CAPITAL MARKETS OVERVIEW

ULI The State of Industrial MarketsLivingston, NJApril 2018

| 2

DISCLAIMER

Holliday Fenoglio Fowler, LP (“HFF”) and HFF Securities LP (“HFFS”) are owned by HFF, Inc. (NYSE: HF). HFF operates out of 26 offices worldwide and is a leading provider of commercial real estate andcapital markets services to the U.S. commercial real estate industry. HFF together with its affiliate HFFS offer clients a fully integrated national capital markets platform including debt placement, investmentsales, advisory services, structured finance, private equity, loan sales, and commercial loan servicing.

Forward-Looking StatementsCertain statements in this presentation are “forward-looking statements” within the meaning of the federal securities laws. Statements about our beliefs and expectations and statements containing the words“may,” “could,” “would,” “should,” “believe,” “expect,” “anticipate,” “plan,” “estimate,” “target,” “project,” “intend” and similar expressions constitute forward-looking statements. These forward-lookingstatements involve known and unknown risks, uncertainties and other factors that may cause results and performance in future periods to be materially different from any future results or performancesuggested in forward-looking statements in this presentation. Investors, potential investors and other readers are urged to consider these factors carefully in evaluating the forward-looking statements and arecautioned not to place undue reliance on such forward-looking statements. Any forward-looking statements speak only as of the date of this presentation and, except to the extent required by applicablesecurities laws, HFF (the Company) expressly disclaims any obligation to update or revise any of them to reflect actual results, any changes in expectations or any change in events. If the Company doesupdate one or more forward-looking statements, no inference should be drawn that it will make additional updates with respect to those or other forward-looking statements.

Industry and Market DataIn this presentation, we rely on and refer to information and statistics regarding economic conditions, trends, and our market in the sectors of that market in which we compete. In particular, we have obtainedgeneral industry information and statistics from certain third-party Source. We believe that these Source of information and estimates are reliable and accurate, but we have not independently verified them.

DisclaimersThe views expressed in this memo are strictly those of the undersigned author. This memo is offered solely for informational purposes only and should not be relied upon in connection with any investment orother decisions of the reader thereof. No representations or warranties are made with respect to any statements set forth in this memo and neither the undersigned nor HFF assumes any liability inconnection herewith. Prior to entering into any investment or other decision or transaction the reader should, among other things, perform its own diligence, research and analysis. The author has not andwill not receive any direct compensation for providing commentary that explicitly contributes to the reader's election to engage HFF and its associated entities for services related to and including, but notlimited to, investment sales, debt placement, advisory services, loan sales, equity placement, securities solicitation and/or loan servicing. Opinions, estimates and projections in this report constitute thecurrent judgment and belief of the author, solely, as of the date of this report. They do not necessarily reflect the opinion of HFF and are subject to change without notice. Neither the author nor HFF has anyobligation to update, modify, amend or continue publishing this report or to otherwise notify a recipient thereof in the event that any opinion, forecast or estimate set forth herein, changes or subsequentlybecomes inaccurate. Prices and availability of financial instruments are subject to change without notice. This report is provided for informational purposes only. It is not an offer or a solicitation of an offer tobuy or sell any financial instruments or commercial real estate asset, or to participate in, or develop, any particular strategy. Investment in commercial real estate assets, loans collateralized by same, or inany financial instrument herein may not be suitable for all investors and investors must make their own informed investment decisions. Stock, bond and derivative transactions can lead to losses as a result ofprice fluctuations and other factors. Past performance is not necessarily indicative of future results. Statements pertaining to beliefs, expectations and statements containing the word(s) may, could, would,should, believe, expect, anticipate, plan, estimate, target, project, intend and similar expressions constitute forward-looking statements. Forward-looking statements involve known and unknown risk,uncertainties and other factors which could cause actual results to differ materially contained in any forward-looking statements.

2 0 1 8 T H E M E S

| 4

2018 THEMES

Hold Periods Elongated Owners are less inclined to sell merely for profit taking

Long-dated capital seeks long-dated investments

Reinvestment risk trumps end-of-cycle risk

CRE Outperforms Traditional Asset Classes Over the past ten+ years, have outperformed stocks, bonds, REITs

Lower volatility, combined with higher average returns, provides outsized alpha over longer hold periods

Institutions increasingly favor private CRE to REITs

01TREND

CRE Allocations at All-Time Highs Average institutional investor allocation to CRE of ~10.5%

Nearly double from ten years prior

Significant increase in dry powder now undercutting new fund raising, retail investors will enter the space en masse

02TREND

Capital Is Abundant, But Not Desperate Transactions volumes remain below 2007 and 2015 highs

Net of NYC metro, volumes are mostly flat

GDP growth should see release up pent up demand in 201803TREND

1Q18 Transaction Volumes up YoY 2017 property sales down 15% from 2015 levels, down 19% from ‘07

Bid-ask gap remains between buyers and sellers

Large inbound queues among both closed-end and open-end funds

Sustained interest in CRE provides a soft floor to asset values

04TREND

05TREND

Values Determined By Property Fundamentals Income Return > Capital Appreciation

Geography and property sub-type matter greatly to investor interest

NOI growth hawked

Proof of tenant demand is paramount

06TREND

Source: HFF Research C M O

| 5Source: HFF Research, National Council of Real Estate Investment Fiduciaries, Standard & Poors, Barclays, National Association of Real Estate Investment Trusts, NCREIF as of 4Q17

