document of the world bank habib bank limited ... financial inclusion in pakistan ... figure 1....

TRANSCRIPT

Document of The World Bank

FOR OFFICIAL USE ONLY

Report No. 96376-PK

INTERNATIONAL DEVELOPMENT ASSOCIATION

PROGRAM DOCUMENT FOR A PROPOSED

CREDIT

IN THE AMOUNT OF SDR 355.6 MILLION

(US$ 500 MILLION EQUIVALENT)

TO

ISLAMIC REPUBLIC OF PAKISTAN

FOR THE

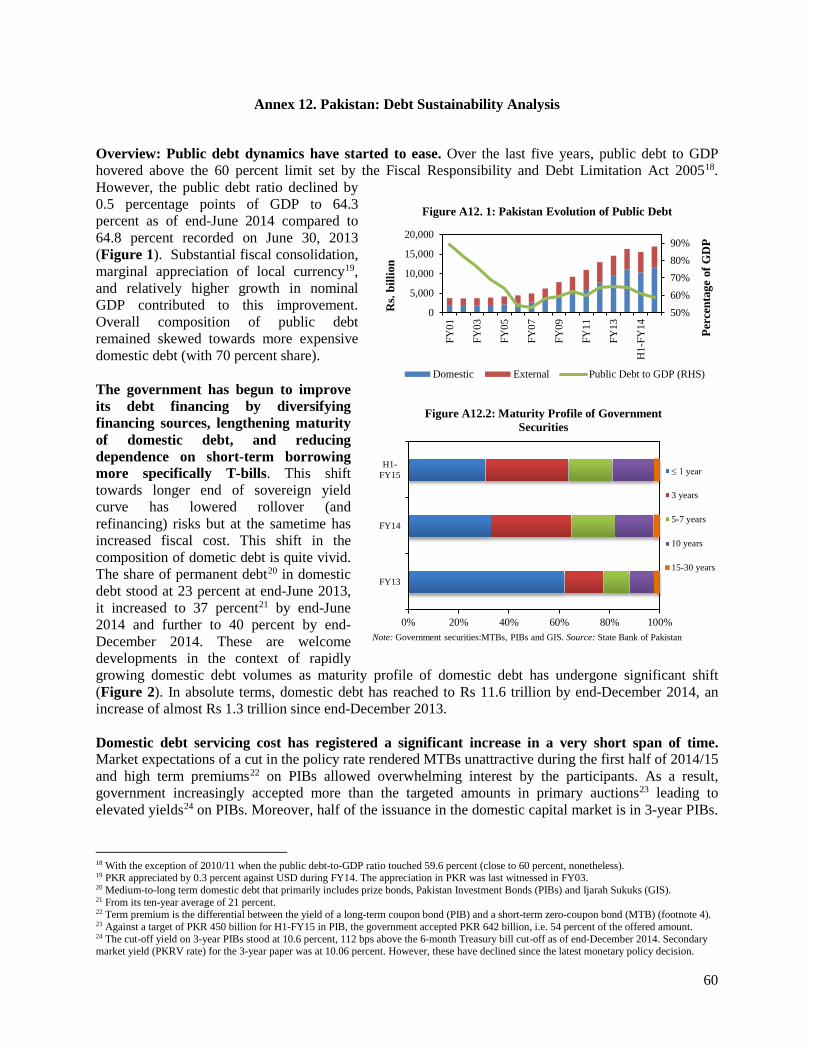

SECOND FISCALLY SUSTAINABLE AND INCLUSIVE GROWTH

DEVELOPMENT POLICY CREDIT

May 21, 2015

Macroeconomic and Fiscal Management South Asia Region

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

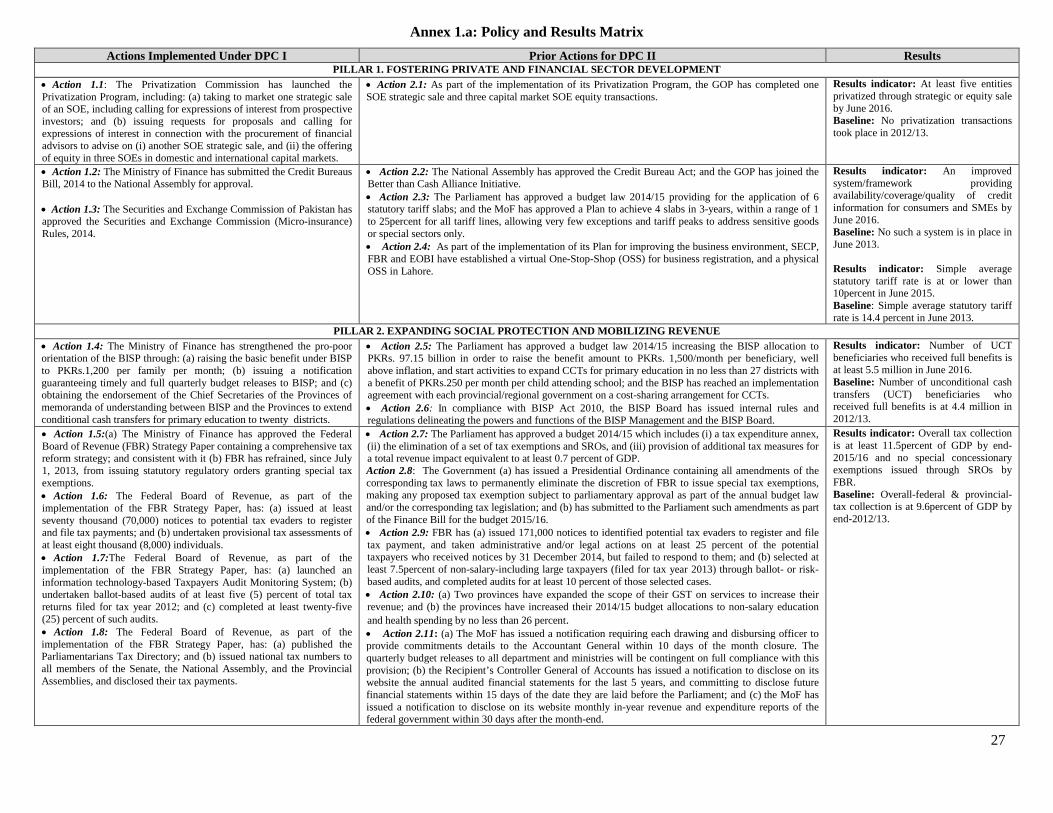

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

GOVERNMENT OF PAKISTAN FISCAL YEAR July 1–June 30

CURRENCY EQUIVALENTS (Exchange Rate Effective as of April 30, 2015)

Currency Unit: Pakistani Rupees US$1.00 = PKRs 101.69 SDR 1.00 = US$1.40642

ABBREVIATIONS AND ACRONYMS ADB Asian Development Bank ABL AML

Allied Bank Limited Anti-Money Laundering

BISP Benazir Income Support Program BOI Board of Investment BOP Balance of Payments BTCA Better Than Cash Alliance CT Cash Transfer CCI Council of Common Interest CCOP Cabinet Committee on Privatization CCT Conditional Cash Transfer CEM Country Economic Memorandum CFT Counter-Terrorist Financing CIB Credit Information Bureau CNI Computerized National Identity CPS Country Partnership Strategy DB Doing Business DFID Department for International Development DPC Development Policy Credit EDB Engineering Development Board EFF Extended Financing Facility EOBI Employees’ Old-Age Benefits Institution EMBI+ Emerging Market Bonds Index Plus EOI Expression of Interest EU European Union FA Financial Advisor FATF Financial Actions Task Force FBR Federal Board of Revenue FDI Foreign Direct Investment FECR Fiscal Electronic Cash Register FESCO Faisalabad Electric Supply Co. FRDLA FSIG

Fiscal Responsibility and Debt Limitation Act Fiscally Sustainable and Inclusive Growth

GDP Gross Domestic Product GCC Gulf Cooperation Countries GIS Geographic Information System GOP Government of Pakistan GPS Global Positioning System GSP Generalized System of Preferences GST General Sales Tax HBL Habib Bank Limited HEC Heavy Electrical Complex HS Harmonized System IBRD International Bank for Reconstruction and Development ICT Information and Communication Technology IDA International Development Association IEG Independent Evaluation Group IESCO Islamabad Electric Supply Co. IFC International Finance Corporation IMF International Monetary Fund IPO Initial Public Offering ITAMS Integrated Tax Audit Mgment. System JICA Japan International Cooperation Agency

KESC LESCO

Karachi Electric Supply Co. Lahore Electric Supply Co.

