2 December 2011

Handelsbanken consumer seminar Mats Berencreutz, Executive Vice President

1

2 2 2

Net sales SEK 107bn

45,000 employees and sales in more than 100 countries

World’s third largest hygiene products company

TEN and Tork leading global brands for incontinence care and Away-From-Home tissue

Europe’s largest private forest owner

Europe’s second largest packaging company

SCA Group A global hygiene products and paper company

2 December 2011 2

3 3

Forest Products

Packaging Tissue

Personal Care

36% 24%

16% 24%

SCA Group Sales split 2010

Sales split

2 December 2011 3

0%

20%

40%

60%

80%

100%

2000 2010

4

% of net sales

Hygiene products (Personal Care and Tissue)

Packaging and Forest Products

46% 60%

40% 54%

2000 2010

Increasing hygiene sales

2 December 2011 4

5

Leading market positions Global and regional

Europe Tissue: 1 Baby diapers: 2 Incontinence care: 1

Australia Feminine care: 1 Incontinence care: 1 Tissue: 2

Mexico Incontinence care: 1 Tissue: 2 Feminine care: 1 Baby diapers: 3 Global

Incontinence care: 1 AFH tissue: 2 Colombia

Incontinence care: 1 Feminine care: 1 Tissue: 1

North America AFH tissue: 3 Incontinence care: 3

2 December 2011 5

6

Strong global and regional brands Two global billion EUR brands

North America

Eastern Europe

Asia Pacific

Europe

Latin America

Sales of SEK 65bn, with sales in more than 100 countries

6 2 December 2011

Strategic focus areas

2 December 2011 7 7

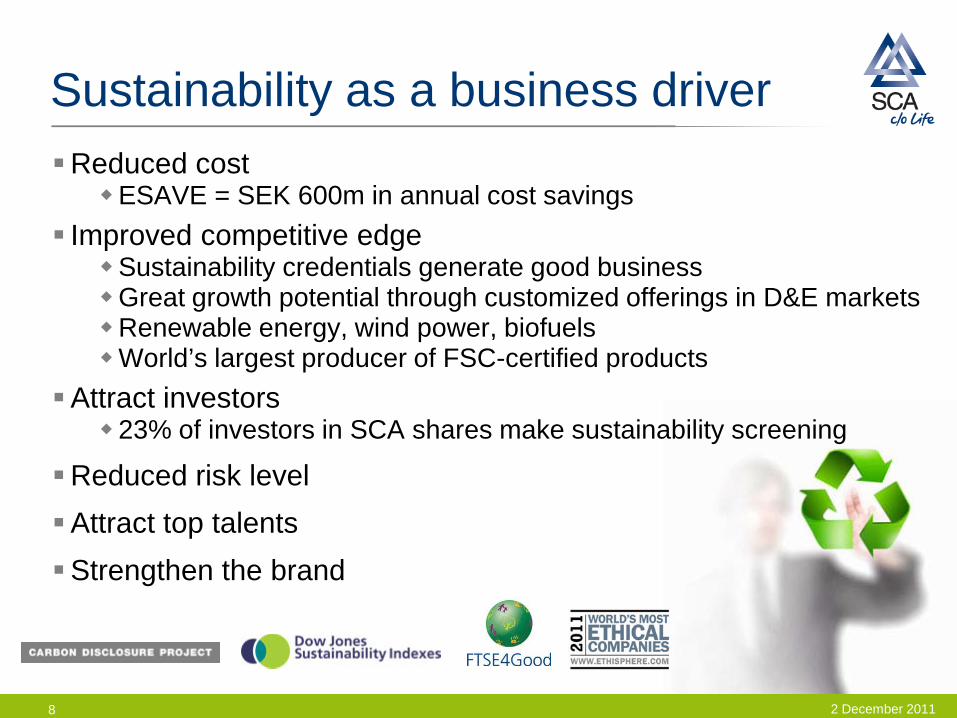

Sustainability as a business driver Reduced cost ESAVE = SEK 600m in annual cost savings

Improved competitive edge Sustainability credentials generate good business Great growth potential through customized offerings in D&E markets Renewable energy, wind power, biofuels World’s largest producer of FSC-certified products

Attract investors 23% of investors in SCA shares make sustainability screening

Reduced risk level Attract top talents Strengthen the brand

2 December 2011 8

9 2 December 2011

Innovation for profitable growth Meet changing demands and requirements Create long-term, profitable differentiation Strengthen market positions Build stronger brands Drive growth

