does the bsc improve performance? a review of the empirical...

TRANSCRIPT

Aarhus University

School of Business and Social Sciences

1st of August 2015

Does the BSC improve performance?

A review of the empirical literature

Author:

Anca Ichim

Academic Supervisor:

Rainer Lueg

Program:

MSc. Management Accounting and Control

Number of characters without spaces: 126.027

Page | 2

Abstract

The Balanced Scorecard is a well known and widely used strategic performance management

system. The evidence of the BSC’s influence on performance is claimed to be both ambiguous

and limited to financial measures. By using a systematic review of empirical literature, this paper

identifies a total of 266 studies published between 1992 and March 2015, out of which only 53

specifically address the performance effects of the BSC. Based on these studies, the author seeks

to offer some insights into how the adoption of the BSC can bring economic and intangible

benefits to organizations, considering, among others, the implementation stage, how the actors

are influenced by the implementation and the way performance is reported. The findings suggest

that a successful BSC implementation leads to a wide variety of performance improvements,

both financial and non-financial. Based on the findings and knowledge gathered from the paper,

some recommendations are also suggested for future research.

Page | 3

Table of contents

1. Introduction ……………………………………………………………………… 5

2. Theoretical background …………………………………………………………... 6

2.1. The balanced scorecard and organizational performance…………………….. 6

2.2. Types of BSC ………………………………………………………………… 7

3. Methodology …………………………………………………………………….. 9

3.1. Planning the review …………………………………………………………... 9

3.2. Conducting the review ……………………………………………………….. 10

3.3. Reporting and dissemination …………………………………………………. 11

4. The literature review ……………………………………………………………… 12

4.1. A brief description of the identified categories ……………………………… 12

4.2. The general context of the studies …………………………………………… 17

4.2.1. The evolution of research over time …………………………………... 17

4.2.2. Sectors of activity and industry settings ……………………………… 18

4.2.3. The geographic location ………………………………………………. 20

4.3. The Author’s Perspective …………………………………………………….. 22

4.3.1. Publication patterns …………………………………………………… 23

4.3.2. Research method and type of data …………………………………… 24

4.3.3. Sizes and types of organizations ……………………………………… 25

4.3.4. The BSC’s implementation status …………………………………….. 26

4.3.5. The research topic …………………………………………………... 26

4.3.6. Key informants ……………………………………………………….. 26

4.4. The organization’s perspective ………………………………………………. 27

4.4.1. The BSC’s time frame ………………………………………………… 28

4.4.2. The BSC’s implementation phase ……………………………………. 28

4.4.3. The BSC’s implementation status ……………………………………. 29

4.4.4. Linked incentives …………………………………………………….. 29

4.4.5. Reasons behind BSC adoption ……………………………………….. 30

4.4.6. The performance effects of the BSC …………………………………. 30

4.4.7. Motivated/ influenced actors …………………………………………. 31

5. Discussion ………………………………………………………………………… 33

Page | 4

5.1. Findings regarding the impact of the BSC on organizational performance …... 33

5.1.1. Non-representative studies ……………………………………………. 33

5.1.2. Representative studies ………………………………………………… 36

5.1.3. Comparison of the representative studies …………………………….. 41

5.2. Recommendations for future research ……………………………………….. 43

6. Limitations and conclusion ……………………………………………………….. 45

6.1. Limitations …………………………………………………………………… 45

6.2. Conclusion …………………………………………………………………… 45

7. References ………………………………………………………………………… 47

8. Appendices ………………………………………………………………………72

Page | 5

1. Introduction

The Balanced Scorecard (BSC) was first introduced in 1992 as a framework for performance

measurement, eventually being transformed and developed into a strategic management tool,

suited for today’s highly competitive, complex and continuously changing business environment,

a performance management system which “provides managers with the instrumentation they

need to navigate to future competitive success” (Kaplan & Norton, 1996a). The framework is

constructed by translating the company’s strategy and mission into objectives and

comprehensive performance measures across four perspectives: financial, customers, internal

business processes and learning and growth.

There are many researchers claiming that evidence of the BSC’s impact on organizational

performance is limited and ambiguous in the literature, focusing mostly on financial performance

improvements (Capelo and Dias, 2009; Tapinos et al., 2008; Chenhall, 2005).

In their third book on the BSC, Kaplan and Norton tracked the performance of many companies

implementing the BSC, companies that they observed achieving breakthrough performance,

especially through alignment and focus. According to them, “many other organizations now have

adopted the Balanced Scorecard and achieved remarkable results”(Kaplan & Norton, 2001). This

paper seeks to investigate Kaplan and Norton’s performance claim of the BSC, to see how the

BSC implementation and use influence the organizational performance. Therefore, the main

research question (RQ) of the paper is: Does the BSC implementation positively impact the

organizational performance within the empirical BSC literature?

Answering the RQ will also imply investigating the way the effects on performance are assessed

and reported, in what stage of implementation they appear and how the BSC motivates its actors

to improve performance.

The paper approaches a systematic literature review focused on empirical research from January

1992 to March 2015 considered relevant for the purpose of this paper, namely 266 worldwide

studies, across all sectors. Even if the main focus will be on the studies that provide evidence of

performance improvement using the BSC, the other empirical studies dealing with the BSC will

be dealt with as well, in order to offer a more insightful view of how the BSC is actually used in

practice.

Page | 6

The paper seeks to contribute to the body of knowledge on the BSC by providing practitioners

with guidance, examples and insights of how the BSC use influences organizational performance

and informing the research community on the up-to-date empirical literature on the BSC and its

effects on performance.

The remainder of this paper is organized as follows: Section 2 presents the theoretical

background for the paper, Section 3 details the methodology used in selecting the empirical

studies, Section 4 covers the literature review, Section 5 is dedicated to the discussion part and

recommendations for future research, while the last part, Section 6, outlines the limitations of the

studies and the conclusion.

2. Theoretical background

2.1. The Balanced Scorecard and organizational performance

The BSC was first introduced in 1992. What started as a performance measurement system soon

became a strategic performance management tool that goes beyond just being a set of financial

and non financial measures. It uses four perspectives to translate the strategy into a linked set of

measure across four perspectives: financial, customers, internal business processes and learning

and growth. In order to achieve performance improvements, the scorecard should have leading

and lagging indicators specific to each organization, linked together by cause-and-effect

relationships (Kaplan and Norton, 1996a, 2001a).

To lead to enhanced organizational performance, a BSC should become the corner stone of the

management system (Kaplan and Norton, 1996c), which “wires every part of the organization to

the strategy” (Kaplan and Norton, 2001b, p. 64).

The BSC has rapidly become a widely used management tool around the world. Since its

appearance, a lot of studies have been conducted to attest its popularity. A more recent example

is a study by Bain and Company, Management Tools and Trends 20131, conducted on more than

12.000 respondents around the world, which shows that the BSC is the 5th most used

1 See http://www.bain.com/publications/articles/management-tools-and-trends-2013.aspx

Page | 7

management tool in the world. The same study also positions the BSC at the top of the list in

Europe, Middle East and Africa.

Besides its wide use and increasing popularity, the BSC faces also considerable critique

regarding its effectiveness and lack of clear evidence in regards to organizational performance.

For example, Nørreklit (2005, p. 611) claims that Kaplan and Norton present no sound

arguments to prove that the BSC actually give the results they claim, creating nothing more than

an illusion by using metaphors and other stylistic devices. She goes even forward in describing

the BSC as being part of the “genre of the management guru text”. Otley (1999, p. 375, 376)

argues ambiguity in target setting, in reward structures, the role of feedback or when analytically

linking leading and lagging indicators, claiming that the chain of events that would lead to

performance improvement is merely a simplified reality.

Even though Kaplan and Norton suggest that “the BSC clearly reveals the value drivers for

superior long-term financial and competitive performance” (Kaplan and Norton, 1996a, p.8),

they also state that it takes sustained effort and time – two to three years from implementation -

for the actual breakthrough performance to be achieved (Kaplan and Norton, 2001c).

Kaplan, in a journal article written in 2012, expressed his concern about the “narrow perspective

on the implications of the BSC for management theory on practice” (Kaplan, 2012, p. 540),

surprised by the fact that the critiques and commentaries regarding the BSC are only focusing on

the BSC as a measurement system, as first described in 1992, and not on the BSC they have been

focusing their attention on for the last 16 years (see Kaplan, 2012 p. 540). This concern is also in

line with the findings of Lawrie and Cobbold (2004, p. 618), that suggest the academic

contributions tend to focus more on the BSC as a management tool for control. On the same

subject, Braam and Nijssen (2004, p. 345) concluded their study by stating that “a focus on

performance measurement instead of performance management will impede the realization of

organizational objectives and may even prove counterproductive by hurting company

performance”.

2.2. Types of BSC

Based on the BSC concept developed by Kaplan and Norton over time, Speckbacher et al. (2003,

p. 363) identified three main types of BSC. Type I BSC is the “minimum standard BSC”

Page | 8

(Speckbacher et al., 2003, p. 362), a performance measurement system using financial and non-

financial measures and linking tangible and intangible assets.

Type II BSC takes the Type I BSC to the next step by describing the strategy using clear cause-

and-effect linkages between objectives and introducing the strategy map. The BSC is still a

performance measurement system, only with measures linked to strategy.

Lastly, Type III BSC is the “fully-developed BSC” (Speckbacher et al., 2003, p. 362) and it goes

from a measurement system to a strategic management system, using defined objectives and

action plans to describe and implement the strategy. It also ties the incentives to the BSC for

positive motivation, which leads, along with communication and action plans, to strategy

implementation.

In the same note, Lawrie and Cobbold (2004) identified 3 generations of BSC. The first

generation BSC was described as a vague control tool for managers, used merely for

measurement and reporting.

The second generation BSC introduced some key innovations like strategy maps, strategic

objectives and causality that helped the process of identifying, filtering and weighting the

measures of the scorecard.

Finally, the third generation scorecard is described as a more functional second generation BSC,

with enhanced strategic relevance. The strategic objectives and target settings are now revised

and validated, identifying the inconsistencies.

Both Type III and the 3rd generation BSC fully fit Kaplan and Norton’s strategic performance

management system, who suggest that “a successful BSC should be a change project, not a

metrics project” (Kaplan and Norton, 2001b, p.64). The cases where the incentives are not yet

linked to the BSC must not be overlooked, following Kaplan and Norton’s (1996a, p. 283)

advice that organizations might need to “get some experience in managing the BSC before

explicitly tying compensation to it”. This way, the value creation that might occur in the earlier

stages of implementation will be also captured.

Page | 9

3. Methodology

In order to investigate and answer the research questions of this paper, the systematic review

methodology will be used - a methodology that has its roots in medical research and consists of a

replicable and transparent process that gathers existing studies and leads to identifying key

contributions to a specific topic or problem (Tranfield et al., 2003, p. 209).

This type of research should not seek to “provide answers or to replace judgment and experience,

but instead […] to inform decision making and action” (Denyer and Tranfield, 2009, p. 686).

Denyer and Tranfield (2009, p. 671) define the systematic review as being “a specific

methodology that locates existing studies, selects and evaluates contributions, analyses and

synthesizes data, and reports the evidence in such a way that allows reasonably clear conclusions

to be reached about what is and what is not known”. The outcomes of the systematic review can

consist either of robust and dependable evidence or incongruent findings that identify knowledge

gaps and areas that need more research (Denyer and Tranfield, 2009, p. 672).

