1

jb

Fisher Center Real Estate ConferenceApril 22, 2013

Dean Wehrli, Vice President

2

2012 Was A Great Year

• Home Prices and SalesRates Were Up

• Giants won the World Series

• Stanford won the Rose Bowl

3

Northern California Price Appreciation Among the Best Nationally

• This is great news for private builders who need equity partners.

• This is also why the public builders are allocating capital to Northern CA

Source: John Burns Real Estate Consulting, Metro Analysis & Forecast, April 2013

4%

4%

5%

5%

6%

6%

6%

7%

7%

7%

7%

8%

9%

9%

12%

12%

13%

13%

14%

15%

16%

17%

22%

0% 5% 10% 15% 20% 25%

Atlanta, GA

Chicago, IL

Charlotte, NC-SC

New York, NY-NJ

Boston, MA-NH

Portland, OR-WA

Los Angeles, CA

Oakland, CA

Minneapolis, MN-WI

Tampa, FL

Seattle, WA

Washington D.C.

Dallas/Fort Worth, TX

Miami, FL

Denver, CO

Orange County, CA

San Diego, CA

Riv/San Bern

San Francisco, CA

Sacramento, CA

San Jose, CA

Las Vegas, NV

Phoenix, AZ

Burns Home Value IndexTM

(12-month Change)

4

Foreclosure Starts Trending Down to Normal through 2014

Distressed still an Issue, but less so all the time

5

Agenda

1. Market Trends Near You

2. The Big Creep

3. Pros and the Cons

6

Cycles

7

JBREC Housing Cycle Risk Index™ looks at4 major categories for fundamentals

I. Demand1. Total Buying Activity (New and Resale)2. Median Resale Price Appreciation3. Job Growth4. Population Growth5. Realtor Market Ratings

II. Supply6. Permit Trends7. Resale Listings

III. Affordability8. JBREC Affordability Index9. Home Equity 10. Mortgage Rates

IV. U.S. Economy

4 major categories, with 11 subcategories and 25 calculations

8

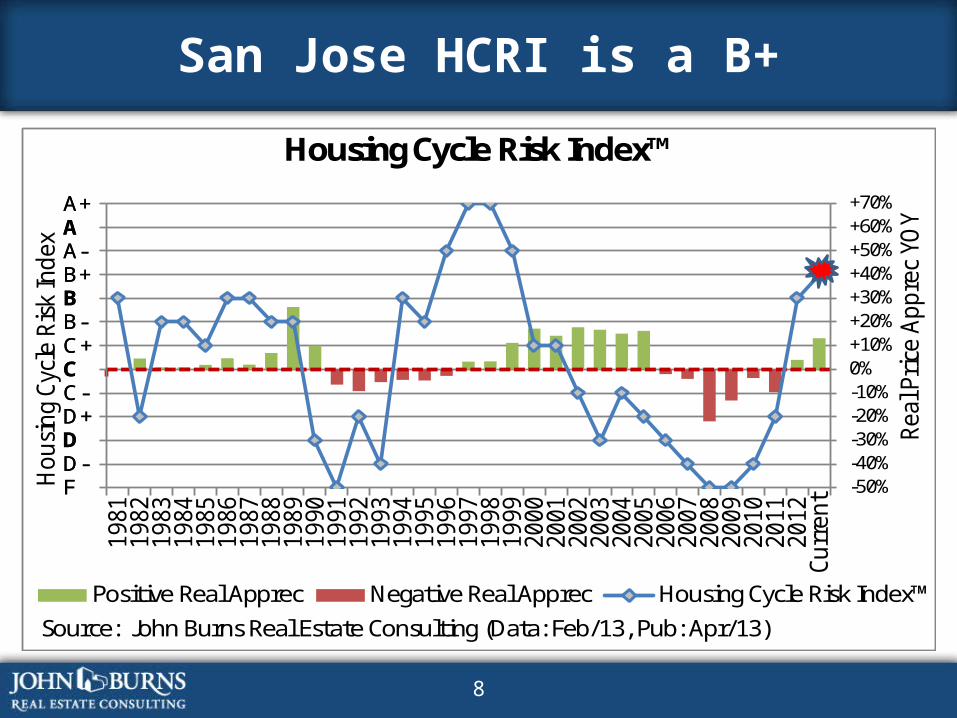

San Jose HCRI is a B+

-50%-40%-30%-20%-10%0%+10%+20%+30%+40%+50%+60%+70%

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Curr

ent

Hou

sing

Cyc

le R

isk

Inde

x

Real

Pri

ce A

ppre

c YO

Y

Positive Real Apprec Negative Real Apprec Housing Cycle Risk Index™

A+AA-B+BB-C+CC-D+DD-F

Source: John Burns Real Estate Consulting (Data: Feb/13, Pub: Apr/13)

