Budgeting, Accounting & Financial Management

plus

Types of Budgets & the Budget Process

57.508-201

The Budget as a Policy, Planning and Information ToolWeek 3 - Spring 2011

U.S. Public Budgeting History

It’s a loooooooooong wayfrom

New York City, NY

to

Sunnyvale, CA

Budget

Q: What is a budget?

Budget

budg et ⋅ [buhj-it] noun

1. An estimate of expected income and expense for a given period

2. A plan of operations based on such an estimate

3. An itemized allotment of resources for a given period

4. The total sum of money set aside or needed for a purpose

Why Public Budgets?

Q: Why do we need public budgeting?

Why Public Budgets?

• Financial Control• Management Improvement• Planning • Prioritization • Accountability

When Public Budgets?

“At the turn of the century the United States was the only great nation without a budget system.”

Arthur Buck (1929)

Budgeting History

Congress, state legislatures, city councils, etc., voted on the money needed to operate their governments in an ad hoc and haphazard manner

Budgeting, to the extent that it existed at all, was the responsibility of the legislative branch

Budgeting History

It was the larger cities in the 19th Century that inspired budget reform because of the patronage-based political machines of the time

Urbanization, industrialization, immigration, etc., drove the growth of cities and their need to spend on a range of public facilities services

Budgeting History

The professional public administration movement was born in the 1880s with an emphasis on efficiency and objective analysis of administrative practices to find the best way to perform a task

Woodrow Wilson , 28th President of the U.S.

PhD in political science

President of Princeton University

Budgeting History

Very influential in promoting municipal finance reform was the New York Bureau of Municipal Research created in 1907

Early Budgeting

• Requests were lump sum

• Little or no supporting data

• Overall spending not related to revenue projections

• Little standardization accounting practices

• Departments bargained with legislators directly

• Little central oversight existed

Early Budgeting

The most significant fiscal reform was the concept of an executive budget

Early Budgeting

First budgets were “object-of-expenditure”

• Had estimated revenues and expenses• Some accompanying support information• Line-item identifying expenditures

– Personnel– Supplies– Capital Items

Early Budgeting

As early as 1924, there was recognition of the limits of line-item budgeting

“The average city official confronted with the budget finds nothing in it that enables him to determine in a large way the value of the activities that are rendered the public; or in lesser way the degree of efficiency with which such activities are conducted.”

Lent D. Upson

Origins of Performance Budgeting

In the 1930s, NY Bureau of Municipal Research had recommended that city budgets be on a unit cost basis and show work done as well as work, but it took nearly 40 years for it to catch on

See: Commission on Organization of the Executive Branch of Government

&

Municipal Finance Officers Association Model

Origins of Performance Budgeting

1940s

Government program expansion during the New Deal and WW II led to wider interest in performance budgeting in order to more efficiently use financial resources by focusing on activities and outputs

Origins of Performance Budgeting

• Criticized even by reformers

• No more useful than line-item budgets

• Work measurement presented problems

• Inputs could be easily measured, but not outputs

• Focused only on what had been accomplished

• Lacked the tools to support long-range planning

Origins of Program Budgeting

1960s

More forward looking while performance budgeting tended to focus on past accomplishments…

Its key elements:

• Long-range planning• Goal setting• Program identification• Quantitative cost-benefit analysis • Performance analysis

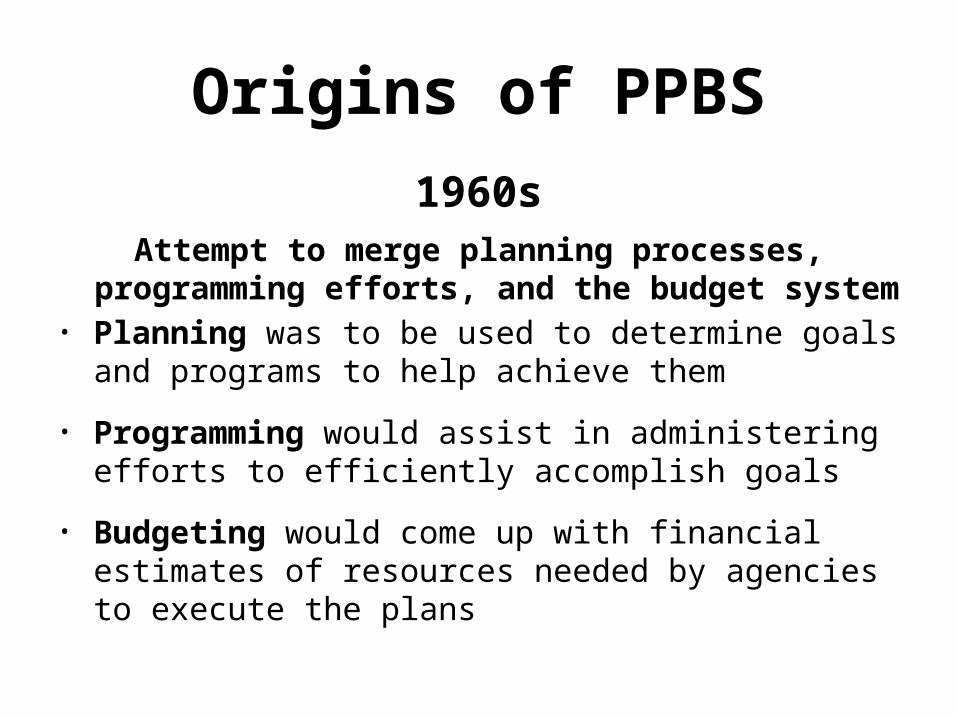

Origins of PPBS

1960sAttempt to merge planning processes, programming efforts,

and the budget system • Planning was to be used to determine goals and programs to

help achieve them

• Programming would assist in administering efforts to efficiently accomplish goals

• Budgeting would come up with financial estimates of resources needed by agencies to execute the plans

Origins of Zero-Based Budgeting

1970s

• Peter Pyhrr of Texas Instruments in Harvard Business Review• Jimmy Carter as GA Governor & US President• Required that programs be annually justified • Managers provided estimates of different levels of funding

– Below current levels– At the current levels– Above the current levels

• A few cities experimented with it, no other states• No panacea against cost increases and anti-tax militancy

Budget Reform

“Budget reform is a continuous, on-going process which is not a destination but a pilgrimage – never perfect, but being perfected – as the light of experience and careful research point the way to greater improvements in the management of public affairs”

Catheryn Seckler-Hudson

Dean of the School of Government

American University 1953

Budget Reform

“Historically, state and local governments have often innovated first successfully and then the innovation has spread to the federal government. Budget innovations have been, and continue to be much more widely adopted and implemented at state and local levels.”

Irene S. Rubin

“Budget Theory and Budget Practice: How Good the Fit?”

Public Administration Review 1990

Budget Reform

“At the municipal level in the United States, many proposed budget reforms have been adopted in whole or in part and have been adapted to the needs and capacities of the local communities. Sometimes it has taken cities many years to implement the changes because they did not have the necessary information base, accounting system or staff time. Sometimes the reform has been interrupted or delayed, or even lost, but budget changes can and do occur gradually.”

Irene S. Rubin

“Budget Theory and Budget Practice: How Good the Fit?”

