October 2017 CCP:HF/JU 17/CRS 1

E

COMMITTEE ON COMMODITY PROBLEMS

JOINT MEETING OF THE THIRTY-NINETH SESSION OF THE

INTERGOVERNMENTAL GROUP ON HARD FIBRES AND THE

FORTY-FIRST SESSION OF THE INTERGOVERNMENTAL GROUP

ON JUTE, KENAF AND ALLIED FIBRES

Tanga, Tanzania, 15 – 17 November 2017

CURRENT MARKET SITUATION AND MEDIUM TERM OUTLOOK

FOR JUTE AND KENAF; SISAL AND HENEQUEN; ABACA AND COIR

I. INTRODUCTION

1. This CRS1 document is composed by three main sections. Section II, “World production, trade

and prices”, provides an analysis of recent developments in the JACKS2 market. Section III, “Medium

term outlook to 2026”, prospects the JACKS markets in the medium term, and section III concludes.

2. The data used in the assessment of the current market situation, and for generating projections

to 2026, were compiled from responses to the Secretariat’s annual questionnaires on JACKS.

Delegates are invited to supplement information and provide insights on the trends pertaining to their

countries. Tables used in the Secretariat’s analysis are tabled in document CCP:HF/JU 17/CRS 2 for

perusal and correction by delegates.

II. WORLD PRODUCTION, TRADE AND PRICES

3. Global production of JACKS fibres increased by 17.9 percent to 4.67 million tonnes in 2016,

compared to output levels in 2015. Jute and kenaf accounted for the largest share of production,

followed by coir, sisal and similar fibres, such as henequen and fique, and abaca (Figure 1).

1 Conference room series. 2 Jute, abaca, coir, kenaf and sisal.

2 CCP:HF/JU 17/CRS 1

Figure 1 – World JACKS Production (thousand tonnes)

Source: FAO IGG/HFJU Secretariat.

A. JUTE AND KENAF PRODUCTION

4. Jute and kenaf production increased by 24.6 percent in 2016/17, reaching 3.31 million tonnes

compared to 2.66 million tonnes in the previous season. The highest increase in output was registered

in India at 41.5 percent, followed by Bangladesh with a 12.5 percent increase in production. This was

mainly due to the good weather conditions in these two major producing countries. Moreover, the

increased outputs in India can also be seen as a result of the significant support that the Government

has been giving to the sector and associated processing industry which has been supplemented by

investments from the private sector, including the Indian Jute Mills Association. (Figure 2).

Figure 2 – Jute and Kenaf Production (thousand tonnes)

Source: FAO IGG/HFJU Secretariat.

0500

100015002000250030003500400045005000

2010 2011 2012 2013 2014 2015 2016

Jute/Kenaf 3376 3410 3182 3097 2779 2657 3312

Coir (brown fibre) 798 798 833 816 903 946 1002

Sisal, Henequen & Fique 280 298 259 254 283 284 273

Abaca 70 86 78 67 77 78 87

0

500

1000

1500

2000

2500

3000

3500

2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17

Bangladesh India Rest of the World

CCP:HF/JU 17/CRS 1 3

B. JUTE PRICES

5. Since 2013, prices increased steadily until the first quarter of 2015, reaching USD 760 per

tonne in March 2015, after which prices declined, reaching a minimum of USD 660 per tonne in the

second quarter of 2015. During the 2015-2016 season, prices increased, reaching a maximum of USD

880 per tonne in March and May 2016. In the last quarter of 2016 prices declined sharply, reaching

USD 660 per tonne in October, remaining more or less constant. In June 2017 the price of jute was

marked at USD 670 per tonne, more or less reflecting the average price during the period 2012-2017

(Figure 3).

Figure 3 – Jute Export Prices (BTD f.o.b. Bangladesh Port)

Source: FAO IGG/HFJU Secretariat.

C. MARKET POSITION OF COMPETING SYNTHETICS

6. Generally, prices of polypropylene (the main synthetic petroleum-based fibre competing with

natural fibres in various applications) follow crude oil prices, although the extent of upward or

downward variation depends on competitive conditions in individual markets. For example, in markets

where polypropylene (PP) fabrics are in close competition with jute fabrics, upward movements in

crude oil prices tend to be absorbed with very little impact on the price of PP fibre applications.

7. Crude oil prices have continued to decrease since 2012. Between October 2014 and April

2016 prices of crude oil rapidly dropped to less than one-third compared to the 2011 levels (Figure 4).

Since then, prices have continued to increase steadily, moving from an average of USD 43.55 in 2016

to USD 51.64 in 2017. Under these circumstances, it would appear that the underlying trends in

competition between natural and synthetic fibres have resumed in favour of the former. The price

levels where competition takes place more closely – in the first stage of processing – reflect the true

economic costs of crude oil-based products.

