Download - In uencer Marketing with Fake Followers

Influencer Marketing with Fake Followers

Abhinav Anand∗

Souvik Dutta†

Prithwiraj Mukherjee‡

September 17, 2020

Abstract

Influencer marketing is a practice where an advertiser pays a popular social me-

dia user (influencer) in exchange for brand endorsement. We develop an analytical

model in a contract-theoretic setting between an advertiser and an influencer who

can inflate her publicly displayed follower count by buying fake followers; and take

a hidden action to legitimately increase her true number of followers. There is an

imperfect audit to detect fraud, which leads to increased costs for the influencer.

We show that the optimal contract exhibits high faking for influencers with inter-

mediate follower counts, while faking levels are low for those with very small or

very large true follower counts. Audits deter fraud only when accompanied by high

penalties, but restitutions paid to the advertiser encourage more fraud. We further

show that revenue sharing deters faking and incentivizes influencers to increase

their true number of followers.

Keywords: Digital marketing, social media, influencer marketing, fake follow-

ers, optimal control, contract theory, moral hazard.

JEL Classification: D82, D86, M31, M37

∗Indian Institute of Management Bangalore, [email protected]†Indraprastha Institute of Information Technology Delhi, [email protected]‡Indian Institute of Management Bangalore, [email protected]§We thank Bruno Badia, Manaswini Bhalla, Pradeep Chintagunta, Tirthatanmoy Das, Sreelata Jon-

nalagedda, Manish Kacker, Ashish Kumar, Sanjog Misra and participants at the Chicago Booth-IndiaQuantitative Marketing Conference (2018) at IIM Bangalore.

1

“At Unilever, we believe influencers are an important way to reach consumers and

grow our brands. Their power comes from a deep, authentic and direct connection with

people, but certain practices like buying followers can easily undermine these relation-

ships.” — Keith Weed, Chief Marketing and Communications Officer, Unilever (Stewart,

2018)

1 Introduction

Advertisers often pay popular social media users known as “influencers” to endorse their

products online. Many of these influencers have large numbers of self-selected followers

who share their interests (travel, fashion, cooking, etc.) and look up to them for advice

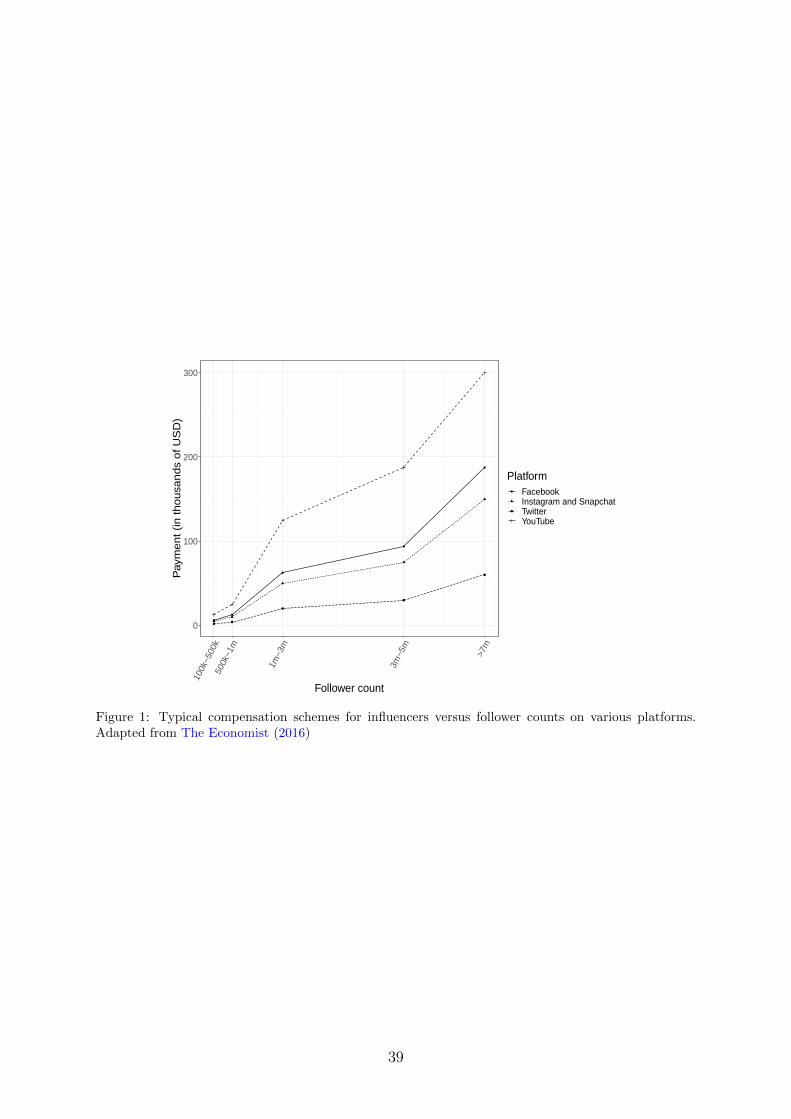

in these domains. According to The Economist (2016), YouTube influencers with over

7 million followers command upto $300,000 per sponsored post, while the corresponding

figures for Instagram, Facebook and Twitter are $150,000, $187,500 and $60,000 respec-

tively, allowing social media followings to be monetized lucratively. Even influencers with

fewer than 250,000 followers can make hundreds of dollars per sponsored post. Figure 1

shows some typical compensations for influencers on various platforms versus their fol-

lower counts. A Linqia (2018) survey across sectors including consumer packaged goods,

food and beverage and retail in the US finds that 86% of marketers surveyed used some

form of influencer marketing in 2017, and of them, 92% reported finding it effective.

39% of those surveyed planned to increase their influencer marketing budgets. Similar

trends reported by eMarketer (2017) and IRI (2018) suggest that influencer marketing is

growing.

Insert figure 1 about here

Influencer marketing has led to the emergence of shady businesses called “click farms”

which offer fake followers to influencers for a price, inflate the number of “likes” on their

fan pages, and post spurious comments on their posts. Influencers use these services to

fraudulently command higher fees from advertisers for promotional posts. A New York

Times expose finds that several influencers have bought fake followers from a prominent

click farm (Confessore et al., 2018).

Sway Ops, an influencer marketing agency estimates the total magnitude of influencer

fraud to be about $1 billion (Pathak, 2017). They find that in a single day, of 118,007

comments sampled on #sponsored or #ad tagged Instagram posts, less than 18% were

made by genuine users. Another study by the Points North Group finds that influencers

hired by Ritz-Carlton have 78% fake followers (Neff, 2018). The corresponding numbers

for Procter and Gamble’s Pampers and Olay brands are 32% and 19% respectively. The

2

quote at the beginning of this paper, by Unilever’s chief marketing and communications

officer at the Cannes film festival, indicates that marketers are acutely aware of the fake

follower problem and seek mechanisms to deal with it. We believe that our paper is an

important step in this direction. The rest of the paper is organized as follows.

Section 2 provides a brief overview of influencer marketing as a practice, and some

theoretical and empirical justification to the common practice of paying influencers by

their follower count. We also describe the widespread fake follower problem and its

prevalent unit economics.

Section 3 briefly describes extant literature on analogous fraud scenarios, as well

as a methodological note explaining the relevance of contract theory in modeling such

problems which contextualizes our work in a larger body of allied literature.

Section 4 outlines our principal (advertiser)–agent (influencer) setup, where the former

proposes to use the latter’s social media endorsement based on the promise of earnings

conditioned on her publicly displayed follower count which can be fake. Such faking is

costly to the influencer, not only because of the cost of buying fake followers, but extra

expenditures needed to sustain the deception by buying fake engagement (likes, shares,

comments). Further, the influencer can also expend resources on a hidden action, i.e.

unobservable effort where she invests in analytics, attends digital marketing seminars or

enhances her content quality to legitimately increase her follower count. The advertiser

must take into account this moral hazard component, and incentivize high levels of this

hidden action accordingly. The advertiser may choose to share some revenue with the

influencer as well. All of this happens in the presence of an imperfect, non-strategic

third party audit by a regulator. If the agent is caught, the regulator may impose fines,

some of which may be returned to the advertiser as restitution. The influencer also

suffers additional reputational losses on detection of her fraud. Drawing from analogous

literature on sharecropping, insurance and accounting fraud, we use control theory to solve

for the optimal ex ante contract between the advertiser and influencer. This method is

established in the economics literature, but to the best of our knowledge, our paper is its

first application in the marketing domain.

Section 5 outlines extensive policy simulations to show how revenue sharing, audit

accuracy, agent’s penalty and principal’s restitution affect the influencer’s fraud level.

First, we demonstrate that moderately famous influencers indulge in more faking, while

A-list celebrities and obscure people have lower incentives to do so. We demonstrate

that revenue sharing is effective in reducing fraud. Further, we also show that an audit

deters fraud not merely on account of its accuracy but requires sufficiently high penalties

in order to discourage faking. While penalties paid to third party regulators play an

effective deterrent in curbing influencer fraud, a clause requiring that a part of that fine

3

will be paid back as restitution to the cheated advertiser actually backfires, increasing

both ex ante payments to the influencer, as well as her endogenous choice of faking level.

