THE CITY OF NEW YORKOFFICE OF THE COMPTROLLER

March 20, 2017

COMMON INVESTMENT MEETINGPublic Session

PERFORMANCE REPORTINGOverview – Fourth Quarter 2016

Asset Class Index Fourth Quarter 2016

FYTD 3 Year 5 Year Expected*

Equities - U.S. Russell 3000 4.2% 8.8% 8.4% 14.7% 7.8%

Equities - Developed Intl MSCI EAFE -0.7% 5.7% -1.6% 6.5% 8.9%

Equities - Emerging Intl MSCI EMF -4.2% 4.5% -2.6% 1.3% 11.0%

Debt – US Treasuries Long Duration Citigroup Treasury 20+ -12.1% -12.6% 8.4% 2.5% 2.1

Debt - US Government NYC Treas/Agency +5 -7.3% -7.8% 4.6% 1.9% 2.8%

Debt - Investment Grade NYC IG Credit -3.1% -1.7% 3.9% 3.8% 3.4%

Debt - High Yield Citigroup BB & B 1.6% 6.8% 4.4% 6.7% 6.1%

3

Market Returns: Q4-2016

Source: State Street

*Average of consultant long-term arithmetic expected returns, as of 2016

Prepared by the New York City Comptroller's Office Bureau of Asset Management

4

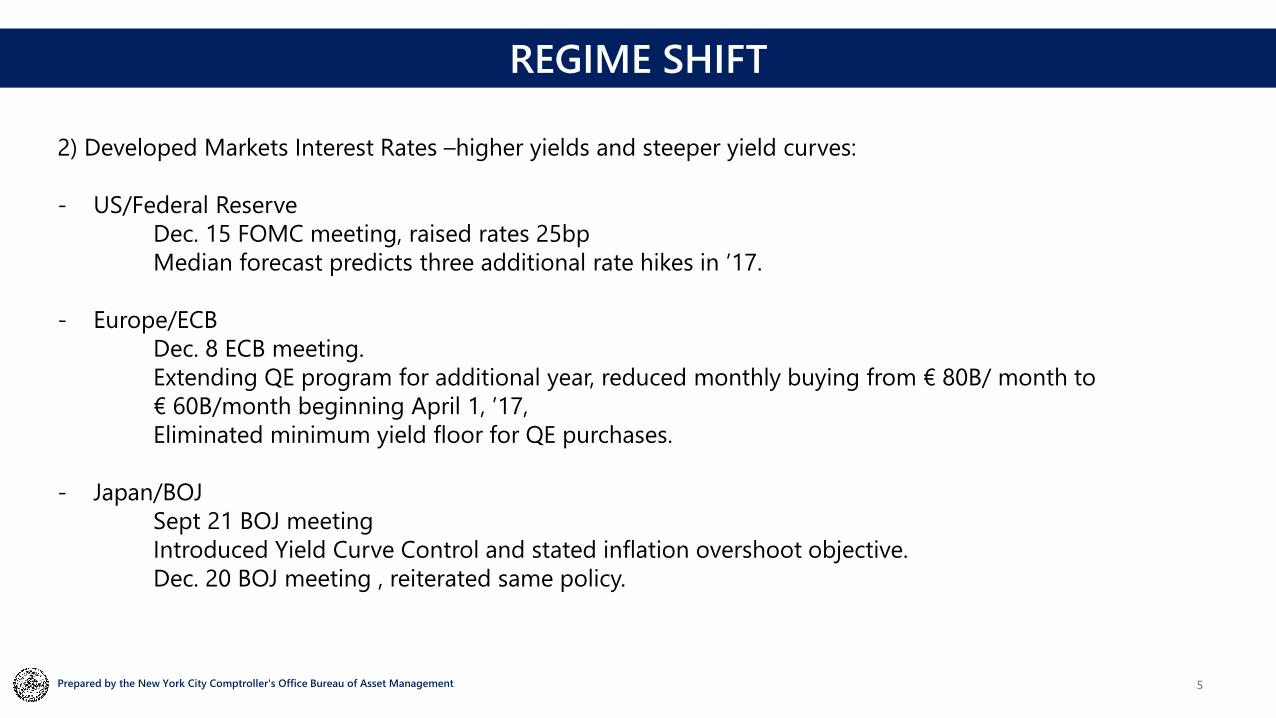

REGIME SHIFTQ4 Themes:

1) US Election/Republican sweep – markets expecting stronger GDP growth and higher earnings based on anticipated policy changes in three key areas.

