Download - HBM M&A Survey - Swiss Biotech

February 2020

1

About the HBM Pharma/Biotech M&A Report

The HBM Pharma/Biotech M&A Report covers all completed trade sales of US and European biotechnology and pharma companies with a therapeutic focus (Rx incl. generics as well as OTC). For 2015-2019, additional data for asset deals and transactions outside of the US and Europe is provided. Where mentioned, M&A data for 2019 may also include announced transactions.

The report does not cover nutritional supplements, diagnostics, medical technology, digital health, life sciences tools, CROs, pharma manufacturing and services. Reverse mergers or minority investments are not included. Acquisitions that were structured as mergers for tax or other reasons are included.

Upfront transaction value is defined in this report as the upfront consideration in cash and/or shares. By contrast, the total transaction value also includes contingent (“biodollar”) payments linked to reaching certain milestones.

Additional data such as invested capital, exit multiples, stage of lead product etc. were collected from various sources. Please note that such data may be based on estimates and may not have been available for all transactions.

Further information about the HBM Pharma/Biotech M&A Report including a list of all transactions can be found under http://www.hbmpartners.com/reports. The use of data and charts is permitted with reference to “HBM Partners Pharma/Biotech M&A Report”.

The authors of the report welcome any feedback or corrections:

Dr Ulrich Geilinger, [email protected] , Dr Chandra Leo, [email protected] and Dr Emil Bujak, [email protected]

HBM Pharma/Biotech M&A Report 2020 Analysis of Biopharma M&A in 2019 (and previous years)

Key Findings

◼ Worldwide biopharma M&A volume of completed and announced deals (including

contingent payments and asset deals) reached a record of $254 billion in 2019 (as compared

to $155 billion in 2018 and $76 billion in 2017).

◼ The two mega-deals, BMS/Celgene ($74 billion) and Abbvie/Allergan ($63 billion) got most

headlines in 2019 with the acquisition of Celgene by BMS being the third largest pharma

acquisition in history.

◼ US biopharma deal activity was very strong with 12 $1-billion-plus deals closed in 2019 and

another 5 such deals announced. European deal volume (outside of the $63 billion

Abbvie/Allergan transaction) was only around $10 billion.

◼ As in previous years, M&A transaction volume outside of the US and Europe in 2019 was

modest with a transaction volume of only $5.4 billion.

◼ Premiums paid in 2019 for public companies reached an average of almost 100%,

demonstrating the continued appetite for companies with new products in development or

on the market.

◼ Return multiples to VC investors from M&A stayed at high levels in 2019 but did not reach

the values of previous years.

◼ VC-backed company trade sales in oncology dropped in number and deal volume, whereas

non-oncology orphan companies generated one third of transaction volume.

HBM Pharma/Biotech M&A Report 2020

2

Record Worldwide Biopharma M&A Transaction Volume in 2019

Worldwide Biopharma M&A Transaction Volume 2015 -2019

Completed transactions and in 2019 announced transactions, including asset deals, sale of subsidiaries and divisions.

Transaction volume including contingent payments. Europe includes Israel.

◼ Worldwide biopharma M&A volume of completed and announced deals (including contingent

payments and asset deals) in 2019 jumped to a record high of $254 billion. This number was driven of

course by the two mega-deals BMS/Celgene ($74 billion) and Abbvie/Allergan1 ($63 billion). M&A

transaction volume outside of these two mega-mergers reached $117 billion, also a historically high

number. Please note that we put the $59 billion Takeda/Shire deal into 2018 even though the

transaction was legally closed only in early 2019 (but was approved by shareholders in late 2018).

◼ The majority of larger M&A deals (above $1 billion transaction volume) were in oncology or in the

orphan/genetic disease areas.

◼ US biopharma M&A activity in 2019 was very strong with 18 private and 16 public companies sold at

$100 million or more. In Europe, only 9 company trade sales reached that level and transaction volume

(excluding the Abbvie/Allergan deal) was only around $10 billion.

◼ As in previous years, biopharma M&A transaction volume outside of the US and Europe remained

relatively low ($5.4 billion) with only a handful of significant transactions reported. It should be noted,

however, that it is difficult to get reliable M&A data from China.

While the mega-mergers attracted the most headlines in 2019, there were a high number of other

significant transactions mainly in the US (see next page), both in the first and second half of the year. Our

prediction that the second half of 2019 could see a slow-down (due to the six companies involved in

recent mega-mergers being absent in the M&A market) turned out to be too pessimistic.

1 The transaction will close only in 2020. Allergan has been classified as a European company, even though main operations

are in the US.

195.6

77.6

28.047.5

148.7

7.6

3.6

3.1

1.9

26.0

17.9

14.4

40.0

78.3

68.03.1

49.8

1.0

23.8

5.7

5.8

3.6

3.8

3.3

5.4230.0

149.0

75.9

154.9

253.9

0

50

100

150

200

250

2015 2016 2017 2018 2019

Up

fro

nt T

ran

sact

ion

Vo

lum

e ($

bill

ion

)

ROW M&A transactions

European divitions/assets sold

European companies sold

US divisions/assets sold

US companies sold

Teva/Allerga Generics

$40.5 billion

J&J/Actelion

$30 billion

Takeda/Shire

$59 billion

BMS/Celgene

$74 billion

Actavis/Allergan

$70.5 billion

Abbvie/Allergan $63 billion

(not completed yet)

HBM Pharma/Biotech M&A Report 2020

3

Table: Largest Completed and Announced Biopharma M&A Transactions in 2019

Notes: Transactions ranked by total transaction value Regions and countries (columns 1 and 3): In case of whole companies sold = location of headquarter; in case of asset/division deals = country of business (if available) NC = Announced transactions, not completed yet at year end 2019 “Asset/Div.” = Sale of assets, divisions and subsidiaries “Market” = Approved or marketed drugs | “NDA” – NDA filed | “1”, “2” and “3” = Phase 1 2 3, stage of lead product

1) Osiris with its regenerative medicine products including skin, bone graft and articular cartilage substitutes was classified as a “biopharma company” even though one could argue that it is more a medtech-like company.

A list of all biopharma US and European M&A transactions since 2005 with disclosed transaction volumes (Excel sheet) can be found here http://www.hbmpartners.com/reports.

Target Company/Business Public/

Private

VC- or PE-

Backed /

Premium

Buyer Upfront

Deal Value

($m)

Total Deal

Value ($m)

Phase/Stage

of Lead

Product

Est. VC

Invest-

ment

($m)

Therapeutic Area(s)

US Celgene / US Public 53% Bristol-Myers Squibb / US 74'000 80'000 Market Oncology, autoimmune diseases

Europe NC Allergan / Ireland Public 45% AbbVie / US 63'000 63'000 Market Medical aesthetics, eye care, CNS

US Otezla (Celgene product) / US Asset/Div. Amgen / US 13'400 13'400 Market Psoriasis, arthritis

US Pfizer Upjohn / US Merger Mylan (new Viatris) / Netherlands 12'000 12'000 Market Various generics

US Array BioPharma / US Public 62% Pfizer / US 11'400 11'400 Market Oncology

US NC The Medicines Company / US Public 24% Novartis / Switzerland 9'700 9'700 3 Genetic cardiovascular diseases

US Loxo Oncology / US Public 68% Eli Lilly / US 8'000 8'000 2 Oncology

US Tesaro / US Public 57% GlaxoSmithKline / UK 5'100 5'100 Market Oncology

US Spark Therapeutics / US Public 122% Roche / Switzerland 4'300 4'300 2 Gene therapy

Europe Merck KGaA Cancer IO Pipeline / Germany Asset/Div. GSK / UK 340 4'200 2 Cancer IO products

US NC Audentes Therapeutics / US Public 110% Astellas Pharma / Japan 2'700 2'700 NDA Genetic neuromuscular diseases

US NC ArQule / US Public 107% Merck & Co. / US 2'700 2'700 2 B-cell malignancies

US NC Synthorx / US Public 172% Sanofi / US 2'500 2'500 1 Cancer, solid tumors

US Peloton Therapeutics / US Private VC Merck & Co. / US 1'050 2'200 2 137 Oncology, kidney cancer

US NC Ra Pharmaceuticals / US Public 100% UCB / Belgium 2'100 2'100 3 Myasthenia gravis

US Alder Biopharmaceuticals / US Public 79% Lundbeck / Denmark 1'950 2'020 NDA Migraine

US IFM Tre / US Private VC Novartis / Switzerland 310 1'575 1 242 NASH, inflammation, genetic dis.

