07 September 2020 Initiating Coverage

Berger Paints

HSIE Research is also available on Bloomberg ERH HDF <GO> & Thomson Reuters

Catalysts missing for a performance encore Berger Paints (BRGR) has gone toe-to-toe with dominant leader APNT over

FY10-20 despite the former's higher industrial salience, implying that its

decorative biz has outpaced APNT’s. Growth has been smartly navigated

alongside improving profitability via aggressive product innovation/

premiumisation, efficient marketing and distribution expansion

(GM/EBITDAM differential has reduced from 856/924bp to 320/560bp over

FY10-20). While this narrative will continue, outperformance is unlikely to be

as steep over FY20-23, given that (1) BRGR will have to contend with APNT's

stepped-up aggression at the bottom of the pyramid and (2) margin levers

seem to be missing. We build in revenue/EBITDA/PAT CAGR of 8/9/10% over

FY20-23E (closely tracking APNT) and initiate coverage on the stock with a

Sell recommendation and a DCF-based target price of Rs. 460/sh (implying 55x

Sep-22 P/E) as there is nothing on the investor table at 66x Sept-22 P/E. RoICs

are likely to mean revert to 22% by FY22/23.

Outperformed market leader: BRGR’s 5/10 year growth rates of 8/13%

mirrors that of APNT’s despite the former's higher industrial salience (20%

of domestic sales), implying that BRGR's decorative biz has outpaced that of

APNT's. It has also narrowed its profitability gap vs APNT over FY10-20

(GM/EBITDAM differential has reduced from 856/924bp to 320/560bp over

FY10-20). Key underpinnings for this outperformance are (1) improvement

in product price ladder, (2) smart brand-building, (3) improving distribution

quality, and (4) strategic tie-ups with strong category partners.

Albeit, do not expect a performance encore: Growth narrative will

continue, albeit BRGR's decorative outperformance vs APNT is not likely to

be material, given the latter's stepped-up aggression in driving sales from

the bottom of the pyramid, thereby restricting BRGR's sales outperformance.

We model 11/12% and 8/9% volume CAGR for APNT/BRGR over FY20-23.

Margin levers absent over FY21-23: Benign RM costs are likely to keep GMs

elevated in FY21 at ~43% (up 170bp YoY) but are likely to mean revert over

FY21-23 as (1) RM costs firm up with demand recovery, (2) the momentum

in low-GM (lower-end) paints outweighs that of premiumisation, and (3)

down-trading gains steam amidst pressure on incomes. Cost of operations is

expected to remain elevated in FY21/22, due to (1) pandemic-led

unfavourable leverage and (2) unabsorbed costs hitting the P&L once the

Sandila Plant is commissioned in FY22. Hence, we build in a modest 60bp

EBITDAM expansion, mostly mimicking GM gains over FY21-23.

Valuation and outlook: While BRGR remains a credible No. 2 in paints; at

66x Sept-22 P/E (18% premium to APNT), risk-reward seems unfavorable.

We assign a DCF-based TP of Rs. 460/sh (implying 55x Sep-21 P/E). Implied

assumptions: (1) 10-year revenue CAGR: 12.6%, (2) FY20-30E/FY30-41E

FCFF CAGR: 20/13.5% resp. (3) WACC: 10.5%, and (4) terminal growth: 6%,

FCF/PAT conversion of ~70% over FY20-30E. Initiate with a Sell Reco.

Financial Summary (Rs mn) FY19 FY20 FY21E FY22E FY23E

Net Revenue 60,619 63,658 58,853 71,948 80,458

EBITDA 8,816 10,610 9,698 12,396 13,902

APAT 4,975 6,561 5,867 7,706 8,684

EPS (Rs) 5.1 6.8 6.0 7.9 8.9

P/E (x) 109.7 83.2 93.0 70.8 62.9

EV/EBITDA (x) 62.2 51.7 56.2 43.9 38.7

Core RoCE (%) 17.9 21.0 17.6 21.5 22.1

Source: Company, HSIE Research

SELL

CMP (as on 04 Sep 2020) Rs 552

Target Price Rs 460

NIFTY 11,334

KEY

CHANGES OLD NEW

Rating - SELL

Price Target - Rs 460

EPS % FY21E FY22E

- -

KEY STOCK DATA

Bloomberg code BRGR IN

No. of Shares (mn) 971

MCap (Rs bn) / ($ mn) 534/7,329

6m avg traded value (Rs mn) 862

52 Week high / low Rs 597/357

STOCK PERFORMANCE (%)

3M 6M 12M

Absolute (%) 9.5 2.0 53.3

Relative (%) (3.3) 2.2 48.9

SHAREHOLDING PATTERN (%)

Mar-20 June-20

Promoters 74.99 74.99

FIs & Local MFs 1.05 1.12

FPIs 11.8 4.02

Public & Others 12.16 19.87

Pledged Shares 0 0

Source : BSE

Jay Gandhi

+91-22-6171-7320

Varun Lohchab

+91-22-6171-7334

Page | 2

Berger Paints: Initiating Coverage

Focus Charts

Industry/organised paints revenue forecasts BRGR has held its own in the oligopolistic paint

industry (Top 4 relative market share, %)

Source: HSIE Research Source: HSIE Research

...and gone toe-to-toe with dominant market leader

APNT…

…with improving share in the sector's profitability

(Top 4 relative PAT share, %)

Source: Companies, HSIE Research Source: Companies, HSIE Research

…as product innovation/premiumisation helped BRGR reduce its profitability gap with the best in business (gross

margin and EBITDAM differential (bp) vs APNT reduced from 856/924bp to 320/560bp over FY10-20

Source: Companies, HSIE Research

17.

8

18.

0

17.

5

17.

7

17.

5

17.

7

17.

5

18.

0

18.

0

18.

4

18.

7

0%

20%

40%

60%

80%

100%

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

Asian Paints Berger Paints

Kansai Nerolac Azko Nobel

9.7

11.

7

11.

4

12.

7

13.

4

13.

1

14.

4

13.

2

14.

2

14.

3

16.

5

0%

20%

40%

60%

80%

100%

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

Asian Paints Berger Paints Kansai Nerolac Azko Nobel

30.0

35.0

40.0

45.0

50.0

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

APNT (std) BRGR (std)

KNPL (std) Azko Nobel

320bp

856bp

5

10

15

20

25

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

APNT (std) BRGR (std) KNPL (std) Azko Nobel

560bp

924bp

8.1 8.4

6.9

1.0

12.9 12.9

11.2 10.9

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

0 0 0 0

APNT (Std) BRGR (Std) KNPL (Std) Azko Nobel

5-yr CAGR 10-yr CAGR

0

9

-7

20

12 12 12 11

-10

-5

0

5

10

15

20

25

0

500

1,000

1,500

FY

19

E

FY

20

E

FY

21

E

FY

22

E

FY

23

E

FY

24

E

FY

25

E

FY

30

E

Total paints revenue

Organized paints revenue

Org. Paints revenue growth (%) - RHS

Rs bn

Page | 3

Berger Paints: Initiating Coverage

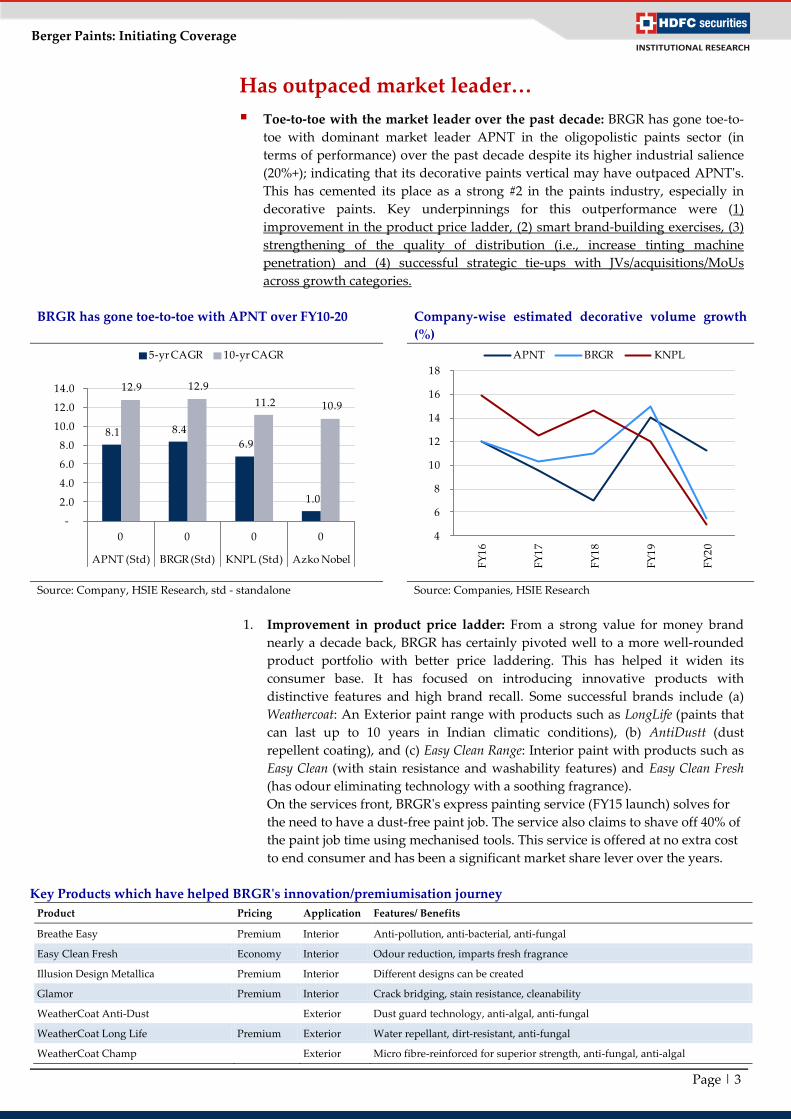

Has outpaced market leader…

Toe-to-toe with the market leader over the past decade: BRGR has gone toe-to-

toe with dominant market leader APNT in the oligopolistic paints sector (in

terms of performance) over the past decade despite its higher industrial salience

(20%+); indicating that its decorative paints vertical may have outpaced APNT's.

This has cemented its place as a strong #2 in the paints industry, especially in

decorative paints. Key underpinnings for this outperformance were (1)

improvement in the product price ladder, (2) smart brand-building exercises, (3)

strengthening of the quality of distribution (i.e., increase tinting machine

penetration) and (4) successful strategic tie-ups with JVs/acquisitions/MoUs

across growth categories.

BRGR has gone toe-to-toe with APNT over FY10-20 Company-wise estimated decorative volume growth

(%)

Source: Company, HSIE Research, std - standalone Source: Companies, HSIE Research

1. Improvement in product price ladder: From a strong value for money brand

nearly a decade back, BRGR has certainly pivoted well to a more well-rounded

product portfolio with better price laddering. This has helped it widen its

consumer base. It has focused on introducing innovative products with

distinctive features and high brand recall. Some successful brands include (a)

Weathercoat: An Exterior paint range with products such as LongLife (paints that

can last up to 10 years in Indian climatic conditions), (b) AntiDustt (dust

repellent coating), and (c) Easy Clean Range: Interior paint with products such as

Easy Clean (with stain resistance and washability features) and Easy Clean Fresh

(has odour eliminating technology with a soothing fragrance).

On the services front, BRGR's express painting service (FY15 launch) solves for

the need to have a dust-free paint job. The service also claims to shave off 40% of

the paint job time using mechanised tools. This service is offered at no extra cost

to end consumer and has been a significant market share lever over the years.

