1

alw

ays c

lose

Tebodin

Tebodin Ukraine CFI

Moskovsky Avenue 16b, floor 4

04073 Kiev

Ukraine

Author: Andriy Balanyuk

- Telephone: +38044812121

- E-mail: [email protected]

August 28, 2015

Order number: 71994

Document number: DR-001

Revision: C

Climate Technologies in Ukraine. Market Penetration Study.

Client: European Bank for Reconstruction and Development

Project: FINTECC Ukraine. Market Penetration Study

2

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 2 / 109

C 28-08-2015

Market Penetration Study Report

Consultants:

O. Cherinko

M. Donkelaar

M. Pribylova

A. Balanyuk

F. Akhmetshyn

P. Rosen

A. Bilan

A. Nikitin, Director B 22-06-2015

A 27-04-2015

Rev. Date Description Author Checked by

© Copyright Tebodin, 2015

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means without

permission of the publisher.

3

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 3 / 109

Table of contents

List of abbreviations 5 Executive Summary 6 1 Introduction and purpose statement 14 2 Methodological note for climate technologies market penetration assessment in Ukraine 16 2.1 Kick-off activities 16 2.2 Available methodological market penetration evaluation techniques and market information 17 2.3 Defining Market Sectors and Sub-Sectors 17 2.4 Climate technologies definition 18 2.5 Best Available Techniques (BAT) in Europe 18 2.6 Current standards in Ukraine 19 2.7 Market penetration analysis in Europe and in Ukraine for the selected climate technologies 20 3 Technology area prioritization 24 3.1 Cogeneration 24 3.1.1 Gas Turbines 26 3.1.2 Gas-fired reciprocating installations 26 3.1.3 Back Pressure Steam Turbines 28 3.1.4 Organic Rankine Cycle 28 3.1.5 Steam Turbine Design Characteristics 29 3.1.6 Steam turbines applications 30 3.2 Heat Recovery 34 3.3 Energy Management 37 3.4 Water Management Systems 39 3.5 Air Cooling Systems 39 4 Current standards in EU 40 4.1 EU Best Available Techniques Reference Documents 40 4.2 EU BATs in Agro industrial sector 41 4.2.1 Cogeneration 41 4.2.2 Heat recovery 42 4.2.3 Energy Management systems, automation and practices 43 4.2.4 Water management systems 44 4.2.5 Air cooling systems (air cooled condensers) 47 4.2.6 Other technologies 47 4.3 EU BATs in Industry 48 4.3.1 Cogeneration 48 4.3.2 Heat recovery 49 4.3.3 Energy Management systems, automation and practices 53 4.3.4 Water management systems: 54 4.3.5 Air cooling systems (air cooled condensers) 56 4.3.6 Other technologies 56 4.4 Examples of BAT Cases in EU (Czech Republic as a reference country) 66 4.4.1 Cogeneration 66 4.4.1.1 Gas-fired (reciprocated) engines 66 4.4.1.2 Steam turbines 68 4.4.1.3 Organic Rankine Cycle (ORC) 71 4.4.2 Heat recovery systems 75 4.4.3 Energy Management Systems, automation and practices 77 4.4.4 Water Management Systems 81 4.4.5 Air cooling systems (air cooled condensers) 85 5 Current standards in Ukraine 86

4

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 4 / 109

5.1 Cogeneration 88 5.2 Heat recovery systems 93 5.3 Energy Management Systems, automation and practicies 94 5.4 Water management systems 95 5.5 Air cooling systems (air cooled condencers) 95 5.6 Identified barriers to climate technology transfer in Ukraine 95 6 Ukraine’s market potential and penetration 99 6.1 Cogeneration market potential and penetration 99 6.2 Heat recovery systems 101 6.3 Energy Management Systems, automation and practicies 101 6.4 Water management systems 105 6.5 Air cooling systems (air cooled condencers) 106 6.6 Summary of penetration and investment potential 108

Attachments

Attachment 1. Climate Technologies EU BATs, penetration and players - Agroindustry

Attachment 2. Descriptions BATs Agroindustry EU

Attachment 3. Climate Technologies EU BATs, penetration and players - Industry

Attachment 4. Descriptions BATs Industry EU

5

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 5 / 109

List of abbreviations

AMS Automated Metering Systems (Automated System for Commercial Accounting of Power Consumption

(ASCAPC)/Automated System of Electric Power Technical Record-Keeping (ASEPTRK)/Automated

Measuring and Information System for Electric Power Fiscal Accounting (AMIS EPFA))

BAT Best Available Technologies

BAU Biomass Association of Ukraine

BREF Best Available Technology Reference Document

CHP Combined Heat and Power

CT Climate Technology

CZK Czech crown (as of 27.08.2015 1 EUR = 27.1 CZK)

EBRD European Bank for Reconstruction and Development

EPWM Electric Power Wholesale Market (Ukraine)

FAO Food and Agriculture Organization of the United Nations

FDI Foreign Direct Investment

FINTECC Finance and Technology Transfer Centre for Climate Change (Programme by EBRD)

GDP Gross Domestic Product

GHG Greenhouse gas

GUE Guidelines for Use of Electricity

HDI Human Development Index

IEA International Energy Agency

IFC International Finance Corporation

LDCPE Local Data Collecting and Processing Equipment

Mt Metric ton

NERC National Energy and Utilities Regulatory Commission (Ukraine)

NG Natural Gas

NREAP National Renewable Energy Action Plan (Ukraine)

ORC Organic Rankine Cycle

PHP Power and Heat Plant

PBP Payback period

WB World Bank

WHRB Waste Heat Recovery Boiler

6

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 6 / 109

Executive Summary

The market penetration analysis is done with aim to gather market evidence of the market penetration of selected basket of

climate technologies in Ukraine through utilizing data from available studies, Consultant’s expertise and market intelligence

from market players such as technology suppliers.

Climate Technologies assessed

Climate technologies (CT) – subject to Market Penetration Study are defined as innovative, low penetrated in Ukrainian

market energy and resource efficiency technologies and practices contributing to reduction of CO2 emissions with big

potential of replication in selected sectors of industry and agroindustry.

The technologies that were prioritized for assessment based on the EBRD/Donor investment priorities and envisaged

EBRD pipeline are presented per the following groups (for details see Chapter 3 of this Report):

1. Co-generation:

Gas engine CHP < 2 MW (piston)

Gas engine CHP > 2 MW < 6 MW (piston)

Organic Rankine Cycle (ORC)

Steam turbine CHP > 2 MW < 6 MW:

Pass-out steam turbine CHP

Back pressure steam turbine CHP

2. Heat recovery:

Low- and Med-temperature (<650ºC)

High-temperature (>650ºC)

3. Management systems, automation and practices

Energy management systems

Advanced automation in drying

4. Water management systems:

Waste water treatment

Reduction of water consumption

5. Air cooling systems (air cooled condensers)

6. Other energy savings technologies and techniques

Market (sub) sectors

Based on the priorities of the EBRD the assignment was focused on the following economic sectors:

Agri-business (including agro and food processing);

Manufacturing and processing industry.

Considering EBRD priorities and anticipated pipeline of projects and importance of subsectors in Ukraine based on brief

market insight (including contribution in terms of resource consumption and CO2 emissions), the following sub-sectors were

defined for the purposes of the Market Penetration Study (given in alphabetical order):

Agroindustry:

Beverages;

Bakeries;

Fat production & oil extraction;

Fruit and vegetable processing

Milk processing;

Sugar mills.

7

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 7 / 109

Industry:

Building materials (cement and dry mixtures, glass, bricks, etc.);

Chemicals (organic and inorganic chemical industry, production of fertilizers, by-product coke industry,

organic synthesis, etc.);

Oil refineries;

Pharmaceuticals;

Plastics and polymers;

Pulp & Paper;

Steel and metals, ferrous and nonferrous metal processing;

Wood working and processing.

In terms of end-users only large and mid-size businesses were considered as target group.

Methodology applied

For selected technology areas the Consultant provided details of a typical technical specification employed in EU and

especially in the benchmark country (Czech Republic, Chapter 4) and Ukraine (Chapter 5) with sector specifics highlights.

For the selected technologies the Best Available Techniques (BAT) Reference Documents (BREFs) of relevant

technologies were studied. In addition, the Consultant prepared a brief BAT technical specification for each of the selected

technologies including functionalities, energy efficiency performance and CO2 reductions benchmarks as well as typical

capital investment outlay required for implementation of the technology together with indicative simple payback.

In this study the main method of market penetration assessment in EU was secondary market research which was to use

data from open sources.

As for Ukraine, in open sources there is a large amount of information about cogeneration, while for the majority of other

technologies assessed the information is scarce. Thus, in parallel to secondary market research, various interviews with

technology providers and suppliers, industry experts and end-users were conducted by the Consultant. The information

was obtained in the form of completed questionnaires, as well as answers on unstructured, open-ended questions.

In order to assess the level of the technology penetration on the EU market, the following levels of application are

determined for each of the proposed technology:

1- ‘introduction of new technology’;

2- ‘increased acceptance of new technology’;

3- ‘growing importance and application of technology’;

4- ‘fully mature technology’

Such classification was done for the purposes of further comparison of penetration level in EU and Ukraine markets.

Considering the potential application of the selected technologies in Ukrainian market, majority of the presented

technologies are classified in the level 3 or 4 on the EU market. Only several highly perspective technologies with

significant energy efficiency and CO2 reduction potential are in the level 1 and 2.

Market penetration in Ukraine was calculated per group of technology and sectors as the ratio of applied cases to the

potential applications based on assumptions of number of sector average end-users that could potentially apply the

technology. Wherever possible the Consultant commented types of the companies identified tend to be faster in

implementation of BAT technologies and type of financing utilized for these technologies.

Based on the inputs of the tasks described above the Consultant further quantified the implementation potential of selected

climate technologies across selected agroindustry and industry sectors in Ukraine (Chapter 6) and presented results by

each sector as well as an aggregated total.

