document of the world bankdocuments.worldbank.org/curated/en/990501468243556306/pdf/490770... · ft...

TRANSCRIPT

Document of The World Bank

FOR OFFICIAL USE ONLY

Report No. 49077-CO

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

PROGRAM DOCUMENT

FOR A PROPOSED LOAN

IN THE AMOUNT OF US$300 MILLION

TO THE

REPUBLIC OF COLOMBIA

FOR A

FINANCIAL SECTOR DEVELOPMENT POLICY LOAN

July 8, 2009

Poverty Reduction and Economic Management Department Colombia and Mexico Country Management Unit Latin America and Caribbean Region

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

COLOMBIA - GOVERNMENT FISCAL YEAR January 1 – December 31

CURRENCY EQUIVALENT (Exchange Rate Effective as of July 1 2009)

Currency Unit Peso 2151 Pesos = US$1

Weights and Measures: Metric System SELECTED ABBREVIATIONS AND ACRONYMS

AFP Pension Fund Administrator BdR Banco de la República CAR Capital Adequacy Ratio CCCH Central Counterparty Clearing House CFC Commercial Financial Company CPS Country Partnership Strategy CPSS Committee on Payment Settlement Systems DPL Development Policy Loan ETD Exchange Traded Derivative FCL Flexible Credit Line FDI Foreign Direct Investment FOGAFIN Fondo de Garantía de Instituciones Financieras FT Financing Terrorism FSAP Financial Sector Assessment Program GDP Gross Domestic Product GoC Government of Colombia IADB Inter-American Development Bank IFC International Financial Corporation

IMF International Monetary Fund IOSCO International Organization of Securities Commissions MHCP Ministry of Finance and Public Credit ML Money Laundering NBFI Non-bank Financial Institution NDP National Development Program NLTA Non-Lending Technical Assistance NPL Non-Performing Loan OTC Over-the-Counter PFM Public Financial Management PFSAL Programmatic Financial Sector Adjustment

Loan SFC Financial Superintendency of Colombia SME Small & Medium Enterprise SS Superintendencia de Sociedades SSS Securities Settlement Systems UIS Unregulated Investment Schemes WEO World Economic Outlook

Vice President Pamela Cox Country Director Axel van Trotsenburg Sector Director Marcelo Giugale Sector Manager Lily Chu Task Manager Eva Gutiérrez

FOR OFFICIAL USE ONLY

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not be otherwise disclosed without World Bank authorization.

COLOMBIA FINANCIAL SECTOR DEVELOPMENT POLICY LOAN

TABLE OF CONTENTS LOAN AND PROGRAM SUMMARY...........................................................................................................1

I. INTRODUCTION ..............................................................................................................................3

II. COUNTRY CONTEXT.....................................................................................................................4

RECENT ECONOMIC DEVELOPMENTS.........................................................................4

MACROECONOMIC OUTLOOK AND CHALLENGES ..................................................8

III. THE GOVERNMENT PROGRAM.................................................................................................21

IV. FINANCIAL SECTOR REFORMS IN THE LAST DECADE AND THE AGENDA FOR FUTURE REFORMS.........................................................................................................................22

V. BANK SUPPORT TO THE GOVERNMENT’S STRATEGY .....................................................27

LINK TO CPS........................................................................................................................27

COLLABORATION WITH THE IMF AND OTHER DONORS .......................................28

RELATIONSHIP TO OTHER WORLD BANK GROUP OPERATIONS .........................30

LESSONS LEARNED...........................................................................................................31

ANALYTICAL UNDERPINNINGS ....................................................................................31

VI. THE PROPOSED FINANCIAL SECTOR DPL ............................................................................33

OPERATION DESCRIPTION..............................................................................................33

POLICY REFORMS SUPPORTED BY THIS OPERATION .............................................34

VII. OPERATION IMPLEMENTATION ..............................................................................................39

POVERTY AND SOCIAL IMPACTS..................................................................................39

ENVIRONMENTAL ASPECTS...........................................................................................40

CONSULTATIVE PROCESS...............................................................................................41

IMPLEMENTATION, MONITORING, AND EVALUATION ..........................................41

FIDUCIARY ASPECTS, DISBURSEMENT, AND AUDITING .......................................42

RISKS AND RISK MITIGATION .......................................................................................43

ANNEXES ANNEX 1: LETTER OF DEVELOPMENT POLICY .................................................................................44

ANNEX 2. POLICY MATRIX........................................................................................................................51

ANNEX 3: FUND RELATIONS NOTE.........................................................................................................53

ANNEX 4: COLOMBIA – ECONOMIC PROSPECTS...............................................................................55

ANNEX 5: COLOMBIA – DEBT SUSTAINABILITY ANALYSIS...........................................................69

ANNEX 6: COLOMBIA- FINANCIAL SECTOR REFORMOS IN THE LAST DECADE...................73

ANNEX 7: COLOMBIA- UPDATE ON THE IMPLEMENTATION OF THE

COUNTRY PARTNERSHIP STRATEGY ...................................................................................................78

ANNEX 8: COLOMBIA – OPERATIONS PORTFOLIO (IBRD/IDA) AND GRANTS.........................83

ANNEX 9: COLOMBIA - STATEMENT OF IFC’S HELD AND DISBURSED PORTFOLIO ............84

ANNEX 10: COUNTRY AT A GLANCE......................................................................................................85

The World Bank Group greatly appreciates the close collaboration of the Government of Colombia in the preparation of this Development Policy Loan. This operation has been prepared by a team composed of: Eva Gutierrez (LCSPF- Task Manager); Rogelio Marchetti, Jane Hwang (LCSPF); Christian Ives Gonzalez, Maria Ivanova Reyes (LCSPE); Teresa Genta-Fons (LEGLA); Mark Hagerstrom (LCC1C); Juan Carlos Belausteguigotia (LCSEN); Maria Dolores Lopez-Larroy (BDM); Jose Janeiro (LOAFC) and Manuel Vargas (LCSFM). The team benefited from comments from other Bank staff including Lily Chu, Esperanza Lasagabaster (LCSPF); Eduardo Somensatto (LCCCO); Jozef Draaisma (LCC1C); David Rosenblatt (LCSPR); Sally Burningham, Reidar Kwan (LCSDE) and peer reviewers Juan Carlos Mendoza (LCRVP); Sophie Sirtaine (ECSPF); and Costas Stephanou (FPDFS). Editorial assistance was provided by Renata Leandro.

1

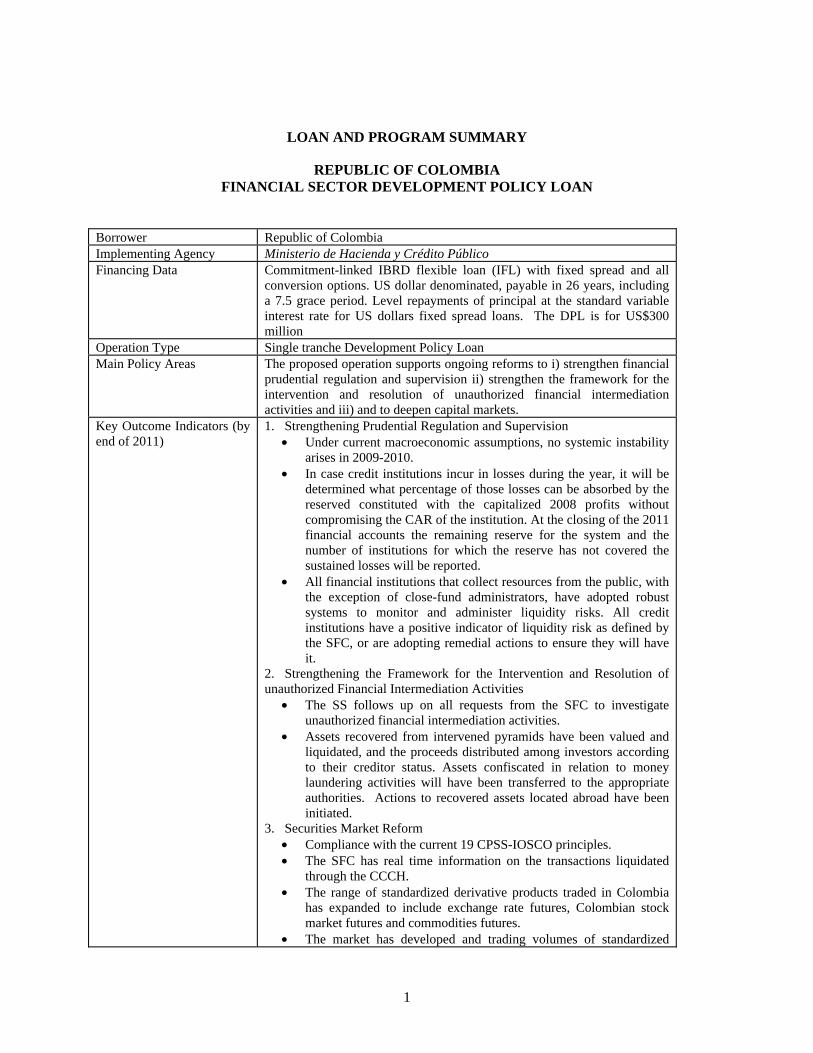

LOAN AND PROGRAM SUMMARY

REPUBLIC OF COLOMBIA FINANCIAL SECTOR DEVELOPMENT POLICY LOAN

Borrower Republic of Colombia Implementing Agency Ministerio de Hacienda y Crédito Público Financing Data Commitment-linked IBRD flexible loan (IFL) with fixed spread and all

conversion options. US dollar denominated, payable in 26 years, including a 7.5 grace period. Level repayments of principal at the standard variable interest rate for US dollars fixed spread loans. The DPL is for US$300 million

Operation Type Single tranche Development Policy Loan Main Policy Areas

The proposed operation supports ongoing reforms to i) strengthen financial prudential regulation and supervision ii) strengthen the framework for the intervention and resolution of unauthorized financial intermediation activities and iii) and to deepen capital markets.

