Download - ARF ReThink 2015 TV+MOBILE

TV + MOBILE Video: THE Secret Weapon to Strengthen Your Dollars

Sable Mi Senior Director, Research Strategic Planning, BrightRoll @Lutemi

Ronjan Sikdar VP, Digital, Media Analytics, Nielsen @FakeRonjan

MEDIA IS THE EXTENSION OF MAN

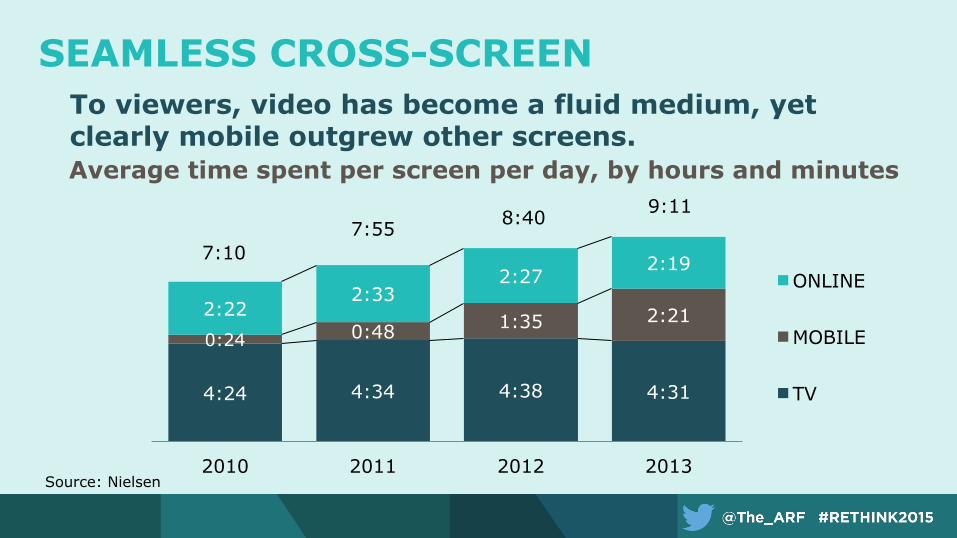

A TYPICAL DAY IN FRONT OF THE TV

Source: Nielsen

4:24 4:34 4:38 4:31

0:24 0:48 1:35 2:21 2:22 2:33

2:27 2:19

2010 2011 2012 2013

ONLINE

MOBILE

TV

SEAMLESS CROSS-SCREEN To viewers, video has become a fluid medium, yet clearly mobile outgrew other screens. Average time spent per screen per day, by hours and minutes

7:10

9:11 8:40 7:55

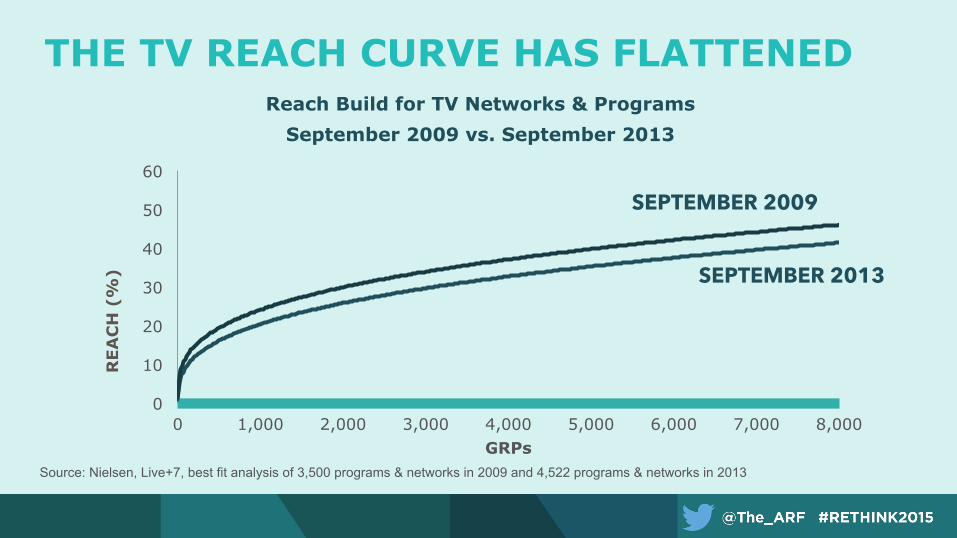

0

10

20

30

40

50

60

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000

REA

CH

(%

)

