Presentation toMorgan Stanley Small Cap Executive Conference

June 13, 2007 – New York

Cheryl K. BeebeVice President and CFO

David A. PrichardDirector, Investor Relations

2

Forward-Looking Statement

This presentation contains or may contain forward-looking statements within the meaning of Section 27A of the Securities Exchange Act of 1933 and Section 21E of the Securities Exchange Act of 1934. The Company intends these forward looking statements to be covered by the safe harbor provisions for such statements. These statements include, among other things, any predictions regarding the Company’s future financial condition, earnings, revenues, expenses or other financial items, any statements concerning the Company’s prospects or future operation, including management’s plans or strategies and objectives therefor and any assumptions underlying the foregoing. These statements can sometimes be identified by the use of forward looking words such as “may,” “should,” “will,” “anticipate,” “believe,” “plan,” “project,” “estimate,”“expect,” “intend,” “continue,” “pro forma,” “forecast” or other similar expressions or the negative thereof. All statements other than statements of historical facts in this report or referred to or incorporated by reference into this report are “forward-looking statements.” These statements are subject to certain inherent risks and uncertainties. Although we believe our expectations reflected in these forward-looking statements are based on reasonable assumptions, stockholders are cautioned that no assurance can be given that our expectations will prove correct. Actual results and developments may differ materially from the expectations conveyed in these statements, based on various factors, including fluctuations in worldwide markets for corn and other commodities, and the associated risks of hedging against such fluctuations; fluctuations in aggregate industry supply and market demand; general political, economic, business, market and weather conditions in the various geographic regions and countries in which we manufacture and/or sell our products; fluctuations in the value of local currencies, energy costs and availability, freight and shipping costs, and changes in regulatory controls regarding quotas, tariffs, duties, taxes and income tax rates; operating difficulties; boiler reliability; our ability to effectively integrate acquired businesses; labor disputes; genetic and biotechnology issues; changing consumption preferences and trends; increased competitive and/or customer pressure in the corn-refining industry; the outbreak or continuation of hostilities including acts of terrorism; stock market fluctuation and volatility; and our ability to maintain sales levels of HFCS in Mexico. Our forward-looking statements speak only as of the date on which they are made and we do not undertake any obligation to update any forward-looking statement to reflect events or circumstances after the date of the statement. If we do update or correct one or more of these statements, investors and others should not conclude that we will make additional updates or corrections. For a further description of these risks factors, see the Company’s most recently filed Annual Report on Form 10-K for the year ended December 31, 2006 and subsequent reports on Forms 10-Q or 8-K.

3

Pure-Play Starch Refiner/Ingredients Company

• Leading global provider of refined, agriculturally based

products and ingredients

– Primary raw materials: corn/other starch-based materials

– No. 1 worldwide dextrose producer

– Regional leader in starch, high fructose corn syrup and glucose

• Major in-country capacity shares typical – ex-US

• Solid balance sheet and strong cash flow generation

4

Pure-Play Starch Refiner/Ingredients Company

SweetenersDextroseGlucoseMaltoseHigh fructose corn syrupFermentation products

StarchesIndustrial starchesProcess food starchesFermentation products

Co-productsCorn gluten feed Corn gluten mealCorn oil

corn syrups

5

End User Products

Customers in About 60 Diverse Industries/70 CountriesFood Industrial Fine Chemicals/

Sweeteners Starches Starches PharmaceuticalsCarbonated beverages Cereals Paper IV DextroseBeer Soups Corrugated boxes Tableting excipientsSports drinks Sauces Textiles Fermentation feedstocksFrozen desserts Drink mixes AdhesivesCanned fruits and vegetables Pudding Baby and face powdersDrink mixes Cakes RubberPresweetened cereals Cookies LeatherBreads Crackers DetergentsFruit juicesJams and jelliesChewing gumCream fillingSyrupsCandy

6

Sales by Product Category & Markets Served

55%

20%

25%

54%

21%

25%

52%

22%

26%

53%

23%

24%

55%

22%

23%

0%

10%

20%

30%

40%

50%

60%

2002 2003 2004 2005 2006

Sweeteners

Starches

Co-Products &Other

Other, 42%

Animal Feed, 10%Brewing Industry, 11%

Soft Drink Industry, 18%

Processed Food Industry, 19%

7

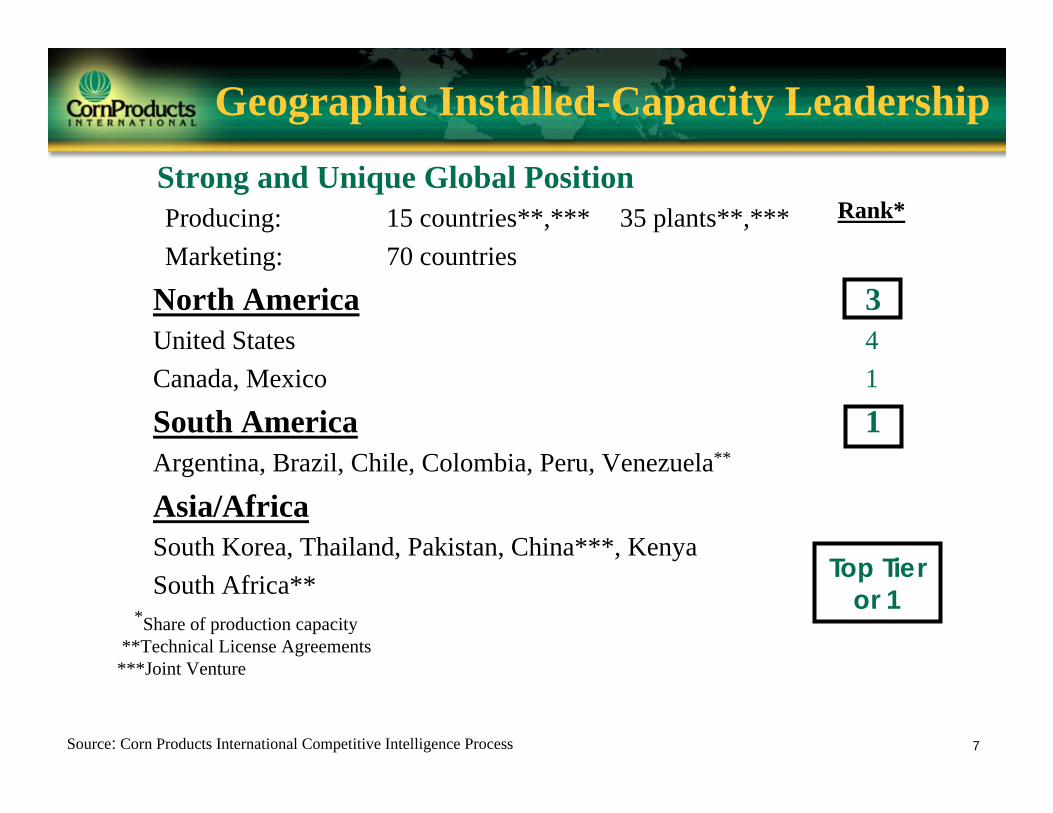

Strong and Unique Global PositionProducing: 15 countries**,*** 35 plants**,***Marketing: 70 countries

North America 3United States 4Canada, Mexico 1

South America 1Argentina, Brazil, Chile, Colombia, Peru, Venezuela**

Asia/AfricaSouth Korea, Thailand, Pakistan, China***, KenyaSouth Africa**

*Share of production capacity**Technical License Agreements***Joint Venture

Geographic Installed-Capacity Leadership

Top Tier or 1

Rank*

Source: Corn Products International Competitive Intelligence Process

8

Positive Drivers/Strategic Focus

Favorable Global Trends

• Rising populations & GDP rates• Improving standard of living• Per capita income growth• Preference for improved diet• Personal/health care awareness