200

300

400

500

600

700

800

900

1000

1100

2010 2011 2012 2013 2014 2015 2016 2017

USD / tonne

4 CCP:HF/JU 17/CRS 1

Figure 4 - Crude Oil Prices (Brent Blend, in USD/barrel)

Source: FAO IGG/HFJU Secretariat.

D. JUTE TRADE

8. World exports of jute goods declined by about 7.1 percent in 2016/17 compared to levels

attained in 2015/2016, while total exports of jute fibre increased by 8.3 percent compared to the

previous year (Figure 5). In fact, total exports of jute fibre presented a 5.9 percent growth p.a. over the

last two years. This is mainly due to exports from Bangladesh which increased, on average, by

14 percent p.a. in the last two seasons.

Figure 5 – Trend of Exports of Jute Goods and Fibre (thousands tonnes)

Source: FAO IGG/HFJU Secretariat.

9. Bangladesh dominates world exports of jute, accounting for approximately 87 percent of

world exports of raw jute and nearly 82 percent of jute goods in 2016/17 (Figure 6). India is also a

significant exporter of jute goods despite its vast domestic demand. In fact, during the last two and

half years, India’s jute goods exports declined by nearly 22 percent p.a., accounting for about 8

percent of global shipments – almost half when compared to 2013/14. Exports of jute goods by other

countries increased by 10.7 percent in 2016/17 compared to levels in 2015/16. Egypt, China, Pakistan

0

20

40

60

80

100

120

140

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

US

D/

barr

el

200

300

400

500

600

700

800

900

1000

1100

1200

1300

2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17

Jute Fibre

Jute Goods

CCP:HF/JU 17/CRS 1 5

and the Russian Federation registered a sharp increase in 2016/17, even if their export volumes were

not very significant.

Figure 6 – Exports of Jute Goods (thousand tonnes)

Source: FAO IGG/HFJU Secretariat.

10. Imports of jute fibre in 2016 increased by 10.8 percent from 2015, totaling 289 790 tonnes

(Figure 7). Global import data are reported on a calendar year basis, rather than on a crop year basis,

leading to differences with export levels owing to leads and lags. Asia accounted for 85 percent of jute

fibre imports, totaling 245 640 tonnes, with India now being the major importer, followed by Pakistan,

Nepal and China.

Figure 7 – Imports of Jute Fibre (thousand tonnes)

Source: FAO IGG/HFJU Secretariat.

