www.bricdata.com

Australian Mining Industry

Outlook – Market Opportunities

and Entry Strategies, Analyses

and Forecasts to 2016

Industry Forecast Report

Reference code: MN0040MR

Published: March 2012

BRICdata

John Carpenter House

7 Carmelite Street

London EC4Y 0BS

United Kingdom

Tel: +44 (0) 20 7936 6400

Fax: +44 (0) 20 7336 6813

www.bricdata.com

EXECUTIVE SUMMARY

Australian Mining Industry Outlook – Market Opportunities and Entry Strategies, Analyses and

Forecasts to 2016 Page 2

© BRICdata. This product is licensed and is not to be photocopied Published: March 2012

1 Executive Summary

Australia is one of the leading producers of several minerals within the global mining industry. Australia possesses

substantial deposits of a variety of minerals, including iron ore, nickel, bauxite, copper, gold, silver, uranium, diamonds,

zinc and coal. BRICdata expects that the volume of minerals produced from the Australian mining industry will increase

from XXX.X million tons in 2011 to X.X billion tons in 2016, at a compound annual growth rate (CAGR) of X.XX% over the

forecast period (2012–2016). This growth will be influenced by the relatively low value of mining in 2011, since flooding in

the country postponed mining activities. However, the growth in mining production volume will also benefit from the

completion of new mining projects across the country, most notably projects by Rio Tinto, BHP Billiton and Xstrata.

Iron ore and bauxite production volume growth

Australia’s iron ore production output is expected to record the highest growth rate, at a CAGR of X.XX% over the forecast

period, with the country’s iron ore production increasing from XXX million in 2011 to XXX.X million tons in 2016. Since iron

ore accounts for the largest proportion of around XX% of the mining industry's output value, this rising iron ore production

volume will have a positive impact on the Australian mining industry value. The growth in iron ore production will be driven

by the mining project expansion activities of BHP Billiton and Rio Tinto. BHP Billiton is expected to increase its iron ore

output in its Western Australian operations from XXX million tons per annum (mtpa) to XXXmtpa in 2014. Meanwhile, Rio

Tinto is anticipated to increase its production in its Pilbara operations from XXXmtpa to XXXmtpa in 2015.

BRICdata also expects that Australia will remain the world's largest bauxite producer by recording average annual output

growth rates of X.X% over the forecast period, to increase output from XXmtpa in 2010 to 99.7mtpa in 2016. The vast

majority of this growth is due to expansion plans at Rio Tinto's Weipa mine, the world's largest bauxite mine, which is

expected to increase production volume from XXmtpa to XXmtpa in 2013.

Changing coal dynamics

Australia’s coal production output is expected to record average annual growth rates of X.X% over the forecast period,

from XXXmtpa in 2011 to XXXmtpa in 2016. The BRICdata forecast for coal production in Australia was revised down

from XXXmtpa to XXXmtpa in 2011, due to the effects of flooding which postponed mining production in Queensland at

the start of the year. BRICdata expects there will be significant changes in the global coal production dynamics over the

forecast period, which could have a substantial impact on global shipping and infrastructure. It is anticipated that

Australia’s coal exports to China and India will reduce over the forecast period, as Indonesia plans to increase its domestic

coal consumption and Australia's taxes on carbon emissions and coal mining profits are likely to deter investment.

Meanwhile, Australia’s coal imports are expected to be replaced by the increased coal production in Southern Africa and

the US. Several coal production projects have been announced in Mozambique and South Africa, and the vast majority of

coal produced in these products will be exported as there is currently little demand for coal in the local region.

Changing regulatory environment

Australia's mining industry is one of the most attractive for investments in the world, and there are both domestic and

foreign mining companies operating in the country. Australia is expected to remain a highly attractive destination for

foreign investment, despite the proposed XX% tax on mining companies' profits in coal and iron ore production. The

proposed tax is not expected to have a significant impact on investments in the Australian mining industry, as investors

concerns regarding the tax are expected to be outweighed by the country's large mineral wealth. Moreover, the proposed

tax could be reduced as the ruling coalition only has a one seat majority, and it may be difficult to get the bill passed

through parliament without compromise. If the bill is implemented, it is expected to become effective from July 2012.

Investments announced despite proposed tax on mining

The proposed XX% tax on mining company profits has not significantly affected investments in the Australian mining

industry, since several new coal and iron ore mining projects were announced in the country after the tax was first

proposed. Xstrata and CBH Resources plan to add another XXmtpa to their coal product by 2013, while Rio Tinto and

Fortescue Metals have announced large-scale plans to increase their iron ore output by a total of XXXmtpa by 2015. Since

the announcement of the new tax, Rio Tinto has proceeded with investments worth US$X.X billion in new Australian

mining projects, and Xstrata has committed US$X.X billion in new coal mine investments. As such, the tax rise has not yet

significantly deterred investment in the Australian mining industry.

EXECUTIVE SUMMARY

Australian Mining Industry Outlook – Market Opportunities and Entry Strategies, Analyses and

Forecasts to 2016 Page 3

© BRICdata. This product is licensed and is not to be photocopied Published: March 2012

Competitive landscape

Due to its strong growth potential and high-quality infrastructure, Australia contains some of the leading companies within

the global mining industry. The multinationals operating in the Australian mining industry include Australian companies,

such as BHP Billiton and Newcrest Mining, and large foreign mining companies, such as Rio Tinto, Norilsk Nickel and

Xstrata. It is expected that Australia's mining industry will remain dominated by large miners, with the exception of coal,

which could become slightly more fragmented as Hancock Coal develops a XXmtpa Alpha coal mine project and Waratah

Coal develops a XXmtpa Galilee coal mine. These mines will begin to produce coal output from 2013. These projects are

the largest planned in the country’s coal production, which will enable the two companies to become significant coal

miners in Australia over the forecast period.

