Tehran

31 May 2015

Angelo TantazziUniversity of Bologna and Prometeia

Financial stability and regulatory compliance in Europe

25° Annual Conference on Monetary and Exchange Rate Policies

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 2

this document is the basis of an oral presentation, without which it is

incomplete and can give rise to misunderstandings

any partial or total reproduction of its content is prohibited without written

consent by Prometeia

copyright © 2015 Prometeia

disclaimer

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 3

agenda 1 | the banking system at the outbreak of

the financial crisis

2 | new regulation to preserve financial

stability

3 | supervision and regulatory uncertainty

4 | the development of risk management

expertise in financial institutions

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 4

1 | the banking system at the outbreak of

the financial crisis

new regulation to preserve financial stability

supervision and regulatory uncertainty

the development of risk management expertise in financial

institutions

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 5

EMU banking sector | asset size almost doubled in 10 yearstotal assets of MFIs/ GDPtotal assets of MFIs in EMU

source: Prometeia calculations on Ecb data

€T

RIL

LIO

NS

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 6

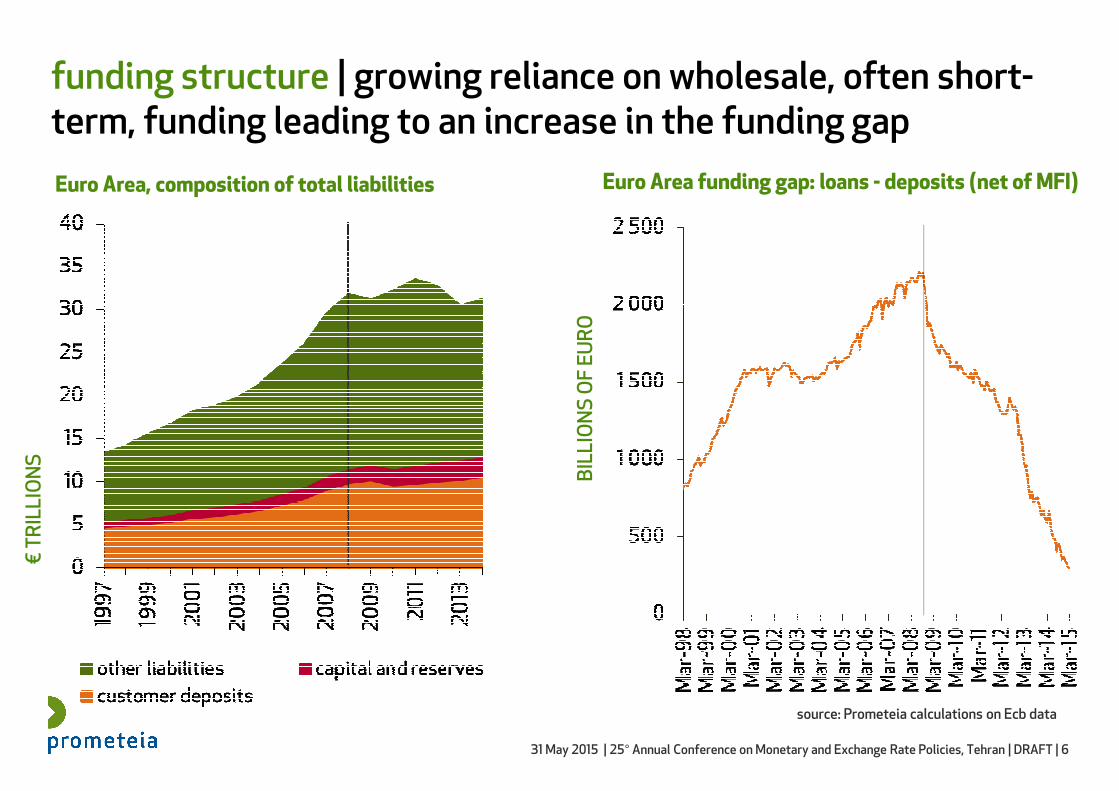

funding structure | growing reliance on wholesale, often short-term, funding leading to an increase in the funding gap

source: Prometeia calculations on Ecb data

Euro Area, composition of total liabilities Euro Area funding gap: loans - deposits (net of MFI)

