Economic Analysis of Housing Policy in Hong Kong

Michael Fung, Michael Leung and Fred Ku

Program for Economic Education

CUHK

Problems and Solutions

• Homeless Problem

• Affordable Housing Problem

• Poverty Problem

Outline

• Real Estate Market and Economics: Macro + Micro

• Facts: Policy History + Data

• Economic Model

• Policy Analysis and Evaluation

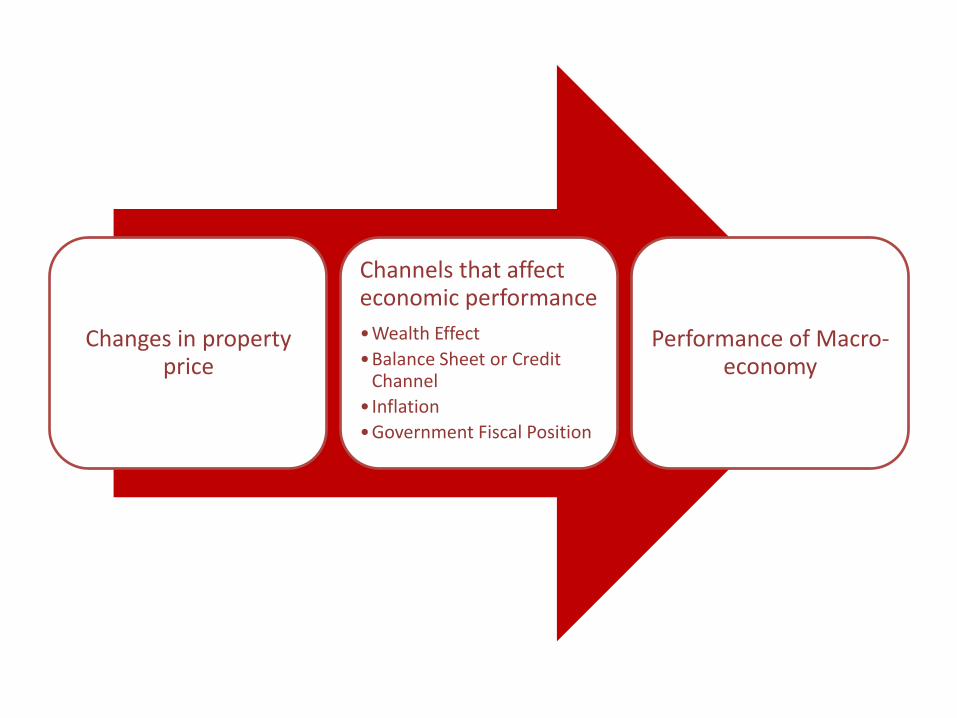

Real Estate Market and Economics

Macroeconomics

Changes in property price

Channels that affect economic performance

•Wealth Effect

•Balance Sheet or Credit Channel

• Inflation

•Government Fiscal Position

Performance of Macro-economy

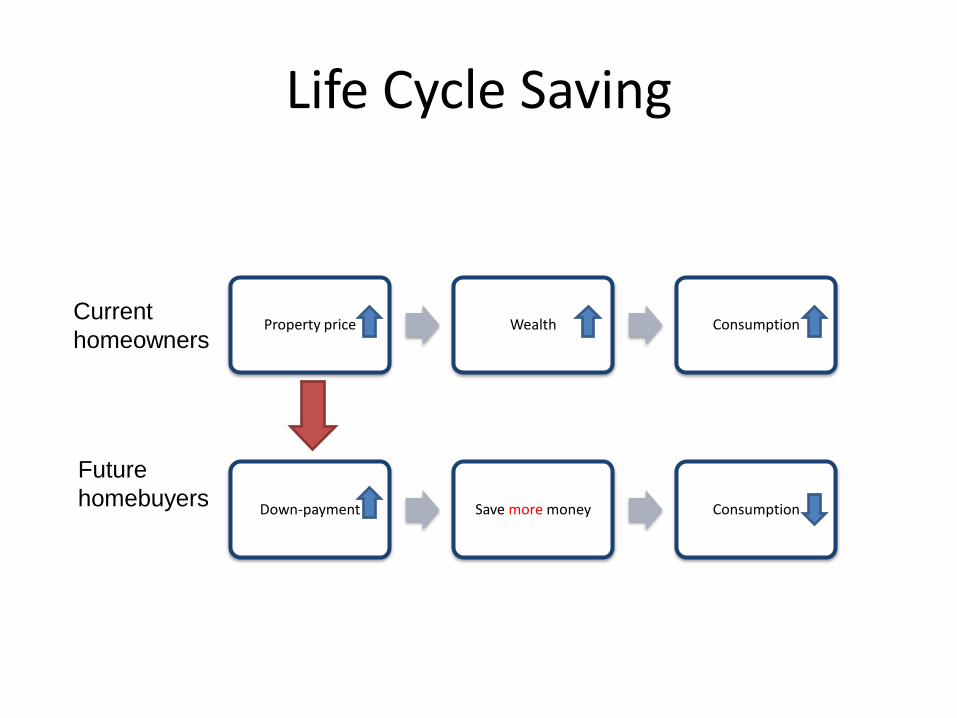

Current

homeowners

Future

homebuyers

Property price Wealth Consumption

Down-payment Save more money Consumption

Life Cycle Saving

Factors Affecting Wealth Effect

Property price changes

• Well-developed and liquid secondary market

• Well-developed financial sector

Wealth Effect

Well-Developed Financial Market

• It allows owners to obtain extra finance when they are in need

• Mortgage for properties

• Second mortgage and Refinancing

*Source:http://www.hkma.gov.hk/eng/key-information/guidelines-

and-circulars/guidelines/guide_581b.shtml

Advertisement from Financial Institutions

• http://www.youtube.com/watch?v=J9m9yMhJjaM (Konew Financial Express)

• http://www.youtube.com/watch?v=TPr3PD1bghA (UA Finance)

Values of New Loans Approved During the Month by Sectors from 2007 Q1 to 2012 Q4

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

2007 2008 2009 2010 2011 2012

Valu

es o

f M

ort

gage

in H

K$ M

illi

on

Values for Refinancing

(HK$ million)

Values for Secondary

market (HK$ million)

Values for Primary

market (HK$ million)

Source: Hong Kong Monetary Authority , Residential

Mortgage Survey

Property Price and Banking Sector

• Mortgage loans and SMEs’ loans have assets as collaterals

• Banks can reduce risks of lending money as the net worth of collaterals increase (balance sheet improves)

• Potential borrowers can increase their borrowing ability by offering collaterals

• Improve information asymmetry

Percentage of Secured Advances in Advances to Customers by Industry Sectors (2012)

Bank* % of Secured Advances in Industrial, Commercial and Financial1

% of Secured Advances in Individuals Loans2

% of Secured Advances in Total Loans for Use in Hong Kong

The Bank of East Asia

72.25 83.12 75.80

Hang Seng Bank 67.1 82.2 74.0

Bank of China (Hong Kong)

50.29 91.69 69.91

HSBC 52.16 83.00 66.59

2 Including loans for the purchase of flats in the Home Ownership Scheme, Private Sector

Participation Scheme and Tenants Purchase Scheme, loans for the purchase of other

residential properties, credit card advances and others

1 Including Property Development, Property investment, Financial concerns,

Stockbrokers, Wholesale and retail trade, Manufacturing, Transport and transport

equipment, Recreational activities, Information technology and others

3 This includes loans for the purchase of flats in

Home Ownership Scheme, Private Sector

Participation Scheme and Tenants Purchase

Scheme, loans for purchase of other residential

properties.

