Insurance generally acceptedaccounting principles (GAAP)update

Page 1 Insurance generally accepted accounting principles (GAAP) update

Disclosures about short-duration contractsAgenda

► Overview► Summary of disclosures► Implementation considerations► Appendix A – Illustrative example

Page 2 Insurance generally accepted accounting principles (GAAP) update

Disclosures about short-duration contractsOverview

► Accounting Standards Update 2015-09, Financial Services –Insurance (Topic 944): Disclosures about Short-Duration Contractsissued in May 2015► Requires additional disclosures about the liability for unpaid claims and

claim adjustment expenses for short-duration contracts in the scope ofAccounting Standards Codification (ASC) 944 Financial Services –Insurance

► Our Technical Line, Insurers will have to make additional disclosuresabout short-duration contracts (SCORE No. BB3110), highlights the newdisclosure requirements, discusses implementation considerations andprovides potential disclosure examples

► Effective date:Public business entity (PBE) Non-PBE Early adoption permitted?Annual 2016Interim – Q1 2017

One year deferral Yes

Page 3 Insurance generally accepted accounting principles (GAAP) update

Disclosures about short-duration contractsOverview

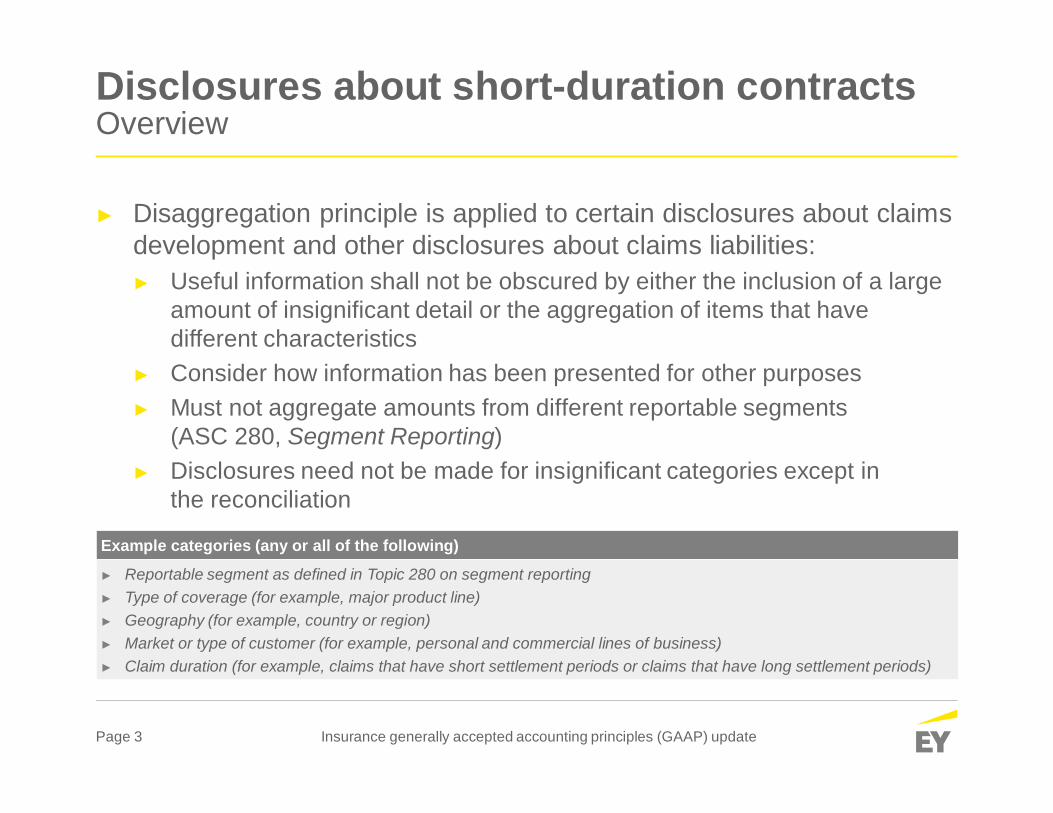

► Disaggregation principle is applied to certain disclosures about claimsdevelopment and other disclosures about claims liabilities:► Useful information shall not be obscured by either the inclusion of a large

amount of insignificant detail or the aggregation of items that havedifferent characteristics

► Consider how information has been presented for other purposes► Must not aggregate amounts from different reportable segments

(ASC 280, Segment Reporting)► Disclosures need not be made for insignificant categories except in

the reconciliation

Example categories (any or all of the following)

► Reportable segment as defined in Topic 280 on segment reporting► Type of coverage (for example, major product line)► Geography (for example, country or region)► Market or type of customer (for example, personal and commercial lines of business)► Claim duration (for example, claims that have short settlement periods or claims that have long settlement periods)

Page 4 Insurance generally accepted accounting principles (GAAP) update

Disclosures about short-duration contractsSummary of disclosures

Disclosures PeriodsSupplementary

information Disaggregated ComparativeIncurred and paid claims development Annual Yes1 Yes No

Reconciliation Annual No Yes No

Incurred but not reported (IBNR)claims and claim frequency

Annual2 No Yes No

Average annual percentage payout ofincurred claims2

Annual Yes Yes No

Significant changes in methodologyand assumptions

Annual No No No

Amounts reported at present value Annual No Yes Yes

Claims and claim adjustmentexpenses rollforward

Interim andannual

No No2 Yes

1 The disclosure is supplementary information except for the most recent reporting period.2 Health insurance claim liabilities have a modified requirement.

Page 5 Insurance generally accepted accounting principles (GAAP) update

Disclosures about short-duration contractsSummary of disclosures

► Modifications to the new disclosures for health insuranceclaim liabilities:► Average annual percentage payout of claims is not required for health

insurance claim liabilities► IBNR disclosure is required for health insurance claim liabilities in interim

and annual periods► Claim and claim adjustment expenses rollforward is disaggregated for

health insurance claim liabilities

Page 6 Insurance generally accepted accounting principles (GAAP) update

Disclosures about short-duration contractsImplementation considerations

► Incurred and paid claims development tables► Present information about the number of years for which claims incurred

typically remain outstanding, but need not exceed 10 years*► Net of risk mitigation through reinsurance

* As a practical expedient, insurers may show five years in the first year of adoption, if impracticable to obtain theinformation for more than five years, adding a year each year subsequent.

Implementation considerations► Treatment of acquisitions and disposals of insurance business► Treatment of certain reinsurance transactions► Incorporation of foreign currency translation adjustment► Differences with pre-existing disclosures, such as Schedule P and Securities Exchange

Commission’s (SEC) Management Discussion and Analysis claim development tables► Data from international insurance subsidiaries

