A REVIEW OF THE WORLD

SHEEPMEAT MARKET

THE EEC (l0)

N. BLYTH

Discussion Paper No. 60

Volume 3

Agricultural Economics Research Unit

Lincoln College

loS.S.N.OI10-7720

THE AGRICULTURAL ECONOMICS RESEARCH UNIT Lincoln College, Ca...Lterbury, N.Z.

THE UNIT was established in 1962 at Lincoln CoJ.lege, University of Canterbury. Its major sources of funding have been al1.l1uai grants from the Department of Scientific and Industrial Research and the College. These grants have been supplemented by others from commercial and other organisations for specific research projects within New Zealand and overseas.

The Unit has on hand a programme of research in the fields of agricyltural economics and management, including production, marketing and policy, resource economics, and the economicsoflocation and transportation. The results of these research studies are published as Research Reports as projects are completed. In addition, technical papers, discussion papers and reprints of papers. published or delivered elsewhere are available on request. For list of previous publications see inside back cover.

The Unit and the Department of Agricultura,lEconomics and Marketing and .the Department of Farm Management and . Rural Valuation maintain a dqse working relationship in research and associated matters. The combined academic staff of the Departments is around 25.

The Unit also sponsors periodic conferences and seminars on appropriate topics, sOl;netimes in conjunction with other organis.ations.

The overall policy of the Unit is set by a Policy Committee consisting of the Director, Deputy Director and appropriate Professors.

UNIT POLICY COMMITTEE: 1981 .

Professor J,R. Dent, B.Se., M.Agr.Sc., Ph.D. (Farm Management and Rural Va.luation)

Professor B.J. Ross, M.Agr.Sc. (Agricultural Economics)

P.D. Chudleigh, E.Se., (Hons), Ph.D.

UNIT RESEARCH STAFF: 1981

Director Professor J.B. Dent, B.Se., M.Agr.Sc., Ph.D.

Deputy Director

P.D. Chudleigh, B.Sc. (Hons), Ph.D.

Research Fellow in Agricultural Policy

J.G. Pryde, G.B.E., M.A., F.N.Z.I.M.

Senior Research Economists KL. Leathers, B.S., M.S., Ph.D.

RD. Lough, B.Agr.Sc.

Research Economists CD. Abbott, B.$c.(Ho!J,s), D.B.A.

AC.Beck, B.Sc.Agr., M.Ec. J.D. Gough, B.Se., M.Com.

RL King, ,B.A. P). McCartin, B.Agr.Com.

C.R-McLeod, B.Agr.Sc. RG.Moffitt,·B.Hort.Sc., N.D.H.

M.M. Rich; Dip.V,F.M., B.Agr.Com., M.Ec. RL.Sheppard, B.Agr.Sc. (Hans)

PostGraduate Fellows N. Blyth, B.Sc. (Hons.)

M. Kagatsume. B.A., M.A N.M. Shadbolt,B. Sc .. (Hons.)

Secr~tary JA Rennie

CONTENTS

PREFACE

SUMMARY

1. A REVIEW OF THE SHE EPMEAT MARKET IN THE EEC

1 .1 Introduc Hon

1.2 Production

1.3 Consumption

1.4 Trade

2. UNITED KINGDOM

2.1 Production

2.2 C~nsumption

2.3 Prices

2.4 Trade

2.4.1 Exports

2.4.2 Imports

3. FRANCE

3.1 Production

3.2 Consumption

3.3 Prices

3.4 Trade

4. IRELAND

4.1 Production

4.2 Consumption

4.3 Trade

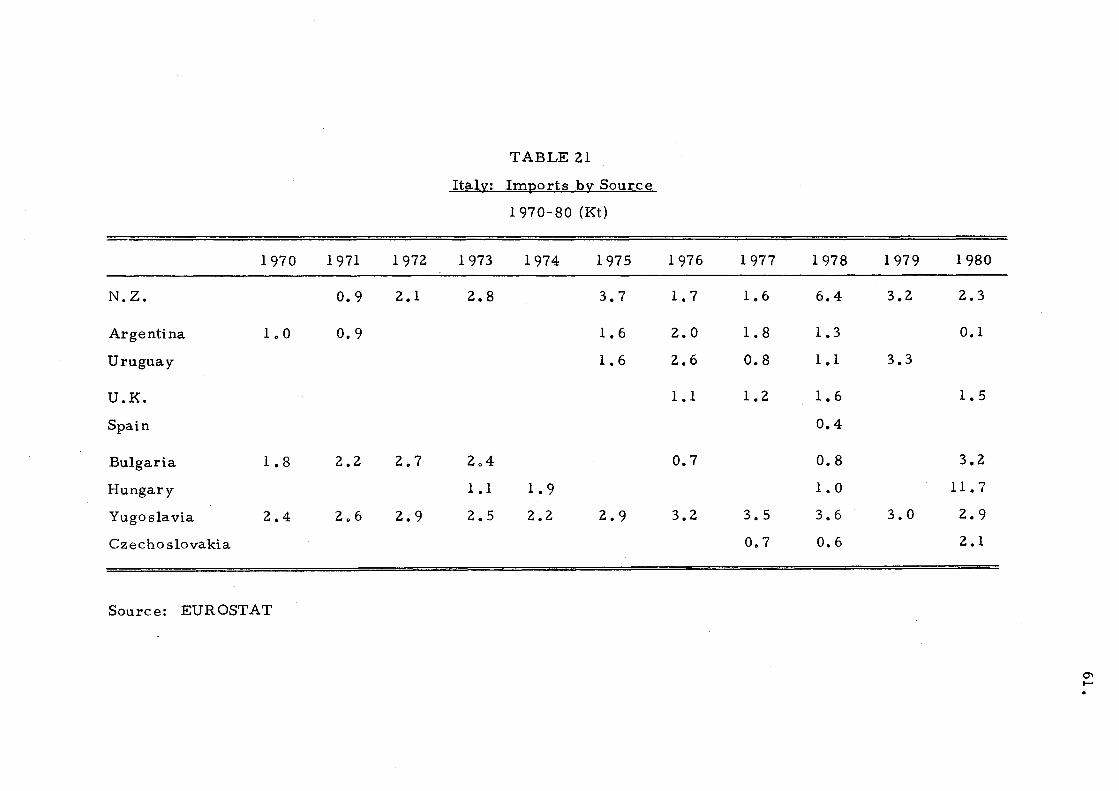

5. ITALY

5.1 Production

5.2 Consumption

5.3 Trade

Page

(i)

1

3

4

7

10

13

13

16

22

23

23

23

29

29

30

34

34

41

41

44

47

53

53

55

57

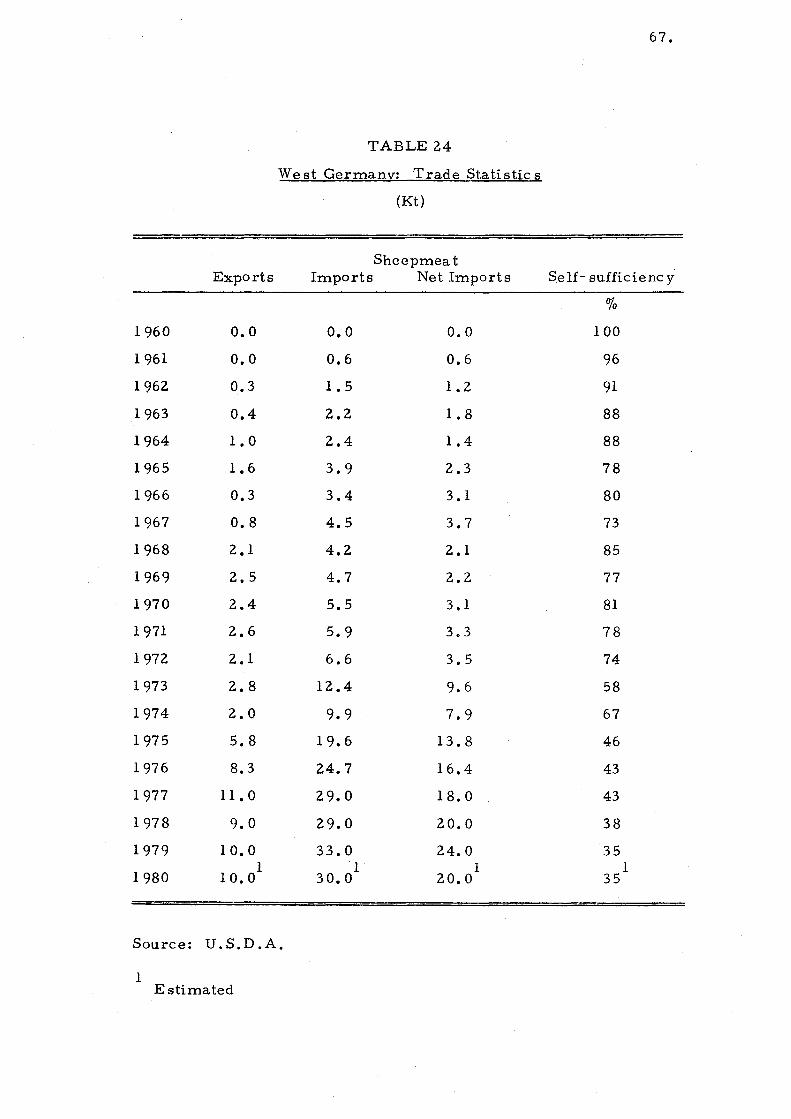

6. WEST GERMANY

6.1 Production

6.2 Consumption

6.3 Trade

7. THE NETHERLANDS

7.1 Production

7.2 Consumption

7.3 Trade

8. BELGIUM AND LUXEMBOURG

8.1 Production

8.2 Consumption

8.3 Trade

9. DENMARK

10.

