Designing Global Payroll and Benefit Programs

Fatima Laher and Maria Tsatas Deloitte LLP Randy Hahn

Guberman Garson Segal LLP

Agenda

Evolving Payroll and Immigration landscape

The “Payroll Gap” Analysis: Adding Value / Pursuing Compliance

Changing demographics: Heightened sensitivity to Audit risk

Disruption : Technology embedded in mobility programs

Policy trends in global mobility

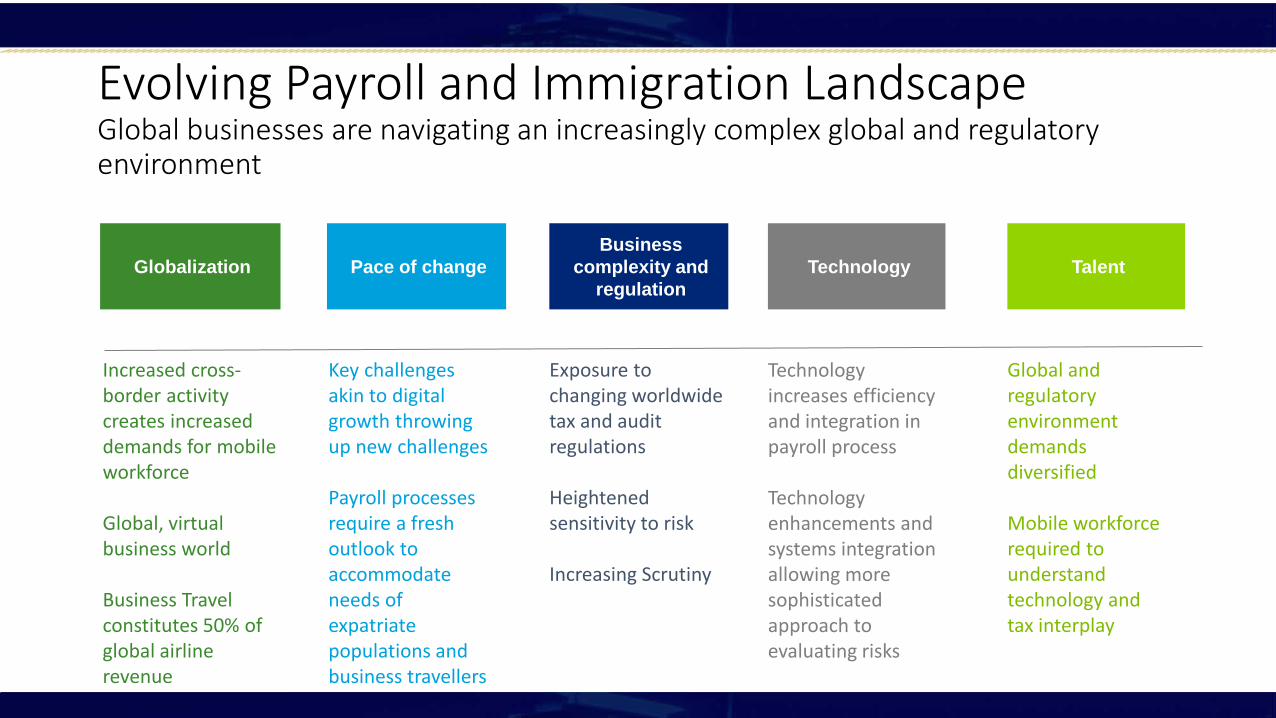

Evolving Payroll and Immigration Landscape

Evolving Payroll and Immigration Landscape Global businesses are navigating an increasingly complex global and regulatory environment

Increased cross-border activity creates increased demands for mobile workforce Global, virtual business world Business Travel constitutes 50% of global airline revenue

Exposure to changing worldwide tax and audit regulations Heightened sensitivity to risk Increasing Scrutiny

Technology increases efficiency and integration in payroll process Technology enhancements and systems integration allowing more sophisticated approach to evaluating risks

Global and regulatory environment demands diversified Mobile workforce required to understand technology and tax interplay

Globalization Business

complexity and regulation

Technology Talent Pace of change

Key challenges akin to digital growth throwing up new challenges Payroll processes require a fresh outlook to accommodate needs of expatriate populations and business travellers