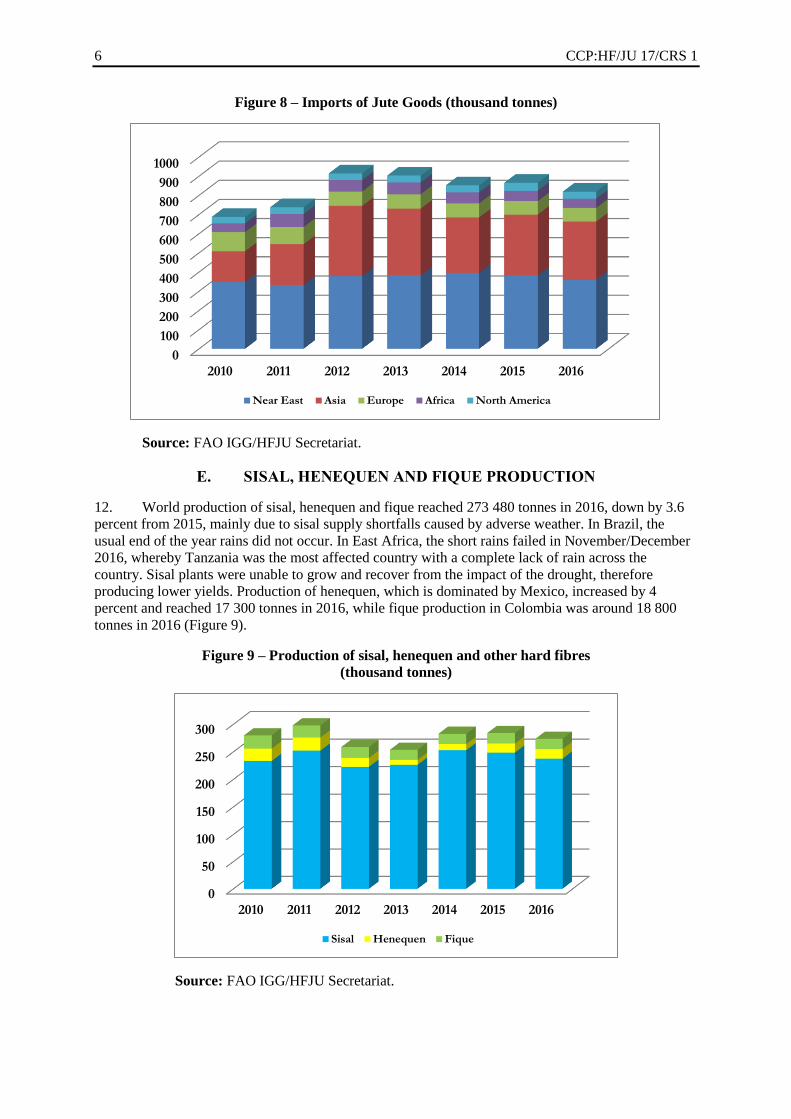

11. World imports of jute goods in 2016 accounted for 884 200 tonnes, reflecting a 17 percent

increase in comparison to 2010, and yet a decrease of 4.3 percent when compared to 2015 (Figure 8).

The Near East remained the largest importing region, with 41 percent of the world imports of jute

goods. Imports into Asia, the second largest importing region, maintained similar levels of 2015,

amounting to 34 percent. Other smaller markets for jute goods include the European Union (EU),

Africa and North America.

0

200

400

600

800

1000

1200

2010/11 2011/12 2012/13 2013/14 2014/15 2015/16 2016/17

Bangladesh India Other

0

100

200

300

400

500

600

2010 2011 2012 2013 2014 2015 2016

China (Mainland) India Nepal Pakistan Other

6 CCP:HF/JU 17/CRS 1

Figure 8 – Imports of Jute Goods (thousand tonnes)

Source: FAO IGG/HFJU Secretariat.

E. SISAL, HENEQUEN AND FIQUE PRODUCTION

12. World production of sisal, henequen and fique reached 273 480 tonnes in 2016, down by 3.6

percent from 2015, mainly due to sisal supply shortfalls caused by adverse weather. In Brazil, the

usual end of the year rains did not occur. In East Africa, the short rains failed in November/December

2016, whereby Tanzania was the most affected country with a complete lack of rain across the

country. Sisal plants were unable to grow and recover from the impact of the drought, therefore

producing lower yields. Production of henequen, which is dominated by Mexico, increased by 4

percent and reached 17 300 tonnes in 2016, while fique production in Colombia was around 18 800

tonnes in 2016 (Figure 9).

Figure 9 – Production of sisal, henequen and other hard fibres

(thousand tonnes)

Source: FAO IGG/HFJU Secretariat.

0

100

200

300

400

500

600

700

800

900

1000

2010 2011 2012 2013 2014 2015 2016

Near East Asia Europe Africa North America

0

50

100

150

200

250

300

2010 2011 2012 2013 2014 2015 2016

Sisal Henequen Fique

CCP:HF/JU 17/CRS 1 7

13. World production of sisal continues to be dominated by Brazil in 2016, accounting for 36

percent of the global total; followed by China (27 percent); Tanzania (15 percent); Kenya (10 percent);

Madagascar (3 percent); and other countries (9 percent). Sisal production in Brazil reached 84 650

tonnes in 2016, 8 percent lower than 2015. Similarly, output in Tanzania fell from 40 000 tonnes in

2015 to 36 750 tonnes in 2016. During the last three years, China has seen its production of sisal

stabilizing at 63 000 tonnes (Figure 10).

Figure 10 – Production of Sisal Fibre (thousand tonnes)

Source: FAO IGG/HFJU Secretariat.

F. SISAL PRICES

14. Price levels for the three main grades of sisal3 produced in East Africa and Brazil increased in

2015 and 2016 as supplies have not reached pre-Brazilian shortfall levels caused by the 2013/2014

severe drought in the sisal growing region of Bahia (Figure11). When expressed in US dollars, the

increase in the price of Brazilian sisal was moderated by the devaluation of the real. In any case, this

situation also put pressure on all African producers and on pricing of the East African sisal fibre. In

January 2016, East Africa prices reached a record high of USD 2 350 per tonne for 3L and USD 2 195

per tonne for UG. During 2015, Brazil had excellent weather conditions, receiving good rains;

therefore sisal production recovered, although well below the levels of the previous decade. Brazilian

sisal quality also increased significantly. The improved quantity and quality of Brazilian sisal resulted

in a dynamic price competition, reducing price levels and increasing the price differentials between

Bahia Type 3 DB and East Africa 3L and UG. This impacted negatively on African sisal during 2016.

In fact, during the second half of 2016, prices sharply declined – by about 11 and 13 percent for 3L

and UG, respectively, when compared to the first semester of 2016.