Page 7 Insurance generally accepted accounting principles (GAAP) update

Disclosures about short-duration contractsImplementation considerations

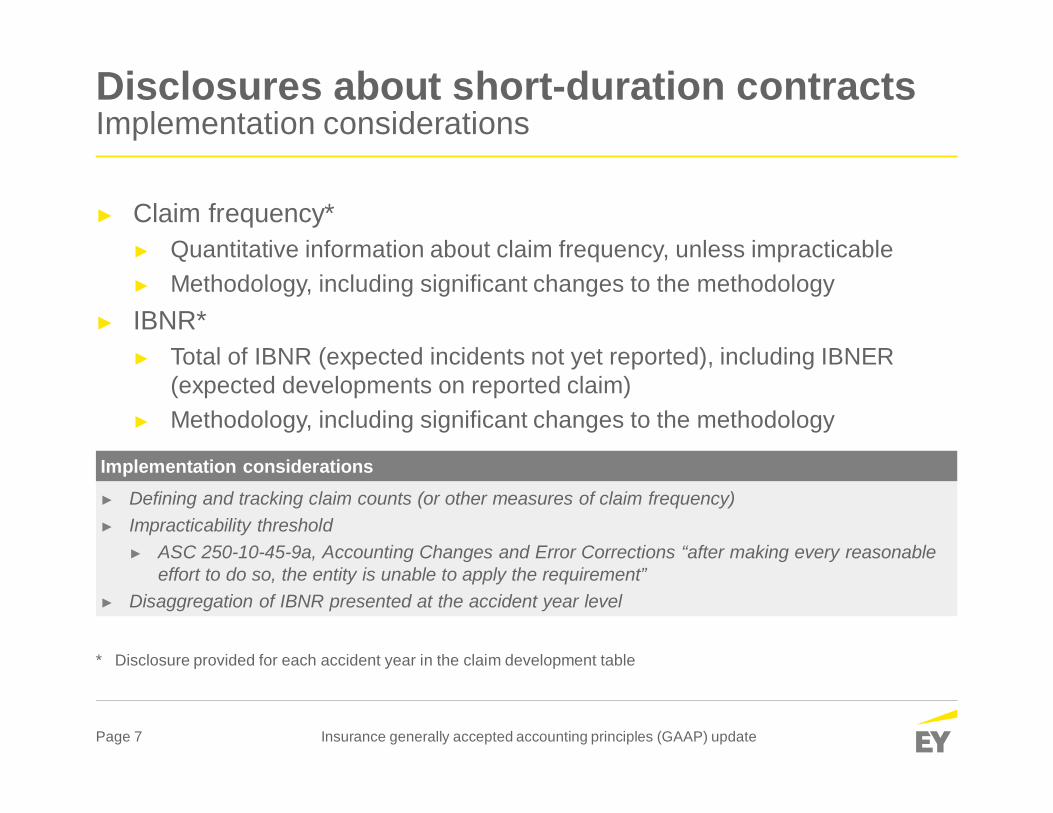

► Claim frequency*► Quantitative information about claim frequency, unless impracticable► Methodology, including significant changes to the methodology

► IBNR*► Total of IBNR (expected incidents not yet reported), including IBNER

(expected developments on reported claim)► Methodology, including significant changes to the methodology

* Disclosure provided for each accident year in the claim development table

Implementation considerations► Defining and tracking claim counts (or other measures of claim frequency)► Impracticability threshold

► ASC 250-10-45-9a, Accounting Changes and Error Corrections “after making every reasonableeffort to do so, the entity is unable to apply the requirement”

► Disaggregation of IBNR presented at the accident year level

Page 8 Insurance generally accepted accounting principles (GAAP) update

Disclosures about short-duration contractsAppendix A – Illustrative example

Incurred claims and allocated claim adjustment expenses, net of reinsuranceFor the years ended December 31

Accidentyear 20X5 20X6 20X7 20X8 20X9 20Y0 20Y1 20Y2 20Y3 20Y420X5 $25,292 $24,107 $22,971 $22,421 $22,223 $22,143 $25,208 $25,064 $25,016 $25,109

20X6 27,693 26,312 25,743 25,335 25,177 27,534 27,369 27,328 27,437

20X7 27,288 26,801 26,536 26,545 28,713 28,590 28,498 28,551

20X8 26,265 26,620 26,962 28,982 28,941 28,953 29,030

20X9 24,367 24,592 26,172 26,319 26,202 26,331

20Y0 24,099 26,512 26,757 26,699 26,871

20Y1 27,072 27,346 27,515 27,729

20Y2 28,126 27,552 27,618

20Y3 28,248 27,982

20Y4 29,073

Total $275,731

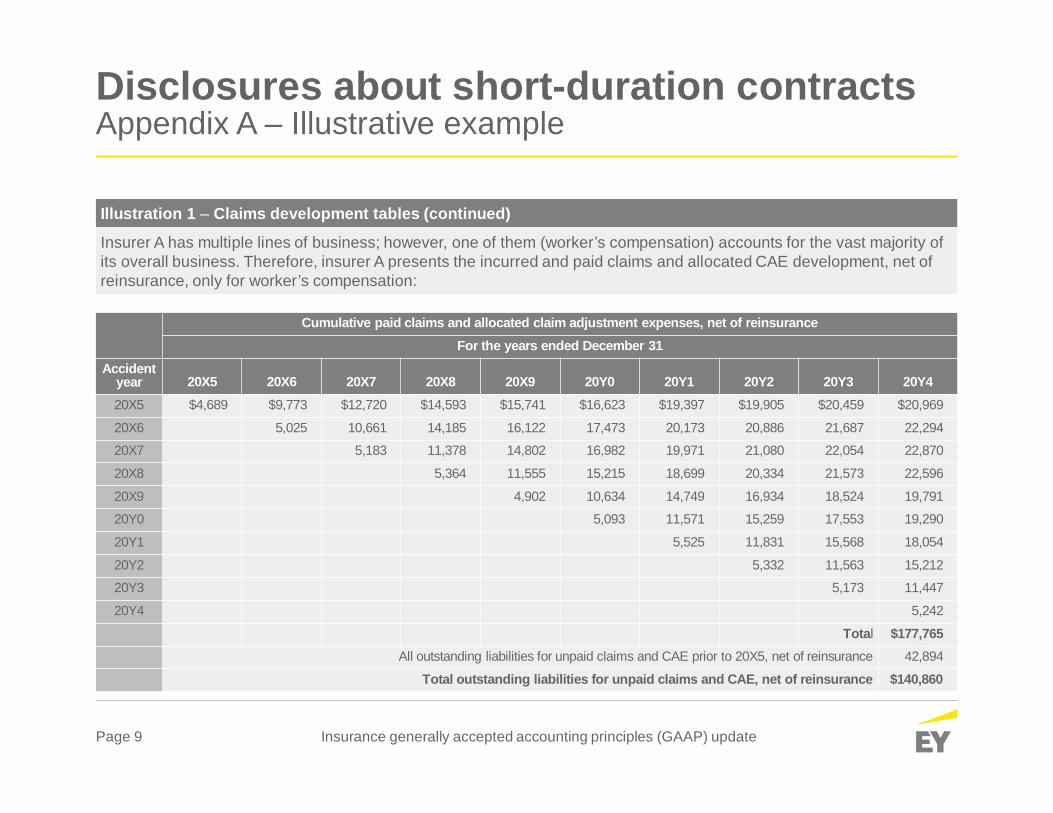

Illustration 1 – Claims development tables

Insurer A has multiple lines of business; however, one of them (worker’s compensation) accounts for the vast majority ofits overall business. Therefore, insurer A presents the incurred and paid claims and allocated claim adjustment expenses(CAE) development, net of reinsurance, only for worker’s compensation:

Page 9 Insurance generally accepted accounting principles (GAAP) update

Disclosures about short-duration contractsAppendix A – Illustrative example

Cumulative paid claims and allocated claim adjustment expenses, net of reinsuranceFor the years ended December 31

Accidentyear 20X5 20X6 20X7 20X8 20X9 20Y0 20Y1 20Y2 20Y3 20Y420X5 $4,689 $9,773 $12,720 $14,593 $15,741 $16,623 $19,397 $19,905 $20,459 $20,969

20X6 5,025 10,661 14,185 16,122 17,473 20,173 20,886 21,687 22,294

20X7 5,183 11,378 14,802 16,982 19,971 21,080 22,054 22,870

20X8 5,364 11,555 15,215 18,699 20,334 21,573 22,596

20X9 4,902 10,634 14,749 16,934 18,524 19,791

20Y0 5,093 11,571 15,259 17,553 19,290

20Y1 5,525 11,831 15,568 18,054

20Y2 5,332 11,563 15,212

20Y3 5,173 11,447

20Y4 5,242

Total $177,765All outstanding liabilities for unpaid claims and CAE prior to 20X5, net of reinsurance 42,894