- Business and personal income tax reform.

- Reduction in business regulations.

- Increase in fiscal spending (infrastructure and defense)

Rotation within US Equities Q4 2016 3 Year

Vulcan Materials Co. (Infrastructure Proxy)

10.22% 32.62% 28.67%

Rotation within US Equities Q4 2016 3 YearRussell 3000 Index 4.21% 12.74% 8.43%Russell 2000 Index 8.83% 21.31% 6.74%Russell 3000 Growth Index 1.20% 7.39% 8.27%Russell 3000 Value Index 7.24% 18.40% 8.55%

Rotation within US Equities Q4 2016 3 YearFinancial Equity ETF 21.02% 22.59% -2.80%Energy Equity ETF 7.24% 28.00% 11.52%

Prepared by the New York City Comptroller's Office Bureau of Asset Management

5

REGIME SHIFT

2) Developed Markets Interest Rates –higher yields and steeper yield curves:

- US/Federal ReserveDec. 15 FOMC meeting, raised rates 25bpMedian forecast predicts three additional rate hikes in ’17.

- Europe/ECB Dec. 8 ECB meeting.Extending QE program for additional year, reduced monthly buying from € 80B/ month to € 60B/month beginning April 1, ’17, Eliminated minimum yield floor for QE purchases.

- Japan/BOJSept 21 BOJ meetingIntroduced Yield Curve Control and stated inflation overshoot objective. Dec. 20 BOJ meeting , reiterated same policy.

Prepared by the New York City Comptroller's Office Bureau of Asset Management

0

0.2

0.4

0.6

0.8

1

1.2

1.4

UST 10YR Yield - Change in bps 84.9 Germany 10Yr Yield - Change in bps 33

JPY 10YR Yield - Change in bps 13.5 UK 10YR Yield - Change in bps 49.3

Feb-17Dec-16Sep-16Jun-16Mar-16

6

Global Yields

Source: Bloomberg

Prepared by the New York City Comptroller's Office Bureau of Asset Management

0

0.2

0.4

0.6

0.8

1

1.2

1.4

US Breakeven 10 Year- Change in bps: 36.1 Germany Breakeven 10 Year- Change in bps: 29.9

Japan Breakeven 10 Year- Change in bps: 26.7 UK Breakeven 10 Year- Change in bps: 33.3

Feb-17Dec-16Sep-16Jun-16Mar-16

7

Global Inflation Breakeven

Source: BloombergPrepared by the New York City Comptroller's Office Bureau of Asset Management

8

REGIME SHIFT

3) US Dollar strength – dollar rallied 5.5 %, contributing factors included:

- Impact of Border Adjustment Taxes.

- Higher US interest rates, both absolute and relative to G7 countries.

- Potential for one-time off shore income tax repatriation.

- Potential for retaliatory trade sanctions.

Prepared by the New York City Comptroller's Office Bureau of Asset Management

Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17116

118

120

122

124

126

128

130

9

US Trade Weighted Broad Dollar Index- 1 Year

Source: BloombergPrepared by the New York City Comptroller's Office Bureau of Asset Management

10

US Trade Weighted Broad Dollar Index- 2000-2017

Source: BloombergPrepared by the New York City Comptroller's Office Bureau of Asset Management

11

REGIME SHIFTCurrent Global Macro Issues:

Domestic:- Probability, timing and specifics of US Tax and Spending Plans.

- Impact on economy and markets of trade and immigration reform.

- Federal Reserve – pace and magnitude of interest rate increases, change

in composition of Fed leadership and board, potential regulatory

changes to Federal Reserve.

”….the process of scaling back accommodation likely will not be as slow

as it was in 2015 and 2016.” Janet Yellen, March 3, 2017.

