Download - analysis quarterly 14.3&4 - Energy

analysis review

quarterly

vto anl

energetics

ornl nrel snl

ta engineering sra/sentech

jake ward amgad elgowainy, steve plotkin, aymeric rousseau, tom stephens, anant vyas, michael wang, joann zhou alicia birky, salil deshpande stacy davis, zhenhong lin, changzheng liu aaron brooker, mark singer becky levinson, dawn manley jim moore, charles taylor russ campbell, jonathan ford, karen sikes 23 feb 2015

14.3&4 3 & 4 Q 2 0 1 4

>

1

topics

energy markets automotive markets technologies studies environmental studies consumer & opinion surveys policy studies

outline

1

qar

2

energy markets

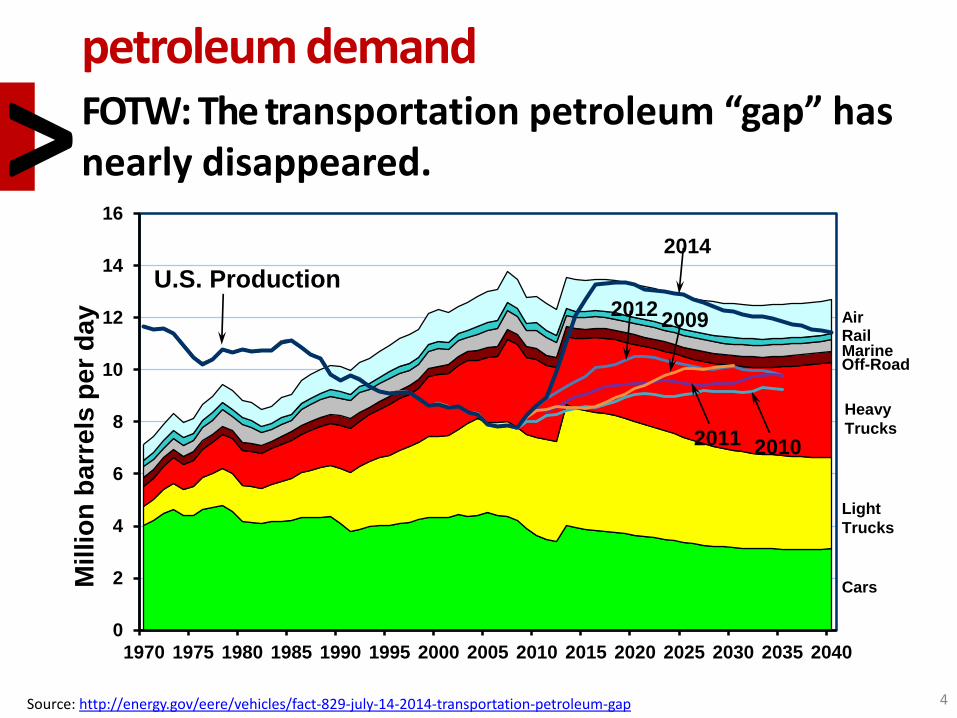

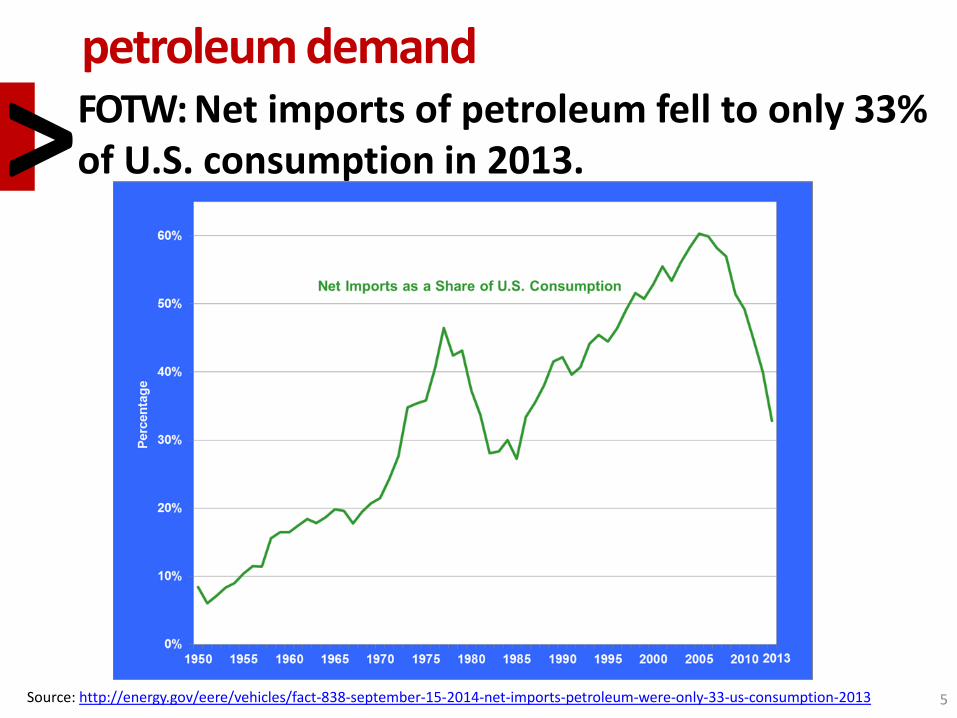

petroleum demand > FOTW: The transportation petroleum “gap” has nearly disappeared. > FOTW: Net imports of petroleum fell to only 33% of U.S. consumption in 2013. > FOTW: World petroleum consumption rises despite declines from U.S. and Europe.

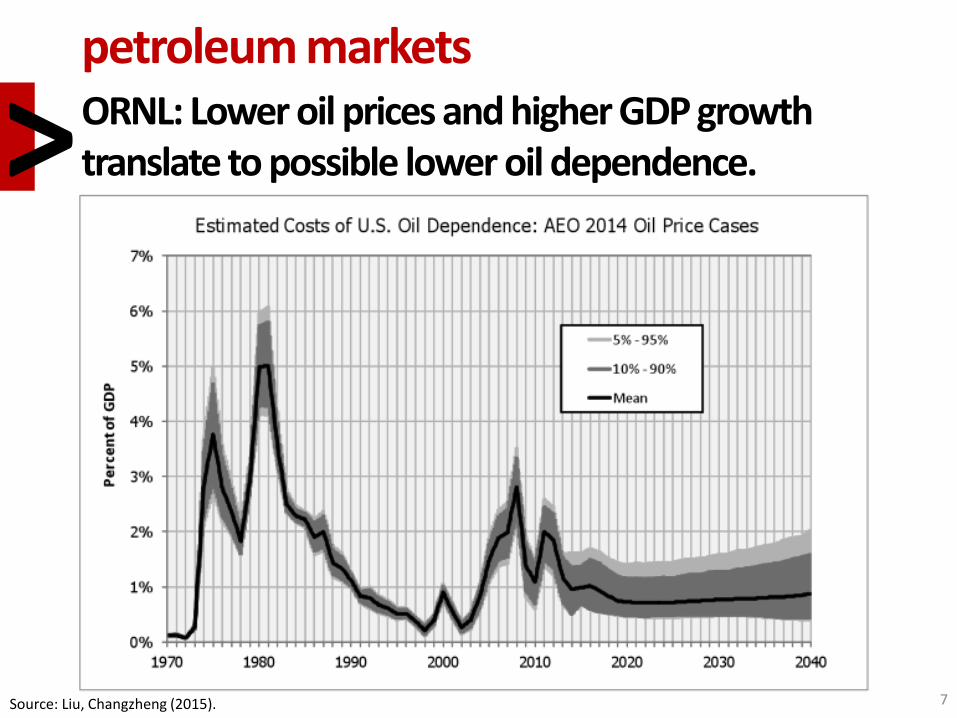

petroleum markets > ORNL: Lower oil prices and higher GDP growth translate to possible lower oil dependence. > FOTW: Non-OPEC countries supply nearly two-thirds of U.S. petroleum imports. > ORNL: OPEC’s market power, though “fuzzy”, is indeed correlated to oil price. > EIA: Recent growth in US oil production is concentrated in Texas and North Dakota. > EIA: Crude oil prices fall sharply in Q4 2014. > FOTW: Retail gasoline prices in 2014 experienced the largest decline since 2008. > EIA: 20-year trend in oil prices shows that even today’s “low” prices are still relatively high > UC-Davis: Breakevens for U.S. shale oil, gas are sensitive to world-market price changes. > EIA: U.S. oil production to increase despite expected near-term reduction in rig count.

natural gas markets > EIA: Shale gas provides largest share of gas production (even exceeding conventional wells). > CBO/EIA: U.S. natural gas production to expand through 2040 (and support net exports).