GRPs

SEPTEMBER 2009

SEPTEMBER 2013

Reach Build for TV Networks & Programs September 2009 vs. September 2013

THE TV REACH CURVE HAS FLATTENED

Source: Nielsen, Live+7, best fit analysis of 3,500 programs & networks in 2009 and 4,522 programs & networks in 2013

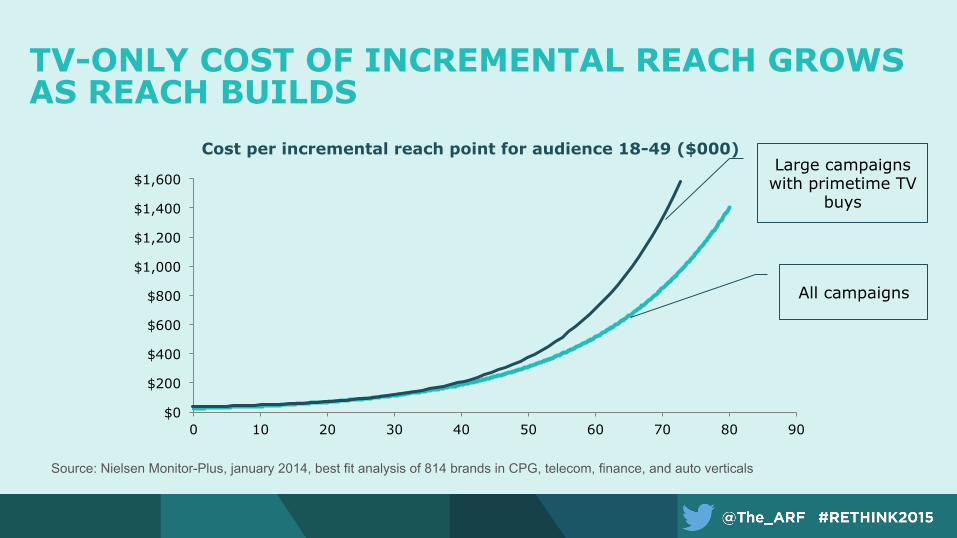

Cost per incremental reach point for audience 18-49 ($000)

TV-ONLY COST OF INCREMENTAL REACH GROWS AS REACH BUILDS

Source: Nielsen Monitor-Plus, january 2014, best fit analysis of 814 brands in CPG, telecom, finance, and auto verticals

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

0 10 20 30 40 50 60 70 80 90

Large campaigns with primetime TV

buys

All campaigns

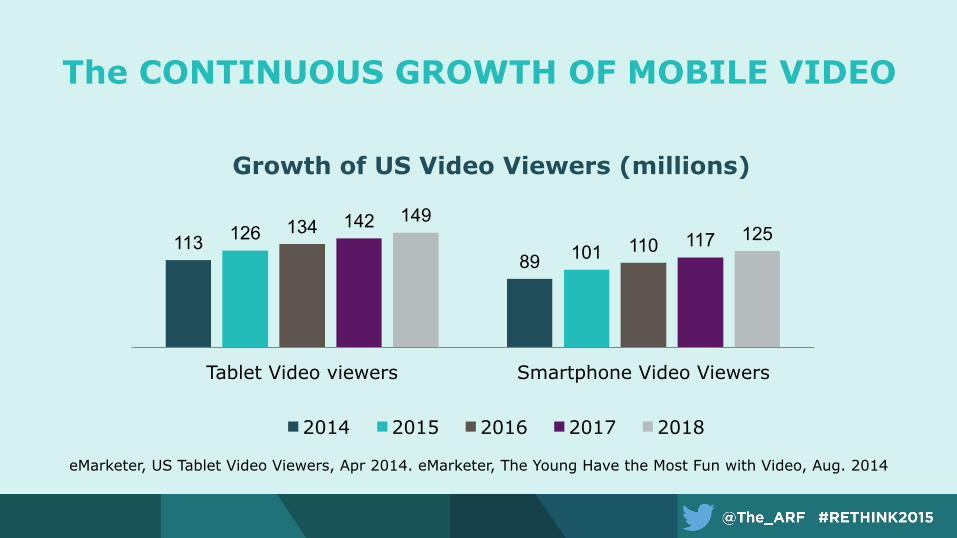

eMarketer, US Tablet Video Viewers, Apr 2014. eMarketer, The Young Have the Most Fun with Video, Aug. 2014

