Download - Guide To Your USAA Mutual Fund Forms 1099

Guide To Your USAA Investment Management Company Mutual Fund Forms 1099 For Tax Year 2018

We are committed to providing accuracy in reporting tax information related to your USAA mutual fund account(s) and help in understanding how it is used.

In this guide you will find helpful information regarding your USAA mutual fund account including a general overview of:

• tax reporting requirements.

• methods used to determine reported income from your investments.

• the way the IRS treats income on your investments.

• descriptions and explanations of tax forms related to your investments.

If applicable to your USAA mutual fund account, you may have received form(s) 1099-DIV and 1099-B.

The information provided here is not legal or tax advice. We recommend that you consult your legal and tax advisors if you need advice regarding your specific situation.

If a tax advisor prepares your income tax return, we encourage you to include the instructions for recipient when providing copies of your form(s) 1099.

Tax Return Assistance on usaa.com

From the usaa.com home page, navigate to My Tools and select View Documents under the Documents & Forms category to sign up to receive your tax forms electronically in the future.

In addition to the information in this guide, on usaa.com/taxes you may:

• view and print your USAA form(s) 1099.

• learn how to download Form 1099 information into TurboTax®.

• receive a discount on your Federal filing using TurboTax® online.

• read articles on recent tax law changes.

• access other tools and information to answer general tax questions and help you complete your tax return.

• link to IRS publications and forms.

1

TurboTax is a registered trademark, and TurboTax Online is a service mark of Intuit Inc. They are used with permission. This document is not legal, tax, or investment advice. Consult your tax and legal advisers regarding your specific situation.

2

I. Form 1099-DIV ..................................................................................................................................................... Page 3

a. What is it? ......................................................................................................................................................... Page 3

b. Who receives it? .............................................................................................................................................. Page 3

c. Where is it reported? ..................................................................................................................................... Page 3

d. Ordinary Dividends .........................................................................................................................................Page 4

e. Qualified Dividend Income ............................................................................................................................Page 6

f. Short-Term Captial Gains ............................................................................................................................... Page 7

g. Schedule D ........................................................................................................................................................Page 8

h. Long-Term Capital Gains ................................................................................................................................Page 8

i. Unrecaptured Section 1250 Gain .................................................................................................................Page 9

j. Nontaxable Distributions ............................................................................................................................. Page 10

II. Understanding Your IRS Form 1099-B ...........................................................................................................Page 1 1

a. Reporting Your Trading Activity .................................................................................................................Page 15

b. Reporting a Wash Sale .................................................................................................................................Page 17

Mutual Fund 1099 Guide – Table of Contents

Form 1099-DIV

3

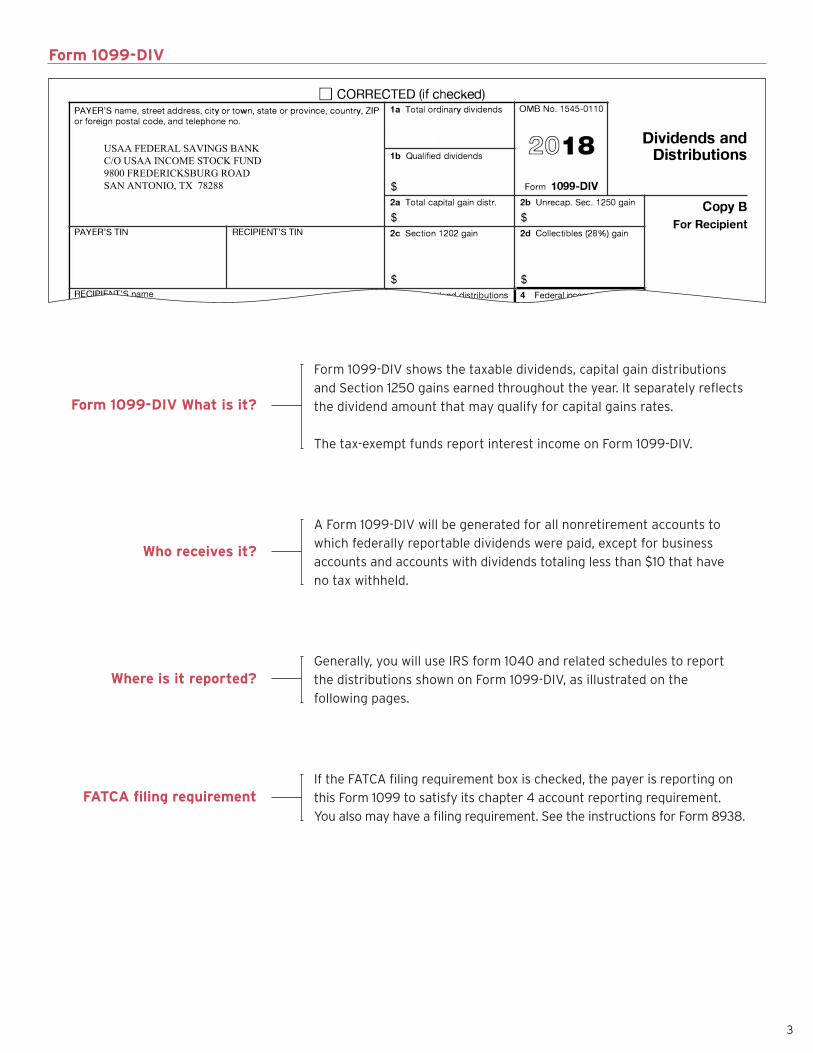

Form 1099-DIV What is it?

Form 1099-DIV shows the taxable dividends, capital gain distributions

and Section 1250 gains earned throughout the year. It separately reflects

the dividend amount that may qualify for capital gains rates.

