dollarization and crises: ways in and out alejandro izquierdo de-dollarization strategies and...

TRANSCRIPT

Dollarization and Crises:Dollarization and Crises:Ways In and OutWays In and Out

Alejandro Izquierdo Alejandro Izquierdo

De-dollarization Strategies and De-dollarization Strategies and Domestic Currency Debt Markets in Domestic Currency Debt Markets in

Emerging EconomiesEmerging Economies

Okinawa, JapanOkinawa, Japan

April 8 2005April 8 2005

OutlineOutline

I.I. Sudden Stop, Devaluation and Dollarization: Sudden Stop, Devaluation and Dollarization: Key Facts Key Facts

II.II. Determinants of Sudden Stops: Domestic Determinants of Sudden Stops: Domestic Liability DollarizationLiability Dollarization

III.III. How did we get there?How did we get there?

IV.IV. Ways out: Successful ExperiencesWays out: Successful Experiences

-60000

-40000

-20000

0

20000

40000

60000

80000

100000

120000

1990

-I

1990

-III

1991

-I

1991

-III

1992

-I

1992

-III

1993

-I

1993

-III

1994

-I

1994

-III

1995

-I

1995

-III

1996

-I

1996

-III

1997

-I

1997

-III

1998

-I

1998

-III

1999

-I

1999

-III

2000

-I

2000

-III

2001

-I

2001

-III

2002

-I

2002

-III

2003

-I

2003

-III

2004

-I

2004

-III

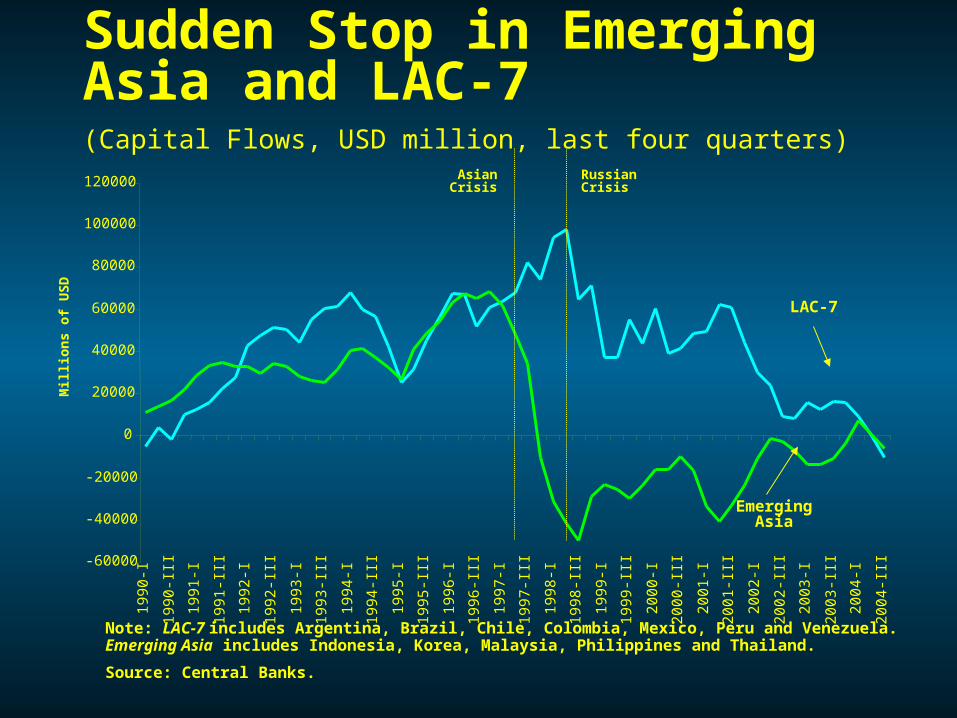

Sudden Stop in Emerging Asia and LAC-7 (Capital Flows, USD million, last four quarters)

Note: LAC-7 includes Argentina, Brazil, Chile, Colombia, Mexico, Peru and Venezuela. Emerging Asia includes Indonesia, Korea, Malaysia, Philippines and Thailand.

Source: Central Banks.