The CONTINUOUS GROWTH OF MOBILE VIDEO

113 89

126 101

134 110

142 117

149 125

Tablet Video viewers Smartphone Video Viewers

Growth of US Video Viewers (millions)

2014 2015 2016 2017 2018

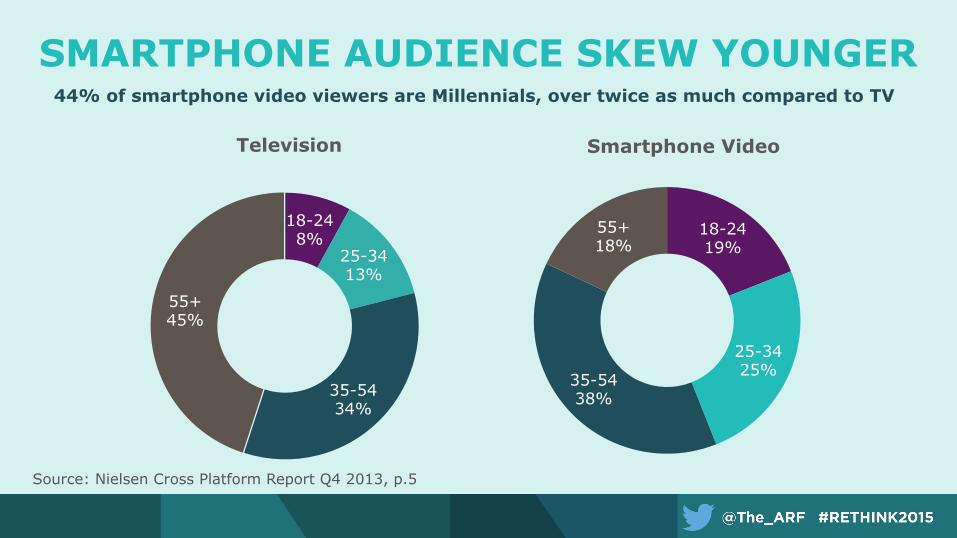

44% of smartphone video viewers are Millennials, over twice as much compared to TV

