Download - ADMS4503_Chap1

1

ADMS 4503 - Nabil Tahani 1

Introduction

Chapter 1

ADMS 4503 Derivatives

Nabil Tahani

ADMS 4503 - Nabil Tahani 2

The Nature of Derivatives

A derivative is an instrument whose value depends on the values of other more basic underlying variables such as stocks, currencies, interest rates, commodities and more recently credit, electricity, weather and insurance

2

ADMS 4503 - Nabil Tahani 3

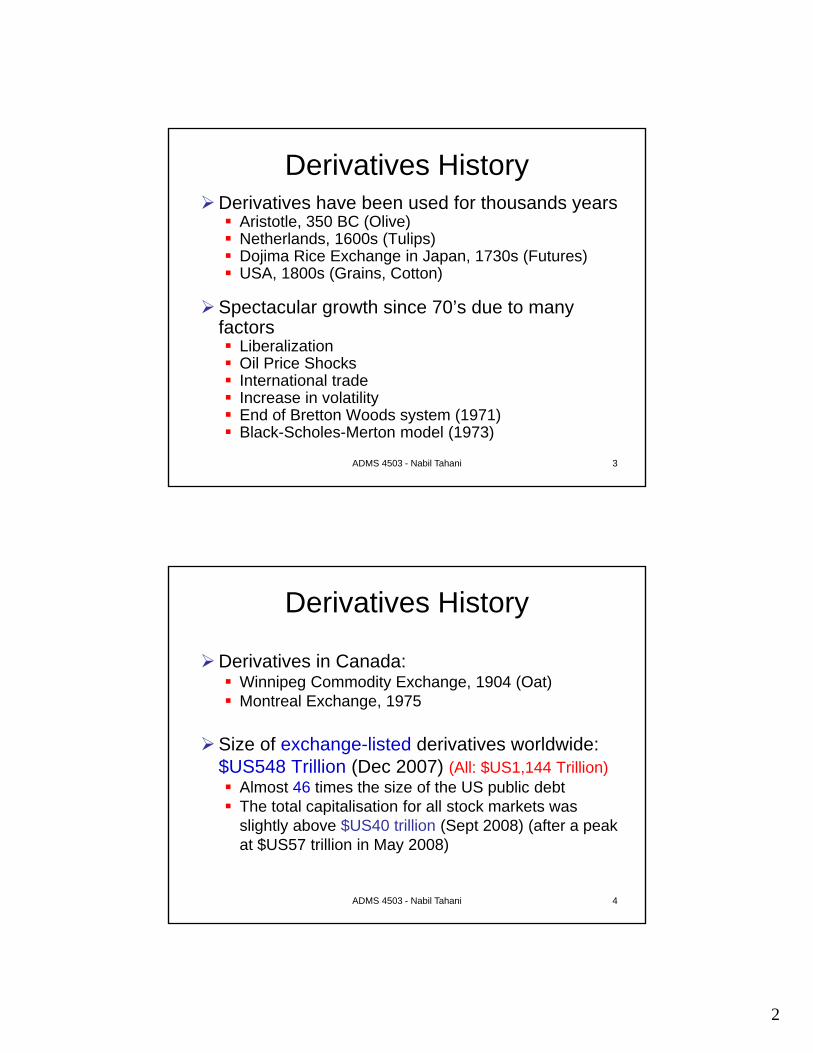

Derivatives HistoryDerivatives have been used for thousands years Aristotle, 350 BC (Olive) Netherlands, 1600s (Tulips) Dojima Rice Exchange in Japan, 1730s (Futures) USA, 1800s (Grains, Cotton)

Spectacular growth since 70’s due to many factors Liberalization Oil Price Shocks International trade Increase in volatility End of Bretton Woods system (1971) Black-Scholes-Merton model (1973)

ADMS 4503 - Nabil Tahani 4

Derivatives History

Derivatives in Canada: Winnipeg Commodity Exchange, 1904 (Oat) Montreal Exchange, 1975

Size of exchange-listed derivatives worldwide: $US548 Trillion (Dec 2007) (All: $US1,144 Trillion) Almost 46 times the size of the US public debt The total capitalisation for all stock markets was

slightly above $US40 trillion (Sept 2008) (after a peak at $US57 trillion in May 2008)