Asian Crisis

Russian Crisis

Mill

ion

s o

f U

SD

LAC-7

Emerging Asia

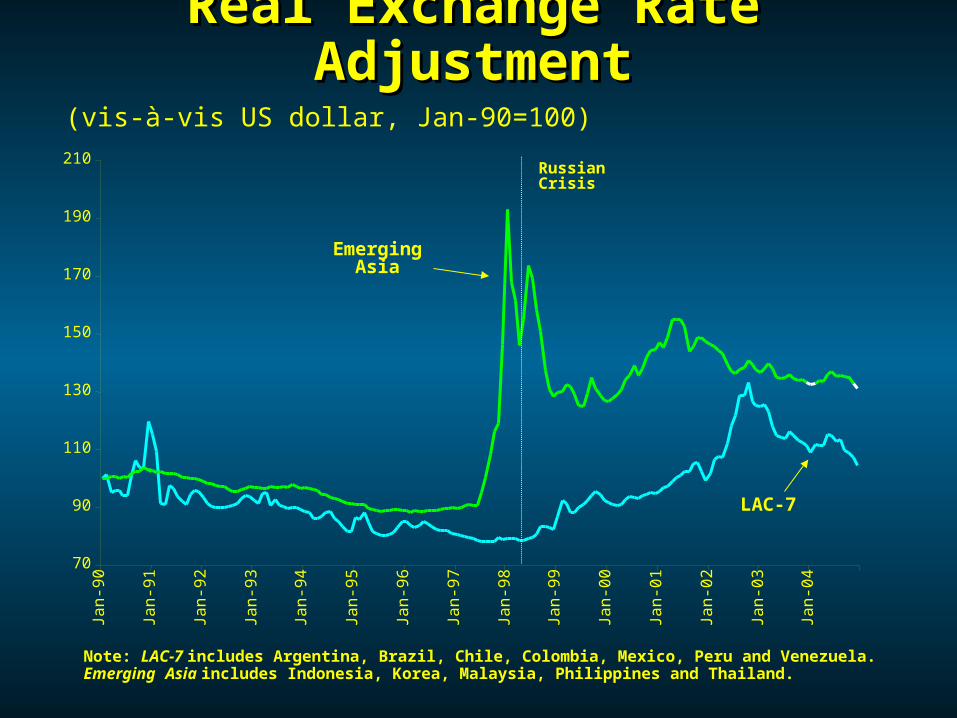

Real Exchange Rate AdjustmentReal Exchange Rate Adjustment(vis-à-vis US dollar, Jan-90=100)

70

90

110

130

150

170

190

210

Jan

-90

Jan

-91

Jan

-92

Jan

-93

Jan

-94

Jan

-95

Jan

-96

Jan

-97

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Emerging Asia

LAC-7

Russian Crisis

Note: LAC-7 includes Argentina, Brazil, Chile, Colombia, Mexico, Peru and Venezuela. Emerging Asia includes Indonesia, Korea, Malaysia, Philippines and Thailand.

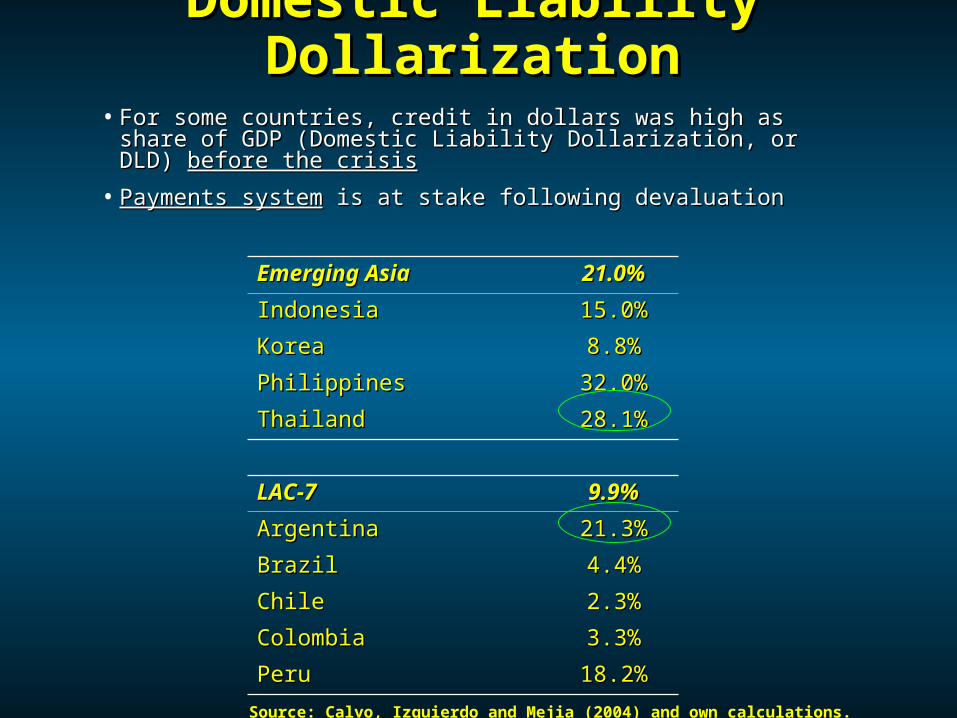

Domestic Liability DollarizationDomestic Liability Dollarization• For some countries, credit in dollars was high as share of GDP For some countries, credit in dollars was high as share of GDP

(Domestic Liability Dollarization, or DLD) (Domestic Liability Dollarization, or DLD) before the crisisbefore the crisis

• Payments systemPayments system is at stake following devaluation is at stake following devaluation

Emerging AsiaEmerging Asia 21.0%21.0%

IndonesiaIndonesia 15.0%15.0%

KoreaKorea 8.8%8.8%

PhilippinesPhilippines 32.0%32.0%

ThailandThailand 28.1%28.1%

LAC-7LAC-7 9.9%9.9%

ArgentinaArgentina 21.3%21.3%

BrazilBrazil 4.4%4.4%

ChileChile 2.3%2.3%

ColombiaColombia 3.3%3.3%

PeruPeru 18.2%18.2%

Source: Calvo, Izquierdo and Mejia (2004) and own calculations.

OutlineOutline

I.I. Sudden Stops and Devaluation: Key Facts Sudden Stops and Devaluation: Key Facts

II.II. Determinants of Sudden Stops: Domestic Determinants of Sudden Stops: Domestic Liability DollarizationLiability Dollarization

III.III. How did we get there?How did we get there?