US Promedior / US Private VC Roche / Switzerland 390 1'390 2 77 Anti-fibrotic diseases

Europe Veloxis Pharmaceuticals AS / Denmark Public Asahi Kasei Corp / Japan 1'300 1'300 Market Prevention of organ rejection

ROW Clementia Pharmaceuticals / Canada Public 70% Ipsen / France 1'000 1'263 3 Genetic diseases

Asia Kyowa Hakko Bio / Japan Public Kirin Holdings / Japan 1'200 1'200 Market Consumer health

US Paragon Bioservices / US Private VC Catalent / US 1'200 1'200 n.a. Gene therapy production

US Achillion Pharmaceuticals / US Public 72% Alexion Pharmaceuticals / US 930 1'100 2 Factor D inhibitors, genetic dis.

Europe GSK (rabies vaccine etc.) / UK Asset/Div. Bavarian Nordic / Denmark 336 1'050 Market Rabies & ensphalitis vaccines

US Exonics Therapeutics / US Private VC Vertex / US 245 1'000 Preclinical Genetic diseases, DMD

US Dova Pharmaceuticals / US Public 36% SOBI Swedish Orphan Biovitrum / Sweden915 965 Market ITP, chronic liver disease

US Semma Therapeutics / US Private VC Vertex Pharmaceuticals Inc / US 950 950 Preclinical Type 1 diabetes

US Rodin Therapeutics / US Private VC Alkermes / Ireland 100 950 Preclinical 45 Neurodegenerative disorders

Europe Nightstar Therapeutics / UK Public 69% Biogen / US 877 877 3 Genetic dis., choroideremia (CHM)

Europe Therachon / Switzerland Private VC Pfizer / US 340 810 1 163 Genetic diseases, achondroplasia

US Tilos Therapeutics / US Private VC Merck & Co. / US not discl. 773 Preclinical 57 Cancer, fibrotic diseases

US Xyphos Biosciences / US Private VC Astellas Pharma / Japan 120 665 Preclinical 100 Cancer, bi-specific AB

ROW Takeda (Russian OTC business) / Russia Asset/Div. Stada Arzneimittel AG / Germany 660 660 Market Various OTC and RX products

US 1) Osiris Therapeutics / US Public Smith & Nephew / UK 660 660 Market Wound healing, regenerative medicine

US BlueRock (remaining 60% ) / US Private VC Bayer / Germany 240 600 1 Cell therapies,neurology, cardiology etc.

US Calporta Therapeutics / US Private VC Merck / US not discl. 576 Preclinical Lysosomal storage disorders

Europe Breath Therapeutics / Germany Private VC Zambon / Italy 156 558 3 Respiratory, bronchiolitis

Asia Kyowa Pharma (subs. Lupin) / Japan Asset/Div. PE Unison Capital / Japan 526 526 Market Branded generics

Europe NovImmune (emapalumab assets) / SwitzerlandPrivate VC SOBI / Sweden 520 520 Market 10 Primary haemophagocytic lymphohistiocytosis

Asia Aspen Japan (subs. Aspen Global) / Japan Asset/Div. Novartis / Switzerland 331 442 Market Generics

US NC Progenics Pharmaceuticals / US Public Lantheus Holdings / US 412 412 Market Oncology

US Modis Therapeutics / US Private VC Zogenix / US 250 400 2 240 Genetic disease; Thymidine Kinase 2 deficiency

US Abide Therapeutics / US Private VC Lundbeck / Denmark 250 400 2 Gilles de la Tourette's syndrome, Neuropathic pain

Europe Amal Therapeutics / Switzerland Private VC Boehringer Ingelheim / Germany not discl. 366 Preclinical Cancer IO and vaccines

Europe Trimb Healthcare / Sweden Private PE Karo Pharma / Sweden 360 360 Market Various, OTC

Europe Pensa (generics subs. Esteve) / Spain Asset/Div. Towa Pharmaceutical / Japan 356 356 Market Generics

US AvKare / US Private Amneal Pharmaceuticals / US 340 340 Market Generics

US Cavion / US Private VC Jazz Pharmaceuticals / Iceland 53 313 2 Essential tremor

US Immune Design / US Public 300% Merck & Co. / US 300 300 2 Cancer vaccines

US Spectrum Pharmaceuticals / US Asset/Div. Acrotech (Aurobindo Subs.) / India 160 300 Market Hematology, oncology

ROW Grupo Biotoscana (51% stake) / Uruguay Public PE Knight Therapeutics / Canada 143 281 Market Specialty generics

Asia Arrow Pharmaceuticals (subs. Strides Pharma Science) / AustraliaAsset/Div. PE Arrotex Australia / Australia 208 272 Market Generics

US BioElectron Technology / US Asset/Div. VC PTC Therapeutics / US 10 210 Phase 2 Genetic mitochondrial diseases

Asia Boan Biological Technology / China Private Luye Pharma / China 103 205 Preclinical Biosimilars

US Synergy (from bankruptcy) / US Asset/Div. Bausch Health / Canada 200 200 Market GI

Asia Takeda (OTC drugs EM) / Japan Asset/Div. Acino / Switzerland 200 200 Market Primary care products

US Semnur Pharmaceuticals / US Private VC Scilex Holding (formerly Sorrento) / US 60 200 3 Non-opioid pain management

HBM Pharma/Biotech M&A Report 2020

4

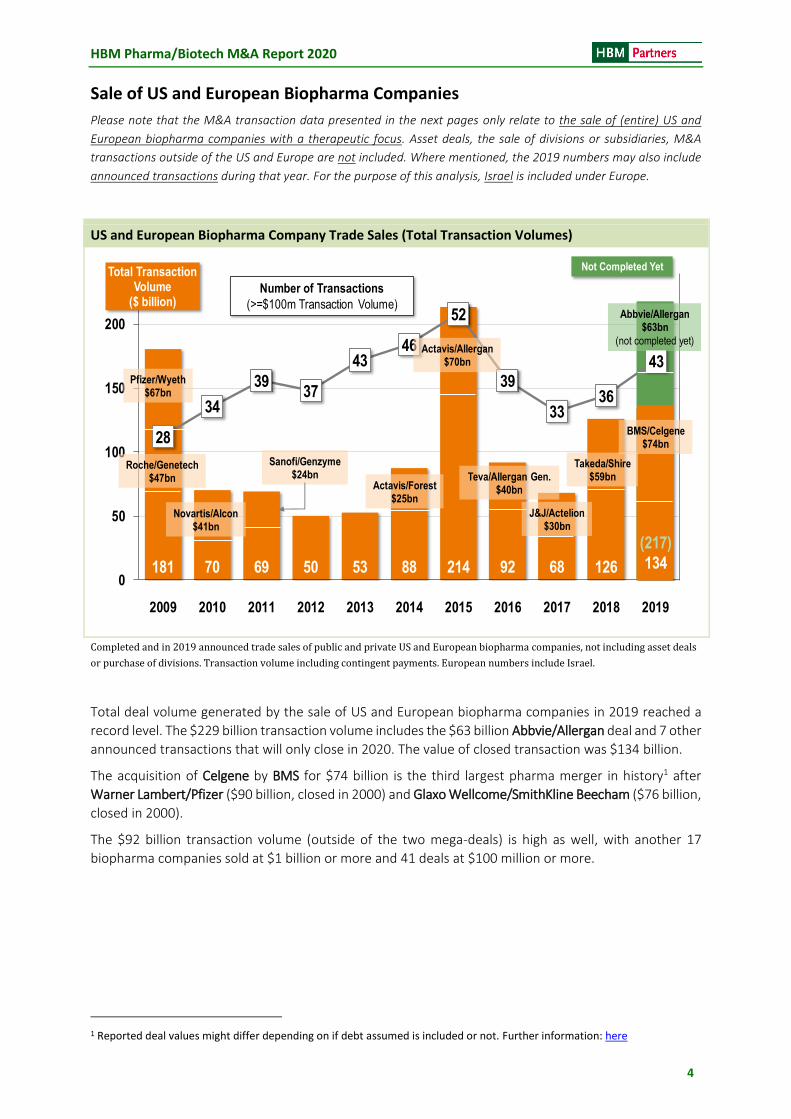

Sale of US and European Biopharma Companies

Please note that the M&A transaction data presented in the next pages only relate to the sale of (entire) US and

European biopharma companies with a therapeutic focus. Asset deals, the sale of divisions or subsidiaries, M&A

transactions outside of the US and Europe are not included. Where mentioned, the 2019 numbers may also include

announced transactions during that year. For the purpose of this analysis, Israel is included under Europe.