Key Products which have helped BRGR's innovation/premiumisation journey

Product Pricing Application Features/ Benefits

Breathe Easy Premium Interior Anti-pollution, anti-bacterial, anti-fungal

Easy Clean Fresh Economy Interior Odour reduction, imparts fresh fragrance

Illusion Design Metallica Premium Interior Different designs can be created

Glamor Premium Interior Crack bridging, stain resistance, cleanability

WeatherCoat Anti-Dust Exterior Dust guard technology, anti-algal, anti-fungal

WeatherCoat Long Life Premium Exterior Water repellant, dirt-resistant, anti-fungal

WeatherCoat Champ Exterior Micro fibre-reinforced for superior strength, anti-fungal, anti-algal

8.1 8.4

6.9

1.0

12.9 12.9

11.2 10.9

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

0 0 0 0

APNT (Std) BRGR (Std) KNPL (Std) Azko Nobel

5-yr CAGR 10-yr CAGR

4

6

8

10

12

14

16

18

FY

16

FY

17

FY

18

FY

19

FY

20

APNT BRGR KNPL

Page | 4

Berger Paints: Initiating Coverage

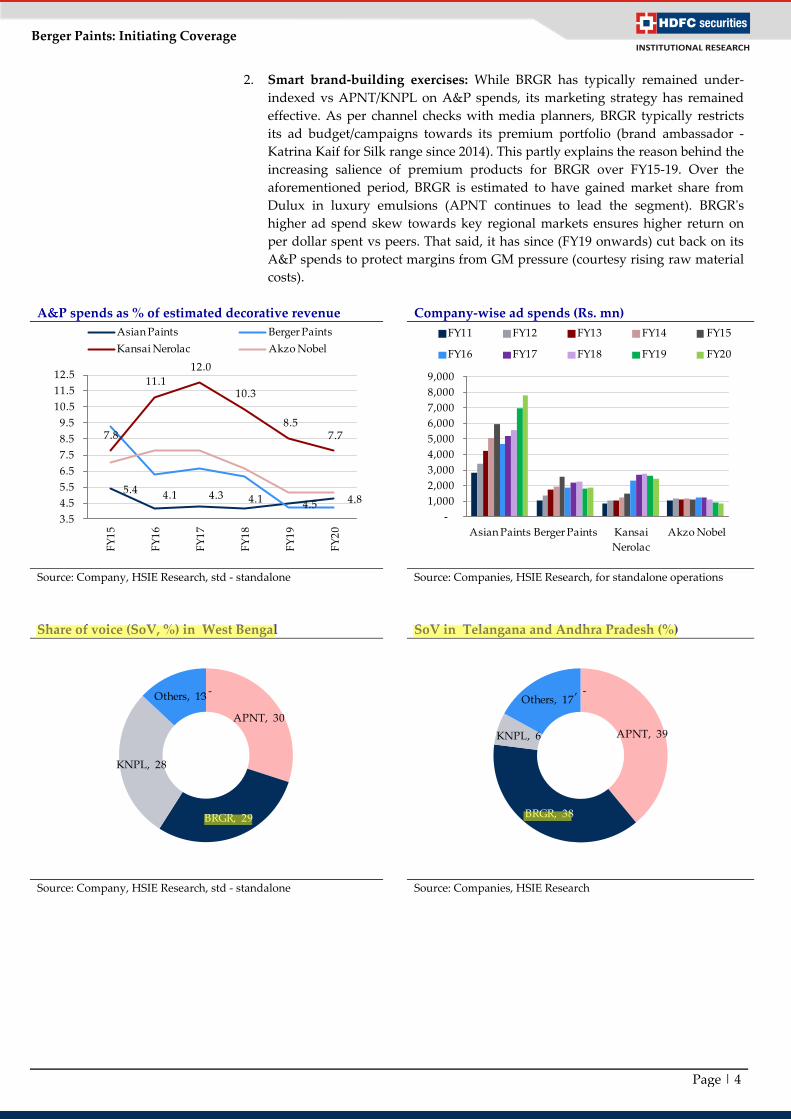

2. Smart brand-building exercises: While BRGR has typically remained under-

indexed vs APNT/KNPL on A&P spends, its marketing strategy has remained

effective. As per channel checks with media planners, BRGR typically restricts

its ad budget/campaigns towards its premium portfolio (brand ambassador -

Katrina Kaif for Silk range since 2014). This partly explains the reason behind the

increasing salience of premium products for BRGR over FY15-19. Over the

aforementioned period, BRGR is estimated to have gained market share from

Dulux in luxury emulsions (APNT continues to lead the segment). BRGR's

higher ad spend skew towards key regional markets ensures higher return on

per dollar spent vs peers. That said, it has since (FY19 onwards) cut back on its

A&P spends to protect margins from GM pressure (courtesy rising raw material

costs).

A&P spends as % of estimated decorative revenue Company-wise ad spends (Rs. mn)

Source: Company, HSIE Research, std - standalone Source: Companies, HSIE Research, for standalone operations

Share of voice (SoV, %) in West Bengal SoV in Telangana and Andhra Pradesh (%)

Source: Company, HSIE Research, std - standalone Source: Companies, HSIE Research

, -

APNT, 30

BRGR, 29

KNPL, 28

Others, 13 , -

APNT, 39

BRGR, 38

KNPL, 6

Others, 17

5.4 4.1 4.3 4.1 4.5 4.8

7.8

11.1

12.0

10.3

8.5 7.7

3.5

4.5

5.5

6.5

7.5

8.5

9.5

10.5

11.5

12.5

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

Asian Paints Berger Paints

Kansai Nerolac Akzo Nobel

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Asian Paints Berger Paints Kansai

Nerolac

Akzo Nobel

FY11 FY12 FY13 FY14 FY15

FY16 FY17 FY18 FY19 FY20

Page | 5

Berger Paints: Initiating Coverage

SoV in Maharashtra (%) SoV in Hindi speaking markets (%)

Source: Company, HSIE Research, std - standalone Source: Companies, HSIE Research

3. Strengthening of quality of distribution (i.e., increase tinting machine penetration): BRGR

has been consistently bettering the quality of its distribution by expanding its dealer network

in Tier 2/3 cities (semi-urban/rural) where penetrating through dealers and installing tinting

machines is easier vs doing the same in Metros/Select Tier 1s. The company has been growing

its dealer network at 10-12% per annum (2,500-3,000 dealers) and has nearly reached a tinting

machine penetration of 80%+ (steadily increasing). This and a lower base has helped BRGR

outpace the leader in decorative paints as (1) throughput/dealer improves with increasing

tinting machine penetration (typically goes up 2.5-3x), (2) the higher skew towards the faster-

growing Tier 2/3 cities and North East market vs peers ensured faster growth.

BRGR: Dealer expansion and tinting machine

penetration (%)

The faster-growing North and East markets remain

BRGR's mainstays, well-represented in South too

though (the largest market)

Source: Company, HSIE Research, std - standalone Source: Companies, HSIE Research

East, 18.9

West, 14.4

North, 16.2

Central,

23.4

South, 27.0

BRGR Depot mix (%)

, -

APNT, 30

BRGR, 27

KNPL, 15

Others, 28

, -

APNT, 52

BRGR, 10

KNPL, 20

Others, 18

0

10

20

30

40

50

60

70

80

90

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

Dealers (#) Tinting machine penetration (%)

Page | 6

Berger Paints: Initiating Coverage

Company-wise revenue per active dealer (Rs. mn) APNT's dealer multiple vs peers

Source: Companies, HSIE Research, NOTE: Revenue adjusted to

account for only decorative revenue. 90% of deco rev assigned to

active dealers

Source: Companies, HSIE Research, How to Read the chart: Eg:

APNT's dealer base has grown from 4.3x of Akzo Nobel in FY13 to

6.5x in FY20

2.9 2.9 2.9 3.0

2.9

1.8 1.8 1.9 2.0

1.8 1.5 1.5 1.5 1.5

1.3

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

FY16 FY17 FY18 FY19 FY20

Asian Paints Berger Paints Kansai Nerolac

2.0 2.0 1.9 1.9 1.9 2.0 2.0 2.1

2.4 2.4 2.3 2.4 2.5 2.5 2.5 2.5

4.3 4.2 4.0

4.4 4.6

5.2

5.8

6.5

1.5

2.5

3.5

4.5

5.5

6.5

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20

Berger Paints Kansai Nerolac Akzo Nobel

Page | 7

Berger Paints: Initiating Coverage

...albeit, do not expect an encore

BRGR will have to contend with APNT's aggressive volume/low-end strategy

While BRGR has managed to outpace APNT in decorative paints, courtesy its

strengthening product portfolio, distribution quality and smart brand building over

14 out of the past 25 quarters, we do not expect the company's top-line

outperformance (divergence with APNT) to continue. APNT is likely to remain

aggressive on its volume strategy over FY20-23 by pushing low-end paint solutions

(low-end emulsions, distempers, primers, putty) as its predisposition would be to

increase its capacity utilisation and absorb as much production/other fixed costs as it

can. Note: APNT recently increased its capacity (over FY18-19) by >50%.

BRGR has outpaced APNT in 14 out of the past 25 quarters…we do not expect an encore

Source: Companies, HSIE Research, NOTE: Revenue adjusted to account for only decorative revenue. 90% of deco rev assigned to active dealers

GM's expansion likely to remain in check: BRGR significantly narrowed the GM

(from 856bp to 320bp) and EBITDAM gap (from 924bp to 560bp) with APNT over

the past decade, underpinned by (1) premiumisation/product innovation, (2)

smart brand-building exercises, (3) strengthening of the quality of distribution

(i.e., increase tinting machine penetration). However, at the margin, GM

expansion/mix improvement levers mostly seem missing as top players (incl.

BRGR) vie for demand (1) at the bottom-of-the-pyramid and sell low margin

products amidst the pandemic and beyond; (2) emanating from any down-

trading trends which play out due to stress on income levels during/in the

aftermath of the pandemic. While premiumisation may continue within the

portfolio, the momentum in lower-end paint solutions and down-trading is likely

to overshadow the positive impact of premiumisation, if any.

We build in a marginal 60bp GM improvement (42.1%) over FY20-23, primarily

stemming from benign RM prices. GM differential with APNT will continue to

gradually narrow though. Note GMs in FY20 improved by 250bp to 41.5%,

primarily led by (1) benign RM prices and (2) the increased skew of high-margin

decorative paints in revenue mix, (3) steady performance of subsidiaries which

typically enjoy higher GMs. Standalone GMs improved 270bp to 40.8% in FY20.

EBITDAM levers over FY20-23, too, remain modest: In FY20, higher cost of

operations negated most of the GM savings. LTL cost of operations increased

140bp to 25.8% (Pre-INDAS 116) as employee costs and SG&A expenses

remained elevated. We presume this might be due to unabsorbed costs of recent

capacities installed (Rishra, Jejuri – FY19). BRGR is likely to witness another

Capex round by FY22 (Sandila Plant – for decorative paints) as it spurs its

capacity to service the bottom of the pyramid. Related costs are likely to be better

absorbed over FY22-24. Hence, we build in a modest 60bp expansion largely

trickling down from GM savings.

(50)

(40)

(30)

(20)

(10)

-

10

20

30

40

1Q

FY

15

2Q

FY

15

3Q

FY

15

4Q

FY

15

1Q

FY

16

2Q

FY

16

3Q

FY

16

4Q

FY

16

1Q

FY

17

2Q

FY

17

3Q

FY

17

4Q

FY

17

1Q

FY

18

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

1Q

FY

21

2Q

FY

21

3Q

FY

21

4Q

FY

21

BRGR (std) APNT (std)

Page | 8

Berger Paints: Initiating Coverage

Consistent improvement in pricing ladder, product

innovation, and premiumisation have helped BRGR

narrow down its GM differential with APNT…

…and it is ditto with EBITDAM differential (%)

Source: Companies, HSIE Research Source: Companies, HSIE Research

BRGR's manufacturing footprint

HOWRAH JEJURI

JAMMU ASSAM (NALBARI)*

SURAJPUR* PUDUCHERRY

HINDUPUR RISHRA

TALOJA HINDUPUR

SIKANDRABAD* ASSAM (NALTOLI)

GOA

Source: Companies, HSIE Research, * - manufacturing for British Paints Division

Company-wise estimated capacity (KL/pa) Estimated capacity utilisation (%)

Source: Companies, HSIE Research Source: Companies, HSIE Research

30.0

35.0

40.0

45.0

50.0

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

APNT (std) BRGR (std)

