Lecture Notes

MATHEMATICAL ECONOMICS

A. Neyman

Fall 2006, Jerusalem

The notes may/will be updated in few days. Please revisit to check for

the updated version. Please email comments to [email protected]

1 Course Outline

Exchange economies, efficient allocations, competitive equilibria, efficiency of

competitive equilibria, existence of competitive equilibrium, generic finiteness

of competitive equilibria, core and competitive equilibria.

2 References

Debreu, G., Theory of Value. New York: Wiley (1959).

Debreu, G., Mathematical Economics, Twenty papers of Gerard Debreu.

Cambridge: Cambridge University Press (1983).

Arrow, K. and Hann, F., General Competitive Analysis. San Francisco:

Holden-Day (1971).

1

Arrow, K., and Intriligator, M., eds. Handbook of Mathematical Economics,

vol. I. New york: North-Holland (1981).

Arrow, K., and Intriligator, M., eds. Handbook of Mathematical Economics,

vol. II. New york: North-Holland (1982).

Mas-Colell, A., The theory of general economic equilibrium: A differentiable

approach. Cambridge U.K.: Cambridge University Press (1985).

Mas-Colell, A., M. D. Whinston and J. R. Green, Microeconomic Theory.

New York Oxford: Oxford University Press (1995).

3

Exchange Economies

An exchange economy consists of:

1) A set of traders T .

2) A vector space V - the space of goods.

3) For every t ∈ T a subset X(t) ⊂ V - the consumption set of trader t.

4) For every t ∈ T , an element e(t) ∈ X(t)- the initial endowment of

trader t.

2

5) For every t ∈ T a binary relation �t on X(t) - the preference relation

of trader t.

For the mean time we assume that the trader set T consists of finitely

many traders, i.e., T is a finite set.

If there are ` goods, V = IR`, and an element x ∈ V , x = (x1, . . . , x`) is

interpreted as a bundle of xi units of commodity i.

The set X(t) represents the consumption set of trader t, i.e. the set of

all feasible consumption bundles of trader t. For instance, if one of the com-

modities is leisure in a given day, it is bounded by 24 hours. Restrictions of

the consumption set may also result by interrelations of several commodities.

The initial endowment e(t) represents the initial bundle of goods of trader

t before trading takes place.

The preference relation �t represents trader’s t preference over his feasible

consumption. Given x, y ∈ X(t), x �t y means that trader t prefers (strictly)

bundle x over bundle y.

Remarks The binary (preference) relation �t is called transitive if x �t y

and y �t z imply x �t z. It is continuous if {(x, y) ∈ X(t)×X(t) : x �t y}

is open in X(t)×X(t).

3

A utility function on X(t) is a real valued function u : X(t) → IR. The

preference relation � induced by a utility function u is the binary relation

x � y ⇐⇒ u(x) > u(y). A binary relation induced by a utility function is

transitive, and a binary relation induced by a continuous utility function is

continuous.

An important implicit assumption in our present modeling of an exchange

economy is that there are no externalities. Each individual cares about his

consumption “alone”.

Example of an exchange economy with 2 traders and 2 commodities:

T = {1, 2}

V = IR2

IR2+ = X(1) = X(2)

e(1) = (4, 0) and e(2) = (0, 2)

�1 is the preference relation induced by the utility function u(x1, x2) = x1x2,

and �2 is the preference relation induced by the utility function u(x1, x2) =

min(x1, x2).

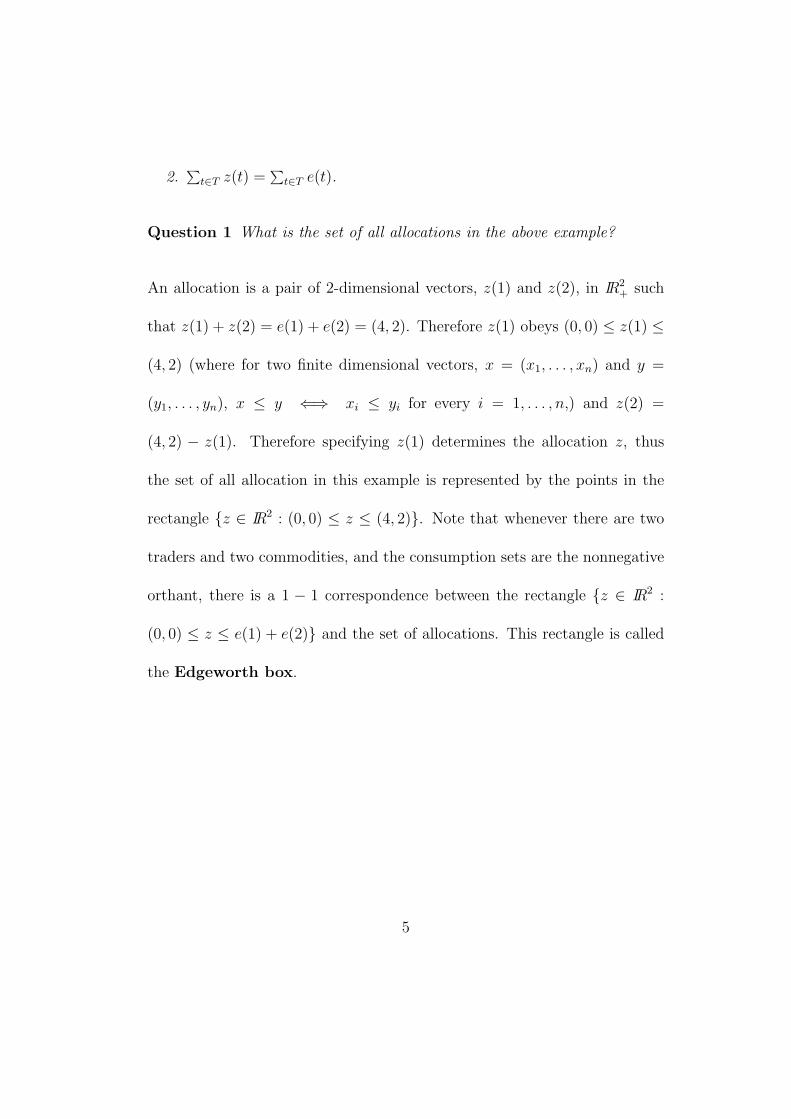

Definition 1 An allocation in an exchange economy 〈T ; V ; (X(t))t∈T ;

(e(t))t∈T ;�t∈T 〉 is a function z : T → V such that

1. ∀t ∈ T , z(t) ∈ X(t)

4

2.∑

t∈T z(t) =∑

t∈T e(t).

Question 1 What is the set of all allocations in the above example?

An allocation is a pair of 2-dimensional vectors, z(1) and z(2), in IR2+ such

that z(1) + z(2) = e(1) + e(2) = (4, 2). Therefore z(1) obeys (0, 0) ≤ z(1) ≤

(4, 2) (where for two finite dimensional vectors, x = (x1, . . . , xn) and y =

(y1, . . . , yn), x ≤ y ⇐⇒ xi ≤ yi for every i = 1, . . . , n,) and z(2) =

(4, 2) − z(1). Therefore specifying z(1) determines the allocation z, thus

the set of all allocation in this example is represented by the points in the

rectangle {z ∈ IR2 : (0, 0) ≤ z ≤ (4, 2)}. Note that whenever there are two

traders and two commodities, and the consumption sets are the nonnegative

orthant, there is a 1 − 1 correspondence between the rectangle {z ∈ IR2 :

(0, 0) ≤ z ≤ e(1) + e(2)} and the set of allocations. This rectangle is called

the Edgeworth box.

5

Edgeworth box

initial endowment

(0,0)

(0,2)

-

6

(4,2)

(4,0)

t ��

Question 2 How can we describe the preferences in the above example?

The consumption set of trader 1 is the positive orthant of IR2 and his prefer-

ence relation, �1 can be described by means of the indifference curves. E.g.,

consider all points x = (x1, x2) ∈ IR2+ with x1x2 = 1. The geometric location

of all these points is called an indifference curve. Similarly, for any given

α ≥ 0, the geometric location of all points x = (x1, x2) ∈ IR2+ with x1x2 = α

is denoted I1α and is an indifference curve. Trader 1 is indifferent between

any two bundles in I1α, and if x ∈ I1

α and y ∈ I1β then x �1 y ⇐⇒ α > β.

Similarly, the consumption set of trader 2 is the positive orthant of IR2

and his preference relation, �2 can be described by means of the indifference

curves. E.g., consider all points y = (y1, y2) ∈ IR2+ with min(y1, y2) = 1.

The geometric location of all these points is an indifference curve of the

6

preference relation �2. Similarly, for any given α ≥ 0, the geometric location

of all points x = (x1, x2) ∈ IR2+ with min(x1, x2) = α is denoted I2

α and is an

indifference curve of �2. Trader 2 is indifferent between any two bundles in

I2α, and if x ∈ I2

α and y ∈ I2β then x �2 y ⇐⇒ α > β.

Definition 2 An allocation z is (weakly) efficient if there is no allocation y

with y(t) �t z(t) for every t ∈ T .

Question 3 What are the (weakly) efficient allocations in the above exam-

ple?

Question 4 Are there efficient allocation in each exchange economy?

Definition 3 A competitive equilibrium of an exchange economy E is an

ordered pair (p, z) such that:

p is a nontrivial linear functional on V .

z is an allocation with p(z(t)) = p(e(t)) for every t ∈ T , and

∀t ∈ T , {x ∈ X(t) : p(x) ≤ p(e(t)) and x �t z(t)} = ∅.

Remarks If V = IR` then any linear functional over V is represented by

a vector p = (p1, . . . , p`) where

p(x) =∑̀i=1

pixi

7

The vector p is called the vector of prices and pi is interpreted as the price

of commodity i.

Question 5 What are the competitive equilibria in the above example?

4

4.1 Efficiency of Competitive Equilibrium

Theorem 1 Let E = 〈T ; V ; (X(t))t∈T ; (e(t))t∈T ; (�t)t∈T 〉 be an exchange econ-

omy, and assume that (p, x) is a competitive equilibrium. Then the allocation

x is weakly efficient.

proof Assume that z is an allocation with z(t) �t x(t) for every trader

t ∈ T . As (p, x) is a competitive equilibrium, p(z(t)) > p(e(t)). As p is a lin-

ear functional, p(∑

t∈T z(t)) =∑

t∈T p(z(t)) and p(∑

t∈T e(t)) =∑

t∈T p(e(t))

and therefore p(∑

t∈T z(t)) > p(∑

t∈T e(t)) which contradicts the equality

∑t∈T z(t) =

∑t∈T e(t)

4.2 The Core

A coalition is a subset of T . Let S ⊂ T be a coalition. An S - allocation is

a function x : S → V such that for every t ∈ S x(t) ∈ X(t) and∑

t∈S x(t) =

8

∑t∈S e(t).

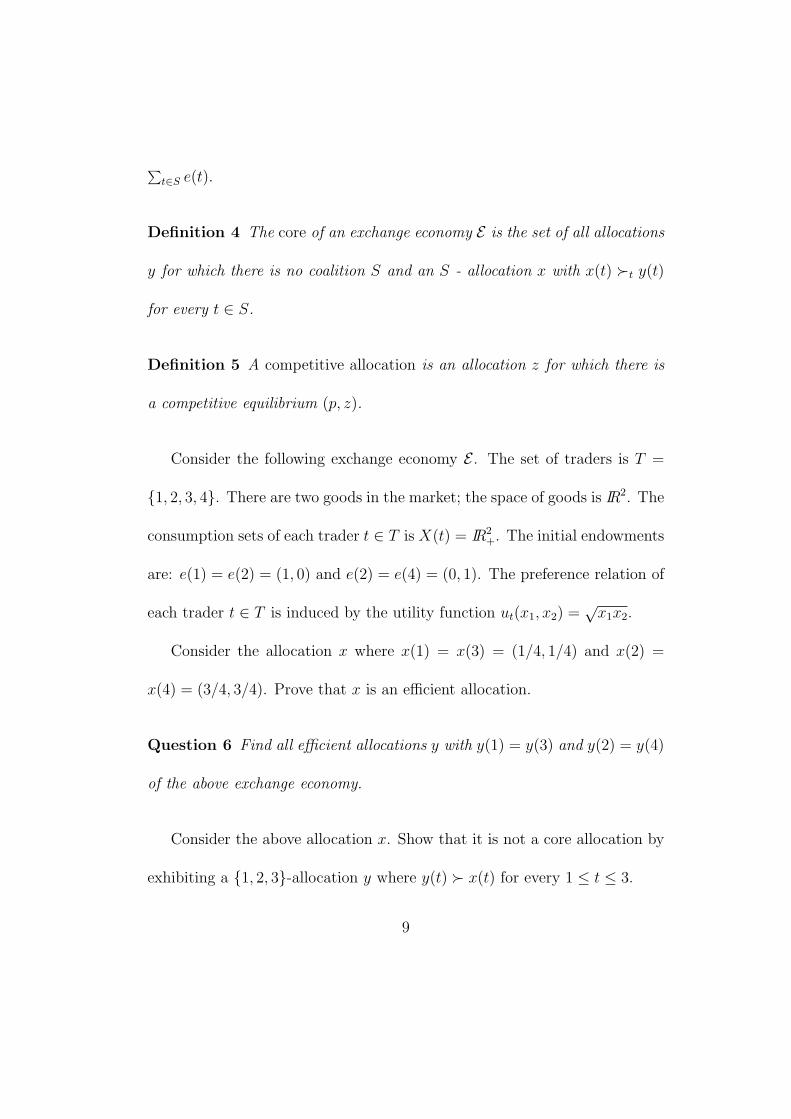

Definition 4 The core of an exchange economy E is the set of all allocations

y for which there is no coalition S and an S - allocation x with x(t) �t y(t)

for every t ∈ S.