PRIVATE CRE OUTPERFORMS: Private Real Estate Values Resilient

C M O

NCREIF, 244

S&P 500, 214

Barclays, 165

NAREIT, 142

0

50

100

150

200

250

300

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Tota

l Ret

urn

Inde

x (D

ec 2

005

= 10

0)

NCREIF S&P 500 Barclays Bond Index NAREIT

| 6

2.1%

3.2%3.7%

2.9%

4.5%5.2%

5.6%

9.6%9.1%

0%

2%

4%

6%

8%

10%

12%

1980 1985 1990 1995 2000 2005 2010 2015 2017 Actual

Port

folio

Tar

get

Allo

catio

n to

Rea

l Est

ate

INSTITUTIONAL ALLOCATIONS CONTINUE INCREASING

2018 Target Allocation10.3%

Target Real Estate Allocation of Institutional Investors

Source: Hodes Weill, Cornell University C M O

| 7Source: HFF Research, NCREIF

CORE UNLEVERED INDUSTRIAL RETURNS PROJECTED TO OUTPERFORM

C M O

| 8Source: HFF Research, NCREIF

WESTERN INDUSTRIAL RETURNS OUTPERFORMING

C M O

| 9Source: HFF Research, NCREIF

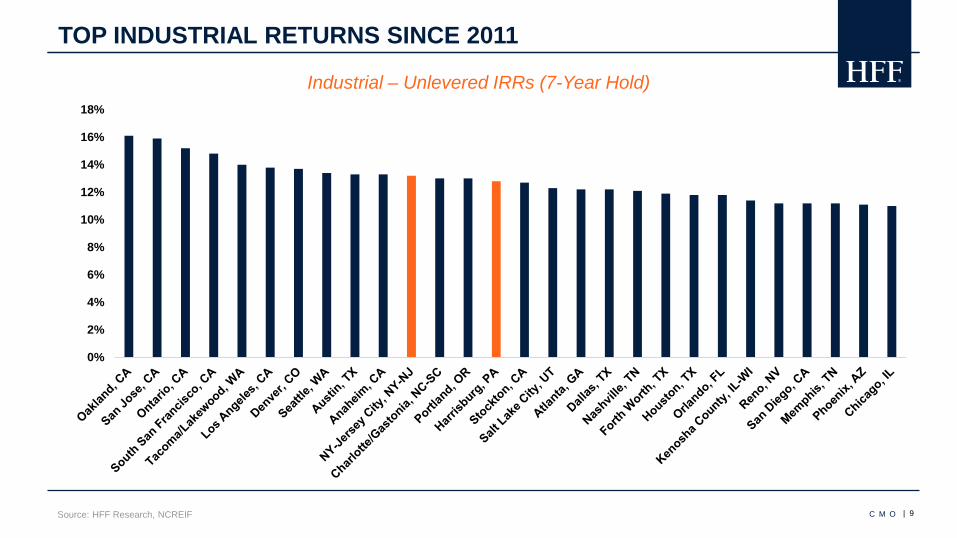

TOP INDUSTRIAL RETURNS SINCE 2011

C M O

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Industrial – Unlevered IRRs (7-Year Hold)

T R A N S A C T I O N V O L U M E S

| 11

$68$84

$106

$160

$275$301 $294

$136

$56

$110

$170

$224$249

$314

$372 $372$359

$80 $88

$93$109

$135

$219

$371

$432

$570

$177

$72

$155

$261

$310

$378

$452

$569

$511$487

$109 $114

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

$0

$100

$200

$300

$400

$500

$600

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 1Q17 1Q18

Bill

ions

Individual Portfolio Entity 10yr UST

1Q2018 TRANSACTION VOLUMES UP 5% YOY

Source: Real Capital Analytics

5%YoY

C M O

| 12

TRANSACTION PACE BASED ON GEOGRAPHY & PROPERTY TYPE

Source: HFF Research, Real Capital Analytics

If key markets are removed from the data set, national transaction volumes would only be down -1%

Hotel, retail and officedragging headline statistics

2017

VOL ($b) YOY

HOTEL 27.5 -24%

RETAIL 63.4 -18%

OFFICE 131.9 -8%

APARTMENT 150.1 -7%

DEV SITE 18.7 0%

INDUSTRIAL 72.2 20%

TOTAL 463.9 -7%

MAJOR METROS 180.3 -14%

SECONDARY MKTS 214.3 -2%

TERTIARY MKTS 67.2 0%

PORTFOLIO 109.4 -12%

SINGLE ASSET 354.5 -5%

NYC / SFO / SEA

- $21.1B(-43%)

REST OF COUNTRY

- $12.1B(-1%)