KNPL (std) Azko Nobel

320bp

5

10

15

20

25

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

APNT (std) BRGR (std) KNPL (std) Azko Nobel

560bp

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

FY17 FY18 FY19 FY20

APNT BRGR KNPL

-

10

20

30

40

50

60

70

80

90

FY17 FY18 FY19 FY20

APNT BRGR KNPL

Page | 9

Berger Paints: Initiating Coverage

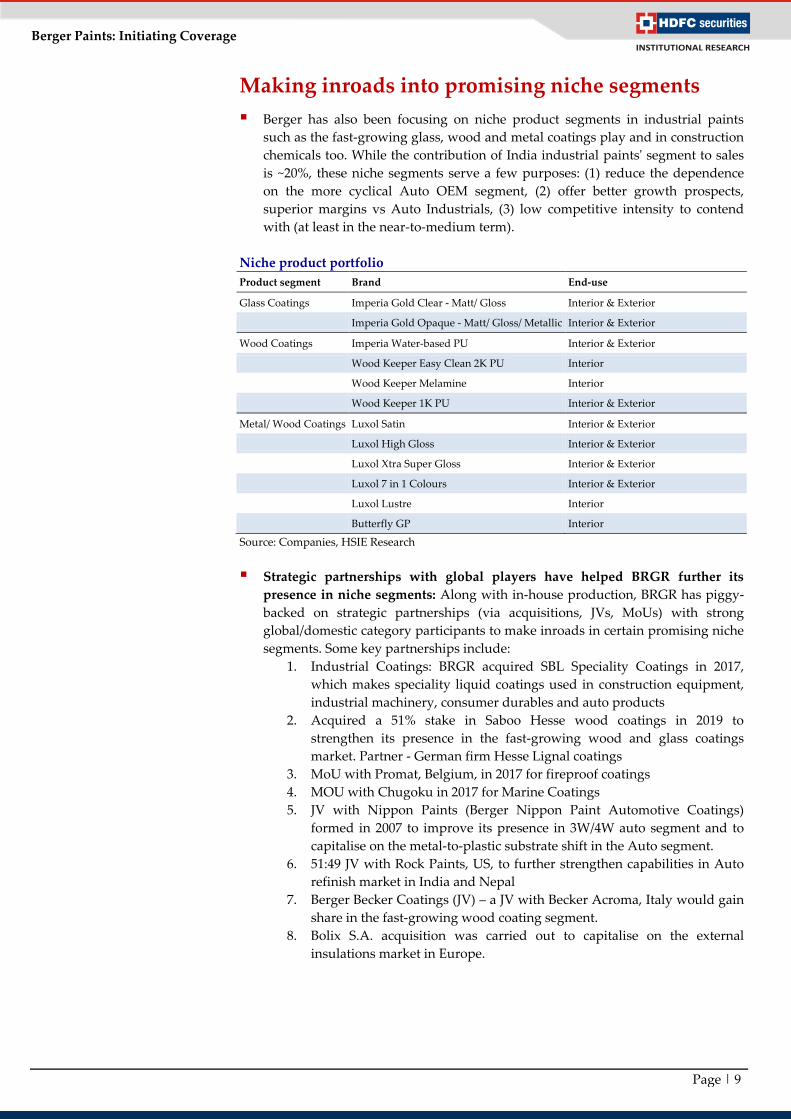

Making inroads into promising niche segments

Berger has also been focusing on niche product segments in industrial paints

such as the fast-growing glass, wood and metal coatings play and in construction

chemicals too. While the contribution of India industrial paints' segment to sales

is ~20%, these niche segments serve a few purposes: (1) reduce the dependence

on the more cyclical Auto OEM segment, (2) offer better growth prospects,

superior margins vs Auto Industrials, (3) low competitive intensity to contend

with (at least in the near-to-medium term).

Niche product portfolio

Product segment Brand End-use

Glass Coatings Imperia Gold Clear - Matt/ Gloss Interior & Exterior

Imperia Gold Opaque - Matt/ Gloss/ Metallic Interior & Exterior

Wood Coatings Imperia Water-based PU Interior & Exterior

Wood Keeper Easy Clean 2K PU Interior

Wood Keeper Melamine Interior

Wood Keeper 1K PU Interior & Exterior

Metal/ Wood Coatings Luxol Satin Interior & Exterior

Luxol High Gloss Interior & Exterior

Luxol Xtra Super Gloss Interior & Exterior

Luxol 7 in 1 Colours Interior & Exterior

Luxol Lustre Interior

Butterfly GP Interior

Source: Companies, HSIE Research

Strategic partnerships with global players have helped BRGR further its

presence in niche segments: Along with in-house production, BRGR has piggy-

backed on strategic partnerships (via acquisitions, JVs, MoUs) with strong

global/domestic category participants to make inroads in certain promising niche

segments. Some key partnerships include:

1. Industrial Coatings: BRGR acquired SBL Speciality Coatings in 2017,

which makes speciality liquid coatings used in construction equipment,

industrial machinery, consumer durables and auto products

2. Acquired a 51% stake in Saboo Hesse wood coatings in 2019 to

strengthen its presence in the fast-growing wood and glass coatings

market. Partner - German firm Hesse Lignal coatings

3. MoU with Promat, Belgium, in 2017 for fireproof coatings

4. MOU with Chugoku in 2017 for Marine Coatings

5. JV with Nippon Paints (Berger Nippon Paint Automotive Coatings)

formed in 2007 to improve its presence in 3W/4W auto segment and to

capitalise on the metal-to-plastic substrate shift in the Auto segment.

6. 51:49 JV with Rock Paints, US, to further strengthen capabilities in Auto

refinish market in India and Nepal

7. Berger Becker Coatings (JV) – a JV with Becker Acroma, Italy would gain

share in the fast-growing wood coating segment.

8. Bolix S.A. acquisition was carried out to capitalise on the external

insulations market in Europe.

Page | 10

Berger Paints: Initiating Coverage

BRGR's inorganic journey

Partner Partnership Type Year Category serviced

STP Ltd Acquisition 2,020 Construction Chemicals

Rock Paints JV 2,018 Auto Refinish

Rock Paints MOUs 2,017 Auto Refinish

Promat MOUs 2,017 Fireproof

Chugoku MOUs 2,017 Marine Coatings

Saboo Coatings Acquisition 2,017 Industrial Coatings

Sherwin Williams (now Bepee Coatings) Acquisition 2,013 Decorative Coatings

Sherwin Williams MOUs 2,013 Wood Coatings

Bolix Acquisition 2,008 External insulation

Nippon JV 2,007 Automotive Paints

ICI Acquisition 2,006 Motor and Industry

Tigerwerke MOUs 2,004 Powder Coatings

Becker JV 1,997 Coil Coatings

Subsidiaries have inched up from 10% to 11.6% of sales, accounting for 8% of bottom-line of BRGR in FY20; the

profitability of key subsidiaries has improved as well

Rs. mn

Subsidiaries % stake

FY20 FY19 Growth (YoY, %) FY 20 Margin

(%) FY 19 Margin (%)

Revenue PBT PAT Revenue PBT PAT Revenue PBT PAT PBT PAT PBT PAT

BJN (Nepal) 100.0 2,145 577 485 1,972 535 403 8.8 8.0 20.2 26.9 22.6 27.1 20.5

Beepee Coatings 100.0 241 22 16 249 38 27 (3.0) (41.3) (41.8) 9.2 6.6 15.2 11.0

SBL Specialty

Coatings 100.0 1,053 213 157 1,063 132 93 (0.9) 61.0 68.8 20.2 14.9 12.4 8.8

Berger Paints

(Cyprus) 100.0 - (2) (2) - (2) (2)

(37.5) (37.5)

Lusako Trading

100.0 - (52) (52) - (38) (38)

37.2 37.2

Berger Paints Overseas 100.0 136 (52) (52) (98) (176) (176) (239.1) (70.7) (70.7) (37.9) (37.9) 180.0 180.0

Bolix S.A 100.0 2,573 207 174 2,479 105 88 3.8 98.3 98.6 8.1 6.8 4.2 3.5

Build Trade BIS 100.0 - (0) (0) - (0) (0)

- -

Bolix UKRAINA

OOO 100.0 31 6 6 27 4 4 15.9 64.9 64.9 19.4 19.4 13.7 13.7

Soltherm

External Insulations

100.0 254 4 3 224 4 2 13.6 19.4 64.7 1.7 1.1 1.6 0.8

Soltherm

Insolations

Thermique

Exterieure

SAS

100.0 24 1 1 16 0 0 53.5 100.0 100.0 3.3 2.5 2.5 1.9

Berger Hessee

Wood Coatings 51.0 97 (1) (1) 14 1 1 619.3 (230.0) (181.8) (1.3) (0.9) 7.4 8.1

Berger Rock

Paints 51.0 83 (35) (35) 15 (9) (9) 449.0 269.1 269.1 (41.9) (41.9) (62.3) (62.3)

STP

Ltd 95.5 778 34 15 - - -

4.3 1.9

Total

7,416 923 716 5,959 592 393 24.4 55.9 82.3 12.5 9.7 9.9 6.6

Joint Ventures % stake Revenue (Rs. mn) PAT (Rs. mn) Attributable PAT (Rs. mn)

Berger Becker Coatings 49.0 3,651 117 58

Berger Nippon Paint Automotive Coatings 49.0 1,566 (141) (69)

Surefire Management Services 75.0

2 2

Total

5,217 (21) (10)

Page | 11

Berger Paints: Initiating Coverage

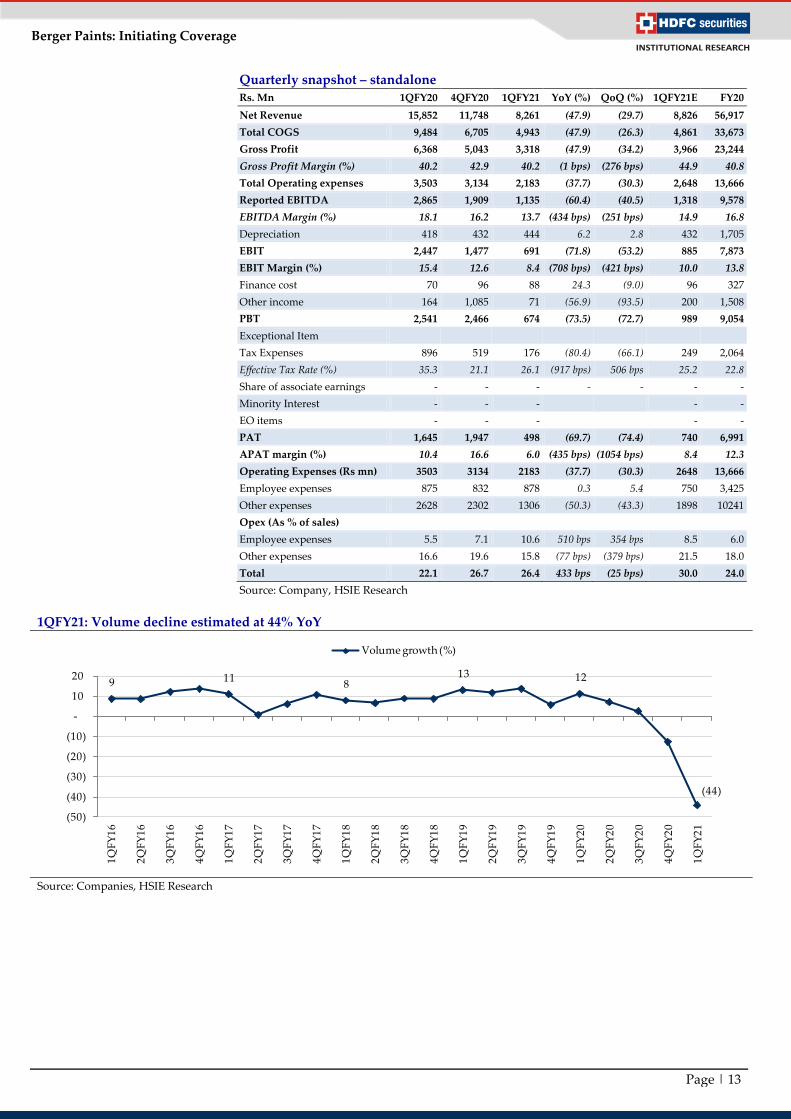

1QFY21: Relatively weak, GMs disappoint

Delivered a relatively weaker sales print: BRGR's 1QFY21 top-line declined

47.9% YoY (vs APNT's 44.1%) - a bit of a surprise, given (1) BRGR's lower

exposure to severely impacted metros/select Tier 1s) vs APNT, (2) lower base

(APNT does 3x the business). We reckon the sequential recovery trend would

have largely mimicked that of APNT (May/June APNT's volume growth trends

(80% of base/~14% YoY respectively), implying that the Paints category, counter-

intuitively, is showing spurts of recovery faster than other consumer

discretionary categories. Standalone volume decline is estimated at 44-45%.

While the recovery is encouraging, we remain circumspect of the real progression

in volume recovery as the May/June recovery is mostly a function of (1) pent-up

demand and (2) incentivised channel up-stocking.

