Africa’s future and the World Bank’s support to it

1

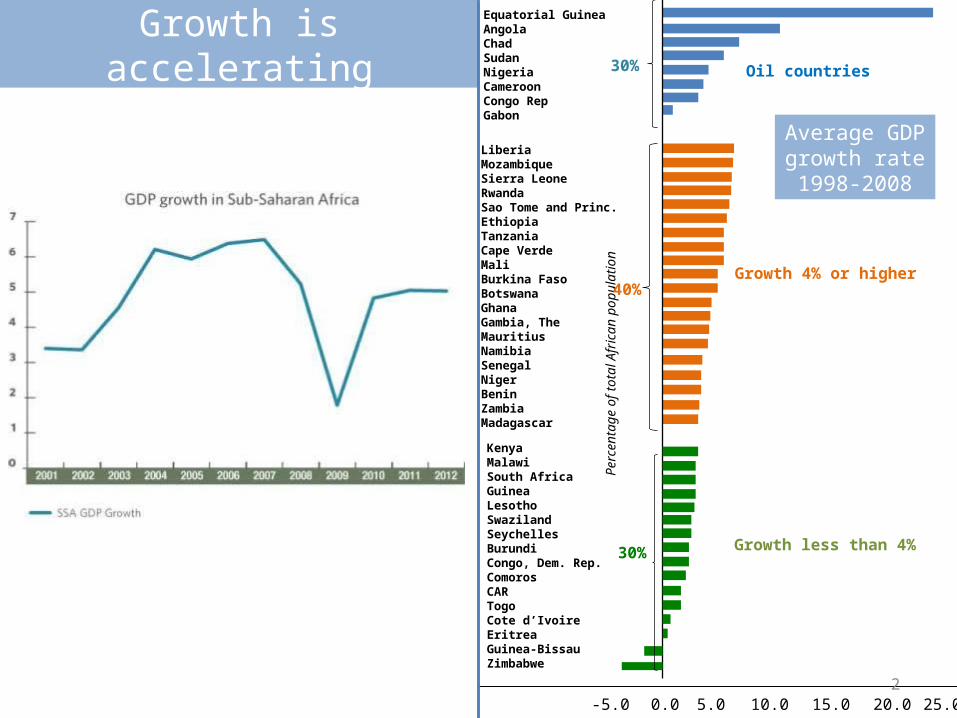

Growth is accelerating•Thanks to continued, prudent economic policies, rapid rebound from the crisis

Equatorial GuineaAngolaChadSudanNigeriaCameroonCongo RepGabon

LiberiaMozambiqueSierra LeoneRwandaSao Tome and Princ.EthiopiaTanzaniaCape VerdeMaliBurkina FasoBotswanaGhanaGambia, TheMauritiusNamibiaSenegalNigerBeninZambiaMadagascar

KenyaMalawiSouth AfricaGuineaLesothoSwazilandSeychellesBurundiCongo, Dem. Rep.ComorosCARTogoCote d’IvoireEritreaGuinea-BissauZimbabwe