TABLE OF CONTENTS

Australian Mining Industry Outlook – Market Opportunities and Entry Strategies, Analyses and

Forecasts to 2016 Page 4

© BRICdata. This product is licensed and is not to be photocopied Published: March 2012

TABLE OF CONTENTS

1 Executive Summary ......................................................................................................................... 2 2 Mining Industry Outlook in Australia............................................................................................... 9

2.1 Mining Industry Market Size and Growth Potential .............................................................................. 9

2.2 Market Share and Production Trend Analysis by Mining Category .................................................... 10

3 Mining Industry Key Trends, Growth Drivers and Challenges ..................................................... 15

3.1 Key Trends and Growth Drivers ........................................................................................................ 15

3.2 End User Market Dynamics .............................................................................................................. 18

3.3 Macroeconomic Drivers .................................................................................................................... 21

3.6 Challenges ....................................................................................................................................... 26

4 Mining Equipment Market Size and Growth Potential .................................................................. 27 5 Regulatory Framework ................................................................................................................... 28

5.1 Regulation of Foreign Investments ................................................................................................... 28

5.2 Organization Health and Safety (OHS) Standards ............................................................................ 29

5.3 Market Entry Route .......................................................................................................................... 29

6 Benchmarking with Key Global Markets ....................................................................................... 31

6.1 Copper ............................................................................................................................................. 31

6.2 Diamond .......................................................................................................................................... 32

6.3 Iron Ore............................................................................................................................................ 33

6.4 Nickel ............................................................................................................................................... 34

6.5 Bauxite ............................................................................................................................................. 35

6.6 Gold ................................................................................................................................................. 36

7 Industry Structure and Dynamics of Coal, Metallic and Non-Metallic Mining ............................. 37

7.1 Five Forces Analysis: Coal ............................................................................................................... 37

7.1.1 Bargaining power of supplier: medium .............................................................................................. 38

7.1.2 Bargaining power of buyer: medium to high ...................................................................................... 38

7.1.3 Barrier to entry: medium ................................................................................................................... 38

7.1.4 Intensity of rivalry: medium ............................................................................................................... 38

7.1.5 Threat of substitution: medium to high .............................................................................................. 38

7.2 Five Forces Analysis: Metallic Minerals ............................................................................................ 39

7.2.1 Bargaining power of supplier: medium to high ................................................................................... 39

7.2.2 Bargaining power of buyer: low to high ............................................................................................. 40

7.2.3 Barrier to entry: medium ................................................................................................................... 40

7.2.4 Intensity of rivalry: low to medium ..................................................................................................... 40

7.2.5 Threat of substitution: low to medium................................................................................................ 41

7.3 Five Forces Analysis: Non-Metallic Minerals ..................................................................................... 42

7.3.1 Bargaining power of supplier: low to medium .................................................................................... 42

7.3.2 Bargaining power of buyer: low ......................................................................................................... 42

7.3.3 Barrier to entry: low .......................................................................................................................... 42

7.3.4 Intensity of rivalry: high ..................................................................................................................... 43

7.3.5 Threat of substitution: low ................................................................................................................. 43

7.4 Five Forces Analysis: Mining Equipment........................................................................................... 44

7.4.1 Bargaining power of supplier: low to medium .................................................................................... 44

TABLE OF CONTENTS

Australian Mining Industry Outlook – Market Opportunities and Entry Strategies, Analyses and

Forecasts to 2016 Page 5

© BRICdata. This product is licensed and is not to be photocopied Published: March 2012

7.4.2 Bargaining power of buyer: low to medium ....................................................................................... 44

7.4.3 Barrier to entry: medium ................................................................................................................... 44

7.4.4 Intensity of rivalry: medium to high .................................................................................................... 45

7.4.5 Threat of substitution: low ................................................................................................................. 45

8 Coal ................................................................................................................................................. 46

8.1 Overview of Coal Mining Category .................................................................................................... 46

8.2 Reserves, Production and Consumption ........................................................................................... 46

8.2.1 Total reserves .................................................................................................................................. 46

8.2.2 Total production ............................................................................................................................... 47

8.2.3 Total consumption ............................................................................................................................ 51

8.3 Imports and Exports ......................................................................................................................... 52

8.3.1 Coal import....................................................................................................................................... 52

8.3.2 Coal export....................................................................................................................................... 53

8.4 Top Active Projects .......................................................................................................................... 54

8.5 Key Processing Units ....................................................................................................................... 55

8.6 News and Deals ............................................................................................................................... 56

8.7 Competitive Landscape .................................................................................................................... 57

9 Iron Ore ........................................................................................................................................... 58

9.1 Overview of Iron Ore Mining Sub-Category ....................................................................................... 58

9.2 Reserves, Production and Consumption ........................................................................................... 58

9.2.1 Total reserves .................................................................................................................................. 58

9.2.2 Total production ............................................................................................................................... 59

9.2.3 Total consumption ............................................................................................................................ 63

9.3 Imports and Exports ......................................................................................................................... 64

9.3.1 Iron ore import .................................................................................................................................. 64

9.3.2 Iron ore export .................................................................................................................................. 65

9.4 Top Active Projects .......................................................................................................................... 66

9.5 Key Processing Units ....................................................................................................................... 67

9.6 News and Deals ............................................................................................................................... 68

9.7 Competitive Landscape .................................................................................................................... 69

10 Phosphate Rock ............................................................................................................................. 70

10.1 Overview of Phosphate Rock Mining Sub-Category .......................................................................... 70

10.2 Reserves, Production and Consumption ........................................................................................... 70

10.2.1 Total reserves .................................................................................................................................. 70

10.2.2 Production ........................................................................................................................................ 71

10.2.3 Consumption .................................................................................................................................... 75

10.3 Imports and Exports ......................................................................................................................... 76

10.3.1 Phosphate rock imports .................................................................................................................... 76

10.3.2 Phosphate rock export...................................................................................................................... 77

10.4 Top Active Projects .......................................................................................................................... 78