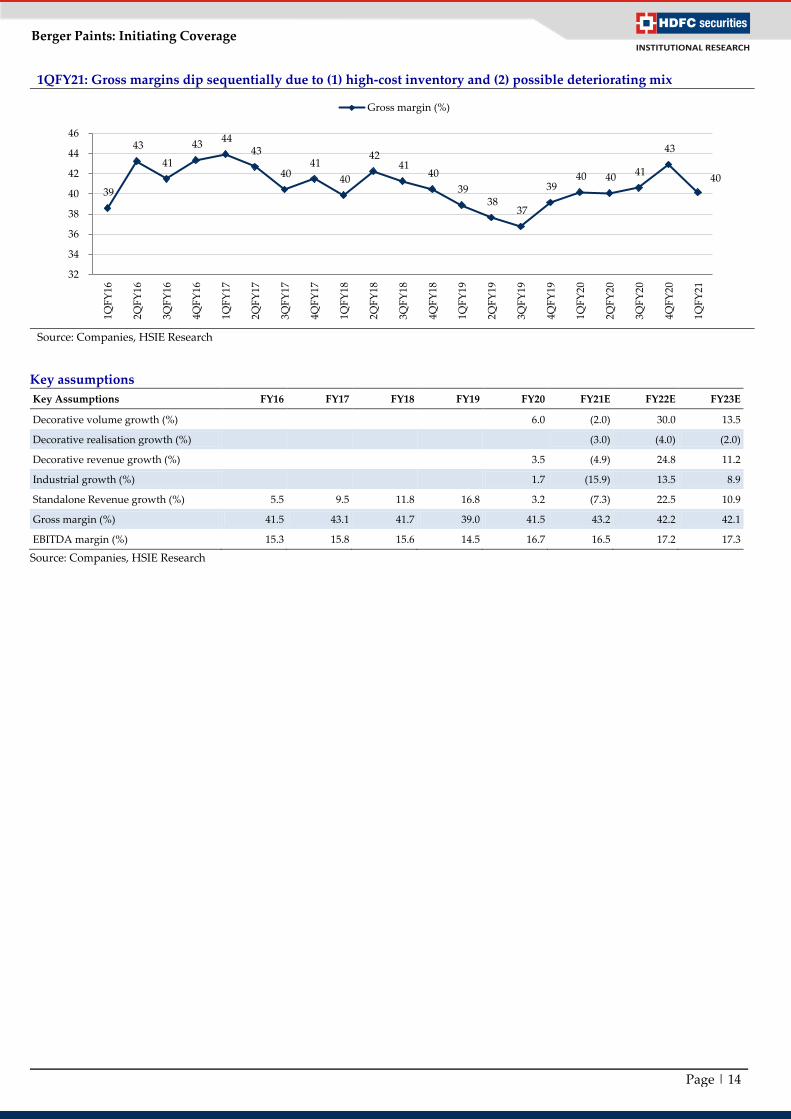

GMs were the bigger disappointment: BRGR's (standalone) GMs for 1Q

remained flat YoY/declined 276bp QoQ to 40.2% despite a benign RM

environment (crude is down 18-20%). Relatively too, BRGR lagged both APNT

(GMs expanded 154bp YoY/contracted 65bp QoQ) and KNPL GMs expanded

340/317bp YoY/QoQ respectively). One would have hoped BRGR would do

better in 1Q at least to the extent of the Decorative skew increasing in the mix (as

the decline in Industrial revenue is likely to have been steeper). Reasons

attributed to the GM disappointment was high-cost inventory consumption in

the ecosystem. However, we suspect such a divergence in BRGR's performance

with the #1/#3 players hints at some significant deterioration in the mix.

Subsidiaries stitched a better show: Subsidiaries clocked a relatively better

quarter. We suspect the STP acquisition (Oct-19) might have aided top-line

performance. The laggards in the portfolio were BJN Nepal as Nepal only had 10

working days in 1Q. BRGR's Polish subsidiary Bolix showed improvement both

in top-line as well as profitability as external insulation's (key product)

application on building sites entails less involvement with the end consumer, and

perceived to be safer than an interior paint job, hence was allowed during the

pandemic. EBITDA losses for subsidiaries stood at Rs. 214mn.

Cost Overheads shaved off by 37%: BRGR did an impressive job of cutting

down its op costs by 37% in 1Q to salvage profitability to the extent it could for

its standalone operations. SG&A expenses (standalone) halved in 1Q. On a

consolidated basis, opex costs declined 27% YoY vs a 47% decline in revenue;

hence, sub-par scale-led deleverage hit profitability. EBITDAM contracted

434/788bp YoY to 13.7%/7.8% for standalone/consolidated operations

respectively.

Other key takeaways:

1. Benign RM cost benefits are likely to be seen 2Q onwards, as (1) high-cost

inventory in the channel has normalised and (2) formulation-led RM savings

kick in. Management indicated that it has managed to re-negotiate better

deals with vendors for key RM.

2. Lower end paint products such as putty, primers, distempers and low-end

emulsions outpaced higher-end paint solutions this quarter. Justifiably so, as

the impact of the pandemic has been relatively less severe in Tier 2-4 markets

where low-end products sell more. Management did not discount the

possibility of down-trading in FY21, courtesy pandemic-led impact on

income levels.

Page | 12

Berger Paints: Initiating Coverage

3. Discounting and rebates to channel remained elevated as more solvent-based

products pushed in 1Q. Price decreases in the last 10 months preceding

COVID19 is ~2%

4. Like in 1Q, management indicated that they do not expect pricing

interventions by the industry anytime soon.

5. Protective coatings typically account for 9-9.5% of revenue and Powder

Coatings is a little less than 2%

6. Within the industrial segment, Auto continues to remain under severe

pressure; however, Protective coatings (9-9.5% of sales) and powder coatings

(~2% of sales) witnessed good recovery.

7. Dealer growth in FY20 was ~12.5%. However, in 1Q, BRGR, justifiably so

could only add dealers for 1.5/3 months. Run-rate is likely to progressively

normalize by end FY21.

Quarterly snapshot – consolidated

Rs. Mn 1QFY20 4QFY20 1QFY21 YoY (%) QoQ (%) 1QFY21 FY20 FY21

Net Revenue 17,165 13,548 9,308 (45.8) (31.3) 10,205 63,658 58,853

Total COGS 10,154 7,639 5,495 (45.9) (28.1) 5,619 37,258 33,441

Gross Profit 7,011 5,910 3,812 (45.6) (35.5) 4,586 26,400 25,412

Gross Profit Margin (%) 40.8 43.6 41.0 11 bps (266 bps) 44.9 41.5 43.2

Total Operating expenses 3,960 3,825 2,892 (27.0) (24.4) 3,258 15,790 15,714

Reported EBITDA 3,052 2,084 921 (69.8) (55.8) 1,328 10,610 9,698

EBITDA Margin (%) 17.8 15.4 9.9 (788 bps) (549 bps) 13.0 16.7 16.5

Depreciation 462 493 504 9.0 2.1 492 1,910 2,132

EBIT 2,590 1,591 417 (83.9) (73.8) 836 8,700 7,567

EBIT Margin (%) 15.1 11.7 4.5 (1060 bps) (726 bps) 8.2 13.7 12.9

Finance cost 99 141 124 24.6 (11.9) 141 470 566

Other income 219 167 78 (64.2) (53.0) 225 685 731

PBT 2,709 1,617 372 (86.3) (77.0) 920 8,915 7,732

Exceptional Item

Tax Expenses 944 560 176 (81.3) (68.6) 252 2,271 1,946

Effective Tax Rate (%) 34.8 34.7 47.4 1253 bps 1272 bps 27.4 25.5 25.2

Share of associate earnings (1) (25) (45) 3,625.0 81.0 (25) (83) (50)

Minority Interest - - -

- - -

EO items - - -

- - -

PAT 1,764 1,032 151 (91.4) (85.4) 643 6,561 5,736

APAT margin (%) 10.3 7.6 1.6 (866 bps) (599 bps) 6.3 10.3 9.7

Operating Expenses (Rs mn) 3960 3825 2892 (27.0) (24.4) 3258 15790 15714

Employee expenses 1117 1237 1162 4.1 (6.0) 1080 4525 4826

Other expenses 2843 2589 1729 (39.2) (33.2) 2178 11265 10888

Source: Company, HSIE Research

Page | 13

Berger Paints: Initiating Coverage

Quarterly snapshot – standalone

Rs. Mn 1QFY20 4QFY20 1QFY21 YoY (%) QoQ (%) 1QFY21E FY20

Net Revenue 15,852 11,748 8,261 (47.9) (29.7) 8,826 56,917

Total COGS 9,484 6,705 4,943 (47.9) (26.3) 4,861 33,673

Gross Profit 6,368 5,043 3,318 (47.9) (34.2) 3,966 23,244

Gross Profit Margin (%) 40.2 42.9 40.2 (1 bps) (276 bps) 44.9 40.8

Total Operating expenses 3,503 3,134 2,183 (37.7) (30.3) 2,648 13,666

Reported EBITDA 2,865 1,909 1,135 (60.4) (40.5) 1,318 9,578

EBITDA Margin (%) 18.1 16.2 13.7 (434 bps) (251 bps) 14.9 16.8

Depreciation 418 432 444 6.2 2.8 432 1,705

EBIT 2,447 1,477 691 (71.8) (53.2) 885 7,873

EBIT Margin (%) 15.4 12.6 8.4 (708 bps) (421 bps) 10.0 13.8

Finance cost 70 96 88 24.3 (9.0) 96 327

Other income 164 1,085 71 (56.9) (93.5) 200 1,508

PBT 2,541 2,466 674 (73.5) (72.7) 989 9,054

Exceptional Item

Tax Expenses 896 519 176 (80.4) (66.1) 249 2,064

Effective Tax Rate (%) 35.3 21.1 26.1 (917 bps) 506 bps 25.2 22.8

Share of associate earnings - - - - - - -

Minority Interest - - -

- -

EO items - - -

- -

PAT 1,645 1,947 498 (69.7) (74.4) 740 6,991

APAT margin (%) 10.4 16.6 6.0 (435 bps) (1054 bps) 8.4 12.3

Operating Expenses (Rs mn) 3503 3134 2183 (37.7) (30.3) 2648 13,666

Employee expenses 875 832 878 0.3 5.4 750 3,425

Other expenses 2628 2302 1306 (50.3) (43.3) 1898 10241

Opex (As % of sales)

Employee expenses 5.5 7.1 10.6 510 bps 354 bps 8.5 6.0

Other expenses 16.6 19.6 15.8 (77 bps) (379 bps) 21.5 18.0

Total 22.1 26.7 26.4 433 bps (25 bps) 30.0 24.0

Source: Company, HSIE Research

1QFY21: Volume decline estimated at 44% YoY

Source: Companies, HSIE Research

9 11 8

13 12

(44)

(50)

(40)

(30)

(20)

(10)

-

10

20

1Q

FY

16

2Q

FY

16

3Q

FY

16

4Q

FY

16

1Q

FY

17

2Q

FY

17

3Q

FY

17

4Q

FY

17

1Q

FY

18

2Q

FY

18

3Q

FY

18

4Q

FY

18

1Q

FY

19

2Q

FY

19

3Q

FY

19

4Q

FY

19

1Q

FY

20

2Q

FY

20

3Q

FY

20

4Q

FY

20

1Q

FY

21

Volume growth (%)

Page | 14

Berger Paints: Initiating Coverage

1QFY21: Gross margins dip sequentially due to (1) high-cost inventory and (2) possible deteriorating mix

Source: Companies, HSIE Research

Key assumptions

Key Assumptions FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

Decorative volume growth (%)

6.0 (2.0) 30.0 13.5

Decorative realisation growth (%)

(3.0) (4.0) (2.0)

Decorative revenue growth (%)

3.5 (4.9) 24.8 11.2

Industrial growth (%)

1.7 (15.9) 13.5 8.9

Standalone Revenue growth (%) 5.5 9.5 11.8 16.8 3.2 (7.3) 22.5 10.9

Gross margin (%) 41.5 43.1 41.7 39.0 41.5 43.2 42.2 42.1

EBITDA margin (%) 15.3 15.8 15.6 14.5 16.7 16.5 17.2 17.3

Source: Companies, HSIE Research

39

43

41

43 44

43

40 41

40

42 41

40

39 38

37

39 40 40 41

43

40

32

34

36

38

40

42

44

46

1QF

Y16

2QF

Y16

3QF

Y16

4QF

Y16

1QF

Y17

2QF

Y17

3QF

Y17

4QF

Y17

1QF

Y18

2QF

Y18

3QF

Y18

4QF

Y18

1QF

Y19

2QF

Y19

3QF

Y19

4QF

Y19

1QF

Y20

2QF

Y20

3QF

Y20

4QF

Y20

1QF

Y21

Gross margin (%)