1

3

petroleum demand FOTW: The transportation petroleum “gap” has nearly disappeared. >

Source: http://energy.gov/eere/vehicles/fact-829-july-14-2014-transportation-petroleum-gap 4

0

2

4

6

8

10

12

14

16

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

Millio

n b

arr

els

per

day

Marine Rail

Cars

Air

Light

Trucks

Heavy

Trucks

U.S. Production

Off-Road

2012

2011

2009

2010

2014

petroleum demand FOTW: Net imports of petroleum fell to only 33% of U.S. consumption in 2013. >

Source: http://energy.gov/eere/vehicles/fact-838-september-15-2014-net-imports-petroleum-were-only-33-us-consumption-2013 5

petroleum demand FOTW: World petroleum consumption continues to rise despite declines from U.S. and Europe >

Source: http://energy.gov/eere/vehicles/fact-839-september-22-2014-world-petroleum-consumption-continues-rise-despite-declines 6

petroleum markets ORNL: Lower oil prices and higher GDP growth translate to possible lower oil dependence. >

7 Source: Liu, Changzheng (2015).

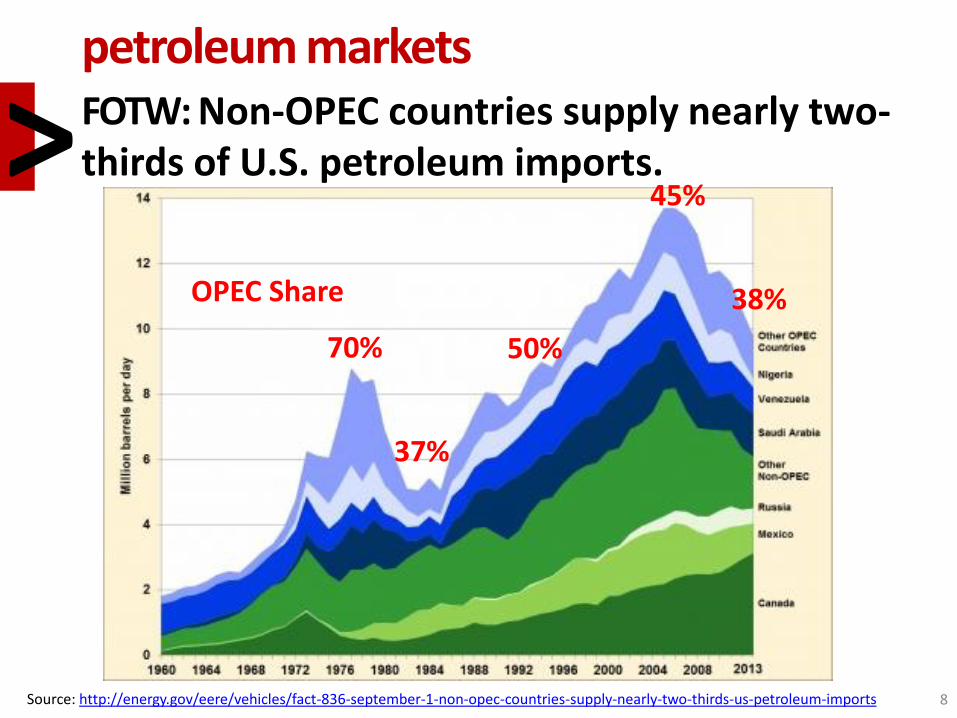

petroleum markets FOTW: Non-OPEC countries supply nearly two-thirds of U.S. petroleum imports. >

8 Source: http://energy.gov/eere/vehicles/fact-836-september-1-non-opec-countries-supply-nearly-two-thirds-us-petroleum-imports

45%

38%

70% 50%

37%

OPEC Share

petroleum markets ORNL: OPEC’s market power, though “fuzzy”, is indeed correlated to oil price. >

9 Source: Liu, Changzheng (2015).

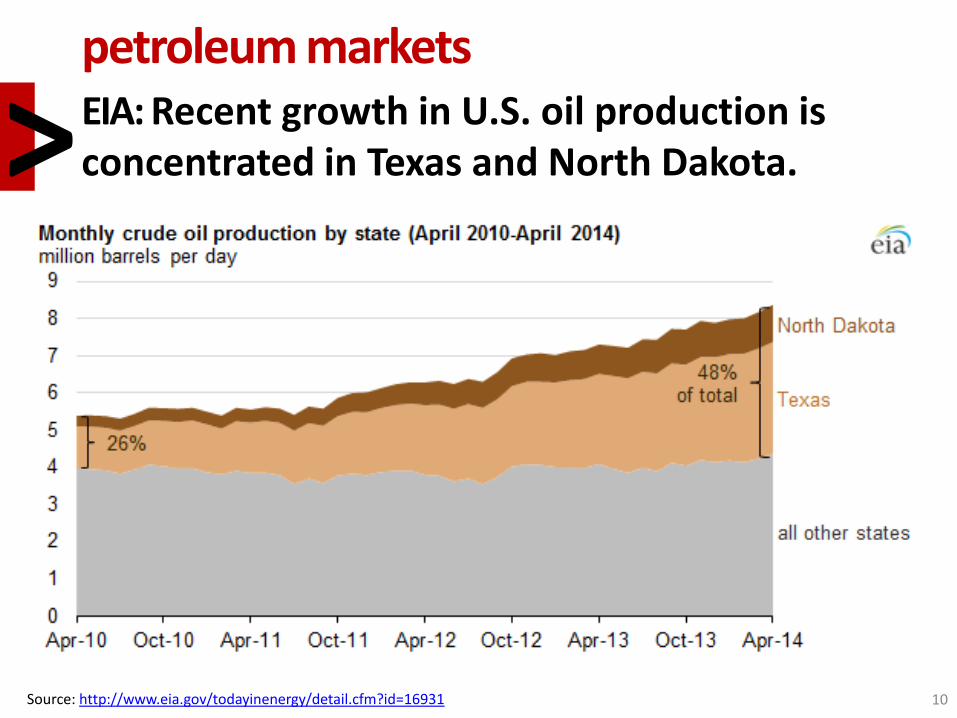

petroleum markets EIA: Recent growth in U.S. oil production is concentrated in Texas and North Dakota. >

10 Source: http://www.eia.gov/todayinenergy/detail.cfm?id=16931

petroleum markets EIA: Crude oil prices fall sharply in Q4 2014. >

11 Source: http://www.eia.gov/todayinenergy/detail.cfm?id=19451

petroleum markets FOTW: Retail gasoline prices in 2014 experienced the largest decline since 2008. >

12 Source: http://energy.gov/eere/vehicles/fact-858-february-2-2015-retail-gasoline-prices-2014-experienced-largest-decline-2008

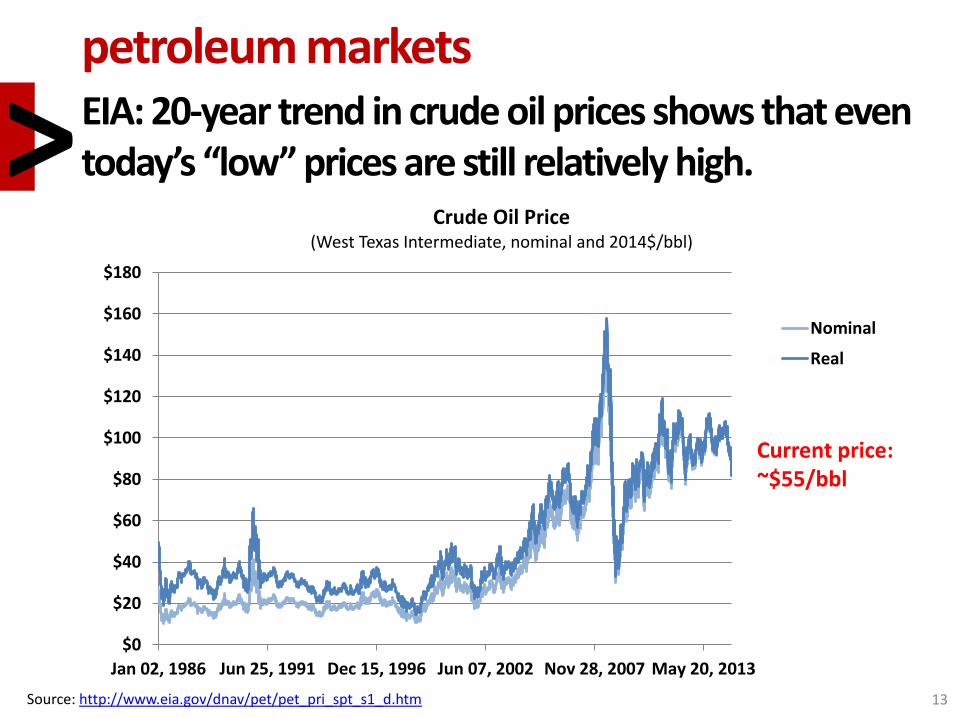

petroleum markets EIA: 20-year trend in crude oil prices shows that even today’s “low” prices are still relatively high. >

13 Source: http://www.eia.gov/dnav/pet/pet_pri_spt_s1_d.htm

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

Jan 02, 1986 Jun 25, 1991 Dec 15, 1996 Jun 07, 2002 Nov 28, 2007 May 20, 2013

Crude Oil Price (West Texas Intermediate, nominal and 2014$/bbl)

Nominal

Real

Current price: ~$55/bbl

petroleum markets UC-Davis: Breakevens for U.S. shale oil and gas are sensitive to recent world-market price changes. >

14 Source: UC-Davis NextSTEPS/Citi Research

Field Breakeven OPEX

Marcellus (gas)

$2.50 $1.00

Barnett (gas) $3.80 $1.80

Haynesville (gas)

$3.60 $1.80

Eagle Ford (oil)

$37 $7-$8

Permian (oil) $49 $10-$12

Bakken (oil) $37 $7-$8

Mississippian $43 $7-$8 Johan SverdrupRumailaJubilee Area

Bina Bawi

ZubairChina Domestic Gas

Campos ExpWest Qurna 1Tempa RossaPNG LNG T3

Gbaran Ubie Ph2Cepu Exp

NgamiaPerla

GoM TiebacksMajnoon

NE Tupi

Itaipu

FrancoWhales Park

CariocaLulaSapinhoa

SkrugardIara

PNG LNG T1-2Hadrian

Yamal Gas

JupiterBig Foot

Trebs TitovSandridge JV

ADMA

Mozambique LNGUganda Bl.1,2,3

Clair Ph 2 AbsheronVankorBl. 15/06 East

North Alexandria HubTiber

West Qurna 2Kaskida

CLOVGhana GasLaggan/Tormore Zaedyus

Block 32

STL Bakken

Colombia OilChina Domestic Oil

Tanzania LNGWheatstone LNG

Yamal LNGOXY Bakken APLNG

PSVM

Ichthys LNG

China Domestic Oil Junin 5Prelude LNGBl. 31 SE Gorgon LNGJack-St Malo

DominoSTL Eagle Ford Browse LNG

Tengiz ExpBolia-ChotaKearlOPL245

Aparo-NsikoSunrise Ph 1 Usan

West Canada LNGRDS Unc Gas STL Marcellus

Filanovsky

Block 61 OmanBG Haynesville

QCLNGSurmont Ph 2

Fort HillsMacKay RiverDover

Abadi FLNGTerre de Grace Kashagan Ph 1

Arrow LNGCarmon Creek Joslyn

GLNG

0

10

20

30

40

50

60

70

80

90

100

0 5 10 15 20 25 30 35 40

2020e Production, Mboe/d

Bre

ak

ev

en

, $

/bb

l

LNG cost

pressures

Pricing-discounts

pushing

unconventionals higher

up the curve

(2Q writedowns)

Low-cost conventional

giants (Brazil & Norway)

remain robust.