10.5 Key Processing Units ....................................................................................................................... 78

10.6 News and Deals ............................................................................................................................... 78

10.7 Competitive Landscape .................................................................................................................... 79

TABLE OF CONTENTS

Australian Mining Industry Outlook – Market Opportunities and Entry Strategies, Analyses and

Forecasts to 2016 Page 6

© BRICdata. This product is licensed and is not to be photocopied Published: March 2012

11 Salt .................................................................................................................................................. 80

11.1 Overview of Salt Mining Sub-Category ............................................................................................. 80

11.2 Reserves, Production and Consumption ........................................................................................... 81

11.2.1 Total reserves .................................................................................................................................. 81

11.2.2 Total production volume ................................................................................................................... 81

11.2.3 Total production value ...................................................................................................................... 83

11.2.4 Total consumption ............................................................................................................................ 85

11.3 Imports and Exports ......................................................................................................................... 86

11.3.1 Salt imports ...................................................................................................................................... 86

11.3.2 Salt exports ...................................................................................................................................... 87

11.4 Top Active Projects .......................................................................................................................... 88

11.5 Key Processing Units ....................................................................................................................... 88

11.6 News and Deals ............................................................................................................................... 89

11.7 Competitive Landscape .................................................................................................................... 89

12 Competitive Landscape and Strategic Insights ............................................................................ 90

12.1 Competitive Landscape: Overview .................................................................................................... 90

12.2 Key Companies ................................................................................................................................ 93

12.2.2 BHP Billiton Ltd: recent announcements and strategic initiatives ....................................................... 93

12.2.3 BHP Billiton Ltd: products ................................................................................................................. 94

12.2.5 Rio Tinto Ltd: recent announcements and strategic initiatives ........................................................... 96

12.2.6 Rio Tinto Ltd: products and services ................................................................................................. 97

12.2.7 Fortescue Metals Group Ltd (Fortescue): overview ........................................................................... 98

12.2.8 Fortescue Metals Group Ltd (Fortescue): recent announcements and strategic initiatives ................. 98

12.2.9 Fortescue Metals Group Ltd (Fortescue): products ........................................................................... 98

12.2.10 BlueScope Steel Ltd: overview ......................................................................................................... 99

12.2.11 BlueScope Steel Ltd: recent announcements and strategic initiatives................................................ 99

12.2.12 BlueScope Steel Ltd: products .......................................................................................................... 99

12.2.13 OZ Minerals: overview .................................................................................................................... 100

12.2.14 OZ Minerals Ltd: recent announcements and strategic initiatives .................................................... 100

12.2.15 Alcoa of Australia Ltd: overview ...................................................................................................... 101

12.2.16 Alcoa of Australia Ltd: recent announcements and strategic initiatives ............................................ 101

12.2.17 Alcoa of Australia Ltd: products and services .................................................................................. 101

12.2.18 Xstrata Australia: overview ............................................................................................................. 102

12.2.19 Xstrata Australia: recent announcements and strategic initiatives.................................................... 102

12.2.20 Xstrata Australia: products and services ......................................................................................... 103

13 Appendix ...................................................................................................................................... 104

13.1 About BRICdata ............................................................................................................................. 104

13.1.1 Areas of expertise .......................................................................................................................... 104

13.2 Methodology .................................................................................................................................. 105

13.3 Definitions ...................................................................................................................................... 106

13.4 Disclaimer ...................................................................................................................................... 107

TABLE OF CONTENTS

Australian Mining Industry Outlook – Market Opportunities and Entry Strategies, Analyses and

Forecasts to 2016 Page 7

© BRICdata. This product is licensed and is not to be photocopied Published: March 2012