15. Towards the end of 2016, Africa and Brazil were affected by El Niño. In Brazil, the normal

end of the year rains did not occur. In East Africa, as previously mentioned, the short rains failed in

November/December 2016, and Tanzania registered a complete lack of rain across the country. In

addition, further pressure for fibre demand was registered as the agricultural twine season in North

America begins, and contracts for 2017/2018 are still being negotiated. Therefore, the price of Bahia

Type 3 DB increased by 8 percent in the first 6 months of 2017, reaching USD 1 600 per tonne. In

3 The three main grades of sisal are 3L and UG in East Africa and Bahia type 3 DB in Brazil.

0

50

100

150

200

250

300

2010 2011 2012 2013 2014 2015 2016

tho

usa

nd

to

nn

es

Brazil China Tanzania Kenya Madagascar Others

8 CCP:HF/JU 17/CRS 1

addition, in the first 6 months of 2017, the price of the African sisal fibre remained constant and

marked at USD 2 050 per tonne for 3L and USD 1 800 per tonne for UG.

Figure 11 - Sisal Price: East Africa (3L and UG) and Brazil (Bahia Type 3 DB)

(USD/tonne)

Source: FAO IGG/HFJU Secretariat.

G. SISAL TRADE

16. Total exports of sisal fibre reached 83.3 thousand tonnes in 2016, a 7.3 percent decrease from

2015, and total exports of sisal manufactures decrease by 8.7 percent reaching 60.7 thousand tonnes

(Figure12). While the major sisal producers in Africa, Brazil and Asia registered a double-digit

decrease in their exports of sisal manufactures, North America and Europe saw a significant increase

in their exports. Shipments of sisal manufactures from North America and Europe increased by 3.3

and 12.4 percent respectively in 2016 and now hold a share of 21 percent of this market.

Figure 12 – World Exports of Sisal Fibre and Manufactures (thousand tonnes)

Source: FAO IGG/HFJU Secretariat.

500

700

900

1100

1300

1500

1700

1900

2100

2300

2500

3L

Bahia Type 3 DB

UG

50

55

60

65

70

75

80

85

90

95

100

2010 2011 2012 2013 2014 2015 2016

Manufactures

Sisal Fibres

CCP:HF/JU 17/CRS 1 9

17. Tanzania, the third major exporter of sisal fibre, which holds a 20 percent share of total

exports, registered a 29.8 percent decrease in 2016. By contrast, both Brazil and Kenya saw a slight

increase in exports of sisal fibre, an increase of up to 0.2 and 1.0 percent respectively. Together, these

two countries contributed 70 percent of the world exports of sisal fibre (Figure 13).

Figure 13 – Exports of Sisal Fibre (thousand tonnes)

Source: FAO IGG/HFJU Secretariat.

18. World imports of sisal manufactures steadily declined to 58 030 tonnes in 2016, with the

United States of America (USA) remaining the largest importer, absorbing 39 percent of the total

imports, followed by the EU, with 23 percent. With the exception of the Near East, all areas of the

world registered a decline in their imports of sisal manufactures. This trend is led by North America,

with a decrease of 21.6 percent in 2016. The Near East registered an increase in imports of sisal

manufactures of about 15.3 percent, mainly led by the Saudi Arabia. However, the Near East market

represents only 5.3 percent of the total world imports of sisal manufactures (Figure 14).

Figure 14 – Imports of Sisal Manufactures (thousand tonnes)

Source: FAO IGG/HFJU Secretariat.

0

10

20

30

40

50

60

70

80

90

100

2010 2011 2012 2013 2014 2015 2016

Brazil Kenya Tanzania Madagascar Other

0

10

20

30

40

50

60

70

80

2010 2011 2012 2013 2014 2015 2016

World North America Europe Asia Africa Near East Latin America Other

10 CCP:HF/JU 17/CRS 1

H. ABACA PRODUCTION

19. Production of abaca fibre was about 86 770 tonnes in 2016, an 11 percent increase when

compared to the previous year. This was mainly driven by the full recovery of the Philippines abaca

industry and the significant 36.9 percent increase in the production of abaca in Ecuador, from 8 560

tonnes in 2015 to 11 710 tonnes in 2016 (Figure 15).

Figure 15 – Abaca Production (thousand tonnes)

Source: FAO IGG/HFJU Secretariat.

I. ABACA TRADE

20. Abaca fibre remains largely for domestic consumption in the Philippines, while Ecuador

exports the raw fibre produced. Exports of abaca fibre and manufactures declined significantly

between 2011 and 2013 reflecting the global weakening in demand but recovered since 2014. The

increase was particularly registered in the exports of abaca fibre, which presents an average of 24

percent p.a. increase for the last three years. Exports of abaca fibre reached about 28.6 thousand tonnes

in 2016, while exports of abaca manufactures totalled 33.8 thousand tonnes in 2016, with abaca pulp

accounting for 64 percent of total manufactures (Figure 16).