0.0-5.0 5.0 10.0 15.0 20.0 25.0

Per

cent

age

of to

tal A

fric

an p

opul

atio

n

30%

40%

30%

Oil countries

Growth 4% or higher

Growth less than 4%

Average GDP growth rate 1998-2008

2

17

2429 31 33 31 33

30 3227 28

31 33

13 13

7 6 6 7 6 5 4 2 3 2 2

0

20

40

60

80

100

120

140

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Av

era

ge

In

fla

tio

n R

ate

%

0

5

10

15

20

25

30

35

40

45

Nu

mb

er

of

Co

un

trie

s Inflation>20%

10%<inflation<=20%

Inflation<=10%

Median inflation rate

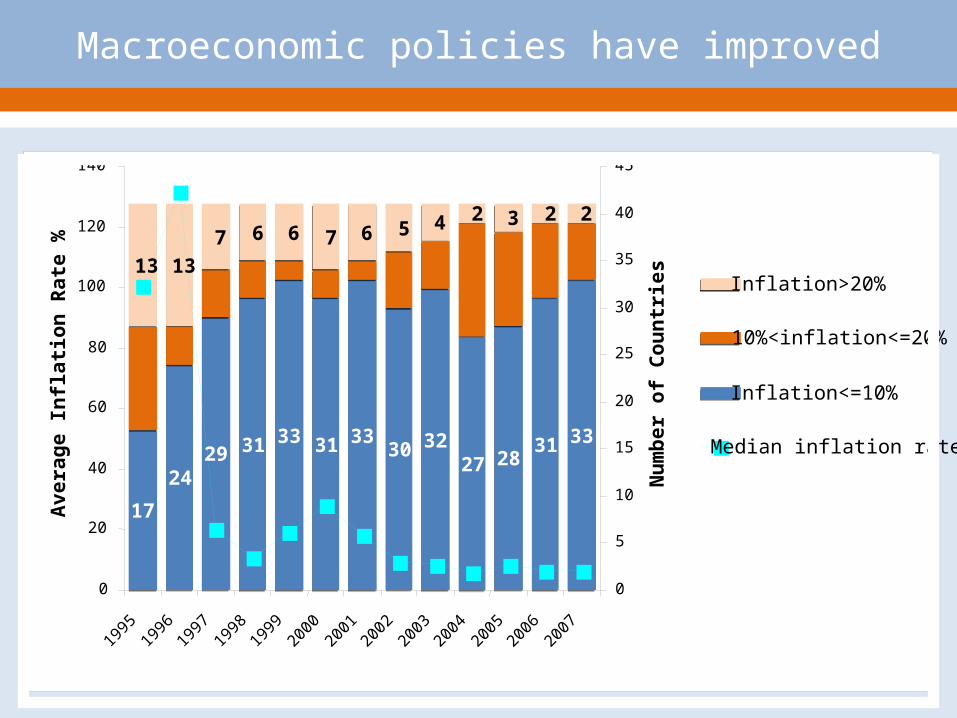

Macroeconomic policies have improved

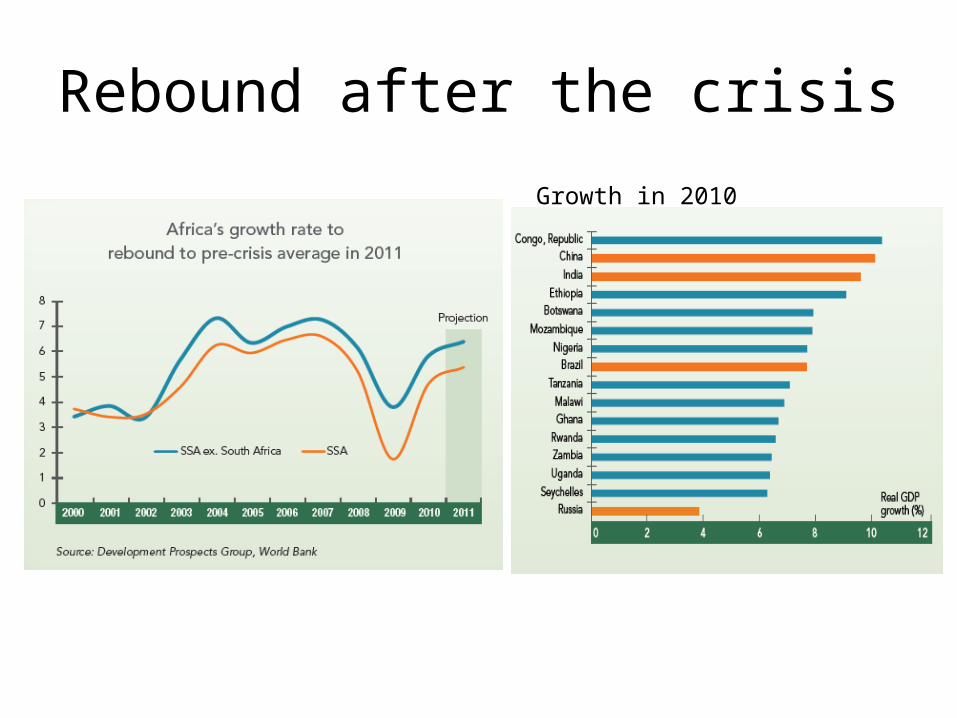

Rebound after the crisis

Growth in 2010

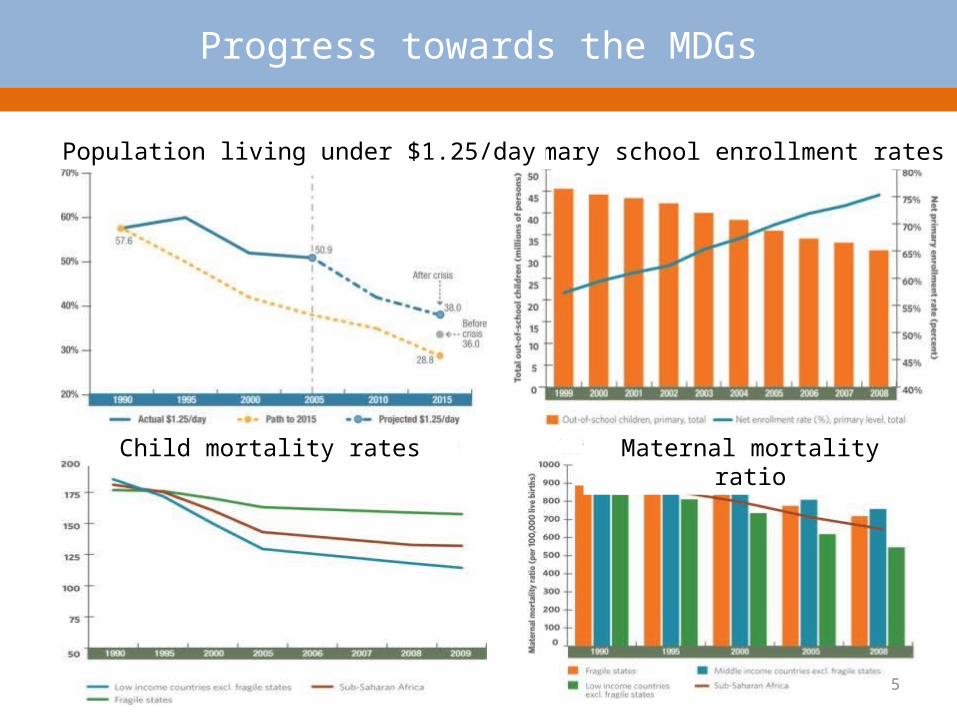

Progress towards the MDGs

Primary school enrollment ratesPopulation living under $1.25/day

Child mortality rates Maternal mortality ratio

5

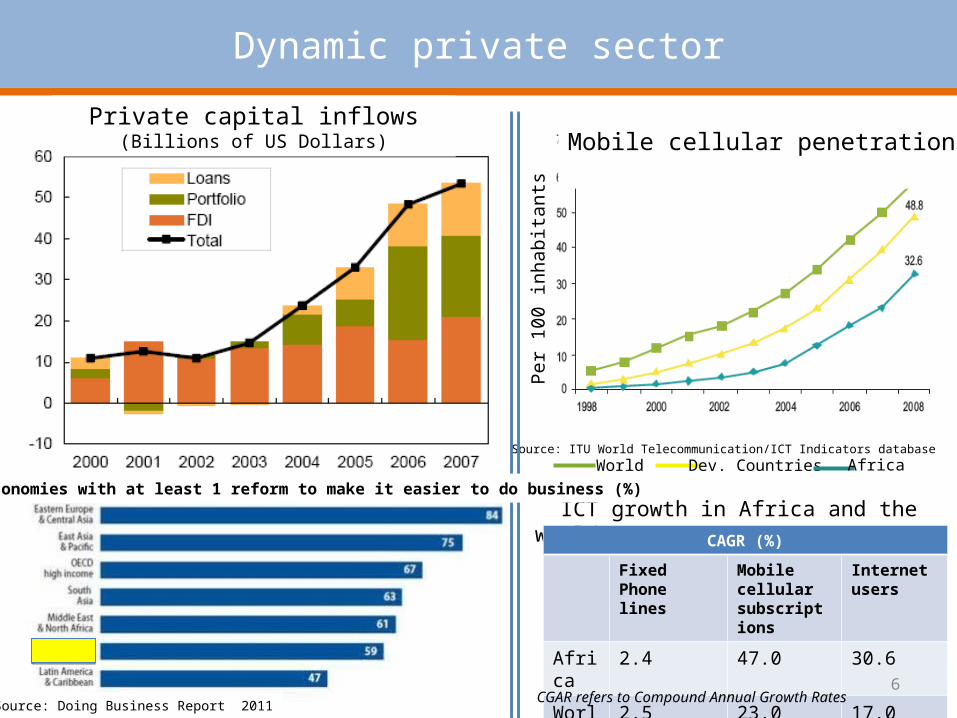

Dynamic private sector

World Dev. Countries Africa

Per 1

00 in

habi

tant

s

Source: ITU World Telecommunication/ICT Indicators database

Private capital inflows(Billions of US Dollars) Mobile cellular penetration

ICT growth in Africa and the world, 2003-2008 CAGR (%)

Fixed Phone lines

Mobile cellular subscriptions

Internet users

Africa 2.4 47.0 30.6

World 2.5 23.0 17.06

CGAR refers to Compound Annual Growth Rates

Share of economies with at least 1 reform to make it easier to do business (%)

Source: Doing Business Report 2011

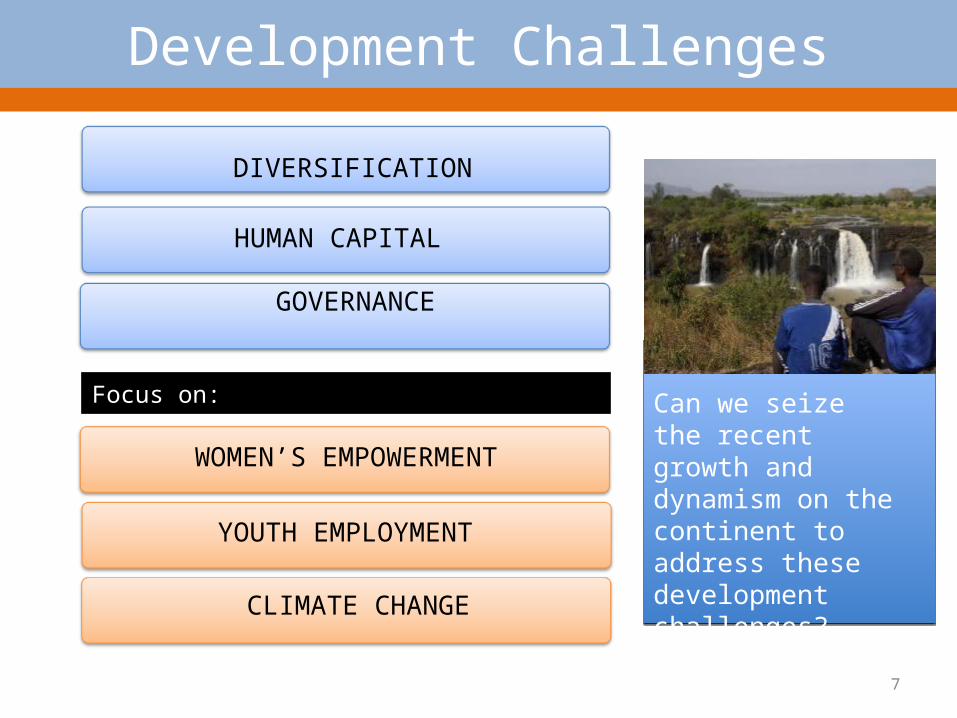

DIVERSIFICATION

HUMAN CAPITAL

GOVERNANCE

Development Challenges

CLIMATE CHANGE

YOUTH EMPLOYMENT

WOMEN’S EMPOWERMENT

Focus on: Can we seize the recent growth and dynamism on the continent to address these development challenges?

7

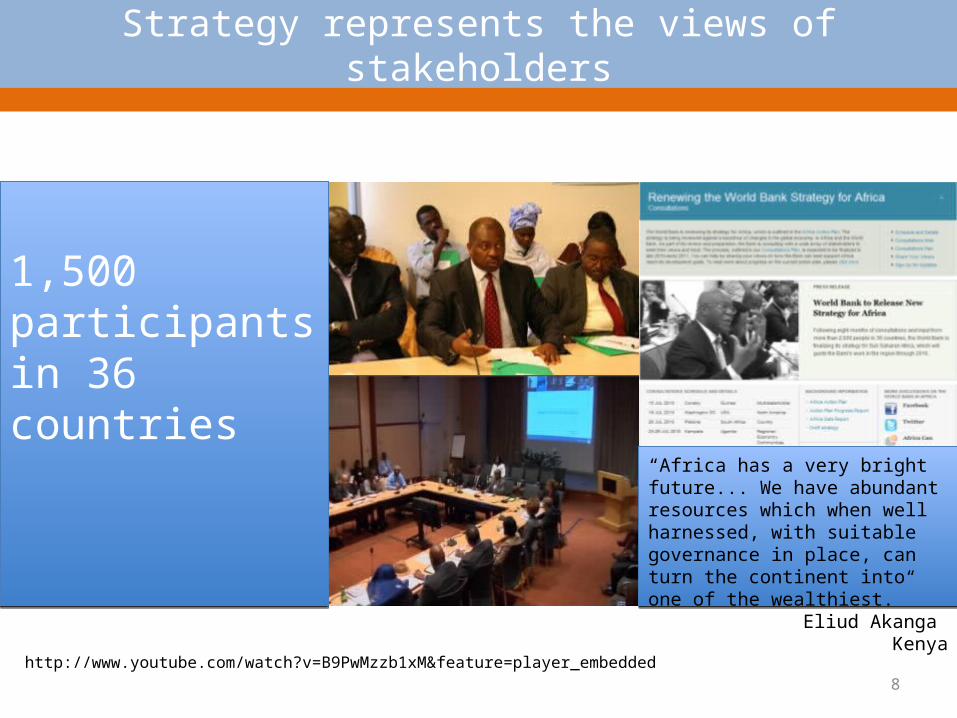

1,500 participants in 36 countries

Strategy represents the views of stakeholders

http://www.youtube.com/watch?v=B9PwMzzb1xM&feature=player_embedded

“Africa has a very bright future... We have abundant resources which when well harnessed, with suitable governance in place, can turn the continent into one of the wealthiest.”