IV.IV. Ways out: Successful ExperiencesWays out: Successful Experiences

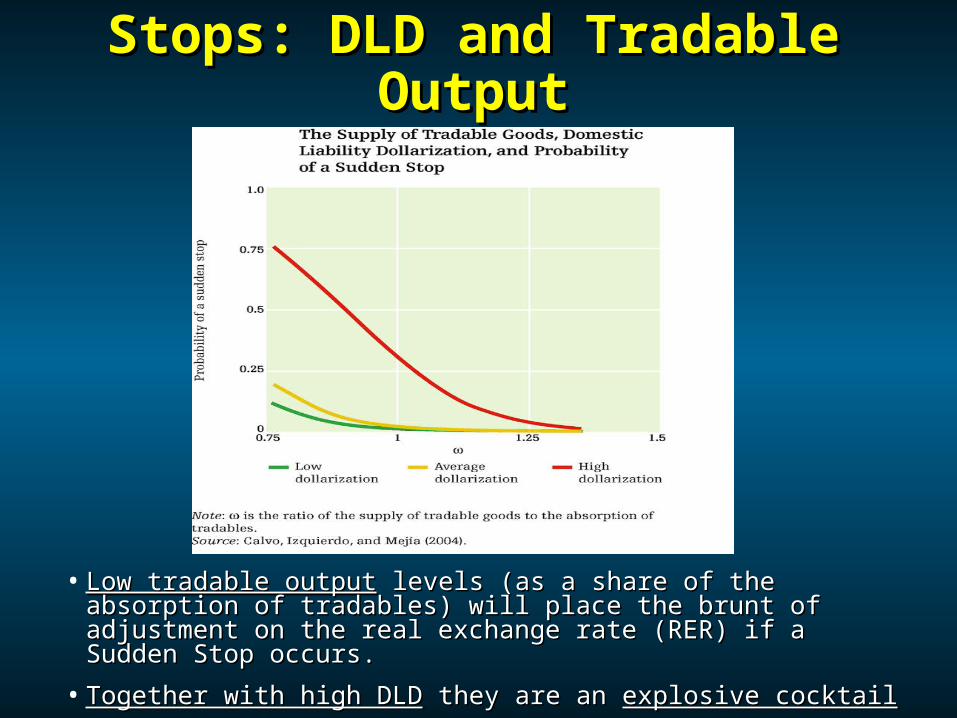

Determinants of Sudden Stops: Determinants of Sudden Stops: DLD and Tradable OutputDLD and Tradable Output

• Low tradable outputLow tradable output levels (as a share of the absorption levels (as a share of the absorption of tradables) will place the brunt of adjustment on the of tradables) will place the brunt of adjustment on the real exchange rate (RER) if a Sudden Stop occurs. real exchange rate (RER) if a Sudden Stop occurs.

• Together with high DLDTogether with high DLD they are an they are an explosive cocktailexplosive cocktail

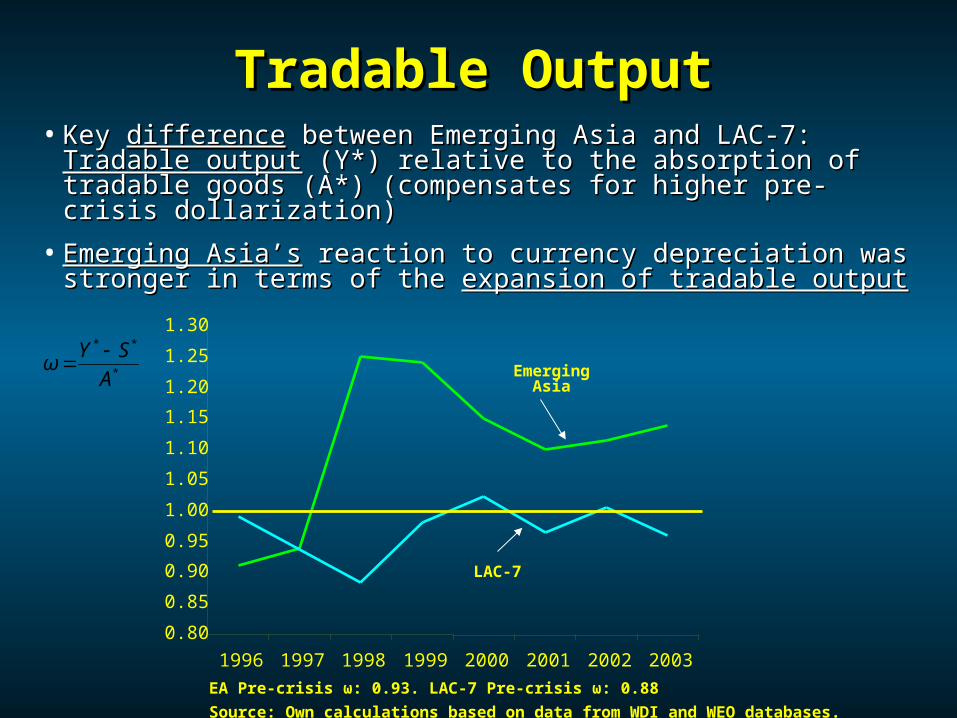

Tradable OutputTradable Output• Key Key differencedifference between Emerging Asia and LAC-7: between Emerging Asia and LAC-7:

Tradable outputTradable output (Y*) relative to the absorption of tradable (Y*) relative to the absorption of tradable goods (A*) (compensates for higher pre-crisis dollarization) goods (A*) (compensates for higher pre-crisis dollarization)

• Emerging Asia’sEmerging Asia’s reaction to currency depreciation was reaction to currency depreciation was stronger in terms of the stronger in terms of the expansion of tradable outputexpansion of tradable output

Source: Own calculations based on data from WDI and WEO databases.