18-24 8%

25-34 13%

35-54 34%

55+ 45%

Television

18-24 19%

25-34 25% 35-54

38%

55+ 18%

Smartphone Video

Source: Nielsen Cross Platform Report Q4 2013, p.5

SMARTPHONE AUDIENCE SKEW YOUNGER

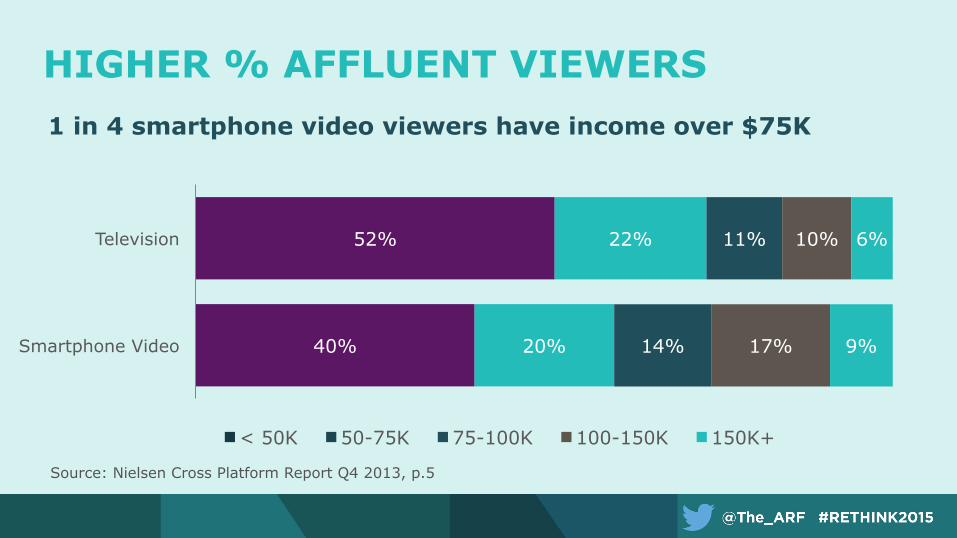

HIGHER % AFFLUENT VIEWERS

40%

52%

20%

22%

14%

11%

17%

10%

9%

6%

Smartphone Video

Television

< 50K 50-75K 75-100K 100-150K 150K+

1 in 4 smartphone video viewers have income over $75K

Source: Nielsen Cross Platform Report Q4 2013, p.5

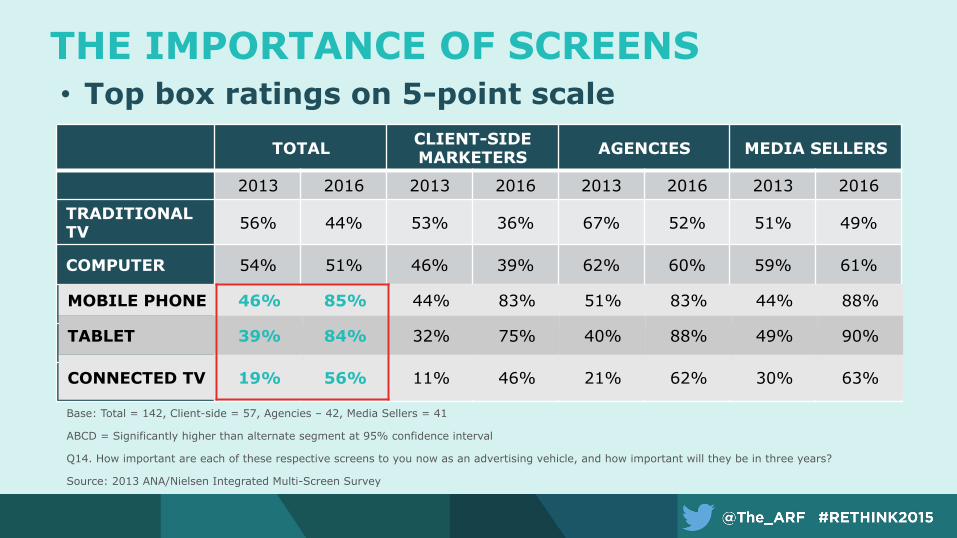

TOTAL CLIENT-SIDE MARKETERS AGENCIES MEDIA SELLERS

2013 2016 2013 2016 2013 2016 2013 2016

TRADITIONAL TV 56% 44% 53% 36% 67% 52% 51% 49%

COMPUTER 54% 51% 46% 39% 62% 60% 59% 61%

MOBILE PHONE 46% 85% 44% 83% 51% 83% 44% 88%

TABLET 39% 84% 32% 75% 40% 88% 49% 90%

CONNECTED TV 19% 56% 11% 46% 21% 62% 30% 63%

THE IMPORTANCE OF SCREENS • Top box ratings on 5-point scale

Base: Total = 142, Client-side = 57, Agencies – 42, Media Sellers = 41

ABCD = Significantly higher than alternate segment at 95% confidence interval

Q14. How important are each of these respective screens to you now as an advertising vehicle, and how important will they be in three years?

Source: 2013 ANA/Nielsen Integrated Multi-Screen Survey

MOBILE PHONE 46% 85% 44% 83% 51% 83% 44% 88%

TABLET 39% 84% 32% 75% 40% 88% 49% 90%

CONNECTED TV 19% 56% 11% 46% 21% 62% 30% 63%

MOBILE TIME SPENT VS. MOBILE AD SPEND

5% 12%

38%

25% 20% 19%

10%

45%

22%

4%

Print Radio TV Internet Mobile

Time Spent

Ad Spend

Source: Advertising spend based on IAB data for full year 2013. Print includes newspaper and magazine. Total dollar spent based on eMarketer August 2013; $27B+ opportunity calculated assuming Mobile ad spend share equal its respective time spent share. Time spent share data based on eMarketer 7/13 (adjusted to exclude outdoors/classified media spend.) Arrows denote Y/Y shift in percent share.