The systematic review can be a rigorous and powerful tool, at the same time raising some

challenges when it comes to synthesizing the results (Denyer et al., 2008, p. 304). In order to

tackle some of these challenges, Rousseau et al. (2008, p. 485) propose not to favor one research

method over another but to that all methods have limitations, consider the cultural and political

implications of evidence, by acknowledging the differences among geographical locations and

considering different theoretical and methodological perspectives.

The systematic review process comprises three main stages: planning the review, conducting the

review and reporting and dissemination (Tranfield et al., 2003, p. 214). All stages will be dealt

with in the following part of the paper, to ensure transparency and understanding of the empirical

literature selection process.

3.1. Planning the review

This first stage of the review helps delimiting the subject area and assessing the relevance and

size of the literature (Tranfield et al., 2003, p.214).

With the research problem in mind, the initial search started with deciding upon the databases

that will be used to identify the studies. The author first employed EBSCO, one of the largest

Page | 10

known scientific databases that provide a broad coverage of research studies. The search was

then extended to ABI Inform (ProQuest) database, in order to consider more relevant studies and

to include also interdisciplinary and alternative perspectives on the topic.

The next inclusion criteria were the language of the studies, set to English, and the time frame,

which has been set from 1992 to March 2015, 1992 being the year when Kaplan and Norton

published their first article on the BSC, and March 2015 being the time this research started. The

search was also limited to studies containing the string “Balanced Scorecard” anywhere in the

articles’ title, key words or abstract. The decision of including also the abstract was based on the

fact that the abstract announces the key themes and main points of the study (Booth et al., 2008,

p. 211).

The last inclusion criterion established on this stage involves the searching source, which was set

to journal contributions. Studies published in journals offer the warranty of a certified, worth

reading contribution (Davis, 2014, p. 200).

A total of 1378 studies resulted from the search within EBSCO database and 960 from ABI

Inform.

3.2. Conducting the review

This second stage of the review consists primarily of assessing the quality of the selected studies,

which is a relatively subjective and challenging process. The bias can be reduced by selecting the

studies based on the implicit quality rating of the journals and by using data extraction forms to

document the entire process (Tranfield et al., 2003, p.217).

To make sure the review considers high quality, relevant studies, only the peer reviewed articles

have been included, published in journals that scored at least 2 in the Academic Journal Guide

20152, the rating 2 being assigned to journals of an acceptable standard. Journals that scored less

than 2 were excluded because they are considered of a “more modest standard […] and few

journals in this category carry a citation impact factor” (Academic Journal Guide 2015, p. 7).

This set of constrains reduced the number of studies to 449 in EBSCO database. ABI Inform

2 See Appendix 1 – The Academic Journals and Subject Areas. See http://www.bizschooljournals.com/academic-

journal-guide-2015/ for more information.

Page | 11

added 90 more studies. A total of 539 relevant articles were revealed after this step of the review

process.

To further decrease the risk of excluding relevant articles, the VHB 20153 journal ranking of the

German Academic Association for Business Research has been used. This ranking “has become

the most influential journal evaluation approach in German-speaking countries” (Schrader and

Hennig-Thurau, 2009, p. 180). Only articles published in journals ranking from A+ (world

leading journals) to C (recognized journals) were considered (Harzing, 2015, p.10). This added

14 extra studies, making a total of 553 articles.

The next step on this stage consisted of examining the abstracts and introductions of all the

articles in order to identify only the empirical studies focusing on the BSC. As a result, 287

articles have been removed from the review.

This was also the step where the data extraction forms were employed, classifying all empirical

studies resulted so far from the search, according to their general information like title, authors,

publication year and publication journal, but also study features and specific information like

industry, geographic location, topic and themes, research methods and key results. At this point,

all information needed to summarize and synthesize the data in a comprehensible and

documented manner is gathered, the final data set basis for this research comprising a total of

266 studies.

3.3. Reporting and dissemination

Reporting and dissemination is the last stage of the review and starts with synthesizing and

organizing all 266 identified empirical studies, based on the main research topic and findings

specified in the data extraction forms, in order to provide an overall up-to-date picture of the

BSC research. To capture all relevant information from the studies, both Excel and the

qualitative research tool Atlas.ti have been used. Seven main categories have been identified

after reading the studies, as it can be observed in Table 1 below. All seven categories for the

classification have been subjectively established by the author after reading the studies and based

on the normative theory of the BSC to ensure the reliability of the process. They will be

3 See Appendix 1 – VHB JOURQUAL 3 ranking. See http://vhbonline.org/service/jourqual/vhb-jourqual-

3/gesamtliste/ and http://www.harzing.com/download/jql_subject.pdf for more information.

Page | 12

described and analyzed in the following part of the paper, with a greater focus on the last

category, which represents the main data set considered for answering the research question.

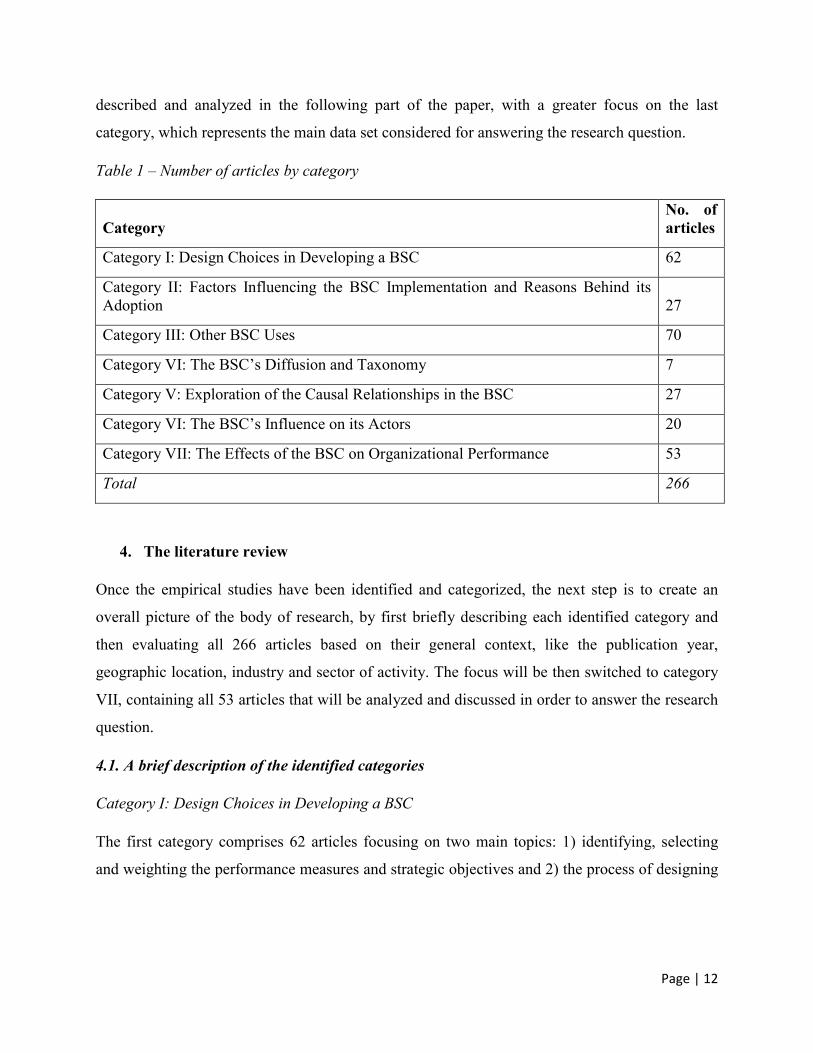

Table 1 – Number of articles by category

Category No. of articles

Category I: Design Choices in Developing a BSC 62

Category II: Factors Influencing the BSC Implementation and Reasons Behind its Adoption 27

Category III: Other BSC Uses 70

Category VI: The BSC’s Diffusion and Taxonomy 7

Category V: Exploration of the Causal Relationships in the BSC 27

Category VI: The BSC’s Influence on its Actors 20

Category VII: The Effects of the BSC on Organizational Performance 53

Total 266

4. The literature review

Once the empirical studies have been identified and categorized, the next step is to create an

overall picture of the body of research, by first briefly describing each identified category and

then evaluating all 266 articles based on their general context, like the publication year,

geographic location, industry and sector of activity. The focus will be then switched to category

VII, containing all 53 articles that will be analyzed and discussed in order to answer the research

question.

4.1. A brief description of the identified categories

Category I: Design Choices in Developing a BSC

The first category comprises 62 articles focusing on two main topics: 1) identifying, selecting

and weighting the performance measures and strategic objectives and 2) the process of designing

Page | 13

a BSC in general4. Only the design choices are dealt with in these articles, offering no details

about the impacts and outcomes of actually implementing and using the BSC.

Close to 70% of all articles in this first category revolve around the first topic. Most of the

studies are researching different methods and models for identifying and selecting performance

measures and strategic objectives. One such method is multiple-criteria decision-making, or

MCDM (Wu et al., 2009 and Grigoroudis et al., 2011), especially using the Analytic Network

Process (ANP) method (Poveda-Bautista et al., 2012; Yüksel and Metin, 2010; Hsu et al., 2011

and Boj et al., 2014) and the Analytic Hierarchy Process (AHP) method (Bentes et al., 2012;

Reisinger et al., 2003; Bhagwat and Sharma, 2007; Lee et al. 2008; and Huang et al. 2011). The

integration of SWOT analysis and BSC is another research topic that presents interest among

researchers in this category, with a total of 6 articles (Truong-Van et al., 2008; Lee et al., 2000;

Lee and Ko, 2000; Quezada et al., 2009; Bentes et al., 2012 and Ip and Koo, 2004).

The second topic includes articles which focus on the design phase of the BSC in general. Most

of them deal with the integration of BSC with different models, like Supply Chain Operation

Reference (SCOR) (Thakkar et al., 2009), European Foundation for Quality Management

(EFQM) (Andjelkovic Pesic and Dahlgaard, 2013), Critical Success Factors (van Veen-Dirks

and Wijn, 2002), system dynamics (Akkermans and Van Oorschot, 2005), systemic quality

(Solano et al., 2003) or the boosting approach (Creamer and Freund, 2010).

Category II: Factors Influencing the BSC Implementation and Reasons behind its Adoption

Appendix 3 presents all 27 articles belonging to this second category, investigating reasons and

factors that facilitate or impede the BSC implementation. Factors influencing the BSC adoption

vary from behavioral ones (de Waal, 2003 and de Waal, 2006), to contingency factors like firm

size and demand volatility (Hendricks et al., 2012) or internal and external forces (Manville,

2006 and Lansiluoto and Jarvenpaa, 2008). The study of Upton and Arlington (2012) revealed

that the BSC has “some degree of racial basis”, while Naranjo-Gil (2009) and Naranjo-Gil et al.

(2009) concluded that the BSC adoption is influenced by the managers’ background and

characteristics. Simulation, inscriptions and graphic representations are also factors identified to

4 See Appendix 2 – Category I: Design Choices in Developing a BSC.

Page | 14

influence the understanding and adoption of the BSC (Capelo et al., 2015; Rachman-Moore and

Kenett, 2006; Kunc, 2008 and Qu and Cooper, 2011).

Category III: Other BSC Uses

70 articles are included in this category5, making it the most popular one and demonstrating that

the BSC is widely used in different domains and for different purposes compared to its original

one, as a strategic performance management tool.

More than 15% of articles in this category explore using the BSC in ranking and rating

companies in different industries, based on their performance (Zhigang et al., 2013; Bai et al.,

2014; Rabbani et al., 2014; Rotchanakitumnuai, 2013; Dias-Sardinha and Reijnders, 2005; Eom

et al., 2008; Huang, 2008; Douglas and Mills, 2004; MacKerron et al., 2015; Kline et al., 2004

and Jamshed et al., 2014).