Total outstanding liabilities for unpaid claims and CAE, net of reinsurance $140,860

Illustration 1 – Claims development tables (continued)

Insurer A has multiple lines of business; however, one of them (worker’s compensation) accounts for the vast majority ofits overall business. Therefore, insurer A presents the incurred and paid claims and allocated CAE development, net ofreinsurance, only for worker’s compensation:

Page 10 Insurance generally accepted accounting principles (GAAP) update

Disclosures about short-duration contractsAppendix A – Illustrative example

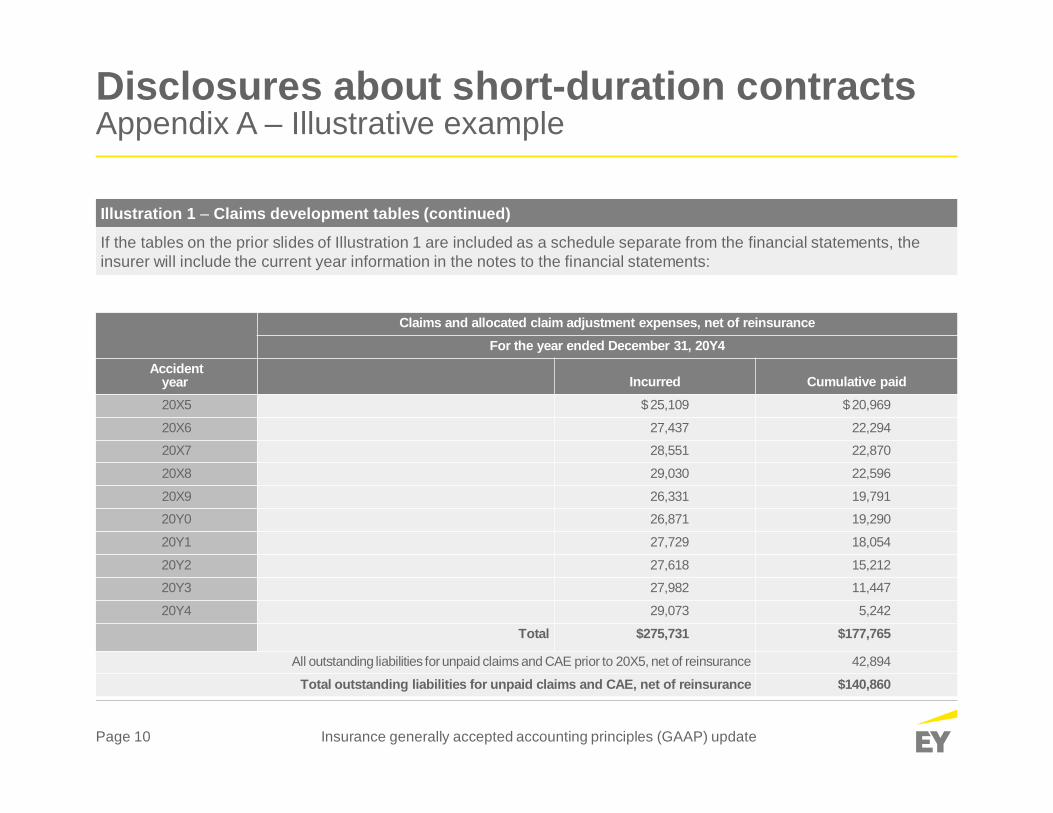

Illustration 1 – Claims development tables (continued)

If the tables on the prior slides of Illustration 1 are included as a schedule separate from the financial statements, theinsurer will include the current year information in the notes to the financial statements:

Claims and allocated claim adjustment expenses, net of reinsuranceFor the year ended December 31, 20Y4

Accidentyear Incurred Cumulative paid20X5 $25,109 $20,969

20X6 27,437 22,294

20X7 28,551 22,870

20X8 29,030 22,596

20X9 26,331 19,791

20Y0 26,871 19,290

20Y1 27,729 18,054

20Y2 27,618 15,212

20Y3 27,982 11,447

20Y4 29,073 5,242

Total $275,731 $177,765

All outstanding liabilities for unpaid claims and CAE prior to 20X5, net of reinsurance 42,894

Total outstanding liabilities for unpaid claims and CAE, net of reinsurance $140,860

Page 11 Insurance generally accepted accounting principles (GAAP) update

Disclosures about short-duration contractsAppendix A – Illustrative example

Illustration 2 – Reconciliation of the claims development information to the consolidated statement offinancial position

Insurer A includes the following disclosure, reconciling the worker’s compensation claims development tables to theliability for claims and CAE in the consolidated statement of financial position. This disclosure is included in the notes tothe financial statements:

December 3120Y4

Net outstanding liabilities for unpaid claims and CAE

Worker’s compensation $140,860

Other insurance lines 12,678

Liabilities for unpaid claims and allocated CAE, net of reinsurance 153,538

Reinsurance recoverable on unpaid claims

Worker’s compensation $41,790

Other insurance lines 11,410

Total reinsurance recoverable on unpaid claims 53,200Unallocated claims adjustment expenses 7,440

Insurance lines other than short duration 704

Impact of discounting 3,755

Total gross liability for unpaid claims and CAE $218,637

Page 12 Insurance generally accepted accounting principles (GAAP) update

Disclosures about short-duration contractsAppendix A – Illustrative example

Illustration 3 – IBNR claims and claims frequency

Insurer A includes the disclosure below about IBNR liabilities and claims frequency. In addition, to show the relationshipof the IBNR liabilities and the claims frequency for each accident year presented, Insurer A has included the cumulativeincurred claims and CAE from the most recent reporting year from the claims development tables:

Accidentyear

As of December 31, 20Y4Incurred claims and allocatedclaim adjustment expenses,

net of reinsurance

Total of incurred but not reportedliabilities plus expected

development on reported claimsCumulative number of

reported claims20X5 $25,109 $1,970 4,140

20X6 27,437 2,596 4,063

20X7 28,551 2,893 3,846

20X8 29,030 3,463 3,519

20X9 26,331 3,622 3,033

20Y0 26,871 4,196 3,063

20Y1 27,729 5,490 3,049

20Y2 27,618 7,311 2,956

20Y3 27,982 10,030 2,856

20Y4 29,073 16,191 2,580

Page 13 Insurance generally accepted accounting principles (GAAP) update

Disclosures about short-duration contractsAppendix A – Illustrative example

Illustration 4 – Claims duration disclosure

Insurer A provides the following disclosure of the average annual percentage payout of incurred claims by age, net ofreinsurance, for the worker’s compensation line of business as supplementary information as of 31 December 20Y4:

Average annual percentage payout of incurred claims by age, net of reinsuranceYear 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Worker’scompensation 18.7% 21.9% 13.2% 8.6% 6.3% 5.3% 5.1% 2.6% 2.2% 2.0%

Page 14 Insurance generally accepted accounting principles (GAAP) update

Disclosures about short-duration contractsAppendix A – Illustrative example

Illustration 5 – Liabilities for unpaid claims and CAE that are reported at fair value

Insurer A includes the following disclosures for the worker’s compensation line of business that is reported at fair value:

Liabilities for unpaid claims and claim adjustment expenses presented at present valueCarrying amount of

liabilities for unpaid claimsand claim adjustment

expenses Discount rateAggregate amount

of discount Interest accretion

As of 31 December As of 31 December As of 31 DecemberFor the years ended

31 December

20Y4 20Y3 20Y4 20Y3 20Y4 20Y3 20Y4 20Y3Worker’scompensation $140,860 $136,717 2.8% 3% $3,755 $4,250 $395 $410

