1

SEPA direct debit scheme - chances and risks for recurring payments

2

Agenda

Chances: 1.Reach 2.Costs 3.Customer Lifetime 4.Merchant managed

Risks: 1. Risk Scoring 2. CRM

3

Chances of SEPA direct debit

4

SEPA is an EU initiative aiming for: • Harmonization of money transfers in Europe • Boost money transfers beyond borders • Advance a secure and cost-efficient payment

system • Independent of creditk card networks

4000 banks, 300M+ bank accounts available since August 2014

Further improved SEPA scheme COR1 will launch in 11/2016

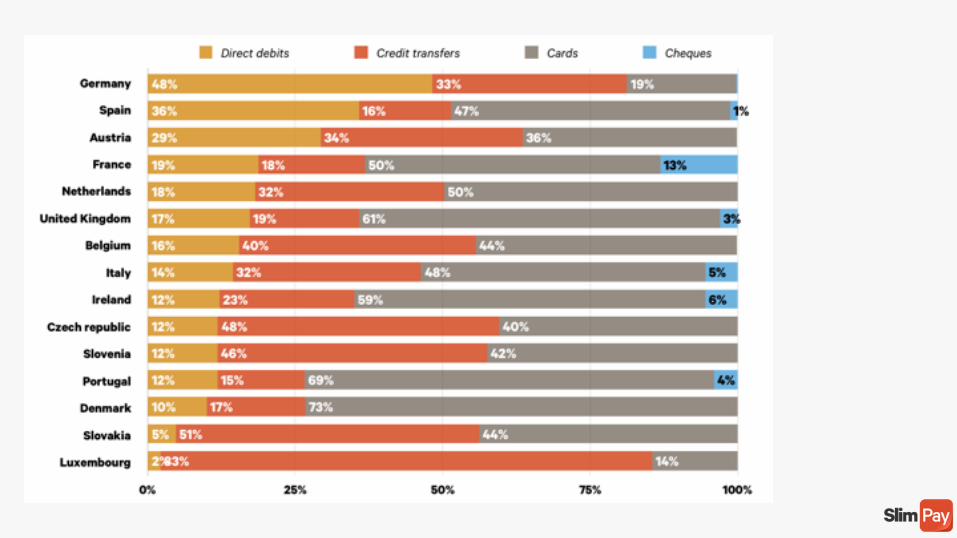

With SEPA, merchants can reach 500M users across 34 countries

6

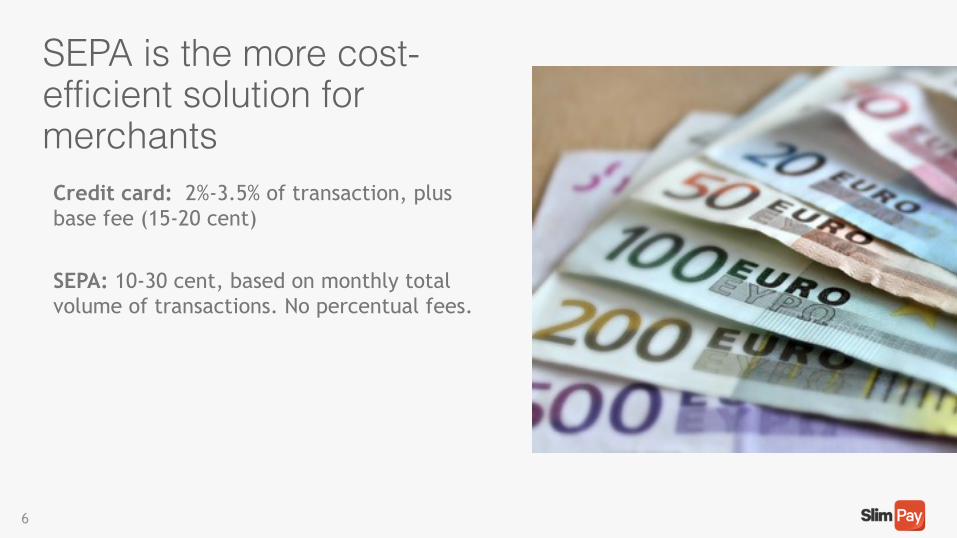

Credit card: 2%-3.5% of transaction, plus base fee (15-20 cent)

SEPA: 10-30 cent, based on monthly total volume of transactions. No percentual fees.

SEPA is the more cost-efficient solution for merchants

Case study- Deezer

Music-Streaming service Deezer leverages SlimPay for processing their monthly service fee of EUR 9,99 – Costs

per transaction compared to credit cards were a main driver for this

decision.