Eliud Akanga Kenya

8

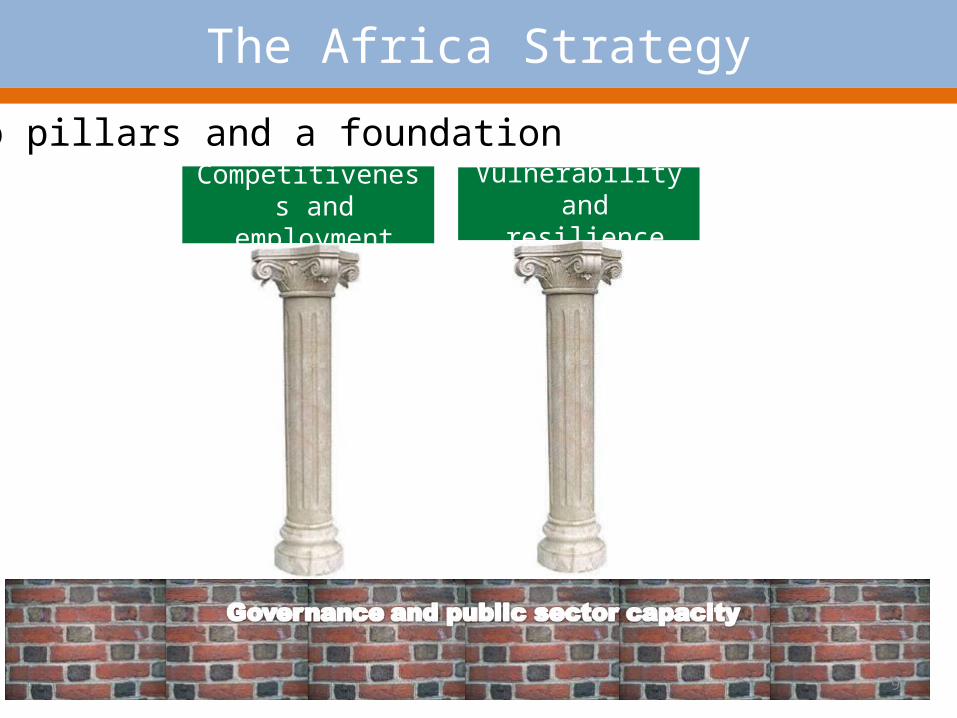

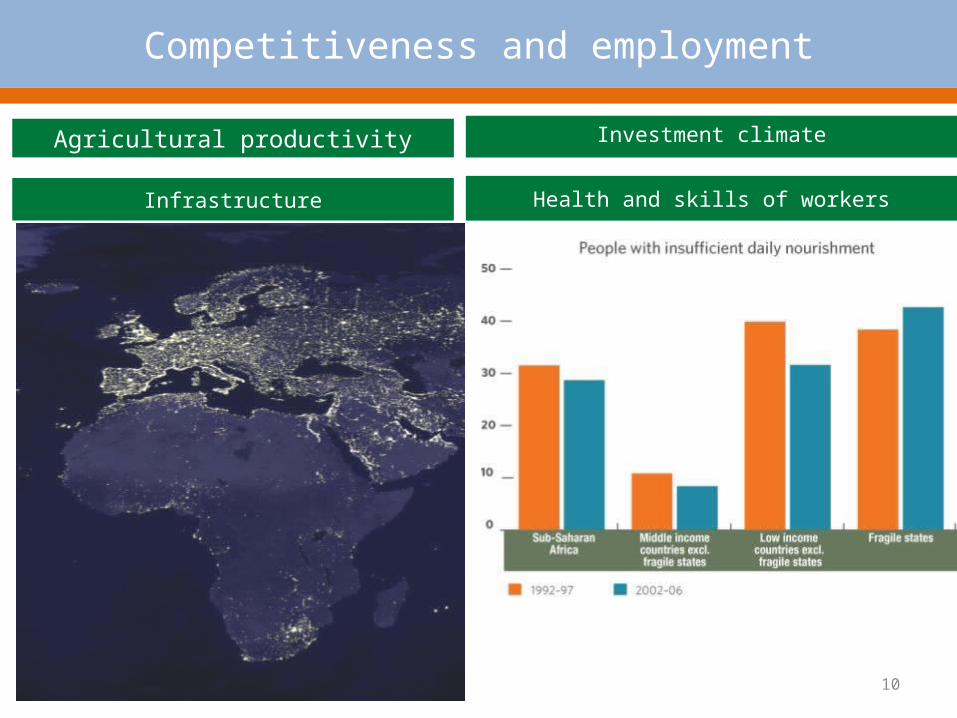

Competitiveness and employment

Vulnerability and resilience

Two pillars and a foundation

The Africa Strategy

9

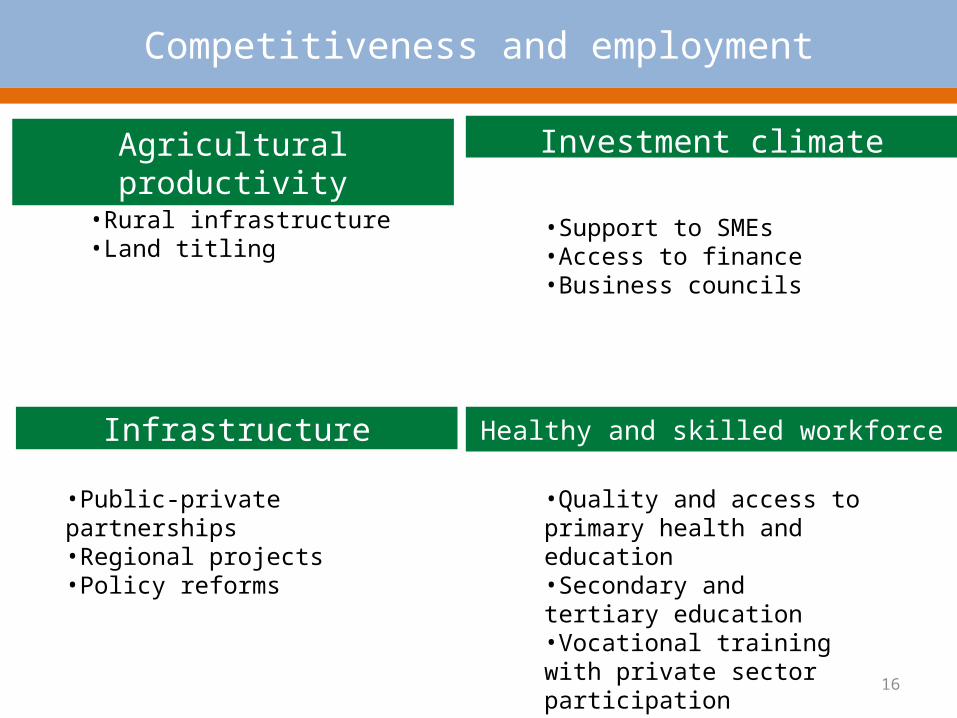

Infrastructure

Investment climate

Health and skills of workers

Competitiveness and employment

Agricultural productivity

Source: Briceño-Garmendia, Smits, and Foster 2008. 10

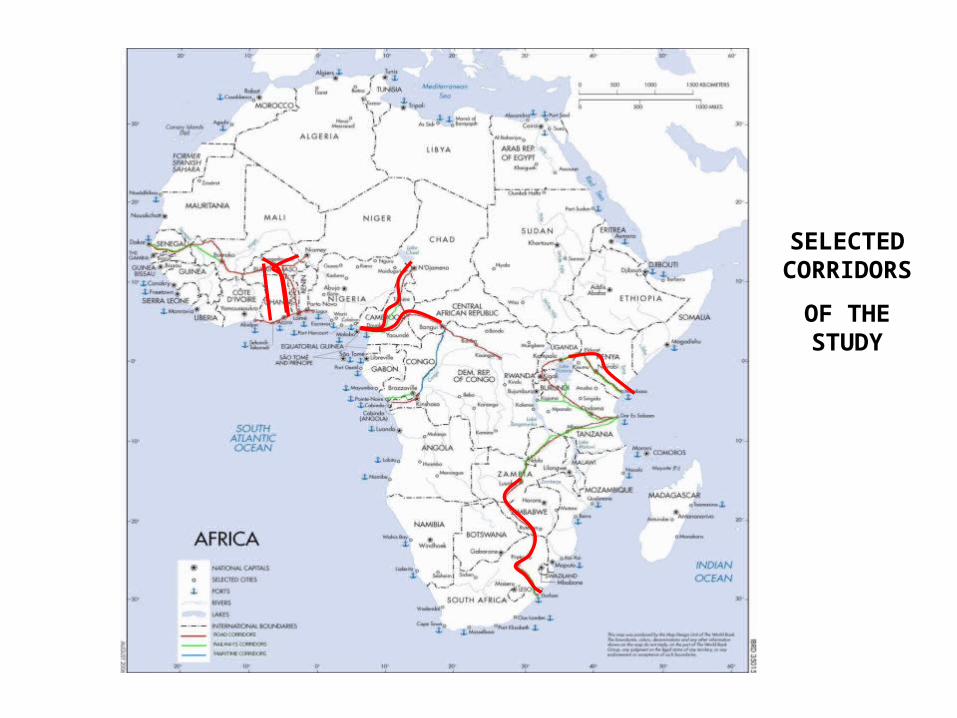

SELECTED CORRIDORS

OF THE STUDY

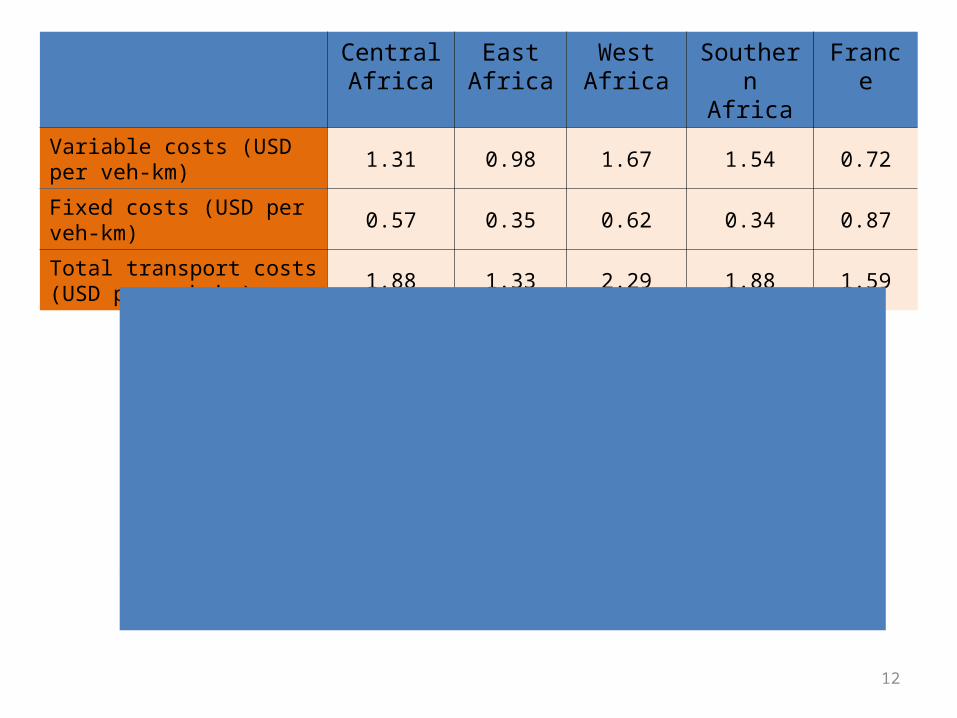

Central Africa

East Africa

West Africa

Southern Africa

France

Variable costs (USD per veh-km) 1.31 0.98 1.67 1.54 0.72

Fixed costs (USD per veh-km) 0.57 0.35 0.62 0.34 0.87

Total transport costs (USD per veh-km) 1.88 1.33 2.29 1.88 1.59

12

23.5 4

5 5 5

78

11

0

2

4

6

8

10

12

14

Pakis

tan

Bra

zil

US

A

Chin

a

Weste

rn

Euro

pe –

long

dis

tance

Afr

ica-

Durb

an-

Lusaka

Afr

ica-

Lom

é -

Ouagadougou

Afr

ica –

Mom

basa

Kam

pala

Afr

ica-

Douala

-

Ndja

ména

Avera

ge t

ransport

prices

(in U

S c

ents

per

tkm

)

Pakis

tan

Braz

il

USA Chin

aW

este

rn Eu

rope

Long

- Dist

ance

Afric

aDur

ban

- Lus

aka

Afric

a – Lo

me-

Ouaga

doug

ouAf

rica

Mom

basa

-Kam

pala

Afric

a

Douala

-Ndj

amen

a

Average Transport Prices(in US cents per tkm)

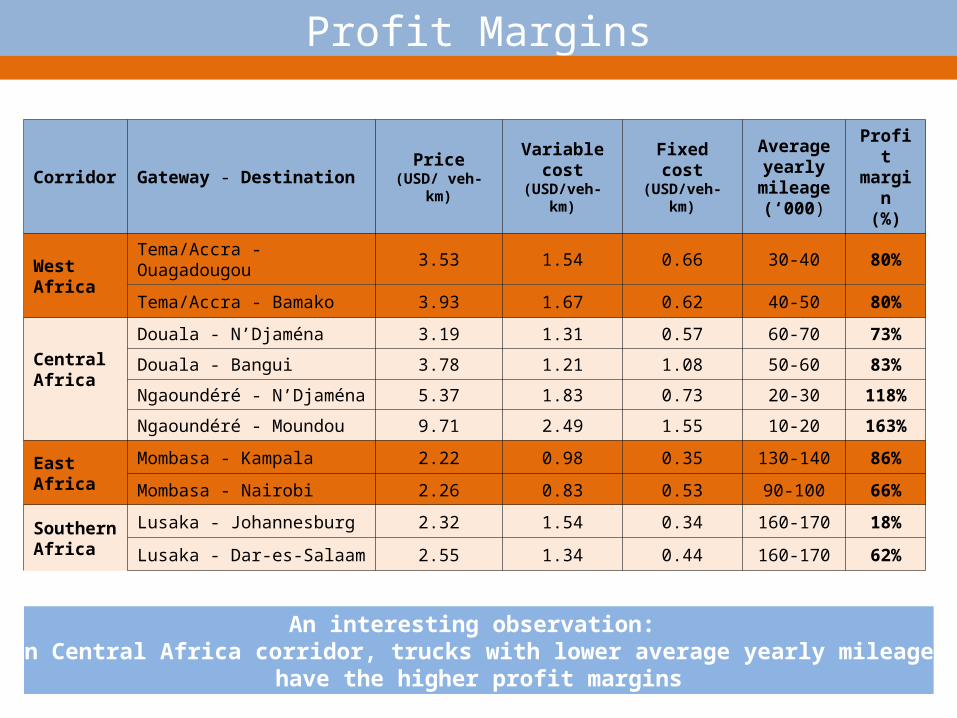

Corridor Gateway - Destination Price(USD/ veh-km)