Heavy oil

expectations

being scaled

back

Disappointing pace in Iraq

sees industry accept

political risk of Kurdistan Bakken

Marcellus

Eagle Ford

Oil Price, July 2014

…Oil Price, February 2015

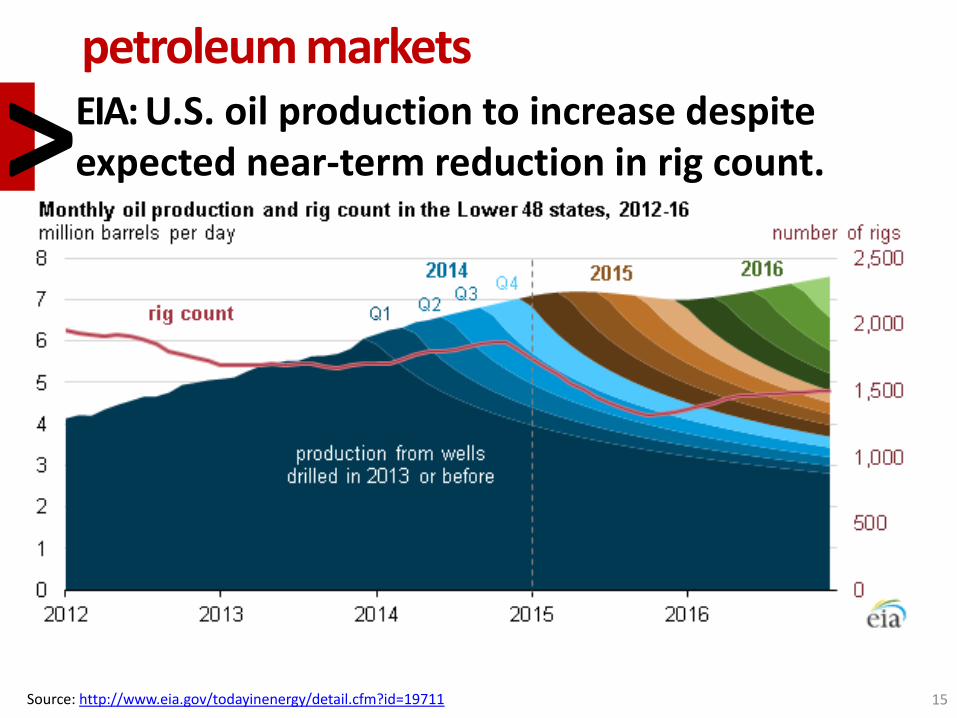

petroleum markets EIA: U.S. oil production to increase despite expected near-term reduction in rig count. >

15 Source: http://www.eia.gov/todayinenergy/detail.cfm?id=19711

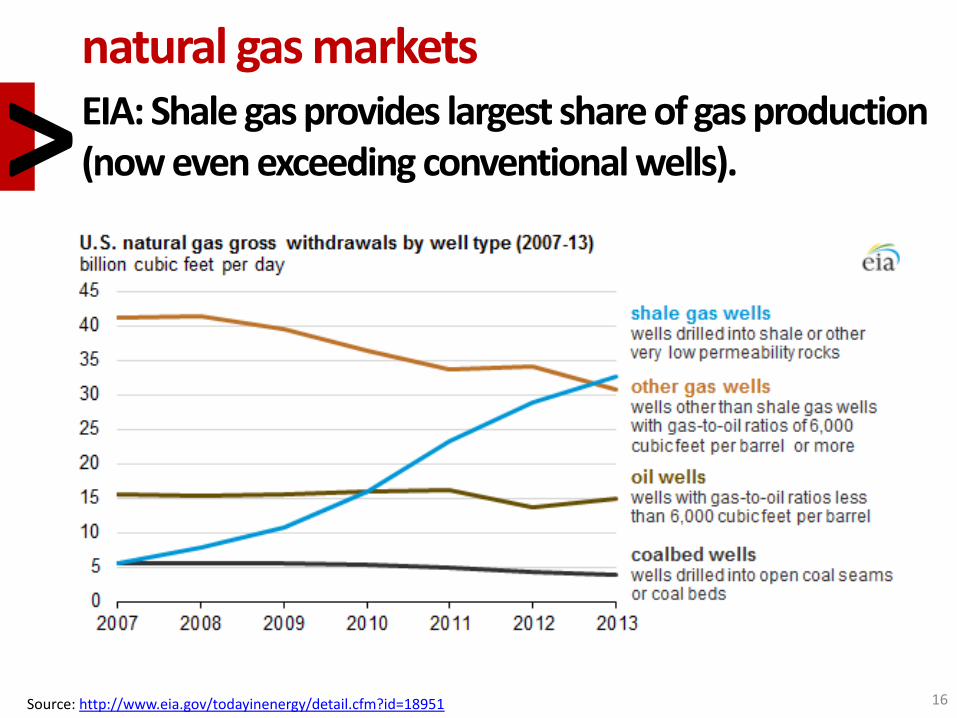

natural gas markets EIA: Shale gas provides largest share of gas production (now even exceeding conventional wells). >

16 Source: http://www.eia.gov/todayinenergy/detail.cfm?id=18951

natural gas markets CBO/EIA: U.S. natural gas production to expand through 2040 (and support net exports). >

17 Source: http://www.dot.gov/sites/dot.gov/files/docs/Draft_Beyond_Traffic_Framework.pdf

topics

energy markets automotive markets technologies studies environmental studies consumers/opinion surveys policy studies

outline

2

qar

18

automotive markets

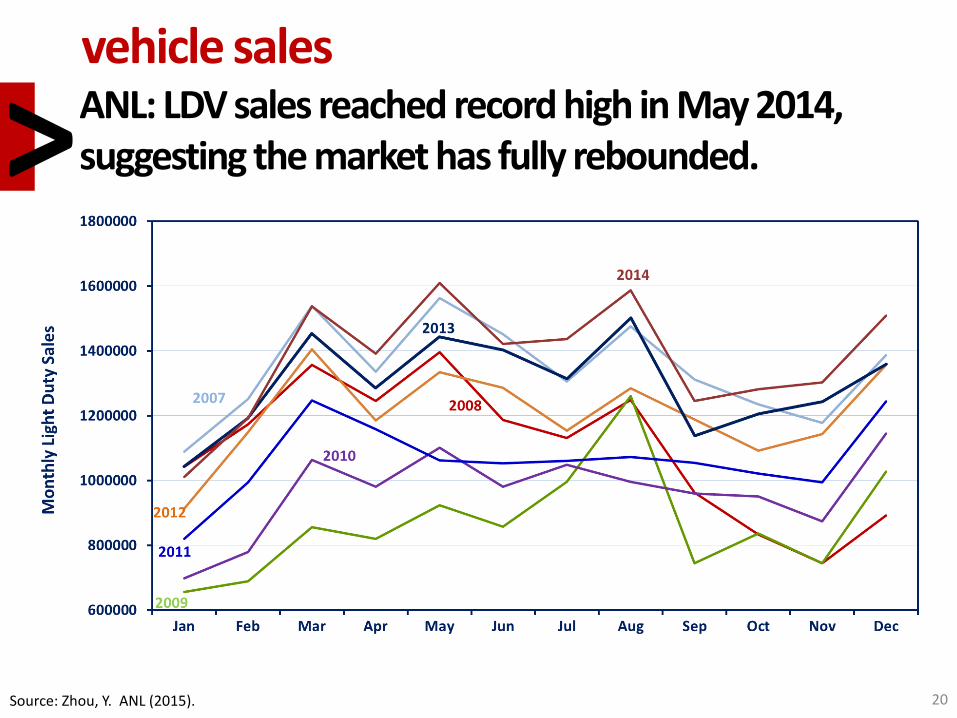

vehicle sales > ANL: LDV sales reached record high in May 2014, suggesting the market has

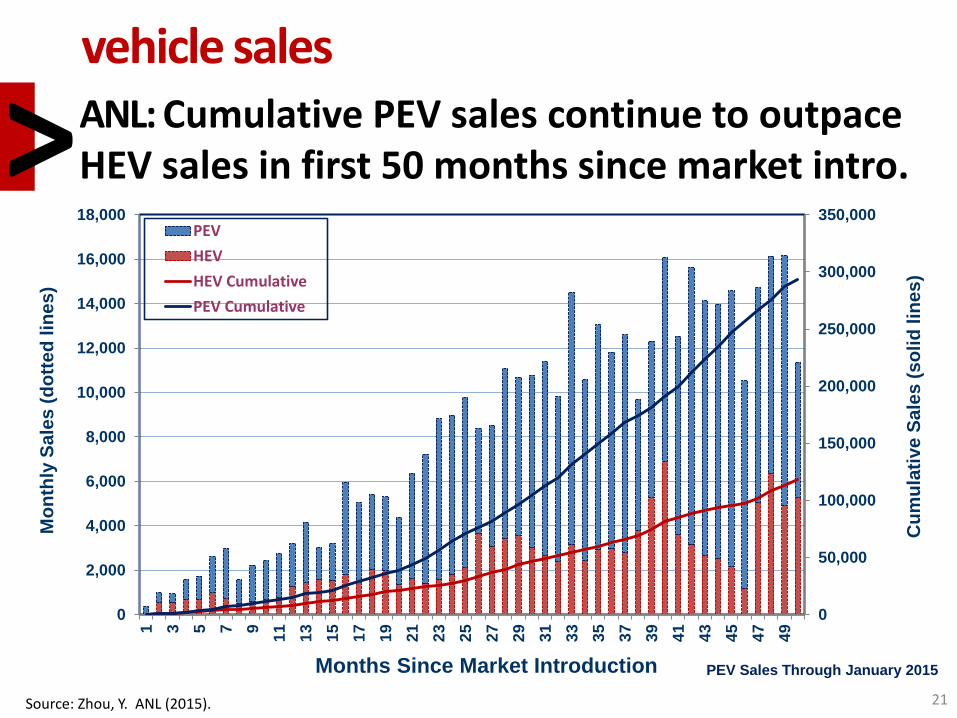

rebounded. > FOTW: ANL: Cumulative PEV sales continue to outpace HEV sales in first 50

months since market intro. > ANL: PEVs comprise more model availability; volume leaders remain the same. > ANL: NEV (xEV+FCV) share of car production in China reaches 0.35% in 2014. > ANL: PEV sales in Europe up >50% from 2013, with 58,582 units sold. > EPIA: EV sales trends mirror those of gas prices.

vehicle trends > FOTW: Vehicles and vehicle travel trends have changed (for the long-term?)

since 2008. > FOTW: Motorization in China is accelerating, but not (yet?) as fast as in early

20th Century U.S. > FOTW: About two-thirds of transportation energy use is gasoline for light

vehicles.

