doing the right thing and knowing the standards - icpas€¦ · doing the right thing and knowing...

TRANSCRIPT

Dave Cotton, CPA, CFE, CGFM

Cotton & Company LLP

Alexandria, Virginia

Doing the Right Thing and Knowing the Standards

2014 Government Conference

28-‐29 April 2014

DAVID L. COTTON, CPA, CFE, CGFM COTTON & COMPANY LLP CHAIRMAN

Dave Cotton is chairman of Cotton & Company LLP, Certified Public Accountants. Cotton & Company is headquartered in Alexandria, Virginia. The firm was founded in 1981 and has a practice concentration in assisting Federal and State government agencies, inspectors general, and government grantees and contractors with a variety of government program-‐related assurance and advisory services. Cotton & Company has performed grant and contract, indirect cost rate, financial statement, financial related, and performance audits for more than two dozen Federal inspectors general as well as numerous other Federal and State agencies and programs. Cotton & Company’s Federal agency audit clients have included the U.S. Government Accountability Office, the U.S. House of Representatives, the U.S. Capitol Police, the U.S. Small Business Administration, the U.S. Bureau of Prisons, the Millennium Challenge Corporation, the U.S. Marshals Service, and the Bureau of Alcohol, Tobacco, Firearms and Explosives. Cotton & Company also assists numerous Federal agencies in preparing financial statements and improving financial management, accounting, and internal control systems. Dave received a BS in mechanical engineering (1971) and an MBA in management science and labor relations (1972) from Lehigh University in Bethlehem, PA. He also pursued graduate studies in accounting and auditing at the University of Chicago, Graduate School of Business (1977 to 1978). He is a Certified Public Accountant (CPA), Certified Fraud Examiner (CFE), and Certified Government Financial Manager (CGFM). Dave served on the Advisory Council on Government Auditing Standards (the Council advises the United States Comptroller General on promulgation of Government Auditing Standards—GAO’s yellow book) from 2006 to 2009. He served on the Institute of Internal Auditors (IIA) Anti-‐Fraud Programs and Controls Task Force and co-‐authored Managing the Business Risk of Fraud: A Practical Guide. He served on the American Institute of CPAs Anti-‐Fraud Task Force and co-‐authored Management Override: The Achilles Heel of Fraud Prevention. He is the past-‐chairman of the AICPA Federal Accounting and Auditing Subcommittee and has served on the AICPA Governmental Account-‐ing and Auditing Committee and the Government Technical Standards Subcommittee of the AICPA Professional Ethics Executive Committee. He authored the AICPA’s 8-‐hour continuing professional education course, Joint and Indirect Cost Allocations—How to Prepare and Audit Them. Dave served on the board of the Virginia Society of Certified Public Accountants (VSCPA) and on the VSCPA Litigation Services Committee, Professional Ethics Committee, Quality Review Committee, and Governmental Accounting and Auditing Committee. He is member of the Greater Washington Society of CPAs (GWSCPA) and serves on the GWSCPA Professional Ethics Committee. He is a member of the Association of Government Accountants (AGA) and past-‐advisory board chairman and past-‐president of the AGA Northern Virginia Chapter. He is also a member of the Institute of Internal Auditors and the Association of Certified Fraud Examiners.

Dave has testified as an expert in governmental accounting, auditing, and fraud issues before the United States Court of Federal Claims and other administrative and judicial bodies. Dave has spoken frequently on cost accounting, professional ethics, and auditors’ fraud detection responsibilities under SAS 99, Consideration of Fraud in a Financial Statement Audit. He is an instructor for the George Washington University masters of accountancy program (Fraud Examination and Forensic Accounting), and instructs for the George Mason University Small Business Development Center (Fundamentals of Accounting for Government Contracts). Dave was the recipient of the AGA’s 2006 Barr Award (“to recognize the cumulative achievements of private sector individuals who throughout their careers have served as a role model for others and who have consistently exhibited the highest personal and professional standards”) as well as AGA’s 2012 Educator Award (“to recognize individuals who have made significant contributions to the education and training of government financial managers”).

dco$on@co$oncpa.com 1

2014 Government Conference

Ethics Pre-Quiz Which United States President promised to have the most ethical administration in history?

A. Barak Obama B. George W. Bush C. Bill Clinton D. George H. W. Bush E. Ronald Reagan F. Jimmy Carter G. Lyndon Johnson H. Richard Nixon

Why is it so difficult to be

ethical?

