Making India Business Friendly

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS

IMPERATIVES

Vol. 2: 2015-16 December 2015

CONTENTS

Executive Summary 2-3

Ease of Doing Business 4-15

Sectoral Updates 16-33

Conclusion 34-35

Annexure 37-41

About BMR 42-43

A decade ago, India seemed

prepared to rival East Asian tiger

China. Annual growth was heading

closer to 10 percent. A growing

population, with rates of savings

and investment of over 30 percent

of GDP, was uplifting the

economy’s potential. Unlike most

East Asian countries, India was

mildly – centre strong with a weak

state, but had a brilliant

entrepreneurial streak to fast-track

the country to prosperity.

However, policy paralysis coupled

with the global crisis of 2008 took

India off the radar.

What went wrong? Primal inputs of

growth – land, labour and capital –

were marginalised. The rate of

savings and investment declined

materially and their ratio went

downhill. High ination pushed

households towards gold

accumulation, swerving money to

unproductive uses. A concoction of

ofcialdom, excessive leverage,

ineptitude and corruption led private

companies to cut investments by

nearly half. What got invested

remained tangled in red tape and

graft. The policy and constitutional

constraints on growth became

binding.

The tide is now clearly shifting. The

country’s economic plan under the

administration of Prime Minister

Narendra Modi is rightly home

grown, with a thrust towards labour

intensive industrialization. PM Modi

has spent the last 18 months in

ofce propagating far and wide the

message, ‘India is a changed

country now’. He has criss-crossed

the world promoting India as the

next industrial destination through

the ‘Make in India’ campaign.

The rst 18 months of National

Democratic Alliance (NDA) regime

has been driven by intense

reforms. The nation witnessed

increased growth rates supported

by benign external factors. There

EXECUTIVE SUMMARY

SUMMARY

2

has been a dramatic revision of

policies on various fronts. All this

has contributed towards a change

in the momentum and triggered

positivity in market sentiments. The

country is focused on launching

itself on a high, perpetual growth

trajectory. There has been a

climactic revision in GDP and

consumer price index (CPI), with an

overall growth gure for FY 2015

standing at 7.3 percent, up from 6.9

percent in FY 2014.

Economic growth is expected to

remain high, backed by a

resurgence in investment. Structural

reforms to improve the Ease of

Doing Business and Make in India

initiatives are expected to boost

corporate investment. On the other

hand, relaxation in scal

consolidation targets will propel

infrastructure spends. However, all

this is constrained by growth in

exports which is subject to demand

revival in advanced economies.

Decline in oil prices though will scale

down pressure on current account

decit, ination and subsidies.

Most argue that all India needs to do

is open up more aggressively and

disinvest stake in public sector

enterprises. However, the business

ecosystem is still weak in many

ways on enforceability of contracts,

lack of liquidity etc. Even in case of

FDI, the impediment is not legal

restrictions but business conditions

that exasperate local rms.

It is in this frame of reference that

the report outlines key issues

confronting India’s business

ecosystem and a series of recent

initiatives taken by the Government

of India (GoI), including thrust for

reforms to accelerate the growth

trajectory. The report is split into the

following sections:

Section A – Ease of doing business

in India - the theme

Section B – Key developments in

various ministries impacting

business

The rst eighteen months of NDA’s regime have been driven by intense reforms.Economic growth is expected to remain high, backed by a resurgence in investment.

3

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

A lot has changed since India rst opened its gates to embrace liberalization over

two decades ago. Back then, it was tough for entrepreneurs to envisage an

entryway into the vocational world. It took an entrepreneur years to acquire

rudimentary licences and approvals for starting a business.

EASE OF DOING BUSINESS IN INDIA

The country rightly opened up its

market for competition but in the

process overlooked the plight of

its factor markets. Land, labour

and capital continued as

challenges. The cost of capital

shot up. Complex laws made it

strenuous to acquire land for

industry or infrastructure.

Incomprehensible labour laws

muzzled manufacturers. With all

this, the country’s industrial

growth has been despondently

limping its way through a crowd of

tough competitors to nd itself a

place.

The new momentum of reforms

introduced by the NDA

government has made change

inevitable. Prime Minister Modi

rightly declared at the

inauguration of the Hannover

Messe Fair in Germany in early

2015 that “India is a changed

country now”. Several economic

ministers led by the PM spanned

the world promoting India as the

next industrial destination. The

vision of Make in India could not

have come at a better time. The

economy imparts a hopeful

picture and is on path of steady

and palpable reformation. The

campaign has received

overwhelming response from

both Indian and global investors.

The World Bank’s Ease of Doing

Business Report 2016, is an

emphatic acknowledgment of the

efforts of the government to make

India a business friendly country.

With the new rankings, India has

shot up 12 spots and has secured th

the 130 position up from earlier nd142 among 189 countries.

According to World Bank’s Chief

India is achanged

country now

SECTION A: EASE OF DOING BUSINESS IN INDIA

4

Economist and Vice President Kaushik Basu,

“For any big economy, a rank improvement

of 12 is a remarkable achievement. Going

from 142 in the world to 130, as India has

done, is very good sign. It gives a good

signal about the way things are moving in

India”. The report takes into account data till

June 2015 and is based on a new

methodology adopted for compiling the

ranks both this year and last year.

Two key reforms in India were responsible for

the improved ranking: the elimination of the

requirements for a paid-in minimum capital

and a certicate to commence business

operations. Beyond these reforms, the Indian

government has sought to address a number

of other ease of doing business issues

through a state by state approach, such as

utilities connections, construction permits,

minority investor protection and property

registration, amongst others.

De facto, this is a time of great expectations

for the country and is plausibly the only time

in recent past when our chances of

unshackling industrial growth are very high.

The new government has not missed a

chance to lure investors pitching the idea of

manufacturing in India. It has pledged to

vault India into the top 50 countries in World

Banks’s Ease of Doing Business rankings.

5

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

EASE OF DOING BUSINESS IS RECOGNISED AS THE SINGLE MOST IMPORTANT FACTOR TO PROMOTE ENTREPRENEURSHIP.

6

SECTION A: EASE OF DOING BUSINESS IN INDIA

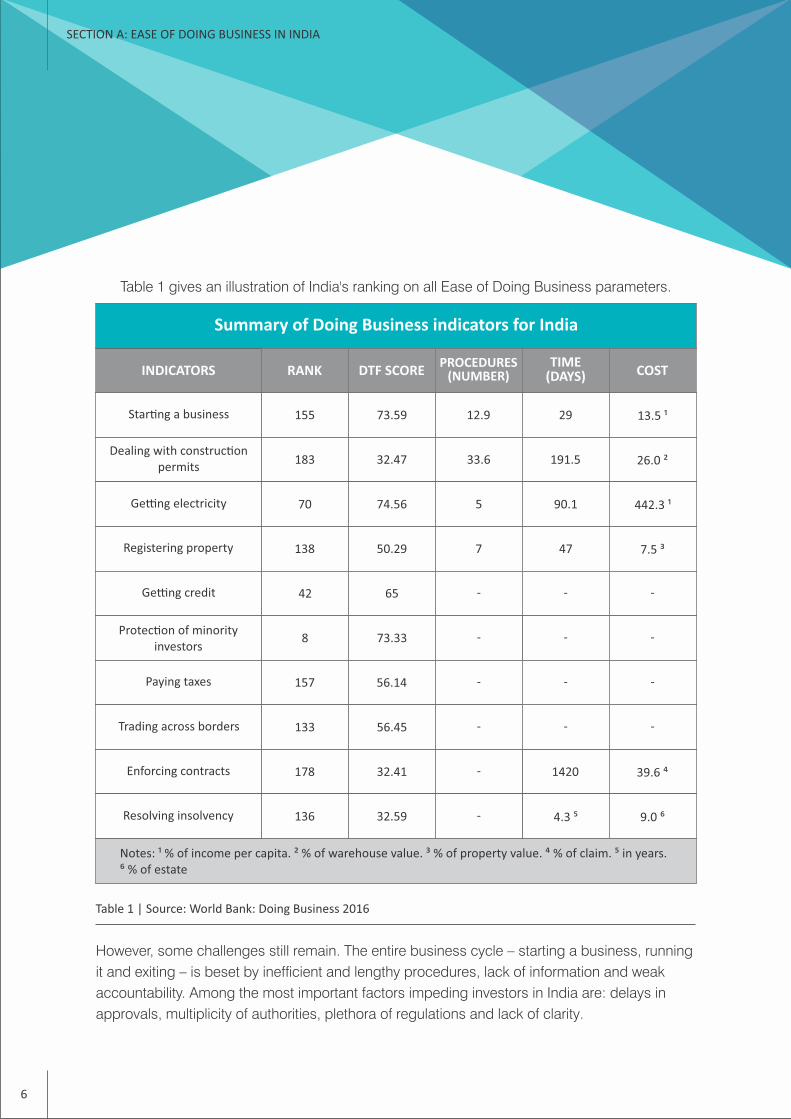

Table 1 gives an illustration of India's ranking on all Ease of Doing Business parameters.

However, some challenges still remain. The entire business cycle – starting a business, running

it and exiting – is beset by inefcient and lengthy procedures, lack of information and weak

accountability. Among the most important factors impeding investors in India are: delays in

approvals, multiplicity of authorities, plethora of regulations and lack of clarity.

