Fees Manual

FEES Contents

Fees Manual

FEES 1 Fees Manual

1.1 Application and Purpose

FEES 2 General Provisions

2.1 Introduction2.2 Late Payments and Recovery of Unpaid Fees2.3 Relieving Provisions2.4 VAT

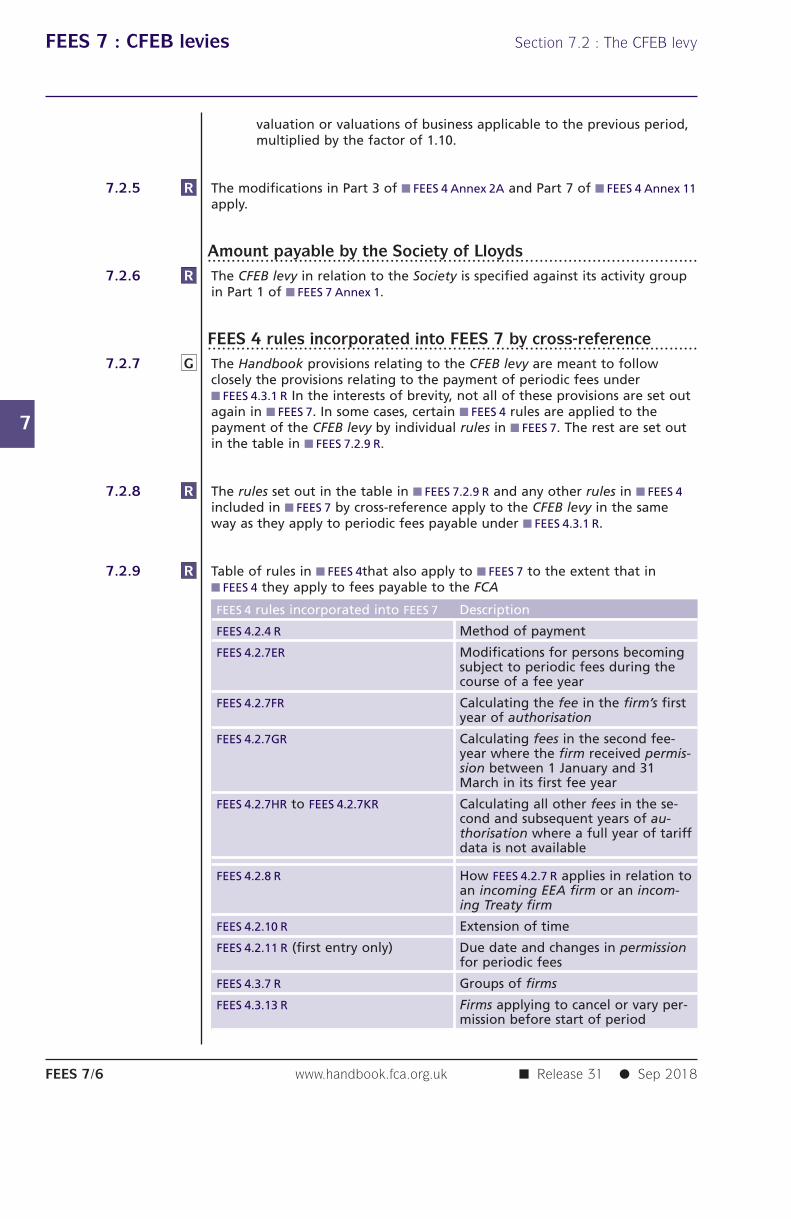

FEES 3 Application, Notification and Vetting Fees

3.1 Introduction3.2 Obligation to pay fees3 Annex 1 Authorisation fees payable3 Annex 2 Application and notification fees payable in relation to collective

investment schemes, ELTIFs, money market funds and AIFs marketed inthe UK

3 Annex 3 Application fees payable in connection with Recognised InvestmentExchanges and Recognised Auction Platforms

3 Annex 4 Application and administration fees in relation to listing rules [deleted]3 Annex 5 Document vetting and approval fees in relation to listing and prospectus

rules [deleted]3 Annex 6 Fees payable by a BIPRU firm for a permission or guidance on its

availability in connection with the BCD and/or CAD3 Annex 6A Fees payable for a permission or guidance on its availability in

connection with the EU CRR3 Annex 6B Part 13 Annex 8 Fees payable for authorisation as an authorised payment institution or

registration as a small payment institution, including notification fees, inaccordance with the Payment Services Regulations

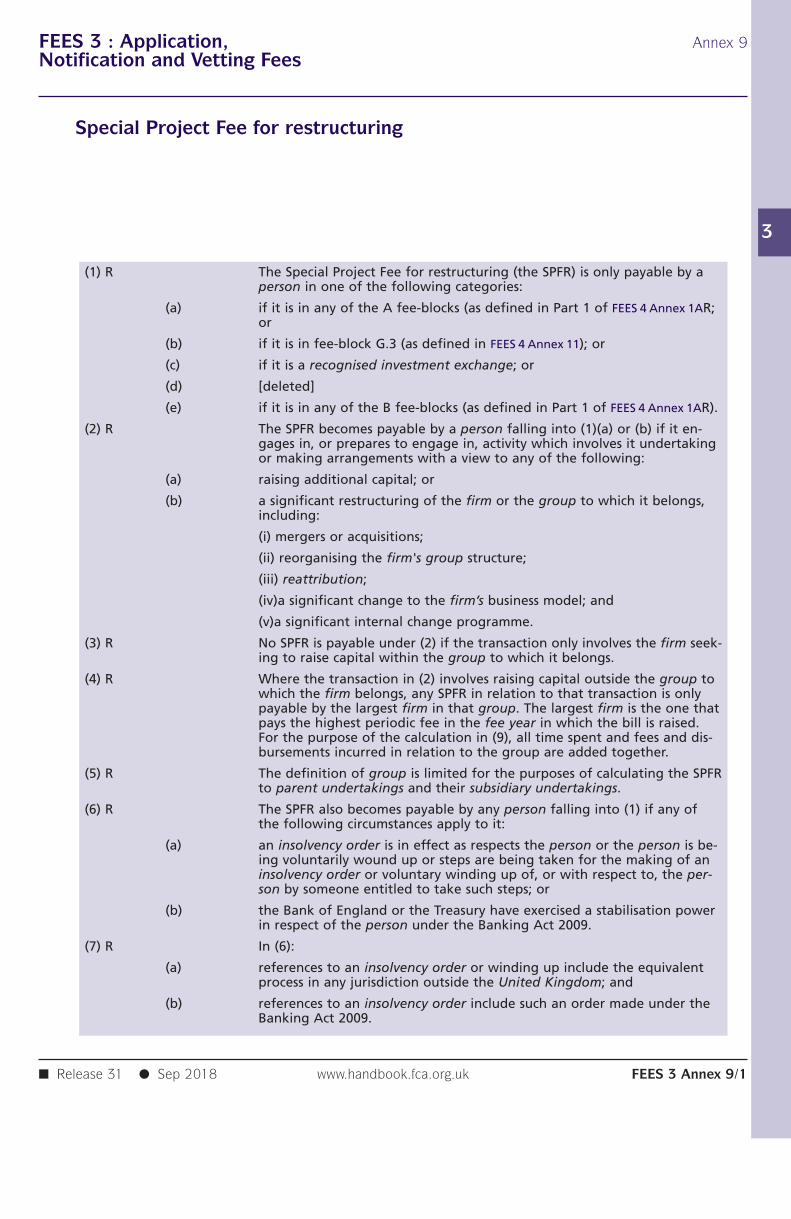

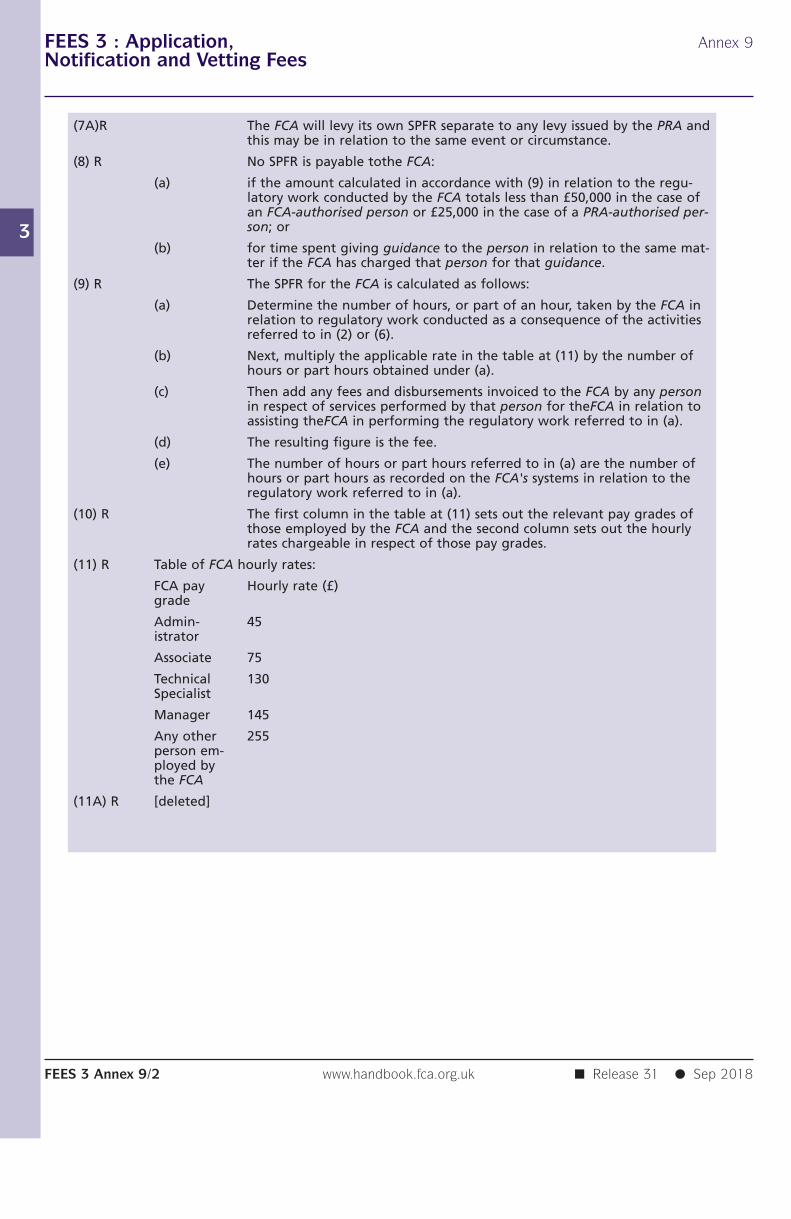

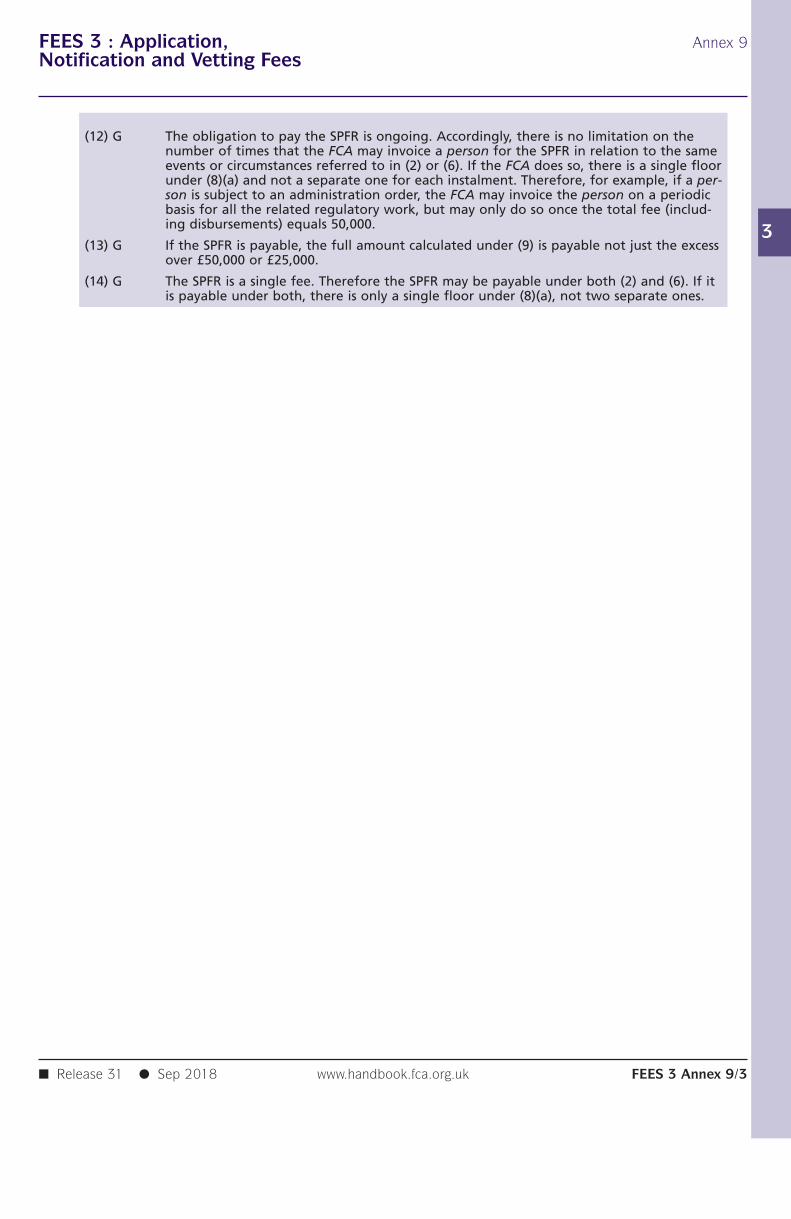

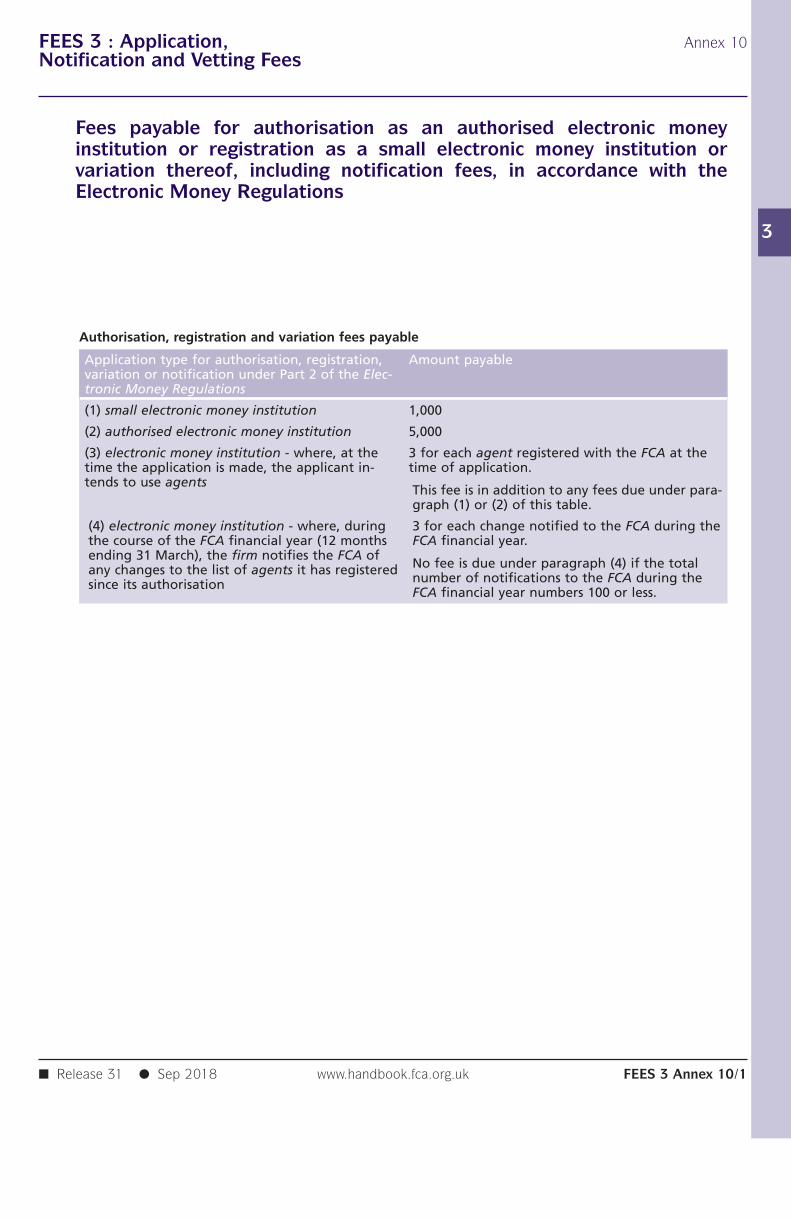

3 Annex 9 Special Project Fee for restructuring3 Annex 10 Fees payable for authorisation as an authorised electronic money

institution or registration as a small electronic money institution orvariation thereof, including notification fees, in accordance with theElectronic Money Regulations

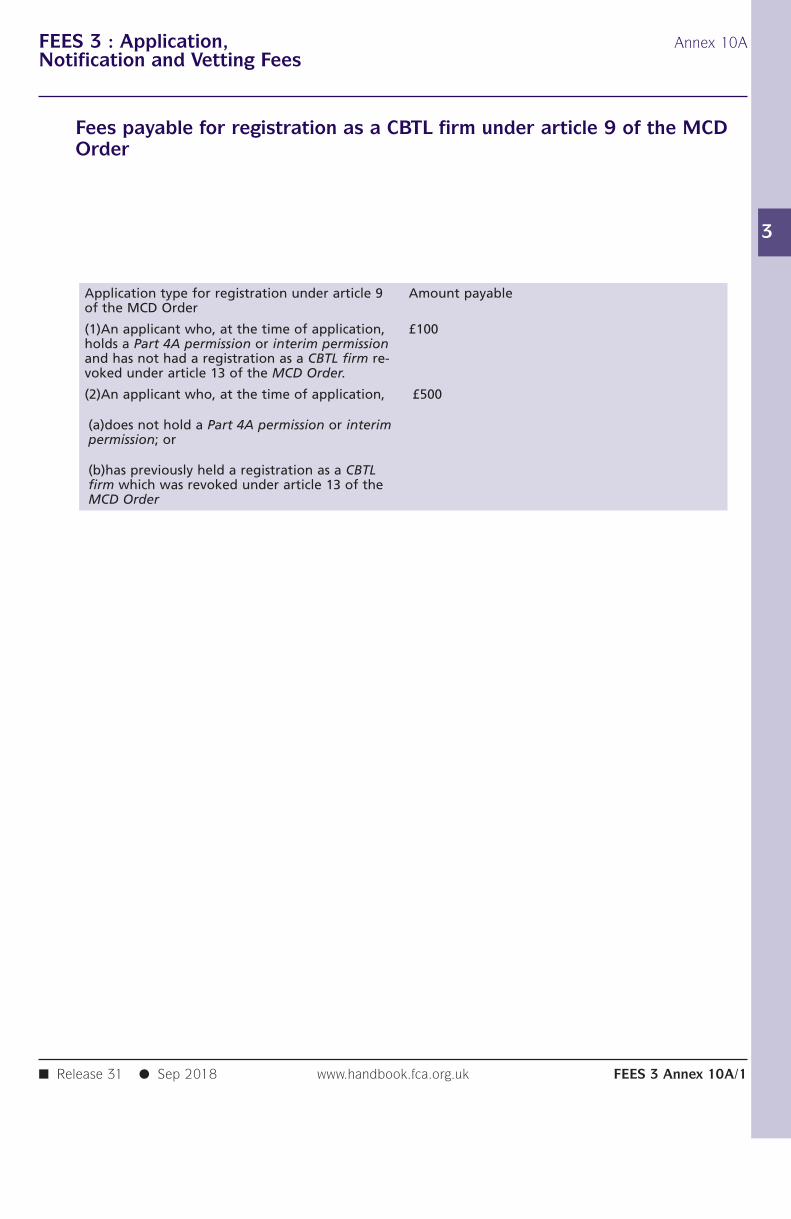

3 Annex 10A Fees payable for registration as a CBTL firm under article 9 of the MCDOrder

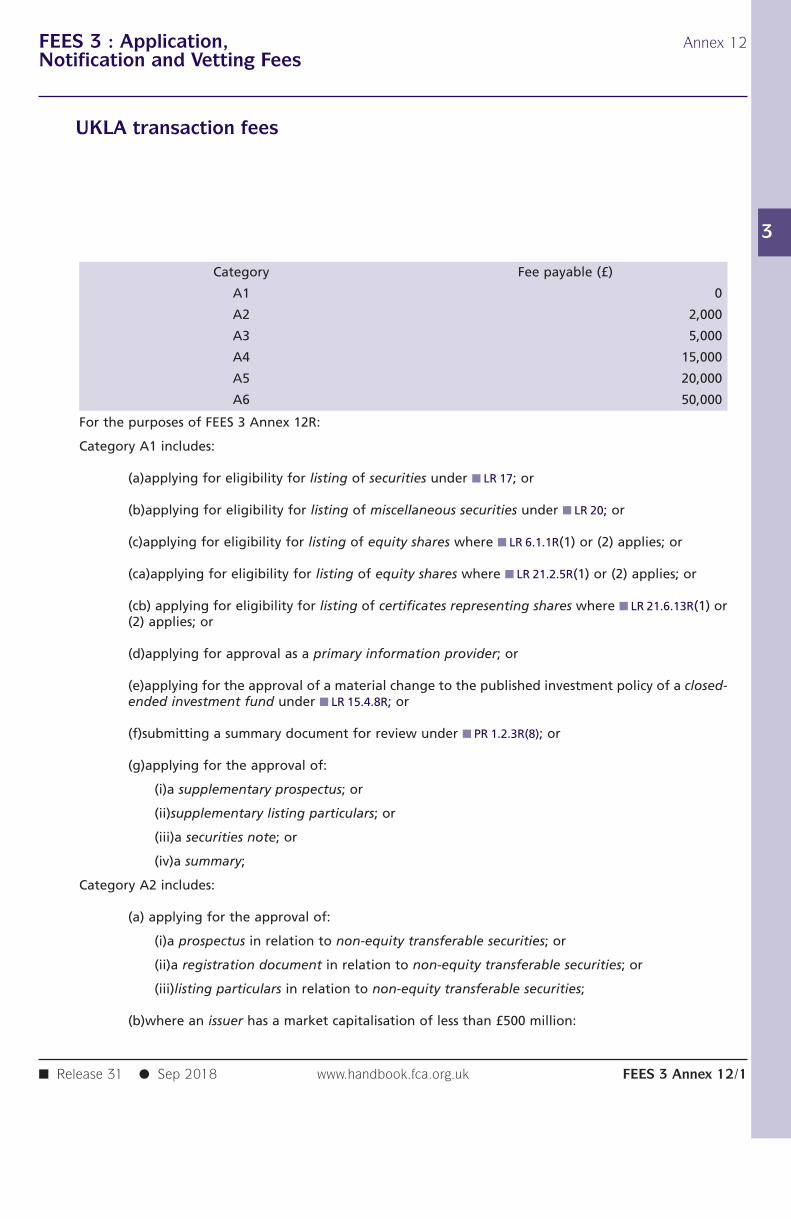

3 Annex 10B Designated Credit Reference Agencies and Finance Platforms Fee3 Annex 10C PPI campaign fees3 Annex 10CR Designated Credit Reference Agencies Fee3 Annex 11 Guidance on fees due under FEES 3.2.7R and FEES 3.2.7AR3 Annex 12 UKLA transaction fees

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES–i

FEES Contents

FEES 4 Periodic fees

4.1 Introduction4.2 Obligation to pay periodic fees4.3 Periodic fee payable by firms (other than AIFM qualifiers, ICVCs and

UCITS qualifiers)4.4 Information on which fees are calculated4 Annex 1A FCA activity groups, tariff bases and valuation dates4 Annex 2A FCA Fee rates and EEA/Treaty firm modifications for the period from 29

June 2018 to 31 March 20194 Annex 2B PRA fee rates and EEA/Treaty firm modifications for the period from 1

March 2014 to 28 February 20154 Annex 2B Ring-Fencing Implementation Fee4 Annex 3A Fees relating to the direct reporting of transactions to the FCA under

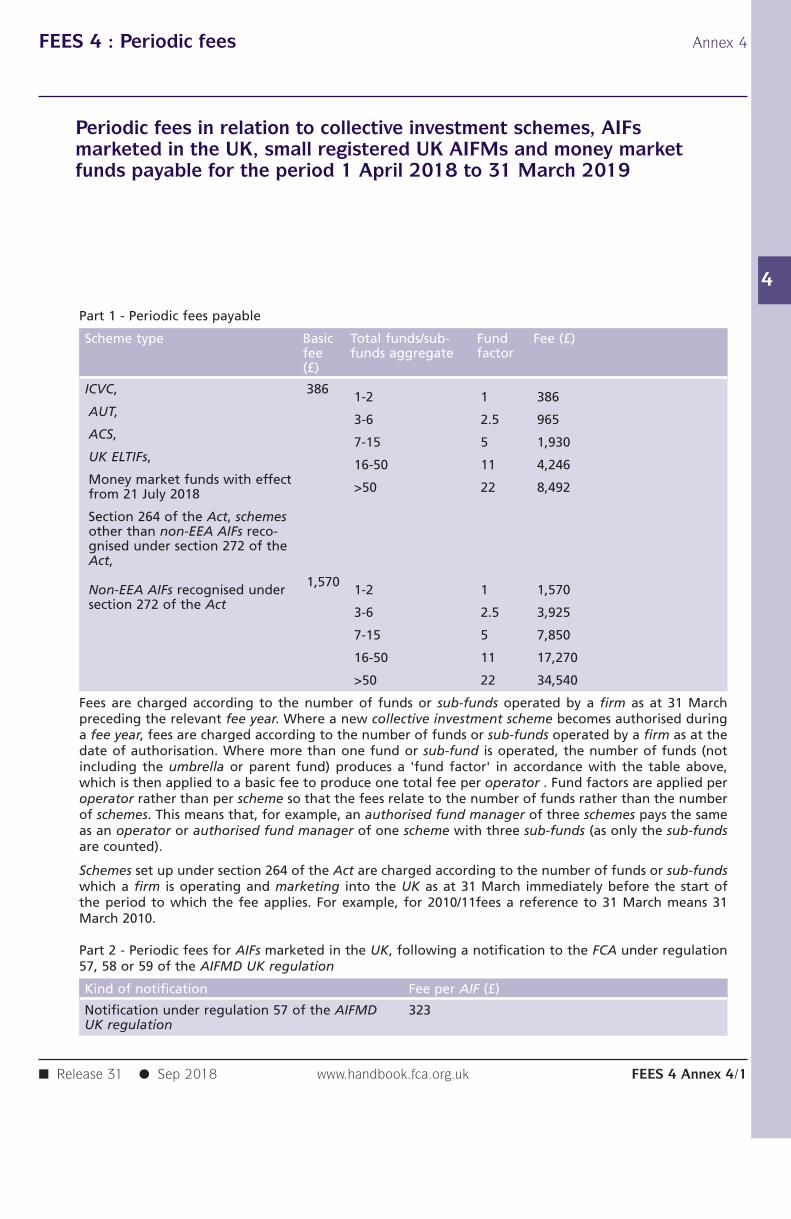

SUP 17A for the period 1 April 2017 to 31 March 2018 [deleted]4 Annex 4 Periodic fees in relation to collective investment schemes, AIFs marketed

in the UK, small registered UK AIFMs and money market funds payablefor the period 1 April 2018 to 31 March 2019

4 Annex 5 Periodic fees for designated professional bodies payable in relation tothe period 1 April 2018 to 31 March 2019

4 Annex 6 Periodic fees for recognised investment exchanges, and recognisedauction platforms payable in relation to the period 1 April 2016 to 31March 2017

4 Annex 7 Periodic fees in relation to the Listing Rules for the period 1 April 2015to 31 March 2016 [deleted]

4 Annex 8 Periodic fees in relation to the Disclosure and Transparency Rules for theperiod 1 April 2015 to 31 March 2016 [deleted]

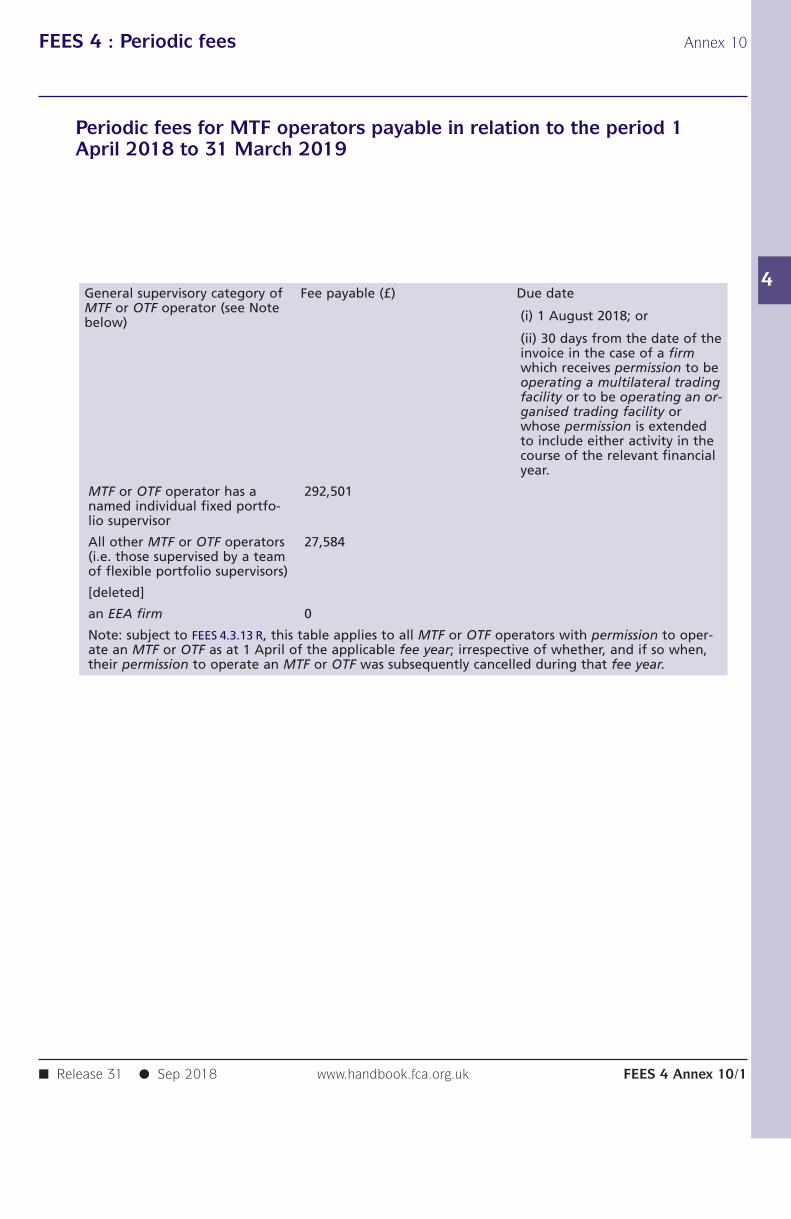

4 Annex 10 Periodic fees for MTF operators payable in relation to the period 1 April2018 to 31 March 2019

4 Annex 11 Periodic fees in respect of payment services, electronic money issuance,regulated covered bonds, CBTL business and data reporting services inrelation to the period 1 April 2018 to 31 March 2019

4 Annex 11A Definition of annual income for the purposes of calculating fees in feeblocks A.13, A.14, A.18, A.19 and B. Service Companies, RecognisedInvestment Exchanges and Regulated Benchmark Administrators

4 Annex 11B Definition of annual income for the purposes of calculating fees in feeblocks CC1 and CC2

4 Annex 12 Guidance on the calculation of tariffs set out in FEES 4 Annex 1AR Part3

4 Annex 13 Guidance on the calculation of tariffs set out in FEES 4 Annex 1AR Part3

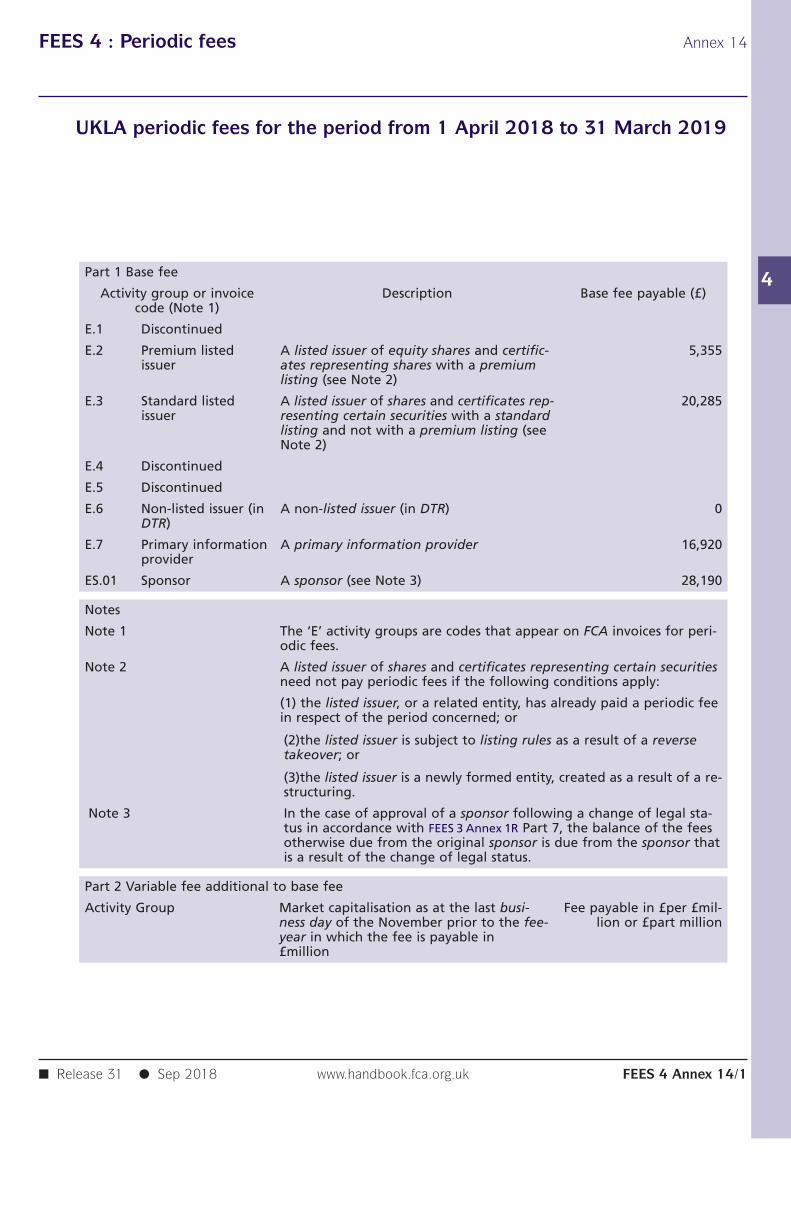

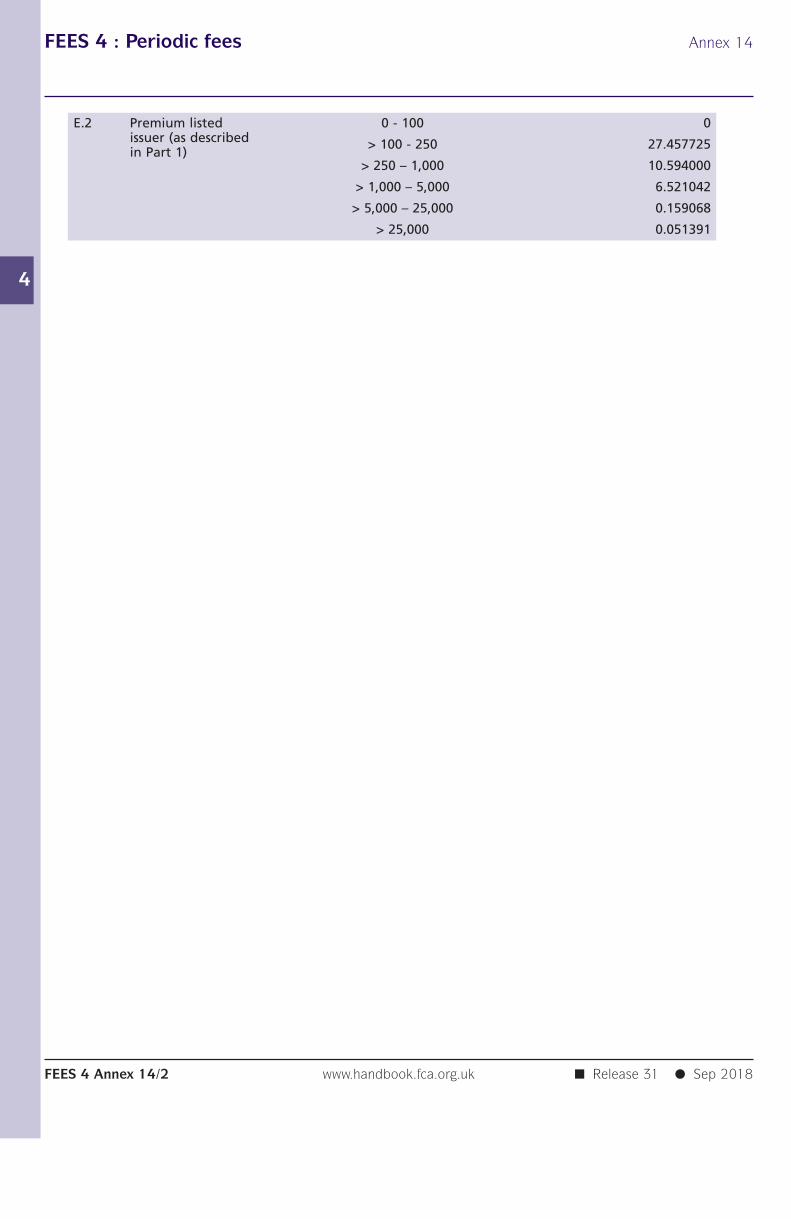

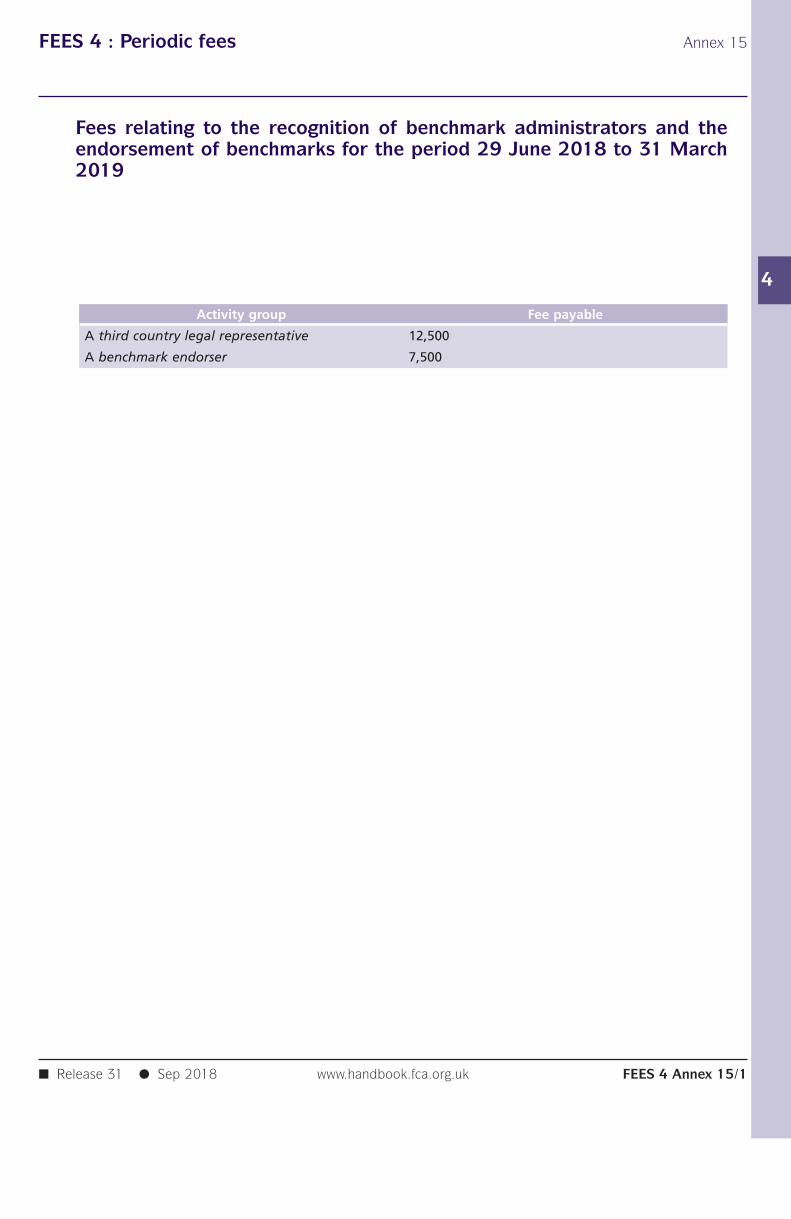

4 Annex 14 UKLA periodic fees for the period from 1 April 2018 to 31 March 20194 Annex 15 Fees relating to the recognition of benchmark administrators and the

endorsement of benchmarks for the period 29 June 2018 to 31 March2019

FEES 5 Financial Ombudsman Service Funding

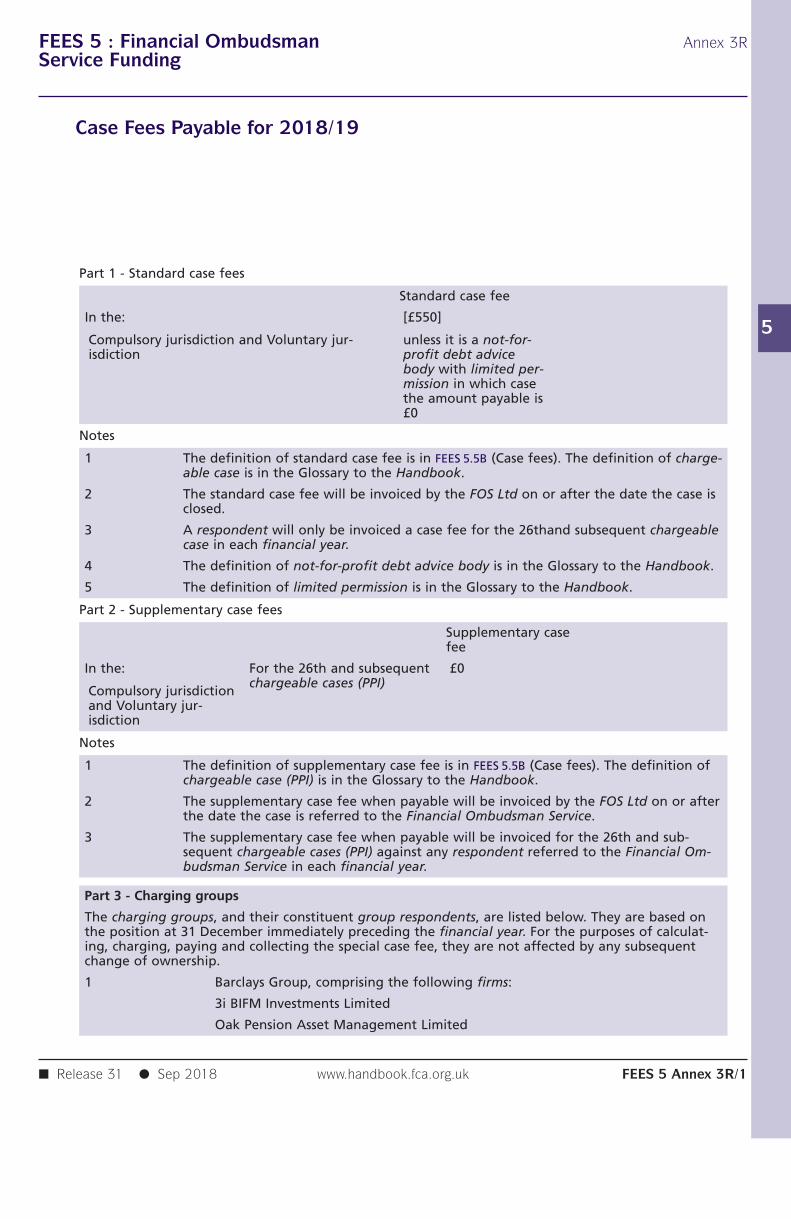

5.1 Application and Purpose5.2 Introduction5.3 The general levy5.4 Information requirement5.5B Case fees5.6 The supplementary levy5.7 Payment5.8 Joining the Financial Ombudsman Service