International: - European political risk – elections in Netherlands (March 15), France

(first round April 23, final May 7), Germany (anticipated in fall ’17)

- ECB and BOJ – potential for slowing or ending of Quantitative Easing

policies.Prepared by the New York City Comptroller's Office Bureau of Asset Management

Gross of fees in public asset classes

(SSB N p.22; T, F p.23; P p.25 ; B p.27)

NYC Pension System Portfolio Std Dev - 1 yr

4th Quarter FYTD One Year Three Year

Five Year

BERS 7.4% 1.1% 5.8% 9.4% 5.2% 9.4%TRS 6.8% 0.5% 4.3% 8.9% 5.3% 8.9%POLICE 6.4% 1.2% 5.1% 9.1% 5.6% 9.2%FIRE 6.3% 0.8% 4.7% 8.7% 5.5% 9.0%NYCERS 6.2% 1.1% 5.0% 9.6% 5.5% 9.0%Median Fund - TUCS 1.1% 4.7% 7.9% 5.3% 9.0%Public Mkt Equiv (65/35 index) 0.6% 4.1% 6.7% 4.5% 8.6%

12

Total NYC Pension Fund (Gross) Performance: 12/31/16

Source: State Street

Prepared by the New York City Comptroller's Office Bureau of Asset Management

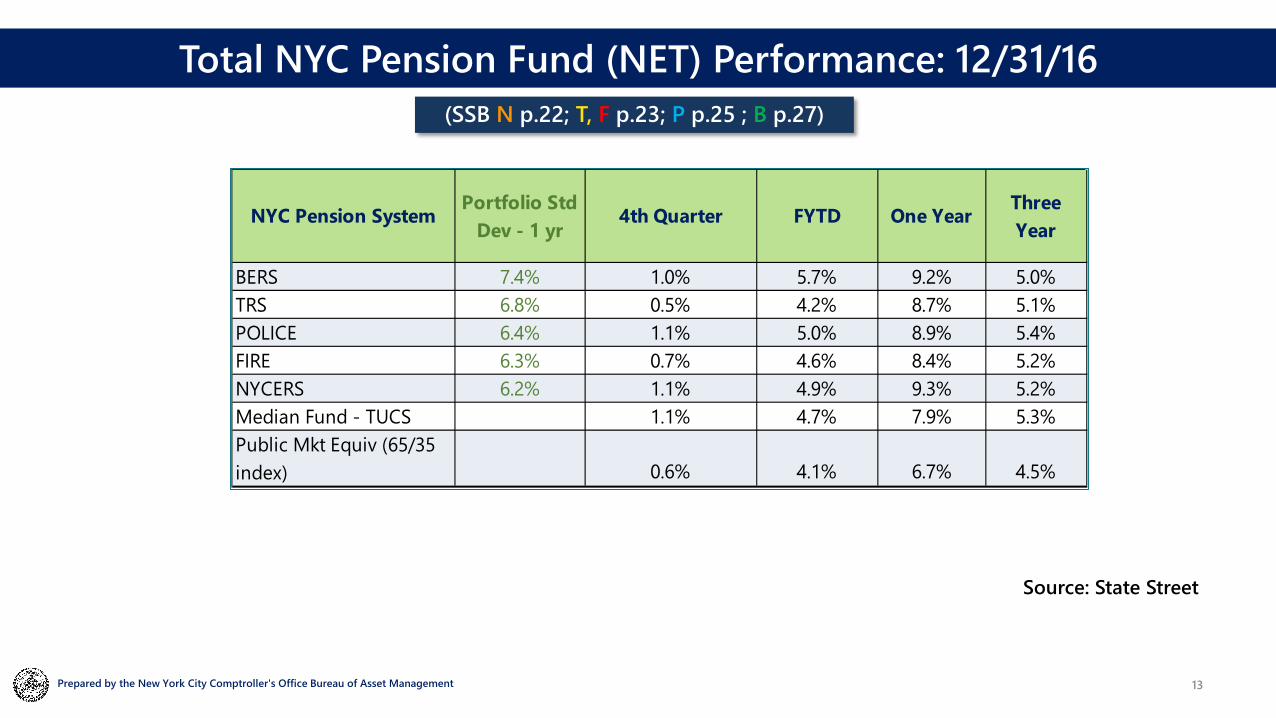

(SSB N p.22; T, F p.23; P p.25 ; B p.27)