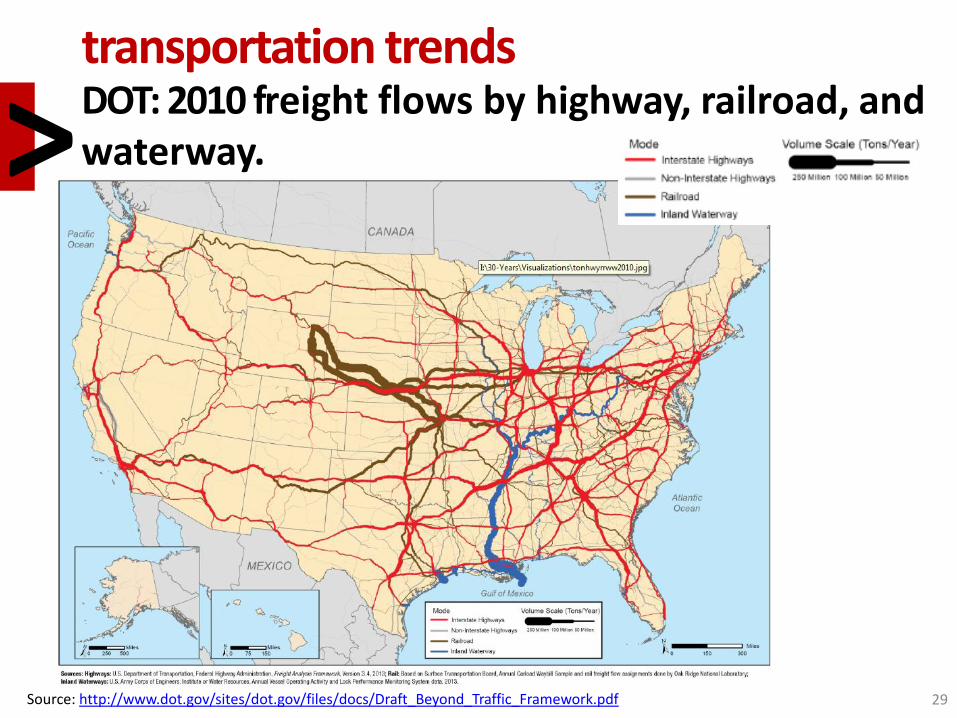

transportation trends > DOT: 2010 freight flows by highway, railroad, and waterway.

2

19

vehicle sales ANL: LDV sales reached record high in May 2014, suggesting the market has fully rebounded. >

20 Source: Zhou, Y. ANL (2015).

vehicle sales ANL: Cumulative PEV sales continue to outpace HEV sales in first 50 months since market intro. >

21

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

1 3 5 7 9

11

13

15

17

19

21

23

25

27

29

31

33

35

37

39

41

43

45

47

49

Cu

mu

lati

ve

Sa

les

(s

oli

d lin

es

)

Mo

nth

ly S

ale

s (

do

tte

d lin

es

)

Months Since Market Introduction

PEV

HEV

HEV Cumulative

PEV Cumulative

PEV Sales Through January 2015

Source: Zhou, Y. ANL (2015).

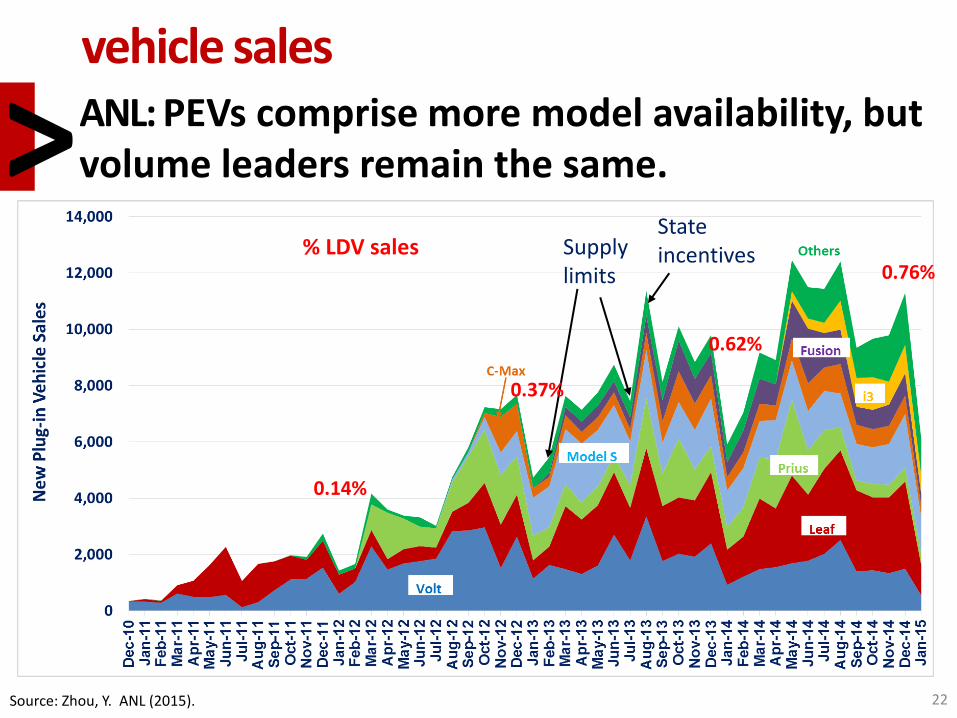

vehicle sales ANL: PEVs comprise more model availability, but volume leaders remain the same. >

22 Source: Zhou, Y. ANL (2015).

4 EV and 2 PHEV Models were introduced in 2014, making the total model availability reached 22 (BME Active E discontinued in 2012)

Supply limits

State incentives

0.76% % LDV sales

0.62%

0.37%

0.14%

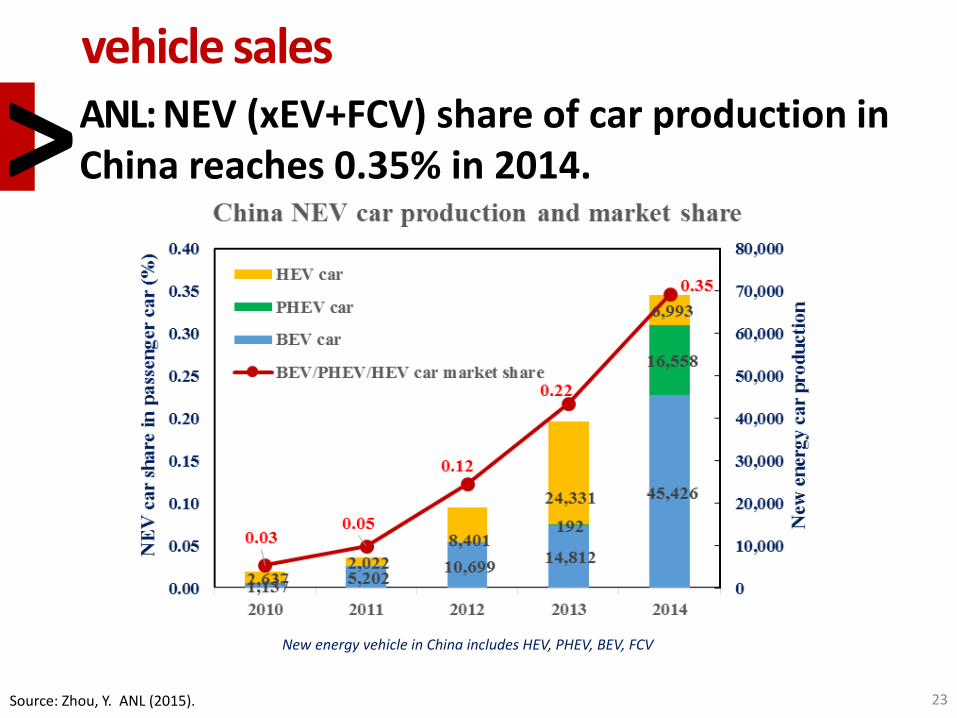

vehicle sales ANL: NEV (xEV+FCV) share of car production in China reaches 0.35% in 2014. >