9.1 Production

902 Consumption

9.3 Trade

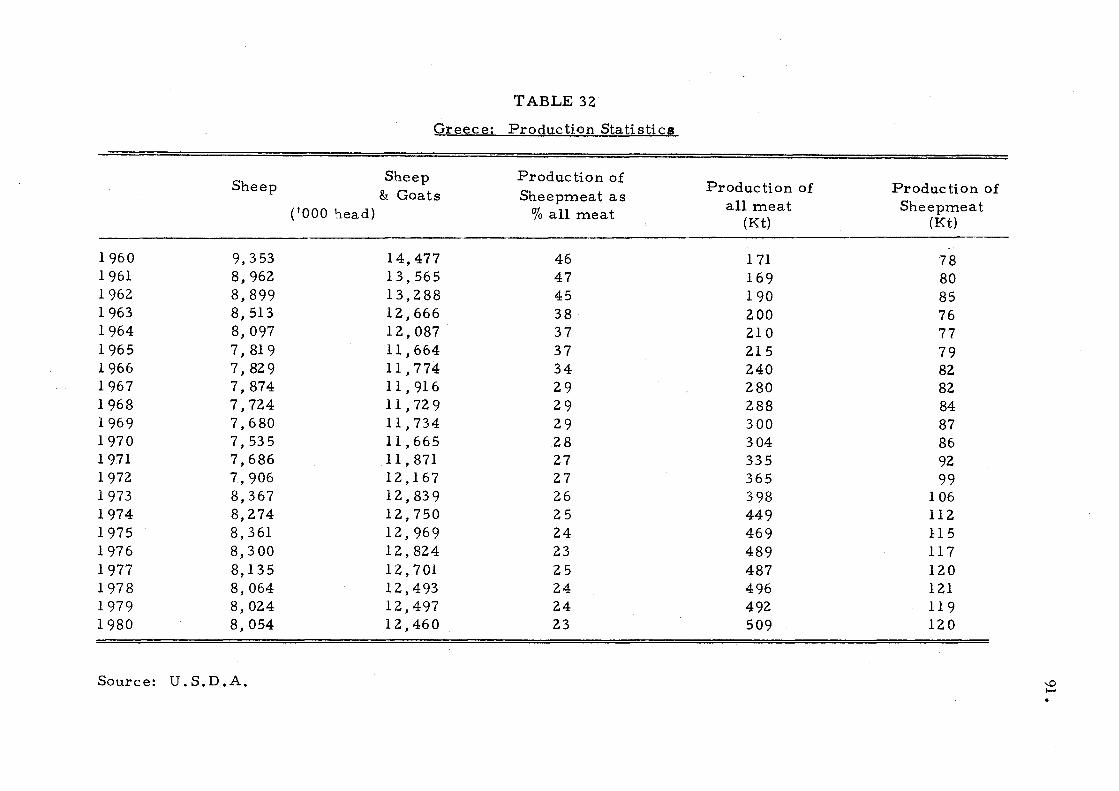

GREECE

10.1 Production

10.2 Consumption

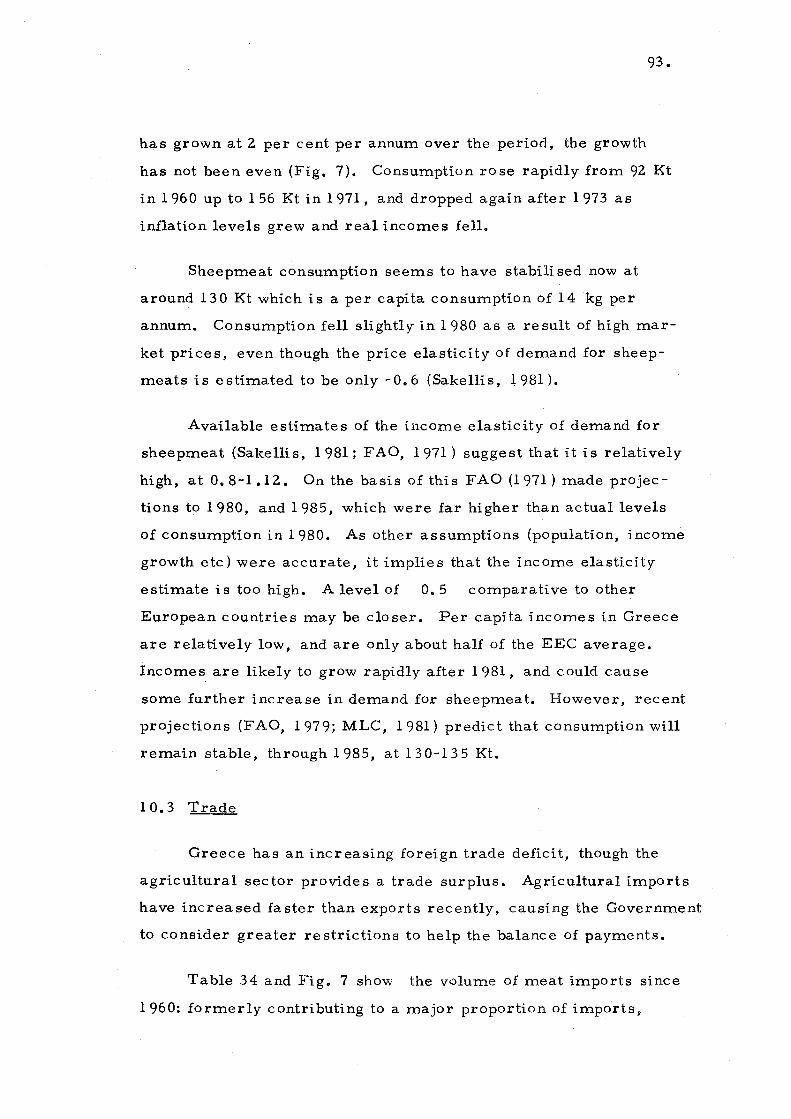

10.3 Trade

10.4 A Note on Greece and the EEC

REFERENCES

Page

63

63

63

68

73

73

75

75

79

79

79

80

85

85

85

88

89

89

92

95

98

Ib3

PREFACE

This volume is the third in a series of five reviewing the

world sheepmeat market. Other volumes in the series are as

follows: Volume One gives an overview of the world sheepmeat

market. In this respect, Volume One can be considered a summary

for the whole serie s. Volume Two pre se nts a review of sheepmea t

production, consumption, and trade in the major exporting countries

of New Zealand, Australia, and Argentinao Volume Four concentrates

on North America, Japan and the Middle East whilst Volume Five

deals with East European countries.

The present paper (Volume Three) reviews sheepmeat

production, consumption, and trade in the EEC countries.

The five volumes of this discussion paper form part of the

A.E.R.U. 's programme of research in the marketing and inter

national trade area. Other paper s relevant to sheepmea t markets

published recently by the A.E.R.U. include Research Report

No.1 09 by R. L. Sheppard on Changes in U. K. Mea t Demand,

Discussion Paper No's 51 and 59 by N. Blyth on the EEC Sheepmeat

Regime and Discussion Paper No. 52 on Future Directions for

New Zealand Lamb Marketing.

(1)

P. D. Chudleigh,

Director

ACKNOWLEDGEMENT

The author wishes to acknowledge the workshop

on "The EEC Sheep Industry; Perspectives and

Implications for N.Z.", held at Massey University

by the Centre for Agricultural Policy Studies in

October 1981. The workshop provided useful background

material for the author whilst completing this volume.

SUMMARY

Patterns of productions, consmnption and trade in the EEC vary

widely among the ten members.

The U. K. and France are major consumers of sheepmeat, followed

by Ireland, Italy, Germany and Greece. In the other States sheepmeat

consumption is relatively unimportant.

Production and trade are similarly distributed. However, the

trends over the period considered show an increase in production in

most states, and an increase in consumption in France, Greece,

Germany and Italy, but a major decline in the United Kingdom.

As the EEC produces only 60 per cent of its consumption, it is

highly dependent on external sources for supply. Imports were at a.

maximum in 1969 (422 Kt), but have dropped steeply since, to 328 Kt.

This is a result of declining demand in the U.K. and the EEC's imposi

tion of a 20 per cent tariff. A further decline is expected following

the introduction of a Common Polic y for sheepmeatB in 1980. The main

suppliers to the Community are N. Z., Argentina, Australia and the

East European states. In 1980 these countries supplied 80.4 per cent,

30 per cent, 1.9 per cent, and 13.1 per cent of total imports respectively.

The outlook for trade is for a continuation of the current trends,

with a net decrease in imports. Trade with Germany, Italy, France

and Greece should continue to grow, but ma y be offset by a decline in

other states, particularly the U.K. Overall, because of the declining

market, and protectionist import policies, the EEC will offer only

limited opportunities for exporters during the 1980's, though will con

tinue to be the major and probably most stable of world markets.

1.

1. A REVIEW OF THE SHEEPMEAT MARKET IN THE EEC (10)

1.1 Introduction

For many years the ten countries of the EEC have been among

the world's major sheepmeat importers, and together have over one

third of world import trade.

Since the formation of the EEC (in 1968) and its enlargement

(in 1973) imports have declined considerably. The preferential trading

arrangements among the member states have encouraged intra-EEC

trade, and reduced imports through the imposition of an ad valorem

tariff, and several forms of non-tariff barrier. In 1980 more formal

arrangements were made, under a Common Sheeprneat Regime to

support EEC sheep producers, and to harmonise the ten markets.

Voluntary Restraint Agreements (VRA's) were negotiated with third

country exporters, to protect the internal EEC markets from disruption.

The VRA's guarantee exporters access to a large and compari

tively wealthy and stable market for the next few years, and as the

allowances are relatively generous they are unlikely to be filled by

exporters. The main reason for exporters not providing the full quota

is that there has been a natural decline anyway. in the major market

(the U. K.}o The decline has partly been offset by growth of the

Continental EEC markets, though much of the increased demand in

these markets has been supplied by British exporters. These trends

are likely to continue, to the detriment of traditional exporters in the

southern hemisphere, who face a diminishing import market.

Nevertheless, there may be opportunities for expansion of trade

with Community markets other than the U. K., and the trade is likely

to remain of major importance within the w orId sheepmeat market.

The objective of this review is to provide a background to each of the

3.

4.

EEC states in order for exporting countries to assess their position

and potential. In the re st of this section a general overview of the

EEC market is given. In following sections production, consumption

and trade in each of the ten member-states is considered in more

detail. and. on the basis of the market characteristic s and outlook to

1985, implications are drawn for exporter s.

1.2 Production

Sheepmeat production in the EEC is aver y minor income-earner.

representing only 1.3 per cent of agric ultural revenue. Only in the

United Kingdom and Ireland does the sheepmeat sector contribute more

than 3 per cent (4.1 per cent and 3.1 per cent respectively). Much

of the general comment here is not therefore relevant to these two

countries as the structure of their industries is qui.te different from

other countries. Compared to other meats. sheepmeat is of little

importance. being 2.4 per cent of all meat production. The community

flock of 43 million accounts for only 4 per cent of world sheep. but

produces 7i per cent of the world's sheepmeat. The sheep industry

in Europe has a different basic structure from other agricultural

enterprise s. Although there are some semi -industriali sed sheep fatten

ing units. it is essentially a small-holding operation. Breeding flocks

tend to be located in hill and mountain regions. and other less-productive

areas, their size and character being determined more by social and

environmental factors than by relative returns. As a consequence.

neither breeding nor fattening elements of the industr yare partic ularly

responsive to market fluctuations in the short to medium term.

Two-thirds of the community's 43 million sheep are found in

areas defined in the EEC Directive (1975) as less-favoured. In France.

70-75 per cent of the sheep flock is located in such regions. whilst in

Italy the proportion is 80-90 per cent. In general. sheep farming is

5.

declining in lowland regions "Wh ere other types of enterprise compete

with it, whereas it is increasing in upland regions and other less

favoured areas. The physical conditions, size of holding, distance

from markets, communication difficulties and traditionalism asso

ciated with these areas create a complex of problems which cannot

be resolved through manipulation of market mechanisms. Hence,

farm incomes have to be supported according to the Directive, though

the common policy on sheepmeats will give direct market-price support.

Within the regions there are significant differences in sheep

production systems and breed of sheep, depending on the relative

importance of meat, wool and milk production. The majority of sheep

are bred for meat, with milking sheep numbering less than 10 per cent

of the flock and confined to Italy and the south of France. Sheep kept

exclusively for wool are gradually disappearing.

The Community's flock is distributed unevenly between states:

only the U. K. and France have a significant number of sheep, and

between them account for 79 per cent of EEC production of sheepmeat.

Though overall sheep numbers aCld production have been stable, with

a small increase since 1976 (Table 1), these figures obscure marked

regional trends: these are discussed further in the specific country

reviews. However, the overall level of production is important since

the introduction of a common sheepmeat polic y in 1980 unite s the

indi vidual state s into a single market. The Regime doe s still allow

each countr y to pur sue its own polic y though, through a system of

differential prices and support mechanisms (Blyth, 1980).

The outlook for production is for an increase in output to 540 Kt

(CEC, 1977): this is lower than FAO (1979) projections to 1985, which

are for an output of 560- 600 Kt. Self- sufficienc y levels are estimated

to remain similar to the present level of 65 per cent.

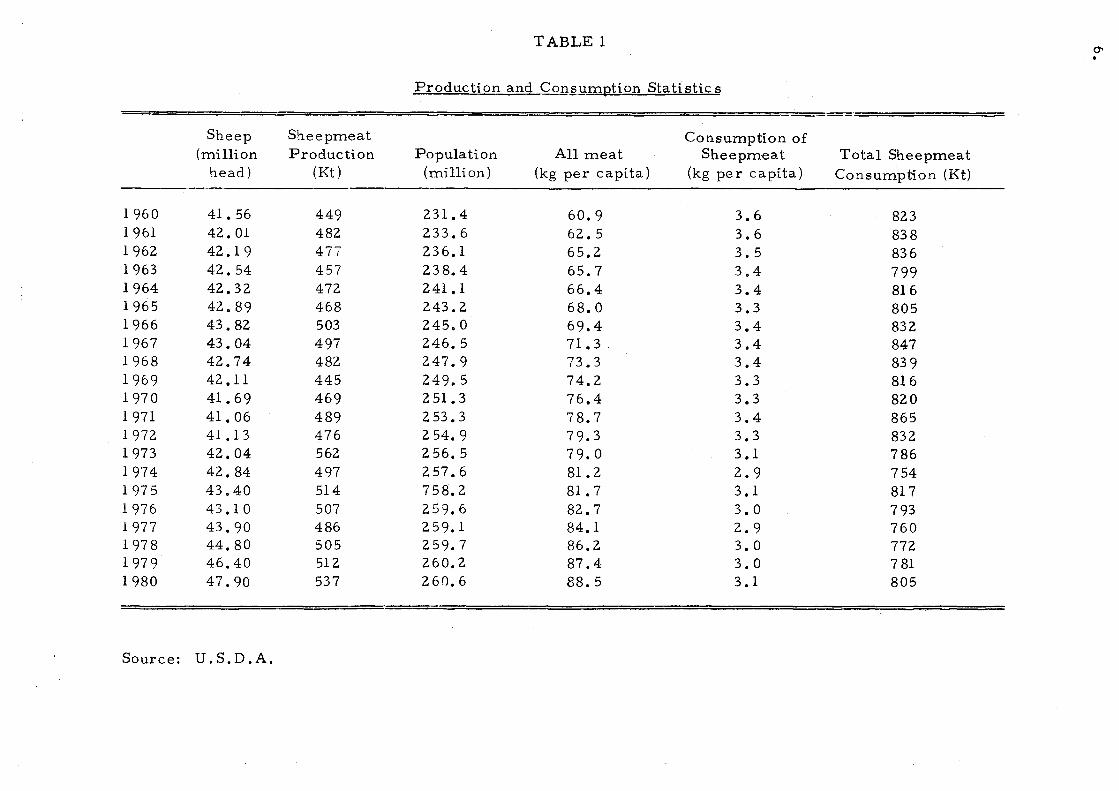

TABLE 1 0' .

Production and Consum12tion Statistic s

-Sheep Sheepmeat Consumption of

(million Production Population All meat Sheepmeat Total Sheepmeat head) (Kt) (million) (kg per capita) (kg per capita) Consumption (Kt)

1960 41.56 449 231. 4 60.9 3.6 823 1961 42.01 482 233.6 62.5 3.6 838 1962 42.19 477 236.1 65.2 3.5 836 1963 42.54 457 238.4 65.7 3.4 799 1964 42.32 472 241.1 66.4 3.4 816 1965 42.89 468 243.2 68.0 3.3 805 1966 43.82 503 245.0 69.4 3.4 832 1967 43.04 497 246.5 71.3. 3.4 847 1968 42.74 482 247.9 73.3 3.4 839 1969 42.11 445 249.5 74.2 3.3 816 1970 41.69 469 251.3 76.4 3.3 820 1971 41.06 489 253.3 78.7 3.4 865 1972 41.13 476 254.9 79.3 3.3 832 1973 42.04 562 256.5 79.0 3.1 786 1974 42.84 497 257.6 81.2 2.9 754 1975 43.40 514 758.2 81. 7 3.1 817 1976 43.10 507 259.6 82.7 3.0 793 1977 43.90 486 259.1 84.1 2.9 760 1978 44.80 505 259.7 86.2 3.0 772 1979 46.40 512 260.2 87.4 3.0 781 1980 47.90 537 260.6 88.5 3.1 805

So ur c e: U. S. D • A.

7.

These projections, based on present trends, could be modified

by the common polic yon sheepmeat adopted by the EEC in 1980. A

drop in producer incomes in less favoured areas would bring about a

fall in output: on the other hand, stability or a rise in the market price

would be an incentive to domestic production (Bryant, 1981; Blyth, 1981),

Indeed, a "revival ll is taking place in sheep farming in several member

states in response to rising demand.