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES–ii

FEES Contents

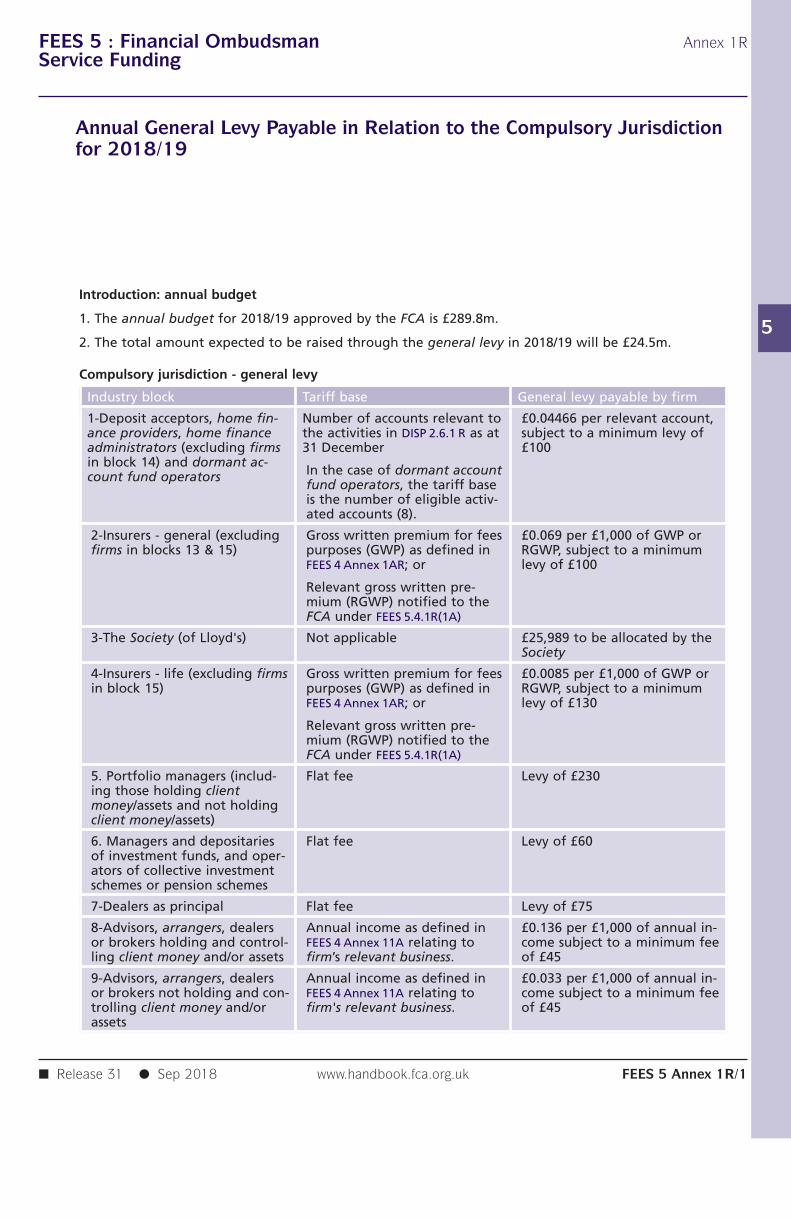

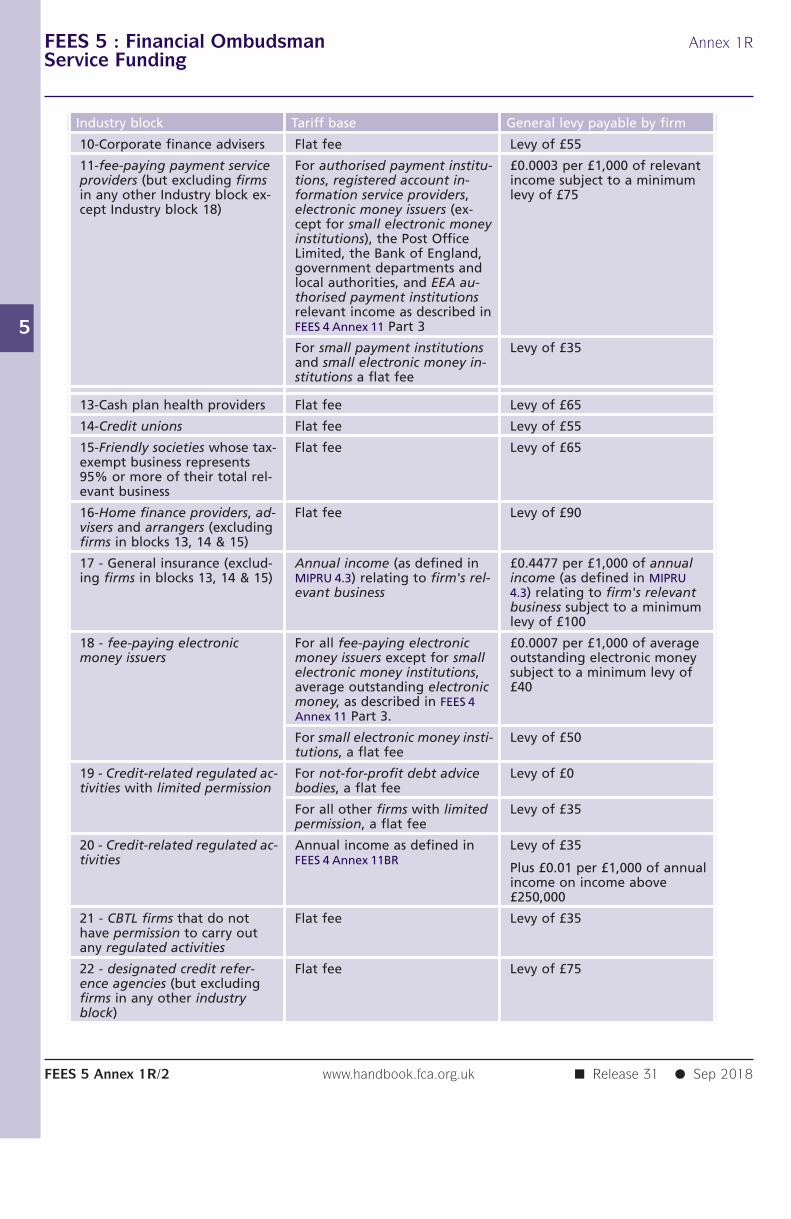

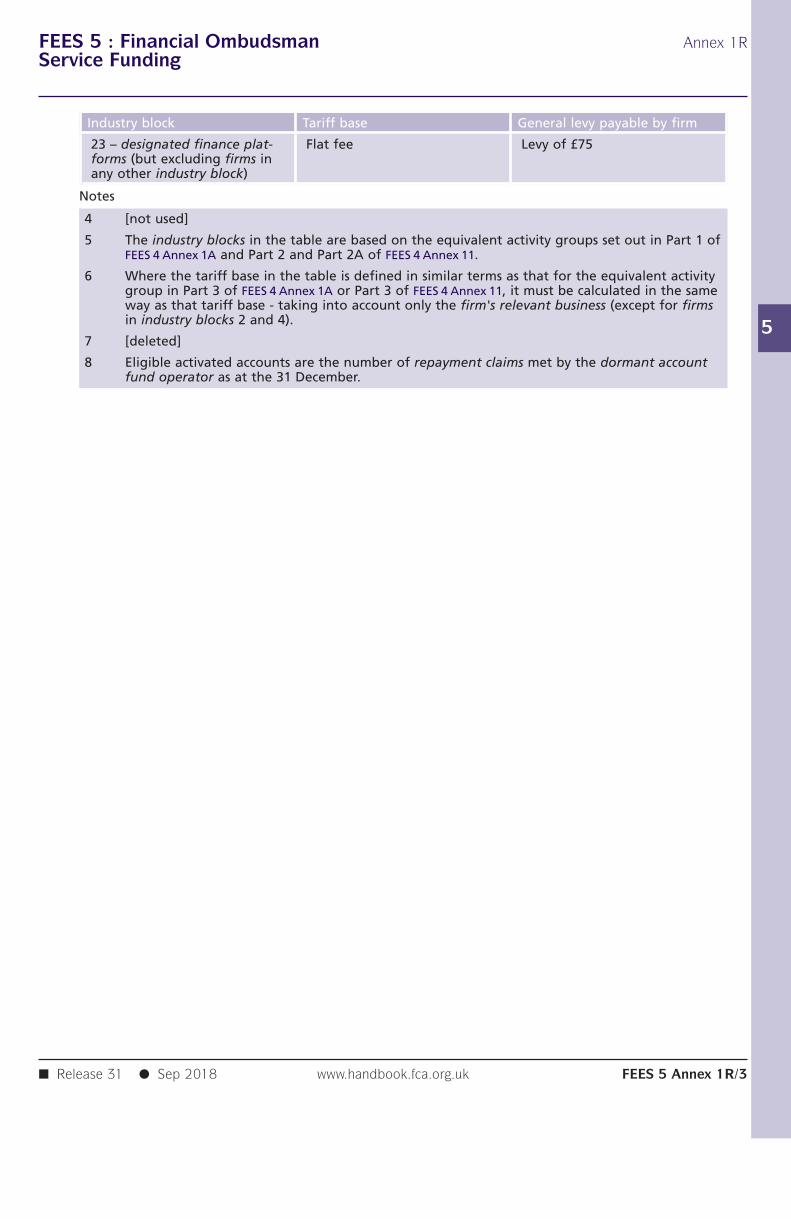

5.9 Leaving the Financial Ombudsman Service5 Annex 1R Annual General Levy Payable in Relation to the Compulsory Jurisdiction

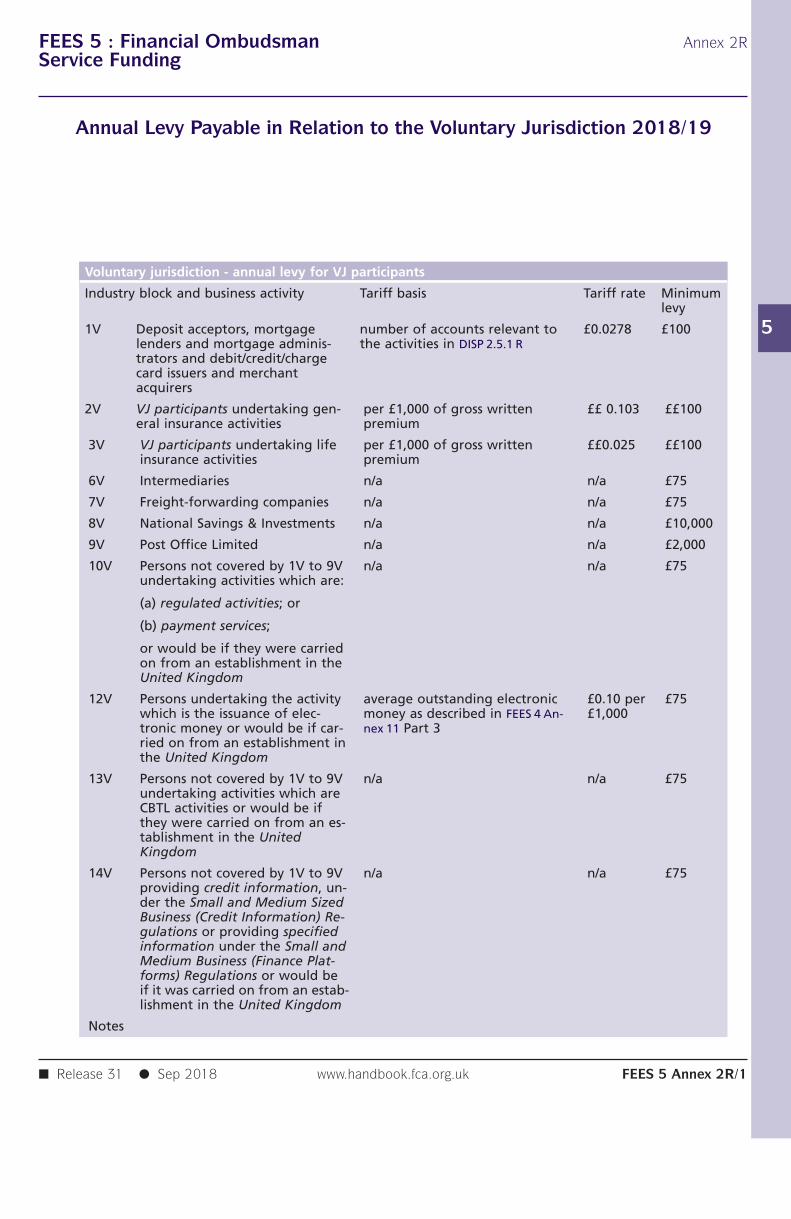

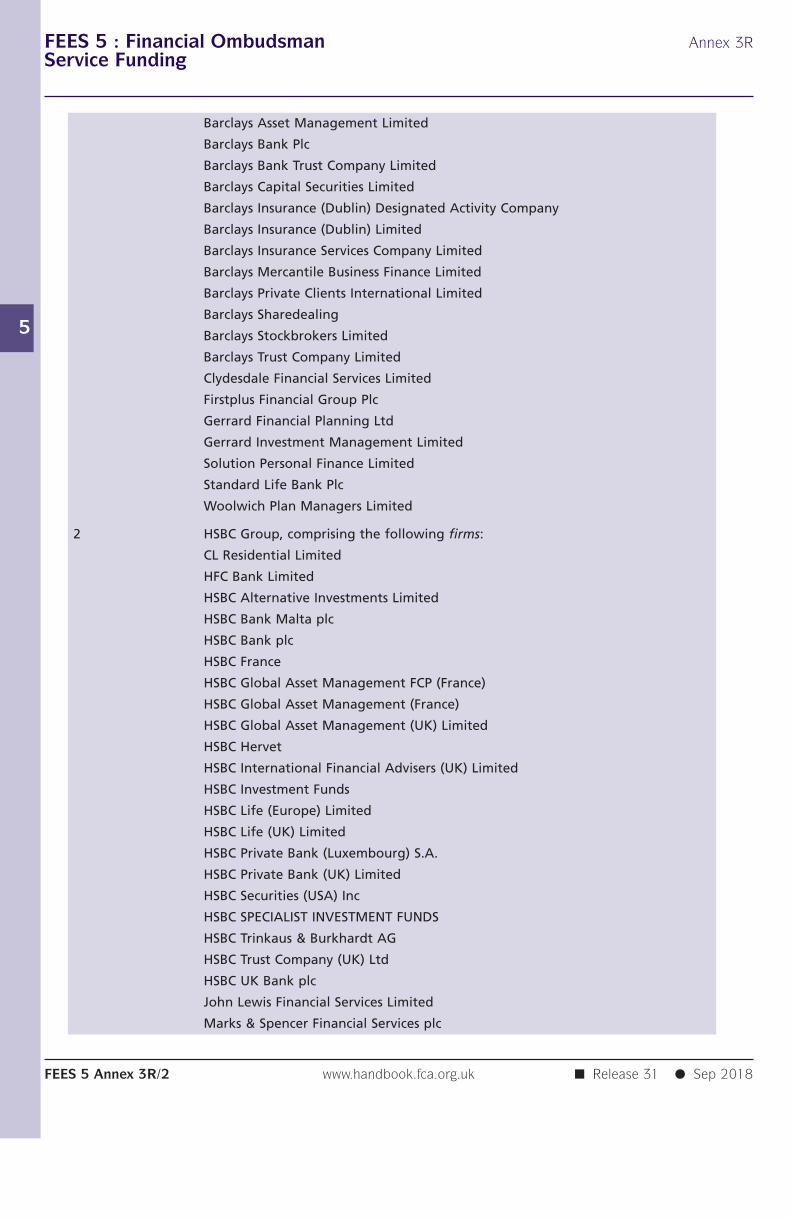

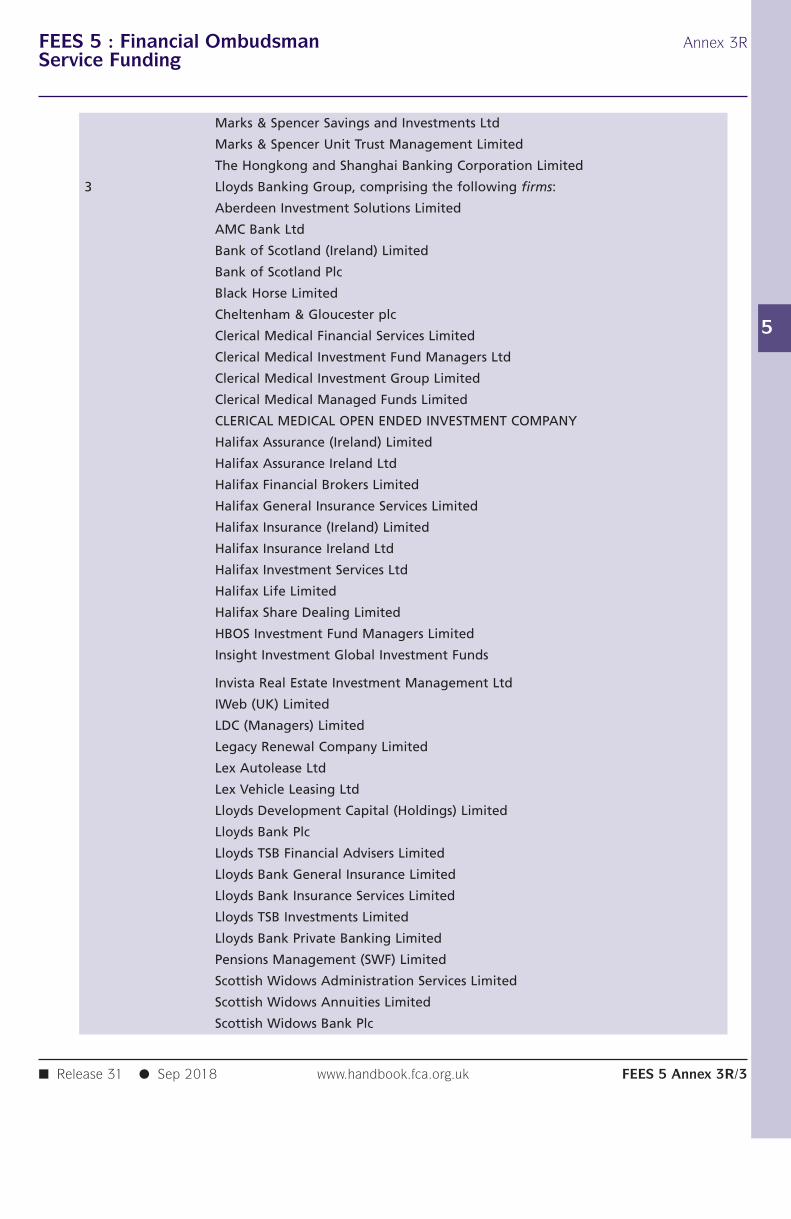

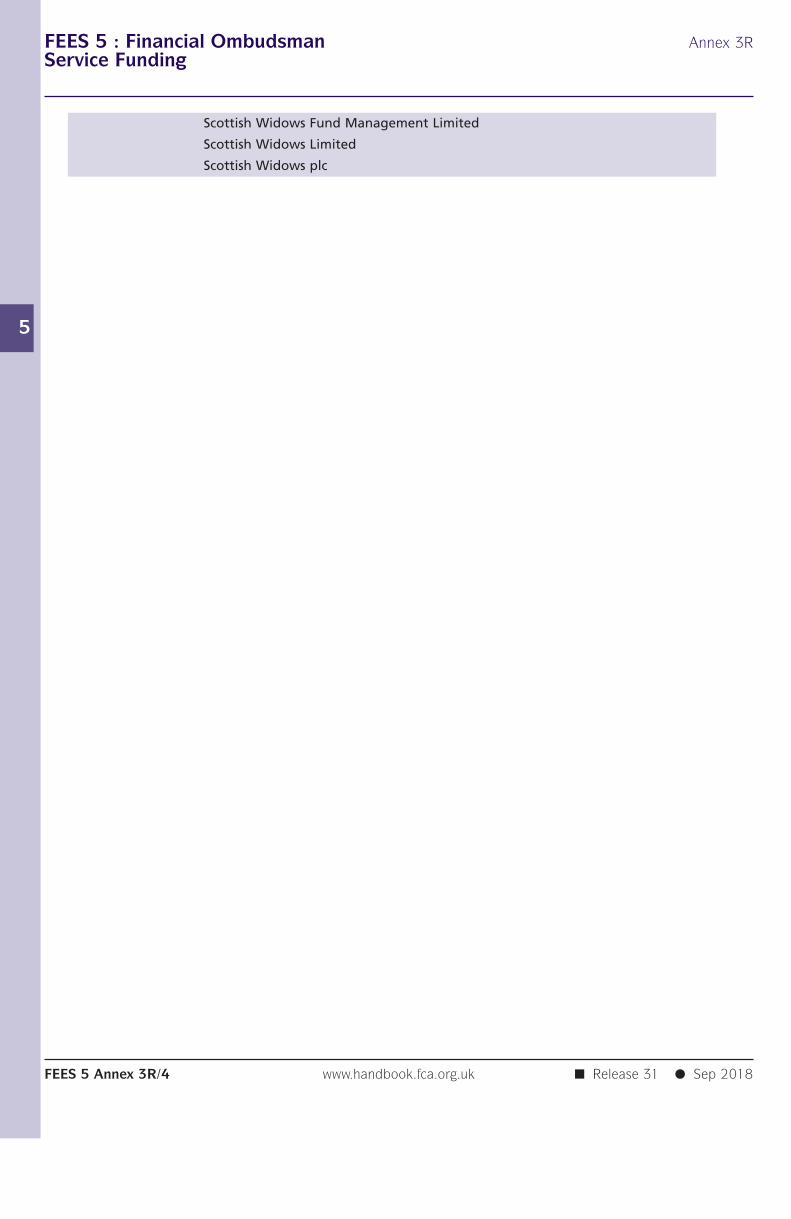

for 2018/195 Annex 2R Annual Levy Payable in Relation to the Voluntary Jurisdiction 2018/195 Annex 3R Case Fees Payable for 2018/19

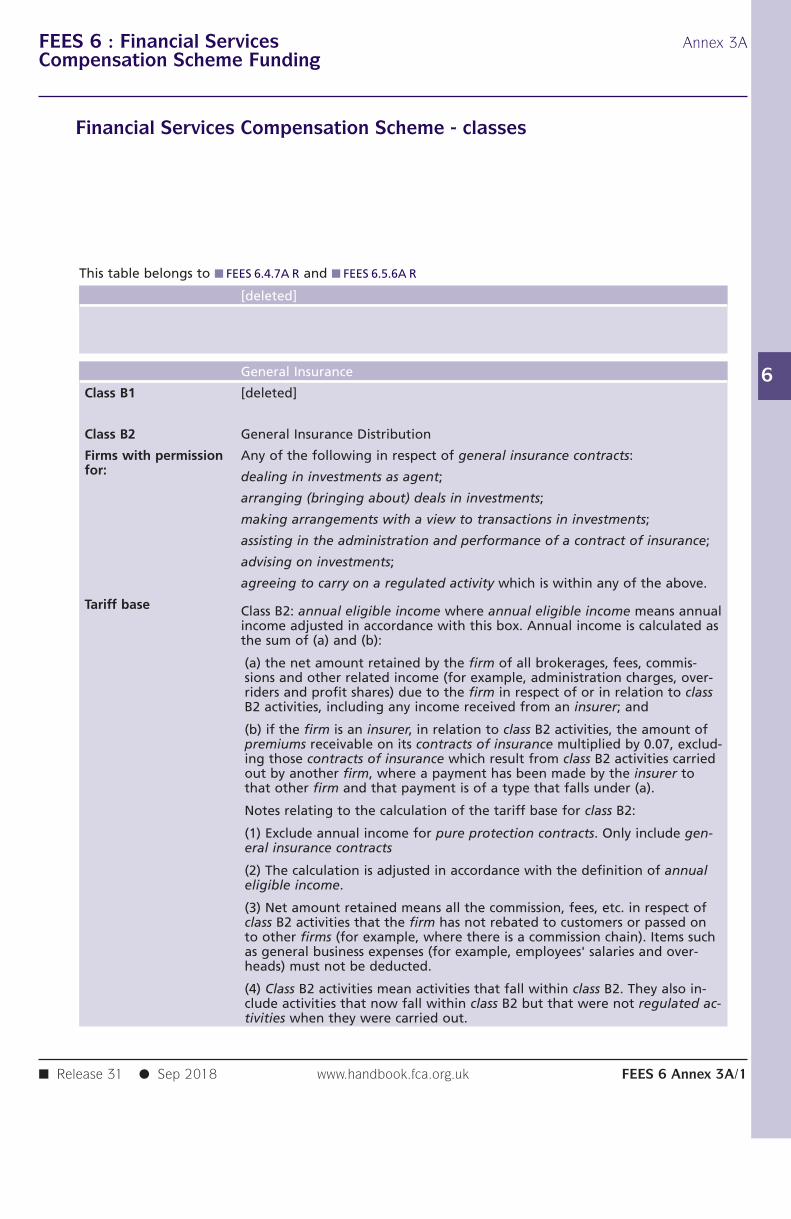

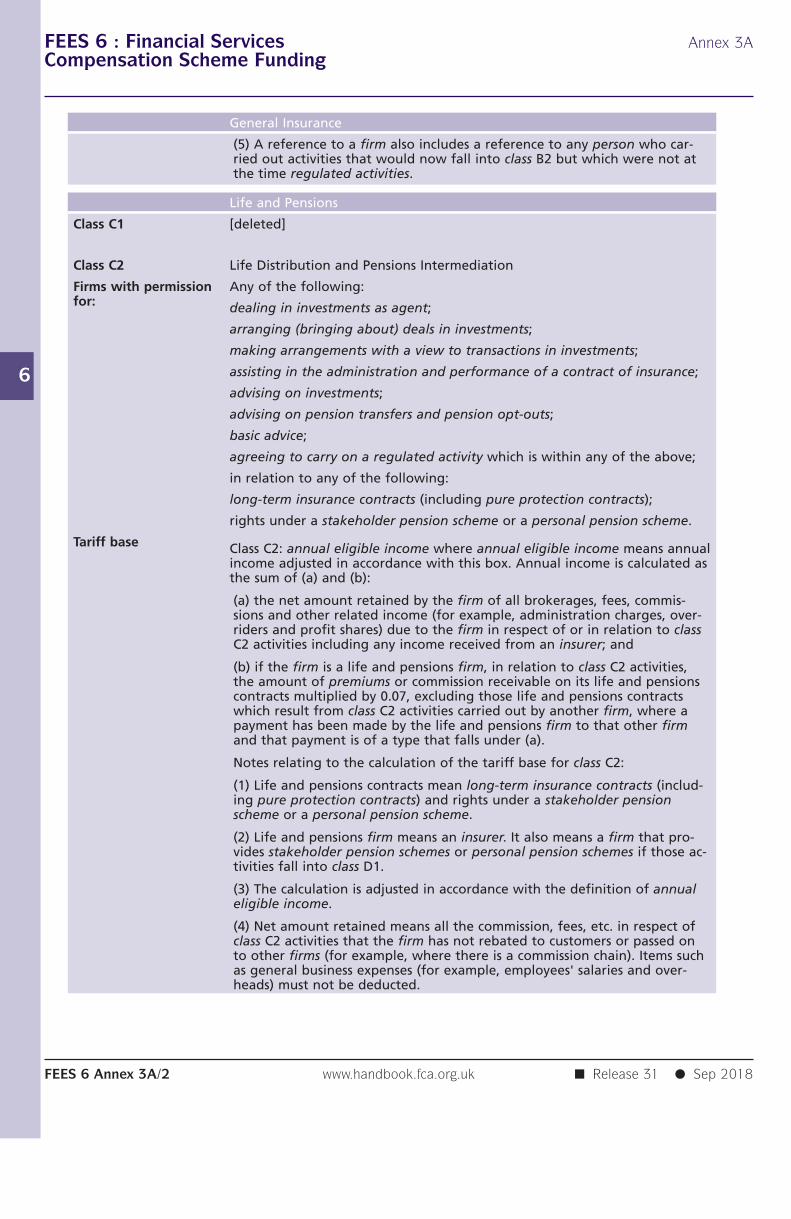

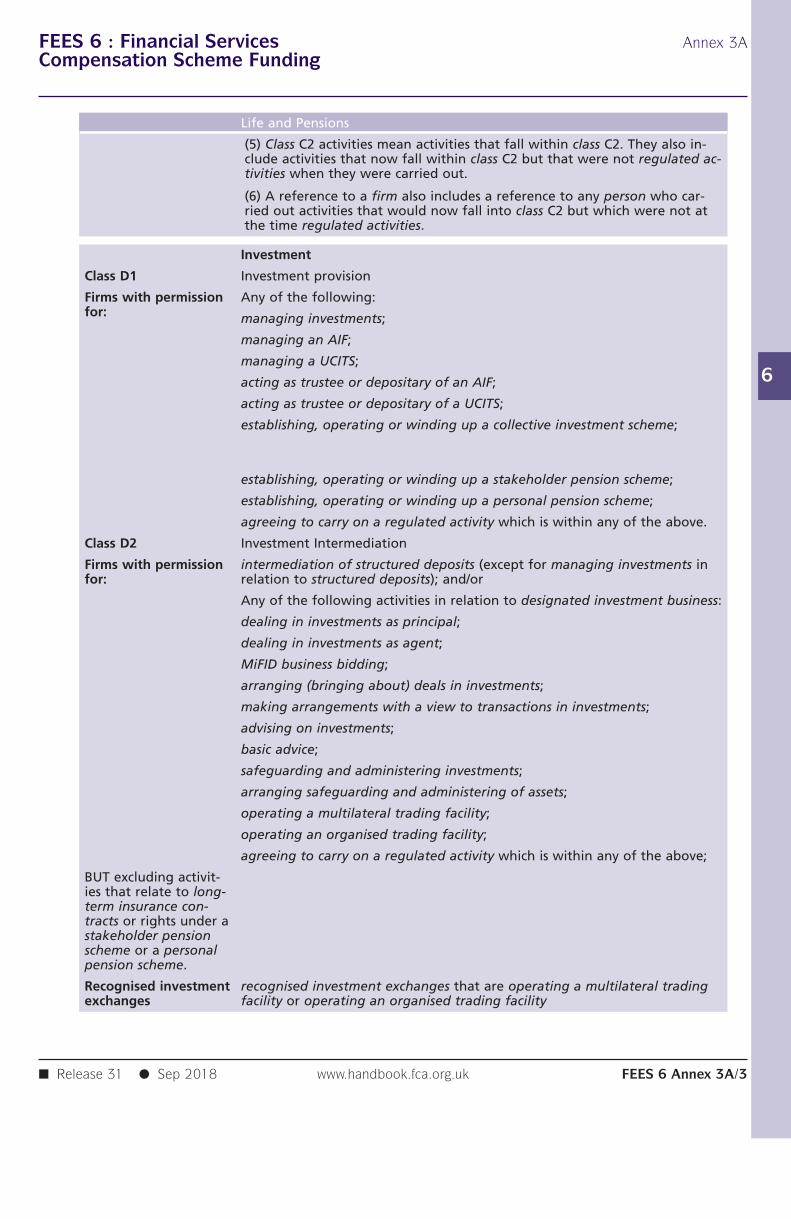

FEES 6 Financial Services Compensation Scheme Funding

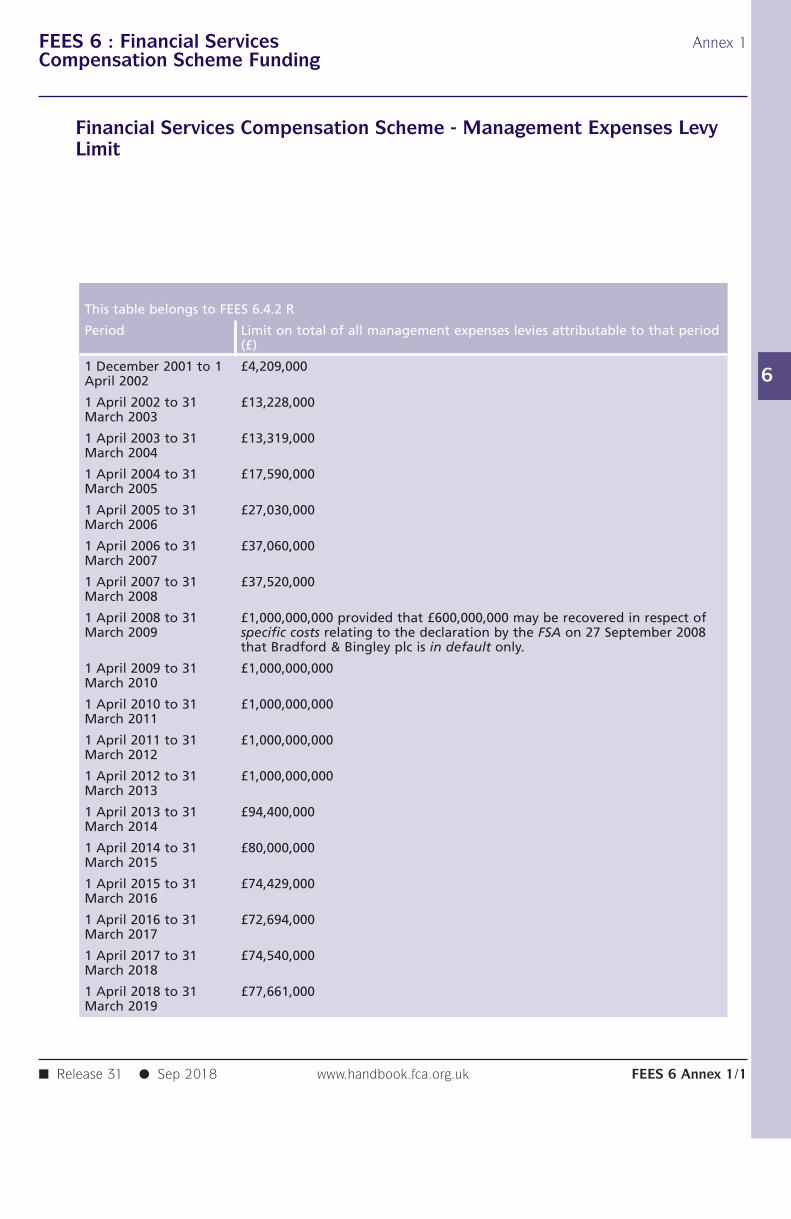

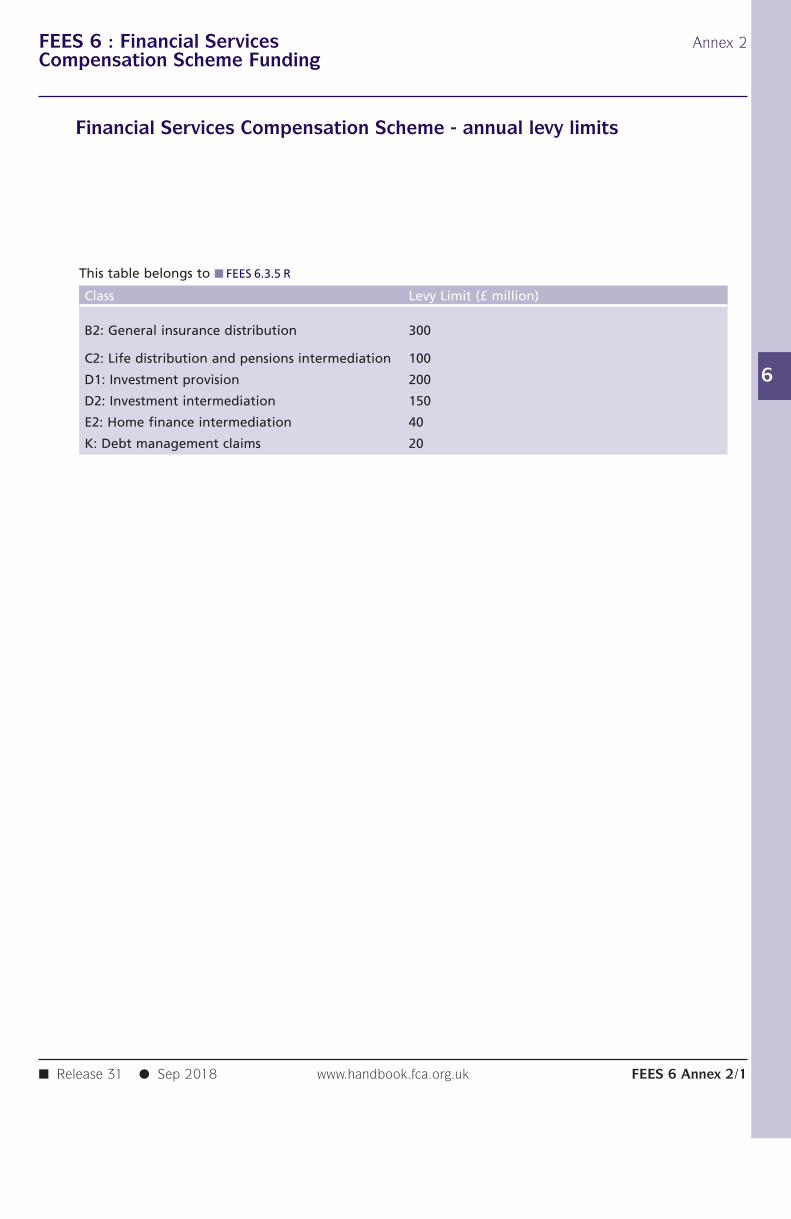

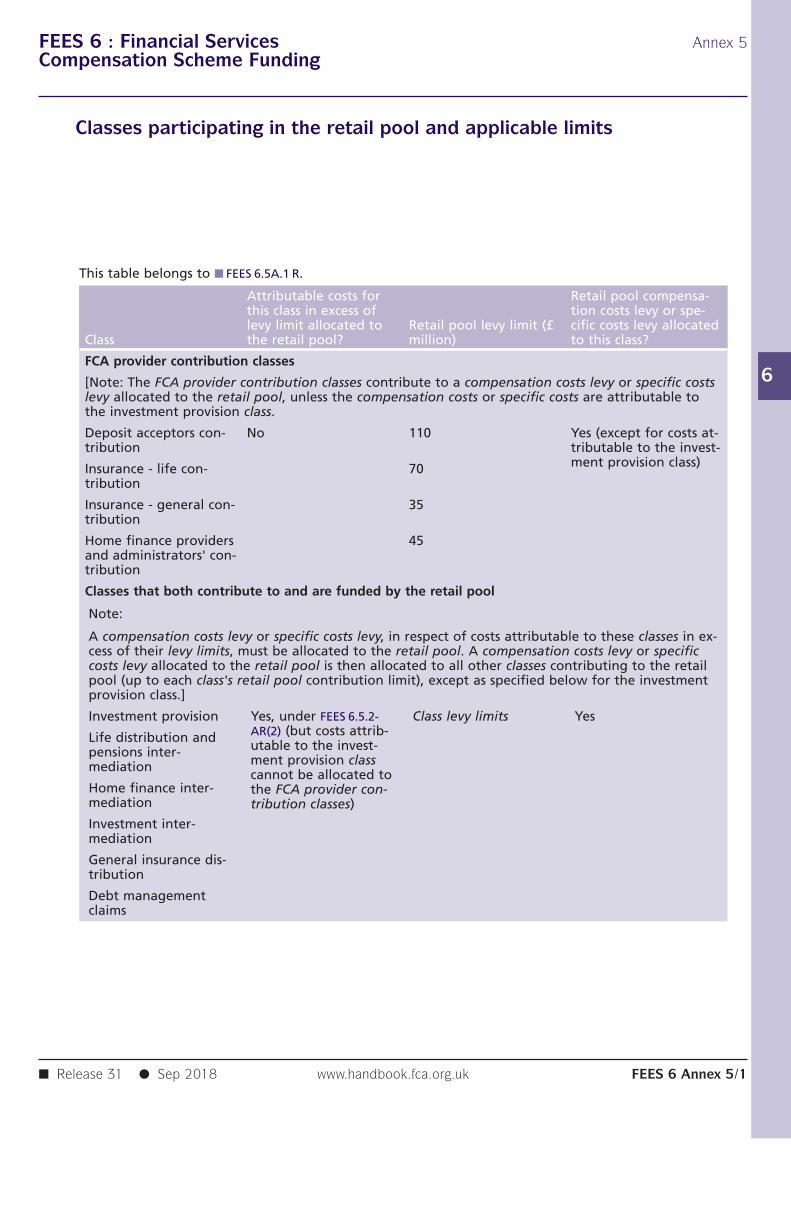

6.1 Application6.2 Exemption6.3 The FSCS's power to impose levies6.4 Management expenses6.4A Management expenses in respect of relevant schemes6.5 Compensation costs6.5A The retail pool6.6 Incoming EEA firms6.7 Payment of levies6 Annex 1 Financial Services Compensation Scheme - Management Expenses Levy

Limit6 Annex 2 Financial Services Compensation Scheme - annual levy limits6 Annex 3A Financial Services Compensation Scheme - classes6 Annex 4 Guidance on the calculation of tariff bases6 Annex 5 Classes participating in the retail pool and applicable limits

