Download - How Consumers Perceive Luxury Brands - Integreon … Consumers Perceive Luxury Brands Grail Research

How Consumers Perceive Luxury Brands in China March 2012

2 | Copyright © 2012 Grail Research, a division of Integreon March 2012

China is the world’s second largest market for luxury goods. While it is attractive due to size and growth, a combination of environmental, economic and cultural factors also make it challenging

Why Brand Tracking Studies are Critical in China

China is not a single homogenous market for luxury and is showing increasing signs of segmentation and differentiation

It has a wide range of consumer segments from aspirational middle class to mature/ sophisticated buyers

Counterfeit goods are widespread and readily available

• Endangering the association of luxury brands with quality

Upward economic mobility and extensive access to luxury products are driving the creation of a new set of luxury customers

Increasing exposure to luxury through travel, the Internet, and prior experience has led to rapidly changing attitudes and perceptions of luxury brands

Size and Segments

Rapid Changes

Counterfeiting

China Factors

Identify the right consumer segment

Recognize the differences and identify underlying commonalities – geographic and cultural trends in variation

Strong need for localization – brands need to reach out to consumers through relevant local messages/media while maintaining their global image

Quick response time and ability to react appropriately to changes in consumer perceptions and needs

Maintain exclusivity/brand uniqueness/desired image with limited control on the external environment

Brand Dilution

Challenges Faced by Luxury Brands

Luxury brands need to keep a

close watch on the pulse of

customers’ perceptions and

brand health

Brand Monitor® can help brands succeed in China

How to position offerings and cater to different segments?

3 | Copyright © 2012 Grail Research, a division of Integreon March 2012

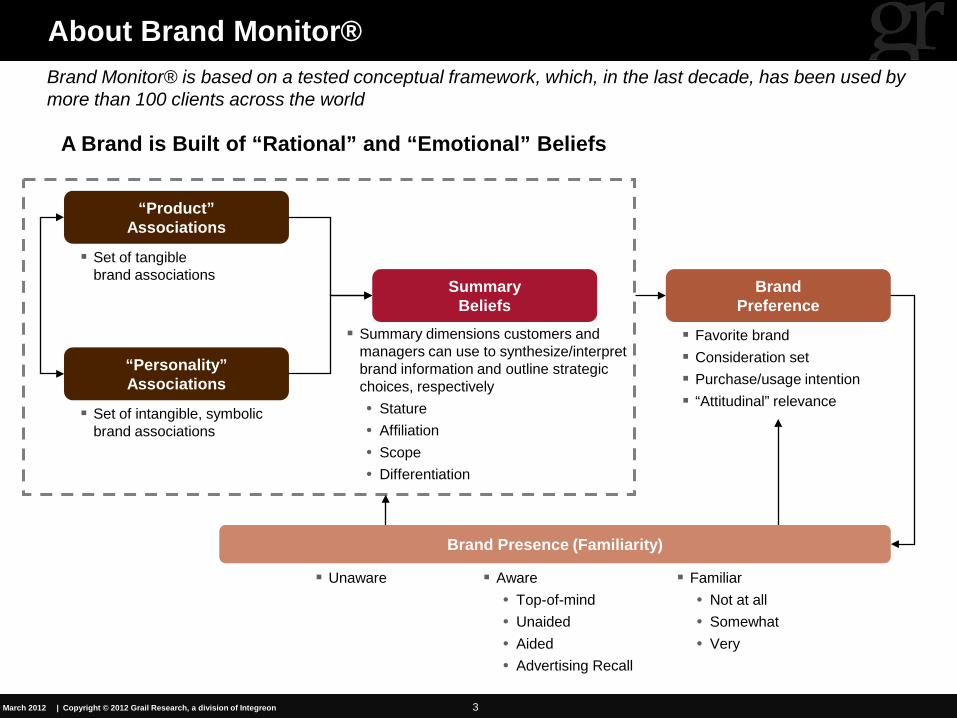

Unaware Aware • Top-of-mind • Unaided • Aided • Advertising Recall

Familiar • Not at all • Somewhat • Very

“Product” Associations

“Personality” Associations

Summary Beliefs

Set of tangible brand associations

Set of intangible, symbolic brand associations

Summary dimensions customers and managers can use to synthesize/interpret brand information and outline strategic choices, respectively • Stature • Affiliation • Scope • Differentiation

Brand Preference

Favorite brand Consideration set Purchase/usage intention “Attitudinal” relevance

Brand Presence (Familiarity)

A Brand is Built of “Rational” and “Emotional” Beliefs

About Brand Monitor® Brand Monitor® is based on a tested conceptual framework, which, in the last decade, has been used by more than 100 clients across the world

4 | Copyright © 2012 Grail Research, a division of Integreon March 2012

2012 Luxury Consumers Survey in China

Surveyed ~260 Chinese consumers about a variety of topics – from their motivation behind purchasing luxury goods to their perceptions of key luxury brands in China

Respondents were spread across 4 cities in China (Beijing, Shanghai, Chengdu, and Dalian), and were above the age of 18 years

Of the respondents, 15% were18-25 years old, 34% 26-35 years, 36% 36-45 years, and 15% 46 years and above

All respondents had shopped for a luxury brand at least once in the last 6 months and had spent more than CNY 5,000 (~$800) in the same period

As part of our brand tracker, we surveyed luxury customers in 4 cities across China to understand the current situation and consumer perception of a selected number of luxury (apparel and accessories) brands

5 | Copyright © 2012 Grail Research, a division of Integreon March 2012

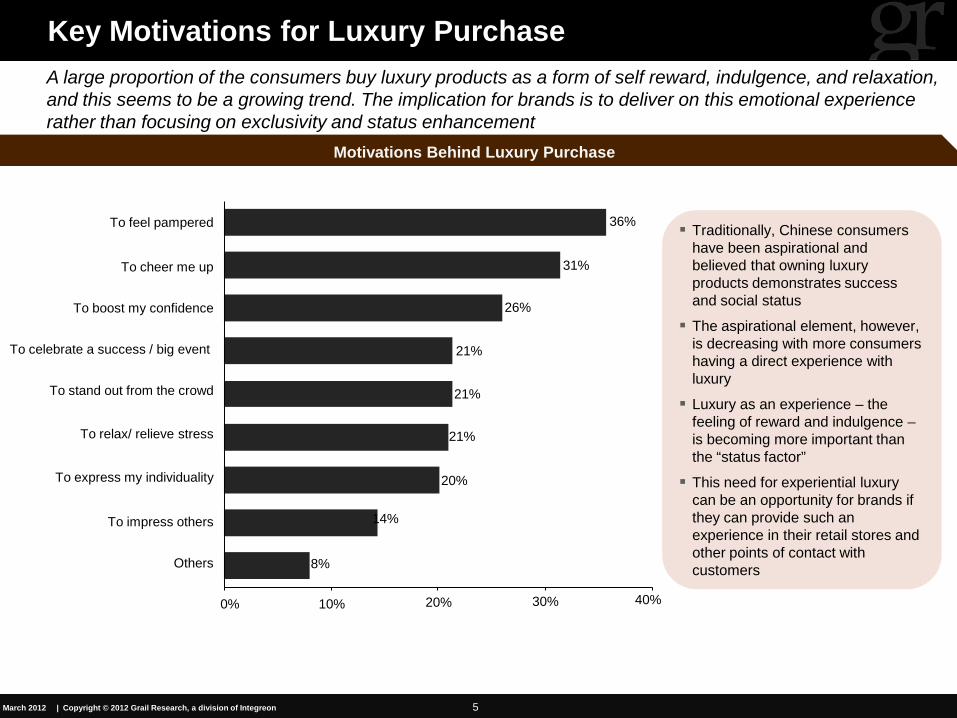

Traditionally, Chinese consumers have been aspirational and believed that owning luxury products demonstrates success and social status

The aspirational element, however, is decreasing with more consumers having a direct experience with luxury

Luxury as an experience – the feeling of reward and indulgence – is becoming more important than the “status factor”

This need for experiential luxury can be an opportunity for brands if they can provide such an experience in their retail stores and other points of contact with customers

