doing business in mozambique · • the most commonly used is the private limited liability...

TRANSCRIPT

Doing Business inMozambique

Johannesburg | South AfricaAugust 2013

www.pwc.com

PwC

Contents

1. Why this seminar?

2. PwC Africa Desk

3. Country Context3.1 Political3.2 Legal3.3 Socio-Economical

4. Business Vehicles4.1 Company vs. Branch4.2 Types of companies

5. Legal Framework5.1 Legal System at a Glance5.2 Public and Private Partnership

Law and Regulations5.3 Land Rights5.4 Investment Guarantees5.5 Labour Issues (Foreign Staff)

6. Tax Framework6.1 Tax Overview6.2 Fiscal Incentives6.3 Structuring

7. Key Issues

8. Contacts

2August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Why this seminar?

3August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Why this seminar?

• The interest in investing in Africa is growing rapidly

• Need for general as well as specific hands-on information

and ability to discuss developments

• PwC Africa Desk to facilitate this by, among

others, organising “Doing business in Africa”

seminars

1. Zambia (March 2013)

2. Mozambique (August 2013)

3. Many more to come. Next seminar expected in

November 2013

Doing Business in Mozambique: Johannesburg & Cape Town | South Africa4

August 2013

PwC

PwC Africa Desk

5

PwC

Other ways the Africa desk may support you

Doing Business in Mozambique: Johannesburg & Cape Town | South Africa6

August 2013

One-stopservice

Because of helicopterview, identification ofother cross-country

alternatives

Thought leadership throughAfritax newsletter, One page taxsummaries per African country,

country seminars, etc

Quick responses ongeneral and specific

questions

Proactivelyinform relevantparties on newdevelopments

PwC

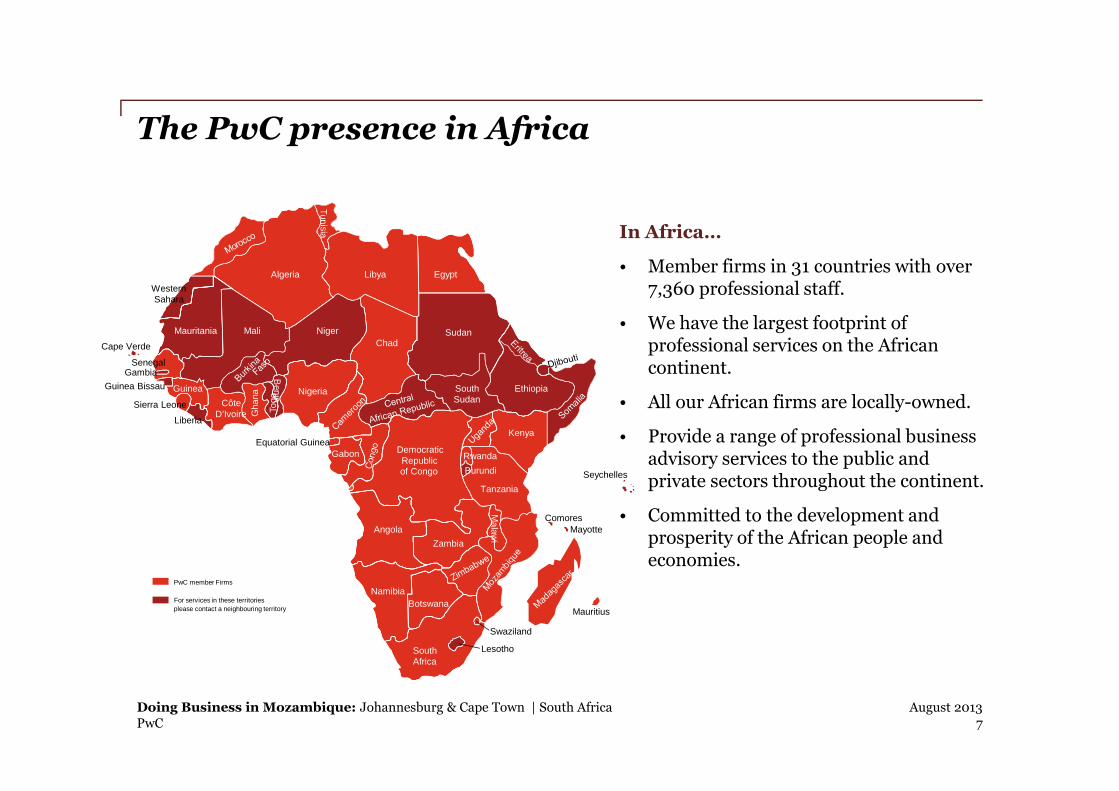

The PwC presence in Africa

In Africa…

• Member firms in 31 countries with over7,360 professional staff.