NYC Pension System Portfolio Std Dev - 1 yr

4th Quarter FYTD One Year Three Year

BERS 7.4% 1.0% 5.7% 9.2% 5.0%TRS 6.8% 0.5% 4.2% 8.7% 5.1%POLICE 6.4% 1.1% 5.0% 8.9% 5.4%FIRE 6.3% 0.7% 4.6% 8.4% 5.2%NYCERS 6.2% 1.1% 4.9% 9.3% 5.2%Median Fund - TUCS 1.1% 4.7% 7.9% 5.3%Public Mkt Equiv (65/35 index) 0.6% 4.1% 6.7% 4.5%

13

Total NYC Pension Fund (NET) Performance: 12/31/16

Source: State Street

Prepared by the New York City Comptroller's Office Bureau of Asset Management

14

Asset Allocation Fourth Quarter 2016 – Equity and Private Markets

Source: State Street

Relative Mix to Adjusted Old Policy Weights (SSB F, T, N, B p.8; P, p.10)

Prepared by the New York City Comptroller's Office Bureau of Asset Management

15

Asset Allocation Fourth Quarter 2016 - Fixed IncomeRelative Mix to Adjusted Old Policy Weights (SSB F, T, N, B p.8; P, p.10)

Source: State Street

Prepared by the New York City Comptroller's Office Bureau of Asset Management

16

Asset Allocation Fourth Quarter 2016 – Equity and Private Markets

Source: State Street

Relative Mix to Adjusted New Policy Weights (SSB F, T, N, B p.8; P, p.10)

Prepared by the New York City Comptroller's Office Bureau of Asset Management

17

Asset Allocation Fourth Quarter 2016 - Fixed IncomeRelative Mix to Adjusted New Policy Weights (SSB F, T, N, B p.8; P, p.10)

Source: State Street

Prepared by the New York City Comptroller's Office Bureau of Asset Management

18

4th Quarter Net Return – Total Portfolio

-200

-150

-100

-50

0

50

100

150

200

4Q Portfolio 4Q Benchmark 4Q Excess

bps

TRS

NYCERS

Police

Fire

BERS

December 31, 2016 (SSB N, F, p.22; T, p.23; P p.24 B p.26)

Source: State StreetPrepared by the New York City Comptroller's Office Bureau of Asset Management