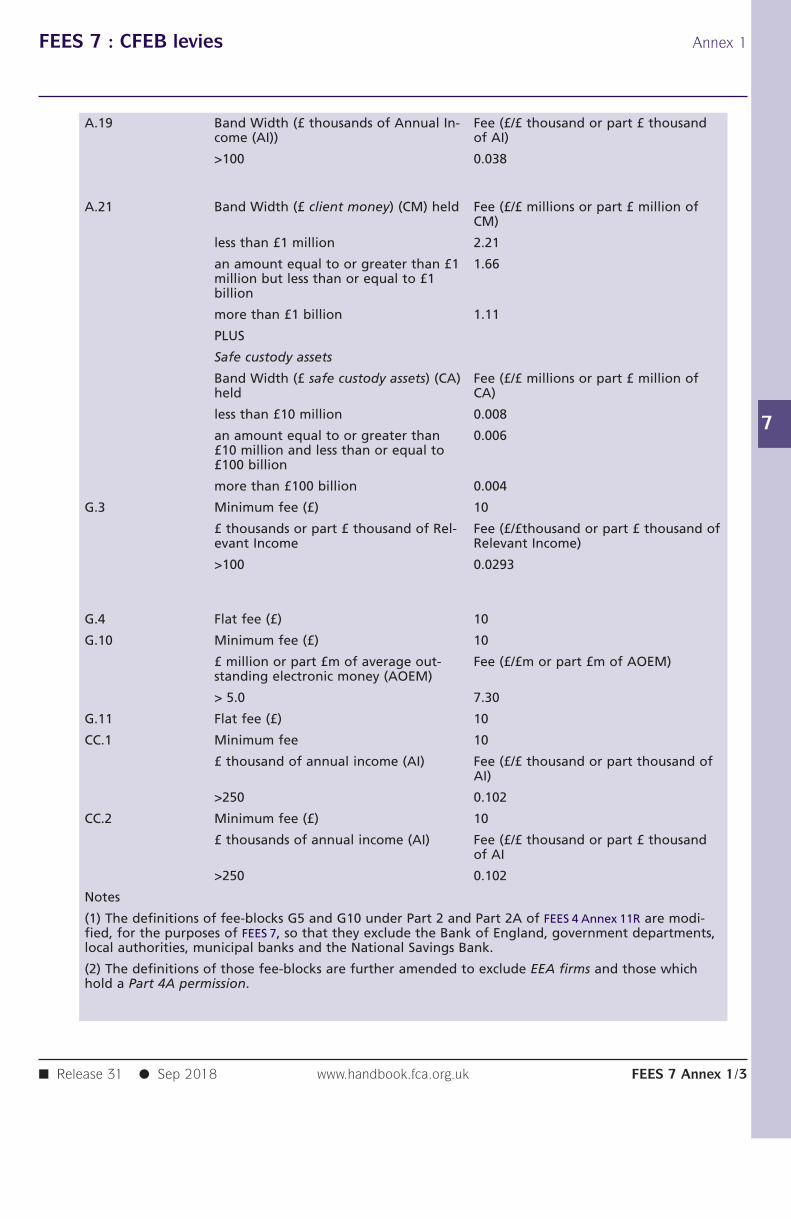

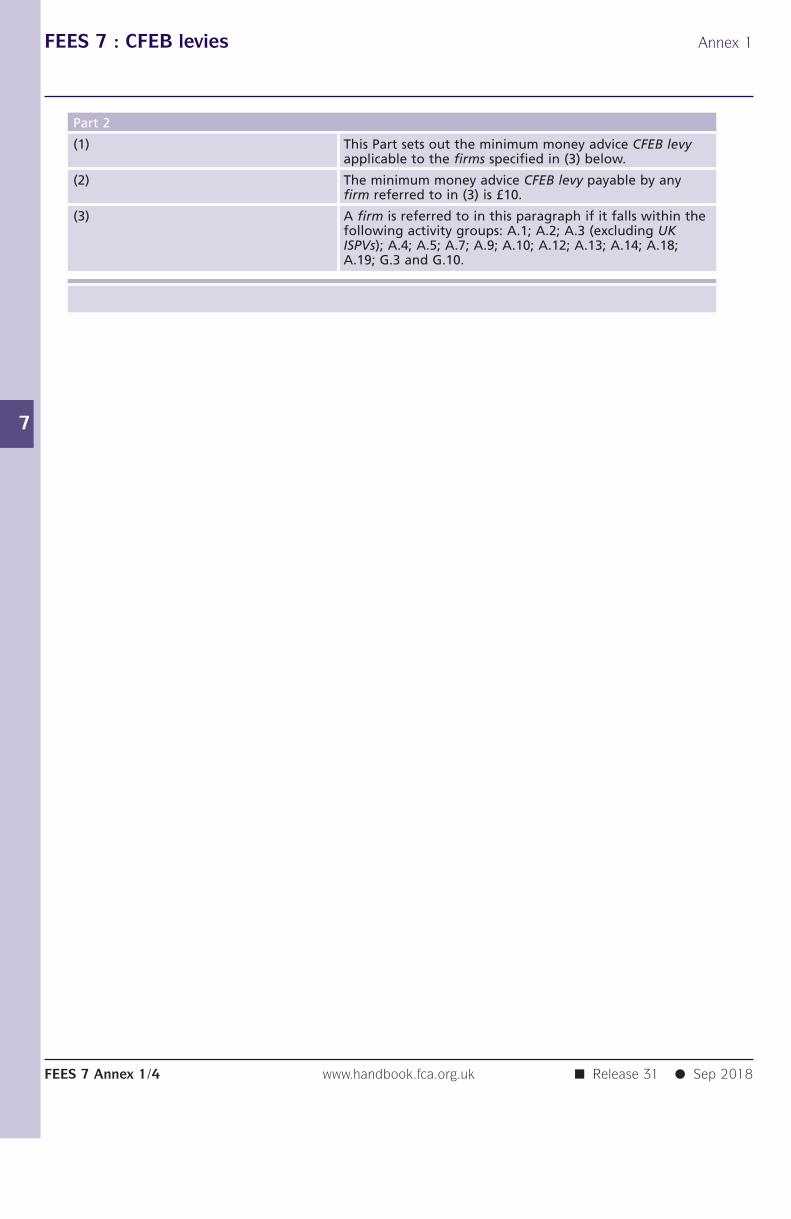

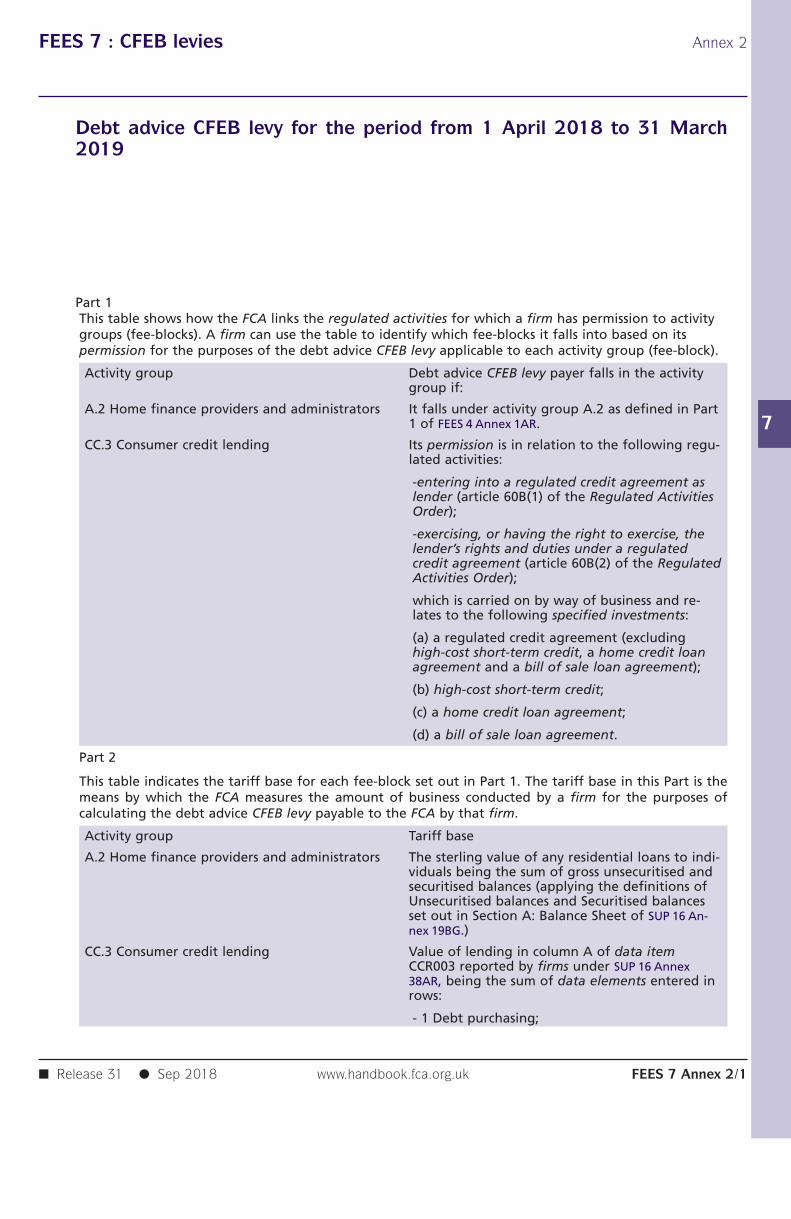

FEES 7 CFEB levies

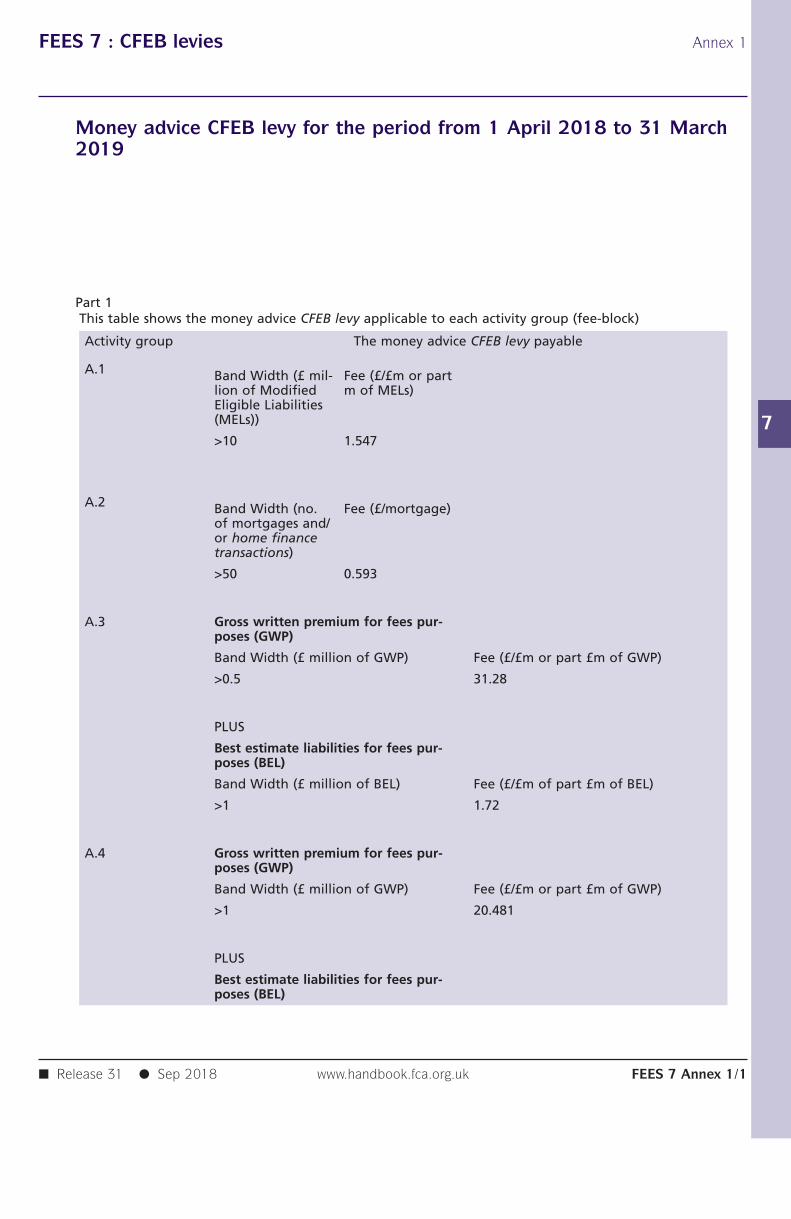

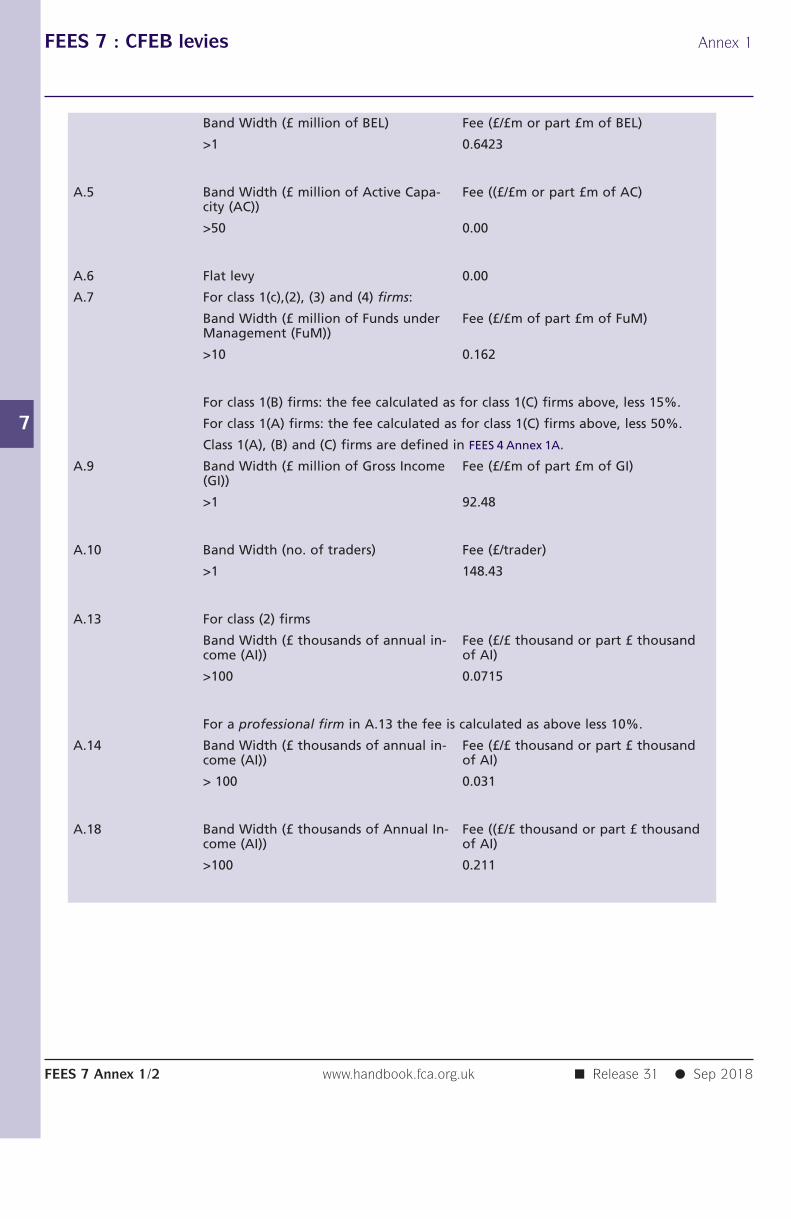

7.1 Application and Purpose7.2 The CFEB levy7 Annex 1 Money advice CFEB levy for the period from 1 April 2018 to 31 March

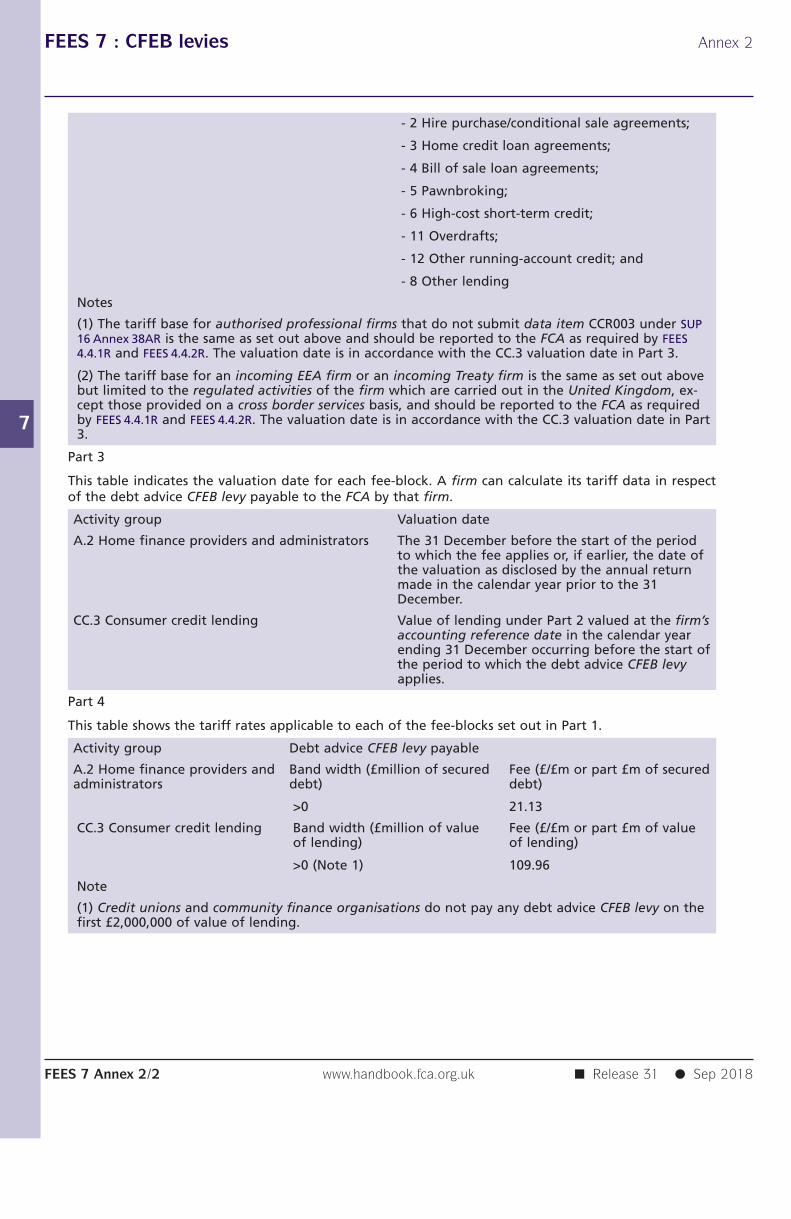

20197 Annex 2 Debt advice CFEB levy for the period from 1 April 2018 to 31 March

2019

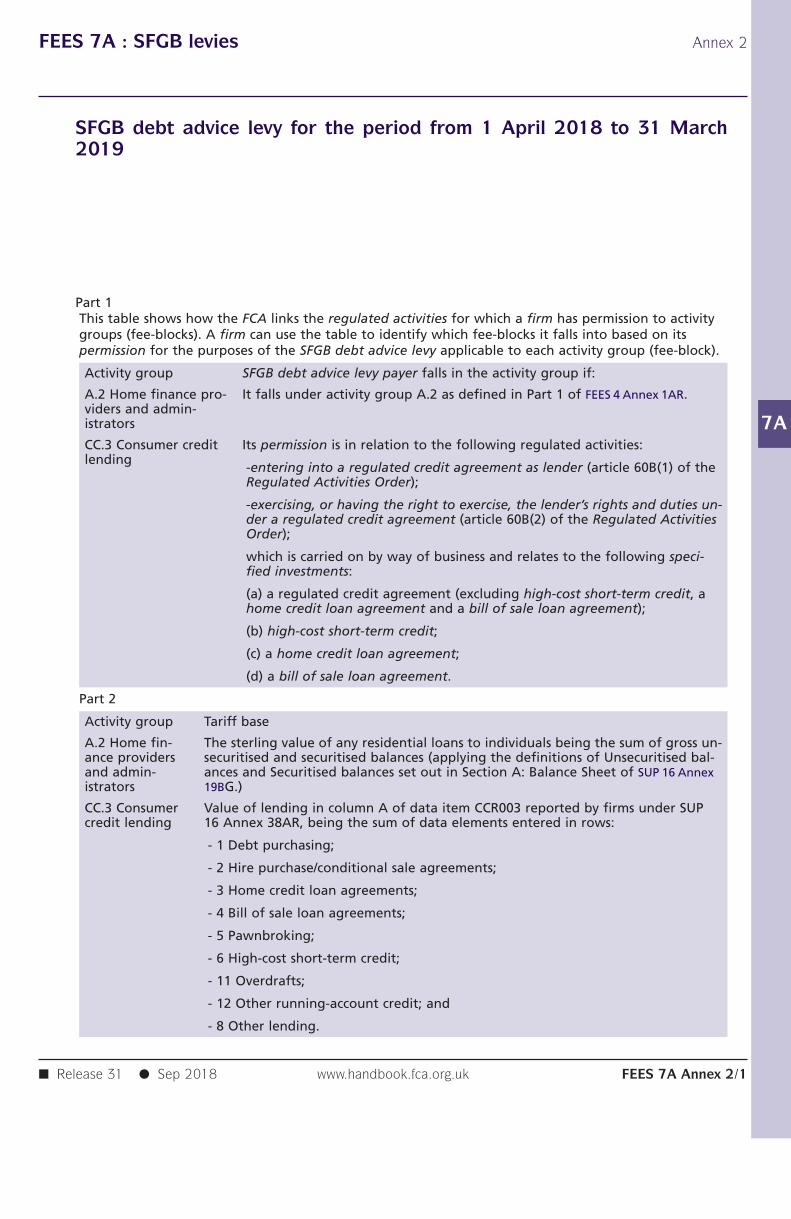

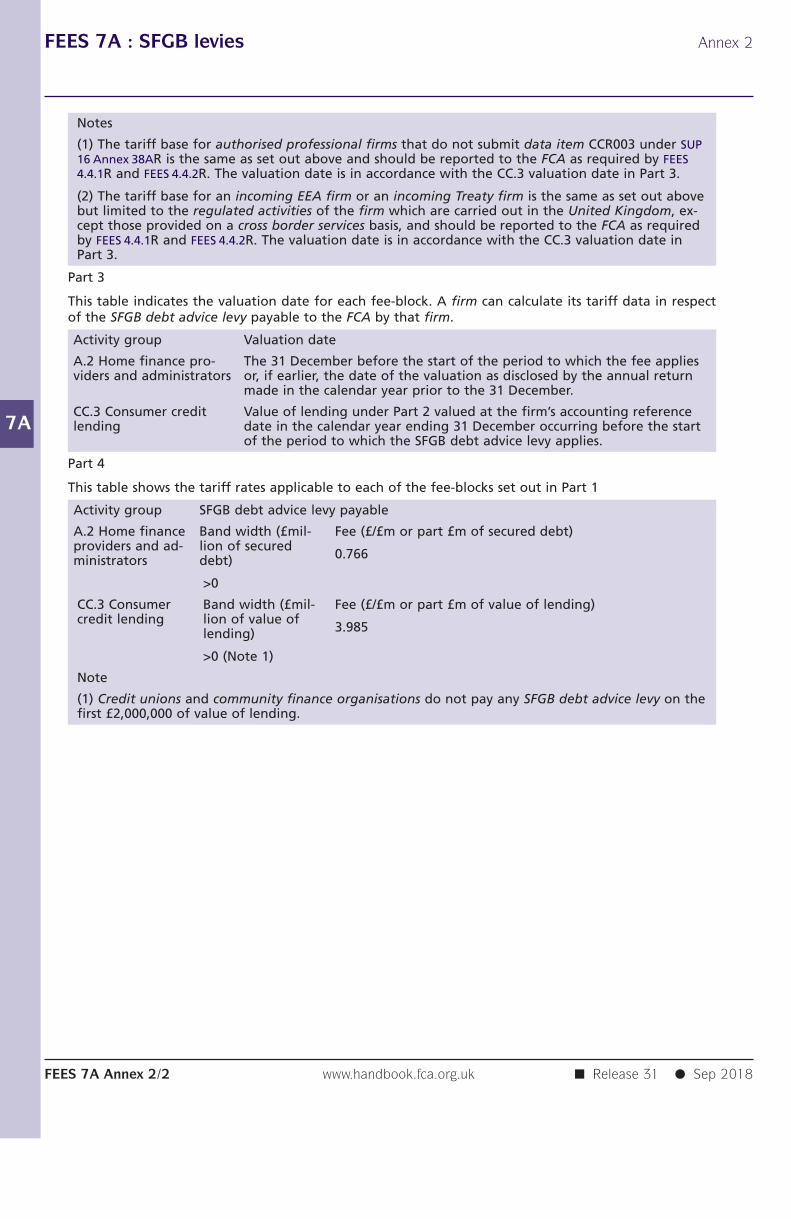

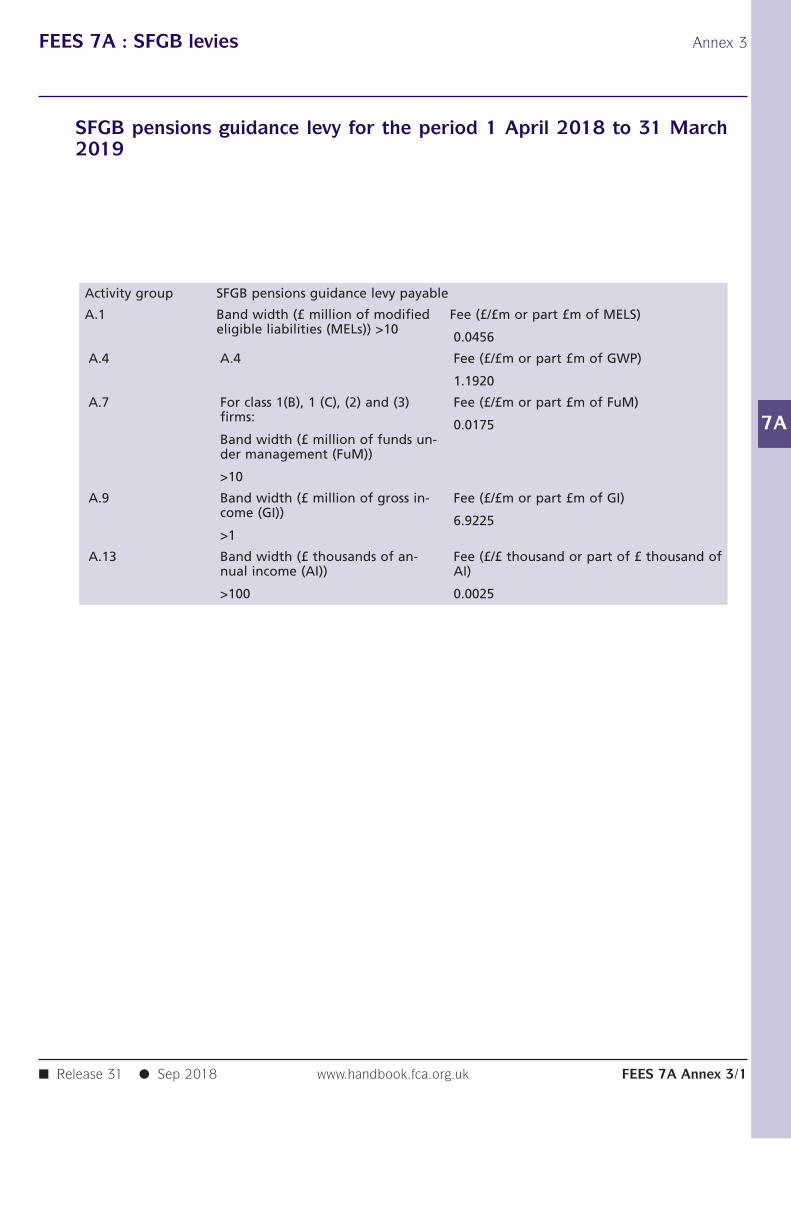

FEES 7A SFGB levies

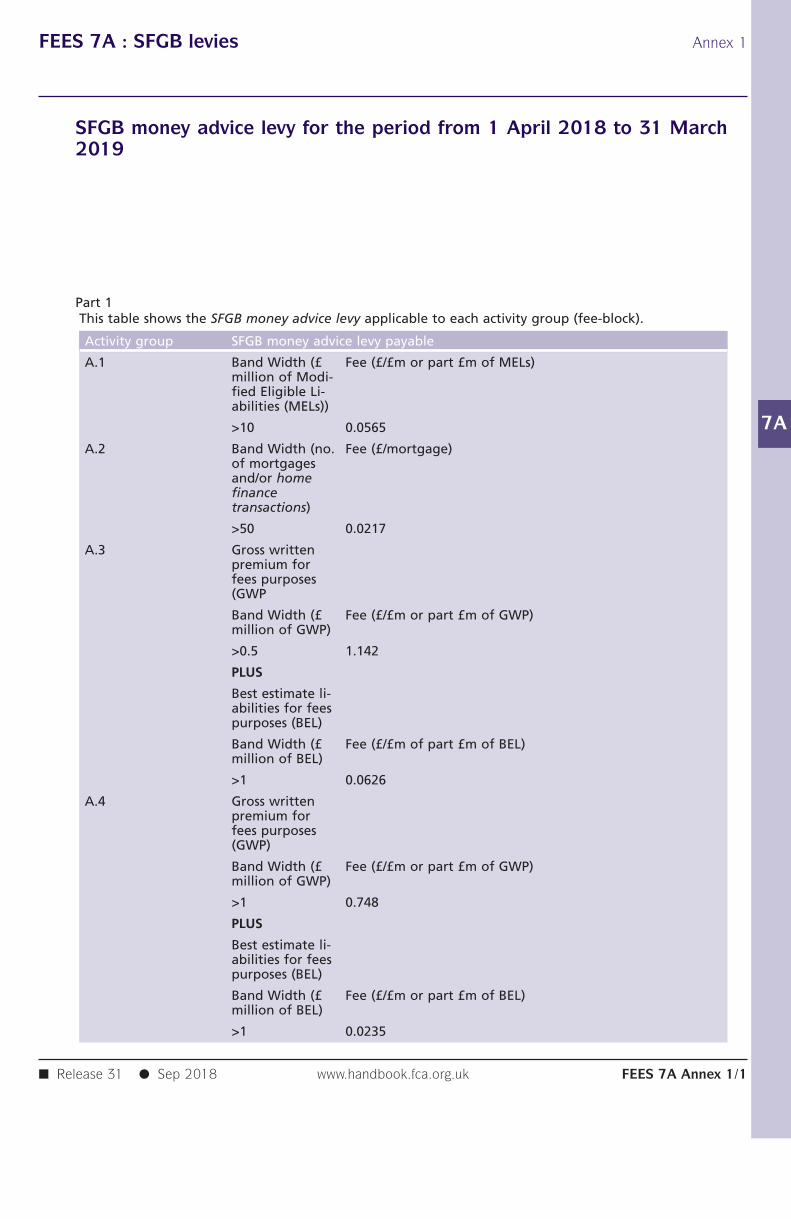

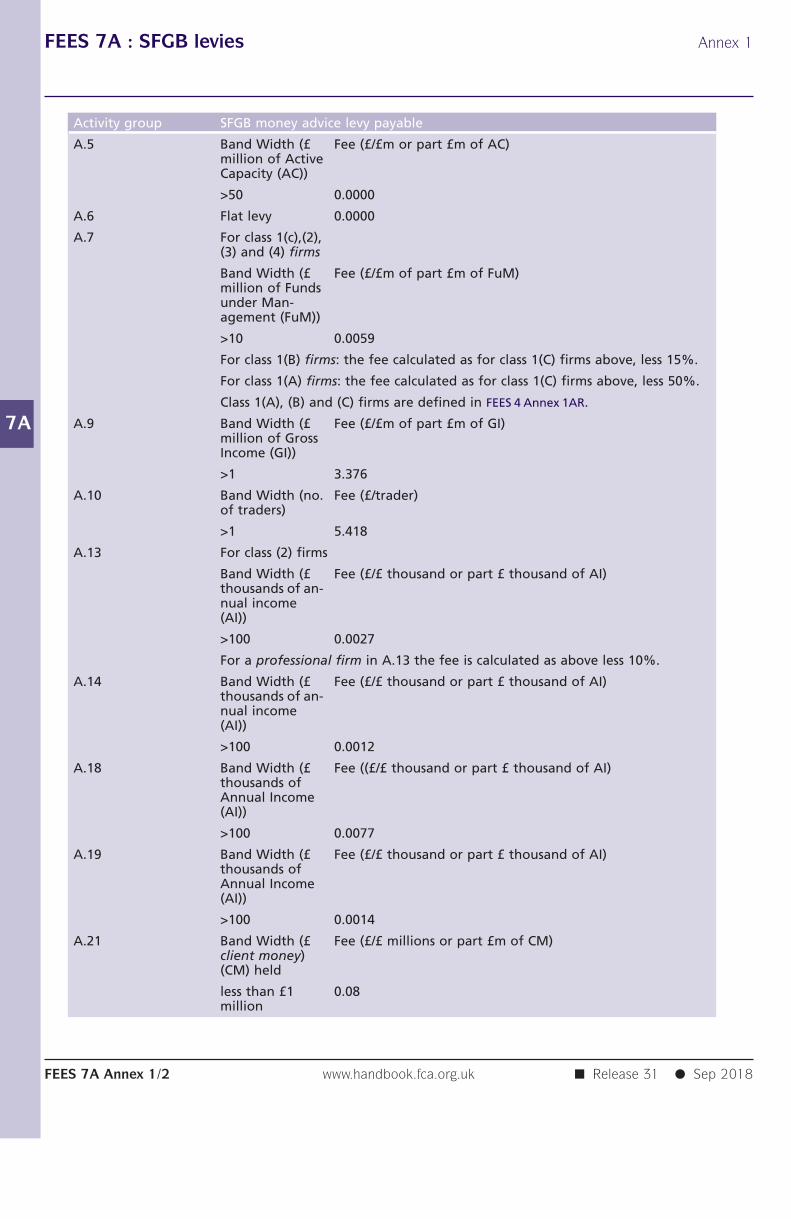

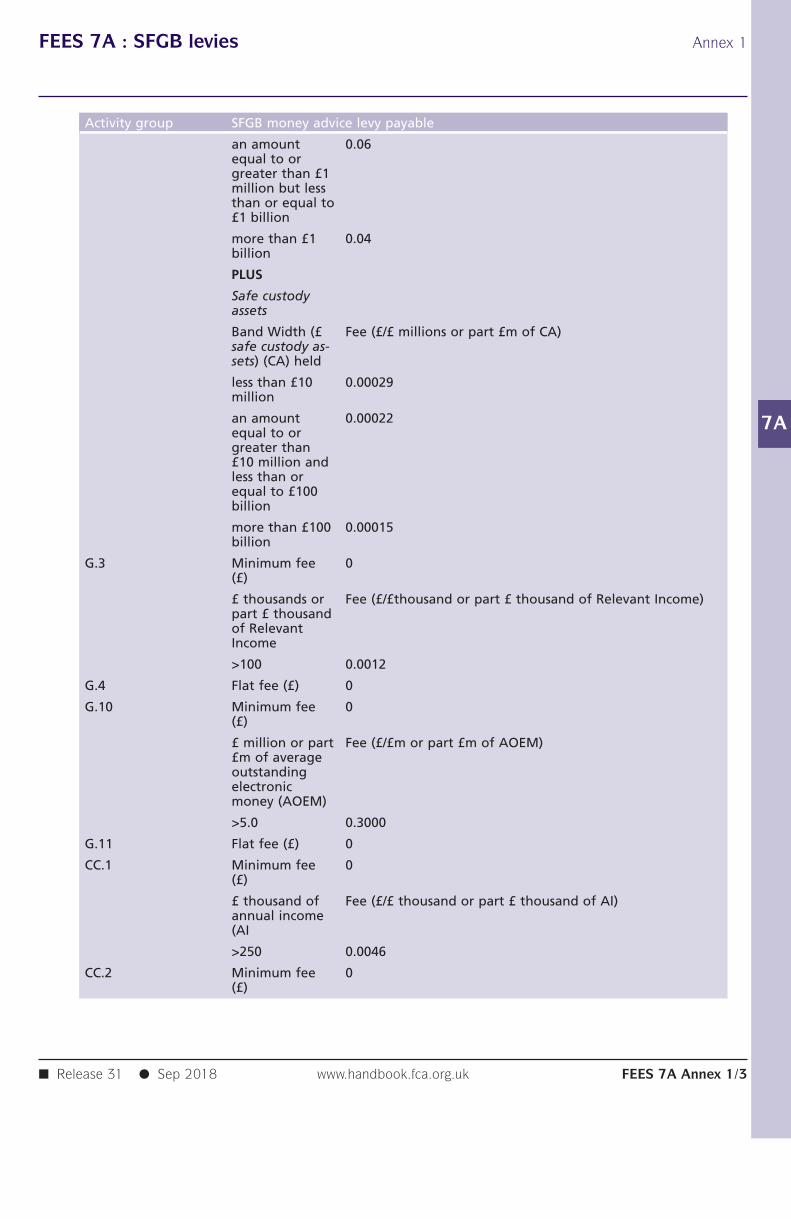

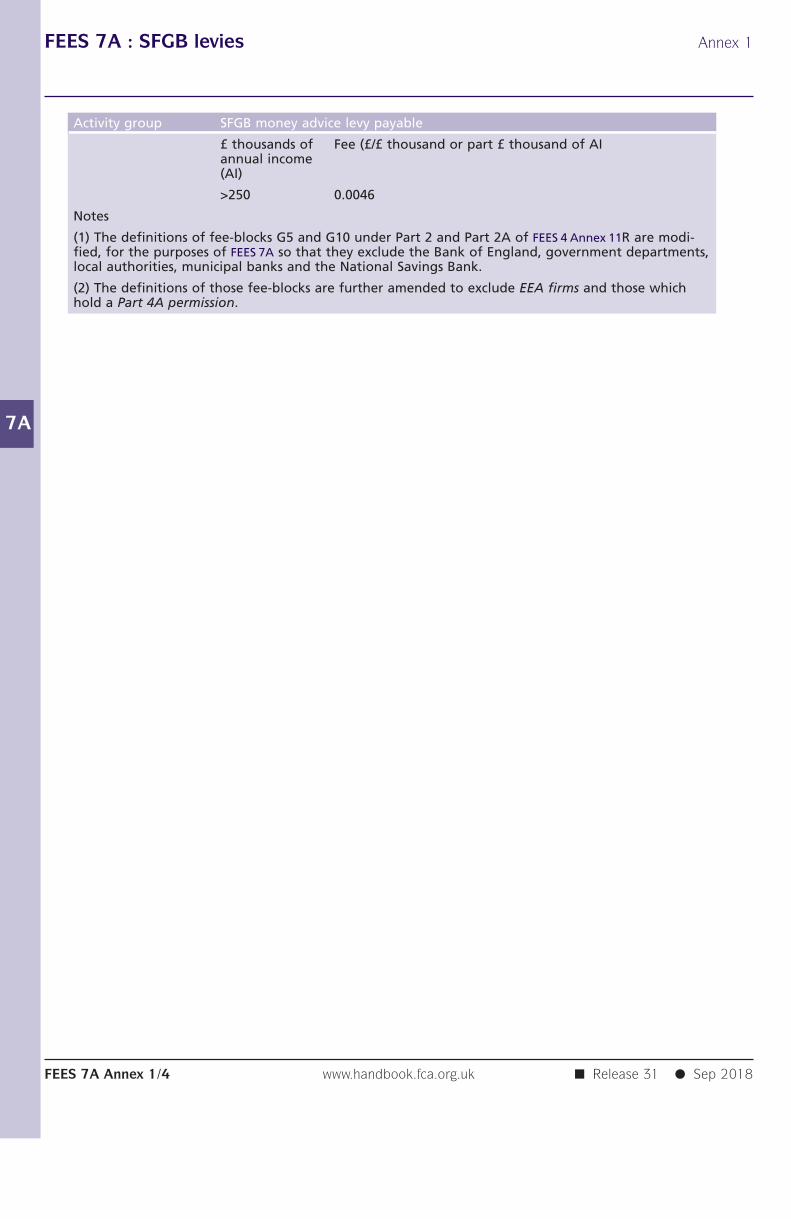

7A.1 Application and Purpose7A.2 The SFGB levy7A.3 The SFGB money advice levy and debt advice levy7A.4 The SFGB pensions guidance advice levy7A Annex 1 SFGB money advice levy for the period from 1 April 2018 to 31 March

20197A Annex 2 SFGB debt advice levy for the period from 1 April 2018 to 31 March

20197A Annex 3 SFGB pensions guidance levy for the period 1 April 2018 to 31 March