Source: 2012 annual reports of The Bank of East Asia, Hang Seng Bank, Bank of China (Hong

Kong) and HSBC

Property Price

Net worth of assets increases

Improves balance sheets of banks and

firms

Encourages banks to increase

credit to the business sector

Property Price and Investment

Property Price and Inflation

Fluctuations in property

prices

Changes in consumption

and investment

Changes in aggregate demand

Prices of other goods may change

Channel 2

Channel 3 Changes in CPI today

Changes of inflationary

expectations today

Changes of wage and

rental contracts

Changes of future CPI

Channel 1 Fluctuations in property prices

Changes in housing cost

component of CPI

Changes in inflation rate

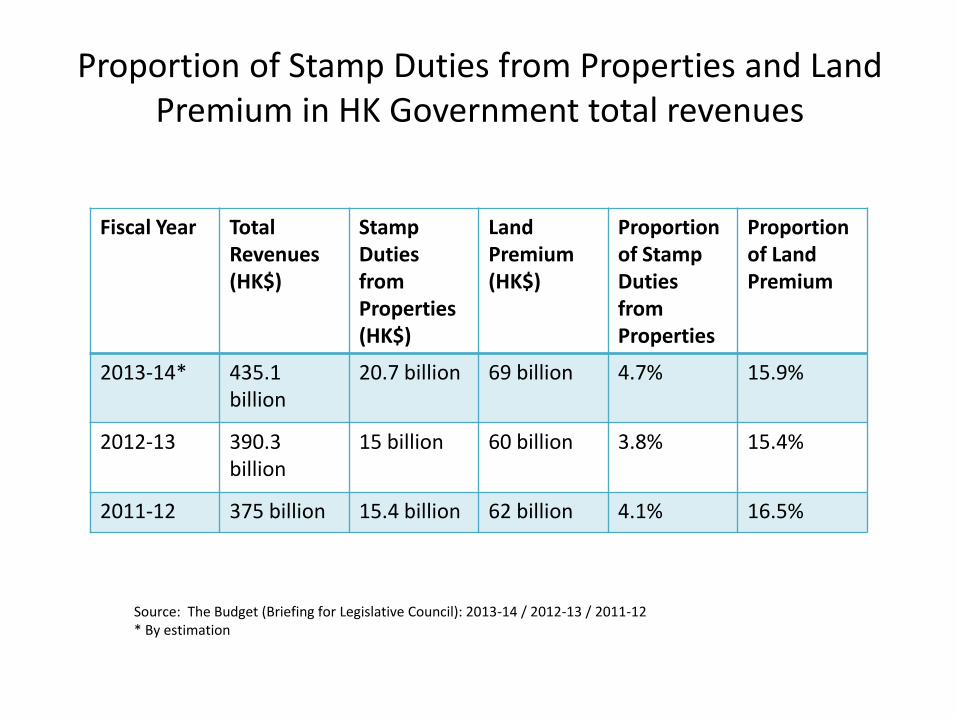

Property Price and Government Fiscal Position

• Land and other property-related income is an important income source of HK government

• Fluctuations of property price may have significant effect on its fiscal position

Proportion of Stamp Duties from Properties and Land Premium in HK Government total revenues

Fiscal Year Total Revenues (HK$)

Stamp Duties from Properties (HK$)

Land Premium (HK$)

Proportion of Stamp Duties from Properties

Proportion of Land Premium

2013-14* 435.1 billion

20.7 billion 69 billion 4.7% 15.9%

2012-13 390.3 billion

15 billion 60 billion 3.8% 15.4%

2011-12 375 billion 15.4 billion 62 billion 4.1% 16.5%

Source: The Budget (Briefing for Legislative Council): 2013-14 / 2012-13 / 2011-12 * By estimation

Real Estate Market and Economics

Microeconomics

Market Participants

Real Estate Market

Owners, owner-users,

speculators, renters Facilitators

Workers in

construction sector Developers

Market Cycles

• Time to Build

• Buildings are long-lasting and impossible to be relocated

• Implies inelastic supply in short run

• Changes of demand is faster than changes of supply

• Time lags of building would cause under-supply or over-supply in the market

Business Cycle and Real Estate Cycle

Expansion Recession

Demand

increases Price

increases

Supply

increases

Business cycle

Real estate cycle

Price

decreases

Time

Time lag due to construction

Heterogeneous Product • Each flat / housing estate is in a unique location

– Locates at north / south, 8th / 18th /28th floor…

• Property markets are segmented and localized

• Subject to surrounding environmental externalities

– Lohas Park (日出康城) locates at the region with a landfill^

^Source: http://www.singtao.com.hk/yesterday/loc/1026ao08.html

Picture credit: http://www.alsosprachanalyst.com/real-estate/hong-kong-real-

estate-chit-chat-with-real-estate-agent.html,

Highly Regulated by Governments

Regulations

Supply

Zoning or environmental

laws

Town Planning Ordinance

Building laws

The Building Ordinance

Consumer protection

The Residential Properties (First-

hand Sales) Ordinance

Demand

Stamp Duties

Ad Valorem Stamp Duty, Special Stamp

Duty, Buyer’s Stamp Duty

Comparison to Perfect Market

Perfect Market Real Estate Market

Number of buyers and sellers

Many participants Fewer participants, seller controls during a seller’s market* while buyer controls during a buyer’s market*

Product knowledge and ease of exchange

Buyers and sellers know well about the product; exchanges take place with ease

Buyers and sellers will not know well about the product; the exchange is legalistic, complex and expensive

Standardized products Products are homogeneous Each flat is unique and heterogeneous

Prices Buyers and sellers are price takers

The price of each flat is varied

Source: Essentials of Real Estate Economics (6th). DJ McKenzie, RM Betts and CA Jensen.

Demand and Supply Curves

Price or rent

Quantity or space

Pe

Demand

Short Run Supply

Long Run Supply

• Demographic factors

size of population, sex ratio, age structure, birth rate, marriage rate, life expectancy, …

Determinants of Demand

Population Pyramid of Hong Kong in Population Census 2011

Source: http://www.census2011.gov.hk/flash/dashboards/population-pyramid-db-102-

en/population-pyramid-db-102-en.html

Some Figures About HK Population

Number of Single Parents* in 1996, 2001, 2006, 2011

1996 2001 2006 2011

Number 42,316 61,341 76,423 81,705

Source: HK Census and Statistics Department, Women and Men in HK Key Statistics 2012

*Single parents: This refers to persons who are never married, widowed,

divorced or separated, and living with child(ren) aged under 18 in the same

household

Determinants of Demand

• Income

• When income increases, the demand for housing increases, vice versa.

• Income inequality and quality of housing

– HK example: Subdivided units vs. private residential units

Picture credit: http://the-sun.on.cc/cnt/news/20110617/00407_020.html , Wikipedia

Determinants of Demand

• Financing

– Availability of credit (Loan-to-value ratio)

– Interest rate (Prime rate)

HK Examples:

– When Hong Kong Monetary Authority reduced the loan-to-value ratio in February 2013^, the demand for housing decreased.

– When prime rate increases, demand for housing decreases, vice versa.

^ Source: http://www.hkma.gov.hk/media/eng/doc/key-information/guidelines-and-circular/2013/20130222e2.pdf

Determinants of Demand

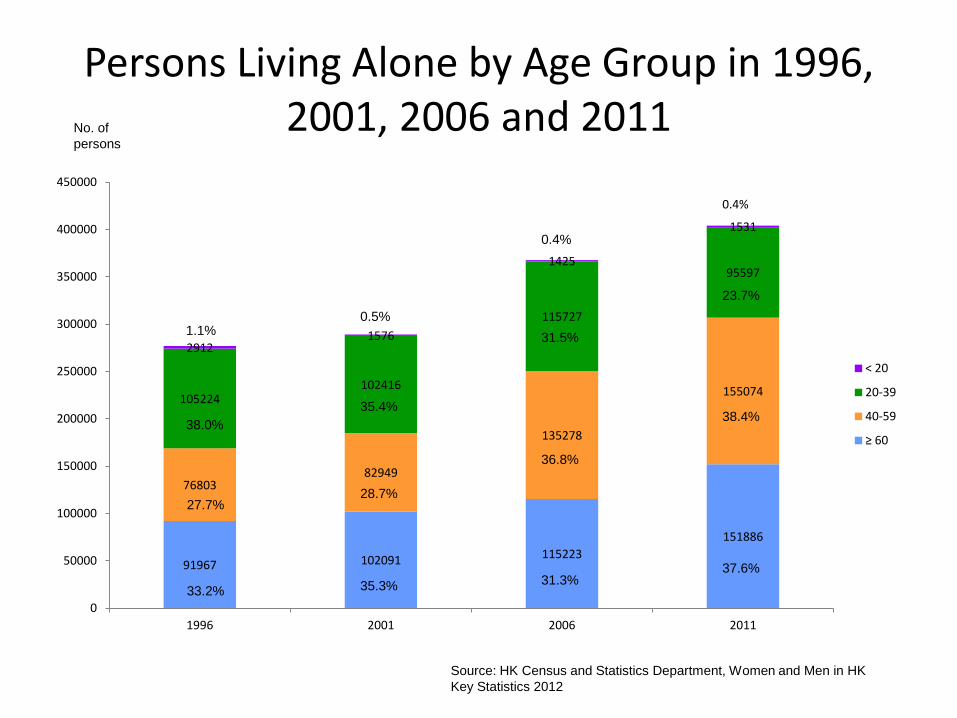

• Changes in preferences

HK example:

– More people prefer to live by their own. This will increase the demand for houses.