LIST OF FIGURES

Figure 1: Australian Mining Production Volume (Million Tons), 2007–2016 ....................................................................................................... 9 Figure 2: Australian Mining Industry Production Volume by Mineral Category (% Share), 2011 and 2016 .................................................... 10 Figure 3: Australian Coal Production Volume (Million Tons), 2007–2016 ......................................................................................................... 11 Figure 4: Australian Iron Ore Production Volume (Million Tons), 2007–2016 ................................................................................................... 12 Figure 5: Australian Bauxite Production Volume (Million Tons), 2007–2016 .................................................................................................... 13 Figure 6: Australian Phosphate Rock Production Volume (Million Tons), 2007–2016 ..................................................................................... 14 Figure 7: Australian Salt Production Volume (Million Tons), 2007–2016 .......................................................................................................... 14 Figure 8: Australian Electricity Production (Billion Kilowatt Hours), 2007–2016 ............................................................................................... 18 Figure 9: Australian Automobile Production Trend (Units), 2007–2016 ............................................................................................................ 19 Figure 10: Australian Construction Net Output at Current Prices (US$ Billion), 2007–2016............................................................................ 20 Figure 11: Australian GDP at Constant Prices (US$ Billion), 2007–2016 (Base Year 1999–2000)................................................................. 21 Figure 12: Australian Inflation Rate (%), 2007–2016 ......................................................................................................................................... 22 Figure 13: Australian Manufacturing Net Output at Current Prices (US$ Billion), 2007–2016 ......................................................................... 23 Figure 14: Australian Electricity Consumption (Billion Kilowatt Hours), 2007–2016 ......................................................................................... 24 Figure 15: Australian Crude Steel Production (Million Metric Tons), 2007–2016 ............................................................................................. 25 Figure 16: Australian Mining and Construction Equipment Industry (US$ Billion), 2007–2011 ....................................................................... 27 Figure 17: Global Copper Production and Reserves in Volume Terms (% Share), 2010 ................................................................................ 31 Figure 18: Global Industrial Diamond Production and Reserves in Volume Terms (% Share), 2010 .............................................................. 32 Figure 19: Global Iron Ore Production and Reserves in Volume Terms (% Share), 2010 ............................................................................... 33 Figure 20: Global Nickel Production and Reserves in Volume Terms (% Share), 2010 .................................................................................. 34 Figure 21: Global Bauxite Production and Reserves in Volume Terms (% Share), 2010 ................................................................................ 35 Figure 22: Global Gold Production and Reserves in Volume Terms (% Share), 2010 ..................................................................................... 36 Figure 23: Australian Mining Industry Dynamics: Coal Category ...................................................................................................................... 37 Figure 24: Australian Mining Industry Dynamics: Metallic Minerals Category .................................................................................................. 39 Figure 25: Australian Mining Industry Dynamics: Non-Metallic Minerals Category .......................................................................................... 42 Figure 26: Australian Mining Industry Dynamics: Mining Equipment Industry .................................................................................................. 44 Figure 27: Australian Coal Production Volume (Million Tons), 2007–2011....................................................................................................... 47 Figure 28: Australian Coal Production Volume (Million Tons), 2012–2016....................................................................................................... 48 Figure 29: Australian Coal Production Value (AUD Billion), 2007–2011 ........................................................................................................... 49 Figure 30: Australian Coal Production Value (AUD Million), 2012–2016 .......................................................................................................... 50 Figure 31: Australian Coal Consumption Volume (Million Tons), 2007–2011 .................................................................................................. 51 Figure 32: Australian Coal Import Volume (Million Tons), 2006–2010 .............................................................................................................. 52 Figure 33: Australian Coal Export Volume (Million Tons), 2006–2010.............................................................................................................. 53 Figure 34: Australian Leading Coal Producers (% Share), 2011 ....................................................................................................................... 57 Figure 35: Australian Iron Ore Production Volume (Million Tons), 2007–2011 ................................................................................................. 59 Figure 36: Australian Iron Ore Production Volume (Million Tons), 2012–2016 ................................................................................................. 60 Figure 37: Australian Iron Ore Production Value (AUD Million), 2007–2011 .................................................................................................... 61 Figure 38: Australian Iron Ore Production Value (AUD Million), 2012–2016 .................................................................................................... 62 Figure 39: Australian Iron Ore Consumption Value (Million Tons), 2007–2016................................................................................................ 63 Figure 40: Australian Iron Ore Import Volume (Million Tons), 2006–2011 ........................................................................................................ 64 Figure 41: Australian Iron Ore Export Volume (Million Tons), 2006–2011........................................................................................................ 65 Figure 42: Australian Leading Iron Ore Producers (% Share), 2011 ................................................................................................................. 69 Figure 43: Australian Phosphate Rock Production Volume (Thousand Tons), 2007–2011 ............................................................................. 71 Figure 44: Australian Phosphate Rock Production Volume (Thousand Tons), 2012–2016 ............................................................................. 72 Figure 45: Australian Phosphate Rock Production Value (AUD Million), 2007–2011....................................................................................... 73 Figure 46: Australian Phosphate Rock Production Value (AUD Million), 2012–2016....................................................................................... 74 Figure 47: Australian Phosphate Rock Consumption Volume (Thousand Tons), 2007–2011 ......................................................................... 75 Figure 48: Australian Phosphate Rock Import Volume (Thousand Tons), 2007–2011 .................................................................................... 76 Figure 49: Australian Phosphate Rock Export Volume (Thousand Tons), 2007–2011 .................................................................................... 77 Figure 50: Australian Salt Production Operations .............................................................................................................................................. 80 Figure 51: Australian Salt Production Volume (Million Tons), 2007–2011 ........................................................................................................ 81 Figure 52: Australian Salt Production Volume (Million Tons), 2012–2016 ........................................................................................................ 82 Figure 53: Australian Salt Production Value (AUD Million), 2007–2011 ........................................................................................................... 83 Figure 54: Australian Salt Production Value (AUD Million), 2012–2016 ........................................................................................................... 84 Figure 55: Australian Salt Consumption Volume (Million Tons), 2007–2011 .................................................................................................... 85 Figure 56: Australian Salt Import Volume (Million Tons), 2007–2011 ............................................................................................................... 86 Figure 57: Australian Salt Export Volume (Million Tons), 2007–2011 ............................................................................................................... 87 Figure 58: Australian Leading Mining Companies – Revenue Comparison (US$ Million), 2007–2011 ........................................................... 91

TABLE OF CONTENTS

Australian Mining Industry Outlook – Market Opportunities and Entry Strategies, Analyses and

Forecasts to 2016 Page 8

© BRICdata. This product is licensed and is not to be photocopied Published: March 2012