19

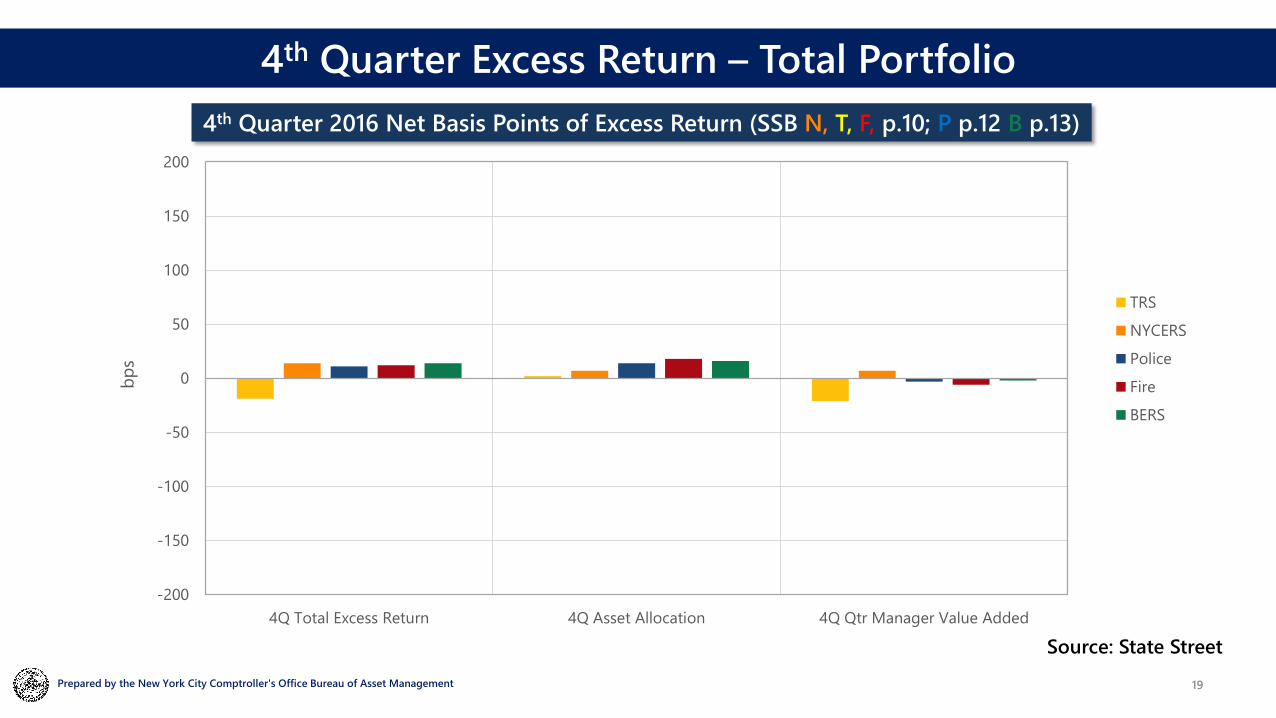

4th Quarter Excess Return – Total Portfolio

-200

-150

-100

-50

0

50

100

150

200

4Q Total Excess Return 4Q Asset Allocation 4Q Qtr Manager Value Added

bps

TRS

NYCERS

Police

Fire

BERS

Source: State Street

4th Quarter 2016 Net Basis Points of Excess Return (SSB N, T, F, p.10; P p.12 B p.13)

Prepared by the New York City Comptroller's Office Bureau of Asset Management

20

4th Quarter Excess Return – Equity & Fixed Income

-200

-150

-100

-50

0

50

100

150

200

4Q Asset Allocation 4Q Total Excess Equity 4Q Total Excess Fixed Income

bps

TRS

NYCERS

Police

Fire

BERS

Source: State StreetPrepared by the New York City Comptroller's Office Bureau of Asset Management

21

Manager Value Added- Total Portfolio

-200

-150

-100

-50

0

50

100

150

200

4Th QTR 3 Year Trailing

TRS

NYCERS

Police

Fire

BERS

bps

Net Basis Points of Excess Return (SSB N, T, F, p.10; P p.12 B p.13)

Source: State Street

Prepared by the New York City Comptroller's Office Bureau of Asset Management

22

Value Added – Total U.S. Equities

-600

-400

-200

0

200

400

600

4Th Qtr 3 Year Trailing

TRS: 30.84%NYCERS: 33.09%Police: 36.84%Fire: 31.92%BERS: 36.41%

Source: State Street

Weights as of12/31/2016

bps

Net Basis Points of Excess Return (SSB N, F, p.22; T, p.23; P p.24 B p.26)

Prepared by the New York City Comptroller's Office Bureau of Asset Management

23

Value Added – U.S. Equities – Mid Cap

-600

-400

-200

0

200

400

600

4Th Qtr 3 Year Trailing

TRS: 0.23%NYCERS: 1.55%Police: 2.04%Fire: 1.94%BERS: 2.45%

Source: State Street

Weights as of12/31/2016

bps

Net Basis Points of Excess Return (SSB N, F, p.22; T, p.23; P p.25 B p.26)