Our Operating Approach

• Strategize globally—execute locally

• Leverage core competencies• Delivered cost leadership in local

markets• Anticipate/satisfy changing

customer and consumer needs• Become even closer to customer

9

• 75+ years – >70% share of capacity• Full territory coverage• Historically outperformed each nation’s underlying GDP• Successfully dealt with currencies, economies• Most advanced ingredient region in CPO• HFCS only in Argentina

Andean RegionColombia 1 corn refining plant

1 tapioca plant2 tolling facilities

Venezuela 1 plant (TLA)Peru 1 plant

Southern ConeArgentina 2 plantsChile 1 plantUruguay Distribution warehouseParaguay/Bolivia Sales agents

Brazil 3 corn refining plants1 tapioca plant1 adhesive & caramel color plant1 polyol plant Ingredient Technology Center

South America Region – Historic Strength

Brazil

Colombia

Chile

Argentina

Venezuela

Peru

Ecuador

Uruguay

10

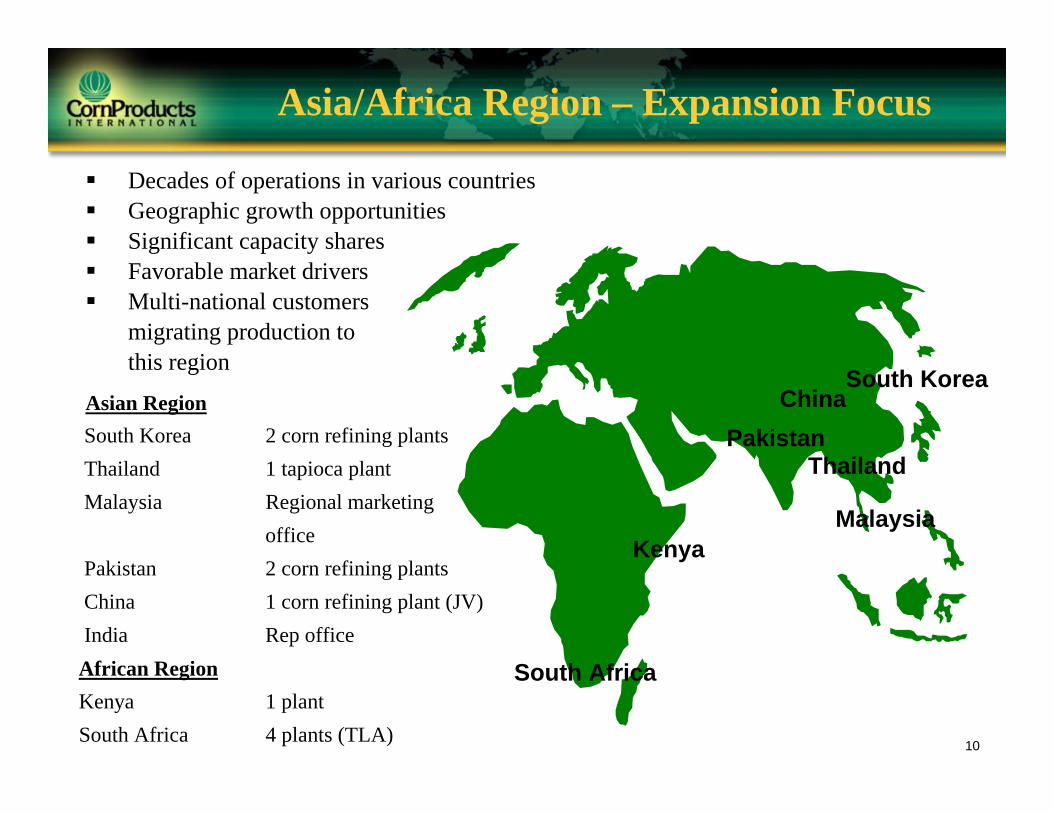

Decades of operations in various countriesGeographic growth opportunitiesSignificant capacity sharesFavorable market driversMulti-national customersmigrating production to this region

Asian RegionSouth Korea 2 corn refining plantsThailand 1 tapioca plantMalaysia Regional marketing

officePakistan 2 corn refining plantsChina 1 corn refining plant (JV)India Rep office

African RegionKenya 1 plantSouth Africa 4 plants (TLA)

Asia/Africa Region – Expansion Focus

Kenya

Pakistan

Malaysia

Thailand

South Africa

South KoreaChina

11

North America Region – Margin Growth

• 100 years old in the US

• Improving industry fundamentals– High capacity utilization rates

– Industry rationalization/plant closures

– Ethanol demand growing

– Higher US, Canadian contract pricing

• Mexico leadership– Resumption of HFCS sales and TRQs

– HFCS beverage usage tax eliminated

• Only North American corn refiner with full-scale sweetener and starch facilities in all 3 NAFTA countries – unique position

Canada 3 plantsMexico 3 plants

United States 5 plants

Canada

Mexico

United States

12

■ Strong Americas position

■ Managing geographic breadth

• Cultural understanding

• Performance in “difficult” environments

■ Reputation/assets/infrastructure

■ Managing alliance relationships

Core Capabilities – A Building Platform

13

Mission and Pathways

2003 2008

1. Excel at the Base Business

5. Be anIngredients Supplier

4. Grow Defensible Businesses in New High-Growth Regions3. Expand Value-

Added Product Portfolio Through Multi-Geographic Alliances and Acquisitions

2. Selectively Drive Organic Growth in the Base Business

To be the Premier Regional Provider of Refined, Agriculturally Based Products and Ingredients Worldwide

14

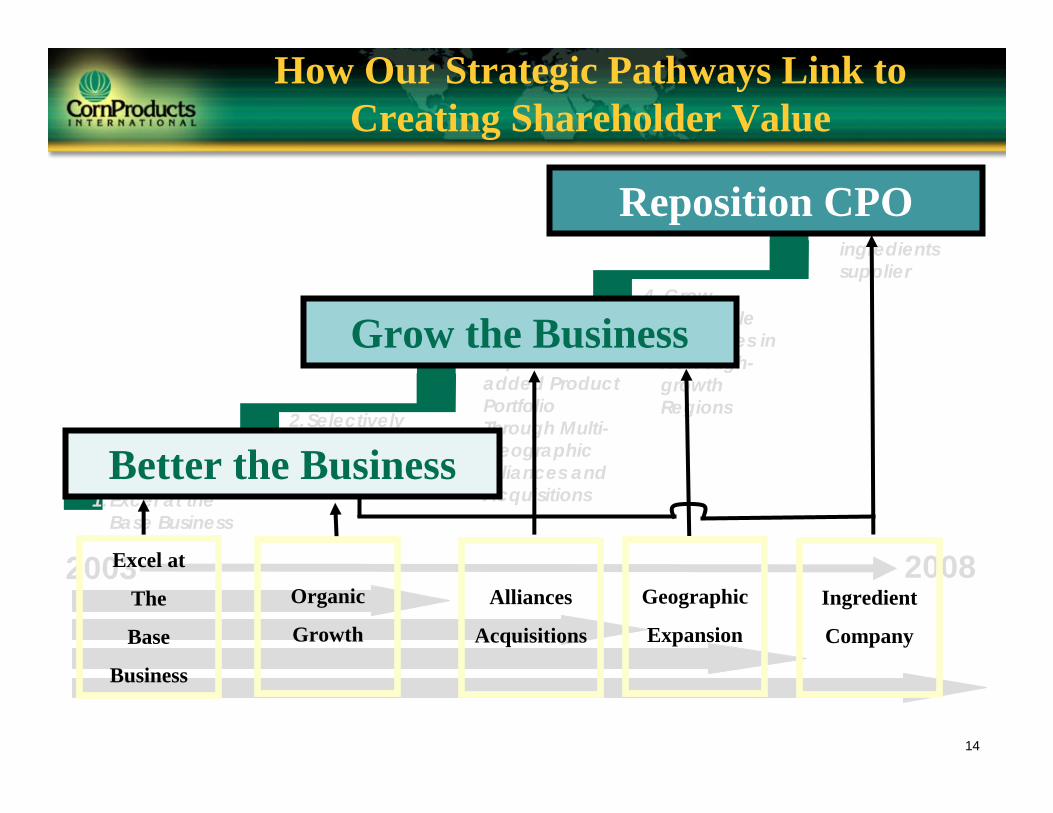

How Our Strategic Pathways Link to Creating Shareholder Value

1.Excel at the Base Business

2.Selectively Drive Organic Growth in the Base Business

2003 2008

5. Be an ingredients supplier

4. Grow Defensible Businesses in New High-growth Regions

3. Expand Value-added Product Portfolio Through Multi-Geographic Alliances and Acquisitions

Better the Business

Grow the Business

Reposition CPO

Excel at

The

Base

Business

Organic

Growth

Alliances

Acquisitions

Geographic

Expansion

Ingredient

Company

15

Pathway Strategy Examples

• Acquisition in February 2007 of SPI Polyols specialty food ingredients business in the US and remaining 50% of Getec, a Brazilian polyols JV