Page 15 Insurance generally accepted accounting principles (GAAP) update

Long-duration contractsAgenda

► Overview► Liability for future policyholder benefits► Deferred policy acquisition costs► Disclosures► Transition

Page 16 Insurance generally accepted accounting principles (GAAP) update

Long-duration contractsOverview

► In April 2014, the Financial Accounting Standards Board (FASB)determined the areas of targeted improvements to accounting forlong-duration contracts, including:► Update assumptions periodically on the liability for future

policyholder benefits► Simplify deferred policy acquisition costs (DAC) amortization methods► Enhance disclosure requirements

► Project status► Board completed targeted improvement decisions in March 2016► Exposure draft expected in Q3 2016► Sweep issues may be addressed in drafting phase or comment

period process

Page 17 Insurance generally accepted accounting principles (GAAP) update

Long-duration contractsLiability for future policyholder benefits

Traditional, limited payment and participating contracts

Current GAAP Proposed GAAP

Cash flowassumptions

► Locked in at contract initiation► Include provision for adverse

deviation (PAD)

► Updated at least annually► Retrospective updates recorded in

current earnings► No PAD

Discount rateassumption

► Expected investment yield approach forcertain contracts

► Participating contracts apply a hierarchyapproach

► Based on a portfolio of high-quality,fixed-income investments

► Locked in at initiation ► Prospectively updated quarterly► Updates recorded in other comprehensive

income (OCI)

Participating contractassumptions

► Model includes only discount rate andmortality assumptions

► Include the following assumptions in themodel: mortality, discount rate, investmentyield, terminations, expenses,dividend payments

Periodic assessment ► Loss recognition/premium deficiency test ► Assessment no longer required

Page 18 Insurance generally accepted accounting principles (GAAP) update

Long-duration contractsLiability for future policyholder benefits

Additional liability on non-traditional contracts (e.g., ULSG)

Current GAAP Proposed GAAP

Assumptions ► Evaluated and updated regularly► Retrospective approach

► Cash flow assumptions updated atleast annually

► Discount rate* updated quarterly

Certain market risk benefits in separate accounts (e.g., variable annuity GMDB)

Current GAAP Proposed GAAP

Valuation model ► Guarantees may be accounted for underthe benefit ratio model or as anembedded derivative

► Recorded at fair value► Changes in fair value recorded in current

earnings except effect of own-credit riskrecorded in OCI

Presentation ► No specific requirements topresent separately

► Report separately in the balance sheet andincome statement

* The methodology to determine the discount rate did not change.

Page 19 Insurance generally accepted accounting principles (GAAP) update

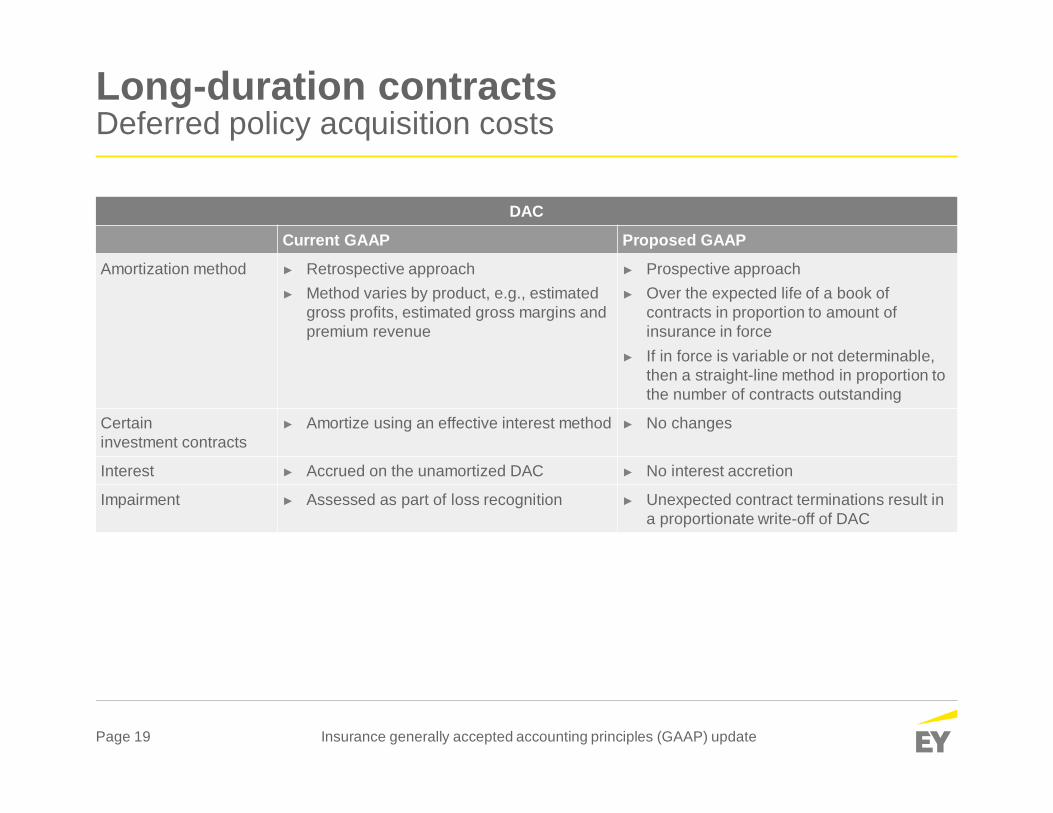

Long-duration contractsDeferred policy acquisition costs

DAC

Current GAAP Proposed GAAP

Amortization method ► Retrospective approach► Method varies by product, e.g., estimated

gross profits, estimated gross margins andpremium revenue

► Prospective approach► Over the expected life of a book of

contracts in proportion to amount ofinsurance in force

► If in force is variable or not determinable,then a straight-line method in proportion tothe number of contracts outstanding

Certaininvestment contracts

► Amortize using an effective interest method ► No changes

Interest ► Accrued on the unamortized DAC ► No interest accretion

Impairment ► Assessed as part of loss recognition ► Unexpected contract terminations result ina proportionate write-off of DAC