Other popular research topics in this category is the use of the BSC in assessing and selecting

investment portfolios (Hanafizadeh et al., 2009; Tsai et al., 2009; Meadows and Pike, 2010;

Tavana et al., 2014 and Hanafizadeh and Moayer, 2008), assessing and selecting information

systems (Martinsons and Davidson, 1999; Loukis and Charalabidis, 2013; Chang et al., 2011;

Tsai et al., 2012; Cebeci, 2009 and Chand et al., 2005) or measuring the performance of

knowledge management (Valmohammadi and Ahmadi, 2015; Chen et al., 2009 and Möller and

Schaltegger, 2003), supply chain management (Bhagwat and Sharma, 2007; Kim and Rhee,

2012; Chang, 2009 and Bhattacharya et al., 2014) and customer management (Shafia et al., 2011;

Kim et al., 2003 and Wu and Hung, 2008).

This category comprises also a number of 5 articles that that explore the BSC used only for

measurement and reporting, without any clear links to strategy (Hoque and Adams, 2011; Malmi,

2001; Länsiluoto and Järvenpää, 2010; Askim, 2004 and Griffith and Neely, 2009).

Category IV: The BSC’s Diffusion and Taxonomy

The fourth category includes only 7 studies, dealing with the classification and spreading of the

BSC6. The study of Speckbacher et al. (2003) investigates the use of BSC in German speaking

countries, identifying 3 types of BSC, while Soderberg et al. (2011) distinguish a five-level BSC

5 See Appendix 4- Category II: Other BSC Uses

6 See Appendix 5 – Category IV: The BSC’s diffusion and taxonomy.

Page | 15

classification by researching the BSC use in Canadian companies. Two of the articles carry out

research on the BSC’s diffusion in Nepal and Nordic countries: the study of Kald and Nilsson

(2000) provides evidence of a wide BSC adoption in Nordic companies, with 27% of

respondents already using it and 61% considering using it in the future, while in Nepal, 40% of

the surveyed companies claimed to use a BSC (Upadhaya et al., 2014).

Category V: Exploration of the Causal Relationships in the BSC

The validity of the causal relationships in the BSC has been contested and criticized over time.

For example, Nørreklit (2000, p. 71) finds the cause-and-effect relationships between the

performance measures in the BSC to be problematic, failing to consider the time dimension. She

also states that the relationships between measures are unclear and “ambiguously defined”

(Nørreklit, 2000, p. 72). Despite the criticism, empirical research brings contrasting evidence,

with more than 44% of the 27 articles7 grouped in this category attesting the validity of the

causal relationships between measures in the BSC perspectives. The study of Huang et al. (2007)

validates the causal model of the BSC in the hospitality industry in China, while in Greece a

sequential positive correlation resulted among the BSC perspectives (Cohen et al., 2008). On the

same note, Chareonsuk and Chansangavej (2010) concluded their study by stating that "the

commonly assumed causal relationships are confirmed". Only one article did not validate the

cause-and-effect relationships, due to a conflict of indicators in the case organization’s BSC

(Patel et al., 2008).

Besides the articles attesting the causal relationships validity, this fifth category includes also

empirical studies that investigate the use of different models and methods to assess the causality,

like Analytic Hierarchy Process (AHP) and linear programming (Quezada and López-Ospina,

2014) or system dynamics (Bernabè, 2011 and Nielsen and Nielsen, 2012).

Category VI: The BSC’s Influence on its Actors

Appendix 7 presents all 20 articles included in this category and exploring the effects the BSC

implementation have on employees, managers and other stakeholders.

The BSC strategy maps are found to positively influence the manager’s mental models and their

performance (Capelo and Dias, 2009) and to reduce the managers’ causal ambiguity regarding 7 See Appendix 6 – Category V: Exploration of the Causal Relationships in the BSC.

Page | 16

the pursued objectives (González, 2012). In line with these findings, we learn from the study of

Cheng and Humphreys (2012) that the strategy maps “enhances both managers' information

relevance and strategy appropriateness judgments” (p.899).

Another topic of research in this fifth category revolves around the influence of common vs.

unique measures in the BSC. Results from Lipe and Salteiro (2000) suggest that common

measures have a higher influence on managers’ performance evaluations than unique measures.

The same results are also confirmed in the study of Banker et al. (2004).

Molina et al. (2014) concluded that BSC implementation and the active involvement of

employees leads to motivation, satisfaction and higher commitment. On the contrary, from

Antonse (2014) we learn that the BSC “strengthens formal control and reduces employees’ scope

for contributing new ideas […] and inhibits the communication of new ideas” (p.49)

The Effects of the BSC on Organizational Performance is the last identified category, covering a

total of 53 articles that represent the main data set which will be thoroughly analyzed in the

remaining of the paper. A detailed presentation of all 53 identified empirical studies can be found

in Appendix 8.

Page | 17

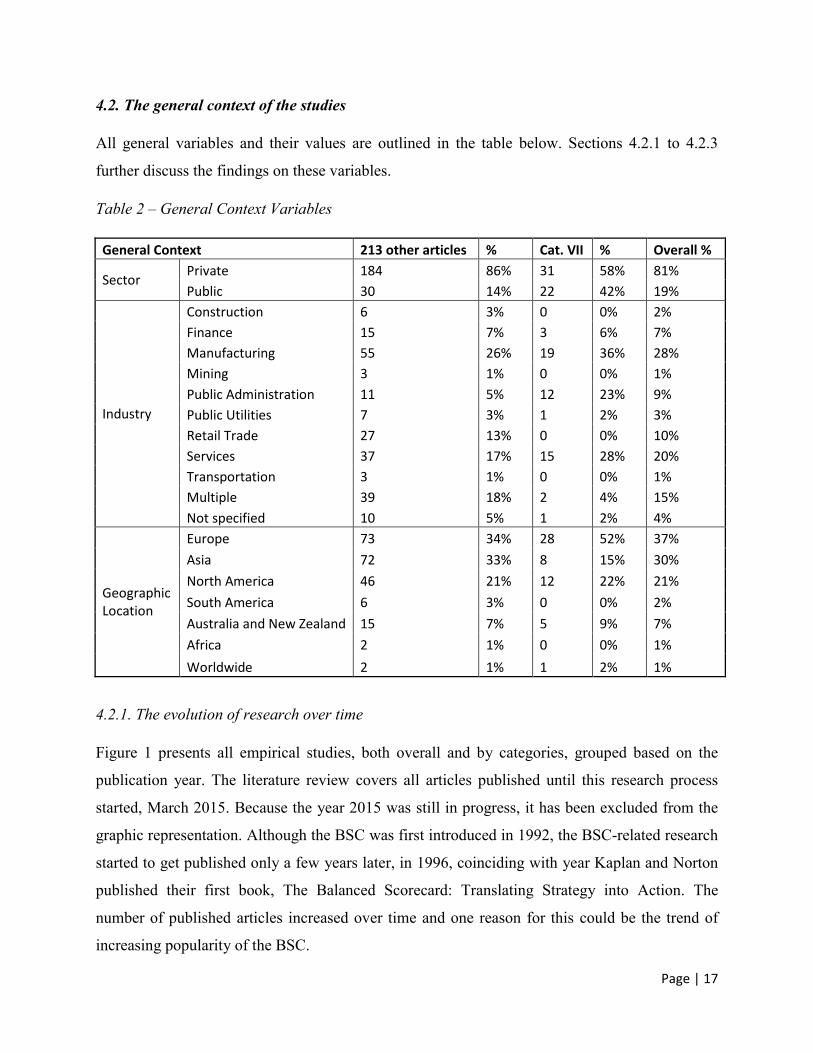

4.2. The general context of the studies

All general variables and their values are outlined in the table below. Sections 4.2.1 to 4.2.3

further discuss the findings on these variables.

Table 2 – General Context Variables

General Context 213 other articles % Cat. VII % Overall %

Sector Private 184 86% 31 58% 81%

Public 30 14% 22 42% 19%

Industry

Construction 6 3% 0 0% 2%

Finance 15 7% 3 6% 7%

Manufacturing 55 26% 19 36% 28%

Mining 3 1% 0 0% 1%

Public Administration 11 5% 12 23% 9%

Public Utilities 7 3% 1 2% 3%

Retail Trade 27 13% 0 0% 10%

Services 37 17% 15 28% 20%

Transportation 3 1% 0 0% 1%

Multiple 39 18% 2 4% 15%

Not specified 10 5% 1 2% 4%

Geographic Location

Europe 73 34% 28 52% 37%

Asia 72 33% 8 15% 30%

North America 46 21% 12 22% 21%

South America 6 3% 0 0% 2%

Australia and New Zealand 15 7% 5 9% 7%

Africa 2 1% 0 0% 1%

Worldwide 2 1% 1 2% 1%

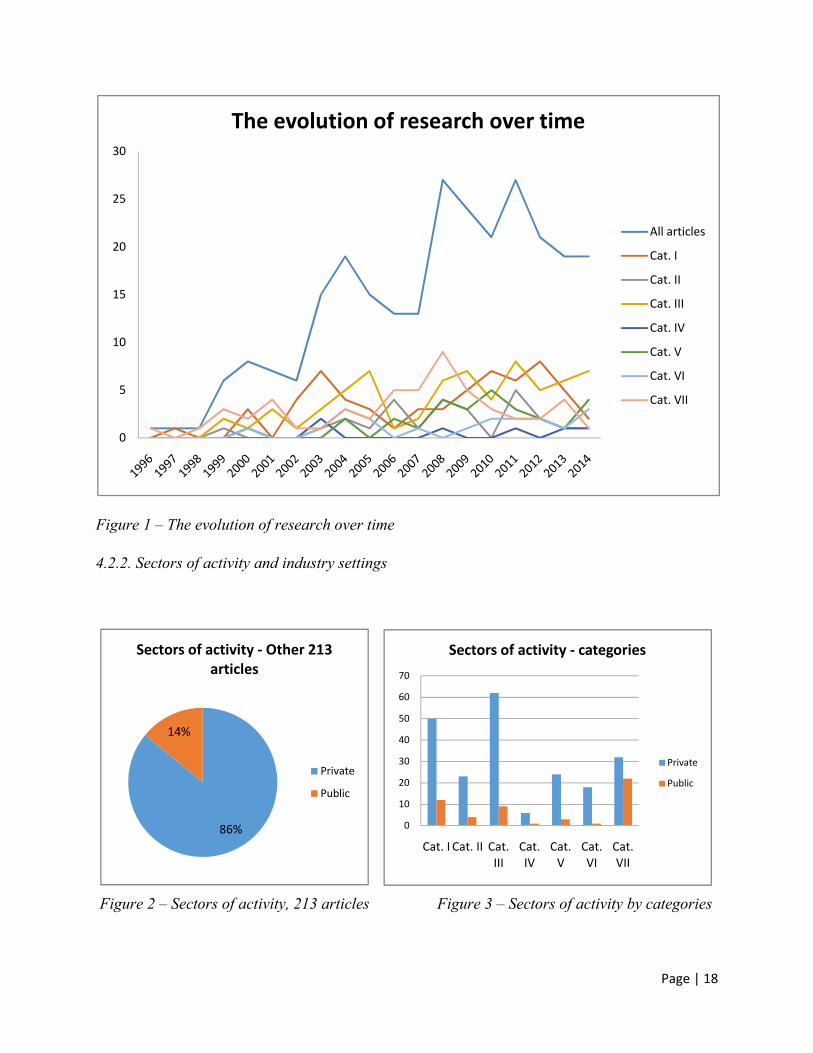

4.2.1. The evolution of research over time

Figure 1 presents all empirical studies, both overall and by categories, grouped based on the

publication year. The literature review covers all articles published until this research process

started, March 2015. Because the year 2015 was still in progress, it has been excluded from the

graphic representation. Although the BSC was first introduced in 1992, the BSC-related research

started to get published only a few years later, in 1996, coinciding with year Kaplan and Norton

published their first book, The Balanced Scorecard: Translating Strategy into Action. The

number of published articles increased over time and one reason for this could be the trend of

increasing popularity of the BSC.