LIST OF TABLES

Table 1: Investments and Announcements of Capacity Expansions by Key Australian Mining Operators in 2008–2009 .............................. 16 Table 2: Australian GDP at Constant Prices (US$ Billion), 2007–2016 (Base Year 1999–2000) .................................................................... 21 Table 3: Australian Inflation Rate (%), 2007–2016 ............................................................................................................................................ 22 Table 4: Australian Mining Industry Entry Strategy of Foreign Companies,...................................................................................................... 29 Table 5: Australian Coal Production Volume (Million Tons), 2007–2011 .......................................................................................................... 47 Table 6: Australian Coal Production Volume (Million Tons), 2012–2016 .......................................................................................................... 48 Table 7: Australian Coal Production Value (AUD Billion), 2007–2011 .............................................................................................................. 49 Table 8: Australian Coal Production Value (US$ Billion), 2007–2011............................................................................................................... 49 Table 9: Australian Coal Production Value (AUD Billion), 2012–2016 .............................................................................................................. 50 Table 10: Australian Coal Production Value (US$ Billion), 2012–2016............................................................................................................. 50 Table 11: Australian Coal Consumption Volume (Million Tons), 2007–2011 .................................................................................................... 51 Table 12: Australian Coal Import Volume (Million Tons), 2006–2010 ............................................................................................................... 52 Table 13: Australian Coal Export Volume (Million Tons), 2006–2010 ............................................................................................................... 53 Table 14: Key Australian Coal Mining Projects, 2011–2016 .............................................................................................................................. 54 Table 15: Key Australian Coal Mines* ................................................................................................................................................................ 55 Table 16: Australian Iron Ore Production Volume (Million Tons), 2007–2011 .................................................................................................. 59 Table 17: Australian Iron Ore Production Volume (Million Tons), 2012–2016 .................................................................................................. 60 Table 18: Australian Iron Ore Production Value (AUD Million), 2007–2011 ..................................................................................................... 61 Table 19: Australian Iron Ore Production Value (US$ Million), 2007–2011 ...................................................................................................... 61 Table 20: Australian Iron Ore Production Value (AUD Million), 2012–2016 ..................................................................................................... 62 Table 21: Australian Iron Ore Production Value (US$ Million), 2012–2016 ...................................................................................................... 62 Table 22: Australian Iron Ore Consumption Volume (Million Tons), 2007–2011 .............................................................................................. 63 Table 23: Australian Iron Ore Import Volume (Million Tons), 2006–2011 ......................................................................................................... 64 Table 24: Australian Iron Ore Export Volume (Million Tons), 2006–2011 ......................................................................................................... 65 Table 25: Key Projects ........................................................................................................................................................................................ 66 Table 26: Key Australian Iron Ore Processing Units .......................................................................................................................................... 67 Table 27: Australian Phosphate Rock Production Volume (Thousand Tons), 2007–2011 .............................................................................. 71 Table 28: Australian Phosphate Rock Production Volume (Thousand Tons), 2012–2016 .............................................................................. 72 Table 29: Australian Phosphate Rock Production Value (AUD Million), 2007–2011 ........................................................................................ 73 Table 30: Australian Phosphate Rock Production Value (US$ Million), 2007–2011 ........................................................................................ 73 Table 31: Australian Phosphate Rock Production Value (AUD Million), 2012–2016 ........................................................................................ 74 Table 32: Australian Phosphate Rock Production Value (US$ Million), 2012–2016 ........................................................................................ 74 Table 33: Australian Phosphate Rock Consumption Volume (Thousand Tons), 2007–2011 .......................................................................... 75 Table 34: Australian Phosphate Rock Import Volume (Thousand Tons), 2007–2011...................................................................................... 76 Table 35: Australian Phosphate Rock Export Volume (Thousand Tons), 2007–2011 ..................................................................................... 77 Table 36: Australian Salt Production Volume (Million Tons), 2007–2011 ......................................................................................................... 81 Table 37: Australian Salt Production Volume (Million Tons), 2012–2016 ......................................................................................................... 82 Table 38: Australian Salt Production Value (AUD Million), 2007–2011............................................................................................................. 83 Table 39: Australian Salt Production Value (US$ Million), 2007–2011 ............................................................................................................. 83 Table 40: Australian Salt Production Value (AUD Million), 2012–2016............................................................................................................. 84 Table 41: Australian Salt Production Value (US$ Million), 2012–2016 ............................................................................................................. 84 Table 42: Australian Salt Consumption Volume (Million Tons), 2007–2011 ..................................................................................................... 85 Table 43: Australian Salt Import Volume (Million Tons), 2007–2011 ................................................................................................................ 86 Table 44: Australian Salt Export Volume (Million Tons), 2007–2011 ................................................................................................................ 87 Table 45: Key Australian Salt Mining Processing Units ..................................................................................................................................... 88 Table 46: Production Capacities of Leading Australian Salt Producers ............................................................................................................ 89 Table 47: Australian Leading Mining Companies – Financial Comparison (US$ Million), 2007–2011 ............................................................ 91 Table 48: Exchange Rate (US$–AUD), 2007–2016......................................................................................................................................... 106

INDUSTRY DYNAMICS: FIVE FORCES ANALYSIS

Australian Mining Industry Outlook – Market Opportunities and Entry Strategies, Analyses and

Forecasts to 2016 Page 9

© BRICdata. This product is licensed and is not to be photocopied Published: March 2012

2 Mining Industry Outlook in Australia

Australia possesses a large supply of natural resources, and the country’s sustainable economic model has attracted a

high level of foreign direct investments (FDIs) during the review period (2007–2011). The country contains the world’s

largest reserves of nickel, silver, zinc and brown coal. In addition, Australia has reserves of bauxite, black coal, copper,

gold, diamond and iron ore that rank within the six largest of their kind in the world. Australia is the world’s largest

producer of bauxite and alumina, and the third-largest producer of zinc, iron ore and gold. Furthermore, the country is a

net exporter of numerous mineral categories.

Australia’s political stability and low levels of political interference make the country’s mining industry one of the most

attractive for investments in the world. Moreover, due to the country’s geographical proximity to the emerging economies

of China and India, Australia is expected to register increased demand for natural resources from these economies.

Australia recorded strong export and production growth in its key minerals in 2009, despite the adverse impact of the

global economic crisis in the same year. This indicates the strength and sustainable economic model being followed in the

country.

2.1 Mining Industry Market Size and Growth Potential

Australian mining production is expected to record a CAGR of X.XX% over the forecast period

Due to Australia’s strong mineral exports growth, the country’s mining production, which includes coal, two major metallic

minerals of iron ore and bauxite and two non-metallic minerals of phosphate rock and salt, grew at a CAGR of X.XX%

during the review period, to reach XXX.X million tons in 2011. The production is also expected to register a CAGR of

X.XX% over the forecast period, to reach a volume of X.X billion tons in 2016.

The majority of Australia’s minerals are exported to developed countries, such as Japan and the EU. However, the share

of exports to developing countries, such as China and India, increased during the review period. The overall mineral

output and exports from Australia will grow over the forecast period, as a result of increased demand due to the global

economic recovery and the rapid development of emerging economies.

The following figure displays the volume of Australian mining production during 2007–2016.