Hygiene business Strategic focus

2 December 2011 10

Strengthen positions and increase growth in main markets and emerging markets

Increase the number of global brands

Increase the pace of innovations

Efficiency improvements

10

Growth potential for hygiene products

2 December 2011 11

Global population growth

An aging population

Increased market penetration

Higher disposable income

Customers and consumers demand more comfort and sustainability

11

12

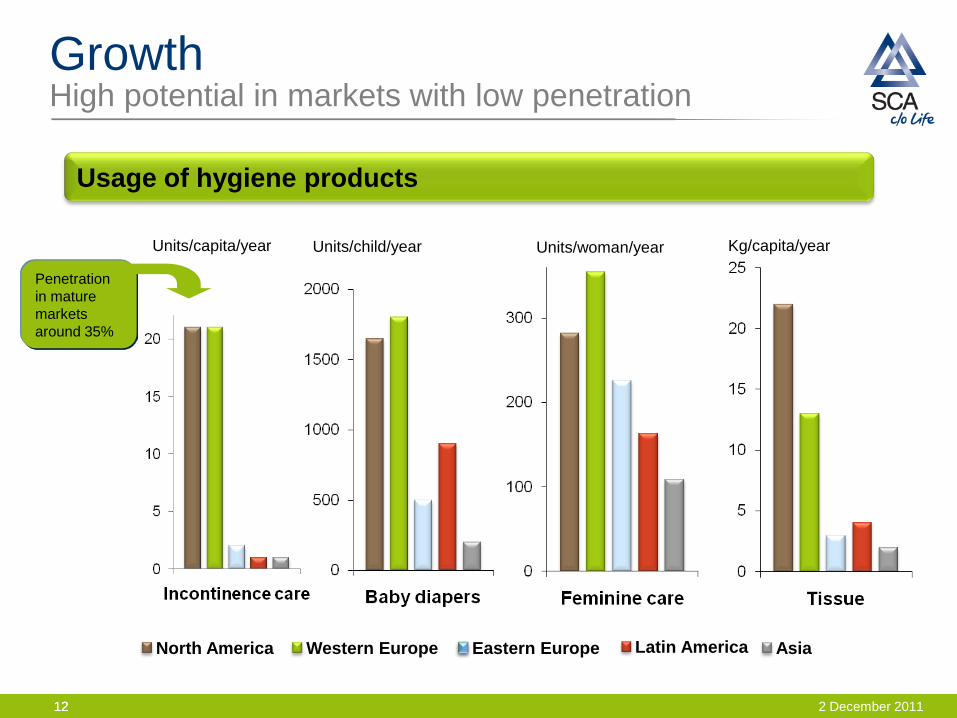

Growth High potential in markets with low penetration

Usage of hygiene products

Units/capita/year Units/child/year Units/woman/year

Western Europe Eastern Europe Latin America Asia North America

Kg/capita/year

Penetration in mature markets around 35%

2 December 2011 12

13 13

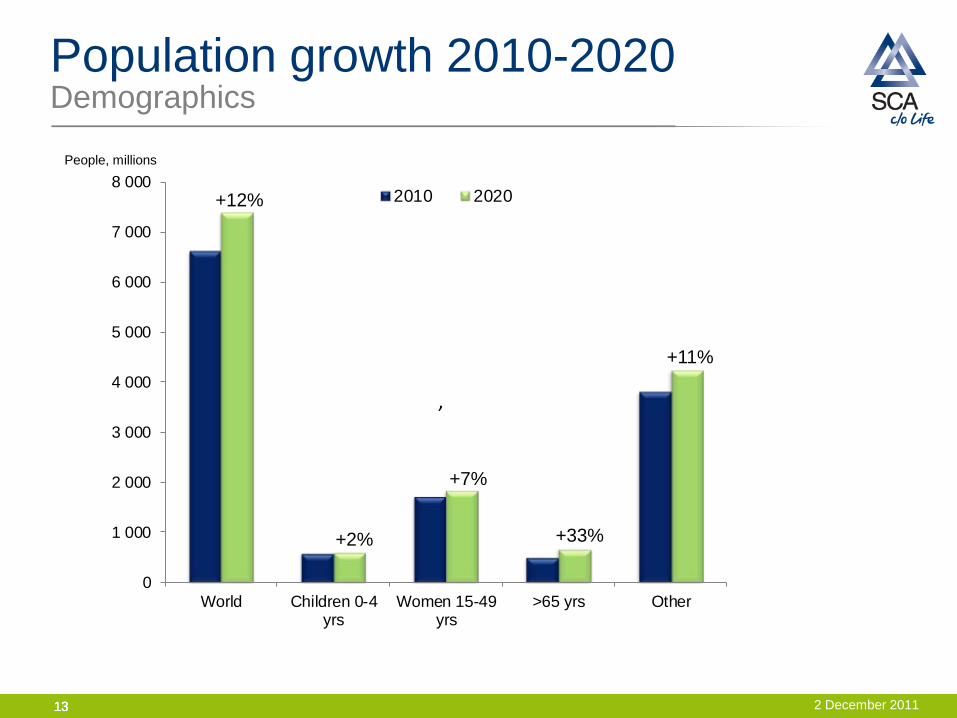

Population growth 2010-2020 Demographics

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

World Children 0-4yrs

Women 15-49yrs

>65 yrs Other

2010 2020

,

+33%

+12%

+2%

+7%

+11%

People, millions

2 December 2011 13

14

Latin America

South East Asia

Eastern Europe /Russia