Key Motivations for Luxury Purchase

40% 30% 20% 10% 0%

Others 8%

To impress others 14%

To express my individuality 20%

To relax/ relieve stress 21%

To stand out from the crowd 21%

To celebrate a success / big event 21%

To boost my confidence 26%

To cheer me up

To feel pampered

31%

Motivations Behind Luxury Purchase

36%

A large proportion of the consumers buy luxury products as a form of self reward, indulgence, and relaxation, and this seems to be a growing trend. The implication for brands is to deliver on this emotional experience rather than focusing on exclusivity and status enhancement

6 | Copyright © 2012 Grail Research, a division of Integreon March 2012

Brand Performance/Product Associations (1/2) The changing desires of consumers is also reflected in their stated expectations of tangible attributes of a brand. Quality (comfort, fit, well-made) wins over other factors tested, such as exclusivity, uniqueness, and recognition from others

Chinese consumers are increasingly exposed to luxury goods through the Internet, international travel, and prior luxury purchase experience. As a result, they have become more discerning in their taste

Function over form: They choose brands to experience quality and comfort as demonstrated by their choice of brand performance attributes

Though affordability was mentioned as important (to varying degrees) by the majority of consumers, only a small percentage rated this as the most important factor. Given that those of the emerging upper middle class are also luxury consumers, affordability will continue to play a part in their brand purchase choice

The reputation of the brand continues to be an important criteria

Brands can focus on promoting their heritage and track record of craftsmanship to capitalize on these trends

Desirability of Performance Attributes

6.1

Comfortable

More affordable

Fits well

5.9

5.8

5.9

5.7

5.7

6.1

5.9

Well-made

Timeless

Stylish design

Suitable for work

Expensive materials

Brand not widely known

Exclusive

Current / en vogue

Unique

6.2

Discreet

Recognizable Brand

5.4

5.4

5.4

5.4

5.3

4.8

High-quality reputation

4.5 5.0 5.5 6.0 6.5

7 | Copyright © 2012 Grail Research, a division of Integreon March 2012

Performance Attributes Perception Map

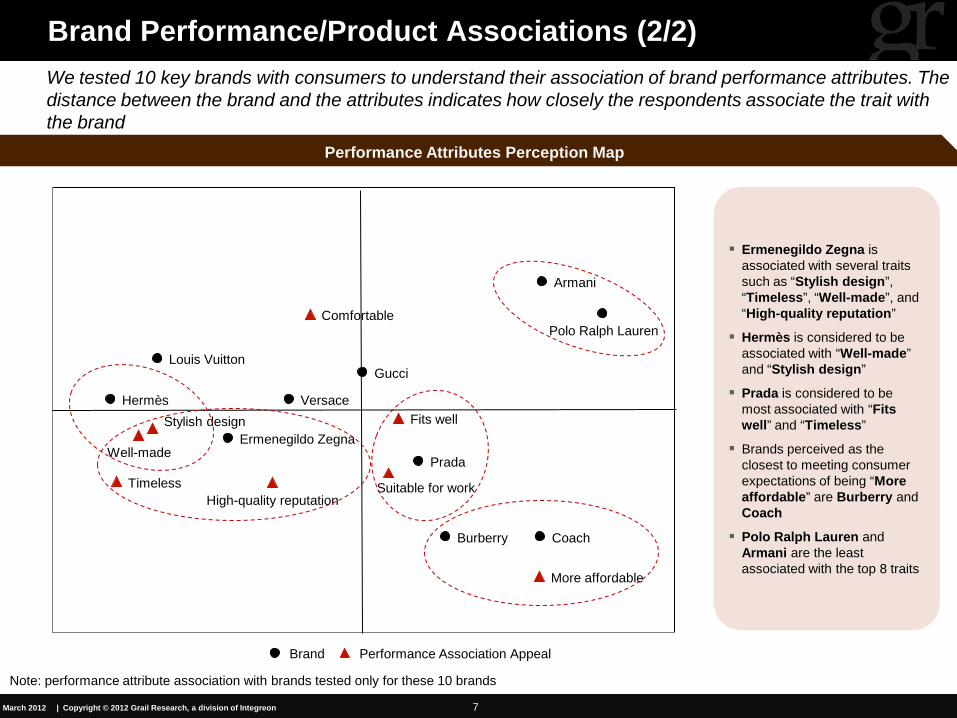

Brand Performance/Product Associations (2/2) We tested 10 key brands with consumers to understand their association of brand performance attributes. The distance between the brand and the attributes indicates how closely the respondents associate the trait with the brand

Ermenegildo Zegna is associated with several traits such as “Stylish design”, “Timeless”, “Well-made”, and “High-quality reputation”

Hermès is considered to be associated with “Well-made” and “Stylish design”

Prada is considered to be most associated with “Fits well” and “Timeless”

Brands perceived as the closest to meeting consumer expectations of being “More affordable” are Burberry and Coach

Polo Ralph Lauren and Armani are the least associated with the top 8 traits

Note: performance attribute association with brands tested only for these 10 brands

High-quality reputation

Fits well

Well-made

Stylish design

Timeless

Comfortable

Suitable for work

More affordable

Versace Hermès

Prada

Polo Ralph Lauren

Louis Vuitton Gucci

Ermenegildo Zegna

Coach Burberry

Armani

Performance Association Appeal Brand

8 | Copyright © 2012 Grail Research, a division of Integreon March 2012

Brand Personality Associations (1/2)

6.1

5.1

Sexy Elegant / Chic

Fashionable

Reliable Relaxed

4.2 3.7

5.7

5.1

4.5

5.1

5.5

5.7

5.5

5.7

5.6

5.9 5.7

5.3 5.2 5.1

Practical / Sensible Glamorous

Celebrity Association Modern

Hedonistic / Opulent Sophisticated Western Style Cutting-edge

Feminine Traditional

Minimalist / Simple Demure / Understated

Young / Playful Masculine

Bold / Loud Irreverent

4.9 4.9 4.9

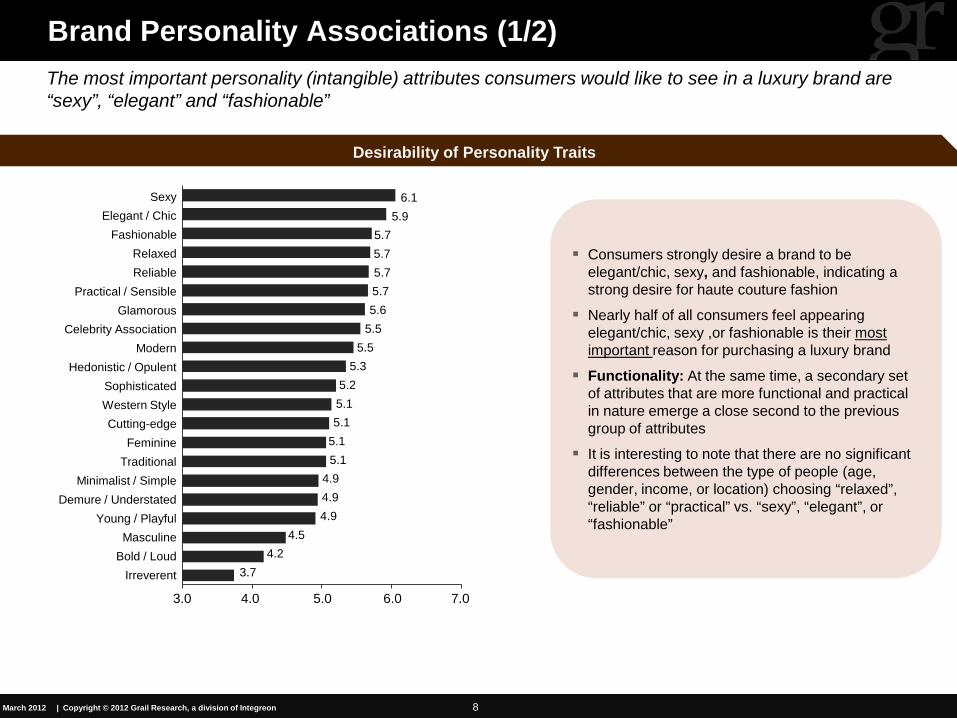

The most important personality (intangible) attributes consumers would like to see in a luxury brand are “sexy”, “elegant” and “fashionable”

