does it pay to care about esg investing? - evestment · pdf filedoes it pay to care about esg...

TRANSCRIPT

Does It Pay To Care About ESG Investing?The Consultant & Investor Perspective

Environmental, social and governance (ESG) investing approaches have increasingly become a hot topic with even the largest institutional investors taking notice. Following much involvement in the ESG space, CalPERS recently decided to more officially throw their hat into the ring with the announcement of a year-long pilot program.

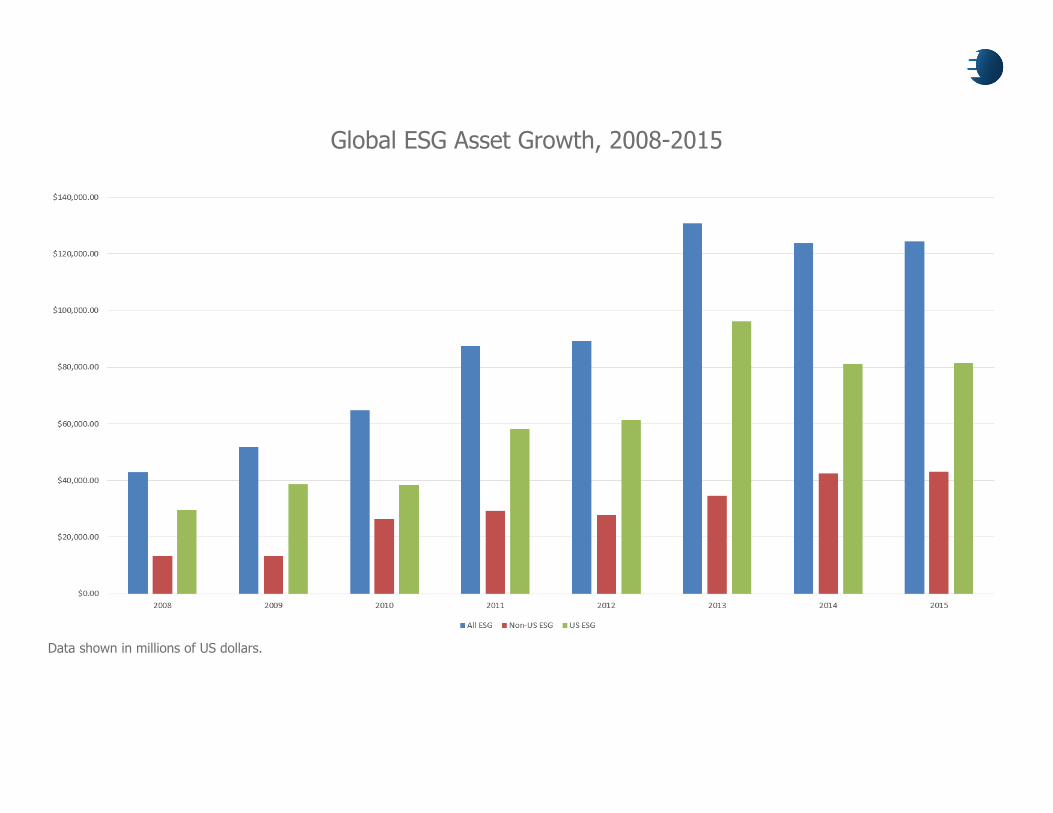

According to eVestment data, overall AUM for ESG strategies has grown steadily over the last several years with assets just over $42.8 billion in 2008 to over $124.5 billion as of 1Q2015. But does it pay to care about ESG? Are non-financial benefits quantifiable? Do investor ESG convictions span across asset classes? What does the future hold for ESG adoption?

To really dig deeper into what investors and consultants are thinking about performance, costs and the future of ESG adoption, we interviewed three well-respected and experienced ESG allocators: Jay Satterfield, CIO, Freed-Hardeman University; Scott Perry, Partner and Impact Investing Team Member, NEPC; and Nichole Roman-Bhatty, Managing Partner and Chair of Impact Investing, Marquette Associates.

Jay Satterfield

Chief Investment Officer Freed-Hardeman

University

Scott Perry

Partner & Impact Investing Team Member

NEPC

Nichole Roman-Bhatty

Managing Partner & Chair of Impact Investing

Marquette Associates

What does the future hold for ESG?