Neither do the projections take into account the enlargement of the

EEC to include Greece, which occurred in January 1981, nor Spain and

Portugal who will join at a later date. Separate projections for Greek

production are given in section 11.1.

1.3 Consumption

Meat consumption in the EEC is high, compared to world levels,

at 87 kg per capita. In relation to this, sheepmeat is comparatively

unimportant, and is only 3.4 per cent of all meat (Table I), at 3.1 kg

per capita. Total sheepmeat consumption has varied around 800 Kt

over the period 1973 - 80: thi s masks the trends within state s, with

consumption falling in the U. K., but rising in France and Italy.

Consumer attitudes and consumption patterns are also diverse,

ranging from continuous consumption at relatively high per capita levels

in Ireland and the U. K. (11.2 kg) to sporadic, 0 r insignificant lIfe stive II

consumption at low levels as in Italy and the Netherlands (0.2 kg). In

other parts of the Community, notably France, lamb is eaten more·

regularly, but as a luxury, high-price meat. In Denmark and Germany

there is evidence that lamb is becoming accepted as a substitute for

other meats. Migrant worker s and other ethnic groups throughout the

EEC often have str )ng preferences for sheepmeats and are regular

consumers of mutton and lamb.

8.

This diversit:, of consumption patterns is reflected in wide varia

tions in the relationship between the price s of sheepmeats and other

meats. In France, where lamb is a luxury meat, retail prices are

substantially above those for other meats, including beef, whilst in the

U. K. lamb se11s at about the same price as beef. The price of home

ki11ed lamb in the U.K. is usually less than 60 per cent of that in France,

though since 1976 the gap has narrowed, due to rising U. K. price sand

fa11ing prices in France (Volans, 1981).

The structure of sheepmeat prices in the EEC is essentia11y

determined in two markets:

(i) The U.K. market directly influences prices in the Irish market

(though in 1978-80 the French market has had a greater influence).

(Ii) The French market determine sthe level of price s received by

producers in states exporting to France (Belgium, Germany,

the Netherlands and also Italy).

However, the market price in Germany and Italy is lower than

that in France, as their markets are influenced by the price of imports

which are often considered to be of a lower quality than home-produced

meat. In general though, price difference s are narrowing,. and wi11

continue to do so, as far as the forces of supply and demand are a110wed

to work freely in the market. The Intervention price of the Sheepmeat

Regime, based on the French market price (applied in all states except

the U.K.) should hasten the process of harmonisation.

The outlook is for consumption levels of 830 Kt (CEC, 1977) by

1985, though FAO (1979) projections are somewhat lower at 760 Kt, or

2.9 kg per capita. The latter is probably more realistic, in the light

of current consumption levels. However, under the proposed Common

Sheepmeat Regime, market prices could rise substantia11y, which

would reduce consumption below this level (MLC, 1981). Population

growth is low overa11 (Table 1) and is not likely to have much effect

on future demand.

9.

TABLE 2

Sheepmeat Trade in the EEC

Total Imports 1 Exports (Kt) (Kt)

1961 385.0 14.8

1962 390.1 22.7

1963 377.4 25.8

1964 375.9 26.4

1965 384.3 29.0

1966 355.4 31.6

1967 381.3 29.5

1968 398.2 27.9

1969 424.1 33.1

1970 388.4 33.5

1971 410.3 43.1

1972 422.6 48.2

1973 352.5 51.3

1974 286.1 52.9

1975 343.1 66.1

1976 320.0 74.3

1977 323.0 77.1

1978 339.0 80.3

1979 330.0 71.4

1980 328.0 70.9

1 Includes intra-EEC trade

Source: U.S.D.A

10.

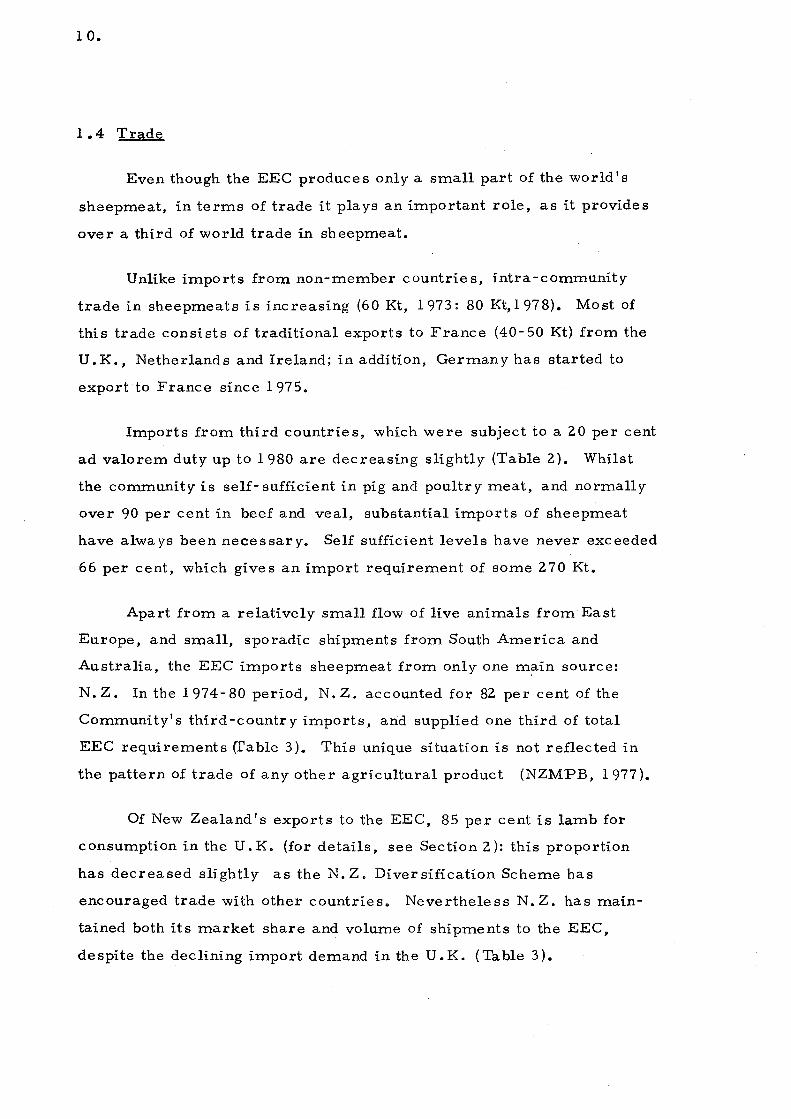

1.4 Trade

Even though the EEC produce s only a small part of the world's

sheepmeat, in terms of trade it plays an important role, as it provides

over a third of world trade in sheepmeat.

Unlike imports from non-member countries, intra-community

trade in sheepmeats is increasing (60 Kt, 1973: 80 Kt,1978). Most of

this trade consists of traditional exports to France (40- 50 Kt) from the

U. K., Netherlands and Ireland; in addition, Germany has started to

export to France since 1975.

Imports from third countries, which were subject to a 20 per cent

ad valorem duty up to 1980 are decreasing slightly (Table 2). Whilst

the community is self- sufficient in pig and poultry meat, and normally

over 90 per cent in beef and veal, substantial imports of sheepmeat

have always been necessary. Self sufficient levels have never exceeded

66 per cent, which gives an import requirement of some 270 Kt.

Apart from a relatively small flow of live animals from East

Europe, and small, sporadic shipments from South America and

Australia, the EEC imports sheepmeat from only one main source:

N. Z. In the 1974- 80 period, N. Z. accounted for 82 per cent of the

Community's third -countr y imports, and supplied one third of total

EEC requirements (I'able 3). This unique situation is not reflected in

the pattern of trade of any other agricultural product (NZMPB, 1977).

Of New Zealand's exports to the EEC, 85 per cent is lamb for

consumption in the U. K. (for details, see Section 2): this proportion

has decreased slightly as the N. Z. Diversification Scheme has

encouraged trade with other countries. Nevertheless N.Z. has main

tained both its market share and volume of shipments to the EEC,

de spite the declining impo rt demand in the U. K. (Table 3).

TABLE 3

EEC lttlIloris of SheeI!Ill!ilat froIll Third Countries (tonnes carcasfi weiljhjJ

1973 1974 1975 1976 1977 1978

Tonnes 0/0 Tonnes % Tonnes 0/0 Tonnes 0/0 Tonnes % Tonnes

N.Z. 251,097 80.1 209,271 85.0 245,429 83.5 222,539 81.4 220,581 82.2 231,766

Argentina 8,406 2.7 6,932 2.8 13,890 4.7 14,467 5.3 16,993 6.3 11,164

Australia 24,418 7.8 7,939 3.2 8,531 3.0 12,713 4.6 5,758 2.1 12,114

Hungary 10,150 3.2 8,530 3.5 8,622 3.0 8,639 3.2 8,043 3.0 6,866

Bulgaria 5,707 1.8 3,596 1.5 4,108 1.5 2,146 0.8 838 0.3 2,488

Czechoslovakia 699 0.3 641

Poland 1,435 0.5 1,939 0.8 3,338 1.2 3,645 1.3 4,232 1.6 4,822

Yugoslavia 2,520 0.8 2,448 1.0 3,123 1.1 3,276 1.2 3,584 1.3 3,824

Iceland 384 0.2 367

Uruguay 334 0.1 2,535 0.9 3,507 1.3 2,450 0.9 2,063

Brazil 1,713 0.6 146

East Germany 1,645 0.6 1,918 0.8 2,274 0.8 2,427 0.8 2,304 0.9 3,625

Rumania 3,082 1.0 1,570 0.6 968 0.3 190 0.1 229 0.1 418

Spain 428 0.2 1,002

TOTAL 313,629 100.0 246,066 100.0 295,937 100.0 273,549 100.0 268,236 100.0 281,306

Source: Agra Europe

1979

0/0 Tonnes 0/0

82.4 218,604 87.0

4.0 10,899 4.3

4.3 8,885 3.5

2.4 1,751 0.6

0.9 2,128 0.8

0.2 650 0.2

1.7 20

1.4 3,040 1.2

0..1 617 0.2

0.7 4,005 1.6

0.1

1.3 6

0.1 130 0.1

0.4 8

100.0 251,088 100.0

1980

Tonnes

195,700

7,300

4,700

1 3,000

3,200

7,200

2,900

1,500

5,000

243,300

0/0

80.4

3.0

1.9

5.5

1.5

2.9

1.2

0.6

2.0

100.0

.... ....

12.

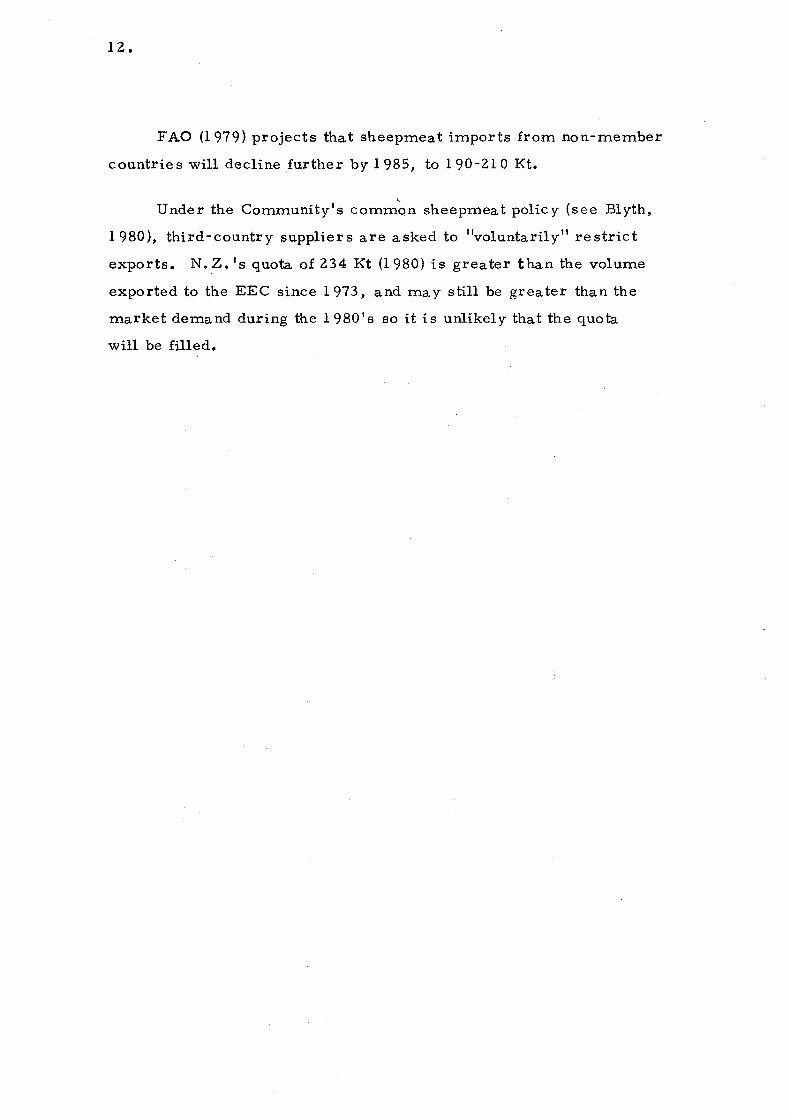

FAO (1979) projects that sheepmeat imports from non-member

countries will decline further by 1985, to 190-210 Kt.

Under the Community's comm'on sheepmeat policy (see Blyth,

1980), third-country suppliers are asked to "voluntarily!' restrict

exports. N. Z. 's quota of 234 Kt (1980) is greater than the volume

exported to the EEC since 1973, and rna y still be greater than the

market demand during the 1980 1 s so it is unlikely that the quota

will be filled.