Page 20 Insurance generally accepted accounting principles (GAAP) update

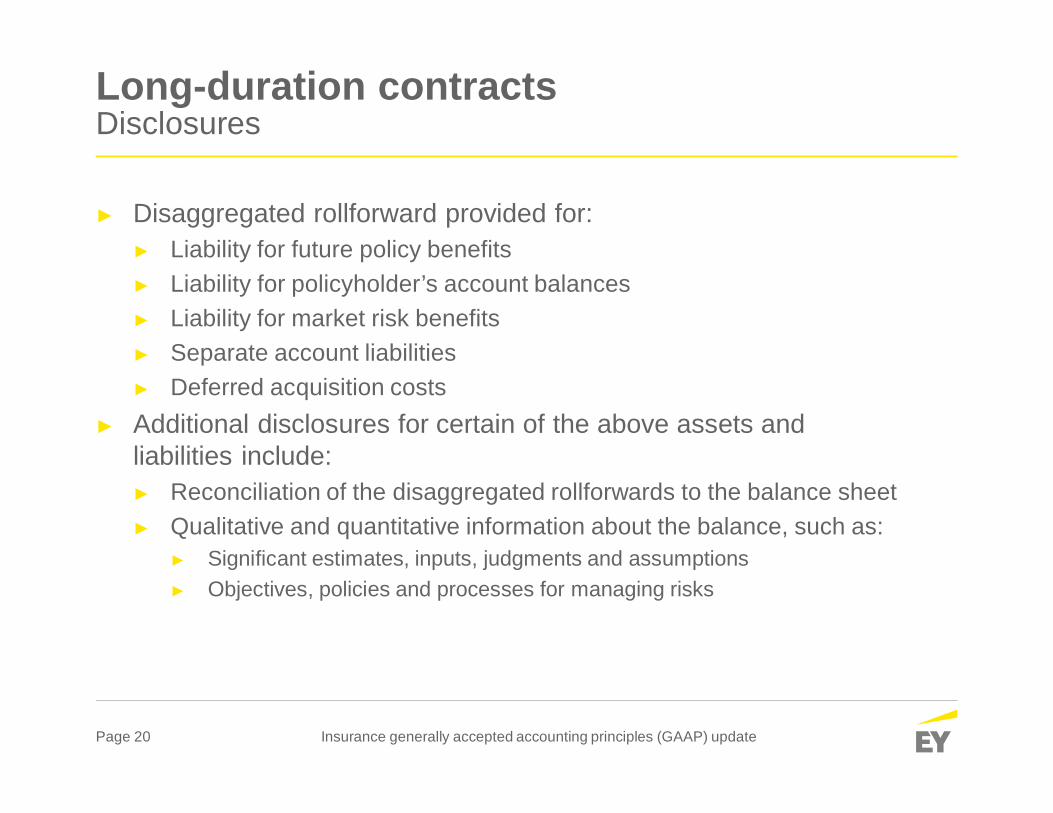

Long-duration contractsDisclosures

► Disaggregated rollforward provided for:► Liability for future policy benefits► Liability for policyholder’s account balances► Liability for market risk benefits► Separate account liabilities► Deferred acquisition costs

► Additional disclosures for certain of the above assets andliabilities include:► Reconciliation of the disaggregated rollforwards to the balance sheet► Qualitative and quantitative information about the balance, such as:

► Significant estimates, inputs, judgments and assumptions► Objectives, policies and processes for managing risks

Page 21 Insurance generally accepted accounting principles (GAAP) update

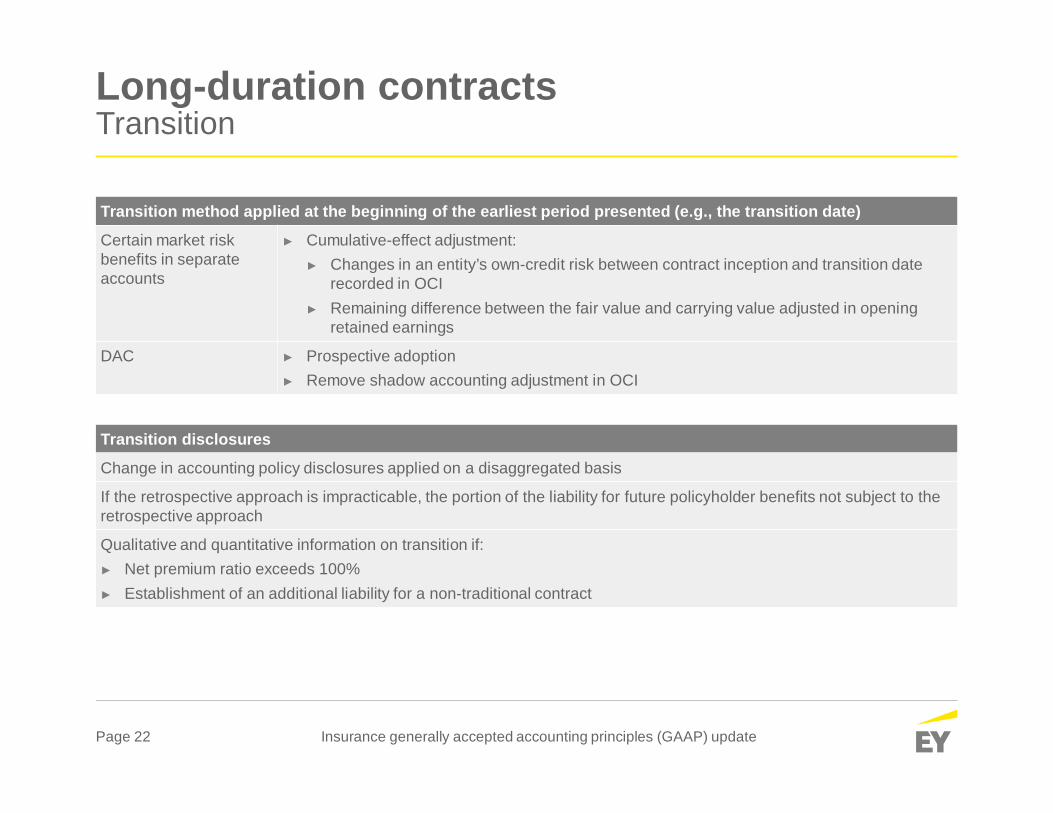

Long-duration contractsTransition

Transition method applied at the beginning of the earliest period presented (e.g., the transition date) for theliability for future policyholder benefits

Cash flow assumptions ► Retrospective approach for each level at which reserves are calculated:► Use actual historical information at the level reserves are calculated► If approach not possible, use objective information to estimate the information at the

appropriate level► If impracticable to apply a retrospective approach:

► Apply guidance to in-force contracts on the basis of their existing carrying amounts atthe transition date and updated future assumptions

► Under this approach, transition date should be considered the contract inception date forpurposes of subsequent adjustments

Discount rate ► Cumulative-effect adjustment of changes in discount rates between contract inception andtransition date recorded in OCI.

Page 22 Insurance generally accepted accounting principles (GAAP) update

Long-duration contractsTransition

Transition disclosures

Change in accounting policy disclosures applied on a disaggregated basis

If the retrospective approach is impracticable, the portion of the liability for future policyholder benefits not subject to theretrospective approach

Qualitative and quantitative information on transition if:► Net premium ratio exceeds 100%► Establishment of an additional liability for a non-traditional contract

Transition method applied at the beginning of the earliest period presented (e.g., the transition date)

Certain market riskbenefits in separateaccounts

► Cumulative-effect adjustment:► Changes in an entity’s own-credit risk between contract inception and transition date

recorded in OCI► Remaining difference between the fair value and carrying value adjusted in opening