% of Time Spent in Media vs. % of Advertising Spending, USA 2013

~$27B+ Opportunity in USA

INTERNET AD = $43B

MOBILE AD = $7.1B

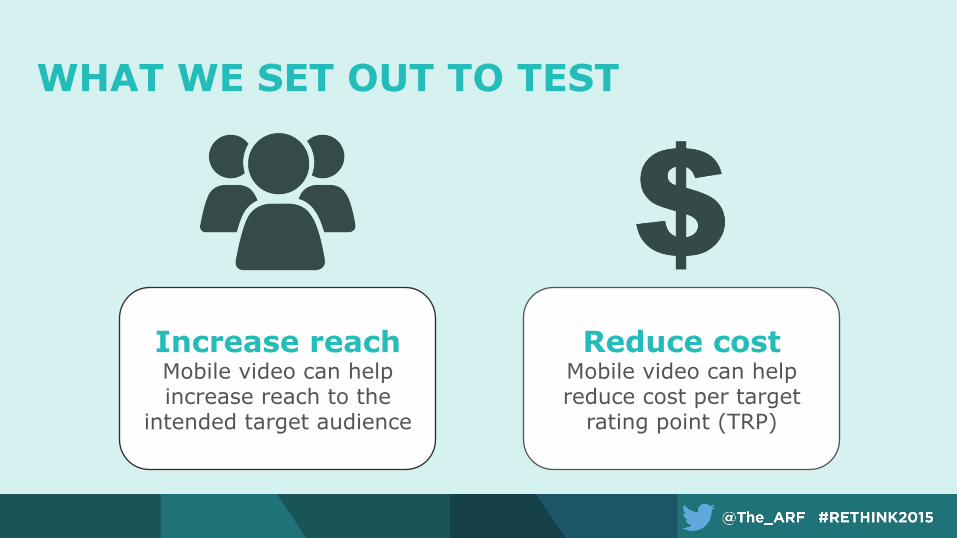

WHAT WE SET OUT TO TEST

Increase reach Mobile video can help increase reach to the

intended target audience

Reduce cost Mobile video can help reduce cost per target

rating point (TRP)