3.0 4.0 5.0 6.0 7.0

Desirability of Personality Traits

Consumers strongly desire a brand to be elegant/chic, sexy, and fashionable, indicating a strong desire for haute couture fashion

Nearly half of all consumers feel appearing elegant/chic, sexy ,or fashionable is their most important reason for purchasing a luxury brand

Functionality: At the same time, a secondary set of attributes that are more functional and practical in nature emerge a close second to the previous group of attributes

It is interesting to note that there are no significant differences between the type of people (age, gender, income, or location) choosing “relaxed”, “reliable” or “practical” vs. “sexy”, “elegant”, or “fashionable”

9 | Copyright © 2012 Grail Research, a division of Integreon March 2012

Performance Attributes Perception Map

Brand Personality/Product Associations (2/2)

Note: Personality attribute association with brands tested only for these 10 brands

Celebrity Association

Reliable

Glamorous

Relaxed

Practical / sensible

Elegant / chic

Fashionable

Sexy Versace

Hermès

Prada Polo Ralph Lauren

Louis Vuitton Gucci

Ermenegildo Zegna

Coach

Burberry

Armani

Personality Association Appeal Brand

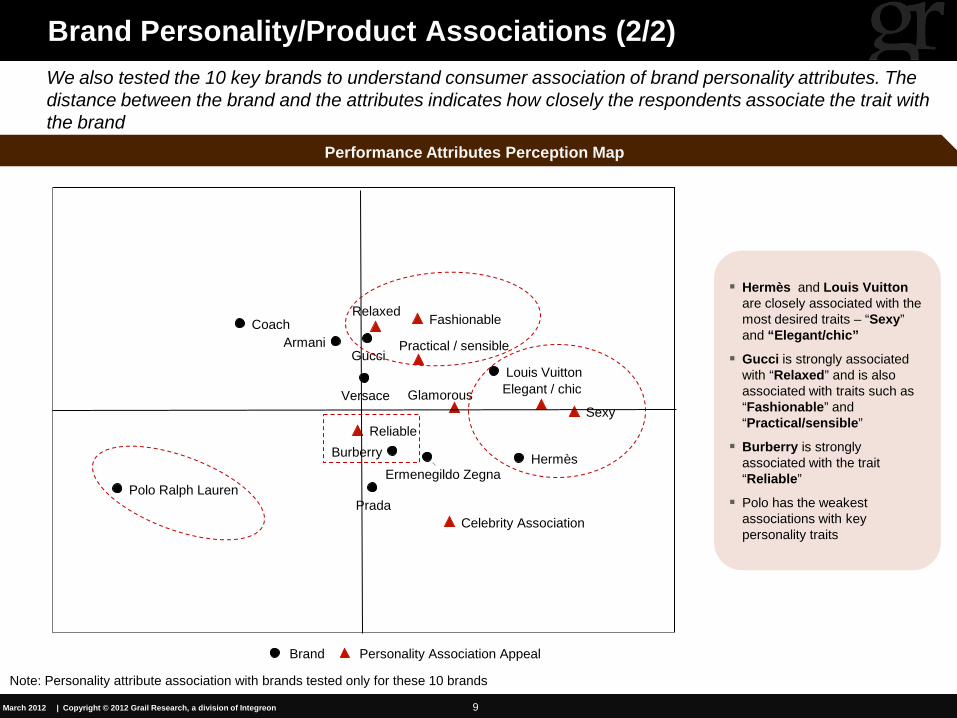

Hermès and Louis Vuitton are closely associated with the most desired traits – “Sexy” and “Elegant/chic”

Gucci is strongly associated with “Relaxed” and is also associated with traits such as “Fashionable” and “Practical/sensible”

Burberry is strongly associated with the trait “Reliable”

Polo has the weakest associations with key personality traits

We also tested the 10 key brands to understand consumer association of brand personality attributes. The distance between the brand and the attributes indicates how closely the respondents associate the trait with the brand

10 | Copyright © 2012 Grail Research, a division of Integreon March 2012

Stature and Trajectory

Meta Perceptions – Stature and Trajectory

5.97

Hermès

5.86

6.10

5.48

Ermenegildo Zegna

5.33

5.54

Burberry Versace

5.58

5.78

Armani

5.64

5.31

5.60

Gucci

5.50

5.65 5.82

Prada

5.54

5.86

Louis Vuitton

5.67

Polo Ralph Lauren

5.23

5.41

Coach

5.37

Stature

Mor

e R

eput

able

/Pos

itive

Cha

nge

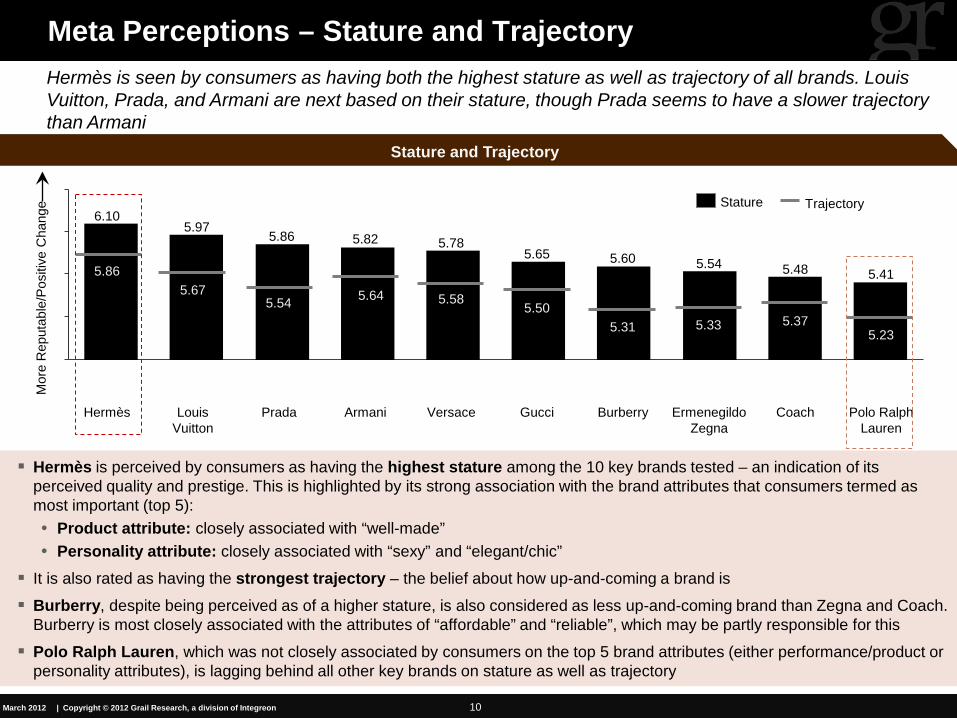

Hermès is perceived by consumers as having the highest stature among the 10 key brands tested – an indication of its perceived quality and prestige. This is highlighted by its strong association with the brand attributes that consumers termed as most important (top 5): • Product attribute: closely associated with “well-made” • Personality attribute: closely associated with “sexy” and “elegant/chic”

It is also rated as having the strongest trajectory – the belief about how up-and-coming a brand is

Burberry, despite being perceived as of a higher stature, is also considered as less up-and-coming brand than Zegna and Coach. Burberry is most closely associated with the attributes of “affordable” and “reliable”, which may be partly responsible for this

Polo Ralph Lauren, which was not closely associated by consumers on the top 5 brand attributes (either performance/product or personality attributes), is lagging behind all other key brands on stature as well as trajectory

Trajectory

Hermès is seen by consumers as having both the highest stature as well as trajectory of all brands. Louis Vuitton, Prada, and Armani are next based on their stature, though Prada seems to have a slower trajectory than Armani