Public Administration Review 1990

Budget Reform

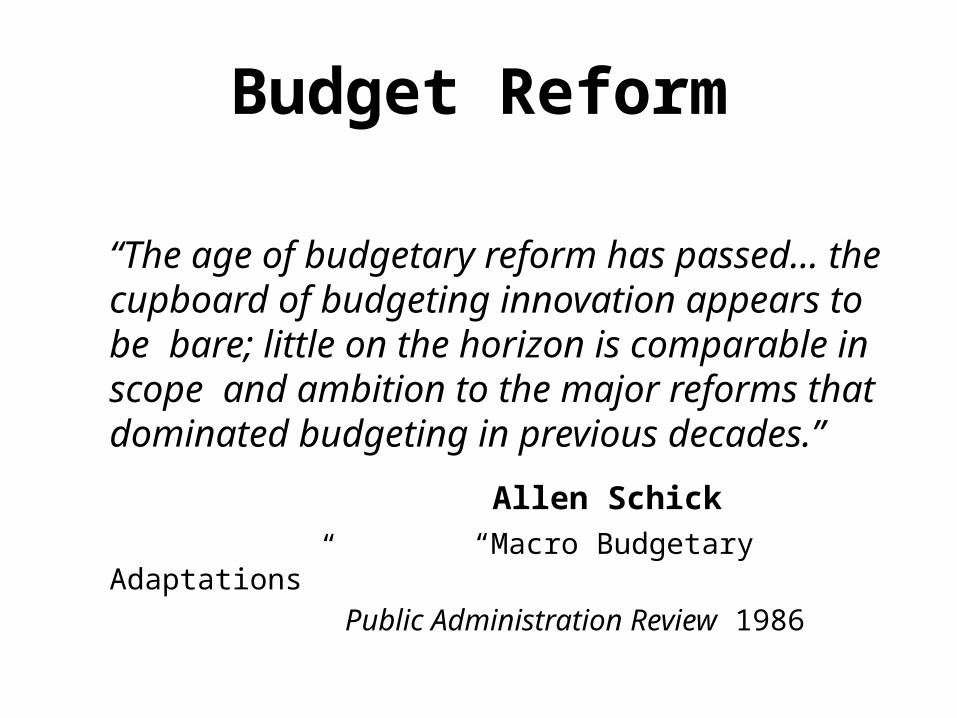

“The age of budgetary reform has passed… the cupboard of budgeting innovation appears to be bare; little on the horizon is comparable in scope and ambition to the major reforms that dominated budgeting in previous decades.”

Allen Schick

“Macro Budgetary Adaptations”

Public Administration Review 1986

Budget Reform

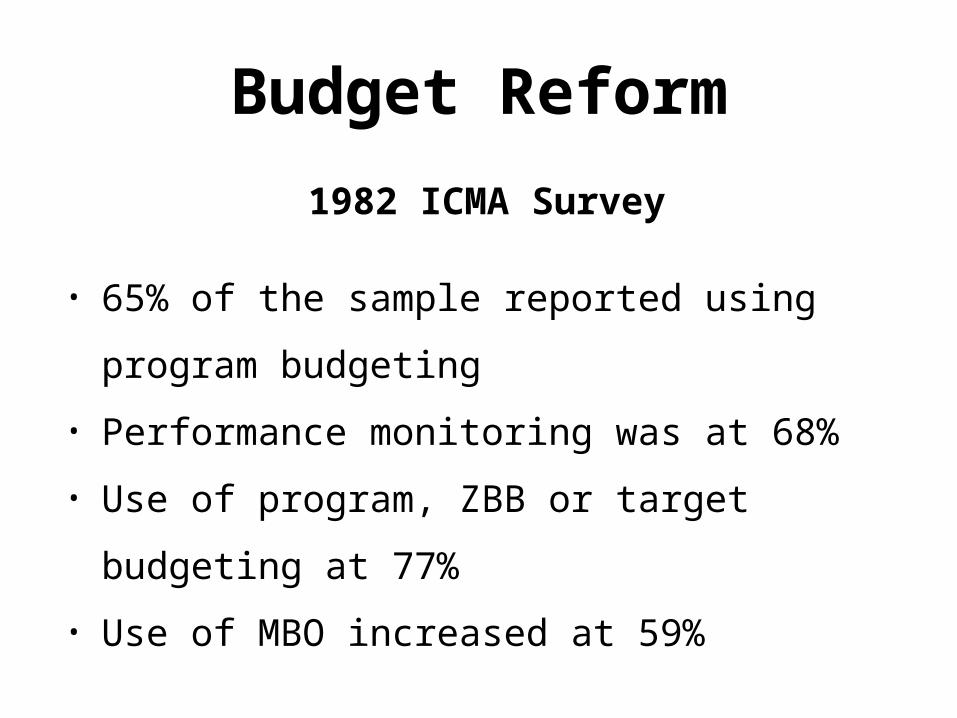

1982 ICMA Survey

• 65% of the sample reported using program budgeting

• Performance monitoring was at 68%

• Use of program, ZBB or target budgeting at 77%

• Use of MBO increased at 59%

Budget Reform

“While many reformers were concerned to limit the growth of government and the access of special interests, it mattered to them how it was to be done.”

Irene S. Rubin

“Budget Theory and Budget Practice: How Good the Fit?”

Public Administration Review 1990

Budget Reform

“Current models of budgeting for outcomes perfectly express the activist, efficiency, and accountability goals of the early reformers”

Irene S. Rubin

“Budget Theory and Budget Practice: How Good the Fit?”

Public Administration Review 1990

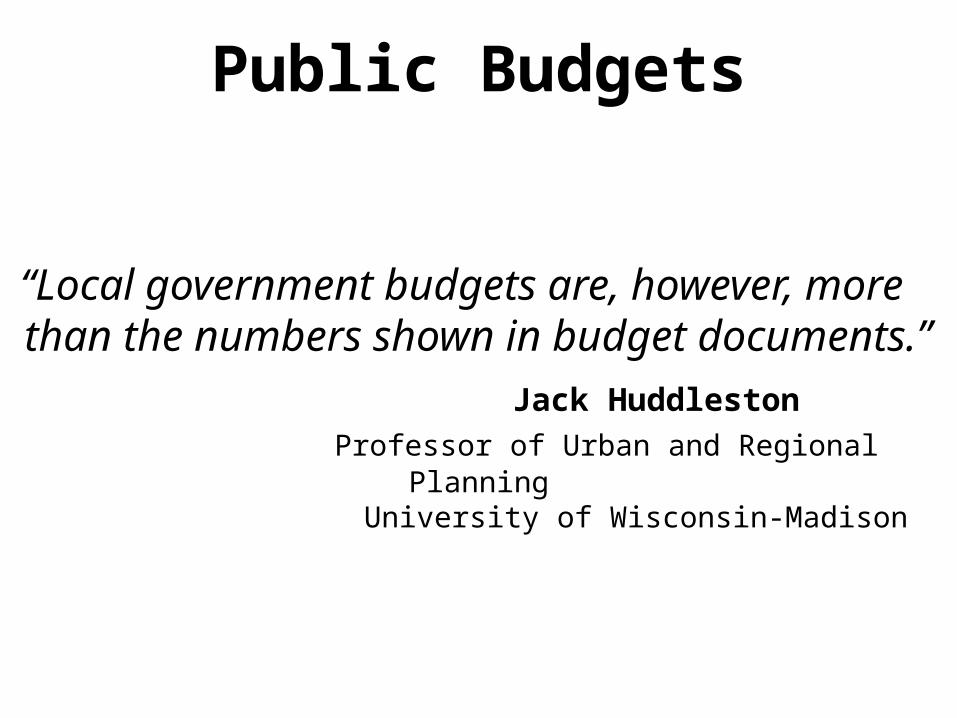

Public Budgets

“Local government budgets are, however, more than the numbers shown in budget documents.”