US and European Biopharma Company Trade Sales (Total Transaction Volumes)

Completed and in 2019 announced trade sales of public and private US and European biopharma companies, not including asset deals

or purchase of divisions. Transaction volume including contingent payments. European numbers include Israel.

Total deal volume generated by the sale of US and European biopharma companies in 2019 reached a

record level. The $229 billion transaction volume includes the $63 billion Abbvie/Allergan deal and 7 other

announced transactions that will only close in 2020. The value of closed transaction was $134 billion.

The acquisition of Celgene by BMS for $74 billion is the third largest pharma merger in history1 after

Warner Lambert/Pfizer ($90 billion, closed in 2000) and Glaxo Wellcome/SmithKline Beecham ($76 billion,

closed in 2000).

The $92 billion transaction volume (outside of the two mega-deals) is high as well, with another 17

biopharma companies sold at $1 billion or more and 41 deals at $100 million or more.

1 Reported deal values might differ depending on if debt assumed is included or not. Further information: here

181 70 69 50 53 88 214 92 68 126 218

28

34

3937

4346

52

39

3336

43

0

50

100

150

200

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Total Transaction Volume

($ billion)

(217)

134

(217)

134

Pfizer/Wyeth$67bn

Roche/Genetech$47bn

Novartis/Alcon$41bn

Sanofi/Genzyme$24bn

Actavis/Forest$25bn

Actavis/Allergan$70bn

Teva/Allergan Gen.$40bn

J&J/Actelion$30bn

Takeda/Shire$59bn

Abbvie/Allergan$63bn

(not completed yet)

Number of Transactions

(>=$100m Transaction Volume)

BMS/Celgene$74bn

Not Completed Yet

HBM Pharma/Biotech M&A Report 2020

5

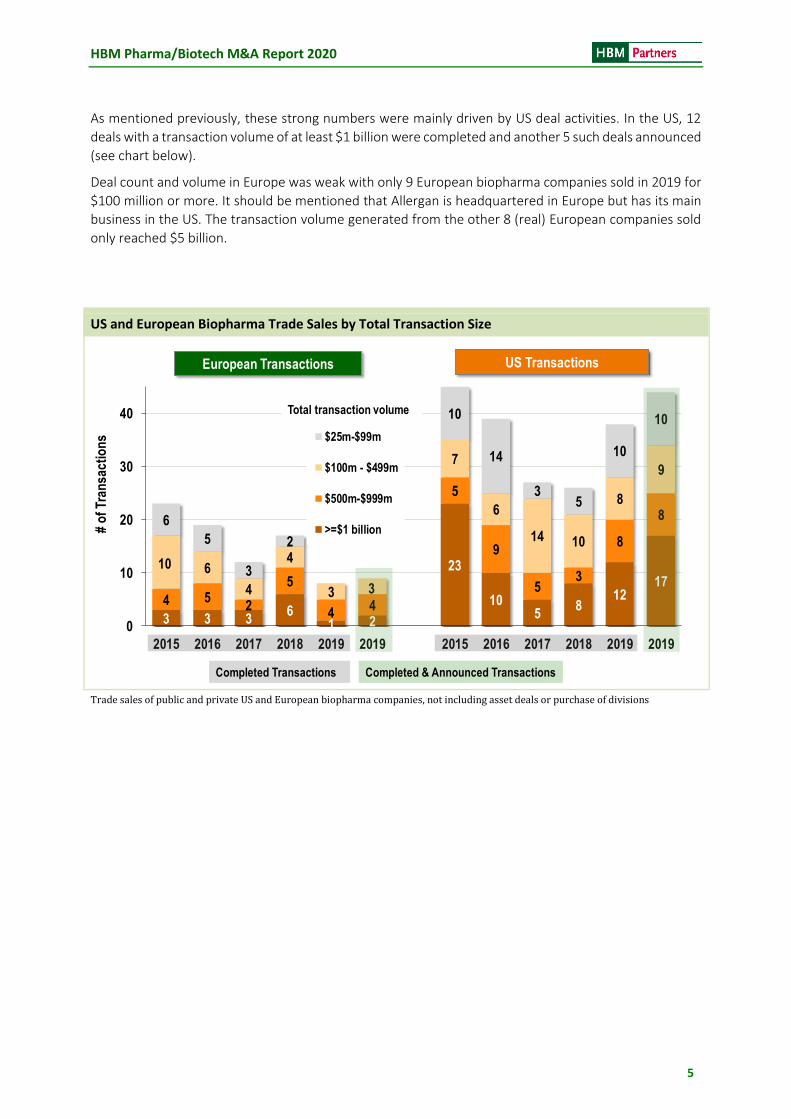

As mentioned previously, these strong numbers were mainly driven by US deal activities. In the US, 12

deals with a transaction volume of at least $1 billion were completed and another 5 such deals announced

(see chart below).

Deal count and volume in Europe was weak with only 9 European biopharma companies sold in 2019 for

$100 million or more. It should be mentioned that Allergan is headquartered in Europe but has its main

business in the US. The transaction volume generated from the other 8 (real) European companies sold

only reached $5 billion.

US and European Biopharma Trade Sales by Total Transaction Size

Trade sales of public and private US and European biopharma companies, not including asset deals or purchase of divisions

3 3 36

1 2

23

105

812

17

4 52

5

44

5

9

53

8

8

10 6

4

4

3 3

7

6

14 10

8

9

6

5

3

2

10

14

35

10

10

0

10

20

30

40

2015 2016 2017 2018 2019 2019 2015 2016 2017 2018 2019 2019

# o

f T

ran

sact

ion

s $25m-$99m

$100m - $499m

$500m-$999m

>=$1 billion

European Transactions US Transactions

Completed Transactions Completed & Announced Transactions

Total transaction volume

HBM Pharma/Biotech M&A Report 2020

6

Premiums Paid for Public US and European Biopharma Companies

Premium = Increase of stock price on the day of deal announcement. Only deals with an upfront consideration of at

least $100 million are included in this analysis. Given the high degree of variation in premiums paid, the average

numbers should be interpreted with caution.

Premiums Paid for US and European Public Biopharma Companies

Completed and announced (2019) trade sales of public US and European biopharma companies with total deal value of at least $100 million. Non-weighted average premiums.

◼ Average premiums paid in 2019 for public US and European biopharma companies reached almost

100%. These very high premiums show that there is a continued appetite for acquisitions despite the

already high valuations of public biopharma companies.

◼ The premiums paid in large deals ($10 billion or more) was generally lower than that for smaller

companies: The average premiums paid in the 13 $10-billion-plus deals done during the five years

2015-2019 was 43% vs. the average premium of 84% paid in smaller transactions).

◼ As seen in the chart above, premiums paid for European companies have - until 2017 – been lower

than for US companies. In 2018 and 2019 premiums paid in Europe caught up with the numbers in

the US.

◼ Smaller and clinical-stage companies generally received higher premiums than companies with

approved or marketed products (see table below).