*

**

A

SYω

EA Pre-crisis ω: 0.93. LAC-7 Pre-crisis ω: 0.88

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

1996 1997 1998 1999 2000 2001 2002 2003

Emerging Asia

LAC-7

Dollarization is an Addiction,Dollarization is an Addiction,Just Like SmokingJust Like Smoking

• We know that We know that dollarizationdollarization is bad for a is bad for a country’s health: it brings country’s health: it brings crisiscrisis (cancer) (cancer)

• As with any addiction, the first step is to As with any addiction, the first step is to acknowledge that there is a problem. But in acknowledge that there is a problem. But in order to quit, two questions must be order to quit, two questions must be answered:answered:

How do countries get hooked on smoking?How do countries get hooked on smoking?

Is there a “patch” to stop smoking?Is there a “patch” to stop smoking?

OutlineOutline

I.I. Sudden Stops, Devaluation and Dollarization: Sudden Stops, Devaluation and Dollarization: Key Facts Key Facts

II.II. Determinants of Sudden Stops: Domestic Determinants of Sudden Stops: Domestic Liability DollarizationLiability Dollarization

III.III. How did we get there?How did we get there?

IV.IV. Ways out: Successful ExperiencesWays out: Successful Experiences

Latin America: Macroeconomic Latin America: Macroeconomic Policies and Currency SubstitutionPolicies and Currency Substitution

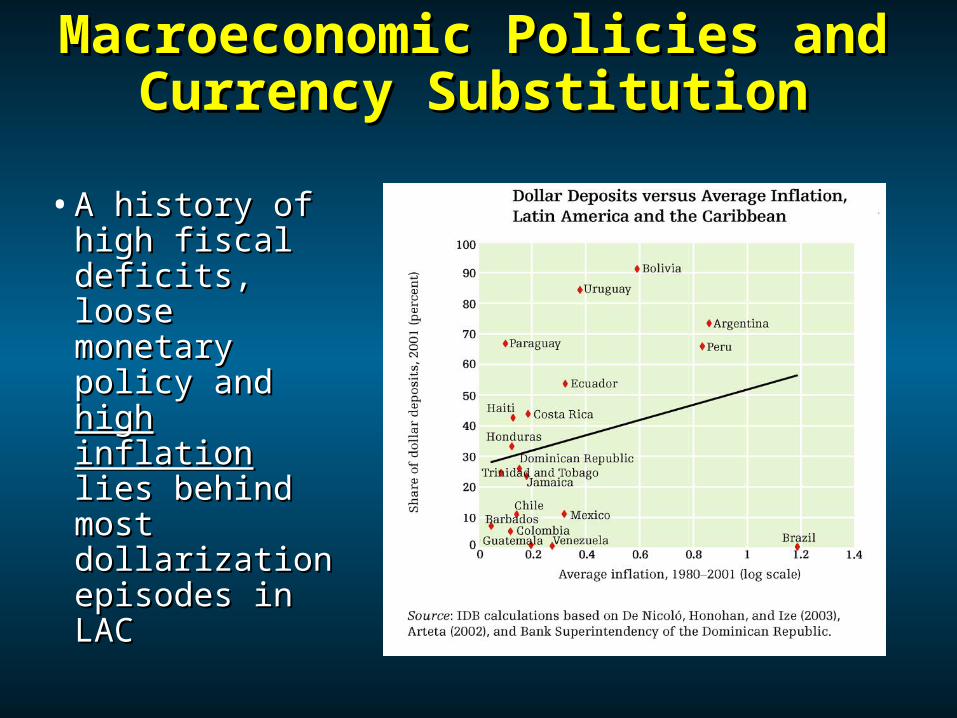

• A history of high A history of high fiscal deficits, fiscal deficits, loose monetary loose monetary policy and policy and high high inflationinflation lies lies behind most behind most dollarization dollarization episodes in LACepisodes in LAC