Section 6 discusses the model’s implications for various stakeholders in the influencer

marketing ecosystem.

2 Influencer marketing: an overview

Since the practice of influencer marketing is relatively new, we present a brief overview

of this domain, linking it to established theories of endorsement and social influence. We

divide this into three parts where we, (i) cover the general practice of influencer marketing,

(ii) discuss the role of follower count in influencer marketing, and (iii) describe how it

leads to the specific problem of fake followers.

2.1 Influencer marketing

Influencer marketing is a promotion method that features brand endorsement using pop-

ular social media users. This makes it a hybrid of advertising and word-of-mouth, espe-

cially when commercial ties between endorsers and brands are not explicitly disclosed.1

Influencer marketing is analogous to celebrity endorsements in advertising, with source

(influencer) credibility (Hovland and Weiss, 1951) and attractiveness (McGuire, 1985; Mc-

Cracken, 1989) contributing to effectiveness of promotional campaigns. Just like endorsers

in advertising, influencers can be domain experts (tech bloggers, chefs, etc.), celebrities

(musicians, actors, etc.), or even lay endorsers (Tellis, 2003, chapter 11). Hughes et al.

(2019) find that effectiveness of influencer campaigns depends on the social media plat-

form used . For example, Facebook influencer campaigns tend to be more effective when

message content is more hedonic than utilitarian.

Nowadays, celebrities like actor Priyanka Chopra (Tiffany and co. jewelry), racing

professional Danica Patrick (Lyft ride sharing), rapper Snoop Dogg (Tanqueray gin)

star in online influencer campaigns alongside expert influencers like gamer H2ODelirious

(Ubisoft gaming) and fashion blogger Jaclyn Hill (Becca cosmetics), and lay influencers

like blogger Kelly Lund’s pet Loki the Wolf Dog (Mercedes-Benz, Toyota automobiles).

Specialist agencies like Bzzagent also enlist ordinary netizens as “nano-influencers” to

promote usually inexpensive consumer brands like chocolates and yoghurt in return for

1This has led to ethical conundrums surrounding undisclosed influencer promotions. The US FederalTrade Commission has taken cognizance of the possibility of consumers being misled by influencer mar-keting, and has mandated that sponsored posts must now clearly mention the relationship between theinfluencer and brand, usually as a hashtag such as #sponsored or #ad. Platforms like Instagram haveimplemented algorithms to automatically detect and tag paid influencer posts (FTC, 2019).

4

free product samples (Berger and Schwartz, 2011; Berger, 2016). Figure 2 provides snap-

shots of some famous influencer campaigns on social media.

Insert figure 2 about here

The study of influence in social networks is another well established research area rele-

vant to influencer marketing. The effects of network structure, personality and contextual

factors are extensively documented in several fields like marketing, sociology and network

science. Influentials on social media are characterized by high reach and spread of mes-

sages, as well as high engagement on their content, leading to social influence (Marsden

and Friedkin, 1993; Kumar and Mirchandani, 2012). Aral and Walker (2012) find that

men are more influential online than women, and that women influence men more than

they influence other women. Kumar et al. (2013) develop an influence score for social

media users using their social network data and word of mouth flow, and demonstrate its

efficacy in promoting Hokey Pokey, an Indian ice cream brand. Their method of iden-

tifying influentials and incentivizing them to spread word of mouth is among the more

sophisticated applications of influencer marketing. Agencies like Klout (now discontin-

ued), and PeerIndex have also provided multidimensional influence metrics with mixed

success. However, a more common practice today, as in figure 1, is to identify people

with large follower counts on social media, and given their personas, pay them to endorse

relevant brands. In the next subsection, we outline how online follower count relates to

influence.

2.2 Follower count and influence

According to the source credibility theory (Hovland and Weiss, 1951), an endorsement

message is more trustworthy when it comes from a source perceived to be an “expert” in a

given domain. In a qualitative study of Instagram users, Djafarova and Rushworth (2017)

find that non-traditional celebrities may be perceived as more credible than traditional

celebrities, and have a powerful impact on consumers’ fashion choices. An experimental

study by Jin and Phua (2014) finds that the perceived credibility of a Twitter user

is positively related to her number of followers. Alongside source credibility is source

attractiveness (familiarity, likeability and similarity) (McGuire, 1985; McCracken, 1989;

Tellis, 2003). Experiments by De Veirman et al. (2017) demonstrate that Instagram

influencers’ perceived likeability is positively related to their follower counts, possibly

driven by perceived popularity.

From a more straightforward perspective, a social media user with a larger follower

count represents an advertising medium with a larger reach. While the reach of traditional

media like TV, radio, hoardings and newspapers can only be approximately estimated, it

5

is reasonable to expect a naive advertiser unaware of fake followers, to place a high amount

of trust in seemingly accurate measures like follower counts, number of likes on sponsored

posts, retweets and impressions offered by web analytics tools. In a large scale study of

74 million Twitter information cascades encompassing over 1.6 million Twitter users,

Bakshy et al. (2011) show a positive link between follower count and online influence.

Agent-based studies of targeted new product seeding like Libai et al. (2013) demonstrate

that targeting hubs with high numbers of acquaintances speeds up the adoption process,

while Yoganarasimhan (2012), in an empirical analysis, suggests that the popularity of a

social media message over and above an individual’s immediate neighborhood is driven

by her follower count.

While follower count is not the only means of determining social influence (see Kan-

nan and Li (2017) for a comprehensive review, or Kumar et al. (2013) for a specific

application), it certainly is a popular metric used by digital marketers today to identify

influentials on social networks. The above discussions shed some light on why adver-

tisers pay more to influencers with higher follower counts, in turn generating incentives

for influencers to boost their own follower counts via unethical means like buying fake

followers.

2.3 The fake follower problem

Influencer marketing today is plagued with a fake follower problem, possibly because

endorsers are paid as per their follower count. A quick Google search for “buy instagram

followers” for example yields hundreds of results, where anyone with a credit card or

Paypal account can buy hundreds of thousands of fake followers instantly (see figure 3).

The rates for follows, retweets, likes and comments are different based on the platform in

question. Paquet-Clouston et al. (2017) report that click farm clients pay an average of

$49 for every 1,000 YouTube followers. The corresponding figures are $34 for Facebook,

$16 for Instagram and $15 for Twitter. Average prices for 1,000 likes on these platforms

are $50, $20, $14 and $15 respectively.

Insert figure 3 about here

A recent audit by the Institute of Contemporary Music Performances, of the Twit-

ter and Instagram followers of some of the most popular social media celebrities indi-

cates significant numbers of fake followers, mostly above 40% and going up to 57% for

Ellen Degeneres, a popular American entertainer (ICMP, 2019).2 Social media platforms

2This is insufficient evidence of influencer fraud as click farms make their bots follow celebrity accountswho may not have bought their services, just to mimic human behavior. In contrast, the New YorkTimes expose of Devumi (Confessore et al., 2018) mentioned in section 1 uncovers actual purchase of

6

sometimes purge fake followers, though this reduces their user numbers considerably, and

often causes outrage from aggrieved users. Of note is a recent incident where Amitabh

Bachchan, a veteran Indian actor with a Twitter following of over 38 million, berated the

platform publicly for reducing his follower count by purging many bot accounts following

him (Mathew, 2018).

3 Background

We briefly outline two streams of literature germane to our problem: (a) models of

economic fraud and (b) applications of contract theory to marketing. Because these

domains are large, we outline only a few studies in each, to motivate and contextualize

our own work. In section 3.1 we discuss related models of economic fraud in online and

offline businesses, and in section 3.2, we motivate our choice of methodology of contract

theory.

3.1 Economic fraud

Online businesses are prone to several kinds of marketing fraud. Advertisers paying per

click frequently encounter click fraud where click farms simulate genuine clicks. Wilbur

and Zhu (2009) in an important, related study investigate the problem of click fraud in

search advertisement in a game theoretic setting. Their results suggest that usage of

a neutral third party to audit click fraud detection can benefit the search advertising

industry. Another form of online fraud consists of fake reviews, when businesses post

either fake positive reviews for themselves or fake negative reviews for their competitors.

Lappas et al. (2016) demonstrate how even a few fake reviews can significantly boost

hotels’ visibility. Luca and Zervas (2016) find that the prevalence of suspicious restaurant

reviews on Yelp has grown over time. They find that restaurants with weaker reputations

tend to engage more in online review fraud when faced with increasing competition.

A model of insurance and sharecropping fraud where agents involve in costly falsifi-

cation is developed in a contract theoretic setting in Crocker and Morgan (1998). Their

model yields results that have been extended to other fraud scenarios, like misreporting

of earnings by CEOs (Crocker and Slemrod, 2007; Sun, 2014), many types of insurance

fraud (Crocker and Tennyson, 2002; Dionne et al., 2009; Doherty and Smetters, 2005),

corporate tax evasion by CEOs (Crocker and Slemrod, 2005), and in designing optimal

product return policies (Crocker and Letizia, 2014).

fake followers based on the click farm’s own client records, including credit card transaction details.Section 5.4.1 discusses the implications of this in detail.