Strong SCA positions Good market growth Favourable socio-demographics

Good market growth Favourable socio-demographics

Middle East

China

Incontinence care products

Growth SCA’s growth markets

2 December 2011

15

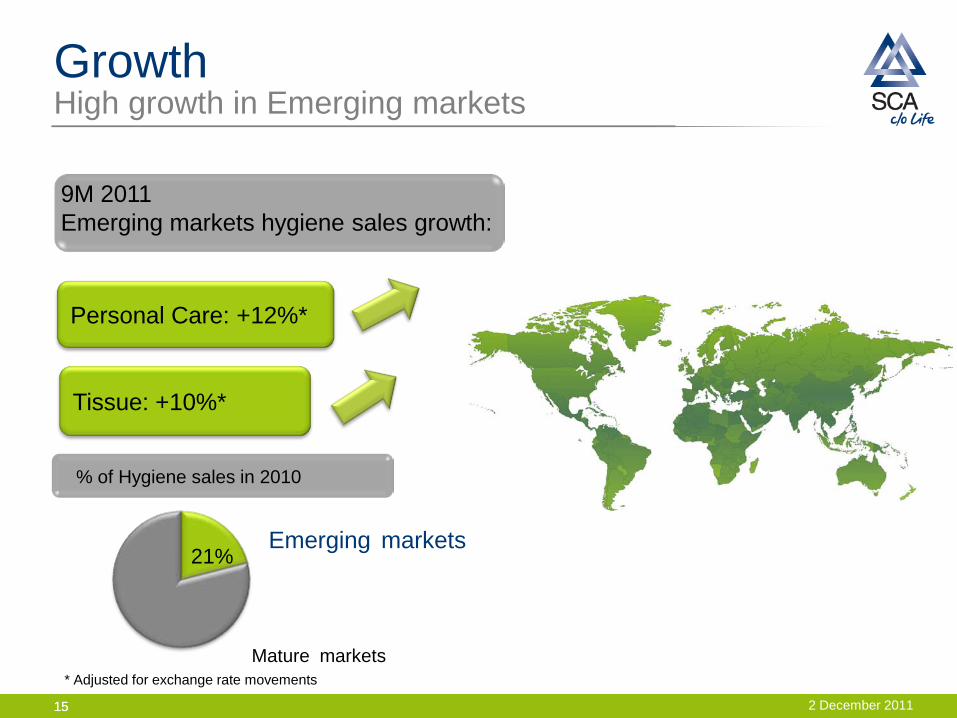

21%

Mature markets

Emerging markets

% of Hygiene sales in 2010

9M 2011 Emerging markets hygiene sales growth:

Personal Care: +12%*

Tissue: +10%*

Growth High growth in Emerging markets

2 December 2011

* Adjusted for exchange rate movements

15

Growth Acquisitions strengthen Emerging markets presence

16

Algodonera Aconcagua

No. 3 in feminine care

Smaller positions in baby diapers and incontinence care products

Copamex No. 3 in baby diapers

San Saglik, 95% No. 2 in incontinence

care products

Komili, 50% No. 4 position in baby

diapers and feminine care

Pro Descart No. 2 in incontinence

care products

Smaller position in baby diapers

2 December 2011

Offered price: EUR 1.32bn

Already in year one the transaction is estimated to contribute to an increase of earnings per share and cash flow

With fully realized synergies earnings per share are expected to increase with approx. SEK 1.70