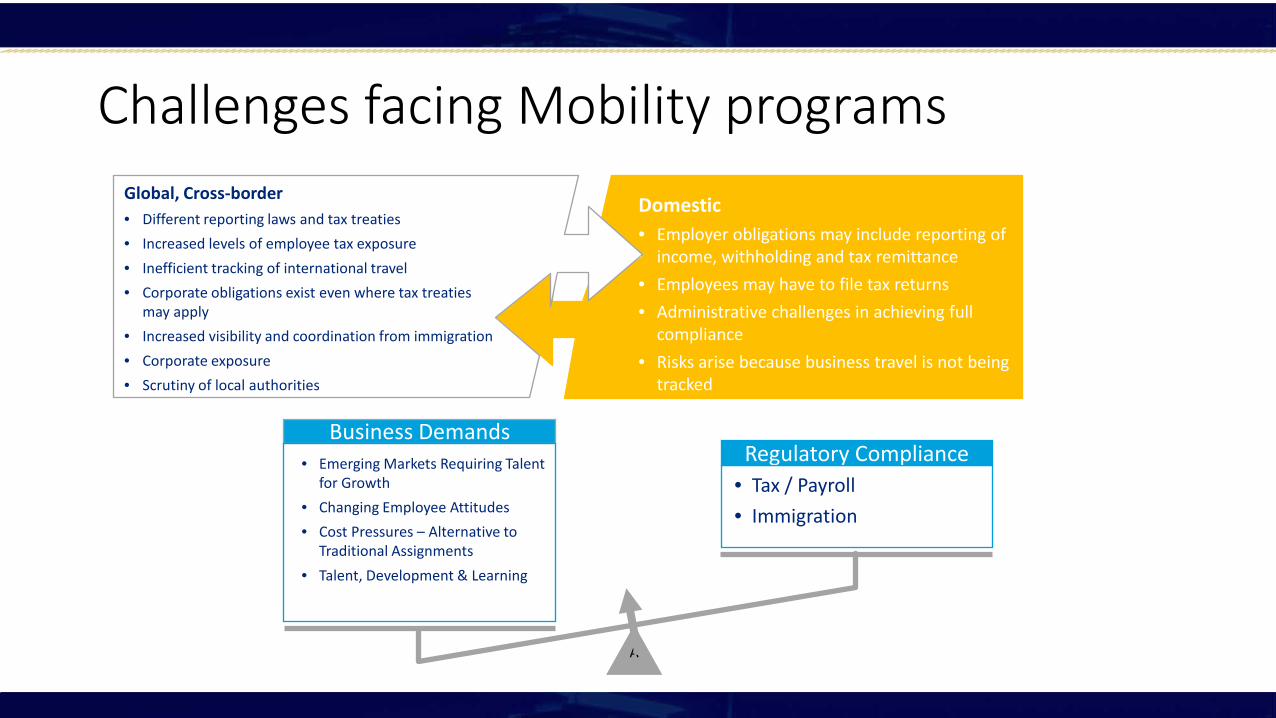

Challenges facing Mobility programs

A

Business Demands • Emerging Markets Requiring Talent

for Growth • Changing Employee Attitudes • Cost Pressures – Alternative to

Traditional Assignments • Talent, Development & Learning

Regulatory Compliance • Tax / Payroll • Immigration

Global, Cross-border • Different reporting laws and tax treaties • Increased levels of employee tax exposure • Inefficient tracking of international travel • Corporate obligations exist even where tax treaties

may apply • Increased visibility and coordination from immigration • Corporate exposure • Scrutiny of local authorities

Domestic • Employer obligations may include reporting of

income, withholding and tax remittance • Employees may have to file tax returns • Administrative challenges in achieving full

compliance • Risks arise because business travel is not being

tracked

The “Payroll Gap” Analysis: Adding Value / Pursuing Compliance

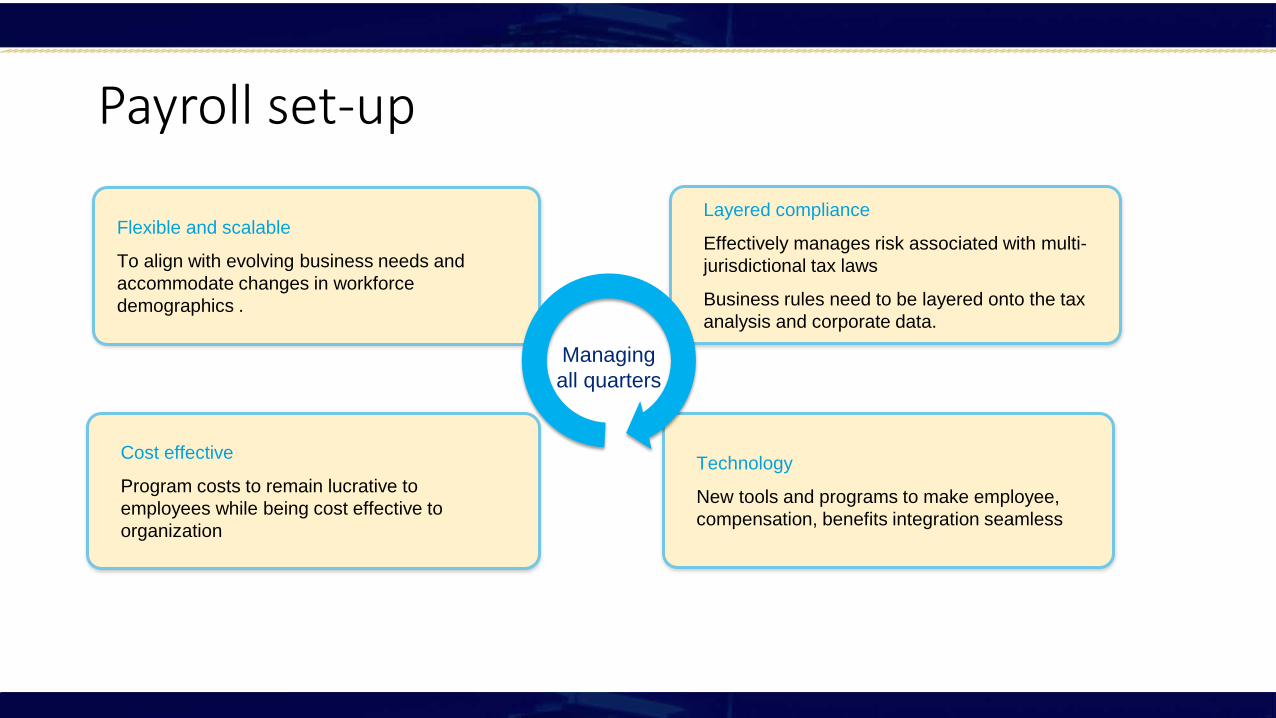

Payroll set-up

Flexible and scalable

To align with evolving business needs and accommodate changes in workforce demographics .

Cost effective

Program costs to remain lucrative to employees while being cost effective to organization

Layered compliance

Effectively manages risk associated with multi-jurisdictional tax laws

Business rules need to be layered onto the tax analysis and corporate data.