Definition 5 A competitive allocation is an allocation z for which there is

a competitive equilibrium (p, z).

Consider the following exchange economy E . The set of traders is T =

{1, 2, 3, 4}. There are two goods in the market; the space of goods is IR2. The

consumption sets of each trader t ∈ T is X(t) = IR2+. The initial endowments

are: e(1) = e(2) = (1, 0) and e(2) = e(4) = (0, 1). The preference relation of

each trader t ∈ T is induced by the utility function ut(x1, x2) =√

x1x2.

Consider the allocation x where x(1) = x(3) = (1/4, 1/4) and x(2) =

x(4) = (3/4, 3/4). Prove that x is an efficient allocation.

Question 6 Find all efficient allocations y with y(1) = y(3) and y(2) = y(4)

of the above exchange economy.

Consider the above allocation x. Show that it is not a core allocation by

exhibiting a {1, 2, 3}-allocation y where y(t) � x(t) for every 1 ≤ t ≤ 3.

9

Question 7 Find all core allocations y with y(1) = y(3) and y(2) = y(4) of

the above exchange economy.

Show that every core allocation y of the above exchange economy satisfies

y(1) = y(3) and y(2) = y(4). Therefore the solution of the previous question

describes all allocations in the core of E .

Theorem 2 Any competitive allocation is in the core.

Proof. Assume that (p, z) is a competitive equilibrium, S a nonempty subset

of T , and x : S → V with x(t) �t z(t) for every t ∈ S. As (p, z) is a compet-

itive equilibrium, px(t) > pz(t) for every t ∈ S, and therefore∑

t∈S px(t) >

∑t∈S pz(t) =

∑t∈S pe(t), i.e., p

∑t∈S x(t) > p

∑t∈S z(t) = p

∑t∈S e(t), imply-

ing that∑

t∈S x(t) 6= ∑t∈S e(t). Thus x is not an S-allocation. We have thus

proved that there is no coalition S and an S-allocation x with x(t) � z(t)

for every t ∈ S, i.e., that z is in the core of the exchange economy.

4.3 Preferences, Utility, and Demand

A binary relation R on a set X is a subset R ⊂ X × X. We write xRy

whenever (x, y) ∈ R. The binary relation R is reflexive if xRx for every

x ∈ X. It is transitive if for every x, y, z ∈ X, “xRy and yRz” implies

10

“xRz.” A binary relation R on X is complete if for every x, y ∈ X either

xRy or yRx.

4.4 Brouwer’s Fixed Point Theorem

Theorem 3 (Brouwer’s fixed point theorem): Let C be a nonempty convex

compact subset of IRn and let f : C → C be a continuous function. Then f

has a fixed point, i.e., there is a point x ∈ C such that f(x) = x.

Remarks The proof of Brouwer’s fixed point theorem in the 1-dimensional

case is equivalent to the mean value theorem of continuous functions. Indeed,

a convex compact subset of IR is a closed interval [a, b], and a continuous

function f : [a, b] → [a, b] satisfies f(a) ≥ a and f(b) ≤ b. Therefore, the

continuous function g : [a, b] → IR defined by g(x) = f(x)−x obeys g(a) ≥ 0

and g(b) ≤ 0 and therefore there is x ∈ [a, b] such that g(x) = 0 i.e. f(x) = x.

Each one of the assumptions in Brouwer’s fixed point theorem necessary. In-

deed, if S1 = {(x, y) ∈ IR2 : x2+y2 = 1}, the continuous function f : S1 → S1

defined by f(x, y) = −(x, y) does not have a fixed point. The continuous

function f : (0, 1] → (0, 1] defined by f(x) = x/2 does not have a fixed point.

The continuous function f : IR → IR defined by f(x) = x + 1 does not have

a fixed point. The function f : [0, 1] → [0, 1] defined by f(x) = x/2 if x > 0

11

and f(0) does not have a fixed point.

The graph of a function f : C → D is the subset {(x, y) : y = f(x)} of

C ×D, and is denoted Γf . When D ⊂ IRn is a compact subset, the function

f is continuous if and only if Γf is a closed subset of C ×D. Indeed, assume

that f is continuous and that the sequence (xk, yk) ∈ Γf converges as k →∞

to a point (x, y) ∈ C ×D. Then xk → x as k →∞ and yk = f(xk). As f is

continuous yk = f(xk) → f(x) and therefore y = f(x), i.e., (x, y) ∈ Γf . In

the other direction, assume that Γf is closed in C × D. Let xk, x ∈ C and

assume that xk → x. We have to prove that yk = f(xk) → f(x) as k → ∞.

Otherwise, as D is compact, there is a subsequence (ykm) which converges to

a point y∗ ∈ D with y∗ 6= f(x); therefore, (xkm , ykm) → (x, y∗) ∈ C ×D. As

(xkm , ykm) ∈ Γf and Γf is closed in C ×D, (x, y∗) ∈ C ×D, i.e y∗ = f(x) a

contradiction.

4.5 Set-Valued Functions

A set-valued function from a set X to a set Y is a function which maps points

in X to subsets of Y . A fixed point of a set-valued function f from X to X

12

is a point x ∈ X such that x ∈ f(x).

Consider the following set-valued function from [0, 1] to [0, 1].

f(x) =

{x + 1/2} if x < 1/2

{0, 1} if x = 1/2

{x− 1/2} if x > 1/2

The graph of a set valued function f from X to Y is the subset {(x, y) :

x ∈ X, y = f(x)} of X × Y . The graph of the above set valued function is

depicted in the following figure:

Figure 1

x

y

-

6

��

��

�

��

��

�

(1,1)

1

1

tt

tt

Note that this set-valued function does not have any fixed point. We

describe next another set-valued function from [0, 1] to [0, 1].

13

f(x) =

{x + 1/2} if x < 1/2

[0, 1] if x = 1/2

{x− 1/2} if x > 1/2

The graph of this set-valued function is depicted in the following figure:

Figure 2

x

y

-

6

��

��

�

��

��

�

(1,1)

1

1

tt

tt

5 Kaukutani’s Fixed point Theorem

Definition 6 A set-valued function f from X to Y is called uppersemicon-

tinuous if xn → x ∈ X, yn → y ∈ Y , and yn ∈ f(xn) for all n imply

y ∈ f(x).

The graph of a set-valued function f from C to D is the subset {(x, y) :

y ∈ f(x)} of C ×D, and is denoted Γf .

14

The function f is uppersemicontinuous if and only if Γf is a closed subset of

C ×D.

Indeed, let f be a set-valued function from C to D and assume that (xn, yn) ∈

Γf ⊂ C×D is a sequence that converges to (x, y) ∈ C×D. If f is uppersemi-

continuous then y ∈ f(x) and therefore Γf is closed in C × D, and if Γf is

closed in C ×D then (x, y) ∈ Γf , i.e., y ∈ f(x) and thus f is uppersemicon-

tinuous.

If f is an uppersemicontinuous set-valued function from C to D, then, for

any x ∈ C, f(x) is a closed subset of D.

If f is a function from C to D, we may identify the function f with the set

valued function which maps a point x ∈ C to the subset {f(x)} of D. Note

that if f is continuous then the associated set-valued function is uppersemi-

continuous, and if D is compact and the associated set-valued function is

uppersemicontinuous then f is continuous.

Given a subset A of IRk and a point x ∈ IRk we define the distance of x

to A, d(x, A), as inf{||x− y|| : y ∈ A}.

Claim 1: Let f be an uppersemicontinuous set-valued function from a

15

subset C of a Euclidean space into a compact subset D of a Euclidean space.

Then, for every x ∈ C and ε > 0 there is δ = δ(x, ε) > 0 such that if x, x′ ∈ C

with ||x− x′|| < δ and z ∈ f(x′), then d(f(x), z) < ε.

Proof. Otherwise, there are x ∈ C, ε > 0, and two sequences (xn)∞n=1, and

(zn)∞n=1 such that ||xn − x|| → 0 as n →∞, zn ∈ f(xn) and d(zn, f(x)) > ε.

W.l.o.g. we assume that zn → z ∈ D as n → ∞ (otherwise we take a sub-

sequence). As f is uppersemicontinuous, z ∈ f(x). Therefore, d(zn, f(x)) ≤

||zn − z|| → 0 as n →∞. A contradiction.

Claim 2: Let A be a convex subset of IRm , y1, . . . , ym ∈ IRm and αi ≥ 0

with∑m

i=1 αi = 1. Then

d(m∑

i=1

αiyi, A) ≤ mmaxi=1

d(yi, A).

Proof. Let ε > 0. For every 1 ≤ i ≤ m there is xi ∈ A with ||xi − yi|| <

d(yi, A) + ε. Note that A is convex and therefore∑m

i=1 αixi ∈ A thus

d(∑m

i=1 αiyi, A) ≤ ||∑mi=1 αiyi −

∑mi=1 αixi|| which by the triangle inequal-

ity is at most∑m

i=1 αi||yi − xi|| which is bounded by maxmi=1 ||yi − xi|| ≤

maxmi=1 d(yi, A) + ε.

We are ready now to state Kakutani’s fixed point theorem which is a

16

generalization of Brouwer’s fixed point theorem.

Theorem 4 (Kakutani’s fixed point theorem) Let f be an uppersemi-

continuous set-valued function from a nonempty convex compact subset C of

IRn into itself (i.e., f(x) ⊂ C for all x ∈ C) such that for all x ∈ C f(x)

is a nonempty convex subset of C. Then f has a fixed point, i.e., there is a

point x ∈ C with x ∈ f(x).

Proof We prove Kakutani’s fixed point theorem from Brouwer’s fixed

point theorem. The idea of the proof is as follows: we construct a sequence

of continuous functions gn : C → C such that any limit point of a sequence of

points (xn, yn) ∈ Γgn is in the graph of f . By Brouwer’s fixed point theorem

it follows that gn has a fixed point xn, i.e., a point xn ∈ C with xn = gn(xn).

Let (x, y) ∈ C ×C be a limit point of (xn, gn(xn)) = (xn, xn). As the ‘diago-

nal,’ {(x, x) : x ∈ C}, is closed in C ×C, y = x and thus x is a fixed point of

f . (Alternatively, w.l.o.g. we assume that xn → x ∈ C as n →∞, (otherwise

we replace the sequence (n)∞n=1 with a subsequence (nk)∞k=1), and therefore

(xn, xn) → (x, x) ∈ Γf i.e., x is a fixed point of the set-valued function f .)

Construction of the functions gn, n = 1, . . ..

17

Fix n > 0 and for every x ∈ C let B(x, 1/n) denote the open ball of

radius 1/n and center x, i.e., B(x, 1/n) = {y ∈ C : ||y − x|| < 1/n}. Recall

that C is compact, and observe that C = ∪x∈CB(x, 1/n). Therefore there

is a finite subset of these balls that covers C, i.e., for any n there is a list

xn1 , . . . , x

nm (m = m(n)) of points in C such that C = ∪m

i=1B(xni , 1/n). Define

the real valued functions δni : C → IR by δn

i (y) = max(0, 1/n − ||y − xi||).

Note that δni (y) > 0 if ||xi − y|| < 1/n and δn

i (y) = 0 if ||y − xi|| ≥ 1/n, and

that∑m

j=1 δni (x) > 0 for every x ∈ C.