LLCs Limited Liability Companies LLP Limited Liability Partnership LRO Local Registration Office LSM Large Scale Manufacturing MFN Most Favored Nation MOC Ministry of Commerce MoF Ministry of Finance MOU Memorandum of Understanding MTB Market Treasury Bill NDA New Domestic Asset NEPRA National Electric Power Regulatory Authority NFA Net Foreign Asset NFC National Finance Commission NFIS National Financial Inclusion Strategy NISP National Income Support Program NPCC Natl. Power Construction Corporation NPGCL Northern Power Generation Company Limited NPL Non-Performing Loan NSS National Savings Scheme NTN National Tax Number OGDCL Oil & Gas Development Co. Ltd. OSS One Stop Shop PC Privatization Commission PBM Pakistan Bait-ul-Mal PDF Pakistan Development Fund PEFA Public Expenditure and Financial Accountability PIA Pakistan International Airlines PIB Pakistan Investment Bond PFM Public Financial Management PML-N Pakistan Muslim League-Nawaz PPG Public & Private Guarantee PAR Pakistan Arab Refinery PIA Pakistan International Airlines PPL Pakistan Petroleum Limited PPRA Public Procurement Regulatory Authority PSE Public Sector Enterprise PSM Pakistan Steel Mills REER Real Effective Exchange Rate RFP Requests for Proposals RRG Regional Review Group SB Structural Benchmark SBP State Bank of Pakistan SECP Securities & Exchange Commission of Pakistan SEZ Special Economic Zone SME Small and Medium Enterprise SOE State Owned Enterprise SRO Statutory Regulatory Order SST Services Sales Tax TA Technical Assistance TAMS TDS

Tax Audit Management System Tariff Differential Subsidies

Vice President: Annette Dixon

Country Director: Rachid Benmessaoud

Practice Director: Satu K. Kahkonen

Practice Manager: Shubham Chaudhuri Task Team Leader: Jose López-Cálix

THE ISLAMIC REPUBLIC OF PAKISTAN

A PROGRAMMATIC DEVELOPMENT POLICY SERIES FOR A

SECOND FISCALLY SUSTAINABLE AND INCLUSIVE GROWTH DEVELOPMENT POLICY CREDIT

1.INTRODUCTION AND COUNTRY CONTEXT .................................................................................... 1 2.MACROECONOMIC POLICY FRAMEWORK ..................................................................................... 3

2.1. Recent Economic Developments ....................................................................................................... 3 2.2. Macroeconomic Outlook ................................................................................................................... 5 2.3. IMF Relations .................................................................................................................................... 9

3. GOVERNMENT’S PROGRAM ............................................................................................................ 10 4. THE PROPOSED OPERATION ............................................................................................................ 10

4.1. Link to Government Program and Operations Description ............................................................. 10 4.2. Prior Actions, Results and Analytical Underpinnings ..................................................................... 12 4.3. Link to Country Assistance Strategy and Other Bank Operations ................................................... 18 4.4. Consultations and Collaboration with Development Partners ......................................................... 18

5. OTHER DESIGN AND APPRAISAL ISSUES ..................................................................................... 20 5.1. Poverty and Social Impact ............................................................................................................... 20 5.2. Environmental Aspects .................................................................................................................... 22 5.3. Public Financial Management, Disbursement and Auditing Aspects .............................................. 23 5.4 Monitoring, Evaluation and Accountability ...................................................................................... 24

6. SUMMARY OF RISKS ......................................................................................................................... 25 Annex 1.a: Policy And Results Matrix ....................................................................................................... 27 Annex 1.b: DPC-II Comparing Original Indicative Triggers And Prior Actions ....................................... 28 Annex 2. Letter of Development Policy ..................................................................................................... 29 Annex 3. Fund Relations Annex ................................................................................................................. 39 Annex 4. Expanding the Scope Of the Safety Net Is Important For The Poor ........................................... 40 Annex 5. Privatization in Pakistan .............................................................................................................. 42 Annex 6. Tariff Simplification and SROs Trade Distortions ...................................................................... 44 Annex 7. Establishing a One-Stop Shop for business Registration in Pakistan .......................................... 49 Annex 8. Doing Business Indicators for Pakistan ....................................................................................... 51 Annex 9. Financial Inclusion in Pakistan .................................................................................................... 52 Annex 10. Creation of Fiscal Space Through Revenue Mobilization ........................................................ 54 Annex 11: Increasing Provincial Revenue for More Social Spending ....................................................... 58 Annex 12. Pakistan: Debt Sustainability Analysis ...................................................................................... 60 Annex 13. Public Financial Management and Procurement ....................................................................... 64 Annex 14. Analytical and Advisory Activities: Major Findings and Recommendations .......................... 66 Annex 15. Country at a Glance ................................................................................................................... 68 LIST OF TABLES: Table 1: Key Macroeconomic Indicators Pakistan FY10/11 to FY18/19 ..................................................... 6 Table 2: Key Fiscal Indicators Pakistan FY11/12 to FY18/19 ..................................................................... 7 Table 3:Pakistan BOP Financing Requirements and Sources FY11/12 to FY15/16 .................................... 9 Table 4: Overall Fiscal Impact under FSIGs and Power DPCs-Actions in years FY13/14 & FY14/15 ..... 17 Table 5: FSIG-II Prior Actions and Analytical Underpinnings .................................................................. 19 Table 6: SORT: Risk Categories ................................................................................................................. 26

ii

Table A4.1: BISP Financial Execution Performance .................................................................................. 40 Table A6. 1. Published Statutory Duty Rates, FY2002/03 to FY2014/15 .................................................. 47 Table A6. 2. Statistics of Statutory Duty Rates, FY2002/03 to FY2014/15 ............................................... 47 Table A6.3: Number of Tariff Lines by Type of Goods and Statutory (MFN) Rate, FY2012/13 .............. 48 Table A6.4. Major General and Sector Specific SROs, FY13/14 (Rs. Billion) .......................................... 48 Table A7. 1: Broad Timeline of Medium Term Implementation Plan........................................................ 50 Table A11.1: Key Features of Provincial Services Sales Tax .................................................................... 59 Table A11.2: Non-Salary Budget Allocations for Education and Health Sectors (Rs. Million), 2013/14 - 2014/15…………………………………………………………………………………………………….59 Table A12.1: DSA: Base case debt projections .......................................................................................... 61 Table A12.2: Key Economic Indicators: Low-Case Scenario .................................................................... 63 LIST OF FIGURES:

Figure 1. Pakistan Debt Sustainability Analysis FY09/10 to FY18/19 ........................................................ 9 Figure A4. 1. Targeting Performance of Federal Social Programs in Pakistan (percent) ........................... 40 Figure A8.1: South Asia DB Rankings 2015 .............................................................................................. 51 Figure A8.2: Pakistan DB Rankings 2015 .................................................................................................. 51 Figure A10. 1. Sequencing of Follow-up Actions in Registering Potential Taxpayers .............................. 55 Figure A11.1: Sectoral Shares in Total Services Sales Tax Collection (percent of total) .......................... 58 Figure A12. 1: Pakistan Evolution of Public Debt ………………………………………………………..60 Figure A12.2: Maturity Profile of Government Securities ……………………………………………….60 Figure A12.3: Bank and Non-Bank Holdings of Pakistan Investment Bonds…...……………………….61 Figure A12.4: Public Debt Sustainability Analysis……………………………………………………….62 LIST OF BOXES

Box 1. Key Economic Priorities of the Government’s Program ................................................................. 11

Box 2. The Impact of BISP Cash Transfers on Women’s Accountability and Education .......................... 21

The Credit is prepared by an International Development Association team consisting of Jose R. Lopez-Calix (Lead Country Economist and Task Team Leader, GMFDR); Gabi George Afram (Practice Leader, GTCDR); Shubham Chaudhuri and Vinaya Swaroop (Practice Managers, GMFDR), Anthony Cholst (Country Program Coordinator, SACAA); Daria Taglioni (Senior Trade Economist, (GTCDR); Paul Welton (Senior Financial Management Specialist GGODR); Qurat Hadi (Financial Management Specialist, GGODR) Hanid Mukhtar (Senior Economist, GMFDR);Yasuhiko Matsuda (Senior Public Sector Specialist, GSPDR); David L. Newhouse (Senior Economist, GPVDR);Muhammad Waheed (Economist, GMFDR); Guillermo Arenas (Consultant, GTCDR);Saadia Refaqat (Economist, GMFDR);Kiran Afzal (Private Sector Development Specialist, GTCDR), Rehan Hyder (Senior Procurement Specialist, GGODR);Amjad Zafar Khan, Social Protection Specialist, GSPDR), Iftikhar Malik (Senior Social Protection Specialist, (GSPDR), Quanita Ali Khan (Specialist, GSPDR), Aijaz Ahmad (Senior Public Private Partnership Specialist, (GCPDR), Irum Touqeer (Consultant, GGODR); Sarmad Ahmed Shaikh (Consultant, GTCDR); Mehwish Ashraf (Research Analyst, GMFDR); Helene Bertaud (Legal Counsel); Michael Goldberg, (Operations Adviser, GPSOS); Chau-Ching Shen (Finance Officer); Anwar Ali Bhatti (Financial Specialist), Shabnam Naz (Program Assistant, SACPK); Muhammad Shafiq (Program Assistant, GMFDR) and Ehtesham-ul Haq (Program Assistant, SACPK). The team is particularly grateful to Pablo Saavedra, Economic Adviser and Manuela Francisco, Economic Adviser (OPSPQ), Markus Kitzmuller, Economist, (SARCE), Manuela Ferro (Director, LCRVP), Peter Mousley (Program Leader, MNCO2), and Martin Melecky, Lead Economist (SARCE) who provided priceless comments and guidance.

iii

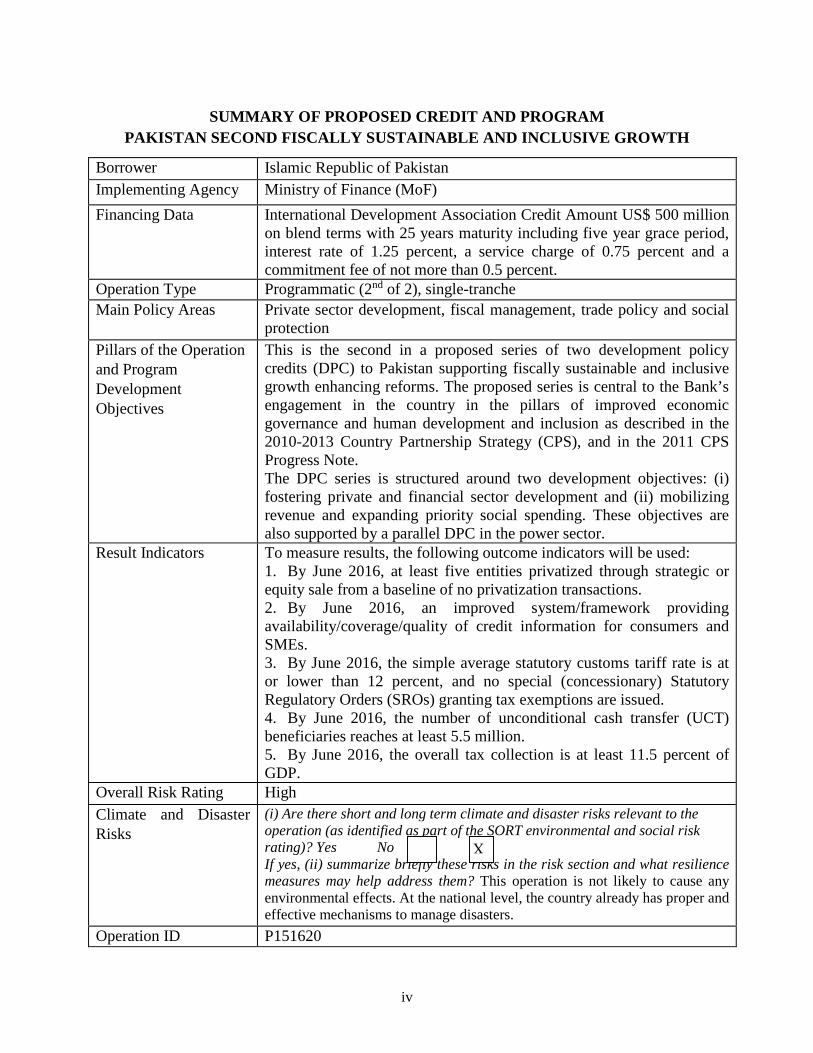

SUMMARY OF PROPOSED CREDIT AND PROGRAM

PAKISTAN SECOND FISCALLY SUSTAINABLE AND INCLUSIVE GROWTH

Borrower Islamic Republic of Pakistan Implementing Agency Ministry of Finance (MoF)

Financing Data International Development Association Credit Amount US$ 500 million on blend terms with 25 years maturity including five year grace period, interest rate of 1.25 percent, a service charge of 0.75 percent and a commitment fee of not more than 0.5 percent.

Operation Type Programmatic (2nd of 2), single-tranche Main Policy Areas

Private sector development, fiscal management, trade policy and social protection

Pillars of the Operation and Program Development Objectives

This is the second in a proposed series of two development policy credits (DPC) to Pakistan supporting fiscally sustainable and inclusive growth enhancing reforms. The proposed series is central to the Bank’s engagement in the country in the pillars of improved economic governance and human development and inclusion as described in the 2010-2013 Country Partnership Strategy (CPS), and in the 2011 CPS Progress Note. The DPC series is structured around two development objectives: (i) fostering private and financial sector development and (ii) mobilizing revenue and expanding priority social spending. These objectives are also supported by a parallel DPC in the power sector.

Result Indicators

To measure results, the following outcome indicators will be used: 1. By June 2016, at least five entities privatized through strategic or equity sale from a baseline of no privatization transactions. 2. By June 2016, an improved system/framework providing availability/coverage/quality of credit information for consumers and SMEs. 3. By June 2016, the simple average statutory customs tariff rate is at or lower than 12 percent, and no special (concessionary) Statutory Regulatory Orders (SROs) granting tax exemptions are issued. 4. By June 2016, the number of unconditional cash transfer (UCT) beneficiaries reaches at least 5.5 million. 5. By June 2016, the overall tax collection is at least 11.5 percent of GDP.