Data shown in millions of US dollars.

Global ESG Asset Growth, 2008-2015

Not surprisingly, many of the respondents in our interviews represent constituents that hold certain core values that drive their ESG policy adoption. These include both religious organizations and those that are generally interested in sustainable companies or “being good shareholders,” as Perry put it.

Perry: “As far as key stakeholders, it is really broad-based. We’ve seen an increasing amount of interest across our client base, specifically endowments, foundations, private wealth, public funds and Taft-Hartley.”

Satterfield: “As a Christian, conservative-based university, we like to stay true to our heritage. Our daily operations strategy and our investment policy are becoming more and more married – they are each driving each other and creating the need for consistency. The investment policy has actually been leading the way as we have taken into account certain basic ESG considerations. As we move forward, I think the issues of the day that we experience in our general operations, such as certain federal legislation or cultural trends, will force us to become more consistent on both fronts.”

The areas of exclusion our respondents felt came up most frequently were tobacco, alcohol, gambling and adult media.

Perry: “For environmental factors, carbon footprint and energy efficiency are definitely a primary area of focus. In the governance area, it’s board independence, separation of senior roles within the organization, as well as executive compensation – meaning that investors want to ensure there are appropriate checks and balances in place. Lastly, one of the bigger issues in the social area – that has also been highlighted recently in minimum wage discussions – is the overall consideration of fair wages.”

Roman-Bhatty: “Many of my clients are also talking about fossil fuel divestment and how that could be achieved. Right now it’s more in the discussion phase versus implementation phase, but it is on the radar.”

Drivers of ESG Investment Policies

Top Five ESG Screening Criteria

1. Animal Rights/Welfare2. Christian Values3. Clean Energy4. Tobacco5. Islamic Values

eVestment data, 2014

Both Perry and Roman-Bhatty either hold or have clients who hold beliefs that ESG practices have a positive impact on the business and the investment portfolio.

Roman-Bhatty: “Overall my religious-affiliated clients believe companies that have better environmental or socially-conscious practices have better run businesses over the long-term. And, it is becoming more standard to incorporate ‘ESG-risks’ assessment into the investment process than before.”

Perry: “There is a general belief at NEPC that ESG integration can be additive to investment results. This is based on the idea that if investment managers are able to access additional information regarding how a company operates, it might provide additional insight that can help their investment process and drive results if used effectively.”

Satterfield: “We don’t believe that ESG managers are always going to beat everyone else out there. We invest in ESG products as a way to remain true to who we are. We still look at performance first. Then we have a conversation with strong managers to see what capabilities they may have as a firm.”

Performance Impact

In general, Marquette doesn’t believe that you will underperform if you have a socially-responsible investing strategy.

“”

Nichole Roman-Bhatty Managing Partner and Chair of Impact Investing, Marquette Associates

Cost ImplicationsCosts associated with taking an ESG stance appear to be in line with industry standards across various asset classes or are not a top factor when selecting a manager.

Roman-Betty: “If clients are looking for an investment manager that just has an ESG-integration team, then typically there is no added cost. But if clients are looking specifically for a fund that does social advocacy, then I would say that is more expensive on average. In that case, those clients are willing to pay a little more.”

Satterfield: “Cost isn’t as high of a priority on our list. We are willing to pay more for a high-performing manager. We certainly want to understand the cost structure and how a manager gets paid, but cost is not a big differentiating factor for us given parity in other areas. That said, we would certainly not accept higher costs from a manager who is not performing.”

Perry: “However, a negative screening approach may have a higher cost and higher tracking error associated to it. There will always be a group of investors who will start with exclusion based on their mission or their organizational beliefs, but there has been a shift to an ESG orientation across the industry.”

People feel good about the types of companies that they’re investing in. These benefits are some of the strongest motivational factors pushing investors to consider ESG policies.

Benefits to taking an ESG approach go beyond performance, of course. Remaining true to values and beliefs is at the core for those interviewed, as well as avoiding other risks such as poor publicity. While endowments such as Freed-Hardeman are able to provide some degree of long-term assistance to their universities, risking the charitable donations of their alumni or other donors is a much bigger risk than any potential performance concerns.