Therefore, for every i = 1, . . . ,m,δni (x)∑m

j=1δnj (x)

is a continuous positive (real

valued) function defined on C, and

m∑i=1

δni (x)∑m

j=1 δnj (x)

= 1.

For any i = 1, . . . ,m let yni ∈ f(xn

i ) and define gn : C → C by

gn(x) =m∑

i=1

δni (x)∑m

j=1 δnj (x)

yni

It follows that gn is a continuous function from C to C. Therefore, by

Brouwer’s fixed-point theorem, gn has a fixed point x̄n, i.e., gn(x̄n) = x̄n. Let

x be a limit point of the sequence (x̄n)∞n=1.

We will show that d(x, f(x)) = 0. As f(x) is closed, it will follow that

x ∈ f(x) i.e., x is a fixed point of f .

18

Fix ε > 0 and let δ = δ(x, ε) be defined as in claim 1. As x is a limit

point of the sequence (x̄n)∞n=1, there is n > 2/δ with ||x̄n − x|| < δ/2. For

every i with ||xni − x̄n|| ≥ δ/2 > 1/n, δn

i (x̄n) = 0, and therefore gn(x̄n)

is a convex combination of finitely many points yj with yj ∈ f(xnj ) and

||xnj − x|| ≤ ||xn

j − x̄n||+ ||x̄n − x|| < δ, implying that d(yj, f(x)) < ε. Thus

x̄n = gn(x̄n) =∑

j:||xnj −x||<δ

δnj (x̄n)∑

j δnj (x̄n)

ynj

with d(yj, f(x)) < ε and thus by claim 2,

d(x̄n, f(x)) ≤∑

j:||xnj −x||<δ

δnj (x̄n)∑

j δnj (x̄n)

d(ynj , f(x)) ≤ ε,

implying that

d(x, f(x)) ≤ ‖x− x̄n‖+ d(x̄n, f(x)) < 2ε.

As this last inequality holds for every ε > 0, d(x, f(x)) = 0, and as f(x) is

closed, x ∈ f(x).

6 Applications of Kaukutani’s f.p. theorem

We start with few remarks:

(i) If Fi is an upper semicontinuous set-valued function from X to Yi, i =

1, . . . , n, then (F1, . . . , Fn) is an upper semicontiuous set-valued function from

19

X to Y1 × . . .× Yn.

(ii) If Yi is a convex subset of a (real) vector space and Fi is a convex valued

set-valued function from X to Yi, i = 1, . . . , n, then (F1, . . . , Fn) is a convex

valued set-valued function from X to Y1 × . . .× Yn.

(iii) If g : X → Y is a continuous function, and F is an upper semicontinu-

ous set-valued function from Y to Z, then F ◦ g is an uppersemicontinuous

set-valued function from X to Z.

(iv) If Fi is an uppersemicontiuous set-valued function from Yi to Xi, i =

1, . . . , n, and πi is a continuous function from X to Xi, then (F1 ◦π1, . . . , Fn ◦

πn) is an uppersemicontinuous set-valued function from X to X1×, . . . , Xn.

(v) If Fi is a convex valued set-valued function from Yi to Xi, where Xi is

a convex subset of a real vector space, i = 1, . . . , n, and πi is a continuous

function from X to Yi, then (F1◦π1, . . . , Fn◦πn) is a convex valued set-valued

function from X to X1×, . . . , Xn.

Theorem 5 Let X1, . . . , Xn be compact convex subsets of Euclidean spaces,

and assume that fi are nonempty convex valued and uppersemicontinuous

set-valued functions from ×ni=1Xi → Xi. The (f1, . . . , fn) has a fixed point.

20

Proof. By remarks (i) and (ii), F = (f1, . . . , fn) is a convex valued up-

persemicontinuous set-valued function. As each fi in nonempty valued, F is

nonempty valued. As each Xi is convex and compact, so is ×ni=1Xi. There-

fore the set-valued function F from ×ni=1Xi to itself obey all the assumptions

of Kakutani’s fixed point theorem, and thus has a fixed point.

Lemma 1 Let X and Y be compact subsets of Euclidean spaces, and let

u : X × Y → IR be a continuous function. Then the set valued function F

from X to Y defined by

F (x) = {y ∈ Y : u(x, y) = maxz∈Y

u(x, z)},

is uppersemicontinuous.

Proof. Assume that xn ∈ X and yn ∈ Y , n = 1, . . . are sequences that

converge to x ∈ X and y ∈ Y respectively, and that yn ∈ F (xn). Let z ∈ Y .

As yn ∈ F (xn),

u(xn, yn) ≥ u(xn, z).

As u is continuous, u(xn, yn) → u(x, y) and u(xn, z) → u(x, z) as n → ∞,

and therefore

u(x, y) = limn→∞

u(xn, yn) ≥ u(x, z) = limn→∞

u(xn, z),

21

and as this holds for any z ∈ Y , y ∈ F (x), and thus F is uppersemicontinu-

ous.

Definition 7 Let X be a convex subset of a Euclidean space. A real valued

function f : X → IR is called quasi concave if for every α ∈ IR the set {x ∈

X : f(x) ≥ α} is convex. If Y is a set, a real valued function f : X×Y → IR

is called quasi concave in x if for every α ∈ IR and every y ∈ Y , the set

{x ∈ X : f(x, y) ≥ α} is convex.

Theorem 6 Let X1, . . . , Xn be compact convex subsets of Euclidean spaces,

and assume that u1, . . . , un are real valued quasi concave continuous function

defined on ×ni=1Xi. Then there is a point x = (x1, . . . , xn) ∈ ×n

i=1Xi such

that for every 1 ≤ i ≤ n and every yi ∈ Xi,

ui(x1, . . . , yi, . . . , xn) ≤ ui(x1, . . . , xi, . . . , xn) = ui(x).

Proof. For every i = 1, . . . , n define the set valued function Fi from ×ni=1Xi

to Xi by

Fi(x1, . . . , xn) = {yi ∈ Xi : ui(x1, . . . , yi, . . . , xn) = maxzi∈Xi

ui(x1, . . . , zi, . . . , xn)}.

Then, as X1, . . . , Xn are compact and ui is continuous, Fi is non empty valued

and uppersemicontinuous (Lemma 1). As X1, . . . , Xn are convex and ui is

22

quasi concave, Fi is convex valued. By remarks (i) and (ii) F = (F1, . . . , Fn)

is a convex valued and uppersemicontinuous, and as each Fi is nonempty

valued F is also non empty valued. Therefore, by Theorem 4 F has a fixed

point, i.e., there is a point x = (x1, . . . , xn) ∈ ×ni=1Xi such that for every i,

xi ∈ Fi(x), i.e., for every yi ∈ Xi,

ui(x1, . . . , yi, . . . , xn) ≤ ui(x1, . . . , xi, . . . , xn) = ui(x).

Definition 8 A set valued function f from X to Y is called lowersemicon-

tiuous if for every sequence xn ∈ X which converges to a point x ∈ X and

every y ∈ f(x), there is a sequence yn ∈ f(xn) which converges to y. It is

called continuous if it is uppersemicontinuous and lowersemicontinuous.

Lemma 2 Let X and Y be compact subsets of Euclidean spaces, and let

u : X × Y → IR be a continuous function, and G a continuous set-valued

function from X to Y . Then the set valued function F from X to Y defined

by

F (x) = {y ∈ G(x) : u(x, y) = maxz∈G(x)

u(x, z)},

is uppersemicontinuous.

23

Proof. Assume that xn ∈ X and yn ∈ F (xn) ⊂ Y , n = 1, . . ., are sequences

that converge to x ∈ X and y ∈ Y respectively. Recall that F (xn) ⊂

G(xn) and G is uppersemicontinuous, and therefore y ∈ G(x). Let z ∈

G(x). As G is a continuous set valued function, there is a sequence zn ∈

G(xn) that converges to z. As yn ∈ F (xn), u(xn, yn) ≥ u(xn, zn). As u

is continuous, u(xn, yn) → u(x, y) and u(xn, zn) → u(x, z) as n → ∞, and

therefore u(x, y) ≥ u(x, z), and as this holds for any z ∈ G(x), y ∈ F (x),

and thus F is uppersemicontinuous.

Given sets X1, . . . , Xn, an index 1 ≤ i ≤ n, an element x = (x1, . . . , xn)

in ×ni=1Xi, and an element yi in Xi, we denote by (x−i, yi) or by (x|yi) the

element (x1, . . . , xi−1, yi, xi+1, . . . , xn) in ×ni=1Xi.

Theorem 7 Let X1, . . . , Xn be non-empty convex compact subsets of Eu-

clidean spaces, X = ×ni=1Xi, and assume that ϕ1, . . . , ϕn are continuous

set-valued functions from X to X1, . . . , Xn respectively such that ϕi(x) is

non-empty and convex for every x ∈ X and 1 ≤ i ≤ n. If ui : X → IR are

continuous and quasi concave in xi, and Fi is the set-valued function from

X to Xi defined by

Fi(x) = {yi ∈ ϕi(x) : ui(x−i, yi) ≥ ui(x−i, zi) for every zi ∈ ϕi(x)},

24

then, the set-valued function (F1, . . . , Fn) from X to X has a fixed point.

Proof. Note that Fi is an uppersemicontinuous set-valued function from

X to Xi with non-empty convex values. Therefore, (F1, . . . , Fn) is an up-

persemicontinuous set-valued function with non-empty convex values and

thus by Kakutani’s fixed point theorem has a fixed point.

Lemma 3 Let ∆ = {p = (p1, . . . , pn) : pi ≥ 0 and∑n

i=1 pi = 1}, e ∈ IRn+

with ei > 0, and let Y be a convex subset of IRn with 0 ∈ Y . Then the

set-valued functions ϕ from ∆ to Y that is given by

ϕ(p) = {x ∈ Y : px =n∑

i=1

pixi ≤n∑

i=1

piei = pe}

is continuous and has non-empty convex values.

Proof. Assume that pk → p ∈ ∆ and xk → x ∈ Y as k →∞ and that pkxk =

∑ni=1 pk

i xki ≤ ∑n

i=1 pki ei = pke. Then it follows that limk→∞

∑ni=1 pk

i xki =

∑ni=1 pixi and limk→∞

∑ni=1 pk

i ei =∑n

i=1 piei and therefore

px =n∑

i=1

pixi ≤n∑

i=1

piei = pe, i.e., x ∈ ϕ(p),

proving that ϕ is uppersemecontinuous. Assume next that pk →k→∞ p ∈ ∆

and x ∈ ϕ(p). If∑n

i=1 pixi = px < pe =∑n

i=1 piei, then for sufficiently

large k,∑n

i=1 pki xi = pkx ≤ pke =

∑ni=1 pk

i ei, i.e., x ∈ ϕ(pk), and therefore

25

by setting xk = x we deduce that xk ∈ ϕ(pk) and xk →k→∞ x. Oth-

erwise, if px = pe, pkx →k→∞ pe > 0. Therefore, if εk is defined by

εk = max(0, (∑n

i=1 pki xi −

∑ni=1 pk

i ei))/∑n

i=1 pki xi, 0 ≤ εk →k→∞ 0. As Y is

convex and contains the points x and 0, xk = (1− εk)x ∈ Y . As εk →k→∞ 0,

xk →k→∞ x and by the definition of εk, xkpk ≤ pke and thus xk ∈ ϕ(pk).

Thus ϕ is lowersemicontinuous.

Lemma 4 Let ∆ = {p = (p1, . . . , pn) : pi ≥ 0 and∑n

i=1 pi = 1}, e ∈ IRn+

with ei > 0, and let Y be a convex subset of IRn that contains a neighborhood

of e and with 0 ∈ Y . Then the set-valued functions ϕ from ∆ to Y that is

given by

ϕ(p) = {x ∈ Y : px =n∑

i=1

pixi =n∑

i=1

piei = pe}

is continuous and has non-empty convex values.

Proof. Assume that pk → p ∈ ∆ and xk → x ∈ Y as k →∞ and that pkxk =

∑ni=1 pk

i xki =

∑ni=1 pk

i ei = pke. Then it follows that limk→∞∑n

i=1 pki x

ki =

∑ni=1 pixi and limk→∞

∑ni=1 pk

i ei =∑n

i=1 piei and therefore

px =n∑

i=1

pixi =n∑

i=1

piei = pe, i.e., x ∈ ϕ(p),

proving that ϕ is uppersemecontinuous. Assume next that pk →k→∞ p ∈ ∆

and x ∈ ϕ(p). Then, pkx →k→∞ px = pe > 0. Y contains a neighborhood

26

of e. Therefore there is α > 0 such that (1 + α)e ∈ Y . Let θk be defined

as inf{θ ≥ 0 | pk(θ(1 + α)e + (1 − θ)xk) ≥ pke}. For every θ > 0 we have

pk(θ(1+α)e+(1−θ)x) →k→∞ pe(1+α) > pe. Therefore, θk → 0 as k →∞.

