Download - Investments - Lecture Notes Intro 2013-08

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 1/30

INVESTMENTS

Lecture Notes

Sean M. Davis, Ph.D.

© Sean M. Davis 2010-2013, all rights reserved

Any material used in class and/or these notes that is not the work of the author is for non-commercial,

educational use, and it remains the sole property of the copyright holder(s).

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 2/30

“Admission of ignoranceis often the first step in our education”

– Stephen R. Covey

“If the only tool you have is a hammer,

you tend to see every problem as a nail.”

– Abraham Maslow

“Great intellects are skeptical”

– Friedrich Nietzsche

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 3/30

Ch 1 ‐ Understanding Investments ‐ Jones

‐ Background and Issues ‐ BKM

An INVESTMENT is ‐‐

the commitment of money or other resources now and over a period of time in the expectation

of reaping future benefit

1 Background

‐‐

you

sacrifice

something

of

value

now

expecting

to

benefit

later

Definitions:

REAL ASSETS

Used to produce goods and services

Examples: land, building, equipment, knowledge, etc

FINANCIAL ASSETS

Claims on real assets or the income generated by them

Previously they were merely pieces of paper, now they are usually electronic

Financial Asset

Types

FIXED INCOME (DEBT)

‐‐ defined cash flow over a specified period

EQUITY

‐‐ ownership share in a corporation (no promise of payment)

DERIVATIVES

‐‐ securities that derive their value from other securities

Financial Markets

Play an informational role

Allow for "consumption timing"

Invest during earning years so one can retire

Financial assets can "store" wealth

Allocate risk

Provide a vehicle or system to separate ownership from management

Investors cannot actively manage large corporations

Managers become the "agents" of the owners

Creates a well known and researched ___________ problem

AGENCY

Corporate governance is used to oversee shareholder interests

Board of directors, Sarbanes‐Oxley, etc

1 Background 1

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 4/30

"INVESTMENTS" is the study of the investment process

PASSIVE Management

‐‐ buying and holding without detailed analysis

ACTIVE Management

Portfolios are a collection of assets, two general approaches are to use …

1 Background

‐‐

ac ve y

ry ng

o

en y

m spr c ng

an or

ren s

Examples of ACTIVE management …

TOP‐DOWN ‐‐ Asset allocation

BOTTOM‐UP ‐‐ Focuses on securities that are attractively priced

Markets are competitive

This creates relatively fair pricing and a TRADEOFF of ______________________

RISK & RETURN

The relationship

between

RISK

and

RETURN,

and

being

paid

appropriately

for

the

risk undertaken, is an ongoing and essential part of investment analysis.

NOTE: Bond prices and yields are inversely related (negatively correlated).

Risk and return are ______________________

POSITIVELY CORRELATED

Returns and Risk

EXPECTED RETURN ‐ the ex ante return expected by investors over some future holding

period

E(rp) = the expected return for a portfolio

E(ri ) = the expected return for individual securities "i "

E(rM) the expected return of "the market" usually proxied by the S&P500

REALIZED RETURN ‐ the actual return realized over the holding period

RISK ‐ the chance that the realized or actual return on an investment differs from the

expected return

" "The "risk

free"

rate

of

return

is

usually

our

benchmark

lowest

expected

return

It is proxied by the US rate of return on Treasuries (usually the 3 month T‐bill)

While investors are usuall risk averse ‐ referrin lower risk investments ‐ the

can also be risk tolerant in that they will accept risk for which they are being

reasonably well compensated.

1 Background 2

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 5/30

This whole course is largely focused on this risk and return relationship ‐‐ how we measure

risk, how we estimate returns, how we can expect certain returns based on risk, how prices

today are affected by changes to risk.

1 Background

"You have to understand that being wrong is part of the process," Peter Bernstein

"At best, estimates are imprecise; at worst, they are completely wrong. The best

one can do is make the most informed return and risk estimates possible," Jones

Ethics in Investing

(refer to the Jones text and the Martha Stewart case)

1 Background 3

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 6/30

Ch 2 ‐ Investment Alternatives ‐ Jones

‐ Asset Classes and Financial Instruments ‐ BKM

TERMS

Indirect Investing

The buying and selling of shares of investment companies (e.g. mutual funds, exchange

2 Assets

, , ,

Direct Investing

Investors buying and selling securities themselves. This is typically done through an

intermediary (a broker), though it can be done directly.

Liquidity

The ease with which an asset can be bought or sold quickly with relatively small changes

in price. The degree to which there is a change in price, between buying in selling, is often

how we measure how "liquid" an asset is.

