www.beyondphilosophy.com

Page 1 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

Customer Experience Management Executive Summary

Global Customer Experience Management Survey 2011 Research Paper

Beyond Philosophy

Who is Beyond Philosophy?

Beyond Philosophy is a Customer Experience Management (CEM) consulting, training and research firm. With headquarters based in Tampa, Florida (USA), we have global reach. Founded in 2002, the company has led the market in CEM working for many well-known Fortune 500 and FTSE brands. What is the Global Leaders of Customer Experience Management Survey 2011? The GLS is an annual global survey of the Customer Experience Management market. Its focus is on the current thinking of ‘Global Leaders of CEM’ i.e., leading analysts, corporate leaders of CEM and managers charged with implementation. As such this is a qualitative report, determining how leaders perceive the key market trends.

www.beyondphilosophy.com

Page 2 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

Abstract From May- July 2011, Beyond Philosophy undertook a comprehensive review of the

state of the global market for Customer Experience Management (CEM). This was

based on a sample of 8,000 Customer Experience (CE) executives from 239 countries

and regions of the world as well as in-depth interviews of 53 leading authorities on

Customer Experience from all continents.

A webinar of the results can be found here:

http://www.youtube.com/watch?v=R1f6kTQHbBI The findings were also featured in the media, including Huffington Post & CNN to name a few.

www.beyondphilosophy.com

Page 3 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

Contents

Abstract 2

1.1 Methodology 5

1.2 Quantitative 5

1.3 Qualitative 5

1.4 Sample 6

2.1 Insights 9

2.2 What is the background of Customer Experience leaders 9

2.3 How is Customer Experience defined 9

2.4 What is the level of adoption of Customer Experience Management around the 9

world?

2.5 Can you provide a model of adoption? Maturity Index 10

2.6 What is the level of adoption of Customer Experience management by company, 12

sector and level of maturity?

2.7 What are the drivers to growth in CE? 12

2.8 What are the challenges to growth in CE? 14

2.9 What is the most admired firm in Customer Experience? 15

3.1 Management Implications 16

3.2 What are the 5 Major Risks? 16

3.3 What is the strategy to manage these risks? 16

3.4 What are the 5 Major Drivers? 18

3.5 A Final View 19

Contacts 21

Figures and Tables

www.beyondphilosophy.com

Page 4 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

Table 1: Distribution of the 53 in-depth interviews including by title 6

Table 2: Summary Distribution of the 53 in-depth interviews by regional percentage 7

Figure 1: Distribution of the 53 in-depth interviews by sector 8

Figure 2: Distribution of 53 Expert Interviews by industry 8

Figure 3: The 7 Stage Maturity Model 10

Figure 4: The Acquisition, Relationship, Retention Stages 11

Figure 5: Key areas of a CE implementation 17

1.0 Methodology

www.beyondphilosophy.com

Page 5 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

1.1 Quantitative Beyond Philosophy undertook an analysis of 8,000 Customer Experience executives.

These executives were sourced from a country by country LinkedIn search; comprising

in-depth analysis of 239 countries and regions i.e., the globe as defined by LinkedIn and

Google drop down country/ region search list.

To qualify for inclusion, the LinkedIn respondents had to have ‘Customer Experience’ in

their ‘current’ job title: note that as a networking tool and to maximize coverage of

possible LinkedIn contacts, all main Customer Experience groups were joined. Likewise

the search was conducted from a well networked Customer Experience consulting group

(LinkedIn contacts were not used for marketing purposes, purely as a means of

research).

In addition, Beyond Philosophy conducted a Google search for firms that apply

Customer Experience across each of the 239 country and region web pages. In this

search, Beyond Philosophy set specific criteria for acceptance as a CE focused firm.

Companies had to have an active presence in Customer Experience ‘within the last year’

and ‘within the country pages’. This was to avoid the presence of non-active firms that

engaged in Customer Experience over one year ago.

2,106 companies were identified as active in Customer Experience Management

from around the world. This equates to an average of around 4 CE executives

per company.