Set yk = θk(1 + α)e + (1 − θk)x. (In other words, yk is the point on the

interval [x, (1+α)e] with pkyk ≥ pke that is the closest point to x.) Note that

yk →k→∞ x. Let εk be defined by εk = (∑n

i=1 pki y

ki −

∑ni=1 pk

i ei)/∑n

i=1 pki y

ki ,

0 ≤ εk →k→∞ 0. As Y is convex and contains the points x and 0, xk = (1−

εk)yk ∈ Y . As εk →k→∞ 0 and yk →k→∞ x, xk →k→∞ x and by the definition

of εk, xkpk ≤ pke and thus xk ∈ ϕ(pk). Thus ϕ is lowersemicontinuous.

27

7 Existence of Competitive Equilibria

Theorem 8 Let E = 〈T ; IR`; (X(t))t∈T ; (e(t))t∈T ;�t∈T 〉 be an exchange econ-

omy such that:

1. ∀t ∈ T , X(t) = [0, M ]` where M >∑

t∈T ei(t)

2. ∀t ∈ T and ∀1 ≤ i ≤ `, ei(t) > 0

3. ∀t ∈ T , the preference relation of trader t, �t, is represented by a contin-

uous and monotonic quasi concave utility function ut : IR` → IR.

Then, there exists a competitive equilibrium (p, x) = (p, x(1), . . . , x(n)) with

pi > 0 for every 1 ≤ i ≤ `.

Proof. Assume that T = {1, . . . , n}. Set X0 = ∆ = {p ∈ IR`+ |

∑`i=1 pi = 1},

and for t ∈ T , set Xt = X(t). The sets Xi, i = 0, 1, . . . , n, are non-empty

convex and compact subsets of Euclidean spaces. For every 0 ≤ t ≤ n we

define a set-valued function ϕt from X = ×ni=0Xi to Xt as follows:

ϕ0(p, x(1), . . . , x(n)) = ∆,

and for 1 ≤ t ≤ n,

ϕt(p, x(1), . . . , x(n)) = {y ∈ Xt | py ≤ pe(t)}.

By Lemma 3 the set valued functions ϕt, 1 ≤ t ≤ n, are continuous and

with non-empty and convex values. Obviously, the set-valued function ϕ0

28

is continuous and with non-empty and convex values. Define the set-valued

functions Fi : X → Xi, i = 0, 1, . . . , n, by:

F0(p, x(1), . . . , x(n)) = {q ∈ ∆ | qn∑

i=1

(x(t)− e(t)) ≥ rn∑

t=1

(x(t)− e(t)) ∀r ∈ ∆}

= arg maxq∈∆

qn∑

i=1

(x(t)− e(t)),

and for 1 ≤ i ≤ n,

Fi(p, x(1), . . . , x(n)) =

{y ∈ ϕi(p, x(1), . . . , x(n)) | ui(y) ≥ ui(z) ∀z ∈ ϕi(p, x(1), . . . , x(n))}.

Note that by Theorem 7 the set-valued function F = (F0, . . . , Fn) from X to

X has a fixed point. Let (p, x(1), . . . , x(n)) be a fixed point of F . We will

show that it is a competitive euilibrium. As x(i) ∈ Fi(p, x(1), . . . , x(n)) ⊂

ϕi(p, x),

px(i) ≤ pe(i) for every 1 ≤ i ≤ n, (1)

and therefore

p(n∑

i=1

(x(i)− e(i))) ≤ 0. (2)

Let f(i) denote the i-th unit vector in IR`. As p ∈ F0(p, x(1), . . . , x(n)), we

deduce that p(∑n

i=1(x(i) − e(i))) ≥ f(j)(∑n

i=1(x(i) − e(i))) =∑n

i=1(xj(i) −

ej(i)) for every 1 ≤ j ≤ `. Therefore, using (5), for every 1 ≤ j ≤ `,

∑ni=1(xj(i)− ej(i)) ≤ 0. In particular, if ε > 0 with ε < M −∑n

t=1 ej(t), then

29

x(t)+εf(j) ∈ Xt. By the monotonicity of ut we deduce that ut(x(t)+εf(j)) >

ut(x(t)). Therefore, as x(t) ∈ Ft(p, x), we deduce that

px(t) + εpj = p(x(t) + εf(j)) > pe(t) ≥ px(t) (3)

and thus we deduce that pj > 0, and as (6) holds for all sufficiently small

ε > 0, we deduce also that px(t) ≥ pe(t) for every t ∈ T which together with

(4) implies that for every t ∈ T ,

px(t) = pe(t).

Therefore, using p > 0 and the inequality∑

t∈T x(t) ≤ ∑t∈T e(t), we deduce

that∑

t∈T x(t) =∑

t∈T e(t). As x(i) ∈ Fi(p, x(1), . . . , x(n)) we conclude that

(p, x(1), . . . , x(n)) is a competitive equilibrium.

The assumption that for every t ∈ T and every 1 ≤ i ≤ ` we have

ei(t) > 0 is restrictive. It assumes that every trader has a strictly positive

quantity of every commodity. The next Theorem replaces this assumption

by the assumption that every commodity is present in the market, namely,

that for every 1 ≤ i ≤ ` we have∑

t∈T ei(t) > 0.

Theorem 9 Let E = 〈T ; IR`; (X(t))t∈T ; (e(t))t∈T ;�t∈T 〉 be an exchange econ-

omy such that:

1. ∀t ∈ T , X(t) = [0, M ]` where M >∑

t∈T ei(t)

30

2. ∀1 ≤ j ≤ `,∑

t∈T ej(t) > 0

3. ∀t ∈ T , the preference relation of trader t, �t, is represented by a contin-

uous and monotonic quasi concave utility function ut : IR` → IR.

Then, there exists a competitive equilibrium (p, x) = (p, x(1), . . . , x(n)) with

pj > 0 for every 1 ≤ j ≤ `.

Proof. Assume that T = {1, . . . , n}. Set X0 = ∆ = {p ∈ IR`+ |

∑`i=1 pi = 1},

and for t ∈ T , set Xt = [0, M ]`. The sets Xi, i = 0, 1, . . . , n, are non-empty

convex and compact subsets of Euclidean spaces. Set X = ×0≤i≤nXi, and

Bi(p) = {y ∈ [0, M ]` : py ≤ pe(t)}.

Define the set-valued functions Fi : X → Xi, i = 0, 1, . . . , n, by:

F0(p, x(1), . . . , x(n)) = {q ∈ ∆ | qn∑

i=1

(x(t)− e(t)) ≥ rn∑

t=1

(x(t)− e(t)) ∀r ∈ ∆}

= arg maxq∈∆

qn∑

i=1

(x(t)− e(t)),

and for 1 ≤ i ≤ n, if pe(i) > 0 then

Fi(p, x(1), . . . , x(n)) =

{y ∈ Bi(p) | ui(y) ≥ ui(z) ∀z ∈ Bi(p)}

and

Fi(p, x(1), . . . , x(n)) = Bi(p)

31

if pe(i) = 0.

The quasi concavity of ut implies that Ft is convex valued for 1 ≤ t ≤

n. Next we show that Fi are upper semi continuous with nonempty val-

ues. Assume (pk, xk(1), . . . , xk(n)) →k→∞ (p, x(1), . . . , x(n)). We have to

prove that p ∈ F0(p, x(1), . . . , x(n)) and that for every 1 ≤ t ≤ n we

have x(t) ∈ Ft(p, x(1), . . . , x(n)). Fix q ∈ ∆. Then q(∑

x(t) − ∑e(t)) =

limk→∞ q(∑

xk(t) − ∑e(t)) ≤ limk→∞ pk(

∑xk(t) − ∑

e(t)) = p(∑

x(t) −

∑e(t)) where the equalities follow from the continuity of the inner prod-

uct and from the assumptions that pk → p and xk(t) → x(t), and the in-

equality follows from the fact that pk ∈ F0(p, x(1), . . . , x(n)). Thus, p ∈

F0(p, x(1), . . . , x(n)). Next we show that x(t) ∈ Ft(p, x(1), . . . , x(n)). Note

that px(t) = lim pkxk(t) ≤ lim pke(t) = pe(t) and thus x(t) ∈ Bt(p) and

thus pe(t) = 0 implies that x(t) ∈ Ft(p, . . .). If pe(t) > 0, set yk = y if

pky ≤ pke(t) and yk = pke(t)pky

y if pky > pke(t). It follows that pkyk ≤ pke(t)

and yk → y. Therefore, for sufficiently large k we have ut(yk) > ut(x

k(t))

and pkyk ≤ pke(t) contradicting the assumption that xk(t) ∈ Ft(p, . . .). Thus

Ft is upper semi continuous.

Note that by Theorem 7 the set-valued function F = (F0, . . . , Fn) from X

to X has a fixed point. Let (p, x(1), . . . , x(n)) be a fixed point of F . We will

32

show that it is a competitive euilibrium. As x(i) ∈ Fi(p, x(1), . . . , x(n)) ⊂

Bi(p),

px(i) ≤ pe(i) for every 1 ≤ i ≤ n, (4)

and therefore

p(n∑

i=1

(x(i)− e(i))) ≤ 0. (5)

Let f(i) denote the i-th unit vector in IR`. As p ∈ F0(p, x(1), . . . , x(n)), we

deduce that p(∑n

i=1(x(i) − e(i))) ≥ f(j)(∑n

i=1(x(i) − e(i))) =∑n

i=1(xj(i) −

ej(i)) for every 1 ≤ j ≤ `. Therefore, using (5), for every 1 ≤ j ≤ `,

∑ni=1(xj(i)− ej(i)) ≤ 0. In particular, if ε > 0 with ε < M −∑n

t=1 ej(t), then

x(t) + εf(j) ∈ Xt.

Assume that 1 ≤ t ≤ n with pe(t) > 0. By the monotonicity of ut we

deduce that ut(x(t) + εf(j)) > ut(x(t)). Therefore, as x(t) ∈ Ft(p, x), we

deduce that

px(t) + εpj = p(x(t) + εf(j)) > pe(t) > 0 (6)

and thus we deduce that for every 1 ≤ j ≤ ` we have pj > 0. Therefore

(w.l.o.g.) pe(t) > 0 for every t. Thus (6) holds for all ε > 0.

33

As (6) holds for all sufficiently small ε > 0, we deduce also that px(t) ≥

pe(t) for every t ∈ T which together with (4) implies that for every t ∈ T ,

px(t) = pe(t).

Therefore, using p > 0 and the inequality∑

t∈T x(t) ≤ ∑t∈T e(t), we deduce

that∑

t∈T x(t) =∑

t∈T e(t). As x(i) ∈ Fi(p, x(1), . . . , x(n)) we conclude

that (p, x(1), . . . , x(n)) is a competitive equilibrium of the exchange economy

E = 〈T ; IR`; (X(t))t∈T ; (e(t))t∈T ;�t∈T 〉.

The next theorem replaces the assumption that X(t) = [0, M ]` where

M >∑

t∈T ei(t) with the assumption that ∀t ∈ T , X(t) is convex and

IR`+ ⊃ X(t) ⊃ [0, M ]` where M >

∑t∈T ei(t). We state and prove the result

for the the special case X(t) = IR`+. However, the same proof applies to the

general case.

Theorem 10 Let E = 〈T ; (X(t))t∈T ; (e(t))t∈T ; (�t)t∈T 〉 be an exchange econ-

omy with ` commodities such that:

1. ∀t ∈ T , X(t) = IR`+

2.∑

t∈T ei(t) > 0 for every 1 ≤ i ≤ `

3. ∀t ∈ T , the preference relation of trader t, �t, is represented by a con-

34

tinuous and monotonic quasi concave utility function ut : IR` → IR. Then,

there exists a competitive equilibrium (p, x) with pi > 0 for every 1 ≤ i ≤ `.