Key Outcome Indicators (by end of 2011)

1. Strengthening Prudential Regulation and Supervision • Under current macroeconomic assumptions, no systemic instability

arises in 2009-2010. • In case credit institutions incur in losses during the year, it will be

determined what percentage of those losses can be absorbed by the reserved constituted with the capitalized 2008 profits without compromising the CAR of the institution. At the closing of the 2011 financial accounts the remaining reserve for the system and the number of institutions for which the reserve has not covered the sustained losses will be reported.

• All financial institutions that collect resources from the public, with the exception of close-fund administrators, have adopted robust systems to monitor and administer liquidity risks. All credit institutions have a positive indicator of liquidity risk as defined by the SFC, or are adopting remedial actions to ensure they will have it.

2. Strengthening the Framework for the Intervention and Resolution of unauthorized Financial Intermediation Activities

• The SS follows up on all requests from the SFC to investigate unauthorized financial intermediation activities.

• Assets recovered from intervened pyramids have been valued and liquidated, and the proceeds distributed among investors according to their creditor status. Assets confiscated in relation to money laundering activities will have been transferred to the appropriate authorities. Actions to recovered assets located abroad have been initiated.

3. Securities Market Reform • Compliance with the current 19 CPSS-IOSCO principles. • The SFC has real time information on the transactions liquidated

through the CCCH. • The range of standardized derivative products traded in Colombia

has expanded to include exchange rate futures, Colombian stock market futures and commodities futures.

• The market has developed and trading volumes of standardized

2

derivatives have increased as a share of spot transactions. In particular futures traded over Colombian sovereign bonds, the Colombian stock market index and the market exchange rate of the Colombian Peso vis-à-vis the US Dollar amount to a third of the spot transactions in those assets.

Program Document Objective(s) and Contribution to CAS

The proposed loan would support sustainable growth and alleviation of poverty by:

• Strengthening the financial system to prevent disruptive and costly financial crises; and

• Consolidating the securities markets as a pillar of economic growth to address the needs of individuals and the productive sector.

Risks and Risk Mitigation

The main risk to the operation arises from further deterioration of macroeconomic conditions, which would negatively affect the health of the financial system and/or delay securities market development.

Operation ID Number P116088

3

IBRD PROGRAM DOCUMENT FOR A PROPOSED FINANCIAL SECTOR DEVELOPMENT POLICY LOAN

TO THE REPUBLIC OF COLOMBIA

I. INTRODUCTION

1. This single-tranche US$300 Development Policy Loan (DPL) has been requested by the Government of Colombia (GoC). The GoC is facing significant macroeconomic challenges from the current global financial crisis, which has resulted in lower capital inflows and increased borrowing costs. Recent growth and poverty reduction in Colombia has been supported by a stable expansion of the financial system, following the financial crisis that Colombia suffered at the end of the 1990s. As the ongoing global crisis impacts Colombia, the GoC is committed to preserving these gains in financial sector development as part of its broader development strategy. This financing will provide support for the two pronged combined approach the government has been implementing to tackle, in the short run, the impact of the international crisis in the Colombian financial sector, while at the same time proceed with the reforms needed to further develop financial markets in the long run. GoC’s commitment to face these issues and the soundness of the approach as well as the overall impact of these reforms in the Colombian economy underpin the support of this loan.

2. Due to the global crisis, Colombia is facing significant macroeconomic challenges, although sound past macroeconomic policies and measures adopted by the authorities will mitigate the impact of the global turbulence. The sustained period of strong growth and moderate inflation experienced by the Colombian economy in recent years ended in 2008. Growth is expected to contract by 0.7 percent in 2009 and remain subdued in 2010 with a forecasted 1.5 percent GDP growth. Growth perspectives compare favorably to those of other large Latin American countries which –with the exception of Peru− are expected to experience a more severe contraction in 2009. Colombia is relatively well positioned as traditional domestic amplifiers of crises − exchange rate, financial, and fiscal − have been well managed and could help mitigate the impact of the crisis.

3. Colombia’s financial sector appears to be sound and well supervised but government efforts to strengthen its foundations need to continue as the global crisis heightens existing vulnerabilities. The main risk for the system is credit risk, particularly the consumer loan portfolio. However, existing capital and provisions buffers appear adequate to cover potential losses and preserve systemic financial stability. Nevertheless, some small financial companies specialized in car loans could experience difficulties. Market and liquidity risks appear contained so far and systemic risks arising from non-bank financial institutions (NBFIs) appear limited.

4. Ongoing regulatory reforms to strengthen financial sector resilience are well structured. The orientation of several measures implemented by the GoC was later validated by the recommendations issued by the G-20. The increase of banks’ capital and liquidity buffers as a prudential countercyclical measure highlights the regulator’s responsiveness and vision to fence off the impact of the global crisis.

5. The measures adopted in the wake of the collapse of pyramid schemes will discourage unauthorized financial intermediation, preserving the strength of the system and protecting the poor. The collapse of fraudulent pyramid schemes prompted swift action from the authorities −which adopted a new and enhanced framework for the intervention of unauthorized financial intermediaries − avoiding contagion effects to the supervised system. These measures will discourage unauthorized financial intermediation, which will strengthen the financial sector and protect financial consumers and especially the poor, which are disproportionally affected by the collapse of pyramids.

4

6. Further development of capital markets in Colombia is necessary to promote savings and to channel those savings efficiently to fund private sector investment and foster growth. The GoC has redoubled efforts to introduce additional regulations to keep on track the securities market reform initiated in 2005. To this end, the authorities issued regulation for an upgraded market infrastructure that increases efficiency and reduces systemic risks to create the conditions for solid market growth. The authorities have also advanced in regulating the securities market intermediaries and the type of transactions that can be negotiated and executed in the market. The regulations have made possible the creation of a central counterparty clearing house and the creation of an exchanged-trade derivatives market. The proposed operation would help achieve the objective of promoting savings and investment needed to sustain growth as identified in the Colombian National Development Program and supported by the current Country Partnership Strategy.

7. The World Bank engagement in Colombia, particularly with respect to policy areas supported by this DPL, has emphasized synergies of IBRD financing with other multilateral organizations. The request of this loan is part of the strategy of the GoC, which has increased its funding from multilateral organizations in the face of a deterioration of the external environment. In May 2009, Colombia obtained US$10.5 billion as a one-year precautionary arrangement under the IMF’s Flexible Credit Line (FCL). Collaboration with other multilaterals is fluid. In particular, World Bank and IMF staff maintains strong coordination and cooperation on both macroeconomic issues as well as financial sector issues.

II. COUNTRY CONTEXT

8. Following the 1999 crisis, Colombia enjoyed a sustained period of growth that supported employment creation and poverty reduction. Real economic growth accelerated from 2.5 percent in 2002 to 7.5 percent in 2007, inflation moderated, and private investment rose from 9.9 percent of GDP in 2002 to over 16 percent in 2007. Colombia’s unemployment rate dropped from over 17 percent in 2002 to approximately 12 percent in 2007. The country’s recovery was driven by favorable external conditions, stable macroeconomic policies and wide-ranging structural reforms.

9. Political stability and improved security contributed to the economic recovery. President Uribe has been in power since 2002 and is credited for the economic comeback of Colombia amid increased security. Congress has approved a Law to call a referendum on changing the Constitution once again to allow President Uribe to run for a consecutive third term next year. The Constitutional Court still has to approve the referendum.

RECENT ECONOMIC DEVELOPMENTS1

10. The sustained period of strong growth and moderate inflation experienced by the Colombian economy in recent years ended in 2008. During 2004-2007, high external demand, improved terms of trade and lower cost of international credit created a favorable environment for growth. During 2008 economic growth slowed down, reflecting past monetary tightening that resulted in a significant reduction in credit growth (from 34.4 percent y-o-y in March 2007 to 18 percent in August 2008) and weakening commodities prices and global demand. In particular, export growth − which had remained relatively resilient− collapsed due to the ongoing global slowdown. The deceleration intensified following the renewed global financial turbulence at end-September 2008. In the last quarter of 2008, GDP contracted by 1 percent y-o-y, and growth for the year as a whole stood

1 See Annex 4 for additional information on macroeconomic developments.

5

at 2.5 percent −a third of the growth rate in the previous year. Shocks to fuel and food prices pushed inflation to 7.7 percent at end-2008 well in excess of the Central Bank (Banco de la República, BdR) target of 5 percent for 2009. Positive terms of trade developments in first half of the year were compensated by a collapse in export volume in the second half and declining oil prices. Thus, the current account for 2008 as a whole ended up in a deficit of 2.8 percent of GDP, a similar figure to the one in 2007 (see Table 1).

Table 1: Key Economic Indicators for Colombia, 2003-2008 Indicator 2003 2004 2005 2006 2007 2008 (e) Real GDP growth (%) 4.6 4.7 5.7 6.8 7.5 2.5 Inflation (%) (end of period) 6.5 5.5 4.9 4.5 5.7 7.7 Nominal Exchange Rate (Average) 2877.7 2628.6 2320.8 2361.1 2078.3 1967.7

Current Account Balance (% of GDP) -1.0 -0.8 -1.3 -1.9 -2.9 -2.8 NFPS Revenues (% of GDP) 30.0 30.0 30.6 32.7 33.2 32.0 NFPS Expenditures (% of GDP) 32.5 31.2 30.8 33.7 34.2 31.9 NFPS Balance (% of GDP) -3.2 -1.5 0.0 -1.2 -1.0 0.1 Net Debt of the Non Financial Public Sector (% of GDP)1/

46.7 42.4 38.9 36.0 32.3 31.9

External Debt/GDP (%) 41.5 34.7 26.6 24.7 21.4 19.1 Investment (% of GDP) 18.9 20.1 21.6 24.3 24.3 24.3 Public sector 6.3 5.9 4.9 6.5 7.7 7.3 Private sector 12.6 14.1 16.7 17.8 16.6 17.0

1/ This is defined as gross debt of the non financial public sector but netting out government and government entity bonds held by the public sector itself. Note: Non-Financial Public Sector (NFPS) data includes ECOPETROL. The NFPS balance includes the statistical discrepancy. Data comes from IMF. Source: MHCP, BdR; IMF and World Bank estimates.