1.2 Qualitative

From the quantitative database, Beyond Philosophy sourced 53 experts to conduct an

in-depth interview on Customer Experience. Experts had to have either overall line

responsibility for managing customer experience on-the-ground (Lead PM) or be at CxO

level (i.e., Director or VP of customer experience). In addition CE experts were sourced

www.beyondphilosophy.com

Page 6 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

i.e., individuals who had deep regional or vertical understanding of CE and were

recognized experts in Customer Experience.

All depth interviews were conducted by phone; excluding one interview that involved a

face to face meeting: Interviews typically lasted 20-25 minutes.

1.3 Sample

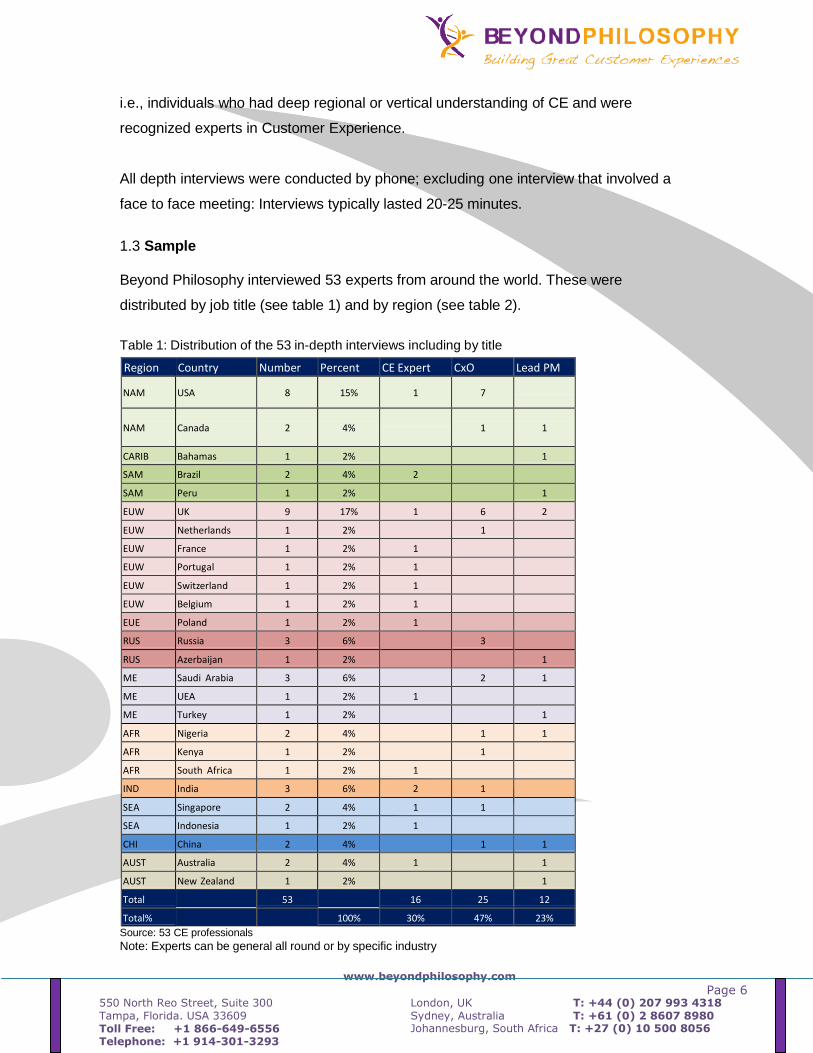

Beyond Philosophy interviewed 53 experts from around the world. These were

distributed by job title (see table 1) and by region (see table 2).