Page | 18

Figure 1 – The evolution of research over time

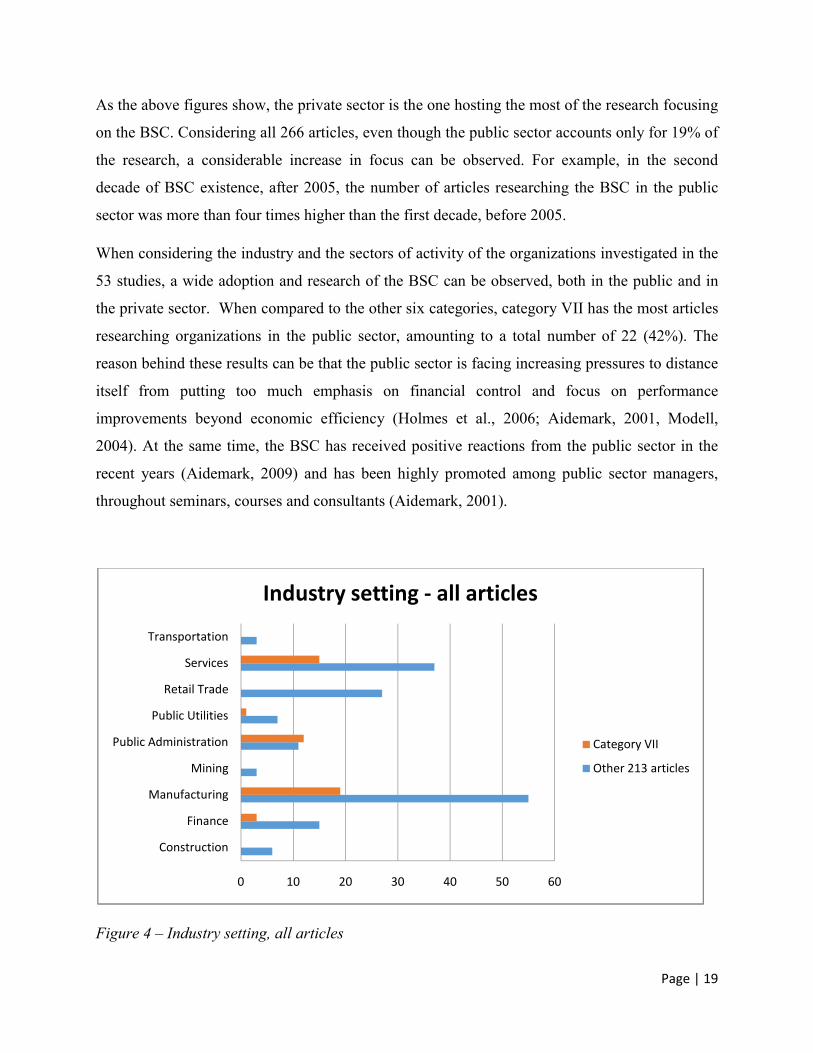

4.2.2. Sectors of activity and industry settings

Figure 2 – Sectors of activity, 213 articles Figure 3 – Sectors of activity by categories

0

5

10

15

20

25

30

The evolution of research over time

All articles

Cat. I

Cat. II

Cat. III

Cat. IV

Cat. V

Cat. VI

Cat. VII

0

10

20

30

40

50

60

70

Cat. I Cat. II Cat. III

Cat. IV

Cat. V

Cat. VI

Cat. VII

Sectors of activity - categories

Private

Public

86%

14%

Sectors of activity - Other 213 articles

Private

Public

Page | 19

As the above figures show, the private sector is the one hosting the most of the research focusing

on the BSC. Considering all 266 articles, even though the public sector accounts only for 19% of

the research, a considerable increase in focus can be observed. For example, in the second

decade of BSC existence, after 2005, the number of articles researching the BSC in the public

sector was more than four times higher than the first decade, before 2005.

When considering the industry and the sectors of activity of the organizations investigated in the

53 studies, a wide adoption and research of the BSC can be observed, both in the public and in

the private sector. When compared to the other six categories, category VII has the most articles

researching organizations in the public sector, amounting to a total number of 22 (42%). The

reason behind these results can be that the public sector is facing increasing pressures to distance

itself from putting too much emphasis on financial control and focus on performance

improvements beyond economic efficiency (Holmes et al., 2006; Aidemark, 2001, Modell,

2004). At the same time, the BSC has received positive reactions from the public sector in the

recent years (Aidemark, 2009) and has been highly promoted among public sector managers,

throughout seminars, courses and consultants (Aidemark, 2001).

Figure 4 – Industry setting, all articles

0 10 20 30 40 50 60

Construction

Finance

Manufacturing

Mining

Public Administration

Public Utilities

Retail Trade

Services

Transportation

Industry setting - all articles

Category VII

Other 213 articles

Page | 20

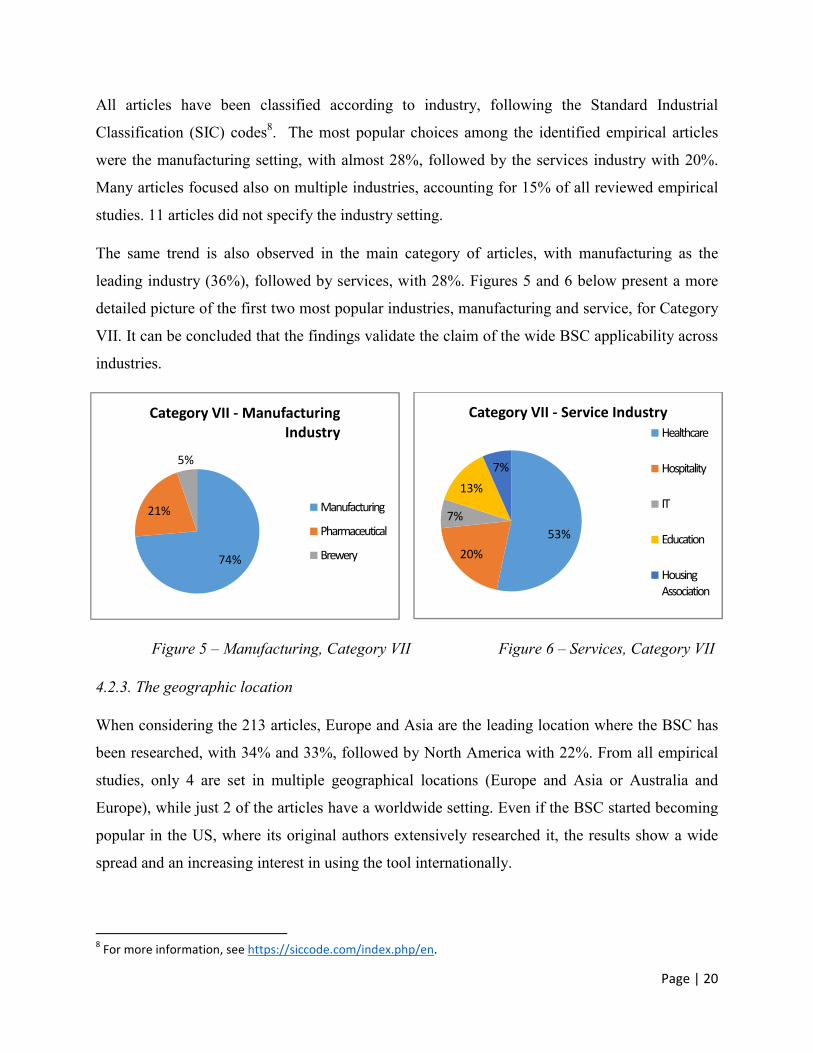

All articles have been classified according to industry, following the Standard Industrial

Classification (SIC) codes8. The most popular choices among the identified empirical articles

were the manufacturing setting, with almost 28%, followed by the services industry with 20%.

Many articles focused also on multiple industries, accounting for 15% of all reviewed empirical

studies. 11 articles did not specify the industry setting.

The same trend is also observed in the main category of articles, with manufacturing as the

leading industry (36%), followed by services, with 28%. Figures 5 and 6 below present a more

detailed picture of the first two most popular industries, manufacturing and service, for Category

VII. It can be concluded that the findings validate the claim of the wide BSC applicability across

industries.

Figure 5 – Manufacturing, Category VII Figure 6 – Services, Category VII

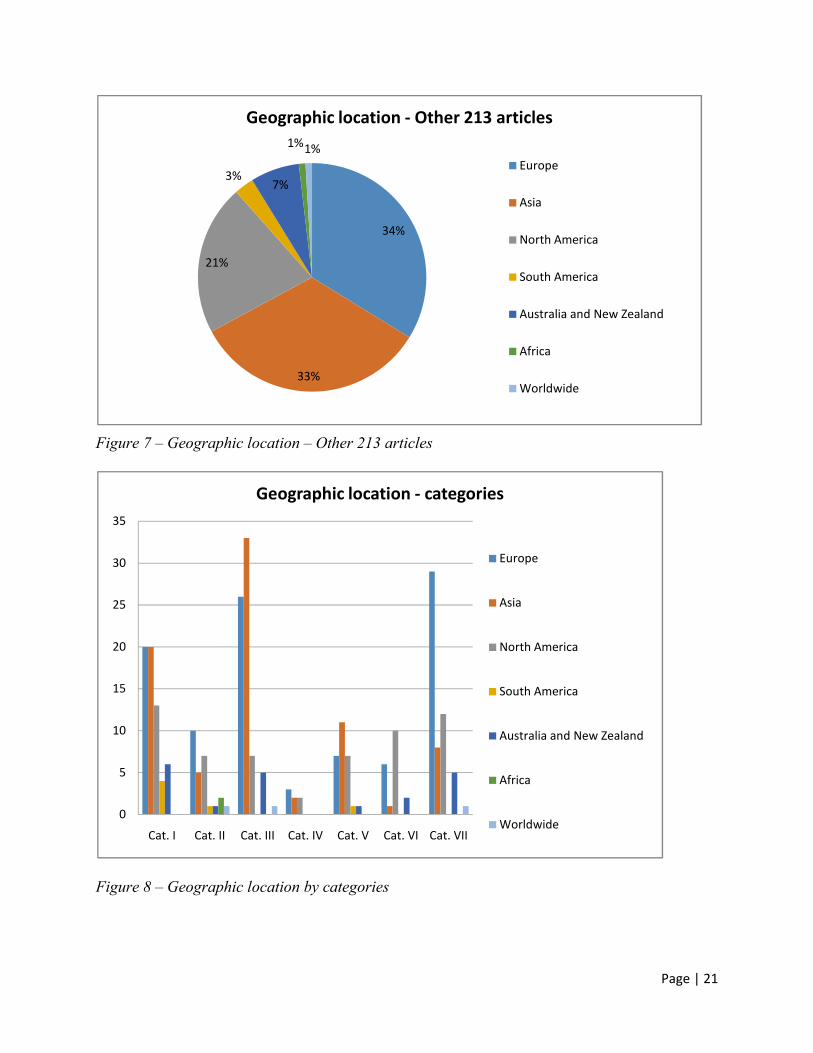

4.2.3. The geographic location

When considering the 213 articles, Europe and Asia are the leading location where the BSC has

been researched, with 34% and 33%, followed by North America with 22%. From all empirical

studies, only 4 are set in multiple geographical locations (Europe and Asia or Australia and

Europe), while just 2 of the articles have a worldwide setting. Even if the BSC started becoming

popular in the US, where its original authors extensively researched it, the results show a wide

spread and an increasing interest in using the tool internationally.