Variable cost

(USD/veh- km)

Fixed cost(USD/veh- km)

Average yearly

mileage (‘000)

Profit margin

(%)

West Africa

Tema/Accra - Ouagadougou 3.53 1.54 0.66 30-40 80%

Tema/Accra - Bamako 3.93 1.67 0.62 40-50 80%

Central Africa

Douala - N’Djaména 3.19 1.31 0.57 60-70 73%

Douala - Bangui 3.78 1.21 1.08 50-60 83%

Ngaoundéré - N’Djaména 5.37 1.83 0.73 20-30 118%

Ngaoundéré - Moundou 9.71 2.49 1.55 10-20 163%

East Africa

Mombasa - Kampala 2.22 0.98 0.35 130-140 86%

Mombasa - Nairobi 2.26 0.83 0.53 90-100 66%

Southern Africa

Lusaka - Johannesburg 2.32 1.54 0.34 160-170 18%

Lusaka - Dar-es-Salaam 2.55 1.34 0.44 160-170 62%

An interesting observation: On Central Africa corridor, trucks with lower average yearly mileage

have the higher profit margins

Profit Margins

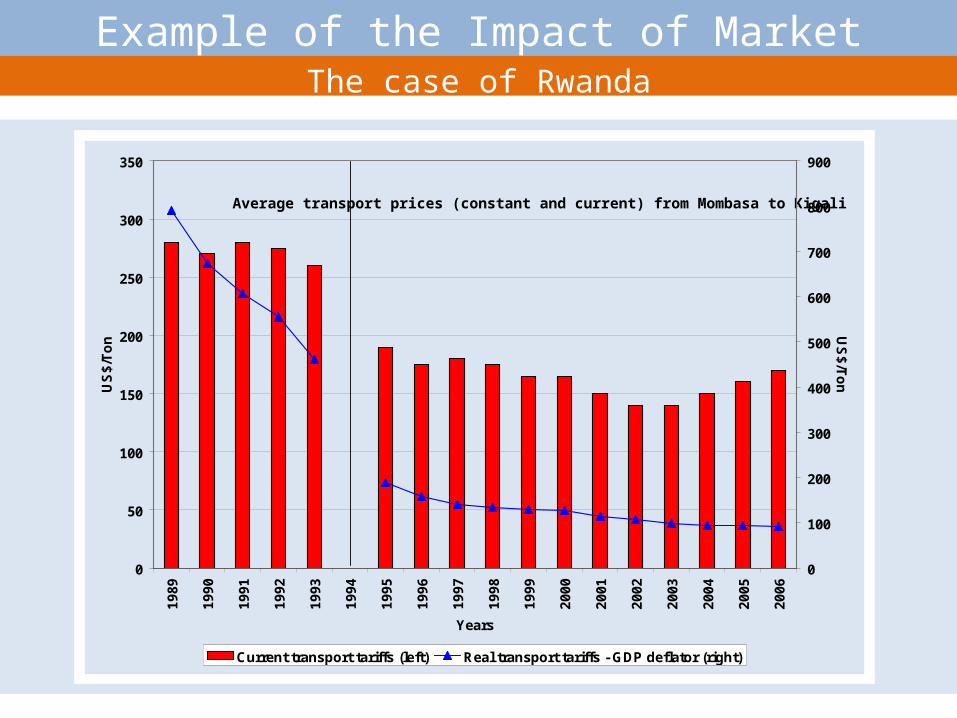

Average transport prices (constant and current) from Mombasa to Kigali

0

50

100

150

200

250

300

3501

98

9

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

Years

US

$/T

on

0

100

200

300

400

500

600

700

800

900

US

$/T

on

Current transport tariffs (left) Real transport tariffs - GDP deflator (right)

After liberalizationBefore liberalization

Example of the Impact of Market Deregulation:The case of Rwanda

Competitiveness and employment

0.0

1.0

2.0

3.0

4.0

5.0

2000-04 2001-05 2002-06 2003-07 2004-2008

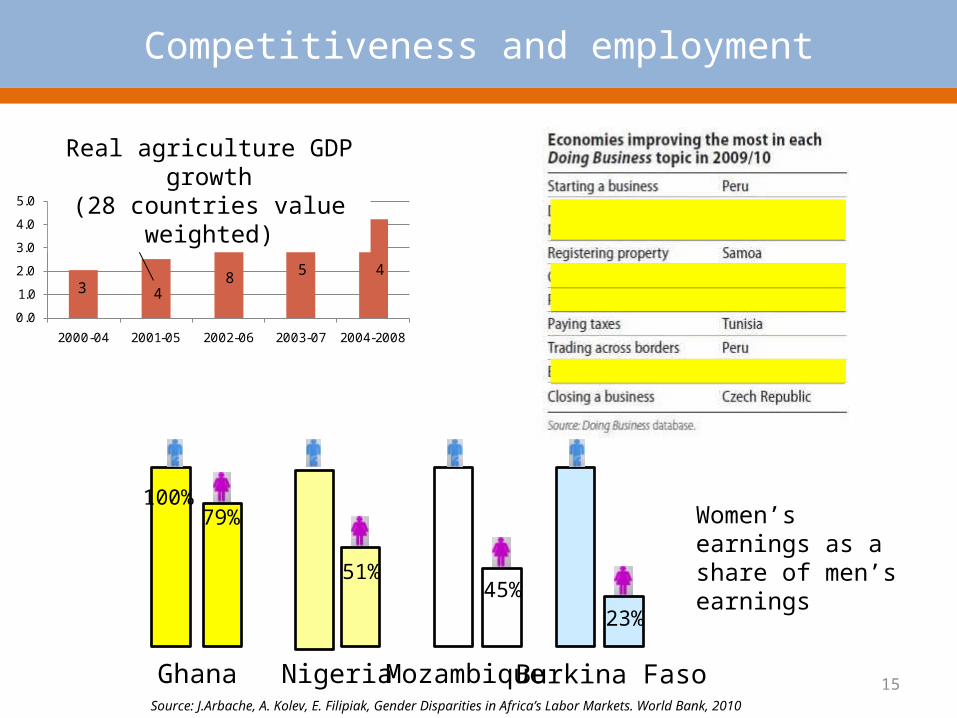

Real Agricultural GDP (28 countries value weighted)

48 5

34

#of countries > 5%/yr

Real agriculture GDP growth(28 countries value weighted)

15Ghana Nigeria Mozambique Burkina Faso

100%

51%45%

23%

79%

Source: J.Arbache, A. Kolev, E. Filipiak, Gender Disparities in Africa’s Labor Markets. World Bank, 2010

Women’s earnings as a share of men’s earnings

Infrastructure

Investment climate

Healthy and skilled workforce

Competitiveness and employment

Agricultural productivity

16

•Rural infrastructure•Land titling

•Support to SMEs•Access to finance•Business councils

•Public-private partnerships•Regional projects•Policy reforms

•Quality and access to primary health and education•Secondary and tertiary education•Vocational training with private sector participation

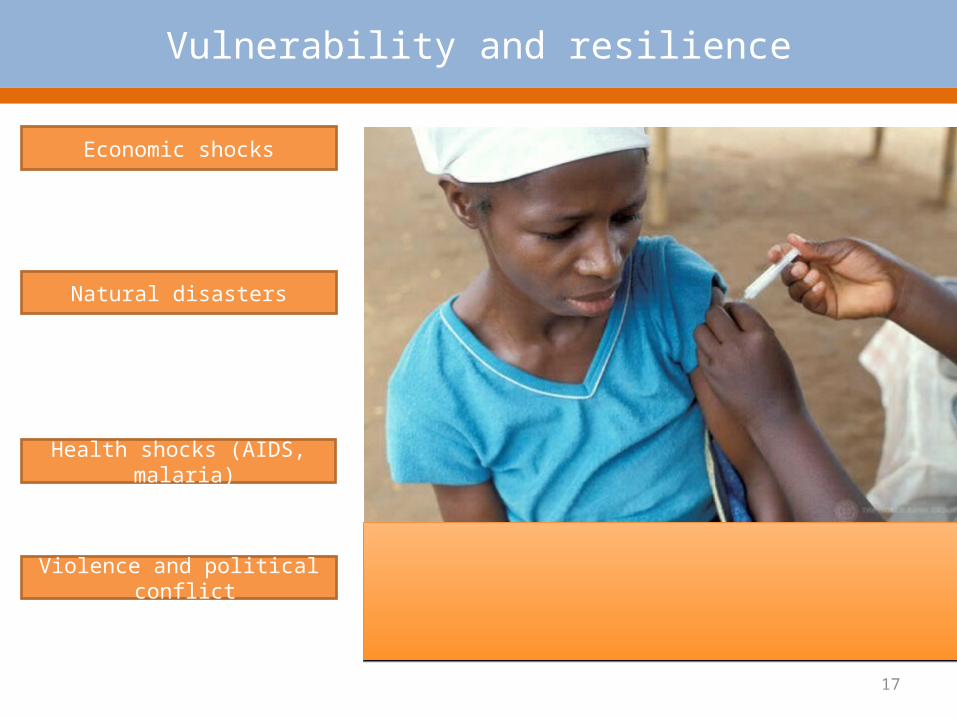

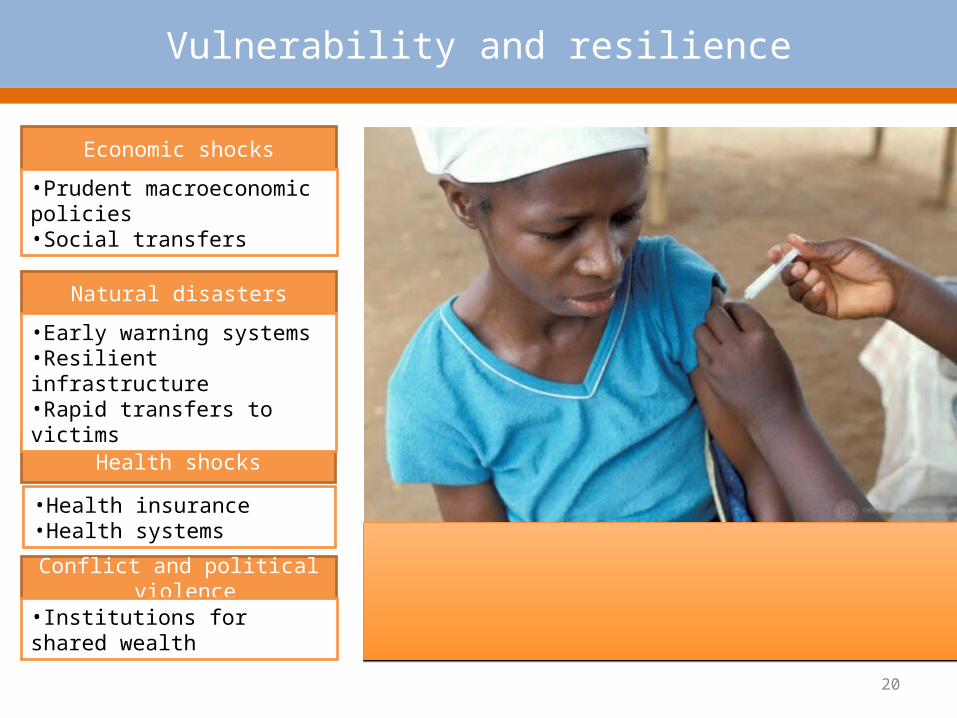

Economic shocks

Health shocks (AIDS, malaria)