7

Employee theft in retail can also be modelled analytically. Mishra and Prasad (2006)

demonstrate that a complete elimination of theft may be economically infeasible and

derive an optimal frequency of random inspections to minimize losses due to theft by

retail employees. With this paper, we contribute to the literature on economic fraud by

modeling the emerging phenomenon of fraud in influencer marketing.

3.2 Contract theory

Contract theoretic approaches have been used in marketing scenarios such as designing

warranties and extended service contracts (Padmanabhan and Rao, 1993) and delegation

of pricing decisions to salespersons (Bhardwaj, 2001; Mishra and Prasad, 2004, 2005)

to name a few. Other noteworthy applications of contract theory in marketing include

explaining product development incentives (Simester and Zhang, 2010); internal lobby-

ing by salespersons for lower prices, which can elicit truthful information about market

demand (Simester and Zhang, 2014); and assessing the performance of exclusive tie-in

contracts (Kolay, 2018). Our paper incorporates contract theory and optimal control the-

ory in the digital marketing literature, illustrating the economics of influencer marketing

fraud.

4 Model

We consider a risk-neutral advertiser (principal) who wishes to reach the followers of a

risk-neutral influencer (agent) with follower count n in order to earn revenue R(n) with

R′ > 0. The advertiser proposes to pay the influencer for brand endorsement via social

media posts like sponsored tweets, videos or pictures. We outline the mathematical setup

of the game that unfolds between the advertiser and influencer. Table 1 provides a ready

reckoner of mathematical notation used henceforth.

Insert table 1 about here

The influencer can buy fake followers to inflate her displayed follower count, which

we denote by the display function u(n). For example, u(n) = n implies that there is

no faking, and u(n) > n implies that the influencer has n true followers and has bought

u(n) − n fake followers. It is important to note that an influencer cannot just get away

with buying fake followers. To pull off the fraud convincingly, she must also pay for more

engagement such as fake replies, fake comments and fake likes on her social media posts.

Unlike the purchase of fake followers which may be a one-time expense, buying fake

online engagement from click farms is a recurrent expense. Thus, the cost of deception

8

gets progressively more expensive as the amount of faking u(n)− n goes up, and is thus

assumed to be convex. We denote such faking cost by the function c(u(n)− n) with the

following assumptions:

1. c(0) = 0 (no faking is costless)

2. c′(0) = 0 (no faking incurs minimum cost)

3. c′(z) > 0 ∀z > 0 (faking cost increases with the level of faking)

4. c′′ > 0 ∀z ≥ 0 (faking cost is convex)

These assumptions are in line with Crocker and Morgan (1998)—a model of adverse

selection—and Crocker and Slemrod (2007)—a model incorporating moral hazard, albeit

in different contexts. However both these models assume that the agent is able to com-

pletely hide her fraud via the expenditure on faking. In our setting however, we relax this

assumption, instead assuming that there is an imperfect non-strategic third-party audit

which can detect the influencer’s fraud with an exogenous probability γ. If the influencer

is not caught, she incurs a cost of only c(u(n) − n), but if caught, her cost escalates by

an exogenous multiplier δ > 1.

Influencer marketing is a new phenomenon, gaining prominence only in the last decade

or so. Conventions are as of yet unclear, as are policy and regulations surrounding it.

For example, the US Federal Trade Commission has outlined guidelines regarding ethical

disclosures of influencer marketing as recently as 2019 (FTC, 2019). At the moment,

there are no clear guidelines regarding fraud in influencer marketing, though there is

a general consensus amongst marketers that policies should be put in place to deter

rampant fake follower fraud in the world of influencer marketing. However, analogous

fraud in the world of high-tech entrepreneurship is well-known, with the cynical aphorism

“fake it till you make it” being accepted wisdom in Silicon Valley today.3 For example,

Uber was made to pay $20 million in restitution to affected drivers by the Federal trade

Commission for having inflated driver earnings (FTC, 2017). In another high-profile

case, Facebook paid out $40 million in damages to video content hosts on its platform for

having inflated viewers by up to 900% (Morris, 2019). Similarly Elizabeth Holmes and

Ramesh Balwani, the former CEO and CFO respectively of Theranos, both paid steep

fines and were barred from being directors of public companies by the US Securities and

Exchange Commission, for exaggerating both company revenue and performance metrics

of Theranos’s at-home diagnostic kits to investors and consumers (SEC, 2018). Deceptive

3This practice has even entered pop culture via HBO’s sitcom Silicon Valley, where the protagonistsuse a click farm service to fake a large user base. Following the episode, Letzter (2016) confirms theprevalence of this practice among app developers to unethically boost their user numbers.

9

advertising also attracts penalties which include restitution to affected consumers. For

example, the Federal Trade Commission ordered John Beck Amazing Products to pay

$478 million to affected consumers for misrepresenting the company’s earning potential

in its infomercials (FTC, 2012). Analogously, while restitutive penalty is not yet a norm

in influencer marketing, we consider it to be an important potential fraud-deterrence and

redressal mechanism which merits serious scrutiny.

As outlined before, the influencer incurs a cost c(u(n)−n) for her fraud. If caught, this

escalates to δc(u(n) − n) where δ > 1. We note that of this, the influencer has already

spent c(u(n) − n) in her faking. Of the remaining (δ − 1)c(u(n) − n), an exogenous

fraction 0 ≤ ρ < 1 is paid as restitution to the advertiser. The remaining (1 − ρ)(δ −1)c(u(n)− n) constitutes the influencer’s reputation damages, and possible fines paid to

non-strategic third parties like the Federal Trade Commission or other regulatory bodies.

This assumption is similar to Crocker and Slemrod (2005), but with some key differences.

First, we decompose audit accuracy and severity into two distinct terms, while Crocker

and Slemrod (2005) bundle them together. Further, in their model of corporate tax

avoidance, both principal and agent suffer exogenous losses if the agent’s fraud is detected;

and there is no restitution paid by the fraudulent agent to the principal. In our model,

the principal does not suffer losses if the agent is caught in an audit; rather, he is partially

compensated by the agent in this event. Finally, our model adapts Crocker and Slemrod

(2007), which has a moral hazard component, but no audit and Crocker and Slemrod

(2005) which features audits but no moral hazard. As will be apparent later, combining

moral hazard with audit and restitutive penalties renders infeasible, explicit comparative

statics which establish the effect of audit parameters on faking or profitability. In lieu

of this, we present an extensive numerical sensitivity analysis in section 5 to guide both

marketers and policy makers. Table 2 summarizes similarities and differences with some

key works we draw from.

Insert table 2 about here

We incorporate moral hazard as follows. The influencer can not only fraudulently

inflate her follower count, but can also legitimately and organically increase it via actions

hidden from the advertiser. For example, in a longitudinal study, Hutto et al. (2013) find

that message content and behavioral choices of Twitter users are significant predictors

of of their follower count. In a study of Pinterest, Chang et al. (2014) find that sharing

diverse types of content online increases follower count. Caro and Martınez-de Albeniz

(2020) envision the online content provider’s job as optimizing between increasing and re-

taining online followers via optimizing content. Apart from the aforementioned examples

of academic research, the idea of unobservable efforts by the influencer yielding organic

10

increases in follower count is intuitive as well. Digital marketing practitioners recommend

strategies like improving content quality, investing in advanced analytics, engaging with

followers, cross-linking content across platforms, hosting product giveaways, and more,

to increase follower count (e.g. Patel, 2018; Ferreira, 2019; Newberry, 2019).

We assume that the influencer undertakes a hidden action a > 0 which the advertiser

does not observe. However, the advertiser knows that the influencer’s true follower count

is distributed according to the continuous probability density function f(n|a) and the

associated cumulative distribution function F (n|a) with support [nL, nH ].4 In line with

Crocker and Slemrod (2007), we make the following assumptions on F :

1. Fa < 0 ∀n ∈ (nL, nH): first order stochastic dominance—an increase in a shifts F

to the right

2. The support [nL, nH ] of F (n|a), does not vary with a

3. Faa(n|a) > 0, ∀n ∈ (nL, nH) which implies Fa(nL|a) = Fa(nH |a) = 0

In standard contract theory terminology, the true follower count n is the agent’s (influ-

encer) type, which can be affected via a as described above. This hidden action is costly

to the agent. We denote this cost function as h(a) with the following assumptions:

1. h(0) = 0

2. h′(0) = 0

3. h′(a) > 0 ∀a > 0

4. h′′(a) > 0 ∀a > 0

While in practice such contracts would be conditioned on the displayed follower count

u(n), we use the revelation principle to look for direct mechanisms instead (Myerson,

1979). This is applicable because all actions by both the advertiser (choosing compen-

sation scheme) and influencer (buying fakes, deciding the display function and choice of

hidden action level) are ex ante.

The advertiser pays the influencer a monetary amount v(n)+w for her services. Here,

w is a fixed payment and v(n) is a payment conditioned on her follower count n.5 Figure

4Though the follower count is an integer, we assume it to be continuous for mathematical convenience.5The fixed payment w is a frequent feature of many influencer marketing payment schemes; as well

as a mathematical necessity to solve for the optimal contract. Hootsuite, one of most popular digitalcampaign management tools, suggests incorporating a fixed component along with variable payment inits blog (Sehl, 2020). It can be interpreted as an incentive for unobservable effort. For example, theinfluencer marketing platform Sideqik suggests that advertisers sponsor business expenses like accessto better analytics tools, attending conferences and product give-aways alongside conventional followercount-based compensation (Sideqik, 2020).