C M O

| 13

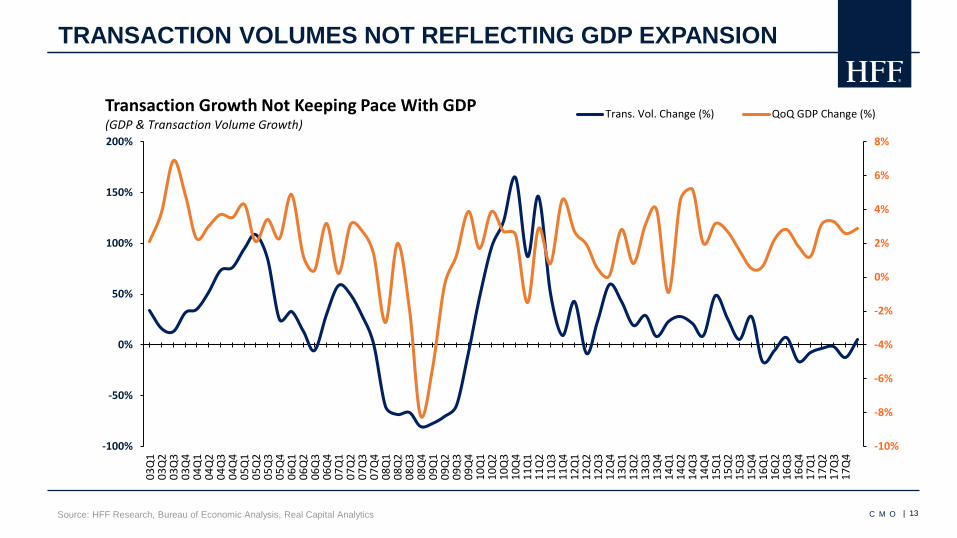

TRANSACTION VOLUMES NOT REFLECTING GDP EXPANSION

Source: HFF Research, Bureau of Economic Analysis, Real Capital Analytics C M O

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

-100%

-50%

0%

50%

100%

150%

200%03

Q1

03Q

203

Q3

03Q

404

Q1

04Q

204

Q3

04Q

405

Q1

05Q

205

Q3

05Q

406

Q1

06Q

206

Q3

06Q

407

Q1

07Q

207

Q3

07Q

408

Q1

08Q

208

Q3

08Q

409

Q1

09Q

209

Q3

09Q

410

Q1

10Q

210

Q3

10Q

411

Q1

11Q

211

Q3

11Q

412

Q1

12Q

212

Q3

12Q

413

Q1

13Q

213

Q3

13Q

414

Q1

14Q

214

Q3

14Q

415

Q1

15Q

215

Q3

15Q

416

Q1

16Q

216

Q3

16Q

417

Q1

17Q

217

Q3

17Q

4

Transaction Growth Not Keeping Pace With GDP(GDP & Transaction Volume Growth)

Trans. Vol. Change (%) QoQ GDP Change (%)

| 14

PORTFOLIO & ENTITY DEALS FLAT YOY

Source: HFF Research, Real Capital Analytics C M O

$25 $26 $29

$59

$96

$131

$277

$41

$13

$38

$63$74

$114 $119

$175

$124$112

$24 $24

$0

$50

$100

$150

$200

$250

$300

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 1Q17 1Q18

Bill

ions

Portfolio Entity

| 15Source: HFF Research, Real Capital Analytics

2017 WAS A RECORD BREAKING YEAR

C M O

$67.3BTotal Transaction Volume*

6.7KTotal Transactions*

+13%Vs. Previous Peak (2007)*

*Data does not include M&A transactions.

| 16Source: HFF Research, Real Capital Analytics

INDUSTRIAL VOLUME UP 34% YOY

C M O

$16 $13

$16

$25

$50 $52

$61

$27

$10

$21

$35 $38

$47 $51

$78

$60

$73

$16

$21

0%

1%

2%

3%

4%

5%

6%

$-

$10

$20

$30

$40

$50

$60

$70

$80

$90

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 1Q17 1Q18

Bill

ions

Individual Portfolio Entity 10 Yr UST

| 17Source: HFF Research, Real Capital Analytics

INDUSTRIAL TRANSACTION VOLUME BY REGION

C M O

18%22%

37%

31%

16%

18%29%

28%

$43

$52

$58

$26

$10

$21

$34$38

$46$50

$78

$60

$73

0

10

20

30

40

50

60

70

80

"05 "06 "07 "08 "09 "10 "11 "12 "13 "14 "15 "16 "17

Bill

ions

($)

East West Midwest South

*Data includes M&A transactions.