Proof. Let E∗ be the economy obtained from E by modifying the con-

sumption set IR` of each trader to the consumption set [0, M ]` where M =

2 maxi∑

t∈T ei(t). By the previous theorem, E∗ has a competitive equilibrium

(p, x) with p > 0. We claim that the competitive equilibrium (p, x) of E∗ is a

competitive equilibrium of E . As x is an allocation of E∗ it is also an alloca-

tion of E . It remains to show that if t ∈ T and y ∈ IR`+ with ut(y) > ut(x(t))

then py > pe(t). Indeed, if ut(y) > ut(e(t)), the continuity of ut implies that

there is a sufficiently small 1 > ε > 0 such that ut((1− ε)y) > ut(x(t)). Set

yε = (1−ε)y. If py ≤ pe(t) then pyε = (1−ε)py < pe(t) and for any 1 ≥ δ > 0

the point yε,δ = δyε + (1 − δ)x(t) obeys pyε,δ < pe(t) , and if δ > 0 is suffi-

ciently small, yε,δi < M . By the quasi concavity of ut, ut(yε,δ) ≥ ut(x(t)). As

ut is monotonic ut(yε,δ + θej) > ut(yε,δ) ≥ ut(x(t)) for every θ > 0 and every

1 ≤ j ≤ `. On the other hand, for sufficiently small θ > 0, yε,δ +θej ∈ [0, M ]`

contradicting the assumption that (p, x) is a competitive equilibrium of E∗.

Consider the following examples of exchange economies.

The set of traders is T = {1, 2} and the number of commodities is ` = 2.

35

The utilities of the traders are u1(x, y) = x + y and u2(x, y) =√

x + 2√

y.

What is the set of competitive equilibrium when e(1) = (1, 2) and e(2) =

(2, 1)?

Show that when e(1) = (1, 0) = e(2) there is no competitive equilibrium.

Show that there is no competitive equilibrium in the case e(1) = e(2) =

(1, 1), u1(x, y) = x2 + y2, and u2(x, y) =√

x +√

y.

8

Definition 9 An abstract social system consists of:

1. A finite set N

2. ∀i ∈ N a nonempty set Ai; set A = ×i∈NAi and A−i = ×j 6=iAj

3. ∀i ∈ N a set-valued function ϕi : A → Ai

4. ∀i ∈ N a set-valued function Pi : A → Ai.

The set Ai is interpreted as the possible actions of agent i, (e.g., in an

exchange economy it may stand for the consumption set). The set-valued

function ϕi represents the constrained feasible actions of agent i as a function

of the actions of all agents or all the other agents, (e.g., if we associate to

36

an exchange economy an additional agent whose action set is the simplex of

prices, the feasible actions of a trader is a consumption bundle in his budget

set). The set-valued function Pi is interpreted as the wishful actions of agent

i as a function of the N -tuple of actions.

Definition 10 An equilibrium of an abstract social system is an element

a ∈ A such that

Pi(a) ∩ ϕi(a) = ∅

Theorem 11 Let 〈N ; (Ai)i∈N ; (ϕi)i∈N ; (Pi)i∈N〉 be an abstract social system

such that:

1. ∀i ∈ N , Ai is a non-empty convex compact subset of a Euclidean space.

2. ∀i ∈ N , ϕi is a continuous set-valued function with nonempty convex

values.

3. ∀a ∈ A, ai /∈ coPi(a), and

4. ∀i ∈ N , the graph of Pi,

Γ(Pi) = {(a, b) ∈ A× Ai | b ∈ Pi(a)}

is an open subset of A× Ai. Then the abstract social system has an equilib-

rium.

We start with a lemma.

37

Lemma 5 Let K ⊂ IRm. Then any point in coK is a convex combination

of m + 1 points in K.

proof. Assume that x ∈ coK. Then x is a convex combination of finitely

many points in K, i.e., x can be written as x =∑k

i=1 aixi where xi ∈ K, ai > 0

and∑k

i=1 ai = 1. Let k be the smallest positive integer for which x can be

written as a convex combination of k points from K. Assume that k > n+1,

and let x =∑k

i=1 aixi where xi ∈ K, ai > 0 and∑k

i=1 ai = 1. It is sufficient

to prove that any other representation of x of the form, x =∑k

i=1 cixi where

xi ∈ K, ci ≥ 0 and∑k

i=1 ci = 1, obeys ci > 0 for every 1 ≤ i ≤ k. Define the

linear transformation T : IRk → IRm+1 by

T (b1, . . . , bk) = (k∑

i=1

bixi,k∑

i=1

bi).

The kernel of T , {b ∈ IRk | Tb = 0}, has dimension at least k− (m + 1) ≥ 1.

Therefore there is b ∈ IRk \ {0} with∑k

i=1 bixi = 0 and∑k

i=1 bi = 0. Set

a = (a1, . . . , ak) and ∆k = {c ∈ IRk | ∑ki=1 ci = 1 and ∀i ci ≥ 0}. Set

J = {j | bj < 0} and note that J is not empty. For every j ∈ J set

tj = −aj/bj. Then tj > 0 , aj + tjbj = 0, and for every 0 < t < tj,

aj + tbj > aj + tjbj = 0. Therefore, if t = min tj, a + tb ∈ ∆k, at least one

of the coordinates of a + tb vanishes, and∑k

i=1(a + tb)ixi = x contradicting

38

the minimality of k. (Alternatively, consider the half line starting in a in

the direction of b and let t = sup{s ≥ 0 | a + sb ∈ ∆k}. Note that ∆k is

convex and bounded and therefore t < ∞. As ∆k is closed a + tb ∈ ∆k and

as ai > 0 for every i it follows that t > 0. If (a + tb)i > 0 for every 1 ≤ i ≤ k

then there is t′ > t with a + t′b ∈ ∆k contradicting the definition of t. Thus

∑ki=1(a + tb)ixi is a representation of x as a convex combination of less than

k points from K.)

Lemma 6 Let X ⊂ IR` and Y ⊂ IRm be convex compact subsets, and assume

that F is an upper semicontinuous set-valued function from X to Y . Then

the set-valued function G from X to Y defined by G(x) = coF (x) is upper

semicontinuous.

Proof. Assume that xn → x ∈ X, yn ∈ G(xn) and yn → y. We have

to prove that y ∈ G(x). By the previous lemma, each yn is a convex

combination of m + 1 elements of F (xn). Therefore, for every n we can

write yn =∑m+1

i=1 ai(n)zi(n) where ai(n) ≥ 0,∑m+1

i=1 ai(n) = 1 and zi(n) ∈

F (xn). The sequence (a1(n), . . . , am+1(n), z1(n), . . . , zm+1(n)), n = 1, . . ., is

a bounded sequence in IRm+1+(m+1)m, and therefore has a subsequence that

converges, i.e. there is a sequence nk →k→∞ ∞ such that limk→∞ ai(nk) = ai

and limk→∞ zi(nk) = zi. It follows that ai ≥ 0 and∑m+1

i=1 ai = 1, and

39

limk→∞∑

i ai(nk)zi(nk) =∑

i aizi. As F is upper semicontinuous zi ∈ F (x)

and therefore∑

i aizi ∈ G(x).

9

We return now to the proof of the theorem. For every i ∈ N we define a

continuous function gi : A× Ai → IR+ such that:

∀x ∈ Pi(a), gi(a, x) > 0

∀x /∈ Pi(a), gi(a, x) = 0

E.g. we define gi(a, x) = dist((a, x), A × Ai \ Γ(Pi)). Note that the graph

of Pi is open and thus its complement in A× Ai is closed and therefore the

distance of (a, x) to A× Ai \ Γ(Pi) is positive (> 0) iff x ∈ Pi(a). For every

i ∈ N define a set-valued function Fi from A to Ai by:

Fi(a) = {x ∈ ϕi(a) | gi(a, x) = max{gi(a, y) | y ∈ ϕi(a)}}.

By lemma 2, Fi is uppersemicontinuous. Next we define a set-valued function

Gi from A to Ai by Gi(a) = coFi(a). Again by a previous result Gi is

upper semicontinuous. Also for every a ∈ A, Fi(a) is nonempty and thus

also Gi(a)is nonempty. Therefore letting G(a) = ×i∈NGi(a), G is an upper

40

semicontinuous set-valued function with non empty convex values from A to

itself and therefore has (by Kakutani’s fixed point theorem) a fixed point,

i.e., there is a∗ ∈ A with a∗ ∈ G(a∗). We will show next that this point a∗

is an equilibrium of the abstract social system. Thus we have to prove that

a∗i ∈ ϕi(a∗) and that ϕi(a

∗) ∩ Pi(a∗) = ∅. Indeed,

a∗i ∈ Gi(a∗) = coFi(a

∗) ⊂ co ϕi(a∗) = ϕi(a

∗)

and thus a∗i ∈ ϕi(a∗). If ϕi(a

∗) ∩ Pi(a∗) 6= ∅, there is x ∈ ϕi(a

∗) ∩ Pi(a∗)

and therefore gi(a∗, x) > 0 implying that Fi(a

∗) ⊂ Pi(a∗) and therefore

Gi(a∗) ⊂ coPi(a

∗) which together with a∗i ∈ Gi(a∗) imply that a∗i ∈ coPi(a

∗)

which contradicts the assumption of the theorem.

Definition 11 An exchange economy with externalities consists of:

1. A set of traders T ,

2. A positive integer `, representing the number of commodities.

3. For every t ∈ T a subset X(t) ⊂ IR` — the consumption set of trader t.

4. For every t ∈ T , a element e(t) ∈ X(t) — the initial endowment of trader

t.

5. For every t ∈ T a set-valued function Pt from ∆ × ×t∈T X(t) to X(t)—

the preference of trader t given the vector of prices and the consumption of

41

each agent.

Definition 12 A competitive equilibrium of an exchange economy with ex-

ternalities, E = 〈T, (X(t))t∈T , (e(t))t∈T , (Pt)t∈T 〉, is an ordered pair (x∗, p∗)

where p∗ ∈ ∆ and x∗ : T → IR` are such that:

1) ∀t ∈ T , x∗(t) ∈ X(t),

2)∑

t∈T x∗(t) ≤ ∑e(t),

3) ∀t ∈ T , p∗x∗(t) = p∗e(t),

4) ∀t ∈ T Pt(x∗, p) ∩ {y ∈ X(t) | p∗y = p∗e(t)} = ∅.

Theorem 12 Let E = 〈T, (X(t))t∈T , (e(t))t∈T , (Pt)t∈T 〉 be an exchange econ-

omy with externalities, such that:

(0) T is finite,

(1) X(t) = IR`+,

(2) 0 < e(t) ∈ IR`+, with ei(t) > 0 ∀1 ≤ i ≤ `,

(3)the graph of the set-valued function Pt : ×t∈T X(t)×∆ →→ X(t) is open,

(4) ∀((x(t))t∈T , p) ∈ ×j∈T X(t)×∆, x(t) /∈ coPt((x(t)), p).

Then there is p∗ ∈ ∆ and x∗ ∈ X = ×i∈T X(t) such that:

(a)∑

x(t)∗ ≤ ∑e(t),

(b) ∀t ∈ T , p∗x∗(t) = p∗e(t),

42

(c) ∀t ∈ T , Pt(x∗, p) ∩ {y ∈ X(t) | p∗y = p∗e(t)} = ∅.

Proof. We construct an abstract social system whose equilibrium points

correspond to those of the economy E . Assume that T = {1, . . . , n}, then

N = {0, 1, . . . , n}, where we imagine player 0 as “the price maker”. A0 = ∆,

and for 1 ≤ i ≤ n, Ai = [0, M ]` where M is a sufficiently large constant, e.g.,

M > max`j=1

∑ni=1 ej(i). For i = 0 we define ϕ0 by

ϕ0(∗) = ∆,

and for i = 1, . . . , n,

ϕi(x1, . . . , xn, p) = {y ∈ Ai | py = pe(i)}.

Define P̂i, i = 0, 1, . . . , n, by

P̂0(x1, . . . , xn, p) = {q ∈ ∆ | q(∑

xi −∑

e(i)) > p(∑

xi −∑

e(i))},

and for i = 1, . . . , n,

P̂i(x1, . . . , xn, p) = Pi(x1, . . . , xn, p) ∩ Ai.

The abstract social system S(M) := 〈N ; (Ai)i∈N ; (ϕi); (P̂i)〉 satisfies:

a) N is finite,

b) ∀0 ≤ i ≤ n, Ai is a convex and compact subset of a Euclidean space,

43

c.1) ϕ0 is a set-valued function with a constant nonempty compact convex

value (∆), and thus is a continuous set-valued function with convex values,

c.2) ∀1 ≤ i ≤ n, ϕi is a continuous set-valued function with nonempty convex

values (by lemma 4)

d.1) as P̂i(a) ⊂ Pi(a) and ai /∈ coPi(a), we have ai /∈ coP̂i(a)

d.2) as P̂0(x1, . . . , xn, p) is convex and p /∈ P̂0(x1, . . . , xn, p) we deduce that

p /∈ coP̂0(x1, . . . , xn, p),

e) ∀0 ≤ i ≤ n, Γ(P̂i) is open in A×∆× Ai (in the relative topology).