8 For more information, see https://siccode.com/index.php/en.

53%

20%

7%

13%

7%

Category VII - Service IndustryHealthcare

Hospitality

IT

Education

Housing Association

74%

21%

5%

Category VII - Manufacturing Industry

Manufacturing

Pharmaceutical

Brewery

Page | 21

Figure 7 – Geographic location – Other 213 articles

Figure 8 – Geographic location by categories

34%

33%

21%

3%7%

1%1%

Geographic location - Other 213 articles

Europe

Asia

North America

South America

Australia and New Zealand

Africa

Worldwide

0

5

10

15

20

25

30

35

Cat. I Cat. II Cat. III Cat. IV Cat. V Cat. VI Cat. VII

Geographic location - categories

Europe

Asia

North America

South America

Australia and New Zealand

Africa

Worldwide

Page | 22

Regarding the geographic location of the 53 studies in the main data base, Europe is the leading

setting, with 52%, followed by North America with 22% and Asia with 15%. Only one study

(Tapinos et al., 2011) conducts the research worldwide, while Africa and South America are not

considered at all as a research setting, contrary to the BSC usage rate of 39% in Latin America

found by Bain & Co for the year 20149. Except for Cooper and Ezzamel (2013), no other study

considers multiple locations across continents.

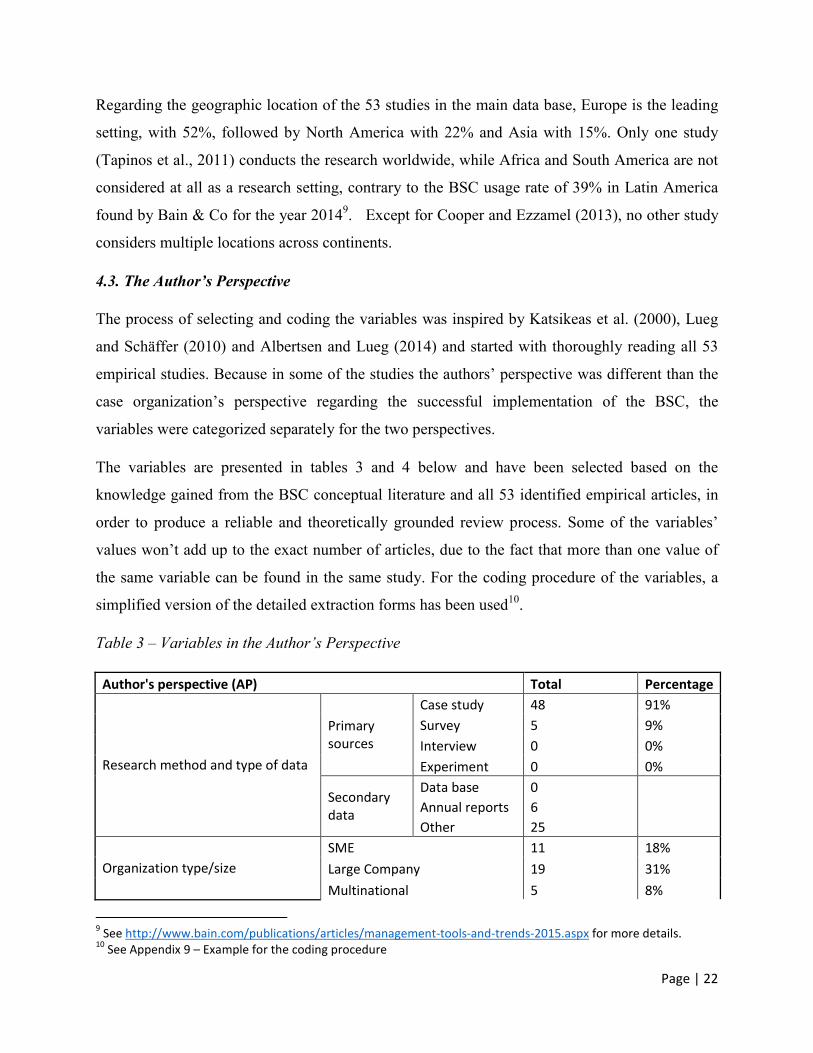

4.3. The Author’s Perspective

The process of selecting and coding the variables was inspired by Katsikeas et al. (2000), Lueg

and Schäffer (2010) and Albertsen and Lueg (2014) and started with thoroughly reading all 53

empirical studies. Because in some of the studies the authors’ perspective was different than the

case organization’s perspective regarding the successful implementation of the BSC, the

variables were categorized separately for the two perspectives.

The variables are presented in tables 3 and 4 below and have been selected based on the

knowledge gained from the BSC conceptual literature and all 53 identified empirical articles, in

order to produce a reliable and theoretically grounded review process. Some of the variables’

values won’t add up to the exact number of articles, due to the fact that more than one value of

the same variable can be found in the same study. For the coding procedure of the variables, a

simplified version of the detailed extraction forms has been used10.

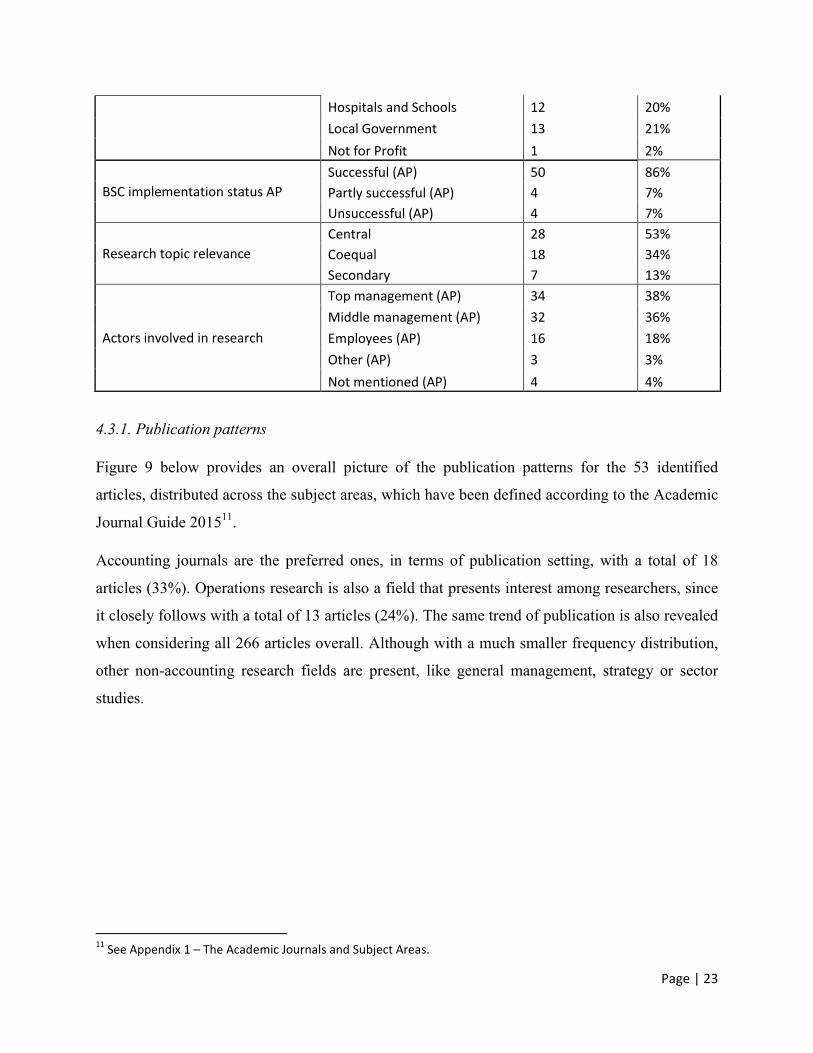

Table 3 – Variables in the Author’s Perspective

Author's perspective (AP) Total Percentage

Research method and type of data

Primary sources

Case study 48 91%

Survey 5 9%

Interview 0 0%

Experiment 0 0%

Secondary data

Data base 0

Annual reports 6

Other 25

Organization type/size

SME 11 18%

Large Company 19 31%

Multinational 5 8%

9 See http://www.bain.com/publications/articles/management-tools-and-trends-2015.aspx for more details.

10 See Appendix 9 – Example for the coding procedure

Page | 23

Hospitals and Schools 12 20%

Local Government 13 21%

Not for Profit 1 2%

BSC implementation status AP

Successful (AP) 50 86%

Partly successful (AP) 4 7%

Unsuccessful (AP) 4 7%

Research topic relevance

Central 28 53%

Coequal 18 34%

Secondary 7 13%

Actors involved in research

Top management (AP) 34 38%

Middle management (AP) 32 36%

Employees (AP) 16 18%

Other (AP) 3 3%

Not mentioned (AP) 4 4%

4.3.1. Publication patterns

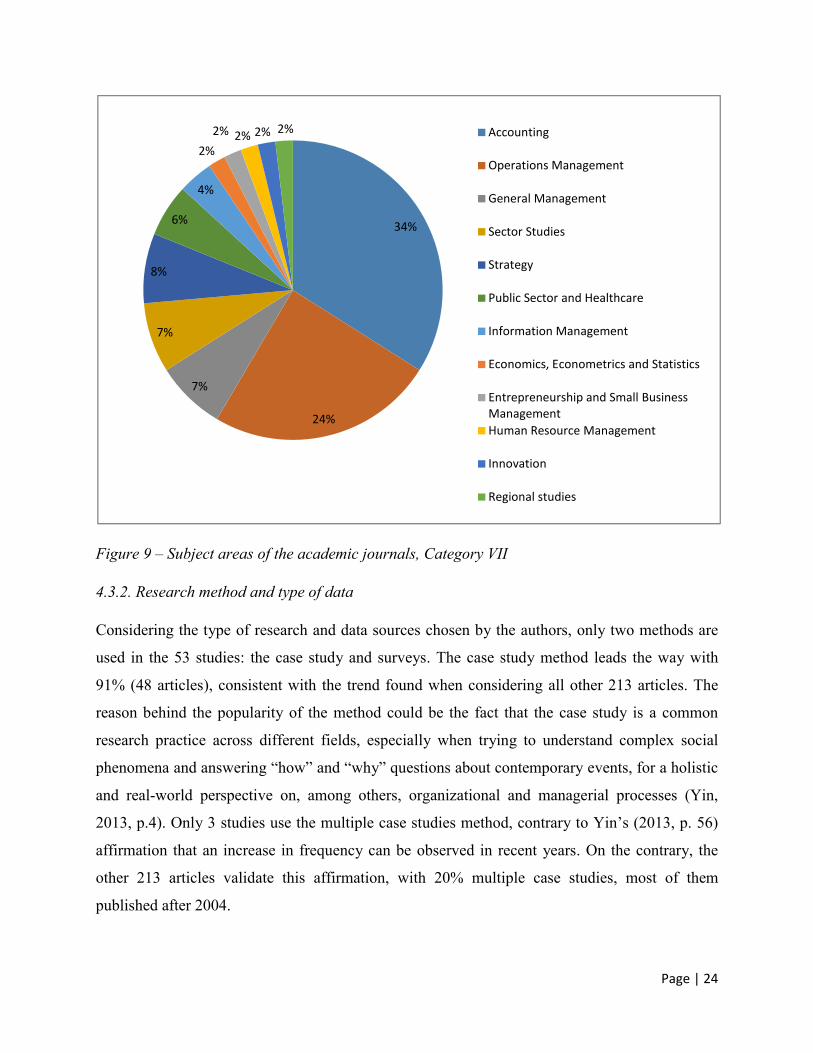

Figure 9 below provides an overall picture of the publication patterns for the 53 identified

articles, distributed across the subject areas, which have been defined according to the Academic

Journal Guide 201511.