11 | Copyright © 2012 Grail Research, a division of Integreon March 2012

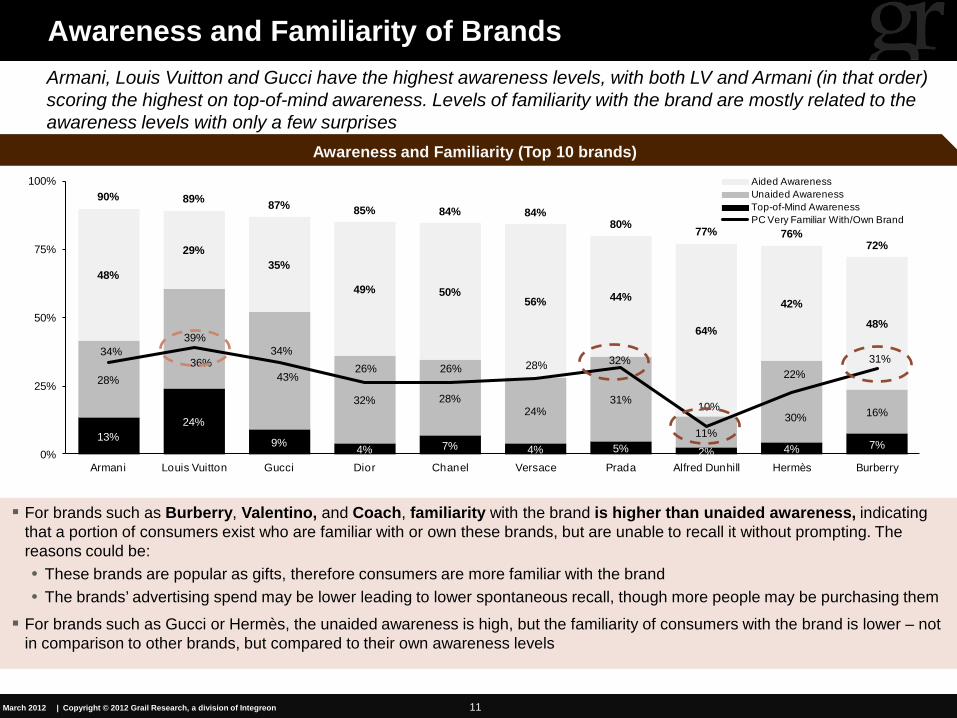

Awareness and Familiarity (Top 10 brands)

Awareness and Familiarity of Brands

For brands such as Burberry, Valentino, and Coach, familiarity with the brand is higher than unaided awareness, indicating that a portion of consumers exist who are familiar with or own these brands, but are unable to recall it without prompting. The reasons could be: • These brands are popular as gifts, therefore consumers are more familiar with the brand • The brands’ advertising spend may be lower leading to lower spontaneous recall, though more people may be purchasing them

For brands such as Gucci or Hermès, the unaided awareness is high, but the familiarity of consumers with the brand is lower – not in comparison to other brands, but compared to their own awareness levels

13%24%

9% 4% 7% 4% 5% 2% 4% 7%

28%36%

43%

32% 28%24%

31%

11%30% 16%

48%

29%35%

49% 50%56% 44%

64%

42%

48%

90% 89% 87% 85% 84% 84%80% 77% 76%

72%

34%39%

34%26% 26% 28% 32%

10%

22%31%

0%

25%

50%

75%

100%

Armani Louis Vuitton Gucci Dior Chanel Versace Prada Alfred Dunhill Hermès Burberry

Aided AwarenessUnaided AwarenessTop-of-Mind AwarenessPC Very Familiar With/Own Brand

Armani, Louis Vuitton and Gucci have the highest awareness levels, with both LV and Armani (in that order) scoring the highest on top-of-mind awareness. Levels of familiarity with the brand are mostly related to the awareness levels with only a few surprises

12 | Copyright © 2012 Grail Research, a division of Integreon March 2012

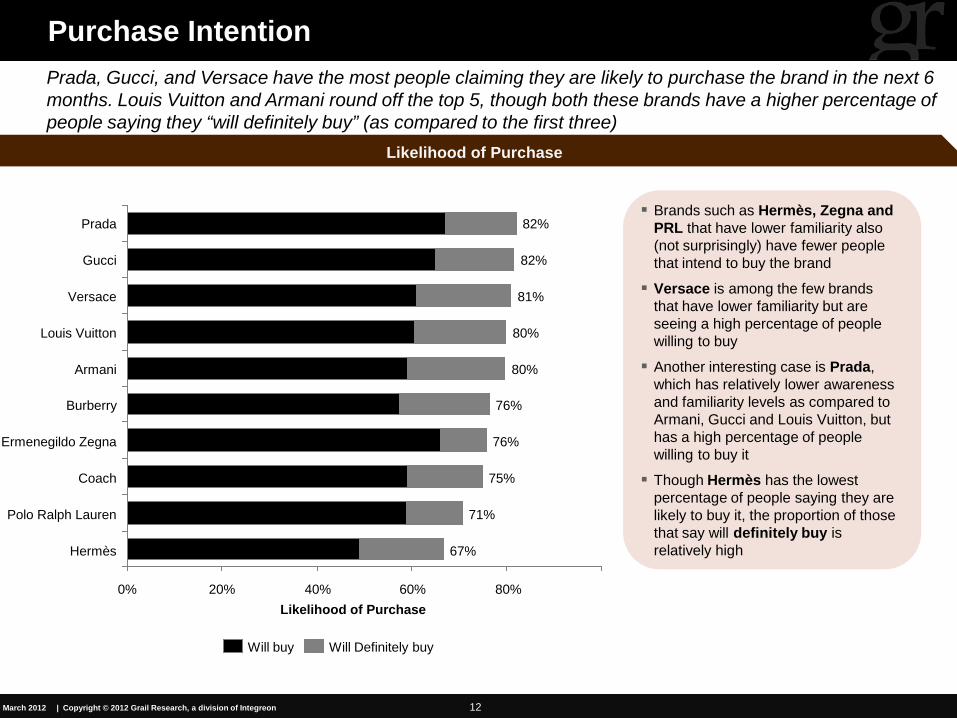

Purchase Intention

Coach

Polo Ralph Lauren

75%

71%

80% 60%

76% Ermenegildo Zegna

Burberry 76%

40% 20% 0%

67% Hermès

Armani 80%

Louis Vuitton 80%

Versace 81%

Gucci 82%

Prada 82%

Will buy Will Definitely buy

Likelihood of Purchase

Brands such as Hermès, Zegna and PRL that have lower familiarity also (not surprisingly) have fewer people that intend to buy the brand

Versace is among the few brands that have lower familiarity but are seeing a high percentage of people willing to buy

Another interesting case is Prada, which has relatively lower awareness and familiarity levels as compared to Armani, Gucci and Louis Vuitton, but has a high percentage of people willing to buy it

Though Hermès has the lowest percentage of people saying they are likely to buy it, the proportion of those that say will definitely buy is relatively high

Prada, Gucci, and Versace have the most people claiming they are likely to purchase the brand in the next 6 months. Louis Vuitton and Armani round off the top 5, though both these brands have a higher percentage of people saying they “will definitely buy” (as compared to the first three)