23 Source: Zhou, Y. ANL (2015).

New energy vehicle in China includes HEV, PHEV, BEV, FCV

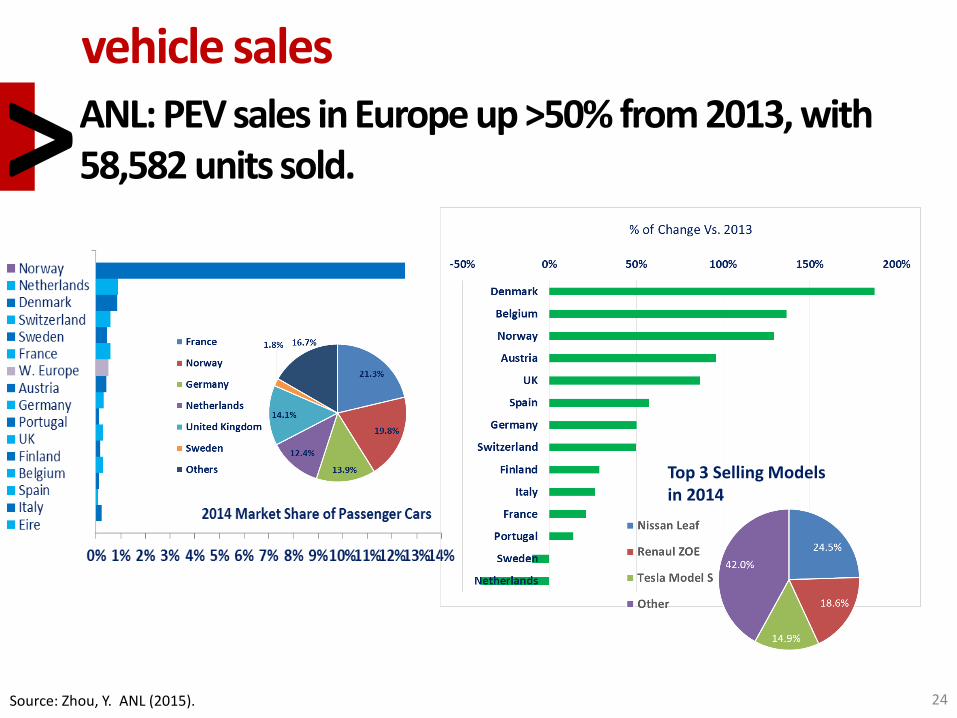

vehicle sales ANL: PEV sales in Europe up >50% from 2013, with 58,582 units sold. >

24 Source: Zhou, Y. ANL (2015).

Top 3 Selling Models in 2014

vehicle sales

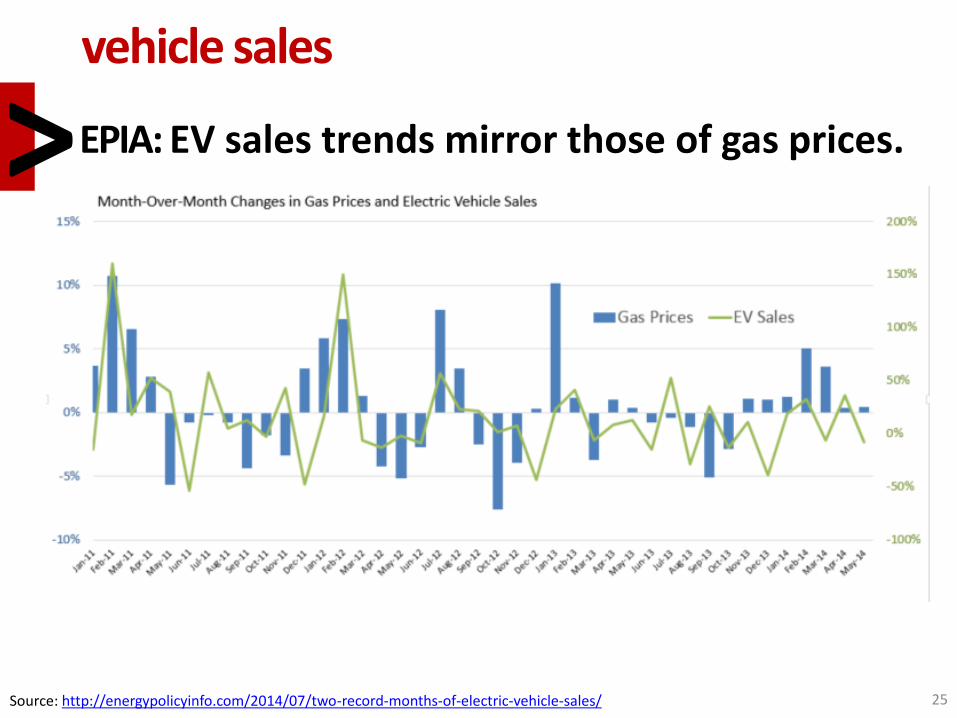

EPIA: EV sales trends mirror those of gas prices. >

25 Source: http://energypolicyinfo.com/2014/07/two-record-months-of-electric-vehicle-sales/

vehicle trends

FOTW: Vehicles and vehicle travel trends have changed (for the long-term?) since 2008. >

Source: http://energy.gov/eere/vehicles/fact-842-october-13-2014-vehicles-and-vehicle-travel-trends-have-changed-2008 26

vehicle trends

FOTW: Motorization in China is accelerating, but not (yet?) as fast as in early 20th Century U.S. >

Source: http://energy.gov/eere/vehicles/fact-841-october-6-2014-vehicles-thousand-people-us-vs-other-world-regions 27

Motorization rate in China grew in 10 years (2002-2012) the same amount U.S. motorization grew in only 7 years, one century earlier (1912-1920). (Though, different market size should be considered.)

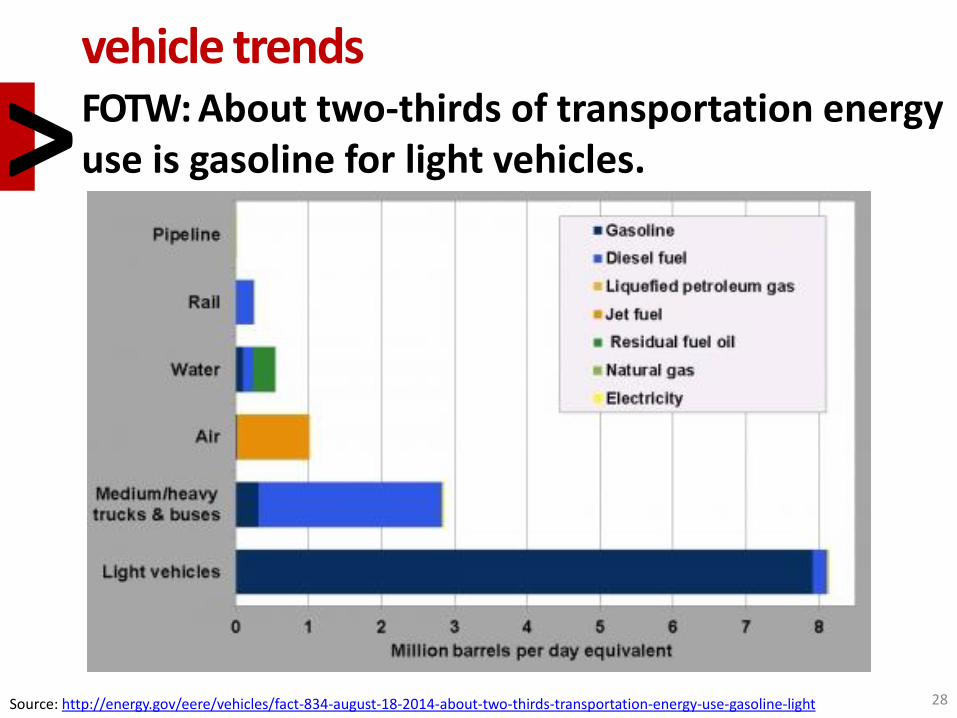

vehicle trends FOTW: About two-thirds of transportation energy use is gasoline for light vehicles. >

Source: http://energy.gov/eere/vehicles/fact-834-august-18-2014-about-two-thirds-transportation-energy-use-gasoline-light 28

transportation trends DOT: 2010 freight flows by highway, railroad, and waterway. >

29 Source: http://www.dot.gov/sites/dot.gov/files/docs/Draft_Beyond_Traffic_Framework.pdf

topics

energy markets automotive markets technologies studies environmental studies consumers/opinion surveys policy studies

outline

3 qar

30

technologies studies

vehicle technology > EPA: Advanced technology and alternative fuel vehicle models increased

through MY 2014. > EPA: Stop/start technology is in ~5% of all new light vehicles produced.

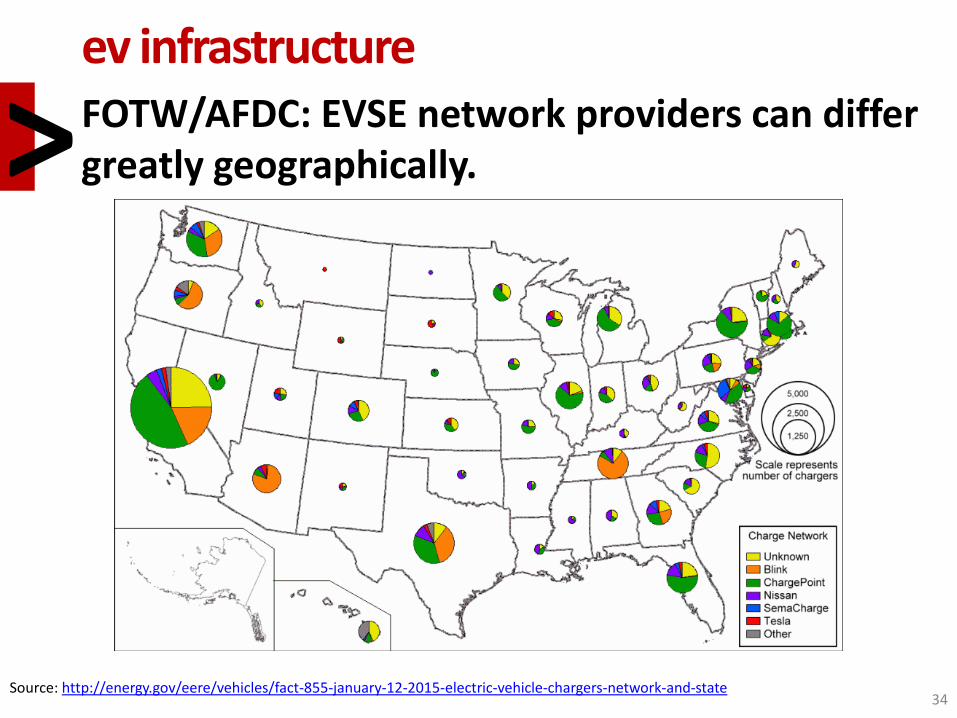

ev infrastructure > FOTW/AFDC: EVSE network providers can differ greatly geographically.

ev range > FOTW: Driving ranges for all-electric vehicles in MY2014 vary (from 62 to 265

miles). > ORNL/FleetCarma: EV efficiency (and, therefore, range) uncertainty a potential

concern?