11. Fiscal discipline resulted in low deficits and a reduction in public sector debt as a share of GDP, although concerns remain regarding expenditure rigidities. In recent years, fiscal policy aimed at reducing public sector and external vulnerabilities by ensuring debt sustainability. The combination of domestic economic growth, improved international conditions, peso appreciation (which reduces the cost of servicing foreign currency-denominated debt), and revenue-enhancing policy reforms improved the fiscal accounts.2 As a result, the combined public sector deficit improved from 3.7 percent of GDP in 2002 to a balance in 2005. However, budget and legal rigidities that resist spending cuts have slowed the progress of policy reforms on the expenditure side. Despite the strong revenue performance, expenditure dynamics −especially pension expenditures and transfers to sub national governments− have resulted in modest fiscal deficits during 2006-2007. Transfers to the main state-run pension system will continue to expand over the next decade −as payouts greatly exceed new contributions− despite the 2005 constitutional reform that reduced the net present value of pension liabilities by 19 percentage points of GDP. This reform eliminated special regimes for state employees and imposed ceilings on benefits in the public-sector pension system. In 2008, the non- financial public sector reached a surplus of 0.1 percent of GDP ‒ the highest balance since 2005‒ well above the government’s target of -0.9 percent of GDP. This improvement over the government’s target is

2 Policy reforms have concentrated on the revenue side. In 2002, Congress approved Law 788, supported by the Bank’s Fiscal and Institutional Adjustment Loan (FIAL) Program (Loan 7163-CO, approved March 2003). The Law expanded the revenue base for the government by eliminating tax exemptions related to VAT, personal and corporate income taxes. The Law introduced a cap on wage exemptions for personal income tax and eliminated the exemptions on capital gains from the sales of stock, mutual funds, real estate and privileged corporate contracts, forms, funds or bonds.

6

explained primarily by 1.1 percent of GDP surplus by local governments, up from the government’s target of 0.3 percent of GDP. The latter is at least partially the result of the recent central government’s policies to enforce fiscal discipline at the local level.

12. The global financial crisis led to a sharp tightening of financing conditions in Colombia, as well as in a large number of emerging market economies. As the global financial turbulence intensified in the second half of 2008, Colombian financial markets were negatively affected in line with developments in other Latin American countries. The withdrawal of liquidity in financial markets amid increased risk aversion resulted in larger sovereign spreads and stock market losses across the region (see Figure 1). In Colombia, the EMBI spread increased to 740 b.p. at end October, The stock market index declined by a third in line with developments elsewhere. The exchange rate appreciation, prompted in part by tightening monetary policy, reversed and the exchange rate depreciated by about 16 percent since end-August 2008, limiting the loss of reserves during 2008 to US$ 125 million (about 0.5 percent of total reserves). In this context the Central Bank removed the controls to capital inflows, a temporary measure to prevent excessive exchange rate volatility. An increase in credit risk premiums and funding costs pushed the lending rate up by 77 b.p. in the last quarter of 2008. However, subsequent decline in policy rates have brought down lending rates to levels similar to those in early 2007.

13. Markets normalized in the first half of 2009, and global sovereign bond issuance and domestic corporate bond issuance increased. Since end-2008 the stock market index increased by 49 percent while the exchange rate has appreciated by 17 percent and reserves were broadly stable. As market sentiment improved, partly due to the authorities’ actions, the Colombian government was able to successfully place a ten-year US$1 billion bond issue in January with a spread of 503 b.p. over US treasuries, and an additional US$ 1 billion in April at a yield of 7.35 and 435 b.p. spread. Spreads have declined further, standing at about 300 b.p. at end-June 2009. Lower inflation perspectives have prompted a rally in government domestic securities, with the yield on the benchmark domestic paper maturing in 2020 trading at the lowest levels since November 2006. In contrast to other emerging markets, domestic commercial paper markets have been quite active. Issuance in 2009 so far reached more than US$2 billion, about 80 percent of total issuance in 2008.

7

Figure 1. Colombia: Stock Market Index, EMBI Spread and International Oil Price

Figure 1(a): EMBI Spreads Chile, Colombia, Latin America & the Caribbean, June 2005-June 2009

Figure 1(b): EMBI Spreads Brazil, Colombia and Mexico, June 2005-June 2009

Chile

Colombia

LAC

0

100

200

300

400

500

600

700

800

900

1000

6/12/05 12/12/05 6/12/06 12/12/06 6/12/07 12/12/07 6/12/08 12/12/08 6/12/09

EMBI Spreads

Chile

Colombia

LAC

Brazil

Colombia

Mexico

0

100

200

300

400

500

600

700

800

900

1000

6/12/05 12/12/05 6/12/06 12/12/06 6/12/07 12/12/07 6/12/08 12/12/08 6/12/09

EMBI Spreads

Brazil Colombia Mexico

Figure 1(c): Stock Market Indices, Selected LAC Countries, June 2008 – June 2009

Figure 1(d): Net International Reserves in Colombia, US$ million, June 2008 – June 2009

BRA

CHL

COL

MEX

40

50

60

70

80

90

100

110

120

6/15/08 8/15/08 10/15/08 12/15/08 2/15/09 4/15/09 6/15/09

Stock Market Indices (Jan 1st, 2008 = 100)

BRA CHLCOL MEX

22,000

22,500

23,000

23,500

24,000

24,500

25,000

25,500

6/10/08 8/10/08 10/10/08 12/10/08 2/10/09 4/10/09 6/10/09

Net International Reserves (US$ Millions)

Figure 1(e): Exchange Rates in Selected LAC

Countries, June 2008 – June 2009 (January 1st, 2008 = 100)

Figure 1(f): Exchange Rates in Selected LAC Countries, June 2008 – June 2009

(January 1st, 2008 = 100)

80

90

100

110

120

130

140

150

6/15/08 8/15/08 10/15/08 12/15/08 2/15/09 4/15/09 6/15/09

Exchange Rates

COL MEX

80

90

100

110

120

130

140

150

6/15/08 8/15/08 10/15/08 12/15/08 2/15/09 4/15/09 6/15/09

Exchange Rates

BRA CHL

Figure 1(a): EMBI Spreads Chile, Colombia, Latin

America & the Caribbean, June 2005-June 2009 Figure 1(b): EMBI Spreads Brazil, Colombia and Mexico,

June 2005-June 2009 Source: Banco de la Republica de Colombia and LCSPE Database.

8

MACROECONOMIC OUTLOOK AND CHALLENGES

14. Ongoing deleveraging and continued high levels of uncertainty have prompted a sharp downturn in global economic activity, world trade and international commodity prices which will negatively affect Colombia through several channels. In light of external developments, economic activity and the prospects for near-term economic growth in Colombia have deteriorated significantly. The main channels of transmission of the global economic and financial shocks to the Colombian economy are the following:

(a) Weaker external demand. Colombia has a relatively open economy; exports of goods and services are equivalent to over 17 percent of GDP while total trade amounts to about 40 percent. Although exports have become more geographically diversified (beyond the U.S), export volume growth has decelerated significantly. Global demand is expected to decline by 0.5 percent in 2009 compare to 2008. It is estimated that a 1 percent decline in export demand lowers GDP growth by 0.3 percent

(b) Lower oil prices. Colombia received a record-high level of revenue from oil exports in 2008

(US$12.2 billion) as a result of a historically high average oil price for the Colombian mix of crude oil that reached US$134.3 per barrel. The dramatic drop of international oil prices has a significant impact on the country’s public finances and the current account deficit. Oil accounts for about 20 percent of total public sector revenues and 24 percent of total exports on average. In 2009 oil prices are expected to average US$47.2 per barrel. The envisioned decline in oil prices −ceteris paribus− will increase the current account deficit and public sector deficit by 1.8 percent and 0.5 percent respectively.

(c) Lower workers remittances. Workers’ remittances, mainly from Colombians living in the

U.S and Spain, have started to decline since the last quarter of 2008. Remittances amounted to US$1 billion in the first quarter of 2009, 4.2 percent below last year. For the year as a whole they are expected to decline by 3 percent.

Figure 2: Remittances in Colombia: Level, Change and Share of GDP

January 2002-May 2009

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

150

200

250

300

350

400

450

2002

Jan M M J S N

2003

Jan M M J S N

2004

Jan M M J S N

2005

Jan M M J S N

2006

Jan M M J S N

2007

Jan M M J S N

2008

Jan M M J S N

2009

Jan M

US

$ M

illio

ns

Remittances Monthly Flow (12-month m.a.) % Change, y/y

Source: WB staff based on data from Banco de la Republica de Colombia.

(d) Lower capital inflows. Capital flows are declining somewhat due to diminished global

liquidity. Capital flows have declined by 3.5 percent in the last quarter of 2008 with respect

9

to the previous quarter. Although FDI flows experienced a significant expansion during 2008, current global conditions might impact negatively on the inflows during the year.

(e) Increased risk aversion. The deterioration in economic perspectives and market turbulence

will likely have a negative impact on risk premiums and credit supply.

15. Factors that typically magnify external shocks resulting in severe economic disruptions do not play an important role in the case of Colombia. In some Latin American countries, external shocks have been typically amplified by severely appreciated real exchange rates, weak domestic financial sectors and public sector balance sheet vulnerabilities. Fortunately, in Colombia’s case, the factors that typically magnify crisis mitigate the impact of the shock.