Jack Huddleston

Professor of Urban and Regional Planning University of Wisconsin-Madison

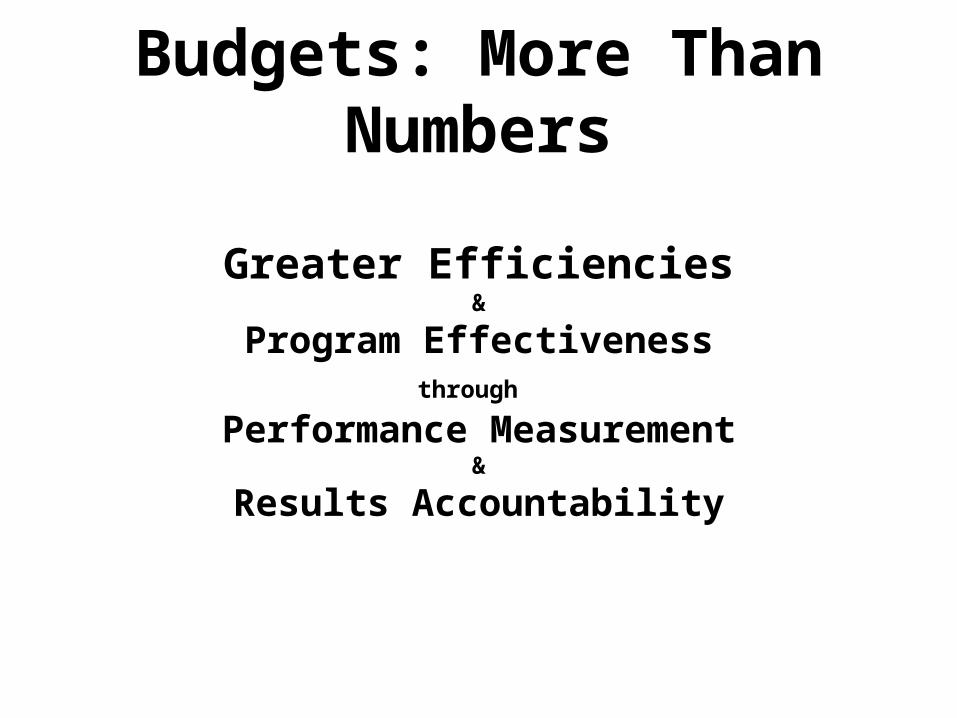

Budgets: More Than Numbers

Greater Efficiencies&

Program Effectivenessthrough

Performance Measurement&

Results Accountability

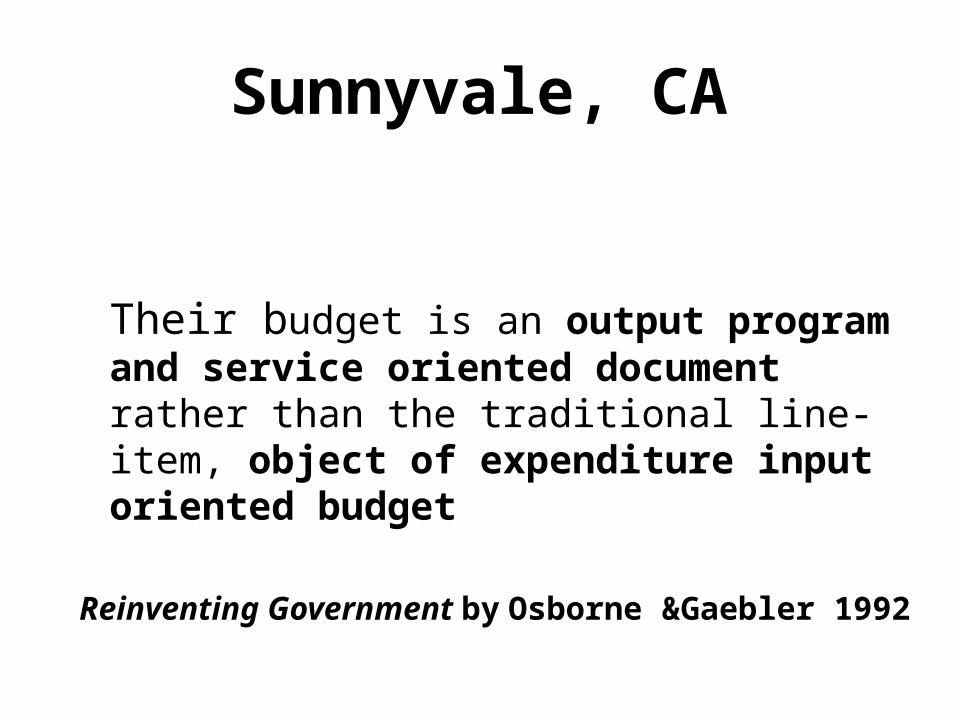

Sunnyvale, CA

Unique in its application of performance measurement and budgeting at the local government level

• “General Plan” projects 5 to 20 years into the future • The plan comprises seven elements and 20 sub-

elements that set goals and policies for the city • “Resource Allocation Plan” is a 10-year budget to

implement the General Plan• Annual budget is a performance budget that targets

specific service objectives and productivity measures

Sunnyvale, CA

Their budget is an output program and service oriented document rather than the traditional line-item, object of expenditure input oriented budget

Reinventing Government by Osborne &Gaebler 1992

Rock Hill, SC

• “Strategic Budgeting”

• Very different from Sunnyvale

• Declining economic base vs. Silicon Valley

• 1/3 size, blue collar population

• GFOA Distinguished Budget Award

Rock Hill, SC• Budget process built on comprehensive strategic plan

• Budget is a policy guide, a financial plan, an operational guide, and a communications device

• Budget includes all funds and addresses all organizational needs through goals and objectives

• No expenditure line-items in the budget

• Expenditures are summarized in terms of program goals, objectives and performance measures

• Uses multi-year time horizons

Rock Hill, SC & Sunnyvale, CAhttp://www.cityofrockhill.com/dynSubPage.aspx?deptID=7&pLinkID=144