The tax-exempt funds report interest income on Form 1099-DIV.

Where is it reported?Generally, you will use IRS form 1040 and related schedules to report

the distributions shown on Form 1099-DIV, as illustrated on the

following pages.

FATCA filing requirementIf the FATCA filing requirement box is checked, the payer is reporting on

this Form 1099 to satisfy its chapter 4 account reporting requirement.

You also may have a filing requirement. See the instructions for Form 8938.

Who receives it?

A Form 1099-DIV will be generated for all nonretirement accounts to

which federally reportable dividends were paid, except for business

accounts and accounts with dividends totaling less than $10 that have

no tax withheld.

□ CORRECTED (if checked)PAYER'S name, street address, city or town, state or province, country, ZIP 1a Total ordinary dividends 0MB No. 1545-0110 or foreign postal code, and telephone no.

$ �@18 Dividends and 1b Qualified dividends Distributions

$ Form 1099-DIV 2a Total capital gain distr. 2b Unrecap. Sec. 1250 gain CopyB $ $ For Recipient

PAYER'S TIN RECIPIENT'S TIN 2c Section 1202 gain 2d Collectibles (28%) gain

$ $ RECIPIENT'S name 3 Nondividend distributions 4 Federal income tax withheld

$ $ This is important tax

information and is 5 Section 199A dividends 6 Investment expenses being furnished to

Street address (including apt. no.) $ $ the IRS. If you are required to file a

7 Foreign tax paid 8 Foreign country or U.S. possession return, a negligence penalty or other

sanction may be City or town, state or province, country, and ZIP or foreign postal code $ imposed on you if

9 Cash liquidation distributions 10 Noncash liquidation distribution, this income is taxable

and the IRS $ $ determines that it has

FATCA filing 11 Exempt-interest dividends 12 Specified private activity not been reported.

requirement bond interest dividends

□ $ $ Account number (see instructions) 13 State 14 State identification no. 15 State tax withheld

$ ----------- --------------------$

Form 1099-DIV (keep for your records) www.irs.gov/Form1099DIV Department of the Treasury - Internal Revenue Service

USAA FEDERAL SAVINGS BANKC/O USAA INCOME STOCK FUND9800 FREDERICKSBURG ROADSAN ANTONIO, TX 78288

4

Ordinary dividends primarily are dividends from individual securities

and the net interest earned from securities in a mutual fund’s portfolio.

These dividends may include net short-term capital gain distributions,

which generally are taxable as ordinary income and are combined

with ordinary dividends on the Form 1099-DIV. The amount is shown

in box 1a .

Ordinary Dividends

Note: Box 1a reflects the total amount of ordinary dividends

distributed and is the amount for which you may owe tax, although

it may be greater than the amount you actually received.

The difference may be due to:

• federal and foreign income taxes withheld (shown in boxes

4 and 6), and/or

• the payment of the $10 fee ($2.50/quarter) for the USAA S&P 500

Index Fund Member Shares

Form 1099-DIV

□ CORRECTED (if checked)PAYER'S name, street address, city or town, state or province, country, ZIP 1a Total ordinary dividends 0MB No. 1545-0110 or foreign postal code, and telephone no.

$ �@18 Dividends and 1b Qualified dividends Distributions

$ Form 1099-DIV 2a Total capital gain distr. 2b Unrecap. Sec. 1250 gain CopyB $ $ For Recipient

PAYER'S TIN RECIPIENT'S TIN 2c Section 1202 gain 2d Collectibles (28%) gain

$ $ RECIPIENT'S name 3 Nondividend distributions 4 Federal income tax withheld

$ $ This is important tax

information and is 5 Section 199A dividends 6 Investment expenses being furnished to

Street address (including apt. no.) $ $ the IRS. If you are required to file a

7 Foreign tax paid 8 Foreign country or U.S. possession return, a negligence penalty or other

sanction may be City or town, state or province, country, and ZIP or foreign postal code $ imposed on you if

9 Cash liquidation distributions 10 Noncash liquidation distribution, this income is taxable

and the IRS $ $ determines that it has

FATCA filing 11 Exempt-interest dividends 12 Specified private activity not been reported.

requirement bond interest dividends

□ $ $ Account number (see instructions) 13 State 14 State identification no. 15 State tax withheld

$ ----------- --------------------$

Form 1099-DIV (keep for your records) www.irs.gov/Form1099DIV Department of the Treasury - Internal Revenue Service

USAA FEDERAL SAVINGS BANKC/O USAA INCOME STOCK FUND9800 FREDERICKSBURG ROADSAN ANTONIO, TX 78288

□ CORRECTED (if checked)PAYER'S name, street address, city or town, state or province, country, ZIP 1a Total ordinary dividends 0MB No. 1545-0110 or foreign postal code, and telephone no.

$ �@18 Dividends and 1b Qualified dividends Distributions

$ Form 1099-DIV 2a Total capital gain distr. 2b Unrecap. Sec. 1250 gain CopyB $ $ For Recipient

PAYER'S TIN RECIPIENT'S TIN 2c Section 1202 gain 2d Collectibles (28%) gain

$ $ RECIPIENT'S name 3 Nondividend distributions 4 Federal income tax withheld

$ $ This is important tax

information and is 5 Section 199A dividends 6 Investment expenses being furnished to

Street address (including apt. no.) $ $ the IRS. If you are required to file a

7 Foreign tax paid 8 Foreign country or U.S. possession return, a negligence penalty or other

sanction may be City or town, state or province, country, and ZIP or foreign postal code $ imposed on you if

9 Cash liquidation distributions 10 Noncash liquidation distribution, this income is taxable

and the IRS $ $ determines that it has

FATCA filing 11 Exempt-interest dividends 12 Specified private activity not been reported.

