doing business in california - squire patton …/media/files/insights/...1 introduction - 1 •...

TRANSCRIPT

39 Offices in 19 Countries

Basics of U.S. Securities Laws(米国証券法の基礎知識)

下田 範幸 (日本およびカリフォルニア州弁護士)Squire Sanders (US) LLP (San Francisco Office) パートナー

Phone: (415) 393-9894Email: [email protected]

September 18, 2013 at Palo Alto OfficeOctober 23, 2013 at San Francisco Office

DOING BUSINESS IN CALIFORNIAVenture Capital Financing –Part 2

1

Introduction - 1

• Venture Capital Seminar Part -1Typical Legal Issues regarding Startups

• Venture Capital Seminar Part -2Basics of U.S. Securities Laws

• Venture Capital Seminar Part -3Preferred Stock Financing Transactions

2

Introduction

• There are many puzzling things in the area of U.S. securities laws, some examples of which are (証券法を理解しないとわからない具体例)

“Investor Questionnaire” (投資家アンケート)“Accredited Investor” as part of required representations and warranties by an investor in a stock purchase agreement (適格投資家の概念)The following standard legend on the back of a stock certificate(株券に記載のレジェンド)

“THESE SECURITIES HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED. THEY MAY NOT BE SOLD, OFFERED FOR SALE, PLEDGED, OR HYPOTHECATED IN THE ABSENCE OF AN EFFECTIVE REGISTRATION STATEMENT AS TO THE SECURITIES UNDER SAID ACT OR AN OPINION OF COUNSEL SATISFACTORY TO THE CORPORATION THAT SUCH REGISTRATION IS NOT REQUIRED.” (これらの証券は1933年証券法における登録がされておらず、同法に基づく登録がされるか、会社が満足する内容での、登録が不要であることについての弁護士の意見書がない限り売却したり、売却の申し込みをしたり、担保に入れたりすることができないものである。 )

3

Why is Securities Law Compliance Important? (なぜ、証券法遵守が重要か)

• The issuance and resale of securities are heavily regulated by U.S. securities laws(証券の発行と発行後の証券の転売についてのきわめて厳密な規制)

• Violations of securities laws can result in potentially severe consequences for the issuing company, its control persons (officers, directors and principal shareholders) and any other “person” who “offers” and “sells” a security (証券法違反によるペナルティは、会社だけでなく、取締役などの個人に及ぶ)

4

Why is Securities Law Compliance Important? (なぜ、証券法遵守が重要か)

• Potential plaintiffs will not be just one individual investor, but may be all securities holders in the same “offering” even if the violation was made specifically with respect to just one security holder (証券法違反があったラウンド

は、違反のあった特定の証券取引だけでなく、その取引が行われたラウンド全体に及ぶ。)

• In addition, a company will usually be required to make representations and warranties as to its compliance with securities laws in past issuances in the context of raising additional funds from venture capital investors or in an acquisition of the company. Failure to comply with securities laws can negatively affect a company’s valuation because it increases the risk to new investors(証券法違反がないことは、投資契約の際、その他M&Aの契約書の中で保証させられる。)

5

Purpose of Securities Laws (目的)

• Protection of investors(投資家保護)

Full public disclosure of all information material to an investment decision (投資判断に関係するすべての情報開示を確保)

Prevention of fraud and misinformation in the distribution of securities (詐欺の防止)

– Civil and criminal liabilities (刑事罰、民事罰)

6

Purpose of Securities Laws (Cont’d)

• Courts and securities laws (裁判所の態度)

Courts interpret securities laws broadly in favor of requiring registration (裁判所は、証券の登録を必要とする

方向に解釈する傾向がある。)

Courts protect those who are unsophisticated or do not have access to material information, or both (裁判所は自

己を防衛できない投資家、および、情報を開示されない投資

家を守る傾向にある。)

Burden is on the issuer or the transferor to establish that the issuance/transfer is exempt from registration (証券法

の除外規定に当たって許される証券の発行であることの主張

立証責任は発行会社にある。)

Whether the issuer satisfies an appropriate exemption often involves a factual determination (除外規定にあたるか

どうかは具体的な事実認定次第)

7

U.S. Securities Laws

• Federal securities laws (連邦証券法)

The Securities Act of 1933, as amended (the “’33 Act” or “Securities Act”) provides for Registration Requirement(登

録必要性を規定)

– Regulates the distribution/offering of securities (both debt and equity)(株式売却および売却申し込みを規制)

– Requires the filing of a registration statement with the Securities and Exchange Commission (the “SEC”), and mandates the distribution of a disclosure document (a “prospectus”) in connection with any public distribution/offering of securities (一般への証券の販売のためには、SECへの登録申請書と目論見書の提出が必要)

– Establishes liability for fraud and misinformation in connection with the public sale and distribution of securities(一般への証券売却とその申し込み関しての詐欺に対する責任を明確化)

8

U.S. Securities Laws (Cont’d)

The Securities Exchange Act of 1934, as amended (the “’34 Act” or “Exchange Act”)) periodic reporting requirements (定期的な情報開示義務)– Regulates the securities industry and post-distribution trading of

issued securities. The various stock exchanges and securities firms are subject to the ‘34 Act (証券業界への規制の根拠法)

– Regulates and prohibits certain activities in relation to securities trading, including margins for the purchase of securities and insider trading in public companies (証券取引のさまざまな面への規制)

– Requires public companies to make periodic disclosures to the SEC(定期的な開示義務)

– Created the SEC, and vested in the SEC broad powers to regulate and enforce the federal securities laws (SECの設立と権限の根拠法)

9

State Securities Laws (Blue Sky Laws)(州証券法)

• Regulate offering of securities and securities broker-dealers and securities firms (証券の売却と申し込みを規制するとともに、株取引ブローカーに対する規制)

• Impose liability for fraud and misinformation in connection with the distribution and sale of securities (証券取引をめぐる詐欺行為などの禁止)

• Establish state agencies to administer the blue sky laws (州の規制官庁の根拠法令)

10

State Securities Laws (Blue Sky Laws) (Cont’d)

• Federal securities laws generally do not preempt blue sky laws (連邦法は当然には州法に優先しない)

One key exception(例外): Covered security– Examples

» Nationally traded securities (registered with SEC) (連邦証券取引所で上場済みの証券)

» Exemption in connection with exempt offerings pursuant to SEC Rule 506 (Rule 506に基づく証券法適用除外が認められた証券)

11

State Securities Laws (Blue Sky Laws) (Cont’d)

• Covered securityStates are prohibited from

– Requiring registration or qualification of a covered security– Undertaking a merit review of an offering or issue in connection with a

covered security(Covered securitiesについては、連邦法が優先し、州は、別途登録を要求したり、上

場要件を満たしているかどうかの判断の対象とすることを禁止される。)

Note– States may require certain informational filings and administrative fees

(ただし、一定の情報提供のための届出を要求することはできる。)

12

Registration Requirements(登録必要性)

• Section 5 of the ‘33 ActProvides in summary:– Unless a registration is in effect as to a security,

it shall be unlawful for any person, directly or indirectly, to sell the security in commerce or through the use of mails. (登録が有効でない限り、証券を一般に販売することは違法である。 )

13

Registration Requirements (Cont’d)

• Registration statement (登録申請書)Describes the offering and the issuer making the offer (株

式売却申し込みの内容と、発行会社の詳細説明)

Filed with the SEC (SECに登録)

Consists of two parts– Prospectus (目論見書)

» Information regarding the issuer, information about the distribution and use of proceeds, and description of the securities of the issuer (発行会社、発行株式、調達資金の用途等の情報開示)

– Second part» Various supplemental technical information, certificates,

signatures and exhibits (さまざまな添付書類)

14

Registration Requirements (Cont’d)

• Registration forms (登録書式)S-1– Requires complete disclosure (もっとも厳密で広

範囲の開示が必要)

– Required for IPO (IPOのときの書式)

