Asia Pacific Office Markets Sentiment Survey

The JLL Office Markets Sentiment Survey aims to capture, measure and track the sentiment and outlook for key office leasing markets around the region.

Q2 2015

INCREASED ACTIVITY STABLE DECREASED ACTIVITY

Shanghai

Ho Chi M

inh

Aucklan

d

Manila

Bangko

k

Sydney

Beijing

Delhi

Toky

o

Jaka

rtaSeo

ul

Singapore

Mumbai

Osaka

Hong Kong

Will leasing activity increase or decrease?

EXPANSIONARYSLIGHTLY CONTRACTIONARY

SLIGHTLY EXPANSIONARY NEUTRAL

Shanghai

Bangko

k

Manila

Aucklan

d

Beijing

Delhi

Ho Chi M

inh

Hong Kong

Jaka

rta

MumbaiOsa

kaTo

kyo

Singapore

Sydney

Seoul

Will tenant activity be expansionary?

RENTS EXPECTED TO RISE

STABLE RENTS EXPECTED TO FALL

Aucklan

d

Manila

Sydney

Beijing

Delhi

Toky

o

Osaka

Mumbai

Shanghai

Ho Chi M

inh

Hong Kong

Bangko

kSeo

ul

Jaka

rta

Singapore

Will rents increase or decrease?

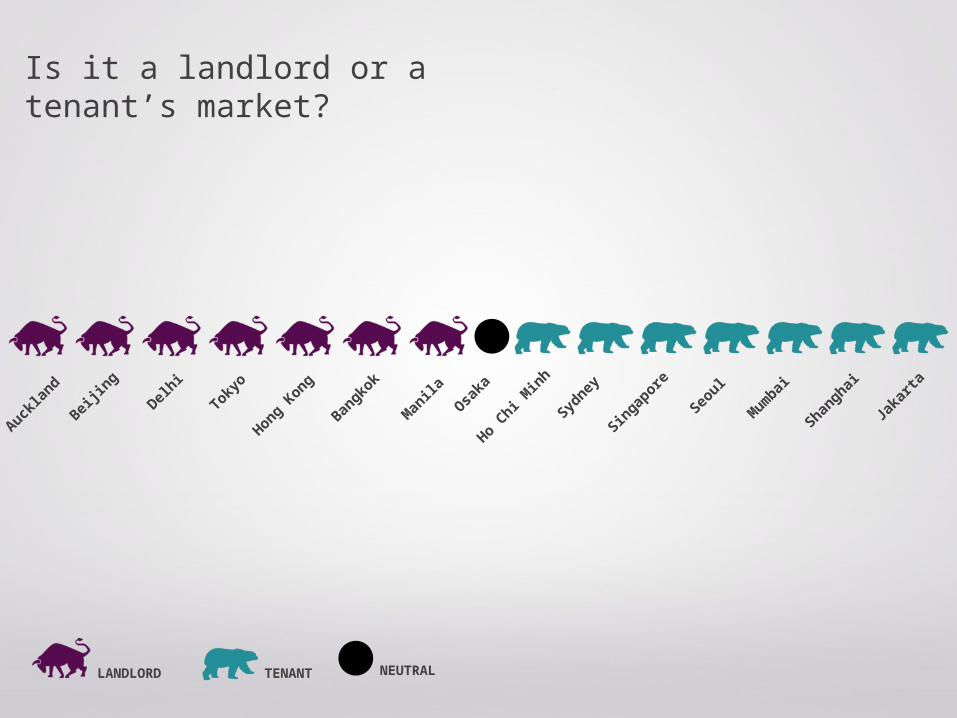

NEUTRALLANDLORD TENANT

Is it a landlord or a tenant’s market?