Figure 16 – World Exports of Abaca Fibre and Manufactures (thousand tonnes)

Source: FAO IGG/HFJU Secretariat.

0

20

40

60

80

100

2010 2011 2012 2013 2014 2015 2016

Ecuador Philippines Other

0

5

10

15

20

25

30

2010 2011 2012 2013 2014 2015 2016

Abaca Fibre Abaca Pulp Abaca Cordage, Twine, Ropes

CCP:HF/JU 17/CRS 1 11

J. ABACA PRICES

21. Abaca prices declined slightly in the first half of 2014, before increasing steadily again until

April 2017. Prices have remained stable since then for all types of abaca. The spread of prices between

abaca type JK and type G have narrowed, registering a 4.5 percent difference in 2017 compared to an

11.2 percent difference in 2014 (Figure 17).

Figure 17 – Philippines Abaca Prices (USD/bale)

Source: FAO IGG/HFJU Secretariat.

K. COIR PRODUCTION

22. Global production of brown coir fibre increased by 6 percent to reach 1 million tonnes in 2016

(Figure18). India accounted for more than 60 percent of the total. India also registered the highest

annual growth, which was about 16 percent p.a. during the last two years. India also produced an

estimated 85 thousand tonnes of white fibre and 70 thousand tonnes of curled fibre. By contrast, coir

production in Sri Lanka, Vietnam and Thailand decreased in 2017.

Figure 18 – Coir Fibre (Brown) Production (thousand tonnes)

Source: FAO IGG/HFJU Secretariat.

100

130

160

190

220

250

280

310

340

2010 2011 2012 2013 2014 2015 2016 2017

S2

JK

G

0

200

400

600

800

1000

2010 2011 2012 2013 2014 2015 2016India (brown fibre ) Sri Lanka VietNam Thailand

12 CCP:HF/JU 17/CRS 1

L. COIR PRICES

23. Coir prices continue presenting mixed trends. Since 2014, twine prices show high price

volatility, increasing 59 percent in 2015, when compared to the previous year, and staying more or less

at the same level in 2016, i.e. at USD 1 115 per tonne. Yarn prices rose too, but more steadily,

increasing by 7 percent in 2016. Mattress, bristle and twisted fibre prices remained relatively stable

since 2013 (Figure 19).

Figure 19. Sri Lanka Export Prices of Coir Fibre and Manufactures

(USD/tonne)

Source: FAO IGG/HFJU Secretariat.

M. Coir Trade

24. Exports of coir fibre continued showing a pronounced upward trend in the last years, with an

average increase of 9 percent p.a. in 2015 and in 2016, reaching nearly 1.1 million tonnes. This

corresponds to an 80 percent increase with respect to the total fibre exports in 2010 (Figure 20). India

leads the contribution to this growth.

Figure 20 – Exports of Coir Fibre (thousand tonnes)

Source: FAO IGG/HFJU Secretariat.

200

350

500

650

800

950

1100

2010 2011 2012 2013 2014 2015 2016

(Mattress, Bristle and Twisted Fibre) Yarn Twine

0

200

400

600

800

1000

1200

2010 2011 2012 2013 2014 2015 2016India Sri Lanka VietNam Others

CCP:HF/JU 17/CRS 1 13

III. MEDIUM TERM OUTLOOK TO 2026

A. METHODOLOGY

25. A multi-country partial equilibrium model of raw and fibre good markets has been constructed

and used as a basis for projections. The model represents economic fundamentals where supply is

projected on the basis of area and yield for each crop, driven by prices, costs and improving

technology/management. An exception is the case of coir, which is modelled as a by-product of

coconut production. The fibre equivalent demand for various fibre goods is driven by incomes,

population and prices of competing fibres, and, in particular, cotton and other synthetic fibres.

Production and final demand for fibre goods affect domestic and international raw fibre markets.

Trade in both raw and fibre goods is driven by country prices and tariffs. While the model serves as a

basis for projection, expert assessment and judgement must be applied in a consensus building process

that incorporates diverse views of factors that are impacting the sector. The draft model of projections

described below have been adjusted by the judgement of FAO experts and, where available, by

industry and government experts. The economic and technological environment surrounding the

preparation of this outlook follows closely that described in the OECD-FAO Agricultural Outlook

2017-26, as well as common methodologies and assumptions used in the projection process.

B. BACKGROUND

26. The medium term outlook for JACKS prospects to 2026 is driven by complex forces. On the

supply side, the per hectare returns of most competitive crops has fallen significantly in recent years.