http://sunnyvale.ca.gov/Departments/Finance/BudgetDocuments.aspx

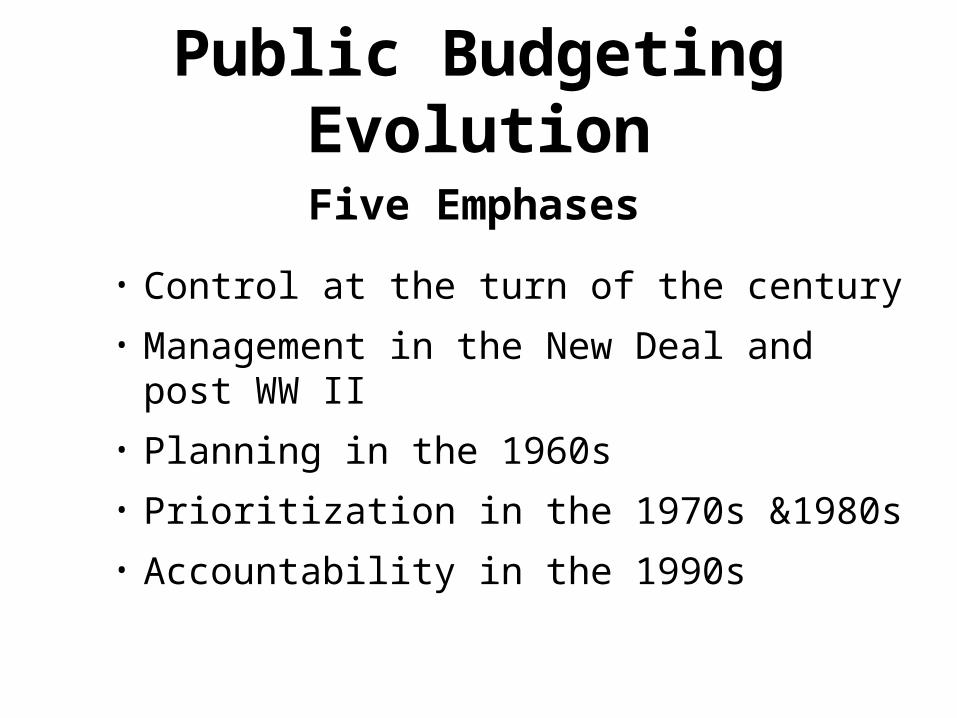

Public Budgeting Evolution

Five Emphases

• Control at the turn of the century

• Management in the New Deal and post WW II

• Planning in the 1960s

• Prioritization in the 1970s &1980s

• Accountability in the 1990s

Where We Are Heading:

Best Practices &

Responsibilities

FrameworkSet Goals to Guide Decision Making

• Assess community needs, priorities, challenges and opportunities

• Identify opportunities and challenges for services & assets

• Develop and disseminate broad goals

Develop Approaches to Achieve Goals

• Develop financial policies

• Develop programmatic, operating and capital plans

• Develop programs & services consistent with policies and plans

• Develop management strategies

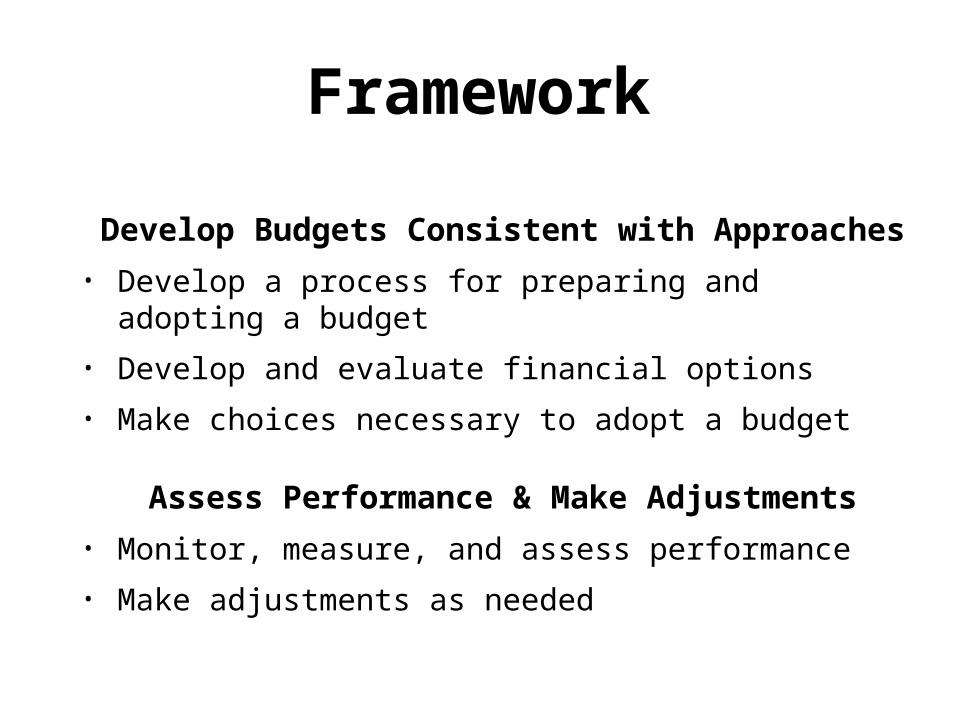

Framework

Develop Budgets Consistent with Approaches

• Develop a process for preparing and adopting a budget

• Develop and evaluate financial options

• Make choices necessary to adopt a budget

Assess Performance & Make Adjustments

• Monitor, measure, and assess performance

• Make adjustments as needed

Generally Accepted Accounting Principles

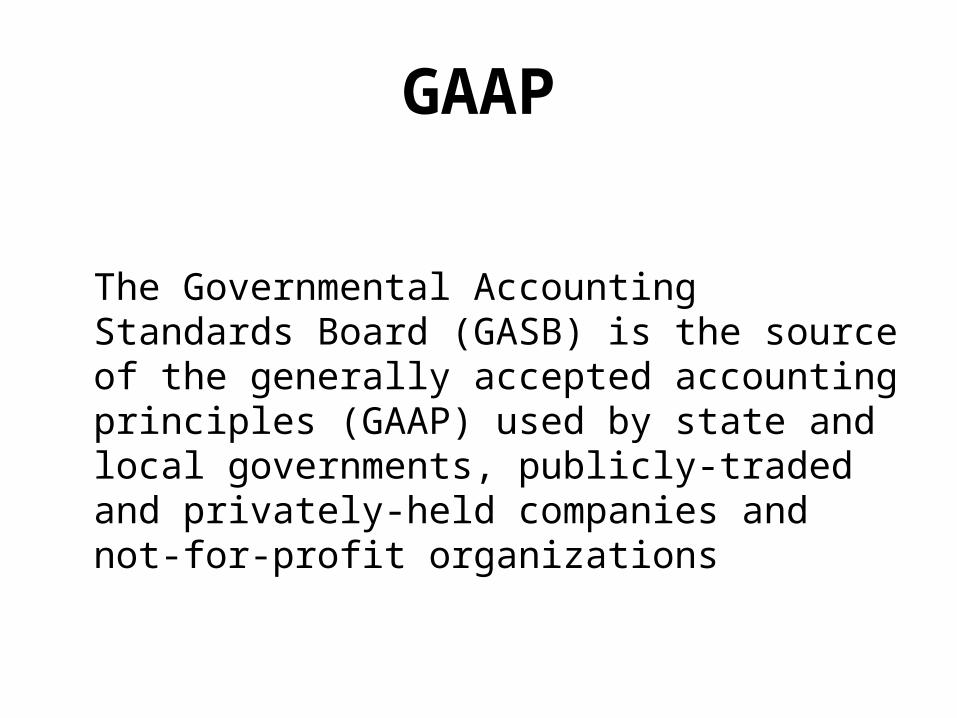

GAAP

The Governmental Accounting Standards Board (GASB) is the source of the generally accepted accounting principles (GAAP) used by state and local governments, publicly-traded and privately-held companies and not-for-profit organizations