Page | 15

Berger Paints: Initiating Coverage

Financial analysis

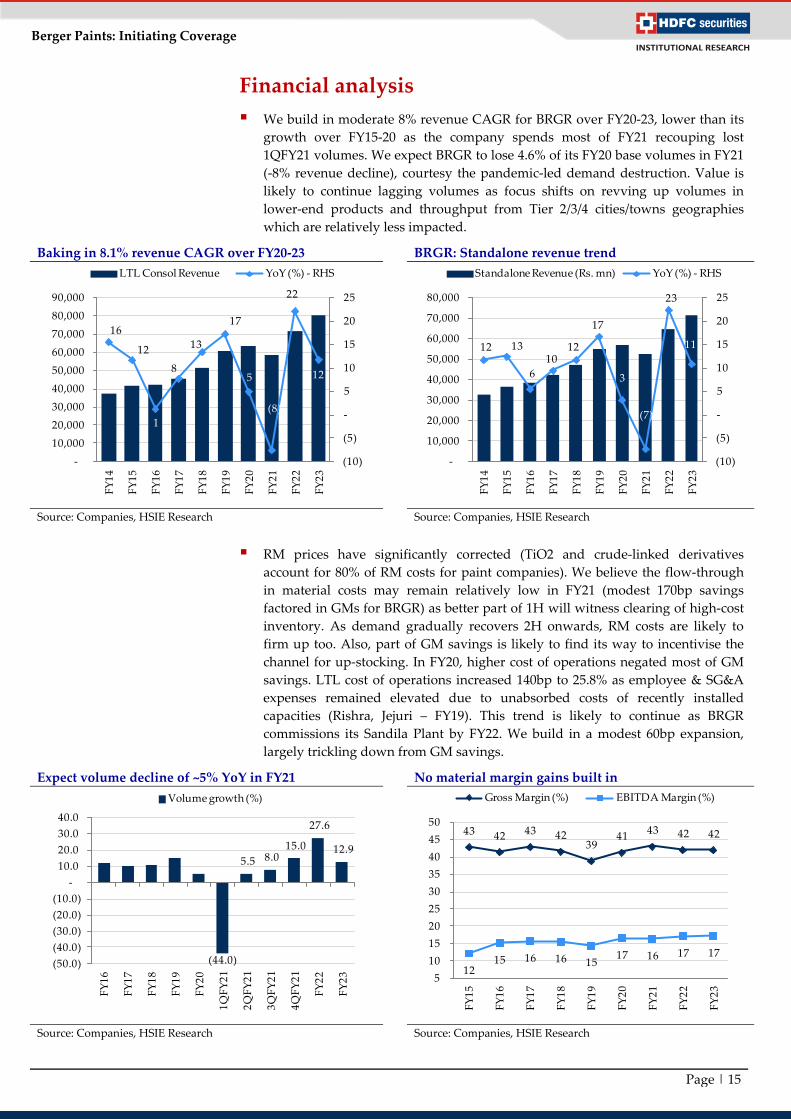

We build in moderate 8% revenue CAGR for BRGR over FY20-23, lower than its

growth over FY15-20 as the company spends most of FY21 recouping lost

1QFY21 volumes. We expect BRGR to lose 4.6% of its FY20 base volumes in FY21

(-8% revenue decline), courtesy the pandemic-led demand destruction. Value is

likely to continue lagging volumes as focus shifts on revving up volumes in

lower-end products and throughput from Tier 2/3/4 cities/towns geographies

which are relatively less impacted.

Baking in 8.1% revenue CAGR over FY20-23 BRGR: Standalone revenue trend

Source: Companies, HSIE Research Source: Companies, HSIE Research

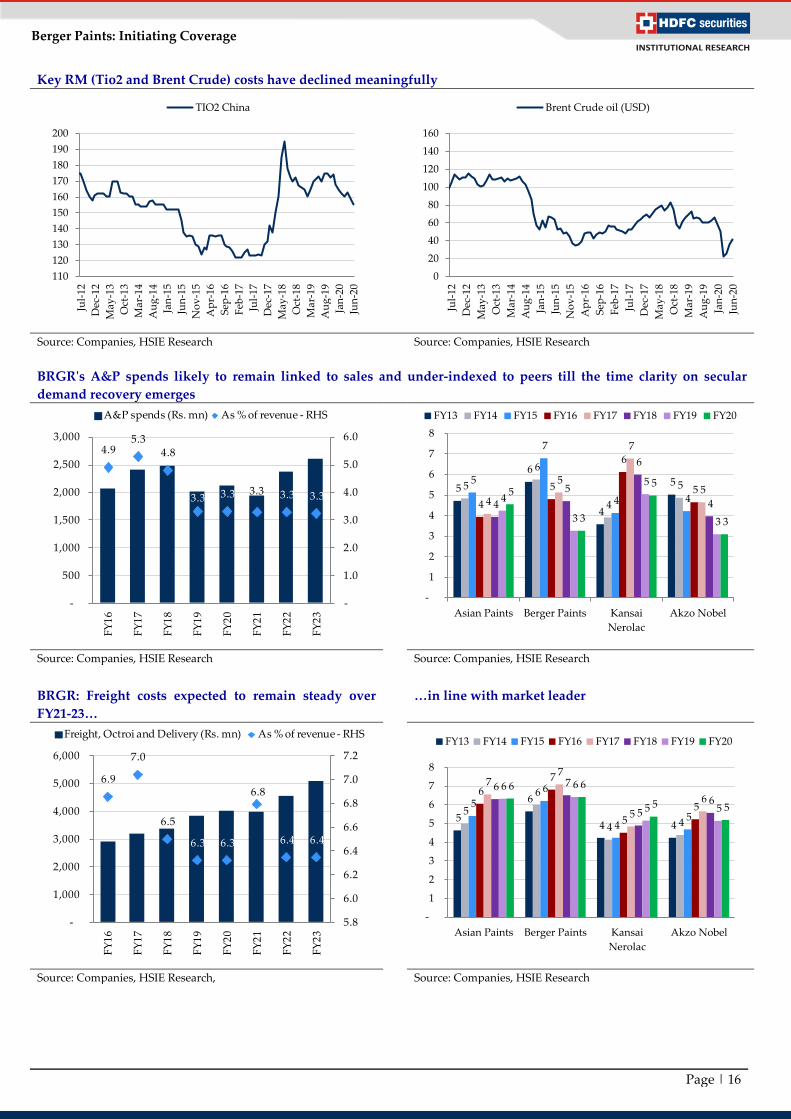

RM prices have significantly corrected (TiO2 and crude-linked derivatives

account for 80% of RM costs for paint companies). We believe the flow-through

in material costs may remain relatively low in FY21 (modest 170bp savings

factored in GMs for BRGR) as better part of 1H will witness clearing of high-cost

inventory. As demand gradually recovers 2H onwards, RM costs are likely to

firm up too. Also, part of GM savings is likely to find its way to incentivise the

channel for up-stocking. In FY20, higher cost of operations negated most of GM

savings. LTL cost of operations increased 140bp to 25.8% as employee & SG&A

expenses remained elevated due to unabsorbed costs of recently installed

capacities (Rishra, Jejuri – FY19). This trend is likely to continue as BRGR

commissions its Sandila Plant by FY22. We build in a modest 60bp expansion,

largely trickling down from GM savings.

Expect volume decline of ~5% YoY in FY21 No material margin gains built in

Source: Companies, HSIE Research Source: Companies, HSIE Research

16

12

1

8

13

17

5

(8)

22

12

(10)

(5)

-

5

10

15

20

25

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21

FY

22

FY

23

LTL Consol Revenue YoY (%) - RHS

12 13

6

10 12

17

3

(7)

23

11

(10)

(5)

-

5

10

15

20

25

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

FY

14

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21

FY

22

FY

23

Standalone Revenue (Rs. mn) YoY (%) - RHS

(44.0)

5.5 8.0 15.0

27.6

12.9

(50.0)

(40.0)

(30.0)

(20.0)

(10.0)

-

10.0

20.0

30.0

40.0

FY

16

FY

17

FY

18

FY

19

FY

20

1Q

FY

21

2Q

FY

21

3Q

FY

21

4Q

FY

21

FY

22

FY

23

Volume growth (%)

43 42 43 42 39

41 43 42 42

12 15 16 16 15

17 16 17 17

5

10

15

20

25

30

35

40

45

50

FY

15

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21

FY

22

FY

23

Gross Margin (%) EBITDA Margin (%)

Page | 16

Berger Paints: Initiating Coverage

Key RM (Tio2 and Brent Crude) costs have declined meaningfully

Source: Companies, HSIE Research Source: Companies, HSIE Research

BRGR's A&P spends likely to remain linked to sales and under-indexed to peers till the time clarity on secular

demand recovery emerges

Source: Companies, HSIE Research Source: Companies, HSIE Research

BRGR: Freight costs expected to remain steady over

FY21-23…

…in line with market leader

Source: Companies, HSIE Research, Source: Companies, HSIE Research

110

120

130

140

150

160

170

180

190

200

Jul-

12

Dec

-12

May

-13

Oct

-13

Mar

-14

Au

g-1

4

Jan

-15

Jun

-15

No

v-1

5

Ap

r-16

Sep

-16

Feb

-17

Jul-

17

Dec

-17

May

-18

Oct

-18

Mar

-19

Au

g-1

9

Jan

-20

Jun

-20

TIO2 China

0

20

40

60

80

100

120

140

160

Jul-

12

Dec

-12

May

-13

Oct

-13

Mar

-14

Au

g-1

4

Jan

-15

Jun

-15

No

v-1

5

Ap

r-16

Sep

-16

Feb

-17

Jul-

17

Dec

-17

May

-18

Oct

-18

Mar

-19

Au

g-1

9

Jan

-20

Jun

-20

Brent Crude oil (USD)

5

6

4

5 5

6

4

5 5

7

4 4 4

5

6

5 4

5

7

5

4

5

6

4 4

3

5

3

5

3

5

3

-

1

2

3

4

5

6

7

8

Asian Paints Berger Paints Kansai

Nerolac

Akzo Nobel

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20

5

6

4 4

5

6

4 4

5

6

4 5

6

7

5 5

7 7

5

6 6 7

5 6

6 6

5 5

6 6

5 5

-

1

2

3

4

5

6

7

8

Asian Paints Berger Paints Kansai

Nerolac

Akzo Nobel

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20

4.9 5.3

4.8

3.3 3.3 3.3 3.3 3.3

-

1.0

2.0

3.0

4.0

5.0

6.0

-

500

1,000

1,500

2,000

2,500

3,000

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21

FY

22

FY

23

A&P spends (Rs. mn) As % of revenue - RHS

6.9

7.0

6.5

6.3 6.3

6.8

6.4 6.4

5.8

6.0

6.2

6.4

6.6

6.8

7.0

7.2

-

1,000

2,000

3,000

4,000

5,000

6,000

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21

FY

22

FY

23

Freight, Octroi and Delivery (Rs. mn) As % of revenue - RHS

Page | 17

Berger Paints: Initiating Coverage

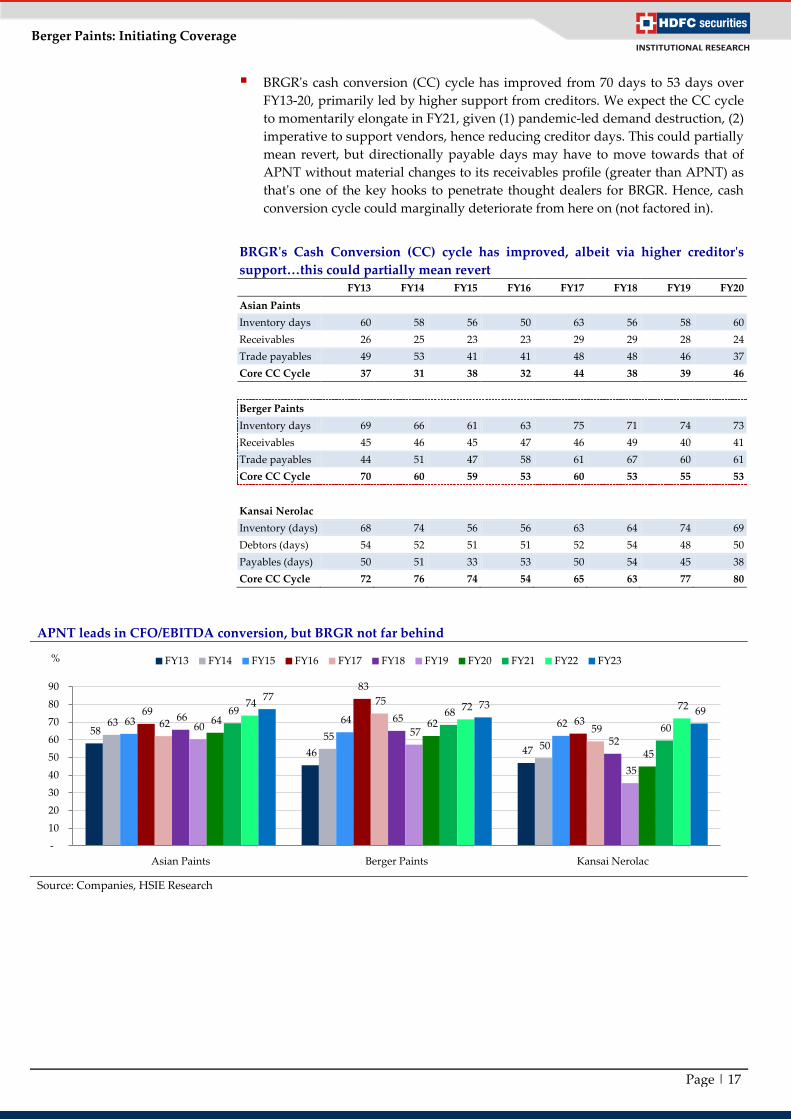

BRGR's cash conversion (CC) cycle has improved from 70 days to 53 days over

FY13-20, primarily led by higher support from creditors. We expect the CC cycle

to momentarily elongate in FY21, given (1) pandemic-led demand destruction, (2)