requirement bond interest dividends

□ $ $ Account number (see instructions) 13 State 14 State identification no. 15 State tax withheld

$ ----------- --------------------$

Form 1099-DIV (keep for your records) www.irs.gov/Form1099DIV Department of the Treasury - Internal Revenue Service

USAA FEDERAL SAVINGS BANKC/O USAA INCOME STOCK FUND9800 FREDERICKSBURG ROADSAN ANTONIO, TX 78288

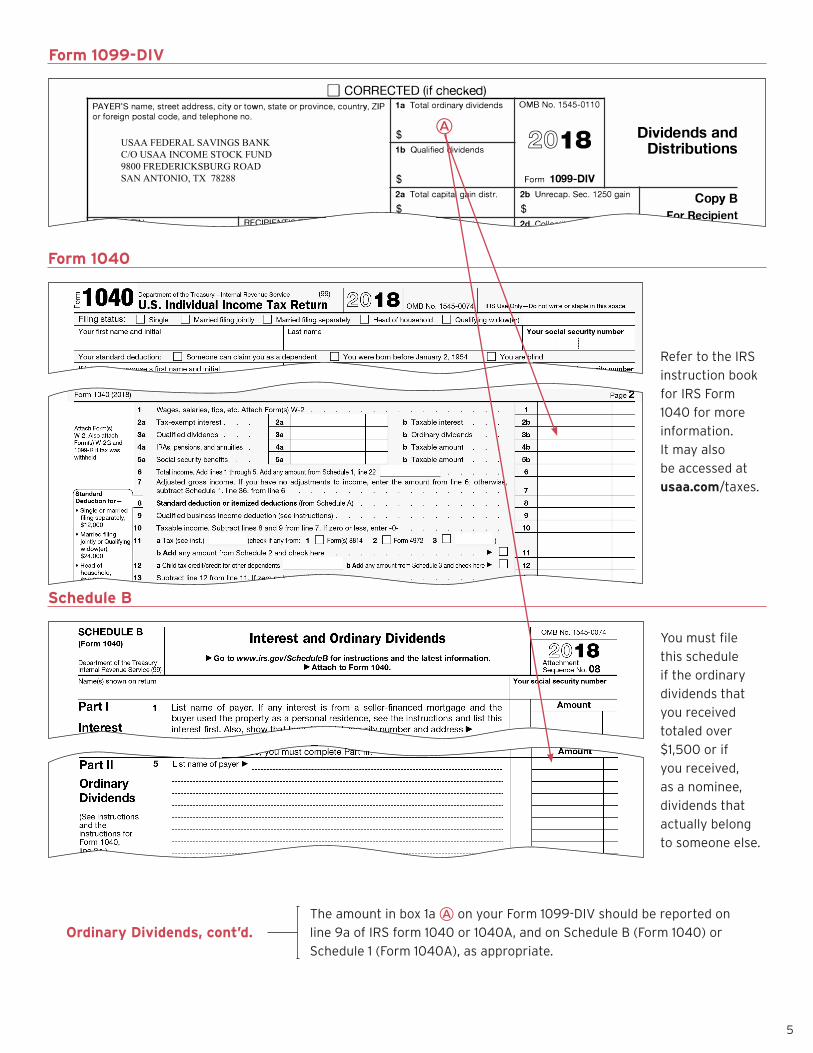

The amount in box 1a on your Form 1099-DIV should be reported on

line 9a of IRS form 1040 or 1040A, and on Schedule B (Form 1040) or

Schedule 1 (Form 1040A), as appropriate.Ordinary Dividends, cont’d.

5

Refer to the IRS

instruction book

for IRS Form

1040 for more

information.

It may also

be accessed at

usaa.com/taxes.

Form 1040

You must file

this schedule

if the ordinary

dividends that

you received

totaled over

$1,500 or if

you received,

as a nominee,

dividends that

actually belong

to someone else.

Schedule B

Form 1099-DIV

□ CORRECTED (if checked)PAYER'S name, street address, city or town, state or province, country, ZIP 1a Total ordinary dividends 0MB No. 1545-0110 or foreign postal code, and telephone no.

$ �@18 Dividends and 1b Qualified dividends Distributions

$ Form 1099-DIV 2a Total capital gain distr. 2b Unrecap. Sec. 1250 gain CopyB $ $ For Recipient

PAYER'S TIN RECIPIENT'S TIN 2c Section 1202 gain 2d Collectibles (28%) gain

$ $ RECIPIENT'S name 3 Nondividend distributions 4 Federal income tax withheld

$ $ This is important tax

information and is 5 Section 199A dividends 6 Investment expenses being furnished to

Street address (including apt. no.) $ $ the IRS. If you are required to file a

7 Foreign tax paid 8 Foreign country or U.S. possession return, a negligence penalty or other

sanction may be City or town, state or province, country, and ZIP or foreign postal code $ imposed on you if

9 Cash liquidation distributions 10 Noncash liquidation distribution, this income is taxable

and the IRS $ $ determines that it has

FATCA filing 11 Exempt-interest dividends 12 Specified private activity not been reported.

requirement bond interest dividends

□ $ $ Account number (see instructions) 13 State 14 State identification no. 15 State tax withheld

$ ----------- --------------------$

Form 1099-DIV (keep for your records) www.irs.gov/Form1099DIV Department of the Treasury - Internal Revenue Service

USAA FEDERAL SAVINGS BANKC/O USAA INCOME STOCK FUND9800 FREDERICKSBURG ROADSAN ANTONIO, TX 78288

Form 1099-DIV

6

The amount in box 1a also includes dividends that may qualify for long-

term capital gains tax rates. This is known as qualified dividend income.