Table 1: Distribution of the 53 in-depth interviews including by title

Region Country Number Percent CE Expert CxO Lead PM

NAM USA 8 15% 1 7

NAM

Canada

2

4%

1

1

CARIB Bahamas 1 2% 1

SAM Brazil 2 4% 2 SAM Peru 1 2% 1

EUW UK 9 17% 1 6 2

EUW Netherlands 1 2% 1 EUW France 1 2% 1 EUW Portugal 1 2% 1 EUW Switzerland 1 2% 1 EUW Belgium 1 2% 1 EUE Poland 1 2% 1 RUS Russia 3 6% 3 RUS Azerbaijan 1 2% 1

ME Saudi Arabia 3 6% 2 1

ME UEA 1 2% 1 ME Turkey 1 2% 1

AFR Nigeria 2 4% 1 1

AFR Kenya 1 2% 1 AFR South Africa 1 2% 1 IND India 3 6% 2 1 SEA Singapore 2 4% 1 1 SEA Indonesia 1 2% 1 CHI China 2 4% 1 1

AUST Australia 2 4% 1 1

AUST New Zealand 1 2% 1

Total 53 16 25 12

Total% 100% 30% 47% 23%

Source: 53 CE professionals

Note: Experts can be general all round or by specific industry

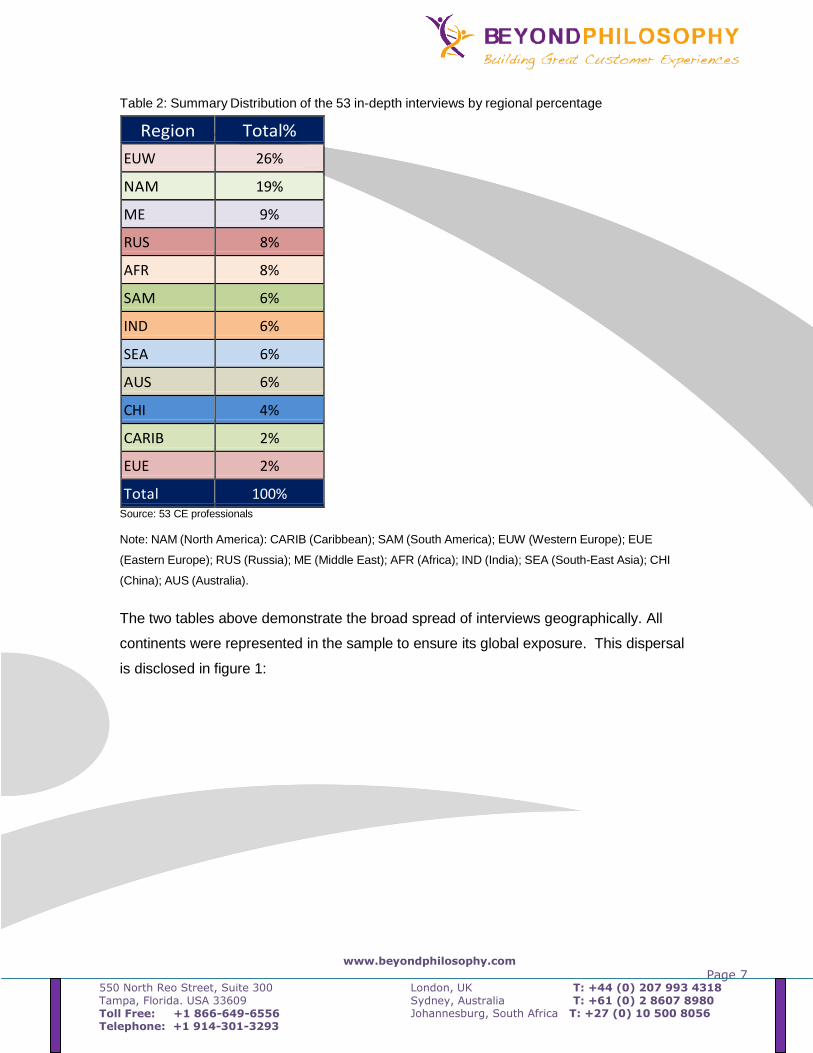

Table 2: Summary Distribution of the 53 in-depth interviews by regional percentage

www.beyondphilosophy.com

Page 7 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

Region Total%

EUW 26%

NAM 19%

ME 9%

RUS 8%

AFR 8%

SAM 6%

IND 6%

SEA 6%

AUS 6%

CHI 4%

CARIB 2%

EUE 2%

Total 100% Source: 53 CE professionals

Note: NAM (North America): CARIB (Caribbean); SAM (South America); EUW (Western Europe); EUE

(Eastern Europe); RUS (Russia); ME (Middle East); AFR (Africa); IND (India); SEA (South-East Asia); CHI

(China); AUS (Australia).