– Used by public companies that do not qualify to use S-3 (S-3が使えない上場会社が使う場合)

15

Registration Requirements (Cont’d)

• Registration forms (cont’d)S-3– Allows maximum use of incorporation by reference of

the ‘34 Act reports (すでに登録済みの情報の引用が最大限許される)

– Requires the least new disclosure to be presented in the prospectus and delivered to investors (目論見書や、投資家へ直接届けられる解除情報が少なくてすむ。)

– Available by companies that have been making periodic filings with the SEC for at least one year (1年以上、SECへの届出をしていることが必要)

– Companies need not to deliver a copy of the annual report to investors along with the prospectus (投資家に目論見書のほかに年次財務諸表を届けることは不要)

16

Federal Issuer Exemptions (発行における除外規定)

• Section 4(2): the traditional private placement exemption (伝統的私的募集除外規定)

Generally– Under Section 4(2), “transactions by an issuer not involving

any public offering” are exempt from the registration requirements of the ‘33 Act (公開募集によらない株式発行者による株式発行、売却は33年法の例外として許される。)

– There is no specific limit on the number of securities that can be issued or the amount of capital that can be raised (発行で

きる株式の数や、購入者の人数や、株式売却の金額等についての制限は一切規定されていない。)

– No specific disclosure or filing requirements are mandated(株式売却の際に公開すべき会社情報についての義務も、担当官庁への届出の義務等も一切規定されていない。)

17

Federal Issuer Exemptions (発行における

除外規定)(Cont’d)

• Section 4(2): the traditional private placement exemption

4 main factors which must be met for Section 4(2) exemption to be available (セクション4(2)除外規定の適用4要件):– The number of offerees must be limited (exact number of

offerees, dates, and identity of offerees, etc. must be specifically known and documented)(株式購入を勧誘する相手の数が限定的であり、それらが書面で証明できること)

– The size and manner of the offering must be limited (i.e., dollar amount of the offering, no public solicitation, resale restrictions, etc.)(株式募集の規模と方法が限定的であること、すなわち、募集金額が小規模であり、募集方法も一般公衆に向けた宣伝などを含まないこと)

18

Federal Issuer Exemptions (発行における

除外規定)(Cont’d)

• Section 4(2): the traditional private placement exemption

4 main factors which must be met for Section 4(2) exemption to be available– The offerees must be sophisticated such that they could

“fend for themselves” (i.e., investment knowledge and experience, sufficient wealth to allow them to hire professional investment assistance, etc.)(株式購入を勧誘する相手が投資経験があり洗練されていて自分の権利を守る能力があり、かつ経済的に投資リスクに耐えられること)

– There must exist a relationship between the issuer and the offeree (i.e., by virtue of the relationship with the issuer, the offeree either had access to material information of the issuer as if it were an insider or received material information similar to what would be found in a registration statement)(株式発行会社と株式購入を勧誘される相手との間にすでに一定の関係があり、それによって、相手が投資判断に必要な株式発行会社に関する十分な情報を入手できる立場にあり、現実に十分な情報の提供を受けたこと)

19

Federal Issuer Exemptions (発行における

除外規定)(Cont’d)

• Section 4(2): the traditional private placement exemption

Practically, even though there is no statutory disclosure requirement, the issuer is required to provide extensive disclosure (事実上、相当広範囲な

情報開示が必要)

The issuer must show that each of the above four factors was satisfied with respect to each “offeree” (not just each purchaser) of the securities (発行会社

が、上記4要件が一人一人の投資家について存在して

いることを立証しなければならない)

20

Federal Issuer Exemptions (発行における

除外規定)(Cont’d)

• Section 4(2): the traditional private placement exemption

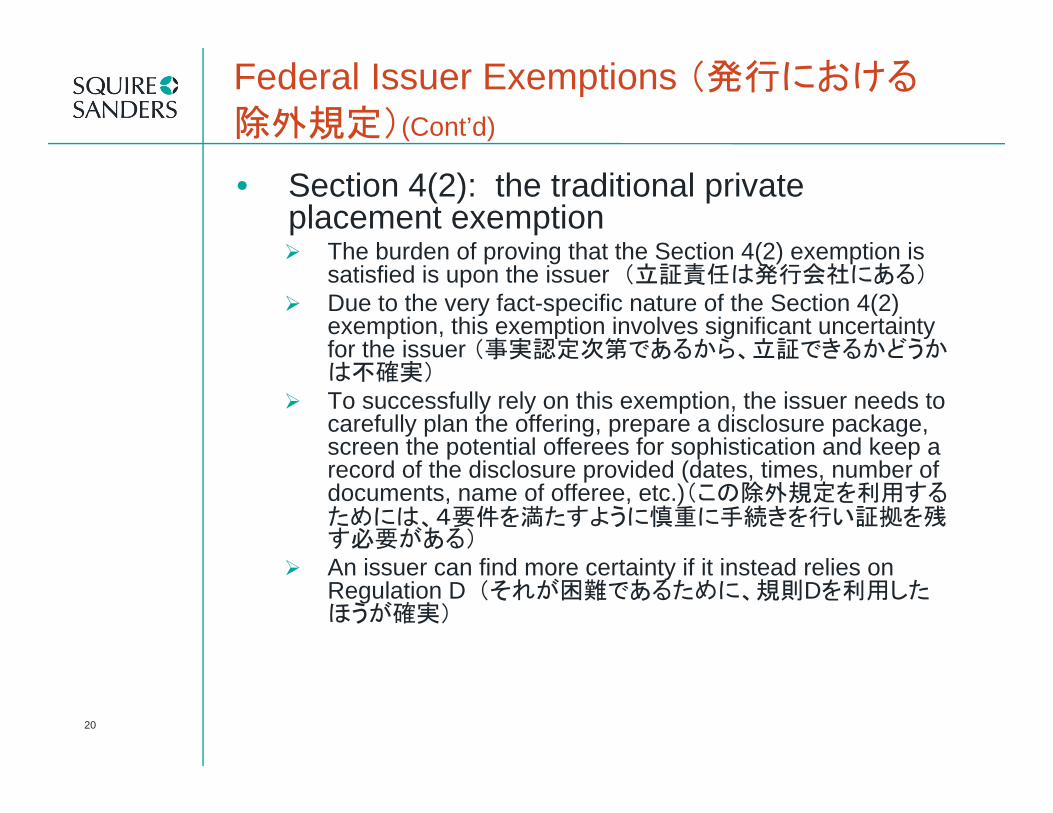

The burden of proving that the Section 4(2) exemption is satisfied is upon the issuer (立証責任は発行会社にある)Due to the very fact-specific nature of the Section 4(2) exemption, this exemption involves significant uncertainty for the issuer (事実認定次第であるから、立証できるかどうかは不確実)To successfully rely on this exemption, the issuer needs to carefully plan the offering, prepare a disclosure package, screen the potential offerees for sophistication and keep a record of the disclosure provided (dates, times, number of documents, name of offeree, etc.)(この除外規定を利用するためには、4要件を満たすように慎重に手続きを行い証拠を残す必要がある)An issuer can find more certainty if it instead relies on Regulation D (それが困難であるために、規則Dを利用したほうが確実)

21

Federal Issuer Exemptions (発行における

除外規定)(Cont’d)

• Regulation D: the safe harbor for Section 4(2) exemption (セクション4(2)除外規定に対する安全港ルー

ル)

Generally– Regulation D is a series of rules establishing three

exemptions, Rules 504, 505, and 506(規則Dは、3つの除外ルールを規定)

– Regulation D is the exemption of choice for many emerging companies when they issue common or preferred stock (規則Dがほとんどのスタートアップの株式発行のための使われている。)