Box 1b B on your Form 1099-DIV separately shows the portion of the

amount in box 1a that may be eligible for the lower tax rates. Report the

eligible amount on line 3a of form 1040.

Tax law specifically prohibits applying the reduced tax rate to certain

dividends, such as dividend distributions from money market or bond

mutual funds. These dividends are not included in box 1b. See IRS

Publication 550 (Investment Income and Expenses) for more information

about restrictions and exclusions.

An amount shown in box 1b may be ineligible for long-term capital gains

rates if the required holding period was not met. You must have held

your shares for 61 days during a 121-day holding period that began

60 days before the fund’s ex-dividend date. This determination is your

responsibility. IRS instructions for forms 1040 and 1040A include

an example.

Qualified Dividend Income

Form 1040

B

Form 1099-DIV

7

Short-term capital gains from mutual funds are net gains from the

sale of securities held by the fund for one year or less and generally

will be subject to ordinary tax rates. The amount is reflected in the

box labeled “Short-Term Capital Gains” C and also is combined with

ordinary dividends in box 1a . See “Ordinary Dividends” on page 4

for an illustration of how the amount in box 1a is to be reported.

Short-Term Capital Gains

Note: Some funds that generate tax-exempt income may also

distribute taxable short-term capital gains, which are shown on

Form 1099-DIV.

C

□ CORRECTED (if checked)PAYER'S name, street address, city or town, state or province, country, ZIP 1a Total ordinary dividends 0MB No. 1545-0110 or foreign postal code, and telephone no.

$ �@18 Dividends and 1b Qualified dividends Distributions

$ Form 1099-DIV 2a Total capital gain distr. 2b Unrecap. Sec. 1250 gain CopyB $ $ For Recipient

PAYER'S TIN RECIPIENT'S TIN 2c Section 1202 gain 2d Collectibles (28%) gain

$ $ RECIPIENT'S name 3 Nondividend distributions 4 Federal income tax withheld

$ $ This is important tax

information and is 5 Section 199A dividends 6 Investment expenses being furnished to

Street address (including apt. no.) $ $ the IRS. If you are required to file a

7 Foreign tax paid 8 Foreign country or U.S. possession return, a negligence penalty or other

sanction may be City or town, state or province, country, and ZIP or foreign postal code $ imposed on you if

9 Cash liquidation distributions 10 Noncash liquidation distribution, this income is taxable

and the IRS $ $ determines that it has

FATCA filing 11 Exempt-interest dividends 12 Specified private activity not been reported.

requirement bond interest dividends

□ $ $ Account number (see instructions) 13 State 14 State identification no. 15 State tax withheld

$ ----------- --------------------$

Form 1099-DIV (keep for your records) www.irs.gov/Form1099DIV Department of the Treasury - Internal Revenue Service

USAA FEDERAL SAVINGS BANKC/O USAA INCOME STOCK FUND9800 FREDERICKSBURG ROADSAN ANTONIO, TX 78288

Schedule D

8

Long-term capital gains are net gains from the sale of securities held

by the fund for more than one year. Long-term capital gains are shown

in box 2a D, and you should report them on line 13 of Schedule D

(Form 1040), or on line 13 of Form 1040 (line 10 of Form 1040A).

Long-Term Capital Gains

Note: Some funds that generate tax-exempt income may also distribute

taxable long-term capital gains, which are shown on Form 1099-DIV.

Form 1099-DIV

You must use

this schedule to

report capital

gains and losses

not reported

directly on IRS

Form 1040, line

13. For additional

information see

IRS Publication

550 and

Schedule D

instructions.

D

□ CORRECTED (if checked)PAYER'S name, street address, city or town, state or province, country, ZIP 1a Total ordinary dividends 0MB No. 1545-0110 or foreign postal code, and telephone no.

$ �@18 Dividends and 1b Qualified dividends Distributions

$ Form 1099-DIV 2a Total capital gain distr. 2b Unrecap. Sec. 1250 gain CopyB $ $ For Recipient

PAYER'S TIN RECIPIENT'S TIN 2c Section 1202 gain 2d Collectibles (28%) gain

$ $ RECIPIENT'S name 3 Nondividend distributions 4 Federal income tax withheld

$ $ This is important tax

information and is 5 Section 199A dividends 6 Investment expenses being furnished to

Street address (including apt. no.) $ $ the IRS. If you are required to file a

7 Foreign tax paid 8 Foreign country or U.S. possession return, a negligence penalty or other

sanction may be City or town, state or province, country, and ZIP or foreign postal code $ imposed on you if

9 Cash liquidation distributions 10 Noncash liquidation distribution, this income is taxable

and the IRS $ $ determines that it has

FATCA filing 11 Exempt-interest dividends 12 Specified private activity not been reported.

requirement bond interest dividends

□ $ $ Account number (see instructions) 13 State 14 State identification no. 15 State tax withheld

$ ----------- --------------------$

Form 1099-DIV (keep for your records) www.irs.gov/Form1099DIV Department of the Treasury - Internal Revenue Service

USAA FEDERAL SAVINGS BANKC/O USAA INCOME STOCK FUND9800 FREDERICKSBURG ROADSAN ANTONIO, TX 78288

Form 1099-DIV

9

Box 2b E shows the portion of the amount in box 2a that is

“Unrecaptured Section 1250 Gain,” taxed at a rate of up to 25%.

Include this amount on line 11 of the worksheet on page D-9

of the instructions for Form 1040 Schedule D.

Unrecaptured Section 1250 Gain

E

□ CORRECTED (if checked)PAYER'S name, street address, city or town, state or province, country, ZIP 1a Total ordinary dividends 0MB No. 1545-0110 or foreign postal code, and telephone no.