Persons Living Alone by Age Group in 1996, 2001, 2006 and 2011

91967 102091 115223

151886

76803 82949

135278

155074 105224

102416

115727

95597

2912 1576

1425

1531

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

1996 2001 2006 2011

< 20

20-39

40-59

≥ 60

1.1%

35.3%

28.7%

35.4%

0.5%

31.3%

36.8%

31.5%

0.4%

37.6%

38.4%

23.7%

0.4%

33.2%

27.7%

38.0%

Source: HK Census and Statistics Department, Women and Men in HK

Key Statistics 2012

No. of

persons

Determinants of Supply

• Availability and costs of factors of production

• Factors of production

– Capital, land, labour, raw materials…

• Technology of building

Determinants of Supply

• Government legislations or regulations

• Policy Risk

Determinants of Supply

• Inelastic supply in short run

– Price is largely determined by demand

• New supplies follow this price, R as initial price

• More elastic supply in long run

– Value, V as discounting cash flows of rents will be compared to construction costs C

Rent

Stock of housing

D R

SH Value

Housing starts,

Hs

V

C

Policy History

Early History of Public Housing

1950s

•Large Influx of refugees

•Poor hill side shelter

Turning point

• On 25 December 1953, a major fire destroyed the Shek Kip Mei squatter areas.

1950-60

•Emergence public shelters

•Provisional Resettlement units

Objectives of public housing policy

50s-60s

•Emergency Housing

•Basic Living environment

•PRH by HK housing Authority

70s and 80s

•Permanent Housing

•Quality Housing

•Ten years housing proramme: New towns, HOS, Private Sector Participation Scheme (PSPS)

•Promotion of Home ownership

1997-2000

•Target of 85,000 flats per year (50,000 public flats)

•Asian Financial Crisis

• Increasing role of the private market

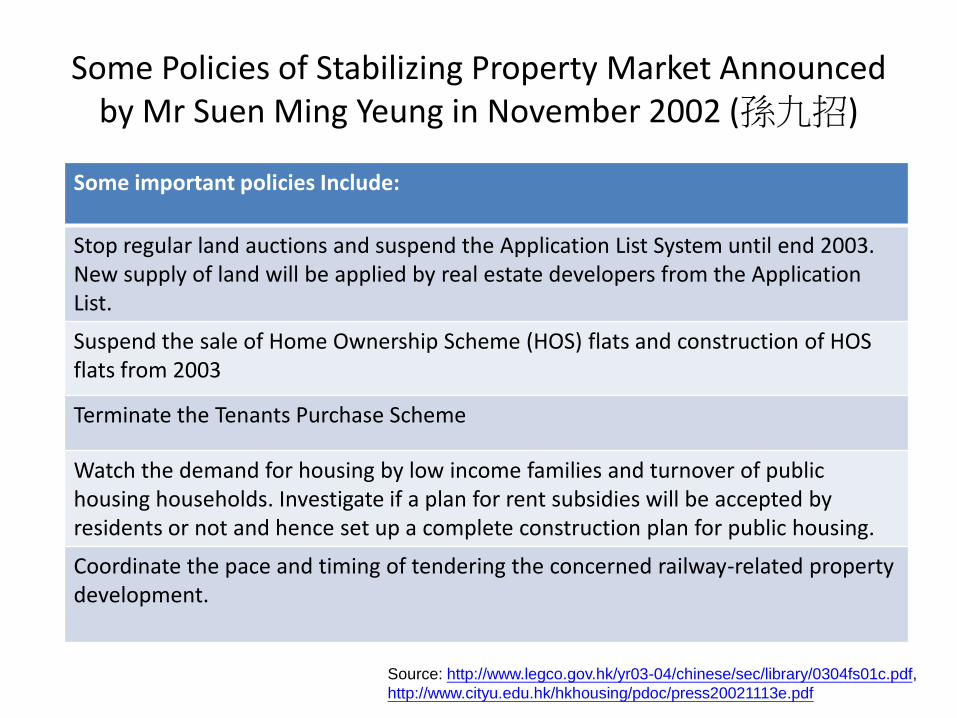

Some Policies of Stabilizing Property Market Announced by Mr Suen Ming Yeung in November 2002 (孫九招)

Some important policies Include:

Stop regular land auctions and suspend the Application List System until end 2003. New supply of land will be applied by real estate developers from the Application List.

Suspend the sale of Home Ownership Scheme (HOS) flats and construction of HOS flats from 2003

Terminate the Tenants Purchase Scheme

Watch the demand for housing by low income families and turnover of public housing households. Investigate if a plan for rent subsidies will be accepted by residents or not and hence set up a complete construction plan for public housing.

Coordinate the pace and timing of tendering the concerned railway-related property development.

Source: http://www.legco.gov.hk/yr03-04/chinese/sec/library/0304fs01c.pdf,

http://www.cityu.edu.hk/hkhousing/pdoc/press20021113e.pdf

Date Ad Valorem Stamp Duty

Special Stamp Duty Buyer’s Stamp Duty

1 April 2010 Increased from the old rates

20 November 2010 – 26 October 2012

Started to levy (Stage 1)

27 October 2012 Adjusted to Stage 2 Started to levy

23 February 2013 Announced for a further adjustment

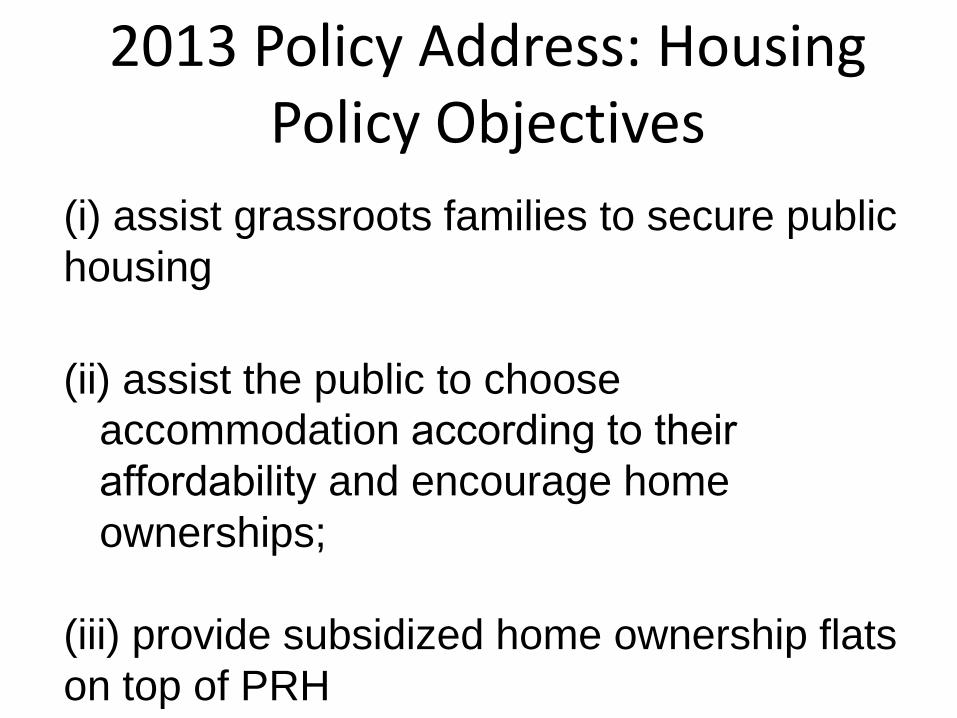

2013 Policy Address: Housing Policy Objectives

(i) assist grassroots families to secure public

housing

(ii) assist the public to choose

accommodation according to their

affordability and encourage home

ownerships;