The market for short‐term, highly liquid, low risk assets

This is a subsector of the debt market

Term/timeframe: ‐‐ short term (a year or less)

Usually measured in _______, ________ or ________ of maturity

DAYS WEEKS MONTHS

Examples:

Treasury Bills, Certificates of Deposit, Commercial paper, etc

Rates like these are sometimes used as a benchmark for other rates charged

T‐Bills ‐ 13wk 0.11% ^IRX

LIBOR ‐ 1 mo 0.24% Yahoo Finance

LIBOR ‐ 3 mo 0.44%

Brokers Call

Treasury Bills ("T‐bills")

Initial maturities in 4, 13, 26 or 52 weeks

Buy from the Treasury or in the secondary market at a DISCOUNT

For example, a $10,000 T‐bill might be sold for $9,837.50

The interest earned is gained by holding the T‐bill until maturity when it

is worth $10,000

Gain: $162.50

Yield: 1.6518% (this would need to be converted

into an annual yield)

2 Assets 4

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 7/30

THE CAPITAL MARKETS

FIXED INCOME SECURITIES

Securities with fixed payment dates and amounts

2 Assets

BONDS

Notes are up to 10 years in maturity

Bonds are 10‐30 years

Minor point here: we mostly refer to "bonds" in class, and they may have under 10 years

to maturity, e.g. a 20 year bond that was bought 15 years ago doesn't suddenly turn

into a "note."

These securities are priced as a _______________ of PAR

PERCENTAGE

The values

after

the

colon

(":")

are

the

fractional

price

in

___________

32nds

Remem er t at coupons are usua y semi‐annua an par is 1000 un ess to ot erwise.

TREASURY NOTES & BONDS

Example (p30)

Feb‐15 105:20 bid 29 chg

4% coupon 105:22 ask 3.017 YTM

What are the bid/ask prices for this bond?

Bid = 105 20/32 or 105.625 … $1056.25

Ask = 105 22/32 or 105.6875 … $1056.875

Chg = +29/32 = .9063% of par … $1000 x .009063 = +$9.0625 chg/day

YTM = 3.017% (more in Ch 10)

MUNICIPALS (Munis)

General Obligation Bond ‐‐ backed by the full faith and credit of the issuer

Revenue Bonds ‐‐ backed by a revenue‐producing municipal asset (turnpike, airport)

Industrial develo ment ‐‐

fundin rivate enter rise

Main characteristic:

TAX EXEMPT

Equivalent Taxable Yield calculations

r mun = r ( 1 ‐ t )

r = rmuni / (1 – t )

t = 1 ‐ rmuni / r

2 Assets 5

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 8/30

What is the Equiv. Taxable Yield of a corporate bond relative to a municipal with a 6% yield

where the investor has a 25% tax rate?

= 6% / ( 1 ‐ .25 ) = 8%

What would you expect a municipal bond to yield that is comparable to a 7.5% corporate

2 Assets

on

n

ra ng

an

r s

w ere

nves ors

ave

an

e ec ve

ax

ra e

o

= 7.5% * ( 1 ‐ .30 ) = 5.25%

The market is pricing the yield for two bonds, one corporate and one municipal, at 9.0% and 7.0%

respectively. What assumption is the market pricing into these yields for an expected tax rate

= 1 ‐ 7.0% / 9.0% = 22.2%

CORPORATE

Secured, Unsecured (debentures), Subordinated debentures, Callable, Convertible

MORTGAGE BACKED

SECURITIES

EQUITIES more on t is ater

INDEXES

There are indexes (or indeces) that are formed to track all manner of investments

… stocks, bonds, materials, market sectors, countries, etc. Anything of interest to a large

enough group of people is being tracked in some form of index.

The ones of interest to us in this class are typically the major stock indexes:

Dow Jones

Industrial

Average 30

large,

"blue

chip"

stocks

(originally

20)

It only represents ~25% of the "market" as measured by market capitalization

Gets a disproportionate amount of media coverage relative to its significance

S&P Indexes* % of market Russell Wilshire

500 Large cap ~80% 1000 Large 5000

400 Mid cap ~7%

600 Small cap ~3%

2000 Small

"Russell 1000"

"Russell 2000"

Actually contains

* together these three indeces represent roughly 90% well over 6000 stocks

of the investable US equities and combine to be the

Russell 3000

are these combined

S&P Composite 1500

2 Assets 6

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 9/30

DERIVATIVE SECURITIES (also more on this later)

Options

Futures

2 Assets2 Assets 7

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 10/30

Ch 3 ‐ Indirect Investing ‐ Jones

Ch 4 ‐ Mutual Funds ‐ BKM

Investment companies are financial intermediaries that invest the funds of investors in securities or

other assets. They provide the opportunity for:

Record keeping

Diversification and divisibilityProfessional management

Lower transaction costs*

*Note that the overall expense ratios vary widely from fund to fund. Actively managed funds tend to

have the highest overall costs.