Bangko

k

Jaka

rta

Ho Chi M

inh

Beijing

Aucklan

d

Shanghai

Sydney

Toky

o

Hong Kong

Manila

Osaka

Delhi

Seoul

Mumbai

Singapore

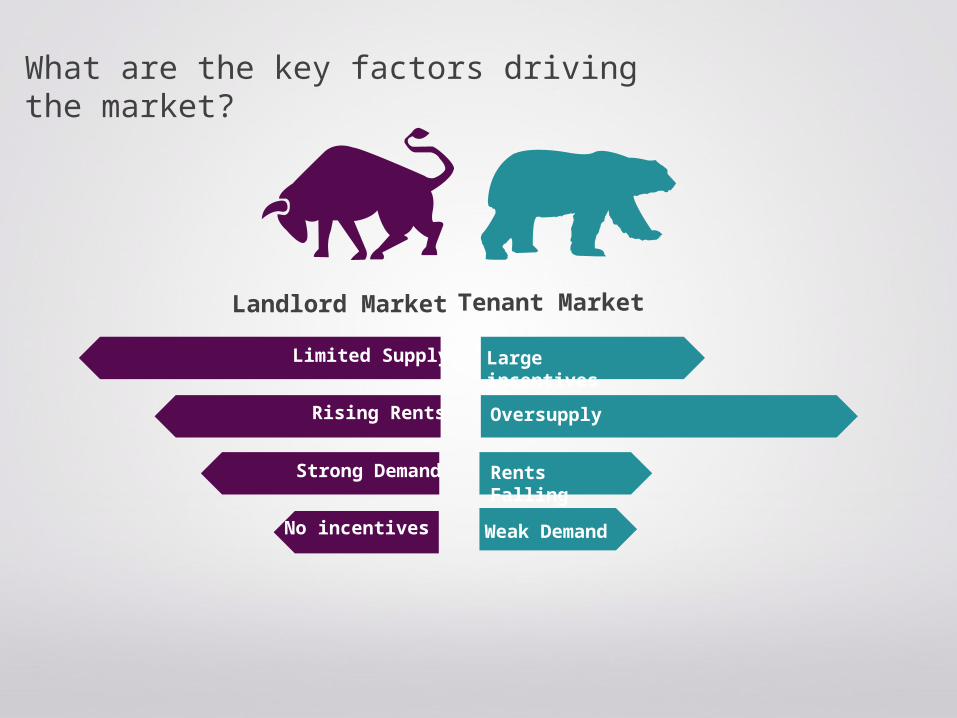

Limited Supply

Rising Rents

Strong Demand

Large incentives

Oversupply

Rents Falling

Weak Demand

Tenant Market Landlord Market

No incentives

What are the key factors driving the market?

Which sectors are the most active?