The two tables above demonstrate the broad spread of interviews geographically. All

continents were represented in the sample to ensure its global exposure. This dispersal

is disclosed in figure 1:

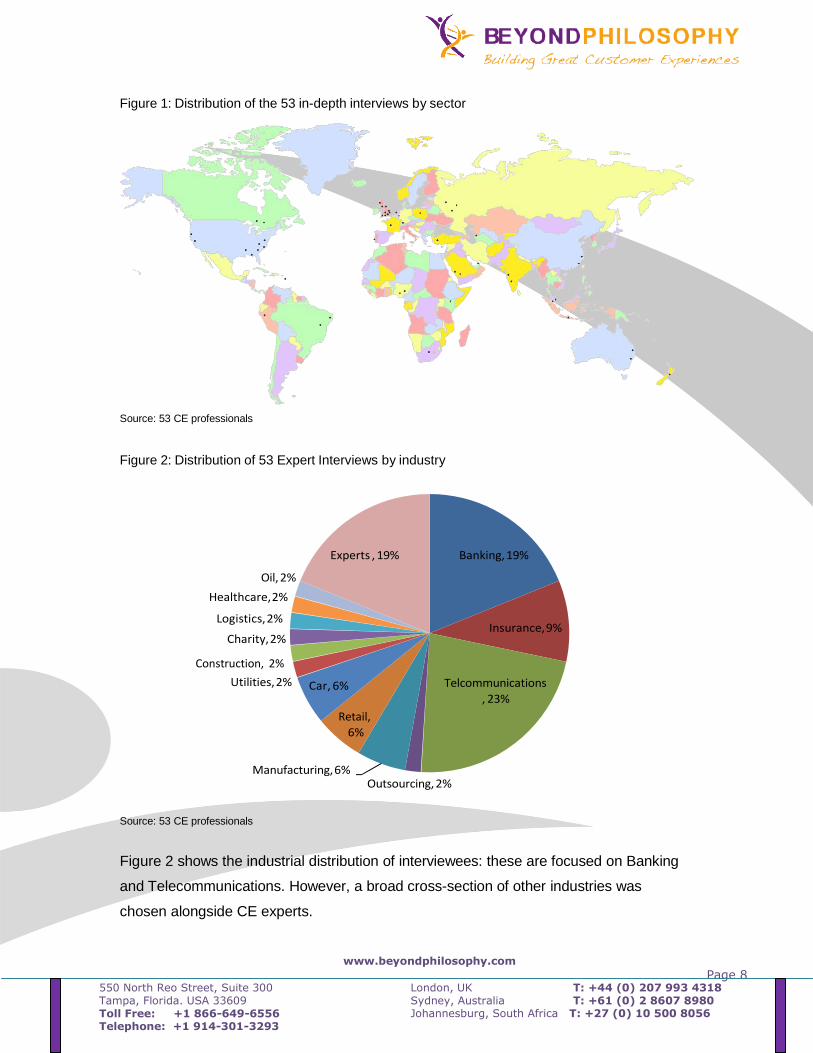

Figure 1: Distribution of the 53 in-depth interviews by sector

www.beyondphilosophy.com

Page 8 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

Source: 53 CE professionals

Figure 2: Distribution of 53 Expert Interviews by industry

Oil, 2%

Healthcare, 2%

Logistics, 2%

Charity, 2%

Construction, 2%

Utilities, 2%

Experts , 19%

Car, 6%

Retail,

6%

Banking, 19%

Insurance, 9%

Telcommunications

, 23%

Manufacturing, 6%

Outsourcing, 2%

Source: 53 CE professionals

Figure 2 shows the industrial distribution of interviewees: these are focused on Banking

and Telecommunications. However, a broad cross-section of other industries was

chosen alongside CE experts.

www.beyondphilosophy.com

Page 9 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

2.0 Insights

2.1 What is the background of Customer Experience leaders?

1. 78 percent of VP’s and Directors of Customer Experience have no background in

Customer Experience Management. The top previous roles are Operational

Management and Customer Service (N=136).