8

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 8 / 109

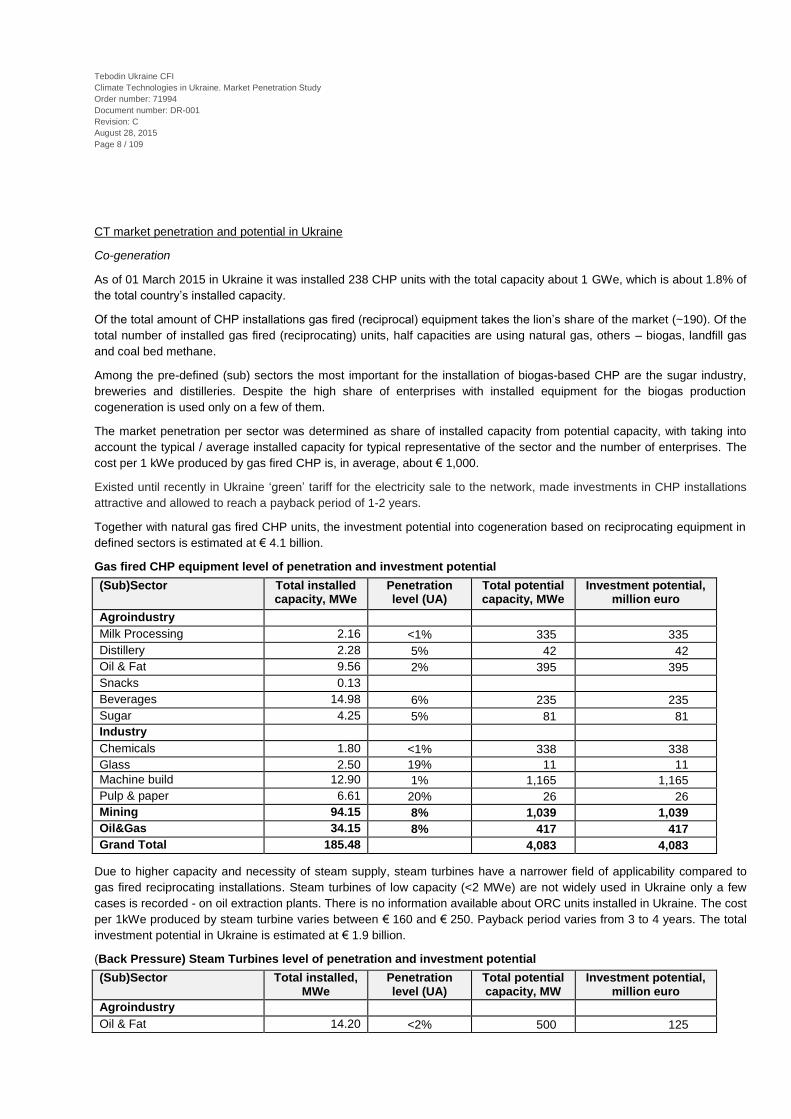

CT market penetration and potential in Ukraine

Co-generation

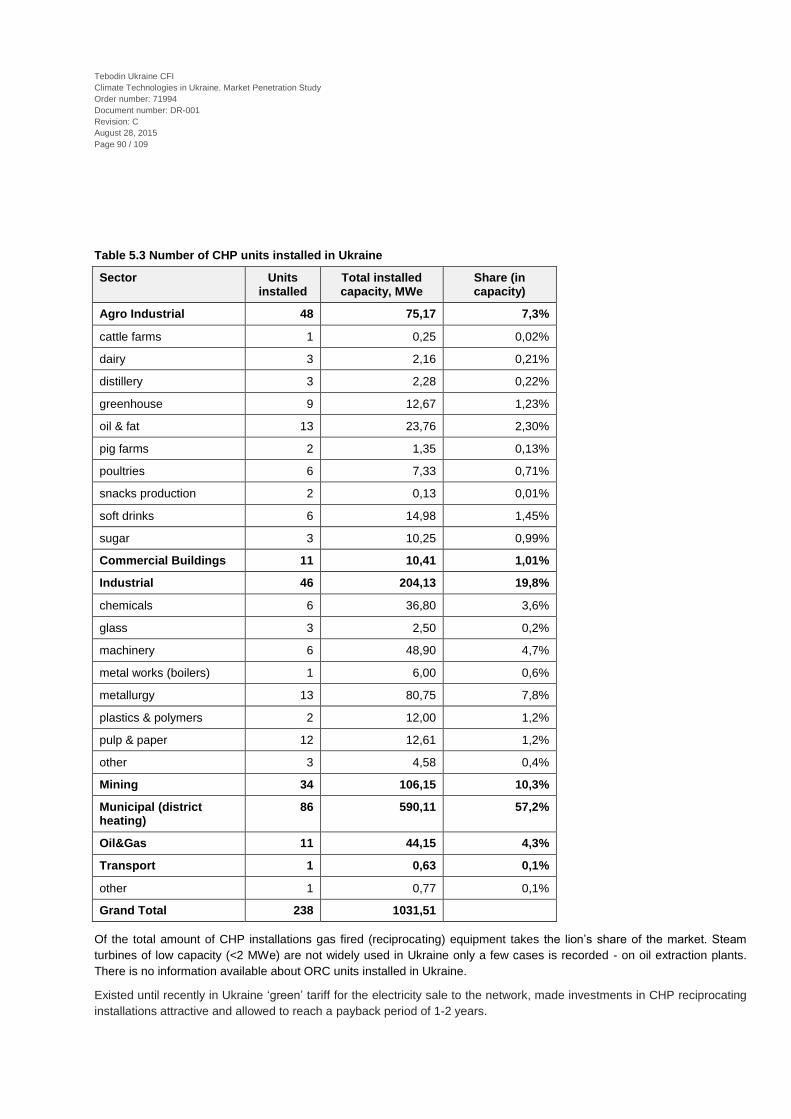

As of 01 March 2015 in Ukraine it was installed 238 CHP units with the total capacity about 1 GWe, which is about 1.8% of

the total country’s installed capacity.

Of the total amount of CHP installations gas fired (reciprocal) equipment takes the lion’s share of the market (~190). Of the

total number of installed gas fired (reciprocating) units, half capacities are using natural gas, others – biogas, landfill gas

and coal bed methane.

Among the pre-defined (sub) sectors the most important for the installation of biogas-based CHP are the sugar industry,

breweries and distilleries. Despite the high share of enterprises with installed equipment for the biogas production

cogeneration is used only on a few of them.

The market penetration per sector was determined as share of installed capacity from potential capacity, with taking into

account the typical / average installed capacity for typical representative of the sector and the number of enterprises. The

cost per 1 kWe produced by gas fired CHP is, in average, about € 1,000.

Existed until recently in Ukraine ‘green’ tariff for the electricity sale to the network, made investments in CHP installations

attractive and allowed to reach a payback period of 1-2 years.

Together with natural gas fired CHP units, the investment potential into cogeneration based on reciprocating equipment in

defined sectors is estimated at € 4.1 billion.

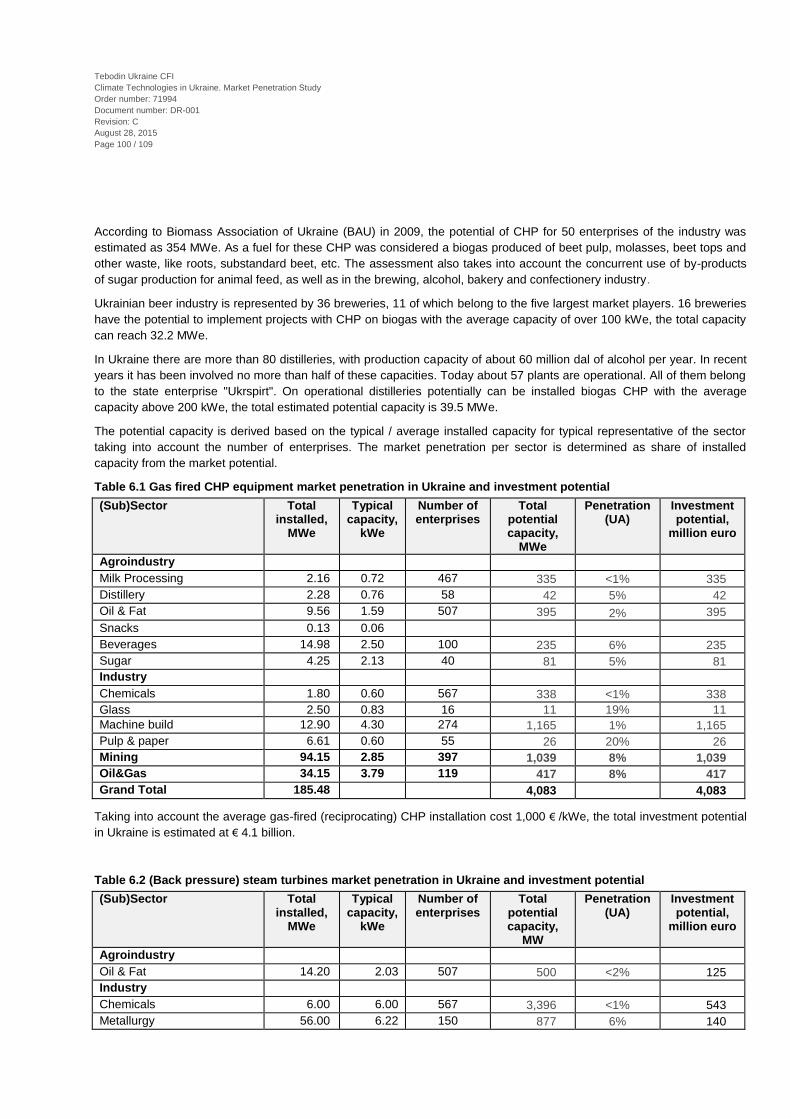

Gas fired CHP equipment level of penetration and investment potential

(Sub)Sector Total installed capacity, MWe

Penetration level (UA)