(iii) provide subsidized home ownership flats

on top of PRH

Data

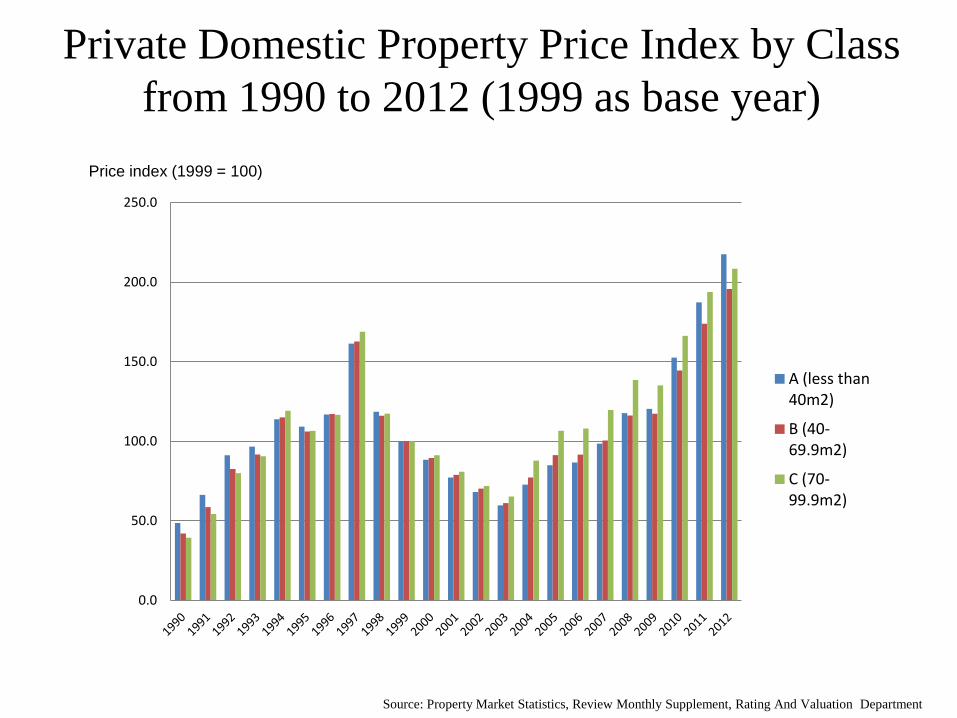

Private Domestic Property Price Index by Class

from 1990 to 2012 (1999 as base year)

0.0

50.0

100.0

150.0

200.0

250.0

A (less than 40m2)

B (40-69.9m2)

C (70-99.9m2)

Source: Property Market Statistics, Review Monthly Supplement, Rating And Valuation Department

Price index (1999 = 100)

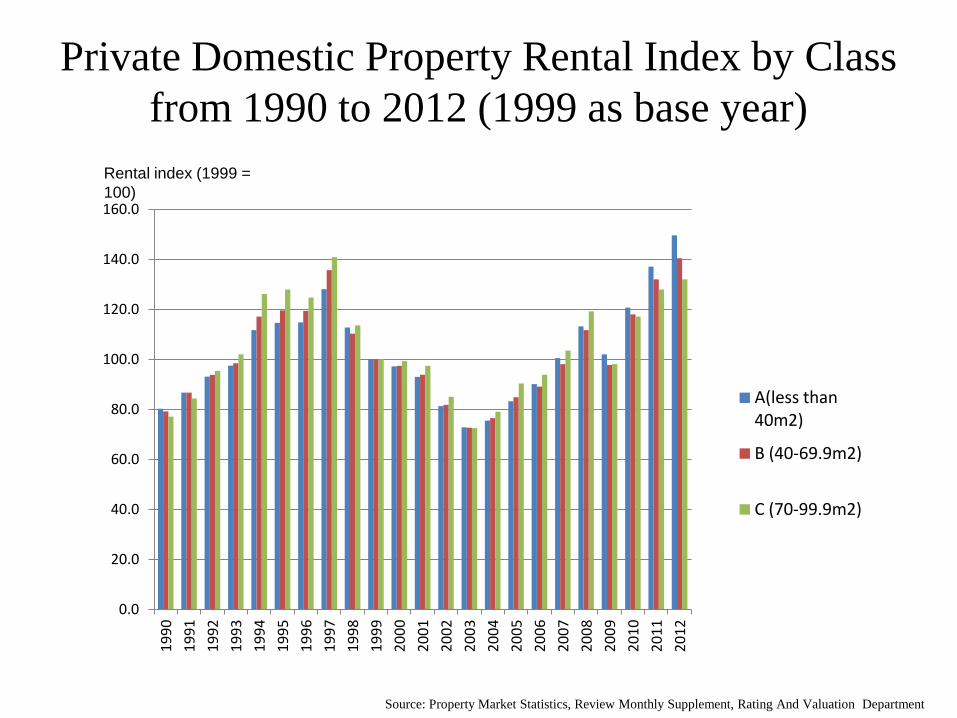

Private Domestic Property Rental Index by Class

from 1990 to 2012 (1999 as base year)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

A(less than 40m2)

B (40-69.9m2)

C (70-99.9m2)

Rental index (1999 =

100)

Source: Property Market Statistics, Review Monthly Supplement, Rating And Valuation Department

Private Domestic Property Rental Index by Class

and CPI (A) from 2003 to 2012 (1999 as base year)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

A(less than 40m2)

B (40-69.9m2)

C (70-99.9m2)

CPI (A) (1999=100)

Rental index (1999 =

100)

Source: HK Census and Statistics Department, Property Market Statistics, Review Monthly Supplement, Rating And

Valuation Department

Private Domestic Property Stock by Class

from 1985 to 2012

Source: Property market statistics, Review Monthly supplement, Rating and Valuation Department

(‘000)

0

100

200

300

400

500

600

700

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Type A (Less than 40 m2)

Type B (40 m2 to 69.9m2)

Type C (70 m2 to 99.9 m2)

*The figures from

2003-2012 have been

adjusted as the original

figures of this period

of time exclude village

houses in the source.

Index of Private Domestic Property Stock by

Class from 2003 to 2012 (2003 as base year)

Source: Property market statistics, Review Monthly supplement, Rating and Valuation Department

2003 = 100

90

95

100

105

110

115

120

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Type A (Less than 40 m2)

Type B (40 m2 to 69.9 m2)

Type C (70 m2 to 99.9 m2)

*The figures from 2003-

2012 have been adjusted

as the original figures of

this period of time

exclude village houses in

the source.

Cumulative Number of Home Ownership Scheme Flats

from 1980 to 2002

(Use year of completion as standard)

0

50000

100000

150000

200000

250000

300000

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Source: http://www.housingauthority.gov.hk/tc/common/pdf/home-ownership/surplus-hos-flats/list-of-hos-courts/hos_flats-b5-250811.pdf

No. of

flats

Source: http://www.housingauthority.gov.hk/tc/common/pdf/home-ownership/surplus-hos-flats/list-of-hos-courts/hos_flats-b5-

250811.pdf

Total Number of Completion of Home Ownership

Scheme Flats from 1980 to 2002

(Use year of completion as standard)

0

5000

10000

15000

20000

25000

30000

35000

40000

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

No. of

flats

Stock of Public Rental Flats

in 2002, 2007 and 2012

640

660

680

700

720

740

760

780

2002 2007 2012

(‘000)