Natural disasters

Violence and political conflict

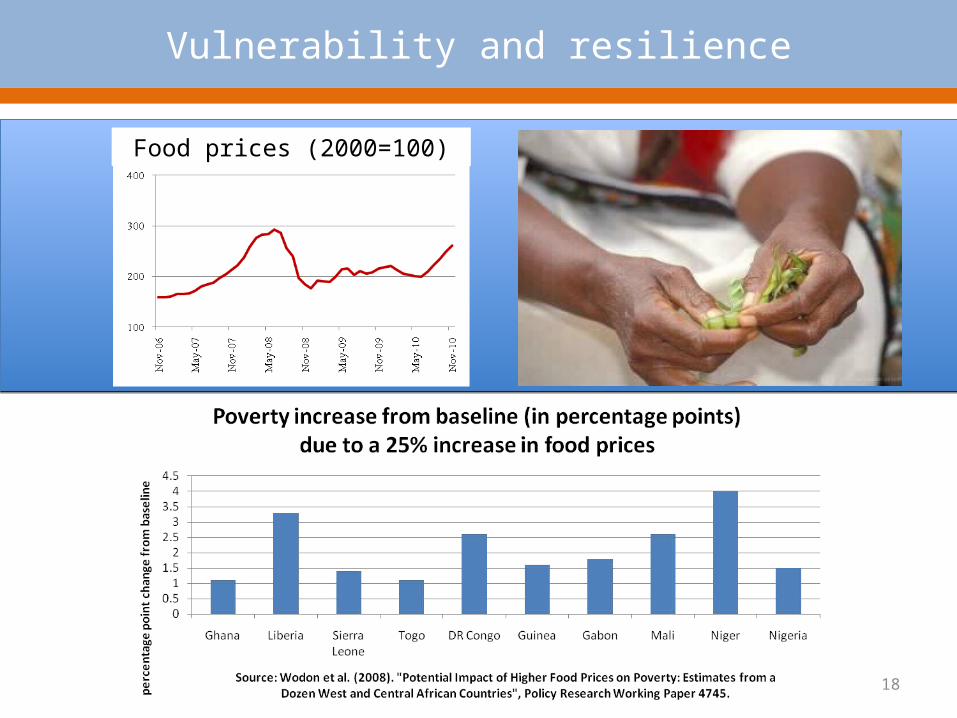

Vulnerability and resilience

17

Vulnerability and resilience

Food prices (2000=100)

18

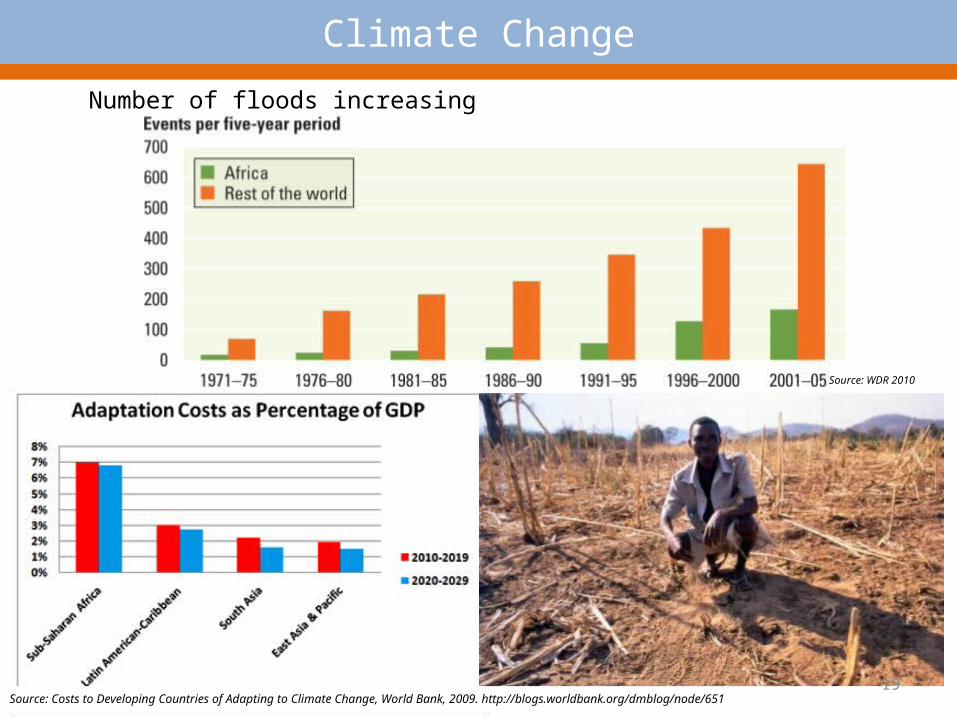

Source: Costs to Developing Countries of Adapting to Climate Change, World Bank, 2009. http://blogs.worldbank.org/dmblog/node/651