John Bogle, a major critic of mutual fund practices and founder of Vanguard ‐‐a leader in

low cost and "index" investing, states that the actual costs of actively managed funds

is 2.5% to as much as 3.0% annually.

Funds report a "NET ASSET VALUE" of the securities under management

NAV = ( Market value of assets minus Liabilities ) / Shares outstanding

Ex: A fund has a portfolio of 150 million

pays its managers/advisors 4 million

owes rent and admin costs of 1 million

has share outstanding of 5 million

3 Funds

[ 150.0 ‐ ( 4.0 + 1.0 ) ] / 5

= 29.00$ NAV per share

Types of funds

Trusts, REITS, Hedge funds, and Managed Investment Companies (which will be our focus)

Managed Investment Companies

Closed end funds

∙ Trade like stock – cash in or out by buying shares

Open end funds

∙ Cash in at NAV, redeem shares or cash out at NAV

Load

∙ sales charge or commission

NAVOffering price =

3 Funds 8

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 11/30

Mutual fund – an open‐end investment company

Money market, equity, sectors, bonds, international, balanced, index

∙ “value” or “growth”

∙ Large cap or small cap

Costs ‐Fee Structure

∙ Operating expenses – usually between 0.2% and 2.0%, i.e. 20 basis and 200 basis

∙ Front end load ∙ Back end load

· “Exit” fee or “contingent deferred sales charges”

∙ 12b-1 charges

· Fees paid for marketing and distribution costs

Returns calculations

Closed‐end funds (including Exchange Traded Funds or ETFs)

Like mutual funds but trade like stock

Are usually tracking an index but the may be actively managed

ETFs tend to have much lower expense ratios than actively managed mutual funds

Rate of return = Δ(NAV) + Distributions

Start of year NAV

Price ‐NAV

NAV=Premium or discount to NAV

3 Funds

Mutual fund companies may discontinue certain funds within their "family" of funds. This creates bias

in the reported results.

If you were to look at ACME Capital Management's family of funds and they all appear to have

performed well relative to the market, ACME may have merely shut down the losing funds. Those

fund managers were fired or transferred, and the assets were merged into the "successful" funds.

3 Funds 9

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 12/30

Ch 4 ‐ Securities Market and Market Indices ‐ Jones

Ch 5 ‐ How Securities are Traded ‐ Jones

Ch 3 ‐ Securities Markets ‐ BKM

HOW FIRMS ISSUE SECURITIES

Primary market

IPO's, SEO's ‐‐ stocks, bonds, private placements

Using an investment banker

Secondary market

NYSE, NASDAQ, AMEX

Using a broker/dealer

HOW SECURITIES ARE TRADED

BROKER

DEALER

Ex:

Stocks & bonds Stocks & bonds

(primary or (secondary market

secondary market) only)

"Specialist" "Specialist" or "market maker"

(a specialist can be both)

4‐5 Markets & Trading

Also: Real Estate Also: Cars

FeesCharge a commission Bid/Ask spread

percentage or flat fee

Key distinction

Brokers do not "own" the Dealers own or take title

product they are selling to what they sell … this entitles

them to any reasonable profit

they can make

Legal limitation: Broker/dealers cannot act as both on the same transaction

How

do

they

get

around

this

limitation?

A separate, legal entity (often a subsidiary) that acts as a dealer is sent (i.e. sold)

the "order flow" by the broker. The "dealer" then fills the order earning the

bid/ask spread.

Why might the move from spreads of an 1/8th or 1/4 of a dollar (i.e. 12.5 to 25 cents) to "decimalization,"

i.e. where spreads are only .01 to .05 or a dollar, or 1 to 5 cents, minimize this issue as a concern?

4‐5 Markets & Trading 10

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 13/30

Types of Orders

Market order ‐ execute immediately at the market price

Time is of the essence ‐ "I want it now"

Limit order (price contingent in the text) ‐ the order executes only if the price is met

Price is what matters ‐ "I only want to buy it if it drops to the price I specify"

Stop order ‐ an order with a price trigger, in effect it is a sort of "limit‐market" order

Stop Loss ‐if a stock drops below a certain price, a holder of the stock can put in a stop loss

to prevent further losses.

Stop Buy ‐ if a stock rises above a certain price, the limit is reached and the stock is purchased

We can think of stop orders as a sort of "limit‐market" order because once the trigger is

reached, we want to buy or sell the stock immediately. Therefore, once triggered, the

stop order becomes a market order.

INTC BA

4‐5 Markets & Trading4‐5 Markets & Trading 11

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 14/30

BUYING ON MARGIN

Securities, like other assets (cars, homes), can be purchased with borrowed money

"Broker's Call Loans" are easily made to investors who want to LEVERAGE their position

in a stock. Leverage increases ________ which also increases potential ___________.