2019

FEES 8 Interim Fees

8.1 Consumer Credit permissions

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES–iii

FEES Contents

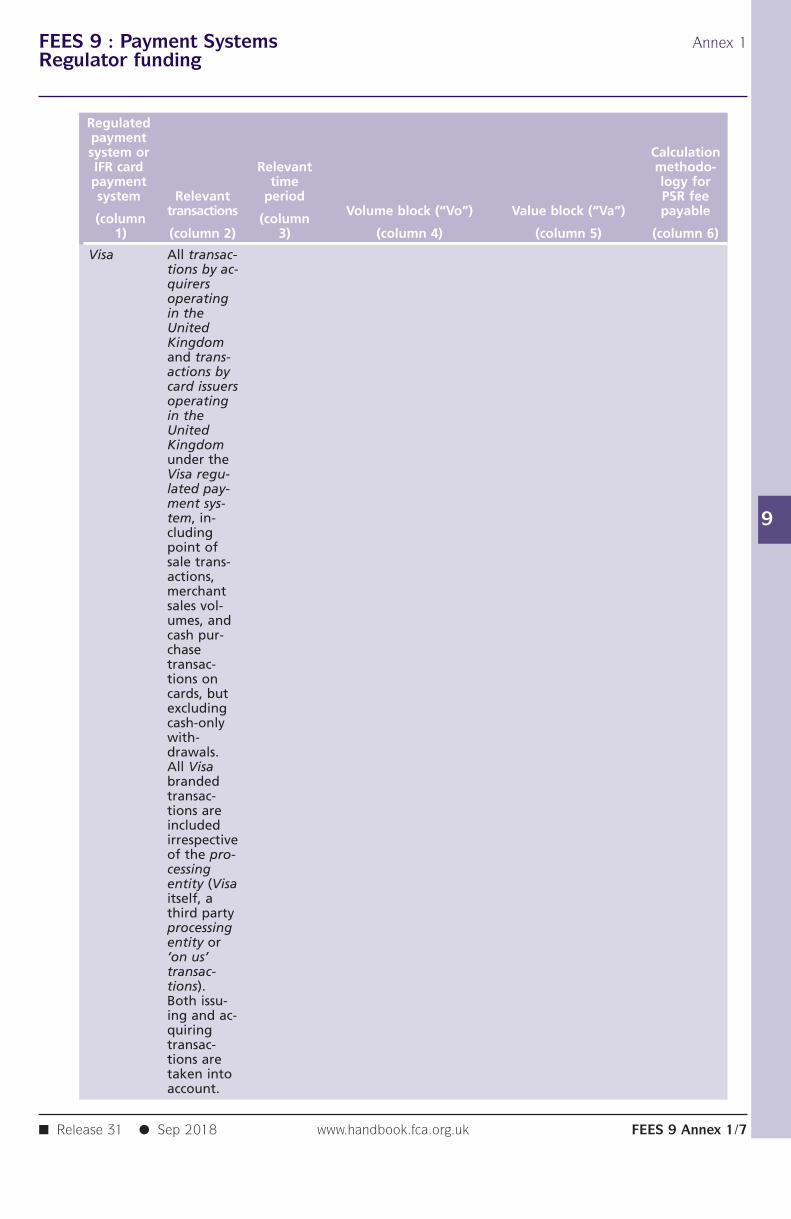

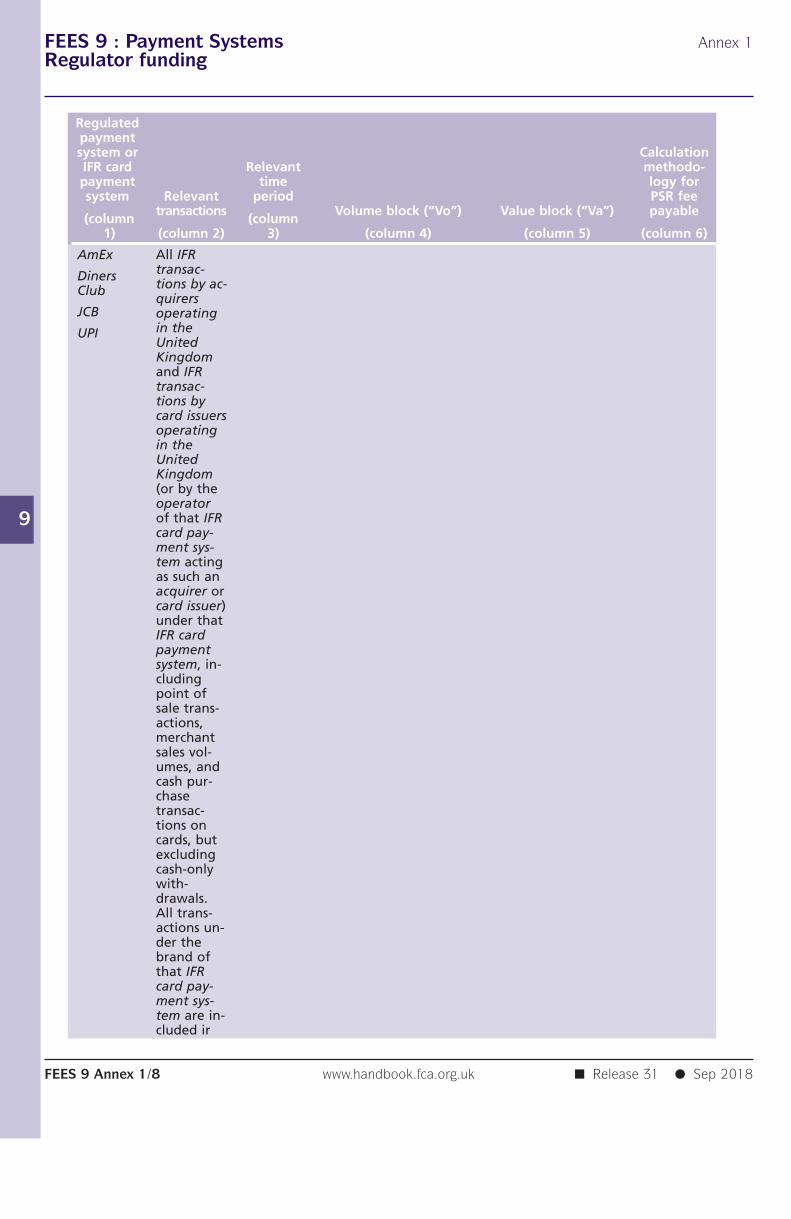

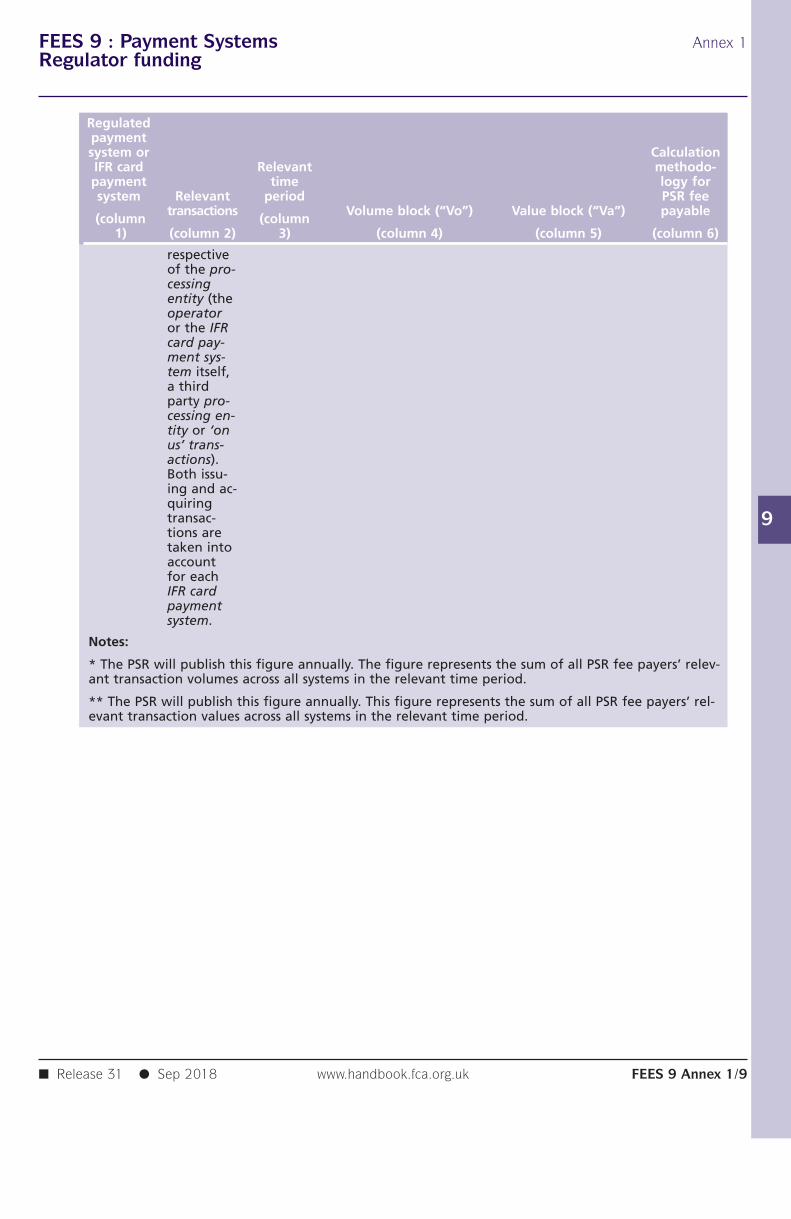

FEES 9 Payment Systems Regulator funding

9.1 Application and purpose9.2 PSR fees9 Annex 1 PSR fees methodology

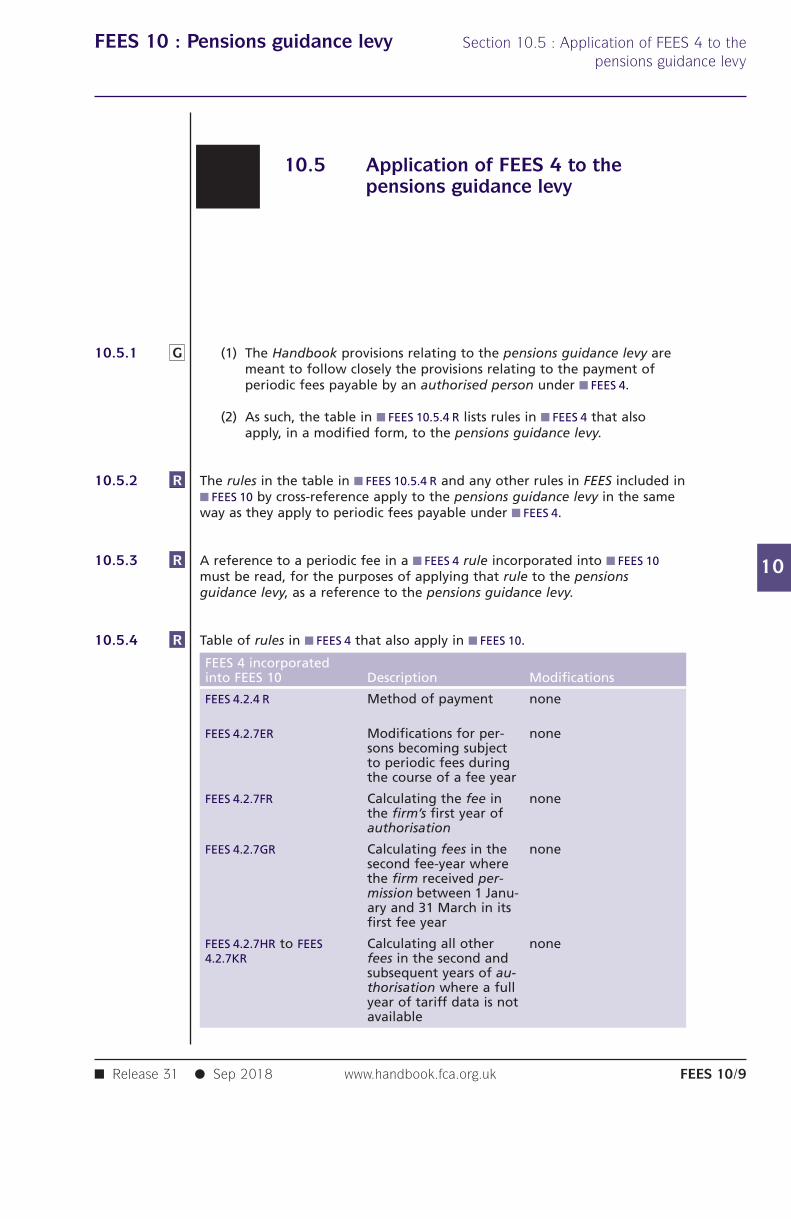

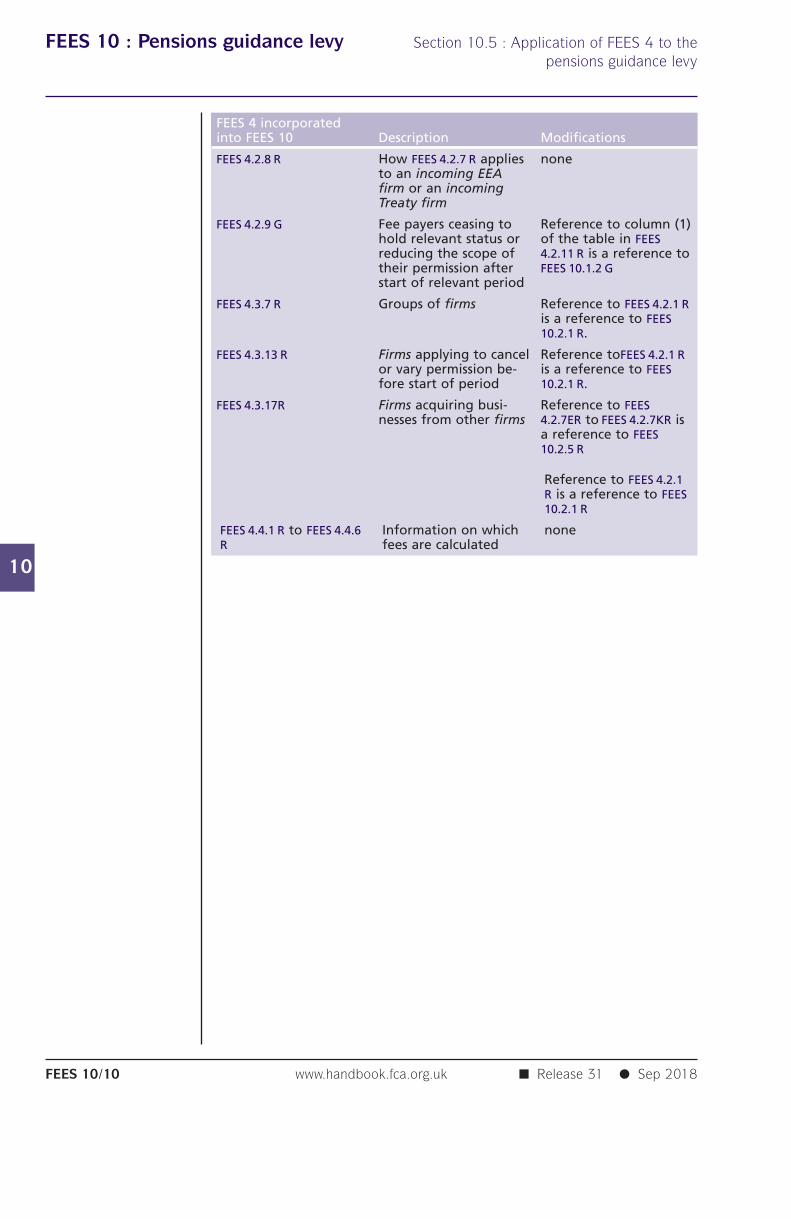

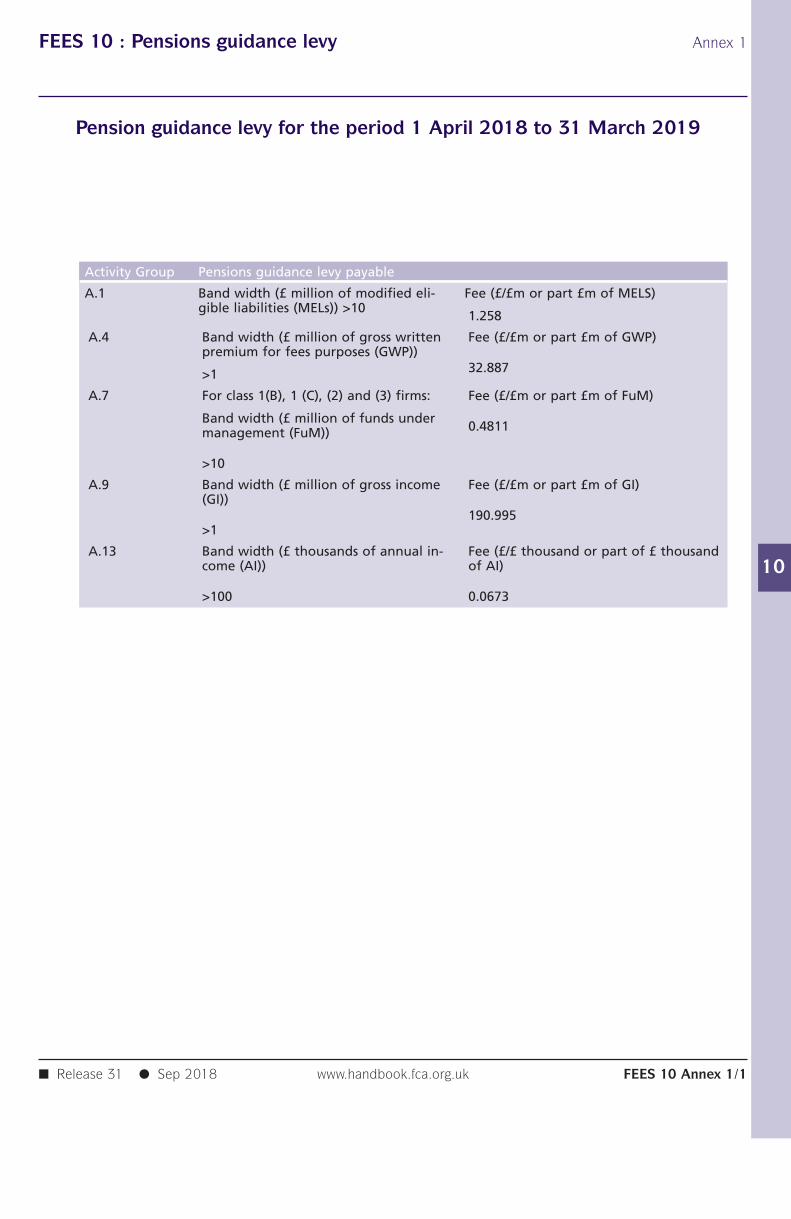

FEES 10 Pensions guidance levy

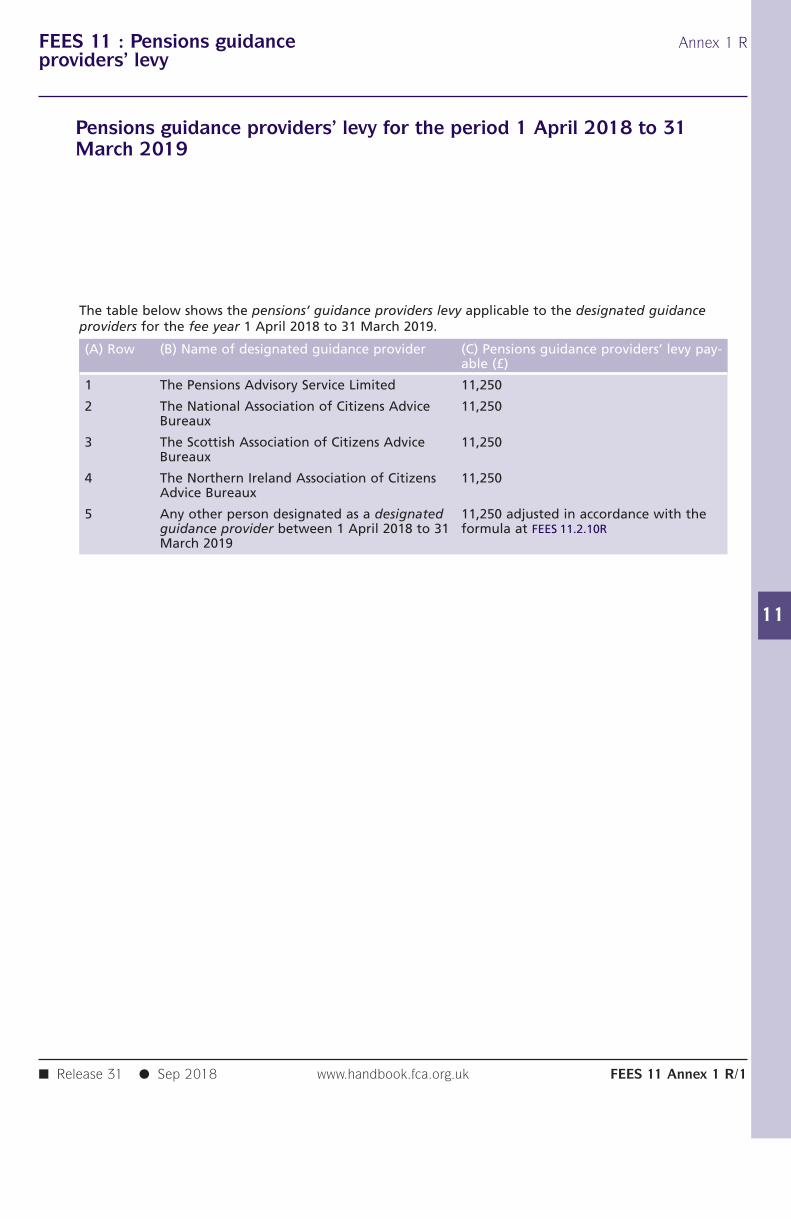

10.1 Application, purpose and background10.2 Pensions guidance levy10.3 Late payments and recovery of unpaid levies10.4 Relieving provisions10.5 Application of FEES 4 to the pensions guidance levy10 Annex 1 Pension guidance levy for the period 1 April 2018 to 31 March 2019

FEES 11 Pensions guidance providers’ levy

11.1 Application, purpose and background11.2 Pensions guidance providers’ levy11 Annex 1 R Pensions guidance providers’ levy for the period 1 April 2018 to 31

March 2019

FEES 12 FOS ADR levy

12.1 Application and Purpose12.2 FOS ADR levy12.3 Late payments and recovery of unpaid levies12.4 Relieving provisions

FEES 13 Illegal money lending levy

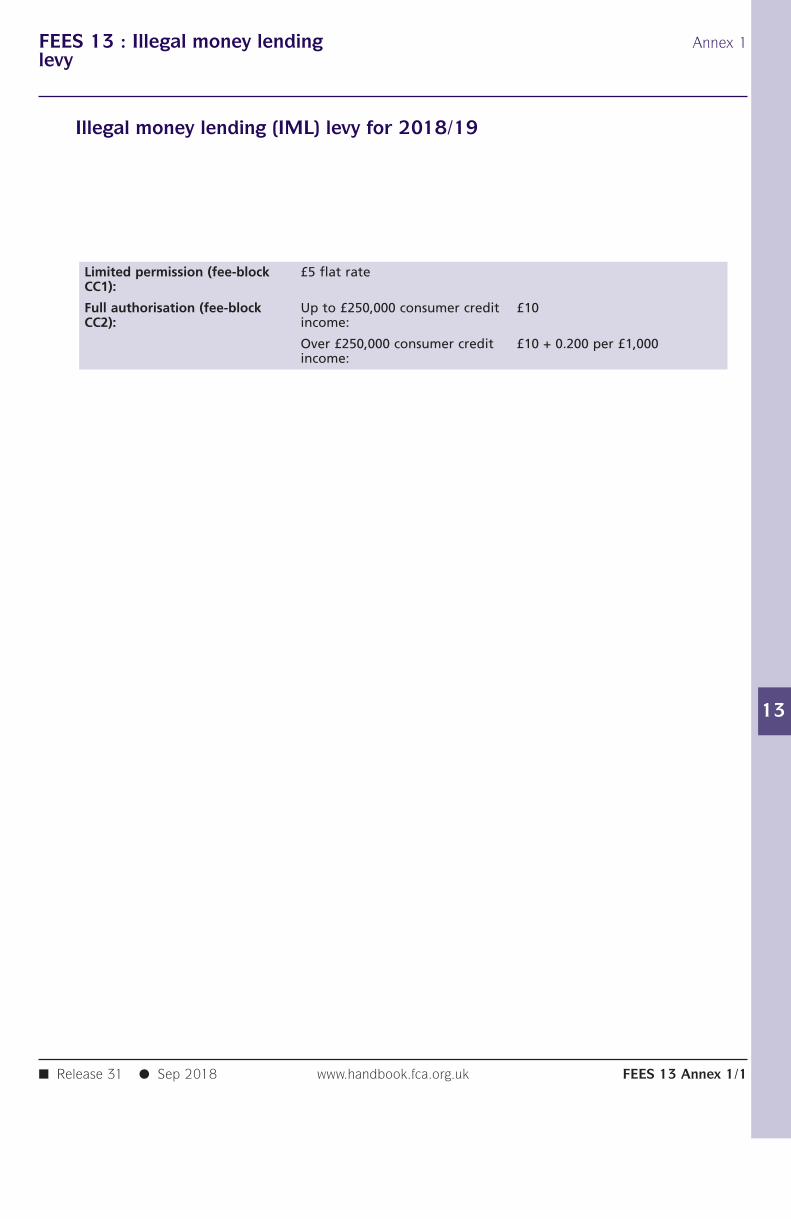

13.1 Application and purpose13.2 The IML levy13 Annex 1 Illegal money lending (IML) levy for 2018/19

FEES App 1 Unauthorised Mutuals Registration Fees Rules

App 1.1 IntroductionApp 1.2 Periodic FeesApp 1.3 Application FeesApp 1 Annex 1 Periodic fees payable for the period 1 April 2018 to 31 March 2019App 1 Annex 1A Application Fees payableApp 1 Annex 2 Further information on feesApp 1 Annex 3 EmergenciesApp 1 Annex 4 Glossary of definitions

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES–iv

FEES Contents

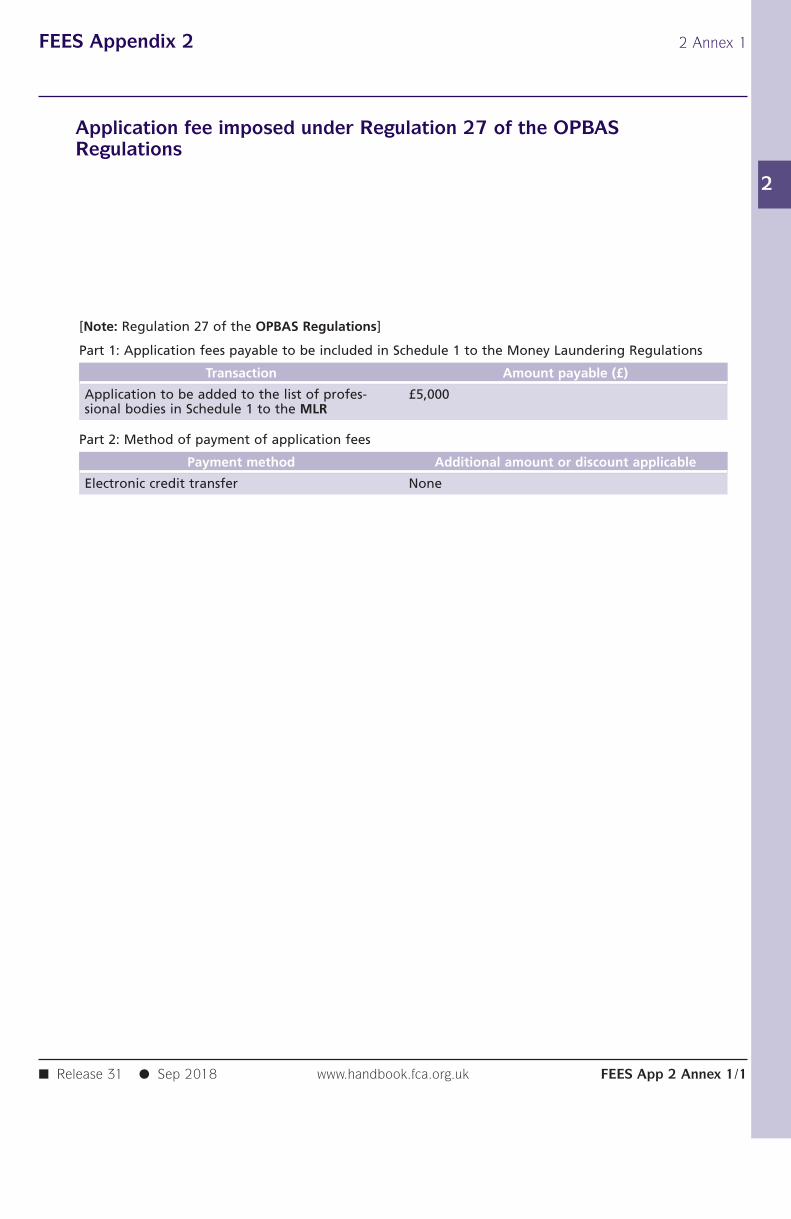

FEES App 2 Office for professional body anti-money laundering supervisionfees

App 2.1 IntroductionApp 2.2 Application fees imposed under Regulation 27 of the OPBAS

RegulationsApp 2.3 Periodic fees imposed under Regulation 27 of the OPBAS RegulationsApp 2 Annex 1 Application fee imposed under Regulation 27 of the OPBAS RegulationsApp 2 Annex 2 Periodic fees imposed under Regulation 27 of the OPBAS Regulations

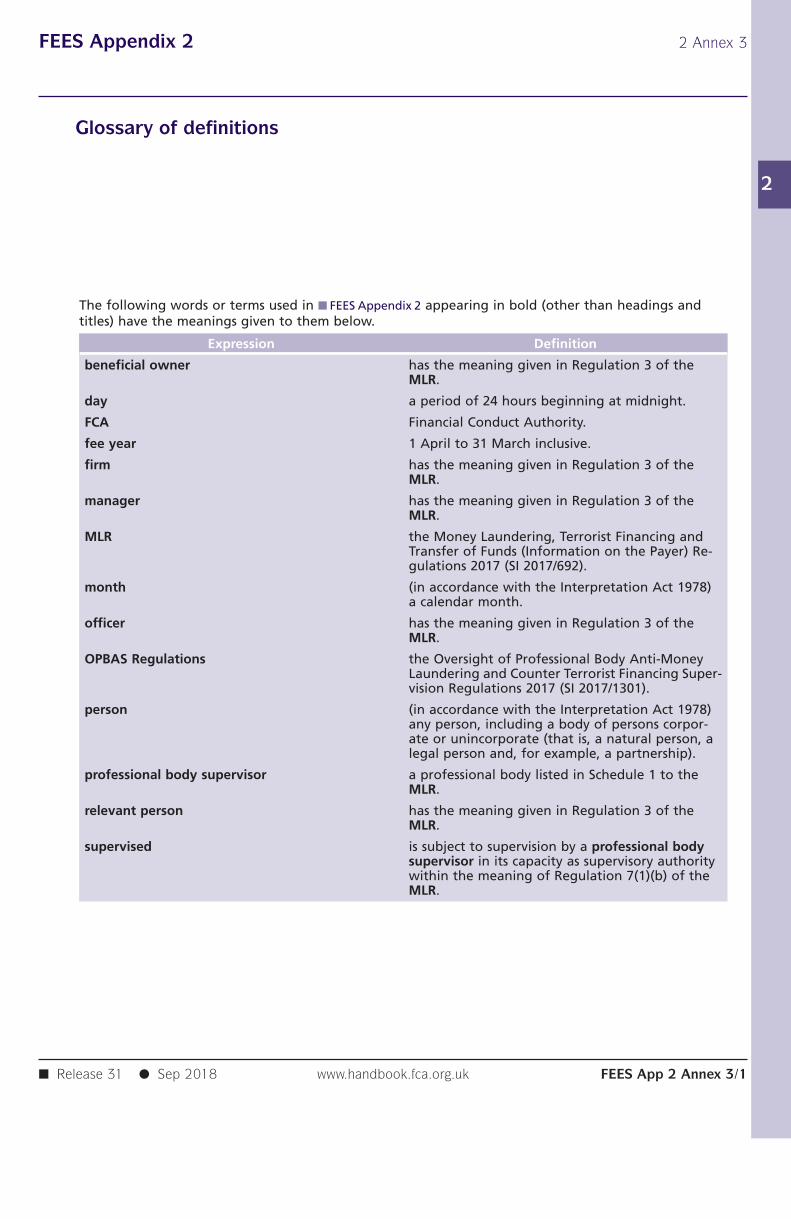

for the period 1 April 2019 to 31 March 2020App 2 Annex 3 Glossary of definitions

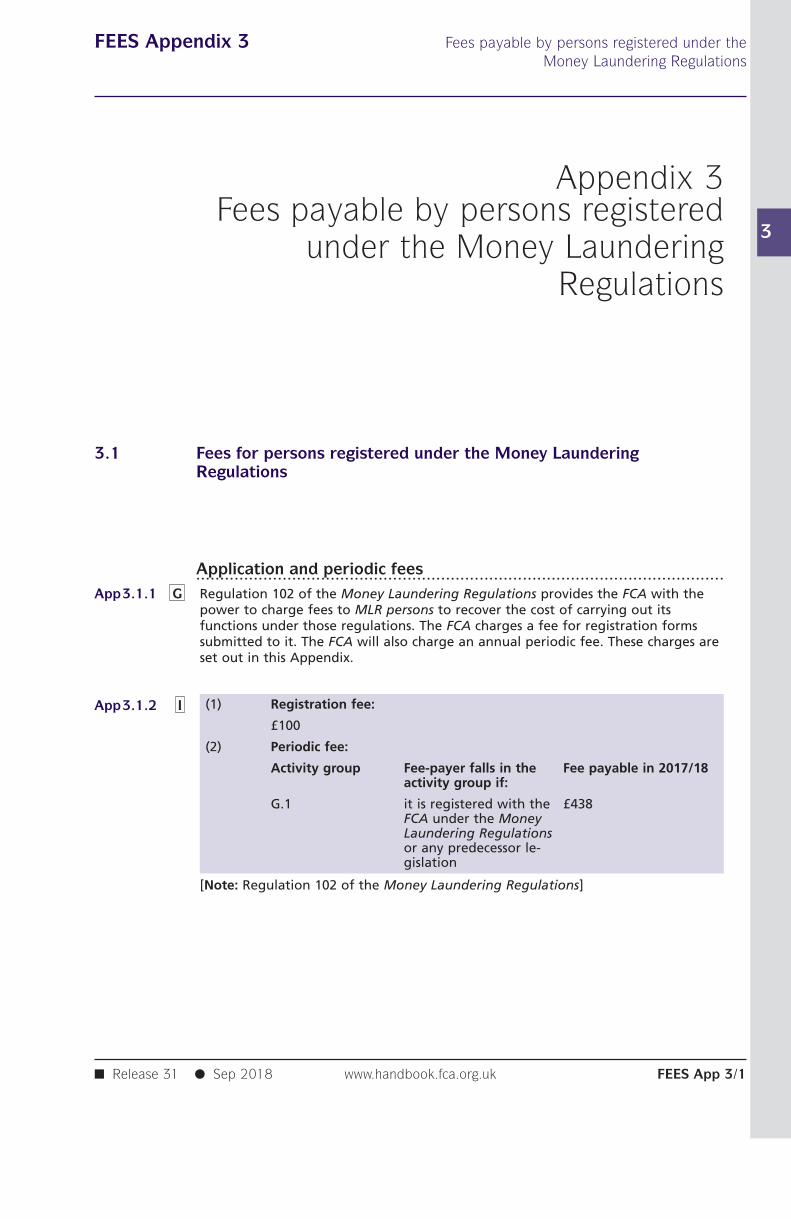

FEES App 3 Fees payable by persons registered under the Money LaunderingRegulations

App 3.1 Fees for persons registered under the Money Laundering Regulations

Transitional provisions and Schedules

TP 1 Transitional ProvisionsTP 2 Transitional provisions relating to changes to the FSCS levy

arrangements taking effect in 2007/8 and in 2008/9TP 3 Transitional provisions relating to changes to the FSCS levy

arrangements taking effect in 2010/11TP 4 Transitional provisions relating to information requirements following

changes to FEES 4 or 5TP 5 Transitional Provisions relating to the Special Project Fee for

RestructuringTP 7 Transitional provisions relating to changes to the FSCS levy

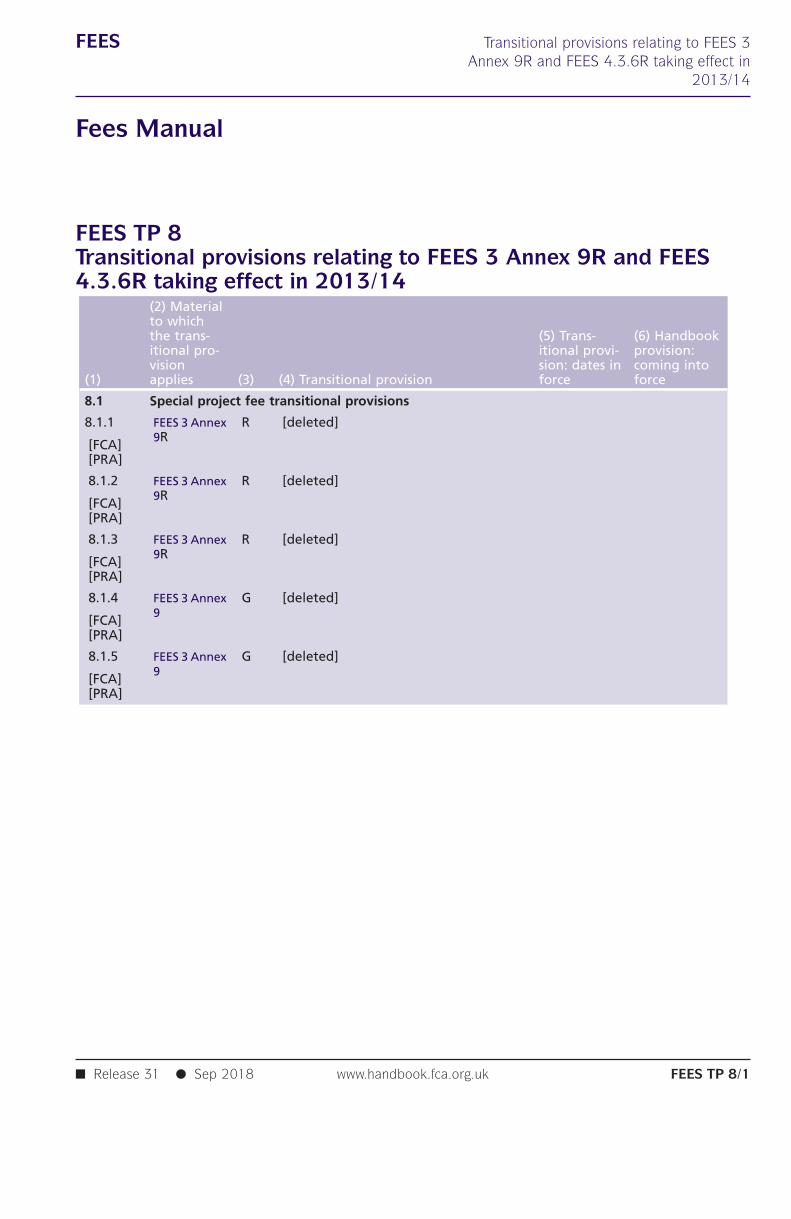

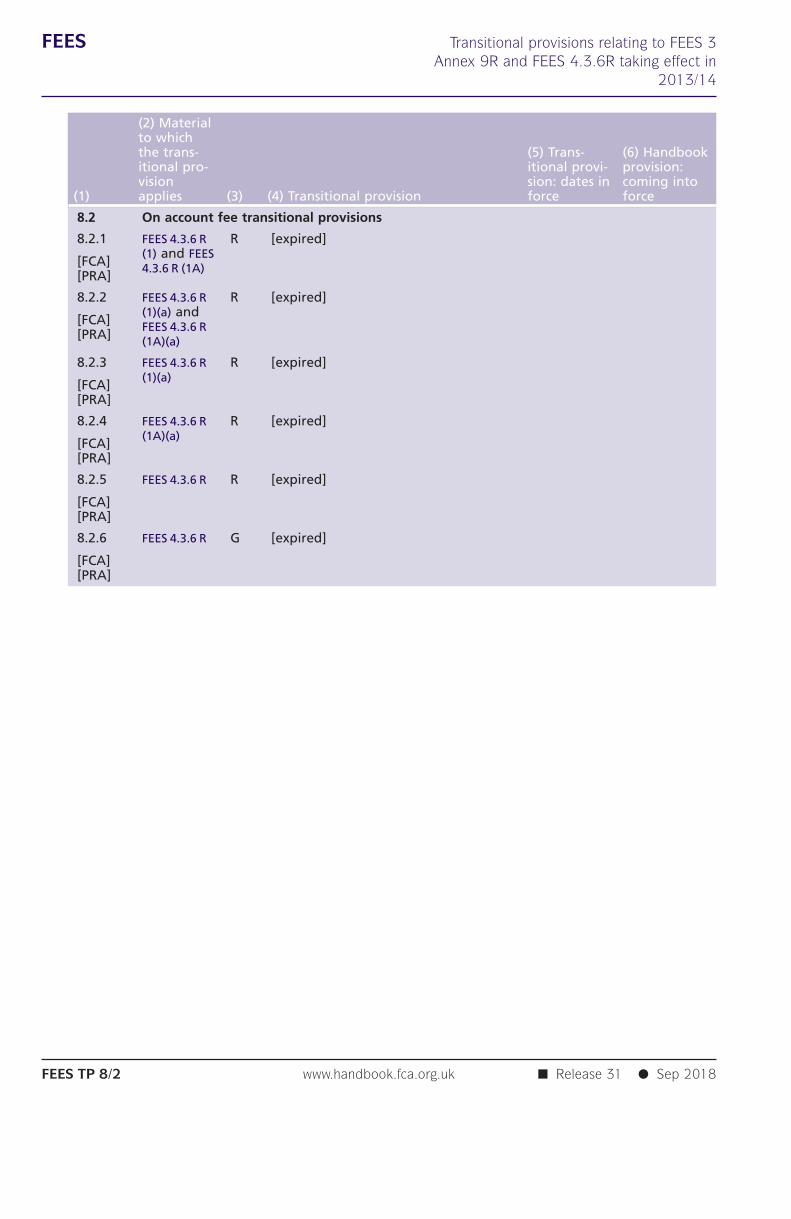

arrangements taking effect in 2013/14TP 8 Transitional provisions relating to FEES 3 Annex 9R and FEES 4.3.6R

taking effect in 2013/14TP 9 Transitional arrangements in relation to amendments introduced by the

Compensation Sourcebook (Investments by Large UnincorporatedAssociations and Certain Large Partnerships) Instrument 2013

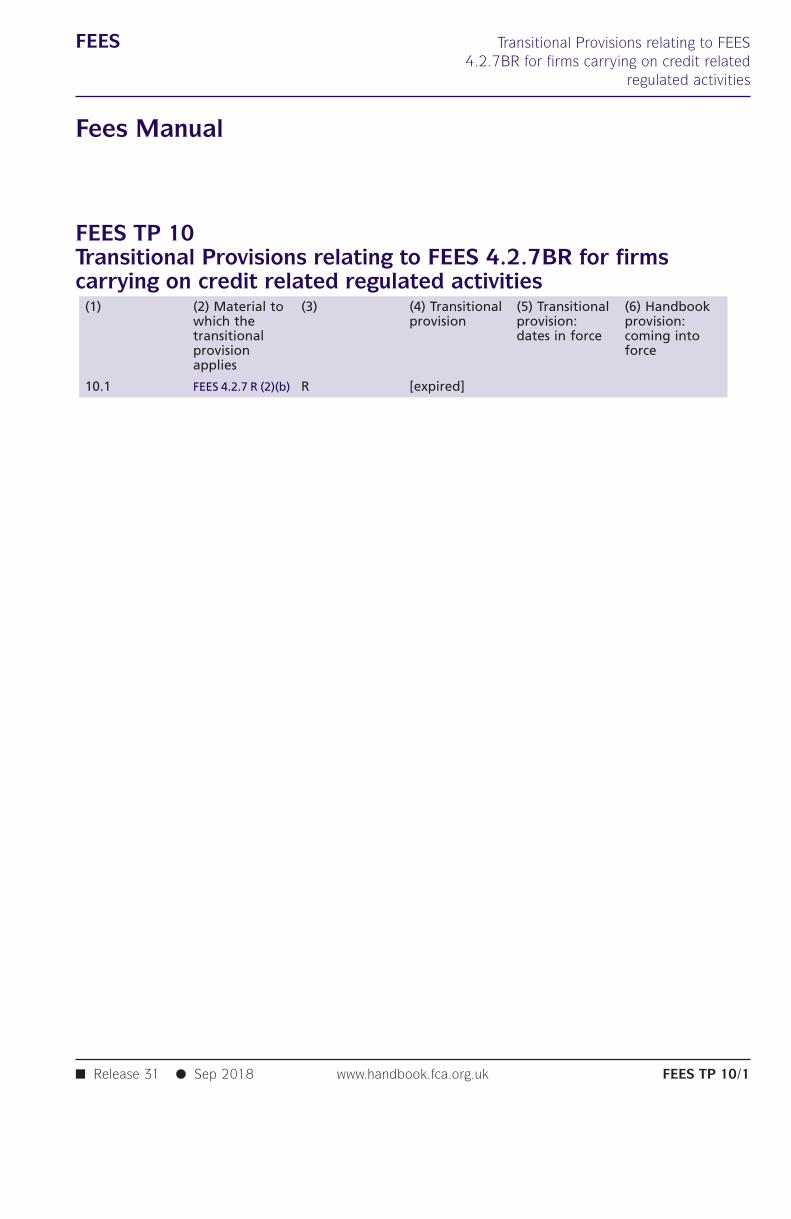

TP 10 Transitional Provisions relating to FEES 4.2.7BR for firms carrying oncredit related regulated activities

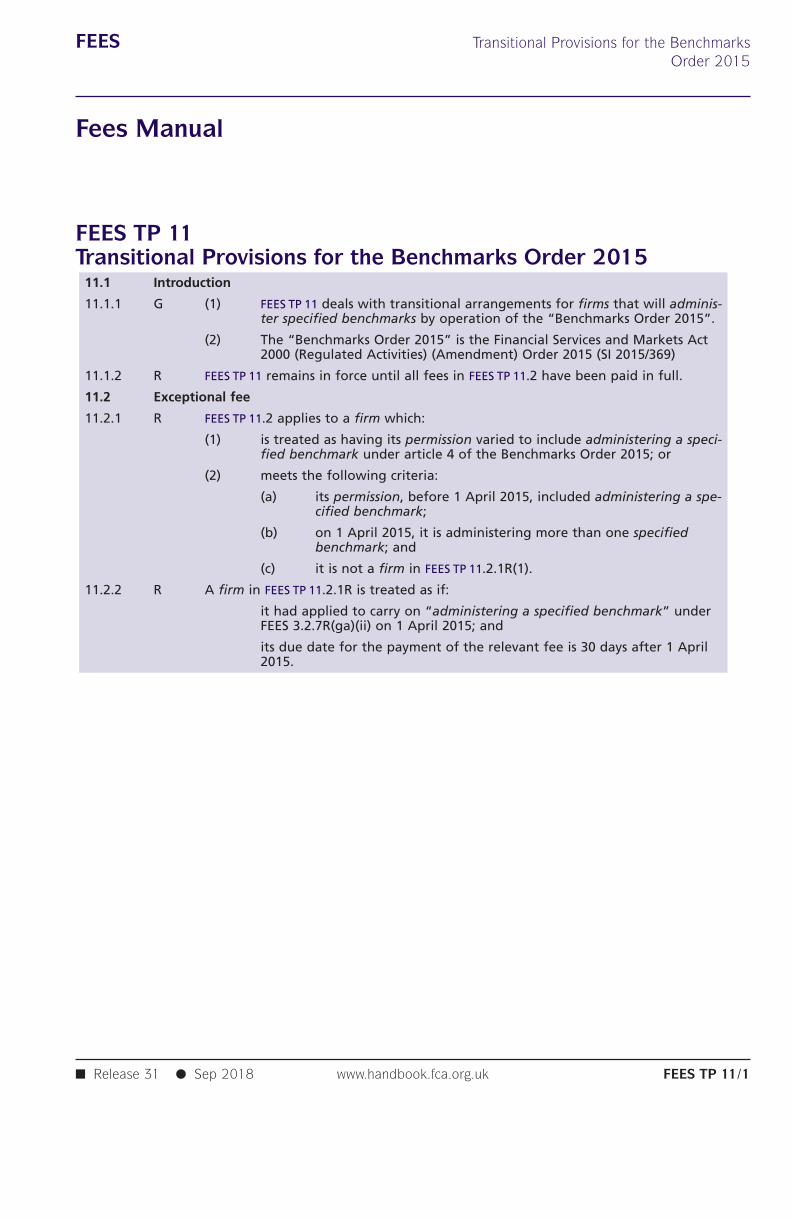

TP 11 Transitional Provisions for the Benchmarks Order 2015TP 13 Transitional provisions relating to the calculation of tariff bases for