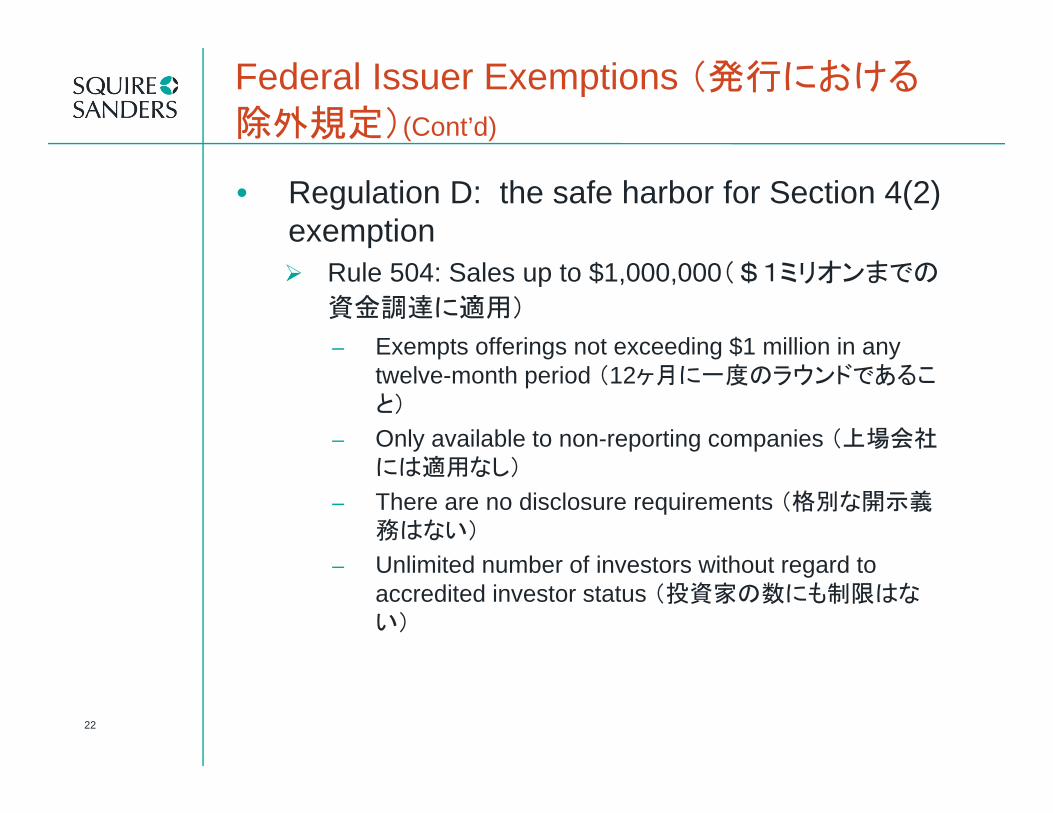

22

Federal Issuer Exemptions (発行における

除外規定)(Cont’d)

• Regulation D: the safe harbor for Section 4(2) exemption

Rule 504: Sales up to $1,000,000($1ミリオンまでの

資金調達に適用)

– Exempts offerings not exceeding $1 million in any twelve-month period (12ヶ月に一度のラウンドであること)

– Only available to non-reporting companies (上場会社には適用なし)

– There are no disclosure requirements (格別な開示義務はない)

– Unlimited number of investors without regard to accredited investor status (投資家の数にも制限はない)

23

Federal Issuer Exemptions (発行における

除外規定)(Cont’d)

• Regulation D: the safe harbor for Section 4(2) exemption

Rule 504: Sales up to $1,000,000 (cont.)– This exemption is convenient particularly for the

issuance of shares very early in a company’s life to founders, friends and family who might not be “accredited investors”(適格投資家の要件を備えていない友人や家族などからの資金調達に適切)

– One difficulty with this exemption is that the applicable blue sky laws frequently impose certain disclosure and sophistication requirements for each offeree (Covered Securitiesではないので、州証券法の適用を受けることが問題)

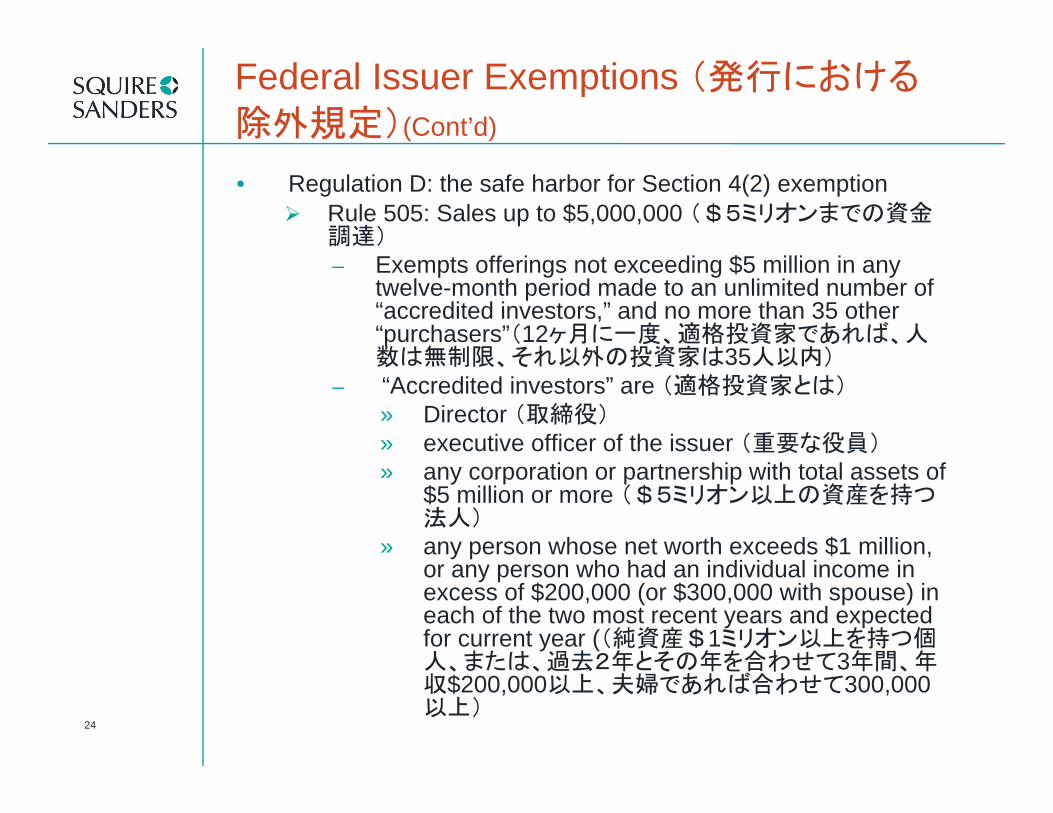

24

Federal Issuer Exemptions (発行における

除外規定)(Cont’d)

• Regulation D: the safe harbor for Section 4(2) exemptionRule 505: Sales up to $5,000,000 ($5ミリオンまでの資金調達)– Exempts offerings not exceeding $5 million in any

twelve-month period made to an unlimited number of “accredited investors,” and no more than 35 other “purchasers”(12ヶ月に一度、適格投資家であれば、人数は無制限、それ以外の投資家は35人以内)

– “Accredited investors” are (適格投資家とは)» Director (取締役)» executive officer of the issuer (重要な役員)» any corporation or partnership with total assets of

$5 million or more ($5ミリオン以上の資産を持つ法人)

» any person whose net worth exceeds $1 million, or any person who had an individual income in excess of $200,000 (or $300,000 with spouse) in each of the two most recent years and expected for current year ((純資産$1ミリオン以上を持つ個人、または、過去2年とその年を合わせて3年間、年収$200,000以上、夫婦であれば合わせて300,000以上)

25

Federal Issuer Exemptions (発行における

除外規定)(Cont’d)