Therefore, the abstract social system 〈N ; (Ai)i∈N ; (ϕi); (P̂i)〉 satisfies all the

conditions of the previous theorem and thus has a fixed point (x∗, p∗).

We show that this is an equilibrium of S(M) = 〈T, ([0, M ]`), (ei), (Pi)i∈T 〉.

As x∗(i) ∈ ϕi(x∗, p∗), p∗x∗i = p∗e(i). Therefore

∑i p

∗x∗i =∑

i p∗e(i) and

thus p∗(∑

i x∗i −

∑i e(i)) = 0. If there is j with (

∑i x

∗i )j > (

∑i ei)j, set-

ting δj = (0, . . . , 1, 0 . . . , 0), δj(∑

i x∗i −

∑i ei) > 0 = p∗(

∑i x

∗i −

∑i ei)

and therefore δj ∈ ϕ0(x∗, p∗) ∩ P0(x

∗, p∗) = ∅, a contradiction. Therefore,

∑i x

∗i ≤

∑i e(i). Obviously, x∗i ∈ ϕi(x

∗, p) implies that x∗i ∈ [0, M ]`, and

as ϕi(x∗, p) ∩ P̂i(X

∗) = ∅ we deduce that for every i ∈ T , Pi(x∗, p∗) ∩ {y ∈

[0, M ]` | p∗y = p∗e(i)} = ∅. Thus (x∗, p∗) is an equilibrium of E(M).

44

Let (x(M), p(M)) be competitive equilibria of the economy E(M). Then

x(M) = (x1(M), . . . , xn(M)) ∈ [0, M ]`n and p(M) ∈ ∆. As both sets,

[0, M ]`n and ∆ are compact, there is a sequence (Mk)∞k=1 such that

Mk →∞ as k →∞,

x(Mk) → x ∈ IR`n as k →∞,

and

p(Mk) → p ∈ ∆ as k →∞.

As∑n

i=1 e(i) ≥ ∑ni=1 xi(Mk) →k→∞

∑ni=1 xi, x is a suballocation.

As pxi = limk→∞ p(Mk)xi(Mk) = limk→∞ p(Mk)e(i) = pe(i), we deduce that

pxi = pe(i). In order to prove that indeed (x, p) is a competitive equilibrium

of E we have to show further that there is no i ∈ T and yi ∈ IR`+ such that

pyi = pe(i) and yi ∈ Pi(x, p). Assume that yi ∈ IR`+ with pyi = pe(i) and

yi ∈ Pi(x, p). Let yi(k) be a sequence such that yi(k) → yi as k → ∞ and

p(Mk)yi(k) = p(Mk)e(i). E.g., yi(k) = p(Mk)e(i)

p(Mk)yi yi. As Pi is continuous, i.e.,

Γ(Pi) is open, it will follow that there is a sufficiently large k, such that

yi(k) ∈ Pi(x(Mk), p(Mk)) ∩ [0, Mk]` = P̂i(x(Mk), p(Mk)) contradicting the

fact that (x(Mk), p(Mk)) is an equilibrium of S(Mk).

45

10 Sard’s Lemma

A rectangular parallelepiped in IRn is a set of the form I = ×ni=1[ai, bi]. Its

volume, vol I, is defined as Πni=1(bi − ai). A subset V of IRn is a set of

measure 0 if for every ε > 0 there is a sequence of rectangular parallelopipeds,

Ik = ×ni=1[a

ki , b

ki ] which cover V , i.e., such that V ⊂ ∪∞k=1Ik and the sum of

their volumes is less then ε, i.e.,∑∞

k=1 Πni=1(b

ki − ak

i ) < ε.

A countable union of sets of measure 0 is a set of measure 0. Indeed, if Vj,

j = 1, . . . is a sequence of subsets of IRn having measure 0, for every ε > 0

and every j ≥ 1, there is a sequence of rectangular parallelopiped Ij,k such

that Vj ⊂ ∪∞k=1Ij,k and∑∞

k=1 volIj,k =∑∞

k=1 Πni=1(b

j,ki − aj,k

i ) < ε2−j. Then

∪∞j=1Vj ⊂ ∪∞j=1∪∞k=1 Ij,k and∑∞

j=1

∑∞k=1 volIj,k =

∑∞j=1

∑∞k=1 Πn

i=1(bj,ki −aj,k

i ) <

ε, and therefore ∪∞j=1Vj is a set of measure 0.

A function f : U → IRn where U is an open subset of IRn is called C1 if

it has continuous partial derivatives. The Jacobian of f at x ∈ U is the

determinant of the n×n matrix J(x) where Ji,j(x) = ∂fi

∂xj(x). A critical point

(of f) is a point x ∈ U with det J(x) = 0. A critical value is a point of the

form f(x) where x is a critical point. A regular value is a point y ∈ IRn which

is not a critical value.

46

Theorem 13 (Sard’s Lemma) . Let f : U → IRn be a C1 function where

U is an open subset of IRn. Then the set of critical values of f has measure

0.

Proof. For every x ∈ IRn we denote maxni=1 |xi| by ‖x‖. Assume first that

[0, 1]n ⊂ U , and we will prove that the set, {f(x) : x ∈ [0, 1]n with det J(x) =

0} has measure 0.

For every x ∈ IRn and α > 0 we denote by I(x, α) the cube {y ∈ IRn : ∀1 ≤

i ≤ n, |yi − xi| ≤ α}.

Fix ε > 0.

For every 1 ≤ i ≤ n, fi(y) − fi(x) =∑

j Jij(x + θi(y − x))(yj − xj) for

some 0 < θi < 1 and therefore, as J(x) is continuous in the compact set

[0, 1]n it is uniformly continuous there, and thus there is δi > 0 such that

|Jij(x + θ(y − x))− Jij(x)| < ε/n whenever ‖x− y‖ < δi and 0 < θ < 1 and

therefore |fi(y) − fi(x) − Ji(x)(y − x)| < ε‖y − x‖ whenever ‖x − y‖ < δi.

Therefore, there is δ > 0 (e.g. δ = min δi) such that for every x, y ∈ [0, 1]n

with ‖x− y‖ < δ, ‖f(x)− f(y)− J(y)(x− y)‖ < ε‖x− y‖.

There is a sufficiently large constant K, such that for every x, y ∈ [0, 1]n,

‖f(x)−f(y)‖ < K‖x−y‖. Let k and ` be two positive integers with k > δ−1

and K/ε < ` ≤ 1 + K/ε . Note that for any two points x, y ∈ [0, 1]n

47

with ‖x − y‖ ≤ 1/(k`), ‖f(x) − f(y)‖ < ε/k. Define for every 1 ≤ i ≤ n,

Ai = {x ∈ [0, 1]n : kxi ∈ ZZ and ∀1 ≤ j ≤ n, k`xj ∈ ZZ} and A = ∪Ai.

Note that the number of points in Ai is ≤ (k + 1)(k` + 1)n−1 ≤ 2n`n−1kn

and thus the number of points in A is ≤ n(k + 1)(k` + 1)n−1 ≤ n2n`n−1kn.

Assume that x0 ∈ [0, 1]n with det J(x0) = 0. As det J(x0) = 0, the kernel

of the linear transformation J(x0) : IRn → IRn is nonempty, i.e., there is

z ∈ IRn with z 6= 0 and J(x0)z = 0. W.l.o.g. assume that x0j ≤ 1/k.

Therefore for any point y on the line {x0 + tz : t ∈ IR}, J(x0)(y − x0) = 0

and therefore, there is x1 in the boundary of [0, 1/k]n with J(x0)(x1−x0) = 0,

and therefore in particular ‖f(x1)− f(x0)‖ ≤ ε/k, and there is x2 ∈ A with

‖x2 − x1‖ ≤ 1/(k`), and therefore in particular ‖f(x2) − f(x1)‖ ≤ K/(k`).

Therefore,

‖f(x0)−f(x2)‖ ≤ ‖f(x0)−f(x1)‖+‖f(x1)−f(x2)‖ ≤ ε/k+K/(k`) < 2ε/k.

Therefore, f(x0) ∈ I(f(x2), 2ε/k). Therefore the set of critical values (in

f([0, 1]n)) is contained in ∪y∈AI(y, 2ε/k) and∑

y∈A volI(y, 2ε/k) ≤ |A|(4ε/k)n ≤

n2n`n−1kn(4ε/k)n ≤ n8n`n−1(ε)n < n8nKnε.

Next assume that x ∈ U and δ > 0 are such that I(x, δ) = {y ∈ IRn :

‖y − x‖ ≤ δ} ⊂ U . The function g : U → IRn defined by gi(z) =

(z − x)/2δ + 1/2 maps I(x, δ) onto [0, 1]n and has a nonvanishing Jaco-

48

bian. Therefore, {f(z) : z ∈ I(x, δ) with det J(z) = 0} = {f ◦ g−1(y) : y ∈

[0, 1]n with det J(f ◦ g−1)(y) = 0} has measure zero by the first part of our

proof.

Next we show that any open set U is the (countable) union of all (rational)

cubes I(x, δ) with x ∈ IQn and δ ∈ IQ which are subsets of U . Indeed, given

x ∈ U there is α > 0 such that I(x, α) ⊂ U . Let δ ∈ IQ with δ < α/2 and

y ∈ IQn with ‖y − x‖ < δ. Then x ∈ I(y, δ) ⊂ I(x, α) ⊂ U which proves our

claim. As the set of all rational cubes which are subsets of U , is a countable

collection of sets which cover U , the set of critical values has measure 0.

11 Generic finiteness of Competitive Equilib-

ria

In the previous sections the models of an exchange economy included as a

basic ingredient the preference relations of the individuals, and the resulting

income as a function of prices (pe(t)) and the demand set-valued functions of

each individual were derived. In the present section we consider a model in

which demand functions are part of the description of the exchange economy.

We consider here a model of an exchange economy which consists of:

49

1. A finite set of traders, T = {1, . . . , n},

2. A finite number of commodities, `,

3. For every t ∈ T , an initial bundle e(t) ∈ IR`++,

4. For every t ∈ T , a demand function δt : ∆× IR++ → IR`++ which satisfies

pδt(p, y) = y.

The demand function δt represents the demand of trader t as a function of

the price vector p ∈ ∆ and his income y ∈ IR++. The condition pδt(p, y) = y

asserts that trader t balances his budget.

A Competitive equilibrium price vector, or an equilibrium price vector for

short, of the economy E = (T ; `; (e(t))t∈T ; (δt)t∈T ) is a price vector p ∈ ∆

such that

∑t∈T

δt(p, pe(t)) =∑t∈T

e(t).

We will state and prove a result that asserts that given demand functions

which satisfy suitable conditions (e.g. continuously differentiable), for almost

all initial endowments, (e(t))t∈T , the exchange economy has finitely many

competitive equilibria.

Theorem 14 Assume that the demand functions δt are continuously dif-

ferentiable and for every y0 > 0, ‖δ1(p, y)‖ → ∞ as p → ∂∆ uniformly in

y ≥ y0, i.e., for every K > 0 there is ε > 0 such that for every y ≥ y0 and ev-

50

ery p ∈ ∆ with min`i=1 pi < ε, ‖δ1(p, y)‖ > K. Then, the set of e(1), . . . , e(n)

(viewed as a subset of IRn`) for which there are infinitely many competitive

equilibria price vectors p ∈ int∆ is a subset of a closed set of measure 0.

Proof. The idea of the proof is as follows. We construct a C1 function

F : int∆× IR++ × IR(n−1)`++ → IRn`

++ such that p is a competitive equilibrium

price vector of (e(1), . . . , e(n)) if and only if

F (p, pe(1), e(2), . . . , e(n)) = (e(1), . . . , e(n)).

The set U = int∆×IR++×IR(n−1)`++ is an open subset of IRn` and F : U → IRn`

is continuously differentiable and therefore by Sard’s lemma the set of critical

values has measure zero. If (e(1), . . . , e(n)) is a regular value and p is a

competitive equilibrium price vector for (e(1), . . . , e(n)), then

F (p, pe(1), e(2), . . . , e(n)) = (e(1), . . . , e(n)),

and

det J(F )(p, pe(1), e(2), . . . , e(n)) 6= 0.

Therefore, in a neighborhood of (p, pe(1), e(2), . . . , e(n)), F is 1 − 1, and

therefore for any price vector q which is sufficiently close to the price vector

p, F (q, qe(1), e(2), . . . , e(n)) 6= (e(1), . . . , e(n)) and thus any price vector q,

51

which is sufficiently close to the price vector p, is not an equilibrium price

vector. We turn to the formal prove.