11

4 (without the optional revenue sharing component) illustrates the setup described thus

far.

Insert figure 4 about here

The payoff for the advertiser becomes:

Π = (1− γ)[R(n)− v(n)− w)] + γ[R(n)− v(n)− w + ρ(δ − 1)c(u(n)− n))]

= R(n)− v(n)− w + γρ(δ − 1)c(u(n)− n) (1)

and the influencer’s payoff can be written as:

Y = (1− γ)[v(n) + w − h(a)− c(u(n)− n)] + γ[v(n) + w − h(a)− δc(u(n)− n))]

= v(n) + w − h(a)− (1− γ + γδ)c(u(n)− n)) (2)

It is important to discuss what the revenue function R(n) truly means to an advertiser

using an influencer, and will be more evident when we discuss revenue sharing in section

4.4. The purpose of advertising (and indeed influencer marketing) often goes beyond

boosting direct sales (usually a short-term tactical move) to more strategic long-term

goals like building brand awareness, liking, and reinforcement of previous choices (Kotler

and Keller, 2012, Chapter 18), or influencing various intermediate (pre-purchase) con-

sumer mental processes (Tellis, 2003, Chapter 4). The effects of an influencer campaign

on variables like brand liking, effect, recall, etc., and their subsequent quantifiable rev-

enue effects are hard to measure. Indeed, the study of advertising effectiveness in the

presence of other marketing mix variables and multiple campaigns in different media is

not straightforward (see for e.g. Lewis and Rao, 2015; Sridhar et al., 2017). Therefore,

in reality, accounting for an influencer campaign has two components: an trackable com-

ponent like R(n) in our model; and and a non-trackable component which we assume to

be zero.

In order for the equilibrium to be incentive compatible, it must be that at the optimal

v∗, u∗, w∗, there is no incentive for the influencer to not act according to her own type.

This happens only if:

Y (v∗(n), u∗(n), w∗) ≥ Y (v∗(n), u∗(n), w∗) ∀n 6= n ∈ [nL, nH ] (3)

For brevity, we denote the optimal value function Y (v∗, u∗, w∗) ≡ Y ∗ and note that since

Y ∗(·) is optimal, its derivative with respect to the arguments v and u must be 0:

∂Y ∗

∂v

∣∣∣∣v=v∗

=∂Y ∗

∂u

∣∣∣∣u=u∗

= 0 (4)

12

Using the envelope theorem, by means of the total derivative, we establish the dependence

of the optimal value function Y ∗ on the parameter n by:

dY ∗

dn=∂Y ∗

∂v∗dv∗

dn+∂Y ∗

∂u∗du∗

dn+∂Y ∗

∂n· 1 (5)

This leads to the standard envelope condition:

dY ∗

dn=∂Y ∗

∂n= (1− γ + γδ)c′(u(n)− n) (6)

Further, since the contract is devised when the influencer does not yet know her true

number of followers n, in order to find participation worthwhile it must be that her ex

ante payoff is at least zero, which is what she gets from not participating. This leads to

the following participation constraint:∫ nH

nL

Y (v, u, w)f(n|a)dn ≥ 0 (7)

Moreover, since the influencer selects a before observing n, she will pick the action that

maximizes her payoff:

maxa

∫ nH

nL

Y (v, u, w)f(n|a)dn (8)

Using the fact that Ya = −h′(a), leads to the following first order condition which we

refer to as the delegation constraint:

d

da

∫ nH

nL

Y (v, u, w)f(n|a)dn = 0⇒∫ nH

nL

(Y fa − h′f)dn = 0 (9)

The above first order condition for the delegation constraint, while necessary, is not

sufficient. For sufficiency, we need the following condition.

Lemma. Faa(n|a) > 0 is sufficient for the action a to maximize the influencer’s expected

payoff∫ nH

nLY (v, u, w)f(n|a)dn

Proof. See Appendix A

4.1 Optimal control problem

The advertiser wishes to maximize its expected profit under the incentive compatibility,

participation and delegation constraints of the influencer. We express it in terms of the

13

following optimization program:

maxv,u,a,w

(∫ nH

nL

Πfdn

)subject to (10)

dY

dn=

∂Y

∂n(11)∫ nH

nL

Y fdn ≥ 0 (12)∫ nH

nL

(Y fa − h′f)dn = 0 (13)

We solve this program by setting up an optimal control problem and finding the

stationary points of the associated Hamiltonian. The expected profit function (10) under

the incentive compatibility constraint (11), the participation constraint (12) and the

delegation constraint (13) can be combined into the following Hamiltonian:

H = Πf + λ(n)Yn + µY f + ψ(Y fa − h′f) (14)

In the above Hamiltonian formulation, Y (·), the influencer’s payoff function is the

state variable with its equation of motion represented by condition (11). The control

variable is u(·); λ(n) is the co-state variable corresponding to the incentive compati-

bility constraint (11); and µ and ψ are the Lagrangian multipliers associated with the

participation constraint (12) and delegation constraint (13) respectively.

4.2 Optimal contract

The proposition below characterizes the necessary conditions for the optimal contract:

Proposition. The necessary conditions which characterize the optimal contract are as

follows:c′(u(n)− n)

c′′(u(n)− n)= −ψFa(n|a)

f(n|a)· (1− γ + γδ)

[1− γ + γδ − γρ(δ − 1)](15)∫ nH

nL

Y f(n|a)dn = 0 (16)∫ nH

nL

Y fa(n|a)dn = h′(a) (17)

∫ nH

nL

[R− (1− γ + γδ − ργ(δ − 1))c(u(n)− n)]fa(n|a)dn

−h′(a) + ψ

[∫ nH

nL

Y faa(n|a)dn− h′′(a)

]= 0 (18)

14

Yn = (1− γ + γδ)c′(u(n)− n) (19)

Proof. See appendix B

This proposition yields a key insight via equation (15)—that the lowest and high-

est type influencers do not fraudulently inflate their follower count. This is because

Fa(nL|a) = Fa(nH |a) = 0 rendering the right hand side zero. By implication, the left

hand side is also zero, leading to c′(u(nL) − nL) = c′(u(nH) − nH) = 0 which in turn

implies that u(nL) = nL and u(nH) = nH given the assumptions on the cost function.

For every other type in (nL, nH), the right hand side of equation (15) is positive, because

Fa(n) < 0 by assumption; and ψ > 0 since the participation constraint is tight [equation

(16)]. This is a key feature of our model which states that the faking level u(n) − n is

a non-monotonic function of n. Moreover, as we show in section 5, the level of faking

assumes an inverted U shape.

Intuitively, this means that faking levels are low for low types and for high types,

but high for intermediate types. Anecdotally too, investigations like Confessore et al.

(2018) uncover that buyers of fake followers tend to be people who are neither completely

unknown, nor A-list celebrities. Rather, their report exposes moderately famous man-

agement gurus, TV personalities, fashion models and specialist influencers as click farm

clients.

Corollary 1. The optimal payment to the influencer is given by:

v(n) = (1− γ + γδ)

[c(u(n)− n) +

∫ n

nL

c′(u(t)− t)dt]

(20)

w = h(a)− (1− γ + γδ)

∫ nH

nL

[∫ n

nL

c′(u(t)− t)dt]f(n|a)dn (21)

Proof. See appendix B.1

4.3 Implementability and sufficiency

Implementability requires that:

∂

∂n

(YuYv

)· dudn≥ 0 (22)

∂

∂n

(−(1− γ + γδ)c′(u(n)− n)

1

)du

dn≥ 0 (23)

The first term in (22) is the Spence-Mirrlees single-crossing condition. Based on the

inequalities above, u′ > 0 is required for implementability which implies that the displayed

follower count must increase with the true number of followers of the influencer.

15

In particular, if the cost function for hiring fakes is assumed to be quadratic, (15)

leads to:

u = n− ψFa(n|a)

f(n|a)·(

1− γ + γδ

1− γ + γδ − γρ(δ − 1)

)(24)

du

dn= 1−

(1− γ + γδ

1− γ + γδ − γρ(δ − 1)

)d

dn

(ψFa(n|a)

f(n|a)

)(25)

Clearly, for u′ > 0, it is sufficient that:

d

dn

(ψFa(n|a)

f(n|a)

)< 1− γρ(δ − 1)

(1− γ + γδ)

4.4 Revenue sharing contracts

Influencer marketing contracts can incorporate revenue sharing as a feature. We assume

that the advertiser shares an exogenous fraction α of the earned revenue R(n) with the

influencer in addition to v(n) + w. This is the most generalized version of a revenue

sharing compensation contract in line with Cachon and Lariviere (2005). We note that

while we account for such revenue sharing in our stylized model, it is not yet common in

influencer marketing. However, as mentioned before, norms in influencer marketing are

still evolving, and such arrangements may become more commonplace in future.