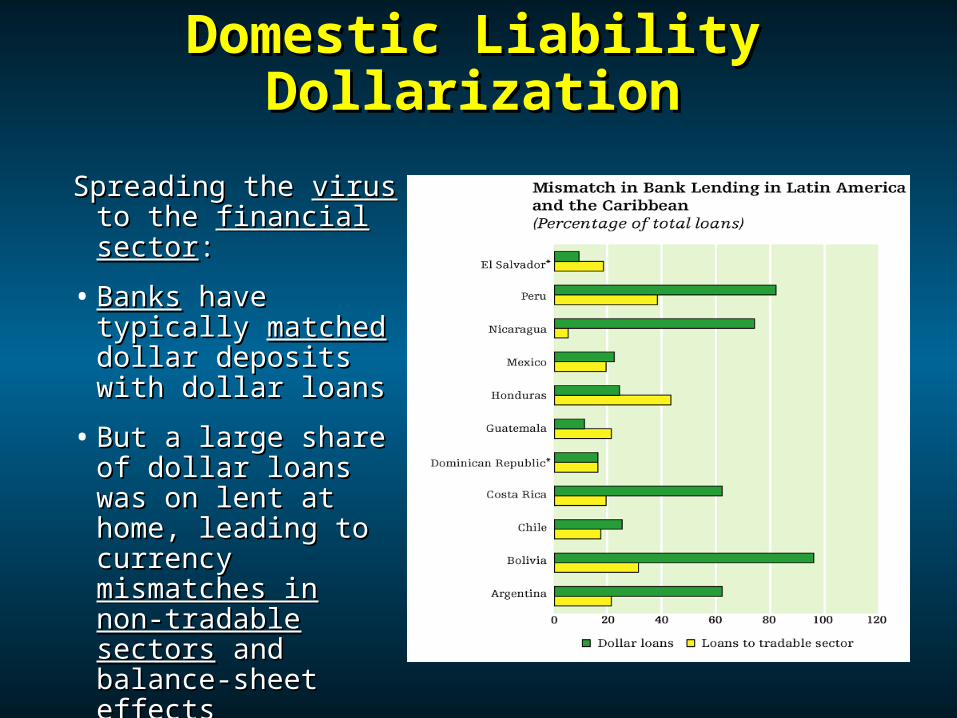

Domestic Liability DollarizationDomestic Liability Dollarization

Spreading the Spreading the virusvirus to to the the financial sectorfinancial sector::

• BanksBanks have typically have typically matchedmatched dollar dollar deposits with dollar deposits with dollar loansloans

• But a large share of But a large share of dollar loans was on dollar loans was on lent at home, leading lent at home, leading to currency to currency mismatches in non-mismatches in non-tradabletradable sectorssectors and and balance-sheet balance-sheet effectseffects

Emerging Asia: Bank Foreign Borrowing(Foreign Liabilities / (Total Deposits + Foreign Liabilities))

Note : Average for Indonesia, Korea, Malaysia, Philippines and Thailand. Source: IFS

5%

10%

15%

20%

25%

30%

Jan-

93

Jul-9

3

Jan-

94

Jul-9

4

Jan-

95

Jul-9

5

Jan-

96

Jul-9

6

Jan-

97

Jul-9

7

Jan-

98

Jul-9

8

Jan-

99

Jul-9

9

Jan-

00

Jul-0

0

Jan-

01

Jul-0

1

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Asian Crisis Russian Crisis

OutlineOutline

I.I. Sudden Stops, Devaluation and Dollarization: Sudden Stops, Devaluation and Dollarization: Key Facts Key Facts

II.II. Determinants of Sudden Stops: Domestic Determinants of Sudden Stops: Domestic Liability DollarizationLiability Dollarization

III.III. How did we get there?How did we get there?

IV.IV. Ways outWays out

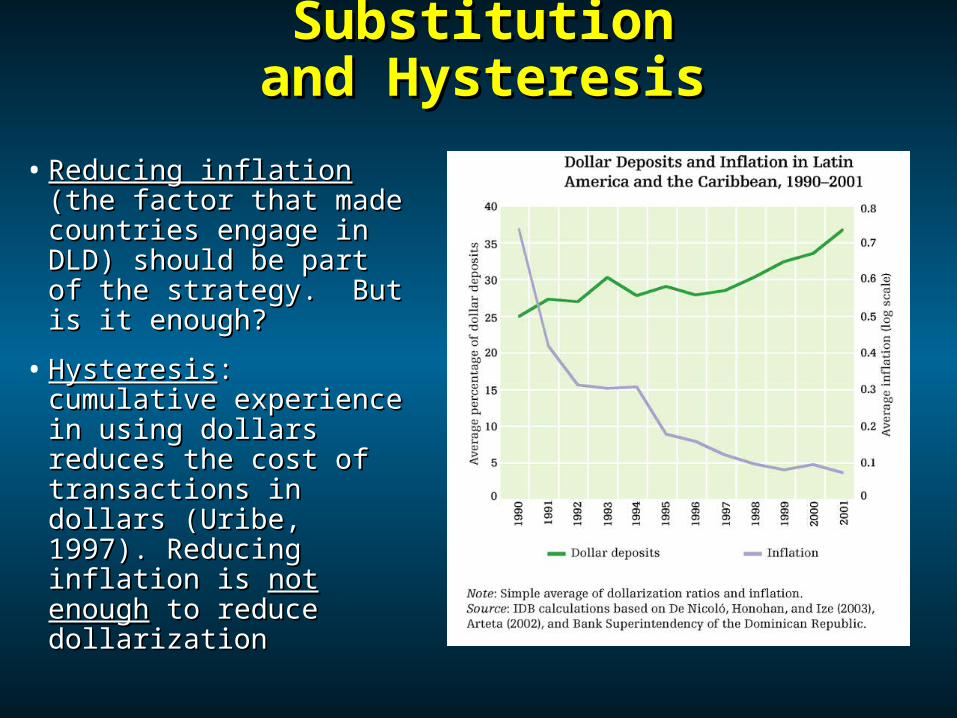

Latin America: Currency SubstitutionLatin America: Currency Substitutionand Hysteresisand Hysteresis

• Reducing inflationReducing inflation (the (the factor that made factor that made countries engage in countries engage in DLD) should be part of DLD) should be part of the strategy. But is it the strategy. But is it enough?enough?