(a) Flexible exchange rate. Although the nominal exchange rate had appreciated considerably during 2007 and 2008, Colombia entered the turbulence period with an exchange rate value close to its equilibrium level3. The flexible exchange rate acts as a shock absorber helping to counter the deceleration in external demand.

(b) Resilient financial sector. The strength of the financial sector, with healthy financial indicators (see paragraph 25), has prevented a credit crunch, and credit to the private sector − although has decelerated due to lower demand and increased risk aversion− continues to grow at about 8 percent in real terms at end April 2009. Financial dollarization is not a destabilizing factor in Colombia, with foreign currency denominated loans amounting only to 6 percent of total loans. The dollarization ratio is even lower for deposits.

(c) Low public deficits and manageable external debt. Fiscal consolidation and the government public debt management strategy put public debt in a declining path and reduce the share of foreign denominated debt. External debt has almost halved since 2003 due to the sustained FDI flows. Reserves (over US$21 billion, or 11 percent of GDP at end-May 2009) more than doubles the annual external debt amortizations, contributing to ensure current account financing even in the difficult global conditions. Given limited external vulnerabilities, exchange rate pressures would likely be moderate..

16. Overall, Colombia is in a relative better position to confront the global crisis than other Latin American countries. This outcome is a result of the factors discussed in the previous paragraph as well as the countercyclical policies implemented by the authorities (see paragraph 18 and Box 1).

3 See IMF 2008, Staff Report for the Article IV Consultation.

10

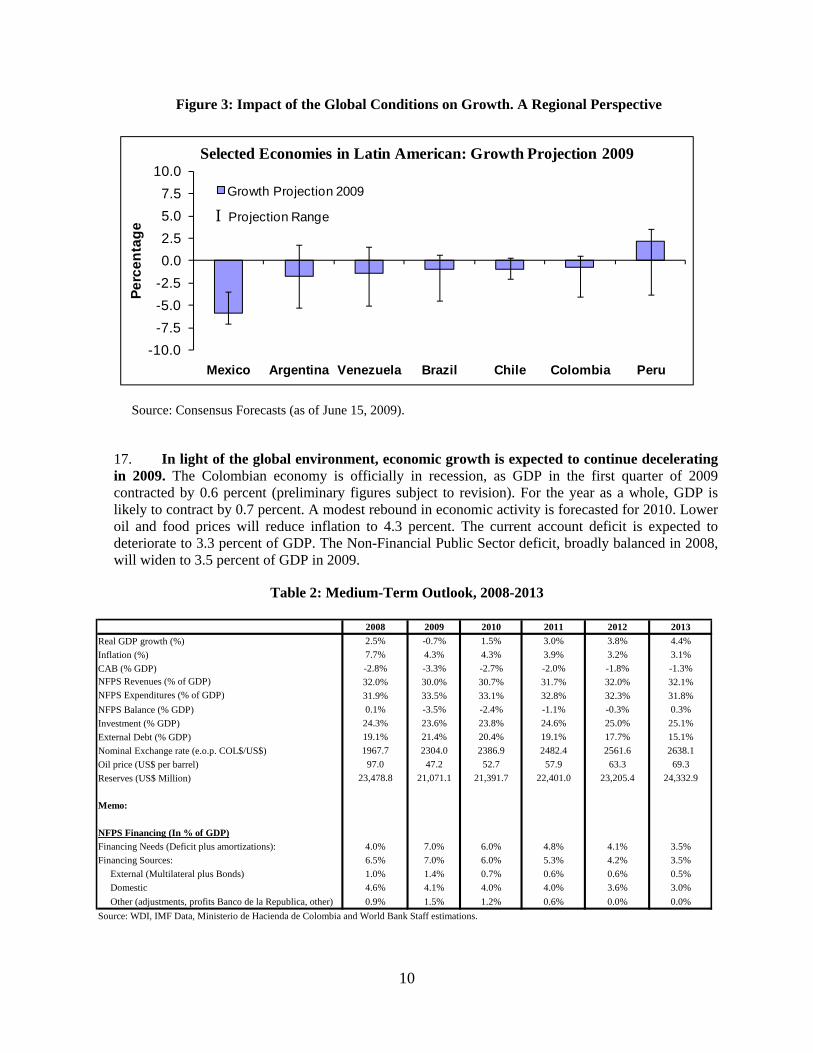

Figure 3: Impact of the Global Conditions on Growth. A Regional Perspective

-10.0

-7.5

-5.0

-2.5

0.0

2.5

5.0

7.5

10.0

Mexico Argentina Venezuela Brazil Chile Colombia Peru

Per

cen

tag

e

I Projection Range

Selected Economies in Latin American: Growth Projection 2009

Growth Projection 2009

Source: Consensus Forecasts (as of June 15, 2009).

17. In light of the global environment, economic growth is expected to continue decelerating in 2009. The Colombian economy is officially in recession, as GDP in the first quarter of 2009 contracted by 0.6 percent (preliminary figures subject to revision). For the year as a whole, GDP is likely to contract by 0.7 percent. A modest rebound in economic activity is forecasted for 2010. Lower oil and food prices will reduce inflation to 4.3 percent. The current account deficit is expected to deteriorate to 3.3 percent of GDP. The Non-Financial Public Sector deficit, broadly balanced in 2008, will widen to 3.5 percent of GDP in 2009.

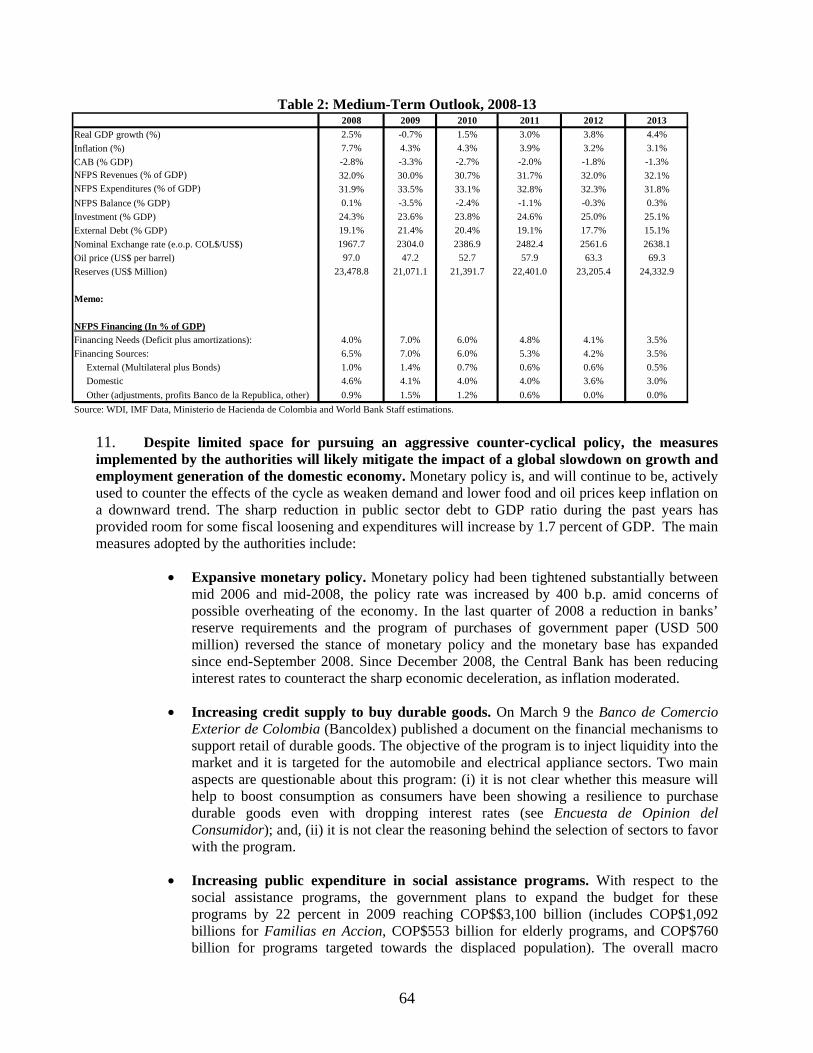

Table 2: Medium-Term Outlook, 2008-2013

2008 2009 2010 2011 2012 2013

Real GDP growth (%) 2.5% -0.7% 1.5% 3.0% 3.8% 4.4%

Inflation (%) 7.7% 4.3% 4.3% 3.9% 3.2% 3.1%

CAB (% GDP) -2.8% -3.3% -2.7% -2.0% -1.8% -1.3%NFPS Revenues (% of GDP) 32.0% 30.0% 30.7% 31.7% 32.0% 32.1%NFPS Expenditures (% of GDP) 31.9% 33.5% 33.1% 32.8% 32.3% 31.8%

NFPS Balance (% GDP) 0.1% -3.5% -2.4% -1.1% -0.3% 0.3%

Investment (% GDP) 24.3% 23.6% 23.8% 24.6% 25.0% 25.1%

External Debt (% GDP) 19.1% 21.4% 20.4% 19.1% 17.7% 15.1%

Nominal Exchange rate (e.o.p. COL$/US$) 1967.7 2304.0 2386.9 2482.4 2561.6 2638.1

Oil price (US$ per barrel) 97.0 47.2 52.7 57.9 63.3 69.3

Reserves (US$ Million) 23,478.8 21,071.1 21,391.7 22,401.0 23,205.4 24,332.9

Memo:3.0% 3.4% 3.0% 3.3% 3.7% 4.9%

NFPS Financing (In % of GDP) 6.9% 10.4% 9.0% 8.1% 7.8% 8.4%Financing Needs (Deficit plus amortizations): 4.0% 7.0% 6.0% 4.8% 4.1% 3.5%Financing Sources: 6.5% 7.0% 6.0% 5.3% 4.2% 3.5% External (Multilateral plus Bonds) 1.0% 1.4% 0.7% 0.6% 0.6% 0.5% Domestic 4.6% 4.1% 4.0% 4.0% 3.6% 3.0%

Other (adjustments, profits Banco de la Republica, other) 0.9% 1.5% 1.2% 0.6% 0.0% 0.0%

Source: WDI, IMF Data, Ministerio de Hacienda de Colombia and World Bank Staff estimations.