Table 1 | Source: World Bank: Doing Business 2016

INDICATORS RANK DTF SCOREPROCEDURES

(NUMBER)TIME

(DAYS) COST

Star�ng a business

Dealing with construc�on permits

Ge�ng electricity

Registering property

Ge�ng credit

Protec�on of minority investors

Paying taxes

Trading across borders

Enforcing contracts

Resolving insolvency

155

183

70

138

42

8

157

133

178

136

73.59

32.47

74.56

50.29

65

73.33

56.14

56.45

1420

4.3 ⁵

32.41

32.59

12.9

33.6

5

7

29

191.5

90.1

47

13.5 ¹

26.0 ²

442.3 ¹

7.5 ³

39.6 ⁴

9.0 ⁶

---

-

-

-

-

-

- -

- -

- -

Notes: ¹ % of income per capita. ² % of warehouse value. ³ % of property value. ⁴ % of claim. ⁵ in years. ⁶ % of estate

Summary of Doing Business indicators for India

7

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

Realizing the urgency, the government has

gone into overdrive announcing and

executing signicant institutional reforms. It

has realized the enormous task to provide

the right ecosystem and amenities for its

business enterprises of all forms to succeed.

Policy stance over the last few months has

been centre-right with a clear focus on

reducing bureaucratic red tape. Pace of

decision making has picked-up. Reforms to

improve the ease of doing business are

underway but cyclical headwinds might delay

their impact. Progress on labour reforms,

relaxation of procedurally complex

environmental rules, and removal of

bottlenecks in the energy sector have largely

exceeded expectations.

Plan of Action: Making it easier

Ease of Doing Business is recognized as the

single most important factor to promote

entrepreneurship. A number of initiatives

have been initiated during last 18 months in

this direction. The aim is to de-license and

deregulate industry in its entire business

lifecycle. The government has partnered with

states to make things simple at

implementation level. Meanwhile, it is

ensuring greater market access for Indian

industry across various trade pacts it is

negotiating.

Recent steps by the government towards

Ease of Doing Business include initiatives

which increase the speed at which protocols

are met with, and increased transparency:

Ÿ Starting a business: The Companies

(Amendment) Act, 2015, has been passed

which waives the obligation of minimum

paid-up capital for companies and need

of a common seal. Employer’s registration

with Employees State Insurance

Corporation (ESIC) and Employees

Provident Fund Organisation (EPFO) has

been made real time. Payments can now

be made online with 56 accredited banks.

There is now a single process for

company incorporation, allotment of

MAKING THE PIECES FIT PERFECTLYTHE GOVERNMENT HAS LAUNCHED A SERIES OF INITIATIVES TO ENCOURAGE AND FACILITATE INVESTMENT IN INDIA, MAKING THE PROCESS SIMPLER AND FASTER

8

SECTION A: EASE OF DOING BUSINESS IN INDIA

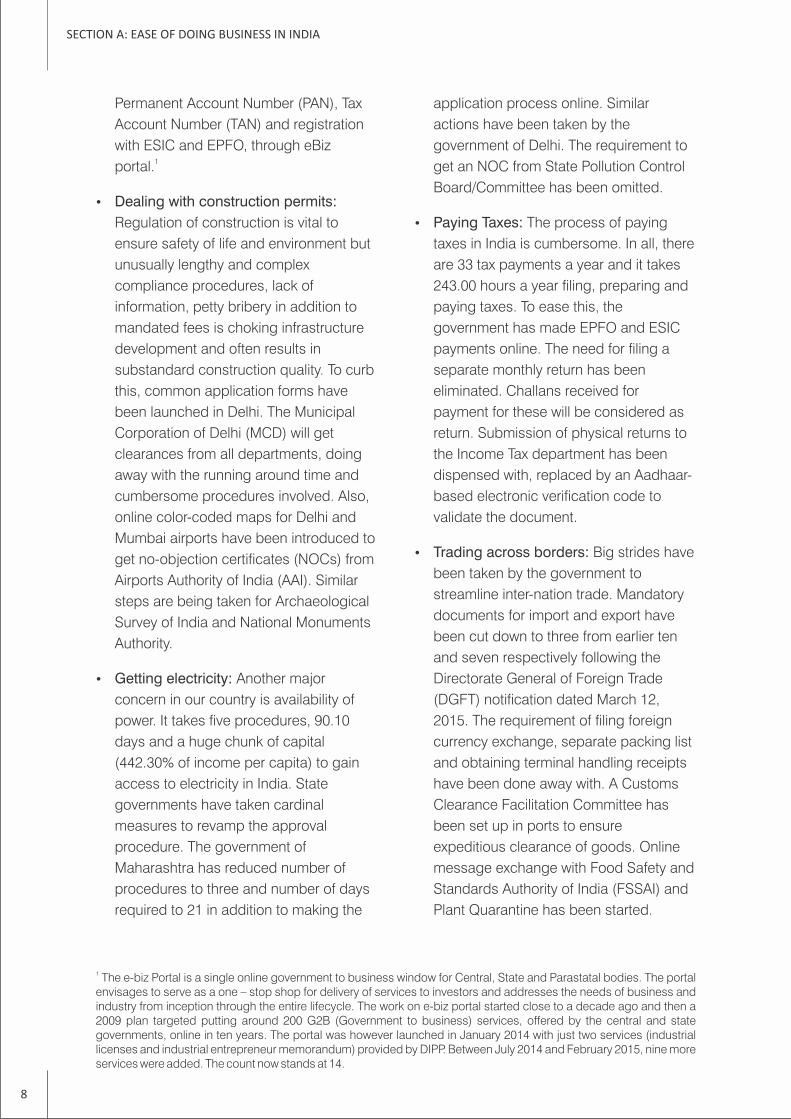

Permanent Account Number (PAN), Tax

Account Number (TAN) and registration

with ESIC and EPFO, through eBiz 1portal.

Ÿ Dealing with construction permits:

Regulation of construction is vital to

ensure safety of life and environment but

unusually lengthy and complex

compliance procedures, lack of

information, petty bribery in addition to

mandated fees is choking infrastructure

development and often results in

substandard construction quality. To curb

this, common application forms have

been launched in Delhi. The Municipal

Corporation of Delhi (MCD) will get

clearances from all departments, doing

away with the running around time and

cumbersome procedures involved. Also,

online color-coded maps for Delhi and

Mumbai airports have been introduced to

get no-objection certicates (NOCs) from

Airports Authority of India (AAI). Similar

steps are being taken for Archaeological

Survey of India and National Monuments

Authority.

Ÿ Getting electricity: Another major

concern in our country is availability of

power. It takes ve procedures, 90.10

days and a huge chunk of capital

(442.30% of income per capita) to gain

access to electricity in India. State

governments have taken cardinal

measures to revamp the approval

procedure. The government of

Maharashtra has reduced number of

procedures to three and number of days

required to 21 in addition to making the

application process online. Similar

actions have been taken by the

government of Delhi. The requirement to

get an NOC from State Pollution Control

Board/Committee has been omitted.

Ÿ Paying Taxes: The process of paying

taxes in India is cumbersome. In all, there

are 33 tax payments a year and it takes

243.00 hours a year ling, preparing and

paying taxes. To ease this, the

government has made EPFO and ESIC

payments online. The need for ling a

separate monthly return has been

eliminated. Challans received for

payment for these will be considered as

return. Submission of physical returns to

the Income Tax department has been

dispensed with, replaced by an Aadhaar-

based electronic verication code to

validate the document.

Ÿ Trading across borders: Big strides have

been taken by the government to

streamline inter-nation trade. Mandatory

documents for import and export have

been cut down to three from earlier ten

and seven respectively following the

Directorate General of Foreign Trade

(DGFT) notication dated March 12,

2015. The requirement of ling foreign

currency exchange, separate packing list

and obtaining terminal handling receipts

have been done away with. A Customs

Clearance Facilitation Committee has

been set up in ports to ensure

expeditious clearance of goods. Online

message exchange with Food Safety and

Standards Authority of India (FSSAI) and

Plant Quarantine has been started.

1 The e-biz Portal is a single online government to business window for Central, State and Parastatal bodies. The portal envisages to serve as a one – stop shop for delivery of services to investors and addresses the needs of business and industry from inception through the entire lifecycle. The work on e-biz portal started close to a decade ago and then a 2009 plan targeted putting around 200 G2B (Government to business) services, offered by the central and state governments, online in ten years. The portal was however launched in January 2014 with just two services (industrial licenses and industrial entrepreneur memorandum) provided by DIPP. Between July 2014 and February 2015, nine more services were added. The count now stands at 14.

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

Ÿ Enforcing contracts: When it comes to

enforcing a contract, there is a heavy

legislative meshwork. Contract

enforcement takes 1420 days and costs

39.60% of the value of the claim. There

are fast track procedures for small

claims, laws are in place to set overall

time standards for key court events in a

civil case. Commercial divisions have

been created in Delhi and Mumbai high

courts for hearing commercial cases.

Two benches in original jurisdiction for

suits involving commercial disputes, two

division benches in appellate jurisdiction

for appeals, two benches in original

jurisdiction for arbitration and one bench

for exclusively dealing with tax matters

have been set up. Besides, one court

each has been designated to deal with

commercial disputes in each district

court. Government has cleared

amendments made to the Arbitration

and Conciliation Act, 1996, specifying

deadlines for awards by tribunals and

incentivising expeditious disposal of

cases.

Ÿ Resolving insolvency: Entry of new

companies and exit of failed ones is part

of the business cycle. There are many

pending litigations related to insolvency

in National Company Law Tribunal due

to the cumbersome process involved.

Realising this, the Ministry of Micro Small

and Medium Enterprises (MSME) has

facilitated revival and rehabilitation of

sick MSMEs through a bankers

committee. The government is working

towards bringing a new bankruptcy law

that will allow faster closure of business

and give investors an easy exit.