$ �@18 Dividends and 1b Qualified dividends Distributions

$ Form 1099-DIV 2a Total capital gain distr. 2b Unrecap. Sec. 1250 gain CopyB $ $ For Recipient

PAYER'S TIN RECIPIENT'S TIN 2c Section 1202 gain 2d Collectibles (28%) gain

$ $ RECIPIENT'S name 3 Nondividend distributions 4 Federal income tax withheld

$ $ This is important tax

information and is 5 Section 199A dividends 6 Investment expenses being furnished to

Street address (including apt. no.) $ $ the IRS. If you are required to file a

7 Foreign tax paid 8 Foreign country or U.S. possession return, a negligence penalty or other

sanction may be City or town, state or province, country, and ZIP or foreign postal code $ imposed on you if

9 Cash liquidation distributions 10 Noncash liquidation distribution, this income is taxable

and the IRS $ $ determines that it has

FATCA filing 11 Exempt-interest dividends 12 Specified private activity not been reported.

requirement bond interest dividends

□ $ $ Account number (see instructions) 13 State 14 State identification no. 15 State tax withheld

$ ----------- --------------------$

Form 1099-DIV (keep for your records) www.irs.gov/Form1099DIV Department of the Treasury - Internal Revenue Service

USAA FEDERAL SAVINGS BANKC/O USAA INCOME STOCK FUND9800 FREDERICKSBURG ROADSAN ANTONIO, TX 78288

Form 1099-DIV Box 3

10

Non-Dividend distributions Box 3 this amount represents a return

of capital. If you received a Non Dividend distribution from a USAA

Mutual Fund, USAA will adjust (reduce) your cost basis, if applicable.

Non-Dividend Distributions

Understanding Your IRS Form 1099-B

11

IRS Form 1099-B Proceeds from Brokers and Barter Exchange Transactions

The amounts indicated in this section of your Tax Information Statement reflects proceeds and basis-related information (when available) from security transactions such as sales, redemptions, tender offer,

maturities, etc.

Trade Date versus Settlement Date

We report sales of USAA Mutual Funds to the IRS, on a trade date basis, on IRS Form 1099-B.

Accordingly, you should report transactions on a trade date basis.

Explanation of Information Presented on IRS Form 1099-B for USAA Mutual Funds

The IRS Form 1099B includes sections that include a summary page, income tax withheld and trading activity.

Summary of Gains and Losses

These amounts are for informational purposes. Cost basis totals include only amounts that were available

to us. Refer to the appropriate detail pages for more information regarding your redemption activity.

Income Tax Withheld from any redemption activity will be reflected here.

Trading activity

This section is broken up into four categories:

( 1 ) Category A – short-term covered securities where basis is reported to the IRS. (2) Category B – short-term noncovered securities where basis is NOT reported to the IRS. (3) Category D – long-term covered securities where basis is reported to the IRS. (4) Category E – long-term noncovered securities where basis is NOT reported to the IRS.

This document is not legal, tax, or investment advice. Consult your tax and legal advisers regarding your specific situation.

12

Understanding Your IRS Form 1099-B (con’t)

Category A – Short-term cost basis reported to the IRS

Category B – Short-term cost basis NOT reported to the IRS

These are your “noncovered” security trades, representing securities that were purchased before 2012

and subsequently sold. USAA provides the cost basis information (if available) for noncovered transactions

on IRS Form 1099-B for your information only. For noncovered securities, USAA will not report basis

information to the IRS.

This category is divided into two sections: one for positions with complete basis information and one for

transactions with missing basis information.

For some mutual fund transactions, where the date of acquisition is “unknown” or “various”, you should refer to

your historical documents to determine if the transaction’s holding period qualifies as long-term or short-term.

Missing basis information

UNDETERMINED HOLDING PERIOD Report on Form 8949, either Part I with Box B checked or Part II with Box E checked

la - Fund Name/ CUSIP /Symbol/ Account Nr

le - Date sold or disposed

Quantity sold l d - Proceeds

USAA INCOME FUND / CUSIP: 903288207 / Symbol: USAIX / Account#:

21.949 $291.0403/04/18 Unknown

Fund Total 21.949 $291.04

5 - Tax lots: NONCOVERED

Unknown $0.00

Unknown $0.00

2) LONG-TERM GAINS AND LOSSES - Cost basis is reported to the IRSReport on Form 8949, Part II, with Box D checked

la - Fund Name/ CUSIP /Symbol/ Account Nr

le - Date sold or Quantity lb - Date disposed sold l d - Proceeds acquired

USAA INCOME FUND / CUSIP: 903288207 / Symbol: USAIX / Account#:

03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18 03/04/18

Fund Total

1••••��•• ��y�r��• ��t�I

0.019 0.066 0.063 0.076 0.066 0.066 0.069 0.064 0.068 0.068 0.057 0.114 0.019 0.065 0.067 0.065 0.077 0.067 0.070 0.072 0.070 0.072 0.073 0.066 0.008 0.182 0.050 0.071

1.890

$0.25 01/27 /12 $0.88 03/28/12 $0.84 04/26/12 $1.01 05/29/12 $0.87 06/27 /12 $0.88 07 /27 /12 $0.91 08/29/12 $0.85 09/26/12 $0.90 10/31/12 $0.90 11/28/12 $0.76 12/07 /12 $1.51 12/18/12 $0.25 01/29/13 $0.86 02/26/13 $0.89 03/27 /13 $0.86 04/26/13 $1.02 05/29/13 $0.89 06/26/13 $0.93 02/27 /12 $0.95 07 /29/13 $0.93 08/28/13 $0.95 09/26/13 $0.97 10/29/13 $0.88 11/26/13 $0.11 12/06/13 $2.41 12/17 /13 $0.66 01/29/14 $0.94 02/26/14