11

18. Countercyclical measures implemented by the authorities will mitigate the impact of a global slowdown on growth and employment generation. Monetary policy is, and will continue to be, actively used to counter the effects of the cycle as weakened demand and lower food and oil prices keep inflation on a downward trend. Regarding fiscal policy, the authorities will allow automatic stabilizers to fully operate. In addition, the sharp reduction in public sector debt to GDP ratio during the past years has provided room for some modest fiscal loosening. In this context expenditures are expected to increase by 1.7 percent of GDP. The main measures adopted by the authorities are included in Box 1.

19. The GoC is seeking to further reduce external vulnerabilities by requesting funding from multilaterals. Authorities indicated they plan to obtain US$2.4 billion from multilaterals this calendar year to help cover the envisioned external financing needs for 2009. Colombia also obtained an IMF precautionary flexible credit line to access US$10.5 billion. At end-May 2009, the World Bank has disbursed US$580 million (see Annex 7 for details on the World Bank program with Colombia).

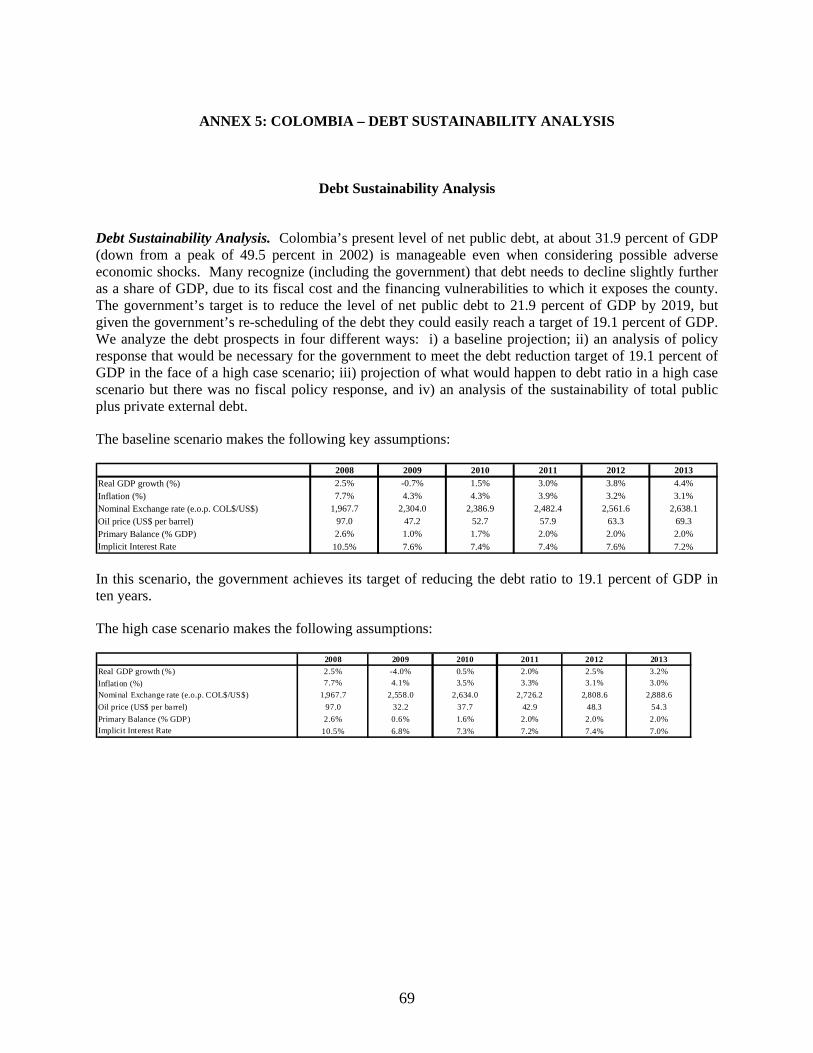

20. While there remains considerable uncertainty as regards to the depth and length of the global recession, neither external nor fiscal sustainability appear at risk. Nevertheless, the current environment characterized by volatility in financial magnitudes and commodity prices poses several downside risks. A fall in oil prices would negatively affect the fiscal outlook and the current account balance. Intensification of the global liquidity squeeze further deteriorates the external balance. To gauge these risks a low growth scenario is evaluated. The scenario shows the impact of a drop of the oil price to a low of US$32 per barrel and a further deterioration of the external environment during 2009. The simulation indicates that Colombia has enough reserves to cushion a potential external financing shock without severely affecting exchange rate stability. This scenario does not pose a serious problem to debt sustainability (See Annex 5).

Table 3: Low Growth Scenario, 2008-13

2008 2009 2010 2011 2012 2013

Real GDP growth (%) 2.5% -4.0% 0.5% 2.0% 2.5% 3.2%

Inflation (%) 7.7% 4.1% 3.5% 3.3% 3.1% 3.0%

CAB (% GDP) -2.8% -1.6% -1.1% -1.1% -1.3% -1.4%NFPS Revenues (% of GDP) 32.0% 29.5% 30.1% 31.3% 31.5% 31.9%NFPS Expenditures (% of GDP) 31.9% 33.5% 32.9% 32.6% 32.2% 32.1%

NFPS Balance (% GDP) 0.1% -4.0% -2.8% -1.3% -0.7% -0.2%

Investment (% GDP) 24.3% 22.4% 23.3% 24.1% 24.6% 24.7%

External Debt (% GDP) 19.1% 24.3% 23.1% 21.7% 20.1% 17.0%

Nominal Exchange rate (e.o.p. COL$/US$) 1967.7 2558.0 2634.0 2726.2 2808.6 2888.6

Oil price (US$ per barrel) 97.0 32.2 37.7 42.9 48.3 54.3Reserves (US$ Million) 23,478.8 20,551.1 20,626.7 20,393.2 20,389.2 20,436.1

Source: WDI, IMF Data and World Bank Staff estimations.

12

Box 1. Countercyclical measures to mitigate the Economic Slowdown

Expansive monetary policy. From mid-2006 to mid-2008, the policy rate was increased by 400 b.p. amid concerns of possible overheating. As result of the renewed global financial turbulence, lending rates increased further in the last quarter of 2008. To inject liquidity in the market BdR expanded monetary base by reducing banks’ reserve requirements and introduced a program of purchases of government paper (US$500 million). From December 2008 to end-June 2009, the sharp moderation in inflation (from 7.9 in November 2008 to 4.8 percent at end-May 2009) has allowed the BdR to reduce interest rates by 550 b.p. and lending rates are now broadly at end-2006 levels. While credit growth has decelerated sharply during the last 12 months, in the latest lending survey by the BdR (May 2009), the majority of respondents ‒particularly in service and manufacture firms‒ anticipate that there will be no change in the amount of credit availability within the next 6 months. The proportion of survey respondents who believe there is sufficient credit in the system is increasing but is still lower than a year ago in April 2008 However, banks have tightened lending criteria with increased attention to the repayment capacity and liquidity position of the borrowing firms. To avoid severe credit disruptions, the authorities have secured US$850 million of funds from the IADB for Colombian public financial institutions (see paragraph 58).

Inflation Developments and Monetary Policy Rates

Source: Banco de la Republica de Colombia

Increased investment in infrastructure. The government has announced a series of measures to invest in infrastructure. The “plan de choque” increases the budget for infrastructure by 25 percent with respect to 2008 to an amount of US$ 2.7 billion. The World Bank will support infrastructure investments with mainly 4 projects in 2009-2010, approximately amounting to USD $1.1 billion. These infrastructure projects are labor intensive and are expected to have a significant impact on employment and growth.

Increased public expenditure in social assistance programs. With respect to the social assistance programs, the government plans to expand the budget for these programs by 18 percent in 2009 reaching US$1.45 billion. The expanded budget includes US$474 million for Familias en Acción ‒a program of cash transfers to poor families conditional on children attending school and meeting basic preventive health care requirements‒, US$240 million for elderly programs, and US$330 million for programs targeted towards the displaced population. These programs protect the poor from the impact of the crisis. The World Bank is supporting Familias en Acción and other social programs with US$ $636.5 million in FY09-10 (see Annex 7).

13

The Financial Sector

21. The Colombian financial system is dominated by domestic banks and it is highly concentrated. The system includes a variety financial intermediaries, including pension funds (AFPs), insurance companies, brokerage houses, trust funds and mutual funds. Credit institutions dominate the financial landscape with almost half of total financial sector assets. Banks are by far the largest credit institutions (about 85 percent of total credit institution assets), which also include finance and leasing companies, financial corporations − similar to investment banks, although regulated− and financial cooperatives. The 1999 crisis resulted in substantial consolidation of private banks, whose number declined from over 30 in 1998 to 17 at end 2008. The largest public banks were privatized and only a small public bank remains in the market (5 percent of the assets of credit institutions). The consolidation process resulted in the formation of large domestic financial conglomerates. The two largest conglomerates account for about half of financial sector assets. Foreign penetration is modest compared with other countries. Foreign owned banks control less than a fifth of banking assets but intensively compete with local banks.

Figure 4: Financial Sector Composition

Banking44%

Trust & Mutual Funds27%

Pension Funds15%

Insurance5% Other

9%

Total Assets in the Financial System by Industry (April 2009)

Source: SFC

22. After a long period of decline due to the crisis of the late 1990s, the banking sector begun to recover in 2004. The resolution of troubled institutions and a favorable external environment stimulated growth and propitiated the recovery of banking intermediation. Strong bank profitability− arising from valuation gains on the banks’ government securities portfolio as interest rates declined from post-crisis highs− allowed for an expansion of loan supply. At the same time, the resumption of domestic economic growth, supported by a favorable external environment increased loan demand. Standard financial performance indicators – solvency, profitability, efficiency and asset quality –significantly improved.