– Combined sales about $100 million annually– Transaction expected to be accretive in first year and meet stated ROCE target– Broadens our sweeteners platform in the Americas

• Acquisition of DEMSA, Peru’s only corn refiner, in December 2006 • New product introductions and development

– Three new modified starch channels started up in Brazil for food and industrial markets– Start-up of Canada FOS production channel – Expansion of Getec sorbitol capabilities – Near doubling of grind capacity at Balsa Nova specialties plant by year-end 2007– Expandex™ modified tapioca starch for gluten intolerance market

• Select, high-return product channel expansions in 2007 capital program– Countries include Argentina, Mexico, Colombia, Pakistan and Thailand

16

Key Financial Targets: 2003-2008

5-Year EPS Growth Target Low Double-Digit

Return on Capital Employed (ROCE) 8.5% to 10+%

Total Debt/EBITDA < 2.25x

Debt/Capitalization 32% to 35%

Operating Working Capital 8% to 10% of Net Sales

See Appendix slides for GAAP reconciliation for the non-GAAP Targets

17

Management/Shareholder Alignment

• Enhancing shareholder value– Officers average nearly 20 years of experience

• Executive compensation aligned with shareholders

• Management variable compensation

• Direct stock ownership targets for officers• Significant inside ownership

Short-term– EPS/Operating Income 80%– Operating Cash Flow 20%

Long-term– Shareholder return 50%– Return on capital employed (ROCE) 50%

Annual Incentive Plan– EPS/Operating Income 60%– Individual 20%– Working Capital/ROCE 20%

18

Financial Review

19

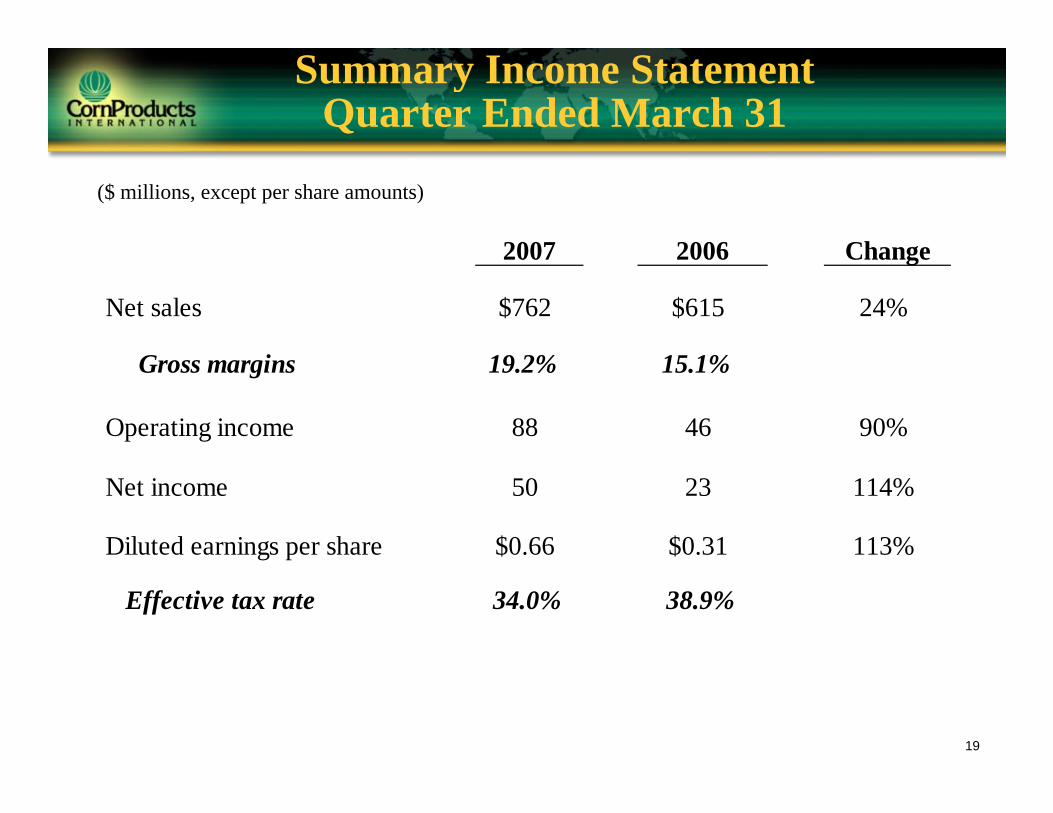

Summary Income StatementQuarter Ended March 31

2007 2006 Change

Net sales $762 $615 24%

Gross margins 19.2% 15.1%

Operating income 88 46 90%

Net income 50 23 114%

Diluted earnings per share $0.66 $0.31 113%

Effective tax rate 34.0% 38.9%

($ millions, except per share amounts)

20

2007 First Quarter

• Strongest quarter in our history follows record 2006 year– New quarterly net sales, earnings and margin records– Excellent performance virtually across the board, especially North

America region

• Factors in margin expansion– Price increases in our North American businesses– Faster pass-through of higher corn costs in our international markets– Stronger co-product values

21

2007 2006

Debt to total capital 26.3% 27.4%

Debt to EBITDA (TTM) 1.5 1.8

Operating working capital $308 $243(excluding short-term debt, cash and deferred tax)

% of 12-month sales 11.1% 10.1%

Net debt (debt less cash) $471 $448

Key MetricsQuarter Ended March 31

($ millions)