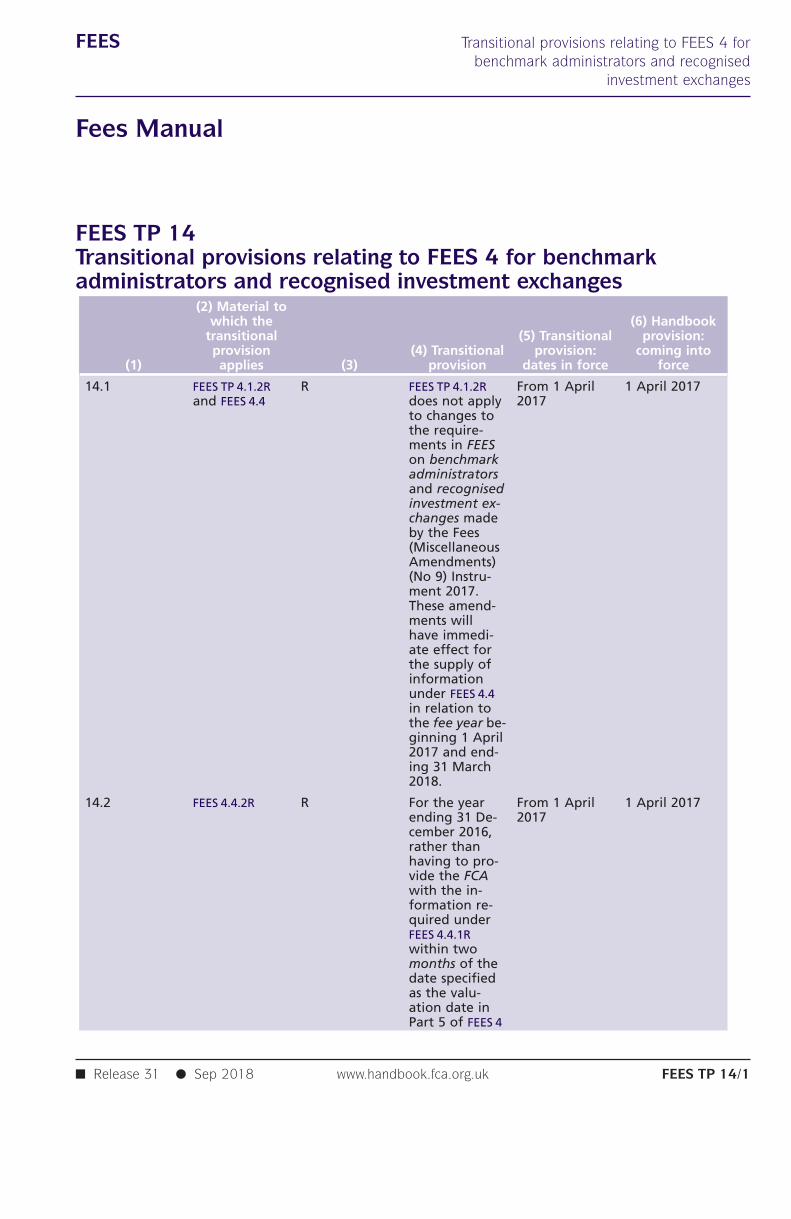

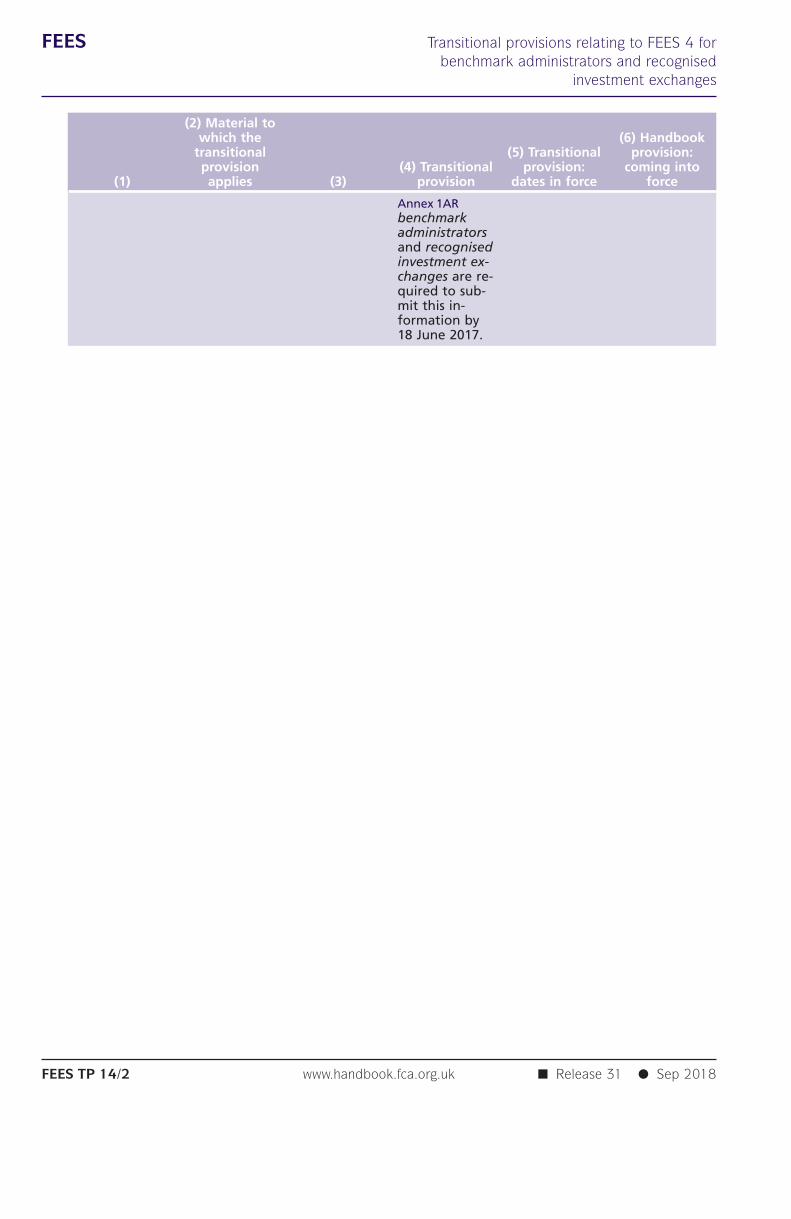

insurersTP 14 Transitional provisions relating to FEES 4 for benchmark administrators

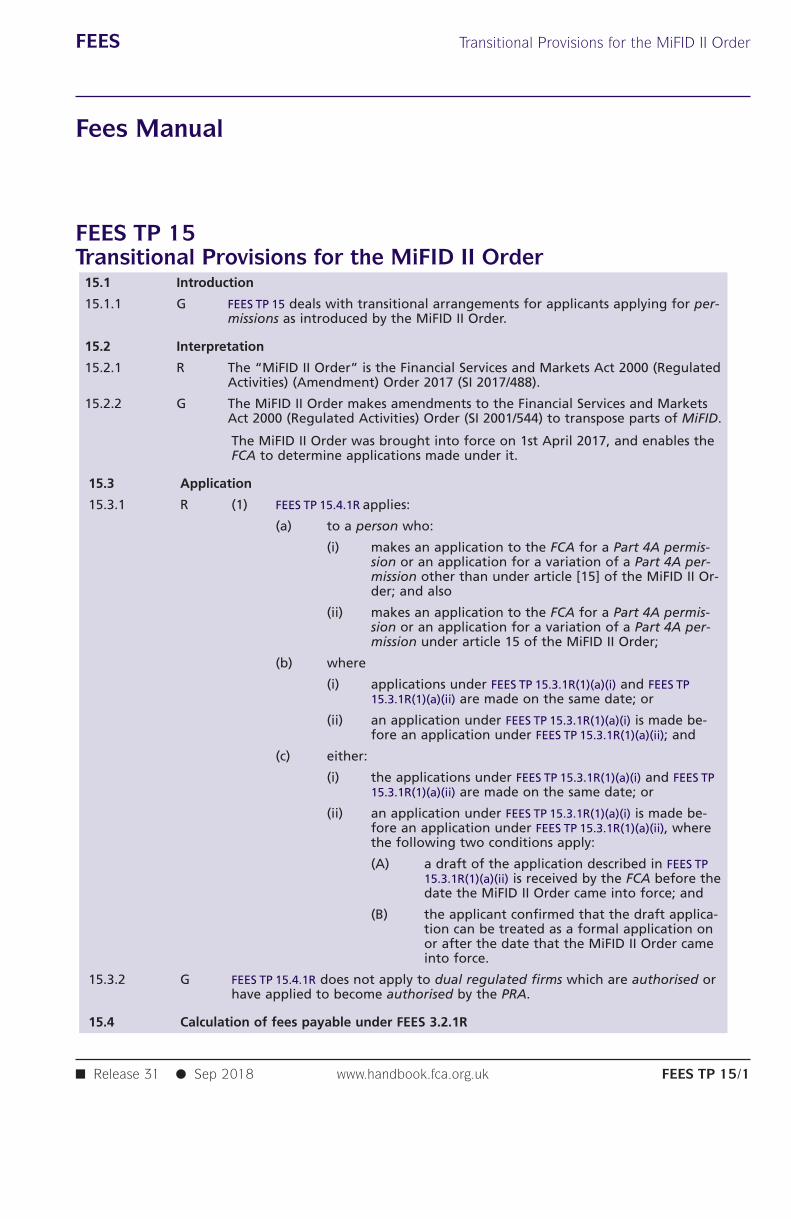

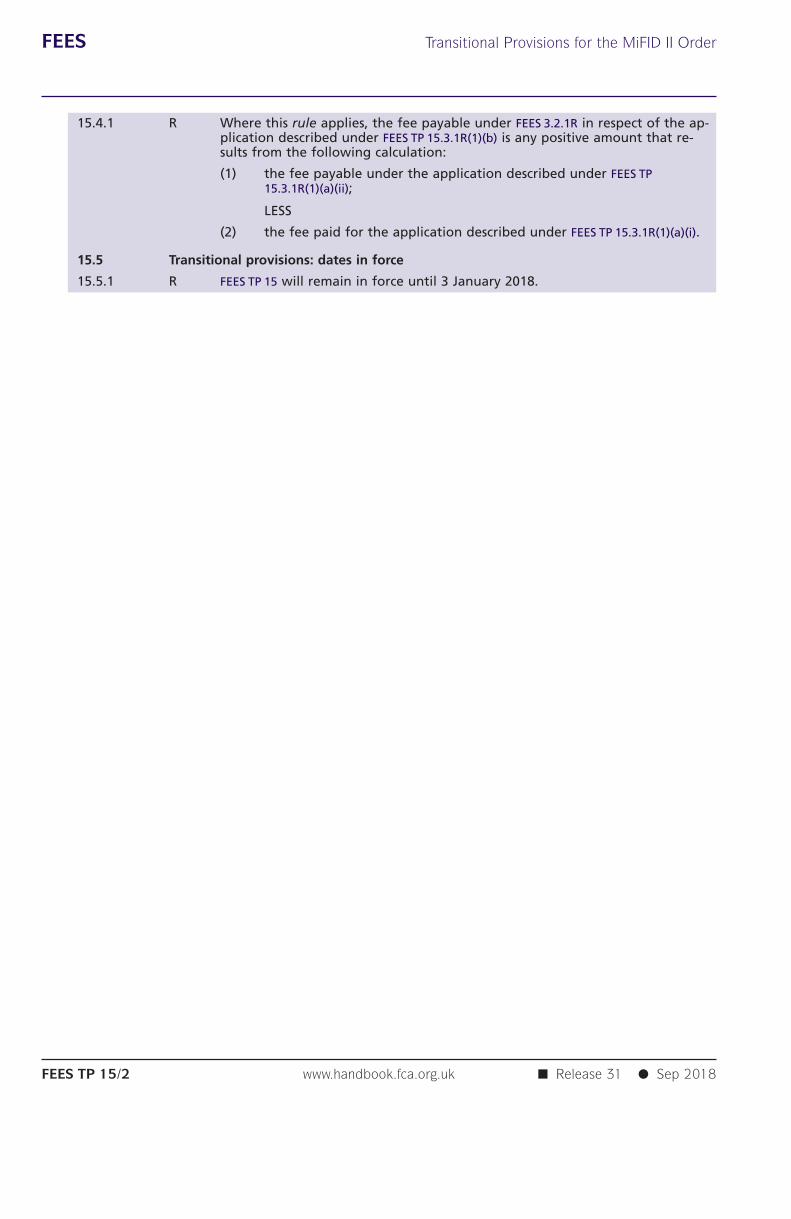

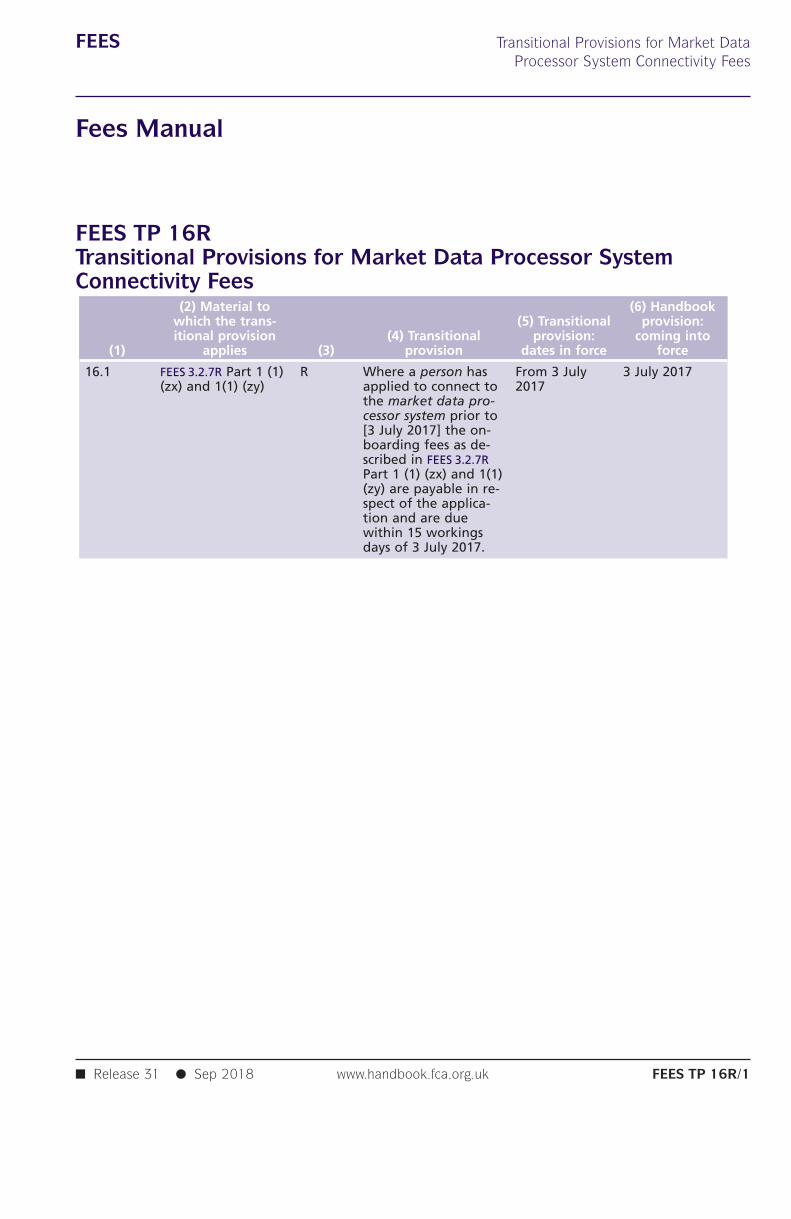

and recognised investment exchangesTP 15 Transitional Provisions for the MiFID II OrderTP 16R Transitional Provisions for Market Data Processor System Connectivity

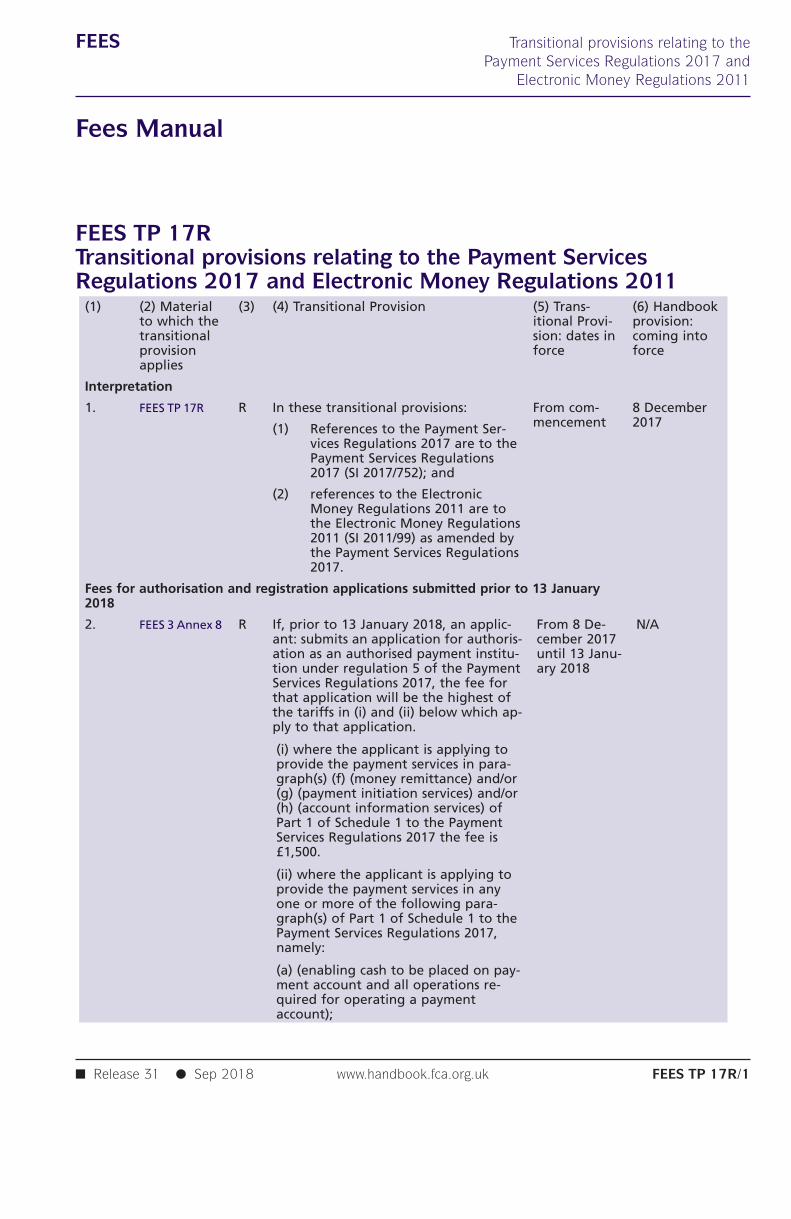

FeesTP 17R Transitional provisions relating to the Payment Services Regulations

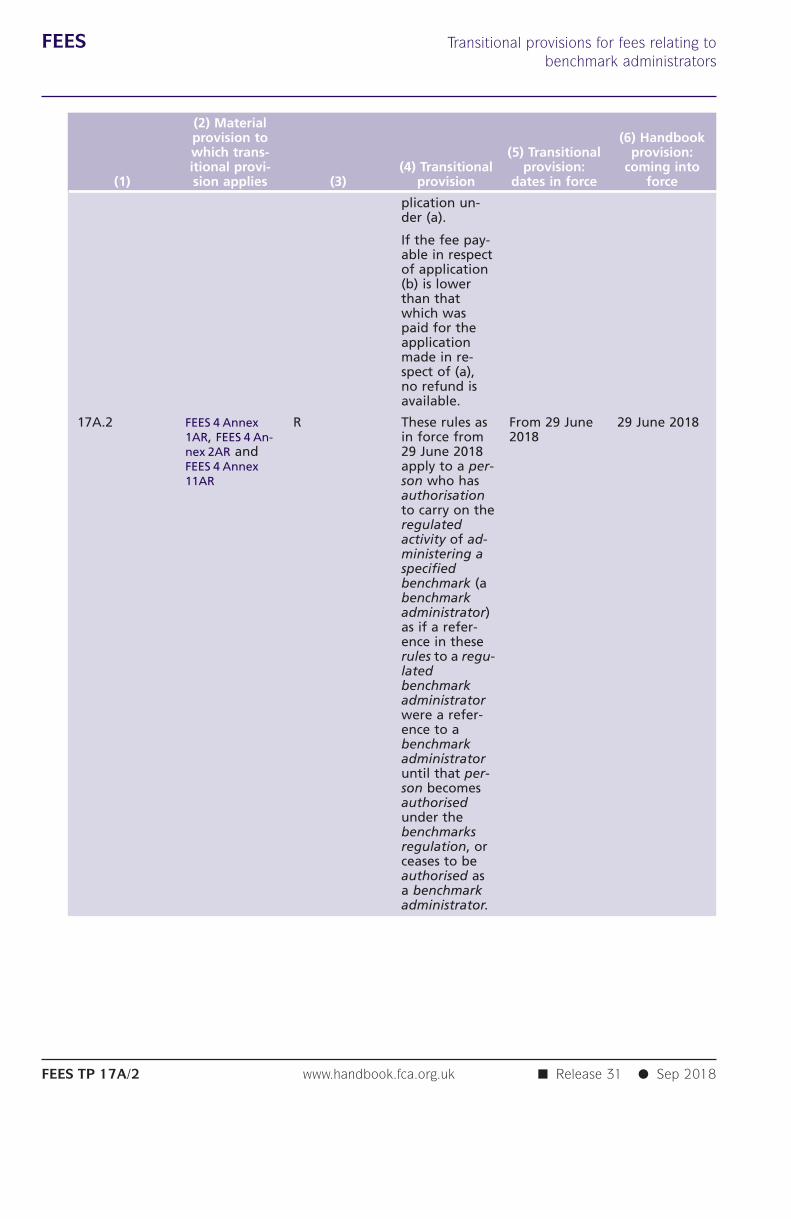

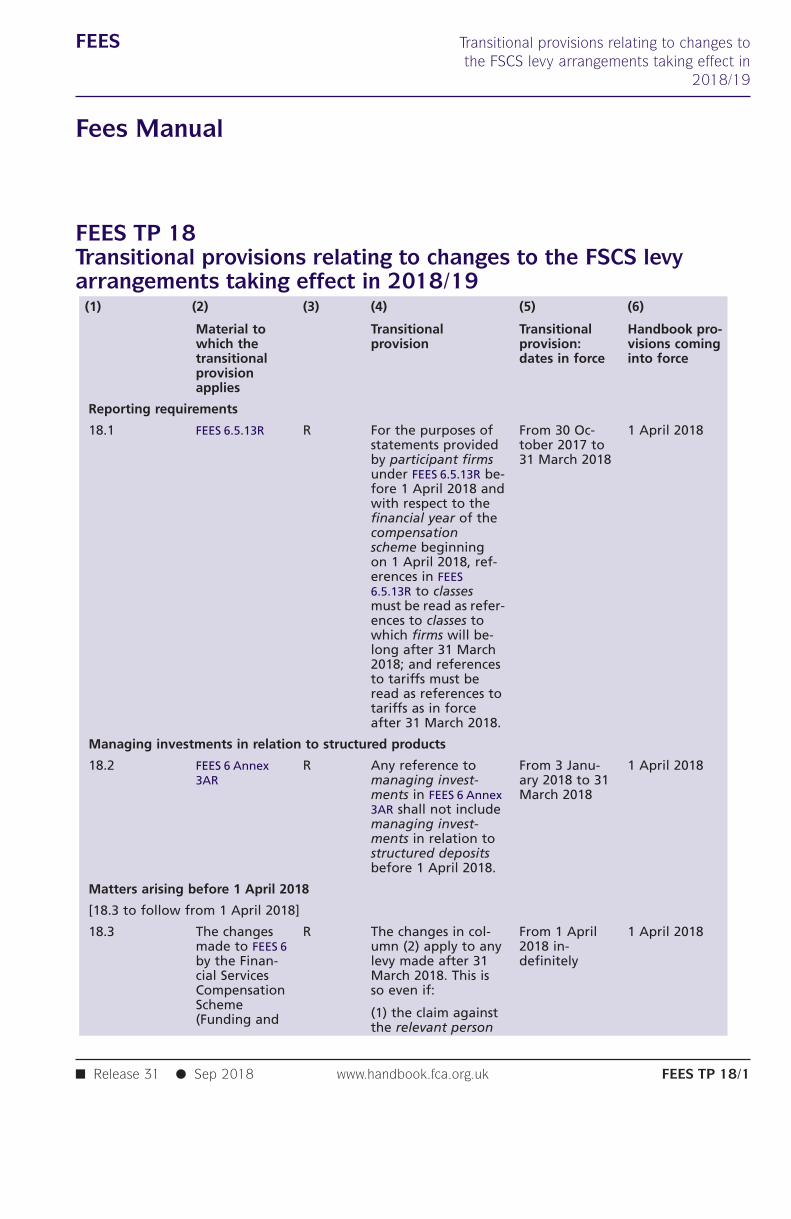

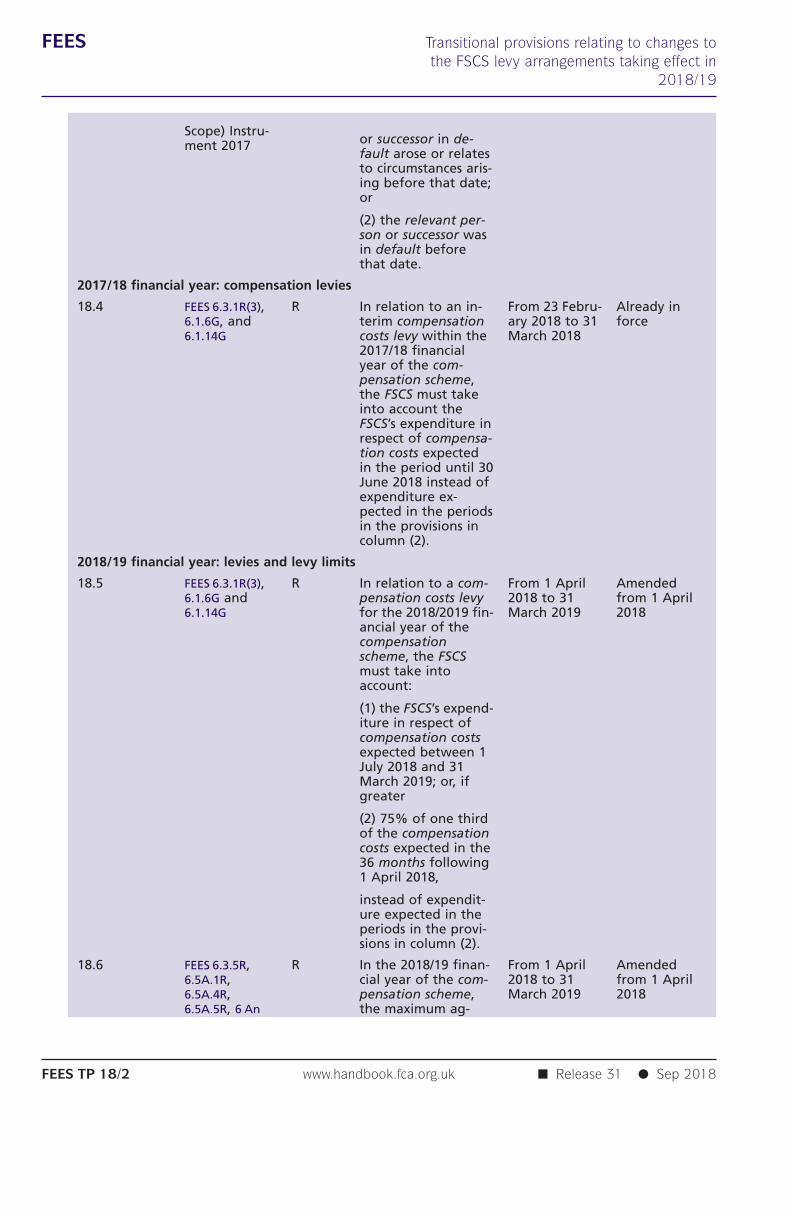

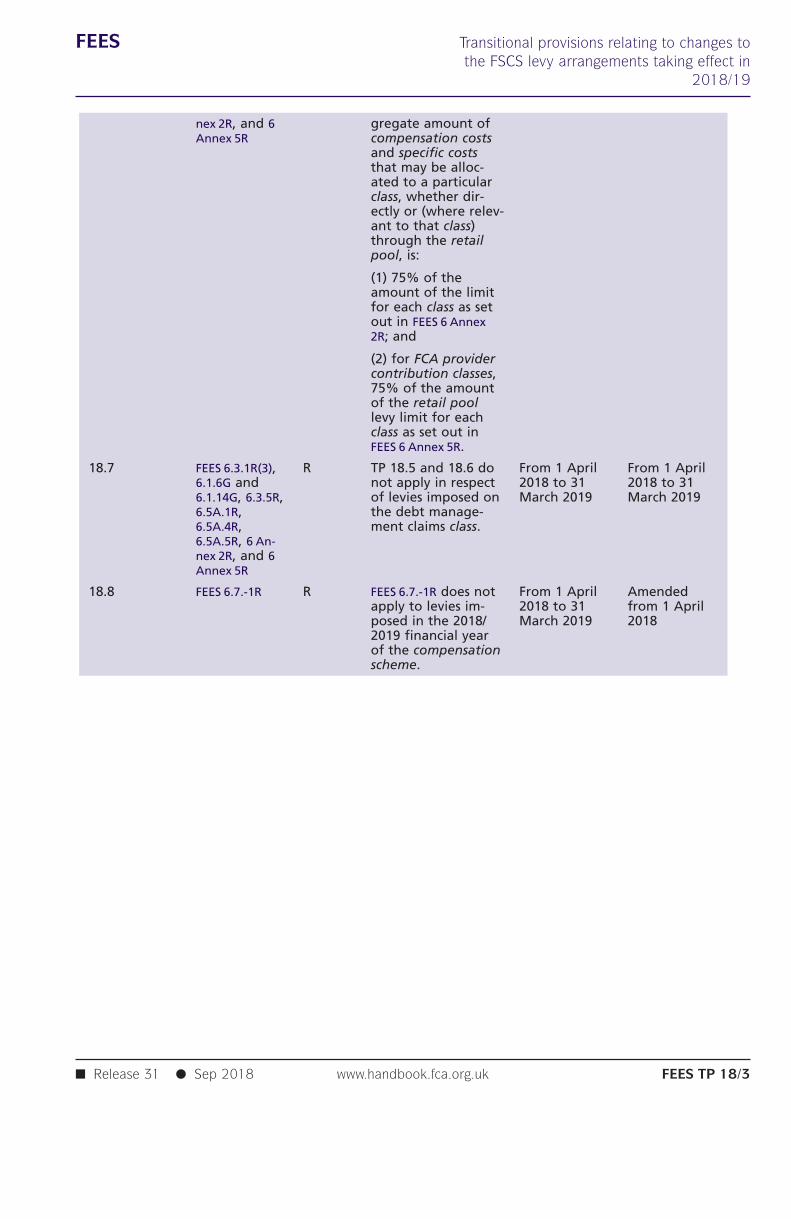

2017 and Electronic Money Regulations 2011TP 17A Transitional provisions for fees relating to benchmark administratorsTP 18 Transitional provisions relating to changes to the FSCS levy

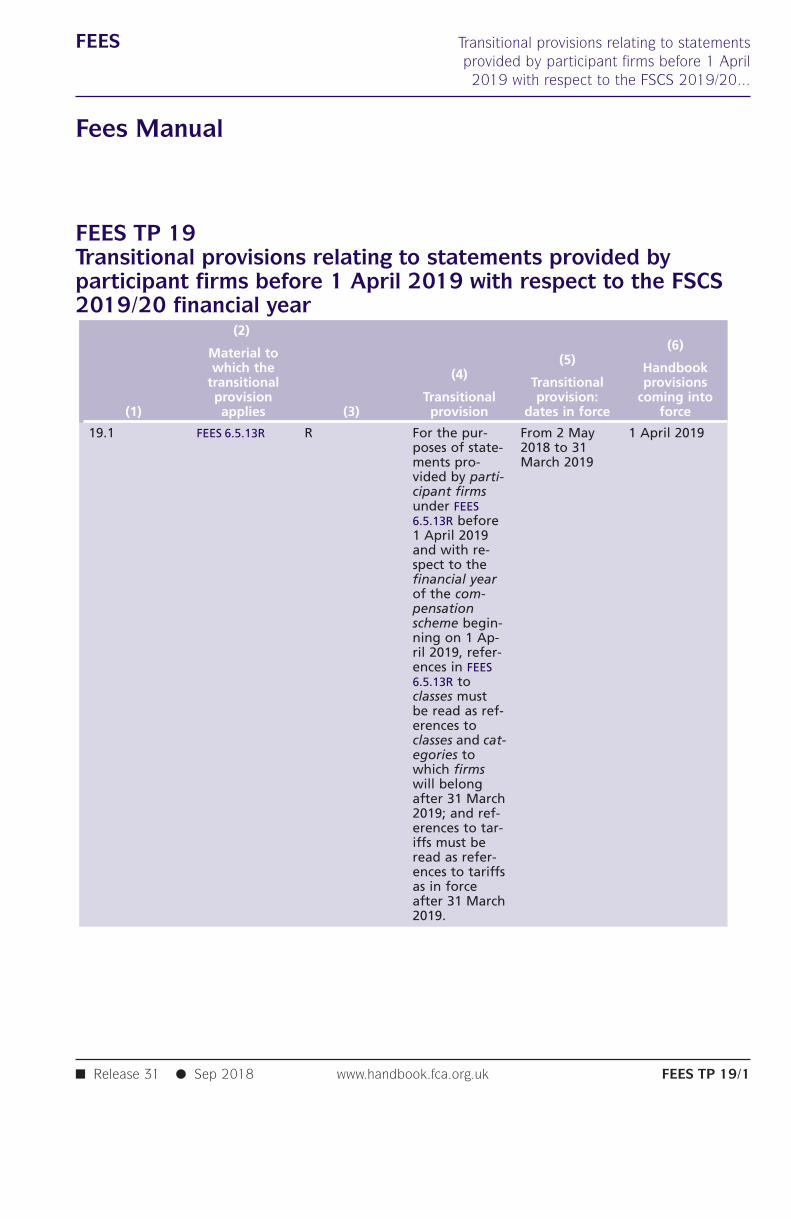

arrangements taking effect in 2018/19TP 19 Transitional provisions relating to statements provided by participant

firms before 1 April 2019 with respect to the FSCS 2019/20 financialyear

Sch 1 [to follow]

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES–v

FEES Contents

Sch 2 [to follow]Sch 3 [to follow]Sch 4 Powers exercisedSch 5 [to follow]Sch 6 Rules that can be waived

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES–vi

FEES Contents

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES–vii

Fees Manual

Chapter 1

Fees Manual

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 1/1

FEES 1 : Fees Manual Section 1.1 : Application and Purpose

1

G1.1.1

G1.1.1A

G1.1.1B

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 1/2

1.1 Application and Purpose

(1) FEES applies to all persons required to pay a fee or levy under aprovision of the Handbook. The purpose of this chapter is to set outto whom the rules and guidance in FEES apply.

(2) ■ FEES 2 (General Provisions) contains general provisions which mayapply to any type of fee payer.

(3) ■ FEES 3 (Application, Notification and Vetting Fees) covers one-offfees payable on a particular event for example:

(a) various application fees (including those in relation toauthorisation, variation of PART 4A permission, registration as aCBTL firm, authorisation of a data reporting services provider,listing and the Basel Capital Accord); and

(b) fees relating to designated credit reference agencies, designatedfinance platforms and certain notifications and document vettingrequests.

(4) ■ FEES 4 (Periodic fees) covers all periodic fees and transactionreporting fees.

(5) ■ FEES 5 (Financial Ombudsman Service Funding) relates to FOS leviesand case fees (in ■ FEES 5.5B).

(6) ■ FEES 6 (Financial Services Compensation Scheme Funding) relates tothe FSCS levy.

(7) ■ FEES 7 relates to the CFEB levy.

(8) ■ FEES 7A relates to the SFGB levy.

■ FEES App 1 Annex 1 applies to all persons required to pay a fee or any otheramount to the FCA under the Unauthorised Mutuals Registration Fees Rules,as made by the Fees (Unauthorised Mutual Societies Registration) Instrument2002 (FSA 2002/4) and amended from time to time.

■ FEES 9 (Payment System Regulator Funding) relates to PSR fees.

FEES 1 : Fees Manual Section 1.1 : Application and Purpose

1G1.1.1C

G1.1.1D

G1.1.1E

G1.1.1F

G1.1.1G

R1.1.2

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 1/3

■ FEES 10 (Pensions guidance levy) relates to the pensions guidance levy.

■ FEES 11 (Pensions guidance providers’ levy) relates to the pensions guidanceproviders’ levy.

■ FEES 12 (FOS ADR Levy) relates to the FOS ADR levy.

■ FEES Appendix 2 (Office for professional body anti-money launderingsupervision fees) applies to the following persons required to pay fees to theFCA:

(1) a person applying to become a professional body listed in Schedule 1to the Money Laundering Regulations; and

(2) professional bodies listed in Schedule 1 to the Money LaunderingRegulations.

■ FEES Appendix 3 (Fees payable by persons registered under the MoneyLaundering Regulations) applies to MLR persons registered with the FCA thatare not authorised persons.

Application......................................................................................................This manual applies in the following way:

(1) ■ FEES 1, ■ 2 and ■ 3 apply to the fee payers listed in column 1 of theTable of application, notification and vetting fees in ■ FEES 3.2.7 R.

(a) [deleted]

(b) [deleted]

(c) [deleted]

(d) [deleted]

(e) [deleted]

(f) [deleted]

(g) [deleted]

(h) [deleted]

(i) [deleted]

(j) [deleted]

(k) [deleted]

(l) [deleted]

(m) [deleted]

(n) [deleted]

(o) [deleted]

(p) [deleted]

(q) [deleted]

FEES 1 : Fees Manual Section 1.1 : Application and Purpose

1

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 1/4

(r) [deleted]

(s) [deleted]

(2) ■ FEES 1, ■ 2 and ■ 4 apply to:

(a) every firm (except an AIFM qualifier, ICVC or UCITS qualifier);

(b) every authorised fund manager of an authorised unit trust orauthorised contractual scheme;

(c) every ACD of an ICVC;

(d) every person who, under the constitution or foundingarrangements of a recognised scheme, is responsible for themanagement of the property held for or within the scheme;

(da) every AIFM of a UK ELTIF;

(e) every designated professional body;

(f) every recognised body;

(g) under the Listing Rules every issuer of shares, depositary receiptsand securitised derivatives;

(h) under the Listing Rules (LR) every sponsor;

(i) under the Disclosure Guidance and Transparency Rules (DTR)every issuer of shares, depositary receipts and securitisedderivatives;

(j) every fee-paying payment service provider;

(k) every fee-paying electronic money issuer;

(l) every issuer of a regulated covered bond;

(m) every AIFM applying to become a small registered UK AIFM andevery small registered UK AIFM;

(n) every AIFM notifying the FCA under regulation 57, 58 and 59 ofthe AIFMD UK regulation and every AIFM which has made such anotification;

(o) [deleted]

(p) a data reporting services provider (FEES 4 does not apply to anincoming data reporting services provider).

(3) ■ FEES 1, ■ 2 and ■ 5 apply to:

(a) every firm (except to the extent it is bidding in emissionsauctions), fee-paying payment service provider and fee-payingelectronic money issuer which is subject to the CompulsoryJurisdiction of the Financial Ombudsman Service; and

(b) every other person who is subject to the Compulsory Jurisdictionin relation to relevant complaints.

(4) ■ FEES 1, ■ 2 and ■ 6 apply to:

(a) every participant firm;

(b) the FSCS; and

(c) the Society.

FEES 1 : Fees Manual Section 1.1 : Application and Purpose

1

R1.1.2A

R1.1.2B

R1.1.2C

G1.1.3

G1.1.3A

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 1/5

(5) ■ FEES 1, ■ 2, ■ 7 and ■ 7A (in relation to the SFGB money advice levyand SFGB debt advice levy only) apply to:

(a) every person having a Part 4A permission;

(b) an incoming EEA firm;

(c) an incoming Treaty firm;

(d) the Society;

(e) every fee-paying payment service provider except the Bank ofEngland, government departments and local authorities;

(f) every fee-paying electronic money issuer except the Bank ofEngland, government departments, local authorities, municipalbanks and the National Savings Bank.

(6) ■ FEES App 1 Annex 1 applies to every:

(a) registered society; or

(b) sponsoring body; or

(c) person who submits a proposal for the registration of aregistered society;

each as defined in ■ FEES Appendix 1.

(7) ■ FEES 7A (in relation to the SFGB pensions guidance levy only) appliesto firms referred to in ■ FEES 7A.1.2R.

■ FEES 1, ■ 2, ■ 7 and ■ 7A do not apply to an incoming EEA firm or anincoming Treaty firm that has not established a branch in the UnitedKingdom.

The application statement at ■ FEES 1.1.2R (3) does not apply to ■ FEES 5.5A,■ FEES 5 Annex 2R or ■ FEES 5 Annex 3R.

■ FEES 1 and ■ FEES 9 apply to:

(1) operators of regulated payment systems;

(2) operators of IFR card payments systems; and

(3) direct payment service providers.

■ FEES 1 and 11 apply to a designated guidance provider.

■ FEES 1 and 12 apply to FOS Ltd.

The application of ■ FEES 5.5A and ■ FEES 5 Annex 3R is set out in■ FEES 5.5A.1 R. The relevant provisions of ■ FEES 5 and ■ FEES 2 are applied toVJ participants by the standard terms (see ■ DISP 4).

[deleted]

FEES 1 : Fees Manual Section 1.1 : Application and Purpose

1G1.1.4

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 1/6

Purpose......................................................................................................The purpose of this manual is to set out the fees applying to the persons setout in ■ FEES 1.

Fees Manual

Chapter 2

General Provisions

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 2/1

FEES 2 : General Provisions Section 2.1 : Introduction

2

R2.1.1

R2.1.1A

R2.1.2

G2.1.3

G2.1.4

G2.1.5

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 2/2

2.1 Introduction

Application......................................................................................................Except to the extent referred to in ■ FEES 2.1.1A R, this chapter applies toevery person who is required to pay a fee or share of a levy to the FCA , FOSLtd or FSCS, as the case may be, by a provision of the Handbook.

This chapter does not apply in relation to:

(1) ■ FEES 5.5A; or

(2) ■ FEES 5 Annex 2R; or

(3) ■ FEES 5 Annex 3R; or

(4) a PSR fee; or

(5) the pensions guidance levy; or

(6) the pensions guidance providers’ levy; or

(7) the FOS ADR levy.

■ FEES 2.2.1R does not apply in respect of any fee payable under ■ FEES 3(Application, notification and vetting fees).

The provisions for late payments in ■ FEES 2.2.1R do not apply to fees payableunder ■ FEES 3 as applications, notifications and requests for vetting aregenerally regarded as incomplete until the relevant fee is paid.

Purpose......................................................................................................The purpose of this chapter is to set out the general provisions applicable tothose who are required to pay fees or levies to theFCA or a share of the FSCSlevy.

(1) The following enable the FCA to charge fees to cover its costs andexpenses in carrying out its functions:

(a) paragraph 23 of Schedule 1ZA of the Act;

(b) regulation 92 of the Payment Services Regulations;

FEES 2 : General Provisions Section 2.1 : Introduction

2

G2.1.5-A

G2.1.5A

G2.1

G2.1.5C

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 2/3

(c) regulation 59 of the Electronic Money Regulations;

(d) article 25(a) of the MCD Order;

(e) regulation 21 of the Small and Medium Sized Businesses (CreditInformation) Regulations.

(f) regulation 18 of the Small and Medium Sized Business (FinancePlatforms) Regulations;

(g) regulation 40 of the DRS Regulations; and

(h) paragraph 25 of the Schedule 1 to the MiFI Regulations.

(2) The corresponding provisions for the FSCS levy, FOS levies, and CFEBlevies are set out in ■ FEES 6.1, ■ FEES 5.2 and ■ FEES 7.1.4G respectively.

(3) Case fees payable to the FOS Ltd are set out in ■ FEES 5.5B.

(4) Fee-paying payment service providers, fee-paying electronic moneyissuers, CBTL firms, designated finance platforms and designatedcredit reference agencies are not required to pay the FSCS levy butare liable for FOS levies.

Regulation 92 of the Payment Services Regulations and regulation 59 of theElectronic Money Regulations each provide that the functions of the FCAunder the respective regulations are treated for the purposes of paragraph23 of Schedule 1ZA to the Act as functions conferred on the FCA under theAct. Paragraph 23(7) however, has not been included .This is the FCA'sobligation to ensure that the amount of penalties received or expected to bereceived are not to be taken into account in determining the amount of anyfee payable.

Article 25 of the MCD Order provides that the functions under the MCDOrder are to be treated for the purposes of paragraph 23 of Schedule 1ZA tothe Act as functions conferred on the FCA under the Act.

(1) The FCA also has a fee-raising power as a result of:

(a) regulation 21 of the Small and Medium Sized Business (CreditInformation) Regulations;

(b) regulation 18 of the Small and Medium Sized Business (FinancePlatforms) Regulations;

(c) regulation 40 of the DRS Regulations; and

(d) paragraph 25 of the Schedule 1 to the MiFI Regulations.

(2) The FCA’s functions under these regulations are treated as functionsconferred on the FCA under the Act for the purposes of its fee-raisingpower in paragraph 23 of Schedule 1ZA to the Act or as if they hadsimilar effect for these purposes.

FEES 2 : General Provisions Section 2.1 : Introduction

2

G2.1.6

G2.1.7

G2.1.8

G2.1.9

G2.1.9A

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 2/4

The FCA’s fees payable will vary from one fee year to another, and willreflect the FCA’s funding requirement for that period and the other keycomponents, as described in ■ FEES 2.1.7G. Periodic fees, which will normallybe payable on an annual basis, will provide the majority of the fundingrequired to enable the FCA to undertake its statutory functions.