Inputs costs sensitive to crude oil prices, such as fertilizer or transportation, have also fallen. On

balance, these support the resurgence of the supply of natural fibres. However, on the demand side,

lower oil prices have also caused competitive prices for non-natural or synthetic fibres to fall.

Potentially, these forces lead to higher supplies of fibres, but at lower prices.

27. Measured at international reference prices, the world production value of jute, sisal, coir and

abaca accounted for USD 2.3 billion, 0.3 billion, 0.4 billion and 0.023 billion in 2016 – a total of over

USD 3 billion which accrues to many smallholder farmers, especially in India, Bangladesh, Sri Lanka,

China, Brazil, Tanzania and Kenya4. Value-added products derived from these raw fibres also provide

an important source of income, and revenues from exports contribute favourably to the trade accounts

of these countries.

28. In the decade prior to the reference period, 2014-16, global raw fibre production fared better

than was earlier projected by FAO studies. Reasons for this include stronger growth in supplying

countries, price competitiveness relative to synthetic fibres as well as a promisingly higher demand in

niche markets for natural fibres. Projections forward from the period 2014-16 – the reference base for

the projections – are hampered by considerable variability that has resulted from changes in markets

due to variations of demand and supply conditions where fibre markets appear to have been in some

disequilibrium. Medium term projections are difficult to make from such a variable base, and also

exhibit less variability since normal weather is assumed for each year of the projection.

C. JUTE OUTLOOK

Jute Production

29. During the decade prior to 2016, global jute production increased at a compound average rate

of 0.1 percent, to a level of 2 916 thousand tonnes (Figure 21). Bangladesh surpassed India as the top

global producer, growing at a rate of 2.4 percent annually. Jute production in India declined by 1.3

4 Reference prices used are: for jute – Bangladesh export price; for sisal – Brazil No. 3; for coir – Sri Lanka

bristle fibre; for abaca – Philippines Grade G.

14 CCP:HF/JU 17/CRS 1

percent annually over the period, mainly due to significantly lower production in 2014 and 2015,

before recovering in 2016. Bangladesh is now projected to retain its position as the top producer over

the next decade, while some recovery is expected in India. Global jute production is projected to

advance at a rate of 1.5 percent annually to a level of 3 410 thousand tonnes by 2026. Growth in jute

production is projected to be broadly based, with growth in Africa at 3.3 percent, Asia at 1.8 percent,

and a recovery in Latin America and the Caribbean at 1.1 percent annually. Recovering production is

largely due to relatively higher returns for jute compared to other competing crops, which had taken

precedence in the run up of global prices in the previous decade.

Jute Trade

30. World exports of jute declined significantly to 253 thousand tonnes in 2014-16, from 435

thousand tonnes in 2004-06, largely reflecting declining exports from Bangladesh, which is by far (94

percent share) the world’s top exporter of raw jute fibre (Figure 21). The decline in raw jute exports

from Bangladesh is entirely due to a rapidly increasing processing sector, which grew during the last

decade at a compound rate of 6 percent annually. In contrast, India’s exports grew in the last decade as

its processing sector contracted in the face of growing competition from Bangladesh. On the import

side, the fall in supply was largely absorbed by Pakistan and China, whose imports fell by more than

half during the decade, while imports into developed countries rose marginally.

Global trade in jute fibre is projected to rebound over the next decade, but not to attain historical

levels. Global exports may reach 323 thousand tonnes by 2026, or about 9 percent of global

production, which is down considerably from its proportion of 10 years ago. Bangladesh, which

contributes 94 of all exports, will increase exports as its jute production will outpace growth in its

processing sector. Additional fibre exports are expected to be absorbed by India and Pakistan.

Figure 21 – Jute Production and Trade to 2026 (thousand tonnes)

Source: FAO IGG/HFJU Secretariat.

D. SISAL OUTLOOK

Sisal Production

31. World sisal production is projected to grow annually by 0.9 percent to 273 thousand tonnes by

2026, after having declined by 0.6 percent annually during the last decade, primarily due to a

significant fall in production in Brazil (Figure 22). Growth in production is anticipated to continue in

0

500

1000

1500

2000

2500

3000

3500

4000

2000 2005 2010 2015 2020 2025

Production Exports Fibre

CCP:HF/JU 17/CRS 1 15

key countries of Africa, namely Tanzania, Kenya and Madagascar, which may grow by 2.5 percent,

1.1 percent and 3.6 percent respectively. Collectively, the production share of African countries is

anticipated to rise to 35 percent by 2026, an increase of 5 percent. Growth is also anticipated to

continue in China, the world’s second largest sisal producer, although at a reduced pace from the

previous decade. A key uncertainty is the prospect for Brazil, and while it is expected to maintain its

dominance as the largest producer, its market share in total production may fall to levels as low as 32

percent, down from 44 percent in 2010.