2.2 How is Customer Experience Defined?

2. Overall, 60 percent of respondents give a touchpoint definition of Customer

Experience while 28 percent define CE through customer research programmes. The

third highest is a definition that includes reference to emotional engagement. In

general while there is consensus, there are some key differences, such as the

greater focus on internal company process and mindset change amongst CxOs and

the customer research bias of Lead PMs (project managers).

2.3 What is the level of adoption of Customer Experience Management around the

world?

3. At least in the use of the term, Customer Experience is a global phenomenon.

4. 2,106 companies have been identified as being active in Customer Experience

Management from around the world. This equates to an average of around 4 CE

executives per company.

5. Regionally 58 percent of CE active companies come from 2 regions: North America

and Western Europe. 42 percent are active outside these regions with the next most

important region being Australasia (Australia and New Zealand) at 7 percent.

6. Some countries have an unexpectedly large number of CE companies. These

countries are India, Singapore, Australia and New Zealand.

7. Customer experience language exists even in countries with lower levels of

economic development such as Bhutan, Fiji and Afghanistan – this reflects its spread

through MnC’s(Multi National Companies), Telecommunications and through a

process of copying best practice from ‘the West.’

www.beyondphilosophy.com

Page 10 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

2.4 Can you provide a model of adoption? Maturity Index

8. Globally, countries and regions can be divided into 7 states of maturity: high; high-

mid; mid; mid-low; low; very low and no presence.

Figure 3: The 7 Stage Maturity Model

9. A noticeable feature of development is an expected ‘telescoping’ i.e., timeframes to

maturity are less than they were in the mature countries.

10. The Maturity Index is underpinned by a 3 stage model of development from a

customer acquisition focus thorough to relationship and then retention. Key

movements are currently being seen from acquisition to relationship in several mid to

low tier countries that are undergoing changing customer expectations with a

burgeoning middle class exposed to western styles of service as well as cross-

vertical expansion prospects in the B2B market.

Figure 4: The Acquisition, Relationship, Retention Stages

www.beyondphilosophy.com

Page 11 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

11. There is a large base of ‘nascent’ countries i.e., those at the tipping point to high

growth – this is the mid-low mature zone and represents countries such as South

Africa, Brazil, China and India as well as key countries in the mid mature zone such

as Turkey and the United Arab Emirates. These represent the best opportunities for

growth in the next 5 years.

12. Other countries to watch are Australia and New Zealand that have a firm platform of

awareness of CEM,

13. The most mature zones still reflect and Anglo-Saxon cultural foundation: UK, USA,

Canada, and Singapore.

14. Customer Experience is spreading out from its Anglo-Saxon centric base but still

remains most mature within this culture and cultures that have a strong English

speaking background (this is not a function of the research method as there are

strongly growing areas such as Brazil, China and Turkey).

15. Customer Experience is a function of levels of comparative economic development

and cultural acceptance e.g., service cultures form a basis for an Experience focus.

www.beyondphilosophy.com

Page 12 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

16. High mature does not mean high adoption as can be seen by the number of

companies covered as ‘actives.’ Indeed, adoption appears to be quite low.

17. Key trends in terms of future CE developments are exhibited at the High mature end.

18. Other less mature countries tend to be ‘me-to’ followers in terms of implementations

and understanding of Customer Experience.

2.5 What is the level of adoption of Customer Experience management by

company, sector and level of maturity?

19. Globally, over 60% of companies that have adopted CE are in four sectors,

Telecommunication, Banking, Retail and IT and services. There are also significant

sectors in Insurance, Motor and Airlines.

20. The 10 most active Global firms in Customer Experience are respectively: HP;

HSBC; Vodafone/ Vodacom; GAP; American Express; Dell; Citibank; Best Buy;

Sprint Nextel and AT&T.

21. In addition a number of key players ex UK and USA are in-country dominant and

becoming increasingly important e.g., Telstra and Turkcell.

22. In Telecommunications, there are a number of pivotal regional CE players such as

LIME in the Caribbean, MTN and Airtel in Africa.