Source: Hong Kong Housing

Authority

Actual Public Rental Housing Production

from 2002/03 to 2011/12

0

5000

10000

15000

20000

25000

30000

2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12

Source: Hong Kong Housing Authority

No. of

flats

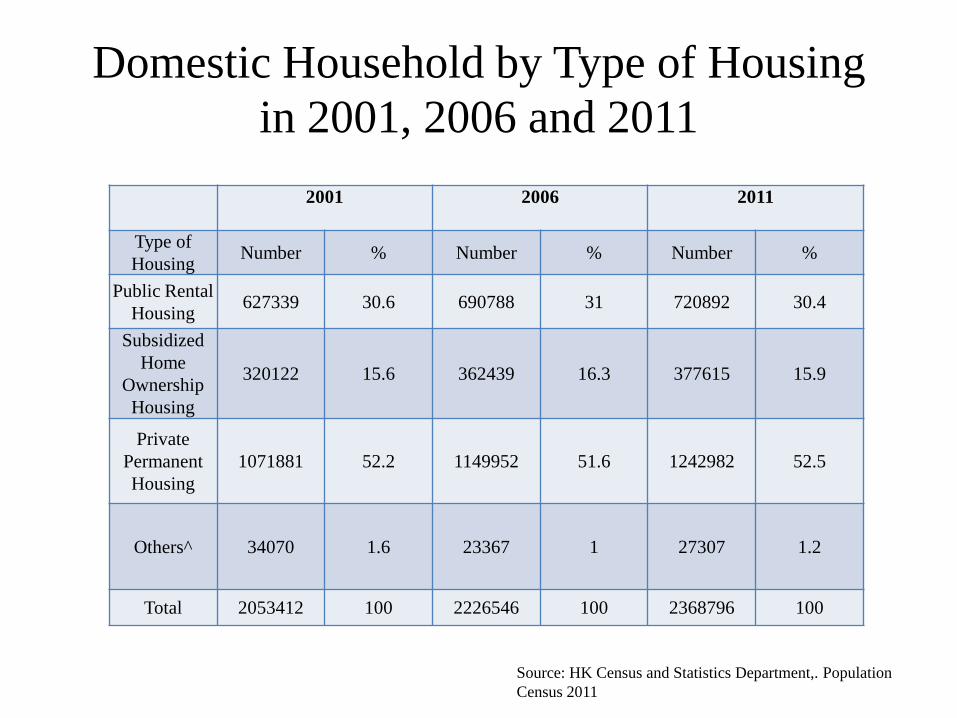

Domestic Household by Type of Housing

in 2001, 2006 and 2011

2001

2006

2011

Type of

Housing Number % Number % Number %

Public Rental

Housing 627339 30.6 690788 31 720892 30.4

Subsidized

Home

Ownership

Housing

320122 15.6 362439 16.3 377615 15.9

Private

Permanent

Housing

1071881 52.2 1149952 51.6 1242982 52.5

Others^ 34070 1.6 23367 1 27307 1.2

Total 2053412 100 2226546 100 2368796 100

Source: HK Census and Statistics Department,. Population

Census 2011

Distribution of Domestic Households by Tenure of

Accommodation (2011)

Source: HK Census and Statistics Department, Population

Census 2011 Table E102 and E103

30.40%

15.90% 36.20%

16.30%

1.20%

Public Rental Housing

Home Ownership Scheme Flats

Pirvate Permanent Housing (Owner-occupiers)

Private Permanent Housing (Renting)

Others

*The calculations of Private Permanent Housing (Owner-occupiers) and

Private Permanent Housing (Renting) are based on an assumption and the

data from HK Census and Statistics Department.

Median Monthly Domestic Household Rent and

Median Rent To Income Ratios By Type Of

Quarters in 2001,2006 and 2011

Median Monthly Domestic

Household Rent (HK$)

Median Household Income

(HK$)

Median Rent to Income

Ratio(%)

Type of

quarters /

Year

2001 2006 2011 2001 2006 2011 2001 2006 2011

Public

Rental

Housing

Units

1300 1390 1210 12500 10296 11415 10.4 13.5 10.6

Private

Permanent

Housing

5300 5100 7500 19413 20238 29182 27.3 25.2 25.7

Source: HK Census and Statistics Department,. Population

Census 2011

Economic Model

54

Objectives Consider a hypothetical situation to study: a) The market of flats i) For sale ii) For rent in the public and private sectors. b) Effects of increase in supply of land for flats development Tool: Linear supply and demand model

55

A flat for accommodation and/or for investment

The value of a flat is made up of :

a) The value of housing services yielded

b) The rate of monetary return of the flat (i.e. rents) as an investment asset

The willingness to pay to buy and willingness to accept to sell depend on the perceived value of the flat.

56

Key Assumption An individual user, who needs a flat, demands only ONE unit of flat.

57

Overview of Housing Market Analysis

Residual Demand

Private

Primary

Market

Residual Demand

Private Secondary

Market

Unmet Demand

Private Rental Market

Residual Demand

Public HOS

Market

Residual Demand

Public PHR

Market

Unmet

Demand

Private Rental Market

Means Tests

Total 2000

demanders for

private flats at zero

price

Among them,

1000 eligible

applicants for

HOS flats at

zero price (600

eligible PRH

applicants)

+

58

Private Primary Flats Market

Quantity demand at zero price = 2000

Demand:

Buyers are willing to pay a first hand flat at different prices

Supply:

Fixed quantity

Quantity Traded:

200 buyers of first hand flats

Quantity of flats

Supply of first hand flats

from developers

Demand

for first

hand flats

Price per flat (in million dollars)

200 2000 0

4.5

Residual demand

59

Private Secondary Flats Market

Quantity demanded at zero price = 2000-200 = 1800

Demand:

Buyers are willing to pay a second hand flat at different prices.

Supply:

Suppliers are willing to accept to sell their flats at different prices

Quantity Traded:

200 buyers of second hand flats.

Quantity of flats

Supply of second hand private flats

Demand for

private

second

hand flats

Price per flat (in million dollars)