BIL

LIO

NS

OF

EU

RO

€T

RIL

LIO

NS

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 7

wholesale funding I with the sovereign debt crisis external funding dropped dramatically

as %

of

MM

F’s

AU

M

as %

of

MM

F’s

AU

M

Money Market Funds exposure to European Bank CDs, CP, Repos and other

external liabilities in % of total assets

% %

source: Prometeia calculations on Ecb data source: Fitch Ratings, MMF public Web sites, SEC filings, Prometeia calculations; data at 05/09/’13

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 8

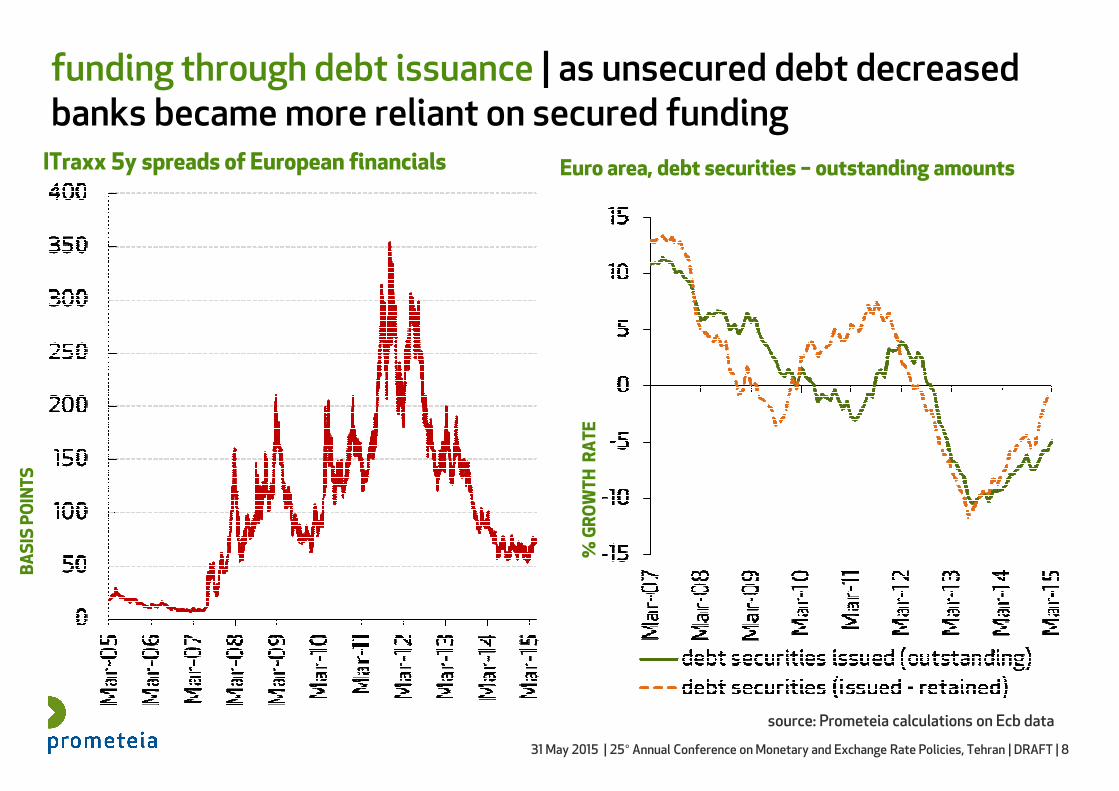

funding through debt issuance | as unsecured debt decreased banks became more reliant on secured funding