dco$on@co$oncpa.com 2

2014 Government Conference

A Theoretical Framework for Making Ethical

Decisions

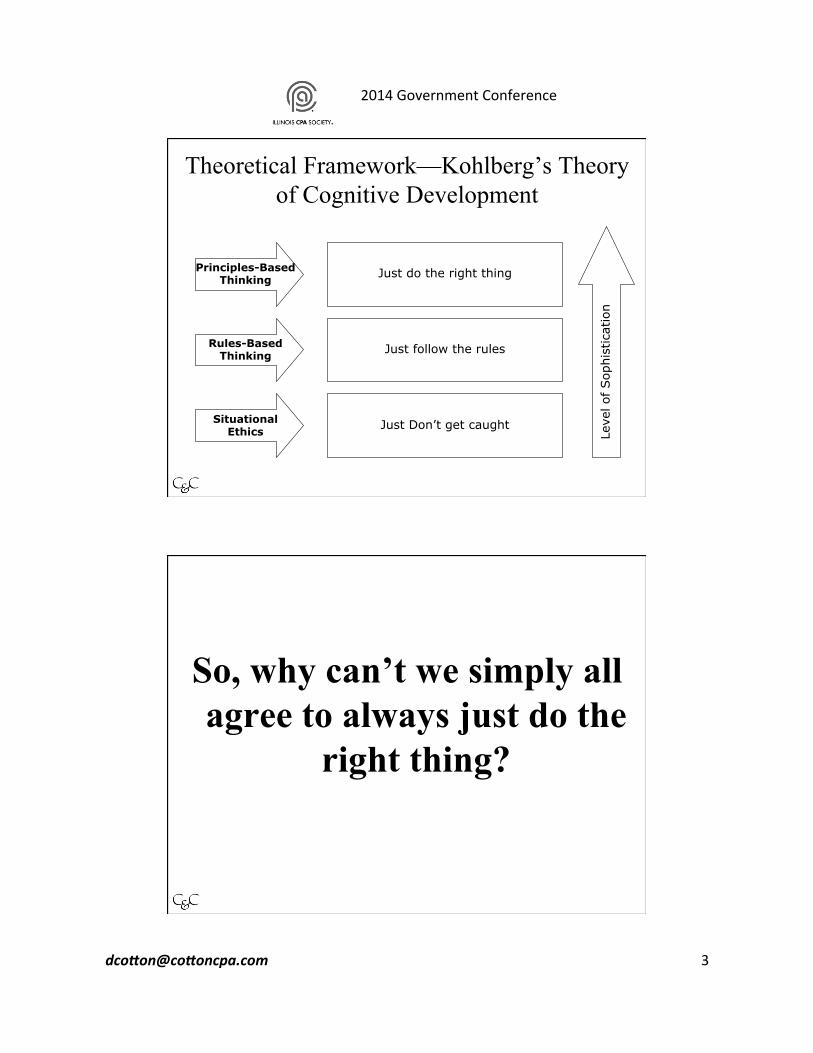

Theoretical Framework—Kohlberg’s Theory of Cognitive Development

Post-conventional Level

Pre-conventional Level

Conventional Level

Individual decides what is right or wrong using universal ethical

principles such as the common good and justice

Individual is concerned about expectations of significant others and relies upon rules and laws to determine what is right or wrong

Individual decides what is right or wrong based on consequences Le

vel o

f Sop

hist

icat

ion

Source: Auditors’ Ethical Reasoning: Insights from Past Research and Implications for the Future, Journal of Accounting Literature, 2003, By Jones, Joanne; Massey, Dawn W.; Thorne, Linda.

dco$on@co$oncpa.com 3

2014 Government Conference

Principles-Based Thinking

Situational Ethics

Rules-Based Thinking

Just do the right thing

Just follow the rules

Just Don’t get caught

Leve

l of Sop

hist

icat

ion

Theoretical Framework—Kohlberg’s Theory of Cognitive Development

So, why can’t we simply all agree to always just do the

right thing?

dco$on@co$oncpa.com 4

2014 Government Conference

Doing the Right Thing

Ø The Right Thing is not something about which everyone always agrees

Ø We are often oblivious to ethical dilemmas

Ø We have a strong ability to rationalize doing the wrong thing

Ø In some situations, it is impossible to follow all of the ethics rules

Ø “It’s the economy, stupid.” --James Carville, 1992

Ø “It’s the conflicts of interest, stupid.” --Dave Cotton, 2012

Doing the Right Thing: Where Should Our Focus Be?

dco$on@co$oncpa.com 5

2014 Government Conference

The Right Thing is not something about which everyone always agrees

Ø A trolley is running out of control down a track Ø In its path are 5 people who have been tied to the track by

a mad philosopher Ø Fortunately, you could flip a switch which will lead the

trolley down a different track to safety Ø Unfortunately, there is a single person tied to that track

Ø Should you flip the switch or do nothing?

Philippa Foot’s Trolley Problem

Philippa Foot, The Problem of Abortion and the Doctrine of the Double Effect in Virtues and Vices (Oxford: Basil Blackwell, 1978)(originally appeared in the Oxford Review, Number 5, 1967.)

dco$on@co$oncpa.com 6

2014 Government Conference

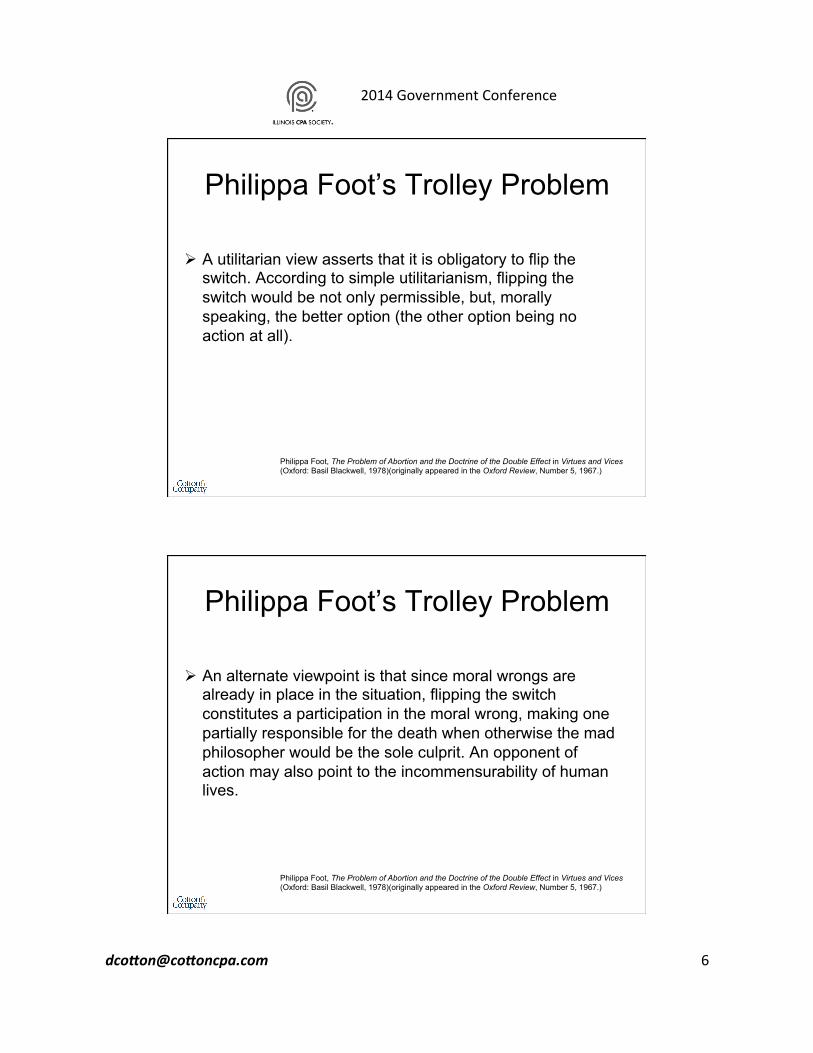

Ø A utilitarian view asserts that it is obligatory to flip the switch. According to simple utilitarianism, flipping the switch would be not only permissible, but, morally speaking, the better option (the other option being no action at all).