3

ADMS 4503 - Nabil Tahani 5

Examples of Derivatives

• Forward Contracts

• Futures Contracts

• Swaps

• Options

• …

ADMS 4503 - Nabil Tahani 6

Examples of Underlying Assets

• Stocks

• Bonds

• Exchange rates

• Interest rates

• Commodities

• Energy

• Number of bankruptcies among a pool of companies

• Temperature, quantity of rain/snow

• Real-estate price index

• Loss caused by an earthquake/hurricane

• Volatility

• Other Derivatives

• …

4

ADMS 4503 - Nabil Tahani 7

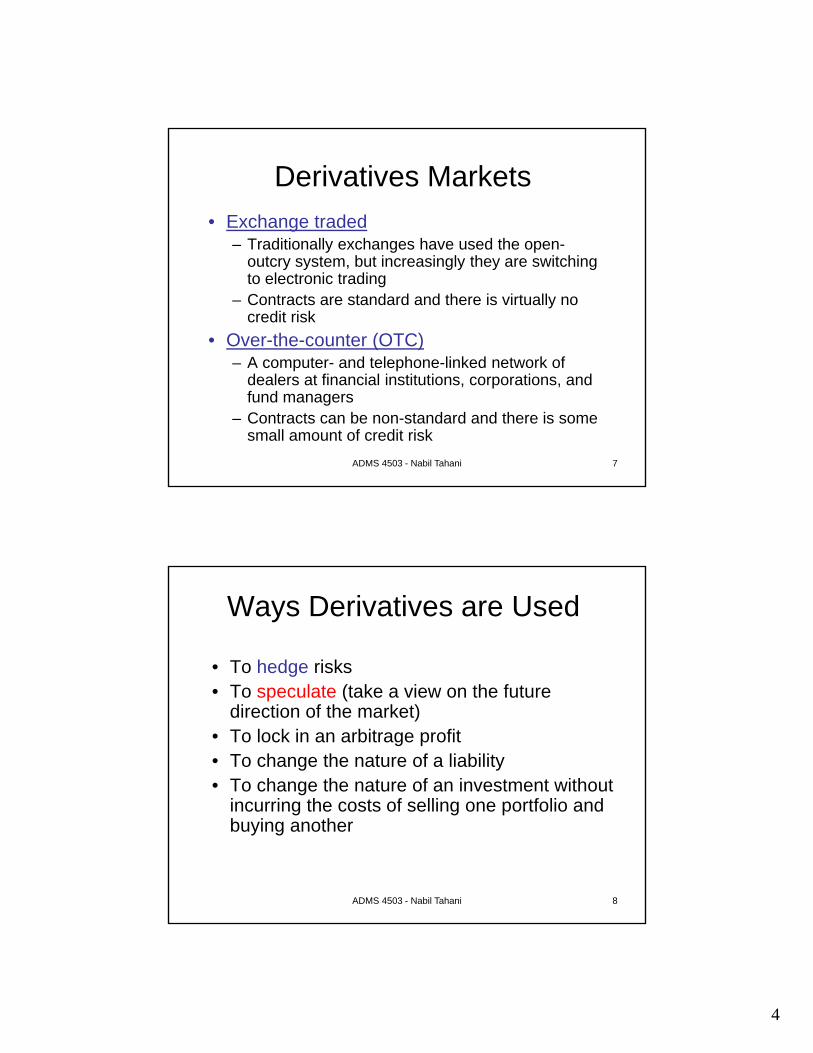

Derivatives Markets

• Exchange traded– Traditionally exchanges have used the open-

outcry system, but increasingly they are switching to electronic trading

– Contracts are standard and there is virtually no credit risk

• Over-the-counter (OTC)– A computer- and telephone-linked network of

dealers at financial institutions, corporations, and fund managers

– Contracts can be non-standard and there is some small amount of credit risk

ADMS 4503 - Nabil Tahani 8

Ways Derivatives are Used

• To hedge risks• To speculate (take a view on the future

direction of the market)• To lock in an arbitrage profit• To change the nature of a liability• To change the nature of an investment without

incurring the costs of selling one portfolio and buying another

5

ADMS 4503 - Nabil Tahani 9

Forward Contracts

• A forward contract is an agreement to buy or sell an asset at a certain time in the future for a certain price (the delivery price)

• It can be contrasted with a spot contract which is an agreement to buy or sell immediately

• It is traded in the OTC market

ADMS 4503 - Nabil Tahani 10

Foreign Exchange Quotes for GBP on Aug 16, 2001

Bid Offer

Spot 1.4452 1.4456

1-month forward 1.4435 1.4440

3-month forward 1.4402 1.4407

6-month forward 1.4353 1.4359

12-month forward 1.4262 1.4268

6

ADMS 4503 - Nabil Tahani 11

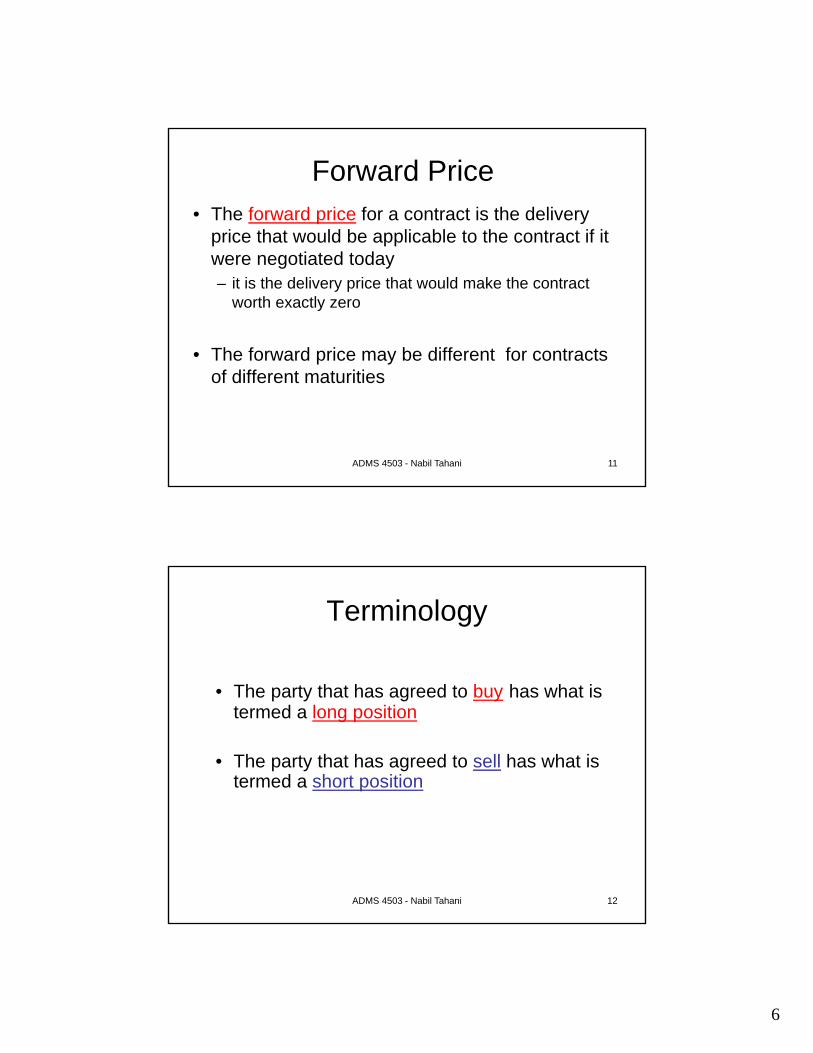

Forward Price• The forward price for a contract is the delivery

price that would be applicable to the contract if it were negotiated today – it is the delivery price that would make the contract