• HysteresisHysteresis: cumulative : cumulative experience in using experience in using dollars reduces the cost dollars reduces the cost of transactions in dollars of transactions in dollars (Uribe, 1997). Reducing (Uribe, 1997). Reducing inflation is inflation is not enoughnot enough to to reduce dollarization reduce dollarization

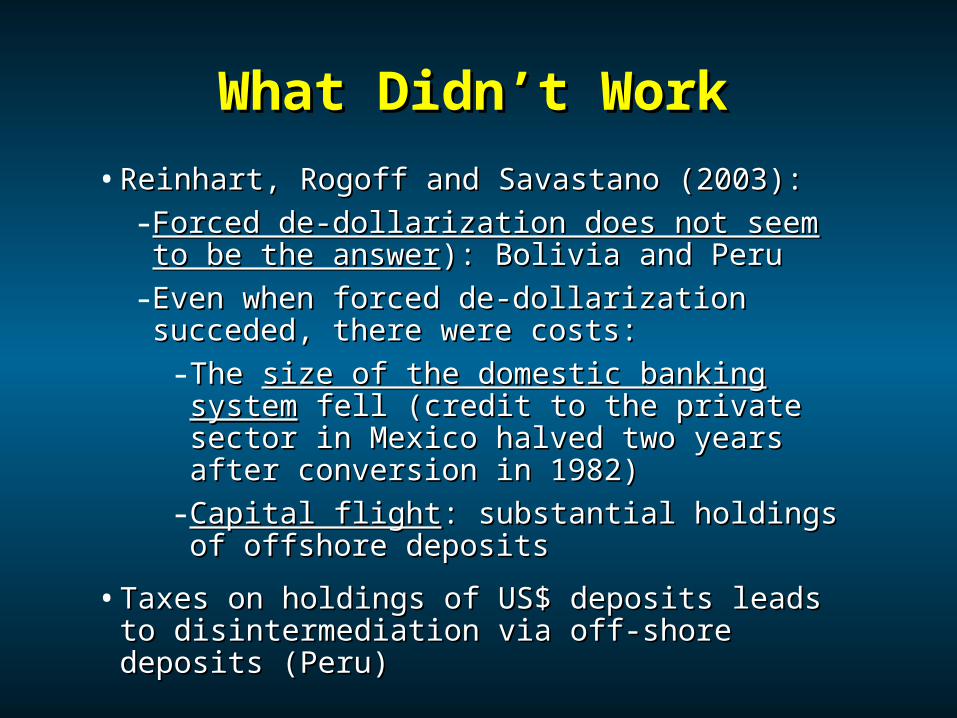

What Didn’t WorkWhat Didn’t Work

• Reinhart, Rogoff and Savastano (2003):Reinhart, Rogoff and Savastano (2003):

- Forced de-dollarization does not seem to be Forced de-dollarization does not seem to be the answerthe answer): Bolivia and Peru): Bolivia and Peru

- Even when forced de-dollarization succeded, Even when forced de-dollarization succeded, there were costs:there were costs:

- The The size of the domestic banking systemsize of the domestic banking system fell (credit to the private sector in Mexico fell (credit to the private sector in Mexico halved two years after conversion in 1982)halved two years after conversion in 1982)

- Capital flightCapital flight: substantial holdings of : substantial holdings of offshore deposits offshore deposits

• Taxes on holdings of US$ deposits leads to Taxes on holdings of US$ deposits leads to disintermediation via off-shore deposits (Peru)disintermediation via off-shore deposits (Peru)

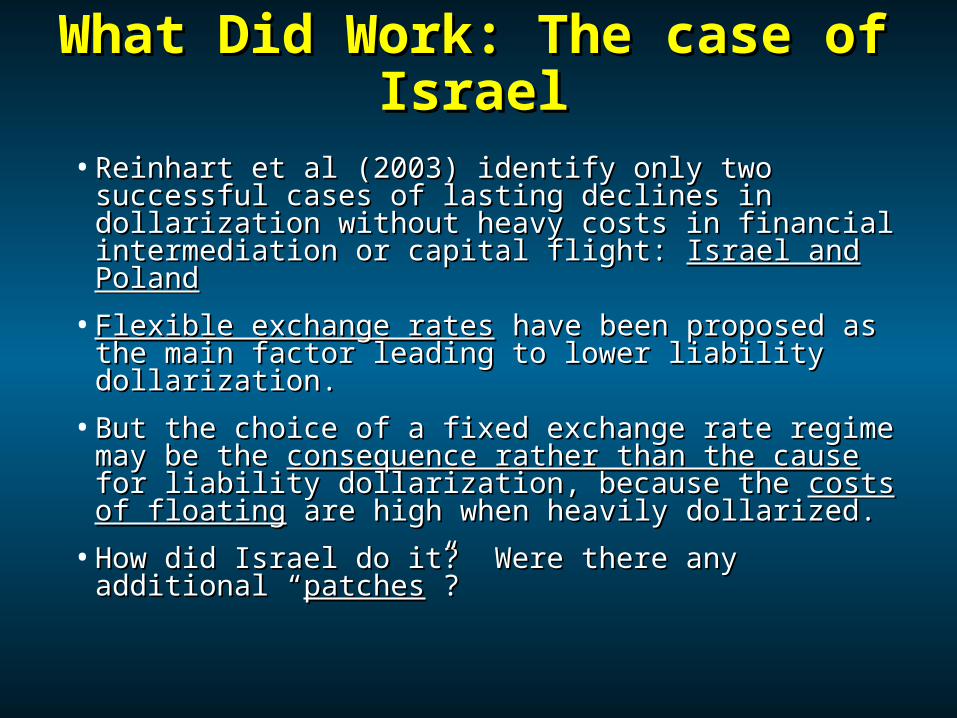

What Did Work: The case of IsraelWhat Did Work: The case of Israel• Reinhart et al (2003) identify only two successful Reinhart et al (2003) identify only two successful

cases of lasting declines in dollarization without cases of lasting declines in dollarization without heavy costs in financial intermediation or capital heavy costs in financial intermediation or capital flight: flight: Israel and PolandIsrael and Poland

• Flexible exchange ratesFlexible exchange rates have been proposed as the have been proposed as the main factor leading to lower liability dollarization. main factor leading to lower liability dollarization.