Total potential capacity, MWe

Investment potential, million euro

Agroindustry

Milk Processing 2.16 <1% 335 335

Distillery 2.28 5% 42 42

Oil & Fat 9.56 2% 395 395

Snacks 0.13

Beverages 14.98 6% 235 235

Sugar 4.25 5% 81 81

Industry

Chemicals 1.80 <1% 338 338

Glass 2.50 19% 11 11

Machine build 12.90 1% 1,165 1,165

Pulp & paper 6.61 20% 26 26

Mining 94.15 8% 1,039 1,039

Oil&Gas 34.15 8% 417 417

Grand Total 185.48 4,083 4,083

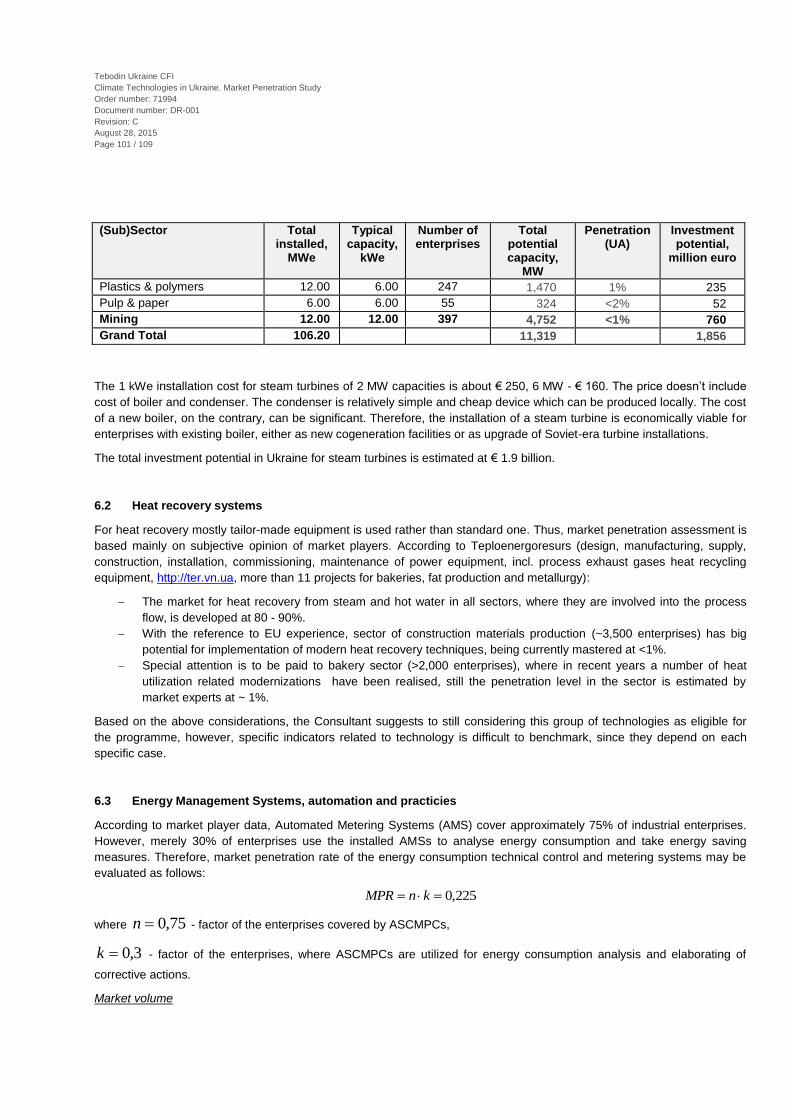

Due to higher capacity and necessity of steam supply, steam turbines have a narrower field of applicability compared to

gas fired reciprocating installations. Steam turbines of low capacity (<2 MWe) are not widely used in Ukraine only a few

cases is recorded - on oil extraction plants. There is no information available about ORC units installed in Ukraine. The cost

per 1kWe produced by steam turbine varies between € 160 and € 250. Payback period varies from 3 to 4 years. The total

investment potential in Ukraine is estimated at € 1.9 billion.

(Back Pressure) Steam Turbines level of penetration and investment potential

(Sub)Sector Total installed, MWe

Penetration level (UA)

Total potential capacity, MW

Investment potential, million euro

Agroindustry

Oil & Fat 14.20 <2% 500 125

9

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 9 / 109

(Sub)Sector Total installed, MWe

Penetration level (UA)

Total potential capacity, MW

Investment potential, million euro

Industry

Chemicals 6.00 <1% 3,396 543

Metallurgy 56.00 6% 877 140

Plastics & polymers 12.00 1% 1,470 235

Pulp & paper 6.00 <2% 324 52

Mining 12.00 <1% 4,752 760

Grand Total 106.20 11,319 1,856

For Heat Recovery mostly tailor-made equipment is used rather than standard one.

In general, it cannot be said that the individual projects on waste heat recovery are always comparable, so the total amount

of heat recovery installation in Ukraine is difficult to estimate. The differences are mainly in the layout configuration of

source, consumption and method of implementation. So market penetration estimation is based mainly on subjective

opinion of market players.

Due to differences in heat recuperation techniques (“flue gas / water”, “flue gas / steam”, “flue gas / air”), the unification

issue is a problem which is difficult to resolve.

Specific investments and payback period is estimated by market players as:

Technology Investments, € / kW PBP, years

flue gas / water 250 - 340 0.3- 0.6

flue gas / steam 350 - 540 0.9- 1.9

flue gas / air 300 - 420 0.8- 1.8

disposal systems with source temperature 60 -: - 70 ° C 850 – 1,230 1.3 - 3.6

The main (sub)-sectors of new technologies applications in Ukraine so far were:

Metallurgy (metallurgical furnaces)

Cement industry (clinker kilns)

By estimation of market players, the market for heat recovery from steam and hot water in all sectors, where they are

involved into the process flow, is developed at 83 - 91%.

With the reference to EU experience, sector of construction materials production (~3,500 enterprises) has big potential for

implementation of modern heat recovery techniques, being currently mastered at 0-1%.

Special attention is to be paid to bakery sector (>2,000 enterprises), where in recent years a number of heat utilization

related modernizations have been realized, still the penetration level in the sector is estimated by market experts at 1.0-

1.5%.

Consultant suggests to still considering this group of technologies as eligible for the program, however, specific indicators

related to technology is difficult to benchmark, since they depend on each specific case.