imperative to support vendors, hence reducing creditor days. This could partially

mean revert, but directionally payable days may have to move towards that of

APNT without material changes to its receivables profile (greater than APNT) as

that's one of the key hooks to penetrate thought dealers for BRGR. Hence, cash

conversion cycle could marginally deteriorate from here on (not factored in).

BRGR's Cash Conversion (CC) cycle has improved, albeit via higher creditor's

support…this could partially mean revert

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20

Asian Paints

Inventory days 60 58 56 50 63 56 58 60

Receivables 26 25 23 23 29 29 28 24

Trade payables 49 53 41 41 48 48 46 37

Core CC Cycle 37 31 38 32 44 38 39 46

Berger Paints

Inventory days 69 66 61 63 75 71 74 73

Receivables 45 46 45 47 46 49 40 41

Trade payables 44 51 47 58 61 67 60 61

Core CC Cycle 70 60 59 53 60 53 55 53

Kansai Nerolac

Inventory (days) 68 74 56 56 63 64 74 69

Debtors (days) 54 52 51 51 52 54 48 50

Payables (days) 50 51 33 53 50 54 45 38

Core CC Cycle 72 76 74 54 65 63 77 80

APNT leads in CFO/EBITDA conversion, but BRGR not far behind

Source: Companies, HSIE Research

58

46 47

63

55 50

63 64 62 69

83

63 62

75

59 66 65

52

60 57

35

64 62

45

69 68

60

74 72 72 77

73 69

-

10

20

30

40

50

60

70

80

90

Asian Paints Berger Paints Kansai Nerolac

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 %

Page | 18

Berger Paints: Initiating Coverage

Capex intensity likely to be high given the capacity

addition imperative

Return profile to decline in the pandemic-stricken

FY21…expect a V-shaped recovery over FY20-23E

Source: Companies, HSIE Research Source: Companies, HSIE Research

BRGR's capital allocation over the years

Sources of funds (Rs bn) FY15 FY16 FY17 FY18 FY19 FY20 FY21E FY22E FY23E

Cash from Operations (excl WC change) 4,023 4,807 5,220 5,499 6,542 8,245 7,658 9,737 10,915

Other Income - - - - - - - - -

Total 4,023 4,807 5,220 5,499 6,542 8,245 7,658 9,737 10,915

Application of funds (Rs bn)

Working Capital (115) (1,138) 1,275 1,280 925 999 602 630 921

Capex 1,602 1,233 2,757 2,878 3,166 4,310 1,317 5,844 3,189

Investments 381 1,477 374 (1,622) 434 (886) - - -

Dividend 1,383 1,085 1,169 2,045 2,105 3,816 2,225 2,225 2,225

Borrowings 149 2,319 (507) (290) (619) (1,014) - - -

Others 303 155 116 824 795 801 (215) (334) (585)

Net change in cash 320 (323) 36 384 (265) 219 3,730 1,373 5,165

Total 4,023 4,807 5,220 5,499 6,542 8,245 7,658 9,737 10,915

3-yr rolling WC + Capex as % of

sources of funds 78 35 40 53 71 67 50 53 44

Source: Companies, HSIE Research

5.5

4.5 4.1 4.1

3.4 2.9 2.8 2.8

-

1.0

2.0

3.0

4.0

5.0

6.0

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21

FY

22

FY

23

Capex (Rs. mn) Asset turnover (x) - Gross Rev/GFA - RHS

19

.7

18

.9

18

.6

17

.9

21

.0

17

.6 21

.5

22

.1

-

5.0

10.0

15.0

20.0

25.0

30.0

FY

16

FY

17

FY

18

FY

19

FY

20

FY

21

E

FY

22

E

FY

23

E

RoE (%) RoCE (%) RoIC (%)

Page | 19

Berger Paints: Initiating Coverage

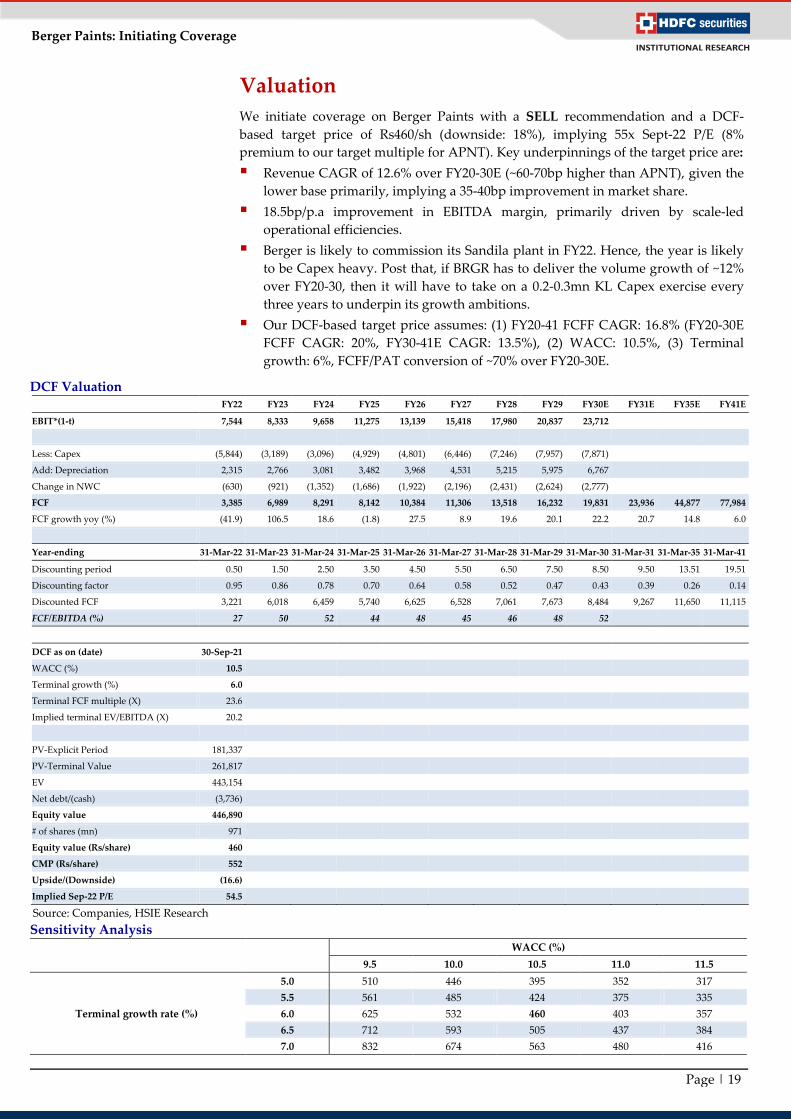

Valuation

We initiate coverage on Berger Paints with a SELL recommendation and a DCF-

based target price of Rs460/sh (downside: 18%), implying 55x Sept-22 P/E (8%

premium to our target multiple for APNT). Key underpinnings of the target price are:

Revenue CAGR of 12.6% over FY20-30E (~60-70bp higher than APNT), given the

lower base primarily, implying a 35-40bp improvement in market share.

18.5bp/p.a improvement in EBITDA margin, primarily driven by scale-led

operational efficiencies.

Berger is likely to commission its Sandila plant in FY22. Hence, the year is likely

to be Capex heavy. Post that, if BRGR has to deliver the volume growth of ~12%

over FY20-30, then it will have to take on a 0.2-0.3mn KL Capex exercise every

three years to underpin its growth ambitions.

Our DCF-based target price assumes: (1) FY20-41 FCFF CAGR: 16.8% (FY20-30E

FCFF CAGR: 20%, FY30-41E CAGR: 13.5%), (2) WACC: 10.5%, (3) Terminal

growth: 6%, FCFF/PAT conversion of ~70% over FY20-30E.

DCF Valuation FY22 FY23 FY24 FY25 FY26 FY27 FY28 FY29 FY30E FY31E FY35E FY41E

EBIT*(1-t) 7,544 8,333 9,658 11,275 13,139 15,418 17,980 20,837 23,712

Less: Capex (5,844) (3,189) (3,096) (4,929) (4,801) (6,446) (7,246) (7,957) (7,871)

Add: Depreciation 2,315 2,766 3,081 3,482 3,968 4,531 5,215 5,975 6,767

Change in NWC (630) (921) (1,352) (1,686) (1,922) (2,196) (2,431) (2,624) (2,777)

FCF 3,385 6,989 8,291 8,142 10,384 11,306 13,518 16,232 19,831 23,936 44,877 77,984

FCF growth yoy (%) (41.9) 106.5 18.6 (1.8) 27.5 8.9 19.6 20.1 22.2 20.7 14.8 6.0

Year-ending 31-Mar-22 31-Mar-23 31-Mar-24 31-Mar-25 31-Mar-26 31-Mar-27 31-Mar-28 31-Mar-29 31-Mar-30 31-Mar-31 31-Mar-35 31-Mar-41

Discounting period 0.50 1.50 2.50 3.50 4.50 5.50 6.50 7.50 8.50 9.50 13.51 19.51

Discounting factor 0.95 0.86 0.78 0.70 0.64 0.58 0.52 0.47 0.43 0.39 0.26 0.14

Discounted FCF 3,221 6,018 6,459 5,740 6,625 6,528 7,061 7,673 8,484 9,267 11,650 11,115

FCF/EBITDA (%) 27 50 52 44 48 45 46 48 52

DCF as on (date) 30-Sep-21

WACC (%) 10.5

Terminal growth (%) 6.0

Terminal FCF multiple (X) 23.6

Implied terminal EV/EBITDA (X) 20.2

PV-Explicit Period 181,337

PV-Terminal Value 261,817

EV 443,154

Net debt/(cash) (3,736)

Equity value 446,890

# of shares (mn) 971

Equity value (Rs/share) 460

CMP (Rs/share) 552

Upside/(Downside) (16.6)

Implied Sep-22 P/E 54.5

Source: Companies, HSIE Research

Sensitivity Analysis

WACC (%)

9.5 10.0 10.5 11.0 11.5

Terminal growth rate (%)

5.0 510 446 395 352 317

5.5 561 485 424 375 335

6.0 625 532 460 403 357

6.5 712 593 505 437 384

7.0 832 674 563 480 416

Page | 20

Berger Paints: Initiating Coverage

Company profile

With modest beginnings in India in 1923, today, Berger Paints India Limited is the

second-largest paint company in the country with a consistent track record of being

one of the fastest-growing, quarter on quarter, for the past few years. It has a

presence in decorative paints, industrial coatings, and construction chemicals

(primarily waterproofing). Berger Paints India is headquartered in Kolkata, with 16

strategically located manufacturing units across India (including subsidiaries), two in

Nepal, one each in Poland and Russia and about 162 stock points. The company also

has an international presence in four countries: Nepal, Bangladesh, Poland, and

Russia. It has 610,000 MT capacity. Berger has the second-largest distribution

network with ~27,000 dealers and a tinting machine penetration of ~80%.