worth exactly zero

• The forward price may be different for contracts of different maturities

ADMS 4503 - Nabil Tahani 12

Terminology

• The party that has agreed to buy has what is termed a long position

• The party that has agreed to sell has what is termed a short position

7

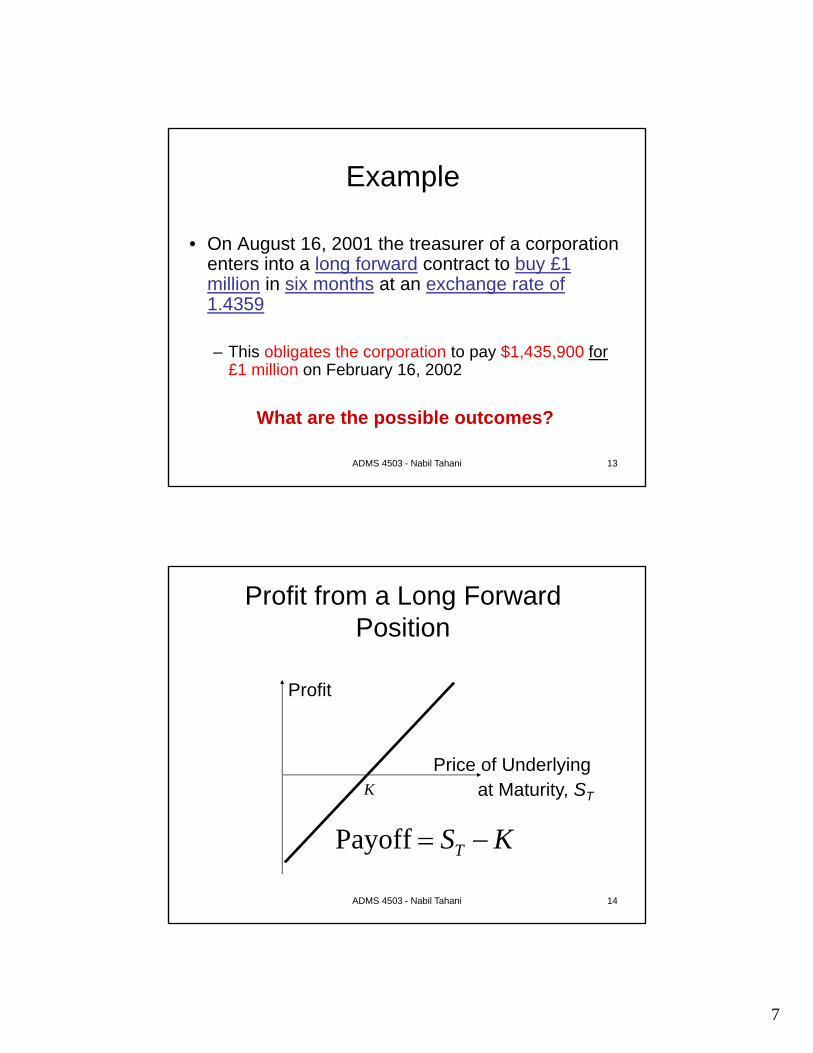

ADMS 4503 - Nabil Tahani 13

Example

• On August 16, 2001 the treasurer of a corporation enters into a long forward contract to buy £1 million in six months at an exchange rate of 1.4359

– This obligates the corporation to pay $1,435,900 for£1 million on February 16, 2002

What are the possible outcomes?

ADMS 4503 - Nabil Tahani 14

Profit from a Long Forward Position

Profit

Price of Underlyingat Maturity, STK

KST Payoff

8

ADMS 4503 - Nabil Tahani 15

Profit from a Short Forward Position

Profit

Price of Underlyingat Maturity, STK

TSK Payoff

ADMS 4503 - Nabil Tahani 16

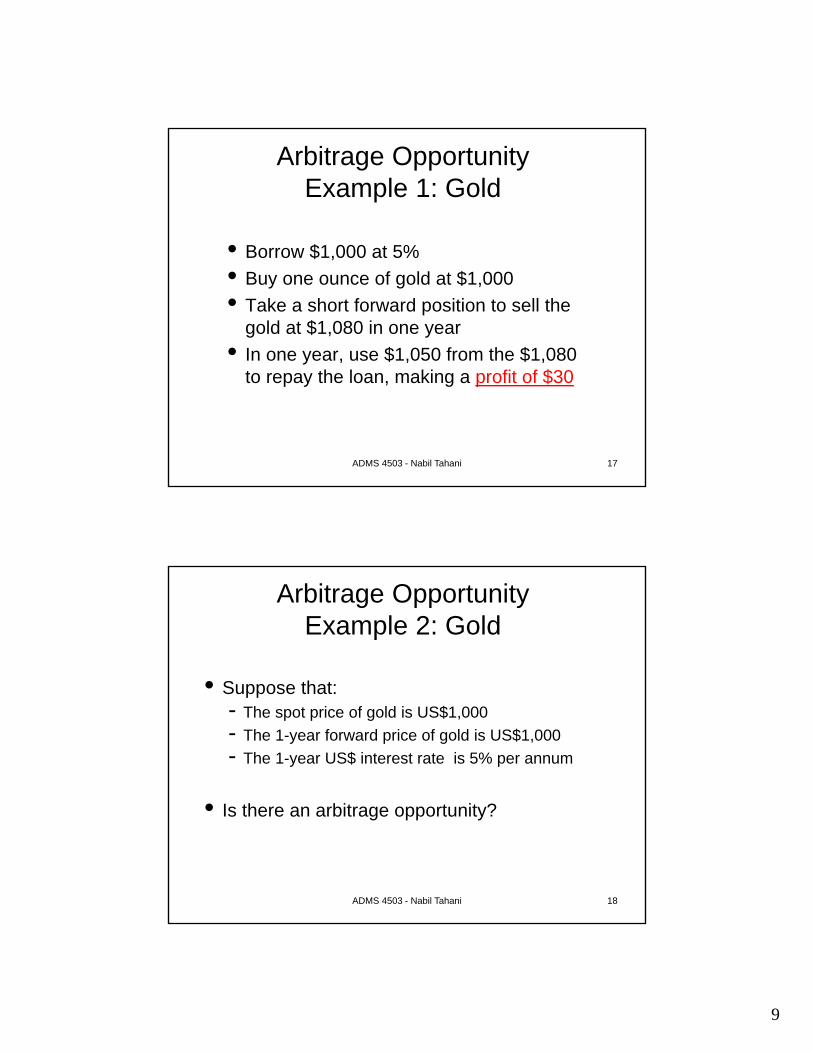

Arbitrage OpportunityExample 1: Gold

• Suppose that:- The spot price of gold is US$1,000

- The 1-year forward price of gold is US$1,080

- The 1-year US$ interest rate is 5% per annum

• Is there an arbitrage opportunity?

(We ignore storage costs and gold lease rate)

9

ADMS 4503 - Nabil Tahani 17

• Borrow $1,000 at 5%

• Buy one ounce of gold at $1,000

• Take a short forward position to sell the gold at $1,080 in one year

• In one year, use $1,050 from the $1,080 to repay the loan, making a profit of $30