7

8

Credit card: • Expiration date • Account Updater often not possible to use

in Europe • High churn rates

SEPA direct debit: • No expiration of banking details • Low churn rates, consumers do not

frequently switch bank accounts

Better customer lifetime with due to low churn rates

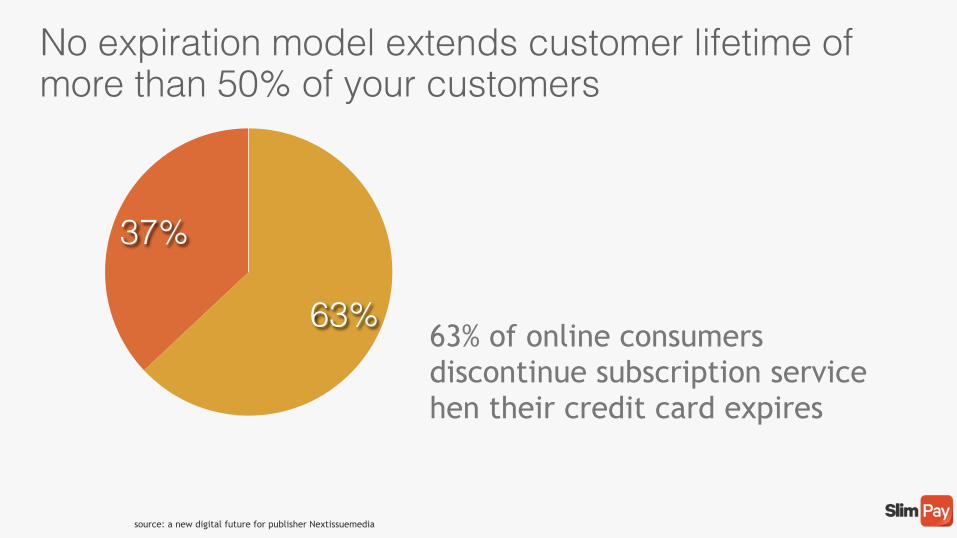

37%

63%63% of online consumers discontinue subscription service hen their credit card expires

source: a new digital future for publisher Nextissuemedia

No expiration model extends customer lifetime of more than 50% of your customers

•This is a titleCase study- SFR

After integrating Slimpay, mobile service provider SFR lowers annual churn rates to

3.6% (for direct debit)

11

• Full automation possible • Consumer shares IBAN once and confirms

electronic mandate (supported tokenization)

• „oneclick“ payment possible for all following transactions

• Invoicing, advance payment, PayPal, SOFORT: requires customer action • Risk: delay of payment, cancellation

or collections

Merchant stays in control with automatic processing in the background

Case study- Nespresso

Coffee re-orders are processed automatically via

SlimPay Direct Debit

12

•This is a title

13

Case study- Greenpeace

1 out of 2 recurring donations in France is processed via Slimpay direct debit.

3X lower churn rate with direct debit compared to credit card donations

14 Boost your customer lifetime value!

Case study- BIP &GO Maut and road tolls

Fully automated booking of EUR600k per 24h

Case study (B2B) - TripAdvisor

15

Online sign up for marketing program – automated payment process with company bank account