Figure 4 illustrates the revenue sharing setup. The advertiser’s revenue can be ex-

pressed by modifying equation (1) as:

Π = (1− α)R(n)− v(n)− w + γρ(δ − 1)c(u(n)− n) (26)

and the influencer’s payoff can be written by modifying equation (2) as:

Y = αR(n) + v(n) + w − h(a)− (1− γ + γδ)c(u(n)− n)) (27)

For this contract, the following necessary conditions holds:

Corollary 2. For the revenue sharing contract specified above, equations (15)-(18) hold.

Instead of equation (19), the following holds:

Yn = αR′(n) + (1− γ + γδ)c′(u(n)− n) (28)

Proof. See appendix B.2

The optimal payment for the revenue sharing contract is given by the following corol-

lary:

16

Corollary 3. The optimal payment for the revenue sharing contract specified above is:

v(n) = (1− γ + γδ)

[c(u(n)− n) +

∫ n

nL

c′(u(t)− t)dt]

(29)

w = h(a)−∫ nH

nL

[αR(n) + (1− γ + γδ)

(∫ n

nL

c′(u(t)− t)dt)]

f(n)dn (30)

Proof. See appendix B.3

It is important to note that while the above corollary suggests that equations (15)-(18)

hold, and hence faking levels are identical, this is not true. This is because u(n), w, ψ

and a are endogenous outcomes that are jointly determined and depend on the value of

α, with α = 0 characterizing the no-sharing condition. In fact, we show in section 5 that

revenue sharing can serve to reduce faking levels.

The case of α = 1 is of special interest to us because there are many popular influencers

starting their own brands, especially in the fashion sector. For example, Chriselle.x JOA,

SSO by Danielle and ARE YOU AM I are apparel brands owned by the popular fashion

influencers Chriselle Lim, Danielle Bernstein and Rumi Neely respectively (Boyd, 2018).

In this setting, the principal and agent are the same, and there is no incentive to the

influencer to fake her follower count.

5 Policy simulations

5.1 Motivation

In our main model, we have three exogenous parameters γ, δ and ρ which characterize the

accuracy, severity and potential restitutive compensation to the advertiser respectively.

Additionally, we have the exogenous parameter α which is the fraction of revenue shared

by the advertiser with the influencer. This specification leads to endogenous outcomes

u(n), v(n), a and ψ which constitute the payoff functions Π and Y . In an ideal scenario,

we would like to present comparative statics of the form du/dγ, du/dδ, etc., to ascertain

the relative effects of changes in exogenous parameters on faking levels and effort (i.e.

hidden action). Such an exercise is ideally the best and most general way to evaluate

policy implications for an analytical model such as ours.

Unfortunately, the complexity of the equations characterizing the optimal contract

renders such an analytical exercise infeasible. As equation (15) indicates, the faking

level u(n) − n and the variable payment v(n) depend on the endogenous Lagrangian

multiplier ψ and the optimal action a, apart from the exogenous parameters α, γ, δ and

ρ. Further, the endogenous outcomes ψ and a themselves are simultaneously determined

17

via equations (17) and (18) in the proposition. All of this renders analytical attempts at

comparative statics difficult and unintuitive.

In lieu of analytical comparisons, we present a detailed numerical simulation analy-

sis. Such methods are common in the marketing literature on agent-based models for

example, where analytical comparative statics are not feasible (eg. Goldenberg et al.,

2010; Libai et al., 2013). Here, we make reasonable assumptions about the functional

forms of R(n), c(u(n)− n), h(a) and F (n|a). We then take multiple combinations of the

exogenous parameter values α, γ, δ and ρ in a full factorial experimental design, and nu-

mercially compute the endogenous outcomes a, ψ, and in turn use them to calculate the

display function u(n) and hence faking level u(n) − n. As this is a randomized experi-

ment with a full factorial design, we then run ordinary least squares regressions on these

dependent variables, using the exogenous parameters α, γ, δ and ρ to evaluate the relative

impacts of each on the faking level and hidden action.

5.2 Numerical setup

We design our numerical sensitivity analysis on the lines of the brief illustration in Crocker

and Slemrod (2007). We assume the following functions:

R(n) = n (31)

c(u(n)− n) =(u(n)− n)2

2(32)

h(a) =a3

3(33)

F (n|a) = na; n ∈ [0, 1] (34)

which further leads to:

Fa(n|a) = na log n (35)

Faa(n|a) = na(log n)2 (36)

f(n|a) = ana−1 (37)

fa(n|a) = na−1(1 + a log n) (38)

faa(n|a) = na−1 log n(2 + a log n) (39)

This formulation allows us to now solve for ψ and a simultaneously from equations (17)

and (18) which yield:

18

[1

(1 + a)2− 2ψ2(1− a)

a2(2 + a)4· (1− γ + γδ)2

{1− γ + γδ − ργ(δ − 1)}

]− a2

+ψ

[−6ψ(1− γ + γδ)2

a(2 + a)4{1− γ + γδ − γρ(δ − 1)}− 2α

(1 + a)3− 2a

]= 0 (40)

2ψ

a(2 + a)3· (1− γ + γδ)2

{1− γ + γδ − γρ(δ − 1)}+

α

(1 + a)2− a2 = 0 (41)

As is evident, there is no closed form solution to a, ψ from the above, and these must be

solved numerically. Equation (15) yields the display function u(n) as:

u(n) = n− ψ

an log n · (1− γ + γδ)

[1− γ + γδ − γρ(δ − 1)](42)

From equation (29) we calculate v(n) as:

v(n) = (1− γ + γδ)

[(1− γ + γδ)2ψ2n2(log n)2

2a2[1− γ + γδ − γρ(δ − 1)]2+

(1− γ + γδ)ψn2(1− 2 log n)

4a(1− γ + γδ)

](43)

5.3 Simulation design

We now outline the design of our simulations based on the setup described in section 5.2.

We vary the parameters α, γ and ρ over 11 levels each between 0 and 1 with increments

of 0.1, and the parameter δ over 19 levels between 1 and 5 with increments of 0.5 in a

full factorial experimental design yielding 11,979 combinations of α, γ, δ, ρ.6 For each of

these, we solve equations (40) and (41) simultaneously using a numeric solver. We then

vary n at 11 levels 0 and 1 in increments of 0.1, and compute u(n) for each using equation

(15). Finally, we use these values to calculate v(n) from equation (20).

The above procedure yields us a synthetic data matrix with 131,769 observations.

Note that while outcomes a, ψ are computed independent of n, the faking level u(n)− ndepends on n. We perform analysis of this large data set.

5.4 Results and managerial implications

We now discuss the results of our policy simulations and their corresponding managerial

implications. Table 3 presents the results of ordinary least squares regressions that as-

certain the effects of exogenous parameters on faking levels and hidden action. Note that

while faking levels are type dependent, the action is not.

6We calibrate our simulations with an upper limit to δ to ensure that the advertiser’s implicit partic-ipation constraint is not violated.

19

Insert table 3 about here

For each of the dependent variables u(n) − n and a, we present two regressions, one

with only main effects of the exogenous parameters, and one with theoretically relevant

interaction effects. As the proposition predicts a non-monotonic relationship between the

faking level and type, the first two models incorporate n and n2. Figure 5 illustrates

these results as well, with a few selected curves depicting the faking level’s sensitivity to

exogenous policy parameters.

Insert figure 5 about here

The regressions demonstrate our key results. First of all, the revenue sharing fraction

α has a significant negative effect on the faking level, as well as a significant positive

effect on the hidden action, i.e. unobservable effort of the influencer (see figure 5 top

left). Thus, it works both to deter fraud and increase effort. Second, the audit accuracy

γ has a significant negative main effect on faking levels and a significant positive main

effect on the hidden action, only when interaction terms are not considered (models 1

and 3). With the relevant interactions , the main effect of γ on the faking level vanishes

(model 2). This is as per intuition—accurate audits only work as fraud deterrents when

they are accompanied by a harsh penalty on the offender. Note that δ is capped because

of the implicit advertiser’s participation constraint. Even a perfect audit γ = 1, along

with a permissibly high penalty factor δ cannot eliminate faking (see figure 5 top right

and bottom left). Thus, revenue sharing is a better solution to deter influencer fraud.

Our third observation is counter-intuitive and a key finding of this paper. While

the restitution factor ρ has a significant and positive main effect on the hidden action

a (model 3), it also encourages more faking, as indicated by the positive and significant

main effect in model 1. This vanishes when interaction terms are included (models 4 and

2 for hidden action and faking level respectively). However, the interaction terms on γρ

and γδρ both have positive significant coefficients in model 2 (for faking level) and only

for γδρ in model 4 (hidden action). Figure 5 (bottom right) illustrates this.

We interpret the above result thus: ρ is the fraction of the escalated costs (δ −1)c(u(n)−n) that the influencer incurs if caught with probability γ. It may be tempting

from an intuitive angle, or even from the point of view of fairness, for a third party

regulator like the Federal Trade Commission to direct the influencer to pay a large part

of its fine as compensation to the cheated advertiser. However, the deterrence effects

of having such a clause in an ex ante contract are questionable. In fact such a policy

backfires, causing the agent to fake her follower count even more. This is because with

expected restitution as indicated in equations (1) and (26), the principal is willing to

20

pay more in terms of v(n) + w, which in turn generates both legitimate incentives for

the influencer on her hidden action, as well as perverse incentives for her to fraudulently

inflate her follower count and cover this up.