23. In Banking there are a number of pivotal regional CE players such as Standard Bank

in Africa, Standard Chartered in Asia.

24. Several key investments in Customer Experience are noted from aviation (Boeing

and Delta ‘http://news.delta.com/index.php?s=43&item=870’).

25. 41 percent of interviewees state competitive intensity in Customer Experience as

strong; 43 percent state it as moderate and 16 percent as weak.

26. Management consultancies and research houses have been active in promoting

CEM alongside the Multi-National Corporations and brand promotion from leading

HQs.

2.6 What are the drivers to growth in CE?

27. In total, 65 percent of respondents stated that Customer Experience was a key

strategy for their company i.e., score of 7 out of 7 on importance. Only 14 percent

stated it as less than 4 out of 7 in terms of importance.

www.beyondphilosophy.com

Page 13 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

28. There is a clear pattern of support for continuing growth of Customer Experience in

Banking and Telecommunications. The other industry sectors do not exhibit a decline

in growth, more a ‘stay the same’ investment level.

29. 73.5 percent of interviewees expect increasing investment within their firms at an

average rate of 15 percent over the next year; 24.5 percent expect investment to be

maintained and 2 percent expect a fall.

30. The top driver to growth in CE remains the importance of differentiating under

conditions of commoditization. However, this is not the only reason, second in the

list are financial considerations around loyalty, retention and churn i.e., to defensively

prevent customers from leaving. Second equal is a new and key driver, the rising

trend of customer empowerment as customers have raised their expectations

through rising incomes and awareness of service quality gained via social media and

travel overseas. Of the customer empowerment drivers 38 percent of respondents

mention specifically the growing importance of Social Media: interestingly in

countries like Peru, Brazil and Turkey this is seen as essential – in effect these mid

to low tier mature countries are leapfrogging a technology.

31. Rates of growth are lower in B2B industries and those with a traditionally lower

customer service baseline.

32. There is a certain nervousness in stated investments i.e., slight, in current projects,

bi-model growth in some banks matched by cutting costs in others.

33. Companies are seeking to invest in the High Mature segment within ‘Stabilization’

projects e.g., IT systems, joining up systems to improve information flow HR and

training. Some international projects are deemed high investment, apportioned to

HQ but in fact driven to expand in High-Low Mature countries.

34. Companies are seeking to invest in the other segments within ‘Growth and

Optimization’ projects e.g., projects to establish Customer Experience or projects to

train in CE. Some of these are kick-started by international branding projects out of

HQ or through Government Regulation.

35. The general view is that these growth rates will be apparent in the third of business

who are interested in Customer Experience. There will be no change in terms of

‘interested industries.’

36. The industry that spends the most is the Telecommunications industry – although

this is by dint of its size in the first place. This is based on the CE investment views

of the 53 experts and the degree of networked arrangements these industries hold

www.beyondphilosophy.com

Page 14 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

i.e., the degree of ‘brand’ and ‘mission’ spread from HQ to other countries. To some

degree this is also symptomatic of a large software push which to a large extent has

been branded as part of corporate CEM initiatives.

2.7 What are the challenges to growth in CE

37. The main challenge to Customer Experience is quite simply whether it is an

operational priority: faced with a cost cutting agenda, legacy metrics and a sales

focus, CE risks falling by the wayside. This is a problem when the returns on

experience are couched in the long-term through increased customer loyalty and

experience adjustments are perceived as cost intensive or difficult. In short, setting

an agenda around fundamental change risks losing executive support.

38. Based on the 53 interviews (103 implementations or circa 2 implementations per

interviewee) the main areas of activity were focused on IT and software

implementations followed by training and customer research.

39. There is a serious disconnect between appreciating the importance of emotion and

how it is actually measured and therefore understood. The majority of interviewees

only undertook qualitative measurement through focus group, sentiment analysis,

verbatim analysis and journey mapping approaches or critical incident type

techniques. The situation quantitatively is even worse, respondents not adapting

current measures and just using Customer Satisfaction or loyalty indicators (NPS,

TRIM) as proxies for emotion. Some avoided the issue as too difficult or of

importance only as an outcome of other measures.