• But the choice of a fixed exchange rate regime may But the choice of a fixed exchange rate regime may be the be the consequence rather than the causeconsequence rather than the cause for for liability dollarization, because the liability dollarization, because the costs of floatingcosts of floating are high when heavily dollarized.are high when heavily dollarized.

• How did Israel do it? Were there any additional How did Israel do it? Were there any additional ““patchespatches”? ”?

Inflation & RER VolatilityInflation & RER Volatility

• If individuals care about buying a basket of goods, If individuals care about buying a basket of goods, they will allocate their savings so that they they will allocate their savings so that they minimize minimize the riskthe risk of being unable to buy that basket. of being unable to buy that basket.

• The The return on dollar depositsreturn on dollar deposits depends on the dollar depends on the dollar price of that basket (price of that basket (RER depreciation)RER depreciation)

• While the While the return on domestic-currency depositsreturn on domestic-currency deposits depends on the “peso” price of that basket (depends on the “peso” price of that basket (inflation)inflation)

• Low Low volatilityvolatility of inflation of inflation relativerelative to the volatility of to the volatility of RER depreciation should lead to de-dollarization.RER depreciation should lead to de-dollarization.

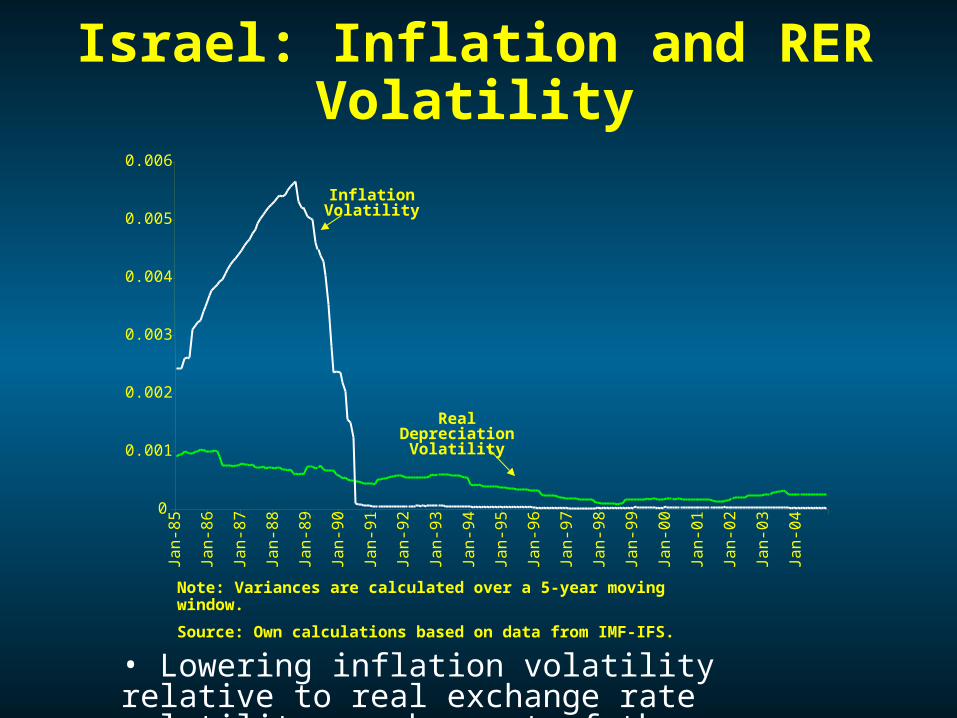

Israel: Inflation and RER Volatility

Note: Variances are calculated over a 5-year moving window.

Source: Own calculations based on data from IMF-IFS.

0

0.001

0.002

0.003

0.004

0.005

0.006Ja

n-8

5

Jan

-86

Jan

-87

Jan

-88

Jan

-89

Jan

-90

Jan

-91

Jan

-92

Jan

-93

Jan

-94

Jan

-95

Jan

-96

Jan

-97

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Inflation Volatility

Real Depreciation

Volatility

• Lowering inflation volatility relative to real exchange rate volatility may be part of the answer