The policy implications of this observation can be summed up in one line: as a

regulator, collect a reasonably high fine commensurate with the degree of fraud you have

incontrovertible evidence for, but keep all of it for yourself, rather than disbursing any

fraction back to the cheated advertiser. This indicates designing an ex ante contract with

a value of δ which is high enough, but ideally no restitution to the advertiser.

5.4.1 Interpreting audits

While we note that our policy simulations cover the whole range of γ ∈ [0, 1], in reality

we expect this accuracy to be low. As discussed in section 2.3, audits such as those

in Mathew (2018), ICMP (2019) and Stanley (2019) uncover the existence of several

fake followers of many well-known social media handles. However these audits do not

provide any evidence that the owners of these popular handles have themselves bought

fake followers. In fact, it is common practice for click farms to train both their human

employees and automated bots to follow popular social media handles. On the other

hand, thorough investigations like that by The New York Times (Confessore et al., 2018)

are rare, given the huge hurdles required to validate damaging claims against subjects of

such investigations.

The Confessore et al. (2018) expose is unique because it manages to get actual proof

of purchase of fake followers, primarily by moderately well-known personalities who are

neither completely obscure, nor A-list celebrities like Justin Bieber, Kim Kardashian or

Ellen Degeneres (named in ICMP, 2019), official Twitter handles of Liverpool, Manchester

United and Arsenal (named in Stanley, 2019) or Amitabh Bachchan (named in Mathew,

2018). Confessore et al.’s evidence consists of credit card details of these influencers (or

their social media managers) found in a well-known click farm’s database—a true smoking

gun that meets the high evidence standards required to establish the actual purchase of

fake followers and fake engagement (likes, shares, comments). In another prominent case,

the police of Mumbai, India claim to have evidence for 10 celebrities who have allegedly

bought fake followers.

Such evidence is almost impossible for even platforms like Twitter and Instagram

to provide without external investigation—while their internal databases and machine

learning algorithms have sophisticated fake follower detection techniques that can detect

both suspicious bot behavior and inexplicable spikes in follower count; unambiguously

proving that these fake followers were paid for by a the owner of a given social media

handle is non-trivial. Managers and regulators should keep this mind while commissioning

21

and interpreting audits.

5.4.2 Implications of revenue sharing

Our model predicts revenue sharing as a device to both increase the hidden action and

decrease the faking level of the influencer. Figure 6 plots the variable payment v(n)

as a function of the publicly displayed follower count u(n). As the top left shows, this

component is unnecessary when α = 1. As with faking levels, the payment v(n) actually

increases with the restitution factor ρ (bottom right). As the top right and bottom left

figures show, the payment to the influencer increases with accuracy γ and severity δ,

because the influencer passes on her higher expected costs back to the advertiser.

Insert figure 6 about here

As the influencer’s stake increases in the brand, her incentives to fake reduce as well.

At higher values of α, it represents a buy-in not unlike consulting and law firms when

employees are promoted as partners. While common in those contexts, the ethics in-

volved in this practice for influencer marketing may be up for debate. In an an analogous

setting, Bennett, Coleman & Co., the publishers of The Times of India (the world’s

largest-circulated English newspaper) and several popular TV news channels, instituted

a controversial initiative called Times Private Treaties, where it buys small stakes in ma-

jor brands and then promotes them in its media outlets. India’s regulatory authorities

stepped in to institute mandatory disclosure norms (Bansal, 2014). Influencer marketing

disclosure norms like those recently instituted by US regulators (FTC, 2019) may con-

sider caveats on revenue sharing arrangements too. As an interesting aside, marketing

researchers are now increasingly studying the effects of commercial relationship disclo-

sures on marketing outcomes in influencer marketing (e.g. Lou et al., 2019; Kim and Kim,

2020).

6 Conclusions

Our work addresses the concerns of a growing number of managers who now realise the

scale of the fake follower problem in influencer marketing. High profile executives like

Estee Lauder’s chief executive officer (Stewart, 2019), Unilever’s chief marketing officer

(Stewart, 2018) and Kellogg’s social media lead in UK & Ireland (Joseph, 2018) have all

gone on record to voice their concerns about this unsavory phenomenon in major industry

summits. There is today a consensus amongst marketers that this menace needs to be

tackled, but none whatsoever on how to do so.

22

Given that the click farms are getting more sophisticated than ever before, with

bot behavior being camouflaged with sophisticated algorithms modeled on real online

user behavior (Silverman, 2018), we expect the fake follower problem to persist, with

click farms developing more sophisticated methods to avoid fake follower detection, both

by human investigators and machine learning algorithms. Our work breaks from the

machine learning tradition of identifying fake followers, and instead studies the fake

follower problem from the fundamental incentives associated with influencer marketing.

Our model maps the influencer’s faking level with her true follower count, demonstrat-

ing an inverted U-shaped relationship with no faking at the highest and lowest types, and

more faking at intermediate types instead. In simple words, we find that the very obscure

“nano-influencers” and high-profile celebrities are unlikely to fake much. Rather, it is the

moderately famous influencers who are more likely to display inflated follower counts by

buying fake followers.

Our model also derives optimal payment schemes, demonstrating how revenue-sharing

can effectively deter faking and simultaneously increase unobserved effort by the influ-

encer. We demonstrate that accurate audits need to be coupled by commensurate penal-

ties to deter influencer fraud. However, such penalties are better collected by third party

industry regulators than given back as restitution to cheated advertisers.

Methodologically, we use contract theory coupled with optimal control; this is well-

established in economics but to the best of our knowledge, new to marketing. Using

analogous scenarios from the insurance and earnings management literature, we model the

advertiser-influencer game in a principal-agent setting, simultaneously including moral

hazard and audits together.

Our results are consistent with observed trends in influencer marketing, illuminating

a dark corner of this unfortunately murky world.

Appendices

A Proof of Lemma

Proof. The delegation constraint requires that the action a chosen by the influencer must

optimize her expected payoff:

maxa

∫ nH

nL

Y fdn (A1)

23

This requires two conditions, first that the derivative of the expected payoff with respect

to a be 0:d

da

∫ nH

nL

Y fdn = 0 (A2)

and the second that the second derivative at the optimal a be negative:

d2

da2

∫ nH

nL

Y fdn < 0 (A3)

d

da

∫ nH

nL

(Y fa − h′f) dn < 0 (A4)∫ nH

nL

(Y faa − h′fa − h′′f − h′fa) dn < 0 (A5)∫ nH

nL

Y faadn− h′′ < 0 (A6)

where the last line follows from∫ nH

nLfadn = Fa(nH |a) = Fa(nL|a) = 0 − 0 = 0. Substi-

tuting the definition of Y we get:∫ nH

nL

[v(n) + w − h(a)− (1− γ + γδ)c(u− n)]faadn− h′′ < 0 (A7)

(w − h(a))

∫ nH

nL

faadn+

∫ nH

nL

[v(n)− (1− γ + γδ)c(u− n)]faadn− h′′ < 0 (A8)

Noting that∫ nH

nLfaadn = Faa(nH |a) − Faa(nL|a) = 0 − 0 = 0 and using integration by

parts for the second term, we get:

[v(n)− (1− γ + γδ)c(u(n)− n)]Faa(n|a)

∣∣∣∣nH

nL

−∫ nH

nL

[v′(n)− (1− γ + γδ)(c′ · (u′ − 1))]Faadn− h′′ < 0 (A9)

Again the first term vanishes since Faa(nH |a) − Faa(nL|a) = 0 − 0 = 0. Further, noting

that

dY

dn= v′ − (1− γ + γδ)c′ · (u′ − 1) =

∂Y

∂n= (1− γ + γδ)c′ (A10)

Substituting the above result, we obtain:

−(1− γ + γδ)

(∫ nH

nL

c′Faadn

)− h′′ < 0 (A11)

Clearly, the above inequality holds if Faa > 0.