Ÿ Getting credit: Globally, India stands at

42 on the ease of getting credit. Credit

information systems provide details of

the borrower's nancial history to

calculate risks. The presence of sound

laws for secured transactions and strong

legal rights for borrowers and lenders

helps businesses to have a better

access to credit.

Ÿ Protecting minority investors: India

stands at number 8 on the strength of

minority investor protection index. A

stronger index protects minority

investors from conict of interest and

indicates the presence of strong

economic regulations in this area.

India strengthened minority investor

protections by requiring greater

disclosure of conicts of interest by

board members, increasing the

remedies available in case of prejudicial

related party transactions and

introducing additional safeguards for

shareholders of privately held

companies.

There is an obvious and direct relation

between ‘Ease of Doing Business’ and

‘Make in India’. Investors are often wary of

starting up any business in India because it

includes various impediments. Recent

steps enumerated above are directed

towards removing such impediments and

making it easier to do business. This will

naturally attract investors who were earlier

reluctant to invest in India thus, boosting

the Make in India programme.

9

Ease of Doing Business – The Tax Regime

Income tax compliance forms part of the overall tax compliance cost which impacts the ease of

doing business. India's income tax administration has simplied the pre-audit logistics for

businesses by implementing electronic tax payments and return lings. However, it is the

subsequent audit and dispute resolution process which forms a substantial part of the current

tax compliance cost. In 2013:

2Ÿ Less than half of pending scrutiny audits were completed - a 59 percent pendency

Ÿ Less than a third of the pending appeals before departmental Commissioners were 3

completed - a 71 percent pendency

Ÿ Pending appeals numbered about 200,000 for departmental Commissioners, 30,000 each for 4tribunals and High Courts and 5000 for the Supreme Court

5Ÿ Transfer pricing adjustments in assessments were in excess of INR 590 billion

Ÿ Total taxes in dispute jumped from about 15 percent to more than 30 percent of total direct

tax collections

2 CAG Audit Report 2013-143 Ibid4 Annual Report 2013-14, Ministry of Finance5 Ibid

0

100000

200000

300000

400000

500000

14.79% 16.41% 14.27%

33.94% 41.56%

2009-10 2010-11 2011-12 2012-13 2013-140.00%

20.00%

40.00%

60.00%

80.00%

100.00%

Direct tax collec�on Taxes in dispute Percentage

Source: Figures from Receipts Budgets, 2009 to 2013

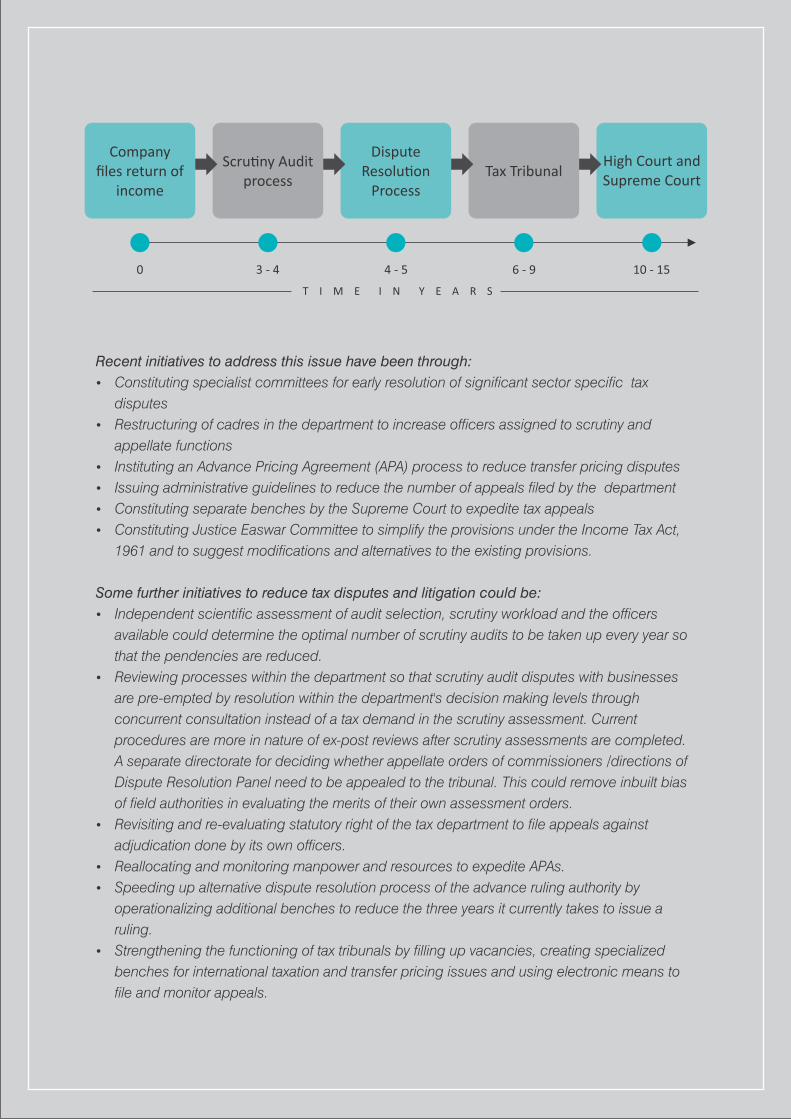

From the date of ling of a company return, it takes the department about 5 years to complete a

scrutiny audit (which is typically nalised only by the statutory outer limit) and adjudicate the rst

level of appeal. Considering further appeals to tax tribunals, High Courts and the Supreme Court,

it takes more than a decade for a scrutiny audit to reach certainty in an ongoing cycle for the

business.

Company files return of

income

Scru�ny Audit process

Dispute Resolu�on

ProcessTax Tribunal

High Court and Supreme Court

0 3 - 4 4 - 5 6 - 9 10 - 15

T I M E I N Y E A R S

Recent initiatives to address this issue have been through:

Ÿ Constituting specialist committees for early resolution of signicant sector specic tax

disputes

Ÿ Restructuring of cadres in the department to increase ofcers assigned to scrutiny and

appellate functions

Ÿ Instituting an Advance Pricing Agreement (APA) process to reduce transfer pricing disputes

Ÿ Issuing administrative guidelines to reduce the number of appeals led by the department

Ÿ Constituting separate benches by the Supreme Court to expedite tax appeals

Ÿ Constituting Justice Easwar Committee to simplify the provisions under the Income Tax Act,

1961 and to suggest modications and alternatives to the existing provisions.

Some further initiatives to reduce tax disputes and litigation could be:

Ÿ Independent scientic assessment of audit selection, scrutiny workload and the ofcers

available could determine the optimal number of scrutiny audits to be taken up every year so

that the pendencies are reduced.

Ÿ Reviewing processes within the department so that scrutiny audit disputes with businesses

are pre-empted by resolution within the department's decision making levels through

concurrent consultation instead of a tax demand in the scrutiny assessment. Current

procedures are more in nature of ex-post reviews after scrutiny assessments are completed.

A separate directorate for deciding whether appellate orders of commissioners /directions of

Dispute Resolution Panel need to be appealed to the tribunal. This could remove inbuilt bias

of eld authorities in evaluating the merits of their own assessment orders.

Ÿ Revisiting and re-evaluating statutory right of the tax department to le appeals against

adjudication done by its own ofcers.

Ÿ Reallocating and monitoring manpower and resources to expedite APAs.

Ÿ Speeding up alternative dispute resolution process of the advance ruling authority by

operationalizing additional benches to reduce the three years it currently takes to issue a

ruling.

Ÿ Strengthening the functioning of tax tribunals by lling up vacancies, creating specialized

benches for international taxation and transfer pricing issues and using electronic means to

le and monitor appeals.

Critical areas for easing the business

environment: Much needed reforms

Ÿ Minimizing regulatory cost of doing

business is one of the most crucial steps

on the road to a thriving economy –

enabling entrepreneurs to create new

value through market transactions. Three

new important laws in the ofng –

litigation policy, bankruptcy code and

arbitration law are steps in the right

direction.

Ÿ Need for widening the tax base is felt. In

this direction, there is a lot of anticipation

about the introduction of the Goods and

Services Tax (GST) from April 2016.

Ÿ Pursuing the disinvestment agenda to

raise resources for the government, as

well as to improve performance of PSUs.

Ÿ Industry expert FICCI has demonstrated in 6

a survey that capacity utilization levels

are still below optimal levels. Consumer

demand has not hit the road in a manner

that could push investments. Further

policy rate cuts by the central bank and

equivalent transmission of same in the

form of lower lending rates by banks for

both consumers and investors is

suggested.

Ÿ Creation of MUDRA (Micro Units

Development and Renance Agency)

bank and Self-Employment and Talent

Utilisation (SETU) mechanism has given a

boost to MSMEs and entrepreneurship.

However, it is felt that there should be a

rebated income tax for small start-up

businesses. Tax benet can be for a

dened rebate proportion of say up to 50

percent and for a limited period of say ve

years. This would empower small start-

ups to grow and expand. A key issue for

small businesses is sanctity of contracts,

and steps must be taken to ensure that

commercial contract can be enforced

quickly.

Ÿ Land reforms and implementation of the

current Land Acquisition Bill is

indispensable (the bill is under

consideration by the Parliamentary Joint

Committee, which will submit its report in

the upcoming winter session).

Ÿ Archaic and primitive labour reforms to be

done away with and replaced by new laws

that are in line with growing business

needs. Suggested labour reforms include:

SECTION A: EASE OF DOING BUSINESS IN INDIA

12

UNLOCKING INDIA’S

POTENTIAL AS A GLOBAL

INVESTMENT DESTINATION

6 Business Condence Survey, July 2015: http://blog.cci.com/business-condence-survey/6296/

13

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

Ÿ grand-fathering existing laws for existing

work force, amending contemporary

laws for new entrants to the work force,

and operationalizing exit policy under

national manufacturing policy.