Average Premiums Paid for US & European Public Biopharma Companies 2015-2019 by Stage of Lead

Product (total deal value $100 million or more)

Phase 2 Phase 3 NDA Filed Approved/

Marketed

Total*

# of public companies sold 15 16 8 36 75

Average premium paid 136% 65% 72% 43% 72%

7HBM Biopharma M&A Report

47%

77%

57%

29%

60%

36%

109%

82%

70%

97%

36%

46%

25%27%

31%

64%

26%

73%

94%

0%

20%

40%

60%

80%

100%

120%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Ave

rag

e P

rem

ium

sP

aid

in P

ub

lic T

akeo

vers

US and European public takeovers with

total deal value of at least $100 million

Including 500% premium paid by

Allergan for Tobira.

Without that deal the average

premium in 2016 would be 70%.

High Premiums Paid in 2018 for Public US & European Companies

Premiums* Paid for Public Take-Overs 2009-2018

Average

Premiums

paid for

European

Companies

Average

Premiums

Paid for US

Companies

Only two

European

transactions

in 2019!

HBM Pharma/Biotech M&A Report 2020

7

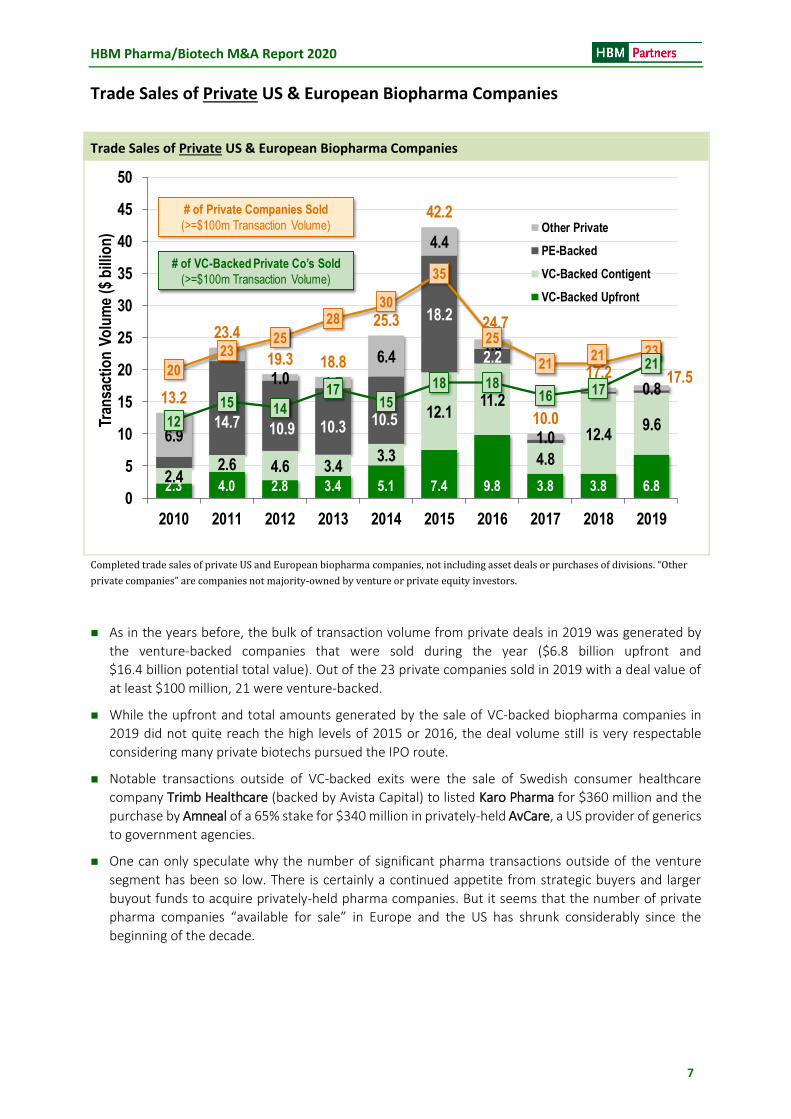

Trade Sales of Private US & European Biopharma Companies

Trade Sales of Private US & European Biopharma Companies

Completed trade sales of private US and European biopharma companies, not including asset deals or purchases of divisions. “Other

private companies” are companies not majority-owned by venture or private equity investors.

◼ As in the years before, the bulk of transaction volume from private deals in 2019 was generated by

the venture-backed companies that were sold during the year ($6.8 billion upfront and

$16.4 billion potential total value). Out of the 23 private companies sold in 2019 with a deal value of

at least $100 million, 21 were venture-backed.

◼ While the upfront and total amounts generated by the sale of VC-backed biopharma companies in

2019 did not quite reach the high levels of 2015 or 2016, the deal volume still is very respectable

considering many private biotechs pursued the IPO route.

◼ Notable transactions outside of VC-backed exits were the sale of Swedish consumer healthcare

company Trimb Healthcare (backed by Avista Capital) to listed Karo Pharma for $360 million and the

purchase by Amneal of a 65% stake for $340 million in privately-held AvCare, a US provider of generics

to government agencies.

◼ One can only speculate why the number of significant pharma transactions outside of the venture

segment has been so low. There is certainly a continued appetite from strategic buyers and larger

buyout funds to acquire privately-held pharma companies. But it seems that the number of private

pharma companies “available for sale” in Europe and the US has shrunk considerably since the

beginning of the decade.

2.3 4.0 2.8 3.4 5.1 7.4 9.8 3.8 3.8 6.82.4

2.6 4.6 3.43.3

12.111.2

4.8

12.49.614.7 10.9 10.3 10.5

18.2

2.2

6.9

2.1

1.0 1.7

6.4

4.4

1.5

1.0

0.7 0.813.2

23.4

19.3 18.8

25.3

42.2

24.7

10.0

17.2 17.520

2325

2830

35

25

2121 23

12

15 14

1715

18 1816 17

21

0

5

10

15

20

25

30

35

40

45

50

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Tran

sact

ion

Vo

lum

e ($

bill

ion

) Other Private

PE-Backed

VC-Backed Contigent

VC-Backed Upfront

# of Private Companies Sold

(>=$100m Transaction Volume)

# of VC-Backed Private Co’s Sold

(>=$100m Transaction Volume)

HBM Pharma/Biotech M&A Report 2020

8

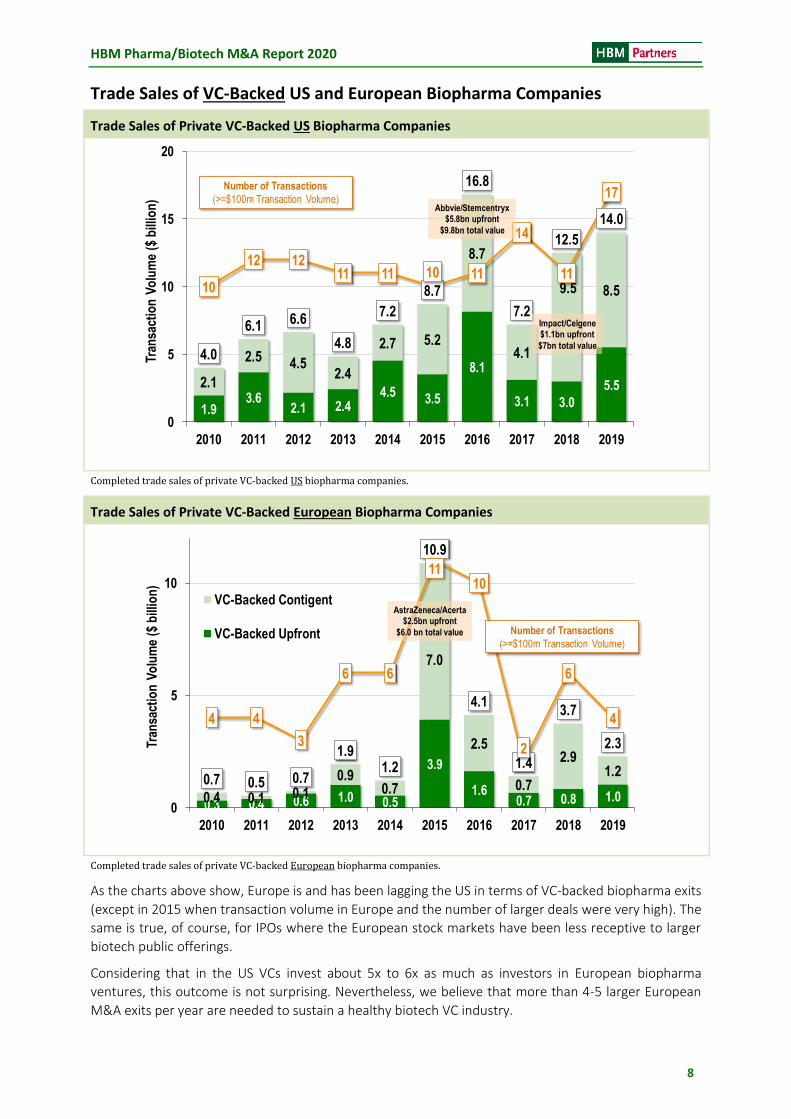

Trade Sales of VC-Backed US and European Biopharma Companies

Trade Sales of Private VC-Backed US Biopharma Companies

Completed trade sales of private VC-backed US biopharma companies.