2. UNITED KINGDOM

2.1 Production

For a highly industrialised densely populated country the U.K.

has a surprisingly large sheep flock of some 20 million head. It is

the largest producer in the EEC, with 50 per cent of the Community's

output. Sheep contribute more to the U. K. IS agricul tural revenue

than in other member states, but this is still only 4 per cent.

Sheep farming systems are very different from the rest of

the EEC. In general they are larger units running an average 380

sheep. Costs tend to be high (Nix, 1979; Brabyn, 1978) though

productivity is higher than the other countries; this results from

specialisation of production which is based on the interdependency

of hill and lowland flocks. Under this system the hill regions

breed hardy sheep which are crossed with larger, upland rams:

the sheep produced from the cros sings a re sent to intermedia te

regions where they are crossed with meat-strain rams, to produce

slaughter lambs. These lambs are fattened on the lowlands prior

to slaughter (Lavercombe. i978).

The specialisation has origins in traditional agriculture,

and has been greatly encouraged by the granting of direct aid per

animal kept in mountain or hill areas (a system which ha s been

replaced with the similar EEC policy on less-favoured regions).

The financial assistance tends to increase the turn-off from the

hills and effectively subsidies the lambs to lowland fatteners;

it also reinforces the specialisation in production of grass-lamb

for slaughter in summer and autumn (Whitby, 1977). Specialisa

tion has been further encouraged by the payment of a Guaranteed

price which eliminates the risk of a drop in income and provides

Ii ttle incentive for out-of- sea son produc tion (HMSO Fa t- Sheep

Guarantee Scheme: Annual). This scheme has been replaced by

Deficiency Payments which are, however, intended to smooth

produc tion in the future (MLC, 1981).

13.

14.

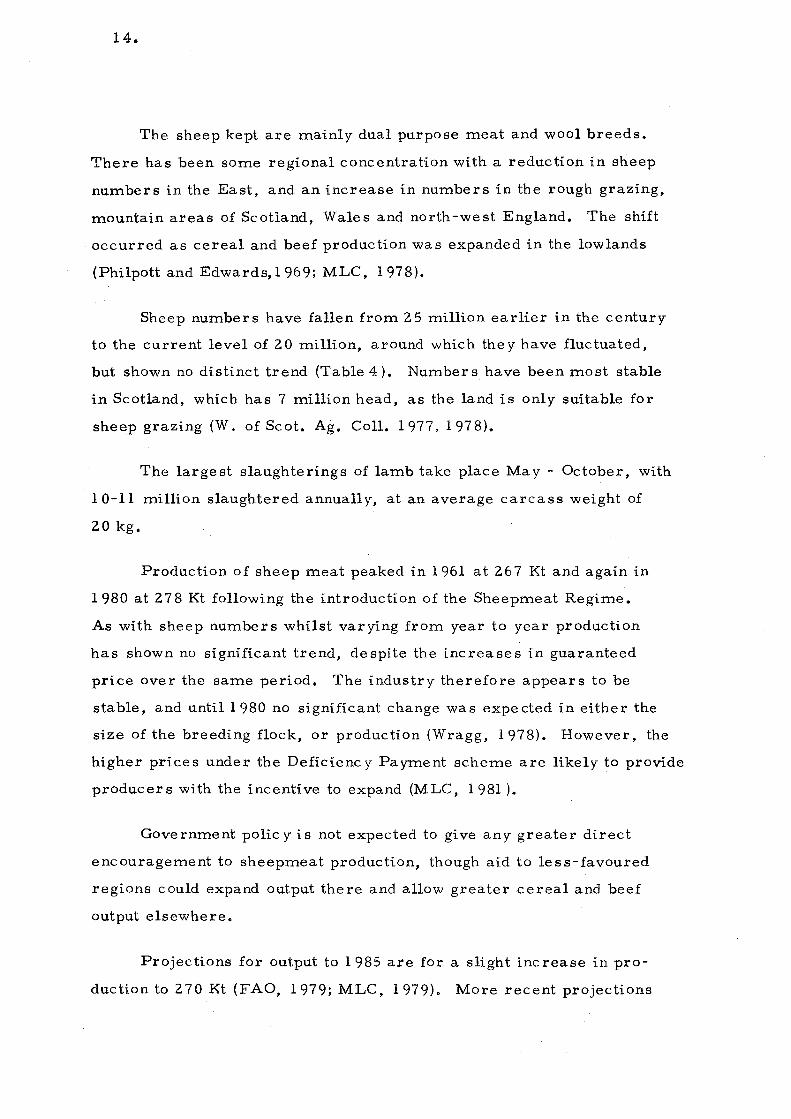

The sheep kept are mainly dual purpose meat and wool breeds.

There has been some regional concentration with a reduction in sheep

numbers in the East, and an increase in numbers in the rough grazing,

mountain areas of Scotland, Wales and north-west England. The shift

occurred as cereal and beef production was expanded in the lowlands

(Philpott and Edwards, 1969; MLC, 1978).

Sheep numbers have fallen from 25 million earlier in the century

to the current level of 20 million, around which they have fluctuated,

but shown no distinct trend (Table 4). Number s have been most stable

in Scotland, which has 7 million head, as the land is only suitable for

sheep grazing (W. of Scot. Ago ColI. 1977,1978).

The largest slaughterings of lamb take place May - October, with

10-11 million slaughtered annually, at an average carcass weight of

20 kg.

Production of sheep meat peaked in 1961 at 267 Kt and again in

1980 at 278 Kt following the introduction of the Sheepmeat Regime.

As with sheep numbers whilst varying from year to year production

has shown no significant trend, despite the increases in guaranteed

price over the same period. The industry therefore appears to be

stable, and until 1980 no significant change was expe cted in either the

size of the breeding flock, or production (Wragg, 1978). However, the

higher prices under the Deficiency Payment scheme are likely to provide

producer s with the incentive to expand (MLC, 1981).

Government policy is not expected to give any greater direct

encouragement to sheepmeat production, though aid to less-favoured

regions could expand output there and allow greater cereal and beef

output elsewhere.

Projections for output to 1985 are for a slight inc rease in pro

duction to 270 Kt (FAO, 1979; MLC, 1979). More recent projections

15.

TABLE 4

United Kingdom: Production Statistics

All meat Sheepmeat as Sheep Slaughter Production Production % all meat

(million head) (Kt) (Kt)

1960 20.0 11.4 228 2149 10.6

1961 20.2 13.2 267 2368 11.2

1962 20.8 12.5 254 2457 10.2

1963 21. 0 12.1 245 2498 9.8

1964 21.2 12.6 255 2499 10.2

1965 21. 8 12.1 244 2528 9.6

1966 21. 0 13.5 270 2599 10.3

1967 20.4 13.1 262 2609 10.0

1968 19.6 12.3 246 2654 9.2

1969 19.1 10.4 207 2672 7.7

1970 18.5 11.4 227 2837 8.0

1971 18.7 11.5 225 2883 7.8

1972 19.5 11. 0 219 2924 7.4

1973 19.9 11.7 232 2871 8.0

1974 20.1 12.9 252 3128 8.0

1975 19.5 13.1 260 3081 8.4

1976 19.8 11.5 248 2983 8.3

1977 20.5 10.1 228 2968 7.6

1978 21. 7 10.6 227 3028 7.8

1979 21. 6 10.3 231 3057 7.5

1980 21. 6 11. 2 278 29901 7.4

1 Estimated

Source: U.S.D.A.

16.

(MLC, 1981) suggest that output c:;:ould be around 5 per cent higher than

this, at 290 Kt, because of the higher support prices.

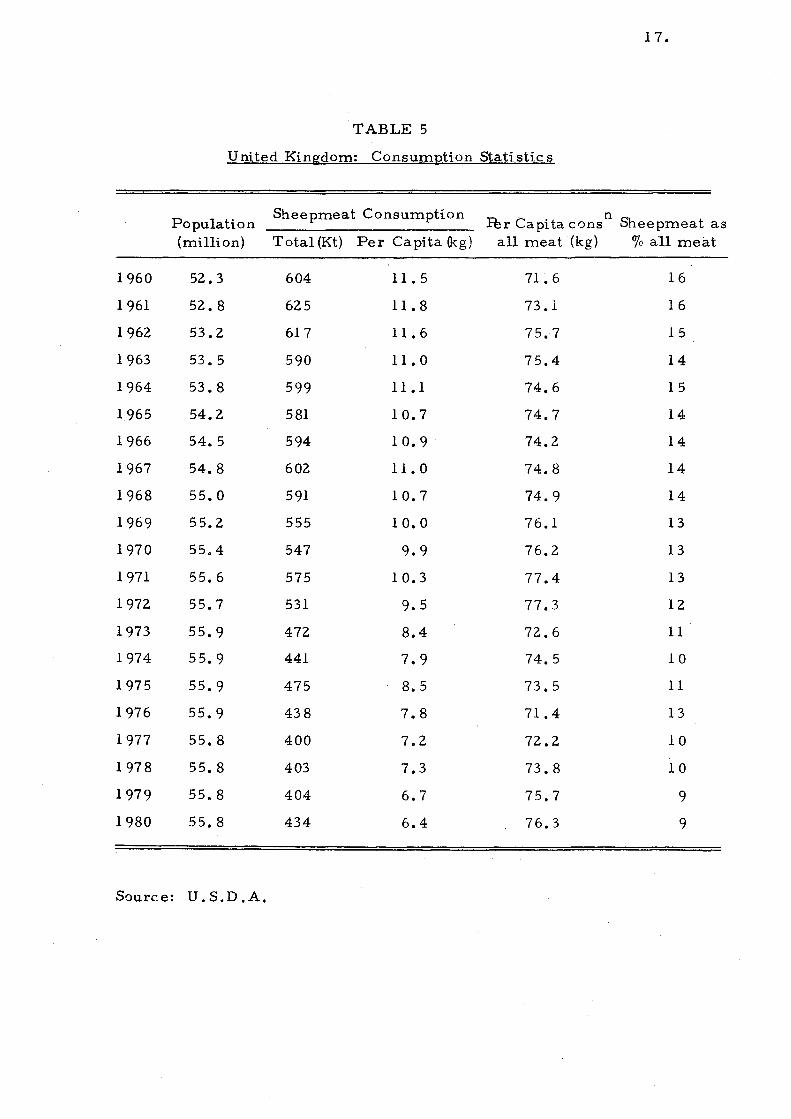

2.2 Consumption

The main features of consumption of sheepmeats in the U.K. are:

(1) the large quantities (both total and per capita) purchased, com

pared to other EEC countries. The U. K. accounts for 52 per

cent of EEC consumption though thi s share has declined from

74 per cent in 1960.

(ii) the rapid decline in the market through the 1970's.

The U. K. is one of the world's main meat-consuming countries,

with a per capita demand of 75 kg (Table 5). The market is dominated

by beef, which accounts for over a third of consumption. There has

been a dramatic growth in poultry-meat consumption as its price has

fallen relative to other meats. Sheepmeat is eaten as a substantial

and regular part of the diet, though its share of total consumption has

fallen from 16 per cent to 10 per cent since 1960 (Table 5).

The U.K. was one of the world's major sheepmeat eating countries

with a per capita demand of 17 kg in the 1930-50's; by 1960 this had

fallen to 11 kg. Over the period 1960- 80 a further decline of 36 per

cent left consumption at 7 kg in 1980.

Total consumption over the same period declined from 604 Kt to

410 Kt - despite an annual population increase of 0.4 per cent and a

total population of 56 million in 1980.

Thus, there has been a drastic change in the pattern of demand

for sheepmeats. The type of meat demanded has also changed, away

from mutton, to lamb which now accounts for 86 per cent of the sheep

meat eaten. Consumer preference is still for fre sh meat, rather than

17.

TABLE 5

United Kinjidom: Consumption Statistics

Population Sheepmeat Consumption n

Fer Capita cons Sheepmeat as (million) Total (Kt) Per Capita (kg) all meat (kg) o/c all meat

1960 52.3 604 11.5 71. 6 16

1961 52.8 625 11.8 73.1 16

1962 53.2 617 11.6 75.7 15

1963 53. 5 590 11.0 75.4 14

1964 53.8 599 11.1 74.6 15

1965 54.2 581 10.7 74.7 14

1966 54.5 594 10.9 74.2 14

1967 54.8 602 11. 0 74.8 14

1968 55.0 591 10.7 74.9 14

1969 55.2 555 10.0 76.1 13

1970 55.4 547 9.9 76.2 13

1971 55.6 575 10.3 77.4 13

1972 55.7 531 9.5 77.3 12

1973 55.9 472 8.4 72.6 11

1974 55.9 441 7.9 74.5 10

1975 55.9 475 8.5 73.5 11

1976 55.9 438 7.8 71.4 13

1977 55.8 400 7.2 72.2 10

1978 55.8 403 7.3 73.8 10

1979 55.8 404 6.7 75.7 9

1980 55.8 434 6.4 76.3 9

Source: U .S.D.A.

18.

frozen imports, which is reflected in the price differences. Demand

is also seasonal, with most purchases of domestic lamb occuring April -

September, when supplies are greatest (Brown, 1959).

Much has been written on demand for me at in the U. K. Bansbeck

(1976) reviews the published material according to whether it deals with

demand analysis, consumer attitudes to meat, the structural, techno

logical and institutional factors affecting meat demand, or forecasts

and projections of the demand for meat.

The majority of the studies which analyse demand for meat,

determine the main factors affecting consumption or price levels, using

regre ssion-analysi s. There is a wide variation in time periods,

estimation procedures and level of market (i. e. wholesale or retail),

but most use data derived from the annual National Food Survey.