Tech

nology

Pharmac

eutic

al

Real E

state

Consumer

Transp

ort

Profes

sional

Service

s

Bankin

g

RENTINCREASED Q on Q STABLE

RENTDECREASED Q on Q

Hong Kong

New D

elhi

Singapore

Bangko

k

Manila

Mumbai

Toky

o

Shanghai

Jaka

rta

Osaka

Beijing

Ho Chi M

inh City

Seoul

Sydney

Aucklan

d

$11.8

$7.9

$5.5

$4.2

$2.8$3.6

$2.4$2.1 $1.8

$1.7

$6.4

$6.2

$4.1

$2.6$2.7

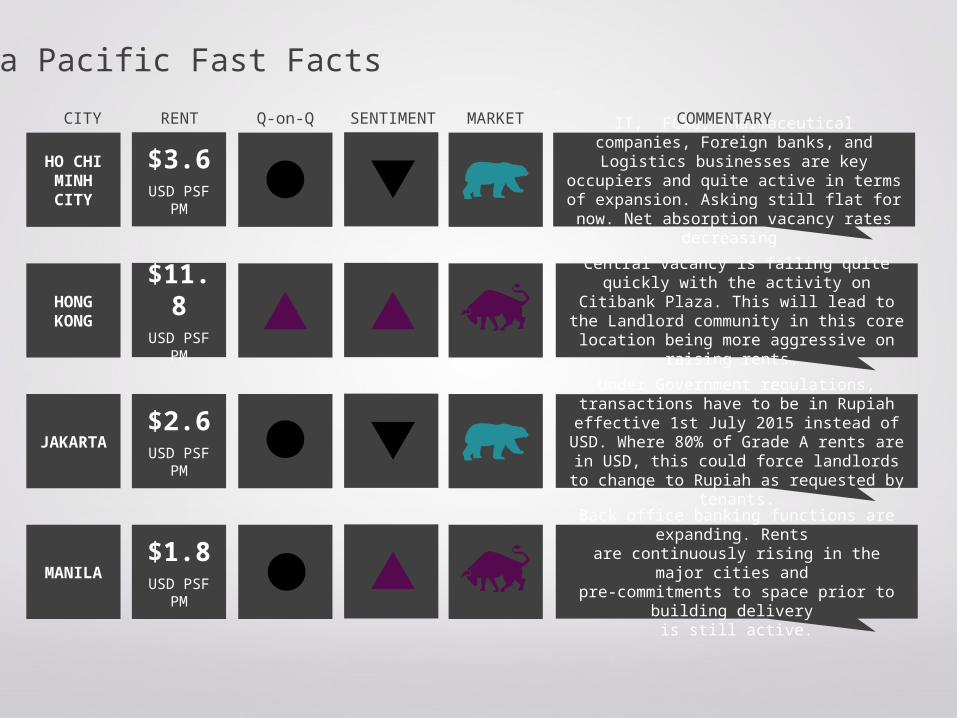

CITY RENT Q-on-Q SENTIMENT MARKET COMMENTARY

AUCKLAND $2.4USD PSF PM

Building supply in the pipeline, but existing availability restricted.

$1.7USD PSF PM

BANGKOKCall centres for insurance companies are very active in

terms of office demand - rental to increase steadily but at a slower pace compared to last year.

BEIJING

Tenant quality remains a focus. Few options in core locations. Companies interested more and more on air

quality filtration. Beijing's urban sprawl continues with new submarkets coming, but few are willing to jump in.

$7.9USD PSF PM

NEWDELHI

Low grade A supply. Tenants in expansionary mode has resulted in a high demand for office space and thus rental

values have increased.

$2.8USD PSF PM

Asia Pacific Fast Facts

HO CHI MINH CITY

$3.6USD PSF PM

IT, FCMG, Pharmaceutical companies, Foreign banks, and Logistics businesses are key occupiers and quite

active in terms of expansion. Asking still flat for now. Net absorption vacancy rates decreasing

$11.8USD PSF PM

HONG KONG

Central vacancy is falling quite quickly with the activity on Citibank Plaza. This will lead to the Landlord community in this core location being more aggressive on raising rents.

JAKARTA

Under Government regulations, transactions have to be in Rupiah effective 1st July 2015 instead of USD. Where

80% of Grade A rents are in USD, this could force landlords to change to Rupiah as requested by tenants.

$2.6USD PSF PM

MANILA

Back office banking functions are expanding. Rents are continuously rising in the major cities and

pre-commitments to space prior to building delivery is still active.

$1.8USD PSF PM

CITY RENT Q-on-Q SENTIMENT MARKET COMMENTARY

Asia Pacific Fast Facts

$4.2USD PSF PM

Markets still tenant oriented and will move to Landlord oriented market over the next 12 - 15 months. Absorbtion likely to increase marginally over this quarter, and rentals

will also witness a minor increase.

$2.1USD PSF PM

Limited Grade A space in the Umeda area is leading large scale tenants to consider space in Yodobashi No large re-development projects scheduled for the Umeda area till

2022.

New supply additions will decline and tenant demand is expected to improve over the next 12 months (compared with the past year). As

a result, vacancy will fall causing tenant incentives to decline slightly – although they will still remain generous as vacancy will

remain well above the historical average

$4.1USD PSF PM

Domestic tenants are still active especially in the financial, professional services and retail sectors. Possible upward

trend in rentals for 2H 2015.

$6.4USD PSF PM

CITY RENT Q-on-Q SENTIMENT MARKET COMMENTARY

MUMBAI

OSAKA

SEOUL

SHANGHAI

Asia Pacific Fast Facts

$6.2USD PSF PM

Vacancy starting to increase moderately due to handback of space by large banking and finance occupiers.

CITY RENT Q-on-Q SENTIMENT MARKET COMMENTARY

$2.7USD PSF PM

High level of net absorption, driven by the time lag of transactions and the usual higher number of transactions

being completed by year end.

Limited new supply in the next few years and continuing expansionary demand is expected to continue to drive

rental growth over the next few quarters.

$5.5USD PSF PM

SYDNEY

TOKYO

SINGAPORE

Asia Pacific Fast Facts