3

31

vehicle technology EPA: Advanced technology and alternative fuel vehicle models increased through MY 2014. >

32 Source: http://epa.gov/otaq/fetrends.htm

vehicle technology EPA/FOTW: Stop/start technology is in ~5% of all new light vehicles produced. >

33 Source: http://energy.gov/eere/vehicles/fact-853-december-29-2014-stopstart-technology-nearly-5-all-new-light-vehicles

ev infrastructure FOTW/AFDC: EVSE network providers can differ greatly geographically. >

34 Source: http://energy.gov/eere/vehicles/fact-855-january-12-2015-electric-vehicle-chargers-network-and-state

ev range FOTW: Driving ranges for all-electric vehicles in MY2014 vary (from 62 to 265 miles). >

35 Source: http://energy.gov/eere/vehicles/fact-854-january-5-2015-driving-ranges-all-electric-vehicles-model-year-2014-vary-62

ev range ORNL/FleetCarma: EV efficiency (and, therefore, range) uncertainty a potential concern? >

36 Source: http://www.fleetcarma.com/Real-World/Gas-Mileage-MPG/Nissan-Leaf/2013

Source: FleetCarma.com 9,351 Trips by 2013 Nissan Leaf

topics

energy markets automotive markets technologies studies environmental studies consumers/opinion surveys policy studies

outline

4 qar

37

environmental studies

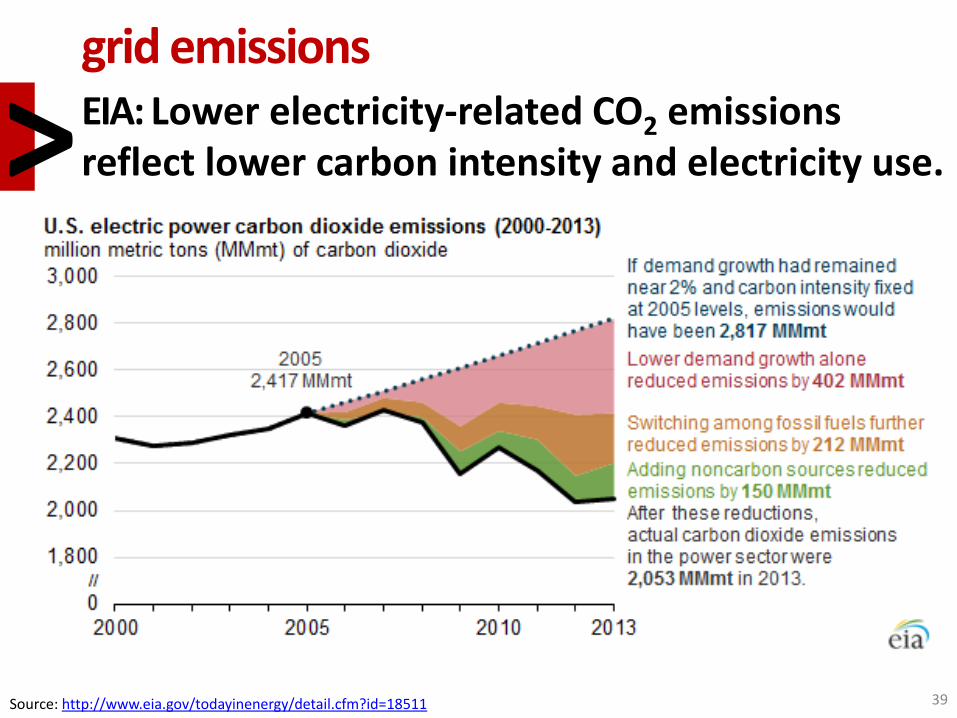

grid emissions > EIA: Lower electricity-related CO2 emissions reflect lower carbon

intensity and electricity use. > FOTW: World renewable electricity consumption is growing (especially

in China).

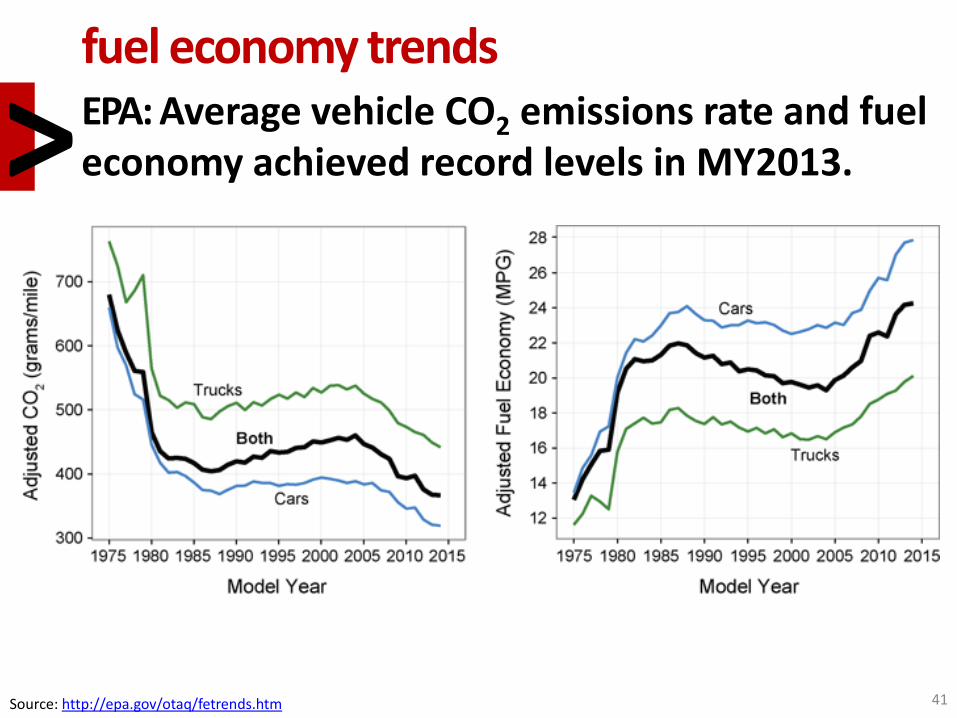

fuel economy trends > EPA: Average vehicle CO2 emissions rate and fuel economy achieved

record levels in MY2013. > EPA: More models meet fuel economy thresholds in MY2014. > EPA: <5% of MY2014 vehicles meet MY 2025 CO2 targets (and all are

advanced powertrain).

4

38

grid emissions EIA: Lower electricity-related CO2 emissions reflect lower carbon intensity and electricity use. >

Source: http://www.eia.gov/todayinenergy/detail.cfm?id=18511

39

grid emissions FOTW: World renewable electricity consumption is growing (especially in China). >

Source: http://energy.gov/eere/vehicles/fact-840-september-29-2014-world-renewable-electricity-consumption-growing

40

fuel economy trends EPA: Average vehicle CO2 emissions rate and fuel economy achieved record levels in MY2013. >