22

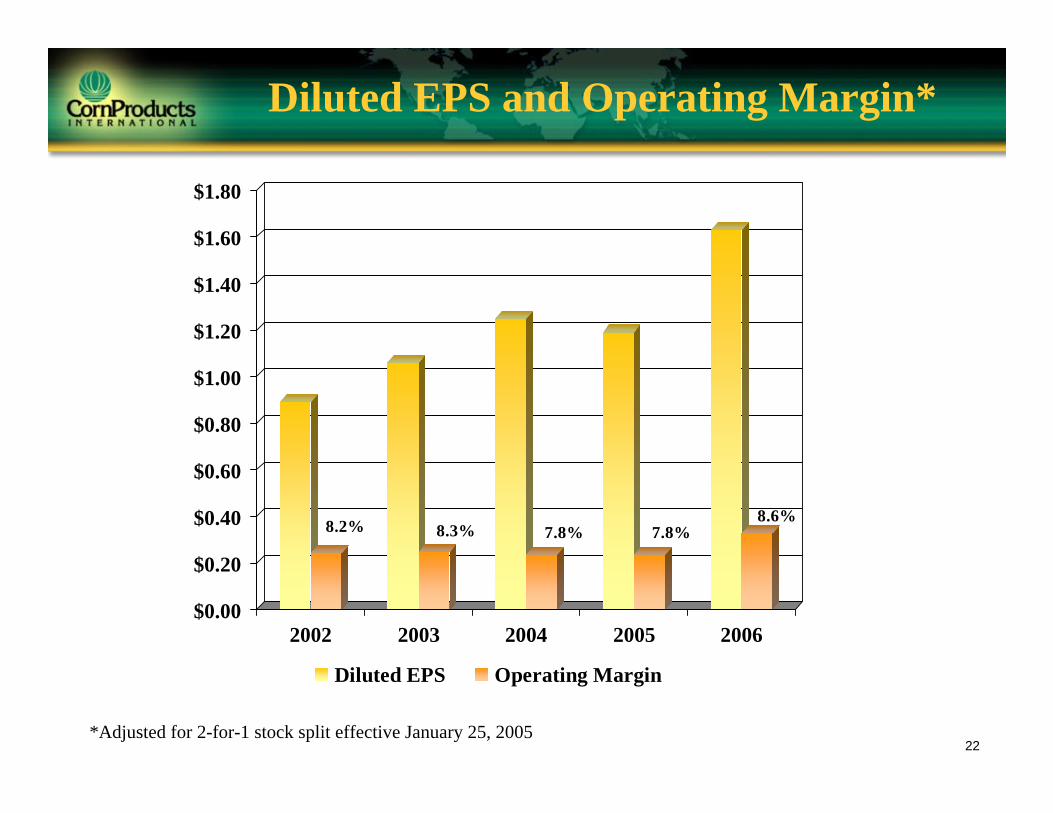

Diluted EPS and Operating Margin*

8.2% 8.3% 7.8% 7.8%8.6%

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

2002 2003 2004 2005 2006

Diluted EPS Operating Margin

*Adjusted for 2-for-1 stock split effective January 25, 2005

23

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

2001 2002 2003 2004 2005 2006

Cap-XD&A

Cap-X and D&A

($ millions)

24

Cash Flow and Total Debt

Cash Flow from Operations

$0

$50

$100

$150

$200

$250

$300

2001 2002 2003 2004 2005 2006

Cash Flow Net Income

Leverage

$0

$100

$200

$300

$400

$500

$600

$700

$800

2001 2002 2003 2004 2005 20060.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

Total Debt Debt to Total Capital

($ millions)

25

Dividend History*

*Adjusted for 2-for-1 stock split effective January 25, 2005

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

1999 2000 2001 2002 2003 2004 2005 2006

Annual Cash Dividend Paid Per Common Share Annual Diluted EPS

26

Shareholder Value Proposition

Strategic StrengthsSingle focus – starch refining

Clear long-term strategySpecific growth pathways

Mgmt/shareholder alignment

ATTRACTIVEGROWTH PROFILE

Low CostModern plants

Favorable locationsWorldwide network

Global cost optimization

Organizational DepthExperienced management

Focused workforceTechnical & market expertise

Financial FlexibilityStrong balance sheetSolid cash generation

Low maintenance cap-xInvestment grade ratings

Leading PositionsDiverse geographies

Product/customer breadthValuable alliances

High barriers to entry

27

28

Appendix

29

Management ProfilesSamuel C. Scott IIIChairman, President and Chief Executive Officer

Samuel Scott, 63, has served as chairman and chief executive officer since 2001. Previously, Scott was the president and chief operating officer of the Company. He held various positions with CPC International Inc. since 1973, including vice president of sales for Corn Products, executive vice president, and president of CPC’s worldwide corn-refining business. He also held positions with Citibank and United Technologies’ Norden Division. Scott serves on the board of Motorola, Inc., where he is lead director and chairman of the compensation committee. He also serves on the board of directors of Abbott Laboratories and The Bank of New York. In addition, he sits on the boards of ACCION International, INROADS Chicago and The Chicago Council on Foreign Relations. He is a trustee of The Conference Board. Scott received a bachelor’s degree in engineering and a master’s degree in business administration from Fairleigh Dickinson University in New Jersey.

Cheryl K. BeebeVice President and Chief Financial Officer

Cheryl Beebe, 51, was appointed vice president and chief financial officer in 2004. Prior to this position, she served as the vice president of finance and corporate treasurerof the Company. Beebe has held various positions of increasing responsibility in marketing, market services, audit, finance and treasury functions, since joining CPC International Inc. in 1980. She has a bachelor’s degree in accounting from Rutgers University in New Jersey, and a master’s degree of business administrationin corporate finance from Fairleigh Dickinson University in New Jersey.

30

Corn Wet Milling Process

31

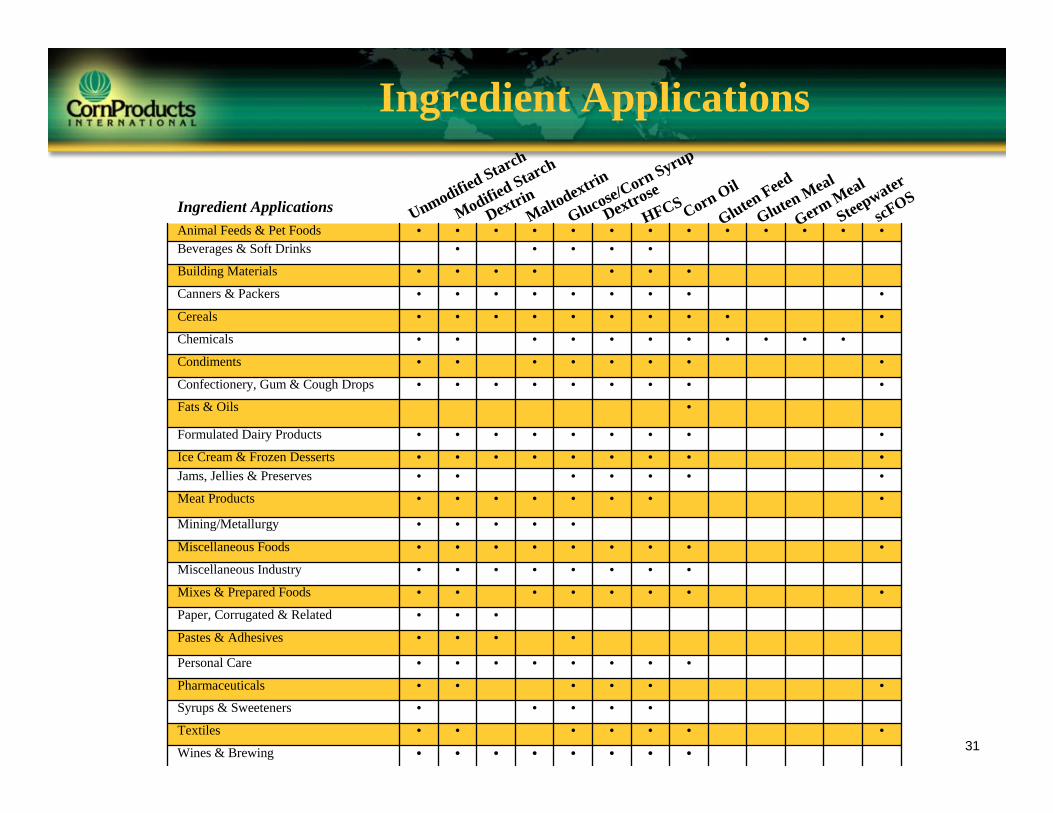

Ingredient Applications

••••••••Wines & Brewing

•••••••Textiles

•••••Syrups & Sweeteners••••••Pharmaceuticals

••••••••Personal Care

••••Pastes & Adhesives

•••Paper, Corrugated & Related

••••••••Mixes & Prepared Foods

••••••••Miscellaneous Industry

•••••••••Miscellaneous Foods

•••••Mining/Metallurgy

••••••••Meat Products•••••••Jams, Jellies & Preserves•••••••••Ice Cream & Frozen Desserts