P R I C E D I F F E R E N T I AT I O N

| 19

2017 TRANSACTION VOLUMES BY MARKET

Source: Real Capital Analytics C M O

| 20Source: HFF Research, Real Capital Analytics

MOST ACTIVE MARKETS BY TRADE VOLUME

C M O

Industrial NOI Growth

E Q U I T Y

| 22

REITS MOVE THE NEEDLE

Source: NAREIT, as of March 31, 2018 C M O

~$1.02 Tn Market Cap

Regional Malls11%

Shopping Centers

6%

Strip4%

Apartments13%

Manufactured Homes

2%

Retail21%

Residential15%

Office12%

Health Care10%

Industrial9%

Data Centers

8%

Self Storage7%

Diversified7%

Lodging/Resorts7%

Specialty4%

| 23

PUBLIC MARKETS OPEN TO REAL ESTATE

Source: NAREIT C M O

$18.8 $19.8

$25.6

$38.8 $38.2

$49.0

$36.0

$18.0

$34.7

$47.5$51.3

$73.3$77.0

$63.6$59.3

$69.6

$92.1

$23.1

$15.0

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 1Q17 1Q18

Billi

ons

Unsecured Common IPO Preferred Secured

35%1Q18 vs

1Q17

| 24

REITS ALSO FAVOR PRIVATE PLACEMENTS

Source: JP Morgan C M O

| 25

CHANGE IN NON-LISTED REIT FEE REPORTING

Source: HFF Research, MTS Research Advisors C M O

14.5%SALES COSTS

AV E R AGE FR ON T-E N D LOAD S

1.3%ASSET MANAGEMENT FEES

AV E R AGE ON -GO IN G FE E

0.4%PROPERTY MANAGEMENT FEES

AV E R AGE ON -GO IN G FE E

$.84

| 26

BLACKSTONE TURNS THE TIDE

Source: Robert A.Stanger & Co, Inc. C M O

$0$200$400$600$800

$1,000$1,200$1,400$1,600

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Oct-16 Jan-17 Apr-17 Jul-17 Oct-17

Mill

ions

Rolling 12-Month Average Monthly Sales

$0

$500

$1,000

$1,500

$2,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Mill

ions

Monthly Sales Trends2015 2016 2017

| 27

OPEN & CLOSED-END FUND AUM UP 114% SINCE 2007

Source: HFF Research, National Council of Real Estate Investment Fiduciaries, Preqin C M O

~$281BILLION + AUM

Open End Funds Closed End Funds

~$469BILLION + AUM

118%INCREASESince 2007

111%INCREASESince 2007

$83 $91 $91 $110 $139$196

$262$351 $336 $306 $342

$429$474

$565$625

$703 $734 $750

$0

$100

$200

$300

$400

$500

$600

$700

$800

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Jun-17

Bill

ions

Closed- End Open-End

| 28

DRY POWDER EXCEEDS $175 BILLION USD

Source: HFF Research, Preqin as of 4/24/18 C M O

$26$37

$54

$70

$83 $85$94

$80

$94$89

$105 $103

$118

$133

$151

$177

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Bill

ions

113%vs 2007

| 29

PACE OF FUND RAISING SLOWS SIGNIFICANTLY

Source: HFF Research, Preqin as of 4/24/18 C M O

$14.0 $12.7

$10.5 $10.0

$28.7

$38.8

$54.6

$62.7

$72.3

$25.7$28.3

$43.6

$49.3

$71.7

$57.5

$83.6

$75.6$72.9

0

50

100

150

200

250

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

No. of Funds

Capi

tal R

aise

d (B

illio

ns)

Aggregate Capital Raised ($bn) No. of Funds

| 30

BUY-SIDE IS DIVERSE

Source: Real Capital Analytics, as of year-end 2017 C M O

O V E R S E A S C A P I TA L

| 32

$50.5B OF FOREIGN INVESTMENT IN 2017

$4

$10 $10$16

$25

$42

$76

$17

$5

$13

$24$30

$40$43

$95

$67

$51

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

$-

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Foreign Market Share (%

)

Tota

l For

eign

Cap

ital I

nves

tmen

t $B

Asia Australia Europe MENA North America South America % Mkt Share

Source: Real Capital Analytics C M O

YE 2017

Rank Country Acquisitions ($b) YoY Change

1 Canada $14.63 18%2 Singapore $6.33 92%3 China $5.98 -65%4 Germany $4.56 -26%5 Netherlands $3.26 924%6 Japan $2.41 -11%7 South Korea $1.93 -50%8 Israel $1.61 -38%9 Hong Kong $1.57 -34%10 Norway $1.16 75%11 Switzerland $1.14 -65%12 Australia $0.98 87%13 United Kingdom $0.89 -37%14 Qatar $0.73 -77%15 Denmark $0.5916 France $0.55 -47%17 Spain $0.48 -56%18 Sweden $0.35 -24%19 Finland $0.31 624%20 Kuwait $0.29 -74%21 Chile $0.17 -40%22 Brazil $0.10 -22%23 Mexico $0.09 -36%24 Ireland $0.08 588%25 India $0.07 -22%