Overall Risk Rating High

Climate and Disaster Risks

(i) Are there short and long term climate and disaster risks relevant to the operation (as identified as part of the SORT environmental and social risk rating)? Yes No If yes, (ii) summarize briefly these risks in the risk section and what resilience measures may help address them? This operation is not likely to cause any environmental effects. At the national level, the country already has proper and effective mechanisms to manage disasters.

Operation ID P151620

X

iv

INTERNATIONAL DEVELOPMENT ASSOCIATION PROGRAM DOCUMENT FOR A PROPOSED CREDIT TO THE ISLAMIC REPUBLIC OF PAKISTAN

1. INTRODUCTION AND COUNTRY CONTEXT

1. This memorandum describes the second Fiscally Sustainable and Inclusive Growth (FSIG-II) single-tranche reform credit for US$500 million to the Islamic Republic of Pakistan. The proposed loan will be the second of a programmatic series of loans. The FSIG series has two broad objectives: fostering private and financial sector development to bolster economic growth, and mobilizing revenue while expanding fiscal space to priority social needs. The operation contributes to the government’s strategy for accelerating economic growth, ensuring fiscal consolidation, increasing investment, and enhancing the openness of the economy to domestic and external competition. A programmatic approach is proposed to customize actions and preserve reform momentum. Moreover, lessons from other similar operations in Pakistan favor a carefully sequenced and continuous reform approach.

2. Going into the May 2013 elections, Pakistan was in a near-crisis economic situation. Unprecedented floods in 2010 and 2011, coupled with continuing security issues, stalling economic reform, falling investment and external financial inflows, increased devolution of responsibilities to the provinces, and fiscal disarray preceding the elections posed critical challenges that severely affected two major macroeconomic imbalances: by the end of the 2012/13 international reserves were around 1.5 months of imports, and the fiscal deficit (excluding grants) reached 8.3 percent of gross domestic product (GDP), a very high level for the third year in a row. Weak fundamentals had the economy bordering on stagflation.

3. The first peaceful transition from one democratically elected government to another in Pakistani history gave the incoming administration a solid reform mandate. On May 11, 2013, 86.2 million registered Pakistanis cast their vote. The results favored the Pakistan Muslim League–Nawaz (PML-N) with a majority of seats. At the provincial level PML-N retained its mandate to govern Punjab. Two opposition parties won mandates as well: Pakistan Tehreek-e-Insaf emerged as the largest party in Khyber Pakhtunkhwa provincial assembly, while the Pakistan People’s Party managed to stay the largest political force in Sindh provincial assembly.

4. Within months of taking office, the new government framed a program of reforms and successfully negotiated an Extended Fund Facility (EFF) with the International Monetary Fund (IMF). Approved in September 2013, the Government’s program articulated an ambitious emergency response to prevent a balance-of-payments crisis, correct fiscal imbalances and put the economy on the road to stabilization and rapid growth recovery. It also contains a growth-oriented agenda focused on the major constraints to growth—energy supply, poor investment climate and low competitiveness.

5. After a year of successful program implementation, domestic shocks—political, natural disaster-related and security-related—hit the economy, affecting the pace of reforms in the second half of 2014. Political conditions started deteriorating in August 2014, due to street sit-ins followed by lengthy demonstrations nationwide until December. Concurrently, floods hit central Punjab in September and damaged some of the major agricultural crops (sugar, rice and cotton). And then in December 2014, security conditions deteriorated with the attack of the Pakistan Taliban on a school in Peshawar. The direct

1

economic impact of these shocks was, fortunately, small and of short-lived. Because of heightened political uncertainty, the rupee depreciated, forcing the State Bank of Pakistan (SBP) to intervene. A few investment decisions were postponed and growth was affected by the paralysis of government services for a few weeks. Government estimates of the floods damage and the cost of added security were also small (each about 0.2 percent of GDP). But, by preoccupying the government, the shocks did slow down the pace of reforms in three areas: power tariff adjustments, privatization and passing of laws. Hence, the measures supported by this operation and the Power Sector Reform DPC aim to reinvigorate reforms implementation.

6. One reason for the limited economic impact of the domestic shocks was the concurrent fall in global oil prices, which came as a windfall for a net oil-importer economy like Pakistan, and opened an opportunity to accelerate structural reforms. The price of crude oil plummeted from about $105 per barrel in June 2014 to around $50 per barrel by December 2014. Since about one-third of Pakistan’s import payments are for crude oil and petroleum products, a 50 percent average decline in prices reduces the annual import bill by about $3 billion, equivalent to about 1 percent of GDP. Besides the direct deflationary and growth effects on the economy of low oil prices, this windfall has provided an opportunity, which the Government has taken an advantage of, to adjust further electricity tariffs that will bring fiscal gains from lower energy subsidies, while also allowing for some fall in consumer tariffs, and saving foreign reserves.1 This has brought back momentum for growth and reforms.

7. The FSIG series fosters inclusion not only through its direct growth impact but also its indirect effects on poverty reduction and shared prosperity. The most recent poverty assessment on Pakistan finds economic growth as the main determinant of poverty reduction and improved shared prosperity. Despite falling and increasingly volatile but positive per capita growth, poverty declined over the last decade in Pakistan. The share of the population below the national poverty line fell from 34.7 percent in 2001/02 to an officially estimated 12.4 percent in 2010/2011 (the latest available poverty data). Real per capita consumption of the bottom 40 percent of the population—a measure of shared prosperity—also exceeded that of the top 60 percent in the same period. BISP cash transfers were an important contributor to the volatile and low but positive rise in income per capita during the period. Analysis also shows that growth has been broadly inclusive, with the national Gini coefficient falling from 0.34 to 0.29 between 1998/99 and 2010/11. This operation supports inclusive growth through several channels. First, by supporting measures to foster private investment, the operation aims to contribute to the creation of more and better jobs. Second, the measures to support financial inclusion among the most vulnerable, should, by raising their access to credit, increase household incomes and consumption. Third, the measures to create fiscal space and reallocate expenditures to priority education and health provincial outlays should contribute to the creation of human capital and increased access to opportunity for the poorest segments of the populations. Fourth, by eliminating tax-exemption privileges, the operation fosters tax equity. And fifth, the measures increase the volume of unconditional cash transfers efficiently targeted to the poor and vulnerable to protect them from volatile growth and frequent natural disasters; and conditional cash transfers to support access by poor children to primary school and, more broadly, build the human capital assets of the poor.

1 The Government implemented a surcharge of PRs0.30/kWh in October 2014 and an additional PRs0.60/kWh in January, and started applying a new FY14/15 uniform electricity tariff including additional production and distribution costs.

2

2. MACROECONOMIC POLICY FRAMEWORK

2.1. Recent Economic Developments

8. Economic conditions have improved over the past twenty one months. The risk of a balance of payments crisis has receded with a significant increase in international reserves resulting from strong remittances, foreign capital inflows and the windfall from lower oil prices. The current account deficit was a modest 0.7 percent of GDP in the first nine months of FY14/15. The foreign exchange market has been stable. Headline inflation reduced to 2.1 percent Y-o-Y up to March 2015. The fiscal deficit was contained at around 5.5 percent of GDP in FY13/14 due to improved tax collection, high non-tax revenues, and restricted expenditures. Private sector credit has also rebounded and supported growth. Non-performing loans continue to decline. The adverse political and security events and floods of the first semester of FY14/15 were offset by the positive effects of the decline in oil prices.

9. Growth has maintained its upward momentum, but remains below required levels needed to accelerate job creation and improve living standards. The industrial sector, accounting for 21 percent of GDP, grew by about 4 percent based on construction, electricity generation, gas distribution and large scale manufacturing (LSM). The services sector, comprising 53 percent of GDP performed well, particularly in wholesale and retail trade and in transport, storage and communication. Growth in FY14/15 has been broad-based, driven by agriculture and services and, to a lesser extent, by manufacturing.