Prepared by the New York City Comptroller's Office Bureau of Asset Management

24

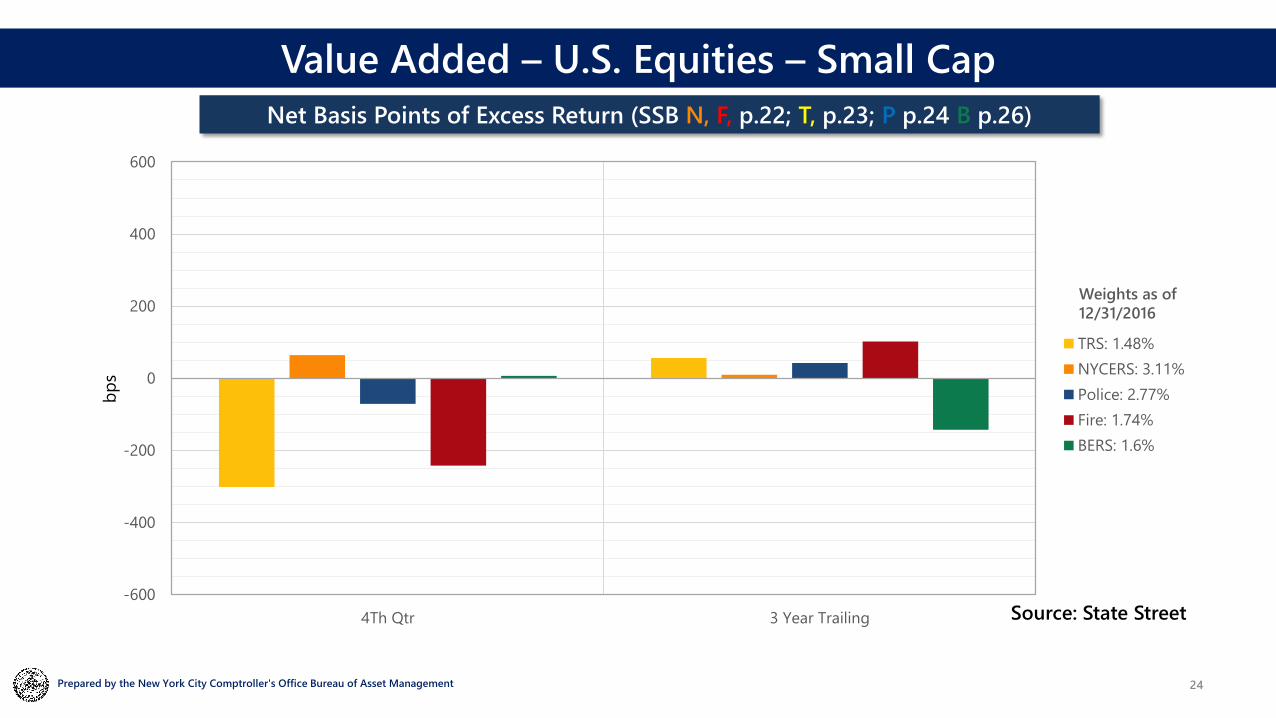

Value Added – U.S. Equities – Small Cap

-600

-400

-200

0

200

400

600

4Th Qtr 3 Year Trailing

TRS: 1.48%NYCERS: 3.11%Police: 2.77%Fire: 1.74%BERS: 1.6%

Source: State Street

Weights as of12/31/2016

bps

Net Basis Points of Excess Return (SSB N, F, p.22; T, p.23; P p.24 B p.26)

Prepared by the New York City Comptroller's Office Bureau of Asset Management

25

Value Added – Developed Growth

-600

-400

-200

0

200

400

600

4Th Qtr 3 Year Trailing

TRS: 3.7%NYCERS: 3.32%Police: 3.04%Fire: 3.83%BERS: 6.83%

Source: State Street

Weights as of12/31/2016

bps

Net Basis Points of Excess Return (SSB N, F, p.24; T, p.25; P p.26; B p.28)

Prepared by the New York City Comptroller's Office Bureau of Asset Management

26

Value Added – Developed Value

-600

-400

-200

0

200

400

600

4Th Qtr 3 Year Trailing

TRS: 3.29%NYCERS: 3.52%Police: 2.94%Fire: 3.57%BERS: 7.38%

Source: State Street

Weights as of12/31/2016

bps

Net Basis Points of Excess Return (SSB N, F, p.24; T, p.25; P p.26; B p.28)