Set U = int∆× IR++× IR(n−1)`++ and observe that U is an open subset of IRn`.

Define F : U → IRn` by: F = (F1, . . . , Fn) where Fi : U → IR` is given by

F1(p, y, z2, . . . , zn) = δ1(p, y) +n∑

t=2

δt(p, pzt)−n∑

t=2

zt,

and for t = 2, . . . , n,

Ft(p, y, z2, . . . , zn) = zt.

Claim 1: the price vector p ∈ int∆ is a competitive equilibrium price vector

of the economy ((δt)t∈T ; (e(t))t∈T iff

F1(p, pe(1), e(2), . . . , e(n)) = e(1),

and this holds iff

F (p, pe(1), e(2), . . . , e(n)) = (e(1), . . . , e(n))

(and this holds iff there is y ∈ IR++ such that

F (p, y, e(2), . . . , e(n)) = (e(1), . . . , e(n)) )

Proof: p is an equilibrium price vector iff∑n

t=1 δt(p, pe(t)) =∑n

t=1 e(t) which

holds iff F1(p, pe(1), e(2), . . . , e(n)) =∑n

t=1 δt(p, pe(t)) −∑n

t=2 e(t) = e(1).

52

The second iff is obious. If F (p, y, e(2), . . . , e(n)) = (e(1), . . . e(n), then

pF1(p, y, e(2), . . . , e(n)) = pδ1(p, y) +∑n

t=2 pδt(p, pe(t))−∑n

t=2 pe(t) = pe(1).

As pδt(p, pe(t)) = pe(t) and pδ1(p, y) = y we deduce that y = pe(1). This

completes the proof of claim 1. We prove next that if (e(1), . . . , e(n)) is a reg-

ular value, any competitive equilibrium price vector p ∈ int∆ is an isolated

equilibrium price vector. Otherwise, for any ε > 0 there is a price vector

q 6= p with ‖q − p‖ < ε and

F (p, pe(1), e(2), . . . , e(n)) = (e(1), . . . , e(n)) = F (q, qe(1), e(2), . . . , e(n))

which contradicts the fact that F is 1−1 in a sufficiently small neighborhood

of p.

Next we prove that there is ε > 0 such that any equilibrium price vector p

obeys min`i=1 pi > ε. Indeed, if y0 = min`

i=1 ei(1), then pe(1) ≥ y0 for every

p ∈ ∆. Thus, if ε > 0 is sufficiently small so that ‖δ1(p, y)‖ >∑n

t=1 ‖e(t)‖

whenever y ≥ y0 and min`i=1 pi ≤ ε, there is no equilibrium price vector p ∈ ∆

with min`i=1 pi ≤ ε.

Finally, we show that the set of critical values of F is a closed subset of

IRn`++. Let ek = (ek(1), . . . , ek(n)) ∈ IRn`

++ be a sequence of critical values

which converges as k → ∞ to (e(1), . . . , e(n)) ∈ IRn`++. Thus, there is a

53

sequence of (pk, yk) such that

F (pk, yk, ek(2), . . . , ek(n)) = (ek(1), . . . , ek(n)) →k→∞ (e(1), . . . , e(n)) ∈ IRn`++

and

det J(F )(pk, yk, ek(2), . . . , ek(n)) = 0.

As the price simplex ∆ is compact, we may assume W.l.o.g. that the sequence

(pk)∞k=1 converges in ∆; (otherwise we take a subsequence). Assume that

pk → p ∈ ∆ as k → ∞. We show now that the limiting price vector p is in

int∆. On the one hand, as F1(pk, yk, ek(2), . . . , ek(n)) = ek(1),

pkF1(pk, yk, ek(2), . . . , ek(n)) = pkek(1).

On the other hand, as

F1(pk, yk, ek(2), . . . , ek(n) = δ1(p

k, yk) +n∑

t=2

δt(pk, pke(t))−

n∑t=2

ek(t),

and pk ∑nt=2 δt(p

k, pke(t)) = pk ∑nt=2 ek(t),

pkF1(pk, yk, ek(2), . . . , ek(n)) = pkδ1(p

k, yk) = yk.

Therefore, yk = pkek(1) →k→∞ pe(1) ≥ minni=1 ei(1) > 0. Setting y0 =

minni=1 ei(1)

2> 0 we deduce that for sufficiently large k, yk > y0. Setting

K = 2∑

t∈T ‖e(t)‖ we deduce that for sufficiently large k,∑

t∈T ‖ek(t)‖ < K.

54

By assumption, there is ε > 0, such that if minni=1 pk

i < ε, and yk ≥ y0,

‖δ1(pk, yk)‖ > K which proves that minn

i=1 pki ≥ ε for sufficiently large k and

thus minni=1 pi ≥ ε. Therefore, p ∈ int∆. Therefore,

(pk, yk, ek(2), . . . , ek(n)) →k→∞ ((p, pe(1)), e(2) . . . , e(n)) ∈ IRn`++,

F (p, pe(1), e(2), . . . , e(n)) = (e(1), . . . , e(n)),

and

0 = det J(F )(pk, yk, ek(2), . . . , ek(n)) →k→∞ det J(F )(p, pe(1), . . . , e(n))

and thus (e(1), . . . , e(n)) is a critical value of F .

12 The Equivalence Principle

The equivalence principle asserts that in large economies any core allocation

is ‘almost’ a competitive equilibrium.

Before stating a theorem to that effect, we introduce few preliminaries from

convexity. Given subsets A and B of IRn their sum A + B is defined by

A + B = {a + b | a ∈ A, b ∈ B}. Note that if both A and B are convex

so is A + B. Indeed, if a, a′ ∈ A and b, b′ ∈ B and 0 ≤ α ≤ 1, then

α(a + b) + (1 − α)(a′ + b′) = αa + (1 − α)a′ + αb + (1 − α)b′ and thus

55

α(a + b) + (1−α)(a′ + b′) ∈ A + B whenever A and B are convex. Similarly,

for any subsets A1, . . . , Ak of IRn we define∑k

i=1 Ai = {∑ki=1 ai | ai ∈ Ai}, or

equivalently,∑k

i=1 Ai =∑k−1

i=1 Ai + Ak. Thus by induction∑k

i=1 Ai is convex

whenever each of the sets Ai is convex. Therefore, for any subsets A1, . . . , Ak

of IRn,∑k

i=1 coAi is convex. On the other hand∑k

i=1 Ai ⊂∑k

i=1 coAi, and

therefore co∑k

i=1 Ai ⊂∑k

i=1 coAi. On the other hand, any point z ∈ coA1 +

coA2 has a representation z = x1 + x2 with xi =∑ni

j=1 αijx

ij, where xi

j ∈ Ai,

i = 1, 2, and αi = (αi1, . . . , α

ini

) ∈ ∆ni . Therefore,

z = x1 + x2 =n1∑

j=1

n2∑`=1

α1jα

2`(x

1j + x2

`)

is a convex combination of points from A1 + A2, and therefore co(A1) +

co(A2) ⊂ co(A1 + A2) and by induction on k,∑k

i=1 coAi ⊂ co∑k

i=1 Ai, and

thus

cok∑

i=1

Ai =k∑

i=1

coAi.

Theorem 15 (Shapley Folkman) Let A1, . . . , Ak be subsets of En. Then

any vector z ∈ ∑ki=1 coAi is a sum z =

∑ki=1 yi where ∀1 ≤ i ≤ k, yi ∈ coAi

with yi =∑ni

j=1 αija

ij where ai

j ∈ Ai, αij ≥ 0 and

∑nij=1 αi

j = 1, such that

∑ki=1 ni ≤ n + k, and thus in particular, |{i : yi 6∈ Ai}| ≤ n.

56

Proof. As z ∈ ∑ki=1 coAi, z is a sum z =

∑ki=1 z(i) where ∀1 ≤ i ≤ k,

z(i) ∈ coAi, and thus each z(i) is a convex combination of finitely many

elements from Ai, i.e, there are αij > 0 with

∑nij=1 αi

j = 1, and ai(j) ∈ Ai, such

that z(i) =∑ni

j=1 αijai(j). Assume that this representation minimizes

∑ki=1 ni.

It is sufficient to prove that then∑k

i=1 ni ≤ k +n. Define T : IR∑k

i=1ni → IRn

by

T (b11, . . . , b

1n1

, . . . , bk1, . . . , b

knk

) =k∑

i=1

ni∑j=1

bijai(j).

The kernel of T , {b ∈ IR∑k

i=1ni | Tb = 0} has dimension at least

∑ki=1 ni− n,

and V = {b ∈ IR∑k

i=1ni | ∀1 ≤ i ≤ k,

∑nij=1 bi

j = 0} is a subspace of dimension

∑ki=1 ni − k. Therefore, if

∑ki=1 ni > k + n, there is b ∈ V \ {0} with Tb = 0.

Set J = {(i, j) | 1 ≤ i ≤ k, 1 ≤ j ≤ ni and bij < 0} and note that J is not

empty. For every (i, j) ∈ J set tij = −αij/b

ij. Then tij > 0, αi

j + tijbij = 0, and

for every 0 < t < tij, αij + tbi

j > 0. Therefore, if t = min{tij | (i, j) ∈ J}, for

every 1 ≤ i ≤ k, αi + tbi ∈ ∆ni , and at least one of the coordinates of α + tb

vanishes, and z =∑k

i=1

∑nij=1(α

ij + tbi

j)ai(j), contradicting the minimality of

∑ki=1 ni.

The Shapley-Folkman theorem implies in particular that the sum of a

large number of subsets of [0, 1]n is almost convex, by asserting that any

point in the convex hull of such a sum is within a fixed bounded distance

57

from a point of the sum. Moreover,

Corollary 1 Let Ki, i = 1, . . . , k, be subsets of IRn and denote by di the

diameter of Ki, i.e., di = max{‖x− y‖ | x, y ∈ Ki}. Then, if∑n

j=1 dij ≤ M ,

for every i1 < i2 < . . . < in, then for every z ∈ co∑k

i=1 Ki there is y ∈

∑ki=1 Ki with ‖y − z‖ ≤ M .

We need an additional classical result, regarding the separation of convex

sets. Recall that for two vectors, x = (x1, . . . , xn) and y = (y1, . . . , yn) in

IRn, the inner product of x and y is defined as xy =∑n

i=1 xiyi, and that the

inner product obeys the following properties:

∀x, y, z ∈ IRn (x + y)z = xz + yz

and

∀x, y ∈ IRn ∀α ∈ IR (αx)y = α(xy).

Theorem 16 Let K and C be two nonempty convex closed subsets of IRn

where one of them, say K, is compact, and with empty intersection, i.e.,

K ∩ C = ∅. Then there is p ∈ IRn with

sup{px : x ∈ C} < inf{py : y ∈ K}

58

Proof. Let α = inf{(y − x)(y − x) : y ∈ K and x ∈ C}. For every positive

integer k, let y(k) ∈ K and x(k) ∈ C with

α ≤ (y(k)− x(k))(y(k)− x(k)) ≤ α + 1/k.

As C is compact, there is a subsequence (nk)∞k=1 of the sequence of positive

integers, for which

x(nk) → x ∈ C as k →∞

It follows that y(nk) ∈ K is a bounded sequence (|yi(nk)| ≤ |yi(nk)−xi(nk)|+

|xi(nk)−xi|+|xi| and thus lim supk→∞ |yi(nk)| ≤ |xi|+α1/2) and as K is closed

we may assume without loss of generality, by possible taking a subsequence,

that

y(nk) → y ∈ K as k →∞.

Therefore, (y − x)(y − x) = limk→∞(y(nk) − x(nk))(y(nk) − x(nk)), and

α ≤ (y(nk)− x(nk))(y(nk)− x(nk)) ≤ α + 1/nk →k→∞ α, and thus

(y − x)(y − x) = α.

As K ∩ C = ∅, x 6= y and thus α > 0. Assume that z ∈ K. Then for every

0 ≤ t ≤ 1, tz + (1− t)y ∈ K. Therefore, the function f : [0, 1] → IR defined

by

f(t) = (tz+(1−t)y−x)(tz+(1−t)y−x) = (t(z−y)+y−x)(t(z−y)+y−x)

59

= (y − x)(y − x) + 2t(z − y)(y − x) + t2(z − y)(z − y)

is differentiable at 0, with f ′(0) = 2(z − y)(y − x). Therefore, as f(0) =

α ≤ f(t), (tz + (1 − t)y ∈ K), the derivative at 0 is nonnegative, i.e.,

(z − y)(y − x) = z(y − x)− y(y − x) ≥ 0, implying that

z(y − x) ≥ y(y − x).