Trade Sales of Private VC-Backed European Biopharma Companies

Completed trade sales of private VC-backed European biopharma companies.

As the charts above show, Europe is and has been lagging the US in terms of VC-backed biopharma exits

(except in 2015 when transaction volume in Europe and the number of larger deals were very high). The

same is true, of course, for IPOs where the European stock markets have been less receptive to larger

biotech public offerings.

Considering that in the US VCs invest about 5x to 6x as much as investors in European biopharma

ventures, this outcome is not surprising. Nevertheless, we believe that more than 4-5 larger European

M&A exits per year are needed to sustain a healthy biotech VC industry.

1.93.6

2.1 2.44.5

3.5

8.1

3.1 3.0

5.52.1

2.5 4.52.4

2.7 5.2

8.7

4.1

9.5 8.5

4.0

6.1 6.6

4.8

7.2

8.7

16.8

7.2

12.5

14.0

10

12 1211 11 10 11

14

11

17

0

5

10

15

20

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Tran

sact

ion

Vo

lum

e ($

bill

ion

)

Number of Transactions

(>=$100m Transaction Volume)Abbvie/Stemcentryx

$5.8bn upfront

$9.8bn total value

Impact/Celgene$1.1bn upfront

$7bn total value

0.3 0.4 0.6 1.0 0.5

3.9

1.60.7 0.8 1.00.4 0.1 0.1

0.90.7

7.0

2.5

0.7

2.91.2

0.7 0.5 0.7

1.91.2

10.9

4.1

1.4

3.7

2.3

4 4

3

6 6

1110

2

6

4

0

5

10

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Tran

sact

ion

Vo

lum

e ($

bill

ion

)

VC-Backed Contigent

VC-Backed Upfront Number of Transactions

(>=$100m Transaction Volume)

AstraZeneca/Acerta$2.5bn upfront

$6.0 bn total value

HBM Pharma/Biotech M&A Report 2020

9

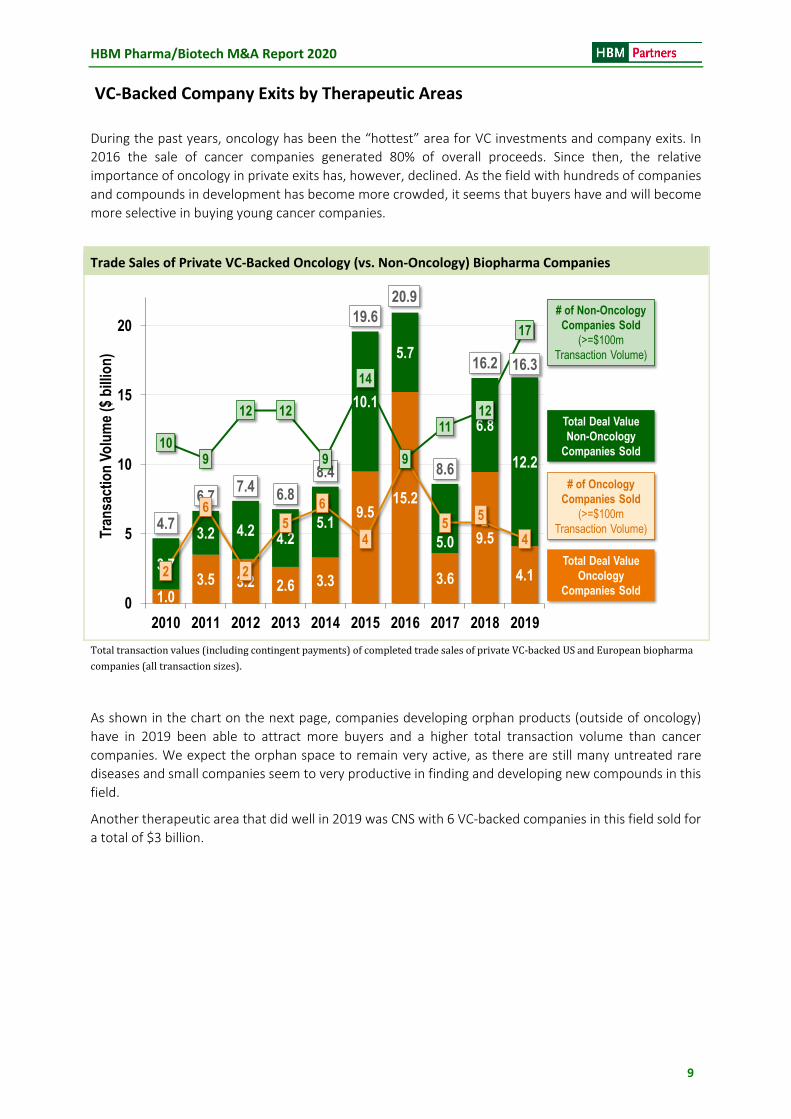

VC-Backed Company Exits by Therapeutic Areas

During the past years, oncology has been the “hottest” area for VC investments and company exits. In

2016 the sale of cancer companies generated 80% of overall proceeds. Since then, the relative

importance of oncology in private exits has, however, declined. As the field with hundreds of companies

and compounds in development has become more crowded, it seems that buyers have and will become

more selective in buying young cancer companies.

Trade Sales of Private VC-Backed Oncology (vs. Non-Oncology) Biopharma Companies

Total transaction values (including contingent payments) of completed trade sales of private VC-backed US and European biopharma

companies (all transaction sizes).

As shown in the chart on the next page, companies developing orphan products (outside of oncology)

have in 2019 been able to attract more buyers and a higher total transaction volume than cancer

companies. We expect the orphan space to remain very active, as there are still many untreated rare

diseases and small companies seem to very productive in finding and developing new compounds in this

field.

Another therapeutic area that did well in 2019 was CNS with 6 VC-backed companies in this field sold for

a total of $3 billion.

12HBM Biopharma M&A Report

Trade Sales of Private Biopharma Companies 2010-2019

1.03.5 3.2 2.6 3.3

9.515.2

3.6

9.5

4.13.7

3.2 4.24.2

5.1

10.1

5.7

5.0

6.8

12.2

4.7

6.77.4

6.8

8.4

19.6

20.9

8.6

16.2 16.3

2

6

2

5

6

4

9

55

4

109

12 12

9

14

9

1112

17

0

5

10

15

20

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Tran

sact

ion

Vo

lum

e ($

bill

ion

)

Trade sales of private US & European biopharma companies (completed transactions)

# of Oncology

Companies Sold

(>=$100m

Transaction Volume)

# of Non-Oncology

Companies Sold

(>=$100m

Transaction Volume)

Total Deal Value

Non-Oncology

Companies Sold

Total Deal Value

Oncology

Companies Sold

HBM Pharma/Biotech M&A Report 2020

10

Trade Sales of VC-Backed Orphan (vs. “Other”) Companies

Total transaction values (including contingent payments) of completed trade sales of private VC-backed US and European biopharma

companies (all transaction sizes).