RISK RETURNS

INITIAL MARGIN required ‐‐ the initial equity percentage ‐‐ is almost always _____________

50%

This intial margin requirement may be satisfied with cash or other stock. We also

can refer to a margin transaction like this as having 2 to 1 leverage …

Example:

ASSETS LIABILITIES & OWNER EQ.

200 shares at 50.00$ Broker Loan $5,000

position value is $10,000 Equity (your cash) $5,000

Equity % 50.0% Position Gain(Loss) $0 0.0%Investor Gain(Loss) $0 0.0%

Equity in the account

Note that this 2:1 leverage ratio applies to retail investors for equity transactions.

You will hear of many examples of much higher leverage ‐‐4:1 (daytraders), 7:1 for

Margin = Value of the stock

4‐5 Markets & Trading

certain institutional investors, even 30:1 (or more) for banks.

Maintenance

marginThe broker who loaned money against the position requires that a minimum level of equity

be "maintained" in the account. If the equity margin percentage falls below a certain

threshold ‐‐ the maintenance margin percentage, this triggers a _____________.

MARGIN CALL

Once a margin call is triggered, the investor will be required to increase the account's equity

level to a pre‐defined level.

To find the price below which a margin call will be triggered:

Shares * Price ‐ Broker Loan

200P ‐ 5000

200P

Shares * Price = Maintenance Margin %

= 30% $35.714P =

4‐5 Markets & Trading 12

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 15/30

A more direct formula to use when solving for the price at which a margin call is triggered is

When going LONG …

( 1 ‐ 0.50 )

( 1 ‐ 0.30 )

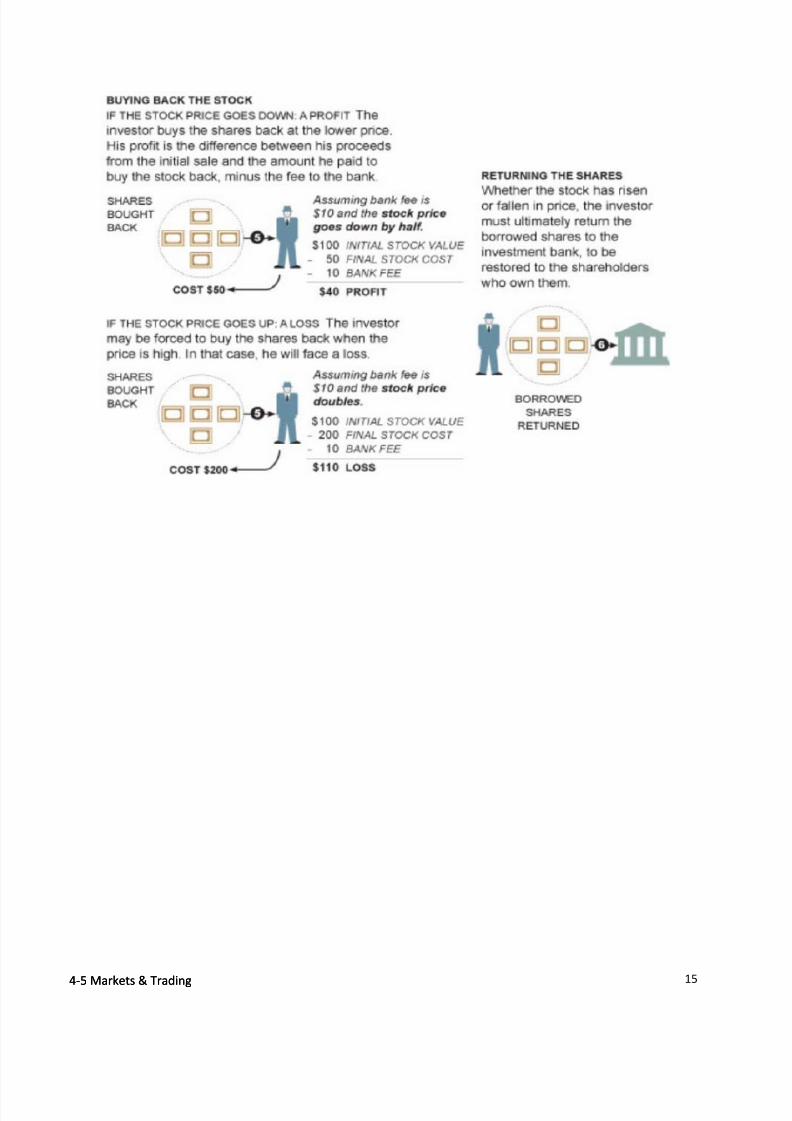

SHORT SALES

Most positions are bought and held "long" on a position statement with an expectation they

will rise in value. Stocks that are expected to decline may be ________________.