The key components of the FCA fee mechanism (excluding the FSCS levy, theFOS levy and case fees, and the CFEB levy which are dealt with in ■ FEES 5,■ FEES 6 and ■ FEES 7) are:

(1) a funding requirement derived from:

(a) the FCA’s financial management and reporting framework;

(b) the FCA’s budget; and

(c) adjustments for audited variances between budgeted and actualexpenditure in the previous accounting year, and reservesmovements (in accordance with the FCA’s reserves policy);

(2) mechanisms for applying penalties received during previous financialyears for the benefit of fee payers;

(3) fee-blocks, which are broad groupings of fee payers offering similarproducts and services and presenting broadly similar risks to the FCA’sregulatory objectives;

(4) a costing system to allocate an appropriate part of the fundingrequirement to each fee-block; and

(5) tariff bases, which, when combined with fee tariffs, allow thecalculation of fees.

The amount payable by each fee payer will depend upon the category (orcategories) of regulated activity or exemption, or other relevant activityapplicable to that person (fee-blocks). It will, in most cases, also depend onthe amount of the business that person conducts in each category (feetariffs).

By basing fee-blocks on categories of business, the FCA aims to minimisecross-sector subsidies. The membership of the fee-blocks is identified in theFEES provisions relating to the type of fees concerned.

PRA-authorised persons and persons seeking to become PRA-authorisedpersons should note that the FCA and the PRA have agreed for the FCA toact as the PRA's collection agent for PRA fees. Where applicable, both PRAand FCA fees should be paid as a single payment to the FCA, which willreceive the payment in its own capacity in respect of FCA fees and in its

FEES 2 : General Provisions Section 2.1 : Introduction

2G2.1.10

G2.1.11

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 2/5

capacity as collection agent for the PRA in respect of the PRA fees.References to this arrangement will be referred to in FEES where applicable.

[deleted]

[deleted]

FEES 2 : General Provisions Section 2.2 : Late Payments and Recovery ofUnpaid Fees

2

R2.2.1

G2.2.2

G2.2.3

G2.2.4

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 2/6

2.2 Late Payments and Recovery ofUnpaid Fees

Late Payments......................................................................................................If a person does not pay the total amount of a periodic fee, FOS levy, orshare of the FSCS levy, or CFEB levy or SFGB levy, before the end of the dateon which it is due, under the relevant provision in ■ FEES 4, ■ 5, ■ 6, ■ 7 or■ 7A,that person must pay an additional amount as follows:

(1) if the fee was not paid in full before the end of the due date, anadministrative fee of £250; plus

(2) interest on any unpaid part of the fee at the rate of 5% per annumabove the Official Bank Rate from time to time in force, accruing on adaily basis from the date on which the amount concerned becamedue.

The FCA, (for FCA and PRA periodic fees, FOS and FSCS levies, CFEB leviesand SFGB levies), expects to issue invoices at least 30 days before the date onwhich the relevant amounts fall due. Accordingly it will generally be the casethat a person will have at least 30 days from the issue of the invoice beforean administrative fee becomes payable.

Recovery of Fees......................................................................................................(1) Paragraph 23(8) of Schedule 1ZA of the Act permits the FCA to

recover fees (including fees relating to payment services, the issuanceof electronic money, CBTL firms, data reporting services providers,designated credit reference agencies, designated finance platformsand, where relevant, FOS levies, CFEB levies and SFGB levies).

(2) Section 213(6) of the Act permits the FSCS to recover shares of theFSCS levy payable, as a debt owed to the FCA and FSCS respectively.

(3) The FCA and FSCS, as relevant, will consider taking action for recovery(including interest) through the civil courts.

In addition, the FCA may be entitled to take regulatory action in relation tothe non-payment of fees, FOS levies, CFEB levies and SFGB levies. The FCAmay also take regulatory action in relation to the non-payment of a share ofthe FSCS levy, after reference of the matter to the FCA by the FSCS. Whataction (if any) that is taken by the FCA will be decided upon in the light ofthe particular circumstances of the case.

FEES 2 : General Provisions Section 2.3 : Relieving Provisions

2

R2.3.1

R2.3.2

G2.3.2A

R2.3.2B

R2.3.2C

G2.3.3

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 2/7

2.3 Relieving Provisions

Remission of Fees and levies......................................................................................................If it appears to the FCA or the FSCS (in relation to any FSCS levy only) that inthe exceptional circumstances of a particular case, the payment of any fee,FSCS levy, FOS levy, CFEB levy or SFGB levy would be inequitable, the FCA orthe FSCS as relevant, may (unless ■ FEES 2.3.2B R applies) reduce or remit all orpart of the fee or levy in question which would otherwise be payable.

If it appears to the FCA or the FSCS (in relation to any FSCS levy only) that inthe exceptional circumstances of a particular case to which ■ FEES 2.3.1R doesnot apply, the retention by the FCA the FSCS, or the CFEB, as relevant, of afee, FSCS levy, FOS levy, CFEB levy or SFGB levy which has been paid wouldbe inequitable, the FCA the FSCS or the CFEB, may (unless ■ FEES 2.3.2B Rapplies) refund all or part of that fee or levy.

A poor estimate or forecast by a fee or levy payer, when providinginformation relevant to an applicable tariff base, is unlikely, of itself, toamount to an exceptional circumstance for the purposes of ■ FEES 2.3.1 R or■ FEES 2.3.2 R. By contrast, a mistake of fact or law by a fee or levy payer maygive rise to such a claim.

The FCA or the FSCS may not consider a claim under ■ FEES 2.3.1 R and/or■ FEES 2.3.2 R to reduce, remit or refund any overpaid amounts paid by a feeor levy payer in respect of a particular period, due to a mistake of fact orlaw by the fee or levy payer, if the claim is made by the fee or levy payermore than 2 years after the beginning of the period to which theoverpayment relates.

For ■ FEES 7A, the FCA is entitled not to consider a claim under ■ FEES 2.3.1Ror ■ FEES 2.3.2R to refund any overpaid amounts due to a mistake of fact orlaw by the fee-paying firm if the claim is made more than two years afterthe beginning of the period to which the SFGB levy subject to the claimrelates.

[deleted]

FEES 2 : General Provisions Section 2.4 : VAT

2

R2.4.1

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 2/8

2.4 VAT

All fees payable or any stated hourly rate under ■ FEES 3 (Application,notification and vetting fees), ■ FEES 4 (Periodic fees), ■ FEES 7 (The CFEB levy)and ■ FEES 7A (The SFGB levy) are stated net of VAT. Where VAT is applicablethis must also be included.

Fees Manual

Chapter 3

Application, Notification andVetting Fees

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 3/1

FEES 3 : Application, Section 3.1 : IntroductionNotification and Vetting Fees

3

R3.1.1

R3.1.1A

G3.1.2

G3.1.3

G3.1.4

G3.1.5

G3.1.5A

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 3/2

3.1 Introduction

Application......................................................................................................This chapter applies to every person set out in column 1 of the Table ofapplication, notification and vetting fees in ■ FEES 3.2.7 R.

fee-paying payment service provider, a CBTL firm, a fee-paying electronicmoney issuer, a designated finance platform, a designated credit referenceagency and a data reporting services provider.

This chapter does not apply to:

(1) an EEA firm that wishes to exercise an EEA right unless it is:

(a) an incoming data reporting services provider connecting to themarket data processor system; or

(b) an EEA firm connecting to the market data processor system; or

(2) an EEA authorised payment institution; or

(3) an EEA authorised electronic money institution.

Purpose......................................................................................................The purpose of this chapter is to set out the FCA fee paying requirements onthe persons set out in ■ FEES 1.1.2R (1).

Most of the detail of what fees are payable by the persons referred to in■ FEES 3.1.3 G is set out in ■ FEES 3 Annex 1 - ■ FEES 3 Annex 12R.

(1) The rates set for authorisation fees represent an appropriateproportion of the costs of the FCA in processing the application orexercise of Treaty rights.

(2) [deleted]

(3) [deleted]

The fees for funds reflect the estimated costs to the FCA of assessingapplications and notifications. The level of fees payable in respect of anapplication or a notification will vary depending upon the provision of theAct under which it is made. This fee is adjusted when the scheme concernedis an umbrella.

FEES 3 : Application, Section 3.1 : IntroductionNotification and Vetting Fees

3

G3.1.5B

G3.1.6

G3.1.6A

G3.1.6B

G3.1.6C

G3.1.6D

G3.1.6E

G3.1.7

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 3/3

Application fees for recognised bodies are calculated from a tariff structureintended to reflect the estimated cost of processing an application of thattype and complexity.

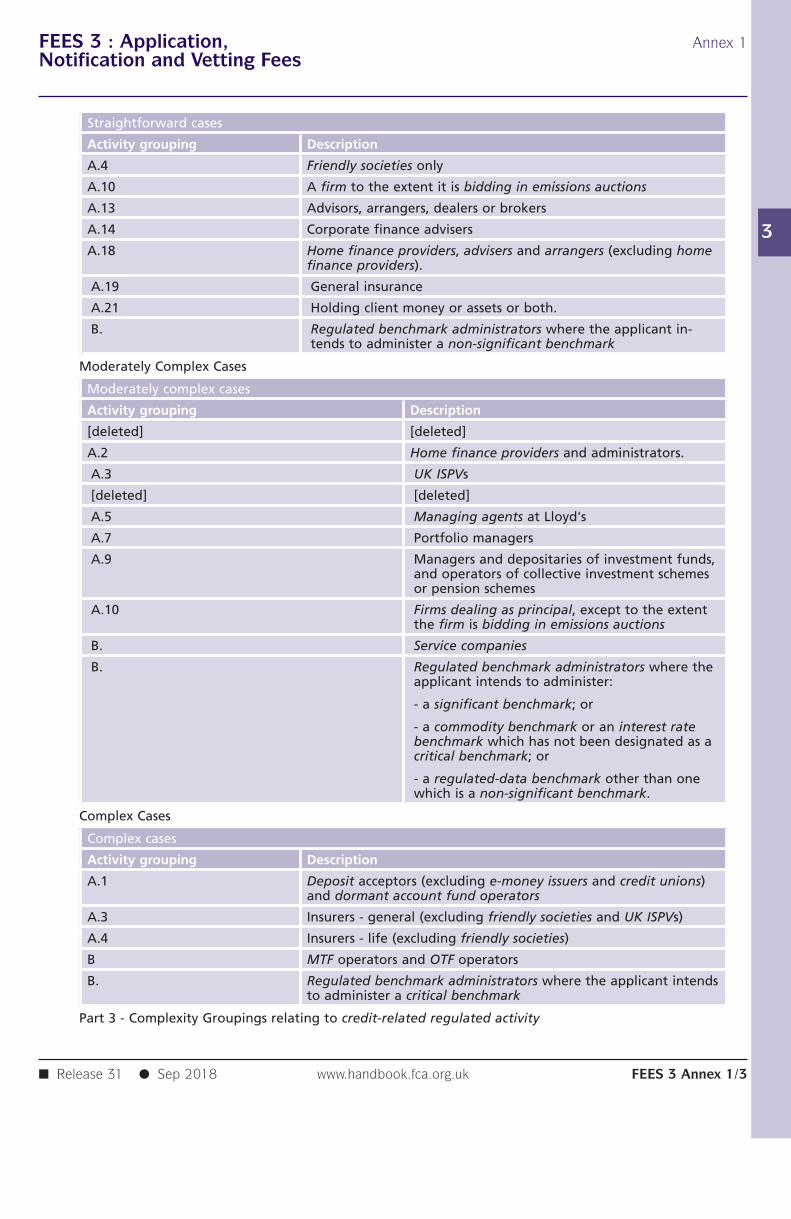

Applications for Part 4A permission (and exercises of Treaty rights) otherthan in respect of credit-related regulated activities are categorised by theFCA for the purpose of fee raising as straightforward, moderately complexand complex as identified in ■ FEES 3 Annex 1. This differentiation is based onthe permitted activities sought and does not reflect the FCA's risk assessmentof the applicant (or Treaty firm).

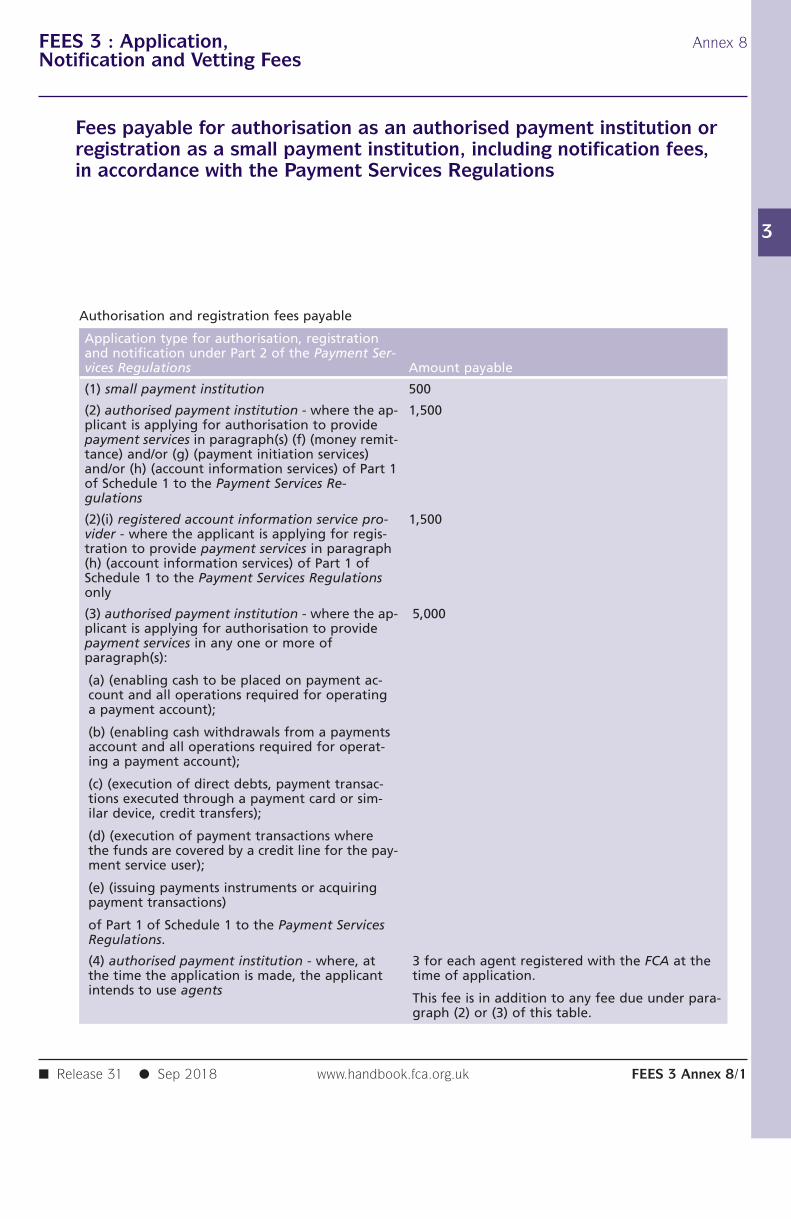

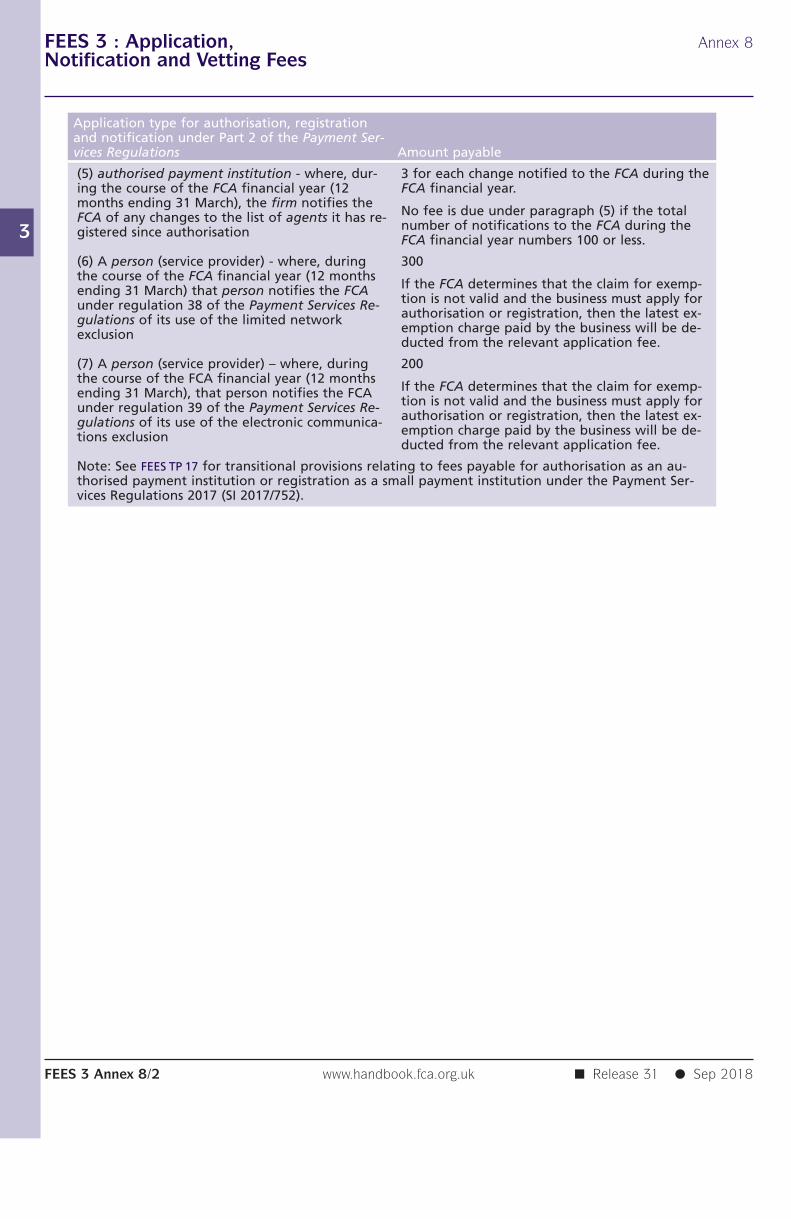

Application fees for authorisation or registration under the Payment ServicesRegulations are set out in ■ FEES 3 Annex 8R . The fee depends on the type ofpayment services a firm wishes to provide and whether it will be a smallpayment institution or an authorised payment institution. The fee may alsodepend on the number of agents it has.

Application fees for authorisation or registration under the Electronic MoneyRegulations are set out in ■ FEES 3 Annex 10 R. The fee depends on whetherthe firm is an authorised electronic money institution or a small electronicmoney institution.

Application fees for registration under article 8(1) of the MCD Order are setout in ■ FEES 3 Annex 10AR. The fee depends on whether the firm holds anexisting Part 4A permission or an interim permission or has previouslyregistered as a CBTL firm and that registration has been revoked underarticle 13 of the MCD Order.

(1) Fees for designated credit reference agencies and designated financeplatforms are set out at ■ FEES 3 Annex 10B.

(2) These fees are charged under regulation 21 of the Small and MediumSized Business (Credit Information) Regulations and regulation 18 ofthe Small and Medium Sized Business (Finance Platforms) Regulations.

(1) Application fees for authorisation under regulation 7 of the DRSRegulations, and for operators of trading venues seeking verificationof their compliance with Title V of MiFID under regulation 8 of theDRS Regulations and for variation of an authorisation underregulation 12 of the DRS Regulations are set out in the table at■ FEES 3.2.7R.

(2) The fee depends on the number of data reporting services for whichthe firm is making an application.

A potential applicant for Part 4A permission (or Treaty firm) has theopportunity to discuss its proposed application (or exercise of Treaty rights)with the FCA before submitting it formally. If an applicant for Part 4Apermission (or Treaty firm) does so, the FCA will be able to use that dialogueto make an initial assessment of the fee categorisation and thereforeindicate the authorisation fee that should be paid.

FEES 3 : Application, Section 3.1 : IntroductionNotification and Vetting Fees

3

G3.1.8

G3.1.8A

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 3/4

[Deleted]

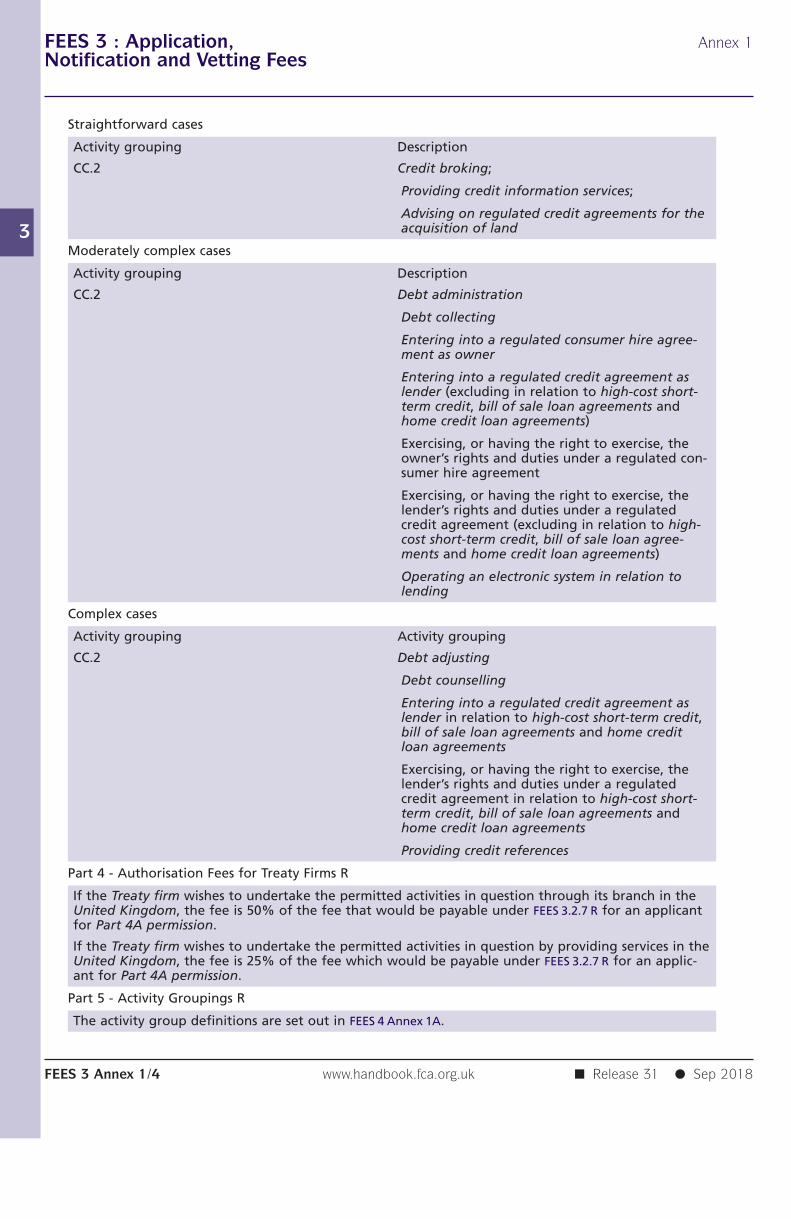

Application fees for applications for and variations of Part 4A permission inrespect of credit-related regulated activities are also set out in■ FEES 3 Annex 1F. Applications for Part 4A permission in respect of credit-related regulated activities are categorised by the FCA for the purposes offee raising as straightforward, moderately complex and complex as identifiedin ■ FEES 3 Annex 1, unless the application is for a limited permission.

[Note: PRA-authorised persons may also pay regulatory transaction fees tothe PRA set out in Chapter 4 of the Fees Part of the PRA Rulebook.]

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

R3.2.1

R3.2.1A

G3.2.2

R3.2.3

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 3/5

3.2 Obligation to pay fees

General......................................................................................................A person in column (1) of the table in ■ FEES 3.2.7 R as the relevant fee payerfor a particular activity must pay to the FCA (in its own capacity or, if the feeis payable to the PRA, in its capacity as collection agent for the PRA) a feefor each application or request for vetting, or request for support relating tocompatibility of its systems with FCA systems, or admission approval made, ornotification or notice of exercise of a Treaty right given, or other matter as isapplicable to it, as set out or calculated in accordance with the provisionsreferred to in column (2) of the appropriate table:

(1) in full and without deduction; and

(2) on or before the date given in column (3) of that table.

A person must pay the fee in Categories A5 and A6 of ■ FEES 3 Annex 12R forthe first submission of a document to the FCA for approval or review inrelation to a significant transaction or super transaction. As an exception to■ FEES 3.2.1R, after that fee is paid, Categories A1 to A4 of ■ FEES 3 Annex 12Rspecify the fees a person must pay for any further documents submitted forapproval or review in relation to the same transaction.

If an application for a Part 4A permission (or exercise of a Treaty right) fallswithin more than one category set out in ■ FEES 3 Annex 1, other than whereone of the applications is an application under the benchmarks regulation,only one fee is payable. That fee is the one for the category to which thehighest fee tariff applies.Where applications are made under the benchmarksregulation, a separate fee will be payable for this application. The relevantfee is set out in ■ FEES 3.2.7R.

Method of payment......................................................................................................(1) Unless (2), (3) or (4) applies, the sum payable under ■ FEES 3.2.1 R must

be paid by bankers draft, cheque or other payable order.

(2) The FCA does not specify a method of payment for a person seekingto:

(a) become a recognised body or a designated professional body; or

(b) be added to the list of designated investment exchanges oraccredited bodies.

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

R3.2.3A

G3.2.3B

G3.2.4

G3.2.5

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 3/6

(3) The sum payable under ■ FEES 3.2.1 R by a firm applying for a variationof its Part 4A permission which is not an application for newpermission solely in respect of one or more credit-related regulatedactivities (■ FEES 3.2.7 R(p)(1) or ■ FEES 3.2.7 R(p)(4) and, if applicable,■ FEES 3.2.7 R(c)) must be paid by any of the methods described in (1)or by Maestro, Visa Debit or credit card (Visa/Mastercard/AmericanExpress only).

(4) Unless ■ FEES 3.2.3A R applies, the sum payable under ■ FEES 3.2.1 R by afirm applying for a Part 4A permission in respect of credit-relatedregulated activities only or a variation of its Part 4A permission toadd solely one or more credit-related regulated activities must bepaid by Maestro, Visa Debit or credit card (Visa/Mastercard/AmericanExpress only).

(5) [deleted]

(1) If the fee payer (as specified in column (1) of ■ FEES 3.2.7 R) in relationto ■ FEES 3.2.3R (4) is:

(a) unable to make a payment by credit or debit card; or

(b) permitted to make a paper application rather than an onlineapplication for a Part 4A permission in respect of credit-relatedregulated activities only or a variation of its Part 4A permission toadd a credit-related regulated activity;

the sum payable under ■ FEES 3.2.1 R can be paid by bankers draft,cheque or other payable order.

If ■ FEES 3.2.3AR (1)(a) applies to a fee payer, that fee payer would beexpected to notify the FCA of these circumstances in advance of making itspayment (and, in any event, no less than 7 days before the date on whichthe application for a Part 4A permission or the variation of a Part 4Apermission is made) unless such notification is impossible in thecircumstances, eg, there is a sudden technological failure.

The FCA expects that a person seeking to become a recognised body or adesignated professional body or to be added to the list of designatedinvestment exchanges or accredited bodies will generally pay their respectivefees by electronic credit transfer.

(1) The appropriate authorisation or registration fee is anintegral part of an application for, or an application for avariation of, a Part 4A permission, authorisation, registrationor variation under the Payment Services Regulations or theElectronic Money Regulations, registration under article 8(1)of the MCD Order, authorisation under regulation 7 of theDRS Regulations or verification under regulation 8 of theDRS Regulations or notification or registration under theAIFMD UK regulation.

(b) Any application or notification received by theFCA without theaccompanying appropriate fee, in full and without deduction (see■ FEES 3.2.1 R), will not be treated as an application or notificationmade, incomplete or otherwise, in accordance with section55U(4), or 55H of the Act or regulation 5(3) or 12(3) of thePayment Services Regulations or regulation 5 or 12 of the

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

G3.2.6

R3.2.7

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 3/7

Electronic Money Regulations or regulation 11(1) and 60(a) of theAIFMD UK regulation, regulation 7(2) of the DRS Regulations orarticle 9 of the MCD Order.

(c) Where this is the case, the FCA will contact the applicant to pointout that the application cannot be progressed until theappropriate fee has been received. In the event that theappropriate fee, in full and without deduction, is notforthcoming, the application will be returned to the applicantand no application will have been made.

(2) With the exception of persons seeking to become a designatedprofessional body, all applications, notifications, requests for vettingor admission approval will be treated as incomplete until the relevantfee is fully paid and the FCA will not consider an application,notification, request for vetting or admission approval until therelevant fee is fully paid. Persons seeking to become a designatedprofessional body have 30 days after the designation order is made topay the relevant fee.

Fees paid under this chapter are not refundable.

Table of application, notification, vetting and other fees payable to theFCA

Part 1: Application, notification and vetting fees

(1) Fee payer (2) Fee payable (£) Due date

(a) Any applicant for (1) Unless (2), (3) or (4) On or before the ap-Part 4A permission (in- applies, in respect of a plication is madecluding an incoming particular application,firm applying for top- the highest of the tar-up permission) whose iffs set out in FEES 3 An-fee is not payable pur- nex 1 part 1 which applysuant to sub- para- to that application.graph (zza) of thistable When both (A) and (B)

apply, 50% of the tariffpayable under (1):

(A) the application onlyinvolves a simplechange of legal statusas set out in FEES 3 An-nex 1 part 6; and

(B) the application is:

(i) a straightforwardcase under paragraph2(d) or 3(g) of FEES 3 An-nex 1;

(ii) a moderately com-plex case under para-graph 2(e) or 3(h) ofFEES 3 Annex 1; or

(iii) a limited permis-sion case under para-graph 3(i) of FEES 3 An-nex 1.

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 3/8

Part 1: Application, notification and vetting fees

(3) If the applicant ap-plies for registrationunder article 8(1) ofthe MCD Order at thesame time as applyingfor a Part 4A permis-sion, the fee payable isthe higher of:

(i) the fee otherwisepayable in (1) or (2);and

(ii) the fee payable inFEES 3 Annex 10AR.

(4) No fee is payable ifthe applicant satisfiesthe criteria set out inFEES 4 Annex 2BR(5)(a).

(aa) A person who As (a) above less any Within 30 days of themakes an application amount paid to the Of- date of the invoice.under section 24A of fice of Fair Trading inthe Consumer Credit relation to the relevantAct 1974 which meets application.the conditions of art-icle 31 (Applicationsfor a standard licencewhere no determina-tion made before 1 Ap-ril 2014) of the Finan-cial Services and Mar-kets Act 2000 (Regu-lated Activities)(Amendment) (No 2)Order 2013 (the “relev-ant application”)

(b) Any Treaty firm (1) Where no certific- On or before the no-that wishes to exercise ate has been issued un- tice of exercise is givena Treaty right to qual- der paragraph 3(4) ofify for authorisation Schedule 4 to the Actunder Schedule 4 to the fee payable is, in re-the Act (Treaty rights) spect of a particular ex-in respect of regulated ercise, set out in FEES 3activities for which it Annex 1, part 4does not have an EEA

(2) Where a certificateright, except for a firmin (i) has been issuedproviding cross borderno fee is payableservices only

(c) Any applicant for a 2,000 On or before the ap-certificate under article plication is made54 of the Regulated Ac-tivities Order

(d) Applicants for an FEES 3 Annex 2R, part 2 On or before the ap-authorisation order plication is madefor, or recognition un-der section 272 of theAct of, a collective in-vestment scheme

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 3/9

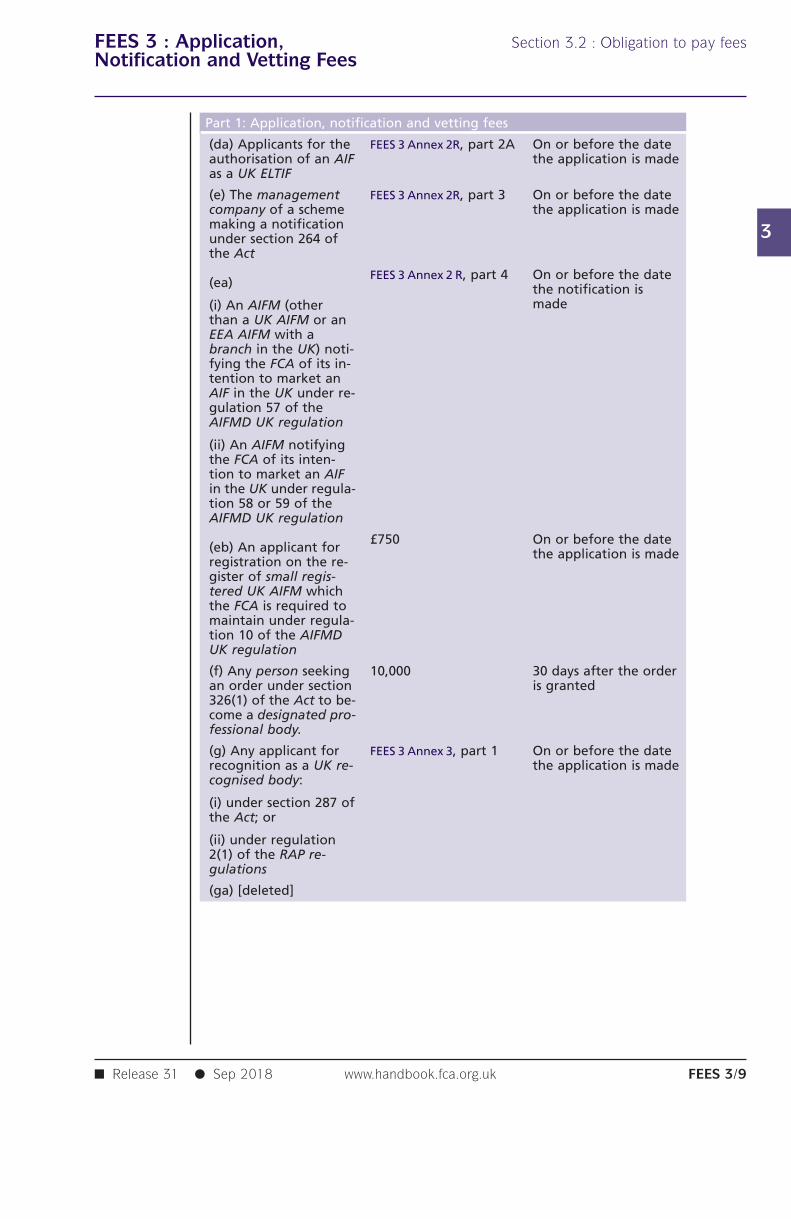

Part 1: Application, notification and vetting fees

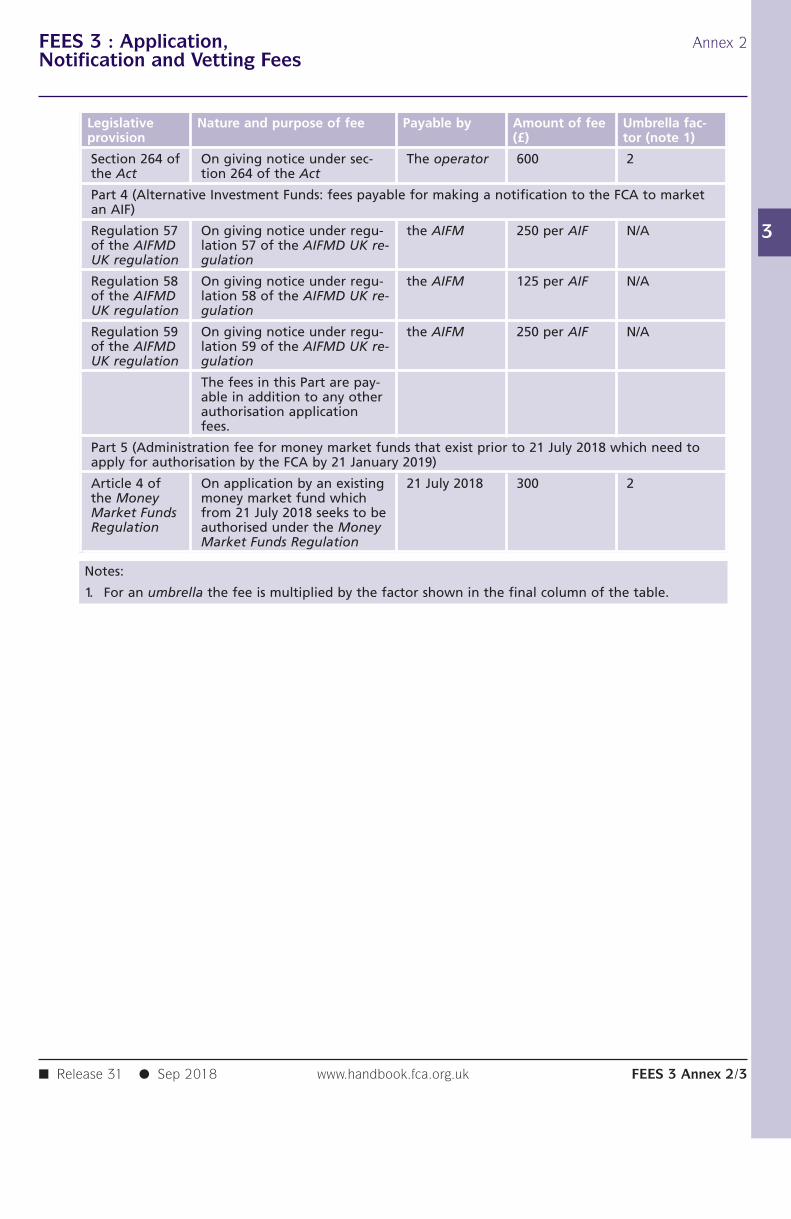

(da) Applicants for the FEES 3 Annex 2R, part 2A On or before the dateauthorisation of an AIF the application is madeas a UK ELTIF

(e) The management FEES 3 Annex 2R, part 3 On or before the datecompany of a scheme the application is mademaking a notificationunder section 264 ofthe Act

FEES 3 Annex 2 R, part 4 On or before the date(ea) the notification is

made(i) An AIFM (otherthan a UK AIFM or anEEA AIFM with abranch in the UK) noti-fying the FCA of its in-tention to market anAIF in the UK under re-gulation 57 of theAIFMD UK regulation

(ii) An AIFM notifyingthe FCA of its inten-tion to market an AIFin the UK under regula-tion 58 or 59 of theAIFMD UK regulation

£750 On or before the date(eb) An applicant for the application is maderegistration on the re-gister of small regis-tered UK AIFM whichthe FCA is required tomaintain under regula-tion 10 of the AIFMDUK regulation

(f) Any person seeking 10,000 30 days after the orderan order under section is granted326(1) of the Act to be-come a designated pro-fessional body.