Technology

New tools and programs to make employee, compensation, benefits integration seamless

Managing all quarters

Payroll obligations

• Payroll legislative requirements are generally complex, in Canada as well as many other countries

• Complexity is augmented for employers with global operations • Achieving payroll compliance is a constant source of frustration for

many global organizations especially in connection with various categories of employees including international assignees and frequent business travellers (‘’FBTs’’) and in dealing with global compensation structures giving rise to different tax treatment, depending on country of assignment.

Payroll complexities

• Determining employer payroll obligations in jurisdiction of employment, employee’s residency and origin of payment

• Inadequate processes to identify and compile complete compensation subject to employer payroll requirements

• Determining taxability of various elements of remuneration, which can differ between home and host

• Particularities of equity and deferred compensation • Lack of expertise in local payroll teams to deal with payroll in cross

border situations

“Payroll Gap” analysis

• Eliminates efficiencies and conserves resources • Identifies red flags for potential non-compliance with income tax

rules • Prevents leakage

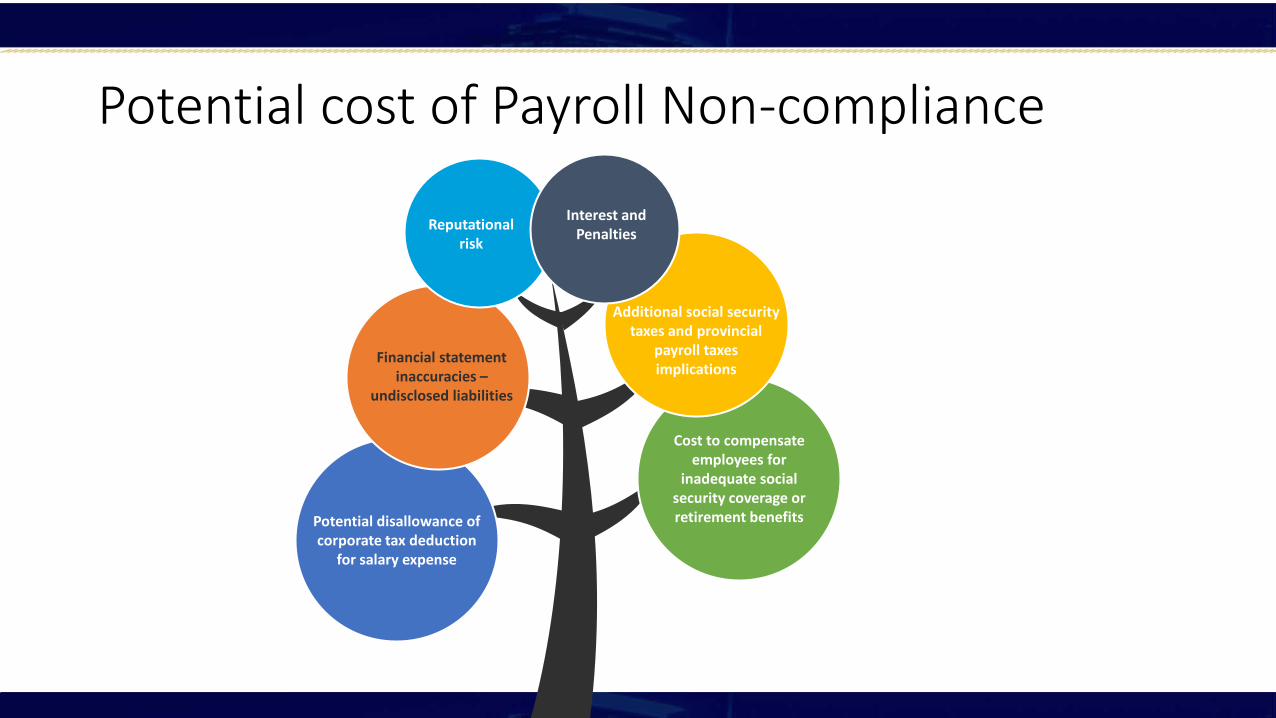

Potential cost of Payroll Non-compliance

Financial statement inaccuracies –

undisclosed liabilities

Potential disallowance of corporate tax deduction

for salary expense

Additional social security taxes and provincial

payroll taxes implications