SOLD SHORT

Example:

Investor's intial account position

ASSETS LIABILITIES & OWNER EQ.Broker Loan $0

T‐bills $50,000 Equity $50,000

Equity % 100.0%

Investor decides to SHORT "Dot Bomb Inc." believing it will drop in price

ASSETS LIABILITIES & OWNER EQ.

Cash from short sale $100,000 1000 DOTB short 100.00$ shr

Margin Call

Price =

Long Price

*

( 1 ‐ Initial Equity )

( 1 ‐Maint margin )

= $50.00 = 35.714

4‐5 Markets & Trading

$100,000

T‐bills $50,000 Equity $50,000

Equity % 50.0% Position Gain(Loss) $0 0.0%

Investor Gain(Loss) $0 0.0%

Remember that finding the equity in a short position is different from a long position

To find the price above which a margin call will be triggered:

1000P P = $115.385

Assets ‐ Liabilities in account

150,000 ‐ 1000P = 30%

Value of the stock owed

Equity in the accountMargin =

= Maintenance Margin %Value of Shares to be paid back

4‐5 Markets & Trading 13

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 16/30

A more direct formula to use when solving for the price at which a margin call is triggered is

When going SHORT …

Shares shorted * (1 + Maint Margin level)

100 shares sold short @ $45 = 4,500$

Investor's initial equity in the account = 2,250$

Maintenance margin level = 30.0%

4,500 + 2,250 6,750

100 x 1.30 130

This can be reduced to

1 + 0.50

1 + 0.30

1.50

1.30

Margin Call

Price =

Cash from sale + Investor's Equity

= = = 51.923

= 1 + Inv Equity %

1 + Maint Margin%

Margin Call

Price = = 51.923

Short

Price *

= 45.00 x

45.00 x

4‐5 Markets & Trading

An investor who expects a stock to fall in price may execute a short sale. If the price of the stock

does

fall,

he

can

make

a

profit.NYT: March 25, 2012

4‐5 Markets & Trading 14

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 17/30

4‐5 Markets & Trading4‐5 Markets & Trading 15

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 18/30

Ch 13 ‐ Economy/Market Analysis ‐ Jones

Ch 14 ‐ Sector/Industry Analysis ‐ Jones

Ch 12 ‐ Macroeconomic and Industry Analysis ‐ BKM

A great deal of time and effort is spent in investment analysis focusing on the firm alone.

13‐14

Industry

Analysis

or

examp e,

one

approac

s

,

w c

nc u es

u

s

no

m e

o:

Balance sheet analysis

Comparisons of ratios with industry norms

Estimates of current and future cash flows

The strength and track record of the management team

The existing and new product pipeline

Barriers to entry in new or current markets

These are all elements of a business under which the company, through management and its

employees, is largely under control.

Some people focus all their time and effort looking for individual companies that are

UNDERVALUED this way, and we consider this a BOTTOM UP approach.

However, there are things well BEYOND the control of the firm, such as:

The Global Economy

The Domestic Macroeconomy

GDP, Employment, Inflation, Interest Rates, etc

Business Cycles

Now, we will still hold the management team of a firm responsible for properly navigating through

a recession or even an expansionary period.

A rising tide lifts all boats, and a falling one tends to lower all boats, but do all tides affect

all irms the same wa ?

13‐14

Industry

Analysis 16

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 19/30

Step 1. Analyze the Economy and/or Market

Step 2. Focus on Sectors/Industries that appear attractive

Step 3. Analyze and value individual companies (using the fundamentals above)

13‐14

Industry

Analysis

…

us

uy

more

o

e

sec ors n us r es

you

e eve

w

o

e er

n

e

near

u ure

We won't be spending a great deal of time on how to analyze the economy (I'll leave that to the

macro‐economics folks), but information is often readily available ‐‐ analysts do specialize in it

and their research is often readily available, plus inferences can be drawn from something as

simple as a yield curve … (see the Jones text for more)

What can we infer from these yield curves? (OK, what's a picture worth?)

How are industries defined? [Important: this can significantly vary by who is doing the defining]

Standard Industrical Classification (SIC) System ‐ still in use, but SIC codes are dated

North American Industry Classification System (NAICS) ‐ allows for more precise classifications

Newer industries that didn't exist in the WW2‐SIC era can be properly classified

Global Industry Classification Standard (GICS) ‐ a global standard from Standard & Poors

13‐14

Industry

Analysis 17

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 20/30

13‐14

Industry

Analysis

SIC Codes are still widely used:

Because they are based on SIC codes, they can have problems in correctly describing an industry as we might

In "Finance" research, it is also common to use "Fama‐French" industry groups. These two highly regarded

authors developed industry groupings based on SIC codes, and these industry groupings range from 5 high‐

level sectors to as many as 49 industry groups. They are still widely used in finanncial research.

envision it today.