• We have the largest footprint ofprofessional services on the Africancontinent.

• All our African firms are locally-owned.

• Provide a range of professional businessadvisory services to the public andprivate sectors throughout the continent.

• Committed to the development andprosperity of the African people andeconomies.

Doing Business in Mozambique: Johannesburg & Cape Town | South Africa7

August 2013

Algeria

Tunisia

Egypt

Sudan

SouthSudan

Mauritania

WesternSahara

Niger

Chad

Ethiopia

Kenya

DemocraticRepublicof Congo

Nigeria

Ben

in

Togo

Gha

na

CôteD’Ivoire

Liberia

Sierra Leone

Guinea

SenegalGambia

Guinea Bissau

Equatorial GuineaGabon

Angola

Zambia

Ma

law

i

Namibia

Botswana

SouthAfrica

Lesotho

Swaziland

Mauritius

Comores

Seychelles

Mayotte

Cape Verde

PwC member Firms

Mali

Rwanda

Burundi

Tanzania

Libya

For services in these territories

please contact a neighbouring territory

PwC

Contents

1. Why this seminar?

2. PwC Africa Desk

3. Country Context3.1 Political3.2 Legal3.3 Socio-Economical

4. Business Vehicles4.1 Company vs. Branch4.2 Types of companies

5. Legal Framework5.1 Legal System at a Glance5.2 Public and Private Partnership

Law and Regulations5.3 Land Rights5.4 Investment Guarantees5.5 Labour Issues (Foreign Staff)

6. Tax Framework6.1 Tax Overview6.2 Fiscal Incentives6.3 Structuring

7. Key Issues

8. Contacts

8August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

Country Context

PwC

Country Context

3.1 Political

3.2 Legal

3.3 Socio-Economical

10August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

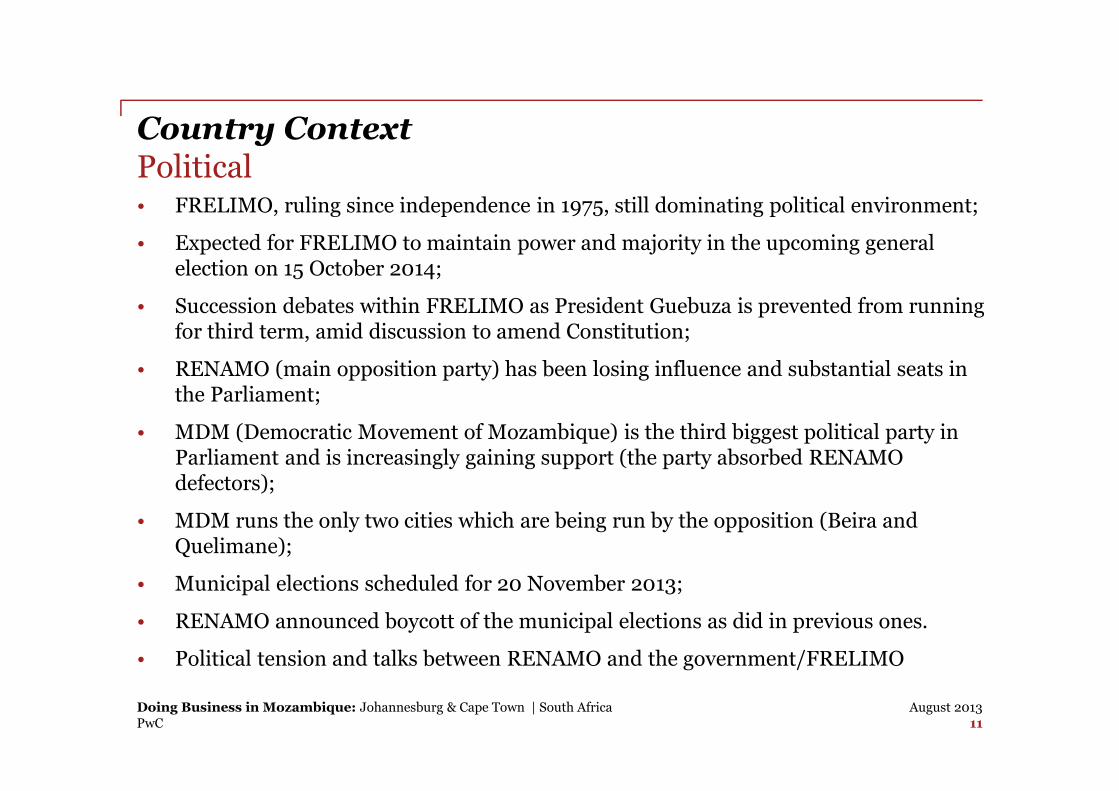

Country ContextPolitical• FRELIMO, ruling since independence in 1975, still dominating political environment;