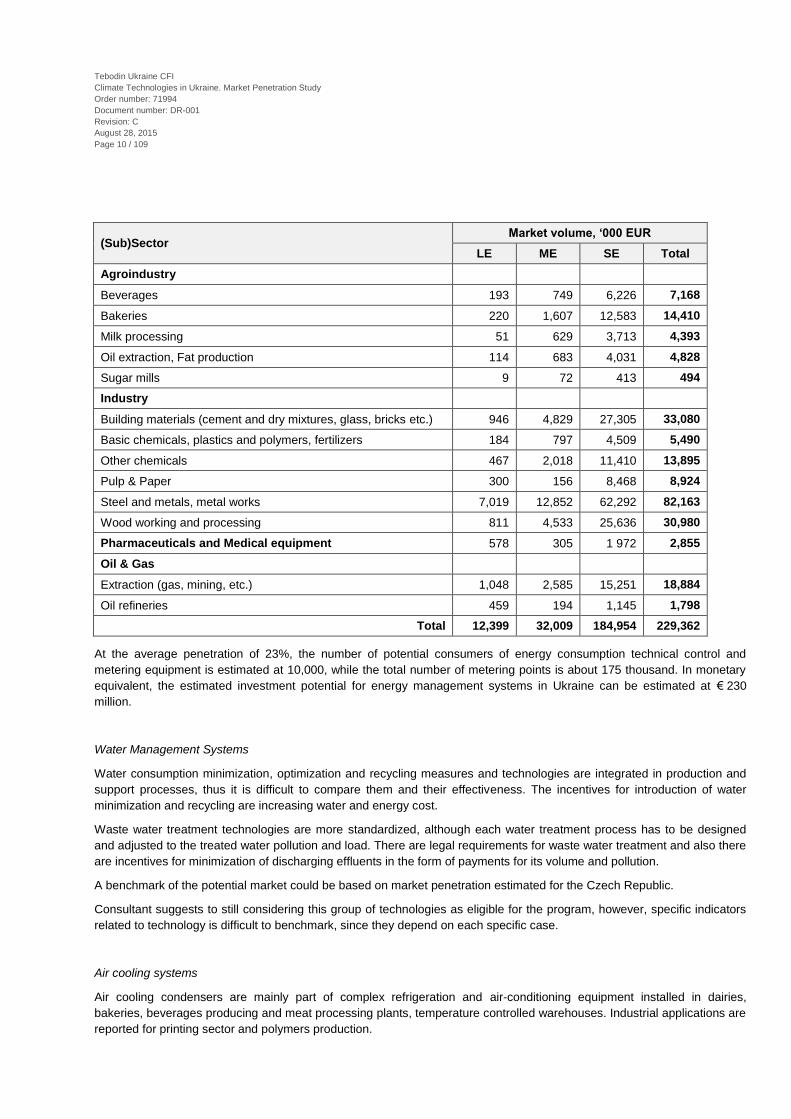

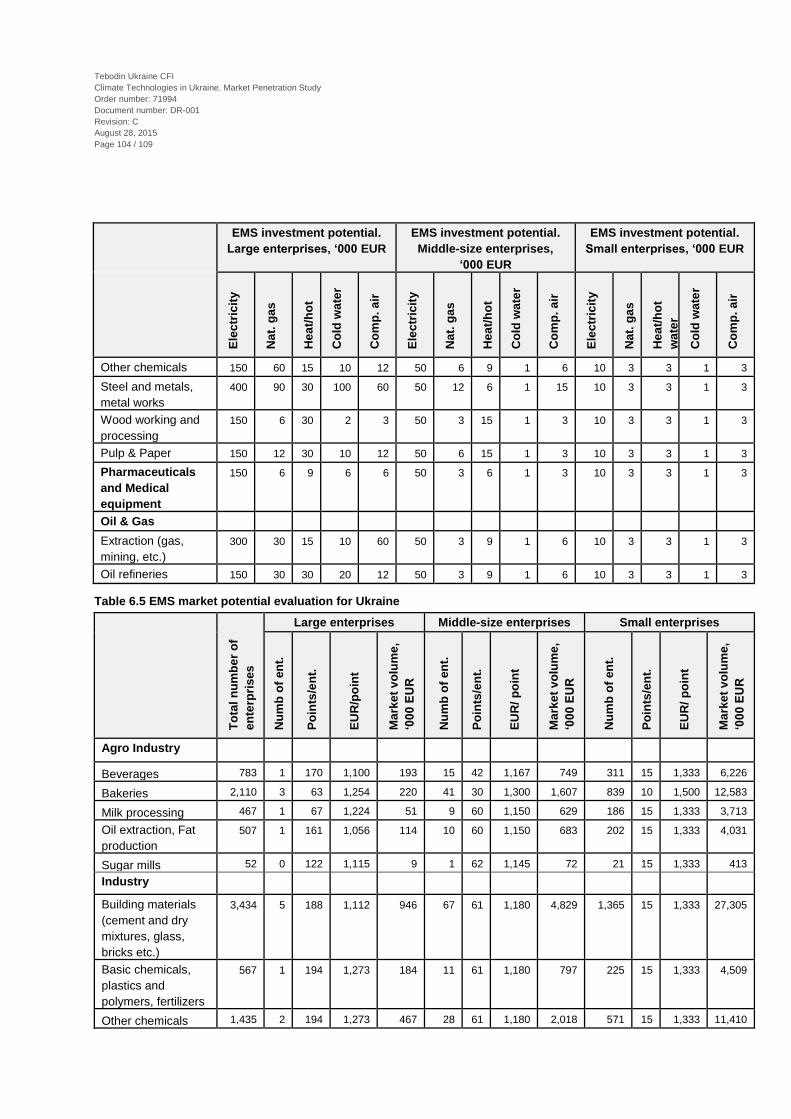

Energy Management Systems

According to market player data, Automated Metering Systems (AMS) cover approximately 75% of industrial enterprises.

However, merely 30% of enterprises use the installed AMSs to analyse energy consumption and take energy saving

measures. For the purpose of investment potential evaluation large (LE), middle-size (ME) and small enterprises (SE) were

analysed separately with taking into account different numbers of points for control.

EMS investment potential in Ukraine

10

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 10 / 109

(Sub)Sector Market volume, ‘000 EUR

LE ME SE Total

Agroindustry

Beverages 193 749 6,226 7,168

Bakeries 220 1,607 12,583 14,410

Milk processing 51 629 3,713 4,393

Oil extraction, Fat production 114 683 4,031 4,828

Sugar mills 9 72 413 494

Industry

Building materials (cement and dry mixtures, glass, bricks etc.) 946 4,829 27,305 33,080

Basic chemicals, plastics and polymers, fertilizers 184 797 4,509 5,490

Other chemicals 467 2,018 11,410 13,895

Pulp & Paper 300 156 8,468 8,924

Steel and metals, metal works 7,019 12,852 62,292 82,163

Wood working and processing 811 4,533 25,636 30,980

Pharmaceuticals and Medical equipment 578 305 1 972 2,855

Oil & Gas

Extraction (gas, mining, etc.) 1,048 2,585 15,251 18,884

Oil refineries 459 194 1,145 1,798

Total 12,399 32,009 184,954 229,362

At the average penetration of 23%, the number of potential consumers of energy consumption technical control and

metering equipment is estimated at 10,000, while the total number of metering points is about 175 thousand. In monetary

equivalent, the estimated investment potential for energy management systems in Ukraine can be estimated at € 230

million.

Water Management Systems

Water consumption minimization, optimization and recycling measures and technologies are integrated in production and

support processes, thus it is difficult to compare them and their effectiveness. The incentives for introduction of water

minimization and recycling are increasing water and energy cost.

Waste water treatment technologies are more standardized, although each water treatment process has to be designed

and adjusted to the treated water pollution and load. There are legal requirements for waste water treatment and also there

are incentives for minimization of discharging effluents in the form of payments for its volume and pollution.

A benchmark of the potential market could be based on market penetration estimated for the Czech Republic.

Consultant suggests to still considering this group of technologies as eligible for the program, however, specific indicators

related to technology is difficult to benchmark, since they depend on each specific case.

Air cooling systems

Air cooling condensers are mainly part of complex refrigeration and air-conditioning equipment installed in dairies,

bakeries, beverages producing and meat processing plants, temperature controlled warehouses. Industrial applications are

reported for printing sector and polymers production.

11

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 11 / 109

Air cooling condensers could be effectively applied under the total capacity of the heat transfer up to 2-3 MW. Under the

larger total heat transfer capacity the cooling water tower should be applied – in case of large enterprises greenfield

construction.

Application of air cooling condensers itself does not lead to energy savings. Energy saving is possible, e.g., under the use

variable speed fans in coolers.

Market information in open sources is scarce, so the market penetration can be assessed based on estimates of market

players.

Most Ukrainian suppliers and assemblers use equipment manufactured by Alfa Laval, Gunter, and SPR.

The total capacity of air cooling condensers installed in Ukraine is estimated at 92 MW.

Air cooling systems potential in Ukraine

(Sub)Sector Total installed capacity, MW

Penetration level (UA)

Total potential capacity, MW

Investment potential, million euro

Agroindustry

Bakery 0.27 <1% 204 10.41

Beverages (water, beer*) 11.03 55% 9 0.46

Distillery 3.13 12% 24 1.45

Vinery 1.82 67% 1 0.05

Cold storage 7.59 3% 232 14.41

Confectionery 3.77 <3% 137 8.23

Oil & Fat 1.87 1% 176 10.54

Meat processing 41.77 11% 267 16.02

Fish processing 0.87 <7% 12 0.83

Fruit & Vegetables processing 0.43 1% 53 2.71

Milk processing 7.41 8% 85 5.08

Industry

Metal processing 0.97 1% 101 5.13

Pharma 2.22 44% 3 0.19

Plastics & polymers 8.73 32% 18 1.10

Printing 0.30 <1% 96 6.64

Grand Total 92.16 1,418 83.22

The total investment potential is estimated at € 83 million.

Summary of penetration and investment potential

Different Climate Technologies have different levels of penetration in the Ukrainian market. Also there is a significant

difference in the level of penetration of the selected CT between the different market sectors.

The high penetration level of heat recovery technologies in some sectors (83-91%) doesn’t reflect the necessity of

modernization (e.g. sugar production, metallurgy, pulp & paper, oil & gas). Taking into account that waste heat utilization is

integrated in production, modernization will create the demand on new heat recovery technologies implementation.

EU benchmark and key indicators for CT implementation in Ukraine

Climate Technology

PBP EU,

years

PBP UA,

years

Penetra-tion EU**

Penetra-tion UA

Technology related CO2 reduction,

t/MWh

CO2 reduction potential, mio t/year

Invest-ment

potential, bn euro

1. Co-generation:

Gas engine CHP < 2 MW 6 - 10 1 - 2* 3 1-20%(3) 0.97 8.77 1.15

12

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 12 / 109

Climate Technology

PBP EU,

years

PBP UA,

years

Penetra-tion EU**

Penetra-tion UA

Technology related CO2 reduction,

t/MWh

CO2 reduction potential, mio t/year

Invest-ment

potential, bn euro

Gas engine CHP > 2 MW < 6 MW

6 - 10 1 - 2* 3 7% (3) 0.99 22.92 2.94

Organic Rankine Cycle (ORC)

7 - 10 2 - 4 2 n/a 1.17 n/a n/a

Steam turbine CHP > 2 MW < 6 MW

7 - 10 3 - 4 3 1 - 6%

(3) 1.17 104.41 1.86

2. Heat recovery 0.5 - 10 < 4 2 - 3 <1%

(except boilers)

effect is present

n/a n/a

3. Management systems, automation and practices

1 - 4 n/a 2 - 3 22.5%

(1) effect is present

n/a 0.23

4. Water management systems: 1 - 6 n/a 2 - 3 - 4 low (1) not relevant - n/a

5. Air cooling systems (air cooled condensers)

3 1 - 67%

(2-3) not relevant - 0.08

Total 136.10 6.25

* - For electricity sellers, depending on feed in tariff

** - Penetration legend: 1-‘introduction of new technology’; 2-‘increased acceptance of new technology’; 3-‘growing importance and application of technology’; 4-‘fully mature technology’

The total assessed investment potential for the eligible technologies is estimated at € 6.25 billion. At that, the CO2

countable reduction is estimated at 136 million tons per year, which means invested € 44 will reduce CO2 emission by

1 Mt/y.

Barriers to CT transfer in Ukraine

Based on Eco questionnaire the Consultant may summarize own and interviewed market players’ vision as of main barriers

and motivators for climate technologies penetration (for details see Section 5.6):

Barriers and motivations The most common answer The next most frequently mentioned

The third leading cause

Obstacles stopping compa-nies or organizations from investing in or working with energy efficiency and renewable energy

Economic and financial (e.g. difficulty obtaining loans, high cost of technology, uncertain financial environ-ment)

Policy/legal/regulatory (e.g. unstable and uncertain policies, problems in getting clearances, import taxations and certification require-ments)

Capacity (e.g. lack of skilled personnel to manage more complex technologies, inadequate training to identify and implement technologies, lack of service providers)

Economic and financial obstacles to investment or involvement with energy efficiency and renewable energy technology

Uncertain financial and economic environment (e.g. electricity tariffs, inflation rate, currency exchange rate)

Difficult to obtain loans with terms acceptable for the type of investment

High capital cost of the technologies

The top market obstacle to investment or involvement

Unstable economic situation Economy of scale difficult / impossible to be achieved

Lack of market transparency (e.g. What products,

13

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 13 / 109

Barriers and motivations The most common answer The next most frequently mentioned

The third leading cause

with energy efficiency and renewable energy technology

services are available and at what price).