For example, Fama‐French industry groups have non‐tech and high‐tech industries intermingled. As an

example, the FF industry group “Business Services” includes Computer Programming, Information Retrieval,

and Computer Maintenance. It also includes Commercial Printing, Credit Reporting Agencies, Industrial

Launderers, and Trailer Rental & Leasing.

13‐14

Industry

Analysis 18

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 21/30

While not always easy to predict, different industries follow different business cycles

First, economic activity tends to follow a cyclical pattern

13‐14

Industry

Analysis

Some in ustries respon very i erent y to economic cyc es

Just like individual companies, some industries are at different stages in their growth cycle

13‐14

Industry

Analysis 19

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 22/30

This leads us to consider SECTOR ROTATION as a potential investment strategy

this is just one potential approach

13‐14

Industry

Analysis

This does NOT mean you would necessarily rotate your entire portfolio from energy

and into HEALTH CARE if you believed the economy was heading into recession.

What does it mean? What are ways to use this type of information

% of % Price Change For

Standard &

Poors

Indeces Index

Value S&P

1500

* 1

Wk 13

Wks YTD '12 5

Yrs

S&P 500 1402.43 88.21 ‐1.9 ‐2.7 11.5 0 ‐0.9

S&P MidCap 400 1004.33 8.23 ‐1.8 1.6 14.2 ‐3.1 3.2

S&P SmallCap 600 467.41 3.56 ‐1.8 ‐0.1 12.6 ‐0.2 3.4

S&P Composite 1500 324.28 100.00 ‐1.9 ‐2.2 11.8 ‐0.3 ‐0.4

Data as o Dec 28 2012

,

Source: S&P Capital IQ, NetAdvantage, Stovall's Sector Card * the S&P1500 represents approximately 90% of all US stock value

Where can you get information like this for class? The UNF Library

http://www.unf.edu/library/research/subjects/Business,_Finance,_Investment.aspx

Then "S&P Net Advantage"

Then "Industries"

Then "Stovall's Sector Card"

13‐14

Industry

Analysis 20

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 23/30

Sectors by Global Industry Classification Relative Recommended

System (GICS) Strength

Consumer Discretionary Sector Summary 3.6 4 Overweight

Consumer Staples Sector Summary 3.9 2 Marketweight

STARS Weighting

Rankings

13‐14

Industry

Analysis

nergy

ec or

ummary

. ar e we gFinancials Sector Summary 3.5 5 Marketweight

Health Care Sector Summary 3.9 4 Overweight

Industrials Sector Summary 3.5 3 Overweight

Information Technology Sector Summary 3.6 3 Marketweight

Materials Sector Summary 3 3 Underweight

Telecommunication Services Sector Summary 3.2 3 Marketweight

Utilities Sector Summary 3.3 1 Underweight

Rankings: 5 (best) to 1 (worst)

Weighting: Overweight= Increased exposure to sector.

Marketweight= No change

in

exposure.

Underweight= Decreased exposure to sector.

% of Relative

S&P 1500 1 Wk 13 Wks YTD '12 5 Yrs Strength

Consumer Discretionary (S 348.75 11.73 ‐1.6 ‐0.5 19.5 3.7 7.3 3.6 4

STARS

% Price Change For

GICS Sub‐Industries for:

Index

Value

Rankings

Consumer Staples (Sector) 372.83 9.87 ‐2.1 ‐3.2 6.6 10.8 3.8 3.9 2

Energy (Sector) 551.82 10.29 ‐3 ‐5 0 2.1 ‐2.7 4.2 2

Financials (Sector) 242.11 16.37 ‐1.4 3.3 22.6 ‐16.6 ‐10 3.5 5

Health Care (Sector) 469.44 11.79 ‐1.9 ‐1.9 14.5 9.6 2.8 3.9 4

Industrials (Sector) 341.88 10.91 ‐1.8 2.1 11.7 ‐3 ‐1 3.5 3

Information Technology (S 468.93 18.65 ‐2.2 ‐7.3 10.9 0.1 2.2 3.6 3

Materials (Sector) 247.23 4.01 ‐0.7 0.8 11.8 ‐10.1 ‐1.2 3 3

Telecommunication Servic 143.33 2.77 ‐1.2 ‐8.1 11.2 0.5 ‐3.2 3.2 3

Utilities (Sector) 197.27 3.58 ‐2.5 ‐5 ‐3.8 14.6 ‐3 3.3 1

Data as of Dec 28, 2012

13‐14

Industry

Analysis 21

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 24/30

Ch 6 ‐ Risk and Return ‐ Jones (Ch 5 in BKM)

Total Return or Holding Period Returns

TR or

HPR =

nding Price ‐ Beginning Price + Cash Dividen

Beginning Price

Put another

way:

Or …

P1 ‐P0 +

Income

(if

any)

P0

P1 + Income

P0

‐ 1

We purchased shares in a fund for

30.00$ and later sold them for

37.50$ being paid dividends of

5.00$ along the way.