Likelihood of Purchase

13 | Copyright © 2012 Grail Research, a division of Integreon March 2012

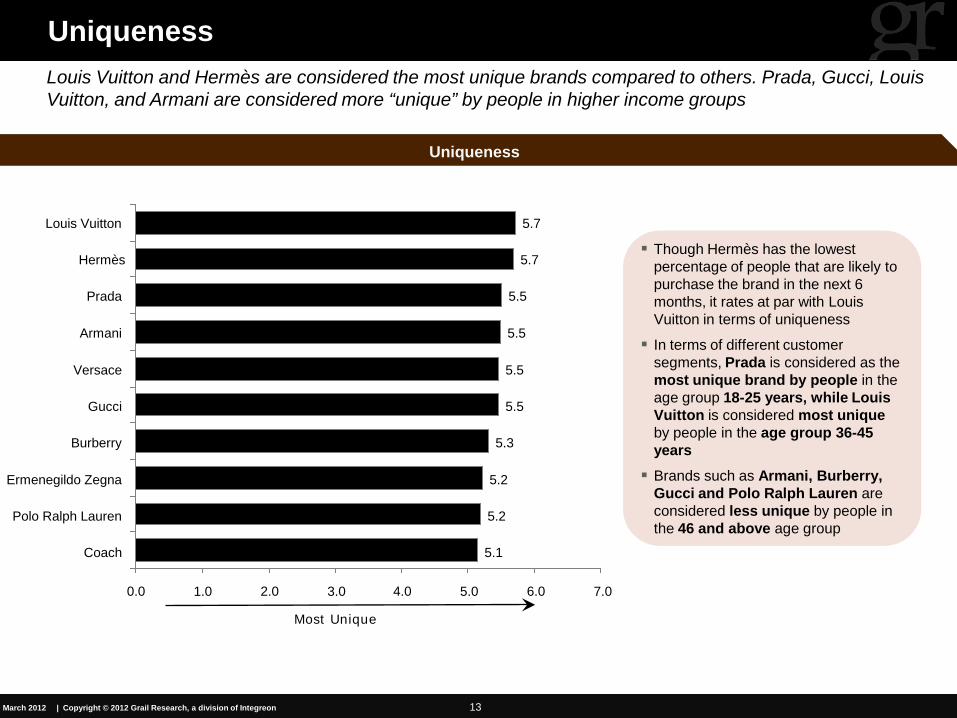

Uniqueness

6.0 4.0 2.0 0.0

Coach 5.1

Polo Ralph Lauren 5.2

Ermenegildo Zegna 5.2

Burberry 5.3

Gucci 5.5

Versace 5.5

Armani 5.5

Prada 5.5

Hermès 5.7

Louis Vuitton 5.7

1.0 3.0 5.0 7.0

Uniqueness

Though Hermès has the lowest percentage of people that are likely to purchase the brand in the next 6 months, it rates at par with Louis Vuitton in terms of uniqueness

In terms of different customer segments, Prada is considered as the most unique brand by people in the age group 18-25 years, while Louis Vuitton is considered most unique by people in the age group 36-45 years Brands such as Armani, Burberry,

Gucci and Polo Ralph Lauren are considered less unique by people in the 46 and above age group

Louis Vuitton and Hermès are considered the most unique brands compared to others. Prada, Gucci, Louis Vuitton, and Armani are considered more “unique” by people in higher income groups

Most Unique

14 | Copyright © 2012 Grail Research, a division of Integreon March 2012

Favorite & Brand for Me

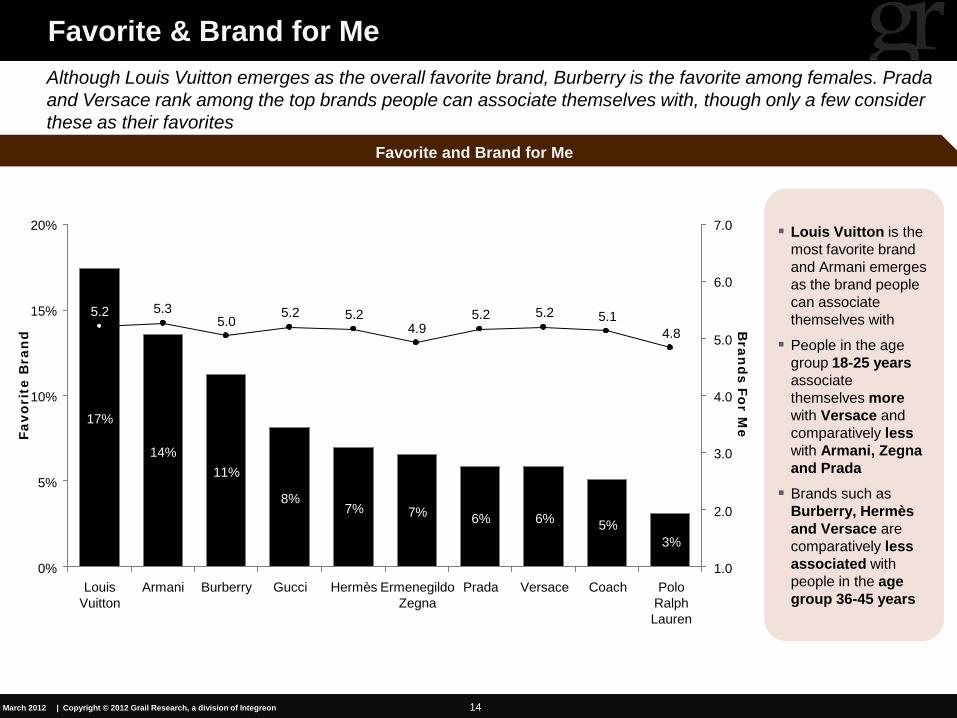

Favorite and Brand for Me

Louis Vuitton is the most favorite brand and Armani emerges as the brand people can associate themselves with

People in the age group 18-25 years associate themselves more with Versace and comparatively less with Armani, Zegna and Prada Brands such as

Burberry, Hermès and Versace are comparatively less associated with people in the age group 36-45 years

Although Louis Vuitton emerges as the overall favorite brand, Burberry is the favorite among females. Prada and Versace rank among the top brands people can associate themselves with, though only a few consider these as their favorites

6.0

5.0

4.0

3.0

2.0

1.0

7.0 20%

15%

10%

5%

0% Polo

Ralph Lauren

3%

4.8

Coach

5%

5.2

Gucci

8%

5.2

Burberry

11%

5.0

Armani

14%

5.3

Louis Vuitton

17%

5.1

Versace

6%

5.2

Prada

6%

5.2

Ermenegildo Zegna

7%

4.9

Hermès

7%

5.2

Bran

ds For M

e Favo

rite

Bra

nd

15 | Copyright © 2012 Grail Research, a division of Integreon March 2012

Recommendation

Recommendation

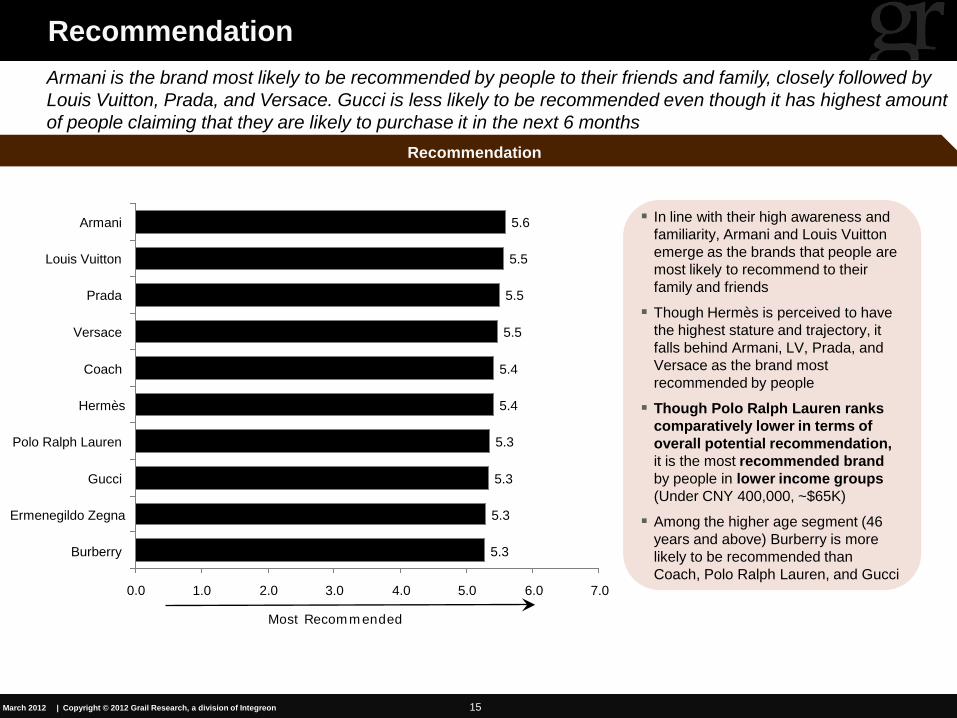

Armani is the brand most likely to be recommended by people to their friends and family, closely followed by Louis Vuitton, Prada, and Versace. Gucci is less likely to be recommended even though it has highest amount of people claiming that they are likely to purchase it in the next 6 months