Philippa Foot’s Trolley Problem

Philippa Foot, The Problem of Abortion and the Doctrine of the Double Effect in Virtues and Vices (Oxford: Basil Blackwell, 1978)(originally appeared in the Oxford Review, Number 5, 1967.)

Ø An alternate viewpoint is that since moral wrongs are already in place in the situation, flipping the switch constitutes a participation in the moral wrong, making one partially responsible for the death when otherwise the mad philosopher would be the sole culprit. An opponent of action may also point to the incommensurability of human lives.

Philippa Foot’s Trolley Problem

Philippa Foot, The Problem of Abortion and the Doctrine of the Double Effect in Virtues and Vices (Oxford: Basil Blackwell, 1978)(originally appeared in the Oxford Review, Number 5, 1967.)

dco$on@co$oncpa.com 7

2014 Government Conference

Ø Under some interpretations of moral obligation, simply being present in this situation and being able to influence its outcome constitutes an obligation to participate. If this were the case, then deciding to do nothing would be considered an immoral act if one values five lives more than one.

Philippa Foot’s Trolley Problem

Philippa Foot, The Problem of Abortion and the Doctrine of the Double Effect in Virtues and Vices (Oxford: Basil Blackwell, 1978)(originally appeared in the Oxford Review, Number 5, 1967.)

Ø A trolley is running out of control down a track Ø In its path are 5 people who have been tied to the track by

a mad philosopher Ø Fortunately, you could flip a switch which will lead the

trolley down a different track to safety Ø Unfortunately, there is a single person—your mother—tied

to that track

Ø Should you flip the switch or do nothing?

Philippa Foot’s Trolley Problem

dco$on@co$oncpa.com 8

2014 Government Conference

We are often oblivious to ethical dilemmas

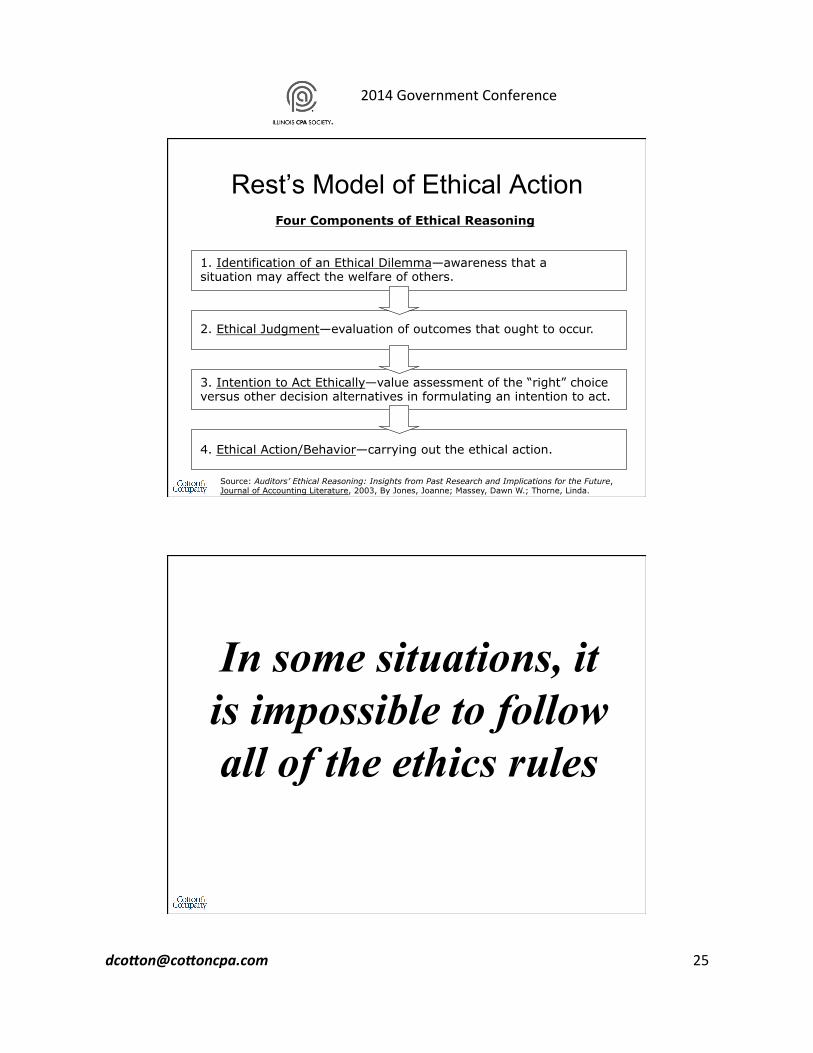

Rest’s Model of Ethical Action Four Components of Ethical Reasoning

1. Identification of an Ethical Dilemma—awareness that a situation may affect the welfare of others.

2. Ethical Judgment—evaluation of outcomes that ought to occur.

3. Intention to Act Ethically—value assessment of the “right” choice versus other decision alternatives in formulating an intention to act.

4. Ethical Action/Behavior—carrying out the ethical action.

Source: Auditors’ Ethical Reasoning: Insights from Past Research and Implications for the Future, Journal of Accounting Literature, 2003, By Jones, Joanne; Massey, Dawn W.; Thorne, Linda.

dco$on@co$oncpa.com 9

2014 Government Conference

You Make the Call • Ben Evolent is a member of the county council and

chairs the public works committee • Ben contacts each applicant for a project approval

and requests that the applicant make a voluntary donation to some deserving group; e.g. – The local high school track was repaved by a

developer ($125,000) – Another developer built new shelves for the

elementary school library ($20,000) • Ben keeps none of the donated money for himself

and always gives ample public credit to the donors.