• Expected for FRELIMO to maintain power and majority in the upcoming generalelection on 15 October 2014;

• Succession debates within FRELIMO as President Guebuza is prevented from runningfor third term, amid discussion to amend Constitution;

• RENAMO (main opposition party) has been losing influence and substantial seats inthe Parliament;

• MDM (Democratic Movement of Mozambique) is the third biggest political party inParliament and is increasingly gaining support (the party absorbed RENAMOdefectors);

• MDM runs the only two cities which are being run by the opposition (Beira andQuelimane);

• Municipal elections scheduled for 20 November 2013;

• RENAMO announced boycott of the municipal elections as did in previous ones.

• Political tension and talks between RENAMO and the government/FRELIMO

11August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Country Context

3.1 Political

3.2 Legal

3.3 Socio-Economical

12August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Country ContextLegal

• Extensive legal reforms made as part of the transition to free marketeconomy, revoking very old colonial legislation:

New commercial, inward investment and tax and customs laws(codes);

Reform of tax system started in 1999 with introduction of VAT;

Introduction of specialized tax receiver units dealing with mega-projects;

Labour and Commercial arbitration;

Public Sector reform including simplification of procedures;

Reforms of sector legislation, such as mining, oil and gas, financialsector, etc;

Adoption of IFRS and implementation in due course.

13August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Country Context

3.1 Political

3.2 Legal

3.3 Socio-Economic

14August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Country ContextSocio-Economic

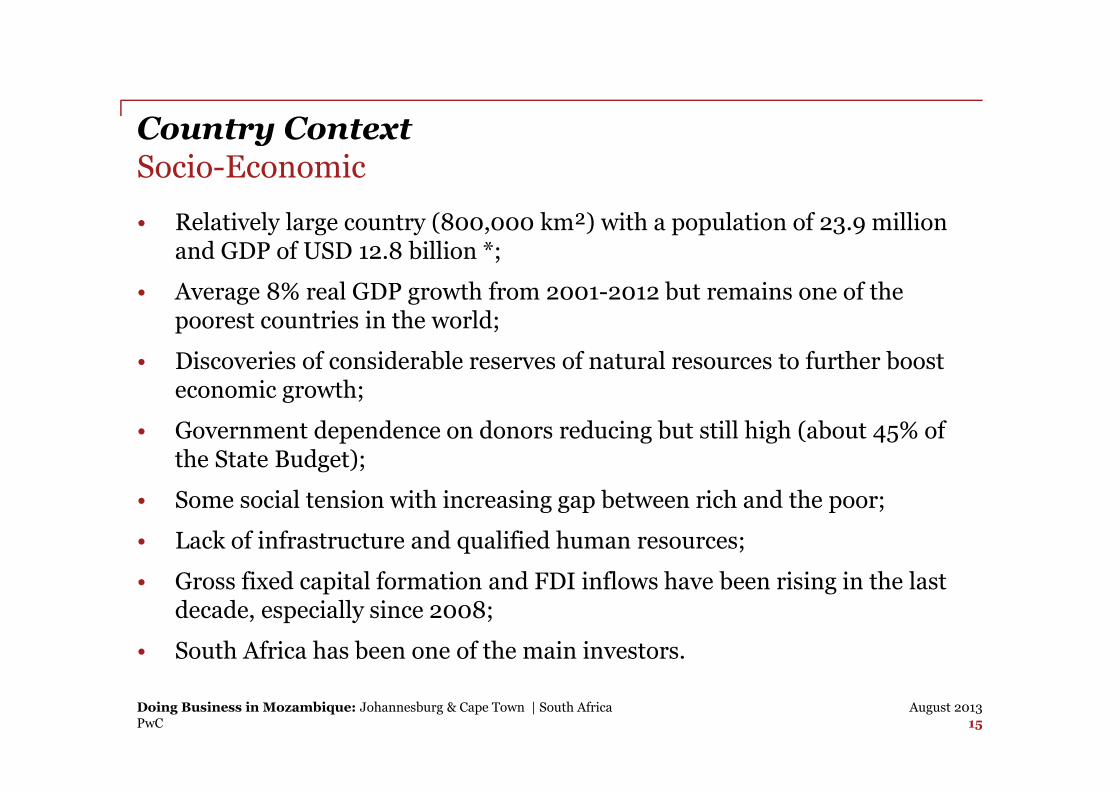

• Relatively large country (800,000 km²) with a population of 23.9 millionand GDP of USD 12.8 billion *;