Source: http://epa.gov/otaq/fetrends.htm

41

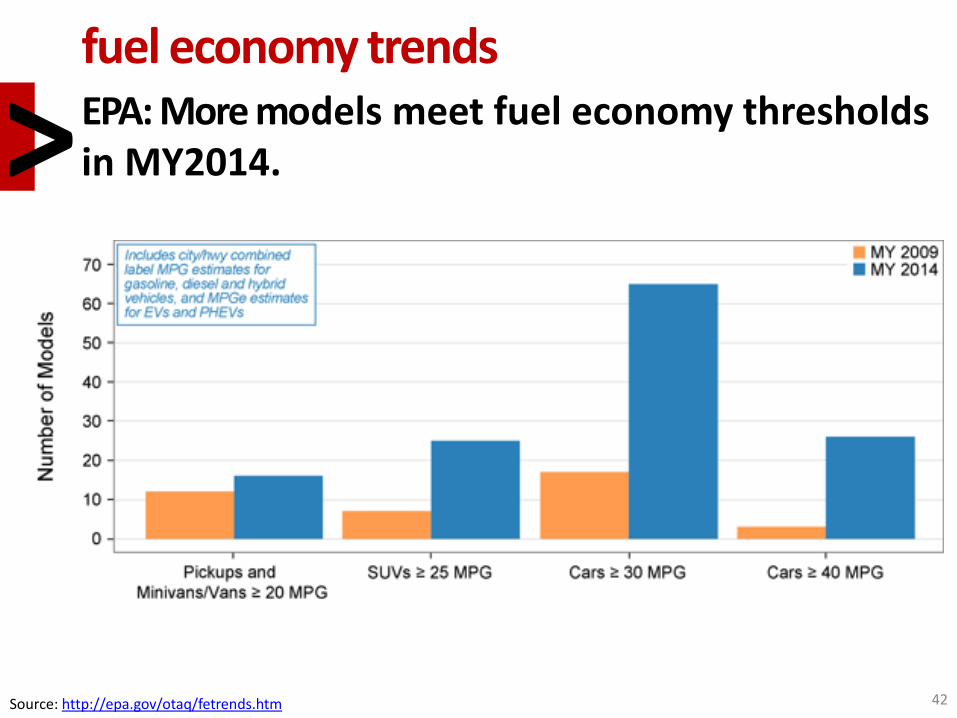

fuel economy trends EPA: More models meet fuel economy thresholds in MY2014. >

Source: http://epa.gov/otaq/fetrends.htm

42

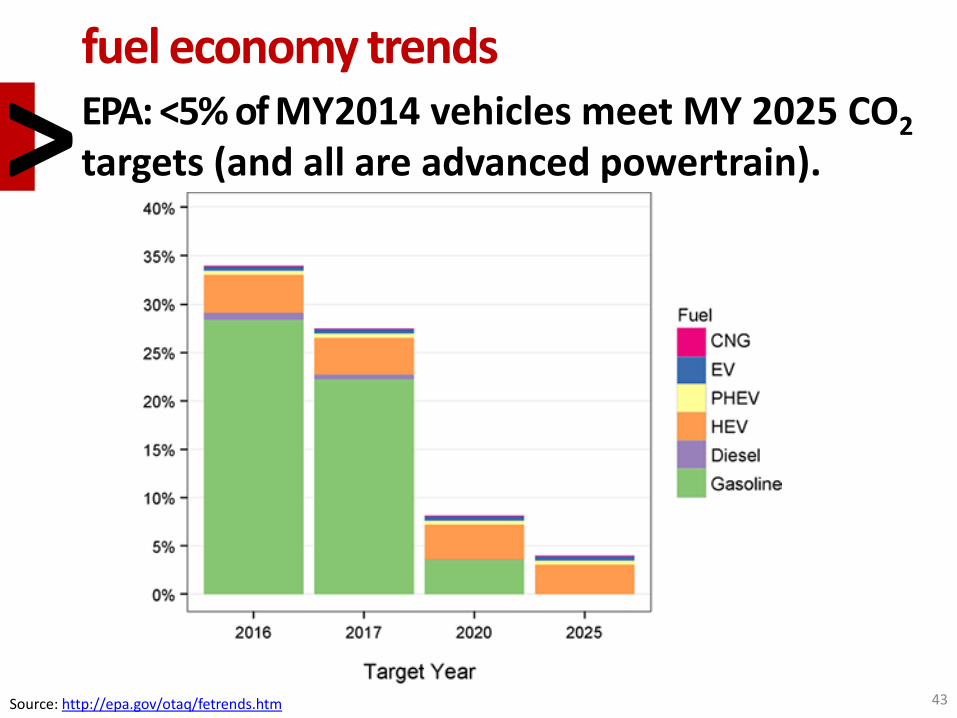

fuel economy trends EPA: <5% of MY2014 vehicles meet MY 2025 CO2 targets (and all are advanced powertrain). >

Source: http://epa.gov/otaq/fetrends.htm

43

topics

energy markets automotive markets technologies studies environmental studies consumers/opinion surveys policy studies

outline 5 qar

44

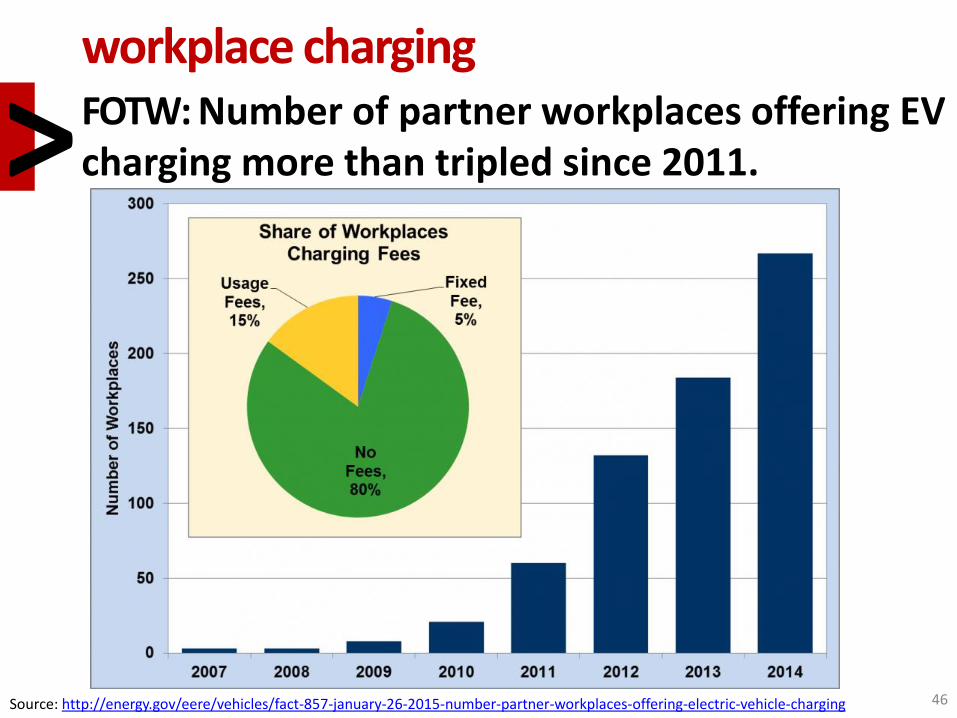

consumer & opinion surveys workplace charging > FOTW: Number of partner workplaces offering EV charging more than

tripled since 2011.

consumer opinion > FOTW: Plug-in and hybrid cars receive high owner satisfaction scores

(Consumer Reports). > FOTW: Relative importance of fuel economy decreases (but still 2nd-

ranked) > UMTRI: Public opinion about self-driving vehicles differs by country. > UT Energy Poll: survey indicates renewable, efficiency, and EV technology

subsidies favored. > CSE: Primary motivations for PEV purchase differ by advanced vehicle

architecture.

5

45

workplace charging FOTW: Number of partner workplaces offering EV charging more than tripled since 2011. >

Source: http://energy.gov/eere/vehicles/fact-857-january-26-2015-number-partner-workplaces-offering-electric-vehicle-charging 46

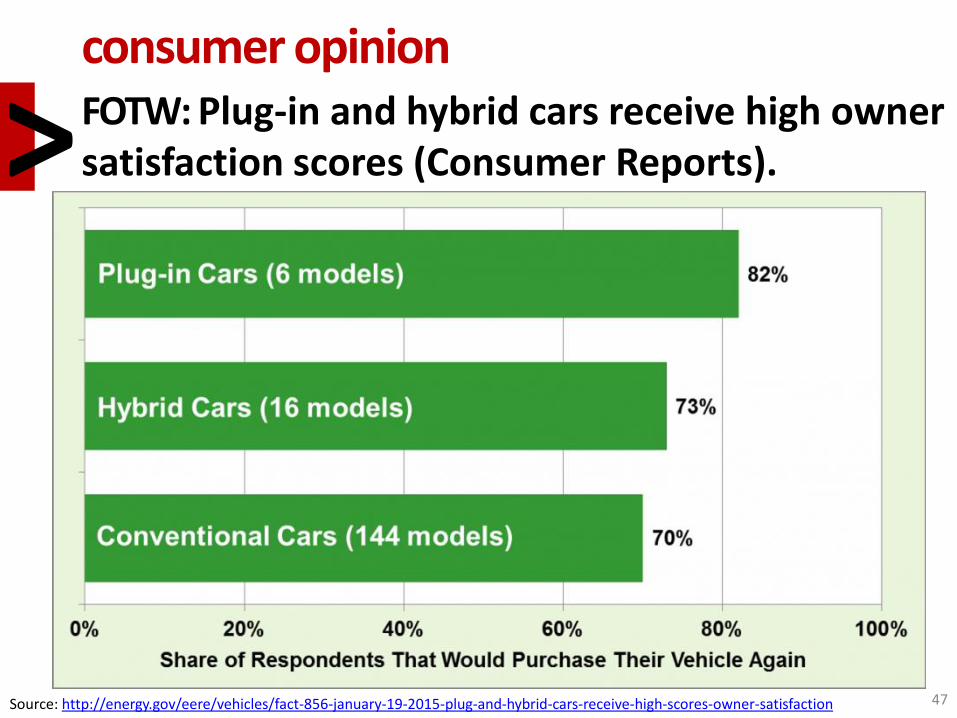

consumer opinion FOTW: Plug-in and hybrid cars receive high owner satisfaction scores (Consumer Reports). >

Source: http://energy.gov/eere/vehicles/fact-856-january-19-2015-plug-and-hybrid-cars-receive-high-scores-owner-satisfaction 47

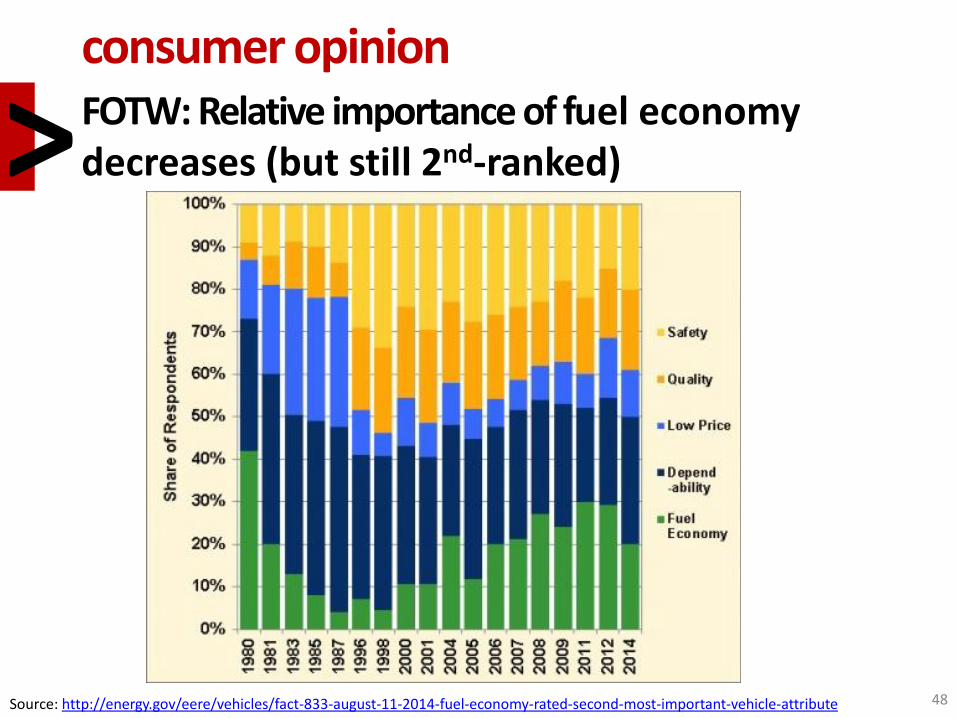

consumer opinion FOTW: Relative importance of fuel economy decreases (but still 2nd-ranked) >