$25.06

$ZS/06

3 - Tax lots: COVERED

le - Cost or lg - Wash Sale other basis Loss Disallowed

$0.25 $0.00 $0.00 $0.88 $0.00 $0.00 $0.84 $0.00 $0.00 $1.01 $0.00 $0.00 $0.88 $0.00 $(0.01) $0.88 $0.00 $0.00 $0.92 $0.00 $(0.01) $0.85 $0.00 $0.00 $0.90 $0.00 $0.00 $0.90 $0.00 $0.00 $0.76 $0.00 $0.00 $1.51 $0.00 $0.00 $0.25 $0.00 $0.00 $0.86 $0.00 $0.00 $0.89 $0.00 $0.00 $0.86 $0.00 $0.00 $1.02 $0.00 $0.00 $0.89 $0.00 $0.00 $0.93 $0.00 $0.00 $0.96 $0.00 $(0.01) $0.93 $0.00 $0.00 $0.96 $0.00 $(0.01) $0.97 $0.00 $0.00 $0.88 $0.00 $0.00 $0.11 $0.00 $0.00 $2.41 $0.00 $0.00 $0.66 $0.00 $0.00 $0.94 $0.00 $0.00

$25.10 $0.00 $(0.04)

$ZS.JO $().()() $(<f,94)

Category D – Long-term cost basis reported to the IRS

Category E – Long-term cost basis NOT reported to the IRS

These are your “noncovered” security trades, representing securities that were purchased before 2012

and subsequently sold. USAA provides the cost basis information (if available) for noncovered transactions

on IRS Form 1099-B for your information only. For noncovered securities, USAA will not report basis

information to the IRS.

This category is divided into two sections: one for positions with complete basis information and one for

transactions with missing basis information.

Understanding Your IRS Form 1099-B (con’t)

13

For some mutual fund transactions, where the date of acquisition is “unknown” or “various”, you should refer to

your historical documents to determine if the transaction’s holding period qualifies as long-term or short-term.

Missing basis information

UNDETERMINED HOLDING PERIOD Report on Form 8949, either Part I with Box B checked or Part II with Box E checked

la - Fund Name/ CUSIP /Symbol/ Account Nr

le - Datesold or disposed

Quantity sold l d - Proceeds

USAA INCOME FUND / CUSIP: 903288207 / Symbol: USAIX / Account#:

21.949 $291.04 Unknown

21.949 $291.04

03/04/18

Fund Total

I Undetermined Total

5 - Tax lots: NONCOVERED

Unknown $0.00

Unknown $0.00

$().()()

1 4

Each page includes a number of columns displaying details related to each transaction.

Date Sold or Disposed - Transactions are reported by trade date and each is reported separately to the IRS.

Accordingly, you should report each transaction separately on your tax return to avoid a mismatch with the IRS.

Quantity Sold - This amount represents the number of shares sold.

Proceeds - Gross proceeds of sale.

Date Acquired - This represents the date you acquired the shares and is used to determine your holding period

for the purpose of determining short-term or long-term classification. Investments that were held for more than

a 12-month period qualify as long-term.

Note: For mutual funds purchased before 2012, the only tax accounting method available with USAA is average

cost. Please consult your tax advisor before using this or another permissible method.

Gain or Loss - This represents the difference between the transactions proceeds and your cost or other basis.

An exception to this rule occurs when the transaction was involved in a wash sale causing a loss deferral.

Reporting your holding Period

Date Acquired - This is used to determine your holding period for the purpose of determining short-term

or long-term classification. Investments that were held for more than a 12-month period qualify as long-term.

In the event your exact purchase date is not available, the 1099B will reflect:

“Various” - The exact date of each purchase is not known, but basis information is available. You will need

to use your statements to determine how many of the shares sold were held for more or less than one year.

“Unknown” - USAA does not know the cost basis information on shares sold. You should refer to historical

statements to determine cost basis information and if you cannot obtain the data needed, you should seek

professional tax advice to determine how to report your cost basis information to the IRS.

Understanding Your IRS Form 1099-B

15

IRS Form 8949

2) SHORT-TERM GAINS AND LOSSES - Cost basis is reported to the IRSReport on Form 8949, Part I, with Box A checked

la - Fund Name/ CUSIP / Symbol / Account Nr

le - Date sold or disposed

Quantity sold Id - Proceeds

lb - Date acquired

le - Cost or lg - Adjustments other basis If - Code, if Any (W

USAA AGGRESSIVE GROWTH FUND / CUSIP: 903288405 / Symbol: USAUX / Account #: 0038-38902688338

01/03/18

Fund Total

I ST Covered Total

0.0500.0071.893

1.950

$1.98$0.28

$75.09

$77.35

12/06/17 $1.87$0.26

$70.98

$73.11

$0.00$0.00$0.00

$0.00

$0.11$0.02$4.11

$4.24

3 - Tax lots: COVERED

01/03/18 01/03/18

12/06/17 12/11/17

Even though your IRS Form 1099-B has a gain or loss figure, do not enter a gain or loss figure on IRS Form 8949. This will be determined when recapped on Schedule D. The final column on IRS Form 8949 is reserved for any adjustments to your cost basis, such as a disallowed loss due to a wash sale transaction.

Beginning for tax year 201 1 , trading activity is reported to the IRS using IRS Form 8949, Sales and Other Dispositions of Capital Assets. Totals from this form are entered on the newly revised Schedule D, Capital Gains and Losses. A separate version of IRS Form 8949 will need to be completed for the different transaction types:

To assist you with your tax preparation our 1099-B design includes a Supplemental Information section that presents a Summary of Gains and Losses summing up the totals of these four categories. NOTE: USAA does not report carryover losses to the IRS.