14

Figure 5: Credit to the Private Sector as Share of GDP in Selected Countries

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

55.0

60.0

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 200760.0

65.0

70.0

75.0

80.0

85.0

90.0

Colombia Argentina Brazil Peru Mexico Chile (right axis)

Source: World Bank, World Development indicators.

23. The level of financial development is in line with regional levels given the country characteristics. Credit to the private sector amounts to about 33 percent of GDP, still below the levels reached in the late 1990s before the crisis. It is lower than the levels for Chile and Brazil but higher than average regional levels, controlling for the country characteristics (see Figures 5 and 6). Efforts to reform and develop the securities market have activated the market, although number of issuers is relatively low and the market liquidity needs to improve.

24. The debt market has been growing in the last few years, dominated by public debt instruments. At the end of 2008, Colombia’s outstanding stock of fixed income securities was US$ 81 billion (equivalent to 56 percent of its GDP), of which US$ 44.6 billion was government debt. While it remains limited, the importance of corporate bonds as a source of financing for firms has increased slightly. While in 2005 there were 18 issuances, which were worth US$962 million (0.6 percent of GDP) in the first half of 2009 alone corporate bond issuance reached more than 1 percent of the forecasted GDP for the year.

15

Figure 6: Colombia: Indicators of Financial Sector Development

ACTUAL AND BENCHMARKED LEVELS OF FINANCIAL DEVELOPMENTLatest year availableSIZE EFFICIENCY AND LIQUIDITY REACH

BANKINGBank Credit to the Private Sector Bank Deposits Net Interest Margin(2000-2007), % of GDP (2000-2007), % of GDP (2000-2007), % of Assets

EQUITIESStock Market Capitalization Stock Market Turnover Ratio Number of Listed Firms(2000-2007), % of GDP (2000-2007) (2000-2007), / Mill. of People

BONDSPrivate Bonds Public Bonds(2000-2007), % of GDP (2000-2007), % of GDP

* Includes assets to GDP of pension funds, insurance companies and mutual funds

Note: The predictions are based on pooled, year-fixed effects OLS regressions for the period 2000-07 with the logarithm of X as a dependent variable. For the predictions that take into account regional influences, separate regressions are used that includ

0

10

20

30

40

50

60

2000 2001 2002 2003 2004 2005 2006 20070

10

20

30

40

50

60

70

2000 2001 2002 2003 2004 2005 2006 2007

0

1

2

3

4

5

6

7

8

9

2000 2001 2002 2003 2004 2005 2006 2007

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004 2005 2006 2007

0

20

40

60

80

100

120

2000 2001 2002 2003 2004 2005 2006 2007

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004 2005 2006 2007

0

2

4

6

8

10

12

14

2000 2001 2002 2003 2004 2005 2006 2007

0

1

2

3

4

5

6

7

8

9

10

2000 2001 2002 2003 2004 2005 2006 2007

0

20

40

60

80

100

120

Bank Credit Bank Deposit Stock MrktCap

PrivateBonds

Public Bonds InstitutionalInvestors'Assets*

Turnover

0

5

10

15

20

25

30

35

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Net InterestMargin Listed Firms / Mill. People

0

1

2

3

4

5

6

7

8

9

0

100

200

300

400

500

600

700

800

900

1000

Accounts per 1,000people

Source: Benchmark is dependent upon Country-Specific Characteristics that can affect financial development. Depending on the financial sector indicator used, a range of 31-160 countries were used for the regression analysis. World Bank Project PCN: Financial Indicator Benchmark Project.

16

25. At end-April 2009, the banking system appeared sound and well supervised. The Colombian banking system is well capitalized and very profitable. Following the 1999 crisis, supervision and regulation were revamped. The Financial Superintendence (Superintendencia Financiera de Colombia, SFC) currently supervises all financial intermediaries through on-site follow up and on-site visits (see section IV for details). The Banking system capital adequacy ratio (CAR) stood at 13.8, with all Colombian banks having a CAR well above the 9 percent regulatory minimum. However, it is important to notice that capital ratios include goodwill4. As a result, the loss absorption capacity of Colombian banks’ capital buffers is lower than that of regional peers, leaving the banks more exposed to potential pressure on asset quality.5 Already asset quality has deteriorated due to the economic slowdown, and non-performing loans (NPLs) reach 5.1 percent of total loans while loans classified as on watch or worse amount to 9.7 percent of total loans in April 2009. Provisions cover all NPLs but only 53.7 percent of classified loans on average, with some banks having substantially lower coverage levels (see Figure 7). While those figures compared unfavorably with that of other Latin American countries, it is worth noting that the Colombian definition of NPLs is rather strict as it includes loans past-due 30 days as opposed to the standard 90 days. Despite increased credit losses, profitability remained strong in 2008. Rising interest rates for most of the year and less-than-perfectly competitive system resulted in higher net interest margins. Recently, valuation increases in the portfolio of government securities have boosted profitability. In the first quarter of 2009, credit institutions reported even bigger profits than in the first quarter of 2008.

Table 4: Banking Sector Indicators in Selected Countries CAR NPL Provision/NPL ROE ROA Argentina 16.8 2.5 122.7 13.1 1.6 Brazil N/A 3.8 180.0 14.1 1.2 Chile 13.4 2.7 94.6 14.4 1.1 Colombia 13.8 5.1 102.0 22.6 2.4 Mexico 15.3 3.4 158.7 11.2 1.0 Peru 12.6 1.4 243.5 30.5 2.5 Source: Central Banks and Banking Superintendencies (Argentina December 2008 Data; Brazil NPLs and Provisions April 2009 Data, CAR ROE and ROA December 2008 Data; Chile and Peru March 2009 Data ; Mexico NPL, Provision, ROE, ROA March 2009 Data, CAR December 2008 Data; Colombia CAR, NPL and Provisions April 2009 Data, ROE and ROA February 2009 Data)

26. Some commercial financing companies (CFCs) could experience difficulties if the economic environment deteriorates further. CFCs −which hold 12.5 percent of the credit institutions’ assets − grant credit and finance themselves mostly with certificates of deposit that are protected by the Deposit Insurance Fund (Fondo de Garantía de Instituciones Financieras, FOGAFIN). CFCs have seen NPLs almost double in the last year reaching 7.15 percent of total loans for the sector in April 2009, with proviiouns covering 77.4 percent of those NPLs. Particularly affected are those companies oriented to automotive sector loans, and some may need to increase regulatory capital if the portfolio continues to deteriorate. On the positive side most of the CFCs belong either to a foreign group or a large domestic group and should not have difficulties in raising capital. Some of the smaller independent CFCs, which altogether hold about 4 percent of credit institutions assets, may have to consolidate or liquidate, although such exit is unlikely to pose systemic consequences.

4 Goodwill denotes the difference between the purchase value of a company and the book value of its assets. According to Basel norms, goodwill and other intangible assets should not be included in regulatory capital. 5 Fitch February 2009. “2009: A Year of Reckoning for Latin American Banks”.

17

Figure 7: Non-Performing Loans and Provisions

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

Non Performing Loans as a Percentage of the Total Portfolio

Commercial Consumer Mortgage* Microcredit Total

0.0%

50.0%

100.0%

150.0%

200.0%

250.0%

Provisions as a Percentage of Non Performing Loans

Commerical Consumer Mortgage Microcredit Total

Source : SFC. 27. Systemic risks arising from other financial intermediaries appear limited. The value of AFPs’ portfolio holdings were negatively affected by the decline in government securities prices (45 percent of AFPs’ investments) and stock market volatility, particularly in the second half of 2008. This issue was aggravated by the definition and measurement period for the minimum return benchmark. A few AFPs were close to being below the minimum return at the peak of market volatility, and could have had to increase capital. At the time, some market participants and regulators expressed concerns that portfolio reallocations by AFPs could put pressure in the government securities market, which would affect other financial intermediaries. However, these concerns have subsided as the market turn around and pension funds reported a profit of US$1.4 billion in the first quarter of 2009, compared to a loss of US$680 million during the same period last year. All other institutions are relatively small. Brokerage houses had been most affected by the decline in the stock market as mutual funds invest mostly in certificates of deposit from domestic financial institutions. While insurance companies technical margins’ are slightly negative, they are in line with average values in the last 15 years. As in the case of AFPs, the recent rally in the government’s Treasury bonds market has improved profitability for all intermediaries.

28. The collapse of fraudulent pyramid schemes prompted swift action from the authorities avoiding contagion effects to the supervised system. Some fraudulent pyramid schemes −which obtained resources from the public by promising exorbitant rates of return − had appeared in Colombia under sophisticated structures (see section VI for details). The companies masked their fraudulent money-collecting activities under the disguise of service provider companies and prepaid card sales. These fraudulent companies operated in 12 departments with a substantial number of investors, mostly in the low-income bracket. So far, the authorities have received more than 700,000 claims from investors amounting to about 1 percent of GDP. In November 2008, the government closed the pyramid schemes, enacted legislation to strengthen the powers of supervisors to act against such illegal operations (action supported by this operation), and began liquidating assets to return the recovered funds to investors. To help address the social costs, the authorities reallocated funds in the 2008 budget toward targeted social spending. Authorities also indicated investors of the pyramids will not be bailed

18

out. Swift action from the authorities prevented contagion effects to credit cooperatives and other supervised institutions operating in the same market segments.

