1 Member of Islamic Development Bank Group

Buyer underwriting : Approach, methodology,

risk factors and financial assessment

Presented By: Mr. Mourad Mizouri

2 Member of Islamic Development Bank Group

Agenda

Buyer underwriting : Approach and methodology

Risk factors and risk mitigation tools

Financial assessment

ICIEC underwriting model

Open discussion

3 Member of Islamic Development Bank Group

1 - Buyer underwriting : Approach and methodology

4 Member of Islamic Development Bank Group

A- Introduction :

What is underwriting? Is it a science or art or involves combined skills? Is there a standard approach among the ECAs and within the same underwriting team?

B- Steps to make credit assessment :

1 – Checking internal eligibility criteria

2 – Identification of the risk factors

3 – Identification of the appropriate credit information sources

4 – Collection of information from different sources

5 – Evaluation of the risk

6 – Underwriter recommendation (Accept/reject – conditions)

5 Member of Islamic Development Bank Group

C- Usual approaches used : standard/practical 1- Standard:

Based on factual data (i.e. financial statements, financial ratios, benchmarking of companies in the same sector, historical data, statistical methods, trading experience with the buyer, etc..).

Issues :

- Inaccurate, absence or old financial information : (mainly in our region)

- Inappropriate in case of changing political conditions

- Less room to underwriter’s judgment or Gut feeling

- Mainly based on documentation (financials, T&P.E, credit reports) rather than field visit findings : May be appropriate for small limits

6 Member of Islamic Development Bank Group

2- Practical:

In addition to factual facts, this approach includes assessment of :

- The sector of activity and the market conditions,

- The management reputation and political influence,

- The country political and economical situation,

- The experience with the PH and the buyer,

- The information received through different channels

- The Policyholder (KYC), etc..

Advantages:

- Comprehensive assessment of all risk factors (details in the next slide)

- More appropriate for high limit requested

- Involves field visit

7 Member of Islamic Development Bank Group

2- Risk factors and risk mitigation tools

8 Member of Islamic Development Bank Group

A- Risk factors :

- Corporate risk : Legal status (e.g. family owned business), date of establishment, quality of the management (e.g .political influent, experience, reputation), premises (owned/hired), staff turnover (environment in the work), financial performance (high level of borrowing, under-capitalization, negative cash flows from operations etc..), Group financial situation (under restructuring, sister company defaulted), payment experience, IT system, etc..

- Product risk : Seasonality of the goods (e.g. related to religious event), life cycle (e.g. maturity or down trend), strategic importance to the buyer and the country (e.g. pharmaceutical, oil, etc..), tenor of the goods (as per B.U standards)

9 Member of Islamic Development Bank Group

- Business sector risk : Competition in the market, market positioning, reputation of the competitors, price determination mechanism, investment in R&D (specific activities), etc…

- Country risk : Transfer restriction, US or UN sanctions, special conditions to approve buyers (e.g. Promissory notes, cheques, etc..), country temporarily off cover for political reasons (exit strategy), etc..

- Others : Terms of Payment, relationship with the PH, adverse information received from local ECAs and banks, etc..

This should lead to SWOT analysis.

10 Member of Islamic Development Bank Group

B- Risk mitigation tools :

1- Buyer risk :

- P.N condition, cash deposit, parent company guarantee

- Shipping guarantee condition (e.g. experience of livestock)

2- Policyholder risk :

- Reduced percentage of cover and claim’s compensation

- Exclusion of risks covered (e.g. transfer risk)

- Setting Maximum liability, increasing the waiting period

11 Member of Islamic Development Bank Group

3- Internal risk :

- Reinsurance support

4- External risk :

- Adopting specific country grading and cover attitude

- Agreements with Central banks, MOF

- Experts views about the sector, the country, etc…

12 Member of Islamic Development Bank Group

3- Financial assessment

13 Member of Islamic Development Bank Group

A- Major financial ratios

• The sales and profitability (e.g. ROAA, ROAE, Net Margin, Net income, Operational results, financial charges).

• The Leverage and borrowings (e.g. D/E ratio, structure of borrowings (short term or medium term, secured or unsecured).

• Liquidity (e.g. analysis of the current ratio, quick ratio and acid test)

• The operating cycle (Days outstanding in receivables, days outstanding in inventory and days outstanding in payables and accruals)

• Cash flow analysis : giving due importance to the cash flow movements in the last years and mainly the operating cash flow and the free cash flow.