16

Risks – what to watch out for

17

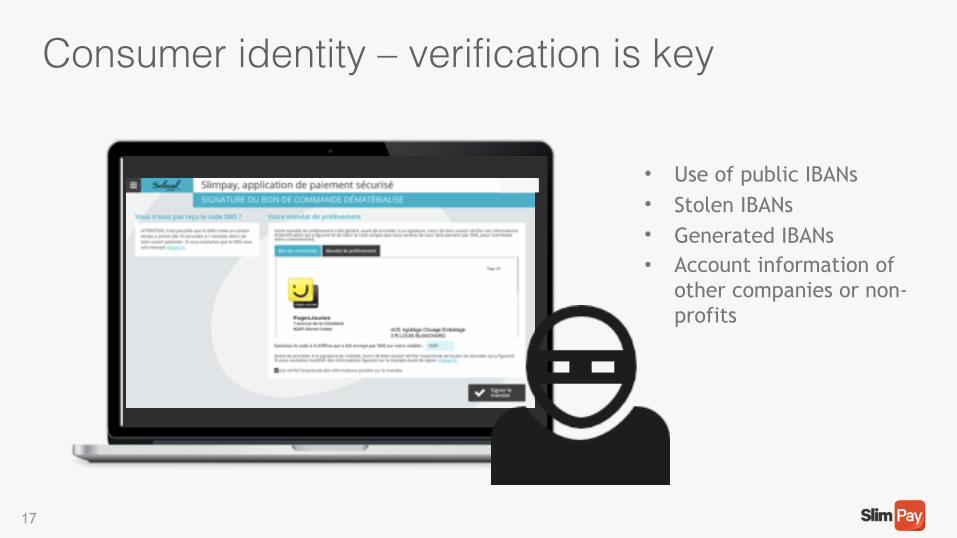

Consumer identity – verification is key

• Use of public IBANs • Stolen IBANs • Generated IBANs • Account information of

other companies or non-profits

18

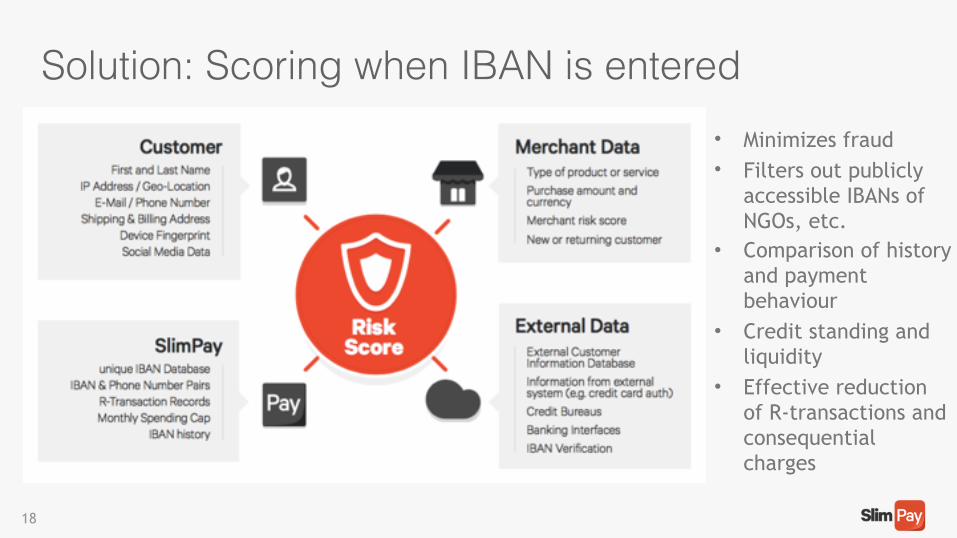

Solution: Scoring when IBAN is entered• Minimizes fraud • Filters out publicly

accessible IBANs of NGOs, etc.

• Comparison of history and payment behaviour

• Credit standing and liquidity

• Effective reduction of R-transactions and consequential charges

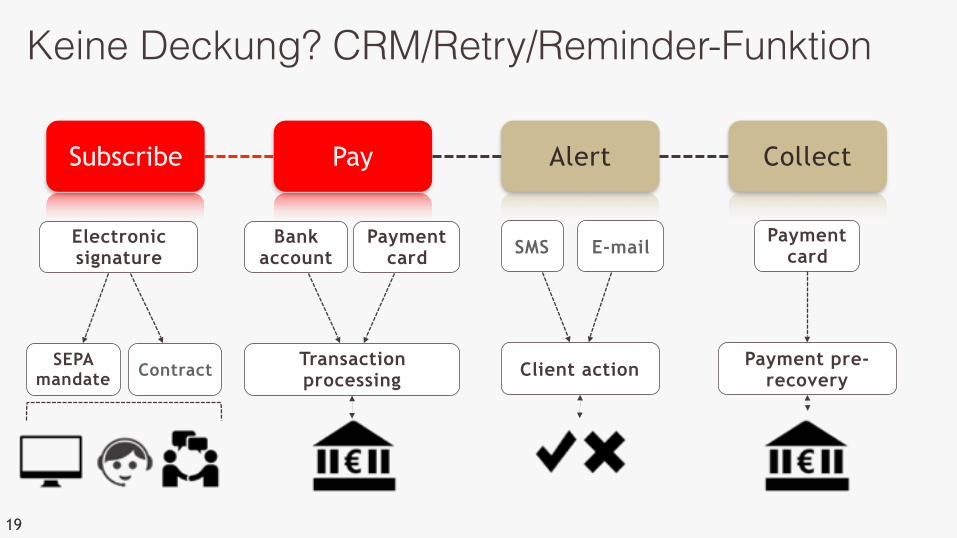

Keine Deckung? CRM/Retry/Reminder-Funktion

Subscribe Pay Alert Collect

SEPA mandate Contract Transaction

processing

Electronic signature

Payment card

Bank account

Payment pre-recovery

Payment card

Client action

E-mailSMS

19

•This is a titleCase study- Bein Sports

2 out of 3 customers prefer Slimpay direct debit over credit cards.

Slimpay leverages scoring, Reminder texts and retry logics for

unsuccessful payments

21

Key Takeaways – SEPA direct debit offers unique benefits

• Broad reach across 34 countries and 500M consumers • Low costs due to competitive pricing model • Higher customer lifetime with lower churn rates • Holistic integration with scoring and CRM functionality is key to avoid

fraud and to avoid deficit in payments