40. In total 65 percent of respondents have heard of NPS and know an organisation

(whether their own or another in their country) that uses it. 35 percent are not aware

of it or are aware of it but do not use it/ believe it should be used.

41. Interestingly, of those organizations that use NPS, there is some conflict starting to

develop in its application.

42. The one question interviewees wanted answering about Customer Experience

comprised: how to implement CE and how to demonstrate a link to financial return.

www.beyondphilosophy.com

Page 15 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

2.8 What is the most admired firm in Customer Experience? 43. Apple was the most admired CE firm.

44. Organisations not well recognised globally but admired regionally include in Brazil,

Brabesco Bank, Ludique et Badin and Natura; in Germany Berlin Airlines; Shoppers

Stop and Jet Airways in India and Turkcell in Turkey; and companies in the UK and

USA such as Screwfix Direct, Bank West, Metro Bank and Denny Marie.

www.beyondphilosophy.com

Page 16 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

3.0 Management Implications

3.1 What are the 5 Major Risks?

1. Risk 1: Use of the term as a rebrand for current operations - Customer

Experience is a well used term as demonstrated by the global spread of

executives with CE in their title. However, there is a disparity between use of the

term and the actual implementation of a CE programme.

2. Risk 2: Misappropriation of the term for vendor sales - Another risk is the active

misappropriation of the term ‘Customer Experience’ by some vendors as a front

for rebranding CRM as CEM in order to sell more solutions.

3. Risk 3: Failure to take account of the customer’s emotional viewpoint e.g., in ROI

- Customer Experience tends to follow a touchpoint definition. This is quite a

defensive position to take.

4. Risk 4: Limitation in its adoption - Beyond Philosophy concludes that the term

Customer Experience has achieved global acceptance. However, this

acceptance is limited to a few key verticals: Telecommunications, Banking, Retail

and several of the smaller sectors with increasing adoption in Aviation, Motor and

Insurance.

5. Risk 5: Timeframe to execute - One of the major problems with CE is that it

depends on the long-term. Its economic basis around loyalty is all about long-

term return, its advantages in terms of being more customer-centric also require

levels of corporate transformation that take years.

3.2 What is the strategy to manage these risks?

6. To avoid the risks companies have to realise that at its heart Customer

Experience is an organisational strategy based upon a holistic approach to the

customer using emotion as a key differentiator. This means embedding from the

very start the message that this is a transformational approach not just one

based on tinkering with the IT infrastructure, adapting call centres or measuring

numerous touchpoints. These may be part of a solution but they are not CE.

www.beyondphilosophy.com

Page 17 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

Figure 5: Key areas of a CE implementation

Understanding CE – get leadership buy-in and understanding as to what exactly

Customer Experience is!

Setting the strategy – define where your organisation is in terms of the

Customer Experience and your organisations understanding of the customer

journey from an emotional perspective and the emotion drivers and destroyers of

value. Build out a case study based on ROI and how CE will reach your

corporate objectives, usually towards competitive differentiation. Develop a

roadmap to change.

Engage the organisation – start to train the organisation in the principles of

customer experience and design in the organisational foundations to support it

long-term e.g., governance.

Embed the CE culture – focus on cultural alignment within the organisation

through training, recruitment, embedding CE in the employee experience and

leadership buy-in and support.

www.beyondphilosophy.com

Page 18 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

Process Improvement - only after the company has started to ‘get it’ should you

move to process improvement. Clearly with time lags, some IT system can be

planned in, but the stage of Cultural engagement should be in place prior to

delivery of a new CE process infrastructure for without employee support no

system emplacement will succeed.

Redesign experiences - finally, pilot implementations of specific customer

initiatives within the first 12 months to ensure proof of concept and the perception

that change at the customer level is happening i.e., we are starting to see how

we can get a return. Use Emotion Journey Maps and Emotional Measurement to

assist in the redesign but critically ensure creative execution.