6.0 4.0 2.0 0.0

Burberry 5.3

Ermenegildo Zegna 5.3

Gucci 5.3

Polo Ralph Lauren 5.3

Hermès 5.4

Coach 5.4

Versace 5.5

Prada 5.5

Louis Vuitton 5.5

Armani 5.6

1.0 3.0 5.0 7.0

In line with their high awareness and familiarity, Armani and Louis Vuitton emerge as the brands that people are most likely to recommend to their family and friends

Though Hermès is perceived to have the highest stature and trajectory, it falls behind Armani, LV, Prada, and Versace as the brand most recommended by people

Though Polo Ralph Lauren ranks comparatively lower in terms of overall potential recommendation, it is the most recommended brand by people in lower income groups (Under CNY 400,000, ~$65K)

Among the higher age segment (46 years and above) Burberry is more likely to be recommended than Coach, Polo Ralph Lauren, and Gucci

Most Recommended

16 | Copyright © 2012 Grail Research, a division of Integreon March 2012

Source of Information & Purchase Behavior

Most Recent Purchase and Source of Information

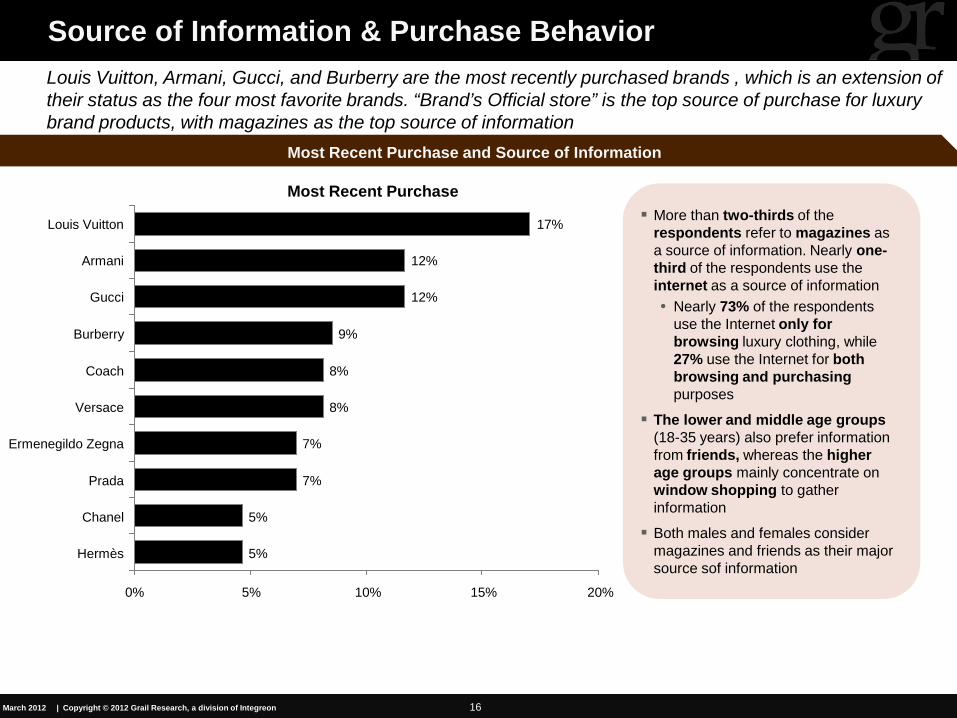

Louis Vuitton, Armani, Gucci, and Burberry are the most recently purchased brands , which is an extension of their status as the four most favorite brands. “Brand’s Official store” is the top source of purchase for luxury brand products, with magazines as the top source of information

7%

0% 15% 5%

7%

9%

12%

17%

5%

12%

5%

8%

8%

Coach

Burberry

Versace

Ermenegildo Zegna

Gucci

Armani

Louis Vuitton

20% 10%

Prada

Chanel

Hermès

More than two-thirds of the respondents refer to magazines as a source of information. Nearly one-third of the respondents use the internet as a source of information • Nearly 73% of the respondents

use the Internet only for browsing luxury clothing, while 27% use the Internet for both browsing and purchasing purposes

The lower and middle age groups (18-35 years) also prefer information from friends, whereas the higher age groups mainly concentrate on window shopping to gather information

Both males and females consider magazines and friends as their major source sof information

Most Recent Purchase

17 | Copyright © 2012 Grail Research, a division of Integreon March 2012

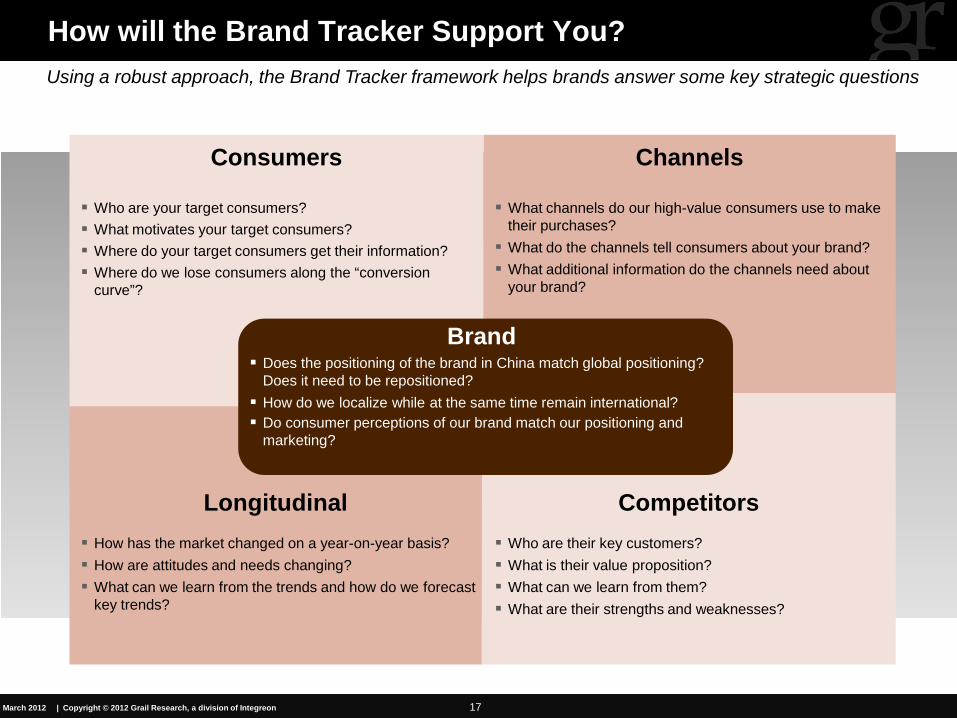

How will the Brand Tracker Support You?

What channels do our high-value consumers use to make their purchases? What do the channels tell consumers about your brand? What additional information do the channels need about

your brand?

Who are your target consumers? What motivates your target consumers? Where do your target consumers get their information? Where do we lose consumers along the “conversion

curve”?

Longitudinal

Consumers Channels

Competitors How has the market changed on a year-on-year basis? How are attitudes and needs changing? What can we learn from the trends and how do we forecast

key trends?

Who are their key customers? What is their value proposition? What can we learn from them? What are their strengths and weaknesses?

Brand Does the positioning of the brand in China match global positioning?

Does it need to be repositioned? How do we localize while at the same time remain international? Do consumer perceptions of our brand match our positioning and

marketing?