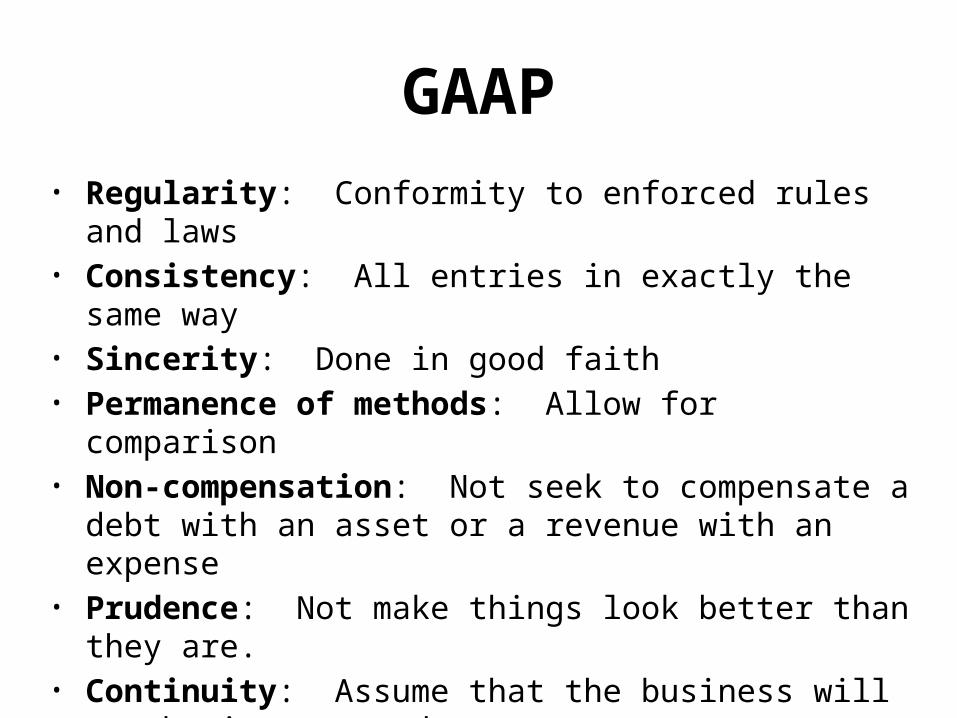

GAAP• Regularity: Conformity to enforced rules and laws• Consistency: All entries in exactly the same way• Sincerity: Done in good faith• Permanence of methods: Allow for comparison• Non-compensation: Not seek to compensate a debt with an

asset or a revenue with an expense• Prudence: Not make things look better than they are. • Continuity: Assume that the business will not be interrupted • Periodicity: Each entry should be allocated to a given period • Full Disclosure/Materiality: All information must be disclosed

Fund Accounting

Governments & NGOs practice fund accounting

Rule: All revenues are designated to be deposited in a particular fund and every item of expenditure comes from some particular fund

Principle: An obligation for reporting to financial statements users to show how money is spent

Fund Structure

• General Fund• Special Revenue Fund• Capital Projects Fund• Debt Service Fund• Enterprise Fund• Internal Service Fund• Special Assessment• Trust and Agency (3rd party)

Auditing

Government Auditing Standards

Generally Accepted Government Auditing Standards (GAGAS)

Standards for audits of “government organizations, programs, activities, and functions, and of government assistance received by contractors, nonprofit organizations, and other nongovernment organizations.”

Budgeting Interrelationship• Both budgeting and accounting are fiscal systems or processes

that involve the allocating, and disbursing of resources

• This results in an interrelationship and a need for coordination between these two fiscal disciplines

• Budgeting is regarded more in terms of planning, preparing and executing a fiscal plan for a period of time

• Budgeting processes are dependent upon the accounting of past-year and current-year expenditures/revenues

• Accounting focuses on the recording, classifying, and interpreting of financial transactions

Budgeting Interrelationship

• Budget and accounting systems function independently

• Each supports the other

• They represent two independent cycles that intersect

• Information produced by one is input for the other

3 Rs of Accounting

• Recording– Each transaction entered into journal– Each has one debit entry and one credit entry– Fund balance = Assets - Liabilities

• Reconciling– Journal entries to a ledger (spreadsheet) – Reorganizes the journal information by accounts (funds)

• Reporting– Financial reports: interim & CAFR– Subject to examination by an external auditor

Budgeting Interrelationship

While each government / nonprofit develops its own processes and rules for budgeting, accounting relies on a common set of rules – GAAP & GAGAS

http://gaqc.aicpa.org/

Types of Budgets & the Budget Process

57.508-201

The Budget as a Policy, Planning and Information ToolWeek 3 - Spring 2011

Budgets as Financial Plans

Most Common Operating Budget Formats

• Line-Item• Program• Performance

Line-Item Budget

• Input oriented & built from the bottom up• Optimizes the control function• Usually only three categories:

– Personnel (salaries, benefits, retirement, etc.)

– Operating Expenses (materials & services consumed )

– Debt Service• Expenditures drive policy• Manager not encouraged to question priorities