Cost to compensate employees for

inadequate social security coverage or retirement benefits

Reputational risk

Interest and Penalties

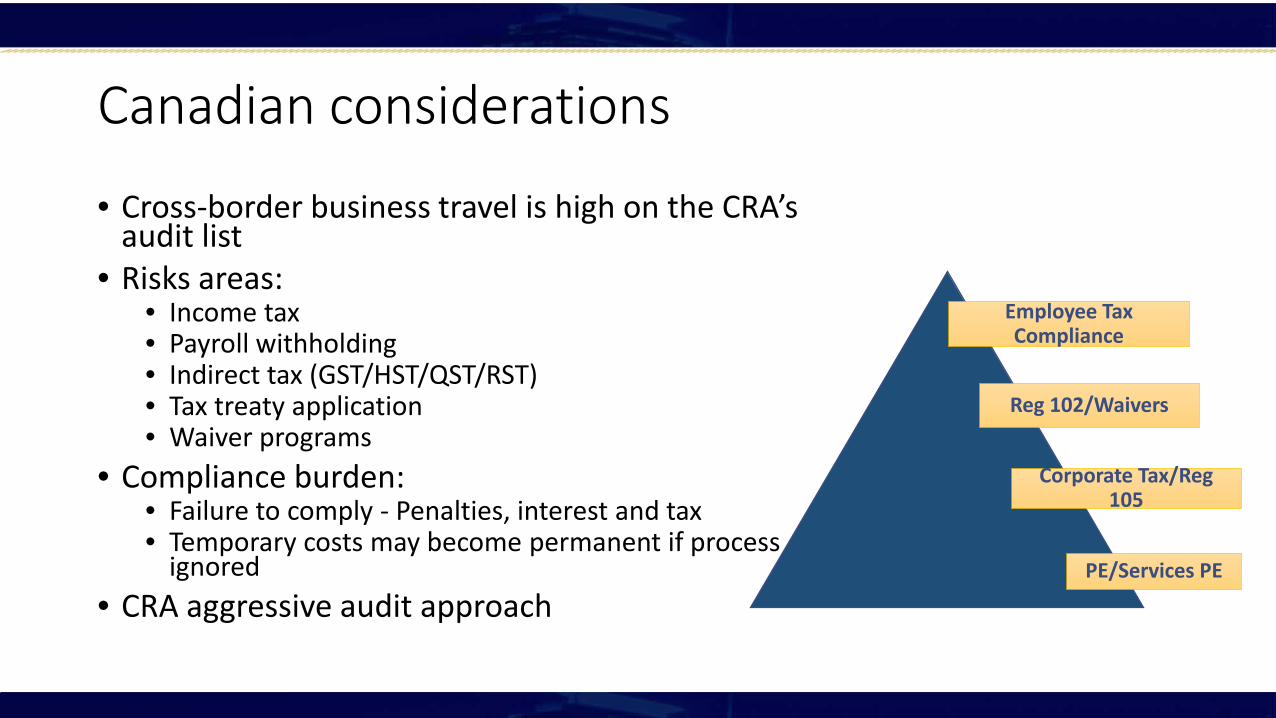

Canadian considerations

• Cross-border business travel is high on the CRA’s audit list

• Risks areas: • Income tax • Payroll withholding • Indirect tax (GST/HST/QST/RST) • Tax treaty application • Waiver programs

• Compliance burden: • Failure to comply - Penalties, interest and tax • Temporary costs may become permanent if process

ignored • CRA aggressive audit approach

Employee Tax Compliance

Reg 102/Waivers

Corporate Tax/Reg 105

PE/Services PE

Witholding Obligations – Canadian perspective • Every person paying remuneration to employees working in Canada must withhold

Canadian income tax at source in respect of their employees’ Canadian source compensation − Withholding obligation applies to non-resident employers − Withholding obligation applies even if the employee is ultimately exempt from

Canadian taxation under the Treaty − Only exception is where a waiver is obtained authorizing no withholding

• Must also report Canadian source compensation and tax withholdings at source on annual information returns (T4 slip and T4 summary)

• Requires the non-resident employer to register and open up a payroll account with CRA

• New relief measures proposed in Budget 2015

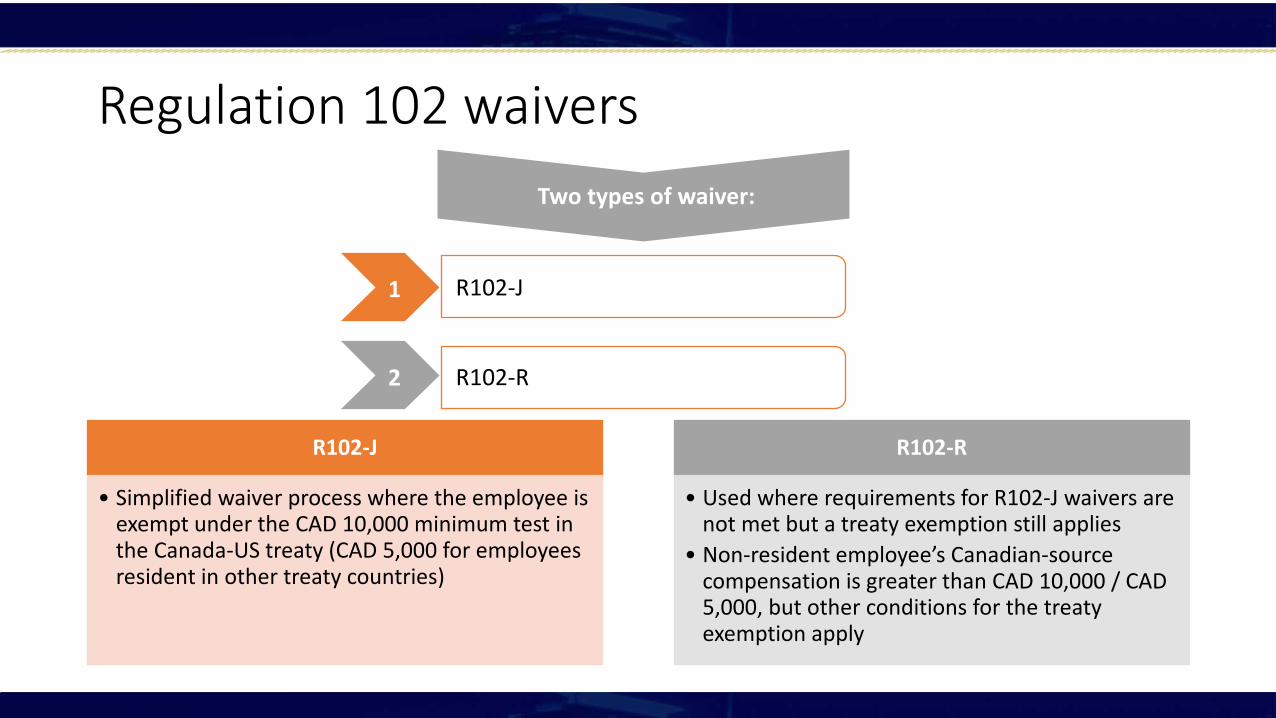

Regulation 102 waivers

R102-J

• Simplified waiver process where the employee is exempt under the CAD 10,000 minimum test in the Canada-US treaty (CAD 5,000 for employees resident in other treaty countries)

