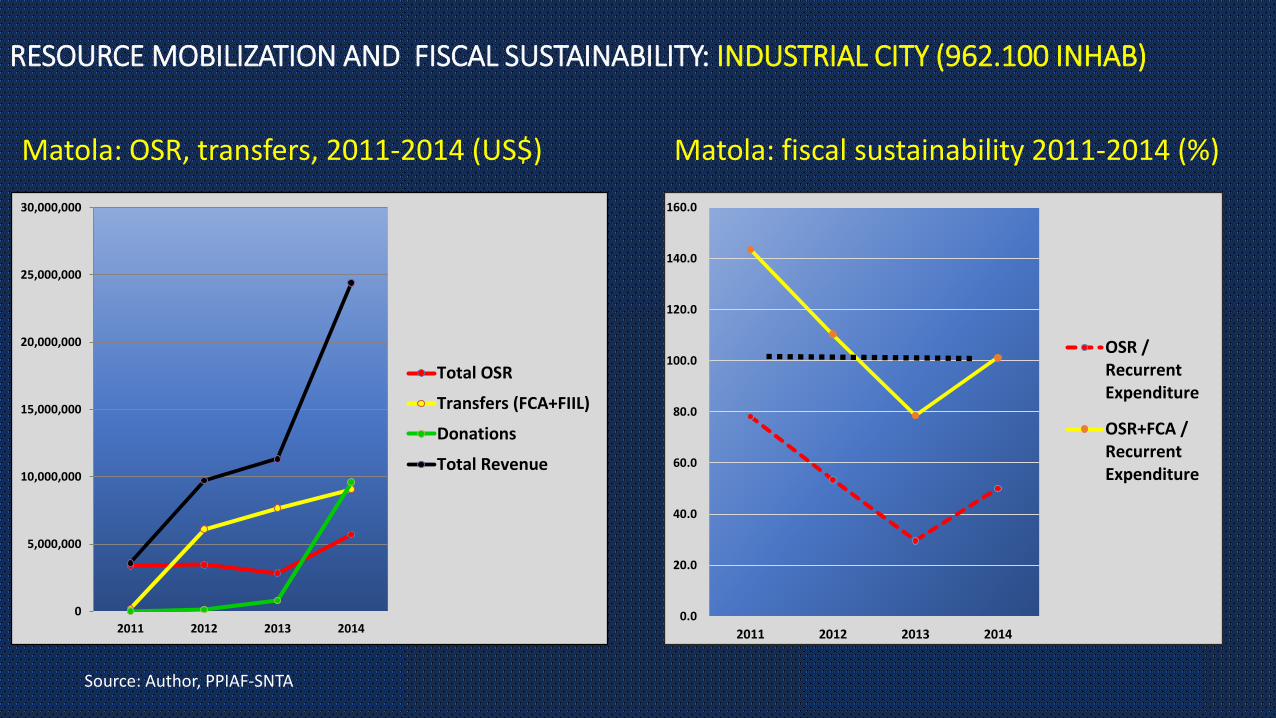

RESOURCE MOBILIZATION AND FISCAL SUSTAINABILITY: INDUSTRIAL CITY (962.100 INHAB)

Matola: OSR, transfers, 2011-2014 (US$) Matola: fiscal sustainability 2011-2014 (%)

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

2011 2012 2013 2014

Total OSR

Transfers (FCA+FIIL)