Arbitrage OpportunityExample 1: Gold

ADMS 4503 - Nabil Tahani 18

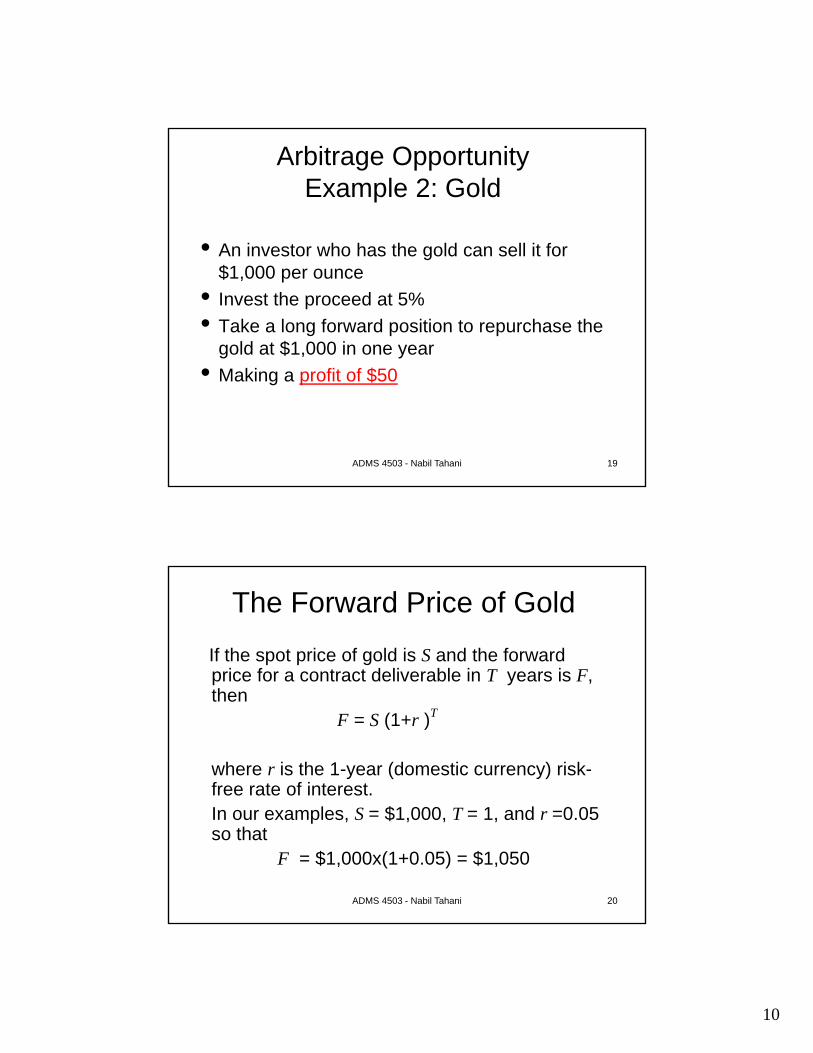

• Suppose that:- The spot price of gold is US$1,000

- The 1-year forward price of gold is US$1,000

- The 1-year US$ interest rate is 5% per annum

• Is there an arbitrage opportunity?

Arbitrage OpportunityExample 2: Gold

10

ADMS 4503 - Nabil Tahani 19

• An investor who has the gold can sell it for $1,000 per ounce

• Invest the proceed at 5%

• Take a long forward position to repurchase the gold at $1,000 in one year

• Making a profit of $50

Arbitrage OpportunityExample 2: Gold

ADMS 4503 - Nabil Tahani 20

The Forward Price of Gold

If the spot price of gold is S and the forward price for a contract deliverable in T years is F, then

F = S (1+r )T

where r is the 1-year (domestic currency) risk-free rate of interest.In our examples, S = $1,000, T = 1, and r =0.05 so that

F = $1,000x(1+0.05) = $1,050

11

ADMS 4503 - Nabil Tahani 21

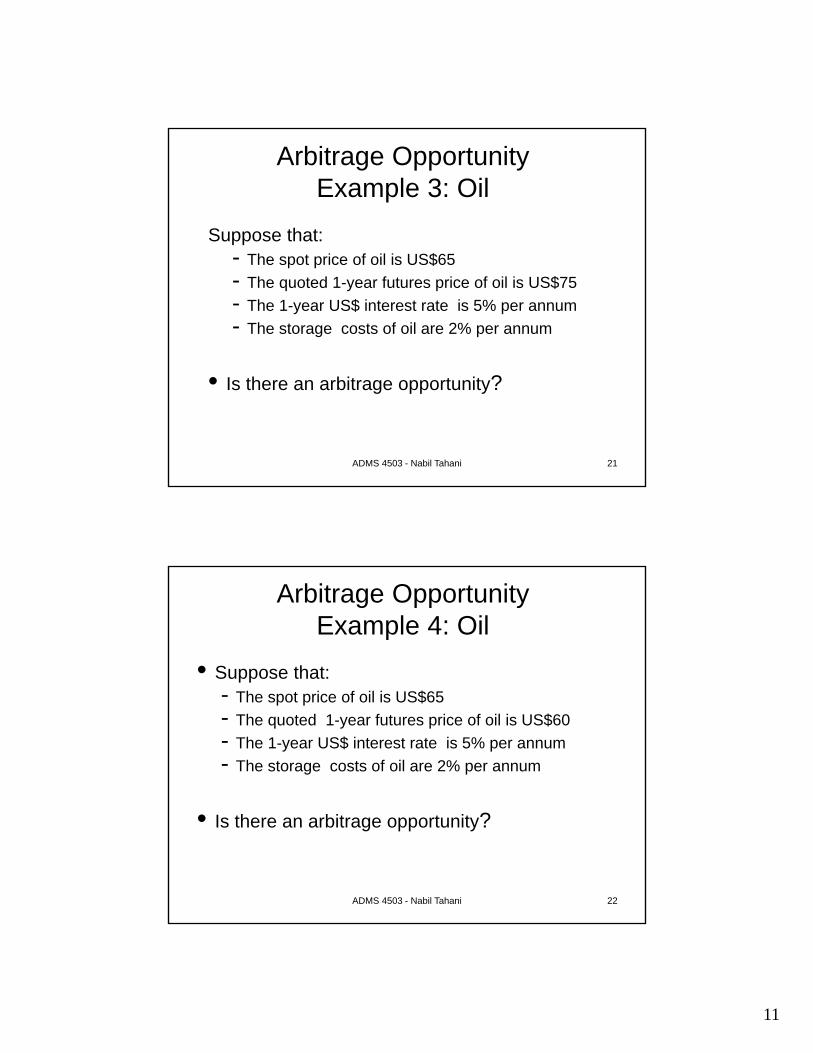

Suppose that:- The spot price of oil is US$65

- The quoted 1-year futures price of oil is US$75

- The 1-year US$ interest rate is 5% per annum

- The storage costs of oil are 2% per annum

• Is there an arbitrage opportunity?

Arbitrage OpportunityExample 3: Oil

ADMS 4503 - Nabil Tahani 22

• Suppose that:- The spot price of oil is US$65

- The quoted 1-year futures price of oil is US$60

- The 1-year US$ interest rate is 5% per annum

- The storage costs of oil are 2% per annum

• Is there an arbitrage opportunity?

Arbitrage OpportunityExample 4: Oil

12

ADMS 4503 - Nabil Tahani 23

Futures Contracts

• Agreement to buy or sell an asset for a certain price at a certain time

• Similar to forward contract

• Whereas a forward contract is traded OTC, a futures contract is traded on an exchange