13HBM Biopharma M&A Report

Trade Sales of Private Biopharma Companies 2010-2019

1.1 1.6 1.3 2.0 2.6

5.5

7.3

17.9 19.6

6.6

13.6

10.8

8.4

19.6

20.9

8.6

16.2 16.3

3 3 3

5

3

8

12

15 15

11

1413

0

5

10

15

20

2014 2015 2016 2017 2018 2019

Tran

sact

ion

Vo

lum

e ($

bill

ion

)

Trade sales of private US & European biopharma companies (completed transactions)

# of Co’s Sold

With Orphan Prod.

(>=$100m

Transaction Volume)

# of Other

Companies Sold

(>=$100m

Transaction Volume)

Total Deal Value

Other Companies

Sold

Total Deal Value

Co’s Sold With

Orphan Products

Noteworthy Venture Exits in 2019

In May 2019, US-based Peleton Therapeutics was sold to Merck for $1.05 billion million upfront plus potential milestone payments of up to $1.15 billion. Peleton with its phase 3-ready kidney cancer drug was founded in 2010. It is estimated that over $200 million were invested by VCs in the company generating significant returns for investors such as Column Group, EcoR1, Nextech, RA and Foresite.

Also in May 2019, US IFM Tre was acquired by Novartis for $310 million upfront plus contingent payments of up to $1.265 billion. IFM Tre’s portfolio of NLPR3 antagonists, consisting of one clinical and two preclinical programs, target chronic inflammatory and fibrotic disorders. With only about $30 million invested, the exit should provide a great return for Atlas and Abingworth. And, another sibling company of IFM was already sold in 2017 to BMS for up to $1.3 billion.

In November 2019, Roche acquired US Promedior for up to $1.39 billion ($390 million upfront), a year after previous suitor BMS opted not to exercise its right to acquire the developer of treatments for fibrotic diseases. Earlier in 2019, Promedior generated positive Phase II results in idiopathic pulmonary fibrosis (IPF) and myelofibrosis (MF). The company, founded in 2006, was financed with an estimated $63 million by various VCs (Forbion, Polaris, Morgenthaler, Healthcare Ventures, Easton Capital), thus providing great returns to investors.

Vertex acquired two companies in 2019. Vertex picked up Exonics Therapeutics in June 2019 (for $245 million upfront and $1 billion total potential value) with its SingleCut CRISPR gene editing technology to develop treatments by repairing mutations that cause DMD and other genetic neuromuscular diseases. Exonics was launched in 2017 and received $45 million of financing by CureDuchenne Ventures and Column Group.

With the acquisition of Semma Therapeutics in October 2019 for $950 million in cash, Vertex made a bet on the use of stem cell-derived human islets as a potentially curative treatment for type 1 diabetes. Semma was founded in 2016 and financed with an estimated $163 million by VCs such as Eight Roads, Arch, MPM, Cowen, F-Prime and the corporate venture funds of Novartis and Medtronic.

HBM Pharma/Biotech M&A Report 2020

11

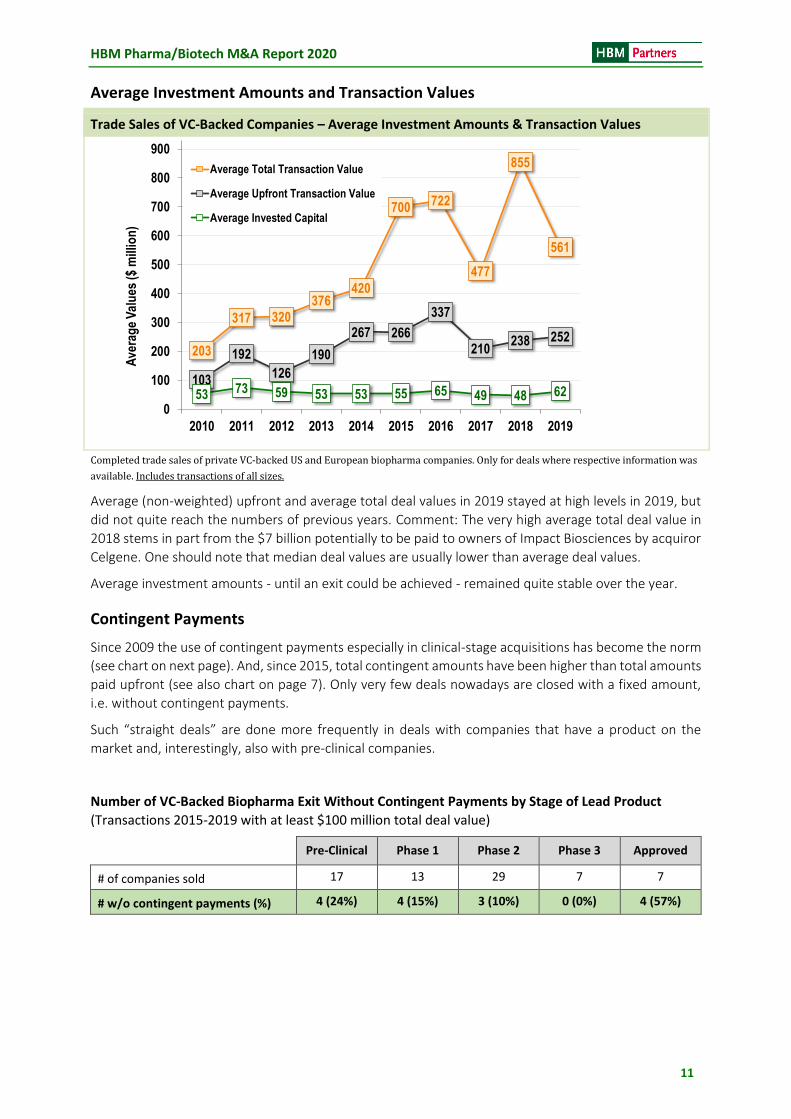

Average Investment Amounts and Transaction Values

Trade Sales of VC-Backed Companies – Average Investment Amounts & Transaction Values

Completed trade sales of private VC-backed US and European biopharma companies. Only for deals where respective information was

available. Includes transactions of all sizes.

Average (non-weighted) upfront and average total deal values in 2019 stayed at high levels in 2019, but

did not quite reach the numbers of previous years. Comment: The very high average total deal value in

2018 stems in part from the $7 billion potentially to be paid to owners of Impact Biosciences by acquiror

Celgene. One should note that median deal values are usually lower than average deal values.

Average investment amounts - until an exit could be achieved - remained quite stable over the year.