24

B Proof of Proposition

Proof. The Hamiltonian for the optimal control program is

H = Πf + λ(n)Yn + µY f + ψ(Y fa − h′f) (B1)

Using the definition of the payoff function Π in equation (1); and the value of Yn from

equation (6), we get

H = (R−h−[1−γ+γδ−γρ(δ−1)]c−Y )f+λ(n)(1−γ+γδ)c′+µY f+ψ(Y fa−h′f) (B2)

The Pontryagin first order conditions are:

1. Optimality condition:

maxu

H ∀n ∈ [nL, nH ] ≡ ∂H∂u

= 0

2. Equation of motion for state:

dY

dn=∂H∂λ

= Yn

3. Equation of motion for costate:

dλ

dn= −∂H

∂Y

4. Transversality condition for state:

λ(nL) = 0

Using the optimality condition:

∂H∂u

= 0⇒ − [1− γ + γδ − γρ(δ − 1)] c′f + λ(1− γ + γδ)c′′ = 0 (B3)

c′

c′′=λ

f

[1− γ + γδ

1− γ + γδ − γρ(δ − 1)

](B4)

Using the equation of motion for costate:

dλ

dn= −∂H

∂Y= − [−f + µf + ψfa] (B5)

= (1− µ) f − ψfa (B6)

25

Moreover, since a and w are independent of n, they must constitute the argmax of the

following objective function:

maxa,w

∫ nH

nL

[Πf + µY f + ψ(Y fa − h′f)] dn (B7)

Thus the derivative of the objective function above with respect to w must be 0. Further,

using the fact that Πw = −1 and Yw = 1, we get

d

dw

∫ nH

nL

[Πf + µY f + ψ(Y fa − h′f)] dn = 0 (B8)∫ nH

nL

[Πwf + µYwf + ψYwfa] dn = 0 (B9)

(−1 + µ)

∫ nH

nL

fdn+ ψ

∫ nH

nL

fadn = 0 (B10)

We note that∫ nH

nLfdn = 1 and that

∫ nH

nLfadn = Fa(nH |a)−Fa(nL|a) = 0− 0 = 0, which

leads to

− 1 + µ = 0⇒ µ = 1 (B11)

Substituting this value of µ in (B6) and using the transversality condition λ(nL) = 0 and

the fact that Fa(nL|a) = 0 we get the expression for λ:

dλ

dn= −ψfa ⇒ λ(n)− λ(nL) = −ψ

∫ n

nL

fadn (B12)

λ(n) = −ψFa(n|a) (B13)

Finally, we substitute the above expression for λ to derive (15):

c′(u(n)− n)

c′′(u(n)− n)= −ψFa(n|a)

f(n|a)

[1− γ + γδ

1− γ + γδ − γρ(δ − 1)

](B14)

We can make some quick observations regarding the display function u(n) from the

equation above. First, at n = nL, since Fa(nL|a) = 0, the RHS equals 0, which in turn

implies that the LHS is 0 leading to the implication that c′(u(nL)−nL) = 0⇒ u(nL) = nL.

Similary, u(nH) = nH . Second, for all types nL < n < nH , the RHS is strictly positive,

since Fa(n|a) < 0 and the tightness of the delegation constraint necessitates that ψ > 0.

This in turn implies that the LHS be strictly positive, leading to u(n) > n.

Returning to the argument that posits that the action undertaken to increase the

follower count is independent of n, we require that the derivative of the objective function

26

with respect to a be 0 and using µ = 1 from (B11), we get:

d

da

∫ nH

nL

[(Π + Y ) f + ψ(Y fa − h′f)] dn = 0

Using the definition of Π and Y and substituting, we get:

d

da

∫ nH

nL

(R− [1− γ + γδ − γρ(δ − 1)] c− h) fdn+ ψd

da

∫ nH

nL

(Y fa − h′f) dn = 0

We note that Ya = −h′(a) and expand the above expression:∫ nH

nL

(R− [1− γ + γδ − γρ(δ − 1)]c) fadn− h′∫ nH

nL

fdn− h∫ nH

nL

fadn+

ψ

(∫ nH

nL

Y faadn− h′∫ nH

nL

fadn− h′∫ nH

nL

fadn− h′′∫ nH

nL

fdn

)= 0

Noting that∫ nH

nLfdn = 1 and that

∫ nH

nLfadn = 0, we simplify the above to derive (18)

∫ nH

nL

[R− (1− γ + γδ − γρ(δ − 1))c] fadn− h′ + ψ

(∫ nH

nL

Y faadn− h′′)

= 0

Finally, partially differentiating Y with respect to n, we obtain equation (19)

Y = v(n) + w − h(a)− (1− γ + γδ)c(u(n)− n)

Yn = (1− γ + γδ)c′(u(n)− n) (B15)

B.1 Proof of Corollary 1

Proof. In order to derive the variable payment schedule we use incentive compatibility

(11)

dY

dt=∂Y

∂t(B16)∫ n

nL

dY

dtdt =

∫ n

nL

∂Y

∂tdt (B17)

Y (n)− Y (nL) =

∫ n

nL

∂

∂t(v(t) + w − h(a)− (1− γ+γδ)c(u(t)− t))dt (B18)

Using the fact that c(u(nL)− nL) = 0 and simplifying

v(n)− v(nL)− (1− γ + γδ)c(u(n)− n) = (1− γ + γδ)

∫ n

nL

c′(u(t)− t)dt (B19)

27

Normalizing v(nL) = 0 without loss of generality, we obtain:

v(n) = (1− γ + γδ)

[c(u(n)− n) +

∫ n

nL

c′(u(t)− t)dt]

(B20)

Now we derive the expression for the fixed payment w. Using the fact that the

expected ex-ante payoff for the influencer is 0, which follows since the corresponding

multiplier µ = 1 (B11), we get:∫ nH

nL

[v + w − h− (1− γ + γδ)c] fdn = 0 (B21)

(w − h)

∫ nH

nL

f(n|a)dn+

∫ nH

nL

[v − (1− γ + γδ)c]fdn = 0 (B22)

Using the value of the variable payment v from above and expanding, we get

w = h−∫ nH

nL

[(1− γ + γδ)c− (1− γ + γδ)

(c+

∫ n

nL

c′dt

)]f(n|a)dn (B23)

w = h(a)− (1− γ + γδ)

∫ nH

nL

(∫ n

nL

c′(u(t)− t)dt)f(n|a)dn (B24)

B.2 Proof of Corollary 2

Proof.

Y = αR + v + w − h− (1− γ + γδ)c(u(n)− n) (B25)

Yn = αR′ + (1− γ + γδ)c′(u(n)− n) (B26)

28

B.3 Proof of Corollary 3

Proof.

dY

dt=∂Y

∂t(B27)∫ n

nL

dY

dtdt =

∫ n

nL

∂Y

∂tdt (B28)

Y (n)− Y (nL) =

∫ n

nL

∂

∂t[v(t) + w + αR(t)− h(a)− (1− γ + γδ)c(u(t)− t)]dt (B29)

=

∫ n

nL

[αR′(t)− (1− γ + γδ)c′(u(t)− t)]dt (B30)

Using the fact that c(u(nL)− nL) = 0 and simplifying

v(n)− v(nL) + α(R(n)−R(nL))− (1− γ + γδ)c(u(n)− n)

= α[R(n)−R(nL)] + (1− γ + γδ)

(∫ n

nL

c′(u(t)− t)dt)

(B31)

Normalizing v(nL) = 0 without loss of generality, we obtain:

v(n) = (1− γ + γδ)

[c(u(n)− n) +

∫ n

nL

c′(u(t)− t)dt]

(B32)

For the fixed payment w

∫ nH

nL

[v + w + αR− h− (1− γ + γδ)c] fdn = 0 (B33)

(w − h)

∫ nH

nL

f(n)dn+

∫ nH

nL

[v + αR− (1− γ + γδ)c]fdn = 0 (B34)

Finally, substituting for the variable payment v and simplifying we get:

w = h(a)−∫ nH

nL

[αR(n) + (1− γ + γδ)

(∫ n

nL

c′(u(t)− t)dt)]

f(n)dn (B35)

29

References

Aral, S. and D. Walker (2012). Identifying influential and susceptible members of social

networks. Science 337 (6092), 337–341.

Bakshy, E., J. M. Hofman, W. A. Mason, and D. J. Watts (2011). Everyone’s an influ-

encer: quantifying influence on Twitter. In Proceedings of the fourth ACM international

conference on Web search and data mining, pp. 65–74. ACM.

Bansal, S. (2014). TRAI calls for ban on private treaties and paid news. Livemint .

Berger, J. (2016). Contagious: Why things catch on. Simon and Schuster.

Berger, J. and E. M. Schwartz (2011). What drives immediate and ongoing word of

mouth? Journal of Marketing Research 48 (5), 869–880.

Bhardwaj, P. (2001). Delegating pricing decisions. Marketing Science 20 (2), 143–169.

Boyd, S. (2018). Influencer owned brands taking the fashion industry by storm. Forbes .

Cachon, G. P. and M. A. Lariviere (2005). Supply chain coordination with revenue-sharing

contracts: strengths and limitations. Management Science 51 (1), 30–44.

Caro, F. and V. Martınez-de Albeniz (2020). Managing online content to build a follower

base: Model and applications. INFORMS Journal on Optimization 2 (1), 57–77.

Chang, S., V. Kumar, E. Gilbert, and L. G. Terveen (2014). Specialization, homophily,

and gender in a social curation site: findings from pinterest. In Proceedings of the

17th ACM conference on Computer supported cooperative work & social computing,

pp. 674–686.

Confessore, N., G. Dance, R. Harris, and M. Hansen (2018). The Follower Factory. New

York Times .

Crocker, K. J. and P. Letizia (2014). Optimal policies for recovering the value of consumer

returns. Production and Operations Management 23 (10), 1667–1680.

Crocker, K. J. and J. Morgan (1998). Is honesty the best policy? Curtailing insurance

fraud through optimal incentive contracts. Journal of Political Economy 106 (2), 355–

375.

Crocker, K. J. and J. Slemrod (2005). Corporate tax evasion with agency costs. Journal

of Public Economics 89 (9-10), 1593–1610.