ADMS 4503 - Nabil Tahani 24

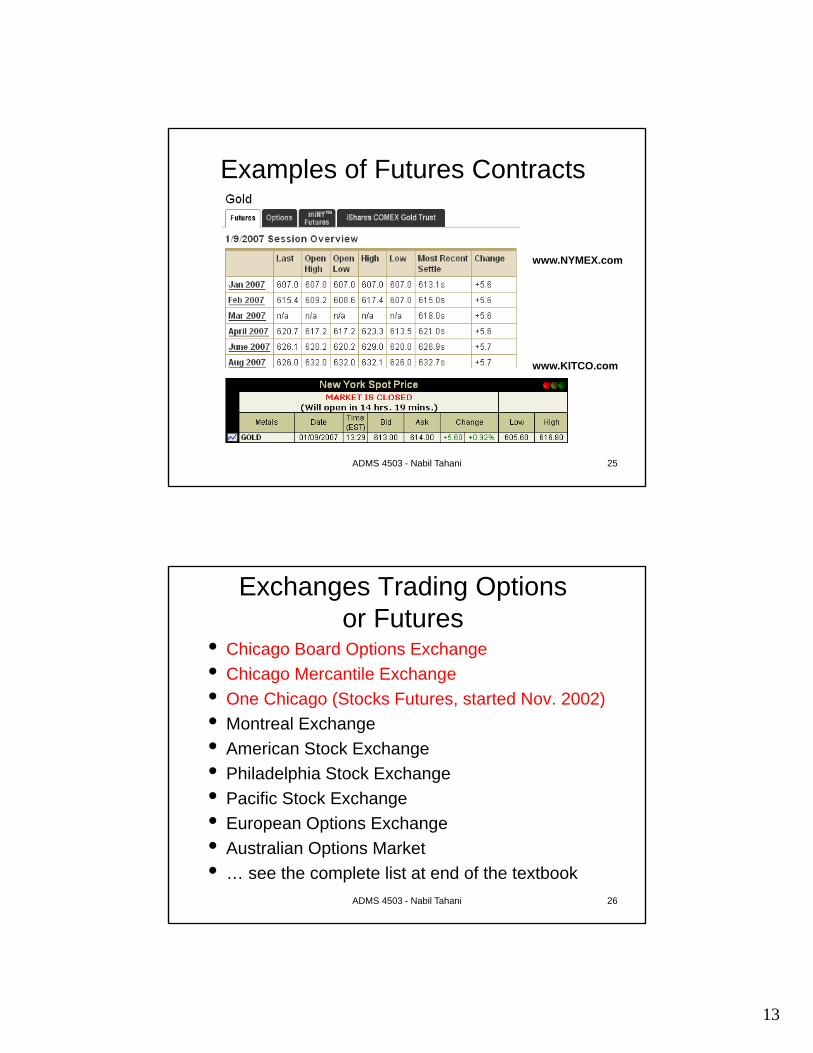

Examples of Futures Contracts

• There are futures contracts on almost everything!

– buy 100 oz. of gold @ US$1,000/oz. in December (COMEX)

– sell £62,500 @ 1.5000 US$/£ in March (CME)

– sell 1,000 bbl. of oil @ US$70/bbl. in April (NYMEX)

• Stock indices, Stocks, Interest rates, Live Cattle, Coffee,… and even Weather

13

ADMS 4503 - Nabil Tahani 25

Examples of Futures Contracts

www.NYMEX.com

www.KITCO.com

ADMS 4503 - Nabil Tahani 26

Exchanges Trading Options or Futures

• Chicago Board Options Exchange

• Chicago Mercantile Exchange

• One Chicago (Stocks Futures, started Nov. 2002)

• Montreal Exchange

• American Stock Exchange

• Philadelphia Stock Exchange

• Pacific Stock Exchange

• European Options Exchange

• Australian Options Market

• … see the complete list at end of the textbook

14

ADMS 4503 - Nabil Tahani 27

Options

• A call option is an option to buy a certain asset by a certain date for a certain price (the strike price)

• A put option is an option to sell a certain asset by a certain date for a certain price (the strike price)

)0,max(Payoff KST

)0,max(Payoff TSK

ADMS 4503 - Nabil Tahani 28

Long Call on Microsoft

Profit/Loss from buying a European call option on Microsoft: option price = $5, strike price = $60

30

20

10

0-5

30 40 50 60

70 80 90

Profit ($)

Terminalstock price ($)

15

ADMS 4503 - Nabil Tahani 29

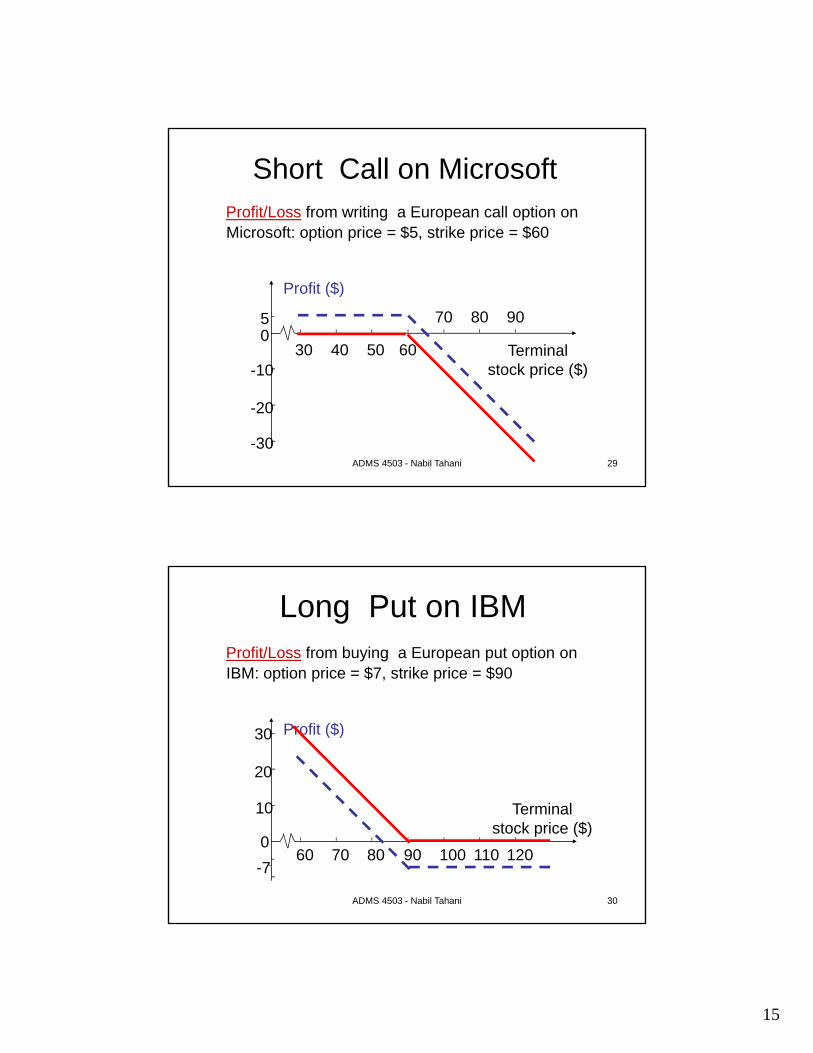

Short Call on MicrosoftProfit/Loss from writing a European call option on Microsoft: option price = $5, strike price = $60

-30

-20

-10

05

30 40 50 60

70 80 90

Profit ($)

Terminalstock price ($)

ADMS 4503 - Nabil Tahani 30

Long Put on IBMProfit/Loss from buying a European put option on IBM: option price = $7, strike price = $90

30

20

10

0

-790807060 100 110 120

Profit ($)

Terminalstock price ($)

16

ADMS 4503 - Nabil Tahani 31

Short Put on IBMProfit/Loss from writing a European put option on IBM: option price = $7, strike price = $90

-30

-20

-10

7

090

807060

100 110 120

Profit ($)Terminal

stock price ($)

ADMS 4503 - Nabil Tahani 32

Payoffs from OptionsWhat is the Option Position in Each Case?