•••••••••Formulated Dairy Products

•Fats & Oils•••••••••Confectionery, Gum & Cough Drops

••••••••Condiments

•••••••••••Chemicals

••••••••••Cereals

•••••••••Canners & Packers

•••••••Building Materials•••••Beverages & Soft Drinks

•••••••••••••Animal Feeds & Pet Foods

Ingredient Applications Modified Starch

Unmodified Starch

DextrinMaltodextrin

Glucose/Corn Syrup

Dextrose

HFCS Corn Oil

Gluten Feed

Gluten Meal

Germ Meal

Steepwater

scFOS

32

Key Target – GAAP ReconciliationReturn on Capital Employed at December 31

($ millions)Return on Capital Employed 2006 2005Total stockholders’ equity* $1,210 $1,081

Add:

Cumulative translation adjustment* 257 292

Minority interest in subsidiaries* 17 18

Redeemable common stock* 29 33

Total debt* 528 568

Less:

Cash and cash equivalents* (116) (101)Capital employed* (a) $2,041 $1,992

Operating income $224 $183

Adjusted for:

Income taxes (at effective tax rates of 35.25% in 2006 and

37.5% in 2005) (79) (69)

Adjusted operating income, net of tax (b) $145 $114

Return on Capital Employed (b ÷ a) 7.5% 6.0%

* Balance sheet items used in computing capital employed represent beginning of period balances

33

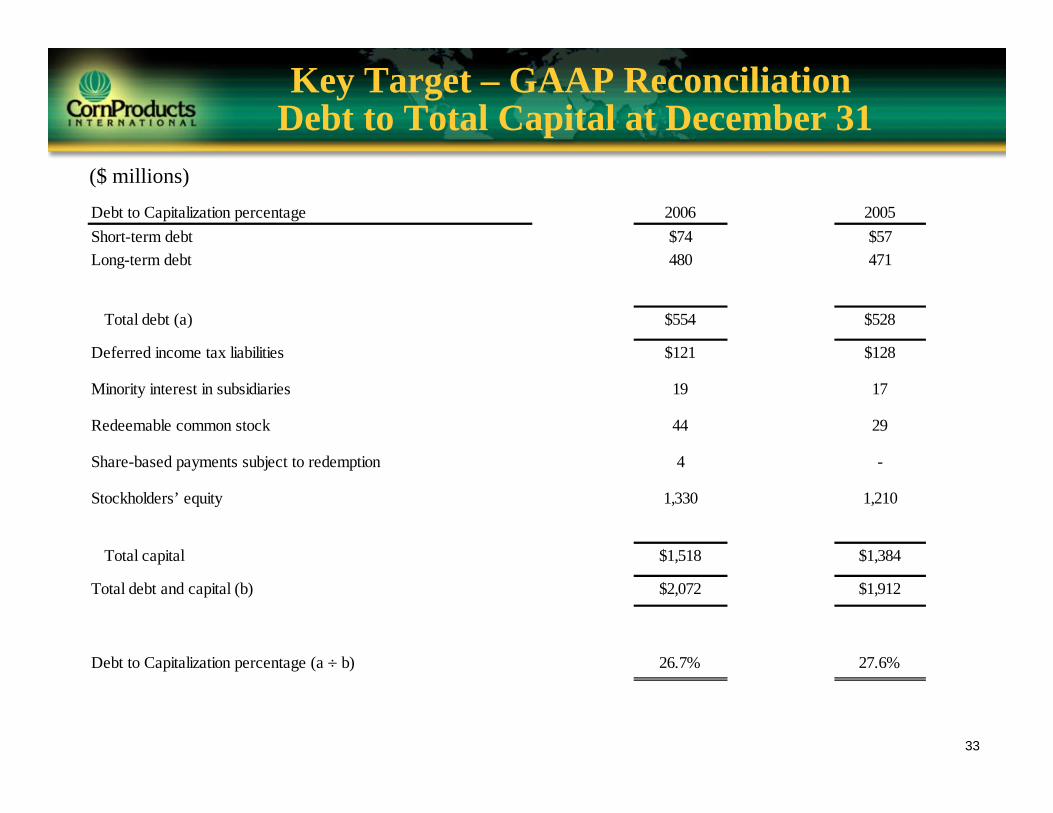

Key Target – GAAP ReconciliationDebt to Total Capital at December 31

($ millions)Debt to Capitalization percentage 2006 2005Short-term debt $74 $57 Long-term debt 480 471

Total debt (a) $554 $528

Deferred income tax liabilities $121 $128

Minority interest in subsidiaries 19 17

Redeemable common stock 44 29

Share-based payments subject to redemption 4 -

Stockholders’ equity 1,330 1,210

Total capital $1,518 $1,384

Total debt and capital (b) $2,072 $1,912

Debt to Capitalization percentage (a ÷ b) 26.7% 27.6%

34

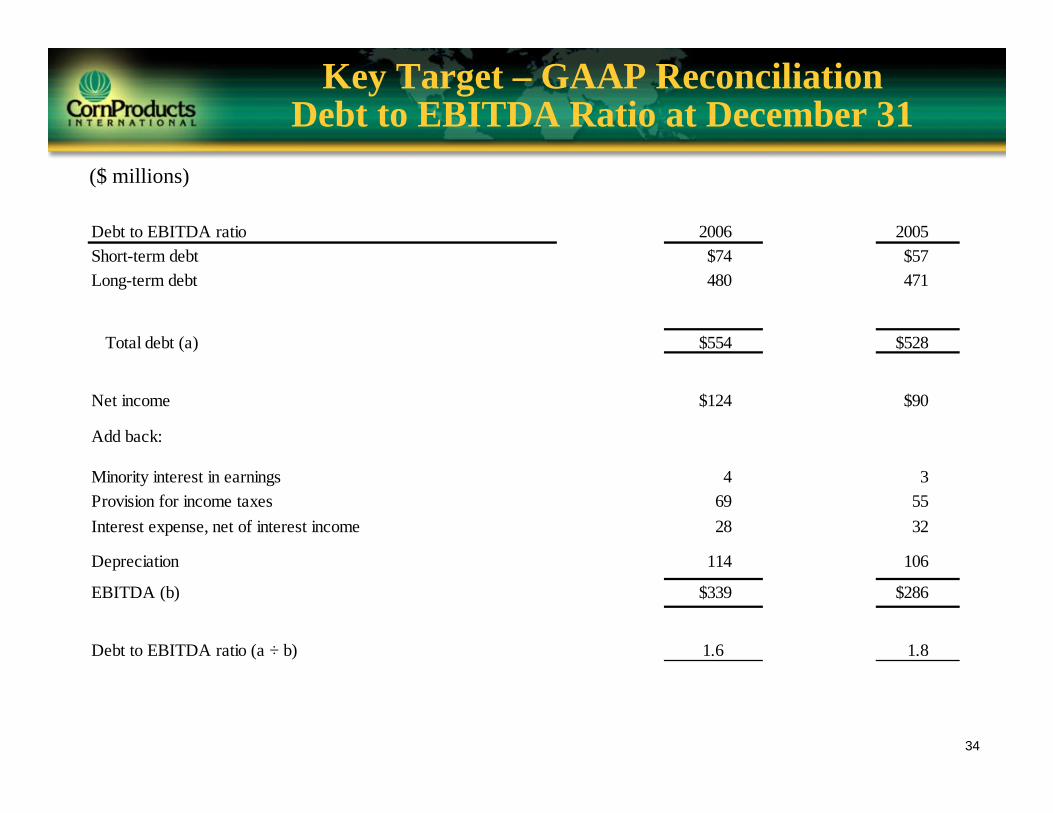

Key Target – GAAP ReconciliationDebt to EBITDA Ratio at December 31

($ millions)

Debt to EBITDA ratio 2006 2005Short-term debt $74 $57 Long-term debt 480 471

Total debt (a) $554 $528

Net income $124 $90

Add back:

Minority interest in earnings 4 3Provision for income taxes 69 55Interest expense, net of interest income 28 32