What's the HPR? 37.50$ ‐ 30.00$ + 5.00$

= 41.7%.

37.50$ + 5.00$

30.00$

IMPORTANT: don't forget to subtract the "1"

if you use this method

= 1.417 Alt:

Note that there is no measurement of __________ in an HPR calculation.

TIME

"Return Relative" is used in the Jones text and refers to the TR or HPR plus 1.

therefore RR = HPR in decimal form + 1.0

HPR in decimal form = RR ‐ 1

Cumulative Wealth Index is another way to measure a Total or Holding Period

Return, but

1) an index value is used, i.e. we assume a starting investment of $1

2) we multiply this value times each period's return plus 1 (or the RR)

3) because we started with $1, our ending value will be in monetary

terms, not in a return. Therefore, the CWI is a measure of wealth

or the money in hand at the end of the holding period. To convert

this to a percentage return, multiply by 100.

If I had an investment with the following returns:

1 2 3 4

HPR 10.0% 25.0% ‐20.0% 25.0%

The CWI would be

1.10 x 1.25 x .80 x 1.25 = 1.375

6 Risk‐Return 22

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 25/30

This means if we started with $1, we would have $1.375 in our account at the end

of year 4

We can use the index to determine how much we'd have no matter how

much with which we started: Starting Ending

10,000 13,750

=Starting * CWI

6 Risk‐Return

MULTI‐PERIOD RETURNS

Arithmetic Average

Period HPR This is merely a simple mean of the returns:

.

2 25.0% 10.0% + 25.0% + ‐20.0% + 25.0%

3 ‐20.0%

4 25.0%

(sum of HPR's) / #Periods … or in Excel "=Average( HPRs )

10.0% … but this value ignores ________________

4

Geometric Average

= ( 1 + GeoAvg ) N

= ( 1 + HPR1 ) * ( 1 + HPR2 ) * ( 1 + HPR3 ) * ... ( 1 + HPRN )

1.10 x 1.25 x .80 x 1.25 = 1.375

Now you need to adjust for the 4 periods of growth.

1.375 1/4 = 1 + the GeoMean

TI BAII: 1.375 "yx" key, ".25", "= 1.0829 ‐ 1 8.29%

HP12c: 1.375 "enter", ".25", "yx"

How can you easily check your result (to make sure you did it right)?

1.0829 4

= 1.375

How could you calculate a geometric average using the TVM functions of your calculator?

TVM: N i PV PMT FV

4 (1.0) 1.375 remember to have one of the

8.29% solve for "I" CFs be negative

6 Risk‐Return 23

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 26/30

Other examples:

Someone offers you an investment claiming to triple your money in 3 years? What

compound annual growth rate (CAGR) is assumed by this investment "opportunity?"

N i PV PMT FV

3 44.2% (1.0) 0 3.0 remember that "0" is assumed if

you don't enter the value, i.e. PMT

6 Risk‐Return

How many years would it take to double your money if it grew at a rate of 15%/year?

N i PV PMT FV

4.96 15.0% (1.0) 0 2.0 remember to clear the TVM registers

between problems

You bought a stock 10 years ago for $12.50 which is now worth $100. The company

re nves e a earn ngs an never pa a v en .

What is the stock's HPR and its CAGR?

HPR = 700% = $100 / $12.50 ‐1

N i PV PMT FV10 23.1% (12.5) 0 100.0

CAGR = 23.1%

Dollar Weighted Returns

Analogous to an investment's IRR. It captures the varying amounts under management.

We won't be spending much time with it.

RISK

Return and risk are opposite sides of the same coin

They are positively correlated. They may not be directly correlated, as in 1 to 1, but

they will always go up and down together. Higher returns come with higher risks.

Lower risks mean you should expect lower returns.

If you take anything away from this class in your future investment lives, make

sure you don't forget this. Anyone who tries to sell you a low risk investment

that has an abnormally high return: is probably underinformed, not telling you

about all the true risks involved, or may be actually trying to cheat you (or all 3).

Interest rate risk

Market risk

Inflation risk

Business risk

Financial risk

Liquidity risk

Currency risk

Country risk

6 Risk‐Return 24

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 27/30

Measuring Risk

If a stock or a mutual fund had the following annual historical returns

1 2 3 4

10% 10% 10% 10%

6 Risk‐Return

We would be very likely to "expect" this investment to return how much

in the following year? 10% of course.