Euro area, debt securities – outstanding amounts

% G

RO

WT

H R

AT

E

source: Prometeia calculations on Ecb data

ITraxx 5y spreads of European financials

BA

SIS

PO

INT

S

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 9

Eurozone | the sovereign debt crisis and the drying up of wholesale funding reintroduced fragmentation in funding markets

financial fragmentation index°

source: Prometeia calculations on Ecb data, National Central Banks, IMF.° based on government bonds market and banking sector data. The index is calculated for 10 Euro area countries (Belgium, Germany, Ireland, Greece, Spain, France, Italy, Netherlands, Austria, Portugal).

ind

ex

Lehman Brothers

OMT

Greece aid plan

LTRO

QE

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 10

agenda the banking system at the outbreak of the financial crisis

2 | new regulation to preserve financial

stability

supervision and regulatory uncertainty

the development of risk management expertise in financial

institutions

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 11

phases of regulation | from Basel 1 to Basel 2

Basel 2 main aim was to establish a more risk sensitive framework to Capital Adequacy compared to

1988 Cooke ratio: the most relevant innovation was the introduction of Internal Rating Approaches to

define regulatoryl capital requirements

- Basel 1 - - Basel 2 -

8% 8%

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 12

phases of regulation | from Basel 2 to Basel 3: capital ratio, leverage and new liquidity requirements

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 13

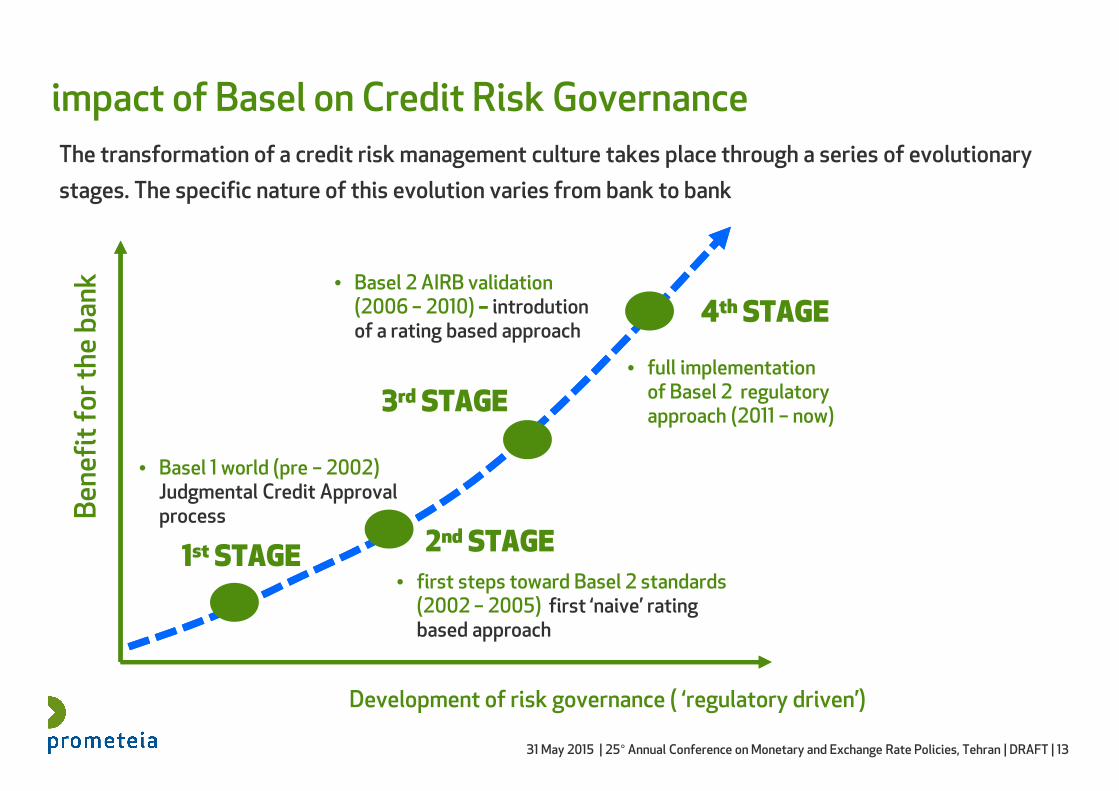

The transformation of a credit risk management culture takes place through a series of evolutionary

stages. The specific nature of this evolution varies from bank to bank

Ben

efit

for

the

ban

k

Development of risk governance ( ‘regulatory driven’)