Table 6 lists econometric studies of the demand for sheepmeats in the

U.K., and summarises their findings on price and income responses.

The re suits of the se studie s show that the main factor s affecting

demand are:

(1) Income Effects:

The income elasticity of demand for sheepmeat is estimated to

lie between 0.2 - 0.7, which implies that as real incomes have increased

little in the U. K .• purchase s of sheepmeats would have inc rea sed by an

even smaller amount, if this were the only factor affecting demand.

Also:

':' It appears that income elasticities are declining over time

(NFS, 1980; Sheppard, 1980).

':' Within the broad category of "sheepmeat" there are signifi

cant differences in income elasticity for the various cuts

of meat (NFS, 1980).

TABLE 6

Studies of the United Kingdom Meat Market

Period Estimated Elasticity

Year Researcher of Data Market Dependent with respect to:

Analysis Level Variable

Own Price Income

1965 Philpott & Mathe son 1955-62 Q R Quantity -1.43 0.77

1967 Mathe son & Philpott 1955-63 Q R Quantity -1.14

1968 Chetwin 1955-63 A Wh Quantity - 0.70

1969 Edwards & Philpott 1955-63 A R Quantity -1.83 0.32

1974 Greenfield 1955-72 A R & Wh Quantity -0.79

1977 Maclaren 1962 -73 Q Wh Price -0.731

1965 Dixon 1955-61 Q Wh Price -1.80

1973 Coleman & Miah 1958-68 Q 1Vh Price - 0.92

1978 National Food Survey 1970-77 W R Quantity -1.24 0.21

1973 Bushnell 1964-71 M Wh Price -0.791

0,58

1976 Boutonnet Unclear A Wh Price -0.271

1979 NZMPB 1964-77 A Wh Price -1 .1 01

0.56

1978 Kelly 1966-71 Q R Quantity -0.96

1980 Sheppard 1970-77 Q R Quantity -1.80 0.54

R = Retail ....

W = weekly M = monthly Q = quarterly A = annual Wh = Wholesale -.D . 1 Price elasticity implied by flexibilities reported.

20.

* There are wide regional differences in income elasticities

(NFS, 1980), with higher elasticities in the North than in

the South of the U. K.

'!< The qualit y component of purchase s increa se s as incomes

rise, hence there is greater demand for lamb than for

mutton (Hamid Miah, 1976).

(ii) Direct-Price Effects:

There has been an increase in interest in the price effects on

purchases in recent years, partly as a result of the sharper price

fluctuations, and partly because the income-effect on consumption is

dec rea si ng.

The studies show little agreement on the effect of lamb and mutton

prices on demand with estimates of own-price elasticities ranging from

-0.2 to -2. O. Estimates were consistently lower for sheepmeats than

for other meats.

Direct price elasticities appeared to be declining according to

studies using pre-1975 data; more recent work suggests that response

to price changes is increasing again (Sheppard, 1980).

(iii) Cross-Price Effects:

Mutton and lamb in the U. K. are thought to be substitute s for the

other meats - beef, pork and poultry. Measures of the extent of sub

stitutability are captured in the cross-price elasticity of demand.

However, there appear s to be no strong competition between sheepmeats

and other meats. All estimates of cross-price elasticities have been

extremely low, and rarely significant, though as with own-price effects

it appears that consumers are becoming more price-cons.cious and

beef and poultr y prices are beginning to affect mutton and lamb demand.

21.

(iv) Population Effects:

As the population growth rate in the U. K. is low, it has little

effect on change s in total consumption though given the large population,

a change in per capita demand has a large effect on total dema~d. Other

population effects (age patterns, urbanisation, employment (MLC, 1981»

are implicitly accounted for in the income-ela sticit y estimate s which are

based on time-series analysis.

(v) Other Factors:

Polic y, institutional and structural factors ar e usually referred to

qualitatively, but rarely quantified in studies. Attempts have been made

to estimate the effects of polic y alternative s on sheepmeat demand, usually

through changes in price (Kelly, 1978; Boutonnet, 1977; Sheppard, 1980).

Other factors such as freezer ownership and changing consumption patterns

are thought to be more important now than in the 1960' s (Bansback, 1977;

Jones, 1979), but are accounted for implicitly, or by including a time-

trend variable.

In conclusion, it appears from the studies that own price and income

effects are the most important in determining sheepmeat demand. It

seems that the retail price elasticity is increasing, and that the income

elasticity is falling. This suggests that mutton and lamb are becoming

inferior goods, and that as prices rise, consumers respond more to price

changes.

The outlook for consumption depends on the above factors, and on

the effects of the EEC Sheepmeat Regime, but it is generally agreed that

sheepmeat consumption will continue to decline. Earlier forecasts (FAO,

1979; Jones, 1977) predicted levels of 380-410 Kt in 1985. More recent

estimates (MLC, 1981) are somewhat lower, at 370-390 Kt.

22.

2.3 Prices

Producer returns in the U. K. were guaranteed by the U . K.

Government up to 1980. Prices rose from £10. 9/cwt in 1960 to £50/

cwt in 1977. The greate st increase was in 1972, and only small defi

cienc y payments have been made since. Since October 1980, producer

price s have been guaranteed by the EEC (FE OGA) at considerably higher

levels (Volans, 1981).

Producer-prices are analysed by Daniels and Savin (1977), Chetwin

(1969), MLC (1978), and show clear seasonal trends. As supplies of

domestic lamb decline, prices rise to peak when the new seasons lamb

arrives on the market. The seasonal pattern appears to be decreasing

(MLC, 1978), as the effect of U. K. I S exports to France evens out price

fluctuations. The peak of domestic production is also coming earlier

in the season, as the EEC price incentives take effect.

Price s for imported sheepmeats ~e specially frozen lamb) are

heavily discounted against fresh domestic supply (NZMPB, 1977). The

seasonal imports offset shortages of domestic supply, so command the

highest prices in December-April, before the new seasons 1 lamb comes

on to the market. Imported lamb and Scotch beef prices tend to move

together, but English beef is generally higher priced than dome sHc lamb.

Further analysis of wholesale prices can be found in Chetwin (1969), Sault

(1964), Taylor (1960), Bushnell (1973), Philpott (1969), and Maclaren

(1977 ).

As in other EEC countries, imports from non-member countries

face a 10 per cent tariff, (reduced from 20 per cent in 1980) which

effectively rai se s the retail price to the consumer (though exporter s

contend that it lowers the returns to the producer). U.K. prices are

c onsi derably lower than those in othe r member - state s, except for

Ireland whose price s tend to move in hne with Smithfield. U. K. price s

23.

were 50 per cent below those in France in 1968, but since 1976, the

gap has narrowed somewhat. Producer prices should be harmonised

by 1984/85, but the gap between U. K. and other EEC market prices

will remain (Blyth, 1981).

2.4.1 Exports

As Table 7 shows, exports from the U. K. have grown considerably,

reaching around 40 Kt by 1980 (which is some 20 per cent of domestic

production). The trade consists mainly of fresh-lamb sales to other

EEC countries, and results from the large, but decreasing price dif

ferentials (Volans, 1975).

Around 4 Kt per year is exported to non-EEC countries, but the

majority of U. K. exports have gone to France, when their import

regulations permitted (see Section 3). Since the advent of the EEC

Sheepmeat Regime in 1980, and the application of a Clawback Tax

(Blyth, 1981), exports to EEC countries have been at reduced levels.

Moreover, the strength of the £ sterling against the French franc,

discouraged exports, resulting in heavier supplies on the domestic

market.

The outlook for U.K. exports is uncertain, depending, among

other things, on the future arrangements of the Sheepmeat Regime, the

strength of the £ sterling and opportunitie s in the U. K. market (MLC,

1981 ).

2.4.2 Imports

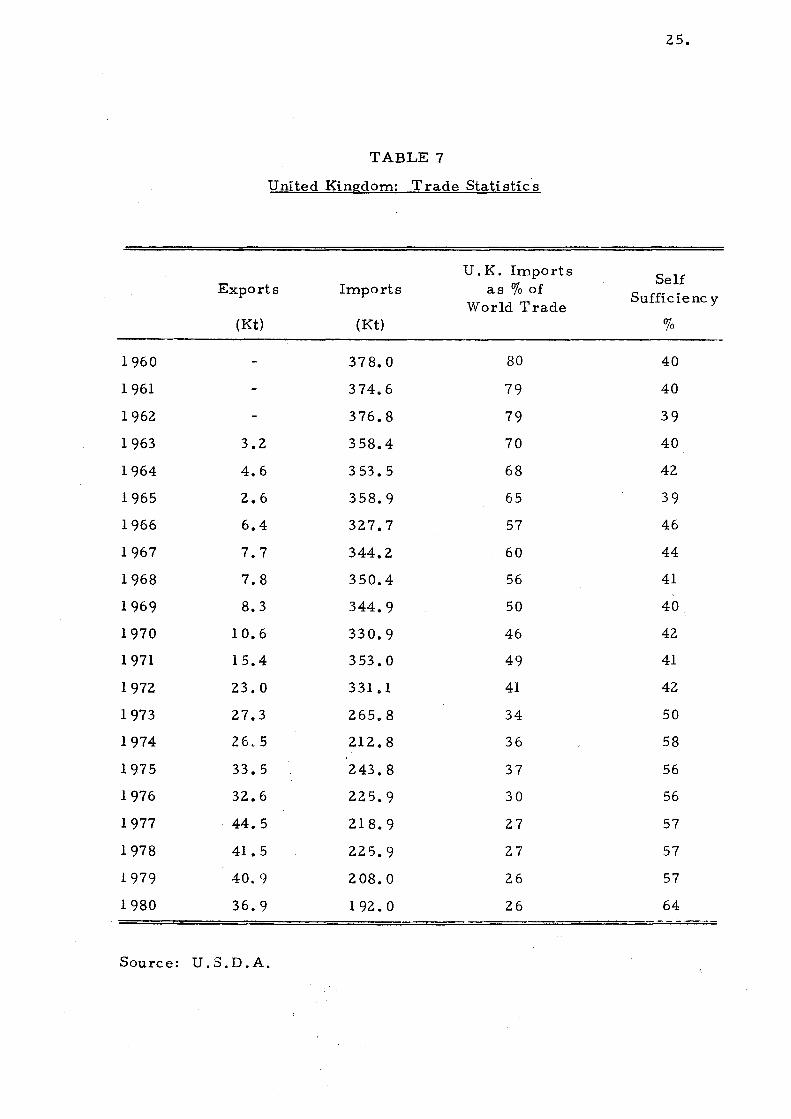

Despite its large domestic production, the U.K. is dE;!pendent on

overseas supply for nearly 50 per cent of consumption (Table 7). This

depe nd enc e is declining as consumption falls (Figure 1) sel£- su££icienc y

rose from 40 per cent in 1960 to 64 per cent in 1980.

24.

The U. K. is still the largest sheepmeat importer in the world;

its imports accounted for 80 per cent of world trade in the 1960's but

only 26 per cent in 1980 (Table 7). The reduction has been caused by

an increase in world trade between other countries, as well as a

decrease in U. K. imports. U. K. imports have declined from 1960-80

by 40 per cent 1. e. from 378 Kt in 1960 to 220 Kt in 1980, a decline

of 2 per cent per annum. As consumption has also fallen, imports

still form a major part of total supply. The U. K; is by far the most

important trader in the EEC, and in 1980 imported 67 per cent of

total EEC sheepmeat imports (thi s has declined, from 75 per cent

in 1975). Imports of fresh and chilled lamb (mainly from Ireland)

coincide closely with production of domestic lamb, and is seen by

the consumer as a similar product: it therefore compete s directly

with domestic supply. This trade has virtually ceased, however,

since 1974.

Frozen imports from the southern hemisphere arrive in the

U. K. when domestic production is low, so act as a complement,

encouraging year - round purc hases. British consumer s gain from

the seasonal production in both regi/0ns and the trade is traditionally

important for producers in both areas. The U. K. still accounts for

40 per cent of the World's lamb trade.

N. Z. is responsible for 95 per cent of imports, which consists

mainly of lamb. and Australia for the other 5 per cent, which is

mainly mutton. Up to 1968 Argentina supplied up to 15 per cent of

imports; this trade has ceased for health reasons - and the small

trade with Ireland has been directed to more profitable EEC markets

(Table 8).

The composition of imports has changed. Frozen mutton was

purchased in the 1960's, from the smaller suppliers. As incomes

have risen, higher quality meat is purchased and the majority of

imports is now lamb (200 Kt), from N.Z.

25.

TABLE 7

United Kingdom: Trade Statistics

U. K. Imports Self

Exports Imports as % of Suffic ienc y

World Trade (Kt) (Kt) %

1960 378.0 80 40

1961 374.6 79 40

1962 376.8 79 39

1963 3.2 358.4 70 40

1964 4.6 353.5 68 42

1965 2.6 358.9 65 39

1966 6.4 327.7 57 46

1967 7.7 344.2 60 44

1968 7.8 350.4 56 41

1969 8.3 344.9 50 40

1970 10.6 330.9 46 42

1971 15.4 353.0 49 41

1972 23.0 331.1 41 42

1973 27.3 265.8 34 50

1974 26.5 212.8 36 58

1975 33.5 243.8 37 56

1976 32.6 225.9 30 56

1977 . 44.5 218.9 27 57

1978 41. 5 225.9 27 57

1979 40.9 208.0 26 57

1980 36.9 192.0 26 64

Source: U .S.D.A.

26.