Figure 1: Australian Mining Production Volume (Million Tons), 2007–2016

Source: BRICdata analysis © BRICdata

COAL

Australian Mining Industry Outlook – Market Opportunities and Entry Strategies, Analyses and

Forecasts to 2016 Page 10

© BRICdata. This product is licensed and is not to be photocopied Published: March 2012

3 Coal

3.1 Overview of Coal Mining Category

Coal is important to the Australian economy, as it is the country’s second-largest exported commodity. In addition, black

coal exports have increased by more than XX% in the country since 2002. Australia is the fourth-largest coal producer in

the world, trailing only China, the USA and India. However, Australia is the world’s largest coal exporter. The total

production of coal Australia totaled XXX million tons in 2011. There are new challenges for the country’s coal production

following the introduction of Australia’s carbon tax, which was passed in November 2011 and is scheduled to become

effective from July 2012. This carbon tax law represents one of the largest economic reforms in this country for a

generation and a huge challenge to the coal mining category. As a result of this tax, coal mining will become the country’s

highest taxed mining category. Consequently, BRICdata projects a XX–XX% increase in Australian coal prices over the

forecast period.

3.2 Reserves, Production and Consumption

3.2.1 Total production

Coal production volume

Australia’s coal production totaled XXX.X million tons, which represents an increase of X.X% compared with 2010. The

country’s iron ore production registered a CAGR of X.XX% during the review period. The production growth rate

decreased due to heavy flood in the Queensland region in 2010.

Table 5: Australian Coal Production Volume (Million Tons), 2007–2011

2007 2008 2009 2010 2011 CAGR

2007–2011

Coal Production Volume

(Million Tons) XXX.X XXX.X XXX.X XXX.X XXX.X X.XX%

Source: BRICdata analysis © BRICdata

Figure 27: Australian Coal Production Volume (Million Tons), 2007–2011

Source: BRICdata analysis © BRICdata

IRON ORE

Australian Mining Industry Outlook – Market Opportunities and Entry Strategies, Analyses and

Forecasts to 2016 Page 11

© BRICdata. This product is licensed and is not to be photocopied Published: March 2012

4 Iron Ore

4.1 Overview of Iron Ore Mining Sub-Category

The Australian iron ore mining sub-category registered impressive growth during the review period. Since 1950, Australia

has been one of the world’s leading iron ore exporters. The sub-category has benefited from factors such as the country’s

abundant natural resources and favorable government policies. However, China’s rapid development in becoming a

leading steel producer and iron ore exporter will provide strong competition for the Australian iron ore mining sub-category

over the forecast period.

4.2 Reserves, Production and Consumption

4.2.1 Total production

Iron ore production volume

Australia’s iron ore production totaled XXX.X million tons in 2011, after recording an annual growth rate of X.XX% during

the year. The iron ore production registered a CAGR of XX.XX% during the review period. This reflects the significant

growth in iron ore demand, especially from the steel manufacturing business. The annual iron ore production growth rate

decreased due to heavy flood in the Queensland region in 2010.

Table 16: Australian Iron Ore Production Volume (Million Tons), 2007–2011

2007 2008 2009 2010 2011 CAGR

2007–2011

Iron Ore Production Volume

(Million Tons) XXX.X XXX.X XXX.X XXX.X XXX.X XX.XX%

Source: BRICdata analysis © BRICdata

Figure 35: Australian Iron Ore Production Volume (Million Tons), 2007–2011

Source: BRICdata analysis © BRICdata

PHOSPHATE ROCK

Australian Mining Industry Outlook – Market Opportunities and Entry Strategies, Analyses and

Forecasts to 2016 Page 12

© BRICdata. This product is licensed and is not to be photocopied Published: March 2012

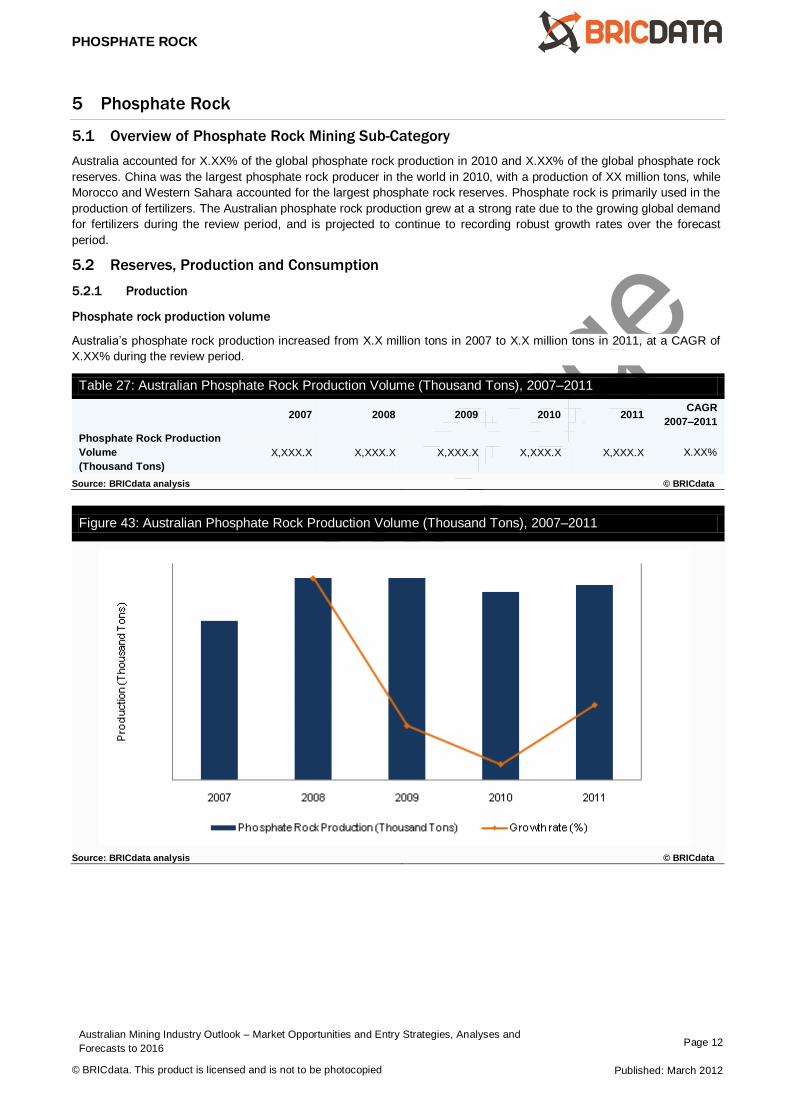

5 Phosphate Rock

5.1 Overview of Phosphate Rock Mining Sub-Category

Australia accounted for X.XX% of the global phosphate rock production in 2010 and X.XX% of the global phosphate rock

reserves. China was the largest phosphate rock producer in the world in 2010, with a production of XX million tons, while