Satterfield: “As a religious-affiliated school, the conversation with donors is often centered around how we will maintain fiduciary responsibility with their assets in a way that upholds integrity. For the most part, the donors that we work with have the expectation that we are going to follow those things that are true to our heritage, such as being environmentally friendly or avoiding investments in alcohol, tobacco and pornography. Being able to discuss our approach openly certainly separates us from other non-profits and endowments.”

Perry: “One benefit our clients think about is a potential reduction in headline risk. For example, if a client is focused on environmental factors, they may avoid investing in a certain energy company if it’s exhibited a pattern of non-compliance. Avoiding headline risk is definitely a motivator and a potential benefit for investors that are pursuing an ESG policy.”

Roman-Bhatty: “Measuring the impact of non-financial gains is not cut and dried. Everyone quantifies gains from ESG a little bit differently. I once met with a manager who uses a metric to measure shareholder engagement which gauges the extent to which companies have changed practices because of shareholder involvement. There is some fear that, if ESG metrics become more quantitative, people will be more focused on making ‘numbers’ in the short-term versus the long-term. We will see more groups trying to attempt to quantify these benefits, but it can be very difficult to do.”

Non-Financial Benefits

“”

Scott Perry Partner & Impact Investing Team Member, NEPC

ESG Convictions Across Asset ClassesESG convictions seem to apply primarily to equity stakes in certain firms, versus other asset classes. However, the desire to more closely align ESG goals with additional types of strategies is certainly present.

Perry: “In a commingled fund structure like a hedge fund, where you’re privy to the guidelines outlined by the manager, there are more limitations around what you can achieve and the associated ESG impact related to those types of investments. Most hedge funds have not pursued ESG approaches. We’re of the hope that more managers, and hedge fund managers specifically, will get there through conversations with NEPC and our clients.”

Satterfield: “We initially tried to monitor alternatives more closely, but it was a challenge. We certainly provide our policy to those managers, but it isn’t something that we have been able to track well. If there are those out there who can do this successfully, I’d like to learn more.”

Roman-Bhatty: “I always tell people to do a best-efforts approach, because there may be some strategies that are good for the portfolio that don’t adopt an ESG approach – including many alternatives. I know there are a few emerging markets ESG funds, but not very many. Most seem to approach ESG trying to do as much as they can.”

When asked specifically about private equity, the respondents said it was definitely of interest but also hard to implement or track in some cases.

Perry: “A growing percentage of our clients are focused on ESG and consider these factors in their selection of investment managers within private equity.”

Satterfield: “We actively invest in private equity, although ESG considerations don’t typically come into play. We would like to make allowances for those convictions, but again it is difficult to implement. Perhaps when we become a bigger player we can invest more directly in this space with ESG in mind.”

Roman-Bhatty: “My clients would consider investing in private equity if some of the portfolio companies within the fund had some level of ESG practices. Although, most of the time we are not able to invest in private equity because of the liquidity issues with operating plans.”

The percentage of hedge fund managers that do incorporate ESG criteria has increased significantly from 25% to 40%, with 73% of private equity managers saying they were willing to adopt these criteria.

2015 Unigestion survey

It may not feasible to police every business unit within a company, so investors tend to remain flexible with their ESG policies.

Satterfield: “We look at obvious affiliations and are not looking at every intricacy of the company. Say we were to invest in a manager that held a theme park franchise. We wouldn’t go so far as to screen them out if that brand also has a cruise line that allows gambling in foreign waters. This would be different to us than buying equity in a casino. The way that we implement our policy is not militant.”

Roman-Bhatty: “If a manager can’t be found that meets ESG standards, there are other ways. I like to get creative with it. If we can’t find a good investment manager in that asset class, maybe we’ll look at some practices or policies that distinguish the firm itself. We are also starting to see more ESG integration. By that I mean if they don’t have a strict ESG strategy, maybe they have an ESG team, where at least it’s being discussed during the investment decision. I always tell clients to try to be as flexible as they can with the policy to make sure that we can still create a portfolio that’s diversified. It’s important to look at it through a lot of different angles.”