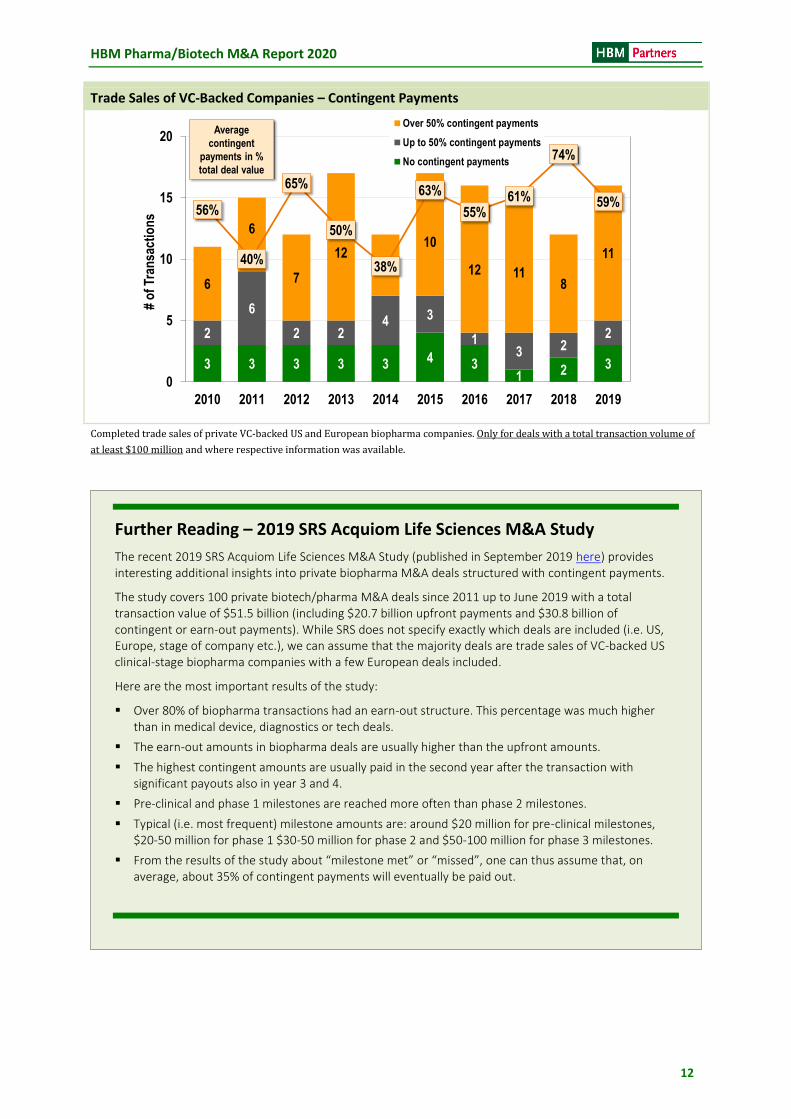

Contingent Payments

Since 2009 the use of contingent payments especially in clinical-stage acquisitions has become the norm

(see chart on next page). And, since 2015, total contingent amounts have been higher than total amounts

paid upfront (see also chart on page 7). Only very few deals nowadays are closed with a fixed amount,

i.e. without contingent payments.

Such “straight deals” are done more frequently in deals with companies that have a product on the

market and, interestingly, also with pre-clinical companies.

Number of VC-Backed Biopharma Exit Without Contingent Payments by Stage of Lead Product

(Transactions 2015-2019 with at least $100 million total deal value)

Pre-Clinical Phase 1 Phase 2 Phase 3 Approved

# of companies sold 17 13 29 7 7

# w/o contingent payments (%) 4 (24%) 4 (15%) 3 (10%) 0 (0%) 4 (57%)

14HBM Biopharma M&A Report

203

317 320

376420

700722

477

855

561

103

192

126

190

267 266

337

210238 252

53 73 59 53 53 55 65 49 48 62

0

100

200

300

400

500

600

700

800

900

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Ave

rag

e V

alu

es ($

mill

ion

)

Average Total Transaction Value

Average Upfront Transaction Value

Average Invested Capital

Average Investment / Average Upfront and Total Deal Values

Trade sales of private VC-backed US &

European biopharma companies

Only for transactions where

respective information was available.

Trade sales of private VC-backed US & European biopharma companies

HBM Pharma/Biotech M&A Report 2020

12

Trade Sales of VC-Backed Companies – Contingent Payments

Completed trade sales of private VC-backed US and European biopharma companies. Only for deals with a total transaction volume of

at least $100 million and where respective information was available.

15HBM Biopharma M&A Report

Contingent „Biodollar“ Payments as % of Total Deal Value

3 3 3 3 3 4 31 2 3

2

6

2 24 3

13 2

2

6

6

7

125

10

12 118

11

56%

40%

65%

50%

38%

63%

55%61%

74%

59%

0

5

10

15

20

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

# o

f Tr

ansa

ctio

ns

Over 50% contingent payments

Up to 50% contingent payments

No contingent payments

Average

contingent

payments in %

total deal value

Trade sales of private VC-backed US & European biopharma companies

Trade sales of private VC-backed US &

European biopharma companies

Only for transactions where

respective information was available.

Further Reading – 2019 SRS Acquiom Life Sciences M&A Study

The recent 2019 SRS Acquiom Life Sciences M&A Study (published in September 2019 here) provides interesting additional insights into private biopharma M&A deals structured with contingent payments.

The study covers 100 private biotech/pharma M&A deals since 2011 up to June 2019 with a total transaction value of $51.5 billion (including $20.7 billion upfront payments and $30.8 billion of contingent or earn-out payments). While SRS does not specify exactly which deals are included (i.e. US, Europe, stage of company etc.), we can assume that the majority deals are trade sales of VC-backed US clinical-stage biopharma companies with a few European deals included.

Here are the most important results of the study:

▪ Over 80% of biopharma transactions had an earn-out structure. This percentage was much higher than in medical device, diagnostics or tech deals.

▪ The earn-out amounts in biopharma deals are usually higher than the upfront amounts.

▪ The highest contingent amounts are usually paid in the second year after the transaction with significant payouts also in year 3 and 4.

▪ Pre-clinical and phase 1 milestones are reached more often than phase 2 milestones.

▪ Typical (i.e. most frequent) milestone amounts are: around $20 million for pre-clinical milestones, $20-50 million for phase 1 $30-50 million for phase 2 and $50-100 million for phase 3 milestones.

▪ From the results of the study about “milestone met” or “missed”, one can thus assume that, on average, about 35% of contingent payments will eventually be paid out.

HBM Pharma/Biotech M&A Report 2020

13

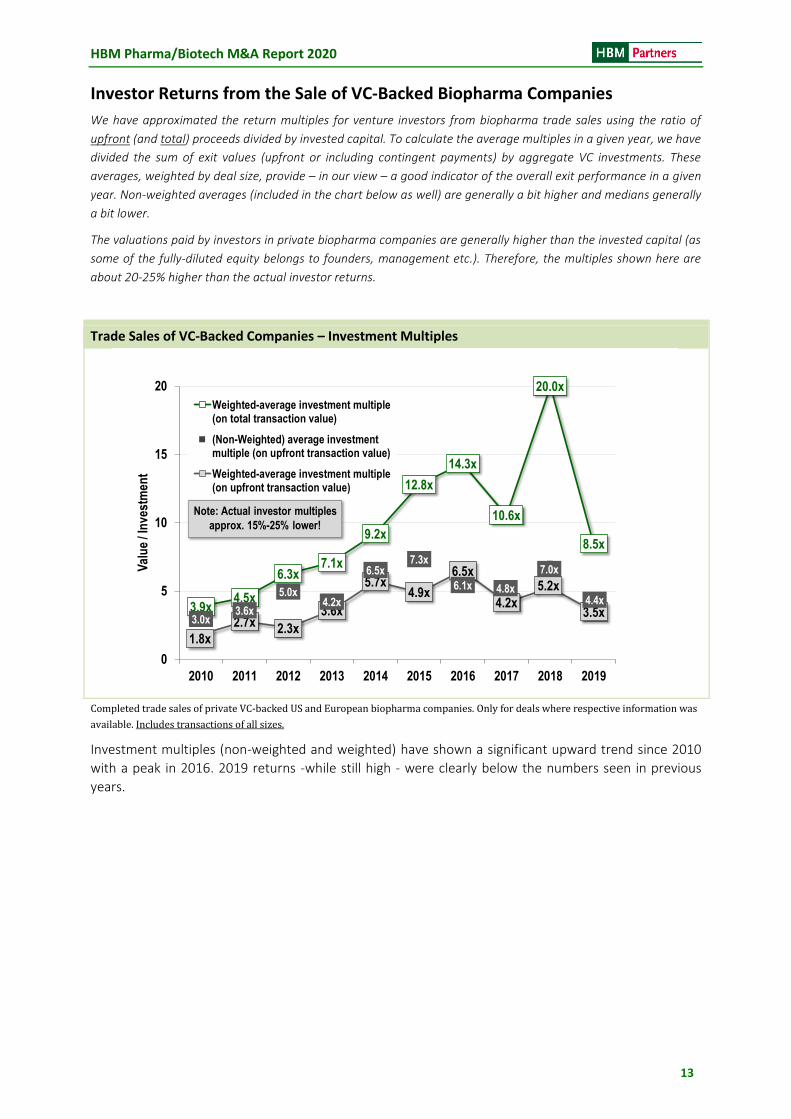

Investor Returns from the Sale of VC-Backed Biopharma Companies

We have approximated the return multiples for venture investors from biopharma trade sales using the ratio of

upfront (and total) proceeds divided by invested capital. To calculate the average multiples in a given year, we have

divided the sum of exit values (upfront or including contingent payments) by aggregate VC investments. These

averages, weighted by deal size, provide – in our view – a good indicator of the overall exit performance in a given

year. Non-weighted averages (included in the chart below as well) are generally a bit higher and medians generally

a bit lower.