You Make the Call

• Robin Plundar is a member of the county council and chairs the public works committee

• Robin contacts each applicant for a project approval and requests a “voluntary donation”

• Some applicants pay Robin the “donation” and their projects receive prompt approval

• Some applicants decline to pay the “donation” and their projects seem to take longer to receive approval

dco$on@co$oncpa.com 10

2014 Government Conference

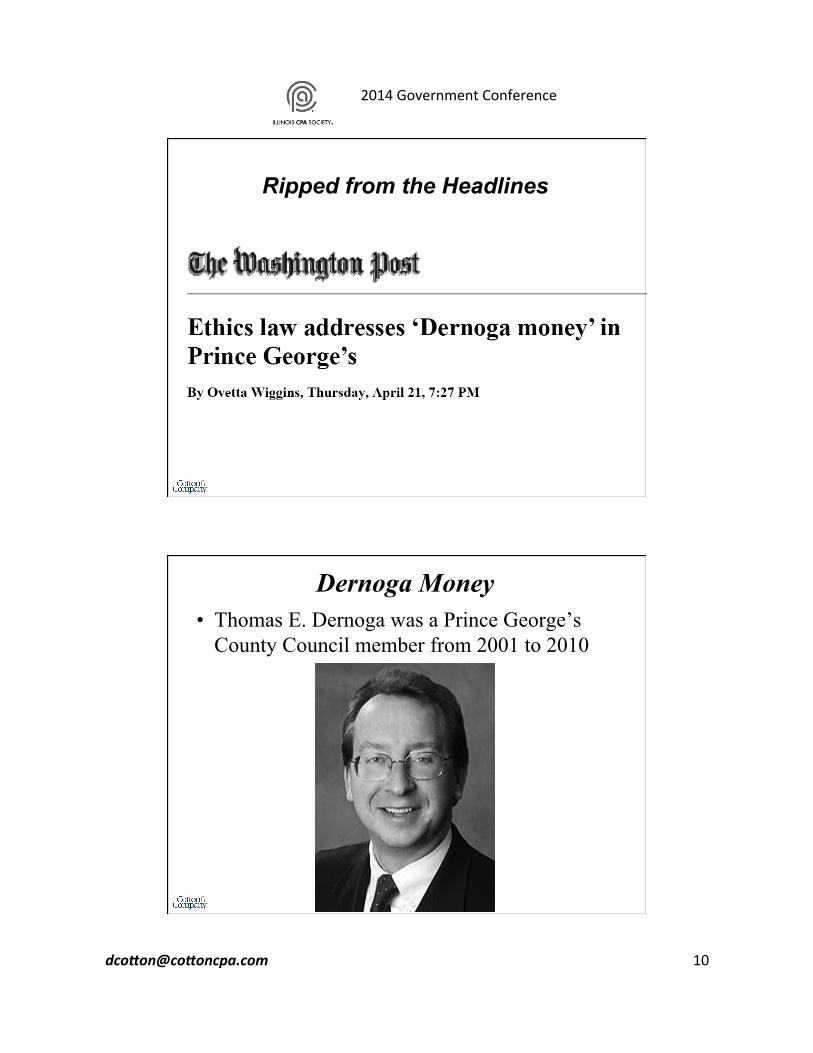

Ripped from the Headlines

Dernoga Money • Thomas E. Dernoga was a Prince George’s

County Council member from 2001 to 2010

dco$on@co$oncpa.com 11

2014 Government Conference

Dernoga Money • Thomas E. Dernoga “jokingly referred to himself as

Robin Hood.” • “contributions to various groups — which totaled

about $1 million during his eight years in office — were Dernoga’s way of getting developers to help improve the communities where they did business, he said.”

• “He said the track at High Point High School was resurfaced with $125,000 he got from a couple of developers, and the bookshelves at the Deerfield Elementary School library were restocked with $20,000 he got from another.”

Dernoga Money

• Dernoga said he “never held up a project because a developer had declined his requests for a donation.”

• He said he “never crossed any ethical or legal boundaries and never used the money for himself.”

• “Dernoga regularly presented checks at back-to-school nights and other programs in his Laurel district. Community and school leaders have called the donations ‘Dernoga money.’”

dco$on@co$oncpa.com 12

2014 Government Conference

Dernoga Money

Dernoga Money From the “Donor’s” Perspective

• “… representatives for developers … said they think it is inappropriate to be asked for money while seeking approval on a project.”

• “The solicitations came in private, and if the developers raised questions, their projects were delayed, they said.”

• “‘It seemed like by not playing the game, we were suffering,’ said a representative for one developer.”

dco$on@co$oncpa.com 13

2014 Government Conference

Classic Rationalizations • “If you don’t want to contribute, I’m not going to

hold it against your project,” he said. “I’ll treat your project fairly. But don’t come look to me for favors.”

• “Most of the people want a favor. They want more density. They want more parking. They all want something. They seem to think they are entitled. You say you want the county to do you a favor that might be good for the county, but it is also going to make you a lot of money. But are you willing to support local needs?”

Classic Rationalizations

• “You have these people making millions, and all this density and all the traffic [we’d] absorb on Route 1. You mean to tell me you have nothing to help out our schools?” Dernoga said. “I found it greedy on the part of the property owners.”

• “Dernoga said that project would have cost the main developers $120 million and that $100,000 would have been a ‘drop in the bucket,’”

dco$on@co$oncpa.com 14

2014 Government Conference

Corruption? • “Any scheme in which a person uses his or her

influence in a business transaction to obtain an unauthorized benefit contrary to that person’s duty to his or her employer.”

-- Fraud Examination, Third Edition, Albrecht, Albrecht, Albrecht, and Zimbelman, South-Western Cengage Learning, 2006

Public Corruption? • “Public corruption involves a breach of public trust

and/or abuse of position by federal, state, or local officials and their private sector accomplices. By broad definition, a government official, whether elected, appointed or hired, may violate federal law when he/she asks, demands, solicits, accepts, or agrees to receive anything of value in return for being influenced in the performance of their official duties.”

-- http://topics.law.cornell.edu/wex/public_corruption

dco$on@co$oncpa.com 15

2014 Government Conference

Was Dernoga a crook?

Or did Dernoga actually believe he was serving the

community by his actions and simply fail to see the ethical

failings of his actions?