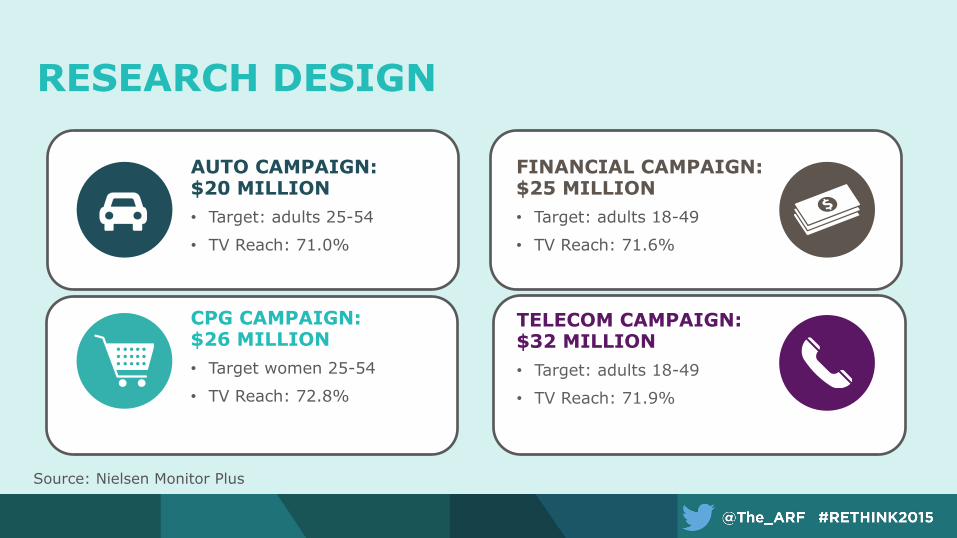

RESEARCH DESIGN

AUTO CAMPAIGN: $20 MILLION • Target: adults 25-54

• TV Reach: 71.0%

FINANCIAL CAMPAIGN: $25 MILLION • Target: adults 18-49

• TV Reach: 71.6%

TELECOM CAMPAIGN: $32 MILLION • Target: adults 18-49

• TV Reach: 71.9%

CPG CAMPAIGN: $26 MILLION • Target women 25-54

• TV Reach: 72.8%

Source: Nielsen Monitor Plus

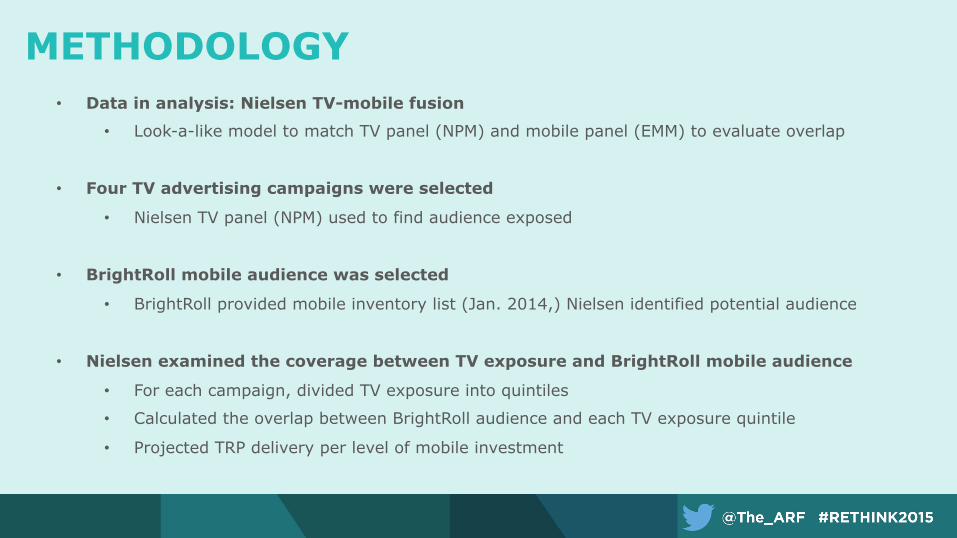

METHODOLOGY • Data in analysis: Nielsen TV-mobile fusion

• Look-a-like model to match TV panel (NPM) and mobile panel (EMM) to evaluate overlap

• Four TV advertising campaigns were selected

• Nielsen TV panel (NPM) used to find audience exposed

• BrightRoll mobile audience was selected

• BrightRoll provided mobile inventory list (Jan. 2014,) Nielsen identified potential audience

• Nielsen examined the coverage between TV exposure and BrightRoll mobile audience

• For each campaign, divided TV exposure into quintiles

• Calculated the overlap between BrightRoll audience and each TV exposure quintile

• Projected TRP delivery per level of mobile investment

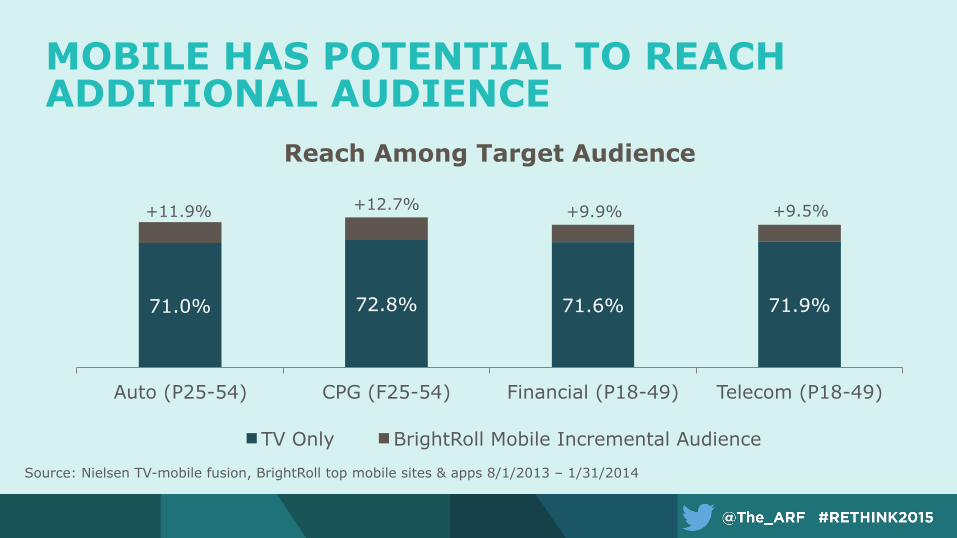

MOBILE HAS POTENTIAL TO REACH ADDITIONAL AUDIENCE

Source: Nielsen TV-mobile fusion, BrightRoll top mobile sites & apps 8/1/2013 – 1/31/2014

71.0% 72.8% 71.6% 71.9%

+11.9% +12.7% +9.9% +9.5%

Auto (P25-54) CPG (F25-54) Financial (P18-49) Telecom (P18-49)