30

Crocker, K. J. and J. Slemrod (2007). The economics of earnings manipulation and

managerial compensation. RAND Journal of Economics 38 (3), 698–713.

Crocker, K. J. and S. Tennyson (2002). Insurance fraud and optimal claims settlement

strategies. Journal of Law and Economics 45 (2), 469–507.

De Veirman, M., V. Cauberghe, and L. Hudders (2017). Marketing through Instagram in-

fluencers: the impact of number of followers and product divergence on brand attitude.

International Journal of Advertising 36 (5), 798–828.

Dionne, G., F. Giuliano, and P. Picard (2009). Optimal auditing with scoring: Theory

and application to insurance fraud. Management Science 55 (1), 58–70.

Djafarova, E. and C. Rushworth (2017). Exploring the credibility of online celebrities’ In-

stagram profiles in influencing the purchase decisions of young female users. Computers

in Human Behavior 68, 1–7.

Doherty, N. and K. Smetters (2005). Moral hazard in reinsurance markets. Journal of

Risk and Insurance 72 (3), 375–391.

eMarketer (2017). Attitudes Toward Influencer Marketing Among US Agency and Brand

Marketers, Nov 2017 (% of respondents). Technical report.

Ferreira, N. M. (2019). How to get followers on Instagram: From 0 to 10k followers.

Oberlo.

FTC (2012). At FTC’s request, US court hands down record $478 million judgment

against marketers of massive get-rich-quick infomercial scams. Federal Trade Commis-

sion.

FTC (2017). Uber agrees to pay $20 million to settle FTC charges that it recruited

prospective drivers with exaggerated earnings claims. Federal Trade Commission.

FTC (2019). Disclosures 101 for social media influencers. Federal Trade Commission.

Goldenberg, J., B. Libai, and E. Muller (2010). The chilling effects of network externali-

ties. International Journal of Research in Marketing 27 (1), 4–15.

Hovland, C. I. and W. Weiss (1951). The influence of source credibility on communication

effectiveness. Public Opinion Quarterly 15 (4), 635–650.

Hughes, C., V. Swaminathan, and G. Brooks (2019). Driving brand engagement through

online social influencers: An empirical investigation of sponsored blogging campaigns.

Journal of Marketing 83 (5), 73–96.

31

Hutto, C. J., S. Yardi, and E. Gilbert (2013). A longitudinal study of follow predictors

on Twitter. In Proceedings of the sigchi conference on human factors in computing

systems, pp. 821–830.

ICMP (2019). Who has the most fake followers?

IRI (2018). BzzAgent and IRI Find Everyday Influencer Marketing Programs Drive the

Highest Return on Ad Spend. Technical report.

Jin, S.-A. A. and J. Phua (2014). Following celebrities’ tweets about brands: The im-

pact of twitter-based electronic word-of-mouth on consumers’ source credibility per-

ception, buying intention, and social identification with celebrities. Journal of Adver-

tising 43 (2), 181–195.

Joseph, S. (2018). ‘we don’t pay influencers on reach’: How Kellogg’s is combating

influencer fraud. Digiday .

Kannan, P. K. and H. A. Li (2017). Digital marketing: A framework, review and research

agenda. International Journal of Research in Marketing 34 (1), 22–45.

Kim, D. Y. and H.-Y. Kim (2020). Influencer advertising on social media: The multiple

inference model on influencer-product congruence and sponsorship disclosure. Journal

of Business Research.

Kolay, S. (2018). Tie-in contracts with downstream competition. Quantitative Marketing

and Economics 16 (1), 43–77.

Kotler, P. and K. Keller (2012). Marketing management 15th edition pearson education

ltd.

Kumar, V., V. Bhaskaran, R. Mirchandani, and M. Shah (2013). Practice prize win-

ner—creating a measurable social media marketing strategy: increasing the value and

ROI of intangibles and tangibles for hokey pokey. Marketing Science 32 (2), 194–212.

Kumar, V. and R. Mirchandani (2012). Increasing the ROI of social media marketing.

MIT Sloan Management Review 54 (1), 55.

Lappas, T., G. Sabnis, and G. Valkanas (2016). The impact of fake reviews on online

visibility: A vulnerability assessment of the hotel industry. Information Systems Re-

search 27 (4), 940–961.

Letzter, R. (2016). Yes, the click farms on HBO’s ’Silicon Valley’ are a real thing and

they aren’t going away.

32

Lewis, R. A. and J. M. Rao (2015). The unfavorable economics of measuring the returns

to advertising. Quarterly Journal of Economics 130 (4), 1941–1973.

Libai, B., E. Muller, and R. Peres (2013). Decomposing the Value of Word-of-Mouth Seed-

ing Programs: Acceleration Versus Expansion. Journal of Marketing Research 50 (2),

161–176.

Linqia (2018). The state of influencer marketing. Technical report, Linqia.

Lou, C., S.-S. Tan, and X. Chen (2019). Investigating consumer engagement with

influencer-vs. brand-promoted ads: The roles of source and disclosure. Journal of

Interactive Advertising 19 (3), 169–186.

Luca, M. and G. Zervas (2016). Fake it till you make it: Reputation, competition, and

Yelp review fraud. Management Science 62 (12), 3412–3427.

Marsden, P. V. and N. E. Friedkin (1993). Network studies of social influence. Sociological

Methods & Research 22 (1), 127–151.

Mathew, S. (2018). Oh my! Amitabh Bachchan is so touchy about his Twitter followers.

The Quint .

McCracken, G. (1989). Who is the celebrity endorser? Cultural foundations of the

endorsement process. Journal of Consumer Research 16 (3), 310–321.

McGuire, W. J. (1985). Attitudes and attitude change. The handbook of social psychology ,

233–346.

Mishra, B. K. and A. Prasad (2004). Centralized pricing versus delegating pricing to the

salesforce under information asymmetry. Marketing Science 23 (1), 21–27.

Mishra, B. K. and A. Prasad (2005). Delegating pricing decisions in competitive markets

with symmetric and asymmetric information. Marketing Science 24 (3), 490–497.

Mishra, B. K. and A. Prasad (2006). Minimizing retail shrinkage due to employee theft.

International Journal of Retail & Distribution Management 34 (11), 817–832.

Morris, C. (2019). Facebook will pay $40 million to settle advertiser lawsuits claiming it

inflated video views by up to 900%. Fortune.

Myerson, R. B. (1979). Incentive compatibility and the bargaining problem. Economet-

rica 47, 61–73.

33

Neff, J. (2018). Study of influencer spenders finds big names, lots of fake followers. AdAge

India.

Newberry, C. (2019). How to get free Instagram followers: 27 tips that actually work.

Hootsuite Blog .

Padmanabhan, V. and R. C. Rao (1993). Warranty policy and extended service contracts:

Theory and an application to automobiles. Marketing Science 12 (3), 230–247.

Paquet-Clouston, M., O. Bilodeau, and D. Decary-Hetu (2017). Can We Trust Social

Media Data?: Social Network Manipulation by an IoT Botnet. In Proceedings of the

8th International Conference on Social Media & Society, #SMSociety17, New York,

NY, USA, pp. 15:1–15:9. ACM.

Patel, N. (2018). How to get more social media followers (without creating content). Neil

Patel’s Blog .

Pathak, S. (2017). Cheatsheet: What you need to know about influencer fraud. Digiday .

SEC (2018). Theranos, CEO Holmes, and former president Balwani charged with massive

fraud. Securities and Exchange Commission.

Sehl, K. (2020). How much do influencers charge? Hootsuite Blog .

Sideqik (2020). The ultimate cheat sheet on how to incentivize influencers. Sideqik .

Silverman, C. (2018). Apps Installed On Millions Of Android Phones Tracked User

Behavior To Execute A Multimillion-Dollar Ad Fraud Scheme. BuzzFeed .

Simester, D. and J. Zhang (2010). Why are bad products so hard to kill? Management

Science 56 (7), 1161–1179.

Simester, D. and J. Zhang (2014). Why do salespeople spend so much time lobbying for

low prices? Marketing Science 33 (6), 796–808.

Sridhar, S., P. A. Naik, and A. Kelkar (2017). Metrics unreliability and marketing over-

spending. International Journal of Research in Marketing 34 (4), 761–779.

Stanley, A. (2019). REVEALED: The Premier League clubs with the most ‘fake followers’

– from lowest to highest. talkSPORT .

Stewart, R. (2018). Unilever’s Keith Weed calls for ’urgent action’ to tackle influencer

fraud. The Drum.

34

Stewart, R. (2019). Estee Lauder now spends a huge portion of its marketing budget on

influencers. The Drum.

Sun, B. (2014, April). Executive compensation and earnings management under moral

hazard. Journal of Economic Dynamics and Control 41, 276–290.

Tellis, G. J. (2003). Effective advertising: Understanding when, how, and why advertising

works. Sage.

The Economist (2016). Celebrities’ endorsement earnings on social media - Daily chart.

Wilbur, K. C. and Y. Zhu (2009). Click fraud. Marketing Science 28 (2), 293–308.

Yoganarasimhan, H. (2012, March). Impact of social network structure on content prop-

agation: A study using YouTube data. Quantitative Marketing and Economics 10 (1),

111–150.

35

Table 1: Summary of notation used in our model