Reporting your

trading activity

• Category A, short-term covered mutual funds where basis is reported to the IRS.

• Category B, short-term noncovered mutual funds where basis is NOT reported to the IRS.

• Category D, long-term covered mutual funds where basis is reported to the IRS.

• Category E, long-term noncovered mutual funds where basis is NOT reported to the IRS.

Form 8949Department of the Treasury Internal Revenue Service

Sales and Other Dispositions of Capital Assets▶ Go to www.irs.gov/Form8949 for instructions and the latest information.

▶ File with your Schedule D to list your transactions for lines 1b, 2, 3, 8b, 9, and 10 of Schedule D.

OMB No. 1545-0074

2018Attachment Sequence No. 12A

Name(s) shown on return Social security number or taxpayer identification number

Before you check Box A, B, or C below, see whether you received any Form(s) 1099-B or substitute statement(s) from your broker. A substitute statement will have the same information as Form 1099-B. Either will show whether your basis (usually your cost) was reported to the IRS by your broker and may even tell you which box to check.

Part I Short-Term. Transactions involving capital assets you held 1 year or less are generally short-term (see instructions). For long-term transactions, see page 2. Note: You may aggregate all short-term transactions reported on Form(s) 1099-B showing basis was reported to the IRS and for which no adjustments or codes are required. Enter the totals directly on Schedule D, line 1a; you aren’t required to report these transactions on Form 8949 (see instructions).

You must check Box A, B, or C below. Check only one box. If more than one box applies for your short-term transactions, complete a separate Form 8949, page 1, for each applicable box. If you have more short-term transactions than will fit on this page for one or more of the boxes, complete as many forms with the same box checked as you need.

(A) Short-term transactions reported on Form(s) 1099-B showing basis was reported to the IRS (see Note above)(B) Short-term transactions reported on Form(s) 1099-B showing basis wasn’t reported to the IRS(C) Short-term transactions not reported to you on Form 1099-B

1

(a) Description of property

(Example: 100 sh. XYZ Co.)

(b) Date acquired (Mo., day, yr.)

(c) Date sold or disposed of

(Mo., day, yr.)

(d) Proceeds

(sales price) (see instructions)

(e) Cost or other basis. See the Note below and see Column (e)

in the separate instructions

Adjustment, if any, to gain or loss. If you enter an amount in column (g),

enter a code in column (f). See the separate instructions.

(f) Code(s) from instructions

(g) Amount of adjustment

(h) Gain or (loss).

Subtract column (e) from column (d) and combine the result

with column (g)

2

Totals. Add the amounts in columns (d), (e), (g), and (h) (subtract negative amounts). Enter each total here and include on your Schedule D, line 1b (if Box A above is checked), line 2 (if Box B above is checked), or line 3 (if Box C above is checked) ▶

Note: If you checked Box A above but the basis reported to the IRS was incorrect, enter in column (e) the basis as reported to the IRS, and enter an adjustment in column (g) to correct the basis. See Column (g) in the separate instructions for how to figure the amount of the adjustment.

For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 37768Z Form 8949 (2018)

16

IRS Form 8949 (con’t.)

Form 8949Department of the Treasury Internal Revenue Service

Sales and Other Dispositions of Capital Assets▶ Go to www.irs.gov/Form8949 for instructions and the latest information.

▶ File with your Schedule D to list your transactions for lines 1b, 2, 3, 8b, 9, and 10 of Schedule D.

OMB No. 1545-0074

2018Attachment Sequence No. 12A

Name(s) shown on return Social security number or taxpayer identification number

Before you check Box A, B, or C below, see whether you received any Form(s) 1099-B or substitute statement(s) from your broker. A substitute statement will have the same information as Form 1099-B. Either will show whether your basis (usually your cost) was reported to the IRS by your broker and may even tell you which box to check.

Part I Short-Term. Transactions involving capital assets you held 1 year or less are generally short-term (see instructions). For long-term transactions, see page 2. Note: You may aggregate all short-term transactions reported on Form(s) 1099-B showing basis was reported to the IRS and for which no adjustments or codes are required. Enter the totals directly on Schedule D, line 1a; you aren’t required to report these transactions on Form 8949 (see instructions).

You must check Box A, B, or C below. Check only one box. If more than one box applies for your short-term transactions, complete a separate Form 8949, page 1, for each applicable box. If you have more short-term transactions than will fit on this page for one or more of the boxes, complete as many forms with the same box checked as you need.

(A) Short-term transactions reported on Form(s) 1099-B showing basis was reported to the IRS (see Note above)(B) Short-term transactions reported on Form(s) 1099-B showing basis wasn’t reported to the IRS(C) Short-term transactions not reported to you on Form 1099-B

1

(a) Description of property

(Example: 100 sh. XYZ Co.)

(b) Date acquired (Mo., day, yr.)

(c) Date sold or disposed of

(Mo., day, yr.)

(d) Proceeds

(sales price) (see instructions)

(e) Cost or other basis. See the Note below and see Column (e)

in the separate instructions

Adjustment, if any, to gain or loss. If you enter an amount in column (g),

enter a code in column (f). See the separate instructions.

(f) Code(s) from instructions

(g) Amount of adjustment

(h) Gain or (loss).

Subtract column (e) from column (d) and combine the result

with column (g)

2

Totals. Add the amounts in columns (d), (e), (g), and (h) (subtract negative amounts). Enter each total here and include on your Schedule D, line 1b (if Box A above is checked), line 2 (if Box B above is checked), or line 3 (if Box C above is checked) ▶

Note: If you checked Box A above but the basis reported to the IRS was incorrect, enter in column (e) the basis as reported to the IRS, and enter an adjustment in column (g) to correct the basis. See Column (g) in the separate instructions for how to figure the amount of the adjustment.

