© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice.

Printing and Personal Systems Dion Weisler Executive Vice President Printing and Personal Systems

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 2 © Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 2

Three waves Printing and Personal Systems

Wave three

Create New categories New ways to use technology

Wave two

Anticipate Internet of things

3D printing

Digital packaging

Services

New ecosystems

Wave one

Capitalize PCs & printing Multi-OS / architecture Detachables / hybrids Solutions

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 3 © Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 3

Wave three

Create Wave one

Capitalize

Wave two

Anticipate

Investment

Segmentation

Execution

Three waves Printing and Personal Systems

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 4 © Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 4

Ink in 2009 A case study

Wave three

Create Wave one

Capitalize

Wave two

Anticipate

Introduced first Ink-in-the-Office product

Recognized SMB and emerging-market need for lower cost

Began investments: - Page-wide array - Ink chemistry

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 5 © Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 5

Ink in 2013 A case study

• Business ink market growing 9%1

• TAM expected to reach $10 billion by 2016 • OfficeJet Pro expected to achieve double-digit

unit growth • Ink-in-the-Office represents ~1/3 of HP’s ink sales

1. Expected market revenue CAGR for '13 - '16 Source: HP internal analysis

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 6

Personal Systems

©2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice.

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 7

Personal Systems accomplishments

#1 Commercial player1

+3pts.

Outgrew PC market1

13pts. Quality improvement2

600

New partners in China #1 In India1

4 Operating systems

1. CQ2'13 IDC PC Tracker (units) 2. HP internal analysis of Q3 FY13 year-over-year improvement

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 8

$112B / 10%

Tablets

Personal Systems market continues to evolve

Source: HP internal analysis, Sept. 2013 (does not include smartphones) All data: Market revenue in 2016 and market revenue CAGR from ’13 – ’16

$21B / 23%

Commercial Tablets

$12B / 65%

Hybrids

$22B / 8%

HP SmartFriend Services

Services

$170B / -4%

PCs

$15B / 4%

All-in-One

$46B / 12% 3% (HW, PCs + tablets)

Emerging markets

Market expected to reach $400B by 2016 with 3% CAGR

$43B / 12%

Accessories

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 9

Commercial personal systems

Market expected to reach $160B and grow 2%1

+8 pts. (CQ2’13)

Outgrew the market2 Market share2 Competition2 (Y/Y unit growth)

Profitability

Core strength

#1 +1.6 pts.

(CQ2’13)

HP Lenovo Dell Acer Apple

5% 0% -2%

-35% -2%

$

#1 Customer base Patents3 Synergies Channel partners

14K 150K Pan-HP

1. HP internal analysis: Market revenue in 2016 and market revenue CAGR from ’13 – ’16 2. CQ2'13 IDC PC Tracker (units) 3. Number of pan-PPS Patents in portfolio

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 10

Commercial personal systems

Desktops

#1

• 20% share

• Opportunity at entry-level

Workstations

#1

• 47% share

• First Ultrabook

• First all-in-one

Thin clients

#1 • 27% share

• Lowest power

• VDI trend

Notebooks

#2

• 21% share

• Elitebook 800

• Self-healing BIOS

Tablets

#4

• 2% unit share

• Hardened OS & security

Market expected to reach $160B and grow 2%

Sources: Market revenue in 2016 and market revenue CAGR from CY ’13 – ’16 based on HP internal analysis; market share data: CQ2'13 IDC PC Trackers (units)

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 11

Opportunity Commercial desktop share

Desktop unit mix for 1H131

41% 31%

38% 42%

12% 17%

9% 10%

Market HP

Value: $400-$699

Entry: <$399

Mainstream: $700-$1,000

Premium: >$1,000

1. 2Q'13 IDC PC Tracker units share 2. Market units CAGR % based on internal HP analysis