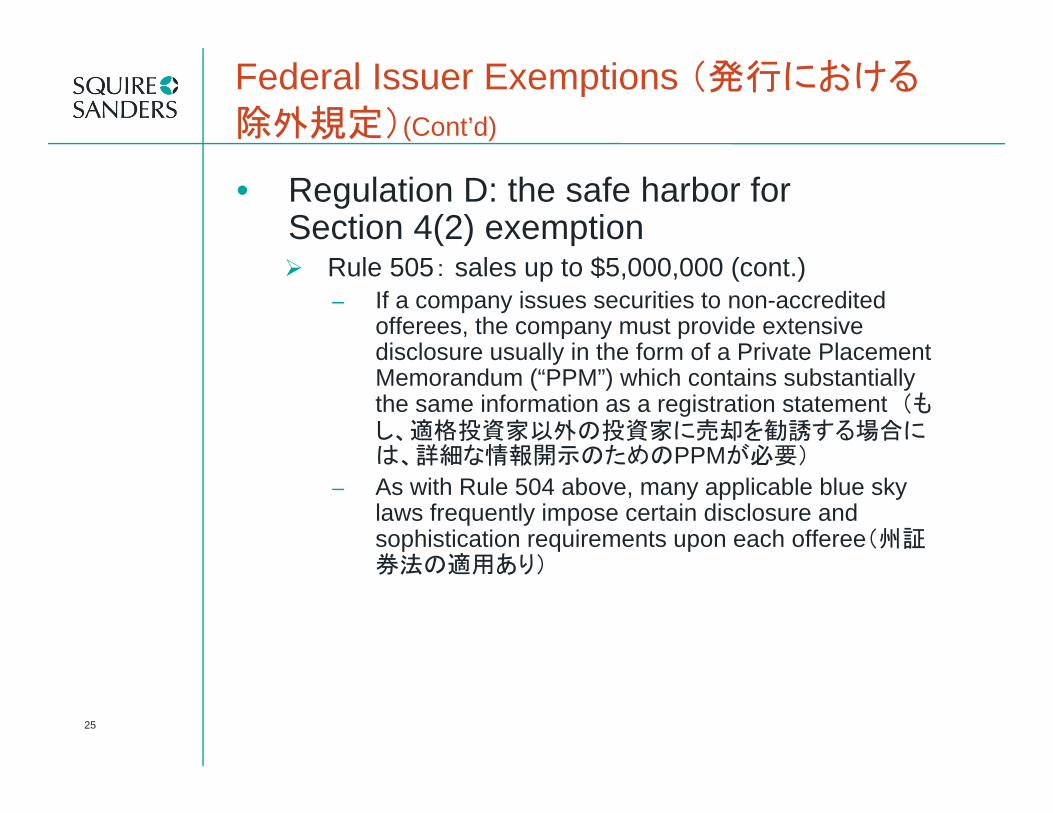

• Regulation D: the safe harbor for Section 4(2) exemption

Rule 505: sales up to $5,000,000 (cont.)– If a company issues securities to non-accredited

offerees, the company must provide extensive disclosure usually in the form of a Private Placement Memorandum (“PPM”) which contains substantially the same information as a registration statement (もし、適格投資家以外の投資家に売却を勧誘する場合には、詳細な情報開示のためのPPMが必要)

– As with Rule 504 above, many applicable blue sky laws frequently impose certain disclosure and sophistication requirements upon each offeree(州証券法の適用あり)

26

Federal Issuer Exemptions (発行における

除外規定)(Cont’d)

• Regulation D: the safe harbor for Section 4(2) exemption

Rule 506: unlimited sales(金額無制限)– Exempts unlimited amount offering to an unlimited number

of “accredited investors”, and to no more than 35 other “purchasers” (適格投資家の人数無制限、それ以外の投資家35人以内)

– If an issuer issues securities to an unaccredited investor, the issuer must provide extensive disclosure (PPM) to the investor. In addition, it is required that the issuer make a determination that the non-accredited investor has sufficient knowledge and experience in business and financial matters so that the investor can evaluate the merits and risks of the investment (適格投資家以外の投資家を勧誘するときにはPPMが必要。また、その適格投資家以外の投資家が投資のリスクを理解できる十分な経験と知識あることを確認する必要がある。)

– The securities issued under this rule are “covered” securities and preempts the blue sky laws, except for certain informational filing and fee requirements in some states (情報手今日を目的としたFilingとFeeを除いて原則として州証券法の適用なし)

27

Federal Issuer Exemptions (発行における

除外規定)(Cont’d)

• Regulation D: the safe harbor for Section 4(2) exemption Other aspects of Regulation D(規則Dを使う場合のそれ以

外の注意事項)

– There will be no integration of any offer or sale made more than six months before the first Regulation D offering or after the last Regulation D sale (Rule 502(a))(規則Dによれば、ラウンドの間に6ヶ月間を空ければ統合を避けることができる。)

– Notice of all Regulation D offerings to the SEC is required by Rule 503(a) on Form D(書式Dによる届出が必要)

– Failure to make timely notice to the SEC used to result in the loss of the exemption. Rule 508 now provides that minor deviations from the requirements of Regulation D will not destroy the exemption (以前は、少しでも書式Dの届出が遅れると違法となったが、今はある程度はゆるされる。)

28

Federal Issuer Exemptions (発行における

除外規定)(Cont’d)

• Regulation D: the safe harbor for Section 4(2) exemption

Common requirements(規則D利用の共通要件)– No advertisement, no public solicitation (Rule 502(c))(宣伝したり、一

般への幅広い勧誘は禁止) subject to recent amendments based on JOBS Act(JOBS Actに基づく 一定の勧誘を許す修正規則が最近採用された)

– The issuer shall exercise reasonable care to assure that the purchasers of the securities are not underwriters, which reasonable care may be demonstrated by the following (Rule 502(d))(以下のことを実行して、株式購入者がUnderwritersでないことを合理的に確認すること)» Reasonable inquiry to determine if the purchaser is acquiring the

securities for himself or for other persons (購入者が自分のために購入するのであって転売等のためでないことを確認)

» Written disclosure to each purchaser prior to sale that the securities have not been registered under the ‘33 Act and, therefore, cannot be resold unless they are registered under the ‘33 Act or unless an exemption from registration is available (売却の証券は登録されていないので、転売は原則できない証券であることを書面で開示)and

» Placement of a legend on the certificate or other document that evidences the securities stating that the securities have not been registered under the ‘33 Act and setting forth or referring to the restrictions on transferability and sale of the securities (証券自体に、同様の趣旨を明示すること)

29

Amendment to Reg. D by JOBS Act(JOBS ActによるReg Dの変更)

• Jumpstart Our Business Startups Act (JOBS Act) JOBS Act is a legislative package designed to jumpstart our economy and restore opportunities to startups for the purpose of creating more jobs for Americans, which requires amendment to Reg. D (JOBS Actは、経済を活性化し、スタートアップにより多くの資金調達の機会を与え、雇用を創出するために採用されたいくつかの法律のパッケージで、その中にはReg Dの変更を義務付けているものがある。):The Access to Capital For Job Creators Act– Removes an SEC regulatory ban preventing small businesses from

using advertisements to solicit investors.(小規模の会社が投資を募る際に宣伝することを認める。)

– Requires the SEC to amend Rule 506 of Reg. D to provide that the prohibition on general solicitation or general advertising shall not apply to offers and sales of securities made solely to accredited investors pursuant to Rule 506.(SECに対して、該当規則のReg. DのRule 506の変更を義務付けている。)

– As amended, Rule 506 will permit the use of general solicitation to offer and sell securities under Rule 506, provided that (i) all terms and conditions of Rule 501 and Rule 502(a) and 502(d) are satisfied; (ii) all purchasers of securities are accredited investors; and (iii) the issuer takes “reasonable steps to verify” that the purchasers of the securities are accredited investors. (改正Rule 506は、他のReg. Dの規則の要件および、勧誘の相手がすべて適格投資家であること、それを確認する合理的なステップを踏むこと、などを条件に一般的な勧誘を認めた。)

30

Amendment to Reg. D by JOBS Act(JOBS ActによるReg Dの変更)