Flexibility is Key

Our process starts out looking for a good quality manager with high performance and good modern portfolio statistics, followed by ESG screening.

“”Jay Satterfield

CIO, Freed-Hardeman University

Broader AdoptionThose leading the way are perceived to be the younger generations, as well as those bigger institutions that are already starting to set the course. For broader adoption to occur, ESG strategies must prove their value in terms of performance.

Roman-Bhatty: “I think with anything, really, you need some very visible groups to start adopting ESG. You just saw CalPERS announce some initiatives for ESG, for example. After this kind of announcement, other public funds may start to investigate and join in. It’s just a matter of having some very large or public groups do it first.”

Satterfield: “I believe that the younger generations are driving some of this adoption. They have been raised with a strong belief to take care of the world around them as well as ‘do no harm’ to either to body or earth. They may take a different attitude and accept lower-level performance in order to be comfortable that they are following an ESG strategy. However, investors in my generation are still highly focused on profitability. And in order for broader adoption of ESG policy and strategies to occur, those managers or companies that focus on social or environmentally-conscious efforts need to demonstrate results.”

Perry: “Educating and convincing investment committees, board members, etc., that an ESG approach is at a minimum neutral, if not additive, to the overall investment process is still the biggest hurdle for impact investing broadly. The performance data and research that’s out there now is supportive of ESG as an additive factor that can influence top-line results. That’s certainly a big motivator and driver of the interest and the growth in ESG.”

Asking the right questions is critical to moving the ball forward on ESG. eVestment has made great strides in terms of the types and number of questions asked around ESG.

“”Scott Perry

Partner & Impact Investing Team, Member, NEPC

Investors and consultants have learned many lessons along the way, advising to engage with current managers to see if they already include an ESG approach or team, as well as warning not to “buy into the hype” and conduct due diligence just as you would on any other manager.

Perry: “The first step is to find out what existing managers are doing, as it relates to ESG, and engage them. Investors might be surprised to learn what their current managers are doing. Some might not have marketed themselves as having an ESG orientation, but they may be looking at many of these factors already.”

Roman-Bhatty: “If you’re just asking your current investment manager to implement an ESG policy, that can also present challenges. For example, we had a separate account for low-volatility equity and we asked a manager to look at the screens, and they just thought that healthcare screened out many other names. You’ve got to be careful about just handing an ESG policy to an investment manager who doesn’t have a lot of experience doing any screening. Sometimes I think if a group really wants to be active that they should just go with firms who have more experience.”

Satterfield: “Be cautious; don’t buy in to the hype. Don’t chase a dream. Make sure that everything makes sense – not just ESG, but performance, volatility, consistent staff, etc. Conduct all the due diligence you would do on any other manager and don’t give out passes just for great ESG statements. You can get sucked in if you don’t apply other screens – using eVestment is one of the ways we make sure we don’t make this mistake.”

Advice for Other Investors

The trend toward institutional investors taking ownership of their ESG decisions appears to be accelerating. As we learned in our interviews, an ESG approach can vary in flexibility and perspective — focusing more on including positive characteristics such as corporate governance, or excluding perceived negative components such as gambling or tobacco stocks. While non-financial benefits and beliefs certainly fuel ESG policies, performance still remains a top priority and is not something investors are willing to sacrifice. Costs on the other hand are negotiable if both considerations can be met.

Additionally it is clear that investment committees and overseers of institutional assets are very eager to engage in the ESG conversation, and not just in regards to traditional asset classes. Applying an ESG orientation is also desirable in the alternatives space, and those interviewed are hopeful for new offerings from both hedge fund managers and private equity firms. Overall, the outlook for ESG strategies is positive, especially if more and more bigger players continue to adopt the approach and positive performance results can be achieved.

In Summary

Learn How We Can Help You

About eVestmenteVestment provides a flexible suite of easy-to-use, cloud-based solutions to help the institutional investing community identify and capitalize on global investment trends, better select and monitor investment managers and more successfully enable asset managers to market their funds worldwide. eVestment’s mission is to help make smart money smarter.

Solutions for Investors Solutions for Asset Managers

Investors use eVestment for ESG manager selection,

due diligence and monitoring.

ESG managers use eVestment to increase visibility among investors and consultants.