TABLE 8

U ni ted' Kingdom: Im9orts, by: Source

(Kt)

N.Z. Australia Other 1

Total

Weight % Weight % Weight % Imports

1960 305 81 28 7 45 12 378

1961 294 78 27 7 55 15 375

1962 296 78 19 5 62 17 377

1963 289 81 29 8 38 11 358

1964 297 84 29 8 30 8 353

1965 299 84 30 9 28 7 357

1966 266 85 12 4 35 11 312

1967 315 88 10 3 33 9 358

1968 318 91 18 5 14 4 350

1969 317 89 28 8 10 3 355

1970 294 89 34 10 3 1 331

1971 319 90 25 7 9 3 353

1972 289 87 27 8 15 5 331

1973 244 91 16 6 7 3 267

1974 204 96 8 4 1 213

1975 234 96 8 3 2 1 244

1976 214 95 12 5 226

1977 213 96 5 4 1 219

1978 214 95 12 5 226

1979 200 96 8 4 208

1980 184 96 5 3 3 1 192

Source: ABS, NZMPB

1 Mainly Argentina to 1968: also Ireland.

FIGURE 1

U. K.: Sheepmeat market trends, 1960-80

Kt i 700 j

'I i

600

500

400

300

200 I

100..!

I ---r---r---r--- --.-~--. ,-- ---I

1960 65 1970 75

, Consumption

Production

Imports

1980

N -J

28.

The contraction of the market has been borne by all the

suppliers; N.Z.'s expot"ts fell from 300 Kt in 1960 to 200 Kt in

1980; Australia's exports fell by half, to 12 Kt. The se two have

maintained their market-shares, whilst supplies from others

have virtually ceased (Table 8).

For N. Z., the U.K. is still its major market, despite

attempts to diversify sales of lamb to other markets. Develop

ments in the U.K. in terms of either prices or import volumes

are of great significance, therefore, to N. Z.

There is still a small trade in live sheep from Ireland,

of 0.5 million head per annum mainly for breeding purposes.

As the U. K. is such an important market in terms of world

sheepmeat trade, prices at Smithfield have the effect of determin

ing prices elsewhere in the world (Meat Producer, Vol. 8 (1),

1979), though recently events in other markets (e. g. Russia, Iran)

ha ve had an effect on the U. K. import pric e.

The outlook for imports (FAO, 1979; MLC, 1981) is for a

further slight decline, withan increase in domestic output caused by

rising prices under the EEC Sheepmeat Regime and a further

decline in consumption. Exports may also increase (MLC, 1981)

so net imports will be down to 140-150 Kt by 1985, with the majority

supplied by N. Z.

Despite this decline, the U.K. will continue to be the world's

largest sheepmeat importer, and N. Z. 's main customer for some

time to come.

3. FRANCE

3.1 Production

France is the EEC's second largest sheepmeat producer, produc

ing 25 per cent of the total supply. Even so, sheep farming is not of

great importance in France, contributing 2 per cent of total agricultural

revenue and less than 3 per cent of total meat production.

However, sheep numbers have increased over the period 1960- 80 from

8 to 11 million, and sheepmeat production has increased over 60 per

cent from 114Kt to 175 Kt (Table 9).

Sheep are produced both for meat and milk in France, according

to the regional climate. Meat is the main product for which sheep are

kept, but in the Massif Central, and parts of South East France they are

kept mainly for milk. Charlet (1973) discusses the regional character

istic s and trends in sheep farming. There has been an increase in sheep

numbers in the South West, which was traditionally associated with the

production of beef and dairy products; the various enterprises are now

run as complements (CEC, 1973). Sheep folding systems have developed

on these farms, which are usually small units (MLC, 1977). On the

larger units the "open-air" system predominates, which is similar to

the U . K. lowland systems. Various other management methods are

common; these are discussed in detail by Kelly (1977,1978); SCEES (1975),

IFOCAP (1978); CEC (1973), and OECD (1980).

Sheep farming is becoming concentrated in marginal agricultural

areas: 75 per cent of the flock are in regions covered by the EEC Directive

on less-favoured areas, so though there are already a few specific aids

to sheep farmer s (see CEC, 1977; Le Bihan, 1973; Mini st~re de l'Agriculture,

1970) the y also benefit from regional support measure s. Even if market

prices were to fall substantially under the Common Sheepmeat Regime,

it is unlikely that production would decline, as provision is made for

29.

3 O.

paying a premium to high cost producers, and giving income support.

F AO (1979) projections to 1985 are for an increa se in sheep

numbers to 13 -14 million, but due to lower offtake rates domestic

production is projected to be similar to 1980 levels of 152 -163 Kt

(which excludes the slaughter of live imports). More recent projections

(MLC, 1981; Boutonnet, 1981) take into account the effects of the EEC

Sheepmeat Regime, and predict a higher output of 170 Kt by 1984/85,

but that thi s will decline to 160 Kt by 1990.

3.2 Consumption

Though per capita consumption of all meats is high (104 kg), Table

10 show s that sheepmeat consumption is relatively small at 3.5 kg.

However, consumption of all types of meat, including mutton and lamb,

increased 50 per cent in 1960-80, so sheepmeat is maintaining its mar

ket share. As the population is some 54 million, total consumption

is large, at 210 Kt. With increasing per capita consumption, and a

population growth rate of 0.6 per cent, total sheepmeat consumption

increased 93 per cent in 1960- 80.

The general requirement is for lean meat from young lambs; in

urban areas even lighter carcasses are preferred, as lamb is a luxury

meat and consumption is concentrated in these high-income areas.

However, at traditional festhral times lamb is consumed by a large

proportion of the population. Mutton is consumed on a more regular

basis by some migrant groups, particularly those from North Africa

(MLC, 1977; Farmers Weekly, 7.3.80).

Apart from these traditional attitudes influencing consumption,

regional variations are marked (MLC, 1977; Kelly, 1978), and the

seasonal variation in demand is even greater than in the U. K. Several

econometric studies have attempted to estimate the strength of price

31.

TABLE 9

France: Produc tion Stati stic s

1,2 All meat Sheepmeat as Sheep Slaughter Production Production % all meat

(000 head) (Kt) (Kt)

1960 8,942 6,870 114.0 3,589 3.1

1961 9,063 6,750 112.0 3,760 2.9

1962 8,924 6,570 109.0 3,921 2.7

1963 8,945 5,908 99.4 3,859 2.5

1964 8,626 6,119 104.9 3,850 2.7

1965 8,821 6,567 112.9 4,020 2.8

1966 9,056 6,889 118.5 4,100 2.8

1967 9,186 7,023 121.0 4,339 2.7

1968 9,510 6,788 119.6 4,437 2.6

1969 9,794 6,583 116.5 4,285 2.7

1970 10,037 6,887 120.1 4,428 2.7

1971 10,239 7,564 132.3 4,639 2.8

1972 10,115 7,543 133.6 4,584 2.9

1973 10, 1 91 7,516 133.3 4,663 2.8

1974 10,104 7,713 137.6 5,11 0 2.6

1975 10, 509 7,611 138.5 5,102 2.7

1976 10,803 8,465 154.9 5,245 2.9

1977 11,046 8,273 133.5 5,151 2.9

1978 11 ,415 8,522 156.5 5,309 3.2

1979 11,640 9,194 171.0 5, 581 3.0

1980 11 , 739 9,500 1 75.0 5,750 3.0

Source: U. S. D. A.

1 Includes slaughter of live i.mports of approximately 8 Kt carcass equivalent.

2 Average dressed carcass weight of 18 kg.

32.

TABLE 10

France: Consumption Stati stic s

Population Sheepmeat Consumption

Per Capita cons' n

Sheepmeatas (tnillion) Total(Kt) Per Capita (kg) all meat (kg) % all meat

1960 45.6 118.0 2.6 76.9 3.3

1961 46.1 115.3 2.5 78.9 3.1

1962 46.9 115.5 2.4 80.3 3.0

1963 47.9 111. 0 2.3 80.9 2.8

1964 48.2 11 7.6 2.4 82.3 2.9

1965 48.7 126.9 2.6 84.4 3.0

1966 49.1 134.0 2.7 86.0 3.1

1967 49.5 138.0 2.8 88.7 3.1

1968 49.9 139.4 2.8 90.6 3.0

1969 50.3 144.2 2.9 90.7 3.1

1970 50.7 151.0 3.0 91. 9 3.2

1971 51.2 163.4 3.2 93.3 3.4

1972 51.7 172.6 3.3 94.4 3.5

1973 52.1 180.0 3.5 95.0 3.6

1974 52.5 181.1 3.5 97.5 3.5

1975 52.7 189.8 3. '6 99.3 3.6

1976 52.9 195.8 3.7 101.6 3.6

1977 53.1 199.2 3.7 104.3 3.5

1978 53.3 202.3 3.8 106.5 3.5

1979 53.5 207.5 3.9 108.9 3.6

1980 53.7 216.0 4.1 111. 0 3.7

Source: U.S.D.A.; U.N.

and income effects on sheepmeat demand (Kelly, 1978; Fouquet, 1970,

1973; Laloux, 1968; Faure, 1967; Boutonnet, 1976). All the studies

conclude that the main factor causing changes in per capita .demand for

mutton and lamb is level of incomes. The strong income effect shows

the luxury nature of the product; the income elasticity of demand is

estimated to be 0.6 for mutton (F AO, 1971), 0.9 - 1.15 for mutton and

lamb (CEC, 1977; Kelly, 1978) and 1.35 for lamb (Laloux, 1968).

33.

The studies suggest that price is not so important in determining

consumption, though estimates of the own-price elastici ty of demand all

lie between -0.57 and -0.87. Cross price elasticities were generally

extremely low, implying that prices of other meats have little effect on

sheepmeat consumption.

However, given an own-price elasticity of demand of -0.6, there

could be a marked increase in consumption after 1980 under the common

EEC sheepmeat p0lic y if market price s were harmoriised wi th other EEC

market prices. In theory this should happen by 1984/85 as other EEC

countries are given greater access to the market, and the increased

supplie s cause prices to fall substantially. In practice this is unlikely

to occur, as the mechanisms of the Regime protect the French market

from such declines in market price (Blyth, 1980).

Thus, any price changes will be minimal as the Intervention

system sets a base price in the market. Change s in income too, are

likely to have little effect during the 1980's, as real per capita incomes

are tending to stagnate, or even decline. FAO (1979) predict that sheep

meat consumption will therefore not change up to 1985, with a per capita

consumption of 3.7 - 3.8 kg, giving a t'::>tal demand of 200-210 Kt. Boutonnet,

1981 predicts, however, that imports will rise slightly and consumption

will be between 205-225 Kt in 1984/85, and rise to 230 Kt by 1990. The

MLC (1981) predict a much higher level of consumption, of 265 Kt in

1985 because of higher levels of French production.

34.

3.3 Prices

French lamb prices which are among the highest in the EEC, follow

their own seasonal pattern (NZMPB, 1978), with spring lamb fetching a

premium due to the special Easter demand when supplies are lowest; prices

then fall as supply becomes more plentiful. Lamb prices are not greatly

affected by the price of other meats, but tend to be higher than beef, and

even veal prices (MLC, Vol. 3, 1979).

Imports of fresh and chilled lamb command the same price as the

domestic prod.uct at retail and wholesale levels. It is difficult to estimate

the relationship between the price of frozen imports and fresh lamb, due

to import restrictions which allow only small quantities of frozen meat

to be sold in France. It appears though (NZMPB, 1978) to be discounted

heavily, especially at the wholesale level, against the fresh product.

Though consumer prices have in the past been about 65 per cent

higher than U. K. and Iri sh prices, the differenc e is narrowing gradually,

as greater trade takes place between them. However, whilst it is intended

that producer prices in the EEC will be harmonised by 1984/85, consumer

prices will continue to vary. French market prices cannot fall below a

base level set by the Intervention system, whereas U. K. market prices

are free to fluctuate above or below this level according to the market

si tuation.

3.4 Trade

Self- sufficienc y levels fell through the 1970 I s, as imports increased

from 4 Kt in 1960 to 46 Kt in 1978 (Table 11, Figure 2).

Only a small volume of imports are from non-EEC countries (6 Kt);

the main trade (90 per cent) comes from within the community, at 40-50 Kt

(Table 12). This trade consists of traditional exports from U.K., Ireland

and the Netherlands, and unexpectedly, since 1975 exports from Germany

35.

which is now France IS third largest supplier. Much of the German

lamb consists of re-exports from Ireland and the U.K., which avoids

French import controls on these countrie s I lamb. Sinc e the introduc

tion of the EEC Sheepmeat Regime, and the removal of controls, direct

trade with the U.K. has resumed, albeit at reduced levels, and the

indirect trade, through West Germany has virtually ceased.

Because of the lower seasonal variation in production, imported

lamb holds a different complementary relation to that in the U. K. Of

the three categories of trade, imported fresh and chilled lamb, and

animals imported live for fattening and slaughter, both tend to compete

directly with domestic production. But imported frozen lamb tends to

complement other sources of supply by appealing to the lower-income

consumer and supplying the catering and institutional market.

Most of the trade from EEC countries is in fresh and chilled meat;

third country trade is mainly frozen meat from Argentina, N. Z. and

Australia, though the U.K. appears to be taking over this market too

(Table 12). Live imports account for about a quarter of sheepmeat

imports and come from the Netherlands, West Germany and East

Europe (Boutonnet, 1981).

Despite the relationship between frozen imports and domestic

supply, imports of frozen sheepmeats have been severely limited by

quantitative re strictions since 1931 (HMSO, 1935). All third -country

imports up to 1980 faced the 20 per cent ad valorem tariff and a vari

able import-licence fee was payable, based on the difference between

the world price and the French Ilthreshoid II price for fresh and chilled

lamb (MLC, 1977).

In 1978, a trading agreement was made with Ireland to regulate

trade between them as a preliminary move towards free trade under

the CAP (Kelly, 1978; Wood, 1979). To regulate trade with N. Z. a

36.