A+AA-B+BB-C+CC-D+DD-F

Housing Cycle Risk Index™

9

-50%-40%-30%-20%-10%0%+10%+20%+30%+40%+50%+60%+70%

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Curr

ent

Hou

sing

Cyc

le R

isk

Inde

x

Real

Pri

ce A

ppre

c YO

Y

Positive Real Apprec Negative Real Apprec Housing Cycle Risk Index™

A+AA-B+BB-C+CC-D+DD-F

Source: John Burns Real Estate Consulting (Data: Feb/13, Pub: Apr/13)

A+AA-B+BB-C+CC-D+DD-F

Housing Cycle Risk Index™

San Francisco HCRI is a B+

10

-50%-40%-30%-20%-10%0%+10%+20%+30%+40%+50%+60%+70%

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Curr

ent

Hou

sing

Cyc

le R

isk

Inde

x

Real

Pri

ce A

ppre

c YO

Y

Positive Real Apprec Negative Real Apprec Housing Cycle Risk Index™

A+AA-B+BB-C+CC-D+DD-F

Source: John Burns Real Estate Consulting (Data: Feb/13, Pub: Apr/13)

A+AA-B+BB-C+CC-D+DD-F

Housing Cycle Risk Index™

Oakland HCRI is an A-

11

-50%-40%-30%-20%-10%0%+10%+20%+30%+40%+50%+60%+70%

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Curr

ent

Hou

sing

Cyc

le R

isk

Inde

x

Real

Pri

ce A

ppre

c YO

Y

Positive Real Apprec Negative Real Apprec Housing Cycle Risk Index™

A+AA-B+BB-C+CC-D+DD-F

Source: John Burns Real Estate Consulting (Data: Feb/13, Pub: Apr/13)

A+AA-B+BB-C+CC-D+DD-F

Housing Cycle Risk Index™

Sacramento HCRI is an A

12

Sales

13

San Jose new home sales growth through 2016 – but still below 2007 levels

Source: John Burns Real Estate Consulting, Metro Analysis & Forecast, April 2013

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,00019

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

12C

urre

nt20

13P

2014

P20

15P

2016

P20

17P

ANNUAL NEW HOME SALES

14

Oakland same story – new home sales to near 6,000 in 2016, but still below 2006

Source: John Burns Real Estate Consulting, Metro Analysis & Forecast, April 2013

0

2,000

4,000

6,000

8,000

10,000

12,00019

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

12C

urre

nt20

13P

2014

P20

15P

2016

P20

17P

ANNUAL NEW HOME SALES

15

Sacramento also better bit below the norm - INVENTORY

Source: John Burns Real Estate Consulting, Metro Analysis & Forecast, April 2013

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,00019

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

12C

urre

nt20

13P

2014

P20

15P

2016

P20

17P

ANNUAL NEW HOME SALES

16

Prices

17

Huge near-term appreciation in San Jose

Source: John Burns Real Estate Consulting, Metro Analysis & Forecast, April 2013

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Cur

rent

ANNUAL MEDIAN NEW HOME PRICE

16%

11%

6%

3%1%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2013P 2014P 2015P 2016P 2017P

New Home Price Appreciation Forecast

18

Milder but still strong in Oakland

Source: John Burns Real Estate Consulting, Metro Analysis & Forecast, April 2013

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Cur

rent

ANNUAL MEDIAN NEW HOME PRICE

9% 9%

6%

3%

1%

0%1%2%3%4%5%6%7%8%9%

10%

2013P 2014P 2015P 2016P 2017P

New Home Price Appreciation Forecast

19

Nowhere to go but up in Sacramento

Source: John Burns Real Estate Consulting, Metro Analysis & Forecast, April 2013

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Cur

rent

ANNUAL MEDIAN NEW HOME PRICE

16%14%

8%

4%

1%0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2013P 2014P 2015P 2016P 2017P

New Home Price Appreciation Forecast

20

New home share of total sales. Not the norm – below even the mid-1990s

Source: John Burns Real Estate Consulting, Metro Analysis & Forecast, April 2013

0%

10%

20%

30%

40%

50%

60%19

89

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Cur

rent

Sacramento Oakland San Jose Stockton Fresno

21

Monthly inventory levels – neither is this

Source: John Burns Real Estate Consulting, Metro Analysis & Forecast, April 2013

0

2

4

6

8

10

12

14

16

2005 2006 2007 2008 2009 2010 2011 2012

Sacramento Oakland San Jose Stockton Fresno

22

Agenda

1. Market Trends Near You

2. The Big Creep

3. Pros and the Cons

23

Nowhere worked

24

Call me if it’s in the core

25

Call Us

26

Please can we buy your land? Pretty please?