Georgia-Pacific´s acceptance of this offer is subject to consultations with works councils where appropriate

The transaction will be subject to customary consultation with employee representatives and will also be subject to approval by relevant competition authorities

17 2 December 2011

Binding offer for Georgia-Pacific’s European tissue operations

Binding offer for Georgia-Pacific’s European tissue operations

Creates a leading European tissue company

Strengthens our product offering and geographic reach in Europe

Enhances our presence in key markets

Good strategic fit in AFH tissue

Substantial synergies

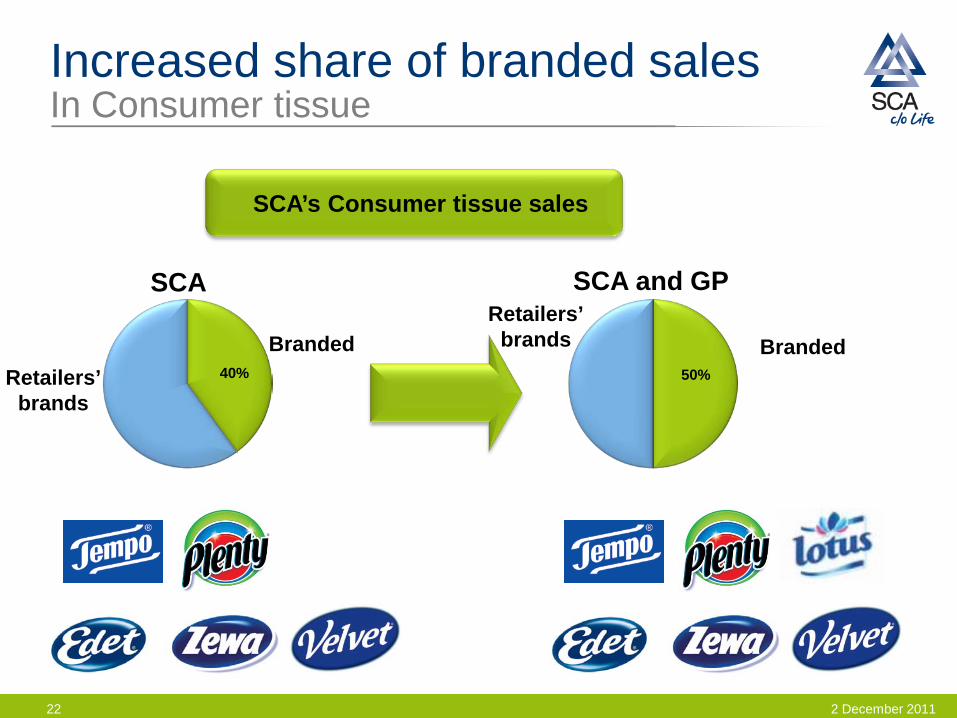

Increased share of branded sales in our consumer tissue portfolio

18 2 December 2011

Sales: EUR 1.25bn* Consumer tissue, approx. 60% AFH tissue, approx. 30% Personal care, approx. 5%

EBIT margins on similar level as SCA’s tissue business Market positions

Consumer tissue, 11% market share AFH tissue, 10% market share

Well-known Lotus brand for AFH tissue and consumer tissue

Approx. 5,000 employees

15 manufacturing sites in 7 countries

670,000 tonnes annual tissue capacity

Georgia-Pacific’s European tissue operations

19 2 December 2011

* Italy and Turkey are not included in the binding offer

Substantial synergies

Annual synergies: EUR 125m

Improves Tissue EBIT margins by 2-2.5 percentage points

Full effect in 3 years after closing

Related costs: EUR 130m

Increased supply chain efficiency Optimization of logistics

More efficient sourcing

Improved SG&A and A&P efficiency

20 2 December 2011

25%

Enhances SCA’s presence In both Consumer tissue and AFH tissue

35%

European Consumer tissue market

European AFH tissue market

SCA

SCA and GP

19% 30% SCA

SCA and GP

21 2 December 2011

Increased share of branded sales In Consumer tissue

SCA’s Consumer tissue sales

40% 50%

Branded

Branded

SCA

SCA and GP

22

Retailers’ brands

Retailers’ brands

2 December 2011

Q & A

2 December 2011 23

24 2 December 2011

Johan Karlsson, VP Investor Relations Tel: +46 8 788 51 30

Jessica Ölvestad, Manager Investor Relations Tel: +46 8 788 52 82

IR Contacts:

Email: [email protected] Website: www.sca.com