The decorative segment makes up nearly 75%+ of Berger's revenue. Traditionally

having a strong foothold in the economy segment, over the past few years, Berger has

gained market share in the premium segment. Through strategic tie-ups/JVs with

global firms, the company has tried to strengthen capabilities in niche areas such as

auto refinishes and glass, wood, marine and fireproof coatings. In the Auto segment

(2W, 3W, CVs), its key customers include Hero, Royal Enfield, Yamaha, TVS, Honda,

Bajaj, Tata Motors, and Ashok Leyland.

The Dhingra family, promoters of Berger Paints, has been in the paints business for

four generations. The family acquired the controlling stake of the company from Mr

Vijay Mallya in 1991. The promoter family continues to have executive powers but is

not involved in day-to-day operations. The company is run by professionals.

Key Personnel

Name Designation Description

Mr. Kuldip Singh Dhingra Chairman

Mr Dhingra is the Chairman of the Board of Directors. He has been a Director of the

company since 1991. He is a Science Graduate from Hindu College, Delhi University.

He is the promoter of the company and an industrialist with a long-standing

experience in paints and related industries. He is the fourth generation of his family

that has been continuously in the paints business since 1898.

Mr. Gurbachan Singh

Dhingra Vice-Chairman

Mr Dhingra is the Vice-Chairman of the Board of Directors. He has been a Director of

the company since 1993. He is a graduate, an industrialist, the promoter and has

considerable experience in the paint industry, especially in its technical aspects. He is

the fourth generation of his family, which has been continuously in the paints business

since 1898.

Mr. Abhijit Roy MD & CEO

Mr Roy graduated in Mechanical Engineering from Jadavpur University, Kolkata and

completed his post-graduation in Business Administration from the Indian Institute of

Management, Bangalore. He started his career with Asian Paints Limited and before

joining Berger was associated with L'Oreal. He was appointed as the Managing

Director & CEO with effect from 1st July 2012.

Mr. Srijit Dasgupta CFO

Mr Dasgupta is a B.Sc (Hons) from Calcutta University, AICWA from Institute of Cost

& Works Accountants of India & Company Secretary from Institute of Company

Secretaries of India having over 29 years of work experience. He started his career with

Machinery Manufacturers Corporation Limited and before joining Berger was

associated with the same organisation.

Mr. Arunito Ganguly

Vice President &

Company

Secretary

Mr Ganguly is a B.Com (Hons.) from St. Xaviers College Kolkata. He is a fellow

Member of the Institute of Company Secretaries of India and has passed LL.B. from the

University of Burdwan. He has 16 years' experience in handling secretarial and legal

matters, including 14 years' experience as Company Secretary/Deputy Company

Secretary in large listed companies.

Source: Company, HSIE Research

Page | 21

Berger Paints: Initiating Coverage

Key Risks

Name Description

Correlation of sales with the

economy

While the three top paint companies have shown resilience in terms

of volume growth over the past few quarters even during the extant

economic slowdown, the sustenance of the slowdown could pose a

downside risk to our estimates.

The sharp rise in input costs

There are several raw materials which are directly driven by crude

oil. Approximately 70% of the input costs can be accounted for by

crude derivations. The remaining ~30% of the input costs arise from

non-crude (TiO2) forms. Therefore, any sharp increase in input costs

could adversely impact the business

Finance risks originating out of

currency fluctuations

The USD-INR exchange is an important component of the input

costs. Hence, a depreciation of INR vis-à-vis the USD could affect

the company's bottom line directly by way of gross margins.

Disruption in the supply chain

In a year of high uncertainty in the macro-environment and

geopolitical scenarios, disruptions in the supply chain are an

important risk to monitor. The unavailability of raw materials could

impact the estimates negatively.

Source: Company, HSIE Research

Page | 22

Berger Paints: Initiating Coverage

Financials Income Statement Year End (March) FY16 FY17 FY18 FY19 FY20P FY21E FY22E FY23E

Net Revenues 42,231 45,523 51,657 60,619 63,658 58,853 71,948 80,458

Growth (%) (2.3) 7.8 13.5 17.3 5.0 (7.5) 22.3 11.8

COGS 24,702 25,923 30,100 36,996 37,258 33,441 41,601 46,602

Employee Expense 2,735 3,067 3,566 4,085 4,525 4,826 5,180 5,753

A&P Expense 2,078 2,413 2,487 2,018 2,119 1,942 2,374 2,615

Freight and handling charges 2,898 3,209 3,360 3,834 4,026 4,002 4,569 5,109

Rent Expense 404 473 530 584 - - - -

Other Expenses 2,967 3,252 3,544 4,286 5,120 4,944 5,828 6,477

EBITDA 6,447 7,186 8,070 8,816 10,610 9,698 12,396 13,902

EBITDA Growth (%) 26.2 11.4 12.3 9.2 20.4 (8.6) 27.8 12.2

EBITDA Margin (%) 15.3 15.8 15.6 14.5 16.7 16.5 17.2 17.3

Depreciation 987 1,081 1,242 1,378 1,910 1,957 2,315 2,766

EBIT 5,461 6,105 6,828 7,438 8,700 7,742 10,081 11,136

Other Income (Including EO Items) 347 545 459 600 685 731 850 1,101

Interest 273 162 246 323 470 566 566 566

PBT 5,535 6,488 7,041 7,715 8,915 7,907 10,365 11,671

Total Tax 1,886 2,294 2,439 2,732 2,271 1,990 2,609 2,938

RPAT before associate earnings 3,649 4,194 4,602 4,984 6,644 5,917 7,756 8,734

Share of Associate earnings 57 101 6 (9) (83) (50) (50) (50)

Minority Interest - - - - - - - -

RPAT 3,706 4,295 4,608 4,975 6,561 5,867 7,706 8,684

Exceptional Gain/(loss) - 442 - - - - - -

Adjusted PAT 3,706 3,853 4,608 4,975 6,561 5,867 7,706 8,684

APAT Growth (%) 40.0 4.0 19.6 7.9 31.9 (10.6) 31.4 12.7

Adjusted EPS (Rs) 3.8 4.0 4.7 5.1 6.8 6.0 7.9 8.9

EPS Growth (%) (0.0) 4.0 19.6 7.9 31.9 (10.6) 31.4 12.7

Source: Company, HSIE Research

Balance Sheet Year End (March) FY16 FY17 FY18 FY19E FY20E FY21E FY22E FY23E

SOURCES OF FUNDS

Share Capital - Equity 694 971 971 971 971 971 971 971

Reserves 14,927 18,045 20,974 23,756 25,630 29,272 34,754 41,213

Total Shareholders Funds 15,621 19,016 21,945 24,727 26,601 30,243 35,725 42,184

Minority Interest - - - 35 71 121 171 221

Long Term Debt 2,108 2,621 2,495 2,389 2,073 2,073 2,073 2,073

Short Term Debt 1,437 1,441 1,727 2,811 3,286 3,286 3,286 3,286

Total Debt 3,544 4,062 4,222 5,201 5,359 5,359 5,359 5,359

Net Deferred Taxes 678 807 825 871 483 483 483 483

Other Non-current Liabilities & Provns 60 68 90 198 2,662 2,662 2,662 2,662

TOTAL SOURCES OF FUNDS 19,903 23,953 27,081 31,031 35,175 38,868 44,399 50,908

APPLICATION OF FUNDS

Net Block 7,765 9,571 10,026 11,029 13,288 12,649 16,178 16,601

CWIP 511 622 972 1,699 1,785 1,785 1,785 1,785

Goodwill 1,865 1,789 2,646 2,693 2,790 2,790 2,790 2,790

Other Non-current Assets 577 611 905 493 3,355 3,355 3,355 3,355

Total Non-current Assets 10,717 12,593 14,548 15,913 21,217 20,578 24,107 24,530

Investments 3,475 4,721 3,331 3,949 3,152 3,152 3,152 3,152

Inventories 7,332 9,355 10,073 12,335 12,785 12,416 14,390 15,981

Debtors 5,454 5,781 6,924 6,715 7,141 7,095 8,082 8,972

Other Current Assets 736 921 2,500 2,323 2,501 2,312 2,728 2,941

Cash & Equivalents 1,053 1,025 2,050 2,385 2,199 5,929 7,302 12,467

Total Current Assets 18,051 21,803 24,878 27,707 27,778 30,903 35,653 43,512

Creditors 6,699 7,612 9,553 9,990 10,658 9,674 11,768 13,094

Other Current Liabilities & Provns 2,166 2,831 2,793 2,599 3,162 2,939 3,593 4,040

Total Current Liabilities 8,865 10,443 12,345 12,589 13,820 12,613 15,361 17,134

Net Current Assets 9,186 11,360 12,533 15,118 13,958 18,289 20,292 26,378

TOTAL APPLICATION OF FUNDS 19,903 23,953 27,081 31,031 35,175 38,868 44,399 50,908

Source: Company, HSIE Research

Page | 23

Berger Paints: Initiating Coverage

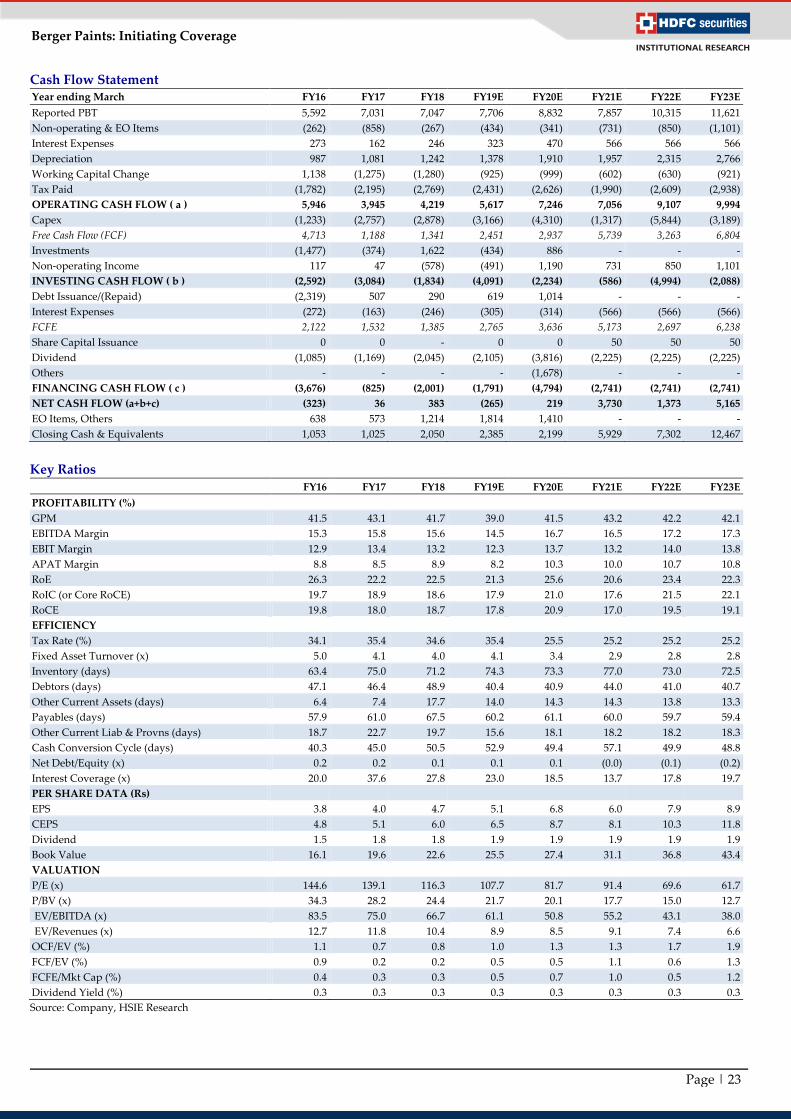

Cash Flow Statement Year ending March FY16 FY17 FY18 FY19E FY20E FY21E FY22E FY23E

Reported PBT 5,592 7,031 7,047 7,706 8,832 7,857 10,315 11,621

Non-operating & EO Items (262) (858) (267) (434) (341) (731) (850) (1,101)

Interest Expenses 273 162 246 323 470 566 566 566

Depreciation 987 1,081 1,242 1,378 1,910 1,957 2,315 2,766

Working Capital Change 1,138 (1,275) (1,280) (925) (999) (602) (630) (921)