If some investments returned

1 2 3 4 E(ri ) σ

A 10% 10% 10% 10% 10.0% 0.00%

B 10% 8% 12% 10% 10.0% 1.63%

C 7% 9% 11% 13% 10.0% 2.58%

‐‐ . .

What would we expect them to return in the next period?

How would be choose from between them?

Risk is often associated with the dispersion of the likely outcomes.

This means the variability of the outcomes

Variability ≈ Variance = (Standard Deviation)2

Therefore we will use the standard definition ‐‐ σ ‐‐ as one of

our measures of the riskiness of an investment.

This does not mean that high StDev investments are bad and should be

avoided. We use this measure to compare different investments and

select which ones return the most relative to their risk.

Expected Returns and Standard Deviation of a Portfolio ‐Scenario Analysis

Some texts use a robabilit distribution at this oint to estimate an "ex ected return" ‐‐

"E R ".

.

There are many ways to estimate an expected return as shown above. For Project 1, USE

THE ARITHMETIC MEAN. We will use probabilities in calculating E(R) later.

NOTE: Your practice problems will ask you to calculate many expected returns and st.dev.

for portfolios by combining assets (stocks, bonds, funds) with known returns or risk.

These are usually nothing more than simple weighted average calculations.

6 Risk‐Return 25

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 28/30

A portfolio is made by combining the two assets:

Secu E(R ) σ % of each Expected value for portfolio

A 14.0% 20.0% 30% E(Rp) σp

B 7.0% 30.0% 70% 9.1% 27.0%

That is, the sum of the weights of each security times the value (return or st. dev.).

* *

6 Risk‐Return

e.g.

P =

A

A +

B

B9.1% .30 x 14.0% + .70 x 7.0%

σp =

27.0% .30 x 20.0% + .70 x 30.0%

RISK PREMIUM

Because we expect to be paid for taking on extra risk ‐ in the form of higher returns,

higher risk investments have "premium" we expect them to pay us for the extra risk,

the risk premium.

Risk Premium

or

RP

=

The

nominal

return

of

the

security

minus

the

T‐

bill

rate

OR = The nominal return usuall e uities minus US Gov't "Lon bond" rate

We can use the arithmetic mean or the geometric mean to estimate the

nominal return. For simplicity in this class, we'll use the arithmetic mean for

expected returns unless told otherwise, and use the T‐bill for your risk free.

A few terms: The real rate on any security is after adjusting for inflation

The nominal rate

is the "named" or stated rate, i.e. not adjusted for i

Long bonds usually refer to the 10 year Treasury bonds, a benchmark

The risk free rate is usually proxied by the T‐bill (the 3 month or 13 week

bill), however the Long Bond may be used in the Risk Premium calculation.

This does not mean we refer to the Long Bond as the "risk free" rate.

In actuality, the "risk free" rate still has risks. (You should be able to

name a couple.) All textbooks tend to use the term ‐‐

Risk free = r f

A more proper term to use would be the "minimal risk" asset

but

r is

not

et

in

wide

use

Reward to Volatility ‐‐The Sharpe Ratio

E(r p ) ‐r f

σ p

S =

Portfolio risk premium

St Dev of the portfolio excess return=

9.1% ‐ 5.0% =

27.0% 15.2%

6 Risk‐Return 26

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 29/30

Interest Rates

Nominal Rate (R) ‐ The rate that has not been adjusted for _____________

INFLATION (i)

Real Rate (r) ‐ Inflation adjusted rate ‐ "the excess of the interest rate over the inflation rate"

Also: The rate that captures the increase in purchasing power

6 Risk‐Return

1 + R R - i

1 + i 1 + i

Asset Allocation and the Capital Allocation Line (CAL)

r ≈ R - i 1 + r = r =

We typically refer to the portfolio we formed above as a ________________ portfolio.

RISKY

When we combine this with a RISK‐FREE ASSET, we call it a ______________ portfolio.

COMPLETE

Secur. E(R ) σ S % of each Expected value for portfolio

R s y 15.5 27.0 15.2 50 p σp

rf 5.0% 0.0% 50% 10.25% 13.50%

Note that as we introduce risk‐free assets into our complete portfolio, the

_________________ declines and _________________ declines

expected return standard deviaion

Calculate the Sharpe ratio for the complete portfolio:

10.25% ‐ 5%

13.50%38.89%=

6 Risk‐Return 27

8/11/2019 Investments - Lecture Notes Intro 2013-08

http://slidepdf.com/reader/full/investments-lecture-notes-intro-2013-08 30/30

Key concept regarding the Sharpe ratio and the CAL:

Recall that a straight line can be expressed as y = mx + b

y = m x + b

E(rp) = Sharpe σp + rf

14.72% 38.89% 25.00% + 5.0%

The Sharpe ratio is the slope of the CAL, and any portfolio formed along

the Capital Allocation Line has the same reward to variability ratio.