Amended Rule 506(c) provides non-exclusive list of “reasonable steps” that issuers can use to verify that purchasers are accredited investors based on net worth(改正Rule 506(c) に規定する、適格投資家であることを確認する合理的なステップ):

– On basis of income, reviewing any IRS form that reports the purchaser’s income for the two most recent years and obtaining a written representation from the purchaser that he or she has a reasonable expectation of reaching the income level necessary to qualify as an accredited investor during the current year(IRSの税金申告書と本人の表明によって、過去2年間の収入と現在の収入を確認)

– On the basis of net worth, review one or more of the following dated within prior three months and obtain written representation from purchasers that all liabilities necessary to make a determination of net worth have been disclosed(純資産に基づく適格投資家要件に関しては、本人の各3か月間における債務についての表明と):» With respect to assets: bank statements, brokerage statements

and other statements of securities holdings, certificates of deposit(銀行口座の残高通知、証券会社の通知など)

» With respect to liabilities: a consumer report from at least one of the nationwide consumer reporting agencies(債務に関しては、少なくとも一つの消費者情報会社からのレポート).または、

31

Amendment to Reg. D by JOBS Act(JOBS ActによるReg Dの変更)

– Amended Rule 506(c) provides non-exclusive list of “reasonable steps” that issuers can use to verify that purchasers are accredited investors based on net worth:» Obtain a written confirmation from one of the following persons or

entities that such person or entity has taken reasonable steps to verify that the purchaser is an accredited investor within the prior three months and has determined that such purchaser is an accredited investor(以下のうちの一人から、適格投資家であることを確認する合理的なステップを踏んだことについての確認書を取得):– Registered broker-dealer;– Investment adviser registered with the SEC;– Licensed attorney or CPA.

– Amended Rule 506 became effective on September 23, 2013.(改正規則は2013年9月23日に有効となった。)

32

Amendment to Reg. D by JOBS Act(JOBS ActによるReg Dの変更)

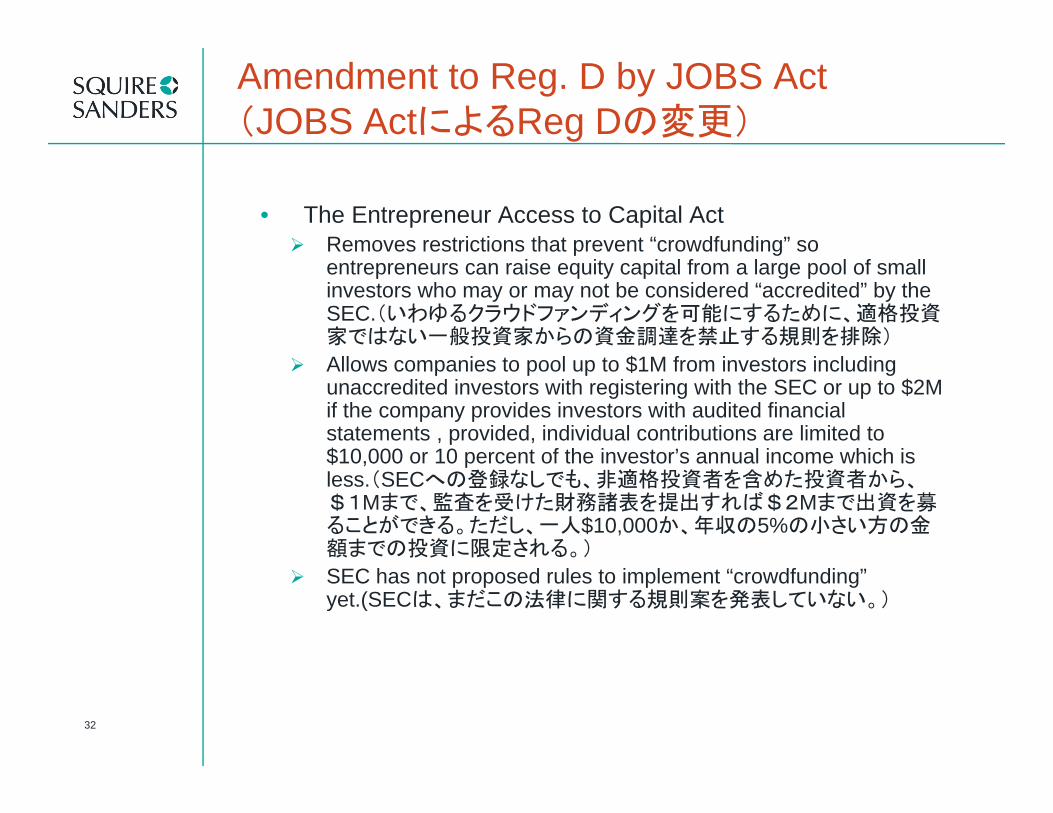

• The Entrepreneur Access to Capital ActRemoves restrictions that prevent “crowdfunding” so entrepreneurs can raise equity capital from a large pool of small investors who may or may not be considered “accredited” by the SEC.(いわゆるクラウドファンディングを可能にするために、適格投資家ではない一般投資家からの資金調達を禁止する規則を排除)

Allows companies to pool up to $1M from investors including unaccredited investors with registering with the SEC or up to $2M if the company provides investors with audited financial statements , provided, individual contributions are limited to $10,000 or 10 percent of the investor’s annual income which is less.(SECへの登録なしでも、非適格投資者を含めた投資者から、$1Mまで、監査を受けた財務諸表を提出すれば$2Mまで出資を募ることができる。ただし、一人$10,000か、年収の5%の小さい方の金額までの投資に限定される。)

SEC has not proposed rules to implement “crowdfunding” yet.(SECは、まだこの法律に関する規則案を発表していない。)

33

Federal Issuer Exemptions (発行における除外規定) (Cont’d)

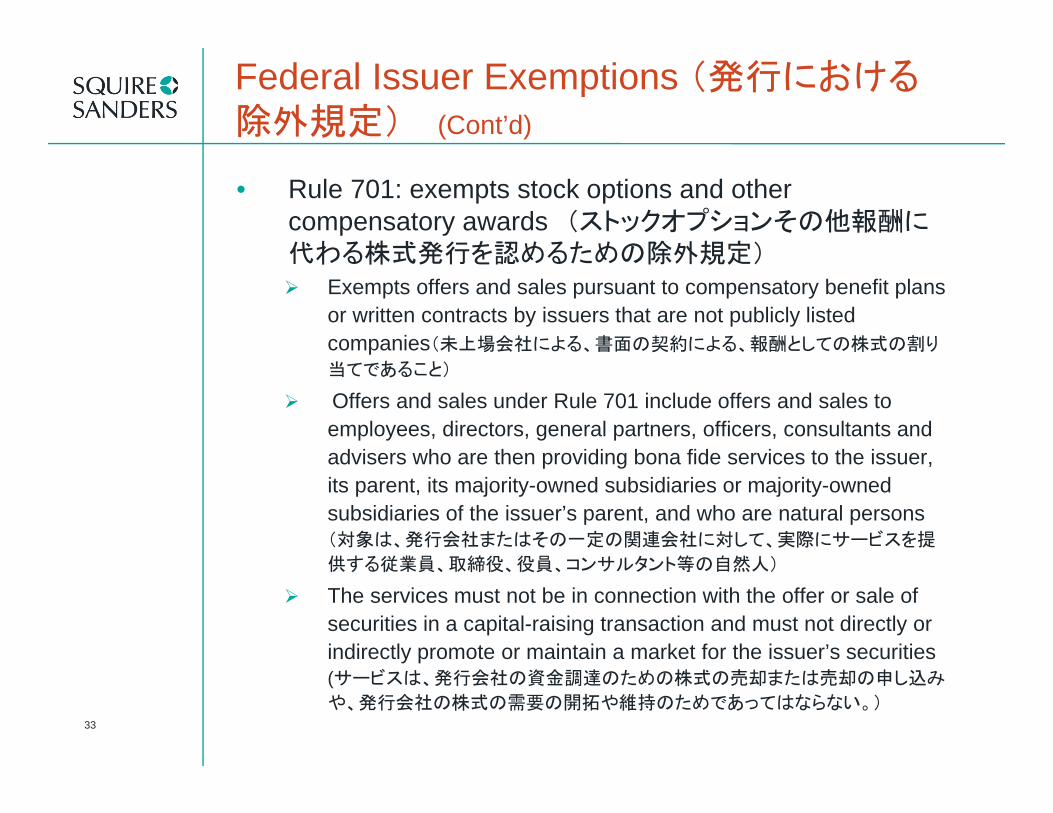

• Rule 701: exempts stock options and other compensatory awards (ストックオプションその他報酬に代わる株式発行を認めるための除外規定)