retained earnings

DAC ► Prospective adoption► Remove shadow accounting adjustment in OCI

Page 23 Insurance generally accepted accounting principles (GAAP) update

Revenue recognitionAgenda

► Overview► Scope for insurance companies► Insurance industry issues

Page 24 Insurance generally accepted accounting principles (GAAP) update

Revenue recognitionOverview

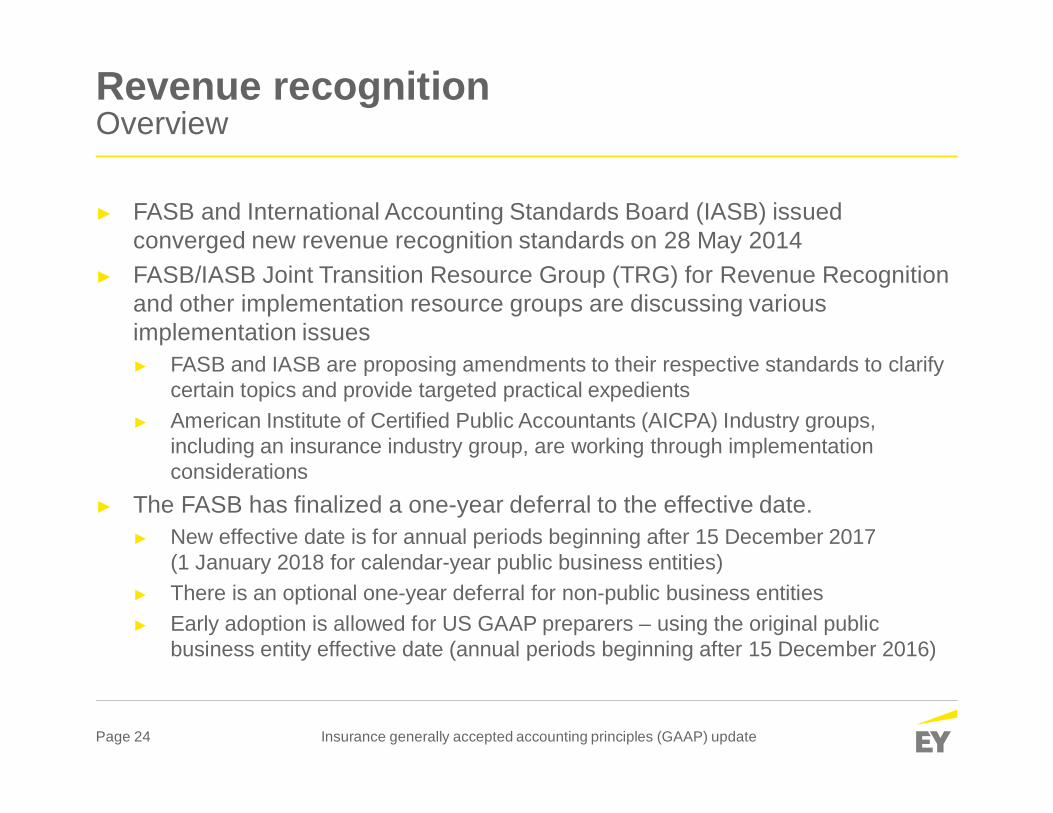

► FASB and International Accounting Standards Board (IASB) issuedconverged new revenue recognition standards on 28 May 2014

► FASB/IASB Joint Transition Resource Group (TRG) for Revenue Recognitionand other implementation resource groups are discussing variousimplementation issues► FASB and IASB are proposing amendments to their respective standards to clarify

certain topics and provide targeted practical expedients► American Institute of Certified Public Accountants (AICPA) Industry groups,

including an insurance industry group, are working through implementationconsiderations

► The FASB has finalized a one-year deferral to the effective date.► New effective date is for annual periods beginning after 15 December 2017

(1 January 2018 for calendar-year public business entities)► There is an optional one-year deferral for non-public business entities► Early adoption is allowed for US GAAP preparers – using the original public

business entity effective date (annual periods beginning after 15 December 2016)

Page 25 Insurance generally accepted accounting principles (GAAP) update

Revenue recognitionScope for insurance companies

► FASB modified* scope exception in ASC 606:► “Insurance contracts within the scope of Topic 944”

► Examples of contracts in scope of ASC 606:Third-party administrator (TPA) Managed care (ASO)► Claims processing and administration services► Property appraisal services► Information risk management services

► Enrollment and member services► Claim payment adjustment and recovery

services► Subrogation services

Asset management Insurance and reinsurance brokerage► Trading and administration services► Investment management services► Business and corporate development services

► Brokerage arrangements► Agency arrangements► Advisory arrangements

* The FASB voted on this amendment in its 20 January 2016 board meeting. The FASB directed the staff to draft anexposure draft to release this decision with other technical corrections for public comment.

Page 26 Insurance generally accepted accounting principles (GAAP) update

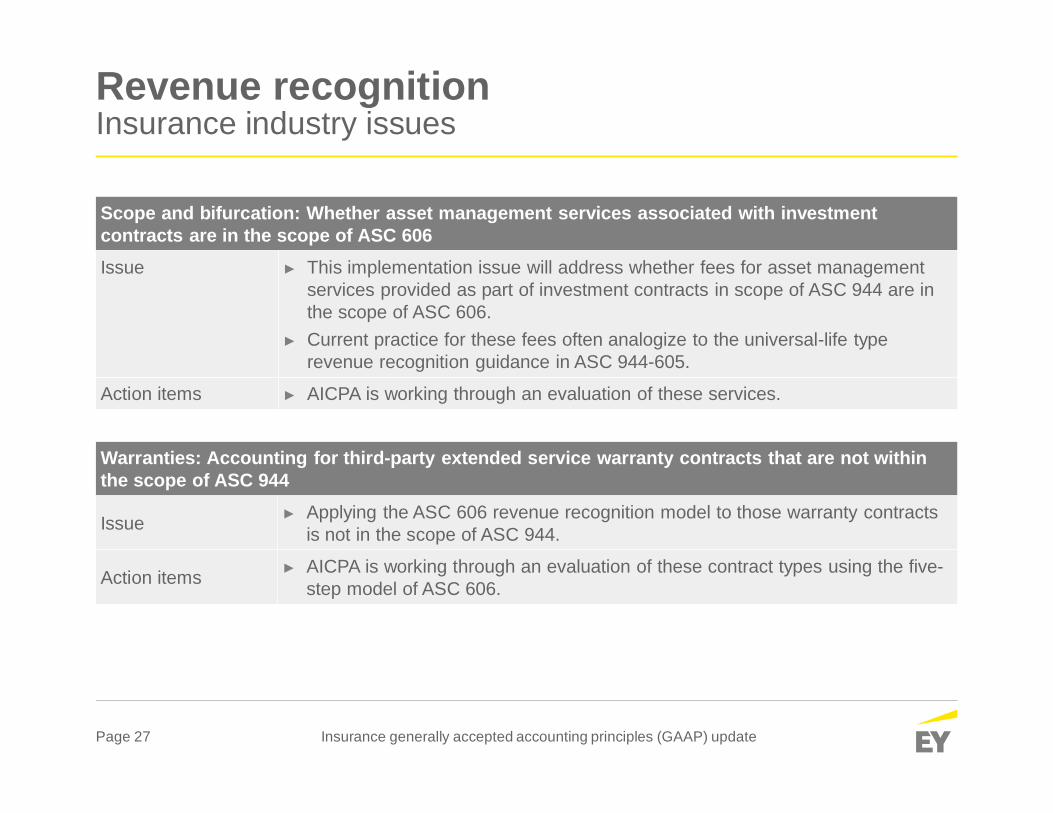

Revenue recognitionInsurance industry issues

Scope and bifurcation: Interaction of contracts accounted for under ASC 944 and the guidancein ASC 606-10-15-2 and 15-4Issue ► Whether to apply ASC 606 when there is a contract with multiple components?

Different viewpoints

► View 1: Entire contract should be scoped out of ASC 606 because insurancecontracts under ASC 944 are scoped out.

► View 2: Companies should bifurcate the components of the contract and applyASC 606 to non-insurance components.

Action items► AICPA submitted an implementation issue to the FASB for discussion.► FASB briefly discussed the concept in a January 2016 technical corrections

Board meeting, no conclusions were reached.

Page 27 Insurance generally accepted accounting principles (GAAP) update

Revenue recognitionInsurance industry issues

Scope and bifurcation: Whether asset management services associated with investmentcontracts are in the scope of ASC 606Issue ► This implementation issue will address whether fees for asset management

services provided as part of investment contracts in scope of ASC 944 are inthe scope of ASC 606.

► Current practice for these fees often analogize to the universal-life typerevenue recognition guidance in ASC 944-605.

Action items ► AICPA is working through an evaluation of these services.

Warranties: Accounting for third-party extended service warranty contracts that are not withinthe scope of ASC 944

Issue ► Applying the ASC 606 revenue recognition model to those warranty contractsis not in the scope of ASC 944.

Action items ► AICPA is working through an evaluation of these contract types using the five-step model of ASC 606.