27

Agenda

1. Market Trends Near You

2. The Big Creep

3. Pros and the Cons

28

The Good

• Economy Picking Up: Knocking on wood.• Boomerang Buyers: Itching to get back into the

for-sale market.• Urgency Back: Prices not falling and how long will

these mortgage rates last? • Inventory: How low can it go?• Rising Prices: With a vengeance.• Rising Sales: But already supply constrained.

29

10% of 2013 demand from “boomerang” buyers

30

The “Concerning”

• Prices Rising: Low payments still, but price to income not great anymore.

• Mortgage Rates: Have to go up – and with them the payments to price ratio.

• Investors: Organic buyers often shut out. • Inventory: Resales inventory has to go up – the

chicken and egg phenomenon.• No Place to Build: We need to get lots to the

market.• Be Careful of the Hype: But a hot market will

eventually lead to mistakes.

31

The Big Re-Set

The Big Switch Flip

The Bi-Polar Market

32

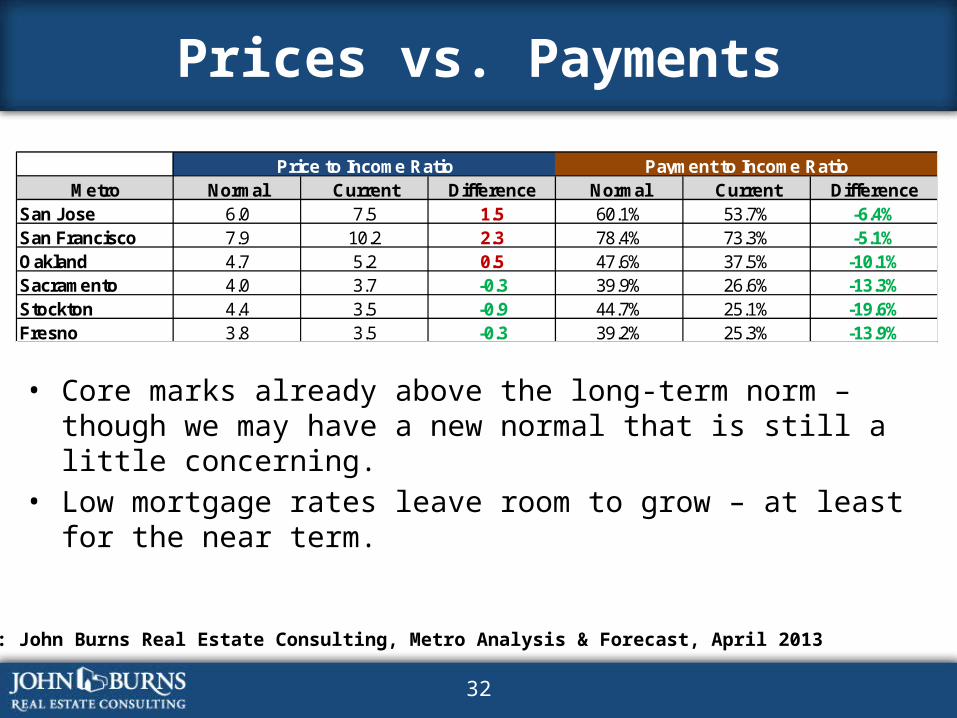

Prices vs. Payments

Metro Normal Current Difference Normal Current DifferenceSan Jose 6.0 7.5 1.5 60.1% 53.7% -6.4%San Francisco 7.9 10.2 2.3 78.4% 73.3% -5.1%Oakland 4.7 5.2 0.5 47.6% 37.5% -10.1%Sacramento 4.0 3.7 -0.3 39.9% 26.6% -13.3%Stockton 4.4 3.5 -0.9 44.7% 25.1% -19.6%Fresno 3.8 3.5 -0.3 39.2% 25.3% -13.9%

Payment to Income RatioPrice to Income Ratio

Source: John Burns Real Estate Consulting, Metro Analysis & Forecast, April 2013

• Core marks already above the long-term norm – though we may have a new normal that is still a little concerning.

• Low mortgage rates leave room to grow – at least for the near term.