Sisal Trade

32. Global trade in sisal is anticipated to remain stagnant over the medium term, with exports at

about 91 thousand tonnes in 2026. The share of exports by African countries will rise considerably to

61 percent by 2026, while that of Brazil continues to fall to about 32 percent. The share of sisal

imports by both China and the EU is projected to fall, as rising import demand in countries such as

Morocco, Saudi Arabia and Algeria take a higher share of trade.

Figure 21 – Sisal Production and Trade to 2026 (thousand tonnes)

Source: FAO IGG/HFJU Secretariat.

E. ABACA OUTLOOK

Abaca production and trade

33. Global production of abaca continued its progressive decline during the last decade, to an

average of 81 thousand tonnes over the 2014-16 period (Figure 22). Growth by the major producers –

the Philippines and Ecuador – has recently taken hold, and the question is whether this growth will be

sustained by growing demand over the medium term. Global production is anticipated to grow slowly

to 84 thousand tonnes by 2026, with Ecuador capturing an increasing market share of production.

With rising production, abaca fibre trade will rebound somewhat from the low average of recent years,

and exports may reach 29 thousand tonnes by 2026, up from 25 thousand tonnes in the 2014-16 base

period. Ecuador, which exports all its raw fiber mainly to the EU, will see its export share rise toward

50 percent, as that of the Philippines falls to 37 percent.

F. COIR OUTLOOK

Coir Production

34. Global coir production remains the fastest growing fibre of the JACKS, having increased at a

compound annual rate of over 5 percent p.a. in the last decade, led by similar growth in India, the

largest producer with a 67 percent global share. Strong growth was also registered by virtually all

0

50

100

150

200

250

300

350

2000 2005 2010 2015 2020 2025

Production Exports Fibre

16 CCP:HF/JU 17/CRS 1

Asian producing countries, with very strong growth in some such as Vietnam and Sri Lanka (6 percent

p.a.), Indonesia (28 percent p.a.) and Thailand (5 percent p.a.). Global coir production is projected to

slow considerably, averaging 2 percent p.a. over the next decade and reaching 1 350 thousand tonnes

(Figure 22). The basis for expected slower growth is the considerably higher base volume which the

industry has attained in major markets, declining market prices under higher supplies and the slow to

declining growth of the coconut sector which provides fibre feedstock. However, considerable supply

capacity still exists, and growth could be higher than projected.

Figure 22 – Abaca Production and Trade to 2026

Source: FAO IGG/HFJU Secretariat.