K = Strike price, ST = Price of asset at maturity

Payoff Payoff

ST STK

K

Payoff Payoff

ST STK

K

Long call

Short call

Long put

Short put

17

ADMS 4503 - Nabil Tahani 33

Example: Google Options(Jan 9, 2007, Stock Price = 485.50)

Strike Price

Jan.

Call

Feb.

Call

Jan.

Put

Feb.

Put

480 11.42 26.60 5.20 18.50

490 6.10 22.70 9.90 23.00

500 2.80 17.30 16.50 28.00

ADMS 4503 - Nabil Tahani 34

Types of Traders• In the markets, we may find traders that are:

• Hedgers

• Speculators

• Arbitrageurs

• Some of the large trading losses in derivatives occurred because individuals who had a mandate to hedge risks switched to being speculators

18

ADMS 4503 - Nabil Tahani 35

Hedging Examples

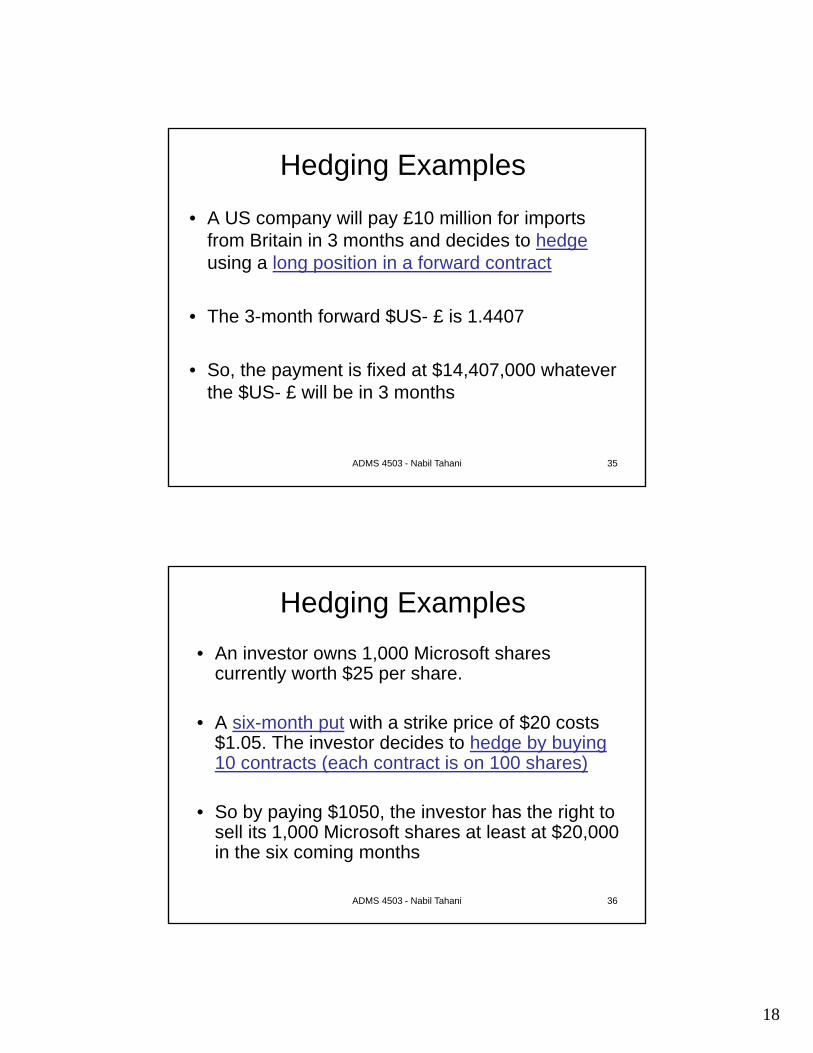

• A US company will pay £10 million for imports from Britain in 3 months and decides to hedgeusing a long position in a forward contract

• The 3-month forward $US- £ is 1.4407

• So, the payment is fixed at $14,407,000 whatever the $US- £ will be in 3 months

ADMS 4503 - Nabil Tahani 36

Hedging Examples

• An investor owns 1,000 Microsoft shares currently worth $25 per share.

• A six-month put with a strike price of $20 costs $1.05. The investor decides to hedge by buying 10 contracts (each contract is on 100 shares)

• So by paying $1050, the investor has the right to sell its 1,000 Microsoft shares at least at $20,000 in the six coming months

19

ADMS 4503 - Nabil Tahani 37

Speculation Example

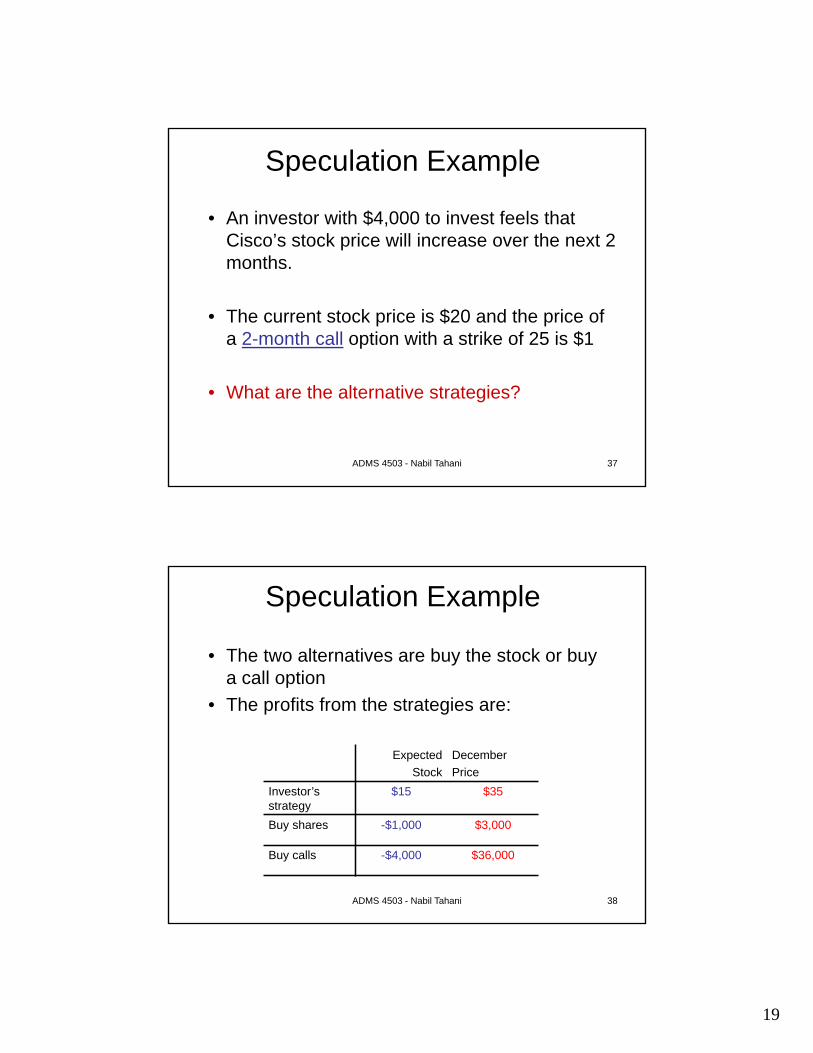

• An investor with $4,000 to invest feels that Cisco’s stock price will increase over the next 2 months.