Prepared by the New York City Comptroller's Office Bureau of Asset Management

27

Value Added – Structured Fixed Income

-600

-400

-200

0

200

400

600

4Th Qtr 3 Year Trailing

TRS: 17.02%NYCERS: 15.41%Police: 14.93%Fire: 15.75%BERS: 13.89%

Source: State Street

Weights as of12/31/2016

bps

Net Basis Points of Excess Return (SSB T, N p.28; F, p.29; P, B p.30)

Prepared by the New York City Comptroller's Office Bureau of Asset Management

28

Value Added – Economically Targeted Investments

-600

-400

-200

0

200

400

600

4Th Qtr 3 Year Trailing

TRS: 0.91%NYCERS: 1.3%Police: 1.01%Fire: 0.74%BERS: 0.6%

Source: State Street

Weights as of12/31/2016

bps

Basis Points of Excess Return (SSB T, N p.29; F p30; B p.31 P p.32)

Prepared by the New York City Comptroller's Office Bureau of Asset Management

Value Added- Hedge FundsBasis Points of Excess Return

-600

-400

-200

0

200

400

600

4TH Qtr 3 Year Trailing

TRS - N/A

NYCERS: 1.05%

Police: 4.74%

Fire: 4.71%

BERS - N/A

Source: Aksia

Weights as of12/31/2016

29

bps

Value Added - Hedge FundsBasis Points of Excess Return (SSB F p.51; N p.52; P p.56)

Prepared by the New York City Comptroller's Office Bureau of Asset Management

PRIVATE MARKET DATA

31

Value Added – Private Equity

-600

-400

-200

0

200

400

600

Excess Return Since Inception; PME Benchmark: Russell 3000 as of 9/30/16

TRS - 07/08/99

NYCERS - 03/29/99

Police - 03/29/99

Fire - 03/29/99

BERS - 07/20/06

Inception Date

300bps Target

Sources: StepStone Groupand Hamilton Lane

Basis Points of Cumulative IRR above Public Market Equivalent

bps

The PME Spread is the difference between the IRR and the PME Benchmark.Prepared by the New York City Comptroller's Office Bureau of Asset Management

32

Value Added – Private Real Estate - Core

-800

-600

-400

-200

0

200

400

600

800

Excess Return Since Inception; Core = 40% Equities- Russell 3000 /60% BarcAgg as of 9/30/16

TRS - 12/6/2002

NYCERS - 12/6/2002

Police - 12/6/2002

Fire - 12/6/2002

BERS - 12/13/2010

Inception Date

Source: State Street

Basis Points of Cumulative IRR above Public Market Equivalentbp

s

The PME Spread is the difference between the IRR and the PME Benchmark.

Prepared by the New York City Comptroller's Office Bureau of Asset Management

33

Value Added – Private Real Estate – Non-Core

-800

-600

-400

-200

0

200

400

600

800

Excess Return Since Inception; Non-core = 60% Equities- Russell 3000/40% BarcAgg as of 9/30/16

TRS - 12/6/2002

NYCERS - 12/6/2002

Police - 12/6/2002

Fire - 12/6/2002

BERS - 12/13/2010

Inception Date

Source: State Street

Basis Points of Cumulative IRR above Public Market Equivalentbp

s

The PME Spread is the difference between the IRR and the PME Benchmark.

Prepared by the New York City Comptroller's Office Bureau of Asset Management

34

Value Added – Opportunistic Fixed Income (OFI)

-600

-400

-200

0

200

400

600

Excess Return Since Inception; PME Benchmark: 50% JP Morgan Global High Yield 50% CS Leveraged Loans as of 12/31/16

TRS - 10/24/2007

NYCERS - 10/24/2007

Police - 10/24/2007

Fire - 10/24/2007

BERS - N/A

Inception Date

300bps Target

Source: State Street

Basis Points of Cumulative IRR above Public Market Equivalent

bps

The PME Spread is the difference between the IRR and the PME Benchmark.