• Average 8% real GDP growth from 2001-2012 but remains one of thepoorest countries in the world;

• Discoveries of considerable reserves of natural resources to further boosteconomic growth;

• Government dependence on donors reducing but still high (about 45% ofthe State Budget);

• Some social tension with increasing gap between rich and the poor;

• Lack of infrastructure and qualified human resources;

• Gross fixed capital formation and FDI inflows have been rising in the lastdecade, especially since 2008;

• South Africa has been one of the main investors.

15August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Country ContextSocio-Economic

• Traditional exports include prawns, sugar, cashew, timber andcotton;

• Commodities such as aluminium, electricity, natural gas and coalovertaken traditional exports since 2004;

• Main imports include machinery and equipment, vehicles, fuel,chemicals, metal products, foodstuffs and textiles;

• Poverty, education and unemployment are critical current and longterm considerations;

16August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

Business Vehicles

PwC

Business Vehicles

4.1 Company vs Branch

4.2 Types of companies

18August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Business VehiclesCompany vs. Branch

Item Distinction factors Company Branch

1 Legal personality Yes No

2 Tax personality Yes Yes

3 Liability

Limited to theamount of the

company’s sharecapital

Head office is fullyresponsible for

branch’s liabilities

4 No. of shareholders Minimum of 2 or 3 Not applicable

5Incorporation/Registration costs

Lower Higher

6Stakeholder’sperception

Long-termpresence

Short-term presence

19August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Business VehiclesCompany vs. Branch (cont.)

ItemDistinction

factorsCompany Branch

7 Audited accountsNot mandatory

(exceptions apply)Mandatory

8 Import license Easy to obtain Difficult to obtain

9 Duration UnlimitedLimited (max 3 years

renewable)

10 Taxation of dividends20% WHT on

dividendsdistribution

No taxation onremittance of profitsfrom branch to head

office

11Eligibility forlicenses/concessions

Suitable for allLimitation (e.g.

mining)

12 Liquidation/closure Complex Simple

20August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Business VehiclesCompany vs. Branch (cont.)

• Little operating difference between a Branch and a Company;

• Main criteria is stakeholder’s intention/ execution of contract/short term

presence or ongoing business/long term presence;

• The main differentiating factors are:

o The tax efficiency of repatriation of profits derived by a Branch vs.

profits derived by a Company;

o The way both are perceived by the different stakeholders

(e.g. Government); and

o The ineligibility or limitation for branches to apply for certain licenses.

21August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Business Vehicles

4.1 Company vs Branch

4.2 Types of companies

22August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Business VehiclesLimited Liability companies

• The most commonly used is the private limited liability companies -

Sociedade por Quotas de Responsabilidade Limitada (Lda.) in opposition

to the public limited liability companies - Sociedade Anónima de

Responsabilidade Limitada (SA).

• The main differentiating factors are related to corporate compliance and

requirements, with Lda being more simple than SA:

- Number of shareholders;

- Issuance and number of shares; and

- Limitation of liability.

• Both companies have the same incorporation procedures.

23August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

Legal Framework

PwC

Legal Framework

5.1 Legal System at a glance

5.2 Public and PrivatePartnership Law andRegulations

5.3 Land Rights

5.4 Investment Guarantees

5.5 Labour Issues (Foreign Staff)

25August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Legal FrameworkLegal System at Glance

Overview

• German based with several regulations being inserted in specific Codes.

• Inherited laws and regulations from the colonial ruler Portugal, which is still

the main legal reference.

• Codification of the laws applies to commercial laws, civil laws, tax laws,

Procedural Law etc.

• Very formal system, with lengthy procedures all required to be in a certain

format.

• Separation of Powers is warranted by the Constitution of the Republic;

• Judiciary comprises general courts, appeal and a supreme court;

• There are also specialized Courts, such as Tax , Customs and Labour

Courts.