1st STAGE

• Basel 1 world (pre – 2002) Judgmental Credit Approval process

2nd STAGE

• first steps toward Basel 2 standards (2002 – 2005) first ‘naive’ rating based approach

3rd STAGE

• Basel 2 AIRB validation(2006 – 2010) –––– introdutionof a rating based approach

4thSTAGE

• full implementation of Basel 2 regulatory approach (2011 – now)

impact of Basel on Credit Risk Governance

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 14

capital adequacy | from Basel 2 to Basel 3

BASEL 2(CRDII)

BASEL 3(CRDIV)

core tier 1 capital2%

tier 2 capital4%

common equity4.5%

tier 2 capital2%

hybrid capital2%

8%

of

RW

A

6%

of

RW

A

8%

of

RW

A

hybrid capital1.5%

conservation buffer2.5%

countercycl. buffer(0-2.5%)

SIFI buffer (0-2.5%)

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 15

capital adequacy | European banks’ capital strengthened markedly since 2008

common equity ratio (Dec-14)vs core tier1 (Dec-08)

source: Prometeia calculations on SNL and balance sheet data

Note: 80 European groups (of which: Italy (15), Germany (16), France (5), Spain (6), Netherlands,( 3). ECB significant groups: 76

7%

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 16

leverage ratio | a non risk-based ratio

to prevent an excessive build-up of leverage on institutions’ balance sheets, Basel III introduces a

leverage ratio to supplement the risk-based capital framework.

>3%

Leverage Ratio

Tier 1 capital

Total Exposure

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 17

liquidity ratios | to tackle the vulnerabilities emerged with the financial crisis

� the systemic liquidity shocks during the global financial crisis promoted the introduction

of quantitative liquidity regulations for the first time

� these regulations aim to reduce liquidity risks arising from maturity mismatches and

dependence on short-term funding and to provide a stronger incentive for banks to shift

their funding mix

� as the recent financial crisis showed, a sustainable and stable funding structure is key to

reduce the likelihood that disruptions to a bank’s regular sources of funding erode its

liquidity position and increase its risk of default and of negative spillovers to the rest of

the financial system

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 18

liquidity ratios | LCR and NSFR

Available Stable Funding

Required Stable Funding

>=100%>=60-100%

Liquidity Coverage Ratio Net Stable Funding Ratio

NSFR

100%

stock of HQLA*

Total Net Cash outflows over the next 30 calendar days

*High Quality Liquid Assets

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 19

Eu regulation | Basel III is only one of the initiatives aimed at increasing financial stability

� Capital requirements regulation and directive (CRR/CRDIV)

� Bank Recovery and Resolution Directive (BRRD)

� Directive on Deposit Guarantee Scheme

� EMIR* e MiFID^

*European Market Infrastructure Regulation^revisions on Markets in Financial Instruments Directive

Banking Union

� Banking structural reform

� to strengthen the resilience of the EU banking sector

� to make resolution of distressed bankseasier and ensure that taxpayers’ moneyis not called upon in a banking crisis

� to enhance deposit guarantee schemes

� to increase banks’ resilience to shocks, reduce their probability of defaults and of negative spillovers

� to account for risks deriving from financial derivatives and market infrastructures

� Single Supervisory Mechanism (SSM)

� to increase financial integration and ensure homogeneous standards of supervision across the euro area

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 20

agenda the banking system at the outbreak of the financial crisis

new regulation to preserve financial stability

3 | supervision and regulatory uncertainty

the development of risk management expertise in financial

institutions

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 21

Euro area banking union | three pillars

1. Single Supervisory Mechanism (SSM)

coverage of more than 6000 EMU banks; the ECB directly supervises the 123 significant banks ofthe participating countries (these banks hold almost 82% of banking assets in the euro area)