HP share1

1H13 units

23%

30%

22%

15%

Market CAGR2

Units ’13 - ’16

-6%

-11%

-3%

+4%

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 12

Consumer personal systems

1. HP internal analysis; market revenue in 2016 and market revenue CAGR from ’13 – ’16 2. CQ2'13 IDC PC Tracker (units)

Market expected to reach $240B and grow 3%1

Platforms Multi-OS Crossover Form factors

Industry “firsts” Retail

160K Retail stores

Pipeline for commercial

Windows Chrome Android Ubuntu

Intel AMD Nvidia Rockchip

Rove Split x2 Revolve

Chrome on Intel

Detachable with Haswell

Embedded LEAP

First at home, then at work

Market share (PCs)2

#2 Ecosystem

HP Connected Smart Friend SMB IT in a Box

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 13

Consumer personal systems

1. HP internal analysis; market revenue in 2016 and market revenue CAGR from ’13 – ’16

Market expected to reach $240B and grow 3%1

Tablets

• Targeted bursts

• Profitable

• Segmented

Services

HP SmartFriend

Form factors Bring your own device & SMB

Multi-OS

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 14

In summary

Commercial is core strength

Consumer is strategic to crossover from home to work

Segmenting to attack the “heat” in the market

Continuing operational excellence

Driving strategy to “capitalize, anticipate and create” across all waves

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 15

Printing

©2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice.

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 16

Printing accomplishments

2 pts.

Enhanced profitability3

16 New multi-function printers

30%

Fewer nodes

Double-digit Growth in Ink-in-the-Office2

#1 Market share1

15%

Reduction in ink SKUs

1. CQ2'13 IDC Hardcopy Tracker 2. Expected year-over-year revenue growth in FY13 3. Year-over-year operating margin improvement in Q1-Q3 FY13 All other data: HP internal analysis

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 17

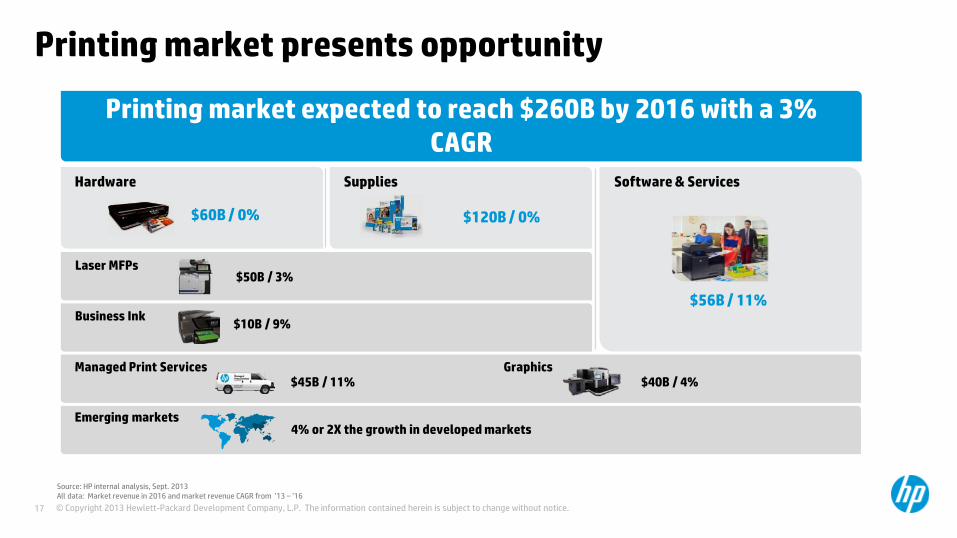

Printing market presents opportunity

Printing market expected to reach $260B by 2016 with a 3% CAGR

Supplies

$120B / 0%

Software & Services

$56B / 11%

Source: HP internal analysis, Sept. 2013 All data: Market revenue in 2016 and market revenue CAGR from ’13 – ’16

Hardware

$60B / 0%

$50B / 3% Laser MFPs

$10B / 9% Business Ink

4% or 2X the growth in developed markets Emerging markets

$45B / 11% Managed Print Services

$40B / 4% Graphics

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 18

Extending HP leadership

#1

Graphics

#3

Managed Print Services Supplies (ink & toner)

#1

Business Ink

#1 #1

Laser MFPs

#1 Laser | Inkjet

Hardware

Sources: Hardware, Laser MFPs, and Graphics - IDC Hardcopy Tracker CQ2'13; Business Ink and Supplies - HP Internal analysis; Managed Print Services - IDC WW Managed Print Services (doc #241884) June 2013

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 19

Driving innovation Stephen Nigro Senior Vice President Inkjet and Printing Solutions

©2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice.