Morocco and Western Sahara accounted for the largest phosphate rock reserves. Phosphate rock is primarily used in the

production of fertilizers. The Australian phosphate rock production grew at a strong rate due to the growing global demand

for fertilizers during the review period, and is projected to continue to recording robust growth rates over the forecast

period.

5.2 Reserves, Production and Consumption

5.2.1 Production

Phosphate rock production volume

Australia’s phosphate rock production increased from X.X million tons in 2007 to X.X million tons in 2011, at a CAGR of

X.XX% during the review period.

Table 27: Australian Phosphate Rock Production Volume (Thousand Tons), 2007–2011

2007 2008 2009 2010 2011 CAGR

2007–2011

Phosphate Rock Production

Volume

(Thousand Tons)

X,XXX.X X,XXX.X X,XXX.X X,XXX.X X,XXX.X X.XX%

Source: BRICdata analysis © BRICdata

Figure 43: Australian Phosphate Rock Production Volume (Thousand Tons), 2007–2011

Source: BRICdata analysis © BRICdata

COMPANY PROFILE

Australian Mining Industry Outlook – Market Opportunities and Entry Strategies, Analyses and

Forecasts to 2016 Page 13

© BRICdata. This product is licensed and is not to be photocopied Published: March 2012

6 Salt

6.1 Overview of Salt Mining Sub-Category

The Australian salt mining sub-category grew strongly during the review period. Australia’s salt production volume reached

XX.X million tons in 2011, after registering a CAGR of X.XX% during the review period. This growth was supported by

factors such as the country’s abundant natural salt resources and favorable government policies for salt mining. BRICdata

anticipates that the country’s salt production output will record a significant increase in output, from XX.X million tons in

2012 to XX.X million tons in 2016, at a CAGR of X.XX% over the forecast period.

The growing demand for salt has encouraged a number of local and international companies to expand their salt mining

business operations in Australia. For example, Dampier Salt is leading company in the country in terms of salt production

capacity, and the company operates three salt processing units in the country. The international company Mitsui & Co. Ltd

also has significant business operations in the sub-category through its subsidiaries: Onslow Salt Pty Ltd and Shark Bay

Salt. Other leading companies operating in the country include Cheetham Salt Limited, Larmon Pty Ltd and Sirius

Minerals.

Figure 50: Australian Salt Production Operations

Source: BRICdata analysis © BRICdata

APPENDIX–

Australian Mining Industry Outlook – Market Opportunities and Entry Strategies, Analyses and

Forecasts to 2016 Page 14

© BRICdata. This product is licensed and is not to be photocopied Published: March 2012

7 Appendix

7.1 About BRICdata

BRICdata publishes in-depth strategic intelligence reports that help its customers better understand opportunities in

emerging markets and industry sectors. Its reports provide an independent, expert view supported by primary research

and access to leading data and intelligence sources.

BRICdata is a comprehensive source of insights and analysis, and publishes a broad range of reports across a number of

different industry sectors, including consumer, retail, financial services, technology, telecoms and construction.

BRICdata is headquartered in London with research, analysis and account management teams based across Europe, the

US and Asia-Pacific. Its global research footprint is supported by a network of external associates, data partners and

industry experts to give the clearest possible perspective on emerging markets.

7.1.1 Areas of expertise

BRICdata operates a dedicated, multilingual team of in-house industry analysts with significant experience of global and

country-level research. BRICdata also maintains data and research partnerships with other research companies, industry

experts and trade associations, along with a network of independent industry consultants and former industry participants

contributing research and reports to bring additional insight and expertise in more specialist areas.

BRICdata’s research offering spans the following industry areas:

Construction BRICdata publishes reports covering the entire construction value chain: construction materials, equipment, construction

services, architectural services and interior design. It also covers the main value sectors of construction activity:

commercial, infrastructure, industrial, institutional and residential.

This comprehensive view of the market enables BRICdata to detail key growth sectors and countries and identify the most

attractive industry opportunities.

Consumer goods Covering a broad range of areas across the consumer goods market, from interior products to fast-moving consumer

goods (FMCG), ingredients, and packaging, BRICdata offers a comprehensive insight into key consumer sectors across

fast-growing markets, identifying key trends, future innovations and growth opportunities.

Comprehensive data sets including unique primary survey-driven research creates accurate market forecasts and

understanding of the factors driving consumption behavior.

Financial services Providing detailed insights into insurance and banking markets, BRICdata’s financial services reports identify key market

opportunities, emerging technologies and channel strategies. The reports provide unique data combined with local

examples of best practice and expert insights into the market.

Retail BRICdata maintains a comprehensive database of forecasts of retail spending, along with a series of unique indicators

enabling a forward view of retailers’ prospects in emerging markets. The reports identify emerging concepts in retail,

including the nascent online and mobile retail sectors in the BRIC countries and other emerging markets.

Technology BRICdata tracks key trends and innovations, emerging technologies and markets, and the key operators in both emerging

markets and technologies. Covering a range of emerging and disruptive technologies including telecoms, social media,

online and mobile retailing, and telemedicine, BRICdata examines strategies for success, the state of the competitive

landscape and the inherent threats and opportunities in the emerging technological economy.