Tax Paid (1,782) (2,195) (2,769) (2,431) (2,626) (1,990) (2,609) (2,938)

OPERATING CASH FLOW ( a ) 5,946 3,945 4,219 5,617 7,246 7,056 9,107 9,994

Capex (1,233) (2,757) (2,878) (3,166) (4,310) (1,317) (5,844) (3,189)

Free Cash Flow (FCF) 4,713 1,188 1,341 2,451 2,937 5,739 3,263 6,804

Investments (1,477) (374) 1,622 (434) 886 - - -

Non-operating Income 117 47 (578) (491) 1,190 731 850 1,101

INVESTING CASH FLOW ( b ) (2,592) (3,084) (1,834) (4,091) (2,234) (586) (4,994) (2,088)

Debt Issuance/(Repaid) (2,319) 507 290 619 1,014 - - -

Interest Expenses (272) (163) (246) (305) (314) (566) (566) (566)

FCFE 2,122 1,532 1,385 2,765 3,636 5,173 2,697 6,238

Share Capital Issuance 0 0 - 0 0 50 50 50

Dividend (1,085) (1,169) (2,045) (2,105) (3,816) (2,225) (2,225) (2,225)

Others - - - - (1,678) - - -

FINANCING CASH FLOW ( c ) (3,676) (825) (2,001) (1,791) (4,794) (2,741) (2,741) (2,741)

NET CASH FLOW (a+b+c) (323) 36 383 (265) 219 3,730 1,373 5,165

EO Items, Others 638 573 1,214 1,814 1,410 - - -

Closing Cash & Equivalents 1,053 1,025 2,050 2,385 2,199 5,929 7,302 12,467

Key Ratios FY16 FY17 FY18 FY19E FY20E FY21E FY22E FY23E

PROFITABILITY (%)

GPM 41.5 43.1 41.7 39.0 41.5 43.2 42.2 42.1

EBITDA Margin 15.3 15.8 15.6 14.5 16.7 16.5 17.2 17.3

EBIT Margin 12.9 13.4 13.2 12.3 13.7 13.2 14.0 13.8

APAT Margin 8.8 8.5 8.9 8.2 10.3 10.0 10.7 10.8

RoE 26.3 22.2 22.5 21.3 25.6 20.6 23.4 22.3

RoIC (or Core RoCE) 19.7 18.9 18.6 17.9 21.0 17.6 21.5 22.1

RoCE 19.8 18.0 18.7 17.8 20.9 17.0 19.5 19.1

EFFICIENCY

Tax Rate (%) 34.1 35.4 34.6 35.4 25.5 25.2 25.2 25.2

Fixed Asset Turnover (x) 5.0 4.1 4.0 4.1 3.4 2.9 2.8 2.8

Inventory (days) 63.4 75.0 71.2 74.3 73.3 77.0 73.0 72.5

Debtors (days) 47.1 46.4 48.9 40.4 40.9 44.0 41.0 40.7

Other Current Assets (days) 6.4 7.4 17.7 14.0 14.3 14.3 13.8 13.3

Payables (days) 57.9 61.0 67.5 60.2 61.1 60.0 59.7 59.4

Other Current Liab & Provns (days) 18.7 22.7 19.7 15.6 18.1 18.2 18.2 18.3

Cash Conversion Cycle (days) 40.3 45.0 50.5 52.9 49.4 57.1 49.9 48.8

Net Debt/Equity (x) 0.2 0.2 0.1 0.1 0.1 (0.0) (0.1) (0.2)

Interest Coverage (x) 20.0 37.6 27.8 23.0 18.5 13.7 17.8 19.7

PER SHARE DATA (Rs)

EPS 3.8 4.0 4.7 5.1 6.8 6.0 7.9 8.9

CEPS 4.8 5.1 6.0 6.5 8.7 8.1 10.3 11.8

Dividend 1.5 1.8 1.8 1.9 1.9 1.9 1.9 1.9

Book Value 16.1 19.6 22.6 25.5 27.4 31.1 36.8 43.4

VALUATION

P/E (x) 144.6 139.1 116.3 107.7 81.7 91.4 69.6 61.7

P/BV (x) 34.3 28.2 24.4 21.7 20.1 17.7 15.0 12.7

EV/EBITDA (x) 83.5 75.0 66.7 61.1 50.8 55.2 43.1 38.0

EV/Revenues (x) 12.7 11.8 10.4 8.9 8.5 9.1 7.4 6.6

OCF/EV (%) 1.1 0.7 0.8 1.0 1.3 1.3 1.7 1.9

FCF/EV (%) 0.9 0.2 0.2 0.5 0.5 1.1 0.6 1.3

FCFE/Mkt Cap (%) 0.4 0.3 0.3 0.5 0.7 1.0 0.5 1.2

Dividend Yield (%) 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3

Source: Company, HSIE Research

Page | 24

Berger Paints: Initiating Coverage

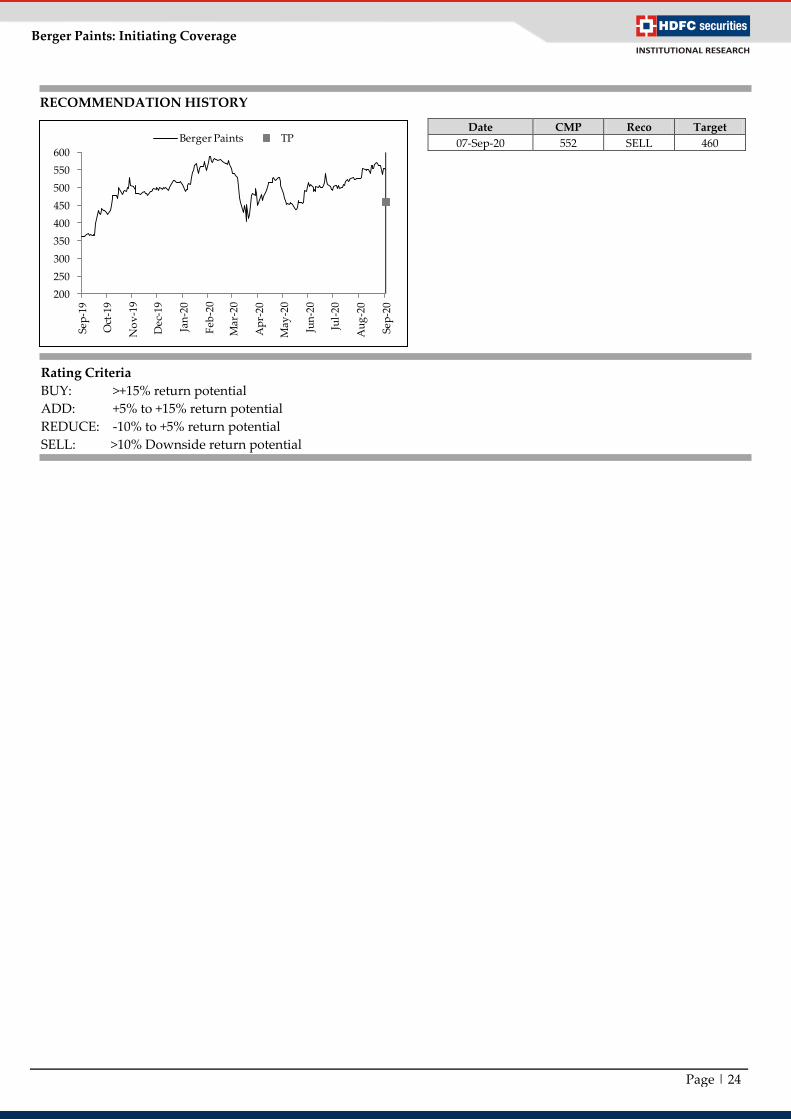

RECOMMENDATION HISTORY

200

250

300

350

400

450

500

550

600

Sep

-19

Oct

-19

No

v-1

9

Dec

-19

Jan

-20

Feb

-20

Mar

-20

Ap

r-20

May

-20

Jun

-20

Jul-

20

Au

g-2

0

Sep

-20

Berger Paints TPDate CMP Reco Target

07-Sep-20 552 SELL 460

Rating Criteria

BUY: >+15% return potential

ADD: +5% to +15% return potential

REDUCE: -10% to +5% return potential

SELL: >10% Downside return potential

Page | 25

Berger Paints: Initiating Coverage

Disclosure:

We, Jay Gandhi, MBA & Varun Lohchab, PGDM, authors and the names subscribed to this report, hereby certify that all of the views expressed in this

research report accurately reflect our views about the subject issuer(s) or securities. HSL has no material adverse disciplinary history as on the date of

publication of this report. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or

view(s) in this report.

Research Analyst or his/her relative or HDFC Securities Ltd. does not have any financial interest in the subject company. Also, Research Analyst or his relative

or HDFC Securities Ltd. or its Associate may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding

the date of publication of the Research Report. Further Research Analyst or his relative or HDFC Securities Ltd. or its associate does not have any material

conflict of interest.

Any holding in stock –No

HDFC Securities Limited (HSL) is a SEBI Registered Research Analyst having registration no. INH000002475.

Disclaimer:

This report has been prepared by HDFC Securities Ltd and is solely for information of the recipient only. The report must not be used as a singular basis of any

investment decision. The views herein are of a general nature and do not consider the risk appetite or the particular circumstances of an individual investor;

readers are requested to take professional advice before investing. Nothing in this document should be construed as investment advice. Each recipient of this

document should make such investigations as they deem necessary to arrive at an independent evaluation of an investment in securities of the companies

referred to in this document (including merits and risks) and should consult their own advisors to determine merits and risks of such investment. The

information and opinions contained herein have been compiled or arrived at, based upon information obtained in good faith from sources believed to be

reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy,

completeness or correctness. All such information and opinions are subject to change without notice. Descriptions of any company or companies or their

securities mentioned herein are not intended to be complete. HSL is not obliged to update this report for such changes. HSL has the right to make changes and

modifications at any time.

This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person or entity who is a citizen

or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be

contrary to law or regulation or what would subject HSL or its affiliates to any registration or licensing requirement within such jurisdiction.

If this report is inadvertently sent or has reached any person in such country, especially, United States of America, the same should be ignored and brought to

the attention of the sender. This document may not be reproduced, distributed or published in whole or in part, directly or indirectly, for any purposes or in

any manner.

Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have an adverse effect on their value or

price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively

assume currency risk. It should not be considered to be taken as an offer to sell or a solicitation to buy any security.

This document is not, and should not, be construed as an offer or solicitation of an offer, to buy or sell any securities or other financial instruments. This report

should not be construed as an invitation or solicitation to do business with HSL. HSL may from time to time solicit from, or perform broking, or other services

for, any company mentioned in this mail and/or its attachments.

HSL and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of

the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a

market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any

other potential conflict of interests with respect to any recommendation and other related information and opinions.

HSL, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments

made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates,

diminution in the NAVs, reduction in the dividend or income, etc.

HSL and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities and financial instruments dealt

in the report, or may make sell or purchase or other deals in these securities from time to time or may deal in other securities of the companies / organizations

described in this report.

HSL or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject

company for any other assignment in the past twelve months.

HSL or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the

date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage

services or other advisory service in a merger or specific transaction in the normal course of business.

HSL or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with

preparation of the research report. Accordingly, neither HSL nor Research Analysts have any material conflict of interest at the time of publication of this

report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. HSL may

have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of

the subject company. We have not received any compensation/benefits from the subject company or third party in connection with the Research Report.

HDFC securities Limited, I Think Techno Campus, Building - B, "Alpha", Office Floor 8, Near Kanjurmarg Station, Opp. Crompton Greaves, Kanjurmarg

(East), Mumbai 400 042 Phone: (022) 3075 3400 Fax: (022) 2496 5066 Compliance Officer: Binkle R. Oza Email: [email protected] Phone: (022)

3045 3600

HDFC Securities Limited, SEBI Reg. No.: NSE, BSE, MSEI, MCX: INZ000186937; AMFI Reg. No. ARN: 13549; PFRDA Reg. No. POP: 11092018; IRDA

Corporate Agent License No.: CA0062; SEBI Research Analyst Reg. No.: INH000002475; SEBI Investment Adviser Reg. No.: INA000011538; CIN -

U67120MH2000PLC152193

HDFC securities

Institutional Equities

Unit No. 1602, 16th Floor, Tower A, Peninsula Business Park,

Senapati Bapat Marg, Lower Parel, Mumbai - 400 013

Board: +91-22-6171-7330 www.hdfcsec.com