| 33

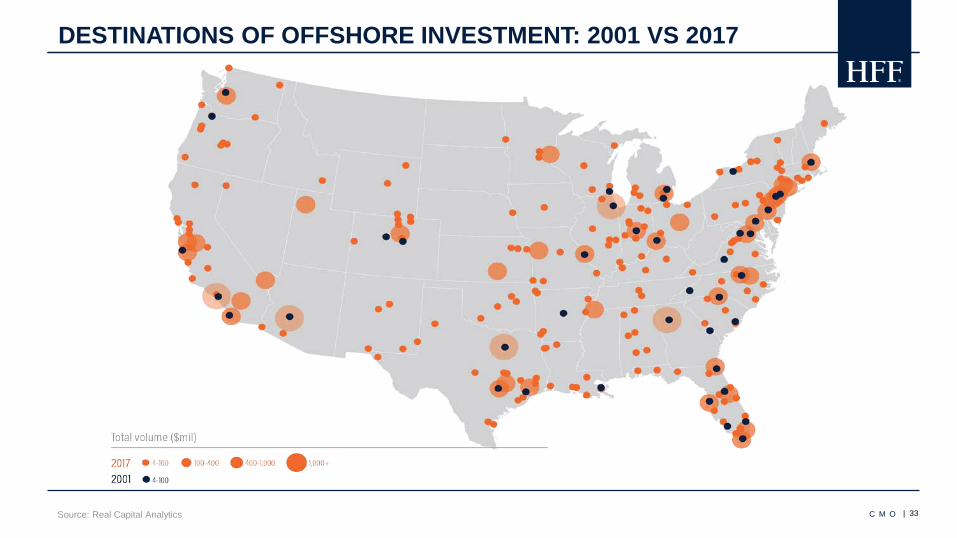

DESTINATIONS OF OFFSHORE INVESTMENT: 2001 VS 2017

Source: Real Capital Analytics C M O

| 34Source: AFIRE 2018 Investment Survey

FOREIGN CAPITAL FAVORS INDUSTRIAL

C M O

Industrial NOI Growth

D E B T

| 36

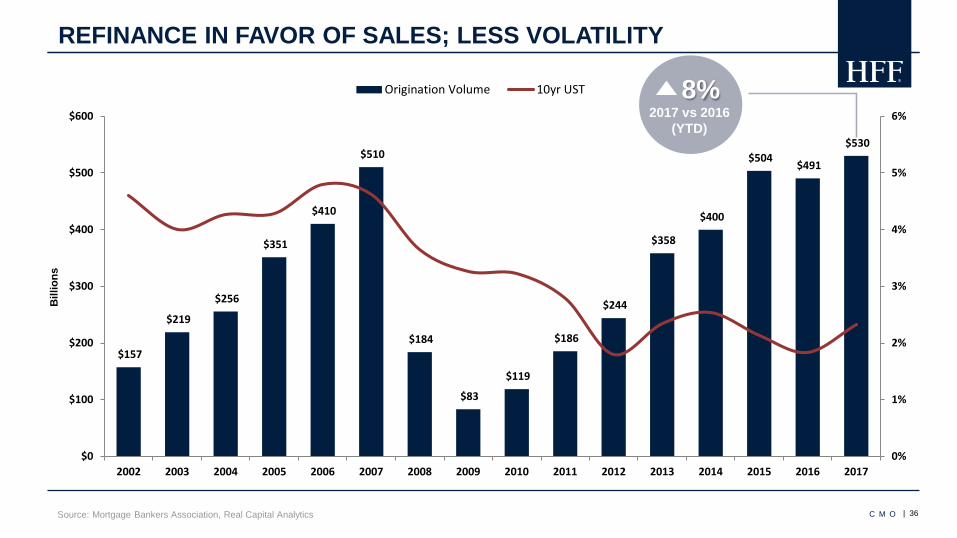

$157

$219

$256

$351

$410

$510

$184

$83

$119

$186

$244

$358

$400

$504 $491

$530

0%

1%

2%

3%

4%

5%

6%

$0

$100

$200

$300

$400

$500

$600

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Bill

ions

Origination Volume 10yr UST

REFINANCE IN FAVOR OF SALES; LESS VOLATILITY

Source: Mortgage Bankers Association, Real Capital Analytics

8%2017 vs 2016

(YTD)

C M O

| 37

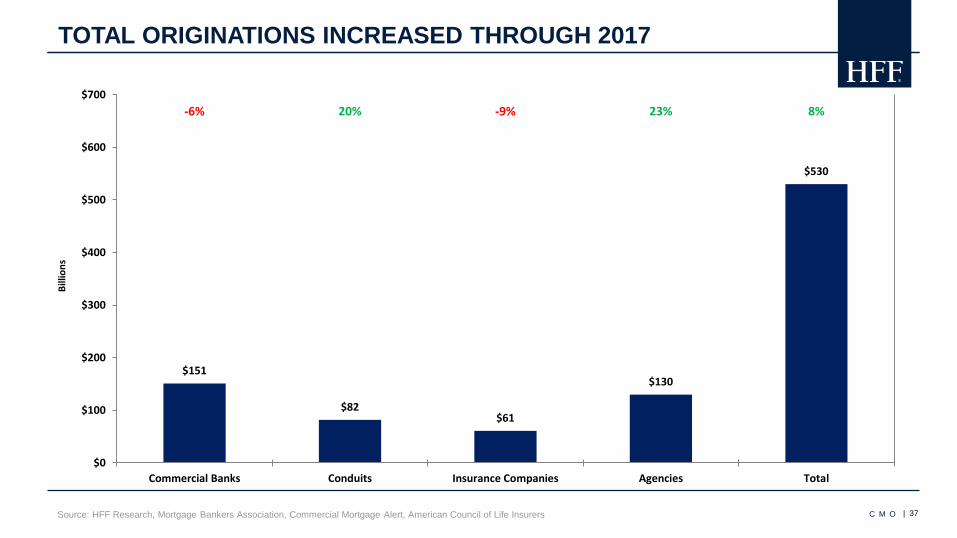

TOTAL ORIGINATIONS INCREASED THROUGH 2017

Source: HFF Research, Mortgage Bankers Association, Commercial Mortgage Alert, American Council of Life Insurers C M O