Accounting journals are the preferred ones, in terms of publication setting, with a total of 18

articles (33%). Operations research is also a field that presents interest among researchers, since

it closely follows with a total of 13 articles (24%). The same trend of publication is also revealed

when considering all 266 articles overall. Although with a much smaller frequency distribution,

other non-accounting research fields are present, like general management, strategy or sector

studies.

11

See Appendix 1 – The Academic Journals and Subject Areas.

Page | 24

Figure 9 – Subject areas of the academic journals, Category VII

4.3.2. Research method and type of data

Considering the type of research and data sources chosen by the authors, only two methods are

used in the 53 studies: the case study and surveys. The case study method leads the way with

91% (48 articles), consistent with the trend found when considering all other 213 articles. The

reason behind the popularity of the method could be the fact that the case study is a common

research practice across different fields, especially when trying to understand complex social

phenomena and answering “how” and “why” questions about contemporary events, for a holistic

and real-world perspective on, among others, organizational and managerial processes (Yin,

2013, p.4). Only 3 studies use the multiple case studies method, contrary to Yin’s (2013, p. 56)

affirmation that an increase in frequency can be observed in recent years. On the contrary, the

other 213 articles validate this affirmation, with 20% multiple case studies, most of them

published after 2004.

34%

24%

7%

7%

8%

6%

4%

2%

2% 2% 2% 2% Accounting

Operations Management

General Management

Sector Studies

Strategy

Public Sector and Healthcare

Information Management

Economics, Econometrics and Statistics

Entrepreneurship and Small Business Management

Human Resource Management

Innovation

Regional studies

Page | 25

Only 2 articles use interviews as a research method, in addition to surveys (Wu and Chen, 2011

and Said, 2013), and they belong to the other 213 articles. One reason for this can be that

interviews take a long time and are harder to interpret and analyze (Ghauri and Groenhaug, 2010,

p. 127).

5 studies conducted their research based on surveys. The number of respondents varies from 41

to 593, with an average response rate of 35.2% (de Geuser et al., 2009 – 14.5%; Hoque and

James, 2000 – 35.1%; Tapinos et al., 2011 – 11.5%; Braam and Nijssen, 2004 – 41% and Lin et

al., 2014 – 74.2%). The findings are consistent with Van der Stede et al. (2005), who reported a

48% average response rate of surveys in leading academic journals. All surveys were sent by

regular mail, except for Tapinos et al. (2011) that used online surveys. They obtained the lowest

response rate among the five studies, validating the findings of Crawford et al. (2001) that online

surveys are more exposed to a lower response rate.

As for the data sources, the articles use interviews and observations as primary data sources,

while only 26 articles use secondary data, in the form of either annual reports or other types like

archival data, internal documents, satisfaction surveys and the internet. Many of these articles

follow a longitudinal case study research, where secondary sources present the advantage of

“excellent historical data” (Ghauri and Groenhaug, 2010, p. 94).

4.3.3. Sizes and types of organizations

As for the size and type of the organizations, when it comes to exploring the effects of the BSC

on organizational performance, most of the research is conducted in large companies, with 31%.

This is not a surprise, since research over time proved that larger companies tend to use more

sophisticated management control systems (Libby and Waterhouse, 1996; Chenhall, 2003) and

are more likely to opt for a BSC than smaller companies (Hoque and James, 2000; Speckbacher

et al., 2003). Considerable research is also conducted in local government and hospitals and

schools, with 21% and 20% respectively, for the same reasons mentioned above, when

discussing the public sector preference. Some researchers found some degree of difficulty when

involving SMEs in performance measurement projects (Garengo et al., 2005 and Tenhunen et al.,

2001) and this can justify the relatively low number of articles that research the effects of the

BSC on organizational performance in SMEs. Only one not-for-profit organization is present

Page | 26

among the articles, in spite of Kaplan’s (2001) statement that “the opportunity for the scorecard

to improve the management of nonprofits should be even greater” (p.354).

4.3.4. The BSC’s implementation status

The implementation status of the BSC, in the author’s perspective, shows a high percentage of

successful implementations: 86% of the investigated organizations, while 7% had only a partly

successful implementation. Only 4 companies failed in implementing the BSC, according to the

author’s perspective (Umashev et al. 2008, Decoene and Bruggenman, 2006; Carmona and

Grölund, 2003 and one of the two companies researched by Kasperskaya, 2008). In the study of

Kasperskaya (2008) the BSC was eventually suspended due to lack of human resources, time and

problems with the collection and interpretation of information, while in the other three studies

the researched organizations failed in implementing the BSC due to ineffective strategy

translation because of lacking flexibility when cascading strategic goals, while in the case of

Kasperskaya (2008), the reason was. These findings validate the findings of Kaplan and Norton

(2001a) that bad strategy execution is the main reason of strategy failure. Surprisingly, in all

three studies the organizations perceived the BSC implementation as being partly successful.

4.3.5. The research topic

From the research topic perspective, more than half of the articles revolve their research around

the BSC’s effects on performance as a central topic, 34% consider it a coequal topic and only 7

studies (13%) treat it as a secondary research topic. Cooper and Ezzamel (2013) explores the role

of BSC in globalization discourses as a central topic, Hu and Huang (2006) and Huang and Hu

(2007) research the use of the BSC in aligning IT initiatives, Hansen et al. (2010) reports on the

integration of corporate community, Phillips (2007) investigates the BSC for strategic control

and finally, the researches of Liu et al. (2012) and Abo-Hamad and Arisha (2013) is centered

around a new framework that incorporates the BSC.

4.3.6. Key informants

The last variable in the author’s perspective concerns the actors involved in research. Top

managers are the preferred key informants (38%), closely followed by middle management with

36%. The employees are also considered key informants in 16 studies (18%), together with top

and middle management, supporting Kaplan and Norton’s opinion that even though the strategic

Page | 27

vision starts at the executive level, the strategy formulation should eventually be an emerging

process, with both top-down and bottom-up feedback and analysis (Kaplan and Norton, 2006,

p.192).

4.4. The organization’s perspective

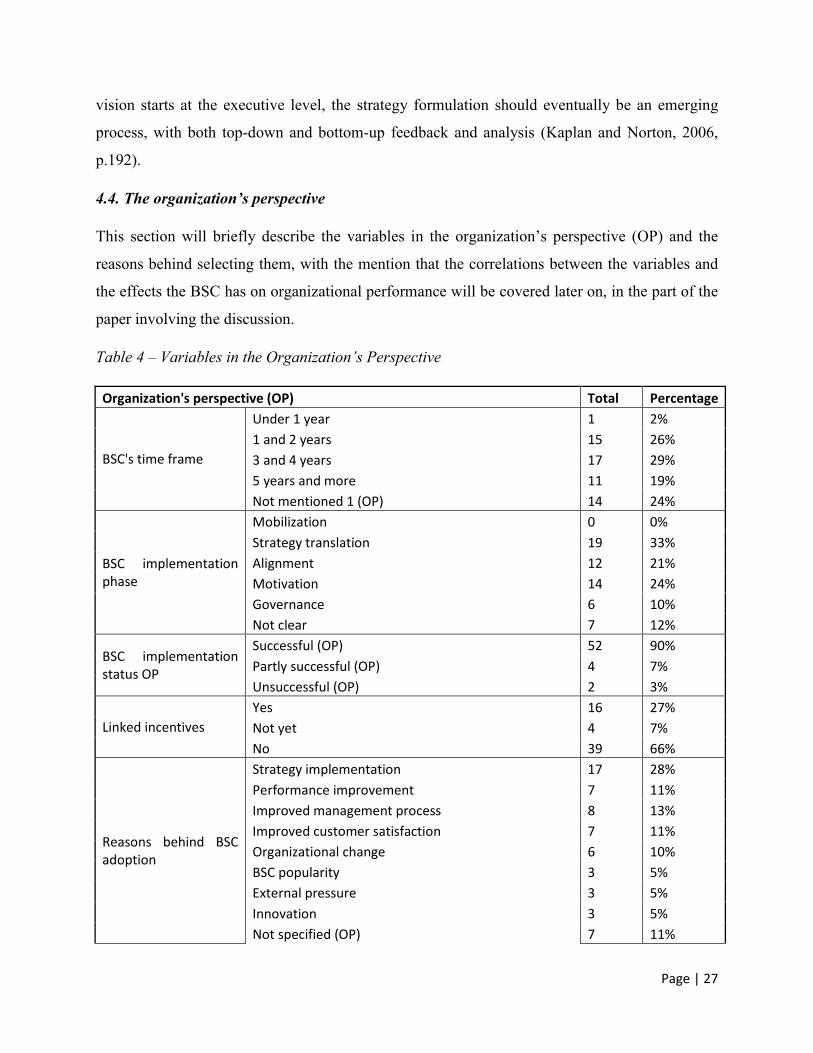

This section will briefly describe the variables in the organization’s perspective (OP) and the

reasons behind selecting them, with the mention that the correlations between the variables and

the effects the BSC has on organizational performance will be covered later on, in the part of the

paper involving the discussion.