For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 37768Z Form 8949 (2018)

Form 8949Department of the Treasury Internal Revenue Service

Sales and Other Dispositions of Capital Assets▶ Go to www.irs.gov/Form8949 for instructions and the latest information.

▶ File with your Schedule D to list your transactions for lines 1b, 2, 3, 8b, 9, and 10 of Schedule D.

OMB No. 1545-0074

2018Attachment Sequence No. 12A

Name(s) shown on return Social security number or taxpayer identification number

Before you check Box A, B, or C below, see whether you received any Form(s) 1099-B or substitute statement(s) from your broker. A substitute statement will have the same information as Form 1099-B. Either will show whether your basis (usually your cost) was reported to the IRS by your broker and may even tell you which box to check.

Part I Short-Term. Transactions involving capital assets you held 1 year or less are generally short-term (see instructions). For long-term transactions, see page 2. Note: You may aggregate all short-term transactions reported on Form(s) 1099-B showing basis was reported to the IRS and for which no adjustments or codes are required. Enter the totals directly on Schedule D, line 1a; you aren’t required to report these transactions on Form 8949 (see instructions).

You must check Box A, B, or C below. Check only one box. If more than one box applies for your short-term transactions, complete a separate Form 8949, page 1, for each applicable box. If you have more short-term transactions than will fit on this page for one or more of the boxes, complete as many forms with the same box checked as you need.

(A) Short-term transactions reported on Form(s) 1099-B showing basis was reported to the IRS (see Note above)(B) Short-term transactions reported on Form(s) 1099-B showing basis wasn’t reported to the IRS(C) Short-term transactions not reported to you on Form 1099-B

1

(a) Description of property

(Example: 100 sh. XYZ Co.)

(b) Date acquired (Mo., day, yr.)

(c) Date sold or disposed of

(Mo., day, yr.)

(d) Proceeds

(sales price) (see instructions)

(e) Cost or other basis. See the Note below and see Column (e)

in the separate instructions

Adjustment, if any, to gain or loss. If you enter an amount in column (g),

enter a code in column (f). See the separate instructions.

(f) Code(s) from instructions

(g) Amount of adjustment

(h) Gain or (loss).

Subtract column (e) from column (d) and combine the result

with column (g)

2

Totals. Add the amounts in columns (d), (e), (g), and (h) (subtract negative amounts). Enter each total here and include on your Schedule D, line 1b (if Box A above is checked), line 2 (if Box B above is checked), or line 3 (if Box C above is checked) ▶

Note: If you checked Box A above but the basis reported to the IRS was incorrect, enter in column (e) the basis as reported to the IRS, and enter an adjustment in column (g) to correct the basis. See Column (g) in the separate instructions for how to figure the amount of the adjustment.

For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 37768Z Form 8949 (2018)

Once you have completed IRS Form 8949, the column totals are then entered onto a Schedule D which is where

you will find your net gain or loss information.

17

Reporting a Wash Sale

Once you have completed IRS Form 8949, the column totals are entered into a Schedule D and when you combine the columns to determine your gain or loss, your allowable loss (if any) will be reflected in column (h).

A wash sale occurs when you sell an investment at a loss, and repurchase a substantially identical investment with a 61-day period that extends from 30 days before the sale until 30 days after the sale. Losses from wash sales are generally not deductible. Instead, the loss is added to the cost basis of the replacement shares. When a wash sale occurs, the net amount of your proceeds and cost basis figures will not equal the amount in the gain or loss column in the amount of the disallowed loss.

Example of

Form 1099-B

with a wash

sale loss

disallowed

18

The Average Cost Basis accounting method simply totals the cost

basis of an entire position and divides it by the number of shares

to determine an average cost per share.

Historically, USAA maintained cost basis for mutual funds using the

Average Cost Basis (ACB) accounting method. If you have previously

sold shares and used another cost basis method on your tax return,

then our records will be different from yours. You are still permitted to

select an alternate method to average cost when filing your tax return.

However, we will only display the average cost for noncovered shares.

Average Cost Basis

In General, the average cost method is only one of several methods

available to determine gains and losses when you sell or exchange

mutual fund shares. Before using the information for tax reporting

purposes, consult your tax advisor to ensure that the average cost

basis is appropriate given your specific tax situation. For additional

information refer to IRS Publication 564, Mutual Fund Distributions.

Reporting Cost Basis using Average Cost

For shares received as a gift, inheritance, or other form of transfer,

special basis determination rules, other than average cost of shares,

will apply. IRS Publication 551, Basis of Assets, provides instructions

on how to calculate the basis of shares received. Please consult your

tax advisor for assistance in calculating your basis in these situations.

Gifted, Inherited or Other Transferred shares

Reporting a Wash Sale (con’t.)

For more information regarding cost basis for mutual funds, visit usaa.com/taxes.

USAA means United Services Automobile Association and its insurance, banking, investment and other companies. Banks Member FDIC. Investments provided by USAA Investment Management Company and USAA Financial Advisors Inc., both registered broker dealers.

The contents of this document is not intended to be, and is not, legal or tax advice. The applicable tax law is complex, the penalties for non-compliance are severe, and the applicable tax law of your state may differ from federal tax law. Therefore, you should consult your tax and legal advisers regarding your specific situation.

33576-0319

For more information regarding your USAA Tax Documents, please visit usaa.com/taxes or contact one of our Member

Service Representatives at 800-531-6347. Questions regarding your specific tax situation should be directed to your

tax and legal advisers.