26August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Legal FrameworkUpdates and Hot topics

• Approved further Simplified Licensing of Economic Activities

• Public-Private-Partnership regulation with local content and other

requirements

• Published first competition law;

• Introduced mandatory centralized electronic/online custom

clearance;

• New tax regimes for mining and oil and gas operations under

discussion;

• Amendment of Corporate and Personal Income Tax codes under

discussion – eyes on capital gains, transfer pricing and simplification

of individuals taxation

27August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Legal Framework

5.1 Legal System at a glance

5.2 Public and PrivatePartnership Law andRegulations

5.3 Land Rights

5.4 Investment Guarantees

5.5 Labour Issues (Foreign Staff)

28August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Legal FrameworkPublic and Private Partnership (PPP) Law and Regulations

• Applicable also to mega-projects and business concession (prospecting,exploration, extraction and/or production of natural and other nationalassets);

• PPP regulation for small projects under discussion;

• Establish share of benefits with financial and socio-economic benefits.

Main Financial Benefits

Imposed reservation of 5% to 20% of the share capital to transfer throughstock exchange;

Local content participation of Mozambican public or private companies onthe share capital under the terms agreed by the parties;

Other (e.g. generation of positive exchange effect to the balance ofpayments; generation of tax revenue; generation and distribution ofdividends).

29August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Legal FrameworkPublic and Private Partnership (PPP) Law and Regulations

Main Socio-Economical Benefits

• Construction, rehabilitation or expansion of infrastructures for productionor rendering of services, in connection or associated to the enterprise;

• Creation of employment and professional training programs forMozambican employees;

• Transfer of technology and know-how to the country;

• Increase and maintenance of the production and export capacity, as well ascoverage of the internal market needs;

• Contribution to the development of the SMEs;

• Implementation of social responsibility projects and for social developmentand sustainability of the local communities.

30August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Legal Framework

5.1 Legal System at a Glance

5.2 Public and PrivatePartnership Law andRegulations

5.3 Land Rights

5.4 Investment Guarantees

5.5 Labour Issues (Foreign Staff)

31August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Legal FrameworkLand Rights

• Land is property of the State and cannot be sold, mortgaged or otherwiseencumbered;

• Individuals and entities are entitled to apply for the concession for the rightto use and exploit land (DUAT) for a determined period of time;

• There are full property rights over the infrastructures built on the land;

• Transfer of the buildings, by means of a public deed, will entail the transferof the respective rights of land use and benefit;

• Transfer of urban tenants does not require prior authorisation from theState.

32August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Legal Framework

5.1 Legal System at a Glance

5.2 Public and PrivatePartnership Law andRegulations

5.3 Land Rights

5.4 Investment Guarantees

5.5 Labour Issues (Foreign Staff)

33August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Legal FrameworkInvestment Guarantees

• Eligible with foreign direct investment (FDI) of about USD85,000.00(different regime and minimal applies for mining and oil and gas);

• FDI in the form of cash, equipment, trade rights and non interest bearingshareholders loan;

• FDI eligible to tax benefits;

• Guarantees include ability to transfer abroad:

Exportable profits resulting from profit export eligible investments;

Royalties or other similar income;

Repayment of capital and interest on loans;

Proceeds of compensation;

Re-exportable foreign capital invested;

Sums corresponding to the payment of obligations towards non-resident entities.

•34

August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Legal Framework

5.1 Legal System at a glance

5.2 Public and PrivatePartnership Law andRegulations

5.3 Land Rights

5.4 Investment Guarantees

5.5 Labour Issues (Foreign Staff)

35August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Legal FrameworkLabour Issues (Foreign Staff)

• Limited employment of foreign staff through the following regimes:

o Short term work (90 consecutive or aggregate days – 180 for companiesin mining/oil and gas industry);

o Quota (automatic with simple communication)

5% in large companies (i.e. > 100 employees);

8% in medium sized companies (i.e. >10 and ≤ 100 employees); and

10% in small companies (i.e. ≤ 10 employees).

Regardless of the number of local employees, small companies areentitled to hire 1 foreign employee.

o Work authorisation (subject to discretionary decision by governmentand produce evidence of competencies)

o Contracts approved by government/investment projects (as establishedin the contract)

36August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

Tax Framework

PwC

Tax Framework

6.1 Tax Overview

6.2 Fiscal Incentives

6.3 Structuring

38August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Tax FrameworkTax Overview

Tax Rate

Corporate Income TaxResidents: 32% final tax

Non- residents: 20% definitive withholding tax

Dividends 20% withholding tax

Capital gainsResidents: 32% final tax

Non-residents: 32% (taper relief available!)