Ÿ Strengthening infrastructure is an

important pillar on which ‘Make in

India’program is based. The government

has highly ambitious plans for Indian

infrastructure and plans to make it

‘Better than the Best’. The plan includes

projects to develop freight corridors

supported by better train linkages,

developing a bullet train network

(Diamond Quadrilateral Project) and

modernizing ports and airports.

Schemes to build an optical-bre

network up to village level ensuring

basic level of infrastructure (home,

electricity, water) and a national highway

programme are on the list. The

government intends to develop industrial

corridors and smart cities to bestow

infrastructure based on modern

technology with high-speed

communication. However, all this is

subject to availability of capital. India’s

closed nancial system articially raises

the cost of capital.

The World Bank has placed India twelve notches

higher than last year in its Ease of Doing Business

rankings for 2016. This comes close on the heels

of the country’s sixteen place leap on the World

Economic Forum’s Global Competitiveness index.

These rankings underline the impact of the recent

spate of reforms, which have come to bear fruit.

Notwithstanding the debate on whether a push up

in these rankings could have been far better, the

outcome is encouraging and signals a trend

reversal of sort.

A number of measures–at the policy and

administrative levels–have contributed to this

development. Amongst key investment reforms a

few initiatives which stood out include

liberalisation of Foreign Direct Investment (FDI)

norms including permitting composite caps,

efcient processing of approval permitting

investments, executive’s intervention to pre-empt

tax controversies and abstinence from

retrospective tax legislations.

Besides, the government’s commitment to

undertake signicant tax policy reforms, such as

tax rate rationalisation to make India a more

competitive investment destination vis-à-vis

BRICS and other emerging economies in Asia,

enhancing efcacy of dispute resolution forums

and a constitutional amendment to facilitate

Goods & Services Tax (GST) have contributed to

revitalising investors’ condence. Improving

macro-economic fundamentals such as moderate

ination and a relatively stable currency have

brought the sheen back to investors’ money. Till

June 2015, FDI ows recorded a year-on-year

growth of 30 percent.

At an administrative level, speedier decision

making, clamp down on disruptive practices such

as retail corruption and a behavioral shift in the

government’s functioning to result orientation are

other positives that drove the change. Push for

competitive federalism initiated a unique

movement of sorts, as states are beginning to

realise their potential by pitting themselves

against each other and taking measures to build

attractiveness for investments. State level land

and labour reforms will further hasten growth in

investments.

A slew of major policy reforms, which have the

potential to sustain investment momentum, are in

the making. Amongst these, two critical reforms

which are hung primarily due to the lack of

political consensus are land reforms and the

introduction of the unied national GST law. In

times when global economies are progressively

slowing down and India is reaping the benets of

low crude and commodity prices, India has a

unique opportunity to add a couple of percentage

points to GDP growth by implementing the GST

regime and thus setting in motion state-level

efciencies for doing business in India. Pending

land reforms tend to

Better global rankings underline India’s potentialMukesh ButaniManaging Partner, BMR Legal

cause more collateral damage to untapped

investment potential for infrastructure

development across the country, though

progressive states are likely to drive the agenda.

That these policy reforms can open the ood

gates for foreign and domestic investments, is a

no-brainer. I reckon it is in the overall interest of

state governments to allow convergence of their

ideology and let GST and land reforms see the

light of day.

Amongst others, unveiling of bankruptcy

legislation will catalyse growth of the ‘startup’

economy which requires easier norms for not only

entry but investment exit as well. The Bankruptcy

Law Reforms Committee has recommended

legislating a unied Insolvency Code for all

entities, which must replace existing disparate

legislations pertaining to insolvency and

liquidation of registered entities. Further, ne-

tuning of the Prevention of Corruption Act shall

address the menace of retail corruption, by

encouraging transparent and bold decision by

civil servants.

A case for impending reforms in labour laws

presents itself, since such reforms could well be

the inection point in reviving the languishing

growth of the manufacturing sector which far from

leading, contributes less than a quarter of the

country’s GDP. Again, states like Rajasthan and

Madhya Pradesh are driving such reforms at the

state level.

Financial sector reforms continue to hold the key.

While the merger of market regulator Sebi with the

Forward Markets Commission is a signicant

action emanating from recommendations of the

Financial Sector Legislative Reforms Commission

(FSLRC), major initiatives are required to realise

the objective of an integrated nancial sector

regulatory framework. Proposals to enact a

unied Indian Finance Code, and constituting a

Monetary Policy Committee as the custodian of

decision making in monetary policy matters are

signicant developments, and will trigger

modernisation of monetary controls.

Major breakthroughs have been witnessed on the

scal policy front in the past twelve months. India

becoming a signatory to the multilateral

agreement on automatic exchange of information

showed the way for embracing best practices in

tax administration. To ensure compliance with

Foreign Account Tax Compliance Act (FATCA),

India is adopting inter government agreements, in

tandem with revised disclosure norms prescribed

by the department of revenue to track reportable

transaction of nancial institutions. Enhanced

rigour on disclosures in tax matters is bound to

promote governance standards.

Continued focus on law making through

consultative processes bodes quite well from

investors’ standpoint. More recently the

government having embarked upon simplication

of income tax laws through a comprehensive

review by an expert group, is yet another instance

of progressive policy thinking. The outcome of

OECD and G20-led BEPS Project has received a

lion’s share of government attention. The nance

minister has hailed BEPS works as a stepping

stone to the rapidly emerging new era of tax

policies. It wouldn’t be far from mark to anticipate

major tax policy announcements in the Finance

Bill 2016 to embrace some of BEPS

recommendations, which have assumed

immediate signicance. An ordinance to amend

the Arbitration Act can facilitate speedier

resolution of commercial disputes in a time-

bound manner.

To sum up, optimism over the Indian growth story

is growing. What is needed is a continued policy

push to unleash reforms, lest India’s growth

pattern is held ransom to hostile politics.

(First published in Forbes India rd(www.forbesindia.com) issue dated 23

November 2015

http://forbesindia.com/blog/economy-

policy/better-global-rankings-underline-indias-

potential/)

Goods and Services Tax –

Where we are and how it could

impact business

The proposed Goods and

Services Tax (GST) is a

destination-based consumption

tax with an objective to eradicate

economic distortions and help in

development of a common

national market. Syncing with the

overall philosophy of ‘ease of

doing business in India’ to a great

extent, on a medium to long term

basis, GST is expected to pave

way for economic development.

ndTo recap, the 122 Constitution

Amendment Bill was passed in

the Lok Sabha and subsequently

got referred, by the Rajya Sabha,

to the Select Committee for its

recommendations. The Cabinet

accepted most of the changes/

suggestions proposed by the

Select Committee in the

Constitution Amendment Bill but

the Bill failed to get approved in

the Rajya Sabha in the recently

concluded monsoon session

owing to opposition from some of

the political parties.

With the Prime Minister and the

Finance Minister hopeful of the

implementation date in 2016, the

Government appears to be

making best efforts to ensure the

passing of the GST legislation in

the winter session scheduled in

November 2015/December 2015

and also laying ground work so as

to effectuate its implementation.

On a practical basis, it is fair to

assume that GST would

unfortunately miss the April 1,

2016 deadline. However, GST

being a transaction tax, the

introduction of the same can

happen anytime during the

nancial year and it is not

necessary that the next target

date only ought to be April 1,

2017.

The biggesttax reform

aimed at eradica�ng

economic distor�ons

and introducinga tax-friendly

businessenvironment

SECTORAL UPDATES

Key Developments in the Ministry of Finance

SECTION B: SECTORAL UPDATES

16

The Government has already released draft

reports on business processes on GST

registration, GST refunds and GST payments

for inviting comments of stakeholders and is

reported to release the draft model CGST,

SGST and IGST laws, along with GST

business processes for ling of returns.

These recent announcements and releases

not only reect a fair amount of back end

work that has been done, but also reects a

welcome approach of consulting different

stakeholders, by releasing drafts and seeking

inputs.

Given the magnitude of the expected impact

of GST on business, businesses should

make best use of this time gap to strategize

their business structures and work on IT

systems, as the roll out is certain though the

effective date of implementation remains

undetermined. Specically, in the run up to

GST, impact areas that business should

focus on should be the following:

a) Financial areas:

(i) Pricing

(ii) Working capital

(iii) Credits and refunds

While GST is expected to benet business to

have more credits of indirect taxes in the

supply chain, with the expected high rates of

GST, businesses should focus on

understanding the nancial impact areas

above. Specically, exporters need to get

prepared for higher credit build up and

refund thereon – as it is expected that upfront

exemptions would be kept minimal under

GST and current exemptions available to STP

units, EOUs and possibly SEZ units may be

replaced by tax payments, eligible for credit/

refund.

b) Operational areas:

(i) Procurements – including impact on key

vendors

(ii) Supply chain

(iii) Dealers/agents

(iv) Review of service contracts (sales and

procurement side)

GST is likely to impact different key functions

of businesses. Understanding the impact on

operations would require companies to be

engaged with business functions in the run

up to GST (e.g., setting up of a core internal

GST committee, typically driven by the

nance/ tax team).

The current CST/ VAT system has often been

a driver in decision making around supply

chain including setting up of warehouses.

This would need a complete relook.