Using a robust approach, the Brand Tracker framework helps brands answer some key strategic questions

18 | Copyright © 2012 Grail Research, a division of Integreon March 2012

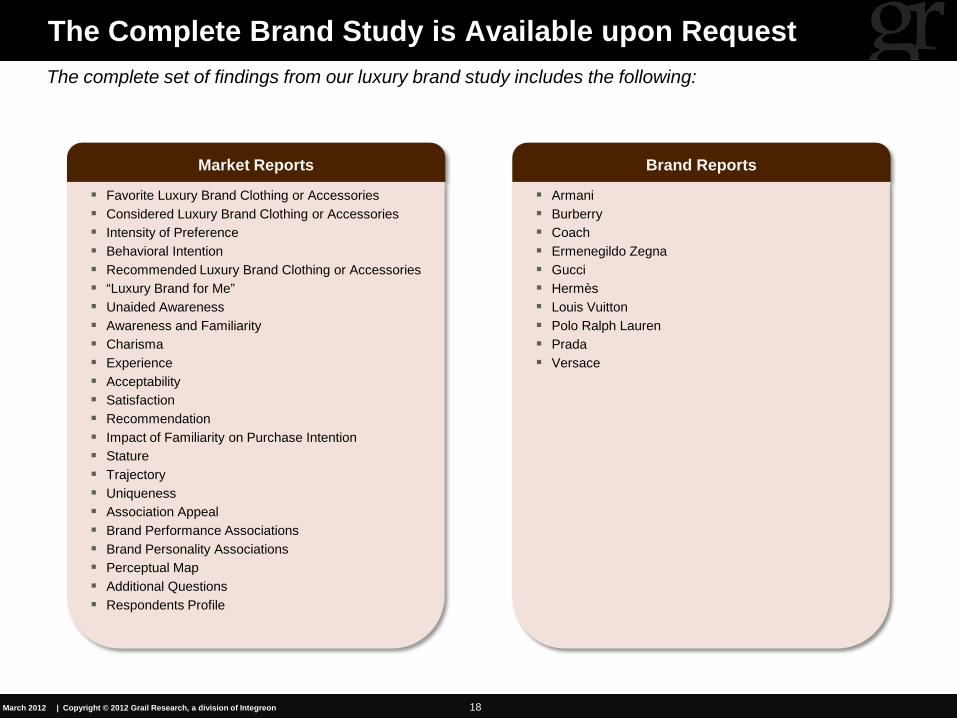

The Complete Brand Study is Available upon Request

Market Reports

Favorite Luxury Brand Clothing or Accessories Considered Luxury Brand Clothing or Accessories Intensity of Preference Behavioral Intention Recommended Luxury Brand Clothing or Accessories “Luxury Brand for Me” Unaided Awareness Awareness and Familiarity Charisma Experience Acceptability Satisfaction Recommendation Impact of Familiarity on Purchase Intention Stature Trajectory Uniqueness Association Appeal Brand Performance Associations Brand Personality Associations Perceptual Map Additional Questions Respondents Profile

Brand Reports

Armani Burberry Coach Ermenegildo Zegna Gucci Hermès Louis Vuitton Polo Ralph Lauren Prada Versace

The complete set of findings from our luxury brand study includes the following:

19 | Copyright © 2012 Grail Research, a division of Integreon March 2012

Illustrative Brand Report

20 | Copyright © 2012 Grail Research, a division of Integreon March 2012

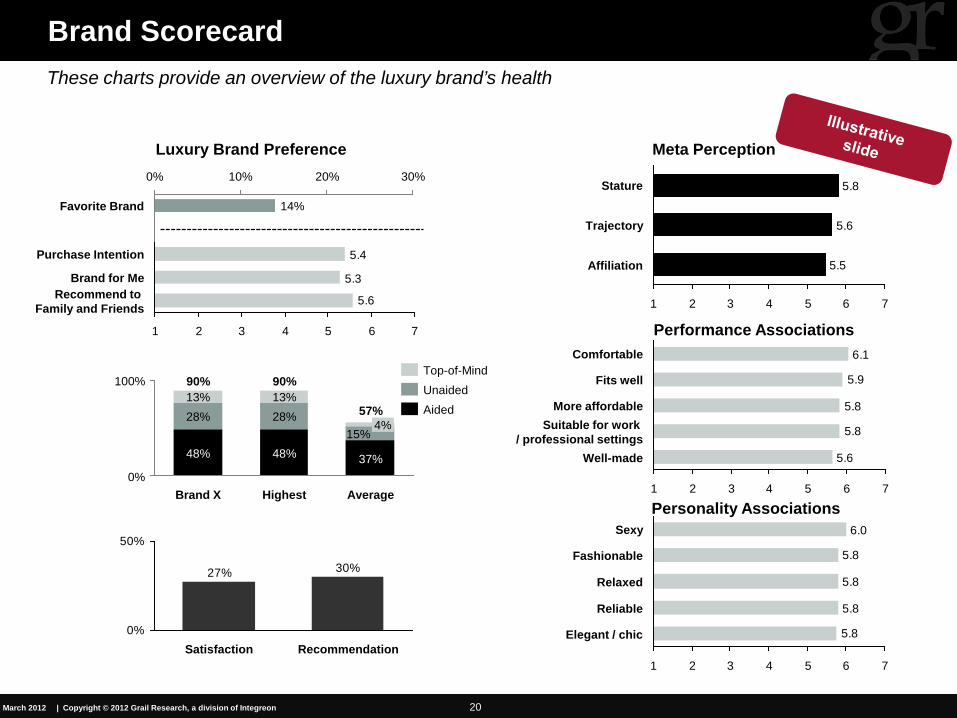

Brand Scorecard These charts provide an overview of the luxury brand’s health

30% 20% 10% 0%

Favorite Brand 14%

5.6

5.3

5.4

1 2 3 4 5 6 7

Recommend to Family and Friends

Brand for Me

Purchase Intention

100%

0% Average

57%

37%

15% 4%

Highest

90%

48%

28% 13%

Brand X

90%

48%

28% 13%

30%27%

0%

50%

Recommendation Satisfaction

5.5

5.6

5.8

7 6 5 4 3 2 1

Affiliation

Trajectory

Stature

5.8

5.8

5.8

5.8

6.0

7 6 5 4 3 2 1

Elegant / chic

Reliable

Relaxed

Fashionable

Sexy

5.6

5.8

5.8

5.9

6.1

1 2 3 4 5 6 7

Well-made

Suitable for work / professional settings

More affordable

Fits well

Comfortable

Aided Unaided Top-of-Mind

Luxury Brand Preference Meta Perception

Performance Associations

Personality Associations

21 | Copyright © 2012 Grail Research, a division of Integreon March 2012

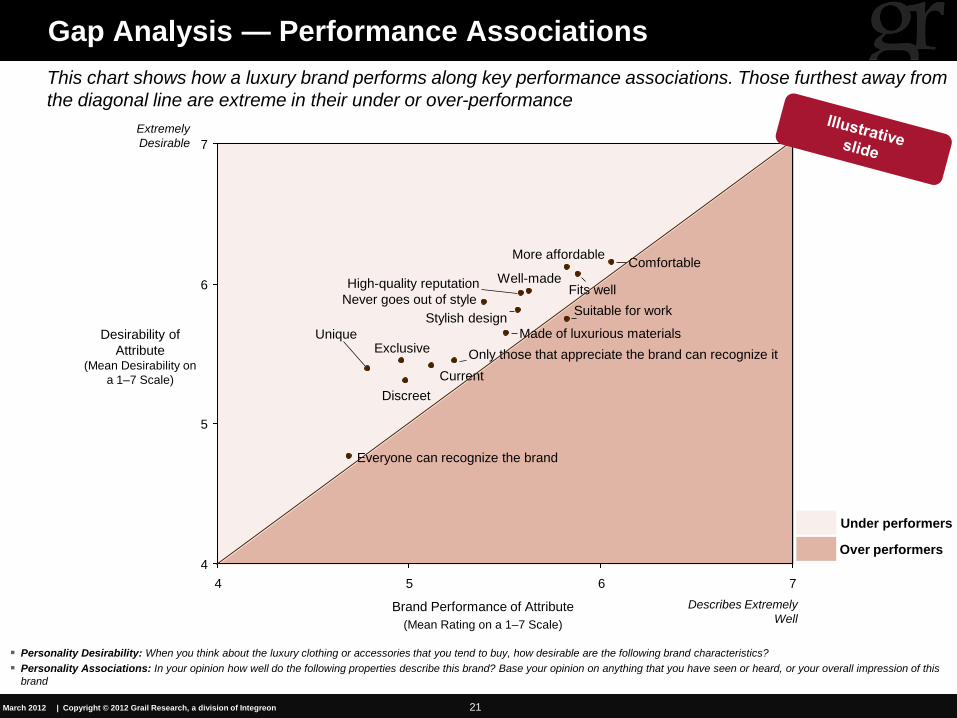

Under performers

Over performers

Desirability of Attribute

(Mean Desirability on a 1–7 Scale)