200 1800 0

4

2

Residual demand

60

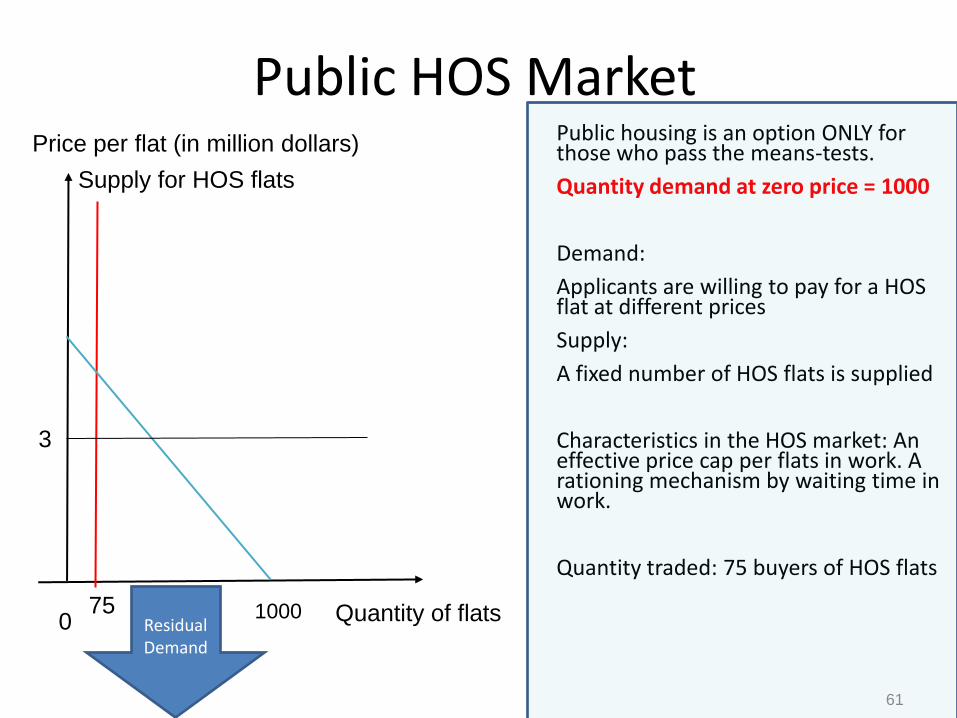

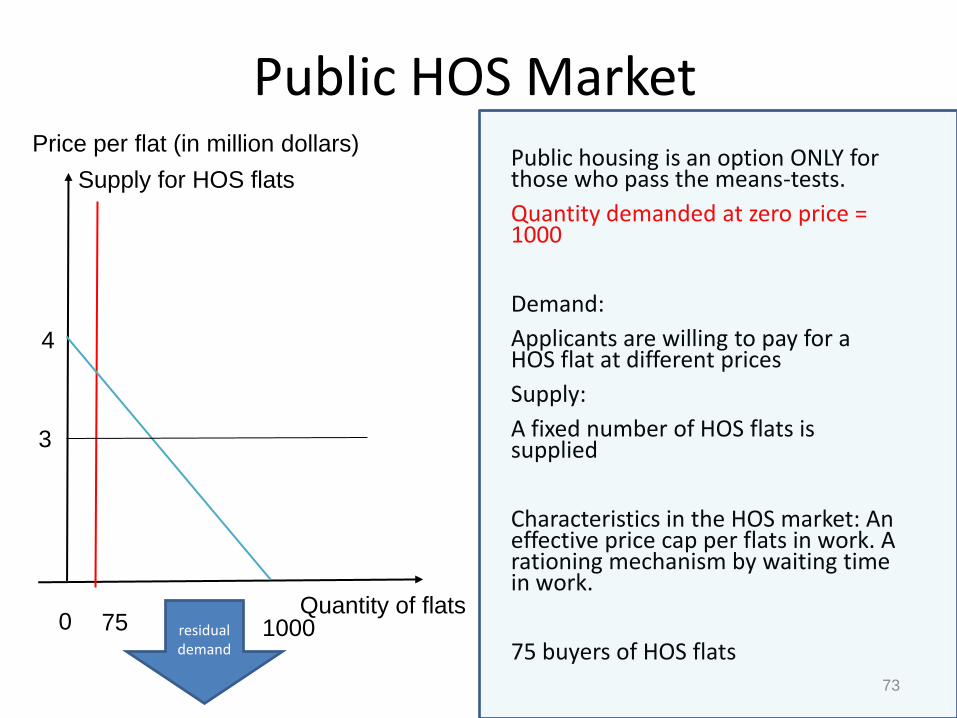

Public HOS Market Public housing is an option ONLY for those who pass the means-tests.

Quantity demand at zero price = 1000

Demand:

Applicants are willing to pay for a HOS flat at different prices

Supply:

A fixed number of HOS flats is supplied

Characteristics in the HOS market: An effective price cap per flats in work. A rationing mechanism by waiting time in work.

Quantity traded: 75 buyers of HOS flats

Supply for HOS flats

3

Quantity of flats

Price per flat (in million dollars)

75 1000 0 Residual Demand

61

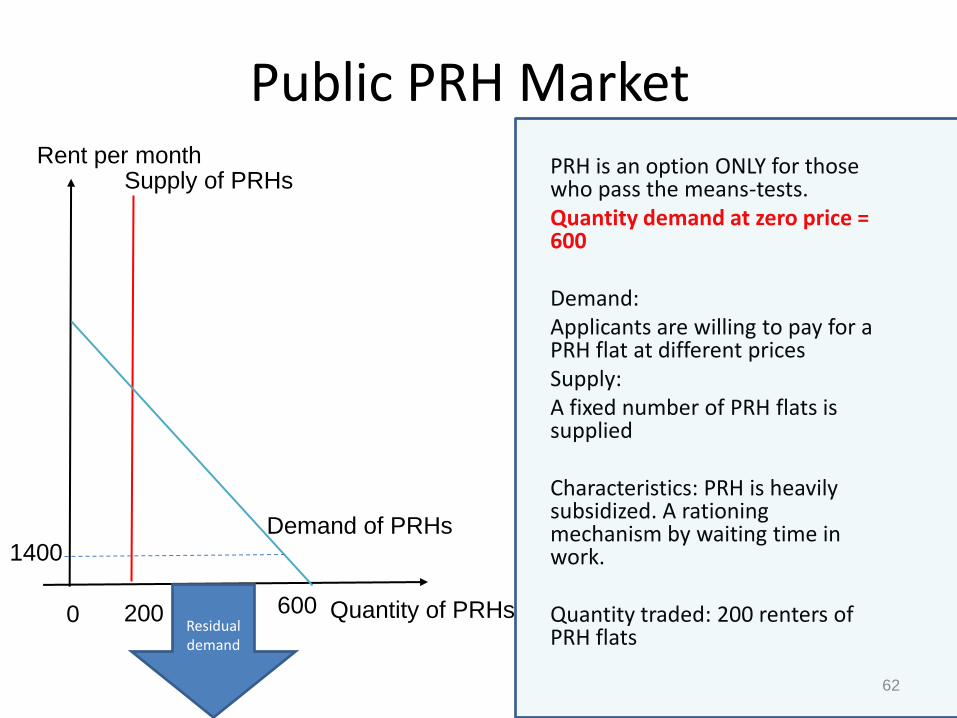

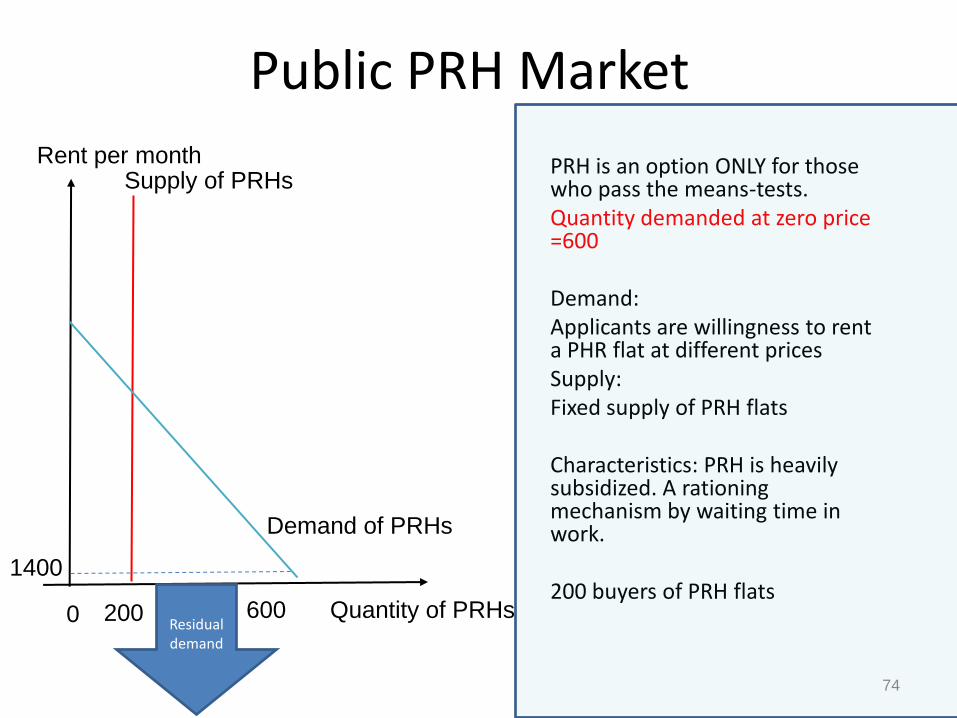

Public PRH Market PRH is an option ONLY for those who pass the means-tests. Quantity demand at zero price = 600 Demand: Applicants are willing to pay for a PRH flat at different prices Supply: A fixed number of PRH flats is supplied Characteristics: PRH is heavily subsidized. A rationing mechanism by waiting time in work. Quantity traded: 200 renters of PRH flats

Supply of PRHs

1400

Quantity of PRHs

Rent per month

Demand of PRHs

200 600 0 Residual demand

62

Private Rental Flats Market

Demand: a) Mix of potential renters of flats = people who

cannot afford the down payment + people who can afford down payment but fail to buy private flats

b) The rents per year at which renters are willing to pay are different.