By far, the most important complex change

that GST is expected to bring about is on

taxation of services at a state level, as

against the current tax regime of taxing

services centrally. This change would have a

signicant impact on service businesses

performing pan India services/contracts and

it is expected that they would need to revise

their service contracts and possibly raise

invoices on a decentralised/ state wise basis.

c) Infrastructural areas:

(i) Redesigning IT systems to be GST

compliant – ensuring compliance as well as

payment of taxes/ recoupment of credits in

appropriate States

(ii) Impact on account of decentralization of

compliances and accounting – adequacy of

and improvements to existing systems and

processes

17

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

IT system changes are known to take a

signicant amount of time. While the ne print

of exact format of invoices, returns and

record keeping is expected to come in only

closer to the date of GST introduction,

industry should make use of time available to

work on transaction ows, map current tax

data elds, possible expected tax data elds,

etc.

As it may be observed, the specic impact

on the business entities would be highly

dependent on individual business operations.

It is advisable for businesses to be updated

with the ongoing changes, understand likely

business impact and to also be engaged in

advocacy/ dialogue with the Government in

this most signicant indirect tax reform in

India.

18

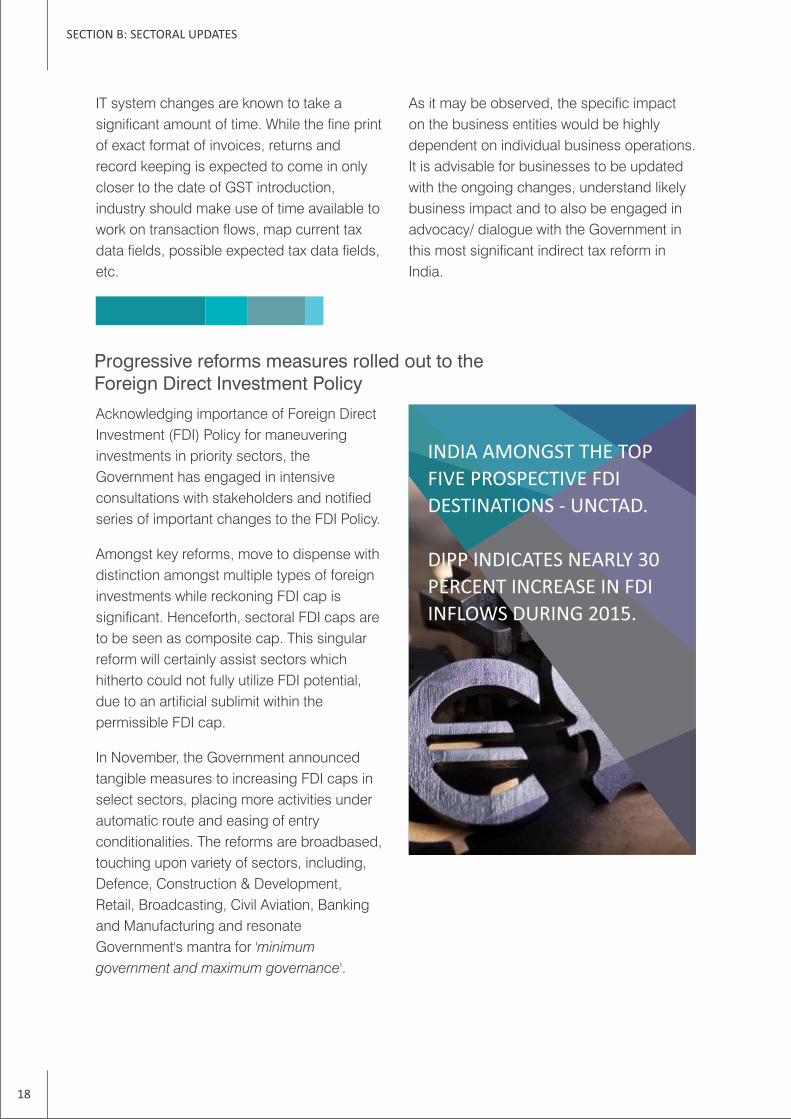

Acknowledging importance of Foreign Direct

Investment (FDI) Policy for maneuvering

investments in priority sectors, the

Government has engaged in intensive

consultations with stakeholders and notied

series of important changes to the FDI Policy.

Amongst key reforms, move to dispense with

distinction amongst multiple types of foreign

investments while reckoning FDI cap is

signicant. Henceforth, sectoral FDI caps are

to be seen as composite cap. This singular

reform will certainly assist sectors which

hitherto could not fully utilize FDI potential,

due to an articial sublimit within the

permissible FDI cap.

In November, the Government announced

tangible measures to increasing FDI caps in

select sectors, placing more activities under

automatic route and easing of entry

conditionalities. The reforms are broadbased,

touching upon variety of sectors, including,

Defence, Construction & Development,

Retail, Broadcasting, Civil Aviation, Banking

and Manufacturing and resonate

Government's mantra for 'minimum

government and maximum governance'.

Progressive reforms measures rolled out to the Foreign Direct Investment Policy

SECTION B: SECTORAL UPDATES

INDIA AMONGST THE TOP

FIVE PROSPECTIVE FDI

DESTINATIONS - UNCTAD.

DIPP INDICATES NEARLY 30

PERCENT INCREASE IN FDI

INFLOWS DURING 2015.

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

19

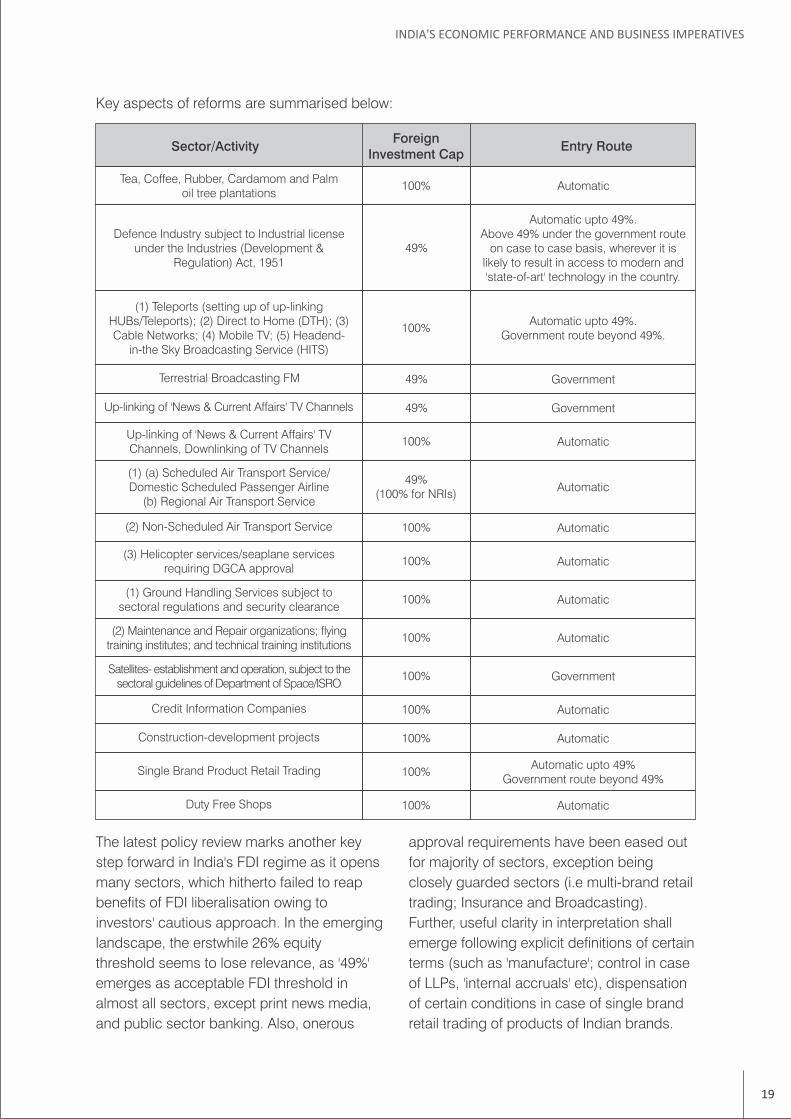

Sector/ActivityForeign

Investment CapEntry Route

Tea, Coffee, Rubber, Cardamom and Palm oil tree plantations

Defence Industry subject to Industrial license under the Industries (Development &

Regulation) Act, 1951

(1) Teleports (setting up of up-linking HUBs/Teleports); (2) Direct to Home (DTH); (3) Cable Networks; (4) Mobile TV; (5) Headend-

in-the Sky Broadcasting Service (HITS)

Terrestrial Broadcasting FM

Up-linking of 'News & Current Affairs' TV Channels

Up-linking of 'News & Current Affairs' TV Channels, Downlinking of TV Channels

(1) (a) Scheduled Air Transport Service/ Domestic Scheduled Passenger Airline

(b) Regional Air Transport Service

(2) Non-Scheduled Air Transport Service

(3) Helicopter services/seaplane services requiring DGCA approval

(1) Ground Handling Services subject to sectoral regulations and security clearance

(2) Maintenance and Repair organizations; ying training institutes; and technical training institutions

Satellites- establishment and operation, subject to the sectoral guidelines of Department of Space/ISRO

Credit Information Companies

Construction-development projects

Single Brand Product Retail Trading

Duty Free Shops

100%

49%

100%

49%

49%

100%

49%(100% for NRIs)

100%

100%

100%

100%

100%

100%

100%

100%

100%

Automatic

Automatic upto 49%. Above 49% under the government route

on case to case basis, wherever it is likely to result in access to modern and 'state-of-art' technology in the country.

Automatic upto 49%.Government route beyond 49%.