Reach Among Target Audience

TV Only BrightRoll Mobile Incremental Audience

31.1%

15.8%

13.0%

10.3%

7.6%

22.2%

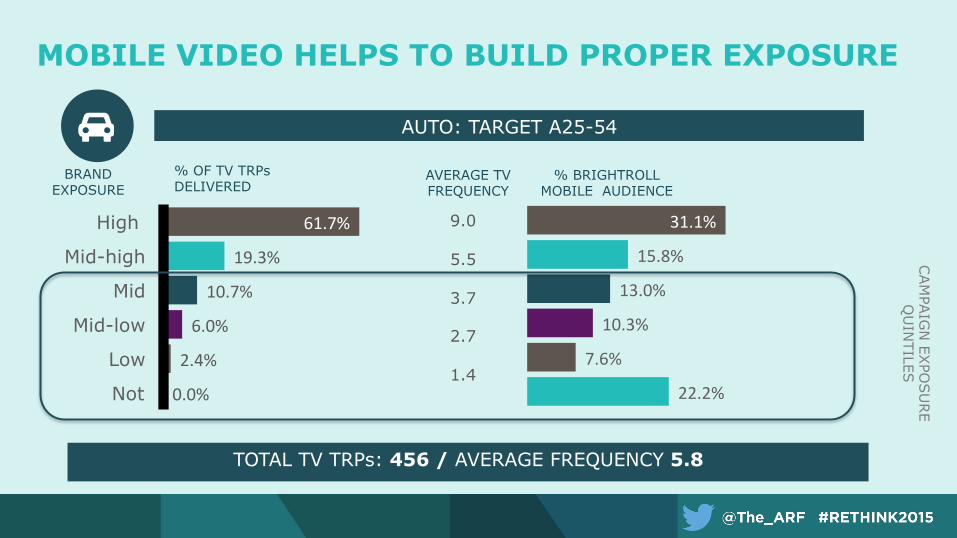

AUTO: TARGET A25-54

CAM

PAIG

N EX

POSU

RE

QU

INTILES

BRAND EXPOSURE

% OF TV TRPs DELIVERED

61.7%

19.3%

10.7%

6.0%

2.4%

0.0%

High

Mid-high

Mid

Mid-low

Low

Not

AVERAGE TV FREQUENCY

% BRIGHTROLL MOBILE AUDIENCE

9.0

5.5

3.7

2.7

1.4

TOTAL TV TRPs: 456 / AVERAGE FREQUENCY 5.8

MOBILE VIDEO HELPS TO BUILD PROPER EXPOSURE

31.1%

17.1%

12.7%

11.2%

7.9%

20.0%

CPG: TARGET F25-54

CAM

PAIG

N EX

POSU

RE

QU

INTILES

BRAND EXPOSURE

% OF TV TRPs DELIVERED

62.2%

19.2%

10.5%

5.7%

2.3%

0.0%

High

Mid-high

Mid

Mid-low

Low

Not

AVERAGE TV FREQUENCY

% BRIGHTROLL MOBILE AUDIENCE

10.7

6.2

4.5

2.8

1.5

TOTAL TV TRPs: 537 / AVERAGE FREQUENCY 6.7

MOBILE VIDEO HELPS TO BUILD PROPER EXPOSURE

34.4%

17.4%

12.8%

12.0%

8.7%

14.7%

TELCOM: TARGET A 18-49

CAM

PAIG

N EX

POSU

RE

QU

INTILES

BRAND EXPOSURE

% OF TV TRPs DELIVERED

62.2%

19.3%

10.6%

5.7%

2.1%

0.0%

HIGH

MID-HIGH

MID

MID-LOW

LOW

NOT

AVERAGE TV FREQUENCY

% BRIGHTROLL MOBILE AUDIENCE

16.7

10.5

7.8

4.4

2.1

TOTAL TV TRPs: 747 / AVERAGE FREQUENCY 10.8

MOBILE VIDEO HELPS TO BUILD PROPER EXPOSURE

31.7%

18.2%

13.7%

12.5%

9.1%

14.7%