10. There is less risk of a balance of payments crisis. Official foreign exchange reserves reached US$11.1 billion in February 2015, equivalent to 2.6 months of next year’s imports, and well above the low of US$3.0 billion in November 2013. The current account deficit remains small at around 1.2 percent of GDP due to growing workers’ remittances, steady receipts from the Coalition Support Fund and a reduced oil import bill. The chronically negative trade balance persists and was 6.7 percent of GDP in FY13/14. The capital and financial account benefitted from steady disbursements from general government loans and receipts in FY13/14 of: US$1.5 billion from Pakistan Development Fund (PDF); US$2 billion from Eurobond issues; US$0.5 billion from privatization proceeds. In another sign of restoring investors’ confidence, US$1 billion was received from Sukuk bond issues in the first half of FY14/15; and FDI flows more than doubled to US$1.8 billion during July-March 2015 with respect to US$0.8 billion in the same period of previous year. The country is now on track to build a reserve buffer well around 4 months of imports. However, this goal remains potentially vulnerable to a downturn in remittances from Gulf Cooperation Countries (GCC), reduced external demand for Pakistani exports, any decline in external support, and lower FDI inflows especially if proceeds from the privatization program do not materialize as expected.

11. Reserves build up caused the Rupee to appreciate in 2013/14 in real terms, but it has mildly depreciated since. A 7.8 percent appreciation of the Real Effective Exchange Rate (REER) in FY13/14 reduced export competitiveness, with exports growing at 1.4 percent compared with import growth of 3.9 percent. Exports were mainly driven by traditional textile products, petroleum products and rice. Imports were driven by domestic production inputs: machinery for power generation, textiles and construction grew by about 26 percent. During the first half of FY14/15, however, the Rupee depreciated by 3.3 percent in real terms, due to political uncertainty, slowing of economic reforms, and the failed placement of Oil and Gas

3

Development Company Limited (OGDCL) shares.

12. Strong fiscal consolidation has corrected the previously loose fiscal stance and improved sustainability, but important challenges remain. During FY13/14, the fiscal deficit (excluding grants) declined from 8.3 percent to 5.5 percent of GDP: revenue increased by 1.2 percent of GDP and expenditures decreased by 1.7 percent of GDP. Spending on subsidies fell slightly from 1.4 to 1.2 percent of GDP. The provinces contributed with a fiscal surplus of 0.6 percent of GDP. Based on the first half of FY14/15, the government is on track to achieve a target fiscal deficit of 4.9 percent of GDP, thanks to new tax measures equivalent to about 0.9 percent of GDP and reduced electricity subsidies. However, falling international oil prices and legal challenges to one important source of revenue, the Gas Infrastructure Development Cess, dampened tax efforts. In addition, the accumulation of circular debt in the power sector remained as a fiscal liability. In February 2015 the government took measures to raise an additional 0.4 percent of GDP, including raising the General Sales Tax (GST) rate on petroleum products from 17.5 percent to 27.5 percent and imposing regulatory duties on some luxury items.

13. Public debt sustainability is starting to improve. The public debt to GDP ratio decreased to 64.3 percent in FY13/14, but it remains above the 60 percent limit stipulated in the Fiscal Responsibility and Debt Limitation Act (FRDLA) 2005.2 Although more expensive domestic debt, at 67 percent of the total, skews the overall debt composition, the last year has seen a move to longer maturities. Recent Eurobond and Sukuk issues, lending from multilaterals and privatization proceeds have allowed the government to reduce its short term borrowing needs from the central and domestic banks and repay expensive domestic debt. As of end-December 2014, total public debt had declined by about 1 percent of GDP compared with the year before, mainly because of an equivalent reduction in its foreign currency component.

14. Private sector credit growth has rebounded despite monetary tightening. Lower demand by the government gave space to the private sector to increase its borrowing from the commercial banking system by 11.2 percent in FY13/14, the highest rate in the past six years.

15. Prices have stabilized due to fiscal consolidation, monetary tightening and low oil prices. For a third year in a row, headline CPI inflation is in single digits. In March 2015 it was 2.5 percent, although core inflation stood at 5.9 percent. Year-on-year, food inflation declined to 3.0 percent. Falling oil prices have not only contributed directly through reductions in petroleum product prices and electricity tariffs but also indirectly through reduced service and manufacturing costs.

16. Financial sector developments are also supporting recovery. To foster private sector credit, the State Bank of Pakistan (SBP) cut its key policy rate by 100 basis points (bps) to 8.5 percent in January 2015, and by a further 50 bps to 8 percent in March, 2015, owing to favorable trends in oil prices and falling inflation. To anchor inflation expectation and improve liquidity management, the central bank also announced a time-bound plan to set the policy rate between the floor and ceiling rates of the interest rate corridor in a forward looking fashion, thus maintaining real interest rates positive and in line with future reserves accumulation and a stable

2 The FRDLA allows a departure from the threshold provided the Finance Minister specifies the reasons and the measures government intends to take to return below the threshold over an estimated period of time [Section 3 (4) of the FRDLA 2005].

4

inflation path. The banking sector has maintained an improved performance and solvency. Year on year banking profitability improved, growing by 52 percent up to December 2014. Non-performing loans (NPLs) declined to 12.3 percent of the overall loan portfolio in December 2014 and by virtue of adequate provisioning, net NPLs were 2.7 percent. The provisions to NPLs coverage ratio increased to 80 percent. The improvement in credit quality is broad based, as NPLs across SMEs, agriculture and consumer sectors decreased from 32.3 percent, 14 percent and 13.6 percent in December 2013 to 30 percent, 12.4 percent, and 11.6 percent respectively in December 2014.

17. Country risk perception is improving. Pakistan’s Emerging Market Bonds Index Plus (EMBI+) risk spread has declined from its peak in March 2013 of 1,011 bps to 461 bps in April 2015. Also, Moody’s changed the outlook on its low Caa1 sovereign credit rating from stable to positive in March 2015. Market confidence allowed Pakistan to raise $2 billion in May 2014 through two dollar-denominated Eurobonds with bullet maturities and coupons of five years and 7.25 percent and ten years and 8.25 percent, implying a spread of about 460-560 basis points over US Treasuries. More recently, the government issued a US$1 billion five-year international Sukuk in November 2014 at 6.75 percent.

2.2. Macroeconomic Outlook

18. The outlook for FY14/15 to FY18/19 is for moderately higher economic growth. As the stabilization of the economy is preserved and the country builds a comfortable cushion in its external reserve position, this assumes steady progress in implementing the key pillars of the Government’s medium term program (Box 1), which preserves the growth momentum, but at moderate levels. Each of those pillars tackles the key constraints to growth: electricity load shedding, poor service delivery by inefficient and fiscal losses-prone State Owned-Enterprises (SOEs), a non-competitive trade regime, a cumbersome business environment, low access to finance, and poor revenue mobilization that constrains the fiscal space. The outlook also assumes that the windfall gains of low oil prices reduce gradually over the next 2-3 years and that political and security risks are well-managed.

19. Growth will be driven by a mix of consumption recovery on the demand side and by productivity gains in the services and large-scale manufacturing sectors on the supply side. Demand side drivers are expected to be low oil prices, strong but declining remittances, reinvigorated private investment, some export growth and, to a lesser extent, public investment. The supply side drivers are expected to be productivity gains in the services and large-scale manufacturing sectors, which should benefit from decreased power load-shedding and improvements in the business climate and public sector enterprises. Stable or declining international commodity prices are expected to help reduce inflationary pressures, lower interest rates and favor consumption. Aided by a gradually improving security situation, structural reforms are expected to spearhead productivity growth, reduce the country risk, promote foreign and domestic investment linked to the sale or restructuring of state-owned enterprises (SOE) and foster competition in the banking, telecom and commercial service sectors.