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 20

HP targeted print growth

Cost savings

• Multi-Function Printers (MFP) • Ink-in-the-Office (IITO) • Indigo

Growth markets • Ink Advantage • Instant Ink • Managed Print Services (MPS)

New business models • ePrint • Cloud, Mobility & Security

Solutions

New Style of IT

Quality

Innovation

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 21

Growing LaserJet MFP share

1. IDC Worldwide Quarterly HCP Tracker, August 2013; and HP internal data CQ2'13

• Growth market • Expanded portfolio of MFPs;

launched 16 new MFPs • #1 in MFP share (+1.5 pts. share gain Y/Y)1

• HW unit growth of 34% Y/Y1

• Outgrew the market for last 5 consecutive quarters

• Expect to continue the momentum

New NFC-enabled HP flow MFPs

• Simple and secured mobile printing with wireless direct and Touch-to-Print

• Extending flow capabilities into department MFPs

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 22

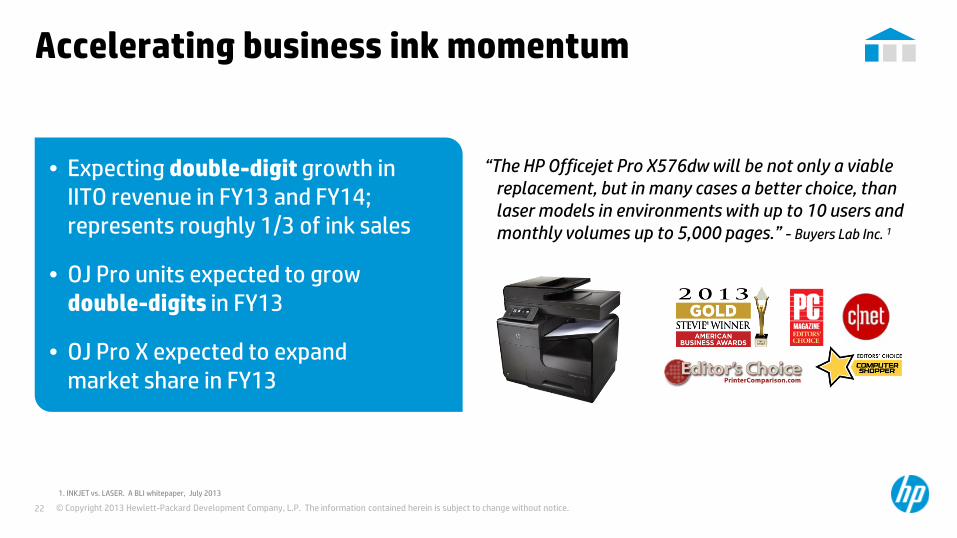

• Expecting double-digit growth in IITO revenue in FY13 and FY14; represents roughly 1/3 of ink sales

• OJ Pro units expected to grow double-digits in FY13

• OJ Pro X expected to expand market share in FY13

Accelerating business ink momentum

“The HP Officejet Pro X576dw will be not only a viable replacement, but in many cases a better choice, than laser models in environments with up to 10 users and monthly volumes up to 5,000 pages.” - Buyers Lab Inc. 1

1. INKJET vs. LASER. A BLI whitepaper, July 2013

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 23

Accelerating growth in graphics Indigo business growth — driven by innovation

Source: Market share and size based on HP estimates

Indigo has an installed base of over 6,000 presses, driving…

Growth and market share Innovation: Indigo packaging

Indigo 20000 • May 2014 • Intro into $3B flexible

packaging market

Indigo 30000 • May 2014 • Intro into $2B folding carton

packaging market

19% CAGR in page growth since 2010

64% Market share Digital press / CQ2'13

+6% points over CQ2'12

Both new packaging platforms being launched are based on the new Indigo 10000 platform launched this year