TABLE 11

France: Trade in Sheepmeats

Total Imports Sel£- sufficienc y Kt 0/0

1960 4 97

1961 5 97

1962 7 95

1963 12 89

1964 13 88

1965 1 5 89

1966 16 87

1967 17 86

1968 20 84

1969 28 77

1970 31 77

1971 31 80

1972 39 75

1973 47 71

1974 44 73

1975 52 69

1976 42 75

1977 47 77

1978 46 77

1979 42 81

1980 38 83

Source: U.S.D..A.

TABLE 12

France: Trade in She!i:lilroeats

lm:!;lorts l!~ So~rce (Kt: Per cent)

Year U.K. Netherlands W. Germany Ireland Argentina N.Z. Australia Belgium 1

Other'

9.0 Volume

1970 9.2 2.3 4.1 2.9 3.5

1971 11.6 9.9 2.6 2.5 2.1 0.2 1.1 0.01 2.3

1972 16.8 9.2 2.1 4.6 1.9 1.2 1.2 0.06 2.2

1973 25.1 8.3 1.8 4.8 2.3 1.1 0.3 0.01 2.4

1974 23.1 12.7 1.9 2.8 1.7 0.4 0.1 0.02 0.2

1975 25.3 14.2 5.4 2.6 2.1 0.7 0.04 0.06 0.1

1976 15.8 13.9 8.4 1.2 1.1 0.5 0.4 0.01 0.1

1977 19.3 14.0 7.9 1.8 1.1 1.3 0.4 0.4

1978 8.7 12.4 8.6 14.2 0.2 1.6 0.3

1979 4.4 12.9 8.9 12.9 0.2 2.5 0.2

1980 4.1 14.0 6.2 13.8 0.1

Year ~o Qf TQta.1 1970 30 30 13 11

1971 37 32

1972 43 23 12

1973 53 17 10

1974 52 29

1975 48 27 10

1976 37 33 19

1977 40 30 17

1978 19 26 18 31

1979 10 32 22 32

1980 11 44 16 42 ..., -.J

Source: EUROSTAT 1 Other = Italy, Spain, Hungary, Morrocco, China ( - ) =Jmports less than 10%, Or negligible volume

Kt ~

200 1 I

I 75 ~

150 1 12 5 ~

100

75

50

25

1960

FIGURE 2

France: Sheepmeat market trends, 1960-80

65 1970 75

Consumption

Imports

1980

\.>l 00 •

39.

partnership was set up between French and N. Z. producers, who formed

a company, FRANZIM', to act as the sole agent for N. Z. lamb and

mutton imports into France, under the global quota system (for details,

see MLC, 1977).

Following the introduction of the EEC Sheepmeat Regime, re stric

tions on imports from other EEC states were removed, and third-country

imports are controlled by the Voluntary Re straint Agreements and a

10 per cent import tariff.

However, imports have not increased rapidly, as the Clawback

Tax, and the strength of the £ sterling against the French franc have

discouraged EEC exporters.

The future of the import demand for sheepmeat relies largely on

the effects of the Sheepmeat Regime, and the effect that resulting price

changes have on supply and demand.

Various scenarios for the future have been presented by several

researchers (Brabyn, 1975; Boutonnet, 1976, 1981; IFOCAP, 1978;

Kelly, 1977, 1978; MLC, 1981), based on possible future market and

producer prices, changes in the mechanisms of the Regime and probable

values of the £ sterling. These studies conclude that trade will be

between 45- 55 Kt, by 1985, and ri se to 90 Kt by 1990.

F AO (1979) also estimate that the import demand in 1985 will be

50 Kt, which accounts for price-effects under a free (EEC) market.

The amount of this which non-EEC countries can expect to supply is

small. Increasing trade will take place with other EEC states, the

majori ty coming from the U. K., though the mechani sms of the CAP

prevent excessive imports from the U. K. being sold on French markets.

The main effect on third country suppliers, therefore, is the indirect

effects on the U. K. market. In general, the greater the volume of U. K.

40.

exports, the stronger is the U.K. domestic market, and the greater

is its ability to absorb third-country imports at reasonable prices.

There may, however, be opportunity for direct expansion of sales

in France, given adequate promotion and advertising, and the availa

bility of meat of a quality required by the French housewife.

4. IRELAND

4.1 Production

The sheep flock in Ireland has alwa ys been a small, but important

feature of agriculture, providing around £27 million a year (1980) or

3 percent of agriculture revenue.

Production is generally treated as a secondary enterprise on low

land farm.s; so there are many farmers who have sheep, but relatively

few specialise in sheep farming. The majority of the 2.5 million sheep

a:re in the counties Galway, Mayo, Roscommon and Wicklow - all areas

covered by the EEC Directive on less-favoured areas. This could have

important long-term effects, as production incentives are given to

farmers, to raise and support their incomes at common-market standards.

Sheepmeat production is not an important enterprise compared to other

meats (Table 13). The proportion has declined from 10 per cent to 4 per

cent over the period, as both beef and pork output rose substantially.

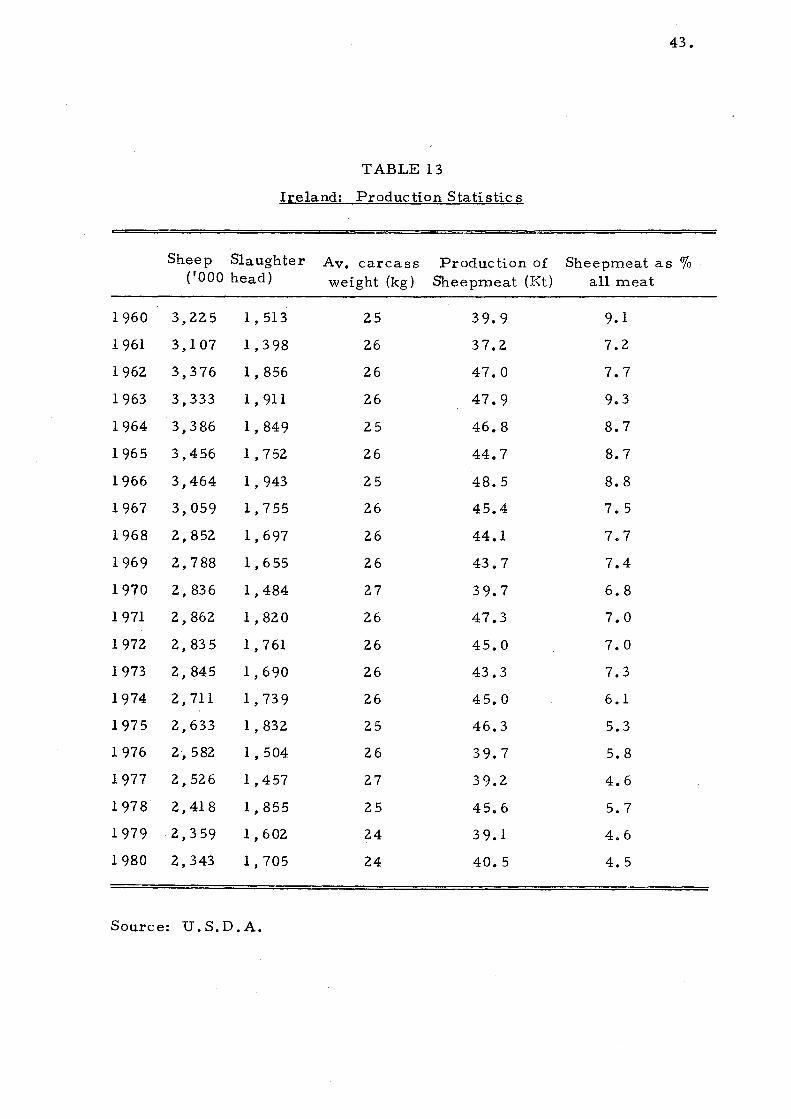

Since 1960 there have been considerable changes in the Irish sheep

flock (Riordan, 1981). Sheep number s have fallen from 3.5 million in

1960, to 2.5 million in 1980 (Table 13), though in anticipation of member

ship of the EEC, and subsequent acces s to larger markets, farmers

expanded sheep numbers after 1970 with Government assistance. However,

in the first year of Community membership (1974), slaughtering increased

in response to higher meat prices, and sheep numbers again fell, at 4 per

cent per annum up to 1980.

At the same time there were significant changes in both the location

and composition of the national flock. Lowland flock numbers fell, and

hill-flocks expanded - they virtually equalised by 1980. The breed com

position has changed in favour of the hill breeds such as Scottish Blackface,

Cheviots, and Leitrim. How much of this change can be attributed to the

41.

42.

impact of the Mountain Sheep Subsidy Scheme (1966) and later, the

EEC Livestock Headage Schemes is assessed elsewhere (Fingleton,

1978). Another factor determining the change has been the relatively

low and fluctuating returns from sheep farming: farmers have continued

to invest in other enterprises in the lowlands with more secure markets

covered by the CAP.

In the longer term, output could be doubled from the mountain

regions (IAI, 1977), whilst further expansion in the lowlands would be

at the expense of cattle or crops (Mosse, 1978). Currently the efficienc y

of production is lower in Ireland than in the U. K., but simil ar to France

(according to calculations made by Kelly, 1978). The move to hill-breeds

coupled with other regional problems, is causing a decline in productivity

(Fingleton, 1978).

However, sheepmeat production has not fallen greatly since 1960.

Slaughterings have been high, at around 1.6 million. There was a sharp

rise of 27.4 per cent in 1977/78 in response to demand from France,

but a fall in 1979. Production also rose in 1977/78 in response to higher

price s, then fell back to previous levels of 40 Kt, in 1979. Production

has fluctuated around this level since 1960, with a slight down-trend

(Table 13, Fig. 3).

Average carcass weights, at 27 kg, tend to be heavier than most

sheep producing countries; this is the type of meat required by the Irish

consumer, and is well-suited to the production systems prevailing in

mountain regions.

Changes in producer prices could have a considerable effect on

production: a study by Kelly (1978) looks at the long-term effects of

increasing prices resulting from the EEC. After 1977 sheepmeat should

have been freely-tradeable within the Community, but barriers still

existed up to 1980. To prevent unacceptably large changes in the system

43.

TABLE 13

Ireland: Production Statistic s

Sheep Slaughter Av. carcass Production of Sheepmeat as % ('000 head) weight (kg) Sheepmeat (Kt) all meat

1960 3,225 1,513 25 39.9 9.1

1961 3,107 1,398 26 37.2 7.2

1962 3,376 1,856 26 47.0 7.7

1963 3,333 1,911 26 47.9 9.3

1964 3,386 1,849 25 46.8 8.7

1965 3,456 1, 752 26 44.7 8.7

1966 3,464 1,943 25 48.5 8.8

1967 3,059 1,755 26 45.4 7.5

1968 2,852 1,697 26 44.1 7.7

1969 2,788 1,655 26 43.7 7.4

1970 2,836 1,484 27 39.7 6.8

1971 2,862 1,820 26 47.3 7.0

1972 2,835 1, 761 26 45.0 7.0

1973 2,845 1,690 26 43.3 7.3

1974 2, 711 1, 739 26 45.0 6.1

1975 2,633 1,832 25 46.3 5.3

1976 2,582 I, 504 26 39.7 5.8

1977 2,526 1,457 27 39.2 4.6

1978· 2,418 1,855 25 45.6 5.7

1979 2,359 1,602 24 39.1 4.6

1980 2,343 1,705 24 40.5 4.5

Source: U. S. D. A.

44.

an Agreement for trade with France was negotiated. This led to

higher prices in Ireland and increased export demand which stimulated

expansion in the short-term. Given this continuing financial incen

tive, and .structural re~adjustment, former output levels

could be ac hieved. As past production and stocking levels indicate

the potential for expansion exists and not necessarily at the expense

of other meat production, as it would be in hill areas which are only

suited to sheep farming (MLC, 1981). Under the EEC Sheepmeat

Regime a differential support-price mechanism operates which is

designed partially to give this incentive to Irish producers. This

Intervention system guarantees producers' returns at a relatively

high and increasing level (80 per cent of the French price in 1980/81),

and producer prices will be aligned with the considerably higher EEC

prices by 1984/85.

Projections for output in 1985 made by FAO (1979) estimate an

increase to 50 Kt. This implies a rather high growth rate of 5.8 per

cent per annum, though this is confirmed by Fingleton (1978). A

more recent projection made in the light of the prices set by the EEC

(Riordan, 1981) is somewhat lower than this, with estimated produc

tion of 32-38 Kt, in 1985 which is also below production levels in

1980.

4.2 Consumption

Trends in food consumption in Ireland for many years have been

towards a higher quality diet, rather than one providing a higher cal

orie intake. The trend has been towards animal products and away

from the staples of potatoes and vegetables.

Sheepmeats have always been an important part of the diet, and

per capita consumption is high at 11 kg, the highe st in the EEC

(Table 14). The population of Ireland is small (3 million) and growing

45.

at a rate of only. 02 per cent per annum. Hence, total consumption

of sheepmeats is relatively stable at around 32 Kt (Table 14).

Since Ireland joined the EEC in 1974, however, with rising

incomes consumption had started to rise slightly, peaking at 35 Kt

in 1975/76. Rising prices, though, have had a strong effect and in

the opposite direction, causing a steep drop in consumption after

1977. Levels in 1980 are virtuall y the same a s in 1960. An own

price elasticity of demand of -1.96 has been estimated (Riordan, 1981).

Compared to consumption of all meats, sheepmeat was important

(17 per cent in 1960), but as more beef and pork has been consumed,

the proportion has fallen to 10 pel cent in 1980 (Table 14). No estimates

of cross-price elasticities are available.

As mentioned above, demand for sheepmeat tends to incre;ase

as incomes rise; expenditure on mutton and lamb is greatest amongst

the upper income groups, though mutton is sti1l an inferior good.