20. As inflation falls, monetary tightening should lessen and support growth. Fiscal consolidation is expected to reduce government’s borrowing needs and create some fiscal space for public investment while reducing public debt. Scheduled banks’ liquidity is in turn expected to increase. As a result, crowding out of private sector credit should decline, favoring private

5

investment. Successful fiscal consolidation, gradual rebuilding of the external position and lowering of the country risk, are expected to facilitate external financing and enable the business environment to stimulate private financial inflows. The baseline macro projections are shown in Table 1 and explained below.3

Table 1: Key Macroeconomic Indicators Pakistan FY10/11 to FY18/19

Source: Pakistani Authorities, IMF and World Bank staff estimates. 1/ National estimates. 2/ Includes medium and long term PPG debt as well as short-term external debt and IMF debt (budget and balance of payments support), foreign currency bonds (NHA/NC) as well as PSE’s non-guaranteed debt. 3/ SBP Gross Reserves exclude Cash Reserve Requirement, gold and foreign currency deposits of commercial banks held with SBP. 4/ In months of next year’s imports of goods and services. 5/ Total external debt is inclusive of medium and long term PPG debt as well as short-term external debt, IMF and private debt. 6/ Source: WDI (as of March 8, 2015).

• Growth and inflation: GDP growth is expected to reach 4.4 percent in FY14/15 and pick up to around 5 percent in FY17/18 and onwards. Services are projected to expand, especially telecom, fostered by new 3G/4G broadband services, electricity and transport. Manufacturing is expected to benefit from improved energy supply and better private sector credit conditions. Consumption will be supported by remittances, albeit with declining growth rates. Private investment is expected to benefit from better business conditions, public investment and from fiscal space opened through fiscal consolidation. Manufactured goods and services exports are expected to grow at an average of 4 percent. They will be supported by strengthened private investment and by the Generalized System of Preferences (GSP)4 plus for 75 new major export

3 All data, tables and figures contained in this document are based on information available until April 30, 2015. 4 The GSP is a preferential tariff system which provides for a formal system of exemption from the more general rules of the World Trade Organization (WTO) (formerly, the General Agreement on Tariffs and Trade or GATT).

FY10/11 FY11/12 FY12/13 FY13/14 FY14/15 FY15/16 FY16/17 FY17/18 FY18/19

Real economyNominal GDP at market prices (in bn. of rupees) 18,276 20,047 22,489 25,402 28,081 30,566 33,536 36,940 40,538 Real GDP growth (at factor cost) 3.6 3.8 3.7 4.1 4.4 4.6 4.8 5.0 5.1Contributions:

Agriculture 0.4 0.8 0.6 0.5Industry 0.9 0.5 0.3 1.2Services 2.2 2.5 2.8 2.5

Per Capita GDP (current US$) 6/ 1,212 1,252 1,275 ..Unemployment rate 1/ 6.0 6.0 6.2 ..Consumer prices (period average) 13.7 11.0 7.4 8.6 5.5 5.0 5.0 5.0 5.0Consumer prices (eop) 13.3 11.3 5.9 8.2

Fiscal sectorExpenditures 19.5 21.6 21.4 19.8 19.5 19.5 19.6 19.7 19.8Revenue 12.4 12.8 13.1 14.3 14.6 15.0 15.4 15.7 15.9Overall balance (excl. grants) -7.1 -8.8 -8.3 -5.5 -4.9 -4.5 -4.2 -4.0 -3.9Total public debt 60.0 64.5 64.8 64.3 63.0 62.4 61.3 59.8 58.7

Foreign currency public debt 2/ 26.7 26.0 22.0 20.9 19.9 20.1 19.9 19.8 20.0Domestic currency public debt 33.3 38.5 42.8 43.4 43.1 42.4 41.4 40.0 38.7

Monetary SectorBroad Money 15.9 14.1 15.9 12.5Credit to non-government 4.0 7.5 -0.6 11.4Interest (key policy interest rate) 14.0 12.0 9.0 10.0

Balance of paymentsCurrent account balance (incl. transfers) 0.1 -2.1 -1.1 -1.3 -1.2 -1.2 -1.6 -1.6 -1.9

Exports of goods & services 14.6 13.2 13.6 12.3 11.3 10.8 10.6 10.8 11.0Imports of goods & services 20.4 21.7 20.9 20.1 18.7 17.9 18.1 18.2 18.7

Capital and financial account 1.1 0.7 0.4 3.0 2.9 1.8 1.8 2.0 2.6Foreign direct investment, net 0.7 0.3 0.5 0.6 0.5 0.8 0.8 0.8 0.7

Gross official reserves (in US$ million, eop) 3/ 15,662 10,852 6,047 9,171 15,443 19,209 19,927 20,733 22,368 Gross official reserves (in months of imports of G&S) 4/ 3.9 2.7 1.5 2.1 3.6 4.2 4.1 4.0 4.0Total external debt 5/ 31.0 29.1 26.2 26.6 25.7 25.5 25.0 24.7 24.4Rupees per U.S. dollar (period average) 85.5 89.2 96.8 102.9

Memo:Nominal GDP at market prices (in US$ billion) 213.8 224.6 232.2 246.9GDP, PPP (current international $) 6/ 750.7 791.0 838.2 ..

Actual

(Percentage change; unless otherwise indicated)

(In percent of GDP; unless otherwise indicated)

(Percentage change; unless otherwise indicated)

(In percent of GDP; unless otherwise indicated)

Projections

6

products entering the European market, recovery in the United States, gradual trade normalization with India and opening of new markets in South and East Asia. Inflation is expected to settle at 5 percent from FY15/16 onwards owing to continued fiscal prudence and an improved global economic outlook. Relatively favorable terms of trade and a close to neutral exchange rate will support Pakistani exports’ external competitiveness and the trade balance.