2. Single Resolution Mechanism (SRM)

Single Resolution Board (SRB)

Single Resolution Fund (SRF)

Banking Recovery and Resolution Directive (bail-in mechanism)

3. Single Deposit Guarantee Scheme

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 22

Banking Union | the new supervisory approach

� a new supervisor, the SSM• significant banks: direct supervision, on-site inspections and off-site analyses

• less significant banks: indirect supervision; direct supervision by National Competent Autorithies (usually the NCBs)

� a new supervisory approach

• proportionality: toughness and intrusiveness increasing with bank significance

• analysis of business models and corporate governance

• based on peer-review analysis (at EMU level)

• less supervisory judgement than for most NCAs

� national resolution authorities (together with the SRM) and strengthening of deposit guarantee schemes

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 23

Banking Union | the new Supervisory Review and Evaluation Process (SREP)

The key purpose of SREP is to ensure that institutions have adequate

arrangements, strategies, processes and mechanisms as well as capital and

liquidity to ensure a sound management and coverage of their risks, to which they

are or might be exposed, including those revealed by stress testing, and risks that

institutions may pose to the financial system

Pillar 2 becomes an essential component in the supervisory dialogue: it should

overcome national discretions to preserve consistency

ECB can impose supervisory measures leading to new quantitative thresholds:

capital ratio, liquidity ratio, etc.

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 24

-10

0

10

20

30

40

50

60

gen-

03

ago-

03

mar

-04

ott-

04

mag

-05

dic

-05

lug-

06

feb

-07

set-

07

apr-

08

nov-

08

giu-

09

gen-

10

ago-

10

mar

-11

ott-

11

mag

-12

dic

-12

lug-

13

feb

-14

set-

14

famiglie imprese settore privato

mar

-15

capital adequacy | stringent capital constraints during a crisis can hamper bank lending

fonte: Prometeia calculations on Ecb data

Emu, loanscumulated growth from jan 2003 and from sept 2008 – % values

note: cumulative net flows of loans from 2003 to 2007 and from 2008 to 2015 on outstanding loans of 2002 and of 2007

households non-fin. corp. total

€6,8 trln

€10,8 trln

€10,8 trln€10,9 trln

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 25

capital adequacy | uncertainty over “final rules” could be a further drag on credit supply

� removal of national discretion in the calculation of capital ratios

� revision of risk weights in the standard approach and introduction of a floor in

the IRB approach

� revision of risk weights for operational risk and market risk

� revision of risk weights on government bonds

� non realised gains/losses on government bonds in the AFS portfolio

� treatment of Deferred tax assets

� Total Loss-Absorbing Capacity (TLAC) for G-SIBs

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 26

source: Prometeia calculations on balance sheet data

LOSS ABSORBENCY CAPACITY

credit | but a solid banking system is a prerequisite for bank lending growth

LOAN-TO-DEPOSIT RATIO

COST OF FUNDING

NPL RATIO

ROA

Credit growth correlation

+

--

-

+

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 27

agenda the banking system at the outbreak of the financial crisis

new regulation to preserve financial stability

supervision and regulatory uncertainty

4 | the development of risk management

expertise in financial institutions

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 28

risk & performance | are the unifying viewpoints for understanding, interpreting and managing banking activity

Insights for Top management on Risk & Finance topics

Technical and Methodological Training for Risk & Finance Resources

Advisory on Policies & Procedures for CFO & CRO departments

Supply and implementation of IT solutions supporting Risk & Performance Management

GAP ANALYSIS

31 May 2015 | 25° Annual Conference on Monetary and Exchange Rate Policies, Tehran | DRAFT | 29

www.prometeia.com

Prometeia

Via G. Marconi 43, 40122 Bolognatel. +39 051 6480911, fax +39 051 220753

Italy

Offices in Milan, Rome, Beirut, Istanbul, London, Moscow, Paris, Lagos