The top policy/legal/regulatory obstacle to investment or involvement with energy efficiency and renewable energy technology

Corruption Unstable and uncertain policies

Insufficient enforcement of regulations

The top capacity obstacle to investment or involvement with energy efficiency and renewable energy technology

Lack of internal capacity to identify opportunities

Lack of service and maintenance specialists

Lack of skilled personnel for preparing projects

The top information and awareness obstacle to invest-ment or involvement with energy efficiency and renewable energy technology

Poor or lack of information about costs and benefits of technologies

Insufficient demonstration of technology in the country

Lack of agencies, organiza-tions or sources to provide information

The top motivator to invest in energy efficiency and/or renewable energy in Ukraine right now

Reduction of operational costs (energy costs, carbon tax)

Energy security Existing legal and regulatory requirements (green tariff)

What would most motivate your company to invest in energy efficiency and/or renewable energy technologies

Operational savings potential

Affordability of technology Legal and regulatory requirements

14

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 14 / 109

1 Introduction and purpose statement

This market Penetration Study Report (the ‘Report’) is elaborated by CFI ‘Tebodin Ukraine’ (Member of Bilfinger Group) in

partnership with ENVIROS, s.r.o. (Member of ENVIROS Group) (together to be referred to as the ‘Consultant’) based on

the Contract C30736/GISF-2015 -01-01/03 for FINTECC TC Program – Market Penetration of climate Technologies in

Ukraine dated 19 February 2015.

In the Bank's region, the number of investments into climate technologies and techniques remains low to date as a result of

underdeveloped supply chains, low awareness levels about the related needs and benefits, lack of technical expertise for

appraisal and risk assessment; lack of implementation capacity, regulatory uncertainties on energy and carbon pricing,

high perceived risk and upfront cost associated with the implementation of such technologies. Companies, if not

incentivised to make investments, delay making strategic decisions and investments and opt for sub-optimal solutions,

thereby locking into continuous inefficiencies. This experience has been particularly pronounced in the region over recent

years. In Ukraine situation is aggravated by current political and economic instability.

The EBRD Finance and Technology Transfer Centre for Climate Change (FINTECC) is a programme that helps companies

in eligible countries to implement innovative climate technologies and create a body of knowledge that can open up market

opportunities for e.g. creating new business models.

The beneficiaries of FINTECC are clients of the EBRD investing into climate technologies with low market penetration in

their respective countries and sectors. The programme offers technical assistance (climate technology audits), as well as

incentive grants for companies to introduce eligible technologies. The grants are available to the companies as a

complement to EBRD financing. In addition to the direct investment support, the Programme anticipates a comprehensive

Policy Dialogue and Knowledge Management aiming at:

Development of methodologies for improving availability and consistency of information on status of climate

technology market as well as guidelines for improving climate resilience of enterprises;

Visibility and knowledge sharing activities to disseminate best practice, and to provide capacity building to policy

makers, local experts and private enterprises;

Policy and regulatory support work, to assist the governments in the host countries to improve existing legislative

frameworks and create enabling environments for the adoption of climate technologies. The FINTECC

Programme in the host countries is funded by the Global Environment Facility (GEF) and the EBRD Shareholder

Special Fund (SSF).

The FINTECC activities are coordinated with other Regional Development Banks as well as with the Climate Technology

Centre and Network and are being delivered in partnership with the International Energy Agency (IEA) and Food and

Agriculture Organization of the United Nations (FAO). FINTECC Ukraine will benefit from the outputs of the activities jointly

developed by FAO and IEA.

A recent study (World Bank, 2014) of 500 companies in the industrial and commercial sectors in Ukraine has revealed that

financial barriers (such as high upfront costs, lack of capital, and long pay back), institutional barriers, knowledge gap, and

technical barriers are the strongest barriers to deployment of energy efficiency technologies. In addition, recently organized

EBRD event for dairy sector in Ukraine highlighted in particular the need:

to address regulatory constraints and complexities associated with permitting procedures;

to address absorption capacities of local businesses;

to offer broad and flexible technical assistance, not one-fit-all as the gaps for individual companies varies.

Experience also shows that underdeveloped supply chains with limited competition result in higher capital and upfront

costs, and longer paybacks thus affecting decision making and perceived risk of investments by companies. As per the

EBRD Transition report 2014, lack of competition will also limit productivity growth and keep firms active in the climate

technology supply chains stuck in low-productivity equilibrium.

15

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 15 / 109

Given the success of the FINTECC pilot in the eligible countries and the clear technology gap in Ukraine, the Bank is

working on FINTECC Programme roll-out to other geographies, starting with the introduction of FINTECC to Ukraine in

2015. It is envisaged that the extension of FINTECC to Ukraine is going to be funded by the Global Environment Facility

and the Neighbourhood Investment Facility (who provided their initial approvals), and will be operational by mid-2015.

To facilitate the preparation of the full implementation proposal for the Global Environment Facility and the Neighbourhood

Investment Facility the Bank has undertaken a series of activities to inform the final design of the Programme in Ukraine,

ensuring that the proposal reflects needs of the businesses in Ukraine and mitigates the risk of low uptake once the

Programme is launched including Market Penetration Study for climate technologies.

The overall aim of this Market Penetration Study is to provide information to the Bank on the market penetration of selected

technologies in the context of Ukraine in order to inform the design and implementation of FINTECC in Ukraine to cover the

following main Tasks:

Task 1: Methodological note for market penetration assessment

Task 2: Technology area prioritization

Task 3: Current standards in the country and BAT

Task 4: Market potential, penetration and benchmarking

It should be mentioned that the Consultant acted in the framework of tight timeframe and broad stated assignment that was

rather challenging. The Consultant thanks the Bank team and consultants of other related activities for the preparation of

FINTECC Programme for the constructive cooperation during the project.

16

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 16 / 109

2 Methodological note for climate technologies market penetration assessment in Ukraine

A summarised methodological note for climate technology market penetration (a general approach for how the market

penetration was assessed and quantified) is given below.

To assess the market penetration of the climate technologies in Ukraine a series of activities were undertaken by the

Consultant in the course of the assignment that forms methodological approach to the Market Penetration Study:

1. Kick-off activities

2. Desk top study of available methodological market penetration evaluation techniques and market information

(including statistics and analytical reports)

3. Defining focus market sectors and sub-sectors

4. Defining the basket of climate technologies

5. Describing Best Available Techniques (BAT) in EU (with reference to BREFs and commenting application cases

in the selected EU countries) under selected basket of climate technologies

6. Describing current standard in Ukraine under selected basket of climate technologies with comparison to EU

practice and technologies prioritization per sectors

7. Performing of market penetration analysis in benchmarking countries and in Ukraine for the selected climate

technologies, including interviews with technology providers and suppliers, industry experts and end-users and

analysis of barriers and motivators for the selected climate technologies penetration.

Methodological approach is commented in more detail in Sub-Sections below.

2.1 Kick-off activities

The following kick-off activities were performed by the Consultant at the initial stage of the assignment:

• Participation in Round table ‘FINTECC in Ukraine’ organized by the EBRD on 10/02/2015 to have an insight into

Programme aims and developments, introduction to EBRD team under Programme and networking with the local

market players-participants of the event.

• Meeting with EBRD FINTECC and Eco Ltd teams on 11/02/2015 to specify EBRD/Donor priorities for shaping

product under FINTECC Programme under two main envisaged components being 1) financial incentives for end-

users of climate technologies and 2) technical assistance to equipment/ technologies manufacturers and suppliers

(local and international) and to secure input for EBRD Proposal to sponsor of FINTECC (GEF) being prepared by

Eco Ltd.

• Initiating of obtaining the following input from EBRD:

Provision of deliverables requirements and sharing of available studies related to the assignment.

Review of the initial list of pre-selected industrial and agro industrial sectors and climate technologies basket.

Inputs from the consultant responsible for elaboration of the EBRD FINTECC proposal to programme sponsor

(GEF) (Eco Ltd.).

• Coordination activities between the Consultant and consultant focused on value chain analysis for climate

technologies (Larive) with facilitation from the EBRD site in order to:

Unify climate technologies that are covered by both studies;

Ensure that the specification of the technologies for each of the assignments is close;

Discussion of possibility that both assignments use the same reference country(ies) for the purpose of

benchmarking;

17

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 17 / 109

Ensure that contacting third parties (market players and experts) is done in a coordinated manner.

• Market insights for Ukraine and EU (after the example of Czech Republic) to identify market data availability

including BATs to define market sectors.

2.2 Available methodological market penetration evaluation techniques and market information

The Consultant performed search, collection and analysis of available methodological market penetration evaluation

techniques presented in the following relevant studies and guidelines (given below in chronological order):

UKEEP: Survey of the Ukrainian Market for Sustainable Energy Technologies, March 2014.

ENSI: Built Environment Sustainable Energy Market Review; Sustainable Energy Toolset 2, June 2012

UNEP RISO Centre. TNA Guidebook Series: Overcoming Barriers to the Transfer and Diffusion of Climate

Technologies, January 2012.

MWH: Identification of Energy Efficiency Opportunities at Retail Outlets in Ukraine and EE Penetration Rate

in Other Neighbouring Countries, August 2011

NREL: Market Penetration of New Energy Technologies, February 1993.

The Consultant also used open source market information (including statistics and analytical reports) reference to which is

given under specific Report Chapters.

2.3 Defining Market Sectors and Sub-Sectors

Based on the priorities of the EBRD the assignment was focused on the following economic sectors:

Agri-business (including agro and food processing);

Manufacturing and processing industry.

Considering EBRD priorities and anticipated pipeline of projects and importance of subsectors in Ukraine based on brief

market insight (including contribution in terms of resource consumption and CO2 emissions), the following sub-sectors

were defined for the purposes of the Market Penetration Study (given in alphabetical order):

Agroindustry:

Beverages;

Bakeries;

Fat production & oil extraction;

Fruit and vegetable processing

Milk processing;

Sugar mills.

Industry:

Building materials (cement and dry mixtures, glass, bricks, etc.);

Chemicals (organic and inorganic chemical industry, production of fertilizers, by-product coke industry,

organic synthesis, etc.);

Oil refineries;

Pharmaceuticals;

Plastics and polymers;

Pulp & Paper;

Steel and metals, ferrous and nonferrous metal processing;

Wood working and processing.