Supply: Flat owners ask for different levels of rent to lease their flats. 63

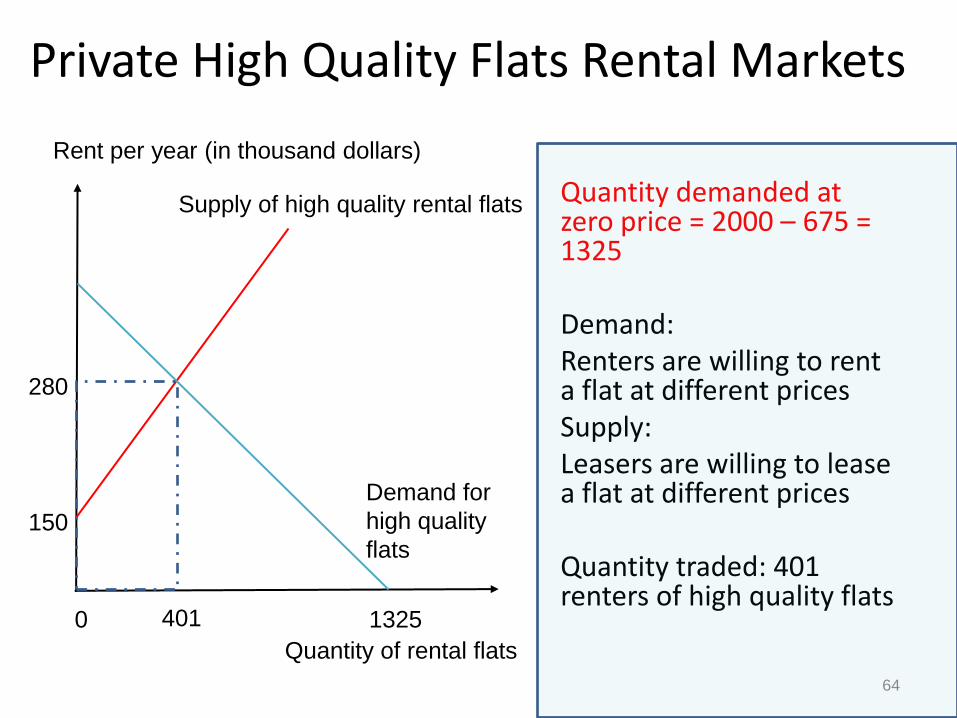

Private High Quality Flats Rental Markets

Supply of high quality rental flats

Demand for

high quality

flats

Quantity of rental flats

Rent per year (in thousand dollars)

401 1325 0

280

150

Quantity demanded at zero price = 2000 – 675 = 1325 Demand: Renters are willing to rent a flat at different prices Supply: Leasers are willing to lease a flat at different prices Quantity traded: 401 renters of high quality flats

64

Private Middle Quality Flats Rental Markets

Supply of middle quality rental flats

Demand for

middle

quality flats

Rent per year (in thousand dollars)

350 924 0

180

Quantity of rental flats

Unmet demand: some left unsatisfied, some

search for low quality rental options

100

Quantity demanded at zero price = 1325-401 = 924 Demand: Renters are willing to rent a flat at different prices Supply: Leasers are willing to lease a flat at different prices Quantity traded: 350 renters of middle quality flats 65

Private Subdivided Units Rental Market

Quantity demanded at price zero = 924-350=574 The rise of the subdivided units in the flats in the private market is to house the residual demanders in other market: a) who cannot find anything

in both the normal private selling and rental market, and

b) who are not yet housed by the public market.

Quantity traded: 170 renters of subdivided units

Supply of subdivided units

3000

Quantity of

subdivided

units

Rent per month

Demand of subdivided units

170 574 0

1000

Unmet demand becomes homeless, or stay

where they live currently 66

Summary

• The private market will not fully cover the need of housing demand.

• There will be excess demand in the subsidized public flats market.

• Private rental market provides tiers of rental flats to meet the demand, including subdivided rental units.

67

Policy Analysis and Evaluation

68

Increasing Land Supply in Private Market

69

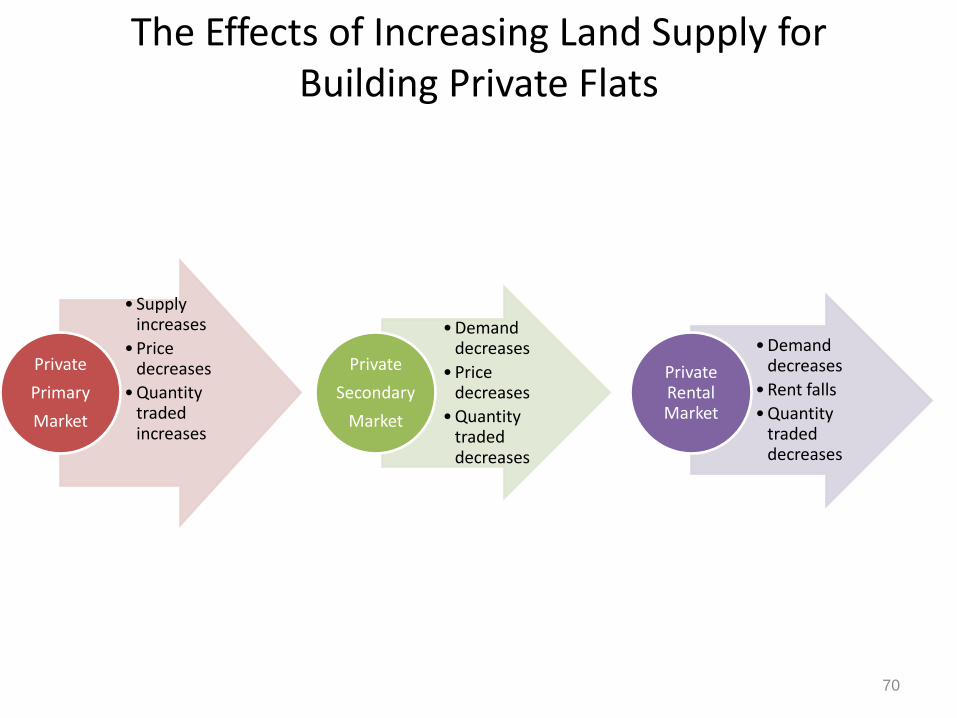

The Effects of Increasing Land Supply for Building Private Flats

• Supply increases

• Price decreases

• Quantity traded increases

Private

Primary

Market

• Demand decreases

• Price decreases

• Quantity traded decreases

Private

Secondary

Market

• Demand decreases

• Rent falls

• Quantity traded decreases

Private Rental Market

70

Private Primary Flats Market

Quantity of flats

Supply of first hand flats

from developers

Demand

for first

hand flats

Price per flat (in million dollars)

200 2000 0

4.5

Residual Demand

5

400

4

2000 potential buyers of first hand flats

Supply increases

Demand unchanged

Price decreases

Quantity traded decreases

400 buyers of first hand flats

71

Private Secondary Flats Market

Quantity demanded at zero price = 1600 = 2000 - 400

Supply unchanged

Demand decreases

Price decreases

Quantity traded decreases

180 buyers of second hand flats

Quantity of flats

Supply of second hand private flats

Demand

for private

second

hand flats

Price per flat (in million dollars)

180 1800 0

4

Residual Demand

2

1600

72

Public HOS Market Public housing is an option ONLY for those who pass the means-tests.

Quantity demanded at zero price = 1000

Demand:

Applicants are willing to pay for a HOS flat at different prices

Supply:

A fixed number of HOS flats is supplied

Characteristics in the HOS market: An effective price cap per flats in work. A rationing mechanism by waiting time in work.

75 buyers of HOS flats

Supply for HOS flats

3

Quantity of flats

Price per flat (in million dollars)

75 1000 0 residual demand

4

73

Public PRH Market

PRH is an option ONLY for those who pass the means-tests. Quantity demanded at zero price =600 Demand: Applicants are willingness to rent a PHR flat at different prices Supply: Fixed supply of PRH flats Characteristics: PRH is heavily subsidized. A rationing mechanism by waiting time in work. 200 buyers of PRH flats

Supply of PRHs

1400

Quantity of PRHs

Rent per month

Demand of PRHs

200 600 0 Residual demand

74

Supply of rental flats of higher quality

Demand for

private high

quality flats

Quantity of rental flats

Rent per year (in thousand dollars)

370 1325 0

280

244

401 1145

150

Quantity demanded at zero price = 2000 – 855 = 1145 Demand decreases Supply unchanged Price decreases Quantity traded decreases 370 renters of high quality flats