Develop your ethical dilemma radar to increase the chances that you will

see ethical dilemmas

dco$on@co$oncpa.com 16

2014 Government Conference

In determining whether you have made the ‘right’ decision the chartered accountant should always pause and ask him/herself the following important questions: Ø Is my decision morally defensible? Ø Would a reasonable (and informed) third party reach the

same conclusion? Ø Will the decision potentially compromise my professional and/

or personal reputation? Ø If my decision was subject to public scrutiny would I, my

family and my colleagues be proud?

If there is any doubt in relation to any of the above questions then there is a threat that needs to be considered and addressed.

Practical Ethics—A Guide to Ethical Decision Making, Heather Briers, Director Professional Standards, Institute of Chartered Accountants in Ireland ,Conference 2005

Rationalizations—The Enemy of Clear Ethical

Thinking

dco$on@co$oncpa.com 17

2014 Government Conference

Classic Rationalizations The Golden Rationalization, or “Everybody does it” “based on the flawed assumption that the ethical nature of an act is somehow improved by the number of people who do it, and if ‘everybody does it,’ then it is implicitly all right for you to do it as well.” (Don’t single me out for your condemnation.)

Source: http://www.ethicsscoreboard.com/rb_fallacies.html

Classic Rationalizations The Gore Misdirection: "If it isn't illegal, it's ethical.“ “Al Gore earned himself a place in the Ethics Distortion Hall of Fame with his defense of the immortal Buddhist temple fundraising visit, in which he noted that because ‘no controlling legal authority’ had declared his visit illegal, it was therefore not an ethical violation.”

Source: http://www.ethicsscoreboard.com/rb_fallacies.html

dco$on@co$oncpa.com 18

2014 Government Conference

Classic Rationalizations Biblical Rationalizations “Judge not, lest ye not be judged” “Let him who is without sin cast the first stone” Imagine the world we would have if only perfect people were allowed to assess the behavior of others.

Source: http://www.ethicsscoreboard.com/rb_fallacies.html

Classic Rationalizations The "Tit for Tat" Excuse “the principle that bad or unethical behavior justifies, and somehow makes ethical, unethical behavior intended to counter it.” Oft-used rationalization for violating the FCPA.

Source: http://www.ethicsscoreboard.com/rb_fallacies.html

dco$on@co$oncpa.com 19

2014 Government Conference

Classic Rationalizations The Trivial Trap, Also known as "The Slippery Slope." “if no tangible harm arises from a deception or other unethical act, it cannot be ‘wrong:’ ‘No harm, no foul.’” “Before too long, one has embraced ‘the ends justify the means’ as an ethical system…”

Source: http://www.ethicsscoreboard.com/rb_fallacies.html

Classic Rationalizations The King’s Pass “One will often hear unethical behavior excused because the person involved is so important, so accomplished, and has done such great things for so many people that we should look the other way, just this once.”

Source: http://www.ethicsscoreboard.com/rb_fallacies.html

dco$on@co$oncpa.com 20

2014 Government Conference

Classic Rationalizations The Dissonance Drag

“… occurs when a person whom an individual regards highly adopts a behavior that the same individual deplores.” You “can lower [your] estimation of the person, or develop a rationalization for the conflict (the person was acting uncharacteristically due to illness, stress, or confusion), or reduce the disapproval of the behavior.”

Source: http://www.ethicsscoreboard.com/rb_fallacies.html

dco$on@co$oncpa.com 21

2014 Government Conference

Classic Rationalizations The Saint's License “This rationalization has probably caused more death and human suffering than any other. The words ‘it's for a good cause’ have been used to justify all sorts of lies, scams and mayhem.”

Source: http://www.ethicsscoreboard.com/rb_fallacies.html

Classic Rationalizations The Futility Illusion "If I don't do it, somebody else will."

“… middle managers go along with corporate shenanigans ordered by their bosses, making the calculation that their refusal will only hurt them without preventing the damage they have been asked to cause.” “The Futility Illusion is just a sad alternative to courage.”

Source: http://www.ethicsscoreboard.com/rb_fallacies.html

dco$on@co$oncpa.com 22

2014 Government Conference

Classic Rationalizations The Futility Illusion "If I don't do it, somebody else will."

“When Elliot Richardson was ordered by Richard Nixon to fire Watergate Special Prosecutor Archibald Cox, he refused and resigned. Cox ended up being fired anyway, but Richardson's protest helped turn public opinion against the White House.”

Courage can make a difference. Source: http://www.ethicsscoreboard.com/rb_fallacies.html

Classic Rationalizations Ethical Vigilantism

“addressing a real or imagined injustice by employing remedial cheating, lying, or other unethical means.”

“When a person who has been denied a raise he was promised surreptitiously charges personal expenses to a company credit card because ‘the company owes me’…”

Source: http://www.ethicsscoreboard.com/rb_fallacies.html

dco$on@co$oncpa.com 23

2014 Government Conference

Classic Rationalizations Hamm's Excuse: "It wasn't my fault.“ “confuses blame with responsibility. Carried to it worst extreme, Hamm's Excuse would eliminate all charity and much heroism, since it stands for the proposition that human beings are only responsible for alleviating problems that they were personally responsible for.”

Source: http://www.ethicsscoreboard.com/rb_fallacies.html

Classic Rationalizations Hamm's Excuse: "It wasn't my fault.“ “named after American gymnast Paul Hamm, who adamantly refused to voluntarily surrender the Olympic gold metal he admittedly had been awarded because of an official scoring error. His justification for this consisted of repeating that it was the erring officials, not him, who were responsible for the fact that the real winner of the competition was relegated to a bronze medal when he really deserved the gold.”

Source: http://www.ethicsscoreboard.com/rb_fallacies.html

dco$on@co$oncpa.com 24

2014 Government Conference

Classic Rationalizations The Comparative Virtue Excuse: “There are worse things.” “It is true that for most ethical misconduct, there are indeed ‘worse things.’ Lying to your boss in order to goof off at the golf course isn't as bad as stealing a ham, and stealing a ham is nothing compared selling military secrets to North Korea. So what? We judge human conduct against ideals of good behavior that we aspire to, not by the bad behavior of others”

Source: http://www.ethicsscoreboard.com/rb_fallacies.html

When you feel yourself beginning to rationalize, it’s a good sign that you

are confronting an ethical dilemma

dco$on@co$oncpa.com 25

2014 Government Conference

Rest’s Model of Ethical Action Four Components of Ethical Reasoning

1. Identification of an Ethical Dilemma—awareness that a situation may affect the welfare of others.

2. Ethical Judgment—evaluation of outcomes that ought to occur.

3. Intention to Act Ethically—value assessment of the “right” choice versus other decision alternatives in formulating an intention to act.