Line-Item Budget

• Used by all types of entities

• Survived in the face of reform efforts

• Users feel comfortable

• Easiest for year-to-year comparisons

• Minimizes policy debate

• Limits administrative liberties

• Framework for accountability

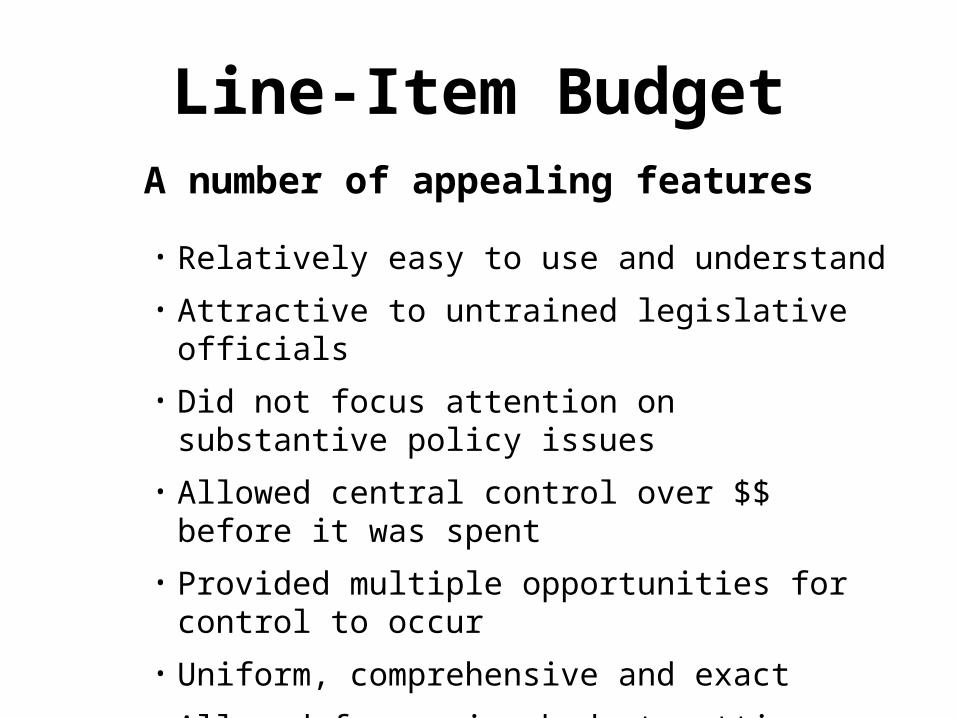

Line-Item BudgetA number of appealing features

• Relatively easy to use and understand

• Attractive to untrained legislative officials

• Did not focus attention on substantive policy issues

• Allowed central control over $$ before it was spent

• Provided multiple opportunities for control to occur

• Uniform, comprehensive and exact

• Allowed for easier budget cutting

Line-Item Budget

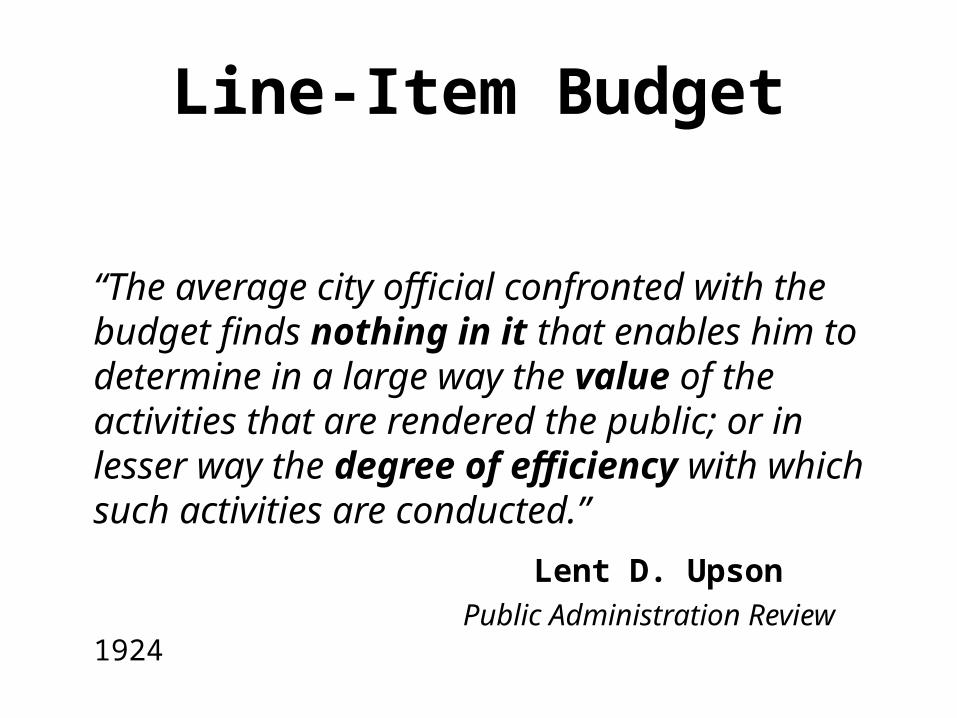

“The average city official confronted with the budget finds nothing in it that enables him to determine in a large way the value of the activities that are rendered the public; or in lesser way the degree of efficiency with which such activities are conducted.”

Lent D. Upson

Public Administration Review 1924

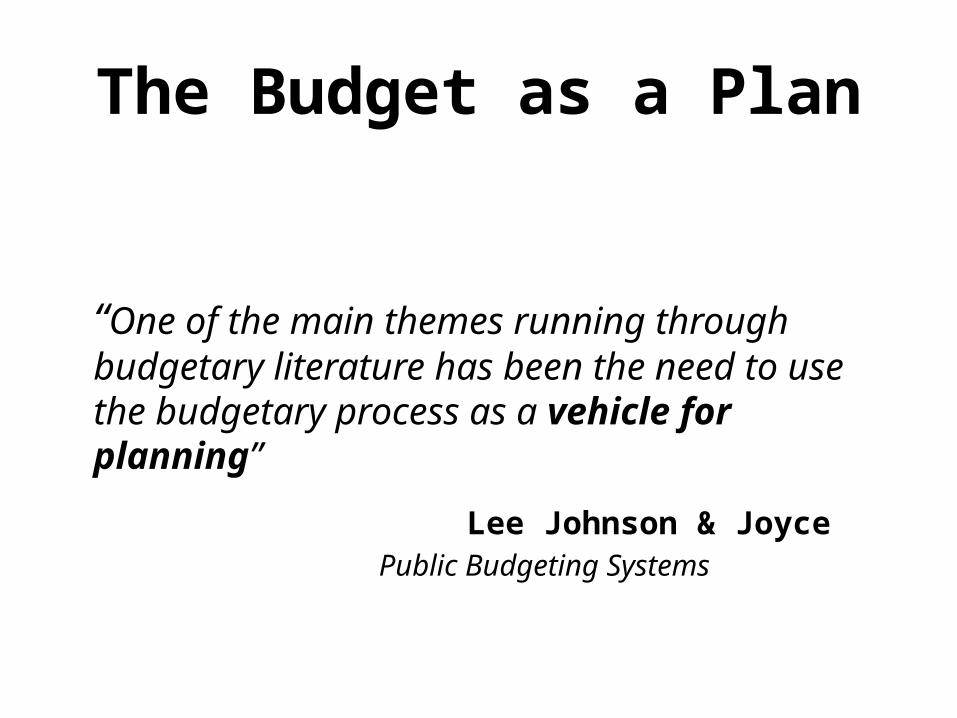

The Budget as a Plan

“One of the main themes running through budgetary literature has been the need to use the budgetary process as a vehicle for planning”