The valuations paid by investors in private biopharma companies are generally higher than the invested capital (as

some of the fully-diluted equity belongs to founders, management etc.). Therefore, the multiples shown here are

about 20-25% higher than the actual investor returns.

Trade Sales of VC-Backed Companies – Investment Multiples

Completed trade sales of private VC-backed US and European biopharma companies. Only for deals where respective information was

available. Includes transactions of all sizes.

Investment multiples (non-weighted and weighted) have shown a significant upward trend since 2010

with a peak in 2016. 2019 returns -while still high - were clearly below the numbers seen in previous

years.

17HBM Biopharma M&A Report

Average Investment Multiples On Upfront and Total Deal Value

3.9x4.5x

6.3x7.1x

9.2x

12.8x

14.3x

10.6x

20.0x

8.5x

1.8x

2.7x 2.3x

3.6x

5.7x4.9x

6.5x

4.2x

5.2x

3.5x3.0x

3.6x

5.0x4.2x

6.5x7.3x

6.1x 4.8x

7.0x

4.4x

0

5

10

15

20

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Val

ue

/ In

vest

men

t

Weighted-average investment multiple(on total transaction value)

(Non-Weighted) average investmentmultiple (on upfront transaction value)

Weighted-average investment multiple(on upfront transaction value)

Trade sales of private VC-backed US & European biopharma companies

Trade sales of private VC-backed US &

European biopharma companies

Only for transactions where

respective information was available.

Note: Actual investor multiples

approx. 15%-25% lower!

HBM Pharma/Biotech M&A Report 2020

14

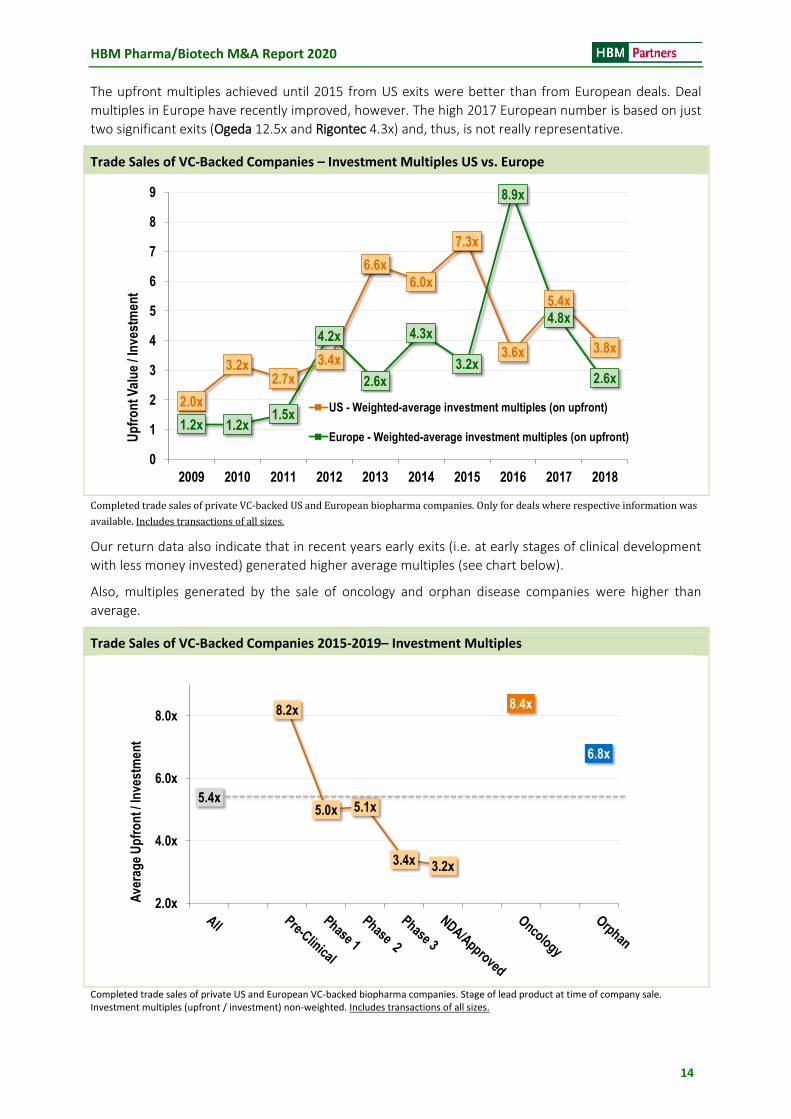

The upfront multiples achieved until 2015 from US exits were better than from European deals. Deal

multiples in Europe have recently improved, however. The high 2017 European number is based on just

two significant exits (Ogeda 12.5x and Rigontec 4.3x) and, thus, is not really representative.

Trade Sales of VC-Backed Companies – Investment Multiples US vs. Europe

Completed trade sales of private VC-backed US and European biopharma companies. Only for deals where respective information was

available. Includes transactions of all sizes.

Our return data also indicate that in recent years early exits (i.e. at early stages of clinical development

with less money invested) generated higher average multiples (see chart below).

Also, multiples generated by the sale of oncology and orphan disease companies were higher than

average.

Trade Sales of VC-Backed Companies 2015-2019– Investment Multiples

Completed trade sales of private US and European VC-backed biopharma companies. Stage of lead product at time of company sale. Investment multiples (upfront / investment) non-weighted. Includes transactions of all sizes.

18HBM Biopharma M&A Report

Average Investment Multiples On Upfront Deal Value – US vs. Europe

2.0x

3.2x2.7x

3.4x

6.6x

6.0x

7.3x

3.6x

5.4x

3.8x

1.2x 1.2x1.5x

4.2x

2.6x

4.3x

3.2x

8.9x

4.8x

2.6x

0

1

2

3

4

5

6

7

8

9

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Up

fro

ntV

alu

e / I

nve

stm

ent

US - Weighted-average investment multiples (on upfront)

Europe - Weighted-average investment multiples (on upfront)

Trade sales of private VC-backed US & European biopharma companies

Trade sales of private VC-backed US &

European biopharma companies

Only for transactions where

respective information was available.

19HBM Biopharma M&A Report

Average Investment Multiples On Upfront Deal Value – US vs. Europe

5.4x

8.2x

5.0x 5.1x

3.4x 3.2x

8.4x

6.8x

2.0x

4.0x

6.0x

8.0x

Ave

rag

e U

pfr

on

t / In

vest

men

t

Trade sales of private VC-backed US & European biopharma companies

Trade sales of private VC-backed US &

European biopharma companies

Only for transactions where

respective information was available.

HBM Pharma/Biotech M&A Report 2020

15

Summary and Outlook

2019 was a strong year for biopharma M&A mainly in the US. Even though some players that have been

engaged in very large transactions might be less active as buyers for some time, the appetite for

biopharma companies with unique assets will remain high.

We expect to see further active M&A deal making especially if the stock markets would become less

receptive for IPOs and if public company valuations come down.

Zug, 1 February 2020

The authors of the report welcome any feedback or corrections:

Dr Ulrich Geilinger, [email protected] , Dr Chandra Leo, [email protected] and

Dr Emil Bujak, [email protected]

About HBM Partners

HBM Partners is among the global leaders in healthcare-focused investing with approximately $1.7 billion in assets under management. HBM focuses on development stage, growth and buy-out financings of private and public biopharma, medical device and diagnostics companies. Investments in private companies usually range between $10 million to $50 million.

HBM Partners advises HBM Healthcare Investments AG (SIX: HMBN) as well as other specialized private & public equity funds.

HBM Partners has been an active contributor to value creation in its portfolio companies, generating over 60 trade sales and IPOs since its inception in 2001.

HBM Partners AG, CH-6300 Zug, Switzerland, www.hbmpartners.com, phone +41 43 888 71 71