APPENDIX–

Australian Mining Industry Outlook – Market Opportunities and Entry Strategies, Analyses and

Forecasts to 2016 Page 15

© BRICdata. This product is licensed and is not to be photocopied Published: March 2012

7.2 Methodology

All BRICdata reports are rigorously sourced and created according to a comprehensive, two-stage methodology. This

includes internal audit and primary research.

A) Internal audit

Review of in-house databases to gather existing data:

o Historic market databases and reports

o Company database

o projects database

B) Primary research

Review of the latest company strategy and asset management trends

1) Research

A. Sources

Collection of the latest market-specific data from a wide variety of industry sources:

o Government statistics

o Industry associations

o Company filings

o Broker reports

o International organizations

B. Expert opinion

Collation of opinion taken from leading industry experts

Analysis of third-party opinion and forecasts:

o Broker reports

o Industry associations

o Official government sources

C. Data consolidation and verification

Consolidation of data and opinion to create historical datasets

Creation of models to benchmark data across sectors and geographies

2) Research Analysis

Market forecasts

Feed of forecast data into market models:

o Macroeconomic indicators

o Industry-specific drivers

Analysis of Market Databases to identify trends by sector:

o Latest trends

o Key drivers of the market

3) Report Writing

Analysis of market data

Discussion of company and industry trends and issues

Integration of survey results

Annual review of trends

Standardization of market definitions using recognized industry classifications

4) Quality Control

A. Templates

Detailed process manuals

Standardized report templates and accompanying style guides

Complex forecasting tool used to ensure forecast methodologies are consistently applied

QC checklists

B. QC process

Peer review

Senior-level QC

Random spot checks on data integrity

Benchmark checks across databases

APPENDIX–

Australian Mining Industry Outlook – Market Opportunities and Entry Strategies, Analyses and

Forecasts to 2016 Page 16

© BRICdata. This product is licensed and is not to be photocopied Published: March 2012

Market data cross-checked for consistency with accumulated data from company filings

7.3 Definitions

For the purposes of this report, the following timeframes apply:

Review period: 2007–2011

Forecast period: 2012–2016

The following table indicates the exchange rates used in the report:

Table 48: Exchange Rate (US$–AUD), 2007–2016

2007 2008 2009 2010 2011

Exchange Rate 0.83898 0.85296 0.7924 0.91994 1.03336

2012 2013 2014 2015 2016

Exchange Rate 1.07636 1.07636 1.07636 1.07636 1.07636

Source: BRICdata analysis © BRICdata

The following are the industry specific definitions:

Definition by categories

Fuel minerals (coal): Includes lignite and excludes petroleum gas and crude oil.

Metallic minerals: Contains iron ore, Bauxite ore, zinc concentrate, bauxite, chromite and other minerals.

Non-metallic minerals: Comprising diamond, Phosphate, garnet, barytes, dolomite, phosphorite, silica sand,

limestone and other minerals.

Definition by coal types

Anthracite coal: This type of coal has the highest carbon content, varying between XX% and XX%. The type is

also called black coal, hard coal or stone coal, and is most frequently associated with home heating.

Bituminous coal: Bituminous coal has a carbon content ranging from XX% to XX%. Bituminous coal is used

primarily to generate electricity and for the process of coking in the steel industry. This type of coal is also known

as black coal.

Sub-bituminous coal: This ranks below bituminous coal with XX% to XX% carbon content. It generally has a

lower sulphur content than other types, which makes it attractive for use because of its cleaner burning. In

addition to being used for electrical generation, it is also used in making coke or coking coal, an essential

ingredient in making steel. In many countries, sub-bituminous coal is classified as brown coal.

Lignite coal: Lignite is a geologically young coal which has the lowest carbon content, XX% to XX%. Also called

brown coal, it is mostly used for electric power generation.

Middlings: A by-product of the coal washing and beneficiation process. It is used by domestic fuel plants, brick

manufacturing units, cement plants, industrial plants and for power generation.

Rejects: The product of the coal washing process after the separation of “clean” coal and middlings. It is used for

power generation, road repairs, briquette making and land filling purposes.

Definition by industry types

Construction industry: Comprises establishments that primarily construct buildings, both residential and non-

residential, and heavy or civil engineering projects such as highways, utility systems, bridges and others. This

may include new work, additions, alterations, maintenance and repairs.

Manufacturing industry: Makes products from raw materials by the use of manual labor or machinery. In a

more limited sense, manufacturing is the assembly of components into finished products on a large scale. The

manufacturing industry includes industries that produce automobiles, chemicals, clothing, computers, consumer

electronics, electrical equipment, furniture and heavy machinery.

Other definitions

Economic demonstrated resources (EDR): Resources judged to be economically extractable, for which the

quality and quantity are computed partly from specific measurements and partly from reasonable extrapolation

based on geological evidence.

APPENDIX–

Australian Mining Industry Outlook – Market Opportunities and Entry Strategies, Analyses and

Forecasts to 2016 Page 17

© BRICdata. This product is licensed and is not to be photocopied Published: March 2012

Sub-economic demonstrated resources (SDR): Similar to economic demonstrated resources in terms of

certainty of occurrence and although considered to be potentially economic in the foreseeable future, these

resources are judged to be sub-economic at present.

7.4 Disclaimer

All rights reserved.

No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form by any means,

electronic, mechanical, photocopying, recording or otherwise, without the prior permission of the publisher, BRICdata.

The facts of this report are believed to be correct at the time of publication but cannot be guaranteed. Please note that the

findings, conclusions and recommendations that BRICdata delivers will be based on information gathered in good faith

from both primary and secondary sources, whose accuracy we are not always in a position to guarantee. BRICdata can,

therefore, accept no liability whatsoever for actions taken based on any information that may subsequently prove to be

incorrect.