Prepared by the New York City Comptroller's Office Bureau of Asset Management

35

Value Added - Infrastructure

-600

-400

-200

0

200

400

600

Excess Return Since Inception; PME Benchmark: 50% R3000 & 50% Barclays Agg. as of 9/30/16

TRS - 11/19/2013

NYCERS - 11/19/2013

Police - 11/19/2013

Fire - 11/19/2013

BERS - 11/19/2013

Inception Date

Source: StepStone Group

Basis Points of Cumulative IRR above Public Market Equivalentbp

s

The PME Spread is the difference between the IRR and the PME Benchmark.

Prepared by the New York City Comptroller's Office Bureau of Asset Management

RISK UPDATE

1. Risk Group Staffing

2. BAM Ribbon & Basket Clause monitoring process

3. Risk Analytic RFP

Risk Update

37Prepared by the New York City Comptroller's Office Bureau of Asset Management

Risk Group Staffing

• In 2015 the Risk Group consisted of Sherma Cooper, Daniel Haas and Miles Draycott.

• In 2016 we added three individuals to the group:

– Nikolay Radev joined the team in February as a Senior Investment Analyst after completing his Master’s degree in Financial Engineering at the Stevens Institute of Technology.

– Chris Lusk joined the team in April as an Application Developer. Prior to joining BAM, Chris worked at Merrill Lynch.

– Alex Dotov joined the team in December as a Senior Investment Officer. Alex was previously a Managing Director in the Office of the CIO of NY Life Investment Management.

Risk Group Staffing

39Prepared by the New York City Comptroller's Office Bureau of Asset Management

BAM Ribbon & Basket Clause Monitoring Process

• The structure of many NYC pension fund investments is complex

• State Street’s financial reports are produced monthly

• The Risk Management Team (Chris Lusk) has developed an application, available via an Excel ribbon, that produces daily P&L and asset allocation reports for all five systems. These reports are derived from:

oState Street holdings and activity data for the six legal entities that hold investments

oMarket prices for public market securities

oSecurities data obtained via the Bloomberg API

41

Asset Allocation and Performance Analysis

Prepared by the New York City Comptroller's Office Bureau of Asset Management

The bubble chart below is produced by the BAM ribbon – as are numerous additional reports useful to BAM’s risk and investment staff.

. The following pages show examples of

42

BAM Ribbon

Prepared by the New York City Comptroller's Office Bureau of Asset Management

43

BAM Ribbon

Prepared by the New York City Comptroller's Office Bureau of Asset Management

44

Equity Breakdown

Prepared by the New York City Comptroller's Office Bureau of Asset Management

45

Fixed Income Breakdown

Prepared by the New York City Comptroller's Office Bureau of Asset Management

• The asset allocation report available through the BAM ribbon is the means by which BAM monitors compliance with the “Basket Clause”.

• The process for monitoring Basket Clause compliance is:

– BAM Risk Group runs the asset allocation report on a daily basis. It is then reviewed by the Financial Reporting function.

– In the event that a System’s basket holdings exceed 23%, 24% or 25%, BAM is required to take specific actions.

46

Basket Clause Monitoring

Prepared by the New York City Comptroller's Office Bureau of Asset Management

The ribbon also produces an asset allocation report that is relied upon by the rebalancing team - chaired by Mike Haddad

47

Basket Clause Monitoring

Prepared by the New York City Comptroller's Office Bureau of Asset Management

Risk Analytic RFP

• BAM’s risk analytics RFP is seeking software able to both estimate the risk of a portfolio and analyze investment/manager returns (an “attribution” platform).

• An important objective is to procure software useful to both the risk team and the asset teams. The software needs to be capable of both top down “factor” analysis of the total plan and granular analysis of an alternative investment.

• BAM loaded one NYC pension system’s holdings into Bloomberg in order to prepare for the upcoming Risk Analytics RFP trials.

Risk Analytics RFP

49Prepared by the New York City Comptroller's Office Bureau of Asset Management

Risk Analytics Procurement Timeline:

1. Due diligence/drafting RFP August 2015 – July 20162. RFP issued August 20163. Responses from 8 vendors August 20164. Scoring of responses December 20165. Trials conducted of 3 applications January – March 2017 6. Recommendation at April CIM April 20177. Execution of contract/Implementation May – September 2017

50

Risk System Timeline

Prepared by the New York City Comptroller's Office Bureau of Asset Management