18

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 18 / 109

In terms of end-users only large businesses were considered as target group.

2.4 Climate technologies definition

Climate technologies – subject to Market Penetration Study are defined as innovative, low penetrated in Ukrainian market

energy and resource efficiency technologies and practices contributing to reduction of CO2 emissions with big potential of

replication in selected sectors of industry and agroindustry.

According to the mentioned criteria the following basket of climate technologies was defined for the purposes of Market

Penetration Study:

1. Co-generation:

Gas engine CHP < 2 MW (reciprocal)

Gas engine CHP > 2 MW < 6 MW (reciprocal)

Steam turbine CHP > 2 MW < 6 MW:

Pass-out steam turbine CHP

Back pressure steam turbine CHP

Organic Rankine Cycle (ORC)

2. Heat recovery:

Low- and Med-temperature (<650ºC)

High-temperature (>650ºC)

3. Management systems, automation and practices

Energy management systems

Advanced automation in drying

4. Water management systems:

Waste water treatment

Reduction of water consumption

5. Air cooling systems (air cooled condensers)

2.5 Best Available Techniques (BAT) in Europe

Selected climate technologies were first subject of technical specification according to EU BATs. The output data are

summarising the typical technical specifications including functionality, energy efficiency and CO2 reduction indicators,

typical capital investment outlay required for implementation and payback period (PBP).

For the technical specifications and reference indicators the Consultant applied the following main documents and

standards as listed below but not limited to:

1. EU Best Available Techniques Reference Documents (given below in alphabetical order):

BREF Common Waste Water and Waste Gas Treatment/ Management Systems in the Chemical Sector

Final Draft (2014)

BREF Non-Ferrous Metals Industries. Final Draft (2014)

BREF Polymers (2007)

BREF Ceramic Manufacturing Industry (2007)

19

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 19 / 109

BREF Energy Efficiency (2009)

BREF Ferrous Metals Processing Industry (2001)

BREF Food, Drink and Milk Industries (2006)

BREF Glass (2013)

BREF Industrial Cooling Systems (2001)

BREF Intensive Rearing of Pigs and Poultry (2003)

BREF Iron and Steel Production (2012)

BREF Large Combustion Plants (2006)

BREF Large volume inorganic chemicals – Ammonia, Acids, Fertilizers (2007)

BREF Large Volume Inorganic Chemicals – Solids and other industry (2007)

BREF Large Volume Organic Chemicals Draft 1 (2014)

BREF Organic fine chemicals (2006)

BREF Production of Cement, Lime and Magnesium Oxide (2013)

BREF Production of Specialty Inorganic Chemicals (2007)

BREF Production of Wood–based Panels (final draft, 2014)

BREF Pulp and paper (2013)

BREF Refining of Mineral oil and gas (2015)

2. Definition of High Efficiency cogeneration (EU Directive 2012/27/EU and 2004/8/EC, http://eur-

lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32012L0027

3. ISO 50001 Standard for Energy Management.

Based on data availability and representativeness benchmark the following EU countries advanced in the deployment of

assessed technology and at the same time comparable to Ukraine were chosen: Czech Republic and The Netherlands.

Where applicable and feasible the Consultant provided samples of process components where selected technologies are

applicable based on the criteria of availability of BAT data.

2.6 Current standards in Ukraine

Next step was evaluation of application selected climate technologies employed in Ukraine versus the technical

specification of BAT in EU. Selected climate technologies specified according to EU BATs were subject of identification as

for their applicability in Ukraine and current standards in Ukraine.

As such, there are no specific standards as for climate technologies in Ukraine. However, there are requirements for e.g.

cogeneration plants, whose owners would like to sell electricity and heat in the network (Law of Ukraine ‘On combined heat

and power generation (cogeneration) and waste energy potential’, #2509-15, revision dd. 02.03.2014), as well as the

procedure for the establishment of such facilities (Procedure of CHP qualification, enacted by Order of CMU #627 dated

12.06.2013).

Consultant used information received from market players – equipment suppliers:

Sinapse (GE Jenbacher equipment, including CHP), www.sinapse.ua ;

Zeppelin (Caterpillar), www.power-ua.com ;

GES (MWM CHP equipment), www.ges-ukraine.com ;

Siemens (back pressure steam turbines, ORC), www.siemens.com ;

Küttner (heat exchangers), www.kuettner.com ;

Teploenergoresurs (design, manufacturing, supply, construction, installation, commissioning, maintenance of

power equipment, incl. process exhaust gases heat recycling equipment), http://ter.vn.ua;

Alfa Laval (heat exchangers, air cooled condensers, various applications for food and pharma industry),

www.alfalaval.com.ua ;

Landis-Gyr (metering solutions), www.landisgyr.eu ;

ЕМН Metering GmbH & Co KG (automated electricity, heat, gas metering systems), http://emh.com.ua ;

20

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 20 / 109

Elster-Metronika (technical solutions in the field of smart grids and energy management),

http://www.elstersolutions.com ;

SRI Energy (energy consulting, testing, and improvements), www.sri-energy.com

ES Engineering (complex services on design, supply, installation of thermal engineering systems), www.ese.ua)

as well as information from market regulators, as indicated below but not limited to:

List of cogeneration installations which meet the qualification requirements (as of 05.01.2015, State Energy

Efficiency Service of Ukraine, http://saee.gov.ua/sites/default/files/documents/perelikKU_05012015.doc)

Register of power producers from alternative sources (as of 01.03.2015, NERC,

http://www3.nerc.gov.ua/?id=5701)

‘Green’ tariffs for electricity generated by the power plants that use alternative energy sources (Resolutions by

NERC)

The output data are summarising the typical technical specifications including functionality, energy efficiency and CO2

reduction indicators, typical capital investment outlay required for implementation and payback period (PBP). Technologies

are given with comparison to EU practice and with prioritization per applicable sub-sectors.

2.7 Market penetration analysis in Europe and in Ukraine for the selected climate technologies

Market penetration analysis in Europe and in Ukraine for the selected climate technologies and analysis of barriers and

motivators for the selected climate technologies penetration were aimed at gathering market evidences of the level of

market penetration in Ukraine of the selected basket of technologies, utilizing data from available studies, Consultant’s

expertise and market intelligence from market players including technology suppliers and potential end-users.

A wide selection of techniques is essential for analysts challenged with forecasting the market penetration of new

technologies1. These technologies are in various stages of development and have varying amounts of data available about

them. For example, some technologies are so new or are evolving so rapidly that much data about them are lacking. In

these cases, techniques demanding less data and resources should be used. Other technologies have a longer track

record so more quality data are available. To obtain the most statistically significant prediction, the most sophisticated

method that fits the data available should be used.

Some prediction methods are more effective than others at different developmental stages of new technologies. Generally,

as the new technology matures, the amount of data about that technology increases, allowing use of more sophisticated

data-demanding methods that require more resources for analysis.

1 Market Penetration of New Energy Technologies, by Daniel J. Packey, National Renewable Energy Laboratory, Colorado, USA, 1993

21

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 21 / 109

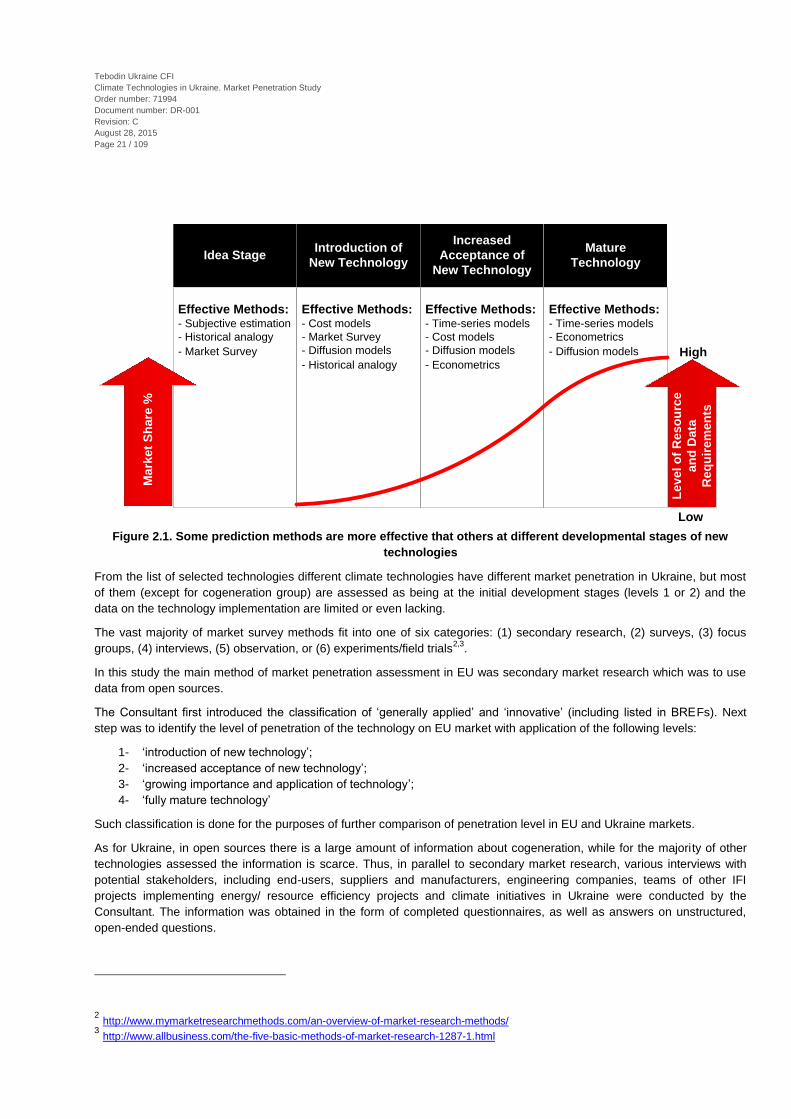

Figure 2.1. Some prediction methods are more effective that others at different developmental stages of new

technologies

From the list of selected technologies different climate technologies have different market penetration in Ukraine, but most

of them (except for cogeneration group) are assessed as being at the initial development stages (levels 1 or 2) and the

data on the technology implementation are limited or even lacking.