NAIC update – Spring 2016

Page 2 NAIC update – Spring 2016

Agenda

► Statutory accounting update► NAIC initiatives► Other regulatory matters

Page 3 NAIC update – Spring 2016

Statutory accounting update

Page 4 NAIC update – Spring 2016

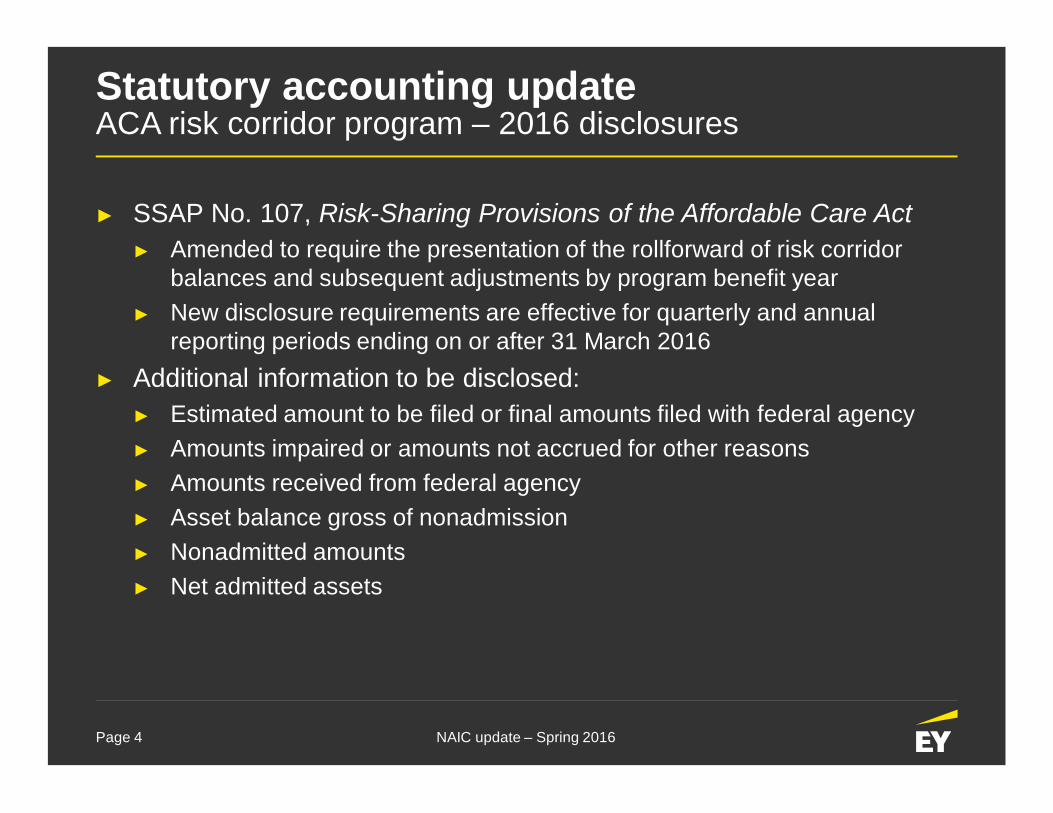

Statutory accounting updateACA risk corridor program – 2016 disclosures

► SSAP No. 107, Risk-Sharing Provisions of the Affordable Care Act► Amended to require the presentation of the rollforward of risk corridor

balances and subsequent adjustments by program benefit year► New disclosure requirements are effective for quarterly and annual

reporting periods ending on or after 31 March 2016► Additional information to be disclosed:

► Estimated amount to be filed or final amounts filed with federal agency► Amounts impaired or amounts not accrued for other reasons► Amounts received from federal agency► Asset balance gross of nonadmission► Nonadmitted amounts► Net admitted assets

Page 5 NAIC update – Spring 2016

Statutory accounting updateACA Section 9010 assessment – 2017 moratorium

► Interpretation 2016-01, ACA Section 9010 Assessment 2017Moratorium► Adopted to clarify the application of statutory guidance in SSAP No. 106,

Affordable Care Act Section 9010 Assessment for the moratoriumimposed on the payment of the health insurance provider fee for calendaryear 2017

► Effective for first quarter 2016 reporting► Consensus reached:

► Liability to be accrued on 1 January 2016 for the fee to be paid in 2016► No segregation of surplus in 2016 (or liability to be accrued on

1 January 2017) since no fee is required to be paid in 2017► Monthly segregation of surplus to resume in 2017 (and liability to be

accrued on 1 January 2018) for the fee to be paid in 2018

Page 6 NAIC update – Spring 2016

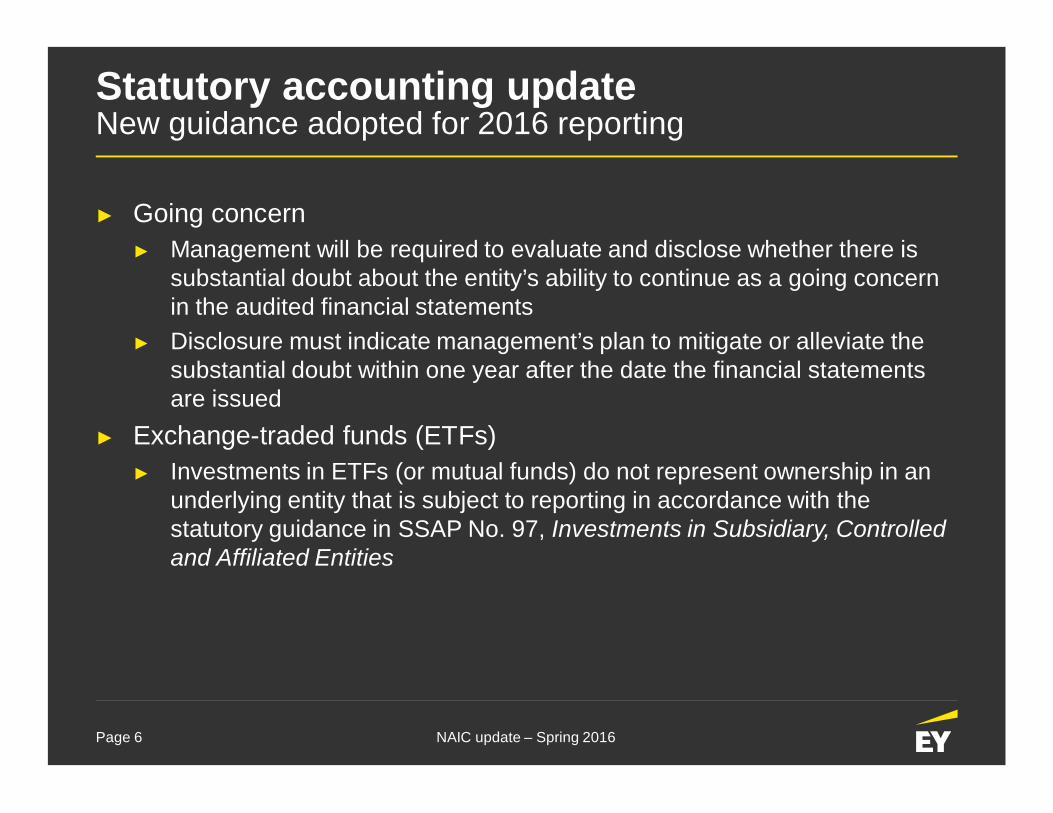

Statutory accounting updateNew guidance adopted for 2016 reporting

► Going concern► Management will be required to evaluate and disclose whether there is

substantial doubt about the entity’s ability to continue as a going concernin the audited financial statements

► Disclosure must indicate management’s plan to mitigate or alleviate thesubstantial doubt within one year after the date the financial statementsare issued