$151

$82$61

$130

$530

-6% 20% -9% 23% 8%

$0

$100

$200

$300

$400

$500

$600

$700

Commercial Banks Conduits Insurance Companies Agencies Total

Billi

ons

| 38

LENDER COMPOSITION

Source: Real Capital Analytics

18%

13%

19%

28%

25%

22%

17%

16%

3%

54%

8%

8%

9%

9%

7%

5%

6%

5%

3%

11%

6%

25%

22%

19%

19%

17%

27%

27%

31%

49%

24%

6%

10%

12%

12%

10%

12%

14%

20%

15%

10%

9%

5%

37%

43%

39%

33%

37%

31%

30%

31%

33%

53%

28%

2017

2016

2015

2014

2013

2012

2011

2010

2009

2008

2007

CMBS Financial Gov't Agency Insurance Pvt/Other Bank

C M O

| 39

HIGH-YIELD DRIVEN DEBT FUNDS RAISING CAPITAL

Source: HFF Research, Preqin as of 4/24/18 C M O

$0.4

$1.6 $1.4 $1.3

$4.4

$2.7

$4.1

$6.3

$12.2

$7.8

$4.2

$9.6

$4.3

$11.0

$16.3

$8.7

$15.4

$18.7

$5.4

0

5

10

15

20

25

30

35

40

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Total Funds Raised

Tota

l Cap

ital R

aise

d

Aggregate Capital Raised ($bn) No. of Funds

| 40

DEBT FUNDS PRICING CREDIT RISK TIGHTLY

Source: HFF Research, HFF CapTrack C M O

0

100

200

300

400

500

600

700

800

900

1,000

45% 50% 55% 60% 65% 70% 75% 80% 85%

Cred

it Sp

read

(bps

)

Loan to Value (%)

Multihousing Office Industrial

P R I C I N G T R E N D S

| 42

SUPPLY FORECAST TO STAY LOW

Source: GreenStreet Advisors as of November 2017

New Completions as % of Existing Stock

C M O

New Completions as % of Existing Stock

Supply in some niches is starting to heat up, but the overall outlook

remains moderate

| 43

REPLACEMENT COST INFLATION LIMITING NEW SUPPLY

Source: Turner Construction, Bloomberg

REIT vs. Construction Cost Index

C M O

80

180

280

380

480

580

680

780

80

100

120

140

160

180

200

220

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

NAREIT Equity REIT Index

(Indexed to 100)Tu

rner

Con

stru

ctio

n Co

st In

dex,

GDP

Def

lato

r & C

ore

CPI

(Inde

xed

to 1

00)

Construction Costs REIT Values

| 44

$1 BILLION MATURING DAILY NEXT THREE YEARS

Source: Trepp, Federal Reserve C M O

$76

$54

$39 $5

5

$58 $7

8 $96

$104 $1

36

$48

$48$5

5 $64 $7

4

$90

$105 $1

20 $132

$145

$166

$188

$205 $2

13

$211 $1

87

$159

$133

$136

$157

$178 $2

03

$225

$221

$178

$129

$86

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

CMBS Banks Life Cos Other

Billi

ons

$1.06 Trillion Matures2018-2020

CMBS Peak Maturities$136.0 Billion In 2017

| 45

CLOSED-END FUNDS: 89% HOLD LESS THAN 7 YEARS

Source: Preqin C M O

3 Years or Less, 14%

3.1-5 Years, 50%

5.1-7 Years, 25%

7.1+ Years, 11%

| 46

2.84%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 1Q18

CAPITALIZATION RATE SPREADS

RCA: 323 vs. 369

2.98% USTSpreads (bps)

Current vs. LT Avg.

JPM: 262 vs. 292NCREIF: 207 vs. 292

Source: Real Capital Analytics, JPMorgan, National Council of Real Estate Investment Fiduciaries, HFF Research C M O

NCREIFCap Rate

RCACap Rate

JPM ImpliedCap Rate

10 YrUST

Current UST2.98%

In 2007… Treasury – 4.4% Negative & Excessive Leverage NCREIF Cap Rate Below 10yr UST Aggressive Underwriting Metrics Total Return Composition Imbalance

| 47Source: Real Capital Analytics**, Bloomberg*

10 YEAR UST VS INDUSTRIAL CAP RATE: 2007 VS. 2018

C M O

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

'06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18

10yr UST* Cap Rate**

373 Basis Points

| 48

25%

20%

17%14%

13%11% 10% 9% 8%

0%

5%

10%

15%

20%

25%

30%

4% 5% 6% 7% 8% 9% 10% 11% 12% 13%

NO

I Gro

wth

Req

uire

d

Starting Capitalization Rate

CAPITALIZATION RATE SENSITIVITY ANALYSIS

Source: HFF Research C M O

NOI Growth vs. Cap Rate Movement

As you can see, these movements are non-linear. The lower a building’s original capitalization rate, the greater the movement in NOI must be in order to maintain a constant gross value.

| 49

BORROWING COST IMPACT ON VALUE

Source: Morgan Stanley Research C M O

Assumes 10 yr Term, 30 yr Amortization, 70% LTV

Annual NOI Growth Required To Maintain IRR Property Value Decline If No NOI Growth…

| 50

COMPOSITION OF TOTAL RETURN

Source: HFF Research, National Council of Real Estate Investment Fiduciaries C M O

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%19

7919

8119

8319

8519

8719

8919

9119

9319

9519

9719

9920

0120

0320

0520

0720

0920

1120

1320

1520

17

Total Return Moderating On Lower Capital Appreciation(Components of NCREIF NPI Total Return)