Similarly, for every z ∈ C,

z(y − x) ≤ x(y − x).

As y(y − x)− x(y − x) = (y − x)(y − x) > 0,

y(y − x) > x(y − x)

and therefore

sup{px : x ∈ C} ≤ x(y − x) < y(y − x) ≤ inf{py : y ∈ K}.

which completes the proof of the theorem.

Theorem 17 (Anderson, 1979) Let E = 〈T ; IR`+; (e(t))t∈T ; (�)t∈T 〉 be an

exchange economy with ` commodities with weakly monotonic preferences,

i.e., x �t y whenever x >> y and if x �t y and z >> 0, then x + z �t y.

60

Then, setting

M = max{∑t∈S

‖e(t)‖ : S ⊂ T with |S| ≤ `},

for any core allocation x of E, there is a price vector p ∈ ∆, for which:

1

|T |∑t∈T

|p(x(t)− e(t))| ≤ 2M

|T |(7)

and

1

|T |∑t∈T

− inf{p(y − x(t)) : y �t x(t)} ≤ 2M

|T |(8)

Proof. Assume that x is a core allocation. For every t ∈ T , set

V (t) = {y − e(t) : y �t x(t)} ∪ {0},

V =∑t∈T

V (t)

Let u = (1, . . . , 1) denote the vector in IR` with all of its coordinates are

equal to 1. We will prove that

−Mu− IR`++ ∩ coV = ∅, (9)

i.e., that for every v ∈ coV there is 1 ≤ i ≤ n with vi ≥ −M . Assume that

v ∈ coV . By the Shapley Folkman theorem, there are elements z(t) ∈ coV (t)

such that

v =∑t∈T

z(t),

61

and the number of elements in the set T̂ = {t ∈ T : z(t) /∈ V (t)} it less than

or equal to `. Set T̄ = T \ T̂ . Note that for every z ∈ V (t), z ≥ −e(t), i.e.,

V (t) ⊂ IR`+ − e(t). As IR`

+ − e(t) is convex it contains also coV (t), i.e., for

every z ∈ coV (t), z ≥ −e(t), and therefore

∑t∈T̂

z(t) ≥∑t∈T̂

−e(t) ≥ −Mu. (10)

Therefore,

v =∑t∈T̄

z(t) +∑t∈T̂

z(t) ≥∑t∈T̄

z(t)−Mu.

We prove next that

∑t∈T̄

z(t) /∈ −IR`++. (11)

Indeed, if∑

t∈T̄ z(t) ∈ −IR`++, the set S = {t ∈ T̄ : z(t) 6= 0} is nonempty,

(otherwise∑

t∈T̄ z(t) = 0 /∈ −IR`++,) and

∑t∈T̄

z(t) =∑t∈S

z(t) ∈ −IR`++

and therefore there is a vector w in IR`++ with

∑t∈S

z(t) + w = 0.

For every t ∈ S, let y(t) ∈ IR`++ with y(t) �t x(t) and z(t) = y(t) − e(t).

Then,

∑t∈S

(y(t) +w

|S|) =

∑t∈S

e(t),

62

i.e., y(t) + w|S| , t ∈ S, is an S-allocation, and as �t is weakly monotonic,

y(t) +w

|S|�t x(t)

contradicting the assumption that x is a core allocation.

Lemma 7 There is p ∈ ∆ such that inf{pz : z ∈ coV } ≥ −M .

Proof. For every k > 0 let Kk = cl{v ∈ coV : ‖v‖∞ < k} (where for a subset

A of IRn, clA denotes the closure of A in IRn,) and Ck = {w ∈ IR` : −k ≤

wi ≤ −M−1/k. The closure of a convex set is convex (indeed, if A is convex

and x, y ∈ clA and 0 < α < 1, there are sequences xn ∈ A and yn ∈ A with

xn → x and yn → y as n →∞, and therefore αxn+(1−α)yn → αx+(1−α)y

as n →∞. As a is convex αxn +(1−α)yn ∈ A and thus αx+(1−α)y ∈ clA,

proving that clA is also convex). The set {v ∈ coV : ‖v‖∞ < k} is the

intersection of two convex sets and thus convex, and therefore the set Kk =

cl{v ∈ coV : ‖v‖∞ < k} is convex closed and bounded. Thus the sets Kk

and Ck are convex and compact, and therefore there is a sequence of vectors

pk ∈ IR` with

sup{p(k)w : w ∈ Ck} < inf{p(k)v : v ∈ Kk} ≤ 0.

In particular p(k) 6= 0 and therefore we may assume without loss of generality

that ‖p(k)‖1 = 1 (where for a vector x we denote ‖x‖1 =∑

i |xi|); otherwise

63

we replace the vectors p(k) with p(k)/‖p(k)‖1. W.l.o.g. assume that p(k) → p

as k → ∞. Then ‖p‖1 = 1. We prove next that p ≥ 0. Let ui denote

the i-th unit vector in IR`. Note that for every every k, 0 ∈ Kk, and for

sufficiently large values of k, −2Mu− kui/2 ∈ Ck. Therefore, p(k)(−2Mu−

kui/2) < p(k)0 = 0, i.e., −kpi(k)/2 < p(k)(2Mu), or equivalently, pi(k) >

−2Mp(k)u/k → 0 as k → ∞ and therefore for every 1 ≤ i ≤ `, pi =

limk→∞ pi(k) ≥ 0. Therefore, p ≥ 0 and as∑`

i=1 pi = 1, the limiting vector p

is in the price simplex ∆. It follows that inf{pv : v ∈ coV } ≥ −M .

Let S = {t ∈ T : p(x(t) − e(t)) < 0}. Note that it follows from weak

monotonicity of �t that for every ε > 0, x(t) − e(t) + εu ∈ V (t) and thus

∑t∈S(x(t)− e(t) + εu ∈ V and therefore

∑t∈S p(x(t)− e(t) + εu) ≥ −M . As

∑t∈S p(x(t)− e(t) + εu) → ∑

t∈S p(x(t)− e(t)) as ε → 0, we deduce that

∑t∈S

p(x(t)− e(t)) ≥ −M.

Note also that as∑

t∈T p(x(t)− e(t)) = 0,

∑t∈T

|p(x(t)− e(t))| = 2∑t∈S

|p(x(t)− e(t))| ≤ 2M,

which proves that the price vector p obeys (7).

Observe that for every ε > 0, x(t) + εu �t x(t) and therefore,

inf{p(y − x(t)) : y �t x(t)} ≤ pεu = ε → 0 as ε → 0+,

64

and therefore the inf is nonpositive. Assume that for every t ∈ T we select

y(t) ∈ IR`+ with y(t) �t x(t). Then y(t)− e(t) ∈ V (t) and thus

∑t∈T (y(t)−

e(t)) ∈ V ⊂ coV implying that

∑t∈T

p(y(t)− e(t)) ≥ −M.

As x is an allocation,∑

t∈T p(y(t)−x(t)) =∑

t∈T p(y(t)−e(t)), and therefore

inf{∑t∈T

p(y(t)− x(t)) : y(t) �t x(t)} ≥ −M

and as inf{∑t∈T p(y(t) − x(t)) : y(t) �t x(t)} =∑

t∈T inf{p(y(t) − x(t)) :

y(t) �t x(t)}, the price vector p obeys (8).

12.1 Replicated economies

Let E = 〈T ; IR`+; (e(t))t∈T ; (�)t∈T 〉 be an exchange economy with ` com-

modities and m consumers. The r replicated exchange economy, Er, is the

exchange economy with mr consumers, where each consumer is indexed by

a pair (t, q), with t ∈ T and q = 1, . . . , r. The first index is refers to the type

of the consumer and the second distinguishes between different consumers of

the same type. Two consumers of the same type t ∈ T have the same pref-

erence relation �t and the same initial endowment e(t). A type-symmetric

allocation of Er is an allocation x : T × {1, . . . , r} → IR`+ for which there is

65

a function y : T → IR`+ with x(t, q) = y(t). It follows that y is an allocation

in E . Given an allocation y of E it induces a type symmetric allocation x

defined by x(t, q) = y(t).

Corollary 2 Let E = 〈T ; IR`+; (e(t))t∈T ; (�)t∈T 〉 be an exchange economy

with ` commodities and m consumers, with strictly positive initial endow-

ments, i.e., e(t) >> 0, and with weakly monotonic and continuous prefer-

ences. Then any allocation y of E such that for every r the induced type

symmetric allocation in Er is in the core of Er is a competitive allocation.

Proof. Let M = ` maxt∈T ‖e(t)‖. By Anderson’s theorem, for every positive

integer r, there is a price vector p(r) ∈ ∆ with

1

mr

∑t∈T

r|p(r)(y(t)− e(t))| ≤ 2M

mr

and

1

mr

∑t∈T

−r inf{p(r)(z − y(t)) : z �t y(t) ≤ 2M

mr.

Therefore, for every t ∈ T ,

|p(r)(y(t)− e(t))| ≤∑t∈T

|p(r)(y(t)− e(t))| ≤ 2M

r

which implies that

lim supr→∞

|p(r)(y(t)− e(t))| = 0,

66

and for every t ∈ T and z ∈ IR`+ with z �t y(t),

−p(r)(z − y(t)) ≤∑t∈T

− inf{p(r)(z − y(t)) : z �t y(t) ≤ 2M

r,

which implies that for every z ∈ IR`+ with z �t y(t),

lim infr→∞

p(r)(z − y(t)) ≥ 0.

W.l.o.g. assume that p(r) → p ∈ ∆ as r → ∞. (Otherwise we take a

subsequence.) It follows that for every t ∈ T , py(t) − pe(t) = 0, and if

z ∈ IR`+ with zt �t y(t) and pz ≥ p(y(t)) = p(e(t)). By continuity of the

preference relation �t, for sufficiently small ε > 0, (1 − ε)z �t y(t) and

therefore also (1 − ε)pz = (1 − ε)pe(t) ≥ pe(t), which is possible only if

pe(t) ≤ 0. However, as the initial endowments are strictly positive, and

p ∈ ∆, pe(t) > 0. Therefore, pz > pe(t) whenever z �t y(t), i.e., (p, y) is a

competitive equilibrium of E .

Corollary 3 Let E = 〈T ; IR`+; (e(t))t∈T ; (�)t∈T 〉 be an exchange economy

with ` commodities and m consumers, with strictly positive initial endow-

ments, i.e., e(t) >> 0, and with weakly monotonic and continuous prefer-

ences defined by strictly concave utility functions. Then any limit point y

of a sequence of allocation yr of E such that for every r the induced type

symmetric allocation in Er is in the core of Er is a competitive allocation.

67

Proof. Let M = ` maxt∈T ‖e(t)‖. By Anderson’s theorem, for every positive

integer r, there is a price vector p(r) ∈ ∆ with

1

mr

∑t∈T

r|p(r)(yr(t)− e(t))| ≤ 2M

mr

and

1

mr

∑t∈T

−r inf{p(r)(z − yr(t)) : z �t yr(t)} ≤ 2M

mr.

Therefore, for every t ∈ T ,

|p(r)(y(t)− e(t))| ≤∑t∈T

|p(r)(yr(t)− e(t))| ≤ 2M

r

which implies that

lim supr→∞

|p(r)(yr(t)− e(t))| = 0.

Let r1 < r2 < . . . with yrk(t) →k→∞ y(t) for every t ∈ T . Then,

limk→∞

|p(rk)(y(t)− e(t))| = 0.

For every t ∈ T and z ∈ IR`+ with z �t yr(t),

−p(r)(z − yr(t)) ≤∑t∈T

− inf{p(r)(z − yr(t)) : z �t yr(t) ≤ 2M

r.

If z ∈ IR`+ with z �t y(t) then for sufficiently large k we have z �t yrk(t)

which implies that

lim infk→∞

p(rk)(z − yrk(t)) ≥ 0,

68

and thus

lim infr→∞

p(rk)(z − y(t)) ≥ 0.

Let p ∈ ∆ be a limit point of the sequence p(rk), k ≥ 1. W.l.o.g. we

may assume that p(rk) →k→∞ p (Otherwise we replace the sequence rk with a

subsequence). It follows that for every t ∈ T , py(t)−pe(t) = 0, and if z ∈ IR`+

with zt �t y(t) then pz ≥ p(y(t)) = p(e(t)). By continuity of the preference

relation �t, for sufficiently small ε > 0, (1 − ε)z �t y(t) and therefore also