Residual Demand

Private High Quality Rental Flats Markets

75

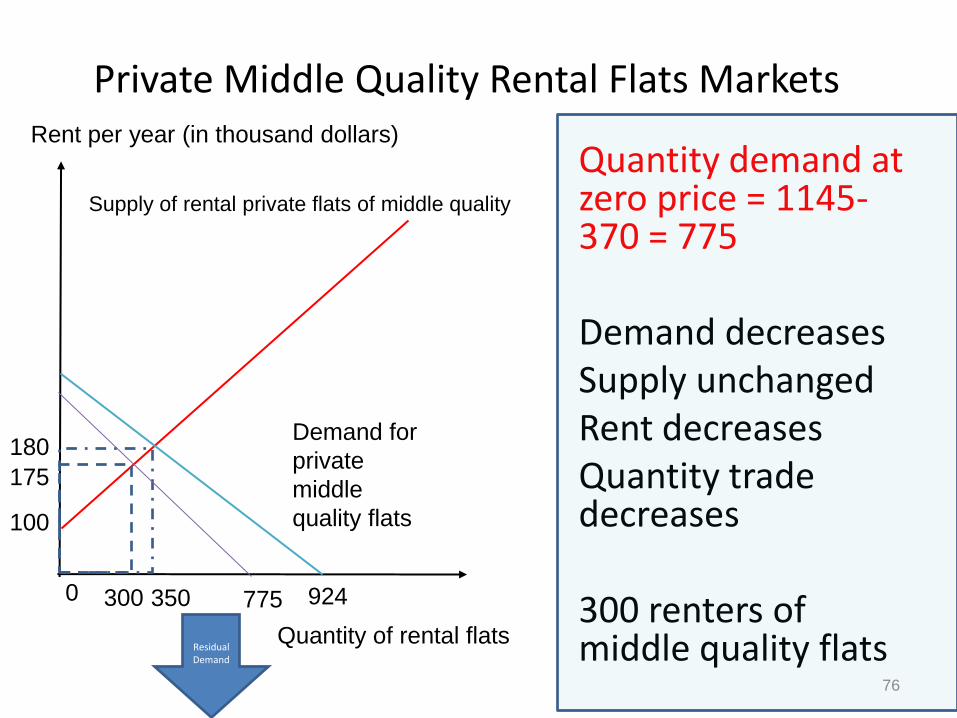

Supply of rental private flats of middle quality

Demand for

private

middle

quality flats

Rent per year (in thousand dollars)

350 924 0

180

Quantity of rental flats

775

100

300

175

Quantity demand at zero price = 1145-370 = 775 Demand decreases Supply unchanged Rent decreases Quantity trade decreases 300 renters of middle quality flats

Private Middle Quality Rental Flats Markets

Residual Demand

76

Private Subdivided Units Rental Market

Supply of subdivided units

3000

Quantity of

subdivided

units

Rent per month

Demand of subdivided

units

170 574 0

1000

475

2210

Unmet Demand

Quantity demanded at zero price = 775-300 = 475 Demand Decreases Supply Unchanged Rent decreases Quantity traded decreases 150 renters of subdivided units

150

77

Policy Evaluation

Will increase land supply for private flats improve the living conditions for the grass root households? Suggested Answer: • It depends on the room it creates in the rental

market for renters to move upstream from the lowest tier market. Yet, the unmet demand in the lowest tier quality market still exists.

• The people who cannot move upstream may be due to low income and/or deposit constrained.

78

Increasing Land Supply in Public Market

79

The Effects of Land Increase for Building Public Flats

• Supply increases

• Quantity traded increases

Public HOS

Market

•Supply increases

•Quantity traded increases

Public PRH

Market

•Decease the demand for subdivided units

•Rent falls

•Quantity traded decreases

Private Rental Market

80

HOS flats and Subdivided Units Rental Market

Supply for HOS flats

3

Quantity of flats

Price per flat (in million dollars)

75 1000 0

4

250

induces

Supply of rental private flats of middle quality

Demand for

private

middle

quality flats

Rent per year (in thousand dollars)

350 924 0

180

Quantity of rental flats

100

175

Residual Demand

81

PRH flats and Subdivided Units Rental Market

Supply of PRHs

1400

Quantity of

PRHs

Rent per month

Demand of PRHs

200 600 0 400

Supply of subdivided units

3000

Quantity of

subdivided

units

Rent per month

Demand of

subdivided units

170 574 0

1000

Unmet Demand

induce

(Freed up by Green Form applicants)

82

a) The rate of monetary return of the flat (i.e. rents) may be reduced.

b) The private market is affected, not immediately, but in a long run the value of first and second hand flats for sell will fall to approach an important theoretical equilibrium condition:

Fundamental value of private flats = Today annual rent + Present value of the future expected annual rents

83

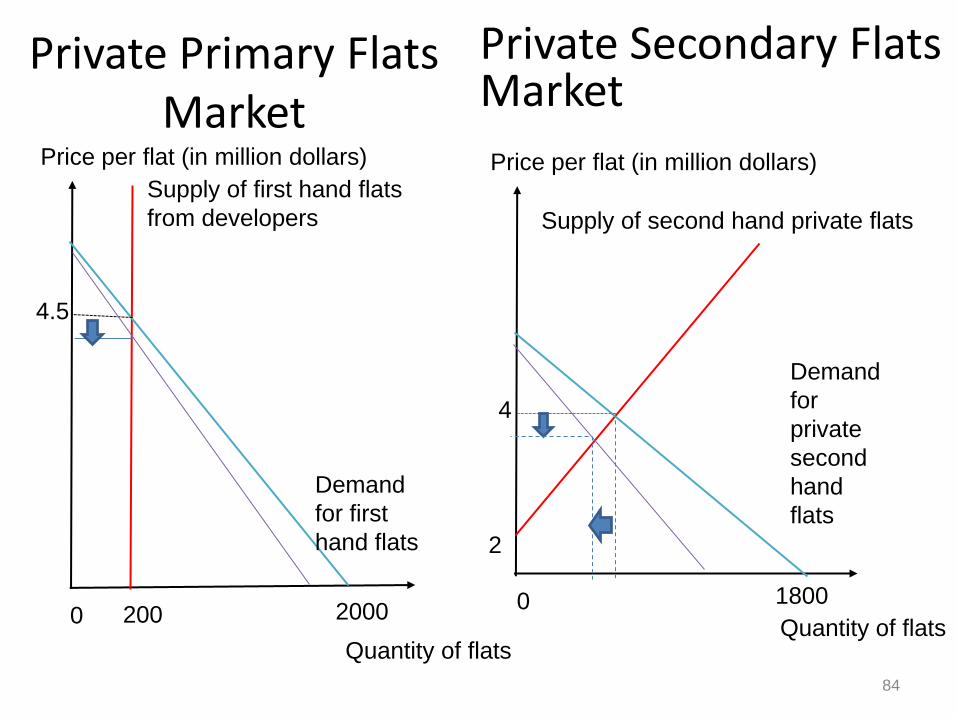

Private Primary Flats Market

Quantity of flats

Supply of first hand flats

from developers

Demand

for first

hand flats

Price per flat (in million dollars)

200 2000 0

4.5

Private Secondary Flats Market

Quantity of flats

Supply of second hand private flats

Demand

for

private

second

hand

flats

Price per flat (in million dollars)

1800 0

4

2

84

Effects of Land Supply Policy

Increase land supply policies in either the private and public sectors:

a) Lower price and rent of flats

b) May reduce quantity of flats rented

c) May reduce the number of homelessness, people living in caged homes and young people with housing needs.

85

Policy Evaluation

Will increase land for PRH improve the living conditions for the grass root households?

Suggestive answer: Yes, it can improve the applicant’s living condition by moving them in the newly developed PRH flats. By paying a subsidized rent, their quality of life will also be improved.

In addition, the living costs of the grass root households may be reduced as these households may pay lower rents for the lowest tier housing (i.e. the subdivided units).

86

Policy Evaluation

Will increase land for HOS improve the living conditions for the grass root households? Suggestive answer: Yes, an increase in HOS can increase the number of the people who are currently living in PRH to move upstream in the accommodation ladder, and thereby free up PRH resources to accommodate the applicants in line, and thus improve the grass root household’s living condition. Again, the living costs of the grass root households may be reduced as they may pay lower rents for the lowest tier housing (i.e. the subdivided units).

87

Policy Evaluation

Which one is a better policy if a policy objective is to raise the living conditions of the grass root households?

Suggestive answer: Increasing the land supply for HOS has an effect to create an upstream accommodation ladder, but increase the land supply for PRH does not. Both policies will improve the living conditions of some grass root households by moving them into the PRH flats. However, the former policy is more dynamic and has the potential to improve the living conditions of those who are currently living in PRHs but wish to own a HOS flat, and thereby freeing up resources.

88