Government

Government

Government

Automatic

Automatic

Automatic

Automatic

Automatic

Automatic

Automatic

Automatic

Automatic

Automatic upto 49%Government route beyond 49%

The latest policy review marks another key

step forward in India's FDI regime as it opens

many sectors, which hitherto failed to reap

benets of FDI liberalisation owing to

investors' cautious approach. In the emerging

landscape, the erstwhile 26% equity

threshold seems to lose relevance, as '49%'

emerges as acceptable FDI threshold in

almost all sectors, except print news media,

and public sector banking. Also, onerous

approval requirements have been eased out

for majority of sectors, exception being

closely guarded sectors (i.e multi-brand retail

trading; Insurance and Broadcasting).

Further, useful clarity in interpretation shall

emerge following explicit denitions of certain

terms (such as 'manufacture'; control in case

of LLPs, 'internal accruals' etc), dispensation

of certain conditions in case of single brand

retail trading of products of Indian brands.

Key aspects of reforms are summarised below:

20

Foreign investors get relief from MAT

The dispute on the applicability of Minimum

Alternate Tax (MAT) to a foreign company

gained momentum in recent years, largely on

account of contrary rulings of tribunals

/quasi-judicial authorities. Tax

administration’s indiscreet approach in

serving show cause notices to foreign

investors levying MAT demand caused

considerable loss to India’s credibility as a

stable and predictable tax jurisdiction.

To prevent further damage to investors’

condence, the government vide Finance Act

2015, introduced MAT exemption, with

prospective effect in case of foreign

companies including FPIs (subject to

prescribed conditions). The amendment

caused disquiet amongst foreign investors as

revenue authorities took an interpretation that

exemption from MAT was only prospective,

and that prior to such conrmation foreign

companies (including FPIs) were liable to

MAT.

The long winding debate on applicability of

MAT to foreign companies has now been put

to rest by the Department of Revenue, vide

its Press Release dated September 24, 2015.

MAT exemption has now been extended,

subject to appropriate amendments to be

carried out to the IT Act, to all foreign

companies with retrospective effect from

April 1, 2001, provided foreign companies do

not have a ‘permanent establishment’ (PE) in

India, or have a registered place of business

in India.

The administrative guidance shall pre-empt

tax litigations and will reinstate investors’

condence in Indian tax policy which has

long been decried for lacking predictability

for foreign investors, in particular. It may help

the cause if legislative amendment is brought

about without further delay, and in the

manner that leaves no room for interpretative

debate.

Indradhanush Plan for PSBs

Public sector banks (PSBs) have played a

pivotal role in building India’s economy,

maintaining a lion's share in project nancing.

But low (global and domestic) demand and

stalled projects due to endowment issues,

delayed approval processes, land acquisition

etc. have adversely hit their protability.

Crippled by bad loans, the government rolled

out second generation banking reforms with

a heavy dose of capital infusion for PSBs and

unleashed a seven-step plan for

improvement. The package, titled

Indradhanush, touches upon several

incremental reform measures such as

creation of a Bank Board Bureau (BBB),

linking the compensation of banks’ top

management to performance, improving

governance standards, focussing on

SECTION B: SECTORAL UPDATES

Going by qualitative statistics released by

World Bank, World Economic Forum and 7UNCTAD , the investment policy reforms,

witnessed over past 18 months have been

recognized as having incremental effect.

Whilst further improvement in statistics is

anticipated on account of the recent policy

review, the current reforms are still not to be

seen as the end of road in FDI landscape.

Hopefully, further reforms shall follow swiftly

as India embarks upon the journey to

become truly an 'open economy'.

7 World Bank's Ease of doing business index; World Economic Forum's Global competitive index; UNCTAD's World Investment Report 2015

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

qualitative aspects of business and infusing

additional capital. Under the scheme, the

entire process of appointing MDs and CEOs

on the boards of banks has been revamped.

The approach for appointment is based on

global best practices and as per the

Companies Act. The government is also set

to launch the BBB, which will regularly

engage with the board of directors to

formulate appropriate strategies for growth

and development.

The Finance Ministry is devising a plan to

infuse INR 250 billion into recapitalisation of

PSBs this nancial year. In conformity, State

Bank of India will get INR 55.31 billion, Bank

of India INR 24.44 billion, IDBI Bank INR

22.29 billion, IOB INR 20.09 billion, Bank of

Baroda INR 17.86 billion, PNB INR 17.32

billion, Union Bank of India INR 10.80 billion

and Corporation Bank INR 8.6 billion.

All this has given a fresh impetus to the

banking sector. Other incremental reform

measures like linking the compensation of

banks’ top management to their performance

are still in the ofng.

GEARING UP FOR GROWTH

India, US sign FATCA to ght tax evasion

To identify and curb offshore tax evasion,

India and the US have taken a rm step

forward by inking an Inter-Governmental

Agreement (IGA), FATCA (Foreign Account

Tax Compliance Act). This is aimed at

bulwarking Indian nancial entities such as

banks, insurance companies, custodians and

broking houses from facing penal taxes when

they fail to disclose dealings of American

citizens and US entities.

FATCA will save nancial institutions the

bother of inking individual agreements with

the US. To date, the US has IGAs with more 8than 110 jurisdictions.

The United States had passed FATCA in

2010 to glean information on accounts held

by US taxpayers in other countries. US

nancial institutions are prescribed to

withhold a portion of payments made to

foreign nancial institutions (FFIs) who

disagree to identify and report information on

US account holders. As per the IGA, FFIs in

India will have to report tax information about

US account holders to the Indian government

directly. The Indian government will relay

such information to the US Internal Revenue

Service (IRS). The IRS will do the same for

Indian account holders.

Besides FATCA, India also signed Multilateral

Competent Authority Agreement (MCAA) on

June 3, 2015, enabling automatic exchange

of information on multilateral basis with 92

nations starting 2017. These are important

milestones in India’s ght against the

menace of black money. It would equip the

Indian revenue authorities to receive nancial

account information of Indians from foreign

countries on an automatic basis.

A firm step forward

22

SECTION B: SECTORAL UPDATES

8 Press Information Bureau, Government of IndiaIndia and United States signs Inter-Governmental Agreement (IGA) to implement the Foreign Account Tax Compliance Act (FATCA) to promote transparency on tax.http://nmin.nic.in/press_room/2015/India_US_sign_IGA09072015.pdf

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

23

TRANSFORMING INDIA THROUGHPOLICY

NITI Aayog to set up monitoring body

The government’s premier think tank NITI

Aayog is planning to set-up a Development

Monitoring and Evaluation Ofce (DMEO) to

oversee the centre’s agship programmes

and evaluate their performance.

The new body will perform much the same

role as the Independent Evaluation Ofce

(IEO) which functioned under the erstwhile

Planning Commission. Though in

coordination, the ofce is to be structured in

a fashion that it can work at arm’s length. It

would subsume the Programme Evaluation

Ofce (PEO) of the Planning Commission in

its realm.

DMEO will have two secretaries to oversee

development, monitoring and evaluation of

infrastructure schemes and social sectors

schemes respectively. The two secretaries

will directly report to the Aayog's vice

chairman, Dr. Arvind Panagariya.

Key Developments in Yojna Bhawan

24

Key Developments in the Ministry of Commerce & Industry

Launch of eBiz Portal

As a part of the Ease of Doing Business

initiative, an eBiz portal offering single

window processing of a number of

essential government-to-business (G2B)

services was launched. The portal is

expected to expand, but its rst incarnation

is promising.

The eBiz portal integrates several

government services in a single website,

facilitating faster delivery of licences,

registrations and clearances. Entrepreneurs

can apply for clearances on the portal, make

electronic payments to process applications

and track status of their application online. It

is also a repository of information on services

for setting up business in India. The website

falls under the government’s Digital India

initiative, designed to create digital

infrastructure and improve government

service provision. Currently, the federal

government offers 14 G2B services through

the portal. Many state and union territory

governments – including those in Andhra

Pradesh, Delhi, Haryana, Tamil Nadu and

Maharashtra – are shifting G2B services to

the portal. Another 40 services from the

federal government and state governments

are expected to be added over the next three

years. Well-organized applicants will nd the

amount of time involved to drop signicantly.

It is undoubtedly a step in the right direction

by the government.

SECTION B: SECTORAL UPDATES

EBIZ PORTAL HAS RADICALLY ABRIDGED THE COMPLEXITY IN OBTAINING INFORMATION AND SERVICES RELATED TO STARTING AND OPERATING BUSINESS IN INDIA.

Industrial Entrepreneurs Memorandum (DIPP)

Employer Registration with EPFO

Allotment of Director’s Identication Number (DIN)

Declaration of Commencement of Business (MCA)

Advance Foreign Remittance (RBI)

Tax Deduction Account Number TAN)

Importer Exporter Code (IEC – DGFT)

14 Government services that have already been integrated with eBiz are:

Industrial License (DIPP)

Employer Registration with ESIC

Company name availability (MCA)

Certicate of company incorporation

RBI’s foreign collaboration - General Permission

Route

Permanent Account Number

Issue of Explosive License (PESO)

Company Law – Recent Developments

The last few months have seen several

relaxations in application of specic

provisions of the newly introduced

Companies Act, 2013. The relaxations are

primarily based on stakeholder feedback and

practical experience gathered in the last year

since the new legislation became effective.

A large portion of these relaxations are

contained in Companies (Amendment) Act,

2015 (Amendment), and notications

released by the Ministry of Corporate Affairs

(Notication) exempting various kinds of

companies from certain provisions of the

Companies Act, 2013 (Act). Amongst

different categories of companies to whom

these notications were directed, private

companies largely welcomed the exemptions

granted from certain procedural requirements

under the Act.