Source: http://energy.gov/eere/vehicles/fact-833-august-11-2014-fuel-economy-rated-second-most-important-vehicle-attribute 48

consumer opinion UMTRI: Public opinion about self-driving vehicles differs by country. >

Source: Michael Sivak and Brandon Schoettle (UMTRI), http://deepblue.lib.umich.edu/bitstream/handle/2027.42/109433/103139.pdf 49

0

10

20

30

40

50

60

China India Japan U.S. U.K. Australia

Very positive

Somewhat positive

Neutral

Somewhat negative

Very negative

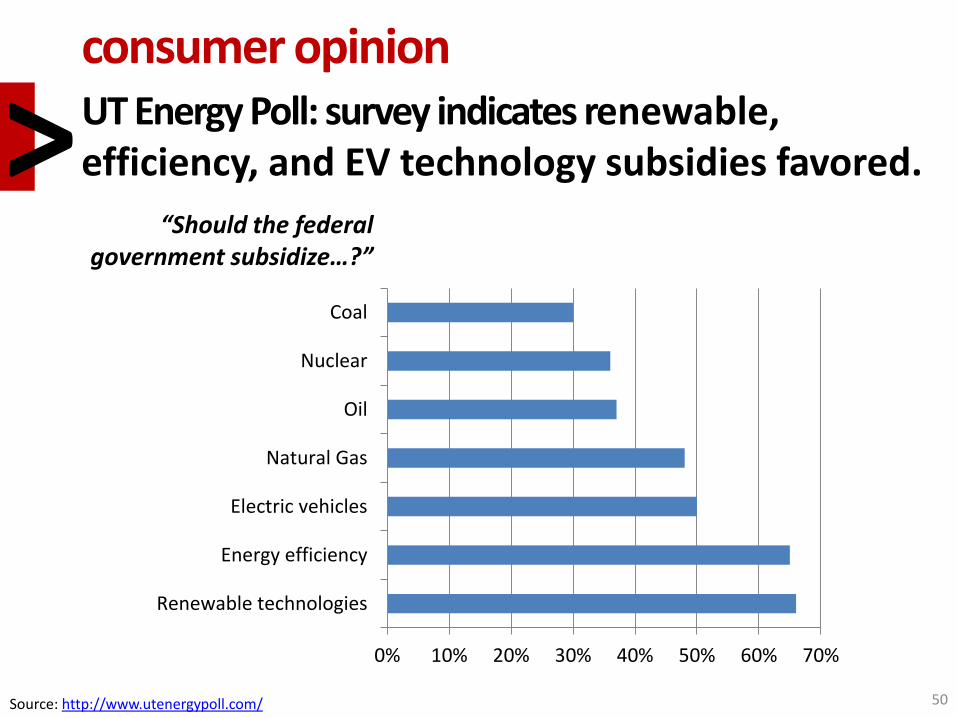

consumer opinion UT Energy Poll: survey indicates renewable, efficiency, and EV technology subsidies favored. >

Source: http://www.utenergypoll.com/ 50

0% 10% 20% 30% 40% 50% 60% 70%

Renewable technologies

Energy efficiency

Electric vehicles

Natural Gas

Oil

Nuclear

Coal

“Should the federal government subsidize…?”

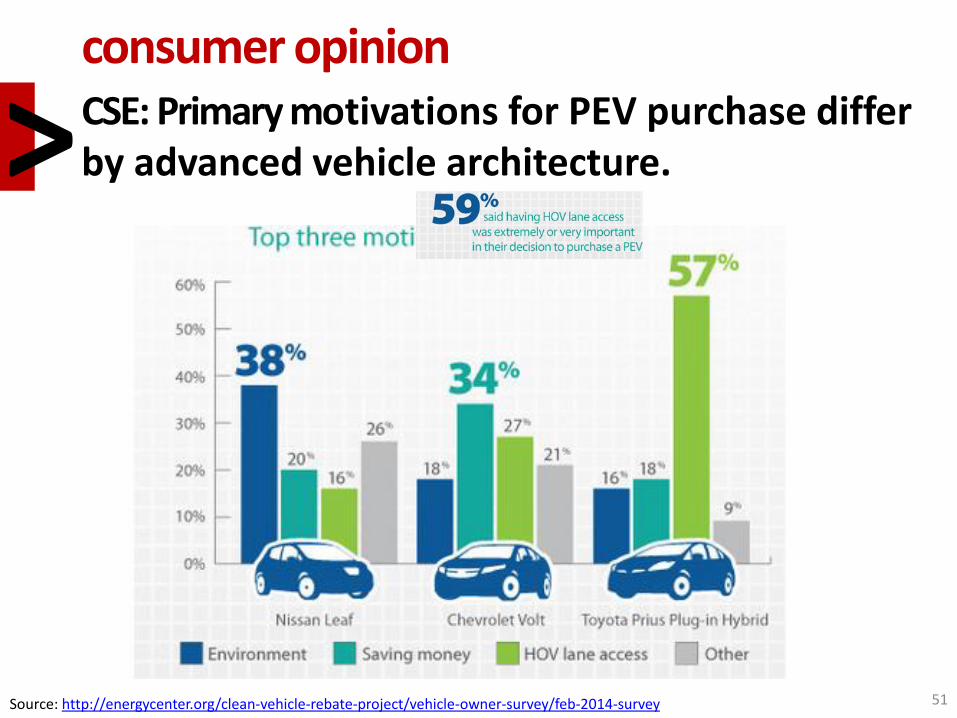

consumer opinion CSE: Primary motivations for PEV purchase differ by advanced vehicle architecture. >

Source: http://energycenter.org/clean-vehicle-rebate-project/vehicle-owner-survey/feb-2014-survey 51

topics

energy markets automotive markets technologies studies environmental studies consumers/opinion surveys policy studies

outline 6 qar

52

policy studies ev incentives > ICCT: Fully monetized state PEV incentives are not directly correlated to state PEV

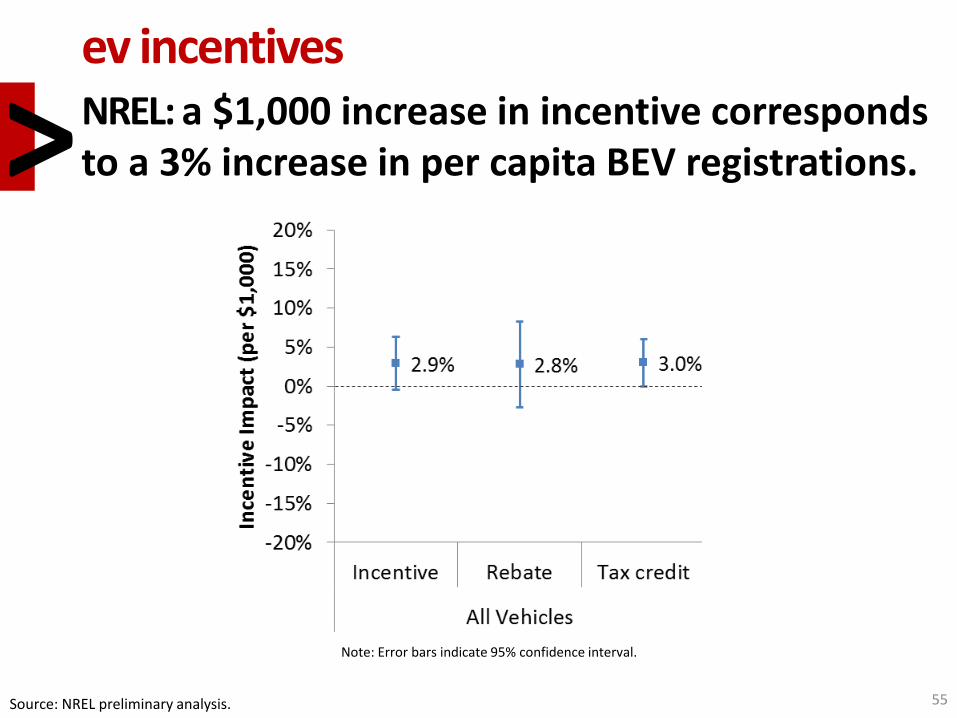

sales. > NREL: a $1,000 increase in incentive corresponds to a 3% increase in per capita

BEV registrations.

evse rollout > ANL: Charging infrastructure and PEV market shares differ greatly by state.

6

53

ev incentives ICCT: Fully monetized state PEV incentives are not directly correlated to state PEV sales. >

Source: http://www.theicct.org/evaluation-state-level-us-electric-vehicle-incentives 54

ev incentives NREL: a $1,000 increase in incentive corresponds to a 3% increase in per capita BEV registrations. >

Source: NREL preliminary analysis. 55

Note: Error bars indicate 95% confidence interval.

evse rollout ANL: Charging infrastructure and PEV market shares differ greatly by state.

>

Source: ANL preliminary analysis. 56

energy

automotive

tech/enviro

opinion/policy

summary qar

>

14.3&4 3 & 4 Q 2 0 1 4

57

market projections estimate a decrease in relatively high-priced tight oil but an overall increase in U.S. domestic production.

the LDV market has more than fully rebounded after the 2008 economic crash.

advanced vehicle/grid technologies continue to grow and offer benefits.

heterogeneity in consumer opinions and motivations complicates policy and technology considerations.

summary observations