Exempts offers and sales pursuant to compensatory benefit plans or written contracts by issuers that are not publicly listed companies(未上場会社による、書面の契約による、報酬としての株式の割り

当てであること)

Offers and sales under Rule 701 include offers and sales to employees, directors, general partners, officers, consultants and advisers who are then providing bona fide services to the issuer, its parent, its majority-owned subsidiaries or majority-owned subsidiaries of the issuer’s parent, and who are natural persons (対象は、発行会社またはその一定の関連会社に対して、実際にサービスを提

供する従業員、取締役、役員、コンサルタント等の自然人)

The services must not be in connection with the offer or sale of securities in a capital-raising transaction and must not directly or indirectly promote or maintain a market for the issuer’s securities (サービスは、発行会社の資金調達のための株式の売却または売却の申し込み

や、発行会社の株式の需要の開拓や維持のためであってはならない。)

34

Federal Issuer Exemptions (発行における除外規定) (Cont’d)

• Rule 701: exempts stock options and other compensatory awards (ストックオプションその他報酬に代わる株式発行を認めるための除外規定)

Exempts offers and sales pursuant to compensatory benefit plans or written contracts by issuers that are not publicly listed companies(未上場会社による、書面の契約による、報酬としての株式の割り

当てであること)

Offers and sales under Rule 701 include offers and sales to employees, directors, general partners, officers, consultants and advisers who are then providing bona fide services to the issuer, its parent, its majority-owned subsidiaries or majority-owned subsidiaries of the issuer’s parent, and who are natural persons (対象は、発行会社またはその一定の関連会社に対して、実際にサービスを提

供する従業員、取締役、役員、コンサルタント等の自然人)

The services must not be in connection with the offer or sale of securities in a capital-raising transaction and must not directly or indirectly promote or maintain a market for the issuer’s securities (サービスは、発行会社の資金調達のための株式の売却または売却の申し込み

や、発行会社の株式の需要の開拓や維持のためであってはならない。)

35

Federal Issuer Exemptions (発行における

除外規定)(Cont’d)

• Rule 701: exempts stock options and other compensatory awards

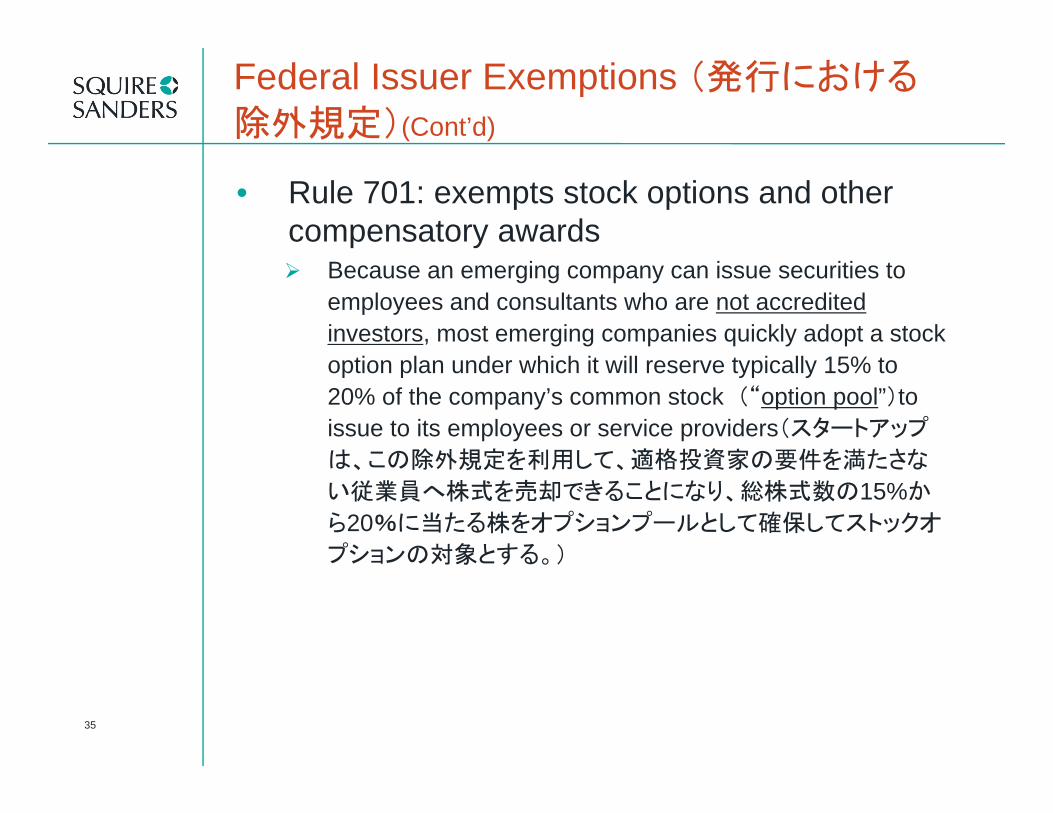

Because an emerging company can issue securities to employees and consultants who are not accredited investors, most emerging companies quickly adopt a stock option plan under which it will reserve typically 15% to 20% of the company’s common stock (“option pool”)to issue to its employees or service providers(スタートアップ

は、この除外規定を利用して、適格投資家の要件を満たさな

い従業員へ株式を売却できることになり、総株式数の15%か

ら20%に当たる株をオプションプールとして確保してストックオ

プションの対象とする。)

36

Federal Issuer Exemptions (発行における

除外規定)(Cont’d)

• Rule 701: exempts stock options and other compensatory awards(ストックオプションの要件)