Income Return Capital Appreciation

89%

51%

34% 37% 35%

-79%

-37%

52%43%

55% 51%45%

38%

60%67%

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Income Return Nearing 75% Of Total Return(Income Return As % of Total Return)

| 51

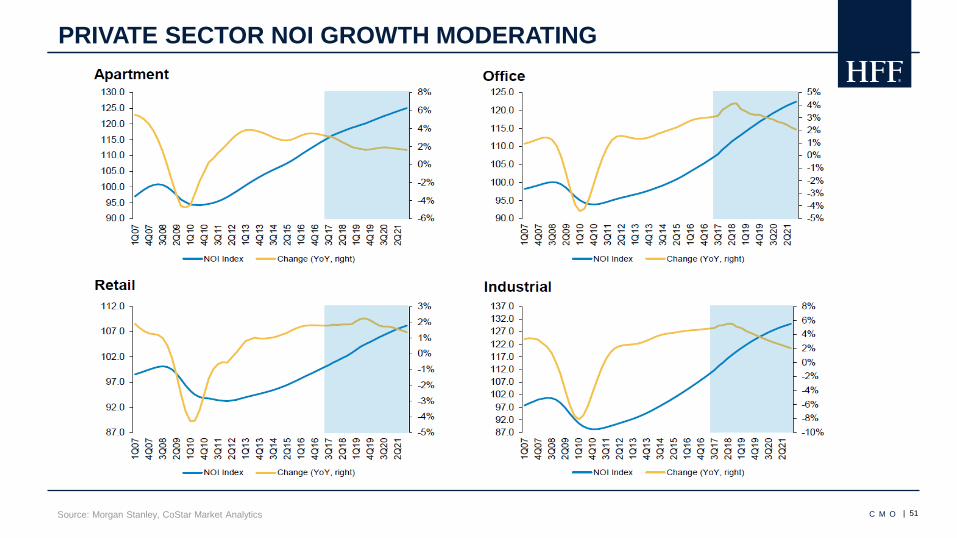

PRIVATE SECTOR NOI GROWTH MODERATING

Source: Morgan Stanley, CoStar Market Analytics C M O

| 52

MATURE NOI GROWTH CYCLE?

Source: National Council of Real Estate Investment Fiduciaries C M O

80

100

120

140

160

180

200

220

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

NO

I Gro

wth

Inde

x (J

an 1

991

= 10

0)

Double-Header or Extra Innings?(Same Store NOI Growth)

1990s NOI Growth Cycle• Lasted 8 yrs• Produced 52% NOI Growth

2000s NOI Growth Cycle• Lasted 4 yrs• Produced 17% NOI Growth

2010s NOI Growth Cycle• 7 yrs old• Has produced 37% NOI Growth

| 53Source: HFF Research, Bloomberg, as of April 24, 2018

U.S. OFFERING ATTRACTIVE YIELDS & PERFORMANCE

COUNTRY 2 YEAR 3 YEAR 5 YEAR 7 YEAR 10 YEAR 30 YEARSwitzerlandJapanNetherlandsGermanyBelgiumSwedenFranceItalySpainDenmarkUnited KingdomUnited States

COUNTRY 2 YEAR 3 YEAR 5 YEAR 7 YEAR 10 YEAR 30 YEARUnited States 2.476 2.636 2.821 2.936 2.975 3.144United Kingdom 0.859 0.903 1.200 1.341 1.537 1.942France -0.504 -0.299 0.088 0.410 0.841 1.668Germany -0.565 -0.406 -0.006 0.250 0.632 1.292Japan -0.138 -0.125 -0.098 -0.036 0.051 0.735