Climate Change

Number of floods increasing

Source: WDR 2010

19

Economic shocks

Health shocks

Natural disasters

Conflict and political violence

Vulnerability and resilience

•Prudent macroeconomic policies•Social transfers

•Health insurance•Health systems

•Early warning systems•Resilient infrastructure•Rapid transfers to victims

•Institutions for shared wealth

20

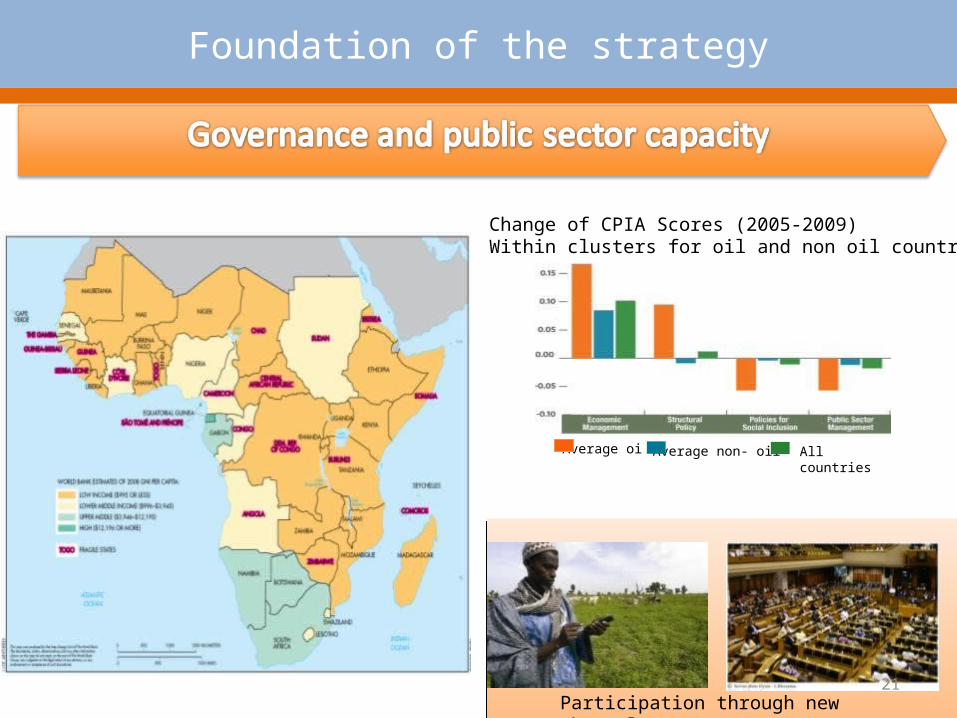

Foundation of the strategy

Change of CPIA Scores (2005-2009)Within clusters for oil and non oil countries

Average oil Average non- oil All countries

Participation through new channels21

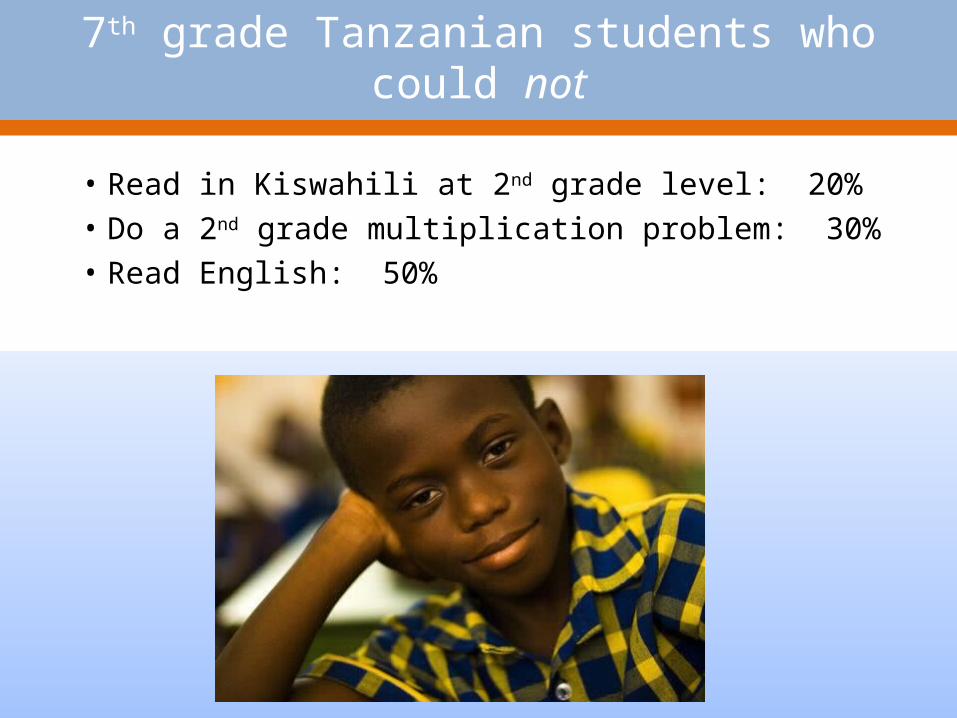

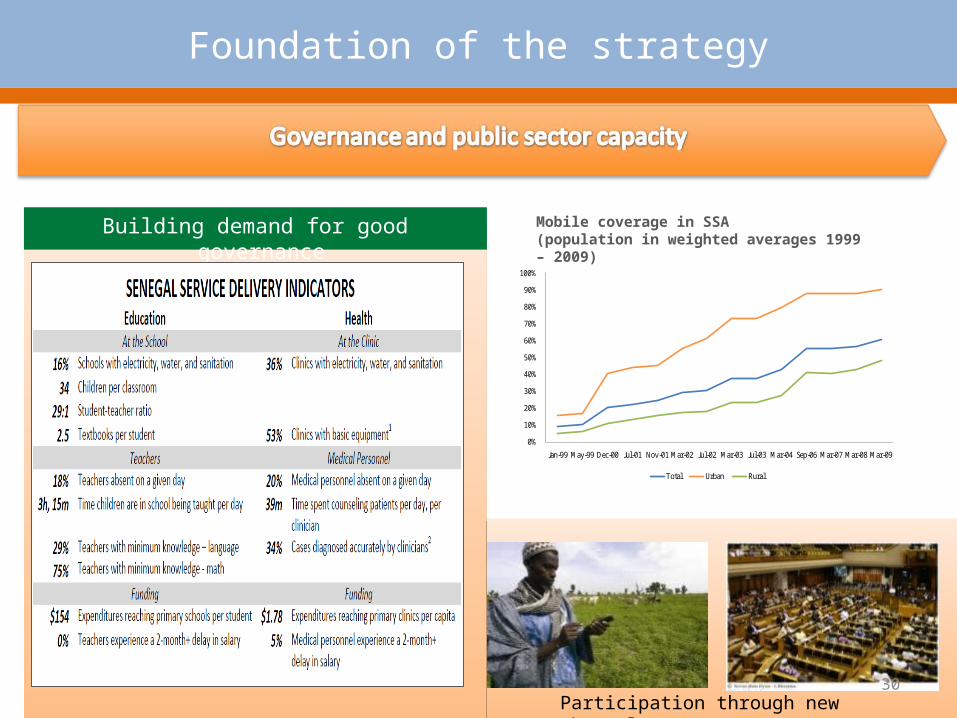

Percentage of 7th grade students in Tanzania who CANNOT

• Read in Kiswahili at 2nd grade level: 20%• Do a 2nd grade multiplication problem: 30%• Read English: 50%

7th grade Tanzanian students who could not

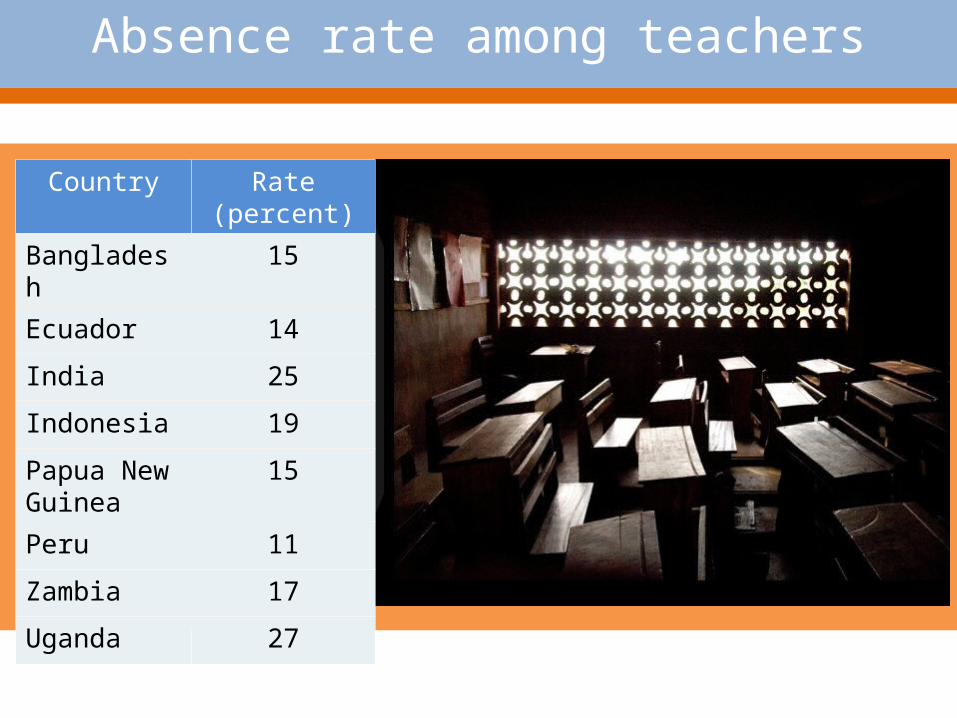

Absence rate among teachers

Country Rate (percent)

Bangladesh 15

Ecuador 14

India 25

Indonesia 19

Papua New Guinea

15

Peru 11

Zambia 17

Uganda 27

24

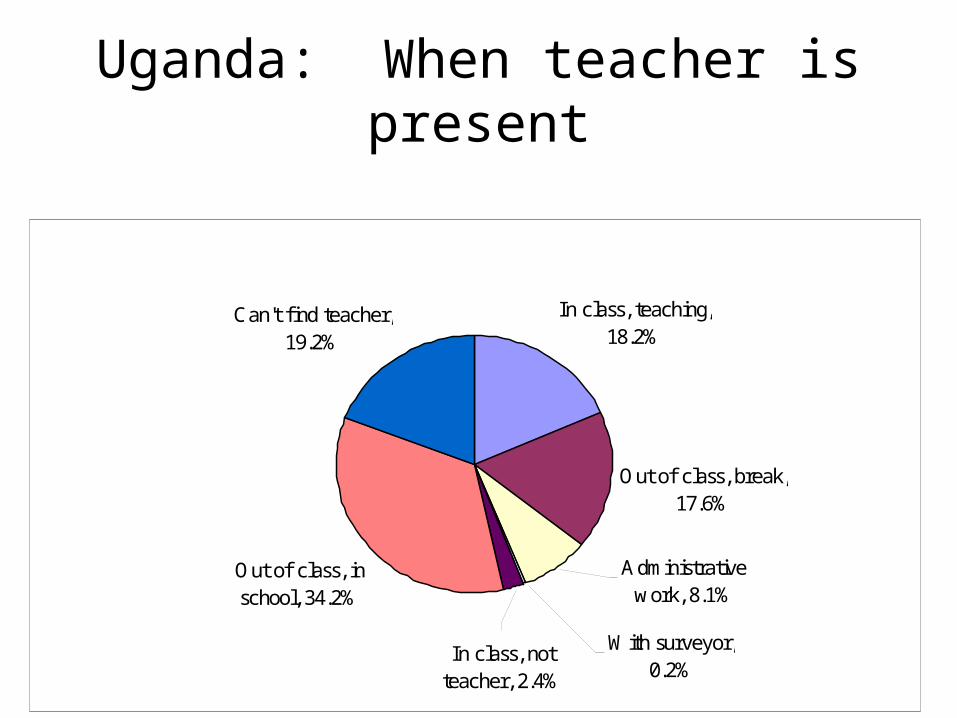

Uganda: When teacher is present

In class, teaching, 18.2%

Out of class, break, 17.6%

Out of class, in school, 34.2%

Can't find teacher, 19.2%

Administrative work, 8.1%

With surveyor, 0.2%

In class, not teacher, 2.4%

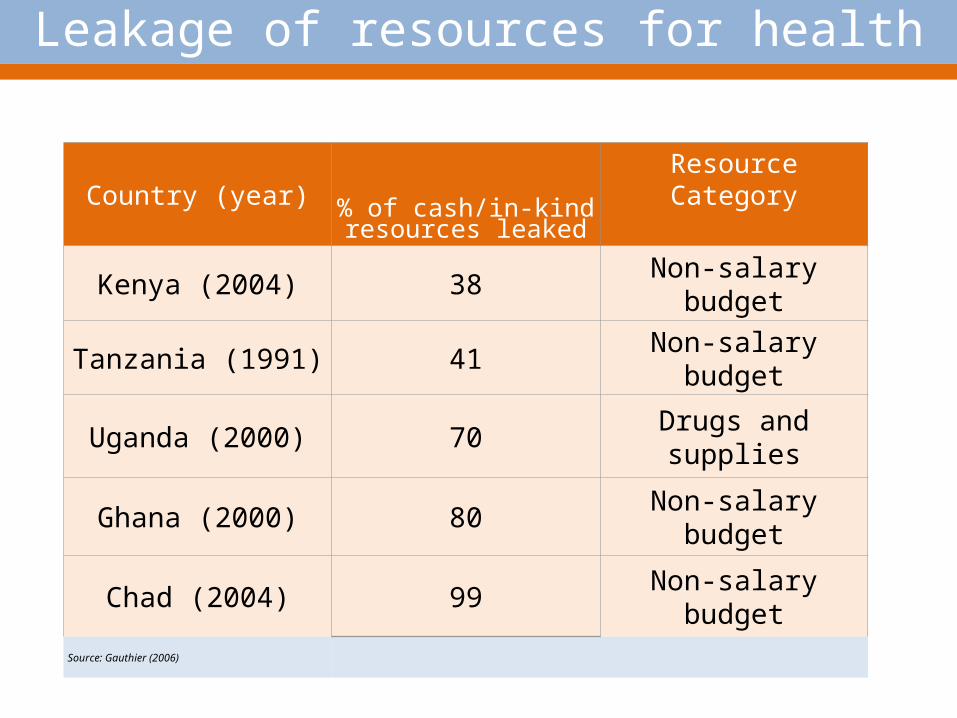

Country (year) % of cash/in-kindresources leaked

Resource Category

Kenya (2004) 38Non-salary

budget

Tanzania (1991) 41Non-salary

budget

Uganda (2000) 70Drugs and supplies

Ghana (2000) 80Non-salary

budget

Chad (2004) 99Non-salary

budgetSource: Gauthier (2006)