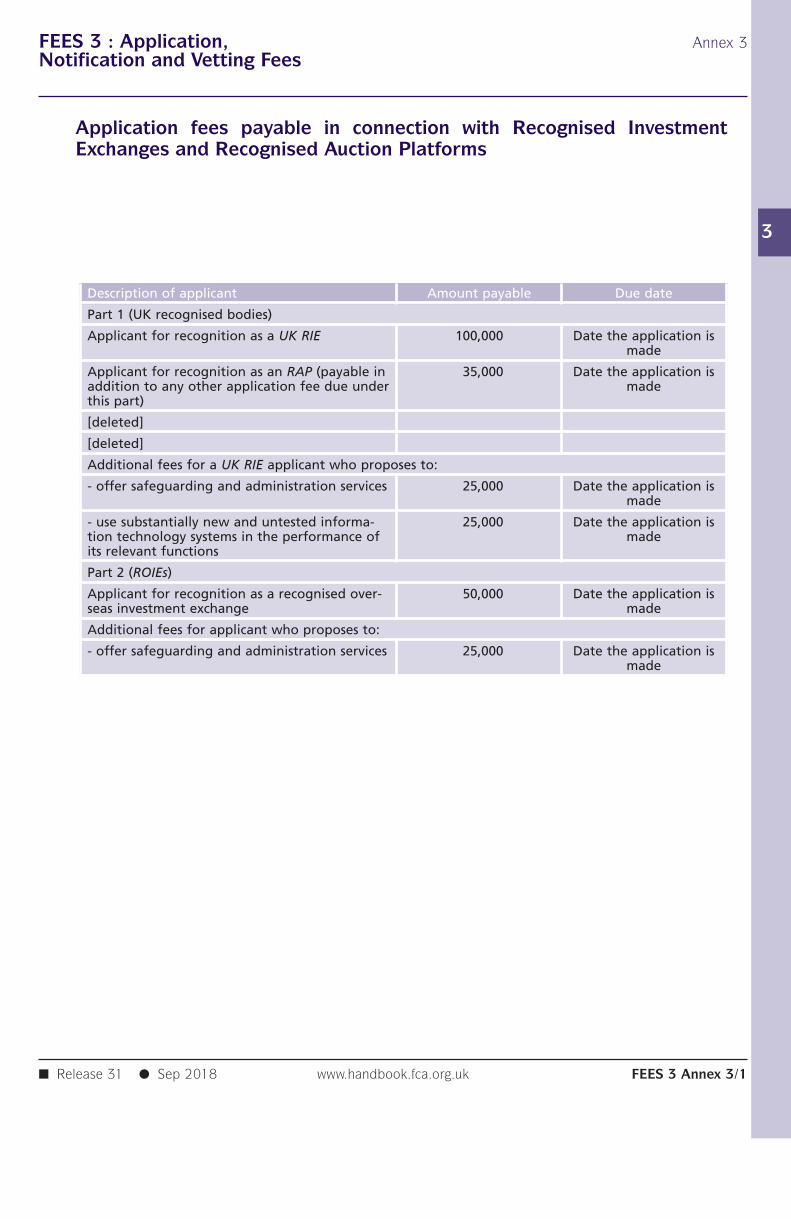

(g) Any applicant for FEES 3 Annex 3, part 1 On or before the daterecognition as a UK re- the application is madecognised body:

(i) under section 287 ofthe Act; or

(ii) under regulation2(1) of the RAP re-gulations

(ga) [deleted]

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 3/10

Part 1: Application, notification and vetting fees

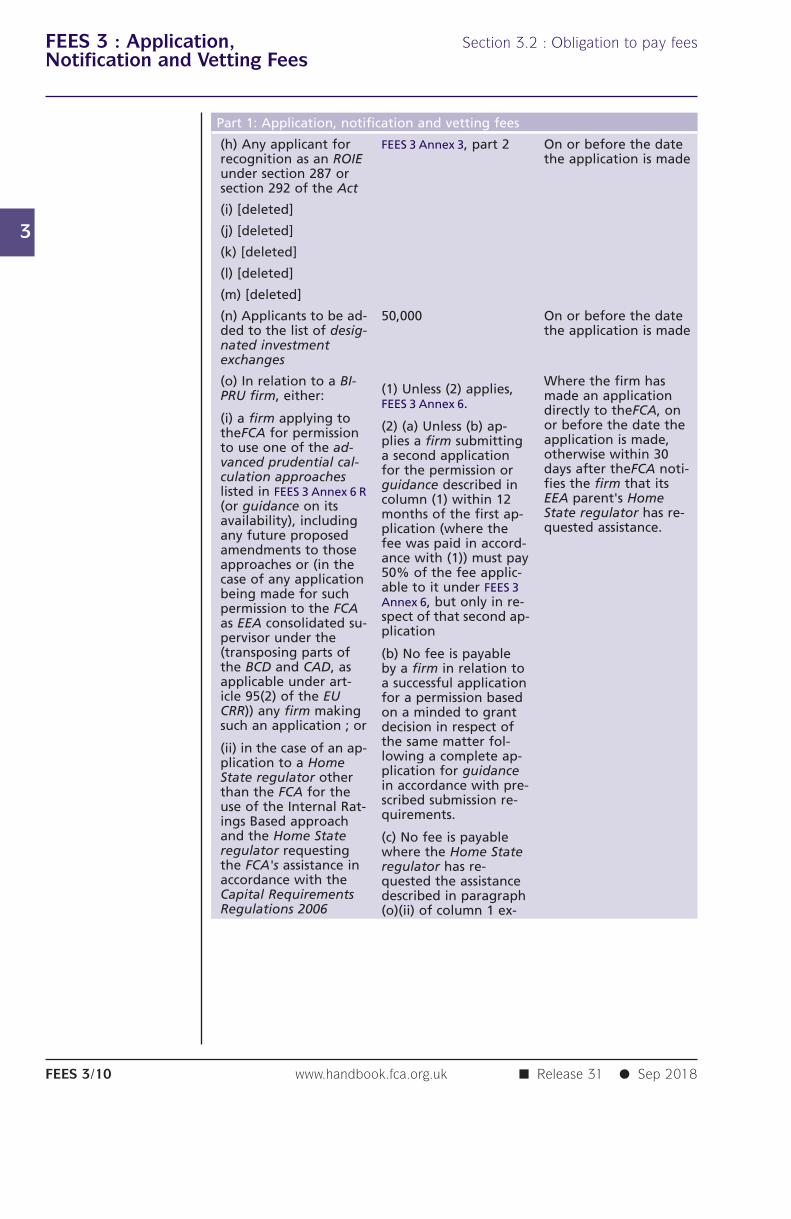

(h) Any applicant for FEES 3 Annex 3, part 2 On or before the daterecognition as an ROIE the application is madeunder section 287 orsection 292 of the Act

(i) [deleted]

(j) [deleted]

(k) [deleted]

(l) [deleted]

(m) [deleted]

(n) Applicants to be ad- 50,000 On or before the dateded to the list of desig- the application is madenated investmentexchanges

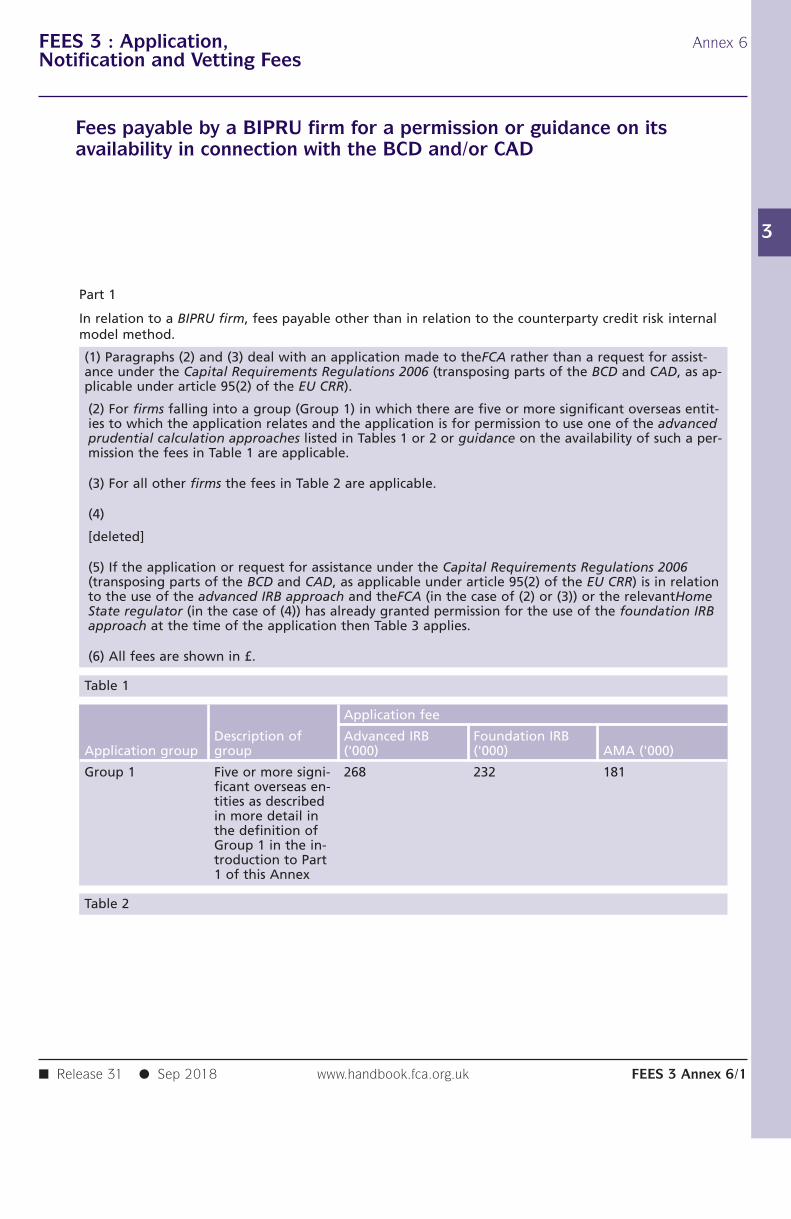

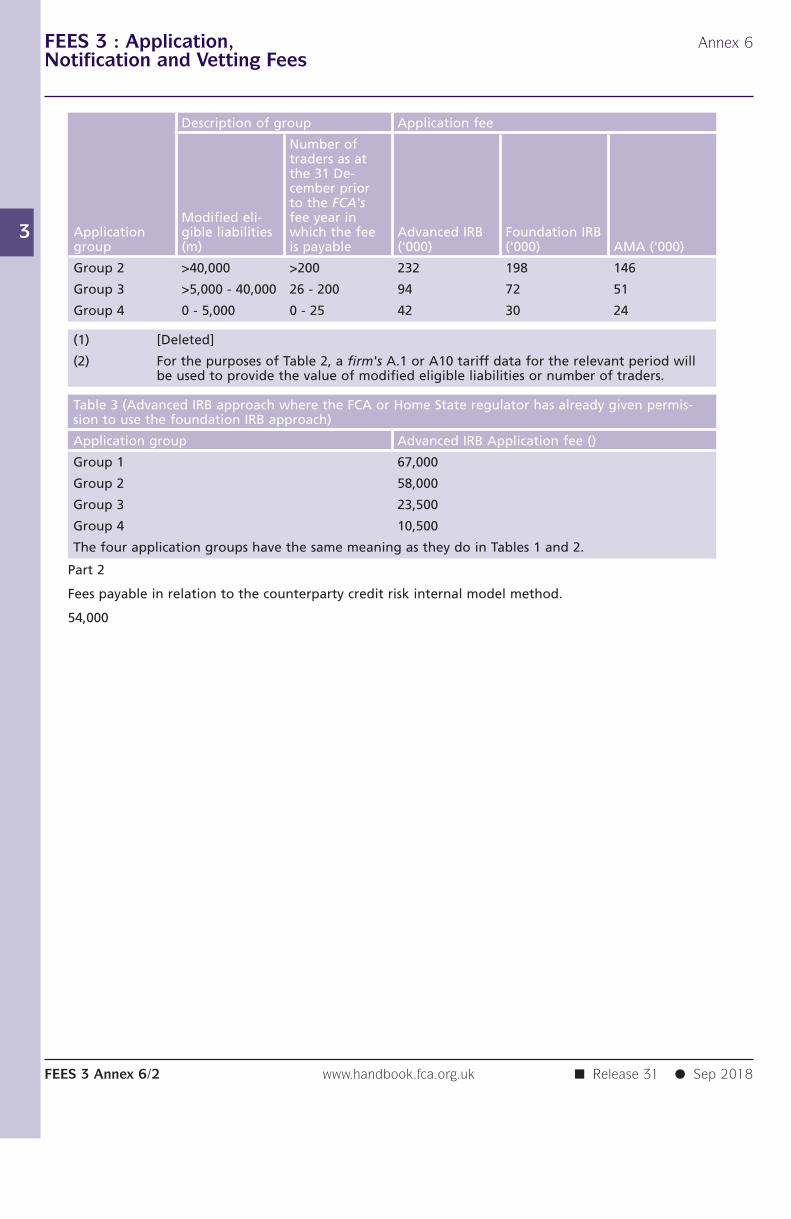

(o) In relation to a BI- Where the firm has(1) Unless (2) applies,PRU firm, either: made an applicationFEES 3 Annex 6. directly to theFCA, on

(i) a firm applying to or before the date the(2) (a) Unless (b) ap-theFCA for permission application is made,plies a firm submittingto use one of the ad- otherwise within 30a second applicationvanced prudential cal- days after theFCA noti-for the permission orculation approaches fies the firm that itsguidance described inlisted in FEES 3 Annex 6 R EEA parent's Homecolumn (1) within 12(or guidance on its State regulator has re-months of the first ap-availability), including quested assistance.plication (where theany future proposedfee was paid in accord-amendments to thoseance with (1)) must payapproaches or (in the50% of the fee applic-case of any applicationable to it under FEES 3being made for suchAnnex 6, but only in re-permission to the FCAspect of that second ap-as EEA consolidated su-plicationpervisor under the

(transposing parts of (b) No fee is payablethe BCD and CAD, as by a firm in relation toapplicable under art- a successful applicationicle 95(2) of the EU for a permission basedCRR)) any firm making on a minded to grantsuch an application ; or decision in respect of

the same matter fol-(ii) in the case of an ap-lowing a complete ap-plication to a Homeplication for guidanceState regulator otherin accordance with pre-than the FCA for thescribed submission re-use of the Internal Rat-quirements.ings Based approach

and the Home State (c) No fee is payableregulator requesting where the Home Statethe FCA's assistance in regulator has re-accordance with the quested the assistanceCapital Requirements described in paragraphRegulations 2006 (o)(ii) of column 1 ex-

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 3/11

Part 1: Application, notification and vetting fees

(transposing parts of cept in the cases speci-the BCD and CAD, as fied in FEES 3 Annex 6.applicable under art-icle 95(2) of the EUCRR), any firm towhich the FCA wouldhave to apply any de-cision to permit theuse of that approach.

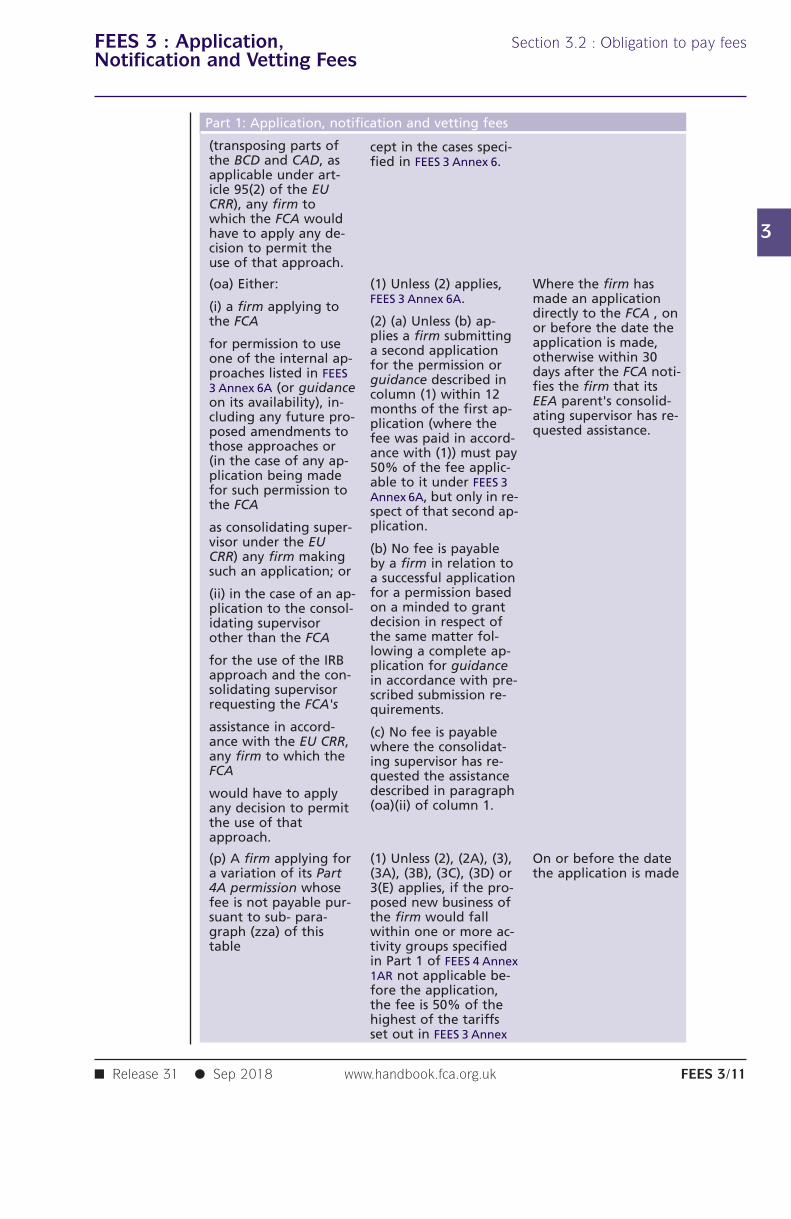

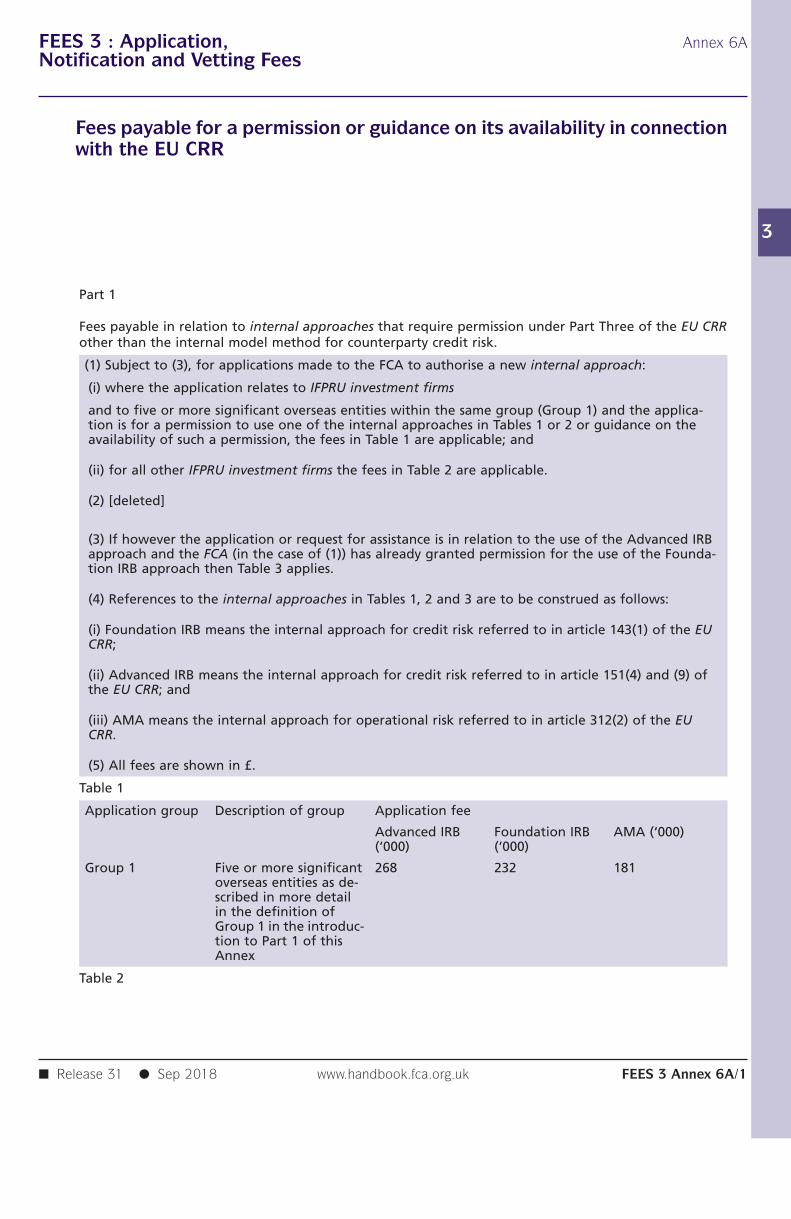

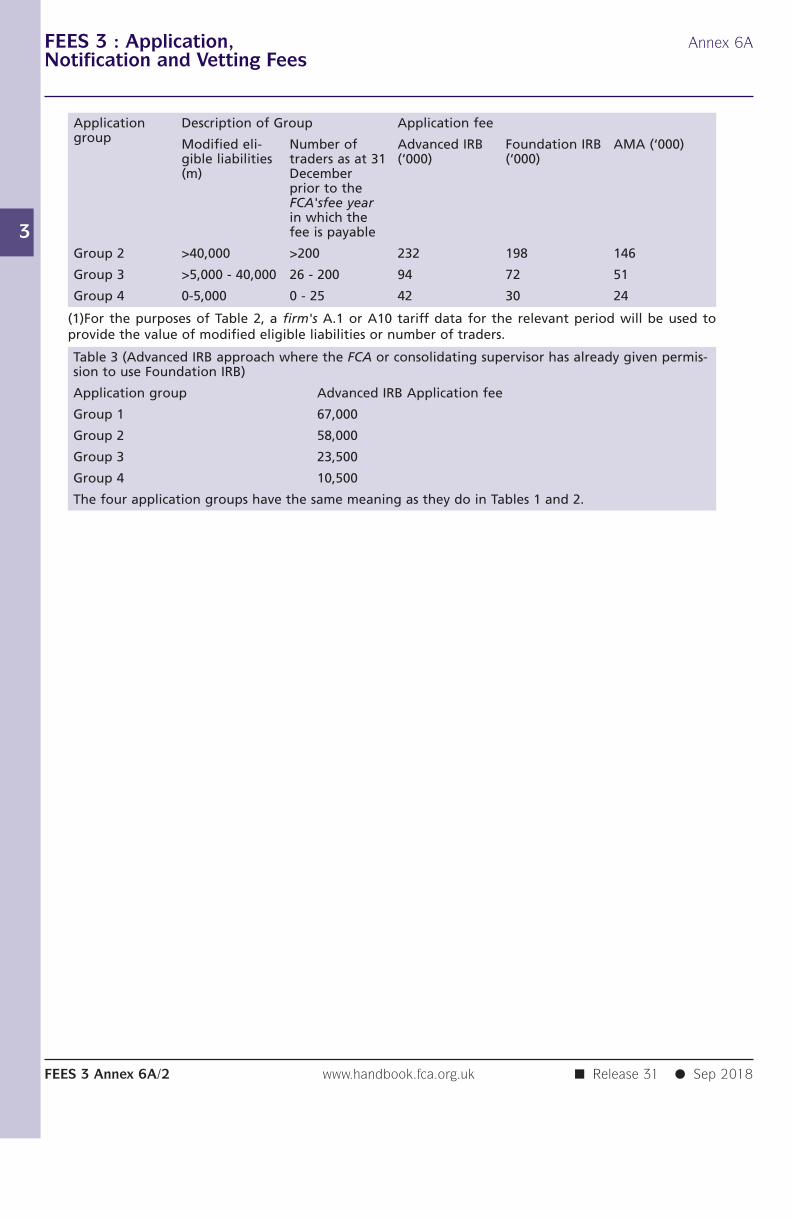

(oa) Either: (1) Unless (2) applies, Where the firm hasFEES 3 Annex 6A. made an application

(i) a firm applying to directly to the FCA , onthe FCA (2) (a) Unless (b) ap- or before the date the

plies a firm submitting application is made,for permission to use a second application otherwise within 30one of the internal ap- for the permission or days after the FCA noti-proaches listed in FEES guidance described in fies the firm that its3 Annex 6A (or guidance column (1) within 12 EEA parent's consolid-on its availability), in- months of the first ap- ating supervisor has re-cluding any future pro- plication (where the quested assistance.posed amendments to fee was paid in accord-those approaches or ance with (1)) must pay(in the case of any ap- 50% of the fee applic-plication being made able to it under FEES 3for such permission to Annex 6A, but only in re-the FCA spect of that second ap-

plication.as consolidating super-visor under the EU (b) No fee is payableCRR) any firm making by a firm in relation tosuch an application; or a successful application

for a permission based(ii) in the case of an ap-on a minded to grantplication to the consol-decision in respect ofidating supervisorthe same matter fol-other than the FCAlowing a complete ap-

for the use of the IRB plication for guidanceapproach and the con- in accordance with pre-solidating supervisor scribed submission re-requesting the FCA's quirements.assistance in accord- (c) No fee is payableance with the EU CRR, where the consolidat-any firm to which the ing supervisor has re-FCA quested the assistance

described in paragraphwould have to apply(oa)(ii) of column 1.any decision to permit

the use of thatapproach.

(p) A firm applying for (1) Unless (2), (2A), (3), On or before the datea variation of its Part (3A), (3B), (3C), (3D) or the application is made4A permission whose 3(E) applies, if the pro-fee is not payable pur- posed new business ofsuant to sub- para- the firm would fallgraph (zza) of this within one or more ac-table tivity groups specified

in Part 1 of FEES 4 Annex1AR not applicable be-fore the application,the fee is 50% of thehighest of the tariffsset out in FEES 3 Annex

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 3/12

Part 1: Application, notification and vetting fees

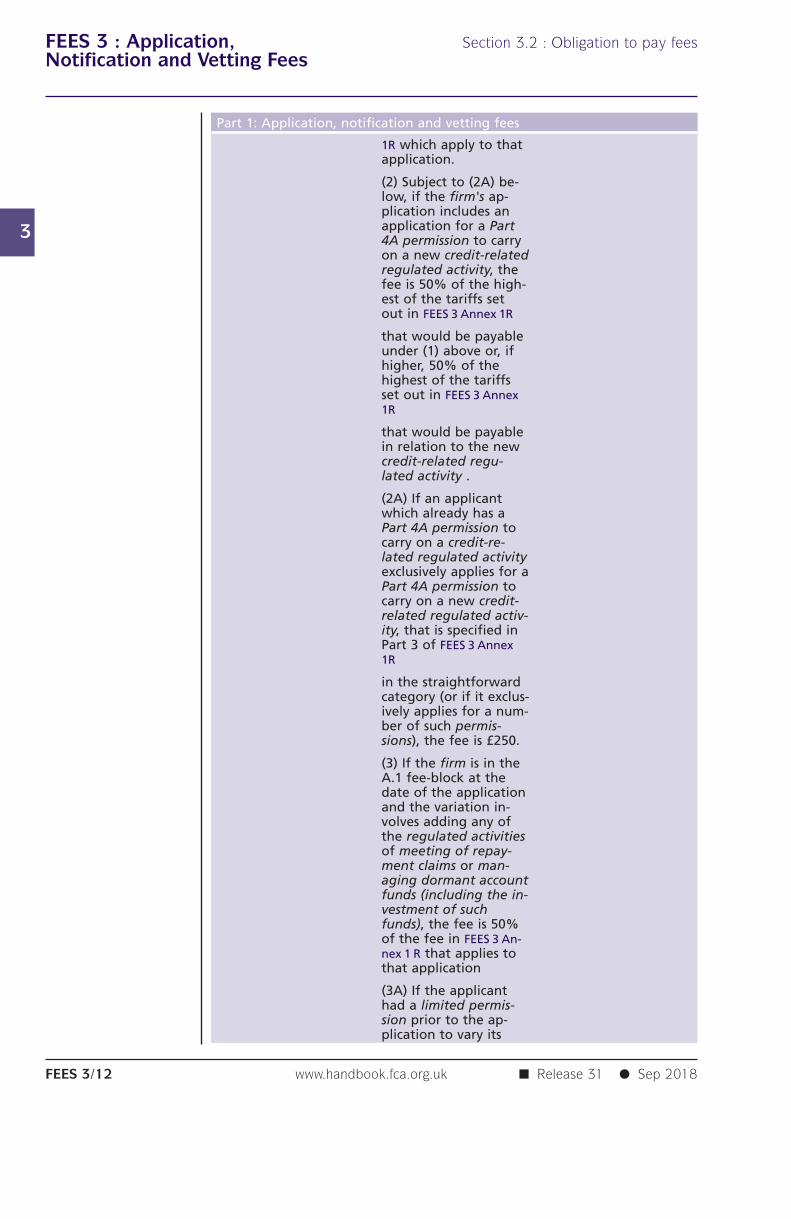

1R which apply to thatapplication.

(2) Subject to (2A) be-low, if the firm's ap-plication includes anapplication for a Part4A permission to carryon a new credit-relatedregulated activity, thefee is 50% of the high-est of the tariffs setout in FEES 3 Annex 1R

that would be payableunder (1) above or, ifhigher, 50% of thehighest of the tariffsset out in FEES 3 Annex1R

that would be payablein relation to the newcredit-related regu-lated activity .

(2A) If an applicantwhich already has aPart 4A permission tocarry on a credit-re-lated regulated activityexclusively applies for aPart 4A permission tocarry on a new credit-related regulated activ-ity, that is specified inPart 3 of FEES 3 Annex1R

in the straightforwardcategory (or if it exclus-ively applies for a num-ber of such permis-sions), the fee is £250.

(3) If the firm is in theA.1 fee-block at thedate of the applicationand the variation in-volves adding any ofthe regulated activitiesof meeting of repay-ment claims or man-aging dormant accountfunds (including the in-vestment of suchfunds), the fee is 50%of the fee in FEES 3 An-nex 1 R that applies tothat application

(3A) If the applicanthad a limited permis-sion prior to the ap-plication to vary its

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 3/13

Part 1: Application, notification and vetting fees

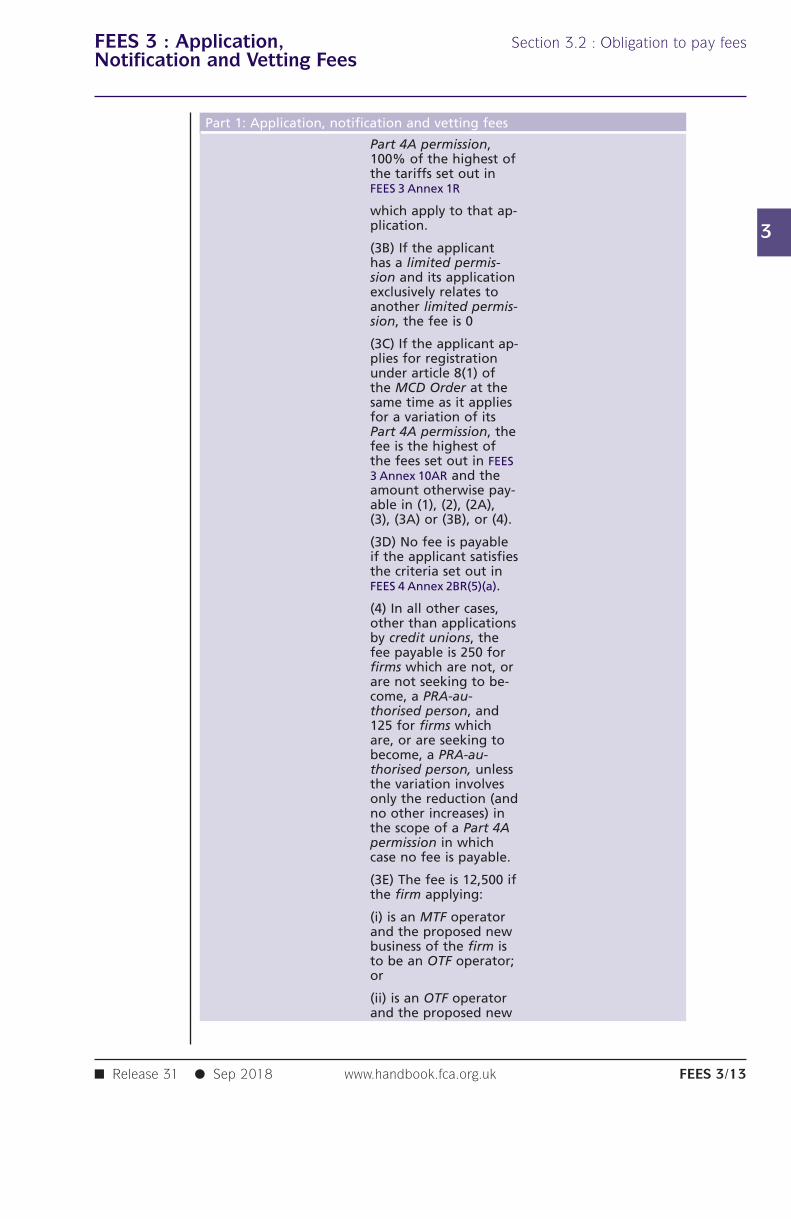

Part 4A permission,100% of the highest ofthe tariffs set out inFEES 3 Annex 1R

which apply to that ap-plication.

(3B) If the applicanthas a limited permis-sion and its applicationexclusively relates toanother limited permis-sion, the fee is 0

(3C) If the applicant ap-plies for registrationunder article 8(1) ofthe MCD Order at thesame time as it appliesfor a variation of itsPart 4A permission, thefee is the highest ofthe fees set out in FEES3 Annex 10AR and theamount otherwise pay-able in (1), (2), (2A),(3), (3A) or (3B), or (4).

(3D) No fee is payableif the applicant satisfiesthe criteria set out inFEES 4 Annex 2BR(5)(a).

(4) In all other cases,other than applicationsby credit unions, thefee payable is 250 forfirms which are not, orare not seeking to be-come, a PRA-au-thorised person, and125 for firms whichare, or are seeking tobecome, a PRA-au-thorised person, unlessthe variation involvesonly the reduction (andno other increases) inthe scope of a Part 4Apermission in whichcase no fee is payable.

(3E) The fee is 12,500 ifthe firm applying:

(i) is an MTF operatorand the proposed newbusiness of the firm isto be an OTF operator;or

(ii) is an OTF operatorand the proposed new

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 3/14

Part 1: Application, notification and vetting fees

business of the firm isto be an MTF operator.

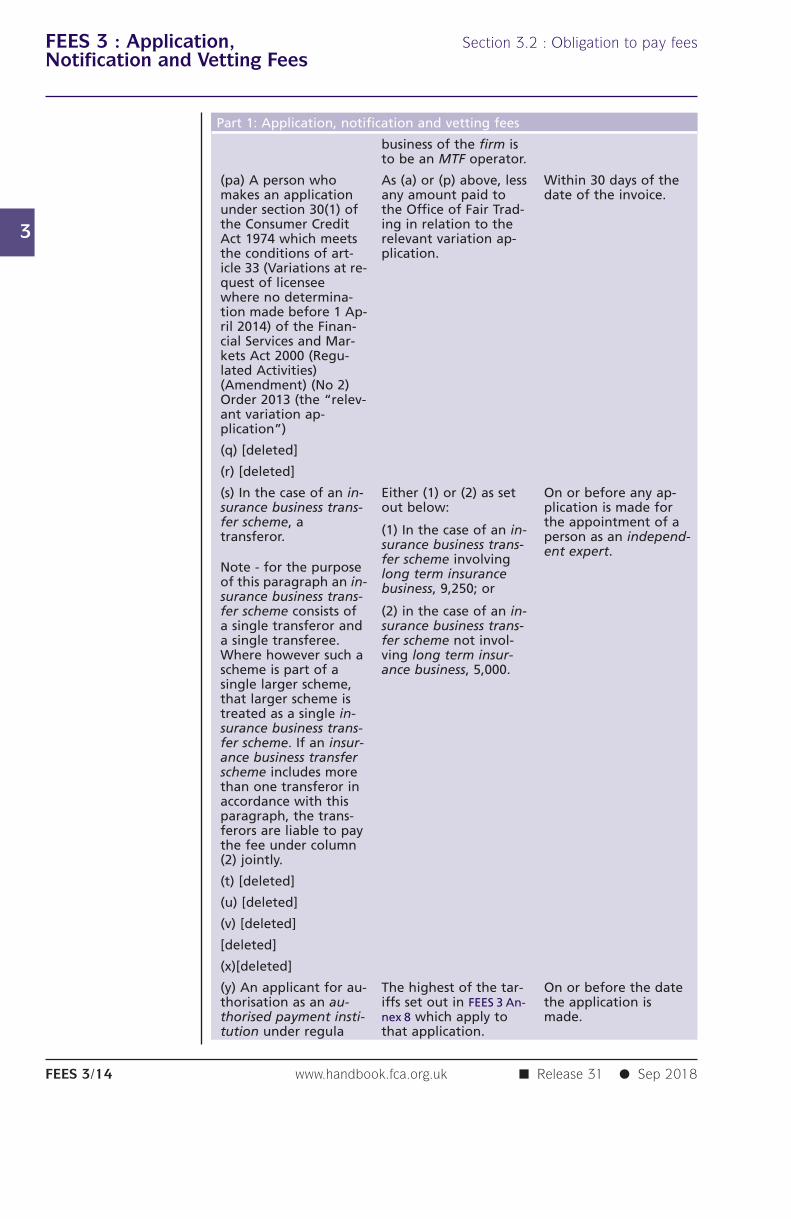

(pa) A person who As (a) or (p) above, less Within 30 days of themakes an application any amount paid to date of the invoice.under section 30(1) of the Office of Fair Trad-the Consumer Credit ing in relation to theAct 1974 which meets relevant variation ap-the conditions of art- plication.icle 33 (Variations at re-quest of licenseewhere no determina-tion made before 1 Ap-ril 2014) of the Finan-cial Services and Mar-kets Act 2000 (Regu-lated Activities)(Amendment) (No 2)Order 2013 (the “relev-ant variation ap-plication”)

(q) [deleted]

(r) [deleted]

(s) In the case of an in- Either (1) or (2) as set On or before any ap-surance business trans- out below: plication is made forfer scheme, a the appointment of a

(1) In the case of an in-transferor. person as an independ-surance business trans- ent expert.fer scheme involving

Note - for the purpose long term insuranceof this paragraph an in- business, 9,250; orsurance business trans-fer scheme consists of (2) in the case of an in-a single transferor and surance business trans-a single transferee. fer scheme not invol-Where however such a ving long term insur-scheme is part of a ance business, 5,000.single larger scheme,that larger scheme istreated as a single in-surance business trans-fer scheme. If an insur-ance business transferscheme includes morethan one transferor inaccordance with thisparagraph, the trans-ferors are liable to paythe fee under column(2) jointly.

(t) [deleted]

(u) [deleted]

(v) [deleted]

[deleted]

(x)[deleted]

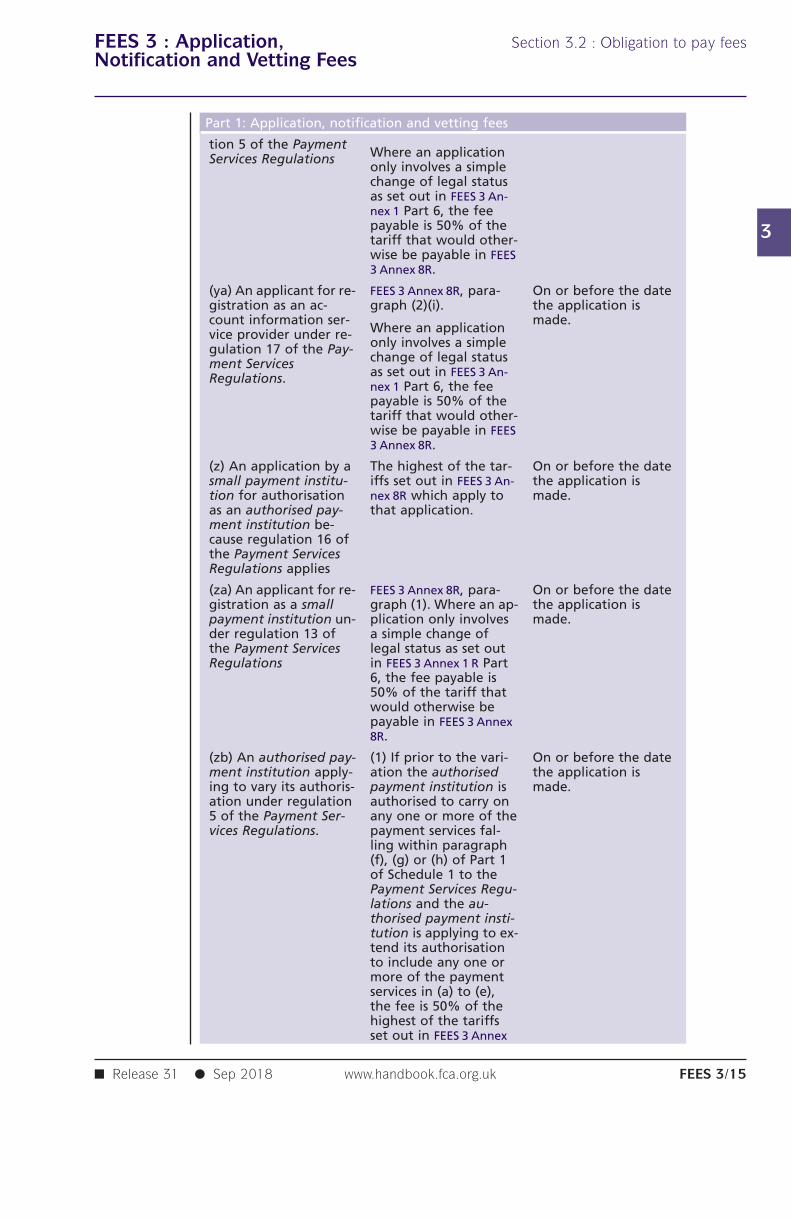

(y) An applicant for au- The highest of the tar- On or before the datethorisation as an au- iffs set out in FEES 3 An- the application isthorised payment insti- nex 8 which apply to made.tution under regula that application.

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 3/15

Part 1: Application, notification and vetting fees

tion 5 of the PaymentWhere an applicationServices Regulationsonly involves a simplechange of legal statusas set out in FEES 3 An-nex 1 Part 6, the feepayable is 50% of thetariff that would other-wise be payable in FEES3 Annex 8R.

(ya) An applicant for re- FEES 3 Annex 8R, para- On or before the dategistration as an ac- graph (2)(i). the application iscount information ser- made.

Where an applicationvice provider under re-only involves a simplegulation 17 of the Pay-change of legal statusment Servicesas set out in FEES 3 An-Regulations.nex 1 Part 6, the feepayable is 50% of thetariff that would other-wise be payable in FEES3 Annex 8R.

(z) An application by a The highest of the tar- On or before the datesmall payment institu- iffs set out in FEES 3 An- the application istion for authorisation nex 8R which apply to made.as an authorised pay- that application.ment institution be-cause regulation 16 ofthe Payment ServicesRegulations applies

(za) An applicant for re- FEES 3 Annex 8R, para- On or before the dategistration as a small graph (1). Where an ap- the application ispayment institution un- plication only involves made.der regulation 13 of a simple change ofthe Payment Services legal status as set outRegulations in FEES 3 Annex 1 R Part

6, the fee payable is50% of the tariff thatwould otherwise bepayable in FEES 3 Annex8R.

(zb) An authorised pay- (1) If prior to the vari- On or before the datement institution apply- ation the authorised the application ising to vary its authoris- payment institution is made.ation under regulation authorised to carry on5 of the Payment Ser- any one or more of thevices Regulations. payment services fal-

ling within paragraph(f), (g) or (h) of Part 1of Schedule 1 to thePayment Services Regu-lations and the au-thorised payment insti-tution is applying to ex-tend its authorisationto include any one ormore of the paymentservices in (a) to (e),the fee is 50% of thehighest of the tariffsset out in FEES 3 Annex

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 3/16

Part 1: Application, notification and vetting fees

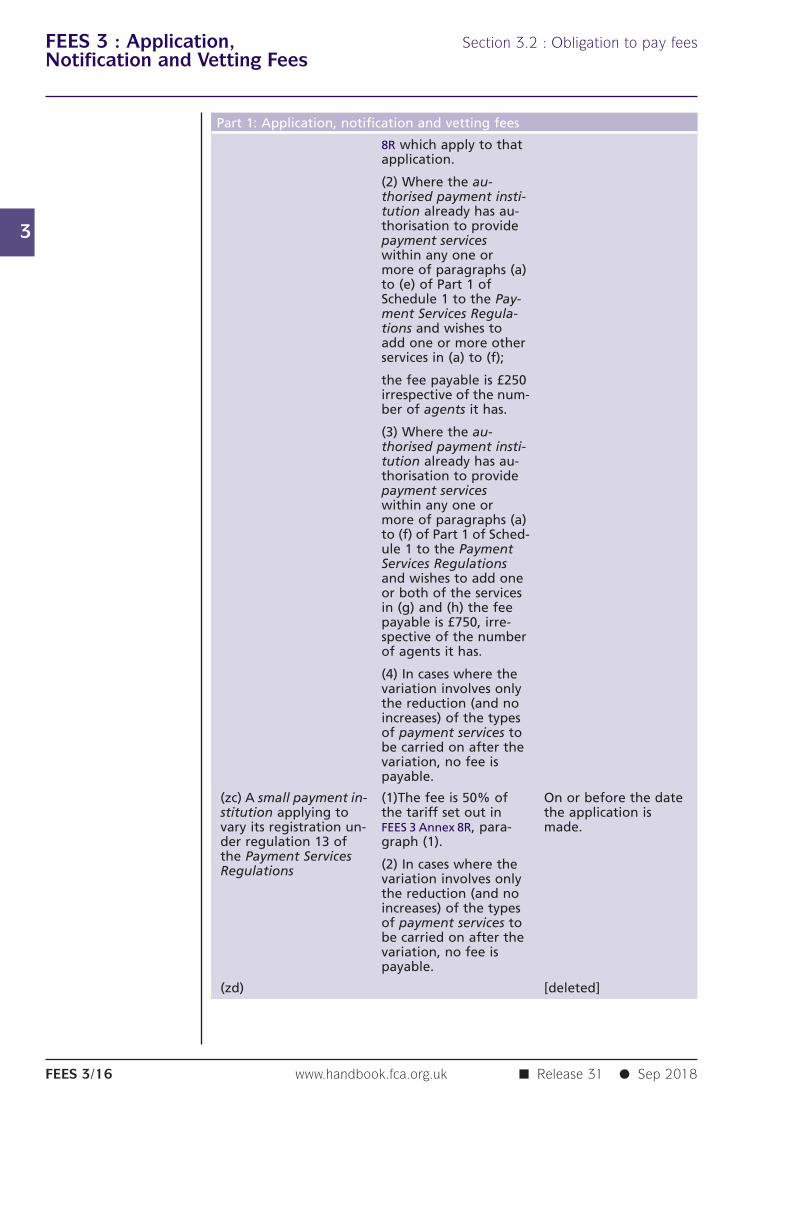

8R which apply to thatapplication.

(2) Where the au-thorised payment insti-tution already has au-thorisation to providepayment serviceswithin any one ormore of paragraphs (a)to (e) of Part 1 ofSchedule 1 to the Pay-ment Services Regula-tions and wishes toadd one or more otherservices in (a) to (f);

the fee payable is £250irrespective of the num-ber of agents it has.

(3) Where the au-thorised payment insti-tution already has au-thorisation to providepayment serviceswithin any one ormore of paragraphs (a)to (f) of Part 1 of Sched-ule 1 to the PaymentServices Regulationsand wishes to add oneor both of the servicesin (g) and (h) the feepayable is £750, irre-spective of the numberof agents it has.

(4) In cases where thevariation involves onlythe reduction (and noincreases) of the typesof payment services tobe carried on after thevariation, no fee ispayable.

(zc) A small payment in- (1)The fee is 50% of On or before the datestitution applying to the tariff set out in the application isvary its registration un- FEES 3 Annex 8R, para- made.der regulation 13 of graph (1).the Payment Services

(2) In cases where theRegulationsvariation involves onlythe reduction (and noincreases) of the typesof payment services tobe carried on after thevariation, no fee ispayable.