Lee Johnson & Joyce

Public Budgeting Systems

Program Budget

• Outcome or result oriented

• Focus on policy and program effectiveness

• Less concerned with expenditure control

• Very top down

• Requires regular affirmation of the mission

• Requires evaluation of programmatic activity

• Functions cut across agencies

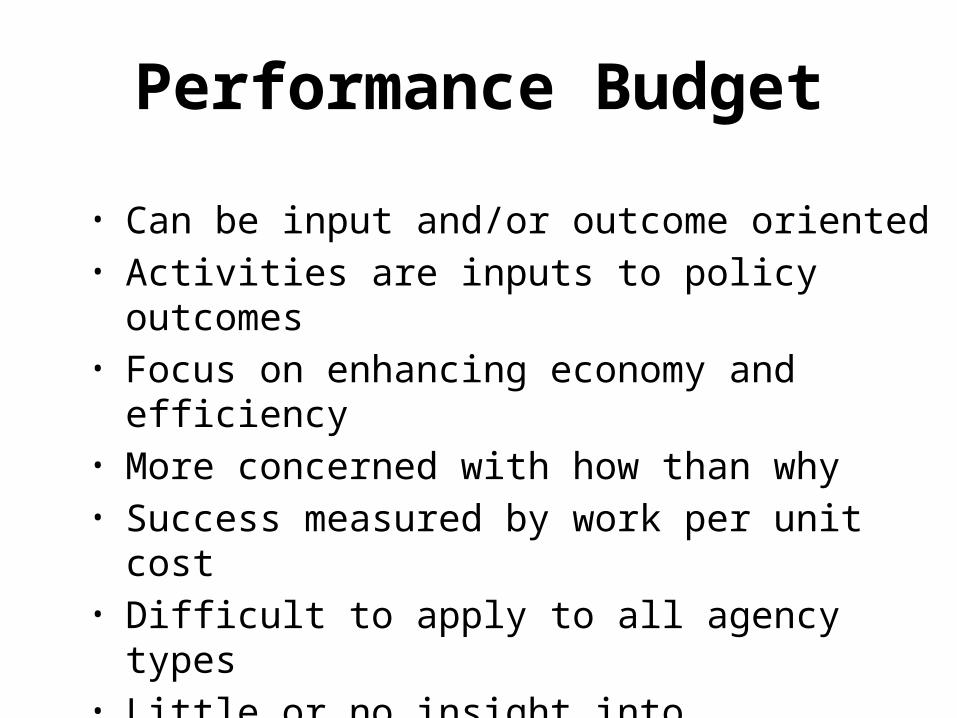

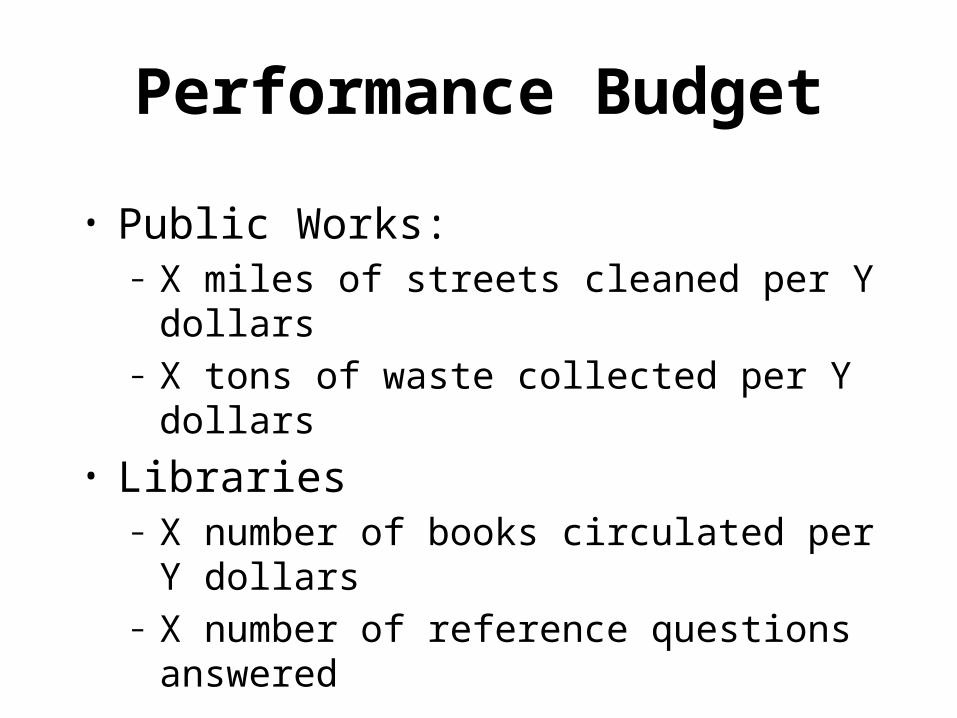

Performance Budget

• Can be input and/or outcome oriented• Activities are inputs to policy outcomes• Focus on enhancing economy and efficiency• More concerned with how than why• Success measured by work per unit cost• Difficult to apply to all agency types• Little or no insight into effectiveness or results• Rarely used alone at the local level

Performance Budget

• Public Works:– X miles of streets cleaned per Y dollars– X tons of waste collected per Y dollars

• Libraries– X number of books circulated per Y dollars– X number of reference questions answered

• Police? Planning? Finance? Education?

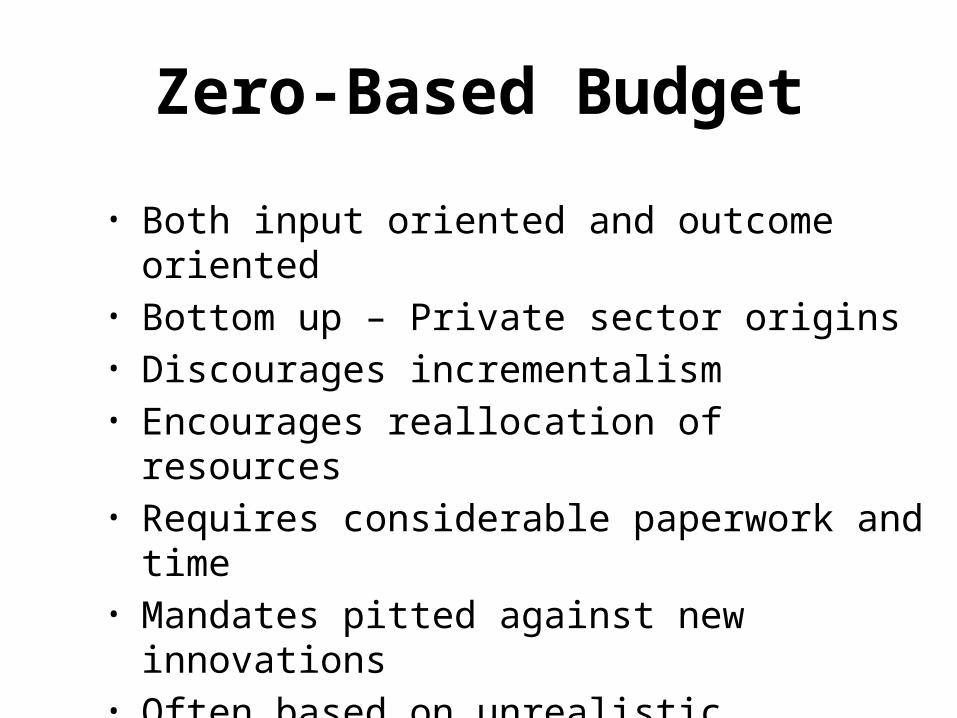

Zero-Based Budget

• Both input oriented and outcome oriented• Bottom up – Private sector origins• Discourages incrementalism• Encourages reallocation of resources• Requires considerable paperwork and time• Mandates pitted against new innovations• Often based on unrealistic assumptions• May be better applied to select programs

Other Budget Formats

• Results Oriented Budgeting

• Target Based Budgeting

• Functional Budgeting

• Planning-Programming-Budgeting System

• Management by Objectives (MBO)

• Formula Budgeting

Optimum Format?

• Control and Comfort of Line-Item• Policy Focus of Program• Efficiency Focus of Performance• Anti-incrementalism of Zero-Based

• Reality:– Managers inherit their entity’s budget– Professional administration vs. organization’s politics

Budget ProcessSeven Steps

1. Executive and staff preparation

2. Submission to policy body budget committee

3. Policy deliberations, amendments and revisions

4. Adoption

5. Execution

6. Evaluation

7. Audit

1. Preparation

• Mayor, manager, executive sends out memo

• Departments and agencies submit requests

• Budget office receives and reviews requests

• May make initial cuts if requests unjustified

• Each agency or program head biased

• Executive makes the tough calls

• Executive prepares budget message

Revenue Forecasting

• Each revenue source analyzed• Investment opportunities and rates• Previous year results plus trend projections• Techniques:

– Regression & multiple regression analysis – General Adaptive Filtering– Econometric modeling– Box-Jenkins

2. Submission

• Draft budget with message sent to policy body

• City council, county legislature, town board, etc.

• Finance committee reviews budget requests– Sometimes invites in all department heads– Sometimes executive represents all requests– Sometimes conflicts between executive & departments– Politics and reality at play

3. Policy Deliberations

• City council or board of aldermen

• Town council or board of selectmen

• County legislature or board of supervisors

• School board

• Regional council or COG governing board

• NGO Board of directors

4. Adoption

• “Ways & Means” looks at expected revenues

• Public hearings held

• Fixed costs & entitlements vs. discretionary

• Council or board members propose changes

• Changes voted on individually

• Consensus achieved on bottom lines

• Full council or board adopts with amendments

5. Execution

• Starts on the 1st day of the new fiscal year• Cash flow… spending rate based on receipts• Investing temporary surplus funds• Inter-department transfers approved by executive• Intra-department transfers approved by departments• Major changes handled by contingency budget• Sort term borrowing (vs. pension fund raids)

• Encumbrances for future payments

Role of the Budget Office

• Management controls

• Accounting system operations

• Reviewing agency or department procedures

• Setting rules for consultants or travel

• Protecting against fraud & waste

• Overseeing agency or department compliance

• Reporting on organization performance

Subsystems of Budget Execution

• Revenue Administration

• Cash Management

• Procurement

• Risk Management

Revenue Administration

• Taxes– Determining the tax– Applying the tax– Collecting the tax– Enforcing the law

• Fees, sales, grants, gifts, loans, etc.