Personality Desirability: When you think about the luxury clothing or accessories that you tend to buy, how desirable are the following brand characteristics? Personality Associations: In your opinion how well do the following properties describe this brand? Base your opinion on anything that you have seen or heard, or your overall impression of this

brand

Describes Extremely Well

Extremely Desirable

Gap Analysis — Performance Associations This chart shows how a luxury brand performs along key performance associations. Those furthest away from the diagonal line are extreme in their under or over-performance

Brand Performance of Attribute (Mean Rating on a 1–7 Scale)

4

5

6

7

4 5 6 7

High-quality reputation

Unique

Discreet

Only those that appreciate the brand can recognize it

Everyone can recognize the brand

Current

Exclusive

Fits well

Made of luxurious materials

Well-made

Stylish design Never goes out of style

Comfortable

Suitable for work

More affordable

22 | Copyright © 2012 Grail Research, a division of Integreon March 2012

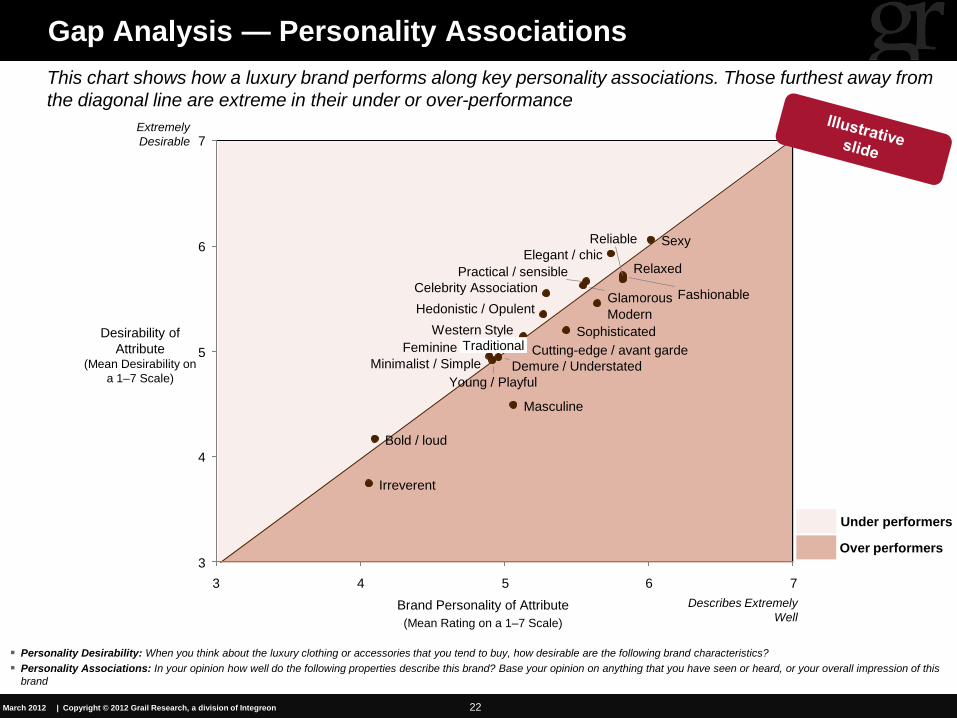

Desirability of Attribute

(Mean Desirability on a 1–7 Scale)

Personality Desirability: When you think about the luxury clothing or accessories that you tend to buy, how desirable are the following brand characteristics? Personality Associations: In your opinion how well do the following properties describe this brand? Base your opinion on anything that you have seen or heard, or your overall impression of this

brand

Describes Extremely Well

Extremely Desirable

Gap Analysis — Personality Associations This chart shows how a luxury brand performs along key personality associations. Those furthest away from the diagonal line are extreme in their under or over-performance

Brand Personality of Attribute (Mean Rating on a 1–7 Scale)

7

6

5

4

3 7 6 5 4 3

Western Style

Celebrity Association Hedonistic / Opulent

Reliable

Glamorous

Feminine

Masculine

Irreverent

Traditional

Relaxed Practical / sensible

Cutting-edge / avant garde Demure / Understated

Modern

Bold / loud

Elegant / chic

Sophisticated

Fashionable

Young / Playful

Sexy

Minimalist / Simple

Under performers

Over performers

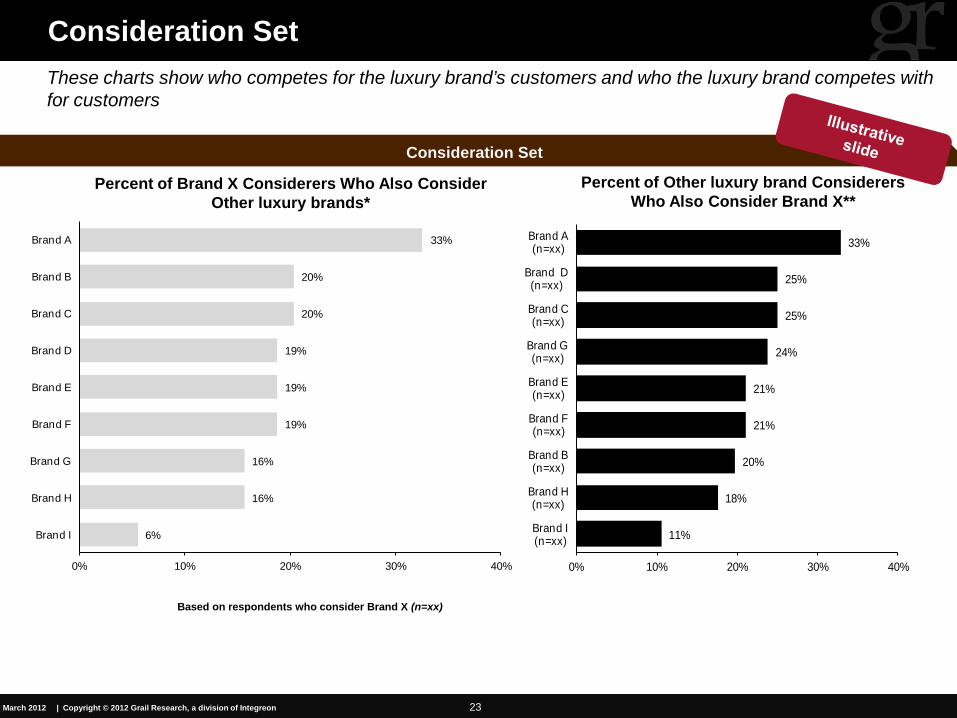

23 | Copyright © 2012 Grail Research, a division of Integreon March 2012

Based on respondents who consider Brand X (n=xx)

Percent of Brand X Considerers Who Also Consider Other luxury brands*

Percent of Other luxury brand Considerers Who Also Consider Brand X**

6%

16%

16%

19%

19%

19%

20%

20%

33%

0% 10% 20% 30% 40%

Brand I

Brand H

Brand G

Brand F

Brand E

Brand D

Brand C

Brand B

Brand A

11%

18%

20%

21%

21%

24%

25%

25%

33%

0% 10% 20% 30% 40%

Brand I(n=xx)

Brand H(n=xx)

Brand B(n=xx)

Brand F(n=xx)

Brand E(n=xx)

Brand G(n=xx)

Brand C(n=xx)

Brand D(n=xx)

Brand A(n=xx)

Consideration Set These charts show who competes for the luxury brand’s customers and who the luxury brand competes with for customers

Consideration Set

For More Information Contact:

Grail Research [email protected]

Copyright © 2012 by Grail Research, a division of Integreon

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means — electronic, mechanical, photocopying, recording, or otherwise — without the permission of Grail Research, a division of Integreon