R102-R

• Used where requirements for R102-J waivers are not met but a treaty exemption still applies

• Non-resident employee’s Canadian-source compensation is greater than CAD 10,000 / CAD 5,000, but other conditions for the treaty exemption apply

R102-J

R102-R 2

1

Two types of waiver:

The challenges …

• Business travel is actively being pursued by CRA • The Canadian rules are onerous and not intuitive, and are often perceived as

having a negative impact on investment in Canada • Essentially the ultimate taxability of income in Canada does not go hand- in-hand

with the tax withholding requirements, whereby tax withholding is due from Day 1 in Canada (both with respect to corporate to corporate payments and payments to employees)

• To be compliant, broadly the options are: • Withhold tax on Canadian sourced income and reclaim this through a tax return; or • Apply to CRA for a waiver to relax the withholding (but not the reporting) requirements; or

• Certification process effective January1, 2016 for all eligible employers • No withholding and reporting obligations for all Qualifying non resident employees under

$10K and under 45 work days in a calendar year/ 90 physical days in any 12 month period • CRA administrative process expected to be rolled out in October 2015

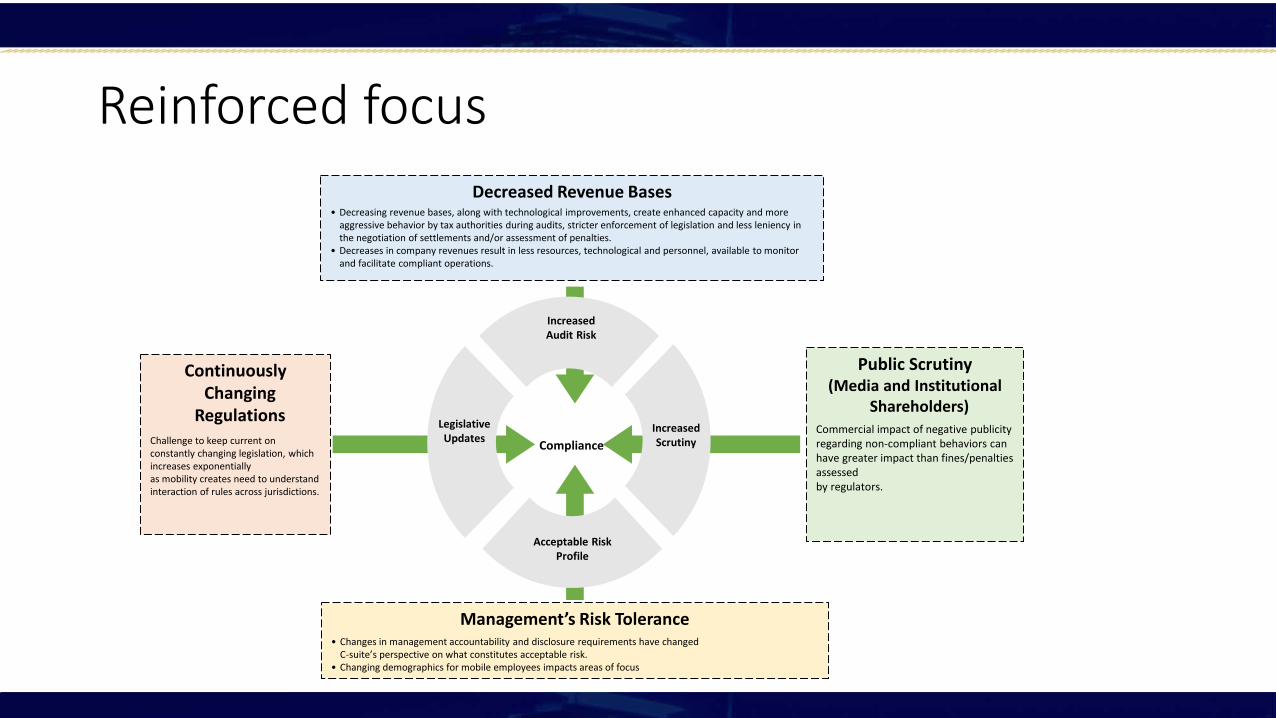

Changing demographics: Heightened sensitivity to Audit risk

Reinforced focus

Public Scrutiny (Media and Institutional

Shareholders) Commercial impact of negative publicity regarding non-compliant behaviors can have greater impact than fines/penalties assessed by regulators.

Decreased Revenue Bases

• Decreasing revenue bases, along with technological improvements, create enhanced capacity and more aggressive behavior by tax authorities during audits, stricter enforcement of legislation and less leniency in the negotiation of settlements and/or assessment of penalties.

• Decreases in company revenues result in less resources, technological and personnel, available to monitor and facilitate compliant operations.

Increased Scrutiny

Acceptable Risk Profile

Increased Audit Risk

Legislative Updates

Compliance

Continuously Changing

Regulations Challenge to keep current on constantly changing legislation, which increases exponentially as mobility creates need to understand interaction of rules across jurisdictions.