(zd) [deleted]

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 3/17

Part 1: Application, notification and vetting fees

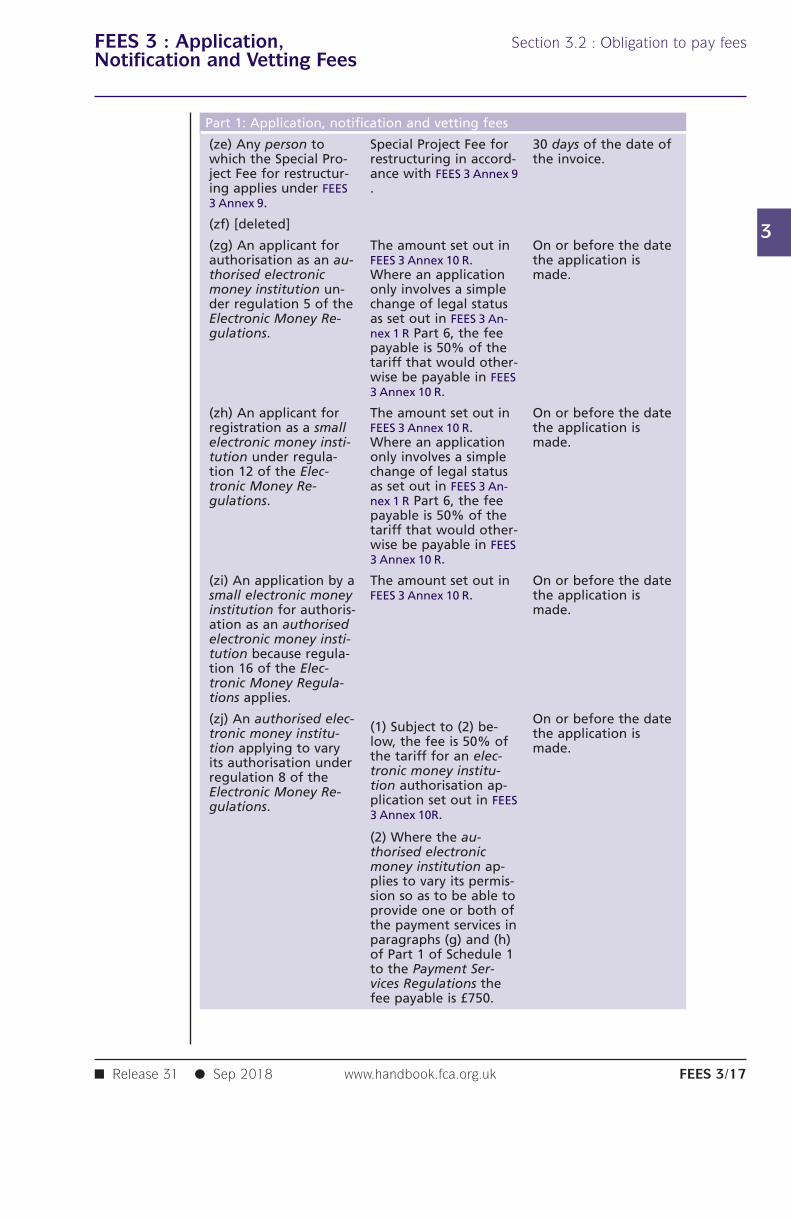

(ze) Any person to Special Project Fee for 30 days of the date ofwhich the Special Pro- restructuring in accord- the invoice.ject Fee for restructur- ance with FEES 3 Annex 9ing applies under FEES .3 Annex 9.

(zf) [deleted]

(zg) An applicant for The amount set out in On or before the dateauthorisation as an au- FEES 3 Annex 10 R. the application isthorised electronic Where an application made.money institution un- only involves a simpleder regulation 5 of the change of legal statusElectronic Money Re- as set out in FEES 3 An-gulations. nex 1 R Part 6, the fee

payable is 50% of thetariff that would other-wise be payable in FEES3 Annex 10 R.

(zh) An applicant for The amount set out in On or before the dateregistration as a small FEES 3 Annex 10 R. the application iselectronic money insti- Where an application made.tution under regula- only involves a simpletion 12 of the Elec- change of legal statustronic Money Re- as set out in FEES 3 An-gulations. nex 1 R Part 6, the fee

payable is 50% of thetariff that would other-wise be payable in FEES3 Annex 10 R.

(zi) An application by a The amount set out in On or before the datesmall electronic money FEES 3 Annex 10 R. the application isinstitution for authoris- made.ation as an authorisedelectronic money insti-tution because regula-tion 16 of the Elec-tronic Money Regula-tions applies.

(zj) An authorised elec- On or before the date(1) Subject to (2) be-tronic money institu- the application islow, the fee is 50% oftion applying to vary made.the tariff for an elec-its authorisation undertronic money institu-regulation 8 of thetion authorisation ap-Electronic Money Re-plication set out in FEESgulations.3 Annex 10R.

(2) Where the au-thorised electronicmoney institution ap-plies to vary its permis-sion so as to be able toprovide one or both ofthe payment services inparagraphs (g) and (h)of Part 1 of Schedule 1to the Payment Ser-vices Regulations thefee payable is £750.

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 3/18

Part 1: Application, notification and vetting fees

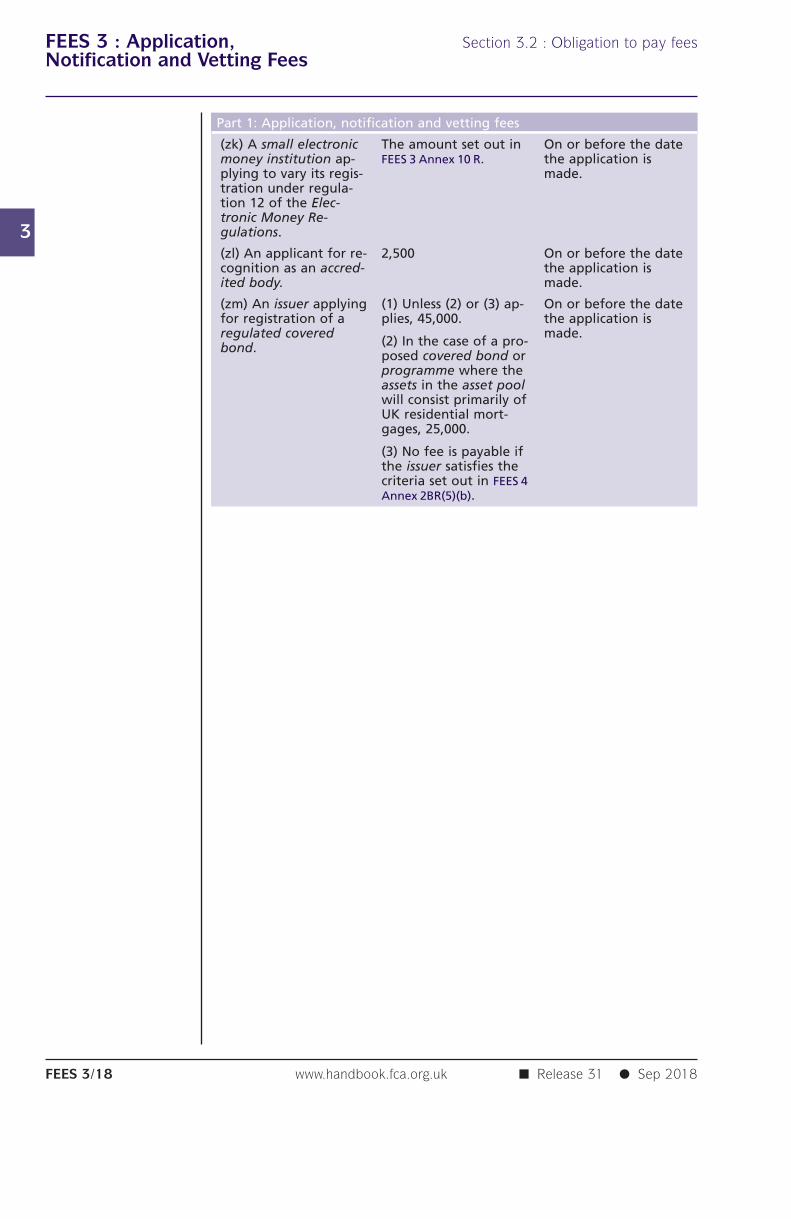

(zk) A small electronic The amount set out in On or before the datemoney institution ap- FEES 3 Annex 10 R. the application isplying to vary its regis- made.tration under regula-tion 12 of the Elec-tronic Money Re-gulations.

(zl) An applicant for re- 2,500 On or before the datecognition as an accred- the application isited body. made.

(zm) An issuer applying (1) Unless (2) or (3) ap- On or before the datefor registration of a plies, 45,000. the application isregulated covered made.

(2) In the case of a pro-bond.posed covered bond orprogramme where theassets in the asset poolwill consist primarily ofUK residential mort-gages, 25,000.

(3) No fee is payable ifthe issuer satisfies thecriteria set out in FEES 4Annex 2BR(5)(b).

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 3/19

Part 1: Application, notification and vetting fees

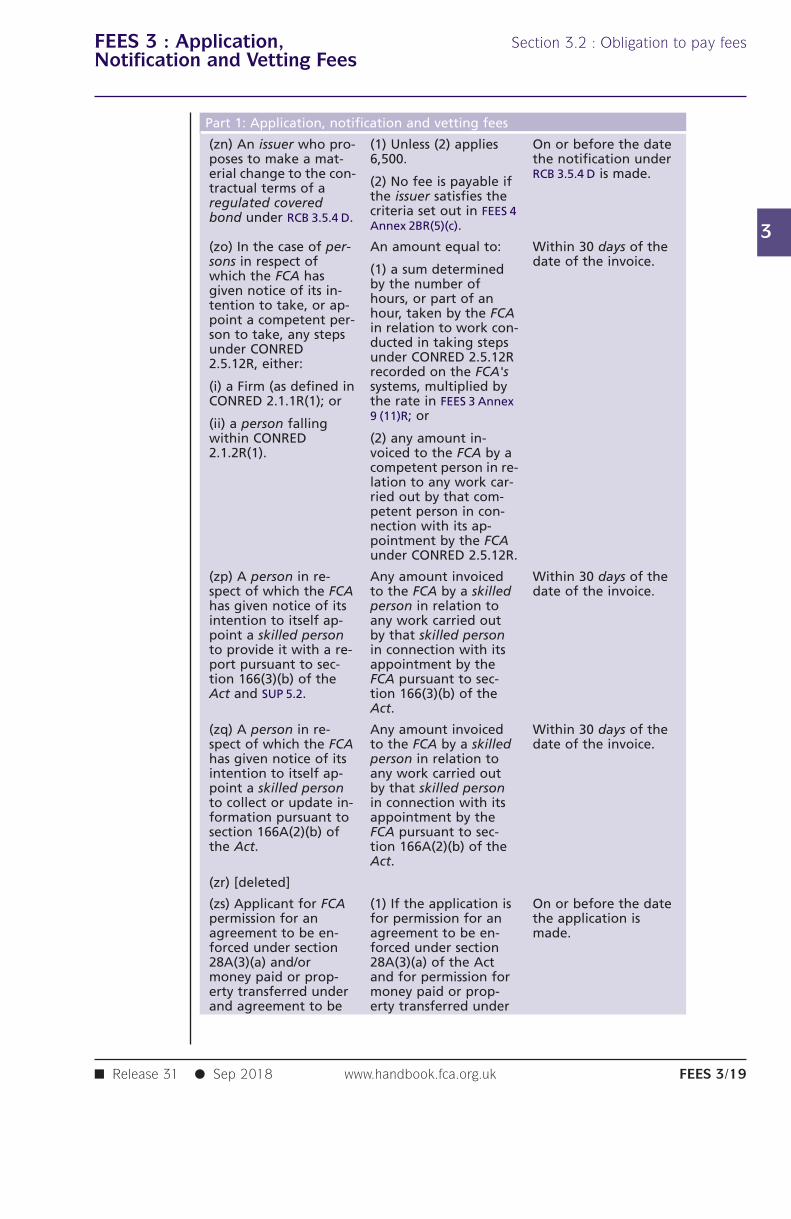

(zn) An issuer who pro- (1) Unless (2) applies On or before the dateposes to make a mat- 6,500. the notification undererial change to the con- RCB 3.5.4 D is made.

(2) No fee is payable iftractual terms of athe issuer satisfies theregulated coveredcriteria set out in FEES 4bond under RCB 3.5.4 D.Annex 2BR(5)(c).

(zo) In the case of per- An amount equal to: Within 30 days of thesons in respect of date of the invoice.

(1) a sum determinedwhich the FCA hasby the number ofgiven notice of its in-hours, or part of antention to take, or ap-hour, taken by the FCApoint a competent per-in relation to work con-son to take, any stepsducted in taking stepsunder CONREDunder CONRED 2.5.12R2.5.12R, either:recorded on the FCA's

(i) a Firm (as defined in systems, multiplied byCONRED 2.1.1R(1); or the rate in FEES 3 Annex

9 (11)R; or(ii) a person fallingwithin CONRED (2) any amount in-2.1.2R(1). voiced to the FCA by a

competent person in re-lation to any work car-ried out by that com-petent person in con-nection with its ap-pointment by the FCAunder CONRED 2.5.12R.

(zp) A person in re- Any amount invoiced Within 30 days of thespect of which the FCA to the FCA by a skilled date of the invoice.has given notice of its person in relation tointention to itself ap- any work carried outpoint a skilled person by that skilled personto provide it with a re- in connection with itsport pursuant to sec- appointment by thetion 166(3)(b) of the FCA pursuant to sec-Act and SUP 5.2. tion 166(3)(b) of the

Act.

(zq) A person in re- Any amount invoiced Within 30 days of thespect of which the FCA to the FCA by a skilled date of the invoice.has given notice of its person in relation tointention to itself ap- any work carried outpoint a skilled person by that skilled personto collect or update in- in connection with itsformation pursuant to appointment by thesection 166A(2)(b) of FCA pursuant to sec-the Act. tion 166A(2)(b) of the

Act.

(zr) [deleted]

(zs) Applicant for FCA (1) If the application is On or before the datepermission for an for permission for an the application isagreement to be en- agreement to be en- made.forced under section forced under section28A(3)(a) and/or 28A(3)(a) of the Actmoney paid or prop- and for permission forerty transferred under money paid or prop-and agreement to be erty transferred under

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 3/20

Part 1: Application, notification and vetting fees

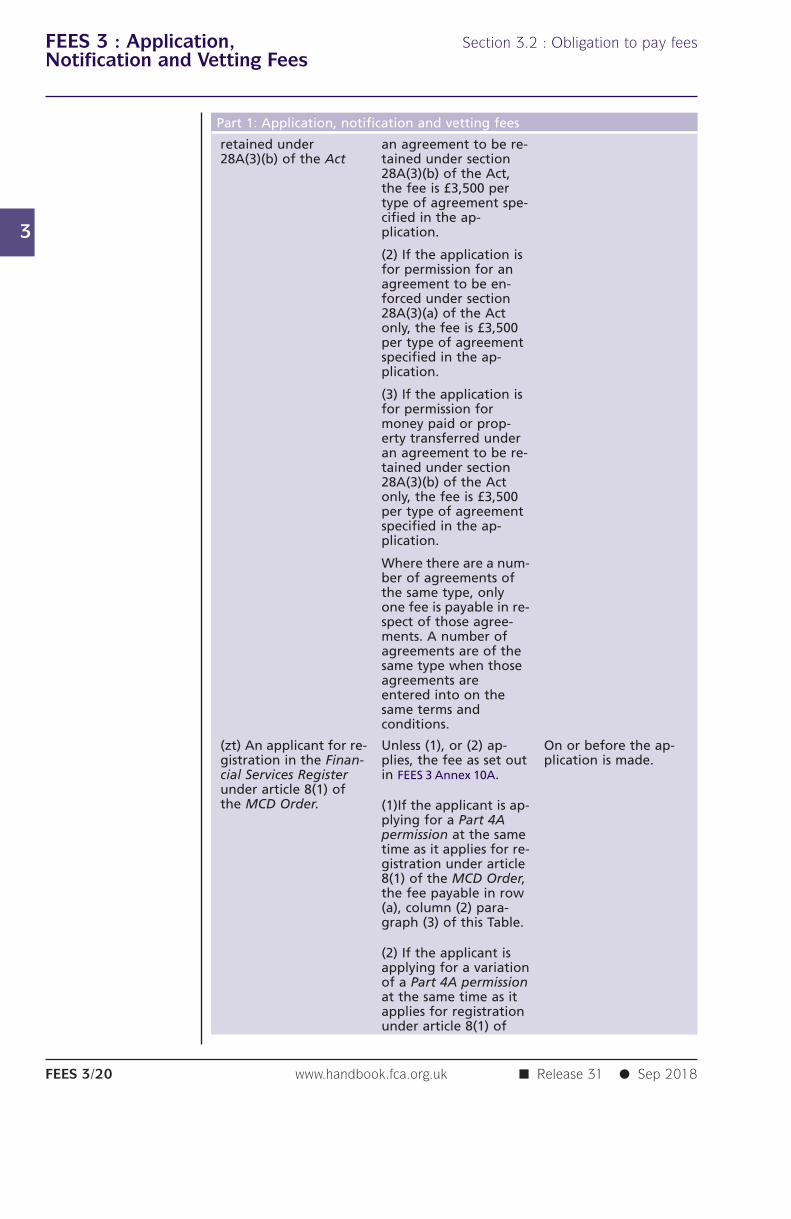

retained under an agreement to be re-28A(3)(b) of the Act tained under section

28A(3)(b) of the Act,the fee is £3,500 pertype of agreement spe-cified in the ap-plication.

(2) If the application isfor permission for anagreement to be en-forced under section28A(3)(a) of the Actonly, the fee is £3,500per type of agreementspecified in the ap-plication.

(3) If the application isfor permission formoney paid or prop-erty transferred underan agreement to be re-tained under section28A(3)(b) of the Actonly, the fee is £3,500per type of agreementspecified in the ap-plication.

Where there are a num-ber of agreements ofthe same type, onlyone fee is payable in re-spect of those agree-ments. A number ofagreements are of thesame type when thoseagreements areentered into on thesame terms andconditions.

(zt) An applicant for re- Unless (1), or (2) ap- On or before the ap-gistration in the Finan- plies, the fee as set out plication is made.cial Services Register in FEES 3 Annex 10A.under article 8(1) ofthe MCD Order. (1)If the applicant is ap-

plying for a Part 4Apermission at the sametime as it applies for re-gistration under article8(1) of the MCD Order,the fee payable in row(a), column (2) para-graph (3) of this Table.

(2) If the applicant isapplying for a variationof a Part 4A permissionat the same time as itapplies for registrationunder article 8(1) of

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 3/21

Part 1: Application, notification and vetting fees

the MCD Order, the feepayable in row (p), col-umn 2 paragraph (3)(c)of this Table.

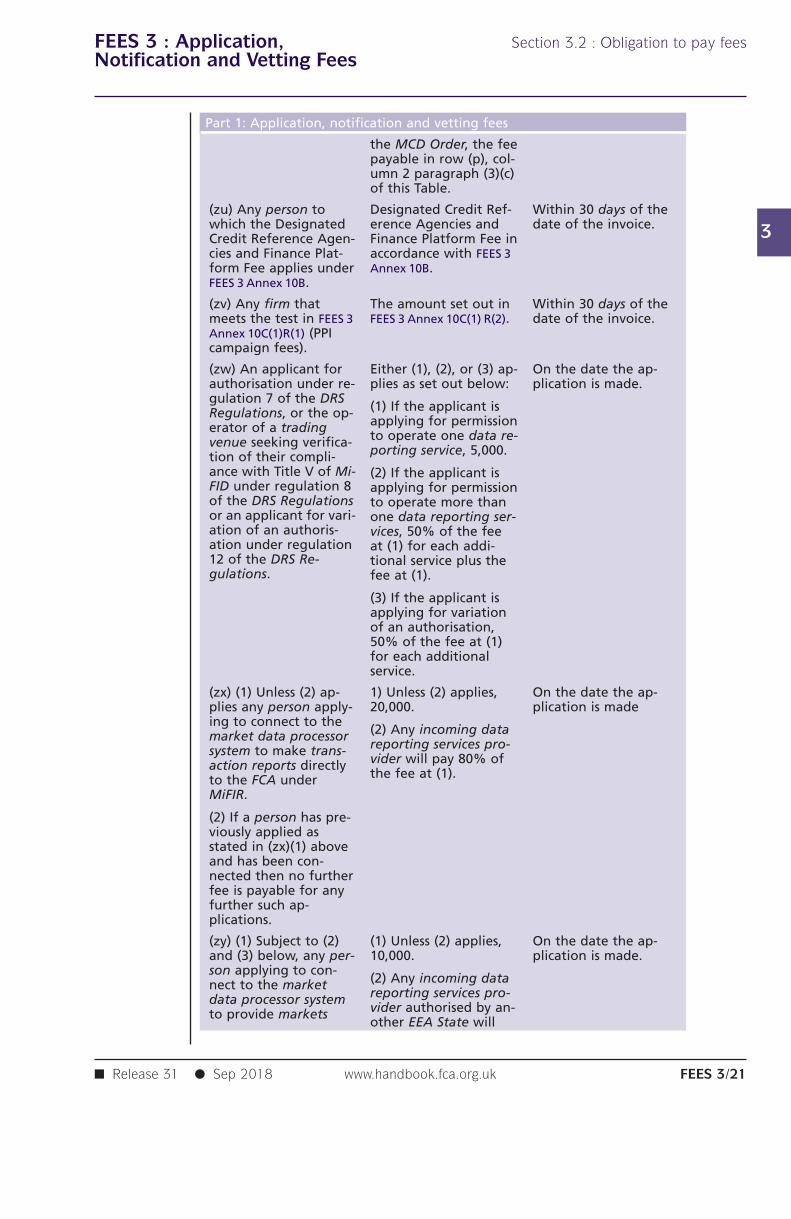

(zu) Any person to Designated Credit Ref- Within 30 days of thewhich the Designated erence Agencies and date of the invoice.Credit Reference Agen- Finance Platform Fee incies and Finance Plat- accordance with FEES 3form Fee applies under Annex 10B.FEES 3 Annex 10B.

(zv) Any firm that The amount set out in Within 30 days of themeets the test in FEES 3 FEES 3 Annex 10C(1) R(2). date of the invoice.Annex 10C(1)R(1) (PPIcampaign fees).

(zw) An applicant for Either (1), (2), or (3) ap- On the date the ap-authorisation under re- plies as set out below: plication is made.gulation 7 of the DRS

(1) If the applicant isRegulations, or the op-applying for permissionerator of a tradingto operate one data re-venue seeking verifica-porting service, 5,000.tion of their compli-

ance with Title V of Mi- (2) If the applicant isFID under regulation 8 applying for permissionof the DRS Regulations to operate more thanor an applicant for vari- one data reporting ser-ation of an authoris- vices, 50% of the feeation under regulation at (1) for each addi-12 of the DRS Re- tional service plus thegulations. fee at (1).

(3) If the applicant isapplying for variationof an authorisation,50% of the fee at (1)for each additionalservice.

(zx) (1) Unless (2) ap- 1) Unless (2) applies, On the date the ap-plies any person apply- 20,000. plication is madeing to connect to the

(2) Any incoming datamarket data processorreporting services pro-system to make trans-vider will pay 80% ofaction reports directlythe fee at (1).to the FCA under

MiFIR.

(2) If a person has pre-viously applied asstated in (zx)(1) aboveand has been con-nected then no furtherfee is payable for anyfurther such ap-plications.

(zy) (1) Subject to (2) (1) Unless (2) applies, On the date the ap-and (3) below, any per- 10,000. plication is made.son applying to con-

(2) Any incoming datanect to the marketreporting services pro-data processor systemvider authorised by an-to provide marketsother EEA State will

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 3/22

Part 1: Application, notification and vetting fees

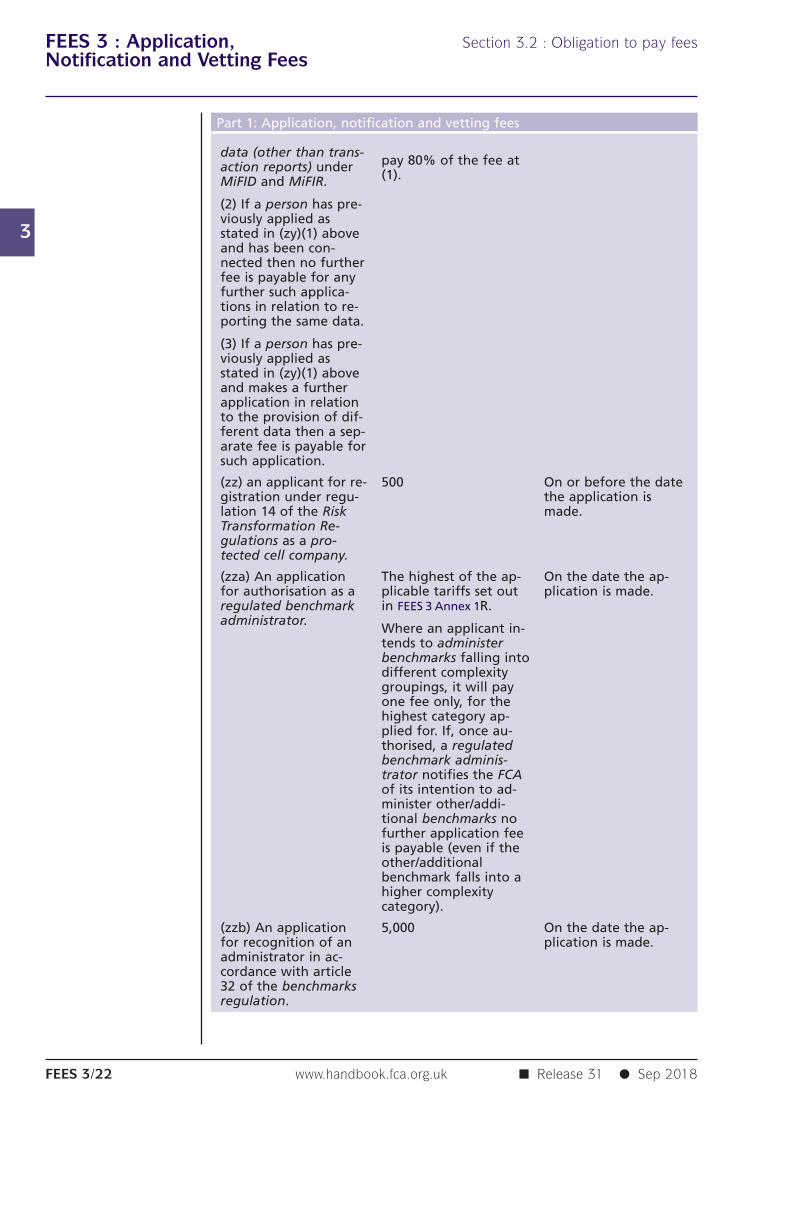

data (other than trans-pay 80% of the fee ataction reports) under(1).MiFID and MiFIR.

(2) If a person has pre-viously applied asstated in (zy)(1) aboveand has been con-nected then no furtherfee is payable for anyfurther such applica-tions in relation to re-porting the same data.

(3) If a person has pre-viously applied asstated in (zy)(1) aboveand makes a furtherapplication in relationto the provision of dif-ferent data then a sep-arate fee is payable forsuch application.

(zz) an applicant for re- 500 On or before the dategistration under regu- the application islation 14 of the Risk made.Transformation Re-gulations as a pro-tected cell company.

(zza) An application The highest of the ap- On the date the ap-for authorisation as a plicable tariffs set out plication is made.regulated benchmark in FEES 3 Annex 1R.administrator.

Where an applicant in-tends to administerbenchmarks falling intodifferent complexitygroupings, it will payone fee only, for thehighest category ap-plied for. If, once au-thorised, a regulatedbenchmark adminis-trator notifies the FCAof its intention to ad-minister other/addi-tional benchmarks nofurther application feeis payable (even if theother/additionalbenchmark falls into ahigher complexitycategory).

(zzb) An application 5,000 On the date the ap-for recognition of an plication is made.administrator in ac-cordance with article32 of the benchmarksregulation.

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 3/23

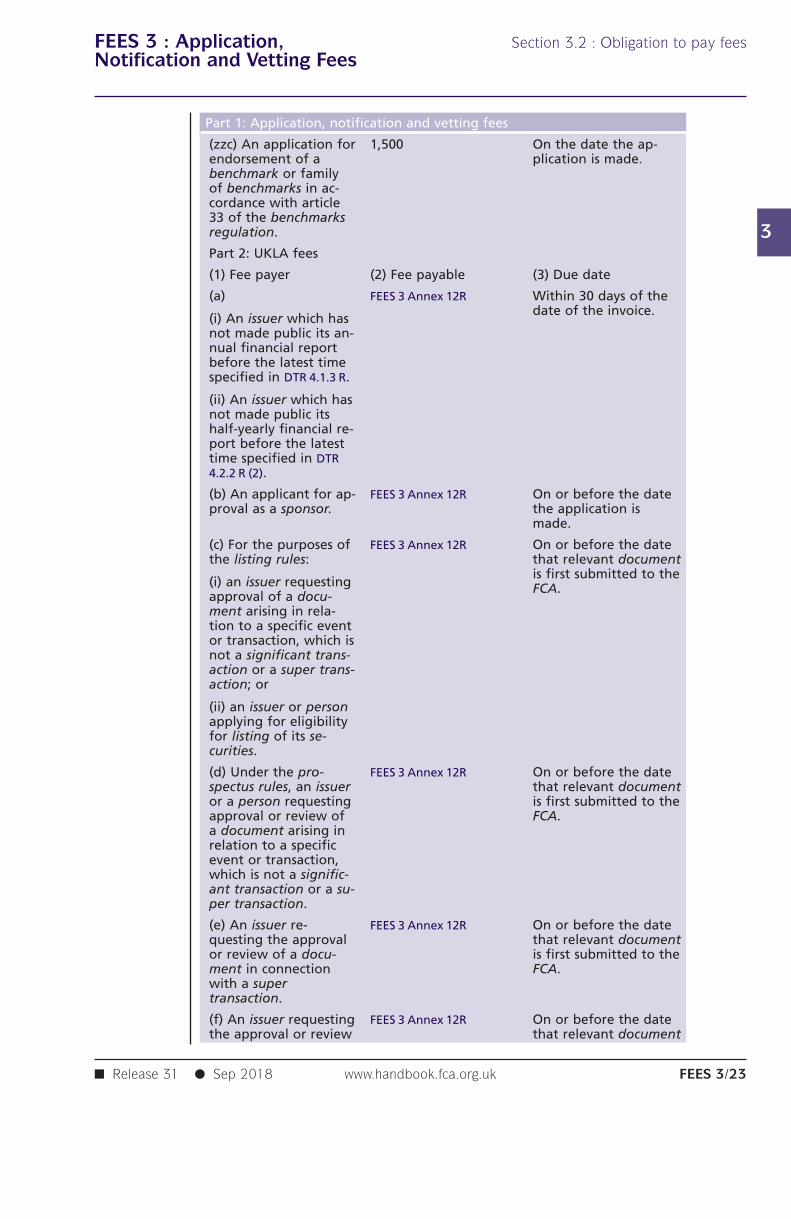

Part 1: Application, notification and vetting fees

(zzc) An application for 1,500 On the date the ap-endorsement of a plication is made.benchmark or familyof benchmarks in ac-cordance with article33 of the benchmarksregulation.

Part 2: UKLA fees

(1) Fee payer (2) Fee payable (3) Due date

(a) FEES 3 Annex 12R Within 30 days of thedate of the invoice.

(i) An issuer which hasnot made public its an-nual financial reportbefore the latest timespecified in DTR 4.1.3 R.

(ii) An issuer which hasnot made public itshalf-yearly financial re-port before the latesttime specified in DTR4.2.2 R (2).

(b) An applicant for ap- FEES 3 Annex 12R On or before the dateproval as a sponsor. the application is

made.

(c) For the purposes of FEES 3 Annex 12R On or before the datethe listing rules: that relevant document

is first submitted to the(i) an issuer requesting FCA.approval of a docu-ment arising in rela-tion to a specific eventor transaction, which isnot a significant trans-action or a super trans-action; or

(ii) an issuer or personapplying for eligibilityfor listing of its se-curities.

(d) Under the pro- FEES 3 Annex 12R On or before the datespectus rules, an issuer that relevant documentor a person requesting is first submitted to theapproval or review of FCA.a document arising inrelation to a specificevent or transaction,which is not a signific-ant transaction or a su-per transaction.

(e) An issuer re- FEES 3 Annex 12R On or before the datequesting the approval that relevant documentor review of a docu- is first submitted to thement in connection FCA.with a supertransaction.

(f) An issuer requesting FEES 3 Annex 12R On or before the datethe approval or review that relevant document

FEES 3 : Application, Section 3.2 : Obligation to pay feesNotification and Vetting Fees

3

R3.2.7A

■ Release 31 ● Sep 2018www.handbook.fca.org.ukFEES 3/24

Part 1: Application, notification and vetting fees

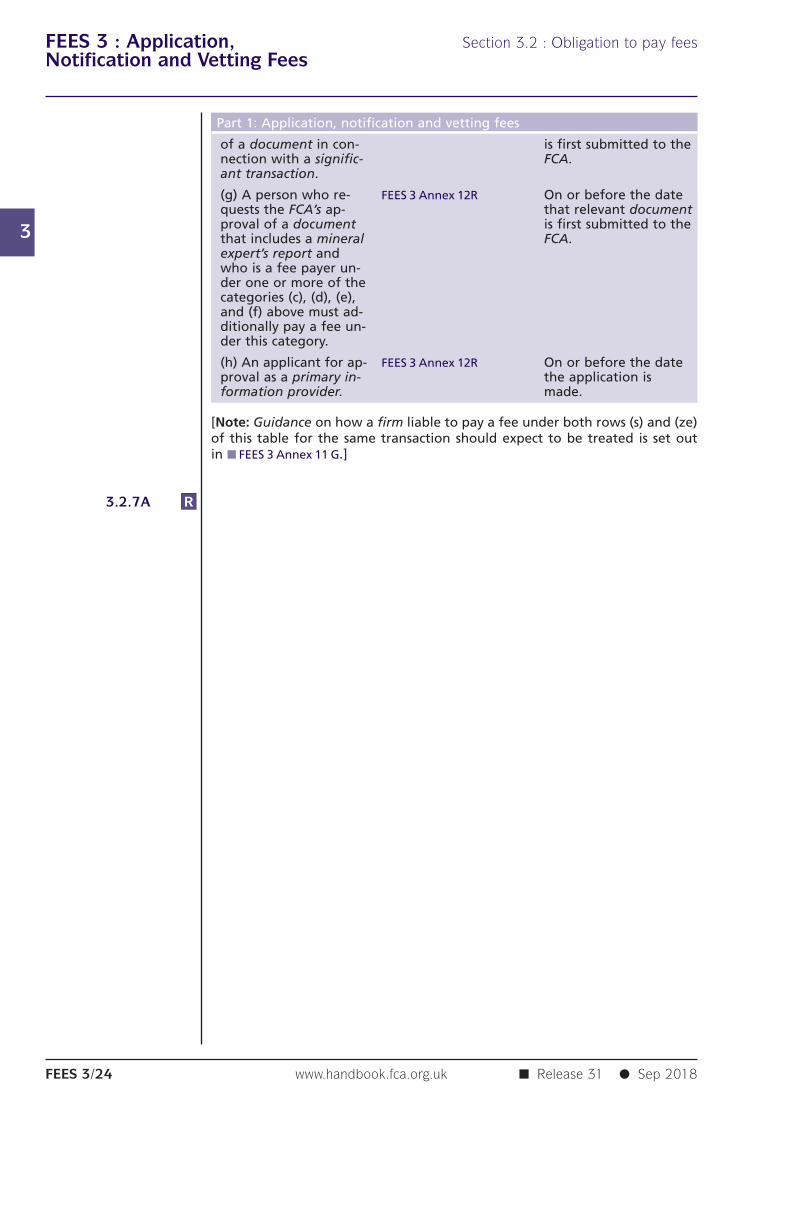

of a document in con- is first submitted to thenection with a signific- FCA.ant transaction.

(g) A person who re- FEES 3 Annex 12R On or before the datequests the FCA’s ap- that relevant documentproval of a document is first submitted to thethat includes a mineral FCA.expert’s report andwho is a fee payer un-der one or more of thecategories (c), (d), (e),and (f) above must ad-ditionally pay a fee un-der this category.

(h) An applicant for ap- FEES 3 Annex 12R On or before the dateproval as a primary in- the application isformation provider. made.

[Note: Guidance on how a firm liable to pay a fee under both rows (s) and (ze)of this table for the same transaction should expect to be treated is set outin ■ FEES 3 Annex 11 G.]

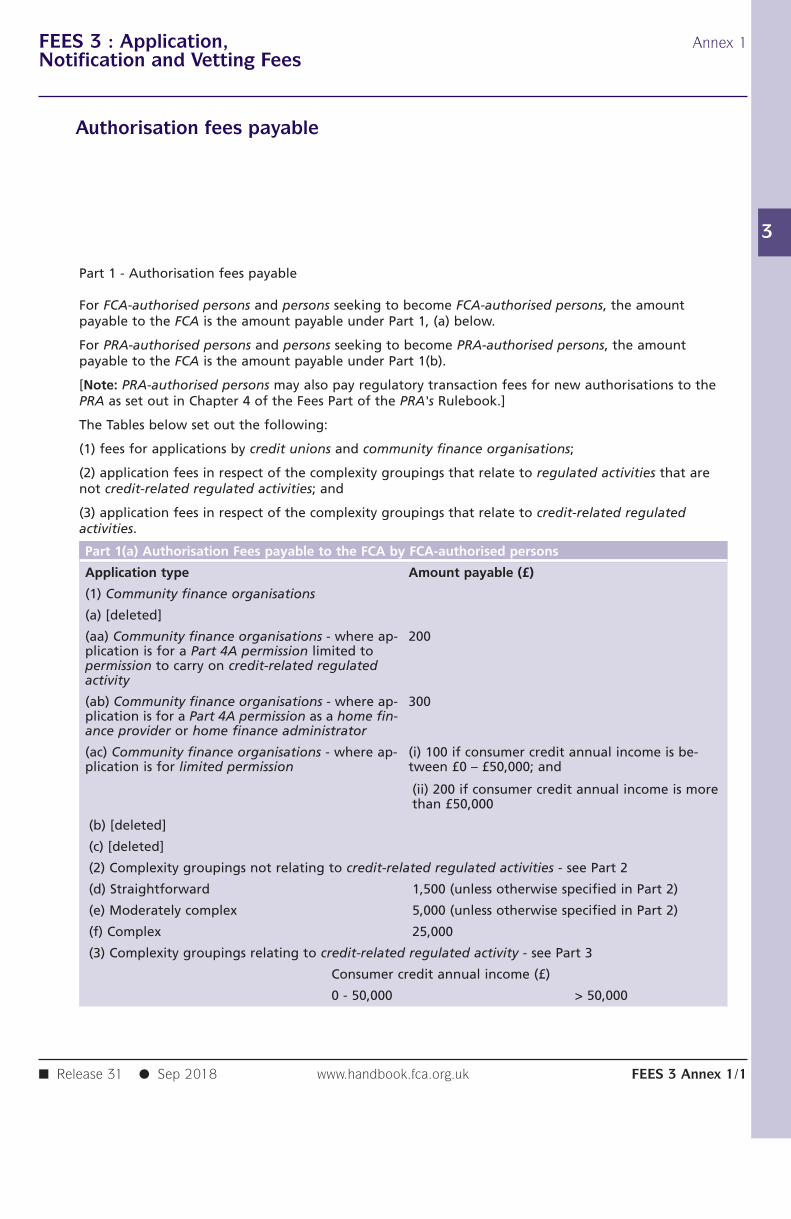

FEES 3 : Application, Annex 1Notification and Vetting Fees

3

Authorisation fees payable

Part 1 - Authorisation fees payable

For FCA-authorised persons and persons seeking to become FCA-authorised persons, the amountpayable to the FCA is the amount payable under Part 1, (a) below.

For PRA-authorised persons and persons seeking to become PRA-authorised persons, the amountpayable to the FCA is the amount payable under Part 1(b).

[Note: PRA-authorised persons may also pay regulatory transaction fees for new authorisations to thePRA as set out in Chapter 4 of the Fees Part of the PRA's Rulebook.]

The Tables below set out the following:

(1) fees for applications by credit unions and community finance organisations;

(2) application fees in respect of the complexity groupings that relate to regulated activities that arenot credit-related regulated activities; and

(3) application fees in respect of the complexity groupings that relate to credit-related regulatedactivities.

Part 1(a) Authorisation Fees payable to the FCA by FCA-authorised persons

Application type Amount payable (£)

(1) Community finance organisations

(a) [deleted]

(aa) Community finance organisations - where ap- 200plication is for a Part 4A permission limited topermission to carry on credit-related regulatedactivity

(ab) Community finance organisations - where ap- 300plication is for a Part 4A permission as a home fin-ance provider or home finance administrator

(ac) Community finance organisations - where ap- (i) 100 if consumer credit annual income is be-plication is for limited permission tween £0 – £50,000; and

(ii) 200 if consumer credit annual income is morethan £50,000

(b) [deleted]

(c) [deleted]

(2) Complexity groupings not relating to credit-related regulated activities - see Part 2

(d) Straightforward 1,500 (unless otherwise specified in Part 2)

(e) Moderately complex 5,000 (unless otherwise specified in Part 2)

(f) Complex 25,000

(3) Complexity groupings relating to credit-related regulated activity - see Part 3

Consumer credit annual income (£)

0 - 50,000 > 50,000

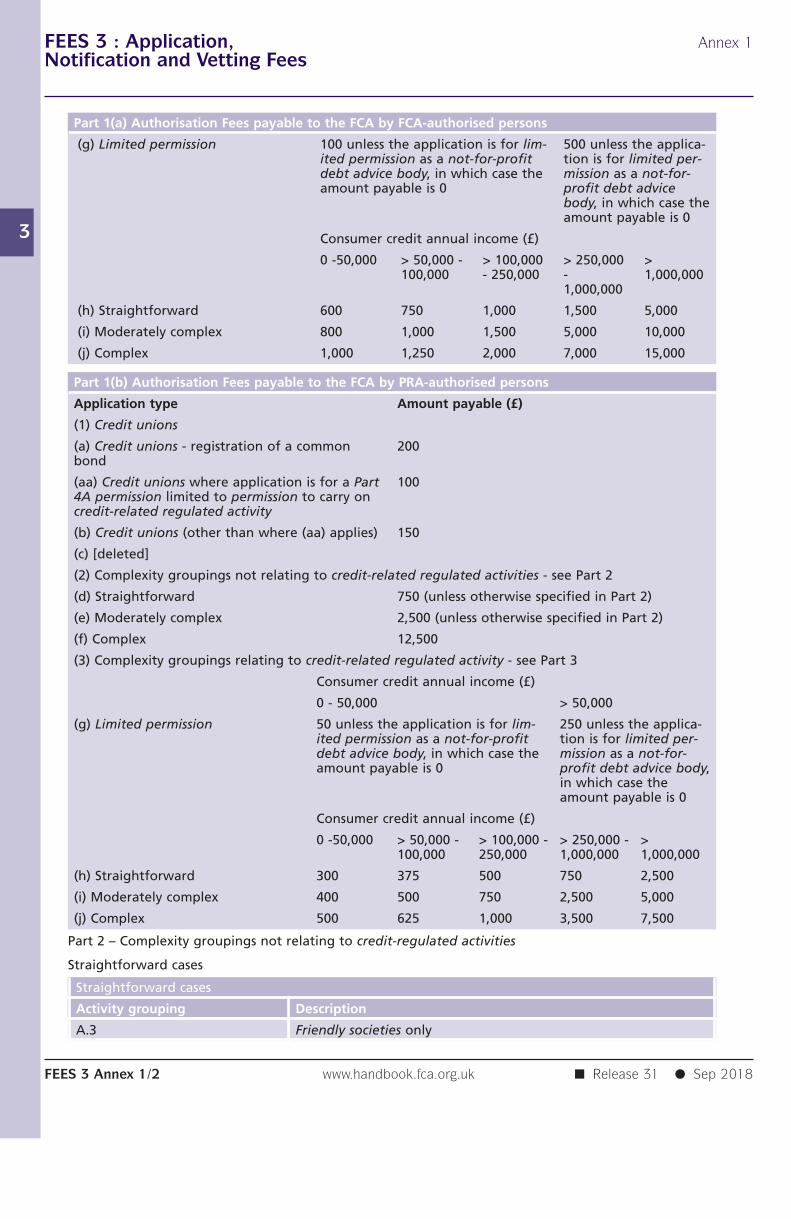

■ Release 31 ● Sep 2018 www.handbook.fca.org.uk FEES 3 Annex 1/1

FEES 3 : Application, Annex 1Notification and Vetting Fees

3

Part 1(a) Authorisation Fees payable to the FCA by FCA-authorised persons

(g) Limited permission 100 unless the application is for lim- 500 unless the applica-ited permission as a not-for-profit tion is for limited per-debt advice body, in which case the mission as a not-for-amount payable is 0 profit debt advice

body, in which case theamount payable is 0

Consumer credit annual income (£)

0 -50,000 > 50,000 - > 100,000 > 250,000 >100,000 - 250,000 - 1,000,000

1,000,000

(h) Straightforward 600 750 1,000 1,500 5,000

(i) Moderately complex 800 1,000 1,500 5,000 10,000

(j) Complex 1,000 1,250 2,000 7,000 15,000

Part 1(b) Authorisation Fees payable to the FCA by PRA-authorised persons

Application type Amount payable (£)

(1) Credit unions

(a) Credit unions - registration of a common 200bond