One of the most signicant relaxations was

with regard to related party transactions. As

per the Act, certain related party transactions

were required to be approved by a

shareholders’ resolution with three-fourths

majority (where the ‘related party’ was not

entitled to vote). With a large proportion of

Indian companies still being promoter

managed and owned, this provision

presented difculties in moving ahead with

related party transactions since building

consensus, at times, became difcult. As a

relief to corporates, but still adhering to the

philosophy of minority protection, the

government relaxed the majority vote

requirement from three-fourths majority

(special resolution of shareholders) to 50.1

percent majority (ordinary resolution).

Further, for private companies, another relief

was provided – shareholders who are related

parties shall have a right to vote on such

resolutions.

A few weeks after this relaxation, the

securities market regulator also made

changes to the corporate governance

requirements to be complied with by listed

companies, such that these requirements

were aligned to relaxations made in the Act.

While certain issues and questions still

remain with regard to related party

transactions, this relaxation itself could pave

Key Developments in the Ministry ofCorporate Affairs

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

25

EASE OF DOING BUSINESS

way for transactions where consensus

building was difcult in environments which

involved dispersed minority shareholders

driven by varying considerations. Additionally,

approval requirements have been entirely

done away with for transactions with wholly

owned subsidiaries. Finally, private

companies are exempted from the

requirement of a shareholders’ resolution for

transactions with a holding, subsidiary,

associate, or fellow subsidiary companies.

In line with industry requests, the

Notications also brought in a number of

procedural relaxations for private companies.

One of the more signicant relaxations here

is non-applicability of Sections 43 and 47 of

the Act (relating to kinds of share capital and

voting rights), to companies. This empowers

private companies to structure investments

by external investors by issuing special

classes of shares. The Notication also

provides that limits on remuneration of

managerial personnel shall not be applicable

to a private company, which makes it easier

for companies to attract talent at key levels.

Additionally, there are many relaxations on

the procedural front. The requirement of

having a minimum paid-up capital to oat a

company (private or public) has been done

away with. The outdated and rarely deployed

‘common seal’ has also been done away

with. For private limited companies, the

Board can transact matters given in Section

180 of the Act (e.g. sale of undertaking,

borrowings beyond a particular threshold

etc.) without prior approval from the

shareholders. For certain private companies,

in which the entire shareholding is held by

non-corporates, provision of loans to

directors and their related entities, otherwise

prohibited under Section 185 of the Act, is

now possible. Finally, private companies can

raise deposits (up to a certain limit) from their

members without complying with certain

onerous conditions as prescribed in Section

73 of the Act. Flexibility has also been

provided to private companies to prescribe

their own regulations as to the conduct of

meetings in their bylaws.

In summary, the regulators have displayed

a pro-industry attitude by understanding

market feedback, and announcing

relaxations in a balanced manner. Though

issues still remain, as expected with any

large and material legislation, the overall

regulatory developments have been

encouraging.

SECTION B: SECTORAL UPDATES

26

SEBI – Simplifying the listing of Startups

As Indian start-ups grow and move towards maturity, challenges of raising further growth capital

in larger amounts and providing a credible exit to existing investors have (or will) come up. The

traditional (or rather conventional) approach to address the challenge has been to seek listings

in overseas markets. Reasons for this are multifarious – the primary three being (1) availability of

sufcient market capacity and sophisticated investors with a favourable mindset to price such

assets, (2) tax considerations of promoters and investors, and (3) regulatory environment

governing the listing process.

Securities and Exchange Board of India (SEBI) has been mindful of the potential ight of valuable

assets to overseas capital markets, and also the challenges faced by existing companies in

current capital raising and listing regime [largely covered under SEBI (Issue of Capital and

Disclosure Requirements) Regulations, 2009, referred to as ICDR herein].

ICDR had itself provided easier capital raising/ listing regimes for companies qualifying as small

and medium enterprises (SMEs) contained in Chapters XB and XC (wherein eligible companies

could simply list, or list along with making a public issue, subject to prescribed conditions).

However, these were not very successful, owing to regulatory constraints. In August 2015, SEBI

issued ‘refreshed’ listing and capital raising regime for ‘eligible’ start-ups with the intention of

developing a market place for this asset class which can be accessed and used by

sophisticated investors.

The ‘refreshed’ regime in summary

To be eligible, a company should have at least 25 percent of its pre-issue capital held by

qualied institutional buyers (QIBs as dened in ICDR), and should be engaged in the use of

technology, information technology, intellectual property, data analytics, bio-technology and

nano-technology to provide products, services or business platforms with substantial value

addition. If companies are not engaged in the businesses mentioned above, QIB holding in pre-

issue capital has to be at least 50 percent. Further, no person, individually, or with others in

concert, shall hold 25 percent or more of post issue capital of the company.

Eligible companies can either list their securities without raising fresh capital from public, or seek

listing pursuant to making a public issue on a special ‘institutional trading platform’. Minimum

trading lot on the platform should be INR 1 million to ensure that the asset class is accessed

only by sophisticated investors with risk taking capability.

In case of companies making a public issue along with listing, the minimum application size

shall be INR 1 million and the number of allottees should be more than 200; 75 percent of the

net offer to public shall be allocated to institutional investors, while the remaining 25 percent can

be allocated to non-institutional investors.

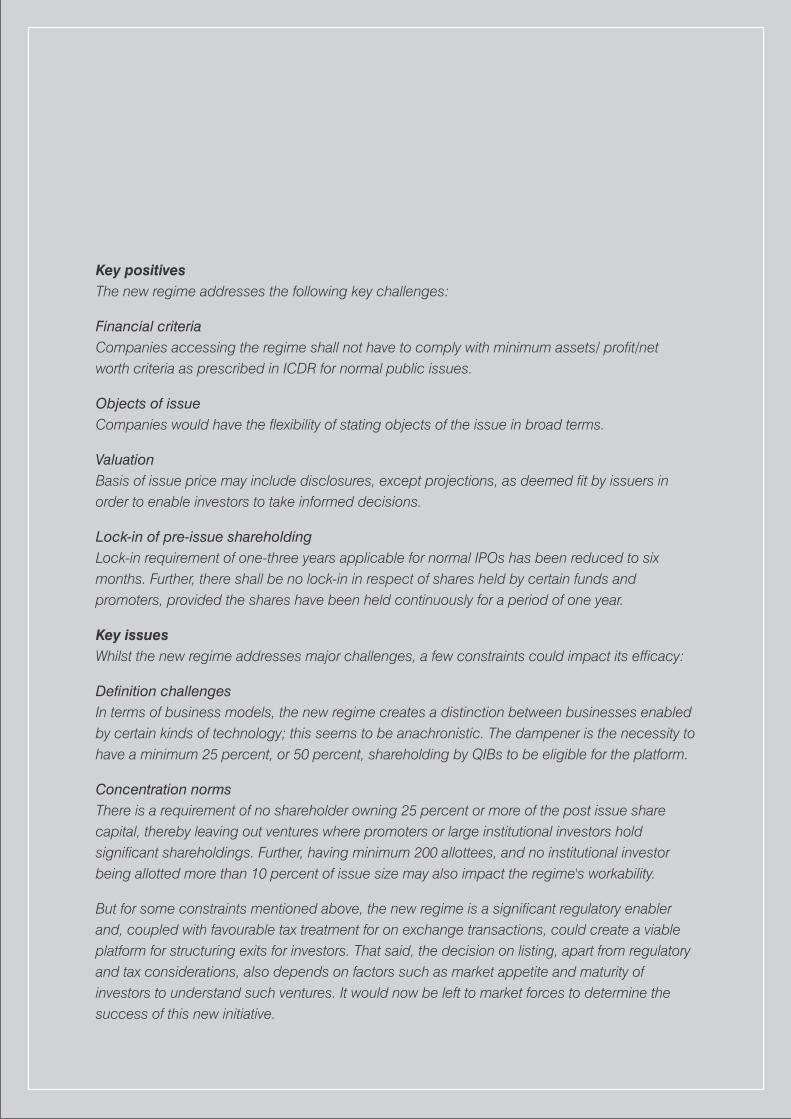

Key positives

The new regime addresses the following key challenges:

Financial criteria

Companies accessing the regime shall not have to comply with minimum assets/ prot/net

worth criteria as prescribed in ICDR for normal public issues.

Objects of issue

Companies would have the exibility of stating objects of the issue in broad terms.

Valuation

Basis of issue price may include disclosures, except projections, as deemed t by issuers in

order to enable investors to take informed decisions.

Lock-in of pre-issue shareholding

Lock-in requirement of one-three years applicable for normal IPOs has been reduced to six

months. Further, there shall be no lock-in in respect of shares held by certain funds and

promoters, provided the shares have been held continuously for a period of one year.

Key issues

Whilst the new regime addresses major challenges, a few constraints could impact its efcacy:

Denition challenges

In terms of business models, the new regime creates a distinction between businesses enabled

by certain kinds of technology; this seems to be anachronistic. The dampener is the necessity to

have a minimum 25 percent, or 50 percent, shareholding by QIBs to be eligible for the platform.

Concentration norms

There is a requirement of no shareholder owning 25 percent or more of the post issue share

capital, thereby leaving out ventures where promoters or large institutional investors hold

signicant shareholdings. Further, having minimum 200 allottees, and no institutional investor

being allotted more than 10 percent of issue size may also impact the regime's workability.

But for some constraints mentioned above, the new regime is a signicant regulatory enabler

and, coupled with favourable tax treatment for on exchange transactions, could create a viable

platform for structuring exits for investors. That said, the decision on listing, apart from regulatory

and tax considerations, also depends on factors such as market appetite and maturity of

investors to understand such ventures. It would now be left to market forces to determine the

success of this new initiative.