3.3 What are the 5 Major Drivers?

7. Major Driver 1: Increasing need to respond to customer empowerment -

Customer Experience Management used to be driven mainly by concerns over

commoditisation: CE in effect being used as a means to differentiation. However,

a new key driver - customer empowerment - has come to the fore globally. This

makes CE a necessity rather than an option:

a. The 10 customer empowerment drivers are: social media; fast society;

burgeoning middle class; development of high value segments; demand

for international brands; deregulation of markets; increased travel;

regulation in favour of the customer; cultural sensitivity and web

aggregator sites.

8. Major Driver 2: Increasing need to manage organisational complexity - Customer

Experience Management is mainly, but not exclusively, a phenomenon of Multi-

National Corporations. Faced with a proliferation of multiple channels and

increasing complexity in terms of IT infrastructure and expansion into new

territories the current siloed structure of organisations is facing breakdown. With

marketing focused on the 4Ps and customer service on service delivery and IT

on the web infrastructure there is a problem of control and communication. This

failure leads to breakage points.

9. Major Driver 3: Increasing awareness of the importance of emotion and how this

translates into loyalty gains - The way of operating marketing has changed from

www.beyondphilosophy.com

Page 19 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

one focused on the 4Ps to one that increasingly looks at emotion as a platform

for differentiation. In part this is driven by the commoditisation challenge, but

also by the evidence from neuroscience and advanced research, that emotions

drive behaviour.

10. Major Driver 4: Move from product based to service based organisations - In

general, the focus of CE is on verticals with a high customer facing base. These

are industries that would have used the term customer service but now use

customer experience instead. Less apparent has been the B2B industries.

However, as many product based organisations face margin collapse with

commoditisation, so they will look to CE as a means to target and develop new

service related propositions. Here, the ability to manage relationships will be

uppermost as the space for differentiation along product lines declines. This is a

trend focused on new wave Customer Experience verticals in the B2B space

e.g., Manufacturing, Logistics, Construction and as current B2C providers

integrate CE into their supply chain.

11. Major Driver 5: Web Experience- The focus on Web enablement is allowing

companies in less mature regions to leapfrog a technology and play on a more

even playing field with the more mature countries. Indeed, in some cases the

Web experience is deemed of greater importance e.g., Brazil.

3.4 A Final View

12. Growth in CE is intimately linked to organisational consciousness of the

customer. This is why some sectors such as Telecoms ‘get it’, there is no where

to hide, while others often in B2B are behind the curve. With increasing push

from regulation and pull from commoditisation, Beyond Philosophy see an

increasing number of firms becoming conscious of the need to organise

themselves towards the customer .

13. In the current market those sectors coming from a low base (such as

manufacturing); facing fast innovation (such as E-tail) and regulatory push (such

as healthcare) will experience the highest growth. However, there is a

comprehensive need even in the first generation to reconsider what Customer

Experience is i.e., are you really doing it!

www.beyondphilosophy.com

Page 20 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

14. it is no good taking a defensive position around measuring touchpoints or

rebranding service and research, organisations need to ensure they ‘truly’

consider the meaning of Customer Experience based on its founding notions of

organisational redesign and an emotional commitment to loyalty.

15. It seems for now CE is standing at a crossroads between success and failure.

The message should be ‘rejuvenate or die.’

16. Companies that have emotions inside understand the customer experience far

better than those that assume customers are always rational. With an emotional

understanding firms are better able to control complexity through customer

action, rather than more controlling measurements.

www.beyondphilosophy.com

Page 21 550 North Reo Street, Suite 300 Tampa, Florida. USA 33609 Toll Free: +1 866-649-6556 Telephone: +1 914-301-3293

London, UK T: +44 (0) 207 993 4318 Sydney, Australia T: +61 (0) 2 8607 8980 Johannesburg, South Africa T: +27 (0) 10 500 8056

Contacts For more information on this report or Customer Experience in general please contact:

Beyond Philosophy Global Headquarters

550 North Reo Street

Suite 300

Tampa Florida. 33609

Toll Free: +1 866-649-6556

Outside USA: +1 914-301-3293

International Contact Numbers

London, United Kingdom: +44 (0) 207 993 4318

Sydney, Australia: +61 (0) 2 8607 8980

Johannesburg, South Africa: +27 (0) 10 500 8056

www.beyondphilosophy.com