Management’s Risk Tolerance • Changes in management accountability and disclosure requirements have changed

C-suite’s perspective on what constitutes acceptable risk. • Changing demographics for mobile employees impacts areas of focus

Canada • Project Permanent Establishment

Concept information sharing between tax and immigration authorities

• Tax withholding reconciliation initiative • T106/Reg 105 exposure

Korea • $3,000 limit on U.S.

treaty dependent services article

Australia • Business travelers coming to Australia

from non-treaty countries, must now apply for a Tax File number visa the Australian Taxation office and then file the Australian tax return

Exposure: No matter where you are

China • Enforcement of immigration

laws with detention or imprisonment

South Africa • An individual is required to file a tax

return if his/her remuneration subject o tax in South Africa exceeds R120,000 or if no PAYE has been withheld

United States • Data sharing between tax and

immigration authorities increasing • Increase in IRS and State Revenue

audits • Regulatory changes at State level to

capture ax revenue (e.g. NY and MN)

United Kingdom • Short Term Business Visitor program to

facilitate tax compliance – recently confirmed as only option to avoid withholding tax at source

• Immigration – new work permit system with significant consequences for non-compliance; employee bans possible for between 1 and 10 years

Germany • Application of Economic

Employer concept

Singapore & Hong Kong • Laws introduced to tax equity

income for those leaving the country

Disruption : Technology embedded in mobility programs

Tax and Technology

• Technology has paved way in redefining global mobility programs • Tax is now integral function of companies’ analytics quest • Tax Analytics helps professionals make informed decisions • End to end automation / monitoring is feasible of payroll process • Data analytics tools allows tax department to see if embedded tax

rules working as intended. • Data extract can be used in data analytics tool against client specific

tax determination logic to identify data errors, tax over/underpayment, etc.