• The current stock price is $20 and the price of a 2-month call option with a strike of 25 is $1

• What are the alternative strategies?

ADMS 4503 - Nabil Tahani 38

Speculation Example

• The two alternatives are buy the stock or buy a call option

• The profits from the strategies are:

Expected

Stock

December

Price

Investor’s strategy

$15 $35

Buy shares -$1,000 $3,000

Buy calls -$4,000 $36,000

20

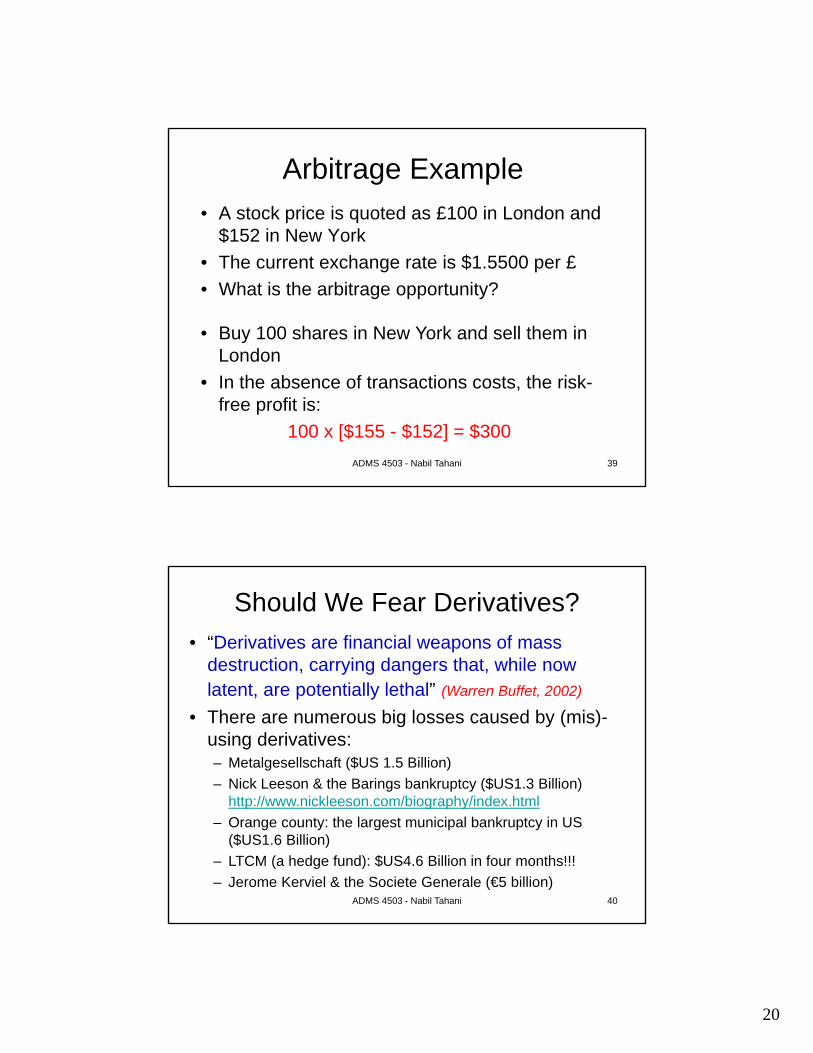

ADMS 4503 - Nabil Tahani 39

Arbitrage Example• A stock price is quoted as £100 in London and

$152 in New York

• The current exchange rate is $1.5500 per £

• What is the arbitrage opportunity?

• Buy 100 shares in New York and sell them in London

• In the absence of transactions costs, the risk-free profit is:

100 x [$155 - $152] = $300

ADMS 4503 - Nabil Tahani 40

Should We Fear Derivatives?

• “Derivatives are financial weapons of mass destruction, carrying dangers that, while now latent, are potentially lethal” (Warren Buffet, 2002)

• There are numerous big losses caused by (mis)-using derivatives:– Metalgesellschaft ($US 1.5 Billion)

– Nick Leeson & the Barings bankruptcy ($US1.3 Billion) http://www.nickleeson.com/biography/index.html

– Orange county: the largest municipal bankruptcy in US ($US1.6 Billion)

– LTCM (a hedge fund): $US4.6 Billion in four months!!!

– Jerome Kerviel & the Societe Generale (€5 billion)

21

ADMS 4503 - Nabil Tahani 41

Should We Fear Derivatives?

• “The answer is no. We should have a healthy respect for them. We do not fear planes because they may crash and do not refuse to board them because of that risk. Instead, we make sure that planes are as safe as it makes economic sense for them to be. The same applies to derivatives. Typically, the losses from derivatives are localized, but the whole economy gains from the existence of derivatives markets” Rene Stulz (Ohio State University)

ADMS 4503 - Nabil Tahani 42

Warren Buffet – GS deal

22

ADMS 4503 - Nabil Tahani 43

Some interesting books-Flash Boys, by Michael Lewis (on HF trading)-The big Short, by Michael Lewis (on the subripme crisis)-Liar’s Poker, by Michael Lewis (on 80s and 90s Wall Street)-FIASCO, by Frank Partnoy (same here)-When Genius Failed: The Rise and Fall of LTCM, by Roger Lowenstein (on the first big bailout after a hedge fund collapse)-The Quants, by Scott Patterson (how a new breed of math whizzes conquered Wall Street and nearly destroyed it)-Fooled by Randomness, by Nassim Nicholas Taleb (the hidden role of chance in life and in the markets)-The Black Swan, by Nassim Nicholas Taleb (the impact of the highly improbable) -Inside the house of Money: Top Hedge Fund Traders Profiting in the Global Markets, by Steven Drobny (the opaque world of hedge funds)