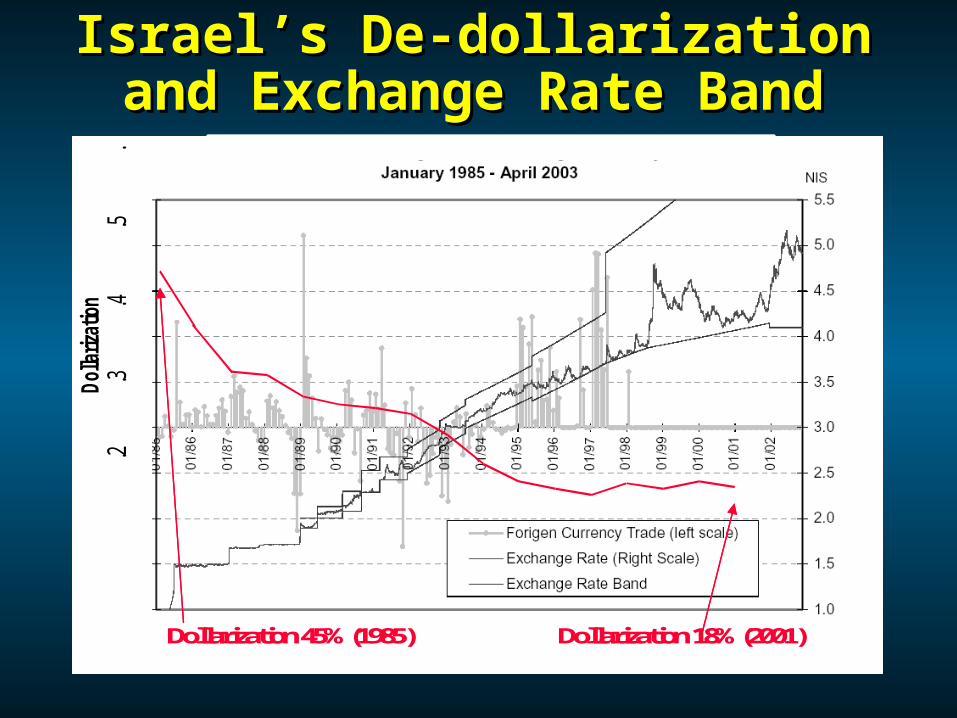

Israel’s De-dollarization and Israel’s De-dollarization and Exchange Rate BandExchange Rate Band

.2.3

.4.5

.

Dolla

riza

tion

Dollarization44% (1985) Dollarization17% (2001)

.2.3

.4.5

.

Dolla

riza

tion

Dollarization45% (1985) Dollarization18% (2001)

.2.3

.4.5

.

Dolla

riza

tion

Dollarization44% (1985) Dollarization17% (2001)

.2.3

.4.5

.

Dolla

riza

tion

Dollarization45% (1985) Dollarization18% (2001)

.2.3

.4.5

.

Dolla

riza

tion

Dollarization44% (1985) Dollarization17% (2001)

.2.3

.4.5

.

Dolla

riza

tion

Dollarization45% (1985) Dollarization18% (2001)

.2.3

.4.5

.

Dolla

riza

tion

Dollarization44% (1985) Dollarization17% (2001)

.2.3

.4.5

.

Dolla

riza

tion

Dollarization45% (1985) Dollarization18% (2001)

Or was it Also the “Patches”or Or was it Also the “Patches”or Additional Measures?Additional Measures?

But Israel also pursued additional policies (Galindo But Israel also pursued additional policies (Galindo and Leiderman (2003)), many of them “and Leiderman (2003)), many of them “patchespatches” ” to to reduce the costs of floatingreduce the costs of floating::

• Initially, one year mandatory holding period Initially, one year mandatory holding period for dollar depositsfor dollar deposits

• Offered Offered CPI-indexedCPI-indexed deposits deposits• Banks required active Banks required active hedginghedging of currency of currency

risk for risk for non-tradable activitiesnon-tradable activities• Active development of Active development of financial derivativesfinancial derivatives

marketsmarkets• Made effort to Made effort to deepen local currency bonddeepen local currency bond

marketsmarkets

And it worked: deposit dollarization went down to And it worked: deposit dollarization went down to 18% of total deposits (2001) from 45% (1985)18% of total deposits (2001) from 45% (1985)

The Current Situation: Long-run The Current Situation: Long-run Trend or Short-run Opportunism?Trend or Short-run Opportunism?

Renewed interest in domestic currency Renewed interest in domestic currency lending (e.g., the case of Colombia, 2004):lending (e.g., the case of Colombia, 2004):

- Is it “Leaning against the wind” policies Is it “Leaning against the wind” policies and and appreciation expectationsappreciation expectations? Or,? Or,

- Based on the Argentine experience: can it Based on the Argentine experience: can it be be more costly to lend in dollarsmore costly to lend in dollars??

The Role of IFIs?The Role of IFIs?

• Multilateral lending in domestic currency, Multilateral lending in domestic currency, hedging currency riskhedging currency risk with the recipient with the recipient country: To what extent does this shield EMs country: To what extent does this shield EMs from the effects of dollarization?from the effects of dollarization?

• Issuance of Issuance of domestic-currency multilateral domestic-currency multilateral debtdebt in the recipient country (on lent in in the recipient country (on lent in domestic currency): Will it crowd out domestic currency): Will it crowd out issuance of public debt?issuance of public debt? (country risk vs. (country risk vs. exchange rate risk).exchange rate risk).

Dollarization and Crises:Dollarization and Crises:Ways In and OutWays In and Out

Alejandro Izquierdo Alejandro Izquierdo

De-dollarization Strategies and Domestic De-dollarization Strategies and Domestic Currency Debt Markets in Emerging Currency Debt Markets in Emerging

EconomiesEconomies

Okinawa, JapanOkinawa, Japan

April 8 2005April 8 2005