Depreciation 114 106

EBITDA (b) $339 $286

Debt to EBITDA ratio (a ÷ b) 1.6 1.8

35

Key Target – GAAP ReconciliationOperating Working Capital as % of Net Sales

($ millions)

Operating Working Capital as a percentage of Net Sales 2006 2005Current assets $837 $685

Less: Cash and cash equivalents (131) (116)Less: Deferred income tax assets (16) (13)Adjusted current assets $690 $556

Current liabilities $517 $424

Less: Short-term debt (74) (57)

Less: Deferred income tax liabilities (14) (1)

Adjusted current liabilities $429 $366

Operating working capital (a) $261 $190

Net sales (b) $2,621 $2,360 Operating Working Capital as a percentage of Net Sales (a ÷ b) 8.1%10.0%

36

Geographic Segments – Annual Net Sales/Operating Income 2001 through 2006

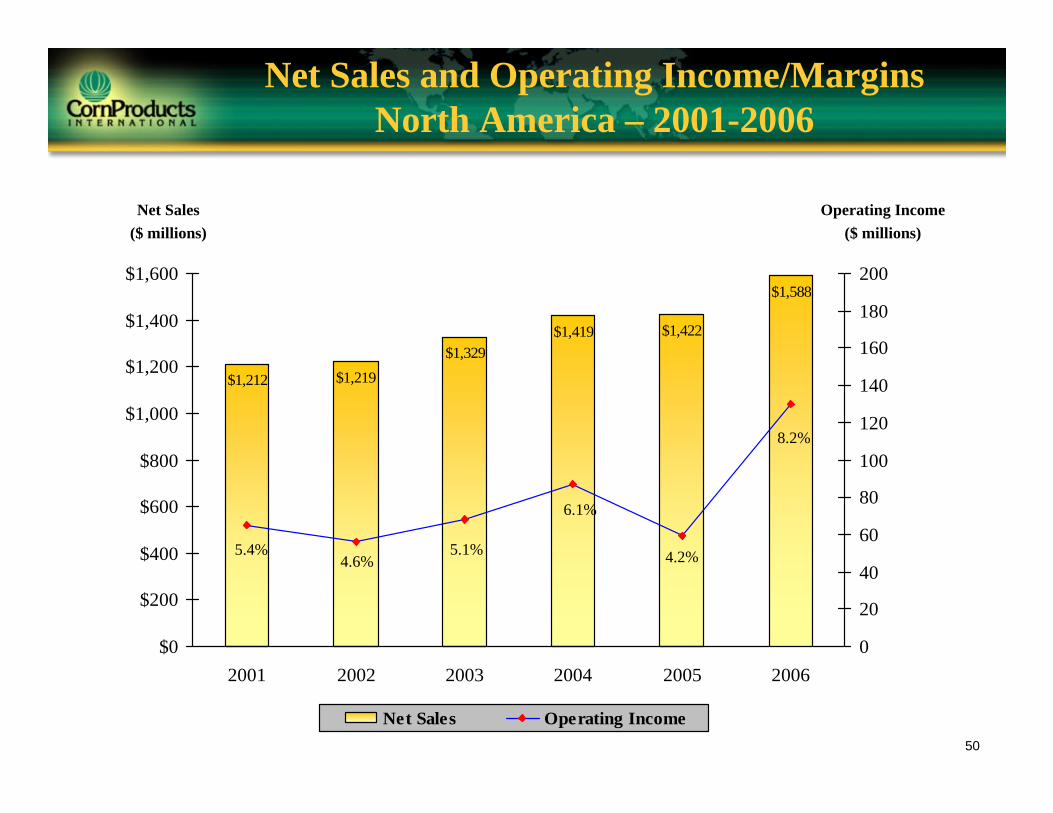

2006 2005 2004 2003 2002 2001Net sales

North America 1,588 1,422 1,419 1,329 1,219 1,212

South America 670 603 556 495 401 440

Asia/Africa 363 335 308 278 251 235

Total 2,621 2,360 2,283 2,102 1,871 1,887

Segment operating income*

North America 130 59 87 68 56 65

South America 84 101 98 83 58 68

Asia/Africa 53 53 48 54 54 45

Total operating income 224 183 179 174 153 166*Geographic segments only

($ millions)

37

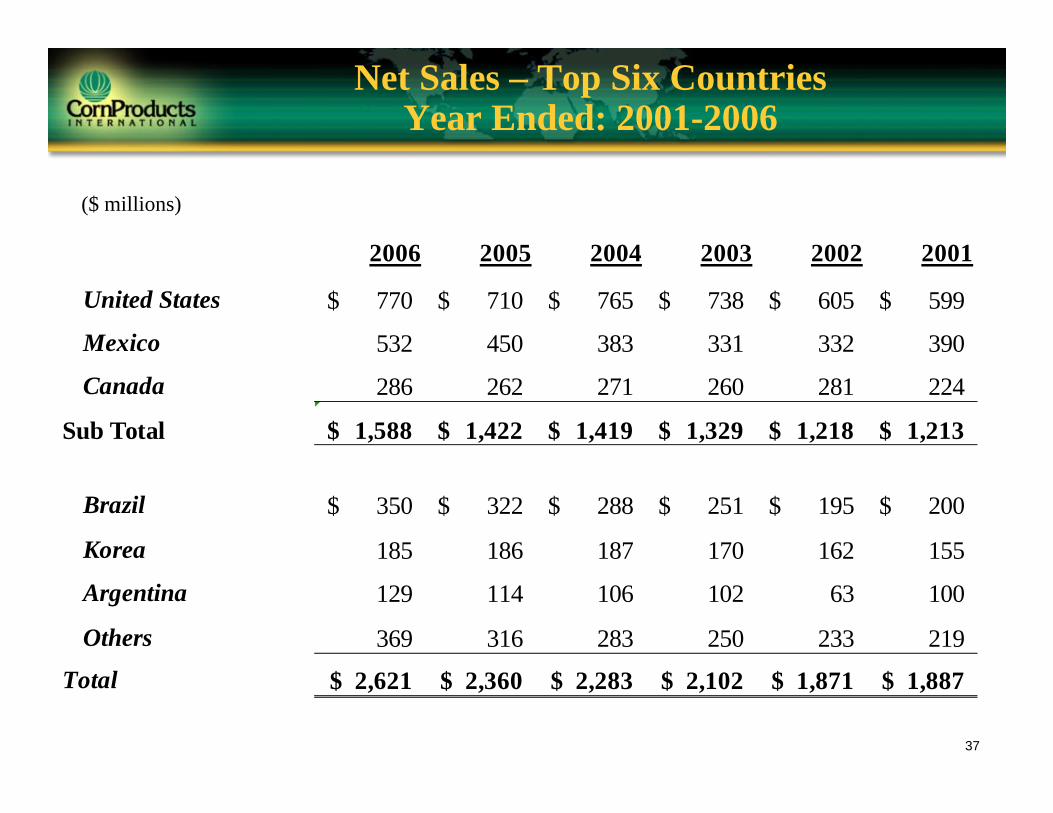

Net Sales – Top Six CountriesYear Ended: 2001-2006

2006 2005 2004 2003 2002 2001

United States 770$ 710$ 765$ 738$ 605$ 599$

Mexico 532 450 383 331 332 390

Canada 286 262 271 260 281 224

Sub Total 1,588$ 1,422$ 1,419$ 1,329$ 1,218$ 1,213$

Brazil 350$ 322$ 288$ 251$ 195$ 200$

Korea 185 186 187 170 162 155

Argentina 129 114 106 102 63 100

Others 369 316 283 250 233 219

Total 2,621$ 2,360$ 2,283$ 2,102$ 1,871$ 1,887$

($ millions)