14 Member of Islamic Development Bank Group

B- With no/limited financial information

In such cases, the underwriter has to prepare his submission based on the following main points:

• Experience with the buyer (Good, buyer under watch list or black list, etc…)

• The Policyholder payment experience with the buyer (previous shipments covered during the last years mentioning the due date of payment)

• Information collected from approved credit sources

• Information gathered from other channels (i.e. ECAs, banks, local agents, brokers, internet, etc…)

• Assessment of the few available financial information about the buyer

• Findings of the buyer visit (if any)

15 Member of Islamic Development Bank Group

4- ICIEC underwriting model

16 Member of Islamic Development Bank Group

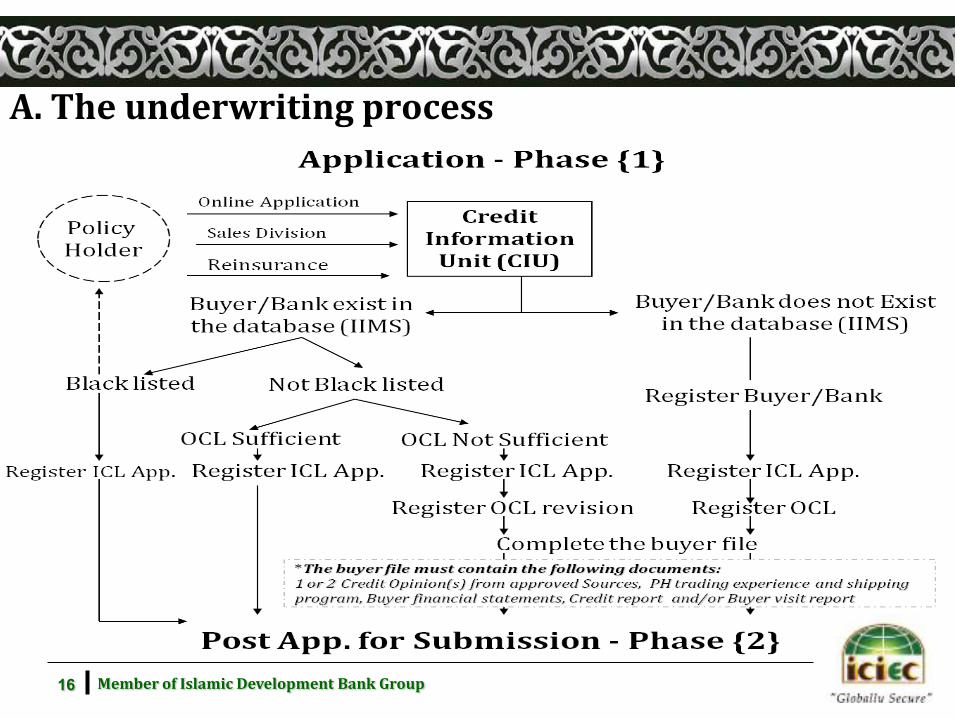

A. The underwriting process

17 Member of Islamic Development Bank Group

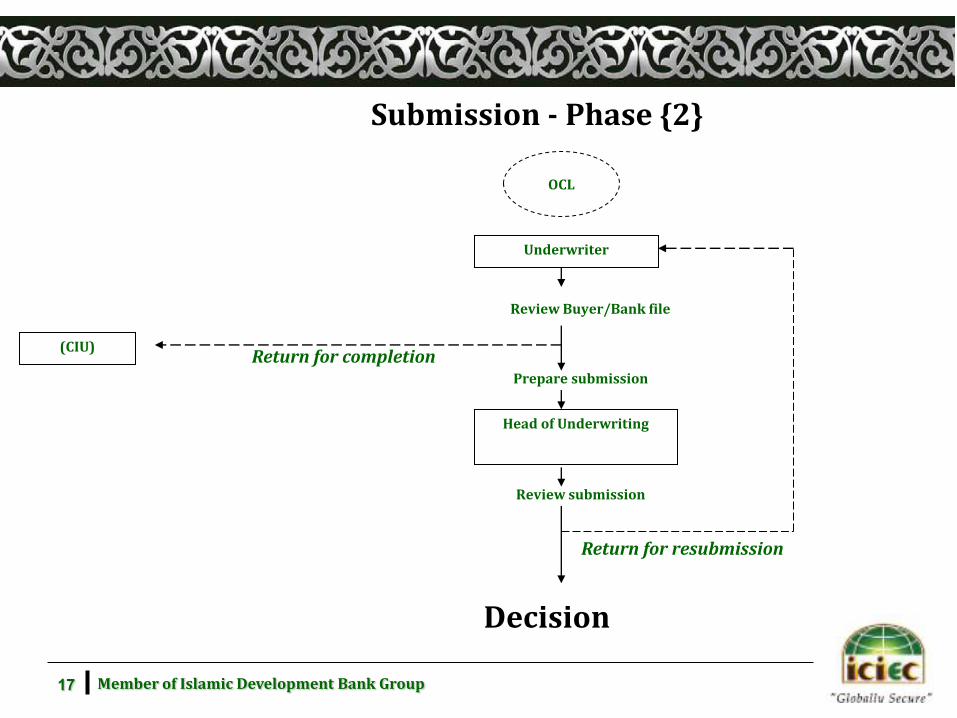

Submission - Phase {2}

Decision

OCL

Underwriter

Head of Underwriting

Prepare submission

Review submission

Review Buyer/Bank file

Return for completion (CIU)