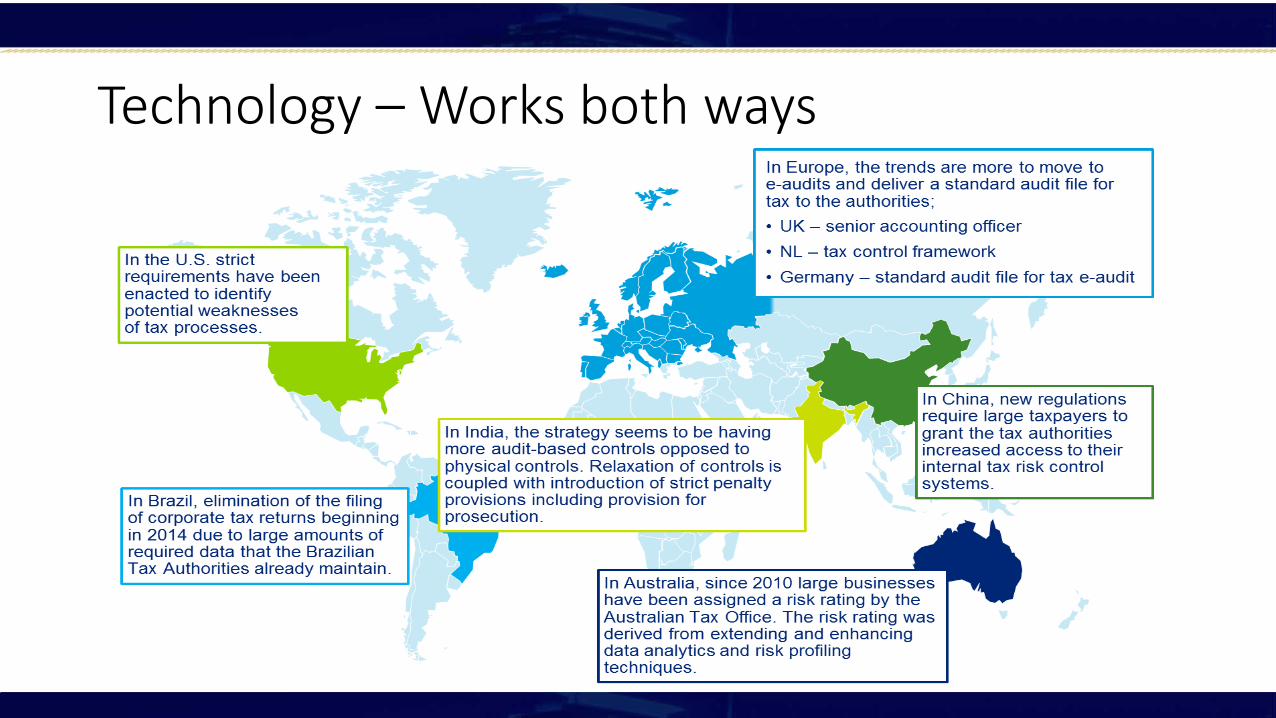

Technology – Works both ways

Policy trends in global mobility

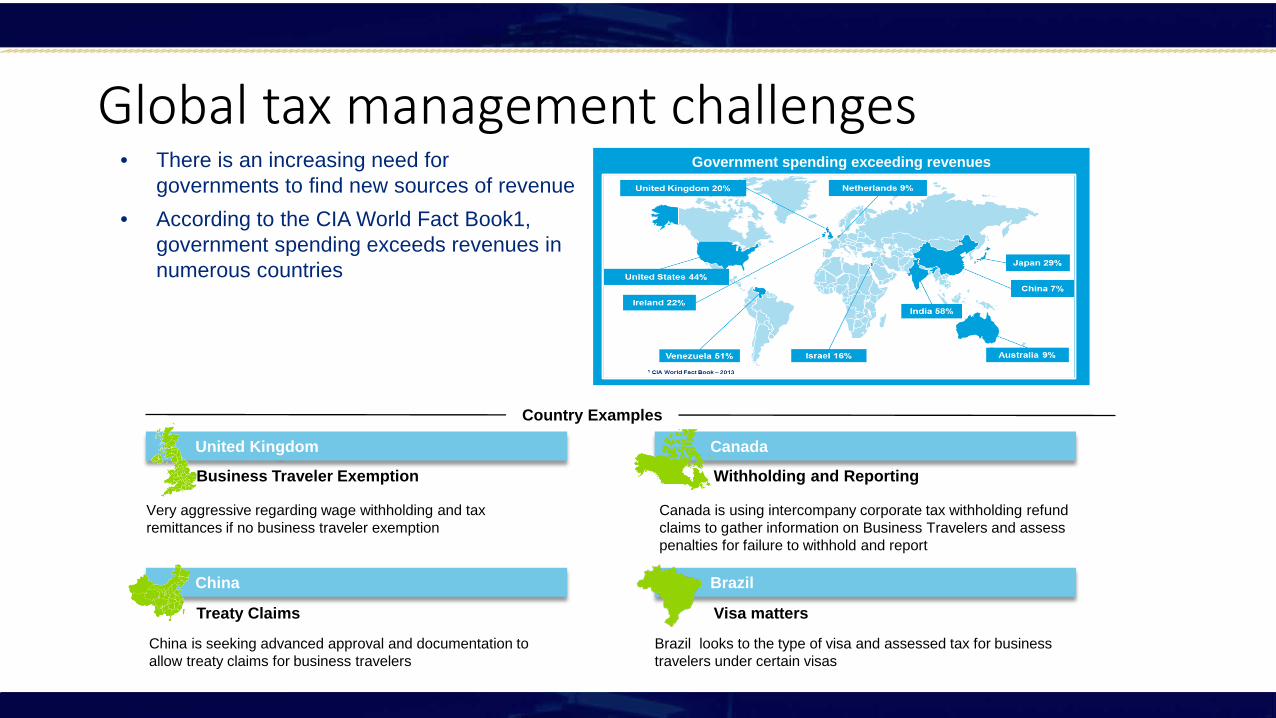

Global tax management challenges Government spending exceeding revenues • There is an increasing need for

governments to find new sources of revenue • According to the CIA World Fact Book1,

government spending exceeds revenues in numerous countries

United Kingdom Canada

Very aggressive regarding wage withholding and tax remittances if no business traveler exemption

Business Traveler Exemption Withholding and Reporting

China Brazil

Treaty Claims Visa matters

Canada is using intercompany corporate tax withholding refund claims to gather information on Business Travelers and assess penalties for failure to withhold and report

China is seeking advanced approval and documentation to allow treaty claims for business travelers

Brazil looks to the type of visa and assessed tax for business travelers under certain visas

Country Examples

Global Indicators Time to be proactive rather than reactive • Immigration authorities sharing information with tax authorities

• U.S. IRS has sent notices to companies to produce proof of filing tax returns for L-1 visa holders

• Singapore has sent companies tax assessments in connection with travelers’ business trips exceeding 60 days

• Failure to withhold taxes for business travelers • UK payroll audits have resulted in significant penalties for not withholding on Business

Travelers • Canada has assessed penalties for failure to withhold taxes on Business Travelers

• Tax authority audits • Japan tax authorities have requested list of all Business Travelers to Japan • U.S. New York State tax auditors’ have requested corporate data records, e.g. Business

Traveler and expenses to review • OECD launched the Tax Inspectors Without Borders initiative on 13 July 2015

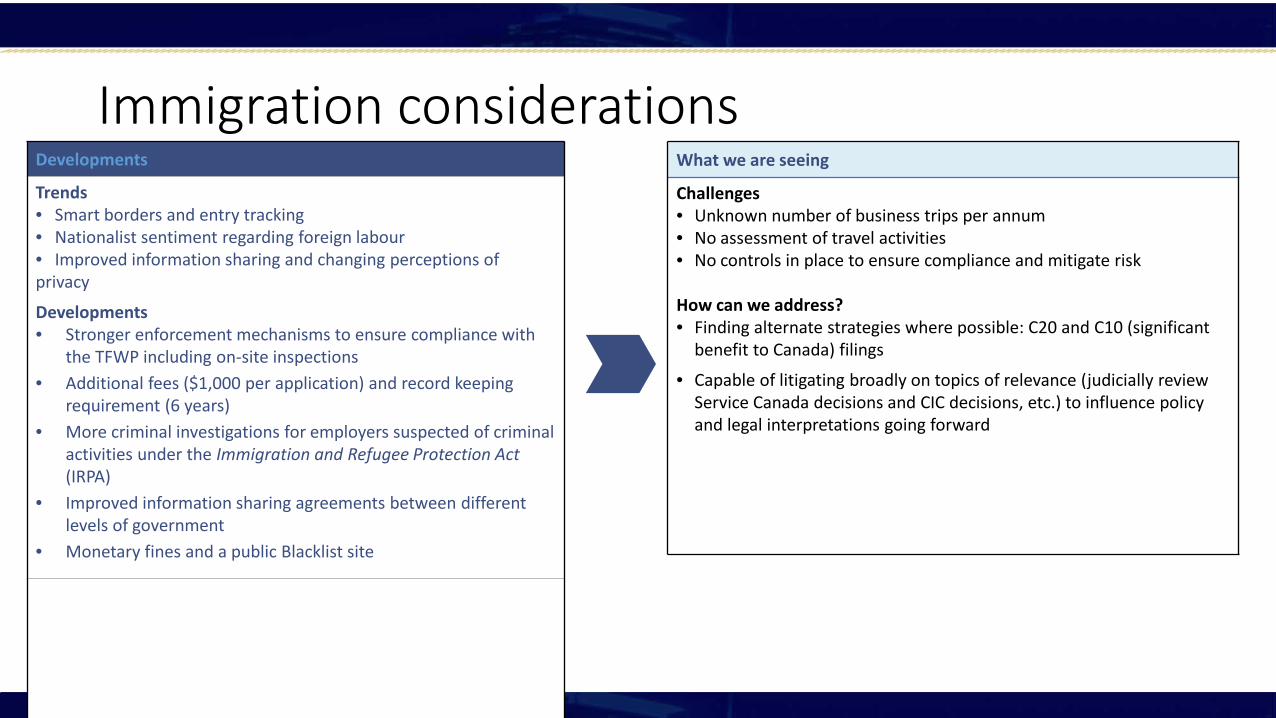

Immigration considerations Developments

Trends • Smart borders and entry tracking • Nationalist sentiment regarding foreign labour • Improved information sharing and changing perceptions of privacy