38

Long-Lived Assets – Top Six Countriesas of December 31: 2001-2006

2006 2005 2004 2003 2002 2001

United States 465$ 428$ 407$ 406$ 433$ 434$

Mexico 365 382 401 426 433 457

Canada 171 176 173 165 147 151

Sub Total 1,001$ 986$ 981$ 997$ 1,013$ 1,042$

Brazil 219$ 160$ 125$ 112$ 88$ 131$

Korea 280 252 243 212 210 186

Argentina 125 120 117 116 67 135

Others 199 183 175 171 146 158

Total 1,824$ 1,701$ 1,641$ 1,608$ 1,524$ 1,652$

($ millions)

39

Percent of Net Sales

2006 2005 2004 2003 2002 2001

Starch 22% 23% 22% 21% 20% 20%

Sweeteners 55% 53% 52% 54% 55% 57%

Co-products & other 23% 24% 26% 25% 25% 23%

Major Industries

Processed foods 19% 19% 22% 21% 21% 22%

Soft drink 18% 18% 17% 17% 17% 20%

Brewing 11%

Animal feed 10% 11% 19% 19% 16% 15%

40

Summary Balance Sheet2006, 2005 and 2004

2006 2005 2004

Current assets 842$ 685$ 684$ Net fixed assets 1,356 1,274 1,211 Other assets 470 430 472 Total assets 2,668$ 2,389$ 2,367$

Current liabilities* 429$ 367$ 374$ Total debt 554 528 568 Other liabilities 307 255 311 Redeemable equity 44 29 33 Stockholders' equity 1,330 1,210 1,081 Total liabilities and equity 2,668$ 2,389$ 2,367$ *Excludes short-term debt

($ millions)

41

Summary Cash Flow2006, 2005 and 2004

2006 2005 2004

Cash flow from operations 230$ 245$ 166$ Net income 124 90 94 Depreciation 114 106 102 Working capital (increase)/decrease (27) 60 (37) Other 19 (11) 7

Cash flow from investing (210)$ (141)$ (149)$ Fixed assets, net (168) (136) (103) Acquisition (42) (5) (68) Sale of investment - - 21 Other - - 1

Cash flow from financing (6)$ (91)$ 13$ Net increase (decrease) in debt 16 (44) 6 Dividends paid to CPO common (26) (21) (17) Issuance (Repurchase) of common, net (2) (25) 30 Dividends paid to minority shareholders - (1) (6)

($ millions)

42

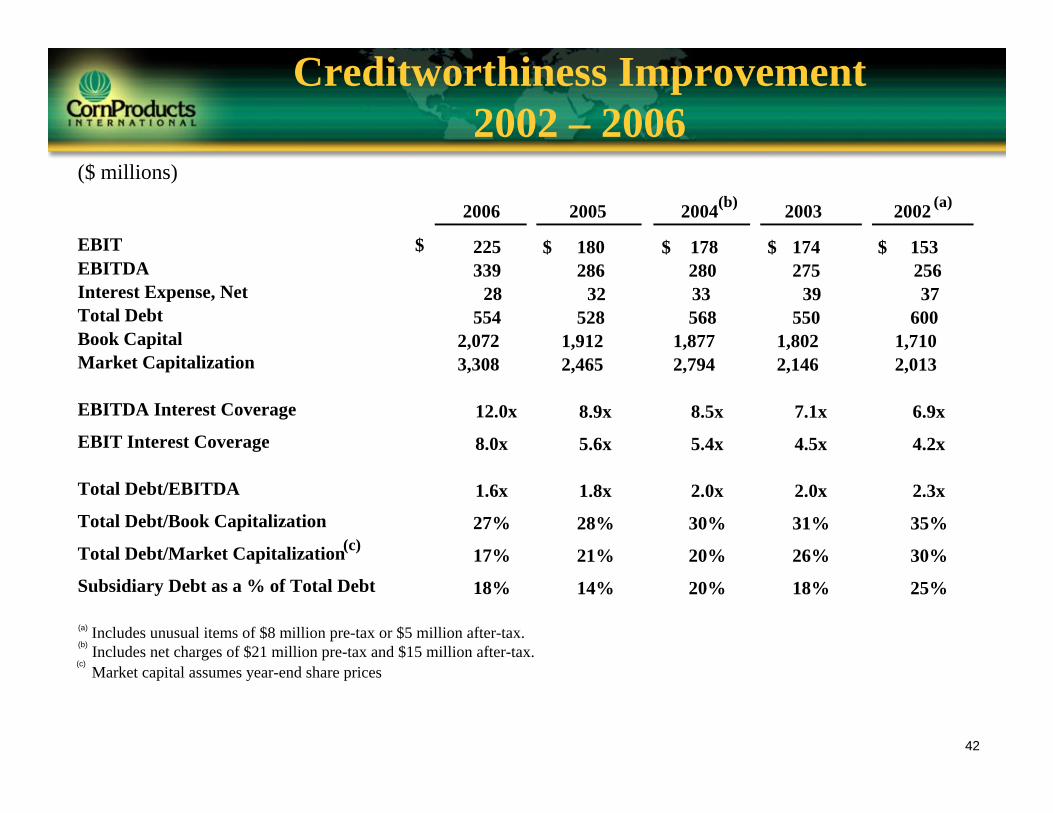

Creditworthiness Improvement2002 – 2006

($ millions)

EBITEBITDAInterest Expense, NetTotal DebtBook CapitalMarket Capitalization

EBITDA Interest Coverage

EBIT Interest Coverage

Total Debt/EBITDA

Total Debt/Book Capitalization

Total Debt/Market Capitalization

Subsidiary Debt as a % of Total Debt

2005 2004(b) 2003 2002 (a)

180$ 178$ 174$ 153$ 286 280 275 256

32 33 39 37528 568 550 600

1,912 1,877 1,802 1,7102,465 2,794 2,146 2,013

8.9x 8.5x 7.1x 6.9x

5.6x 5.4x 4.5x 4.2x

1.8x 2.0x 2.0x 2.3x

28% 30% 31% 35%

21% 20% 26% 30%

14% 20% 18% 25%

2006

(c)

225339

28554

2,0723,308

12.0x

8.0x

1.6x

27%

17%

18%

(a) Includes unusual items of $8 million pre-tax or $5 million after-tax.(b) Includes net charges of $21 million pre-tax and $15 million after-tax.(c)