Kelly (1978) cites income elasticities of demand which have

been calculated by several authors. The estimates showed that

the income elasticity of demand for sheepmeat is fairly constant

over time, and lies between 1.14 and 1.63. The studies which

differentiate between mutton and lamb show that the income elasti

city for mutton is well below unity, ranging from 0.4 to 0.65, whereas

that for lamb is greater than unity. This is evidence of the 'luxury'

nature of lamb as opposed to mutton, as increasing incomes lead

to more than proportionate increases in expenditure on lamb"

The outlook for sheepmea t consumption in Ireland is fairly

stable; current levels of total demand are likely to continue as the

effects of rising incomes and small increases in popula tion will

be off- set by rising price effects.

46.

TABLE 14

Ireland: Consumption Statistics

Population Sheepmeat Consumption

Sheepmeat as 0/0 (million) Per Capita (kg) 'I' otal (K t) all meat consumed

1960 2.84 10.6 29.8 17.0

1961 2.81 11.2 31. 7 16.9

1962 2.82 11.4 32.2 16.8

1963 2.84 11.1 31. 8 15.9

19"64 2.86 11.2 32.0 16.6

1965 2.87 10.8 30.5 15.0

1966 2.88 10.7 31.1 14.6

1967 2.90 11.0 32.0 14.6

1968 2.91 10. Q 31.4 14.0

1969 2.92 10.9 32.4 13.5

1970 2.95 10.8 32.8 13.0

1971 2.97 11.1 33.2 12.9

1972 3.01 10.9 33.2 12.7

1973 3.05 10.5 31. 6 12.3

1974 3.08 11.0 33.9 11. 9

1975 3.12 11.2 34.6 11.1

1976 3.16 10.5 32.4 10.8

1977 3.23 10.3 32.8 11.2

1978 3.27 9.5 30.4 10.1

1979 3.31 8.3 30.0 10.0

1980 3.37 7.8 26.0 10.3

Source: U. S. D. A., U. N.

47.

FAO (1979) project consumption to be 13-15 kg per head by

1985, given an income elasticity of 0.4. However, as the population

growth rate is actually Ie ss than the FAO figure of 1.2 per cent per

annum and because demand appears to be quite responsive to price

changes, per capita consumption is, and is likely to continue to be,

much lower than projected. A more recent study confirms this (Riordan,

1981 ): his prediction is for a 5 per cent decline in consumption from

1980, giving a per capita consumption of 7.4 kg by 1985, and a total

c 0nsumption of 18 Kt.

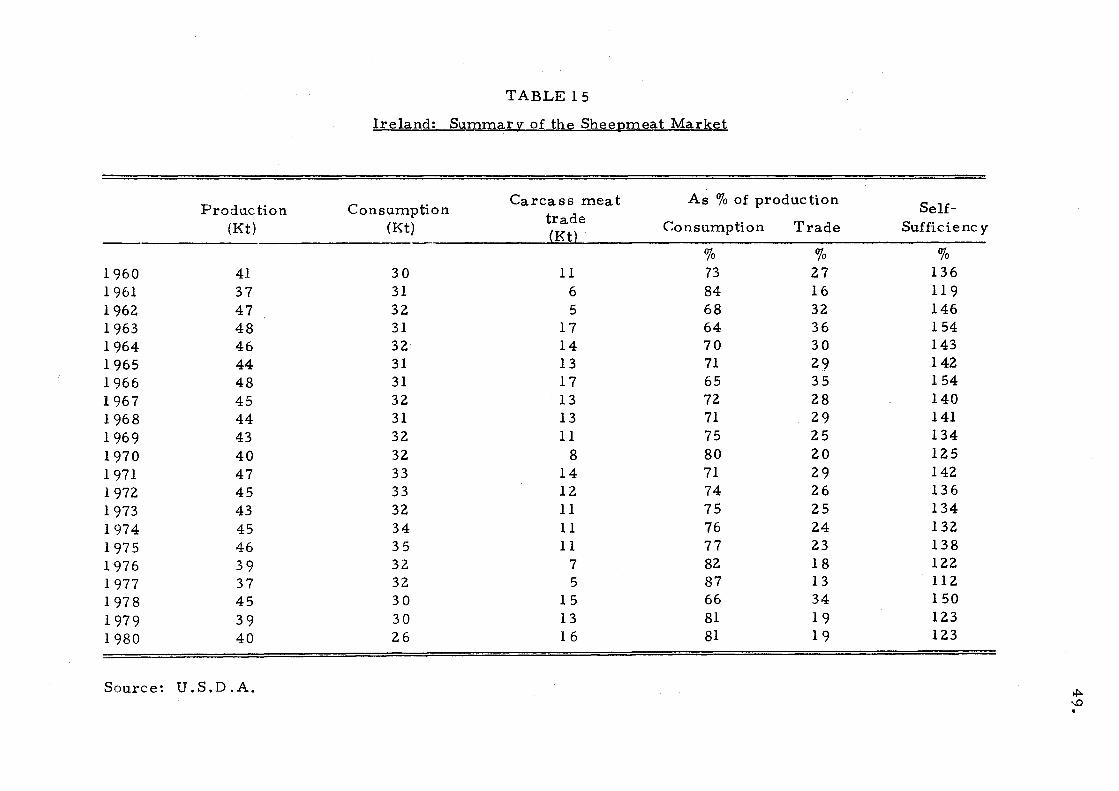

4.3 Trade

As self- sufficienc y has ranged from 112 per cent to 150 per cent

over the period (Table 15) a large proportion of production has been

available fo r export. Ireland is therefore the second large st exporter

in the EEC, although in terms of world trade, its share has declined

from 3 per cent to 1 per cent.

With consumption levels which are relatively stable, exports

fluctuate in line with production (Table 15, Fig. 3), and have varied

from 7 to 1 7 Kt ove r the period.

Prior to EEC entry, the most important measure to benefit Irish

agricultural exports was the Anglo-Irish Free Trade Area Agreement

made in 1966, which guaranteed unrestricted access to the U.K. market

for Irish store cattle and sheep. At the time, trade in live sheep with

the U.K. was important (details are given byMosse, 1978). It is not

likely to be SO in the future, as carcass exports have increased at the

expense of live sheep exports; for example, there was a 56 per cent

fall in live sheep trade in 1978, as carcass exports increased sharply.

During the 1960's exports were high, but steadily decreasing, as

production fell and consumption rose; exports fell even further in the

early 1970's and after Ireland joined the EEC.

48.

However, as EEC prices rose, a trading agreement between

France and Ireland was introduced in 1978 to prevent Irish sheepmeat

disrupting the French market. As a result of the bilateral deal, prices

to the producer rose and the difference between French and Irish

prices was only 12 per cent in 1980 compared to 45 per cent in 1976,

when Irish prices were roughly equal to U. K. prices.

France has always been cine of the main buyers; purchases by

Belgium/ Luxembourg, and Germany were important in the early 1970 I s

but have declined markedly (Table 16). Italy buys small quantities,

and Libya makes irregular, but often large, purchases.

Table 17 show s the importance of Iri sh expo-rts to each of the se

markets. Supplies were significant in Belgium/ Luxembourg, but they

now import from other suppliers. Imports into France have varied

widely: any change in their total imports is related to a change in imports

from Ireland. Libya, it seems, imports sheepmeat regularly, but only

buys from Ireland if the price is low. Irish supplies in other markets

are minimal, and possibly too small to affect trade flows or prices.

From the above scenario of production and consumption it appears

that Ireland has the potential to increase exports to the higher levels of

the mid 1960 I s (FAO, 1979; Riordan, 1981). Much of the trade (10-15 Kt)

is likely to be absorbed into other EEC states rather than be sold on the

lower-priced world markets.

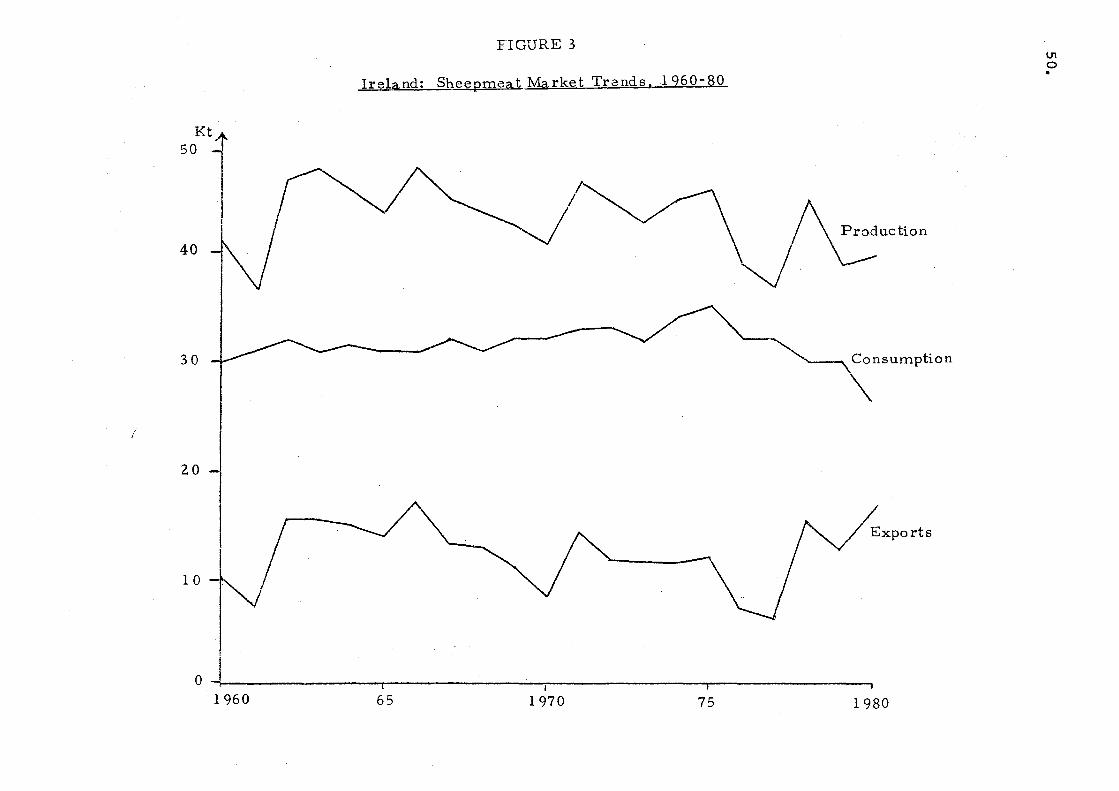

TABLE 15

Ireland: Summary of the Sheepmeat Market

Production Consumption Carcass meat As % of production

Self-(Kt) (Kt)

trade Consumption Trade Sufficienc y

{Ktl .

% % % 1960 41 30 11 73 27 136 1961 37 31 6 84 16 119 1962 47 32 5 68 32 146 1963 48 31 17 64 36 154 1964 46 32 14 70 30 143

1965 44 31 13 71 29 142 1966 48 31 17 65 35 154

1967 45 32 13 72 28 140

1968 44 31 13 71 29 141

1969 43 32 11 75 25 134

1970 40 32 8 80 20 125

1971 47 33 14 71 29 142

1972 45 33 12 74 26 136

1973 43 32 11 75 25 134

1974 45 34 11 76 24 132

1975 46 35 11 77 23 138

1976 39 32 7 82 18 122

1977 37 32 5 87 13 112

1978 45 30 15 66 34 150

1979 39 30 13 81 19 123

1980 40 26 16 81 19 123

Sourc e: U. S • D . A. ~ -.0 .

FIGURE 3

Ireland: Sheepmeai Market Trc nds, 1960- 80

50

Kti I I

40

30 "--- Consumption

\ /

20

Exports

I

o ~ I

1960 65 1970 75 1980

U1 o •

51.

TABLE 16

Ireland: Shee12meat EX120rts (b~ de stination)

(1974-80){fonnes)

1974 1975 1976 1977 1978 1979 1980

Belgium/Lux. 5,084 4,769 2,548 1,884 86 777

France 3,555 3,139 1.163 1,971 14,600 12,800 13,908

Germany 1,057 1,018 377 412 239

Italy 10 323 309 137 569

U .. K. 1,120 1,847 508 978 365 200 62

Libya 634 2,024 756 3

Total 11,116 11 , 658 7,273 6,396 15,190 13,000 15, 555

Source: CSO

TABLE 17

Irish SUP121~ as Percentage of Countr~ls Imports

1974 1975 1976 1977 1978 1979 1980

% % 0/0 % % % %

Belgium/Lux. 63.0 50.0 21. 0 3.0

France 8.0 6.0 3.0 4.0 31.2 30.2

Germany 8.0 5.0 1.2 1.4

Italy 2.1 2.4 1.1 1.0

U.K. 0.5 0.6 0.1

Libya 48.0 100.0 58.0

Algeria 51. 0

Source: Table 16, and U.S.D.A.

5. ITALY

5.1 Production

Sheep farming is not an important enterprise in Italy, even though

it is the third largest producer in the EEC, producing 7 per cent of the

Community's sheepmeat.

In the 1920's Italy had a stock of over 12 million sheep, with a

large export trade in live sheep; sheep numbers have now fallen to

8 million, and have been stable over the period 1960- 80 (Table 18).

Most of the sheep are in the southern part of the country and the trend

is towards further concentration in these areas,.(Ferrara, 1972;

Kelly, 1977; Cupo, 1979). However, over-concentration has led to an

inflexible supply response, due to the absence of alternative enter

prises in these marginal farming regions. Unless sheepfarming

becomes more profitable, relative to othe r activities, it is unlikely

to expand into the main areas of cultivation in the North.

The southern regions, Sardinia, Sicily and the Peninsula, con