ADMS 4503 - Nabil Tahani 44

Basic Finance Concepts

A review

23

ADMS 4503 - Nabil Tahani 45

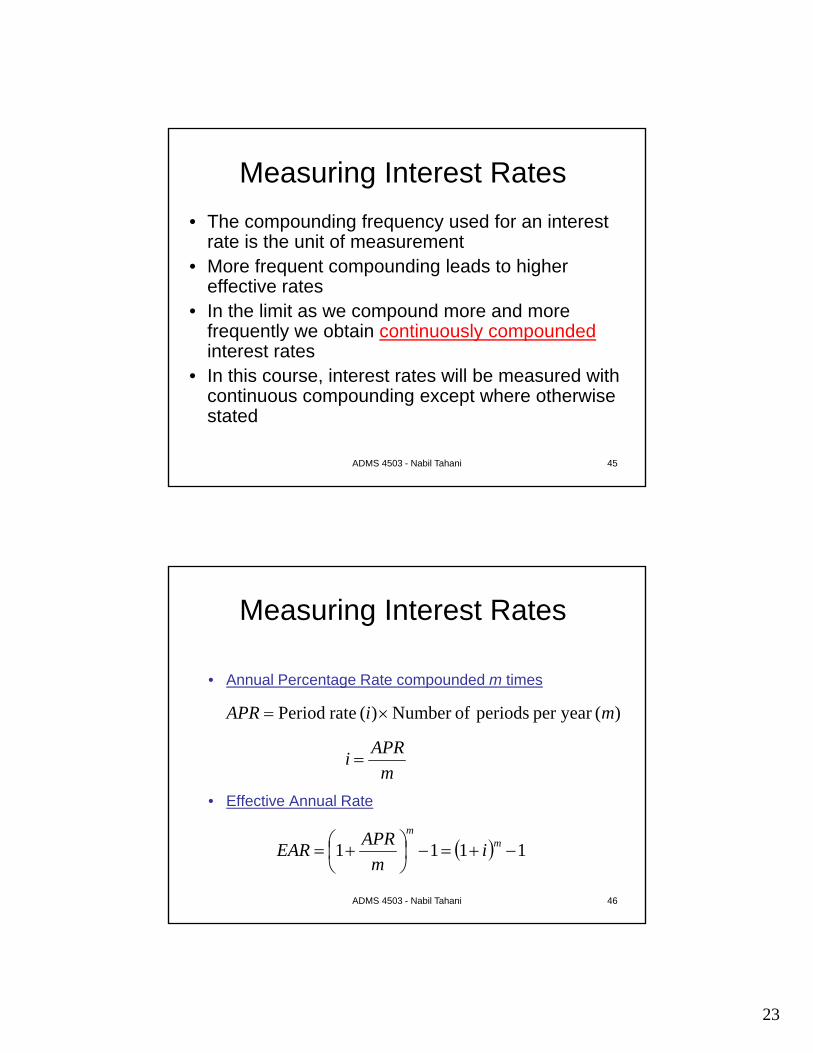

Measuring Interest Rates

• The compounding frequency used for an interest rate is the unit of measurement

• More frequent compounding leads to higher effective rates

• In the limit as we compound more and more frequently we obtain continuously compoundedinterest rates

• In this course, interest rates will be measured with continuous compounding except where otherwise stated

ADMS 4503 - Nabil Tahani 46

• Annual Percentage Rate compounded m times

• Effective Annual Rate

miAPR )(year per periods ofNumber )( rate Period

1111

m

m

im

APREAR

m

APRi

Measuring Interest Rates

24

ADMS 4503 - Nabil Tahani 47

• Continuously compounded rate

where EARc is the continuous effective rate

1 APRc eEAR

Measuring Interest Rates

ADMS 4503 - Nabil Tahani 48

Measuring Interest Rates

• Example

Compounding EAR of an APR of 10%Annually 1 10.0000%Semiannually 2 10.2500%Quarterly 4 10.3813%Monthly 12 10.4713%Weekly 52 10.5065%Daily 365 10.5156%Continuous infinity 10.5171%

25

ADMS 4503 - Nabil Tahani 49

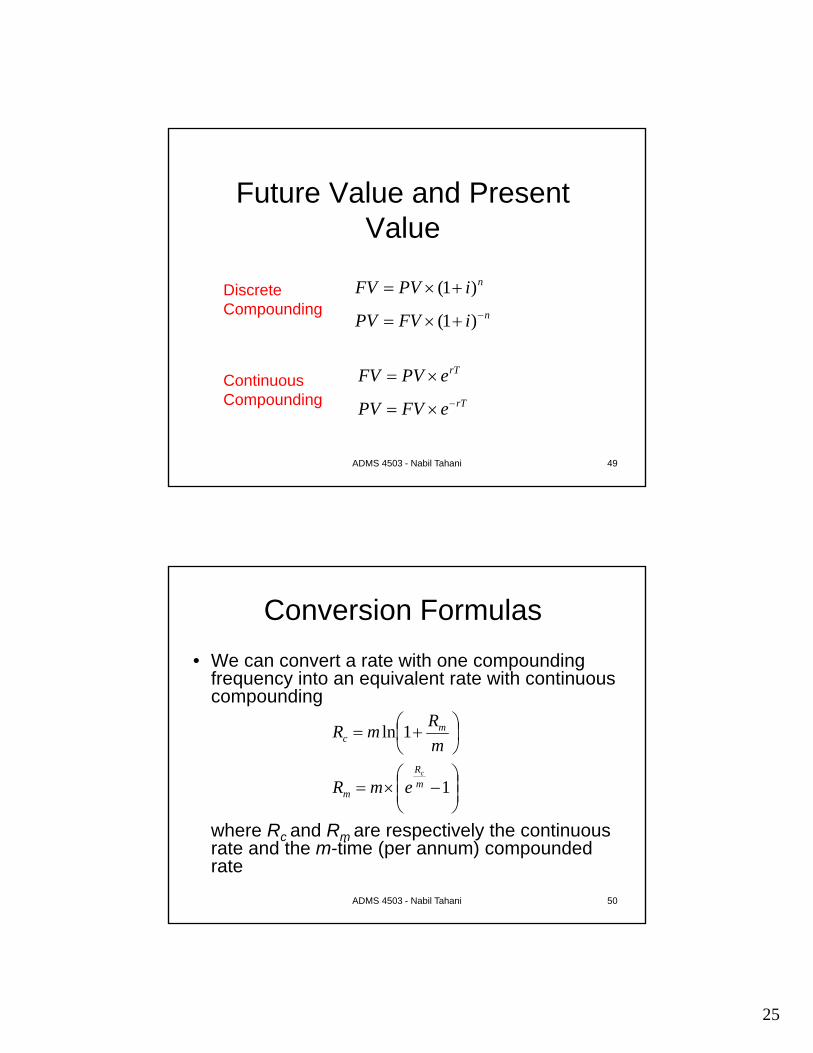

niPVFV )1( niFVPV )1(

Future Value and Present Value

rTePVFV rTeFVPV

Discrete Compounding

Continuous Compounding

ADMS 4503 - Nabil Tahani 50

Conversion Formulas

• We can convert a rate with one compounding frequency into an equivalent rate with continuous compounding

where Rc and Rm are respectively the continuous rate and the m-time (per annum) compounded rate

1

1ln

m

R

m

mc

c

emR

m

RmR

26

ADMS 4503 - Nabil Tahani 51

Conversion Formulas

Example• An interest rate is quoted as 10% per annum

with semi-annual compounding• The equivalent continuous rate is

%7580.92

%101ln2

cR

ADMS 4503 - Nabil Tahani 52

Conversion Formulas

Example• An interest rate is quoted as 8% per annum with

continuous compounding• The equivalent quarterly compounded rate is

%0805.814 4

%8

4

eR