• Investment management

Cash Management

• Depositing revenue promptly

• Expenditure planning

• Paying bills promptly

• Short term borrowing

• Contingency funds

• Investment planning and management

Procurement• System with unambiguous and precise policies• Centralized vs. decentralized• Group or contract purchasing• Low cost, timely delivery, quality product• Bid procedures, RFPs• Purchase vs. lease• Outsourcing & privatizing• Contract management • Efforts to ensure competition, public notice, etc.• Can further policies like…

– MBEs & WBEs– Energy efficiency or environmental quality

Risk Management

• People, property and records to protect

• Liability, exposure to litigation

• Faulty equipment or hazardous location

• Identify probability of extreme events

• Insurance vs. self-insuring

• Premiums, awards, settlements, etc.

6. Evaluation

• The budget as a management tool

• Program efficiency and effectiveness

• Performance measures

• Budget office oversight

• Legislative or policy body oversight (budget committee)

7. Audit

• Compliance Audit– According to laws and regulations

• Management Audit– Review for economy and efficiency

• Program Audit– Are results being achieved

• Can be either internal or external

Budget Cycle

• Preparation begins months ahead

• One prepared while one being executed

• Fiscal years vary (calendar vs. quarter)

• Intergovernmental cycles overlap

• Local level most dependent upon others

• Mandates, local aid, grants, tax rates

Budget Overlap

• Cycles run into one another• Preparation for next fiscal year in last• Audits for last fiscal year in next• Carry-over from FY to FY

– Encumbrances– Contingency funds– Debt service

Fund Structure

• General Fund• Special Revenue Fund• Capital Projects Fund• Debt Service Fund• Enterprise Fund• Internal Service Fund• Special Assessment• Trust and Agency (3rd party)

Accounting and Controls• Recording all financial transactions• Accrual or modified accrual basis accounting• GAAP & GASB (Governmental Accounting Standards Board)

• Budget oversight and expenditure monitoring• Revenue monitoring• Program or outcome monitoring• Purchasing controls• Staffing changes• Supplemental appropriations

Program Audits

• Formal and informal evaluations

• Data collected and analyzed

• Cost-benefit analysis

• Many problems with results measurement

• Many problems with activity costing

• Central vs. program analytical responsibilities

Intergovernmental Interrelationships

Intergovernmental Relations

The body of activities and interactions occurring between governmental units at the various levels

Most basic & significant: fiscal relations

Main instruments: • Grants

– block grant– categorical grants

• Revenue sharing • Intergovernmental transfers• Direct payment to individuals

(Recommended a new revenue sharing formula)

Intergovernmental Relations

Federal-state, interstate, state-local arrangements for the provision of services

• Multiple levels delivering services• Transferring responsibilities and priorities• Vertical imbalance

– Best level to deliver service?– Best level to pay for it?

• Inadequate funding to meet local needs• National standards equal unfunded mandates?

Whose Responsibility?• Greatest local autonomy, but…

– Federal revenue sharing– Block grants– Categorical aid (WIC, food stamps)

• National issues vs. state or local priorities• Differences in political philosophies• Differences in income and wealth

– U.S. per capita income = $38k– Mississippi per capita income = $27k– Connecticut per capita income = $51k

• Results in different levels of service

Whose Responsibility?

Q: Who is responsible for…

• National defense• Public education• Welfare / public assistance• Environmental protection• Land use and building regulation• Community development

Whose Responsibility?

Q: Who is responsible for adequate housing?

a) Local governments

b) State governments

c) Federal government

d) The free housing market

e) Evil greedy housing developers

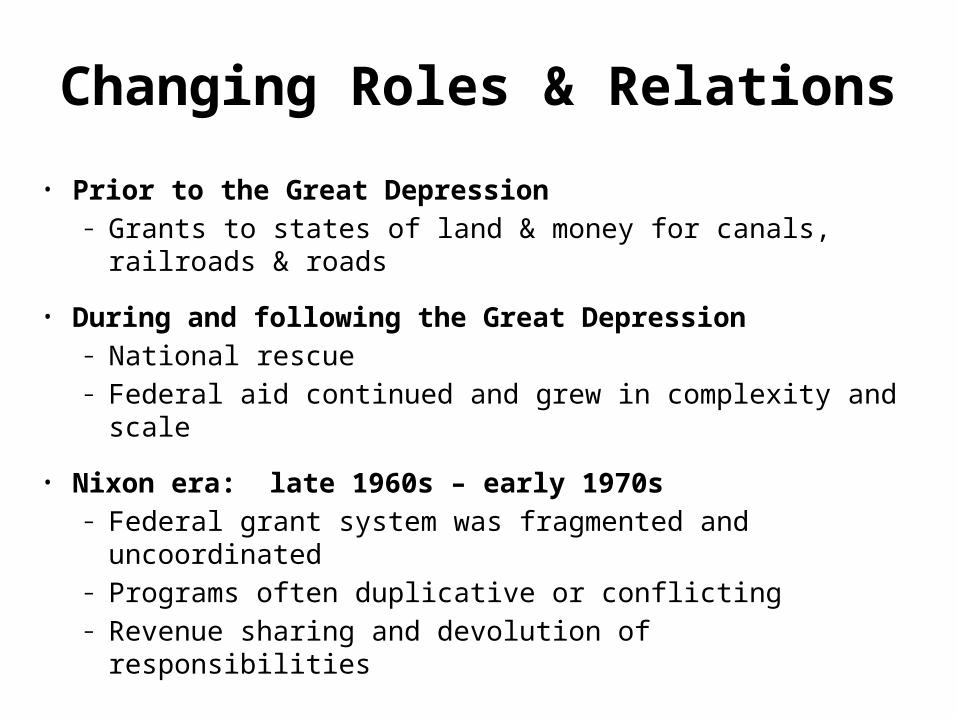

Changing Roles & Relations

• Prior to the Great Depression – Grants to states of land & money for canals, railroads & roads

• During and following the Great Depression– National rescue– Federal aid continued and grew in complexity and scale

• Nixon era: late 1960s – early 1970s– Federal grant system was fragmented and uncoordinated– Programs often duplicative or conflicting– Revenue sharing and devolution of responsibilities

Changing Roles & Relations• Reagan era: 1980s

– Consolidation of categorical grants into block grants– Further devolution of responsibilities downward– Massive federal deregulation – “New Federalism”

• “Contract with America”: early-mid 1990s“Block grants should be used to restore discretion to the states because they are more knowledgeable about their own circumstances.” Gingrich– The Fiscal Responsibility Act– The Personal Responsibility Act– The Family Reinforcement Act

• Clinton era: later 1990s– Welfare Reform of 1996

Major Issue with Devolution

While the gross dollar figure has risen each year, federal aid as a percentage of state & local revenues has declined since 1980

• 1980 = 27%• 2007 = 17%

Devolution means shifting or transferring power

Devolution has meant reduction in federal aid

Impact of New Federalism

Q: What’s been the effect of the changing responsibilities roles and relationships on the financial health of cities, counties & states?