► Exchange-traded funds (ETFs)► Investments in ETFs (or mutual funds) do not represent ownership in an

underlying entity that is subject to reporting in accordance with thestatutory guidance in SSAP No. 97, Investments in Subsidiary, Controlledand Affiliated Entities

Page 7 NAIC update – Spring 2016

Statutory accounting updateNew guidance adopted for 2016 reporting

► State prescribed and permitted practices► Disclosure must indicate whether the practice is a departure from

NAIC statutory accounting practices or state prescribed practices and thefinancial statement reporting lines predominantly affected

► Requirement for the potential disclosure of all state prescribed orpermitted practices used by the reporting entity has been exposed withcomments due by 20 May 2016

► Surplus notes► Surplus notes rated with a designation equivalent of NAIC 1 or 2 to be

reported at amortized cost in accordance with revised statutory guidancein SSAP No. 41R, Surplus Notes

► Surplus notes rated with a designation equivalent of NAIC 3 to 6(or not rated) to be reported at the lower of amortized cost or fair value

Page 8 NAIC update – Spring 2016

Statutory accounting updateOther guidance under consideration

► Disclosures about short-duration contracts► Feedback requested on whether revisions to existing statutory disclosures

should be considered for reporting in both the annual statement andaudited financial statements

► Leases► Three proposed options for the revision of statutory guidance for operating

and financing leases in SSAP No. 22, Leases► Discount rate used to measure net periodic benefit cost

► Preliminary recommendation for the use of an alternative method(i.e., spot rate approach) to develop the discount rate forstatutory accounting

► Impact of a change from the weighted average approach would bereported as a change in estimate in accordance with SSAP No. 3,Accounting Changes and Corrections of Errors

Page 9 NAIC update – Spring 2016

NAIC initiatives

Page 10 NAIC update – Spring 2016

NAIC initiativesPrinciples-based reserving (PBR)

► State legislation to adopt the revised Standard Valuation Law (#820)and implement PBR as a national standard► Adopted by 42 states representing 75% of direct premiums written

(as of the NAIC Spring 2016 National Meeting)► Legislation must have been enacted with “substantially similar terms and

provisions” to the NAIC model law► Expected date for PBR implementation continues to be 1 January 2017

► Small company exemption to PBR valuation requirements► Applicable to insurers with less than US$300m and insurance groups with

less than US$600m in ordinary life premiums► Exemption required to be filed with the insurance commissioner of the

state of domicile on an annual basis if certain conditions are met

Page 11 NAIC update – Spring 2016

NAIC initiativesInvestment classification review project

► Long-term project intended to clarify and improve the statutoryaccounting and reporting for investments

► Currently focused on the statutory guidance in SSAP No. 26, Bonds► Potential revisions to SSAP No. 26 based on the proposed approach

(by BlackRock) to calculating a proxy for the “amortized cost” of a fixed-income ETF have been exposed with comments due by 20 May 2016

► Issue paper to be prepared that will incorporate the definition of a securityunder US generally accepted accounting principles (US GAAP) inSSAP No. 26 and indicate that some investments within its scope do notmeet the definition of a bond

► Issue paper to be prepared that will clarify the definition of investmentsthat are not included in the proposed bond definition for treatment asbond-like investments (i.e., Schedule D reporting)

Page 12 NAIC update – Spring 2016

NAIC initiativesRisk-based capital (RBC) developments

► Regulator intent for the consistent application of asset factors in eachof the RBC formulas by year-end 2017

► Potential update to bond factors:► Expand the NAIC designations and related factors from 6 to 20► Consideration for maintaining the current six-designation system with

updated factors for the non-life RBC formulas► Potential update to common stock factor:

► Increase the factor from 15% to 19.5% for the non-life RBC formulas► Same factor would be used for Schedule BA investments, except for the

special categories within that framework that have unique charges

Page 13 NAIC update – Spring 2016

NAIC initiativesGroup capital calculation

► US group capital calculation to be developed by the NAIC for thestate-based system of insurance regulation► RBC aggregation approach will utilize existing regulatory calculations for

entities within the insurance holding company system► Intended to improve the ability of state insurance regulators to monitor

solvency at the group level► Not intended to establish a group capital requirement

► Activities affecting the work performed by the NAIC:► Federal Reserve Board – development of a US capital standard for

domestic insurance groups subject to its regulatory authority► International Association of Insurance Supervisors (IAIS) – development

of a global insurance capital standard (ICS) for internationally activeinsurance groups (IAIGs)

Page 14 NAIC update – Spring 2016

NAIC initiativesCybersecurity

► Insurance Data Security Model Law► Exposed draft of new cybersecurity model law intended to establish the

exclusive standards for data security and investigation and notification ofa breach of data security

► Incorporates elements of two existing NAIC models, along with theguidance included in the Principles for Effective Cybersecurity and theCybersecurity Bill of Rights

► Identifies parameters for the information security program to beimplemented by licensees

► Provides the state insurance commissioner with authority to conductinvestigations and impose sanctions or monetary penalties againstlicensees that have violated provisions of the model law

Page 15 NAIC update – Spring 2016

Other regulatory matters

Page 16 NAIC update – Spring 2016

Other regulatory mattersNAIC solvency framework

► Current framework was developed to support the state-based systemof insurance regulation► Provides a uniform regulatory process, while allowing individual state

insurance commissioners to exercise discretionary authority for unusual orexceptional circumstances

► Establishes statutory accounting and reporting requirements that can bemodified by state prescribed and permitted practices

► Potential areas of improvement► Intended to address concerns that exist when single-state solutions are

implemented for multi-state problems► Not intended to eliminate the use of permitted practices► Not intended to eliminate and replace statutory accounting with US GAAP

Page 17 NAIC update – Spring 2016

Other regulatory mattersSupervision of internationally active insurance groups

► Revisions to the Insurance Holding Company System Regulatory Actadopted in 2014 to address the group-wide supervision of IAIGs► Provides states with the authority to act as a group-wide supervisor► Identification of the group-wide supervisor to be based on defined factors► Not intended to include a group capital requirement within the provisions

of the NAIC model act► State legislation to adopt the 2014 revisions:

► Adopted by 11 states, with action under consideration by an additional3 states as of 14 March 2016

► Recommendation for the inclusion of the 2014 revisions as anaccreditation requirement exposed for a one-year comment periodthat began on 1 January 2016

Page 18 NAIC update – Spring 2016

Other regulatory mattersFederal and international regulation

► Solvency II regulatory framework► Effective in the European Union on 1 January 2016► US is not currently considered an equivalent jurisdiction► Negotiations on a covered agreement for reinsurance collateral to occur at

the federal level in order to achieve equivalence► Global ICS

► Concerns raised on the rapid pace of IAIS work and the potential forunintended consequences that would affect policyholders of US-domiciledinsurance companies

► Valuation approach embedded in IAIS filed testing is representative of theSolvency II principles of market adjusted valuation

► IAIS seeking to resolve how to define and measure risk associated withnon-traditional and non-insurance activities and products

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisoryservices. The insights and quality services we deliver help build trustand confidence in the capital markets and in economies the worldover. We develop outstanding leaders who team to deliver on ourpromises to all of our stakeholders. In so doing, we play a critical rolein building a better working world for our people, for our clients andfor our communities.

EY refers to the global organization, and may refer to oneor more, of the member firms of Ernst & Young Global Limited,each of which is a separate legal entity. Ernst & YoungGlobal Limited, a UK company limited by guarantee, does notprovide services to clients. For more information about ourorganization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm ofErnst & Young Global Limited operating in the US.

© 2016 Ernst & Young LLP.All Rights Reserved.

1605-1929956ED None

This material has been prepared for general informational purposesonly and is not intended to be relied upon as accounting, tax or otherprofessional advice. Please refer to your advisors for specific advice.

ey.com