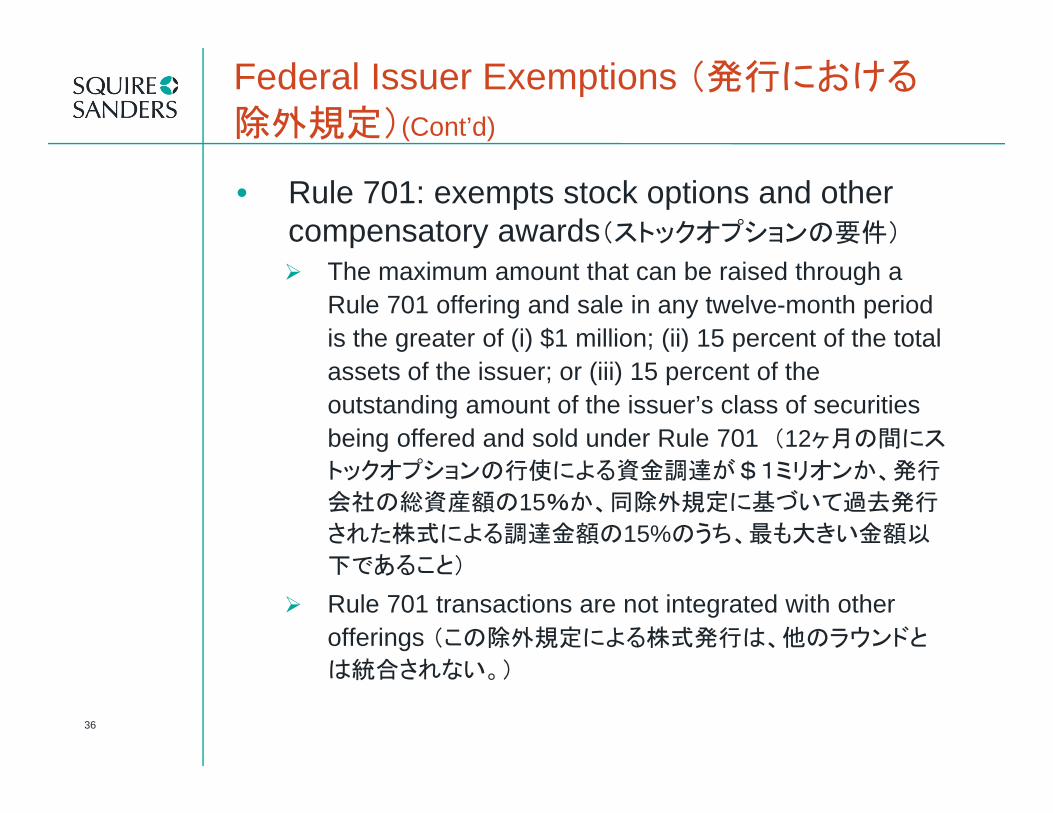

The maximum amount that can be raised through a Rule 701 offering and sale in any twelve-month period is the greater of (i) $1 million; (ii) 15 percent of the total assets of the issuer; or (iii) 15 percent of the outstanding amount of the issuer’s class of securities being offered and sold under Rule 701 (12ヶ月の間にス

トックオプションの行使による資金調達が$1ミリオンか、発行

会社の総資産額の15%か、同除外規定に基づいて過去発行

された株式による調達金額の15%のうち、最も大きい金額以

下であること)

Rule 701 transactions are not integrated with other offerings (この除外規定による株式発行は、他のラウンドと

は統合されない。)

37

Federal Issuer Exemptions (発行における

除外規定)(Cont’d)

• Regulation S: offshore sale exemption (海外発行除外)

Regulation S generally permits the sale and purchase of securities outside of the U.S. without registration so long as certain procedures are implemented to ensure that the securities come to rest abroad and do not flow back into the U.S. in the near future (アメリカ国外で取引された株式が近い将来アメリカ国内に舞い戻ってこないことを確保するために一定の手続きを遵守することを条件に、アメリカ国外で行われるアメリカの会社の株式取引を例外として許すもの。)Regulation S does not require any specific disclosure and does not distinguish between accredited and non-accredited investors(格別な会社情報の開示義務を課しておらず、また、適格投資家とそうでない投資家の区別もしていない。 )Securities issued pursuant to Regulation S must contain restrictive legends stating such (この除外規定に基づいて発行された株式には、株券に、その趣旨が記載される必要がある。)

38

Federal Issuer Exemptions (発行における

除外規定)(Cont’d)

• Regulation S: offshore sale exemption Requirements under Regulation S(規則Sの要件):– Offers and sale of the securities must be made only in an

“offshore transaction”(株式の購入の勧誘および実際の売却がアメリカ国外で行われること)

– Offers and sales of the securities must be made only to non-U.S. persons. (株式購入の勧誘および実際の販売が、「非アメリカ人」に対して行われなければならないこと)

» A “U.S. person” is defined under Regulation S to include, (i) any natural person resident in the United States, (ii) any partnership or corporation organized under U.S. law, or (iii) any agency or branch of a foreign entity located in the U.S.(規則Sにおけるアメリカ

人とは、(1)アメリカに居住する自然人、(2)アメリカ法に基いて設立されたパートナーシップや株式会社、(3)アメリカに所在する外国法人の代理店または支店であると定義される)、

39

Federal Resale Exemptions(転売除外規定)

• Resales and secondary distributions in general(転売の際の除外規定一般)

Securities laws generally prohibit resales of securities unless the security or the resale is exempt (上場株か、一

定の除外規定の適用がない限り、すでに発行された株式を転

売する取引も禁止されている。)

The number of resale exemptions is very limited(転売を認

める例外規定は数少なく、限定されている。)

A resale in violation of securities laws may adversely affect an emerging company’s issuer exemption with respect to the entire offer, exposing the company and its control persons to potential liability(証券法違反の転売は、

もともとの株式発行において使われた除外規定の有効性を破

壊し、もともとの株式発行自体を違法なものとしてしまうリスク

がある。)

40

Federal Resale Exemptions(転売除外規定)(Cont’d)

• Resales and secondary distributions in general

Three principal methods of resales– Hold the securities long enough that the investor can

be said to have assumed the economic risk of the investment (Section 4(1))(購入した株式を、当初の株式購入時点では転売する意思が客観的になかったと確実に判断される程度に長期間保有した上で、例外規定であるSection 4(1)に基づいて転売する。)

– Comply with all the conditions of certain safe harbor provisions (Rule 144, Regulation S)(証券法上認められるルール144(Rule 144)などの安全港ルールや規則Sなどの要件を満たした方法で転売する。)or

– Sell such securities to other sophisticated investors who intend to hold the securities for investment purposes (Section 4(1 ½) exemption)(適格投資家の要件を満たし、転売の意思がないなどの規則Dに記載されている適格投資家への株式発行と同様な要件を満たした取引によって転売する。)

41

Federal Resale Exemptions(転売除外規定)(Cont’d)

• Section 4(1) exemptionSection 4(1) exempts from registration “transactions by any person other than an issuer, underwriter, or dealer”(セクション4(1)は、株式発行会社、株式引受人、または株

式のディーラー以外による株式売却は登録の例外として許さ

れると規定している 。)

The key legal inquiry is whether the reseller would be deemed an “underwriter” under Section 4(1)(転売者が株

式引受人に当たると判断されるかどうかがポイント)

Determining whether the seller of the securities is acting as an “underwriter” to effect a “distribution” (i.e., a public offering) of securities is difficult (株式引受人にあたるどう

かの判断は困難)

42

Federal Resale Exemptions転売除外規定)(Cont’d)

• Section 4(1) exemptionThe “underwriter” is defined as “any person who has purchased from an issuer with a view to, or offers or sells for an issuer in connection with, the distribution of any security, or participates or has a participation in the direct or indirect underwriting of such undertaking[.]”(株式を転売

する考えを持って、または転売に関連して、発行会社から株

式を購入したすべての者、または、発行会社のためにその株

式の購入を勧誘し、または、販売したすべての者、または、そ

のような転売に直接であれ、間接であれ、なんらかの形で参

加したすべての者 )

It is very difficult to establish that a person is not an “underwriter” because this determination depends on the facts and circumstances and the case law does not provide definitive guidance in most cases(事実認定次第で

あり、判例は明確な基準を示していないので、判断は困難)

43

Federal Resale Exemptions(転売除外規定)(Cont’d)

• Section 4(1) exemptionAny investor which purchases securities from the issuer in a private placement may be deemed to be an underwriter if they are found to have purchased the securities with the intention of distributing the securities to others(私募におい

て、発行会社から、転売目的で購入したものはUnderwriterと判断される。)

Ultimately, the investment intent of the investor is a question that will depend on all the facts (e.g., holding period, representations of investment intent at time of initial purchase, change of circumstances) of a particular situation (投資目的か転売目的かは、さまざまな事実の総

合判断よって判断される。)

44

Federal Resale Exemptions(転売除外規定)(Cont’d)

• Section 4(1) exemptionPractical legal risks under Section 4(1)(現実的なリスク)– Emerging companies receive great pressure from their

founders and investors to permit such transfers(スタートアップは、投資してくれた株主から、転売を承諾するように要求される。)

– In most cases, the company will not be able to receive a definitive analysis or comfort that the resale in fact meets the exemption(転売除外規定に当たるどうか明確な判断が困難)

– This means that the company will inevitably be taking some ongoing risk that the sale violates securities laws if the company permits the resale, and the resale is later litigated(転売を認めると、後に裁判等起こされるリスクがある。)