Developments • Stronger enforcement mechanisms to ensure compliance with

the TFWP including on-site inspections • Additional fees ($1,000 per application) and record keeping

requirement (6 years) • More criminal investigations for employers suspected of criminal

activities under the Immigration and Refugee Protection Act (IRPA)

• Improved information sharing agreements between different levels of government

• Monetary fines and a public Blacklist site

What we are seeing

Challenges • Unknown number of business trips per annum • No assessment of travel activities • No controls in place to ensure compliance and mitigate risk How can we address? • Finding alternate strategies where possible: C20 and C10 (significant

benefit to Canada) filings

• Capable of litigating broadly on topics of relevance (judicially review Service Canada decisions and CIC decisions, etc.) to influence policy and legal interpretations going forward

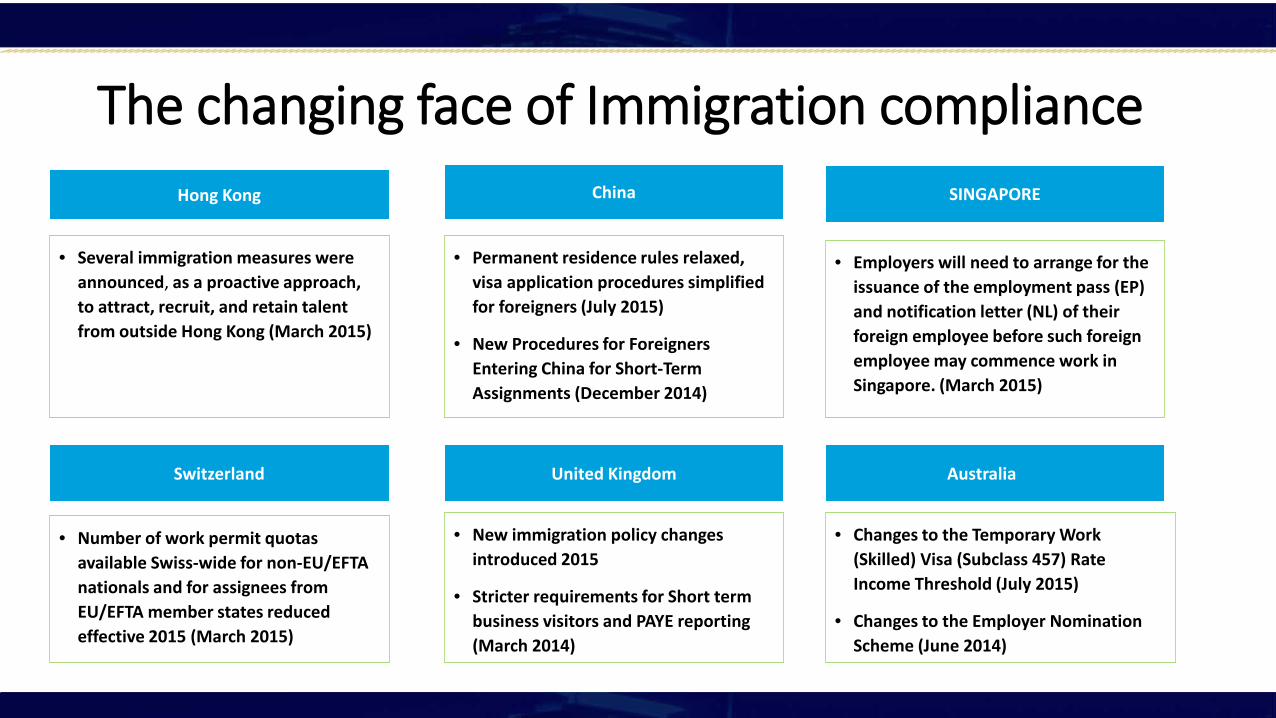

The changing face of Immigration compliance

• New immigration policy changes introduced 2015

• Stricter requirements for Short term business visitors and PAYE reporting (March 2014)

SINGAPORE

• Permanent residence rules relaxed, visa application procedures simplified for foreigners (July 2015)

• New Procedures for Foreigners Entering China for Short-Term Assignments (December 2014)

China

• Several immigration measures were announced, as a proactive approach, to attract, recruit, and retain talent from outside Hong Kong (March 2015)

Hong Kong

• Number of work permit quotas available Swiss-wide for non-EU/EFTA nationals and for assignees from EU/EFTA member states reduced effective 2015 (March 2015)

Switzerland

• Employers will need to arrange for the issuance of the employment pass (EP) and notification letter (NL) of their foreign employee before such foreign employee may commence work in Singapore. (March 2015)

United Kingdom

• Changes to the Temporary Work (Skilled) Visa (Subclass 457) Rate Income Threshold (July 2015)

• Changes to the Employer Nomination Scheme (June 2014)

Australia

Lets talk!