FINANCIAL SERVICES: TARGET A 18-49

CAM

PAIG

N EX

POSU

RE

QU

INTILES

BRAND EXPOSURE

% OF TV TRPs DELIVERED

67.7%

17.3%

8.8%

4.5%

1.6%

0.0%

High

Mid-high

Mid

Mid-low

Low

Not

AVERAGE TV FREQUENCY

% BRIGHTROLL MOBILE AUDIENCE

21.5

10.3

7.0

3.9

1.9

TOTAL TV TRPs: 626 / AVERAGE FREQUENCY 12.3

MOBILE VIDEO HELPS TO BUILD PROPER EXPOSURE

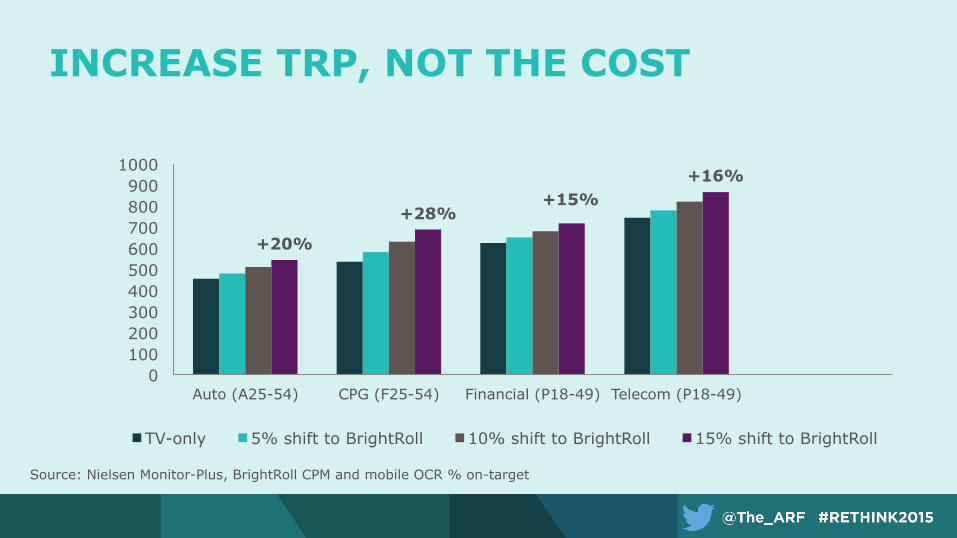

INCREASE TRP, NOT THE COST

+20%

+28% +15%

+16%

0 100 200 300 400 500 600 700 800 900

1000

Auto (A25-54) CPG (F25-54) Financial (P18-49) Telecom (P18-49)

TV-only 5% shift to BrightRoll 10% shift to BrightRoll 15% shift to BrightRoll

Source: Nielsen Monitor-Plus, BrightRoll CPM and mobile OCR % on-target

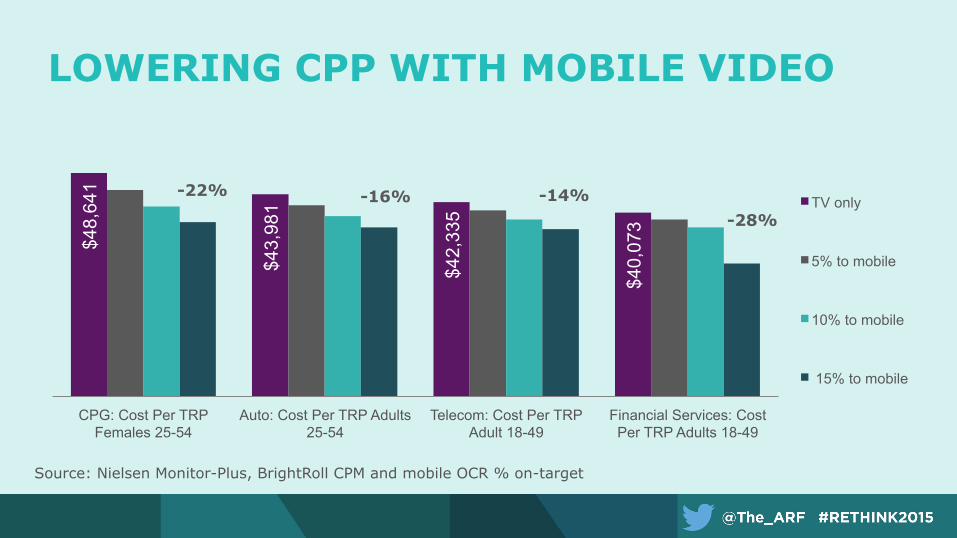

LOWERING CPP WITH MOBILE VIDEO

Source: Nielsen Monitor-Plus, BrightRoll CPM and mobile OCR % on-target

$48,

641

$43,

981

$42,

335

$40,

073

CPG: Cost Per TRP Females 25-54

Auto: Cost Per TRP Adults 25-54

Telecom: Cost Per TRP Adult 18-49

Financial Services: Cost Per TRP Adults 18-49

TV only

5% to mobile

10% to mobile

15% to mobile

-22% -16% -14% -28%

CONCLUSION: MOBILE SOLUTIONS FOR ADVERTISERS

INCREMENTAL REACH

FREQUENCY DISTRIBUTION

COST EFFICIENCY

Q&A

![[ ] ARF slides.ppt](https://cdn.vdocuments.site/doc/165x107/55ca7deabb61eb604e8b456c/-arf-slidesppt.jpg)