Macro Financial Linkages

29. During 2005-2006, credit growth accelerated sharply. The favorable macroeconomic environment underpinned credit growth, with growth rates of almost 30 percent in real terms at the beginning of 2007. Credit grew particularly in the consumer segment, with real growth rates close to 50 percent at the height of the credit boom. Increased competition among credit institutions has played an important role, aided by the decline in interest rates. For example, the 90-day fixed-term deposit rate (Depósito a Término Fijo or DTF), which forms the benchmark reference rate for most loans, declined from almost 8 percent in early 2005 to less than 5 percent at end-March 2006. The credit growth outpaced the strong deposit growth and as a result the loan to deposit ratio increased from 81 percent at end-2005 to 93 percent at end-2008. The credit expansion was partly funded with the reduction in banks’ investment portfolio. The decline in the banks’ portfolio of government securities increased liquidity risks while decreasing exposure to market risks. The past credit boom increased corporate and household balance sheet vulnerabilities, which in the current economic environment could result in substantial credit losses for bank. Tightening monetary policy and economic deceleration reduced the real growth rate of credit to 10.6 percent at end-September 2008. Since the global financial turbulence erupted, the growth rate has declined further to 7.9 at end April-2009 due to the deceleration in consumer and housing loans, while commercial lending growth rates remained broadly stable.

Figure 8: Credit Growth and Loan to Deposit Ratio

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

-50.0%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Real Credit Growth Rates

Commercial Consumer Total Mortgage (right axis)

75%

80%

85%

90%

95%

100%

Credit InstituionsLoan to Deposit Ratio

Source: SFC.

19

30. Corporate balance sheets appear relatively resilient, although concerns regarding the quality of data remain. A recent IMF paper concluded that the Colombian corporate sector is well capitalized, with relatively low leverage, adequate liquidity, improved profitability, and well hedged6. Balance sheet data from over 20,000 firms revealed that the sector liabilities amount only to half of the assets. Liquid assets cover about 148 percent of short-term obligations mitigating default risks in this portfolio. While average corporate profitability does not compare well with the region, it is close to the maximum levels during the last decade, despite the recent economic deceleration. Data from a much smaller sample, accounting for a fifth of the sector liabilities, pointed to limited foreign exchange exposure (6.5 percent of capital). Further convergence toward international accounting standards, more stringent auditing practices, and effective regulatory enforcement are required to overcome limitations and inconsistencies in reported corporate financial information. These deficiencies might undermine the diagnosis of existing weaknesses across firms and sectors7. In fact, data from the SFC indicates that NPLs are growing fastest among commercial loans, although the NPL ratio for the segment remains modest (2.9 percent in April 2009).

Figure 9: Growth Rate of Non Performing Loans by Segment

-40%

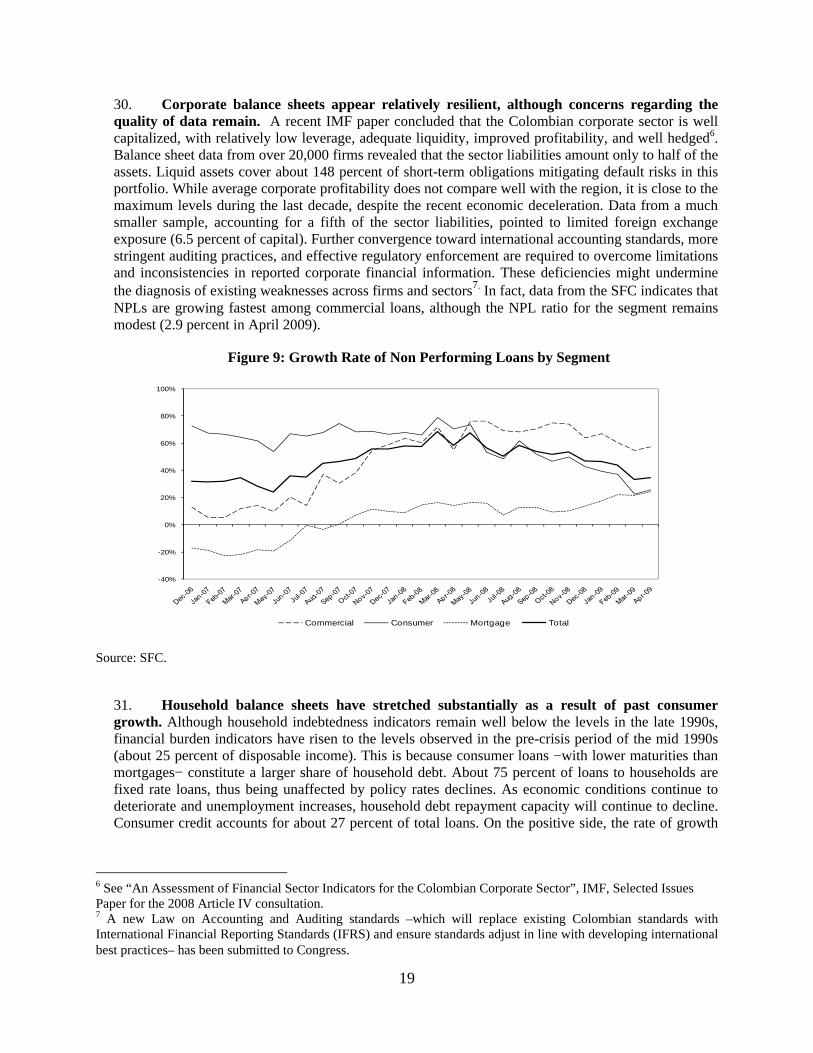

-20%

0%

20%

40%

60%

80%

100%

Commercial Consumer Mortgage Total

Source: SFC.

31. Household balance sheets have stretched substantially as a result of past consumer growth. Although household indebtedness indicators remain well below the levels in the late 1990s, financial burden indicators have risen to the levels observed in the pre-crisis period of the mid 1990s (about 25 percent of disposable income). This is because consumer loans −with lower maturities than mortgages− constitute a larger share of household debt. About 75 percent of loans to households are fixed rate loans, thus being unaffected by policy rates declines. As economic conditions continue to deteriorate and unemployment increases, household debt repayment capacity will continue to decline. Consumer credit accounts for about 27 percent of total loans. On the positive side, the rate of growth

6 See “An Assessment of Financial Sector Indicators for the Colombian Corporate Sector”, IMF, Selected Issues Paper for the 2008 Article IV consultation. 7 A new Law on Accounting and Auditing standards –which will replace existing Colombian standards with International Financial Reporting Standards (IFRS) and ensure standards adjust in line with developing international best practices– has been submitted to Congress.

20

of consumer NPLs has declined substantially as banks improved credit origination practices during 2007.

32. The financial sector can cover the GoC’s additional financing needs without crowding out private sector credit. Domestic financing requirements for the public sector deficit are expected to remain modest at about 4 percent of GDP (close to US$8.5 billion). In recent years, domestic issuance of Treasury bonds has been as high as 5.9 percent of GDP as external debt was substituted with domestic debt.

Main Financial Sector Risks

33. The deterioration of the loan portfolio in the event of a severe economic downturn poses the main risk to the financial system, although measures recently adopted by the SFC provide adequate buffers against such risk. The BdR periodically conducts stress tests using an error correction model to estimate the impact of changes in macroeconomic variables on delinquency rates for banks’ commercial, consumer and household portfolios. The impact on profits is then calculated taking into account the effect of additional provisions and declined interest income due to the higher delinquency. Tests are conducted over a 1-year horizon. The latest tests indicate that in case of a severe macroeconomic shock –similar to the one occurred during the financial crisis of the late 1990s– almost all banks in the system would incur losses amounting to COP$ 1.4 billion8. The SFC also conducts stress tests regularly to calibrate additional provisioning requirements. In the event of an increase in delinquency rates similar to those observed during the crisis, and given current exposures, credit institutions −including financial companies, cooperatives, and other specialized credit institutions− would have to increase provisions by about COP$ 2.2 billion over the next two years. Given concerns regarding the quality of the loan portfolio in the current uncertain macroeconomic environment, the SFC requested credit institutions to capitalize part of the 2008 utilities, a measure supported by this operation. As result of the measure, credit institutions constituted additional capital reserves of about COP$ 2.1 billion. This additional cushion would ensure a CAR level for the system above the 10 percent level during 2009-2010 even in case of severe economic contraction.

34. Market risk, although increasing, remains modest. Data from the SFC shows that banks’ market risk −measured according to a Value-at Risk model− increased by 50 percent from November 2008 to February 2009 (see Figure 10). The increment is mostly due to the increase in the holdings of government securities. The declining trend in the size of banks’ investment portfolio has recently reversed as economic perspectives deteriorated, risk aversion increased and inflation expectations moderated. The BdR reports that from August 2008 to February 2009, credit institutions increased their holdings of Treasury bonds by US$2.6 billion. However, market risk remains modest as a percentage of regulatory capital (4 percent) and below the levels at end-2006.

35. Colombian financial institutions continue to maintain adequate liquidity buffers although sustained credit growth in past years has increased banks liquidity risks. A new liquidity regulation, supported by this operation (see paragraph 74), establishes requirements for the management of liquidity risks and forces credit institutions to maintain liquid assets to cover liabilities potentially due within one week. Additionally, the BdR’s liquidity risk indicator –current liabilities minus liquid assets and tradable investments (with prices adjusted by a haircut)− reflects that liquid assets exceed liquid liabilities for all institutions. Nevertheless, liquidity buffers have declined due to past credit growth (from -25.0 percent at end-2005 to -5.8 percent at end-2008). Only a severe stress

8 The scenario considers a negative GDP growth of 6.8 percent, a 13.7 percent contraction in internal demand, a 4.2 percentage point increase in unemployment rates, a 450 b.p. increase in interest rates and an 8 percent decline in housing prices. The tests used information on exposures at end-2008.

21

scenario poses serious liquidity risks. In the event of a 12 percent withdrawal of deposits, institutions holding about 60 percent of total banking assets would have to recur to illiquid assets to met liquidity needs9.