Individual Income Tax 10% - 32%

VAT 17%

Property Transfer Tax 2% / 10%

Social Security4% (employer)3% (employee)

Stamp Duty0,2% -50%

200,00 MT – 2.500,00 MT

OtherCustoms Duties

Excise Duties, Municipal

39August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Tax Framework

6.1 Tax Overview

6.2 Fiscal Incentives

6.3 Structuring

40August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Tax FrameworkFiscal Incentives

• Dependent on approval of investment project/contract;

• General trend and national debate for reduction;

• In general granted for 5 years;

• Scope of incentives vary depending on type of activity and project location;

• Mining and the Oil and Gas with specific regime;

• Main benefits:

- Customs duties and VAT exemptions on import of goods (mainly Class“K” of the Customs Tariff Schedule);

- Corporate tax incentives consist mainly in tax credits varying from 5 to10%;

- Reduction of corporate tax for specific areas (e.g. Agriculture andtechnologies).

41August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Tax Framework

6.1 Tax Overview

6.2 Fiscal Incentives

6.3 Structuring

42August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Tax FrameworkTax structuring - General

• Key tax considerations:

- How do you repatriate funds?

- Exit strategy in terms of capital gains tax

- Which holding location to choose?

Doing Business in Mozambique: Johannesburg & Cape Town | South Africa43

August 2013

PwC

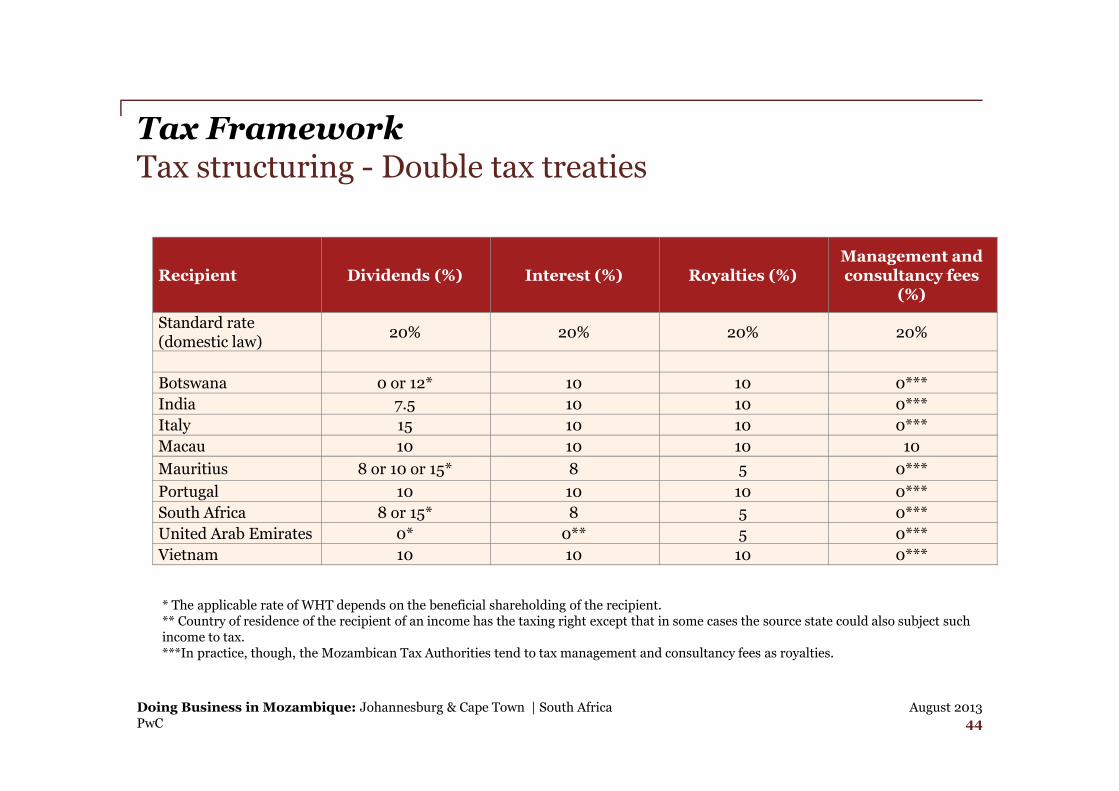

Tax FrameworkTax structuring - Double tax treaties

Doing Business in Mozambique: Johannesburg & Cape Town | South Africa44

August 2013

Recipient Dividends (%) Interest (%) Royalties (%)Management andconsultancy fees

(%)

Standard rate(domestic law)

20% 20% 20% 20%

Botswana 0 or 12* 10 10 0***

India 7.5 10 10 0***

Italy 15 10 10 0***

Macau 10 10 10 10

Mauritius 8 or 10 or 15* 8 5 0***

Portugal 10 10 10 0***

South Africa 8 or 15* 8 5 0***

United Arab Emirates 0* 0** 5 0***

Vietnam 10 10 10 0***

* The applicable rate of WHT depends on the beneficial shareholding of the recipient.** Country of residence of the recipient of an income has the taxing right except that in some cases the source state could also subject suchincome to tax.***In practice, though, the Mozambican Tax Authorities tend to tax management and consultancy fees as royalties.