Table 2: Key Fiscal Indicators Pakistan FY11/12 to FY18/19

Source: World Bank Staff estimates

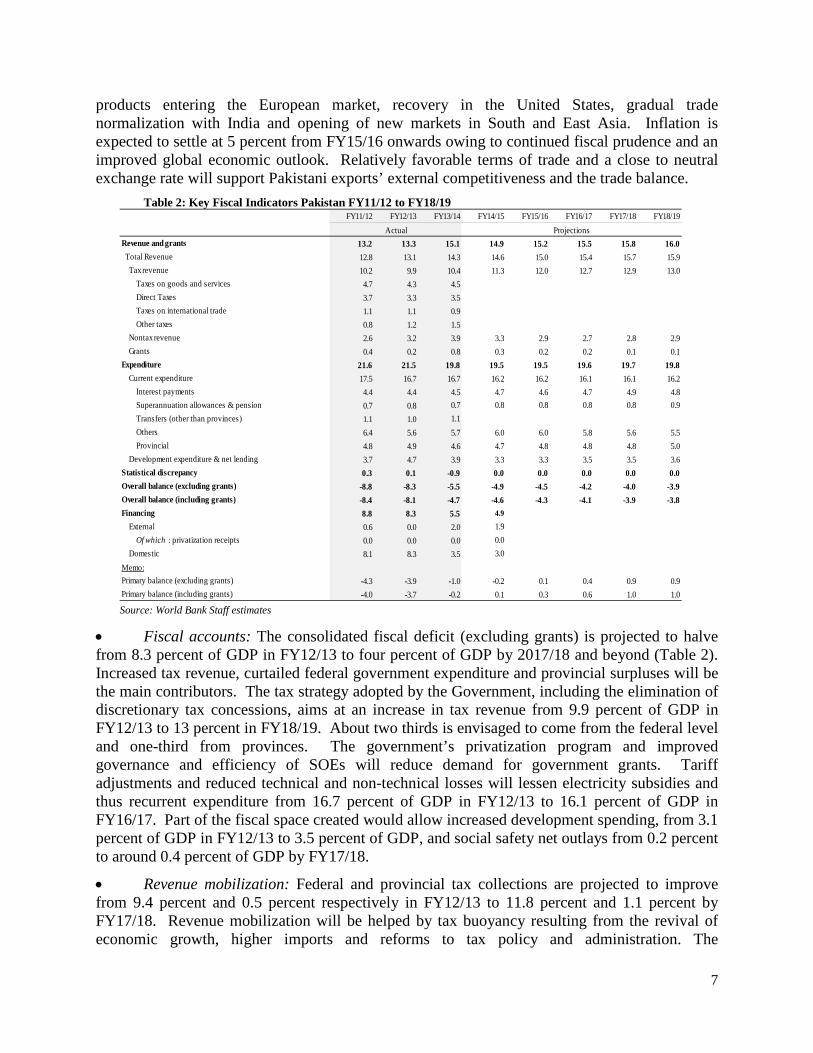

• Fiscal accounts: The consolidated fiscal deficit (excluding grants) is projected to halve from 8.3 percent of GDP in FY12/13 to four percent of GDP by 2017/18 and beyond (Table 2). Increased tax revenue, curtailed federal government expenditure and provincial surpluses will be the main contributors. The tax strategy adopted by the Government, including the elimination of discretionary tax concessions, aims at an increase in tax revenue from 9.9 percent of GDP in FY12/13 to 13 percent in FY18/19. About two thirds is envisaged to come from the federal level and one-third from provinces. The government’s privatization program and improved governance and efficiency of SOEs will reduce demand for government grants. Tariff adjustments and reduced technical and non-technical losses will lessen electricity subsidies and thus recurrent expenditure from 16.7 percent of GDP in FY12/13 to 16.1 percent of GDP in FY16/17. Part of the fiscal space created would allow increased development spending, from 3.1 percent of GDP in FY12/13 to 3.5 percent of GDP, and social safety net outlays from 0.2 percent to around 0.4 percent of GDP by FY17/18.

• Revenue mobilization: Federal and provincial tax collections are projected to improve from 9.4 percent and 0.5 percent respectively in FY12/13 to 11.8 percent and 1.1 percent by FY17/18. Revenue mobilization will be helped by tax buoyancy resulting from the revival of economic growth, higher imports and reforms to tax policy and administration. The

FY11/12 FY12/13 FY13/14 FY14/15 FY15/16 FY16/17 FY17/18 FY18/19

Revenue and grants 13.2 13.3 15.1 14.9 15.2 15.5 15.8 16.0

Total Revenue 12.8 13.1 14.3 14.6 15.0 15.4 15.7 15.9

Tax revenue 10.2 9.9 10.4 11.3 12.0 12.7 12.9 13.0

Taxes on goods and services 4.7 4.3 4.5

Direct Taxes 3.7 3.3 3.5

Taxes on international trade 1.1 1.1 0.9

Other taxes 0.8 1.2 1.5

Nontax revenue 2.6 3.2 3.9 3.3 2.9 2.7 2.8 2.9

Grants 0.4 0.2 0.8 0.3 0.2 0.2 0.1 0.1

Expenditure 21.6 21.5 19.8 19.5 19.5 19.6 19.7 19.8

Current expenditure 17.5 16.7 16.7 16.2 16.2 16.1 16.1 16.2

Interest payments 4.4 4.4 4.5 4.7 4.6 4.7 4.9 4.8

Superannuation allowances & pension 0.7 0.8 0.7 0.8 0.8 0.8 0.8 0.9

Transfers (other than provinces) 1.1 1.0 1.1

Others 6.4 5.6 5.7 6.0 6.0 5.8 5.6 5.5

Provincial 4.8 4.9 4.6 4.7 4.8 4.8 4.8 5.0

Development expenditure & net lending 3.7 4.7 3.9 3.3 3.3 3.5 3.5 3.6

Statistical discrepancy 0.3 0.1 -0.9 0.0 0.0 0.0 0.0 0.0

Overall balance (excluding grants) -8.8 -8.3 -5.5 -4.9 -4.5 -4.2 -4.0 -3.9

Overall balance (including grants) -8.4 -8.1 -4.7 -4.6 -4.3 -4.1 -3.9 -3.8

Financing 8.8 8.3 5.5 4.9

External 0.6 0.0 2.0 1.9

Of which : privatization receipts 0.0 0.0 0.0 0.0

Domestic 8.1 8.3 3.5 3.0

Memo:

Primary balance (excluding grants) -4.3 -3.9 -1.0 -0.2 0.1 0.4 0.9 0.9

Primary balance (including grants) -4.0 -3.7 -0.2 0.1 0.3 0.6 1.0 1.0

ProjectionsActual

7

government’s strategy to broaden the tax base and reduce the tax gap is focused on five areas: (i) minimization of tax expenditure under a three-year program phasing out SROs; (ii) upward revision of sales tax and general excise tax rates; (iii) upward revision of the capital gains tax on securities and immovable property; (iv) renewed procedures and thresholds for income and sales tax registration; and (v) identification of tax evaders in commercial and professional services sectors. While the first stage of removal of SRO-supported concessionary tax exemptions is estimated to increase revenues by around 0.35 percent of GDP, as part of existing measures accounting for 0.7 percent of GDP in FY14/15, the total estimated additional revenue expected from the three-year plan for phasing out SROs is about one percent of GDP (Annex 10). A gradual decrease of nontax revenues is assumed, which are projected to fall from 3.2 percent of GDP in FY12/13 to 2.8 percent of GDP in FY18/19, the result of reduced Coalition Support Funds provided by the United States. • External Sector. The current account deficit is expected to increase to 1.6 percent in FY16/17—slightly up from 1.3 percent of GDP in FY13/14. Faster growth will require higher imports of raw materials and fuels. Strong remittances will contribute to a modest but growing current account deficit in the medium term. Slightly higher foreign investment inflows attracted by a gradually lower country risk, initial privatizations, and declining multilateral financial net inflows will support the financial account. Official foreign exchange reserves are projected to be at 3.6 months of import coverage by end FY14/15 and reach a plateau of 4 months in 2015/16. • Financing Gap. Gross financing requirements from the balance of payments are expected to be about US$7.7 billion by end-FY16/17 and their mix is expected to change. IMF and official creditors’ amortization is projected to decline by almost US$3.2 billion between FY13/14 and FY16/17. In contrast, the current account deficit is projected to widen in absolute terms by about US$1.8 billion by 2016/17. Multilateral, bilateral and private debt-creating flows coupled with disbursements under the EFF and DPCs are expected to be early financing sources; later supported by modest increases in FDI. In FY14/15, the main sources of official financing are projected to be: the Coalition Support Fund (US$1.8 billion), IMF (US$2.7 billion), World Bank (US$1 billion), and the Asian Development Bank (US$0.74 million). Issuance of US$1.0 billion of Sukuks has also contributed to fill the financing gap. In FY16/17 the government plans to issue Eurobonds and Sukuks to the tune of $2.2 billion. Modest increases in FDI inflows originating from privatization are expected to close this financing gap. FDI and portfolio investment flows are projected to increase from US$2.8 billion in FY14/15 to US$3.6 billion by FY16/17. Balance of Payment financing requirements are shown in Table 3.