Figure 10: Market Risk for Banks

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

Dec-06

Jan-07

Feb-

07

Mar

-07

Apr-0

7

May

-07

Jun-07

Jul-0

7

Aug-

07

Sep-

07

Oct-

07

Nov-07

Dec-07

Jan-08

Feb-

08

Mar

-08

Apr-0

8

May

-08

Jun-08

Jul-0

8

Aug-

08

Sep-

08

Oct-

08

Nov-08

Dec-08

Jan-09

Feb-

09

Millo

ns

of P

esos

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

Per

centa

ge

Market Risk Market Risk / Technical Net Worth

Source: SFC.

III. THE GOVERNMENT PROGRAM

36. The GoC’s general strategy is laid out in two documents: the National Development Plan and Visión Colombia 2019. In anticipation of Colombia’s bicentennial anniversary, the National Planning Department launched an initiative to develop a longer term vision for the country and a strategy to reach it. The process involved the development of a proposal, Visión Colombia II Centenario: 2019 - Propuesta para Discusión, followed by rounds of discussions with citizens and sub-national governments to refine the vision and generate national ownership. The process culminated in the elaboration of Visión Colombia 2019, a longer term policy planning document outlining objectives over the next fifteen years. The document considers several policy areas aiming to create an economic environment that guarantees greater levels of well-being. Visión Colombia 2019 and the National Development Program (NDP) 2002-2006 which was based on the results of a broad consultative process, constituted two of the main inputs for the formulation of the NDP 2006-2010: Estado Comunitario: Desarrollo para Todos. The plan lays out a comprehensive set of programs to implement in these four years and provides guidance for monitoring results and outcomes. The new NDP was formally adopted through Law 1151 of July 2007.

37. Both documents identify financial development as key for improving competitiveness to ensure high sustainable growth. High sustainable growth constitutes one of the five pillars of Visión Colombia 2019, which also include peace and security, promotion of equity, environmental sustainability and state reform to better serve citizens. The program recognized that developing a competitive business sector requires increasing financing to private sector companies. To do so, it

9 The 12 percent withdrawal rate corresponds to the average of the highest drop in deposits of each institution during the period 1994-2008

22

proposes to progressively deepen financial markets by raising the ratio of broad money to GDP from 40 percent to 80 percent by 2019. The ongoing securities market reform supported by this DPL constitutes an essential block in the strategy to achieve this objective, and the subsequent NDP 2006-2010 explicitly referred to this reform. The NDP also indentifies securities market reform as a priority to deepen Colombian financial markets in order to promote high sustainable growth. To promote savings and to channel those savings efficiently to fund private sector investment and foster growth, the NDP envisions a comprehensive reform of the securities market regulatory framework. The NDP specific objective with respect to securities market development is to increase market capitalization and the value of transactions to the average level in Latin America by 2019.

38. Capital markets have a relevant impact on the productivity of the corporate sector, through the provision of financing and risk management tools. Capital markets have a direct impact on the business sector, offering an alternative to bank debt financing (i.e. bond instruments) and owners’ capital contributions (i.e. equity instruments) as well as risk management instruments. Capital markets also have an indirect effect on business productivity, as the domestic public debt market and money market provide the basis for the effective pricing of corporate bonds.

39. As the global financial crisis erupted the authorities focused on mitigating the effects of the crisis to avoid economic recession and preserve social gains. In order to contain the effects of the crisis, the authorities adopted countercyclical monetary and fiscal policies and increased funding from multilaterals. In the financial sector area, the authorities focused on strengthening the financial sector so that financial instability would not amplify the impact of the shocks. To avoid dispersing government and regulators focus and efforts beyond controlling the impact of the crises, and to revise the mid-term strategy as necessary in light of developments, the draft Financial Reform Law was withdrawn from Congress and was reintroduced in May after including some amendments related to crisis management although unfortunately some of those amendments were not approved by Congress (see paragraph 52).

IV. FINANCIAL SECTOR REFORMS IN THE LAST DECADE AND THE AGENDA FOR FUTURE REFORMS

40. Strengthening the financial sector and developing capital markets have been at the core of the financial development agenda in the last decade. The reforms have resulted in a different financial landscape with a consolidated banking sector, more prudent supervision and regulations, and the development of a capital market. Following the 1999 banking crisis, recovery efforts included addressing insolvent state-owned banks –through privatization, liquidation or recapitalization–, and deleveraging risk in housing finance through securitization of the mortgage market. As the situation stabilized, focus shifted to revamping financial sector regulation and supervision in order to strengthen financial sector stability. In order to deepen financial intermediation and provide alternative and efficient sources of funding to corporations, the authorities launched a comprehensive securities market reform. The government efforts of the past 10 years have been extensively supported by the World Bank and other multilaterals through a number of operations including loans, technical assistance, analytical work and policy dialogue. This section summarizes some of the most important reforms undertaken in the last decade (see Annex 6 for details) as well as the most recent reform developments.

41. On the institutional side, a single financial supervisor was created in early 2006 to improve coordination, reduce the scope for regulatory arbitrage and strengthen overall financial regulation and supervision. Based on Decree 4327/2005, the banking, insurance and pension’s

23

supervisory agency (Superintendencia Bancaria) and the securities supervisory agency (Superintendencia de Valores) merged in January 2006 into an integrated financial supervisor (SFC). This merger was supported by the Second Programmatic Financial Sector Adjustment Loan (PFSAL II). Even though the technical and organizational challenges of integrating the two agencies were significant, the merger process proceeded smoothly. Market participants indicated that the objectives of the merger have been achieved to a large extent.

42. In addition to regulatory reforms and capital market development, substantial efforts have also been devoted to promote financial outreach and inclusion. A decree in 2006 established a public-private partnership trust fund, Banca de las Oportunidades. The goals of this trust fund were to increase access to finance to provide targeted financial education, as well as technical assistance for financial intermediaries, partial credit guarantees for micro credit institutions, and targeted subsidies. The Credit Information Law (Ley de Habeas Data) regulated the activities of the credit reporting industry to improve the legal framework underpinning the supply of credit. Correspondent banking arrangements, which refer to bank partnerships with typically non-bank commercial outlets in order to provide a range of banking services through them, were allowed and regulated in order to expand access to banking services. All these reforms were supported by the Business Productivity and Efficiency DPL programmatic series. The introduction of differentiated interest rate ceilings for micro loans has allowed the expansion of credit. However, interest rate caps on mortgages continue to hamper the access to credit to low income households and banks cannot fully charge for the risks associated to lending to this segment. A program of housing subsidies aimed to facilitate access to finance was introduced, although the subsidies are poorly targeted and also benefit upper-income households.

43. Financial sector supervision and regulation has been substantially strengthened in the last decade. The Financial Reform law of 1999 was instrumental in facilitating the resolution of troubled institutions and in upgrading regulation. Supervision now covers all financial institutions on a consistent basis, using on-site examination and off-site monitoring. The Financial Reform Law of 2003 further upgraded the regulatory framework as well as the banking resolution procedures. Financial supervision has been revamped, with a movement towards a risk-based supervision framework. Among the new regulations, financial institutions have been obliged to adopt, where applicable, internal systems to manage credit, market, and more recently liquidity and operational risks. Such systems comprise policies, procedures and a corporate governance structure to deal with each type of risk − including internal limits, remedial actions, and contingency plans− as well as a framework to measure each particular risk.

44. Already prior to the global financial crisis, Colombia introduced countercyclical provision regulations in line with recent recommendations by the G-20. Under the new regulations, lending institutions constitute additional specific provisions in the boom part of the cycle that can be used to compensate for higher expenses due to increased provisioning during the downturn. At present, the SFC instructs each year whether the institutions need to provision in excess or below expected losses. In 2007 and 2008, the SFC instructed institutions to constitute the countercyclical provision according to the difference between two transition matrices (one with through-the-cycle probabilities of default and other with probabilities of default based on more recent observations) provided in the norm. The countercyclical provisions for commercial loans entered into effect in July 2007, while the countercyclical provisions for consumer loans entered into effect in July 2008. As of end-March 2009, countercyclical provisions reached US$800 million. Currently, the SFC is contemplating the possibility of allowing credit institutions to accumulate or deplete countercyclical provisions according to their delinquency experiences and financial strength. The main drawback of the scheme is that the specific nature of the provisions limits the flexibility for reallocation among

24

delinquent loans and raises tax issues. The reform proposal aims at addressing these issues but in the future, the adoption of a generic countercyclical provision should be considered10.

45. As the global crisis erupted, the authorities took measures to increase their preparedness against an eventual emergency. In 2008, the financial supervisory authorities conducted a crisis simulation exercise designed and executed with the assistance of World Bank staff to test the framework for resolution, largely introduced after the 1999 crisis and therefore untested. The exercise pointed out the need for greater clarity in the sequencing of actions and responsibilities of the different institutions involved in the process. In light of the experience, the authorities have requested funding from FIRST to finance technical assistance to draft internal protocols to clarify resolution procedures. The Financial Surveillance Committee −including representatives of the SFC, the Ministry of Finance (Ministerio de Hacienda y Crédito Público, MHCP), the BdR and FOGAFIN− has intensified its activities to coordinate actions across agencies involved in financial sector stability issues and develop contingency plans.

46. To further strengthen the deposit insurance scheme, the copayment was eliminated in early 2008. FOGAFIN guarantees deposits and certificates of deposit issued by credit institutions up to about US$10,000 per person per institution11. This limit covers 98.5 percent of depositors and 20 percent of total deposits. The institutions pay a risk-adjusted insurance premium. Currently, funds cover about 5 percent of total deposits. To increase confidence in the system, the copayment by depositors was eliminated in early 2009, in line with IMF recommendations12. To further strengthen the framework, consideration should be given to extend the premium to all debt liabilities and to better publicize the existence of the fund. FOGAFIN has recently launched a revision of the available tools to facilitate the resolution of insolvent institutions and to ensure prompt repayment of depositors.