Coir Trade

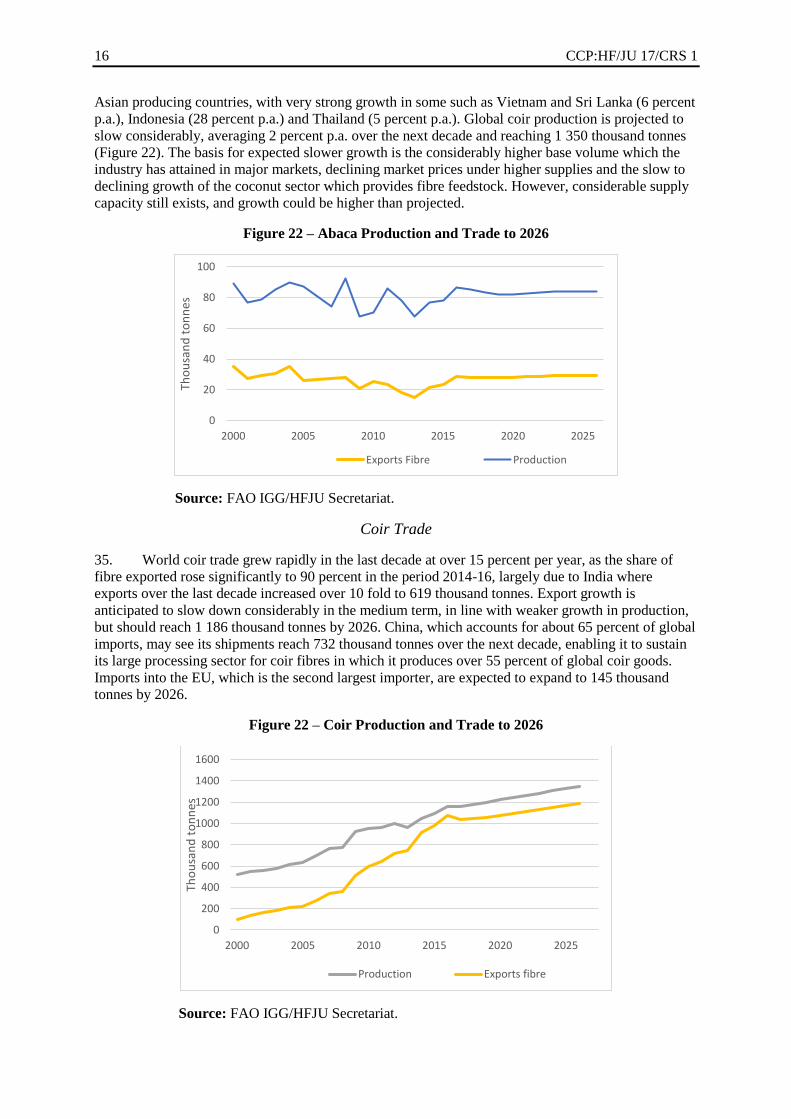

35. World coir trade grew rapidly in the last decade at over 15 percent per year, as the share of

fibre exported rose significantly to 90 percent in the period 2014-16, largely due to India where

exports over the last decade increased over 10 fold to 619 thousand tonnes. Export growth is

anticipated to slow down considerably in the medium term, in line with weaker growth in production,

but should reach 1 186 thousand tonnes by 2026. China, which accounts for about 65 percent of global

imports, may see its shipments reach 732 thousand tonnes over the next decade, enabling it to sustain

its large processing sector for coir fibres in which it produces over 55 percent of global coir goods.

Imports into the EU, which is the second largest importer, are expected to expand to 145 thousand

tonnes by 2026.

Figure 22 – Coir Production and Trade to 2026

Source: FAO IGG/HFJU Secretariat.

0

20

40

60

80

100

2000 2005 2010 2015 2020 2025

Tho

usa

nd

to

nn

es

Exports Fibre Production

0

200

400

600

800

1000

1200

1400

1600

2000 2005 2010 2015 2020 2025

Tho

usa

nd

to

nn

es

Production Exports fibre

CCP:HF/JU 17/CRS 1 17

IV. CONCLUDING REMARKS

36. The medium term prospects for the JACKS sector are conditioned by the macroeconomic and

broader agricultural environment surrounding them. Prospects for economic growth in most

developing and developed countries appear moderately strong, compared to historical rates, with an

important exception of China, where growth is slowing. Energy prices and those for associated by-

products are relatively low, but are expected to rise moderately. Most global agricultural crop prices

are anticipated to remain lower in real terms compared to past peaks, but to rise marginally in nominal

terms over the decade. The main implication for this setting is for low energy related input costs and

synthetic fibre prices, and some incentives to increase production where fibre crops compete for land

resources with other crops. While economic growth will encourage higher demand for all fibres,

competition from synthetic fibres, given their lower prices, may be stronger in the next decade than in

the past one. A key question is the extent to which this competition matters, in the context of the

changing demand for natural fibres. While transport costs for raw fibre have been reduced with lower

energy costs, labour costs have continued to escalate in key countries such as India, China and Brazil.

Such changes encourage the diversification of trade patterns for raw and processed products toward

lower cost countries, and for sisal in particular, these include a number of key African suppliers such

as Tanzania, Kenya and Madagascar.

37. Global jute and hard fibre production has grown at about 0.8 percent annually in the last

decade, and is projected to increase slightly in the next decade, at 0.9 percent p.a. This growth is

largely due to increases in coir production, particularly in China. These trends mask the actual

variability of annual production, which will remain an important feature of the sector in the years to

come. The supply of fibres is increasingly concentrated in a few developing countries, particularly

those in South and Southeast Asia. For jute, India and Bangladesh will remain the dominant suppliers

with a 96 percent production share that should persist over the next decade. For sisal, the production

share is somewhat more disperse, but nevertheless the top 5 suppliers (Brazil, China, Tanzania, Kenya

and Haiti) will continue to provide over 90 percent of production, but Brazil’s share is projected to fall

in comparison to that of China, Tanzania and Kenya. For abaca, the Philippines is anticipated to retain

its dominant share, while Ecuador’s share is expected to rise from 14 percent in 2016 to 23 percent by

2026. For coir, the major 5 producers (India, Vietnam, Sri Lanka, Thailand and Indonesia) will

continue to supply about 96 percent of production, with India’s share continuing to dominate at over

60 percent. Given the concentrated structure of raw fibre supply, exchange rate movements may play

an important role in profitability, particularly in key suppling countries such as India (jute and coir),

Bangladesh (jute), Brazil (sisal) and the Philippines (abaca). Exchange rates and domestic inflation

will also play an important role in fibre goods production and trade as they affect competitiveness

among suppliers, as well as import demand by processors.