The vast majority of market survey methods fit into one of six categories: (1) secondary research, (2) surveys, (3) focus

groups, (4) interviews, (5) observation, or (6) experiments/field trials2,3

.

In this study the main method of market penetration assessment in EU was secondary market research which was to use

data from open sources.

The Consultant first introduced the classification of ‘generally applied’ and ‘innovative’ (including listed in BREFs). Next

step was to identify the level of penetration of the technology on EU market with application of the following levels:

1- ‘introduction of new technology’;

2- ‘increased acceptance of new technology’;

3- ‘growing importance and application of technology’;

4- ‘fully mature technology’

Such classification is done for the purposes of further comparison of penetration level in EU and Ukraine markets.

As for Ukraine, in open sources there is a large amount of information about cogeneration, while for the majority of other

technologies assessed the information is scarce. Thus, in parallel to secondary market research, various interviews with

potential stakeholders, including end-users, suppliers and manufacturers, engineering companies, teams of other IFI

projects implementing energy/ resource efficiency projects and climate initiatives in Ukraine were conducted by the

Consultant. The information was obtained in the form of completed questionnaires, as well as answers on unstructured,

open-ended questions.

2 http://www.mymarketresearchmethods.com/an-overview-of-market-research-methods/

3 http://www.allbusiness.com/the-five-basic-methods-of-market-research-1287-1.html

Effective Methods:- Subjective estimation

- Historical analogy

- Market Survey

Idea StageIntroduction of

New Technology

Increased

Acceptance of

New Technology

Mature

Technology

Effective Methods:- Cost models

- Market Survey

- Diffusion models

- Historical analogy

Effective Methods:- Time-series models

- Cost models

- Diffusion models

- Econometrics

Effective Methods:- Time-series models

- Econometrics

- Diffusion models

Ma

rke

t S

ha

re %

Le

ve

l o

f R

es

ou

rce

an

d D

ata

Re

qu

ire

me

nts

Low

High

22

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 22 / 109

Market survey was used to obtain information about market size for different technologies and, where possible, the level of

innovations implemented.

Consultant compared the subjective estimations by different experts to get averaged benchmarks for different technologies

as for their availability, application level and potential. Market penetration then was calculated per group of technology and

sectors as the ratio of applied cases to the potential applications based on assumptions of number of sector average end-

users that could potentially apply the technology. Wherever possible the Consultant commented types of the companies

identified tend to be faster in implementation of BAT technologies and type of financing utilized for these technologies.

Implementation potential then was summarised as aggregated total (total investment potential) and presented in a table

format.

On each technology separate paragraph is devoted summarising the identified quantifiable implementation potential and

the barriers faced in Ukraine versus the situation and barriers faced in the selected BAT country, including conclusions on

how the financial and technical traits of technologies may form potential and barriers for investment and penetration of

technology in Ukraine.

Methodological approach to the market penetration ratio and potential estimations per specific group of technologies is

commented as cases below.

Cogeneration

The total number of CHP units installed in Ukraine was analysed based on open sources and interviews with market

players (e.g. Zeppelin (Caterpillar), Sinapse (Jenbacher), Siemens, etc.). For the selected sectors the average installed

capacity was determined. The market capacity per sector was calculated by multiplying the total number of companies per

sector by using the latest statistical data available. The penetration level is calculated as a ratio of installed capacity per

sector to the market potential.

Heat recovery

In general, it cannot be said that the individual projects on waste heat recovery are always comparable, so the unification of

heat recovery installations is not possible. The differences are mainly in the layout configuration of source, consumption

and method of implementation.

Waste heat can be used on all devices that generate a waste heat transfer medium at a higher temperature, while the

waste heat can be used not only in the device itself, but also for other equipment or purposes (heating, domestic hot water,

etc.). This measure can thus reduce the consumption of any fuel or electricity.

Theoretically waste heat from the appropriate technological equipment in any kind of industrial operation or ventilation of

larger halls can be used. Waste heat can be supplied not only to a lower temperature (by heat exchanger) but also at a

higher temperature (heat pumps, thermal transformers). At temperatures of waste heat higher than about 150°C it is

possible to re-supply not only heat but also electricity (e.g. through ORC).

Use of waste heat must allow specific design of the facility, which produces waste heat - e.g. clear drying air inlet and clear

exhaust air outlet. The problem with some machines is that they do not have a clear inlet for drying air (because many

openings suck air into the machine) and exhaust air is not extracted from one specific point.

It remains difficult to compare a simple heat recovery from the exhaust of ventilation air into the intake air in one single heat

exchanger with the production of electricity from waste combustion.

So market penetration estimation is based mainly on subjective opinion of market players (e.g. Teploenergoresurs (design,

manufacturing, supply, construction, installation, commissioning, maintenance of power equipment, incl. process exhaust

gases heat recycling equipment, http://ter.vn.ua).

Energy Management Systems

In EU today, more than ever, effective energy management is a crucial issue for the success of any business. For many,

the answer is an Energy Management System (EMS) – a framework for the systematic management of energy. As well as

23

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 23 / 109

enhancing energy efficiency, an EMS can cut costs and reduce Greenhouse Gas (GHG) emissions providing you with a

competitive advantage. The ISO 50001:2011 represents the latest best practice in energy management system upon

existing national standards and initiatives.

In Ukraine, the key precondition for successful introduction of energy management system is energy consumption control

and metering. Although ISO50001 standard does not require to launch automated energy consumption control and

metering (technical metering, ASCMPC), this system, if available at the enterprise, multiplies effects of energy saving and

where corrective measures are taken it provides the enterprise the opportunity to save more energy resources. The

Guidelines for Use of Electricity GUE encourage consumers to use systems for analysis of energy consumption with

automated systems of commercial metering.

According to market player data, ASCMPC systems cover approximately 75% of industrial enterprises. However, merely

30% of enterprises use the installed ASCMPCs to analyse energy consumption and take energy saving measures.

Therefore, market penetration rate of the energy consumption technical control and metering systems may be evaluated as

follows:

MPR = n·k = 0.225

where n = 0.75 - factor of the enterprises covered by ASCMPCs,

k = 0.3 - factor of the enterprises, where ASCMPCs are utilized for energy consumption analysis and elaborating of

corrective actions.

Water management systems

Water minimisation, optimisation and recycling measures and technologies are integrated in production and support

processes, thus it is difficult to compare them and their effectiveness. The incentives for introduction of water minimisation

and recycling are increasing water and energy cost.

Waste water treatment technologies are more standardised, although each water treatment process has to be designed

and adjusted to the treated water pollution and load. There are legal requirements for waste water treatment and also there

are incentives for minimisation of discharging effluents in the form of payments for its volume and pollution.

A benchmark of the potential market could be based on market penetration estimated for the Czech Republic.

Based on the above considerations, the Consultant suggests to still considering this group of technologies as eligible for

the programme, however, specific indicators related to technology is difficult to benchmark, since they depend on each

specific case.

Air cooling systems

Air cooling condensers are mainly part of complex refrigeration and air-conditioning equipment installed in dairies,

bakeries, beverages producing and meat processing plants, temperature controlled warehouses. Industrial applications are

reported for printing sector and polymers production.

Application of air cooling condensers itself does not lead to energy savings. Energy saving is possible, e.g., under the use

variable speed fans in coolers.

Market information in open sources is scarce, so the market penetration can be assessed based on estimates of market

players (e.g. company ‘ES Engineering’, complex services on design, supply, installation of thermal engineering systems,

www.ese.ua).

The potential capacity is derived based on the typical / average cooling capacity for typical representative of the sector

taking into account the number of enterprises. The market penetration per sector is determined as share of installed

capacity from potential.

24

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 24 / 109

3 Technology area prioritization

3.1 Cogeneration

Combined Heat and Power (CHP) or Cogeneration is the simultaneous production of useful heat and electricity in the same

installation. Conventional electricity generation is via large power stations releasing low-grade heat into the atmosphere as

a wasted by-product. By retrieving some of this rejected heat via heat exchangers and being situated near where it can be

used, CHP plants can greatly increase their overall efficiency and provide heat to commercial, industrial or public sectors at

the same time as producing electricity.

Figure 3.1. Efficiencies of conventional power generation, cogeneration and trigeneration

Trigeneration (electricity, heat and cold generation) has the highest system efficiency and is about 300 % more efficient

than typical central power plant.

There are five principal types of CHP system:

1. Gas turbine systems, where fuel is combusted in the gas turbine and the exhaust gases are normally used in a waste

heat boiler to produce usable heat, though the exhaust gases may be used directly in some process applications.

2. Reciprocating engine systems, producing two grades of waste heat: high grade heat from the engine exhaust and low

grade heat from the engine cooling circuits. Two principal types of engine exist: compression ignition and spark

ignition, dependent on their firing method.

3. Back pressure steam turbine systems, where steam at high pressure is generated in a boiler and is wholly or partly

used in a turbine being exhausted from the turbine at the required pressure for the site. A proportion of the steam used

by the turbine may also be extracted at an intermediate pressure from the turbine (a pass-out/back pressure steam

turbine).

4. Pass-out condensing steam turbine systems, where a proportion of the steam used by the turbine is extracted at an

intermediate pressure from the turbine with the remainder being fully condensed before it is exhausted at the exit

(pass-out/condensing steam turbine).

5. Combined cycle systems, where the plant comprises one or more engines (usually gas turbines but in some cases

reciprocating engines) whose exhaust gases are utilised in a steam generator, the steam of which is used wholly or in

part in one or more steam turbines.