4. Ethical Action/Behavior—carrying out the ethical action.

Source: Auditors’ Ethical Reasoning: Insights from Past Research and Implications for the Future, Journal of Accounting Literature, 2003, By Jones, Joanne; Massey, Dawn W.; Thorne, Linda.

In some situations, it is impossible to follow all of the ethics rules

dco$on@co$oncpa.com 26

2014 Government Conference

You Make the Call

• Ivana Dotha-Righthing, CPA, has been engaged to audit the financial statements of “Bernie L. Madhatter Investment Securities LLC”

• Halfway through the audit, Ivana discovers that Bernie is not really investing his customers’ money as he is promising, but is instead just running a Ponzi scheme

• Ivana consults the AICPA Code of Professional Conduct for guidance

You Make the Call • Ivana notes that Article II—The Public

Interest, states that: Members should accept the obligation to act in a way that will serve the public interest, honor the public trust, and demonstrate commitment to professionalism.

• But then she sees that Rule 301—Confidential Client Information says that: A member in public practice shall not disclose any confidential client information without the specific consent of the client.

dco$on@co$oncpa.com 27

2014 Government Conference

You Make the Call What should Ivana do?

A—Ivana should resign from the engagement and uphold her very specific ethical obligation under Rule 301—Confidential Client Information. (That “Public Interest” thing is pretty general and kind of vague.)

B—Ivana should report what she has found to law enforcement authorities.

Good news if you do Yellow Book audits

GAGAS Paragraph 4.30 Auditors should report known or likely fraud, noncompliance with provisions of laws, regulations, contracts, or grant agreements, or abuse directly to parties outside the audited entity in the following two circumstances.

dco$on@co$oncpa.com 28

2014 Government Conference

Good news if you do Yellow Book audits

GAGAS Paragraph 4.30 a. When entity management fails to satisfy legal or regulatory

requirements to report such information to external parties specified in law or regulation, auditors should first communicate the failure to report such information to those charged with governance. If the audited entity still does not report this information to the specified external parties as soon as practicable after the auditors’ communication with those charged with governance, then the auditors should report the information directly to the specified external parties.

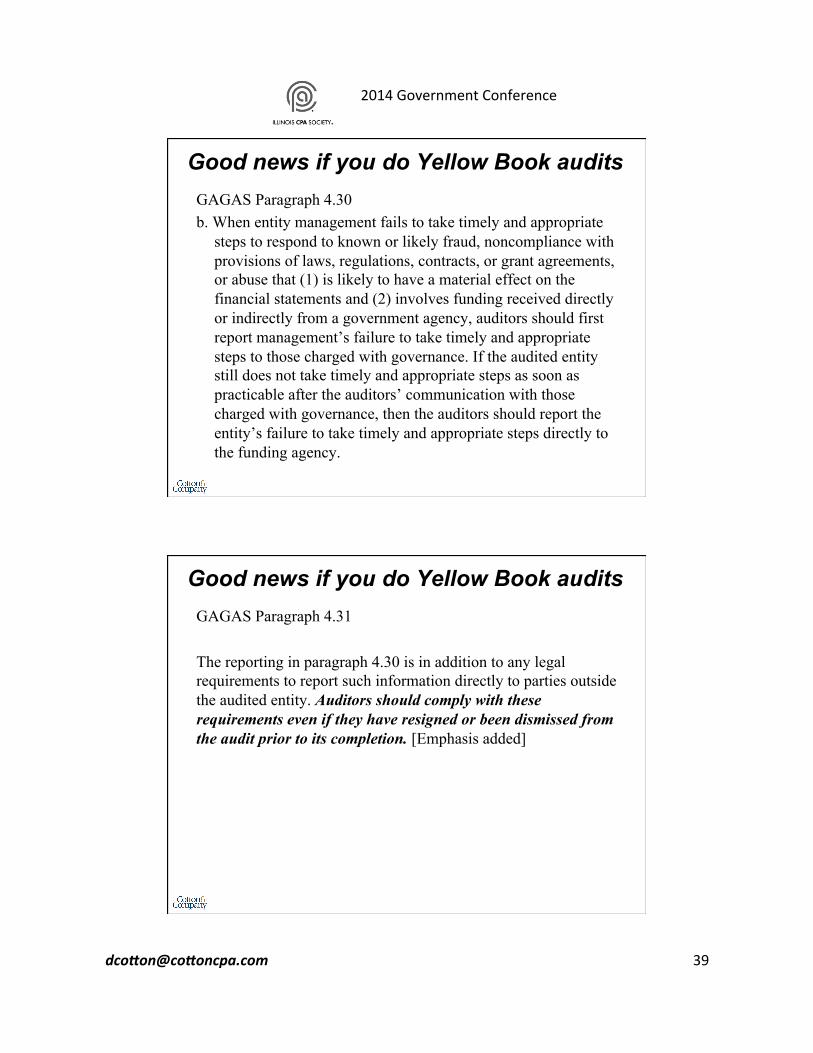

Good news if you do Yellow Book audits GAGAS Paragraph 4.30 b. When entity management fails to take timely and appropriate

steps to respond to known or likely fraud, noncompliance with provisions of laws, regulations, contracts, or grant agreements, or abuse that (1) is likely to have a material effect on the financial statements and (2) involves funding received directly or indirectly from a government agency, auditors should first report management’s failure to take timely and appropriate steps to those charged with governance. If the audited entity still does not take timely and appropriate steps as soon as practicable after the auditors’ communication with those charged with governance, then the auditors should report the entity’s failure to take timely and appropriate steps directly to the funding agency.

dco$on@co$oncpa.com 29

2014 Government Conference

Good news if you do Yellow Book audits GAGAS Paragraph 4.31 The reporting in paragraph 4.30 is in addition to any legal requirements to report such information directly to parties outside the audited entity. Auditors should comply with these requirements even if they have resigned or been dismissed from the audit prior to its completion. [Emphasis added]