Leakage of resources for health

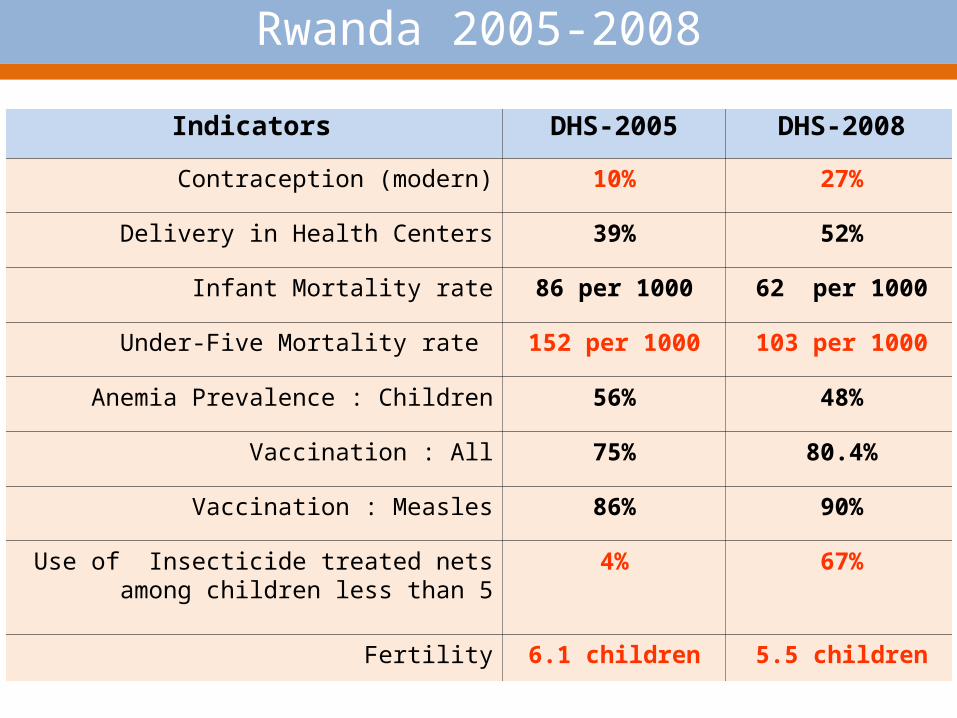

Indicators DHS-2005 DHS-2008

Contraception (modern) 10% 27%

Delivery in Health Centers 39% 52%

Infant Mortality rate 86 per 1000 62 per 1000

Under-Five Mortality rate 152 per 1000 103 per 1000

Anemia Prevalence : Children 56% 48%

Vaccination : All 75% 80.4%

Vaccination : Measles 86% 90%

Use of Insecticide treated nets among children less than 5

4% 67%

Fertility 6.1 children 5.5 children

Rwanda 2005-2008

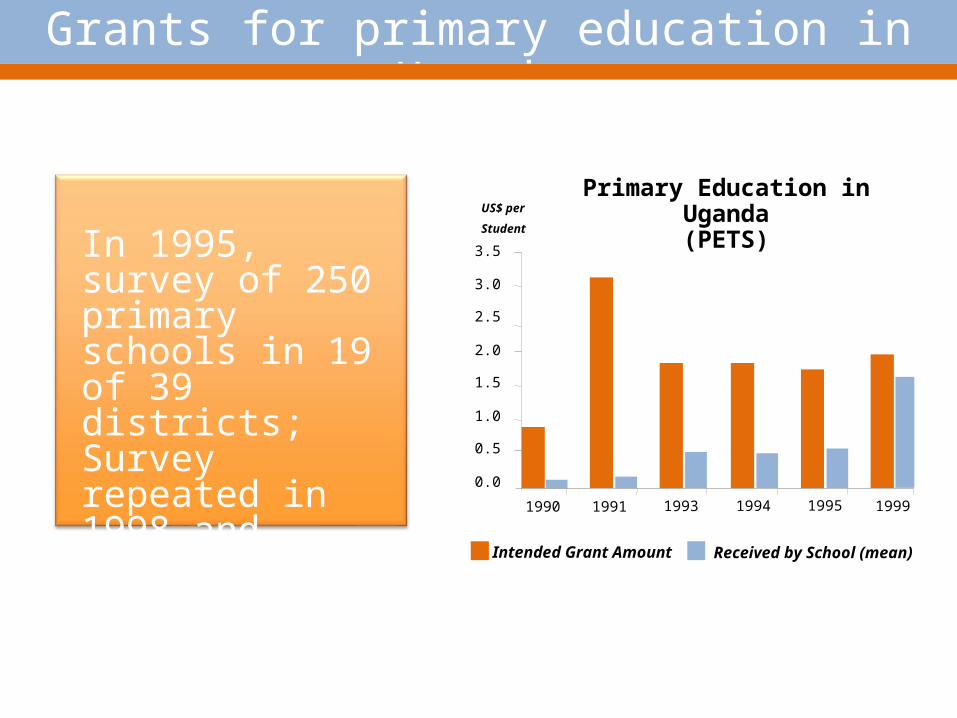

Primary Education in Uganda(PETS)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1990 1991 1993 1994 1995

US$ per

Student

Intended Grant Amount Received by School (mean)

1999

Grants for primary education in Uganda

In 1995, survey of 250 primary schools in 19 of 39 districts;Survey repeated in 1998 and 2000.

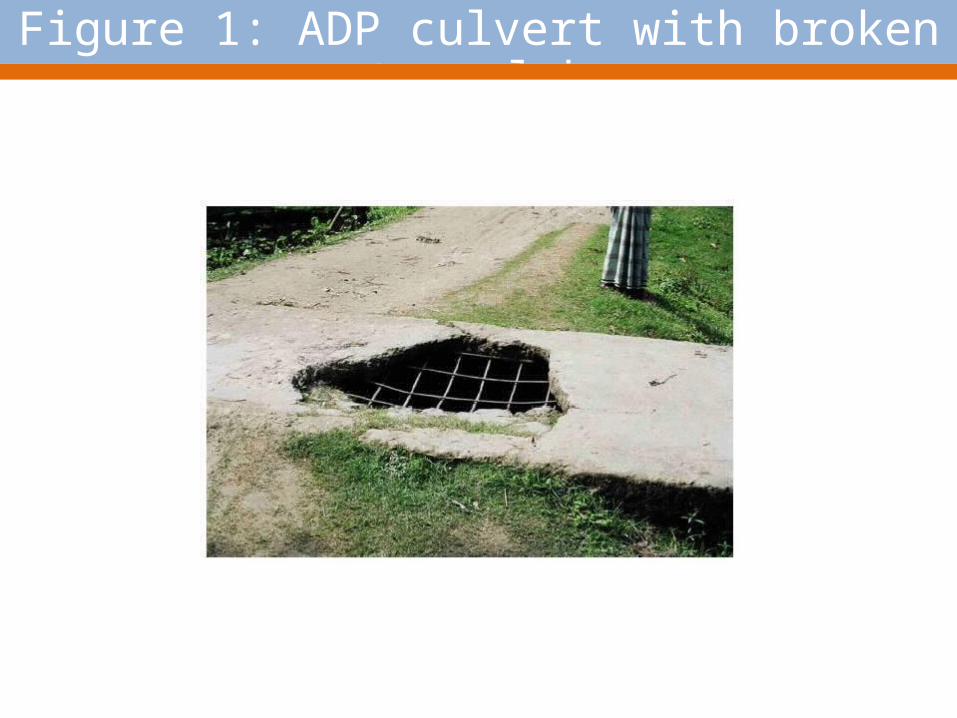

Figure 1: ADP culvert with broken top slab

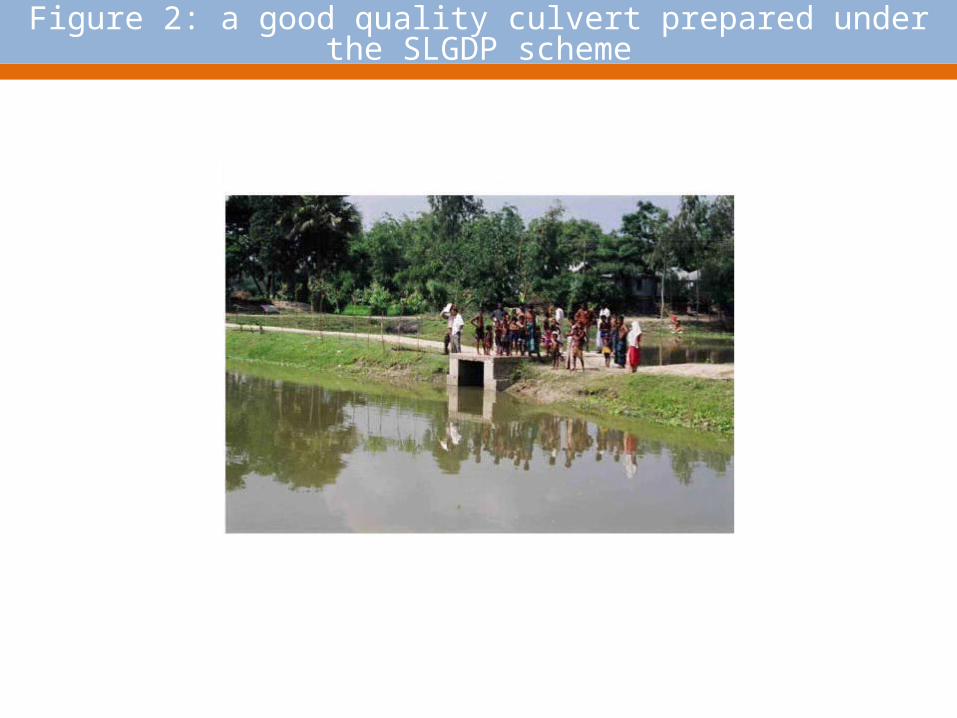

Figure 2: a good quality culvert prepared under the SLGDP scheme

Foundation of the strategy

Building demand for good governance

Participation through new channels30

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan-99 May-99 Dec-00 Jul-01 Nov-01 Mar-02 Jul-02 Mar-03 Jul-03 Mar-04 Sep-06 Mar-07 Mar-08 Mar-09

Total Urban Rural

Mobile coverage in SSA (population in weighted averages 1999 – 2009)

Knowledge

Finance

Partnerships

Implementation of the strategy

Leverage•Domestic resources•IDA, IBRD, IFC,MIGA•Private capital

•Analysis to inform policy•Evidence to nourish public debate

-Government-Civil society-Private sector-Other development actors

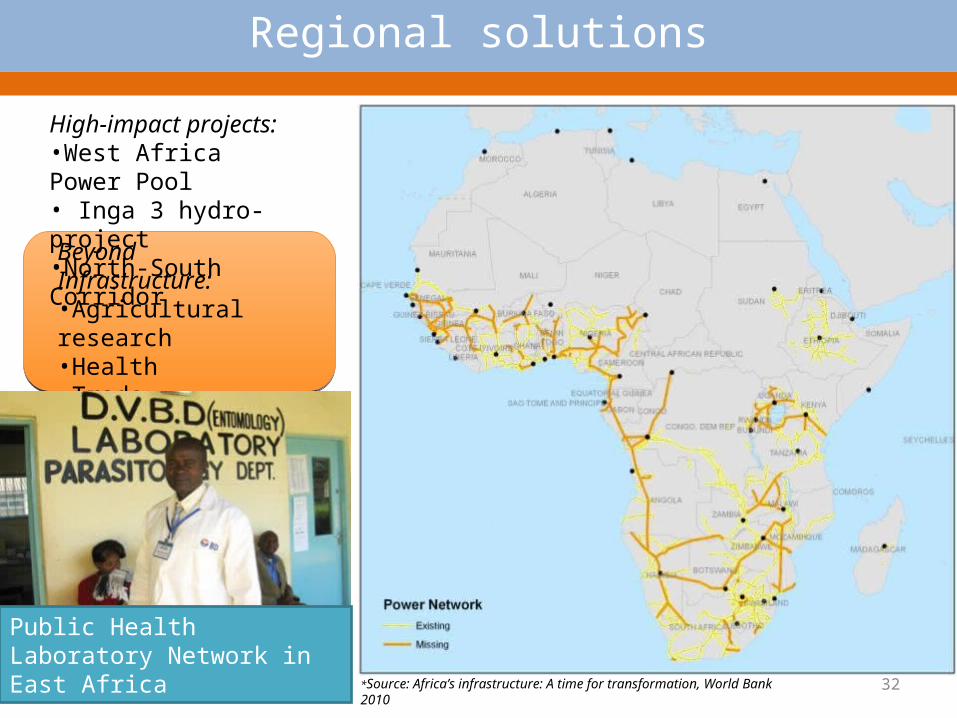

*Source: Africa’s infrastructure: A time for transformation, World Bank 2010

Regional solutions

Beyond Infrastructure:•Agricultural research•Health•Trade integration

Public Health Laboratory Network in East Africa

High-impact projects:•West Africa Power Pool• Inga 3 hydro-project •North-South Corridor