PwC

Tax FrameworkTax structuring - example

• Create a gateway through SA for holdingAfrican activities, amongst whichMozambique.

• Benefits of SA head quarter company:

• No withholding tax on dividend,interest and royalties to parent

• Participation exemption on dividendincome

• Limited exchange control

• No transfer pricing

• Treaty access

• CGT participation exemption ondisposal of assets

• “Look through” for CFC purposes

• Strict requirements to be met to qualify

Doing Business in Mozambique: Johannesburg & Cape Town | South Africa45

August 2013

SA HQcompany

AfricanOpco

SA activities

HoldCo

AfricanOpco

MozOpco

PwC

Tax FrameworkTax structuring - example

• Capital gains are taxed as part of the normal income at the rate of 32%

• Ways to mitigate:

- Holding location with treaty that allocates taxing rights to other country (forexample Mauritius)

- Sell at level of blocker company, since (currently) there is no indirect taxation ofcapital gains (different interpretation may apply in practice)

Doing Business in Mozambique: Johannesburg & Cape Town | South Africa46

August 2013

Key Issues

PwC

Key Issues

48August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Key Issues

VAT:

Self assessment (or reversecharge) requirements onimport of services intoMozambique

Failure to comply withadministrative requirements(raising VAT and claiming VATsimultaneously) results in VATassessments and penalties.

49August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Key Issues

VAT:

Exemption on servicesacquired by Oil and Gastaxpayers in theirexploration phase

Requires the issuance of adeclaration to the supplier,otherwise resulting in VATassessments and penalties.

50August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Key Issues

VAT:

Contractors and localsubcontractors are subjectto VAT and are required toincur input VAT and applyfor refunds later

Delays in refunding input VATimpacts the cash flow management

51August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Key Issues

Corporate tax:

Introduction of ring fencingregime in the Mining andOil and Gas space

Uncertainty on practical aspectsdue to lack of regulation/procedures for practicalimplementation