Benefits:

Economic/Management

Depending on the site and the correct choice of plant, savings made on electricity should more than offset the increase in

fossil fuel (usually gas) requirements. This is especially true in the market where electricity prices/unit is considerably more

than gas prices/unit. In some cases further savings from reduced maximum demand charges can also be made. For

CO

GE

NE

RA

TIO

N U

NIT

BO

ILE

RP

OW

ER

GE

NE

RA

TO

R

60

%

10

0%

Th

erm

al e

ne

rgy c

on

tain

ed

in th

e fu

el

sa

vin

g

40

%

ELECTRICITY

HEAT

ELECTRICITY

HEAT

LOSSES DURING

COGENERATION

LOSSES DURING CONVENTIONAL

POWER GENERATION

25

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 25 / 109

suitable small/medium scale CHP sites, energy bills can be reduced by as much as 40 % with typical paybacks of down to

3 or 4 years.

Having an independent supply of electricity avoids relying on the fluctuating price of supplied electricity, and also increases

security of power supply, as the CHP unit can continue to supply power should the grid fail, and vice versa.

The Environment

In conventional generation, 30-50% of the energy consumed is converted to electricity, the remainder being rejected to the

environment as heat, mainly through cooling towers or condensers. About 8% of this electricity (i.e. a further 3% of energy

input) is lost during transmission and distribution to the end-user. The fuel efficiency of industrial CHP plant can be around

80% or more and, as the plant is situated on-site, the losses from transmission and distribution are minimal. For a given

combination of industrial electricity and heat demands using CHP, 10-40% less fuel is required than with conventional

systems. The increased fuel efficiency of CHP gives it a potentially useful role in helping to combat global warming, through

curbing the emission of carbon dioxide (CO2), the principal man-made greenhouse gas. This table shows how this effect

depends on the fuel being displaced by CHP.

Table 3.1. Typical characteristics of CHP systems

Gas Turbine Spark

Ignition

Engine

Compression

Ignition

Engine

Back

Pressure

Steam

Turbine

Pass Out

Steam

Turbine

Combined

Cycle

Fuel Type Natural Gas,

Biogas, Gas

Oil

Natural gas,

Biogas

Natural gas,

Biogas, Gas

oil, Heavy oils

All types All types Natural Gas,

Biogas, Gas

Oil

Capacity

Range

>1 MWe 30 kWe to 2

MWe

100 kWe to 20

MWe

>500 kWe >1MWe >3 MWe

Heat: Power

Ratio

1.5:1 to 2.5:1

(5:1 with

supplementary

firing)

1:1 to 3:1 0.5:1 to 1.5:1

(3:1 with boost

firing)

3:1 to 10:1 3:1 to 8:1 1:1 (3:1 with

supplementary

firing)

Heat Output

Quality

High Grade

Steam

LPHW, Steam

(rare)

LPHW, Steam Medium

Grade Steam

Steam at 2

pressures

Medium

Grade Steam

Electrical

generating

Efficiency %

25-40 25-33 35-42 7-20 10-20 35-50

Overall

Efficiency %

65-80 (75-82

with suppl.

firing)

70-78 65-75 (75-82

with boost

firing)

75-84 75-84 73-80 (80-85

with suppl.

firing)

26

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 26 / 109

3.1.1 Gas Turbines

Gas turbines are able to provide the widest range of electric power - from ten to several tens of megawatts (with the usage

of so-called micro turbines the range can be extended to 1 MWe).

Figure 3.2. Gas turbine principle of operation

In such installations the flow of gas formed in the combustion of fuel creates a torque on turbine blades and rotates the

rotor, which in turn is connected to a generator. Electrical efficiency of systems of this type can be up to 39%. Use of the

gas turbines in combination with steam turbines can increase the electrical efficiency up to 59% (but the overall efficiency

not exceeding of 90%). Gas turbines can be used in many sectors of the economy, but the main sectors are still the oil and

gas production, metallurgy and energy generation with permanently high power consumption.

Inability to scale the system, the complexity of maintenance and the requirement for highly qualified personnel are major

disadvantages of the system. For the purpose of current study the gas turbines market was not investigated deeply.

Figure 3.3. Efficiencies of gas engines and gas turbines

3.1.2 Gas-fired reciprocating installations

The most popular units for CHP purposes are gas-fired (reciprocating or piston) installations. They gained popularity mainly

due to the relative ease of maintenance and management, lower cost and a higher rate of total efficiency (the sum of

electrical and thermal efficiency).

NATURAL GAS

100%

NATURAL GAS

100%

GAS ENGINE GAS TURBINE

ELECTRICITY

42%

ELECTRICITY

26%

HEAT

48%

HEAT

64%

LOSSES

10%

LOSSES

10%

27

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 27 / 109

Figure 3.4. Main components of CHP installation

The main components of a typical system are:

the engine or prime mover which drives the generator.

the generator which produces electricity.

the heat recovery system that recovers the waste heat from both the engine water cooling jacket and exhaust

gases.

the exhaust system to take away the products of combustion.

the control panel to monitor the operation.

Fuel flexibility: Modern equipment is able to work on a variety of gases: natural, landfill and waste water biogas, and

associated petroleum gas, coal mine methane, coke, blast furnace, ferroalloy gases, pyrolysis (synthesis) gas as well as

propane, butane and so on. If necessary, engines can be adjusted to operate on a mixture of different of gases

simultaneously.

Reliability and life: Gas engines in CHP installations are characterized by long periods of work between scheduled

maintenance: the life of spark plugs is up to 15,000 working hours, cylinder heads up to 30,000 – 40,000 hours.

Size range: Gas-fired CHP installations are supplied as skid-mounted and container mounted pre-assembled units (≤ 3

MWe) as well as stand-alone units, which require additional engineering for wrap around piping and covering structures.

Emissions: Emissions data of International producers are consistent with those described in EPA CFR 40 Part 89 Subpart

D & E and ISO8178-1 for measuring HC, CO, PM, NOx.

Electrical Efficiency: Gas-fired CHP units are equipped with electrical generators. The electrical generating efficiency of

CHP units is within the range 39-47%.

Thermal output: Heat recovery system allows recovering the heat of exhaust gases as well as the waste heat from the

engine water cooling reaching 52% of overall system efficiency.

CHP System Efficiency: The combined efficiency of modern CHP units reaches 92%.

28

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 28 / 109

3.1.3 Back Pressure Steam Turbines

Back pressure steam turbine systems, where steam at high pressure is generated in a boiler and is wholly or partly used in

a turbine being exhausted from the turbine at the required pressure for the site. A proportion of the steam used by the

turbine may also be extracted at an intermediate pressure from the turbine (a pass-out/back pressure steam turbine).

Figure 3.5 Boiler/Steam Turbine scheme and cogeneration system components

Back pressure steam turbine Extraction (pass out) steam turbine

This is the most widely used back-pressure type

turbine. Its aim is to expand the available steam

through the turbine stages.

It provides a constant pressure steam through a

controlled extraction at various loading conditions of the

turbine based on seasonal variations.

Figure 3.6 Type of back pressure steam turbines

3.1.4 Organic Rankine Cycle

The Rankine cycle is a thermodynamic cycle used to generate electricity in many power stations. Superheated steam is

generated in a boiler, and then expanded in a steam turbine. The turbine drives a generator, to convert the work into

electricity. The remaining steam is then condensed and recycled as feed water to the boiler.

Steam

Process or Condensor

Heat out

Power out

Turbine

Pump

FuelBoiler

Power out

Turbine

High Pressure

Steam

Low Pressure Steam

to ProcessCondensor

Power out

Turbine

High Pressure

Steam

Medium / Low

Pressure Steam

to Process

29

Tebodin Ukraine CFI

Climate Technologies in Ukraine. Market Penetration Study

Order number: 71994

Document number: DR-001

Revision: C

August 28, 2015

Page 29 / 109

Organic substances can be substituted for steam when temperatures are limited to less than 400 degree Celsius. This is

called an Organic Rankine Cycle (ORC).

ORC can make use of low temperature waste heat to generate electricity. At these low temperatures a steam cycle would

be inefficient, due to enormous volumes of low pressure steam, causing very voluminous and costly plants. ORCs can be

applied for low temperature waste heat recovery (industry), efficiency improvement in onsite power generation, and

recovery of geothermal and solar heat.

Several organic compounds have been used in ORCs (e.g. refrigerants, iso-pentane or ammonia) to match the

temperature of the available waste heat. Waste heat temperatures can be as low as 60°C. The efficiency of an ORC is

estimated to be between 10 and 20%, depending on temperature levels. On many sites no suitable use is available for low

temperature waste heat, hence upgrading by the use of a heat pump (or transformer) or an ORC are good energy recovery

candidates. Figure below shows a typical ORC where waste heat (1) evaporates the refrigerant which passes through the

turbine producing power (2). The refrigerant is then condensed (3) and pumped back to the waste heat source (4). The

system utilizes a closed-loop Rankine cycle using an advanced refrigerant.

Figure 3.7. Organic Rankine Cycle Unit Scheme

3.1.5 Steam Turbine Design Characteristics

Custom design: Steam turbines can be designed to match CHP design pressure and temperature requirements. The steam

turbine can be designed to maximize electric efficiency while providing the desired thermal output.

Thermal output: Steam turbines are capable of operating over a very broad range of steam pressures. Utility steam

turbines operate with inlet steam pressures up to 241 bar and exhaust vacuum conditions as low as one inch of Hg

(absolute). Steam turbines can be custom designed to deliver the thermal requirements of the CHP applications through

the use of back-pressure or extraction steam at appropriate pressures and temperatures.

Fuel flexibility: Steam turbines offer a wide range of fuel flexibility using a variety of fuel sources in the associated boiler or

other heat source, including coal, oil, natural gas, wood, and waste products.

Reliability and life: Steam turbine life is extremely long. There are steam turbines that have been in service for over 50

years. Overhaul intervals are measured in years. When properly operated and maintained (including proper control of

boiler water chemistry), steam turbines are extremely reliable. They require controlled thermal transients as the massive

casing heats up slowly and differential expansion of the parts must be minimized.

Size range: Steam turbines are available in sizes from under 100 kW to over 250 MW. In the multi-megawatt size range,

industrial and utility steam turbine designations merge, with the same turbine (high pressure section) able to serve both

industrial and small utility applications.