It’s the conflicts of interest, stupid.

dco$on@co$oncpa.com 30

2014 Government Conference

The vast majority of ethical dilemmas we find ourselves facing

stem from conflicts of interest

AICPA’s Conceptual Framework: 7 Categories of Threats

1. Self-review 2. Advocacy 3. Adverse interest 4. Familiarity 5. Undue influence 6. Financial self-interest 7. Management participation

60"

dco$on@co$oncpa.com 31

2014 Government Conference

Independence v Conflict of Interest Ø Rule 101—Independence: 18,379 words Ø Rule 102-2—Conflicts of Interest: 451 words

Ø 2012 Yellow Book: “Independence” appears 167 times

Ø 2012 Yellow Book: “conflict of interest” appears 2 times

Independence v Conflict of Interest Ø Rule 101—Independence: 18,379 words

§ The word “interest” appears 117 time § The word “conflict” appears 0 times

Ø What’s up with that?

dco$on@co$oncpa.com 32

2014 Government Conference

Conflict of Interest A situation that has the potential to undermine the impartiality of a person because of the possibility of a clash between the person's self-interest and professional interest or public interest.

--www.businessdictionary.com A conflict between the private interests and the official responsibilities of a person in a position of trust.

--Merriam-Webster

Our Current Audit Model

Audit Firm Company Being Audited

Audit Report

Fees

dco$on@co$oncpa.com 33

2014 Government Conference

Congressional Hearing on Audit Quality Managing partner of firm that failed to note material misstatements in a governmental audit was being grilled by a congressman …

Congressman: “Isn’t it true that in the year of this audit period, your firm received more than $20 million in consulting fees from this government?”

Managing partner: “Congressman, my firm had $8.9 billion in revenue last year. We would never compromise our integrity for $20 million in consulting fees.”

Congressman: “Well, how much would it take?”

Our Current Audit Model

Audit Firm Company Being Audited

Audit Report

Fees

Not a Conflict of Interest Says the AICPA

dco$on@co$oncpa.com 34

2014 Government Conference

Rule 102-2, Conflicts of Interest

A conflict of interest may occur if a member performs a professional service for a client or employer and the member or his or her firm

has a relationship with another person, entity, product, or service that could, in the member's professional judgment, be viewed by the client,

employer, or other appropriate parties as impairing the member's objectivity.

What audit organizations find and report more fraud, waste, and abuse

than any others?

dco$on@co$oncpa.com 35

2014 Government Conference

Our Current Audit Model

Audit Firm Company Being Audited

Audit Report

Fees

Until we can find a better audit model, we better recognize that this IS a conflict of

interest and make sure we have safeguards in place that assure that we Do The Right Thing.

Independence Impairment versus

Conflict of Interest

• Is there really a difference? • No. • Ditch the 18,830 words in Rules 101 and

102-2 and replace them with 10 words • Avoid Conflicts of Interest and Just Do the

Right Thing

dco$on@co$oncpa.com 36

2014 Government Conference

In some situations, it is impossible to follow all of the ethics rules

You Make the Call

• Ivana Dotha-Righthing, CPA, has been engaged to audit the financial statements of “Bernie L. Madhatter Investment Securities LLC”

• Halfway through the audit, Ivana discovers that Bernie is not really investing his customers’ money as he is promising, but is instead just running a Ponzi scheme

• Ivana consults the AICPA Code of Professional Conduct for guidance

dco$on@co$oncpa.com 37

2014 Government Conference

You Make the Call • Ivana notes that Article II—The Public

Interest, states that: Members should accept the obligation to act in a way that will serve the public interest, honor the public trust, and demonstrate commitment to professionalism.

• But then she sees that Rule 301—Confidential Client Information says that: A member in public practice shall not disclose any confidential client information without the specific consent of the client.

You Make the Call What should Ivana do?

A—Ivana should resign from the engagement and uphold her very specific ethical obligation under Rule 301—Confidential Client Information. (That “Public Interest” thing is pretty general and kind of vague.)

B—Ivana should report what she has found to law enforcement authorities.

dco$on@co$oncpa.com 38

2014 Government Conference

Good news if you do Yellow Book audits

GAGAS Paragraph 4.30 Auditors should report known or likely fraud, noncompliance with provisions of laws, regulations, contracts, or grant agreements, or abuse directly to parties outside the audited entity in the following two circumstances.

Good news if you do Yellow Book audits

GAGAS Paragraph 4.30 a. When entity management fails to satisfy legal or regulatory

requirements to report such information to external parties specified in law or regulation, auditors should first communicate the failure to report such information to those charged with governance. If the audited entity still does not report this information to the specified external parties as soon as practicable after the auditors’ communication with those charged with governance, then the auditors should report the information directly to the specified external parties.

dco$on@co$oncpa.com 39

2014 Government Conference

Good news if you do Yellow Book audits GAGAS Paragraph 4.30 b. When entity management fails to take timely and appropriate

steps to respond to known or likely fraud, noncompliance with provisions of laws, regulations, contracts, or grant agreements, or abuse that (1) is likely to have a material effect on the financial statements and (2) involves funding received directly or indirectly from a government agency, auditors should first report management’s failure to take timely and appropriate steps to those charged with governance. If the audited entity still does not take timely and appropriate steps as soon as practicable after the auditors’ communication with those charged with governance, then the auditors should report the entity’s failure to take timely and appropriate steps directly to the funding agency.

Good news if you do Yellow Book audits GAGAS Paragraph 4.31 The reporting in paragraph 4.30 is in addition to any legal requirements to report such information directly to parties outside the audited entity. Auditors should comply with these requirements even if they have resigned or been dismissed from the audit prior to its completion. [Emphasis added]

dco$on@co$oncpa.com 40

2014 Government Conference

Read the case study in Attachment A; select the

best answer.

Fun, interactive, and educational activity …

Case Study: Generosity Begins at Home What should Ida do? [ ] A. Ida should do nothing. She has an ethical obligation not to improperly

use information obtained in performing her job. [ ] B. Ida should refer the matter to the secretary of DOH; if he does not take

appropriate action, Ida should contact the Illinois Election Commission, the Illinois Bureau of Investigation, the Federal Bureau of Investigation, the Justice Department, and the IRS for further advice.