– In such a case, the company and its control persons risk potential liability to every person in the offering that loses its exempt status by virtue of the non-compliant resale(のちに転売が許されないことになると、その転売者はUnderwriterと判断され、その転売者が参加したラウンド全体が違法と判断される危険性がある。)

45

Federal Resale Exemptions(転売除外規定)(Cont’d)

• Rule 144: a Section 4(1) safe harbor(セクション

4(1)に対する安全港ルール )

Rule 144 was promulgated by the SEC to provide a safe harbor under the Section 4(1) exemption for holders of restricted securities selling their shares without registration (SECは、セクション4(2)に対する安全港ルー

ルである規則Dと同様な意味で、セクション4(1)に対する安

全港ルールを作った。それが、ルール144)

As a safe harbor, Rule 144 provides objective criteria to ensure that the reseller is not an “underwriter” or otherwise engaged in a “distribution” and that the sale is exempt under securities laws(ルール144に記載してある要

件を満たせば、株式引受人とは判断されず、その所有株式の

転売は禁止されている一般公開にあたる分配にあたらないも

のと判断され、転売を行うことができる。)

46

Federal Resale Exemptions(転売除外規定)(Cont’d)

• Rule 144: a Section 4(1) safe harborRequirements of Rule 144(ルール144の要件)

– Adequate current information regarding the issuer must be available (i.e., registration under the ‘33 Act and reports filed pursuant to Section 12 of the’34 Act)(当該株式の発行会社に関する適切な最新の情報

が入手可能であること。この要件を満たすためには、実際上、その会社が証券法33年法によってSECに登録されており、その後34年法によって定期的にSECに対して会社情報のリポートがなされていることが必要である。)

– Seller must meet a one-year holding period (in the case of non-affiliate – 6 month)(当該株式を売却する者が1年間以上(非関連者の場合は6ヶ月)その株式を保有していること)

47

Federal Resale Exemptions(転売除外規定)(Cont’d)

• Rule 144: a Section 4(1) safe harborRequirements of Rule 144– The volume of shares that may be sold during three-

month period is limited(3ヶ月間における転売株式数が以下の制限内であること)

» The greater of 1% of the outstanding common stock and the average weekly reported volume of trading for the preceding four weeks(その会社の発行済みで、現在も有効に存在している普通株式総数の1%に当たる株式数か、直近の4週間を通算して株式市場で販売されたと公表された株式数の1週間の平均販売株式数、のどちらか大きい方。)

– Securities must be sold in ordinary brokerage transactions, without solicitation (株式の売却が勧誘なしの、株式取引のブローカーを通しての通常の売却であること )

48

Federal Resale Exemptions(転売除外規定)(Cont’d)• Rule 144(K): a section 4(1) safe harbor for non-

affiliatesAn “affiliate” is “a person that directly or indirectly through one or more intermediaries, controls, or is controlled by, or is under common control with, such an issuer”(会社関連者とは、直接、または間接に、株式発行会社を支配し、または、支配され、または共通の支配に服している者)Officers, directors and large shareholders (holders of more than 10% of the outstanding shares of a company) are affiliates (発行済み株式総数の10%以上の株式を保有している者、当該会社の取締役や役員)Rule 144(k) allows non-affiliate to resell securities without current public information being available, volume limitations, or a brokered sale so long as the non-affiliated seller has held the restricted securities for one year(非会社関連者は、上記のルール144で説明した要件、当該株式の発行会社に関する適切な最新の情報が入手可能であること、や、売却株式数の制限や、株式市場におけるブローカーによる通常取引であること、などを満たす必要がなく、未公開株であれ、上場株であれ売却することができる。必要な要件は唯一つ、1年間の株式の保有である。)

49

Federal Resale Exemptions(転売除外規定)(Cont’d)

• Section 4(1½)(セクション4(1と2分の1)の例外)

Section 4(1½) is a hybrid exemption that has been recognized by the SEC and the courts but which does not exist in the statutory text(法律にはないが、判例とSECの判断によって認められてきた法理)

The so-called “Section 4(1½) exemption allows bothaffiliates and non-affiliates to make private resales of securities without registration with the following requirements (以下の要件を満たせば、会社関連者にも会社非関連者にも適用される転売除外である)

– Requirements for sales Section 4(2) or Regulation D private placement exemptions in original issuance and resale transaction are satisfied (株式発行時、および転売取引において、セクション4(2)の要件、または、規則Dの要件を備えること)

50

Federal Resale Exemptions (転売除外規

定)(Cont’d)

• Section 4(1½)Difficulty of Section 4(1½) to rely on– If the issuer’s original offering was not properly

exempt under securities laws, this exemption is not available(最初の発行に証券法違反があれば、のちの

転売も、当初の違法な発行の一部として除外規定が使えなくなる。)

– An emerging company’s original private placement may defective in some way (e.g., no documentation that all offerees were sophisticated, existence of unaccredited investors without proper disclosure) (ス

タートアップの当初の株式発行においてなんらかの証券法違反があることがある)

51

Federal Resale Exemptions (転売除外規

定)(Cont’d)

• Section 4(1½)Difficulty of Section 4(1½) to rely on– If there was a violation of securities laws in the issuer’s

original issuance, even if a resale appears properly made pursuant to Section 4(1½), such resale may be considered part of a public “distribution” in connection with the offering as a whole, and therefore nevertheless violate securities laws (最初の発行に証券法違反があれば、のちの転売も、それだけを見るとセクション4(1と2分の1)の例外の要件を満たして

いるように見えても、当初の発行の一部として転売も違法となる危険性がある。)

– Thus, an issuer should plan properly and document its original issuer exemption so that it can avoid unnecessary resale and other problems in the future (株式発行については

会社設立の最初の段階から、証券法遵守を重視することが、将来のリスクを避けるために重要である。)

52

Federal Resale Exemptions (転売除外規

定)(Cont’d)

• Regulation S: offshore resale exemption(海外転売除外規定)

Regulation S is also available to resales (規則Sは、転売

の場合の例外規定としても適用することができる。)Regulation S does not require any specific disclosure for purposes of meeting the exemption and does not distinguish between accredited and non-accredited investors(会社情報開示について格別な義務は課しておらず、

また、売却の相手が適格投資家でなければならないという制

限もない) Generally, resales by affiliates are subject to greater restrictions than resales by non-affiliates (会社関連者が転

売するときの要件は厳しい)

53

Federal Resale Exemptions (転売除外規

定)(Cont’d)

• Regulation S: offshore resale exemptionRequirements for resale by an “affiliate” (会社関連社が

転売する場合の要件)

– Offers and sale of the securities must be made only in an “offshore transaction” (アメリカ外で取引が行われること)

– Offers and sales of the securities must be made only to non-U.S. persons (取引が非アメリカ人に対して行われること)

– Certain offering restrictions and purchaser certifications and agreements identified in Regulation S must be implemented (規則Sで要求される義務を記載した書面を取り交わすこと)

– Securities resold pursuant to Regulation S must contain a restrictive legend stating, among other things, that the securities may only be transferred pursuant to Regulation S, registration under the ‘33 Act or an exemption therefrom (転売される株券には、規則Sの要件を記載したレジェンドが記載されること)

54

Federal Resale Exemptions (転売除外規

定)(Cont’d)

• Regulation S: offshore resale exemptionRequirements for resale by a non-affiliate (非会社関連者が転売する場合の要件)

– Offers and sale of the securities must be made only in an “offshore transaction” (アメリカ外の取引であること)

– Offers and sales of the securities must be made only to non-U.S. persons (非アメリカ人に対する取引であること)

Because the non-affiliate need only be concerned with the “non-U.S. person” and “off-shore transaction” requirements, Regulation S provides the non-affiliate significant flexibility to resell its shares (非会社関連者による転売の場合は以上の2点だけが要件であるから、転売は容易)

39 Offices in 19 Countries

www.squiresanders.com