Prime Minister Modi visited ve Central Asian

countries – Uzbekistan, Kazakhstan,

Turkmenistan, Kyrgyzstan and Tajikistan – in

July to reinvigorate India's traditional ties with

the region. Central Asian countries are

resource rich and India is looking at investing

and building partnerships in the region. India

sealed several agreements with nations on

energy and trade and held discussions on

security issues and cultural interchange.

Kazakhstan, the biggest producer of uranium

in the world, supplied India with 2,100 metric

tonnes of uranium between 2009 and 2014.

India signed a fresh deal to secure 5,000

tonnes of uranium supply over the next four

years. This would allow operations to restart

in many nuclear plants, which are currently

closed due to lack of fuel.

A major landmark of India's engagement with

Central Asia is the TAPI (Turkmenistan-

Afghanistan-Pakistan-India) Project – an

ambitious pipeline for transporting natural

gas from Central Asia to South Asia. The

proposed 1,700 km pipeline is a USD 10

billion project, passing through Afghanistan

and Pakistan. Turkmenistan has the world's

largest reserve of natural gas and could be a

steady source of natural resource. However,

given the unrest and political equation with

neighbours, questions regarding completion

of the project remain.

In Kyrgyzstan, pacts to boost co-operation in

medicine and information technology were

signed. During Modi's Uzbekistan visit, both

sides discussed strengthening bilateral

economic relations, ways to improve

connectivity with the landlocked Central

Key Developments in Foreign Affairs

SIGNING LANDMARK DEALS WITH ITS NEIGHBOURSPM NARENDRA MODI MEETS HEADS OF STATE OF TAJIKISTAN, UZBEKISTAN AND TURKMENISTAN

29

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

Asian nation and implementing the contract

for supply of uranium from mineral-rich

republic.

Modi’s recent visit to the United Arab

Emirates (UAE) chalked discussions on

security, trade and cultural exchanges. The

prime ministers’ attempts to woo UAE

investors for infrastructure projects saw

success when the two parties were able to

establish the UAE-India Infrastructure

Investment Fund. This fund aims to reach a

target of USD 75 billion to support investment

for rapid expansion of next generation

infrastructure capabilities.

Prime Minister Modi’s visit in September to

the US marked a signicant step on the road

to strengthening Indo-US ties and business

relations. During his ve-day visit, he not only

met US President Barack Obama, but also

sought to invite investment from prominent

CEOs of the Silicon Valley. During his one-

hour meeting with President Obama, a range

of issues were discussed, including terrorism

and climate change. Several path-breaking

MoUs were signed between various Indian

and US rms. The Prime Minister promised to

provide lifetime visas to Persons of Indian

Origin (PIO) cardholders and visa on arrival

to American tourists visiting India. The

merger of PIO and Overseas Citizens of India

(OIC) schemes to facilitate hassle free travel

to the Indian diaspora was announced. PM

Modi pitched India to some of the largest

global investors and nanciers, urging them

to shed any fears they might have developed

in recent years about investing in the country.

Over a series of one-on-one meetings and a

power breakfast, Modi met top executives of

Fortune 500 companies such as BlackRock’s

Laurence D. Fink, Lloyd Blankfein of

Goldman Sachs and KKR's Henry Kravis as

well as CEOs of manufacturing rms,

including Boeing’s James McNerney, General

Electric’s Jeffrey Immelt and IBM's Virginia

Rometty. He also met executives from Merck,

Cargill, AES, Citigroup, PepsiCo etc.

Besides, PM Modi took the opportunity of

meeting head honchos of global tech giants

– Google, Apple and Microsoft – to promote

his Digital India initiative. During his tour of

the Google campus, he announced that in

collaboration with Google, Indian Railways

would provide free wi- services to 500

railway stations in India.

Bilateral meetings with British Prime Minister

David Cameron and France’s President

Francois Hollande were held on key issues

like terrorism, UN Security Council (UNSC)

reforms and climate change.

On the last day of his visit, PM addressed the

UN Peacekeeping Summit where he made

another strong pitch for UNSC reforms. He

also attended the UN General Assembly

where a number of subjects centred around

collective world development were touched

upon. PM Modi pledged his uncompromising

commitment to ghting climate change

without hurting development.

30

SECTION B: SECTORAL UPDATES

PM NARENDRA MODI MEETING WITH CEOS OF GLOBAL TECH GIANTS – SUNDER PICHAI OF GOOGLE, SATYA NADELA OF MICROSOFT AND TIM COOK OF APPLE – TO PROMOTE THE ‘DIGITAL INDIA’ INITIATIVE.

Relaxation of Offset Discharge Procedure

The Ministry of Defence recently made

important modications to the offset policy

forming part of Defence Procurement

Procedure (DPP) 2013, with the intent of

providing greater headroom to OEMs in

meeting their offset commitments.

Key takeaways emerging from

modications brought about in the DPP

2013.

Enhanced exibility to OEMs in choosing

Indian Offset Partners

The earlier offset policy permitted OEMs to

change the Indian offset partner

(IOP)/components only “in exceptional

cases” after seeking prior approval from

relevant government authorities. Whilst any

change in the IOP required prior approval

from the secretary, defence production, a

change in the offset component required

approval of the defence minister pursuant to

recommendations of the Defence Production

Board.

In order to

simplify the

approval

process, the

notication

proposes that aforesaid changes in IOP and

offset components shall now be subject to

approval by the defence production

secretary. Such a change in IOP/offset

components shall no longer be restricted to

“exceptional cases� only; such change could

be uniformly sought by OEMs.

Calibrated approach to submitting offset

work plans

Hitherto, OEMs were required to submit the

detailed technical offset proposal for review

by the Technical Offset Evaluation Committee

(TOEC) at the bid stage. The proposal

required to be submitted by OEMs had to

specify offset components, names and

eligibility documents of IOPs and IOP wise

work share. Further, OEMs were required to

ensure that the proposal is in conformity with

the offset guidelines.

Under the amended policy, if OEMs fail to

provide an offset plan comprising details

pertaining to IOP wise work share, specic

products and supporting documents

indicating IOP eligibility, at TOEC stage, it

may choose to provide such details as

under:

a) OEM may furnish such details to the

Defence Offset Management Wing (DOMW)

one year prior to discharging offset

obligations through IOPs.

The approval of the proposal shall be

intimated by the DOMW within three months

of receipt of complete documents. In case

Key Developments in the Ministry ofDefence MAKING POLICY

THAT ISMANUFACTURINGFRIENDLY

31

INDIA'S ECONOMIC PERFORMANCE AND BUSINESS IMPERATIVES

NITI Aayog to bring Integrated

Energy Policy

NITI Aayog is expected to announce an

integrated energy policy for decontrolling

energy prices. The policy, a blueprint for

developing energy security and right pricing

mechanism, would push competition on

quality standards.

In 2013-14, the erstwhile Planning

Commission had created the India Energy

Security Scenarios (IESS) 2047, which was

launched in February 2014. Its role was to

assess and predict India’s energy needs,

domestic supplies and imports. NITI Aayog

has planned to take IESS 2047 to the next

level by bringing its rened version IESS 2047

2.0, which allows for three GDP growth

scenarios 7.4 percent, 6.7 percent and 5.8 9

percent in 2012-47 and accords a series of

energy consumption projections.

This initiative will boost power generation

from various sources like solar, wind, gas and

coal and counterbalance growing demand.

Today, India has an installed power

generation capacity of over 250,000 MW from

all sources, while peak power decit lies

roughly at 3.6 percent. The government has

set an ambitious target of generating 175,000

MW from renewable sources by 2022,

including 1,00,000 MW solar power.

India has the potential to emerge as a major

manufacturing hub in renewable power. Wind

energy in India accounts for nearly 70

percent (21.1 GW) of installed capacity,

making it the world's fth largest wind energy

producer. The government has set a capacity

addition target of 30 GW, taking total

renewable capacity to almost 55 GW by

2017. This includes 15 GW from wind power,

10 GW from solar power, 2.9 GW from

biomass power and 2.1 GW from small

hydropower.

the proposal is found ineligible, the vendor

may be required to rephrase the offset plan.

It is useful to note that in case there is any

change in annual commitments, there shall

be a consequential enhancement of 5

percent in obligations.

Alternatively,

b) OEM may furnish such details to DOMW at

the time of seeking offset credits.

In this scenario, DOMW shall evaluate the

proposal in light of the present offset

guidelines. On such evaluation, if proposal is

found to be ineligible, DOMW may levy

penalty treating transactions as invalid.

The aforesaid amendments shall come into

effect immediately and shall be applicable to

all Offset contracts and ongoing procurement

cases, irrespective of the applicable DPP.

The industry has long awaited rationalization

of the offset policy allowing OEMs to

calibrate their offset commitments as these

near actual implementation stage in the

project lifecycle. The latest amendment to

offset regime is a progressive policy move as

it permits OEMs to change non- performing

IOPs and offset component on near time

basis.

Key Developments in the Ministry ofPower & New and Renewable Energy

32

SECTION B: SECTORAL UPDATES

9 India Energy Scenarios Version 2.0, 2047: http://indiaenergy.gov.in/docs/Handpercent20Book.pdf

THE PROPOSED NATIONAL RENEWABLE ENERGY ACT, WILL HELP TO BRING IN CLEAR INSTITUTIONAL, FINANCIAL, STRUCTURAL ROADMAP FOR THE SECTOR AT THE NATIONAL LEVEL.

National Renewable Energy Act in pipeline

To reinforce the renewable energy sector and

give it institutional design, the government

has drafted the National Renewable Energy

Bill 2015. It is due in parliament next year and

once passed will cover all aspects of

renewable energy supply chain. Through an

independent law, the Ministry of New and