Bond Maturity in Years

NEGATIVE INTEREST RATE POSITIVE INTEREST RATE

C M O

I N D U S T R I A L T R E N D S

| 55Source: HFF Research, Green Street Advisors, SNL Financial

INDUSTRIAL REITS ARE OUTPERFORMING OVERALL MARKET

C M O

| 56Source: HFF Research, Real Capital Analytics, CBRE Research

CAPITAL BEING CAUTIOUS LATE IN THE CYCLE

C M O

Industrial NOI Growth

| 57Source: HFF Research

NATIONAL PRICING METRICS

C M O

| 58Source: HFF Research, CoStar

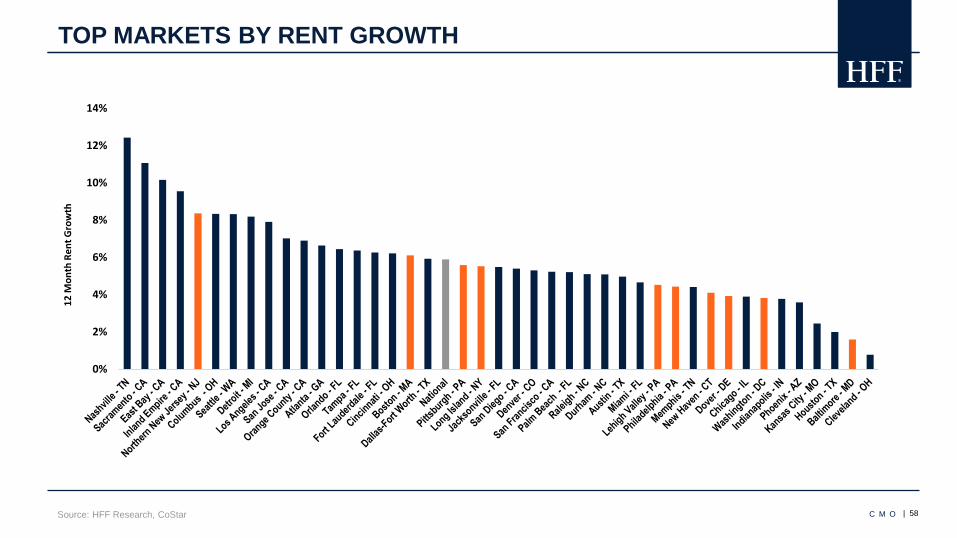

TOP MARKETS BY RENT GROWTH

C M O

0%

2%

4%

6%

8%

10%

12%

14%

12 M

onth

Ren

t Gro

wth

| 59Source: HFF Research, NAIOP

EVOLVING CONSUMER HABITS

C M O

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

E-Commerce Retail Sales as % of Total Sales

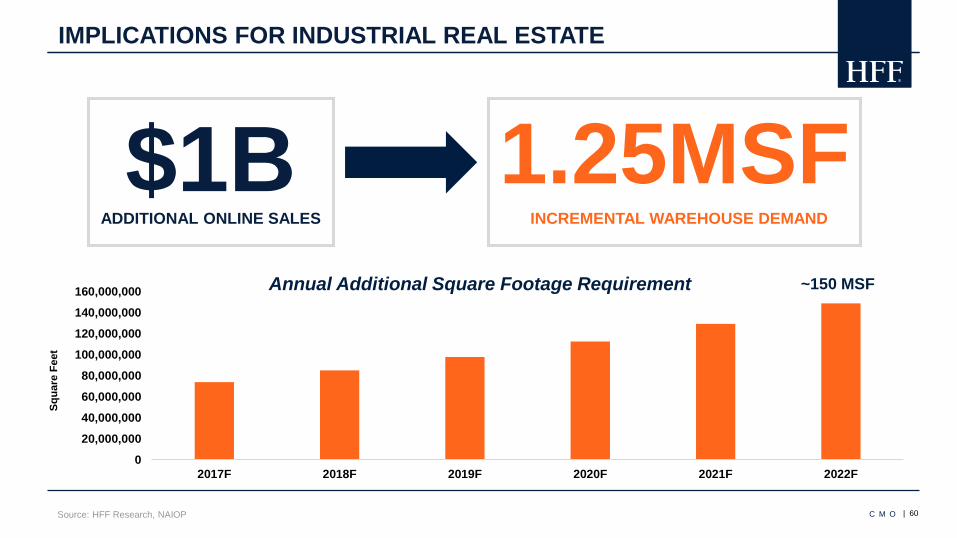

• Online sales at $452 billion in 2017 (17% increase year-over-year)• Forecasted to increase from 9.1% in 2017 to 25% of overall sales by 2025.

| 60Source: HFF Research, NAIOP

IMPLICATIONS FOR INDUSTRIAL REAL ESTATE

C M O

020,000,00040,000,00060,000,00080,000,000

100,000,000120,000,000140,000,000160,000,000

2017F 2018F 2019F 2020F 2021F 2022F

Squa

re F

eet

~150 MSFAnnual Additional Square Footage Requirement

$1BADDITIONAL ONLINE SALES

1.25MSFINCREMENTAL WAREHOUSE DEMAND

| 61Source: HFF Research, Los Angeles / Long Beach Port Tonnage Freight Report

TOP PORT SYSTEM ACTIVITY

C M O

RANK PORT TEU’S

1 Los Angeles / Long Beach 15.0M

2 New York / New Jersey 6.4M

3 Savannah 3.7M

4 Seattle / Tacoma 3.6M

5 Hampton Roads 2.6M

6 Oakland 2.4M

7 Houston 2.2M

8 Charleston 2.0M

| 62Source: HFF Research, World Shipping Organization, Panama Canal Authority

IMPACT OF PANAMA CANAL PROJECT

C M O

| 63Source: HFF Research, NAIOP

CAPITALIZING ON TRADE FLOW FROM CHINA

C M O

| 64Source: HFF Research, NAIOP

COLD STORAGE IS GAINING MOMENTUM

C M O

• Online sales at $19 billion (3% of total grocery sales) in 2017 • Forecasted to $100 billion (13%) by 2024.

36% of survey participants plan to order groceries online in 2018, up from 22% in 2017.

8%

19%22%

36%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2015 2016 2017 2018

2015-2018 eGrocery Adoption

% of US consumers who grocery shopped online

| 65Source: The Washington Post

INDUSTRIAL SECTOR IMPACTED BY POTENTIAL TRADE REGULATIONS

C M O

| 66Source: The Washington Post

EXPORTS EFFECTED BY POTENTIAL TARIFFS

C M O

H F F L P . C O M

PRESENTER

Jimmy HintonManaging Director(713) [email protected]

Atlanta | Austin | Boston | Carolinas | Chicago | Denver Dallas | New Jersey | Houston | Indianapolis | Los AngelesMiami | New York | Orange County | Orlando | PhiladelphiaPhoenix | Pittsburgh | Portland | San Diego | San FranciscoSeattle | Tampa | Washington, D.C. | London