Market capital assumes year-end share prices

$

43

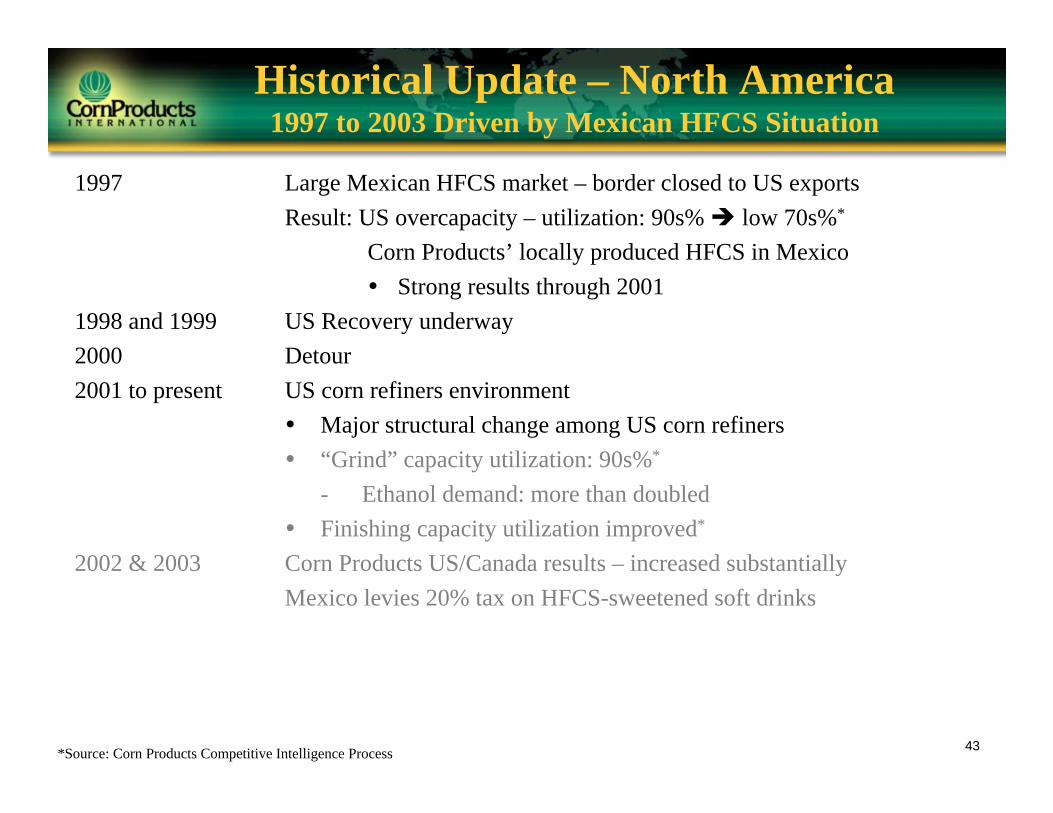

Historical Update – North America1997 to 2003 Driven by Mexican HFCS Situation

*Source: Corn Products Competitive Intelligence Process

1997 Large Mexican HFCS market – border closed to US exportsResult: US overcapacity – utilization: 90s% low 70s%*

Corn Products’ locally produced HFCS in MexicoStrong results through 2001

1998 and 1999 US Recovery underway2000 Detour2001 to present US corn refiners environment

Major structural change among US corn refiners“Grind” capacity utilization: 90s%*

- Ethanol demand: more than doubledFinishing capacity utilization improved*

2002 & 2003 Corn Products US/Canada results – increased substantiallyMexico levies 20% tax on HFCS-sweetened soft drinks

44*Source: Corn Products International Competitive Intelligence Process**Source: Associated Press, August 17, 2004 ; ***Source: Decatur Daily, October 4, 2005

Competitive arena*: US HFCS processor company changes

November 2000: 7 HFCS producers – 3 with 17% of capacity

March 2002 thru present: 4 HFCS producers with 97% of capacity

Historical Update – North America

ProGold MCP Cerestar

Cargill

Cargill ADM 30%

CPMCP

ADM

Coors

Gone1997

2000

2002

2004

2005

2006

Cargill

Shuts ½ Dayton

Idles Dimmitt, TX**

Idles Decatur, AL***

Restarts Decatur, AL

45*Source: Corn Products Competitive Intelligence Process

1997 Large Mexican HFCS market – border closed to US exportsResult: US overcapacity – utilization: 90s% low 70s%*

CPO’s locally produced HFCS in MexicoStrong results through 2001

1998 and 1999 US Recovery underway2000 Detour2001 to present US corn refiners environment

Major structural change among U.S. corn refiners“Grind” capacity utilization: 90s%*

- Ethanol demand: more than doubledFinishing capacity utilization improved*

2002 & 2003 CPO US/Canada Operating Income – increased substantiallyMexico – 20% tax on HFCS-sweetened soft drinks

Except for ethanolNo expansions since 1997*

Historical Update – North America1997 to 2003 Driven by Mexican HFCS Situation

46

High Value Ingredients• Product differentiation• Internal source

– Line extensions– New ingredient commercialization

• External source– Acquisitions– Alliances

Basic Ingredients• No product differentiation• Commodity-oriented pricing• Advances

– Quality, timeliness, reliability– Ingredient supplier approach

• Geographic growth

High Value Specialty Ingredients

• IP-based differentiation• Alliances • Acquisitions• New ingredient commercialization

Specialty Ingredients

• Product/service differentiation• Line extensions • Success as ingredient supplier

Value

Spec

ializ

atio

nOur Approach …

Ingredient Positioning

47

South America Ingredients

BASIC INGREDIENTS

High Maltose Syrup Regular StarchGlucose Corn SyrupHFCSLiquid DextroseSyrup Blends

SPECIAL INGREDIENTS

• Food Modified Starches• Industrial Modified Starches• Dried Blends• Crystalline Dextrose• Dried Syrups• Maltodextrine• Sorbitol, Mannitol, Liquid

Maltitol• Fructooligosaccharide• Caramel Color• Adhesives & Dextrines• Fats & Emulsifiers• Refined Corn Oil

ANIMAL NUTRITION & HEALTH

• Gluten Feed• Gluten Meal• Other, Basic & Special

Ingredients

Raw Materials:

Regular and Waxy Corn, Tapioca, Wheat & Soy Flour, Sucrose

48

Net Sales & Operating Income/MarginsSouth America – 2001-2006

$440$401

$495$556

$603

$670

$0

$200

$400

$600

$800

2001 2002 2003 2004 2005 20060

20

40

60

80

100

120

140

160

180

200

Net Sales Operating Income

Net Sales($ Millions)

Operating Income($ Millions)

16.8%

17.6% 16.8%12.5%

14.5%15.5%

49

North America Ingredients

BASIC INGREDIENTS

HFCSCorn StarchCorn SyrupLiquid DextroseBlends

SPECIAL INGREDIENTS

• Refined Corn Oil• Crystalline Dextrose• Modified Starches• Maltodextrine• Sorbitol• Fructooligosaccharide• Caramel Color

ANIMAL NUTRITION & HEALTH

• Gluten Feed• Gluten Meal• Other

50

Net Sales and Operating Income/MarginsNorth America – 2001-2006

$1,588

$1,422$1,419

$1,219$1,212

$1,329

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2001 2002 2003 2004 2005 20060

20

40

60

80

100

120

140

160

180

200

Net Sales Operating Income

Net Sales($ millions)

Operating Income($ millions)

5.1%

6.1%

4.2%

8.2%

4.6%5.4%

51

Asia/Africa Ingredients

BASIC INGREDIENTS

Corn StarchCorn SyrupHFCSTapioca StarchTapioca SyrupDextrose

SPECIAL INGREDIENTS

• Refined Corn Oil• Modified Textile starch• Modified Paper Starch• High Maltose Syrup• Dextrines• Tapioca Oxidized Starch• Tapioca Maltodextrine• Oligosaccharides

ANIMAL NUTRITION & HEALTH

• Gluten Feed• Gluten Meal• Other

52

Net Sales & Operating Income/MarginsAsia/Africa – 2001-2006

$235$251

$278$308

$335$363

$0

$50

$100

$150

$200

$250

$300

$350

$400

2001 2002 2003 2004 2005 20060

20

40

60

80

100

120

Net Sales Operating Income

Net Sales($ Millions)

Operating Income($ Millions)

19.4%15.6%

15.8% 14.6%21.5%19.2%

53

Specialty Ingredients Examples of Progress

• Food starches - specialties– Variety of raw materials: corn – dent and waxy; tapioca; blends

• Applications: sauces, mayonnaise, dressings, frozen desserts, yogurt, beverages, flavors

• Types: cross-bonded and pregelatinized, OSA, HPS and CSW starches• ExpandexTM modified tapioca starch for gluten intolerance market• Industrial starches

– Ecopolymers for plastic replacement– Casein-based adhesive for labeling– Pregelatinized starch for mining and tissue– Acetylated thin-boiling waxy starch for paper coating

• Health and personal care– OSA aluminum and calcium for creams– Cationic starch for softener– Sorbitol for tooth paste and tableting

54

CornBasic Structure and Approximate Yield*

Kernel Structure• Hull – Fiber• Starch• Protein• Germ

Approximate Yield• Starch 68%• Gluten Feed 19%• Gluten Meal 5%• Germ

– Corn oil 4%– Germ meal 3%

*Note: These are only approximations due to our use of varieties of hybrids throughout our world