52August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Key Issues

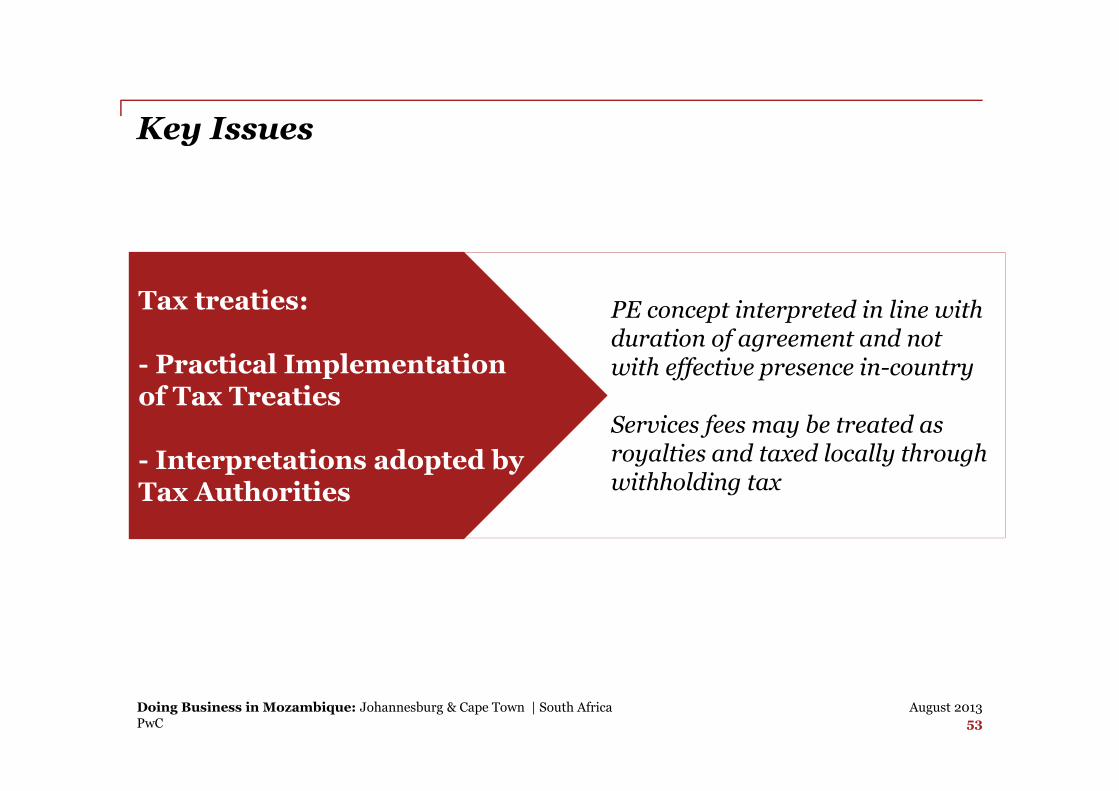

Tax treaties:

- Practical Implementationof Tax Treaties

- Interpretations adopted byTax Authorities

PE concept interpreted in line withduration of agreement and notwith effective presence in-country

Services fees may be treated asroyalties and taxed locally throughwithholding tax

53August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Key Issues

Branch / PE:

Practicalities regardingearly remittance of branchprofits from Mozambique

No WHT on remittance of profits atthe end of the fiscal year – but mayimpact cash flow

If profits are remitted before yearend there may be potentialwithholding tax exposure

54August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Key Issues

Withholding tax:

Whether withholding tax islevied on accrual orpayment of the invoiceamount

Uncertainty regarding the newlegislation and potentially differenttreatment for interest, royalties,and management fees

55August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Key Issues

Individuals:

Lengthy procedures forwork/residency permits incase of exhausted quota orif out of short termcommunication of 90 days

Delays in engaging requisiteskills/expertise for the operation ofvarious time-bound projects

56August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Key Issues

General:

Lack of experience andknowledge of TaxAuthorities i.r.o. industryspecific issues

Application of interpretations thatdiffer from the internationalpractice standards

57August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Key Issues

Accounting:

Electronic invoicing andbookkeeping require priorapproval of software by theMTA

Uncertainty on practical aspectsdue to lack of regulation/procedures for practicalimplementation

58August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Contacts

59August 2013Doing Business in Mozambique: Johannesburg & Cape Town | South Africa

PwC

Contacts

PricewaterhouseCoopers | MozambiquePestana Rovuma Hotel,Centro de Escritórios, 5º andar, Rua da Sé, 114, MaputoOffice: +258 (21) 350 400 | Fax: +258 (21) 307 621

60August 2013

Elandre Brandt

Tax Director

Office: + 27 (11) 797 75822

Email: [email protected]

João Martins

Country Senior Partner

Office: +258 (82) 314 7 820

Email: [email protected]

Malaika Ribeiro

Associate Tax Director

Office: +258 (82) 309 3240

Email: [email protected]

Mateus Chale

Senior Tax Consultant

Office: +258 (82) 305 0560

Email: [email protected]

Jelle Keijmel

Senior Manager - Africa Desk

Office: + 27 (11) 797 5990

Email: [email protected]

Driaan Rupping

Senior Tax Consultant

Office: +258 (82) 328 3870

Email: [email protected]

PricewaterhouseCoopers | South Africa2 Eglin Road, Sunninghill, 2157, JohannesburgOffice: +27 (11) 797 5000

Ibikunle Olatunji

Manager - Africa Desk

Office: + 27 (11) 797 5317

Email: [email protected]

PwC

We are here to serve you...

Thank you!Obrigado!Baie dankieKhanimambo!

This publication has been prepared for general guidance on matters of interest only,and does not constitute professional advice. You should not act upon the informationcontained in this publication without obtaining specific professional advice. Norepresentation or warranty (express or implied) is given as to the accuracy orcompleteness of the information contained in this publication, and, to the extentpermitted by law, PwC, its members, employees and agents do not accept or assumeany liability, responsibility or duty of care for any consequences of you or anyone elseacting, or refraining to act, in reliance on the information contained in thispublication or for any decision based on it.

© 2013 PricewaterhouseCoopers (“PwC”), the Mozambican firm. All rights reserved.In this document, “PwC” refers to PricewaterhouseCoopers in Mozambique, which isa member firm of PricewaterhouseCoopers International Limited (PwCIL), eachmember firm of which is a separate legal entity and does not act as an agent of PwCIL.