32

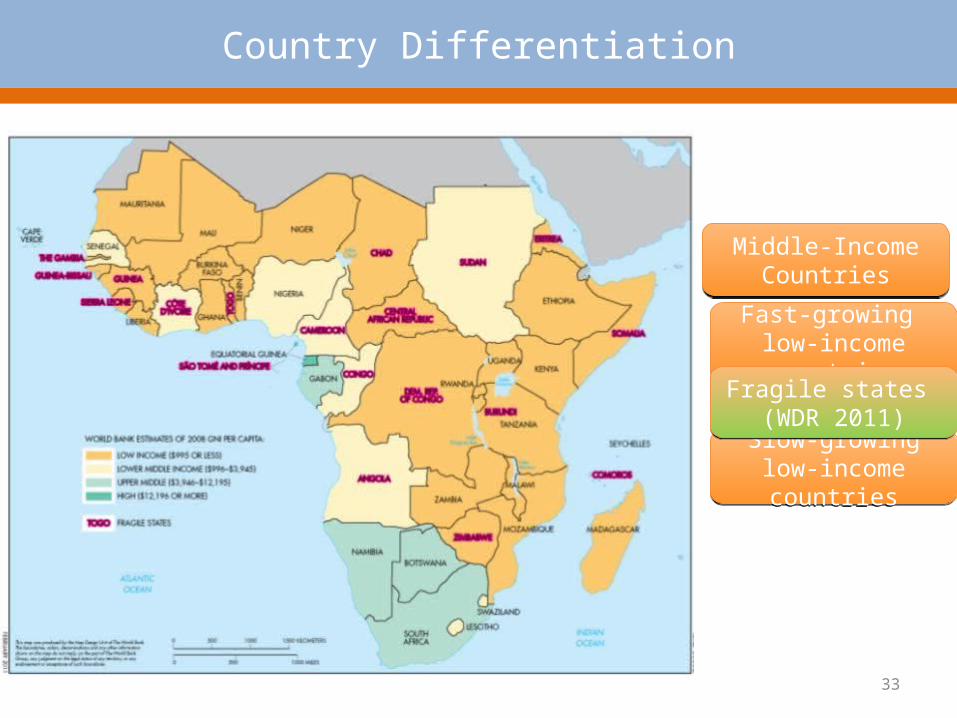

Middle-Income Countries

Middle-Income Countries

Fast-growing low-income countries

Fast-growing low-income countries

Country Differentiation

33

Slow-growing low-income countries

Slow-growing low-income countries

Fragile states (WDR 2011)

Fragile states (WDR 2011)

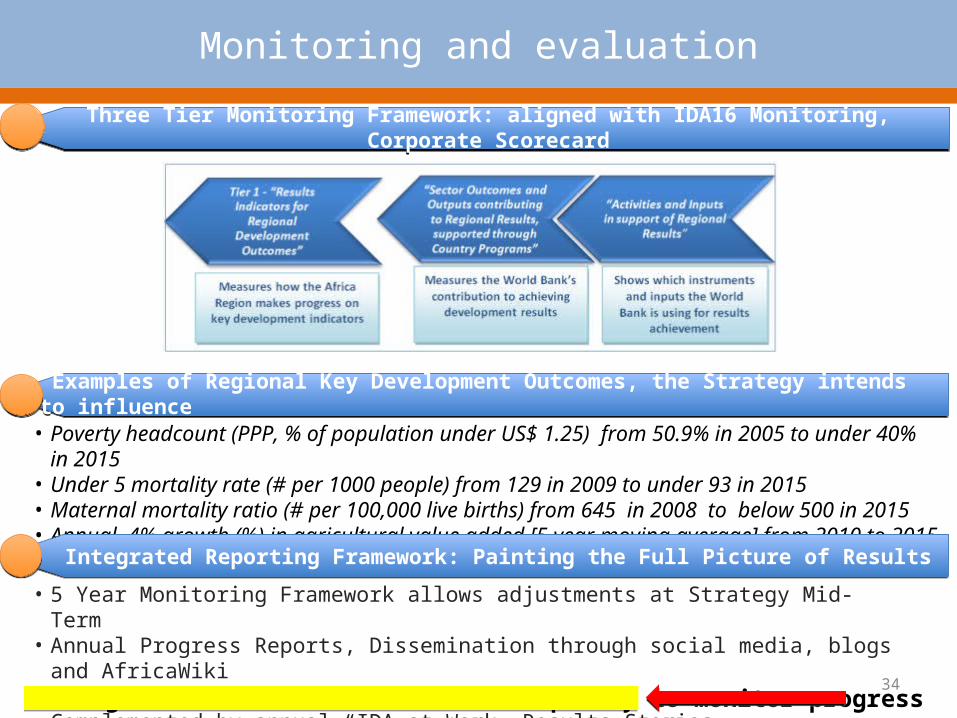

• 5 Year Monitoring Framework allows adjustments at Strategy Mid-Term• Annual Progress Reports, Dissemination through social media, blogs and AfricaWiki• Drawing from CAS results• Complemented by annual “IDA at Work” Results Stories

Monitoring and evaluation

• Poverty headcount (PPP, % of population under US$ 1.25) from 50.9% in 2005 to under 40% in 2015• Under 5 mortality rate (# per 1000 people) from 129 in 2009 to under 93 in 2015• Maternal mortality ratio (# per 100,000 live births) from 645 in 2008 to below 500 in 2015• Annual 4% growth (%) in agricultural value added [5 year moving average] from 2010 to 2015

Three Tier Monitoring Framework: aligned with IDA16 Monitoring, Corporate Scorecard

Three Tier Monitoring Framework: aligned with IDA16 Monitoring, Corporate Scorecard

Examples of Regional Key Development Outcomes, the Strategy intends to influence

Examples of Regional Key Development Outcomes, the Strategy intends to influence

Integrated Reporting Framework: Painting the Full Picture of Results Integrated Reporting Framework: Painting the Full Picture of Results

Strengthen countries’ statistical capacity to monitor progress34

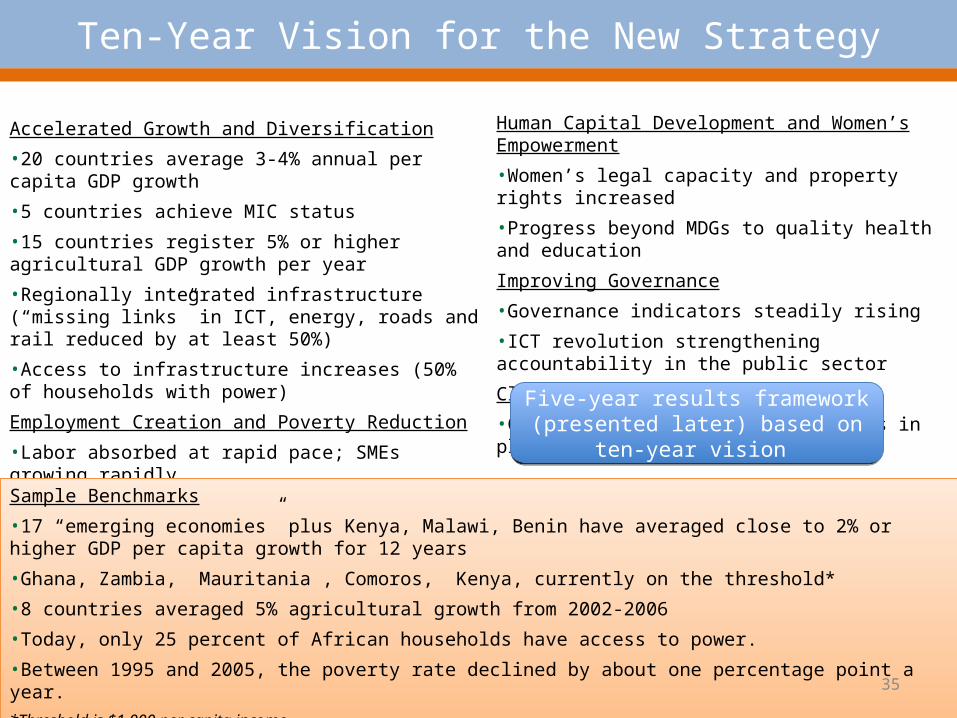

Ten-Year Vision for the New Strategy

Accelerated Growth and Diversification

•20 countries average 3-4% annual per capita GDP growth

•5 countries achieve MIC status

•15 countries register 5% or higher agricultural GDP growth per year

•Regionally integrated infrastructure (“missing links” in ICT, energy, roads and rail reduced by at least 50%)

•Access to infrastructure increases (50% of households with power)

Employment Creation and Poverty Reduction

•Labor absorbed at rapid pace; SMEs growing rapidly

•Decline in poverty rate by 12 percentage points

Sample Benchmarks

•17 “emerging economies” plus Kenya, Malawi, Benin have averaged close to 2% or higher GDP per capita growth for 12 years

•Ghana, Zambia, Mauritania , Comoros, Kenya, currently on the threshold*

•8 countries averaged 5% agricultural growth from 2002-2006

•Today, only 25 percent of African households have access to power.

•Between 1995 and 2005, the poverty rate declined by about one percentage point a year. *Threshold is $1,000 per capita income

Sample Benchmarks

•17 “emerging economies” plus Kenya, Malawi, Benin have averaged close to 2% or higher GDP per capita growth for 12 years

•Ghana, Zambia, Mauritania , Comoros, Kenya, currently on the threshold*

•8 countries averaged 5% agricultural growth from 2002-2006

•Today, only 25 percent of African households have access to power.

•Between 1995 and 2005, the poverty rate declined by about one percentage point a year. *Threshold is $1,000 per capita income

Human Capital Development and Women’s Empowerment

•Women’s legal capacity and property rights increased

•Progress beyond MDGs to quality health and education

Improving Governance

•Governance indicators steadily rising

•ICT revolution strengthening accountability in the public sector

Climate Change

•Climate change adaptation measures in place

Five-year results framework (presented later) based on ten-year vision

Five-year results framework (presented later) based on ten-year vision

35