Return for resubmission

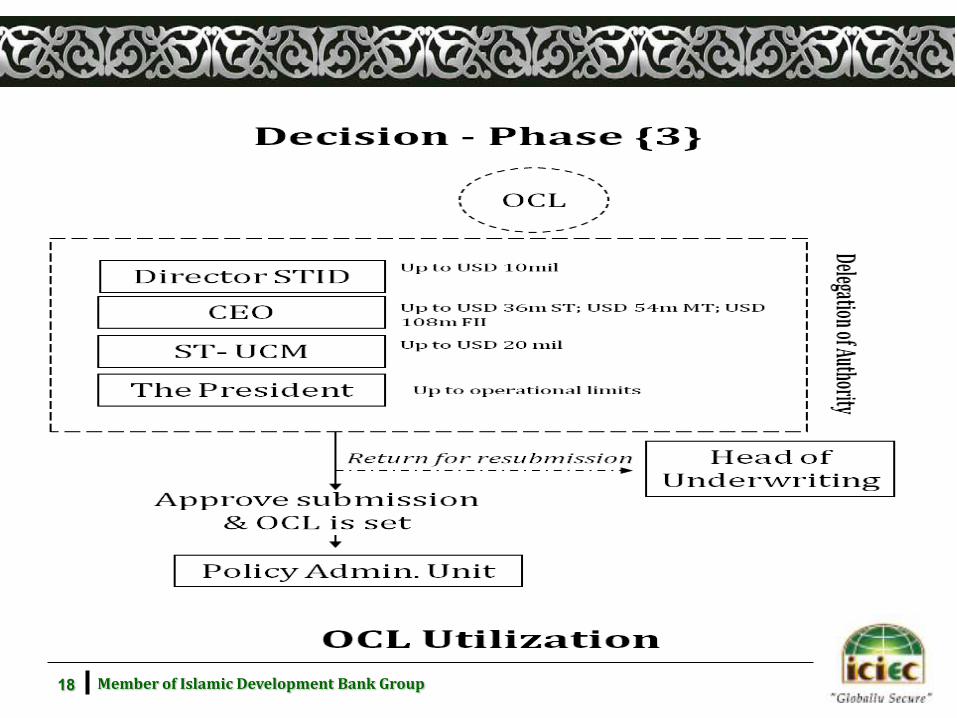

18 Member of Islamic Development Bank Group

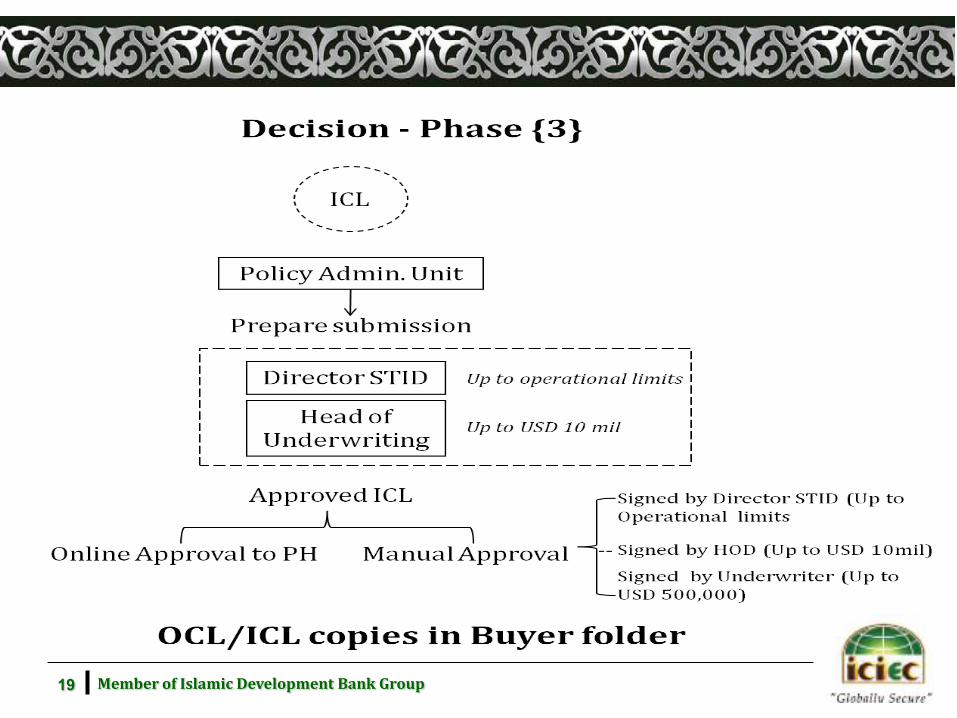

19 Member of Islamic Development Bank Group

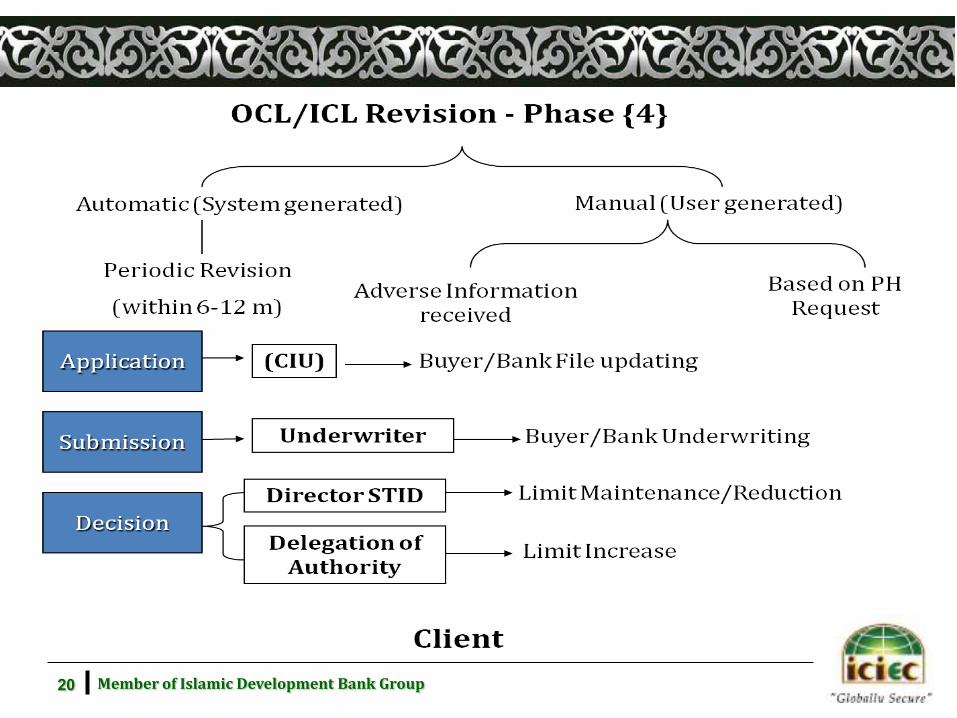

20 Member of Islamic Development Bank Group

21 Member of Islamic Development Bank Group

B- Risk mitigation and minimization tools

- Risk Monitoring of the buyers : Made on regular basis based on Buyer/Group/Country economic or political changes. At least twice a year.

- Diversification of the sources of information : 26 approved sources

- Cover attitude : ICIEC developed specific confidential cover attitude for countries (open account, special condition required, only covered business covered).

- CRAD : (Country Risk Analysis Division) in charge of grading countries and updating the underwriter with any relevant information about the country risk and sector.

22 Member of Islamic Development Bank Group

- Exit strategy : depending on country situation (economic, political), sector involved (life cycle), buyer/group situation (late payments), adverse information reported.

- Reinsurance support : RFA and Quota share treaty

- Technical task force : (livestock business)

- Buyer due diligence visit : For high limit

23 Member of Islamic Development Bank Group

Thank you

Any comments?