Table 4 – Variables in the Organization’s Perspective

Organization's perspective (OP) Total Percentage

BSC's time frame

Under 1 year 1 2%

1 and 2 years 15 26%

3 and 4 years 17 29%

5 years and more 11 19%

Not mentioned 1 (OP) 14 24%

BSC implementation phase

Mobilization 0 0%

Strategy translation 19 33%

Alignment 12 21%

Motivation 14 24%

Governance 6 10%

Not clear 7 12%

BSC implementation status OP

Successful (OP) 52 90%

Partly successful (OP) 4 7%

Unsuccessful (OP) 2 3%

Linked incentives

Yes 16 27%

Not yet 4 7%

No 39 66%

Reasons behind BSC adoption

Strategy implementation 17 28%

Performance improvement 7 11%

Improved management process 8 13%

Improved customer satisfaction 7 11%

Organizational change 6 10%

BSC popularity 3 5%

External pressure 3 5%

Innovation 3 5%

Not specified (OP) 7 11%

Page | 28

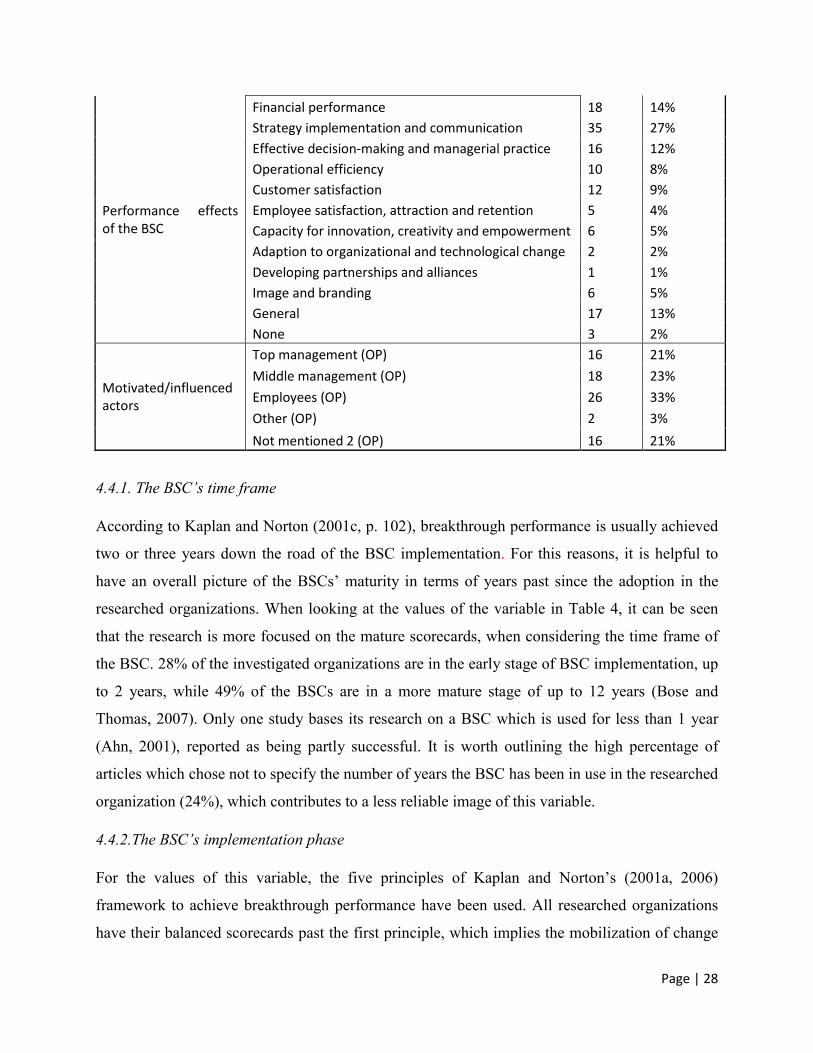

Performance effects of the BSC

Financial performance 18 14%

Strategy implementation and communication 35 27%

Effective decision-making and managerial practice 16 12%

Operational efficiency 10 8%

Customer satisfaction 12 9%

Employee satisfaction, attraction and retention 5 4%

Capacity for innovation, creativity and empowerment 6 5%

Adaption to organizational and technological change 2 2%

Developing partnerships and alliances 1 1%

Image and branding 6 5%

General 17 13%

None 3 2%

Motivated/influenced actors

Top management (OP) 16 21%

Middle management (OP) 18 23%

Employees (OP) 26 33%

Other (OP) 2 3%

Not mentioned 2 (OP) 16 21%

4.4.1. The BSC’s time frame

According to Kaplan and Norton (2001c, p. 102), breakthrough performance is usually achieved

two or three years down the road of the BSC implementation. For this reasons, it is helpful to

have an overall picture of the BSCs’ maturity in terms of years past since the adoption in the

researched organizations. When looking at the values of the variable in Table 4, it can be seen

that the research is more focused on the mature scorecards, when considering the time frame of

the BSC. 28% of the investigated organizations are in the early stage of BSC implementation, up

to 2 years, while 49% of the BSCs are in a more mature stage of up to 12 years (Bose and

Thomas, 2007). Only one study bases its research on a BSC which is used for less than 1 year

(Ahn, 2001), reported as being partly successful. It is worth outlining the high percentage of

articles which chose not to specify the number of years the BSC has been in use in the researched

organization (24%), which contributes to a less reliable image of this variable.

4.4.2.The BSC’s implementation phase

For the values of this variable, the five principles of Kaplan and Norton’s (2001a, 2006)

framework to achieve breakthrough performance have been used. All researched organizations

have their balanced scorecards past the first principle, which implies the mobilization of change

Page | 29

through executive leadership. The majority of the organizations (33%) are in the phase of

implementing the second principle, strategy translation, which implies defining strategy maps,

setting targets and selecting initiatives. Principles 3 and 4 are also consistently represented

among the studies, with 12 organizations in the alignment phase, where business and support

units are aligned with strategy, and 14 organizations in the motivation phase, where target

setting, communication, training and incentives are used to motivate employees in achieving

strategic goals. Only 6 companies reached the last phase, governance, which involves

redesigning the planning, budgeting and control systems in order to integrate strategy (Kaplan

and Norton, 2008). The findings on this matter point out that some organizations have already

started to take steps towards moving forward with the principles, like the study of Aidemark

(2001) where even if the BSC is in the alignment phase, the author informs us about the goal and

target setting (motivation) and about the integration of strategy in the planning and control

system of the organization. Other examples are found in the study of Ahn (2001) and Farneti

(2009) where the organization has its BSC in the strategy translation phase, but has taken also

some initiatives for governance phase, by taking basic steps toward integrating the BSC with the

planning system. The organization researched by Ahn (2001) was also implementing programs

to communicate the strategy to the employees (motivation phase). Kollberg and Elg (2010) is

another example in which a company has taken steps for the next implementation phase, by

integrating the planning system with the BSC.

4.4.3. The BSC’s implementation status

As mentioned before, this variable is present in both the author’s and the organization’s

perspective, because in some studies they differ from one another. The values are the same:

successful, partly successful and unsuccessful. The BSC was seen as successful in its

implementation in 90% of the cases, compared to only 86% in the author’s perspective. Two

organizations deemed the implementation unsuccessful: the one researched by Lorden et al.

(2008) and one company in Kasperskaya’s (2008) study. Lorden et al. (2008) found the BSC to

be partly successful.

4.4.4. Linked incentives

Kaplan and Norton (2007) call for precaution when tying incentives to the BSC, as it carries

considerable risks, especially when the measures are not properly selected. They also consider

Page | 30

the linkage to be powerful and attractive. This variable considers whether the incentives are

linked to the BSC and informs us that the majority of the investigated companies (66%) does not

have this link, although 4 of them (6%) were considering it by the time of research (Sundin et

al., 2010; Huang and Hu, 2007; Rhodes et al., 2008 and Ahn, 2001). Half of the companies with

linked incentives have the BSC in place for more 3 years, following Kaplan and Norton’s

(1996a) advice for patience when making the link, while 7 organizations (30%) decided to tie the

incentives to the BSC, despite the early implementation stage (1 to 2 years). One of these 7

organizations, researched by Decoene and Bruggeman (2006), informs us about the risks

mentioned above and the consequences of tying the incentives too early: de-motivating the

middle managers in achieving strategic goals.

4.4.5. Reasons behind BSC adoption

Strategy implementation is the main reason for implementing the BSC among the researched

organizations, with 28%. This result corresponds with the BSC’s main role as a strategic

management system, to communicate and implement the strategy (Kaplan and Norton, 2001a).

Improvement in the management process is the second most mentioned reason for the

implementation (13%), in line with the findings of Kaplan and Norton (2007, p. 161) that the

BSC is also known as having the advantage of enabling the alignment of the management

process. The next two reasons for implementation follow closely, with 11%: performance

improvement and improved customer satisfaction. Again according to Kaplan and Norton (2007,

p. 161), the BSC is “most effective when it's part of a major change process in an organization”,

which can justify why organizational change (8%) is chosen as another popular reason to

implement the scorecard. Only 3 of the organizations adopted the BSC due to its popularity:

because its endorsement by Harvard Business School (Carmona and Grölund, 2003), after

reading an article (Gumbus and Lussier, 2006) and because it was “in vogue” (Woods and

Grubnic, 2008). External pressures also motivate the BSC adoption, as demonstrated in 3 studies:

Hansen et al., 2010 mentions pressures for community involvement, while legislative

requirements were identified by Rhodes et al.(2008) and Farneti (2009).

4.4.6. The performance effects of the BSC

The values of the variable performance effects of the BSC have been established based on the

BSC conceptual literature and the organizational effectiveness factors identified by Sink (1985).

Page | 31

After the BSC implementation, the majority of the organizations reported performance

improvements in strategy implementation and communication, which includes effective

information sharing, strategic learning and strategic alignment. The management process is

another area that has been improved after the BSC, according to 12% of the case organizations.

Many articles (17) mentioned general improvements and among them, 4 limited their results only

to general statements about performance effects of the BSC, like:

“BSC use […] positively influences overall company performance” (Braam and Nijssen, 2004).

“Use of BSC […] has led to better results” (Cooper and Ezzamel, 2013).

"Organization B achieved 86% of its targeted strategic objectives and 87% of its actions […] a

6% improvement with respect to 2003" (Kasperskaya, 2008).

"BSC usage is positively and significantly correlated with organizational performance" (Hoque

and James, 2000).

One reason for the general statements mentioned above can be that, except for Braam and

Nijssen (2004), all studies had the topic of BSC’s effects on performance as a secondary or

coequal one.

Kaplan and Norton (1996a) suggest that all improvements in the non-financial areas after the

BSC implementation should be eventually linked to economic performance; based on their

findings, it usually takes two, three years for the breakthrough performance to be achieved

(Kaplan and Norton, 2001c). This corresponds to the findings of 18 studies, which reported

improvements in the financial performance measures after the BSC adoption. The majority of the

organizations in these 18 studies had a BSC in place for more than 3 years.

The 3 studies that didn’t report any performance effects of the BSC are the ones researching the

unsuccessful BSCs, from the author’s perspective.

4.4.7. Motivated/ influenced actors

The last variable is considered relevant in identifying the BSC’s propagators and key change

agents, as well as all other influenced stakeholders – either in a positive or a negative way. The

values in Table 4 show a mostly even distribution across employees, top and middle

management when it comes to the impact of BSC implementation, confirming that a BSC

Page | 32

implementation requires more than just leadership commitment. The entire organization should

be focused and everyone should have an active contribution in strategy implementation (Kaplan

and Norton, 1996c, 2001b).

The findings regarding this variable provide evidence of the fact that BSC propagators and

change agents can be found at all levels in the organization. Modell (2009) found that employees

saw the BSC as a “fresh start” and middle management as a “born again experience”, while the

BSC in the case organization of Huang and Hu (2007) made the employees proud of contributing

to strategic goals. High commitment among both employees and management was also reported

in the studies of Kollberg and Elg (2010), Hu and Huang (2006), Rhodes et al. (2008) and

O’Connor and Feng (2005).

Even though in the majority of the organizations with a successful BSC implementation the

actors were positively influenced, some of the studies provide also evidence of resistance among

management and employees. In a Swedish hospital, Aidemark (2001) found that even if the BSC

was “extremely attractive” for the head of the clinic, not all doctors were as enthusiastic. This

changed over time, as proved by a later study (Aidemark, 2006). On the same note, Kasperskaya

(2008) reported some resistance among department managers and a decline in the top

management’s enthusiasm due to “technical difficulties” with the BSC, while inconsistency in

staff support across the organization was found by Woods and Grubnic (2008). The BSC

implementation in the case organization researched by Papalexandris et al. (2004) improved

employee morale while in the same time led to conflicts between divisional managers, while in

the case of Fernandes et al. (2006), although 90% of employees were convinced of the BSC’s

benefits, “the rest were skeptical or negative”.