[ ] C. The importance of this matter is such that the public’s right to the transparency of this information outweighs any other considerations, so Ida should contact the The Chicago Sun Times, The Chicago Tribune, The Wall Street Journal, FOX News, and The Drudge Report.

[ ] D. The importance of this matter is such that the public’s right to the transparency of this information outweighs any other considerations, so Ida should contact The Chicago Sun Times, The Chicago Tribune, The Wall Street Journal, FOX News, and The Drudge Report, anonymously.

[ ] E. Other: _________________________________________________

dco$on@co$oncpa.com 41

2014 Government Conference

Doing the Right Thing Isn’t Easy

Ø The Right Thing is not something about which everyone always agrees

Ø We are often oblivious to ethical dilemmas Ø We have a strong ability to rationalize doing

the wrong thing Ø It’s all about conflicts of interest Ø In some cases, it is impossible to follow ALL

the rules

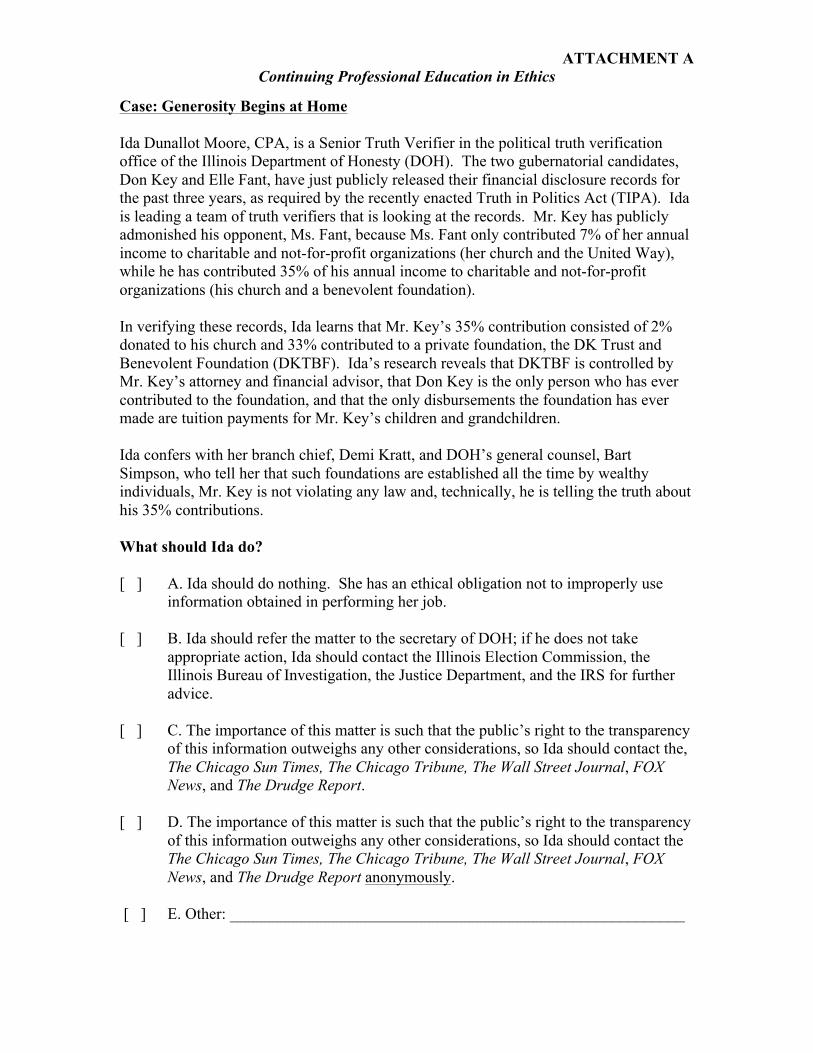

ATTACHMENT A Continuing Professional Education in Ethics

Case: Generosity Begins at Home Ida Dunallot Moore, CPA, is a Senior Truth Verifier in the political truth verification office of the Illinois Department of Honesty (DOH). The two gubernatorial candidates, Don Key and Elle Fant, have just publicly released their financial disclosure records for the past three years, as required by the recently enacted Truth in Politics Act (TIPA). Ida is leading a team of truth verifiers that is looking at the records. Mr. Key has publicly admonished his opponent, Ms. Fant, because Ms. Fant only contributed 7% of her annual income to charitable and not-for-profit organizations (her church and the United Way), while he has contributed 35% of his annual income to charitable and not-for-profit organizations (his church and a benevolent foundation). In verifying these records, Ida learns that Mr. Key’s 35% contribution consisted of 2% donated to his church and 33% contributed to a private foundation, the DK Trust and Benevolent Foundation (DKTBF). Ida’s research reveals that DKTBF is controlled by Mr. Key’s attorney and financial advisor, that Don Key is the only person who has ever contributed to the foundation, and that the only disbursements the foundation has ever made are tuition payments for Mr. Key’s children and grandchildren. Ida confers with her branch chief, Demi Kratt, and DOH’s general counsel, Bart Simpson, who tell her that such foundations are established all the time by wealthy individuals, Mr. Key is not violating any law and, technically, he is telling the truth about his 35% contributions. What should Ida do? [ ] A. Ida should do nothing. She has an ethical obligation not to improperly use

information obtained in performing her job. [ ] B. Ida should refer the matter to the secretary of DOH; if he does not take

appropriate action, Ida should contact the Illinois Election Commission, the Illinois Bureau of Investigation, the Justice Department, and the IRS for further advice.

[ ] C. The importance of this matter is such that the public’s right to the transparency

of this information outweighs any other considerations, so Ida should contact the, The Chicago Sun Times, The Chicago Tribune, The Wall Street Journal, FOX News, and The Drudge Report.

[ ] D. The importance of this matter is such that the public’s right to the transparency

of this information outweighs any other considerations, so Ida should contact the The Chicago Sun Times, The Chicago Tribune, The Wall Street Journal, FOX News, and The Drudge Report anonymously.

[ ] E. Other: _________________________________________________________