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 24

Making ink more affordable with new ink models

• Expecting triple-digit year-over-year unit growth for FY13

• Available in more than 130 countries

• HP ink usage connect rate is more than 2.3X that of comparable products1

• Estimated gross margin improvement of more than 30 ppts. on hardware (Combined hardware + supplies = 15 ppts. estimated gross margin improvement)

HP Ink Advantage Exceeding our connect rate, usage and after-market share objectives

1. HP internal analysis, usage connect rate data based on usage improvement 2012-2013

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 25

Instant Ink expansion addresses customer needs Customers save up to 50%1 on original HP Ink, enjoy convenience of never running out of ink2, and lower their carbon footprint for cartridge consumption by ~65%3

Monthly printing plans: Occasional Moderate Frequent $2.99 for 50 pages

$4.99 for 100 pages

$9.99 for 300 pages

• Up to 50 rollover pages • $1 for 15 more pages

• Up to 100 rollover pages

• $1 for 20 more pages

• Up to 300 rollover pages

• $1 for 30 more pages

• ~93% customer retention rate4 • Nationwide rollout underway in Best

Buy, Office Max, HP Shopping • Improves system model with 100%

supplies aftermarket share

1. Savings do not apply for Officejet Pro printers used in $2.99 plan. Savings are based on the HP Instant Ink service plan price for 12 months, using all pages in the plan without purchasing additional blocks of pages, compared to the estimated street price of Original HP standard-size in cartridges and published yield printing ISO/IEC 24711 pages, ISO pages are a mix of text and graphics, color and black, 8.5” x 11” pages that meet ISO testing guidelines. Actual savings may vary depending on the number of pages printed per month, print resolution, type and size of pages printed, plan, and printer platform. For more information on ISO standards, see hp.com/go/pageyield 2. Based on plan usage, internet connection to an eligible HP printer, valid credit/debit card, email address, and delivery service in your geographic area 3. Source: "Summary of Data and Assumptions for Instant Ink Program Carbon Footprint Analysis" 2013 study performed by Four Elements Consulting. Analysis includes the CO2 equivalent associated with customer trips to purchase ink cartridges at a retail store versus delivering directly to a customer’s house, and it includes recycling empty ink cartridges versus throwing them away 4. Instant Ink Pilot results as of Sept 1, 2013

hp.com

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 26

Managed Print Services Capturing the growing MPS market

Advantage HP

Source: HP internal analysis 1. Cumulative growth from 2012-1H’13 2. Results from 1H'13

• Expect $45B TAM in 2016

• Expect 11% revenue CAGR '13 - '16

• Printer and copier convergence

• Contractual model expanding to solutions

Market dynamics Strategic focus • Strategic partner

• Automation and intelligence

• Global scale and flexibility

• Service delivery

Service Delivery Excellence

• 23% MPS TCV growth1

• Partner-MPS growth = 4x market2

• Partnering for reach

• Global expansion

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 27

Mobility Cloud Security

Print solutions for the New Style of IT

• 37% of WW workforce mobile by 20151

• 1/3 of wireless printers are receiving prints from mobile devices2

• Total U.S. mobile pages expected to grow 12.5% from CY12 – CY163

• 700M print-enabled tablets and smartphones

• 1 trillion pages to be digitized by 20154

• ePrint shows 69% '11 – '13 CAGR4

• $5.5M average cost per incident of corporation information theft5

• Simple and secured mobile printing for SMB/Enterprise

Flow CM

Access Control

Imaging and Printing Security Center

1. IDC, Mobile Printing Landscape: Transition to Early Adopters, August, 2012 2. Pages and printers estimated 3. IDC Multi-client Study: Mobile Devices and Impact on Print – and End-User Analysis and Print Volume Forecast, 2012 4. HP internal research 5. U.S. Cost of a Data Breach report, Ponemon Institute, 2012

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 28

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice. 29

Profitability

• Accelerating in print

• Applying three “waves” in personal systems

• Leveraging commercial strength

• Segmenting maniacally

• Creating market “crossovers”

• Innovating across the business

Strong momentum to win

© Copyright 2013 Hewlett-Packard Development Company, L.P. The information contained herein is subject to change without notice.

Thank you