In one the two studies with an unsuccessful BSC from the organization’s perspective (Lorden et

al., 2008), the implementation of the scorecard was only actively supported by 2 of the 5 vice

presidents, while in the other one (Kasperskaya, 2008) the enthusiasm of the management team

decreased when encountering technical problems, making them not act upon the collected

information through the BSC. These aspects coincide with Kaplan and Norton’s (2001a, p. 361)

findings that lack of senior management commitment is a common cause in BSC failure. As for

the unsuccessful balanced scorecards from the author’s perspective, one case study (Decoene and

Bruggeman, 2006) reports negative impact of the BSC on the intrinsic motivation of middle

Page | 33

managers, while the BSC in the case of Carmona and Grölund (2003), besides of being non

relevant and time consuming at the local police level, a positive attitude is also found among the

central officers when considering the usefulness of the tool.

5. Discussion

Based on the knowledge gained from analyzing all 53 identified studies researching the impacts

of the BSC on organizational performance, the first part of this section will seek to offer some

insights into positively associating the BSC implementation with improved performance beyond

just the economic dimension. The discussion will also focus on the way performance is assessed

and reported and how the actors are motivated by the BSC, identifying in the same time some of

the best-practice representative studies. The reasons for excluding some of the articles from the

representative group will also be tackled, ending with some recommendations future research

based on the main findings of this paper.

5.1. Findings regarding the impact of the BSC on organizational performance

5.1.1. Non-representative studies

The effects the BSC has on organizational performance in all 53 identified studies have different

degrees of explicitness and relevancy and are different in regards to the way they are assessed

and reported. This last part of the paper will mainly focus on discussing the representative

studies and, in order to identify them, I started with excluding the ones that do not contribute to

the best-practice body of research. The exclusion is based on the knowledge gained from each

article, focusing especially on the methodology of the study, its limitations and details of the

BSC implementation, from both author’s and organization’s perspective.

All studies which reported an unsuccessful implementation of the BSC were excluded, since they

didn’t provide any evidence of performance improvement.

Articles which based their research on surveys (Lin et al., 2014; Braam and Nijssen, 2004;

Tapinos et al., 2011; Hoque and James, 2000 and De Geuser et al., 2009) were also excluded,

since they didn’t capture the implementation, use and development stages of the BSC. All studies

Page | 34

suggested a positive correlation between the use of the BSC and improved organizational

performance.

The overly long development process of the BSC is identified as a common reason for the BSC

failure (Kaplan and Norton, 2001a, p. 361), therefore another exclusion criterion considers the

correlations between the BSC’s maturity and its implementation phase. The organization in

Cooper and Ezzamel’s (2013) study has its BSC in the alignment phase, despite using it for 10

years. The authors rendered the BSC partly successful. The same situation is present also in the

study of Aidemark (2009), where “The BSC remained as a tool on the ward level for a decade"

(p. 264). Even if some general performance improvements in the case companies are reported,

the one successful scorecard investigated in Kasperskaya’s (2008) article is still in the translation

phase after 4 years of implementation. The same author reports that the organization is not

mature enough for strategy maps and causal linkages. Grando and Belvedere (2008) claim the

BSC to be useful in supporting decision-making and information sharing, while their

investigated company, despite using the BSC for 4 years, didn’t complete the alignment phase in

the department where it was introduced. In the same time, the organization decided not to extend

the scorecard to the other departments yet.

Studies like Joseph (2009) and Davis (1996), presenting success stories without giving any

details on the theory used, methodology and data collection, have been also included in the “non

representative” category. Huckestein et al. (1999), Ashton (1998), Irwin (2002) and Denton and

White (2000) are other examples of such studies. Lack of consistent evidence and clarity in data

collection is also observed in the study of Bose and Thomas (2007) and Fottler et al. (2006),

where evidence of performance effects due to BSC implementation is hard to trace, being only

presented as quotes from annual reports in the first study, while the second one only speculates

the outcomes: “"Results to date indicate that the HR Balanced Scorecard […] will result in

improved performance in a number of HR indices (i.e., staff retention) and customer service (i.e.,

patient satisfaction) indices (p. 72)". The study of Mooraj and Oyon (1999) is the last one

excluded here, since it only gives general observations about the BSC in Tetra Pak and gives no

details about data collection.

A final criterion concerns again the maturity of the BSC, only this time only organizations with a

BSC in a very early stage of implementation are considered, since more time can be required to

Page | 35

validate the BSC’s effectiveness. Three of the cases are found in the public sector; the

implementation of the BSC in the study of Kampschroer and Heerwagen (2005) led to improved

customer satisfaction and effective communication and information sharing but it was positioned

in its early stages of development due to its complexity, despite being adopted for 2 years.

Bianchi and Montemaggiore (2008) and Cugini et al. (2011) are two other studies in the public

sector, which investigated a BSC implemented for 1 year in Italy, in a local government agency

and a university department. The BSC implementation impacted the performance by improving

communication and enhancing management learning in the first case, and by clarifying the

strategy and improving the resource allocation in the second one. Finally, the article of Chesley

and Wenger (1999) was also excluded due to insufficient time to validate the effectiveness of the

BSC. Here, even though the BSC implementation improved employee and customer satisfaction

and improved the strategic management process, it was still reported as “partly successful” by

the authors, because "at the time this study ended, the executives were struggling with

fundamental questions [on strategy development]" (p.57).

As for the private sector, the article of Ahn (2001) has been excluded due to focusing on a pilot

project of BSC introduction (only 4 months of use). O’Connor and Feng (2005) didn’t fully

validate the effectiveness of the implemented BSC, claiming that “more time is required to

determine the effectiveness of the scorecard" (p. 29), in spite of the 3 years of BSC use in the

case organization and performance improvements in the form of a more effective management of

intangible assets, better value for customers and higher profits. The study of Hansen et al.(2010)

is also excluded, based on the statement of the authors: “Considering that the case study covers

the time briefly after implementation, a judgment on its ultimate success requires further

longitudinal research" (p.397). It is worth mentioning that the BSC was effective in developing

strategic alliance and was also "considered a significant step towards responsible leadership

systems" (p.397). Malina and Selto (2001) are exploring a BSC implemented for 1.5 years,

which facilitated strategy implementation and communication, a more effective management

process and a “modest but observable” financial performance. It is still considered too early to

validate the true effects on performance, since the authors reported some of the measures to be

inaccurate and imposed down to the distributors without using strategy maps. The same authors

inform us about the company changing its BSC in regards to selecting and identifying the

measures, right after the data collection.

Page | 36

Besides the criteria mentioned above, some of the articles have been excluded based on different

information and limitations mentioned by the authors. For example, Liu et al. (2012) and Abo-

Hamad and Arisha (2013) do not explore the effects of the BSC on organizational performance

as a central or coequal topic, but are focusing instead on the benefits of integrating the BSC with

soft system methodology and simulation respectively. Huang and Hu (2007) also treat the

performance impacts of the BSC as a secondary topic, mainly focusing their research on the

integration of IT with the BSC. Wisniewski and Dickson (2001), Farneti (2009) and Dreveton

(2013) are focusing only on the early development process of BSC and its impact on the

organization, while Davis and Albright (2004) captured only the financial dimension of

performance. Papalexandris et al., (2004) focused more on the 3 months development process of

the BSC, reporting the performance improvements only by comparing targets with actual results

after 1 year of BSC use. Lastly, Woods and Grubning (2008) explored a local government

agency in UK which found the BSC useful in making them “appear innovative”. Even if the

authors found the BSC implementation successful, reporting continuous performance

improvement in general and in strategy implementation, they also reported cultural issues in

cascading the BSC and mixed results, sustaining that translating the strategy "may not be enough

in itself to guarantee performance improvement", making the article suitable for exclusion.

5.1.2. Representative studies

A total number of 12 articles have been identified as best-practice representative studies. This

section will include the outlining of the main characteristics of each study, followed by a

comparison which will highlight their similarities and differences.

The first representative article belongs to Modell (2009) and explores the case of Swedish

National Board of Student Aid and their experience with the BSC implementation, which

succeeded after a second trial and a change in leadership. Data is collected between 2004 and

2007, through semi structured interviews, group discussions and secondary data like archival

data and internal documents. The first attempt to adopt the BSC failed due to “little effort […] on

analyzing or mapping causal relationships between various focus areas” (p. 76). The new

strategic management system was seen both as a balanced scorecard and as “something in

between TQM and the balanced scorecard” (p.79) by the new general manager, who was

perceived as an example of great leadership. The BSC adoption was seen as a “fresh start” and a

Page | 37

“born again experience” by employees and middle management, improving performance in

customer satisfaction and strategy implementation and communication.

Jazayeri and Scapens (2008) is the second study, investigating the multinational British company

BAE Systems, with an 8 month data collection process based on open-ended interviews with

senior and divisional managers in the Customer Solutions and Support division and secondary

data like internal documents, archival data and a book published about the company. The

organization has a mature BSC in place (8 years since the implementation and in the last stage of

implementation, governance, with linked incentives) and was implemented due to a need of a

change in the company’s culture. The performance effects associated with the use of the BSC are

in the form of improvements in financial performance like a higher stock price, better sales and

profits, as well as a better strategy formulation and improved management ability. The author

argues the difficulty of isolating the BSC’s effect on performance, an opinion shared also at the

management level of the organization: “I find it difficult to actually say there’s particular benefit

from only the business value scorecard” (p. 67), especially due to the time lag in the cause and

effect relationships of the BSC, as one manager puts it: “You would probably see the impact

over a longer time period. I think poor performance you tend to notice quicker than you notice

good performance” (p. 65). According to the authors, the BSC used in this case differs from the

original approach of Kaplan and Norton by using coherence instead of cause and effect

relationships.

The study of Sundin et al. (2010) has also been selected as a representative one. It explores the

impacts of the BSC on performance in a large Australian electricity company, where data was

collected in a two and a half years period, in the form of direct observations at all levels and

involving more than 100 employees, semi-structured interviews at top management level and

archival data. The BSC had been in place for 3 years, in the implementation phase of principle 5

(govern to make strategy a continual process), even though the incentives were not yet linked:

“The management of Energyco has considered formally linking remuneration to BSC

performance indicators – although there are significant concerns about the effects of this” (p.

230). The performance effects of the BSC implementation were reported in the form of effective

information sharing and strategy implementation and a more balanced and systematic decision-

making process. The scorecard mobilized everyone in the company, making people “passionate

Page | 38

about their own patch and […] go to extraordinary lengths to make sure the customer is happy"

(p. 230).

Rhodes et al. (2008) researched the central bank of Indonesia, which had a BSC in place for 3

years and in the alignment phase of implementation. The reason for adopting the BSC was

external pressure in the form of legislative requirements. The incentives are not linked, as the

company "has yet to design a reward system around the BSC" (p. 1182). Performance

improvements are reported in the managerial process, by increasing the support in leadership and

transparency, as well as in strategy implementation, by realigning the thinking and initiatives

with strategic directions. The image of the company was improved in the eyes of external

stakeholders after the BSC implementation and enhanced financial performance is achieved

through a better cost management. All these evidence of performance impacts is gathered

through staff and external stakeholder surveys and public statements. The top management is

significantly committed to the BSC.

The study of Greatbanks and Tapp (2007) explores the BSC implementation in a New Zealand

city council call center department. The research adopted a longitudinal case study method,

based on semi-structured interviews with staff and managers and internal documents. The

company was in the phase of implementing the fourth principle, motivate to make strategy

everyone’s job, with a BSC in place for 4 years and linked incentives. The BSC led to

performance improvement immediately after its implementation, in the form of increased call

center performance and decreased waiting time and abandoned calls. The managers claimed the