Donations

Total Revenue

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

2011 2012 2013 2014

OSR /RecurrentExpenditure

OSR+FCA /RecurrentExpenditure

Source: Author, PPIAF-SNTA

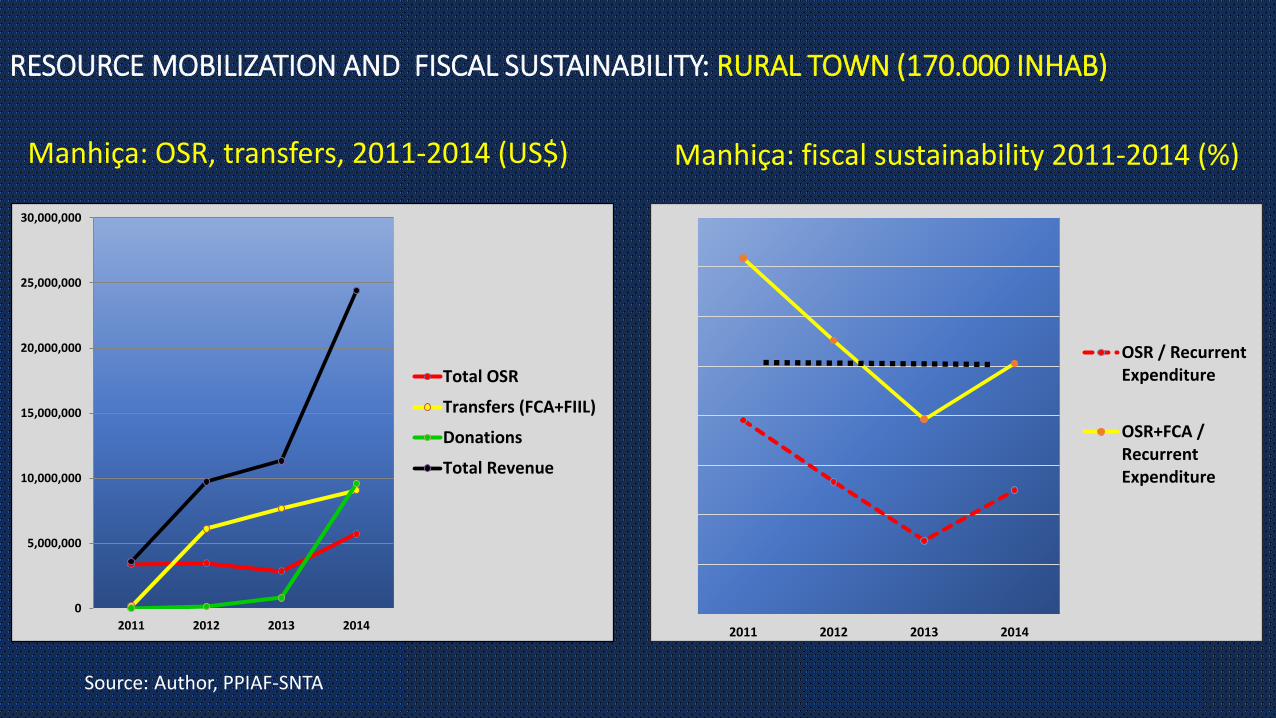

RESOURCE MOBILIZATION AND FISCAL SUSTAINABILITY: RURAL TOWN (170.000 INHAB)

Manhiça: OSR, transfers, 2011-2014 (US$) Manhiça: fiscal sustainability 2011-2014 (%)

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

2011 2012 2013 2014

Total OSR

Transfers (FCA+FIIL)

Donations

Total Revenue

2011 2012 2013 2014

OSR / RecurrentExpenditure

OSR+FCA /RecurrentExpenditure

Source: Author, PPIAF-SNTA

DIAGNOSTIC: MAIN CONCLUSIONS

1. Average unused tax reserve (sample, 2009) equivalent to:

• 150% of average OSR collection

• 50% of overall average revenue (OSR+Transfers)

• 400% of average capital expenditure

2. Least used sources: taxes on Property and property transaction, poll tax

3. Most used sources: market fees, vehicle tax

4. Major variations between sample Municipalities (tax registers, tax compliance, leadership)

5. Limited capacity for Investment in Infrastructure and services 2009 (2014): 32% (40%) of total expenditure

6. Municipalities (large, small) hardly fiscally sustainable without major mobilization effort

7. Donor municipal budget / project support makes difference

REVENUE MOBILIZATION STRATEGIES- OPTIONS1. TA for Capacity Building (Institutional, HR) with focus on:

• Untapped sources with high potential and buoyancy

• Invest in cadastres, register and mgt tools , municipal financial management strategy

• Taxation value chains for Property related revenue (land, building, transaction)

• Strengthen internal control and audit

• Earmark incremental revenue for capital expenditure / public service delivery (incentive for tax payer)

• Fiscal education and ‘social contract’

2. Outsourcing taxation (PPP)

• New experience (Matola, Pemba)

• Private partner receives (?) % share of additional revenue collected

• Little transparency (share for private profit, procurement)

3. Intensified collaboration Municipalities - National Tax Authority

• Sharing of registers

• Joint HR training and fiscal education programmes

• Transfer ISPC to Municipalities

4. Review of allocation criteria in transfer system (WB)

• Include potential, tax effort / performance as allocation criteria

• Incentives / disincentives

• Option 1: to link allocating grants with the rate of growth of OSR

• Option 2: matching principle’, where revenues collected by a municipality are matched by the

central government through a co-financing grant

5. Review sharing of natural- resource based revenue

• 2013: 2.75 % of the royalties generated by mining and natural gas sectors to seven ‘localities ‘

• 20% of profit of large scale agricultural and forestry projects to ‘communities’

• Allocation criteria and procedures lack transparency

6. Combination of 1-5

• requires reform of intergovernmental transfer system

REVENUE MOBILIZATION STRATEGIES- OPTIONS, CONT

MAIN OBSTACLES TO REVENUE MOBILIZATION

1. Capacity Building (Option 1): has been mainstreamed in municipal support projects, with little overall success (with variations). Causes:

• Clientilist rent seeking and tax evasion practises by local elites and SOE

• Decentralized Corruption (sub-valorization of properties)

• Lack of incentives for performance (HR, leadership )

• Property tax: too complex, not commensurate with economic capacity

• Absence of internal control , external audits of municipal accounts

• Lack of citizens engagement and social control

2. Macroeconomic and fiscal crisis at national level produces

• Shrinking local economic and taxation base , transfers

• Declining purchasing power and availability of income

• Risk of double taxation (ISPC->national Tax Authority; local Business fee-> municipal tax department)

• Resistance to (local and national) taxation – > tax evasion

• Informalization of economy

3. Political crises implies

• Declining confidence in Government and ruling party

• Uncertainties, human and economic cost of war

• Potentially: Review of intergovernmental transfer system impacting on municipal revenue base and transfers

CONCLUDING QUESTIONS

Under what conditions can local revenue mobilization work in a LAO State, which

• Dos not deliver basic public goods and services with sufficient quality and coverage;

• Produces economic and fiscal crises not conducive to inclusive human , social and economic development , trust in government;

• Shows biased taxation favouring elite and big business to the detriment of ordinary citizens;

• Shows high rates of ‘Taxation by Corruption’ ( including by the national and local tax authorities), exacting a high cost and regressive effect on the poorer strata

• Lacks an institutionalized public (Habermas), in which rules of the game are discussed, established and controlled , incl in matters of fiscal policy and taxation?

THANK YOU