1

Essential Question:Essential Question:Explain the goal of checking “Productivity;”

define input and output; list and describe fixed costs, variable costs, and marginal costs.

Making Production DecisionsMaking Production DecisionsSECTION 3

2

Productivity and producers:Productivity and producers:Productivity is the process of maximizing

the amount of output, while attempting to minimize the amount of input

Producers check productivity because: They want to see how efficiently resources are

being used. They want to ensure that there is as little waste

as possible.

Making Production DecisionsMaking Production DecisionsSECTION 3

3

Input/Output and the law of Input/Output and the law of diminishing marginal returns:diminishing marginal returns: Input- any resource (human/natural/capital)

that is addedOutput- the quantity of products produced

By increasing levels of input, output will increase. Eventually, adding input will result in lower output. This is the law of diminishing returns.

Making Production DecisionsMaking Production DecisionsSECTION 3

4

Total Product vs. Marginal Product:Total Product vs. Marginal Product:Total product- this is the total quantity of

goods or services you produce within a given period of time

Marginal Product- this is the change in total product that occurs when you add additional input (ex. Workers)

Making Production DecisionsMaking Production DecisionsSECTION 3

5

Increasing Returns/Decreasing Increasing Returns/Decreasing Returns/Negative Returns:Returns/Negative Returns: Increasing returns- means that as you add

input, output increases as wellDiminishing returns- means that as you add

input, output increases, but by a smaller amount each time

Negative returns- means that as you add input, output decreases

Making Production DecisionsMaking Production DecisionsSECTION 3

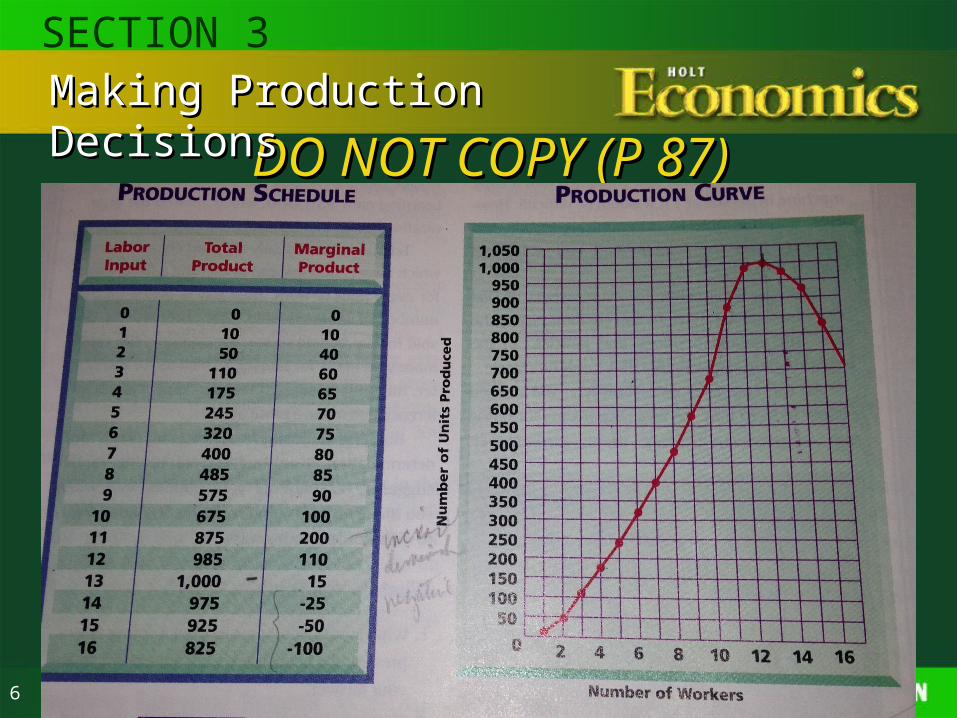

6

DO NOT COPY (P 87)DO NOT COPY (P 87)Making Production DecisionsMaking Production DecisionsSECTION 3

7

Production Costs:Production Costs:Fixed Costs- these are the costs that never

change regardless of the quantity for total product- example rent for your factory

Variable costs- these are the costs that change with the level of output- example material costs for each item, or # of workers.

Making Production DecisionsMaking Production DecisionsSECTION 3

8

Production Costs:Production Costs:Total Costs- The sum of adding Fixed Costs

and Variable costs together. Once you know your total costs, you divide it by

the total product to determine what each unit of output costs.

Marginal Costs- the costs that occur to make one more total product.

Making Production DecisionsMaking Production DecisionsSECTION 3

9

The big picture:The big picture:As a producer, you can have some control

over costsEvery time you add a cost, you must analyze

whether that cost will add to your overall profit or subtract from it

Making Production DecisionsMaking Production DecisionsSECTION 3