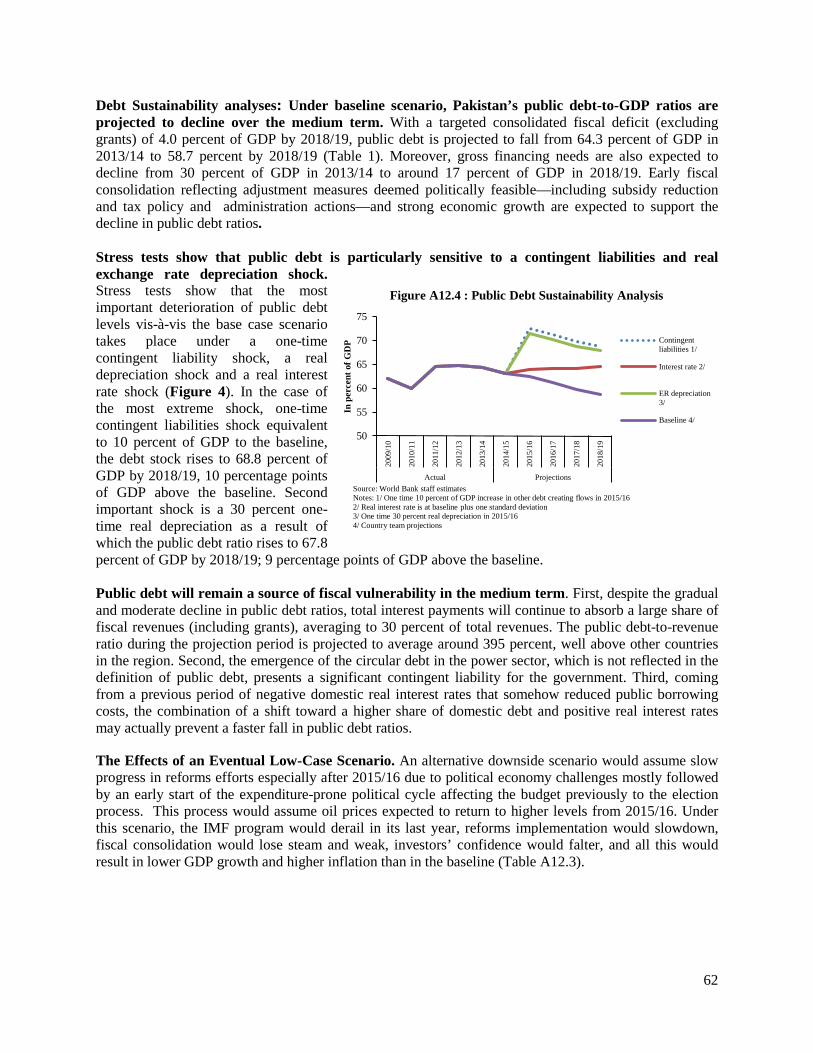

• Public Debt. Pakistan’s public debt to GDP ratio is projected to decline in FY14/15 to 63.0 percent and cross below the threshold of 60 percent by 2017/18. The sources of financing for the projected 2014/15 fiscal deficit of around 4.9 percent of GDP will be domestic (three percent of GDP, down from 3.5 percent of the previous year) and external (1.9 percent of GDP, slightly below the two percent of the previous year). A debt sustainability analysis shows that the debt path is highly sensitive to exchange rate depreciation shocks and, to a lesser extent, the materialization of contingent liabilities, either from power circular debt or SOE losses which might put the level of public debt much above the threshold of 60 percent of GDP. The debt sustainability analysis is shown in Figure 1 and discussed further in Annex 12.

8

Table 3: Pakistan BOP Financing Requirements and Sources FY11/12 to FY15/16

Actual Projections In million US Dollars FY12/13 FY13/14 FY14/15 FY15/16 FY16/17 Financing requirements 7,934 8,897 7,338 7,808 7,733 Current account deficit 2,496 3,057 3,240 3,470 4,782 Maturing short-term debt 391 5 409 1,436 373 Amortization of medium- and long-term debt 5,047 5,835 3,689 2,902 2,579

To IMF 2,538 2,230 1,182 200 20 To other official creditors 1,891 2,702 2,308 1,702 1,778 To private creditors 618 903 200 1,000 781

Financing sources 7,932 8,897 7,338 7,808 7,733 FDI and portfolio investments (net) 1,284 4,295 2,817 3,220 3,650 Capital grants 250 326 641 534 341 Other net capital and financial inflows -1,067 1,380 614 -97 780 Short term debt disbursements 256 732 1,849 803 803 Long term debt disbursements 2,683 5,447 7,852 7,164 2,928

From IMF 0 1,657 2,798 2,091 93 From other official creditors 2,274 3,525 2,904 4,573 2,554 From domestic private creditors 409 265 2,150 500 281

Change in reserves (decrease = +) 4,530 -3,283 -6,435 -3,816 -768 Source: World Bank Staff calculations and estimates

21. The macroeconomic framework is adequate for the proposed operation. Economic activity is picking up, inflation is significantly declining, and the fiscal deficit is narrowing down. Previous external imbalances are declining, the current account deficit remains modest and a minimum cushion in foreign exchange reserves has been successfully rebuilt.

2.3. IMF Relations

22. The IMF program is on track. Pakistan entered into a 36-month EFF with IMF in September 2013 for an amount of SDR 4,393 million. So far Pakistan has undergone six successful quarterly program reviews with IMF and has received an amount of $ 3.75 billion from IMF under EFF in six quarterly installments. Last May, Staff level agreement was reached on the Seventh review and Executive Board approval is expected in end-June 2015 with another tranche of SDR 360 million (about US$506 million) to be made available. Pakistan met all end of March 2015 performance criteria, including those on the budget deficit and accumulation of net international reserves. Program performance has been strong and no waiver has been required

Figure 1. Pakistan Debt Sustainability Analysis FY09/10 to FY18/19 External Debt Composition as of December 31, 2014

USD(mn)

Share of total debt % of GDP

Monetary authoriities 6,241 9.7% 2.3%

General Government 47,303 73.5% 17.2%

Banks 2,252 3.5% 0.8%

Other sectors 8,541 13.3% 3.1%

Of which intercompany lending 3,053 4.7% 1.1%

Total External debt 64,338 100.0% 23.4%

Long term 58,804 91.4% 21.4%

Short term 5,534 8.6% 2.0%Sources: Pakistan authorities

Figure 1. Pakistan Debt Sustainability Analysis FY09/10 to FY18/19

50

55

60

65

70

75

200

9/1

0

201

0/1

1

201

1/1

2

201

2/1

3

201

3/1

4

201

4/1

5

201

5/1

6

201

6/1

7

201

7/1

8

201

8/1

9

Actual Projections

In p

erc

en

t of

GD

P

Public Debt Sustainability Analysis

Contingentliabilities 1/

Inte rest ra te 2/

ER depreciation 3/

Baseline 4/

Source: World Bank staff estimatesNotes: 1/ One time 10 percent of GDP increase in other debt creating flows in 2015/162/ Real interest rate is at baseline plus one standard deviation3/ One time 30 percent real depreciation in 2015/164/ Country team projections

10

20

30

40

200

9/1

0

201

0/1

1

201

1/1

2

201

2/1

3

201

3/1

4

201

4/1

5

201

5/1

6

201

6/1

7

201

7/1

8

201

8/1

9

Actual Projections

In p

erc

en

t of

GD

P

External Debt Sustainability Analysis

Current account 1/

Combined 2/

ER depreciation 3/

Baseline 4/

Source: World Bank staff estimatesNotes: 1/ Non-interest current account is at baseline minus one-half 10-year historical standard deviations2/ Combination of three shocks: i. Non-interest current account is at baseline minus one-quarter standard deviation, ii. Real GDP growth is at baseline minus one-quarter standard deviation, iii. Nominal interest rate is at baseline plus one-quarter standard deviation3/ One time 30 percent real depreciation in 2015/164/ Country team projections

9

since the fifth review. The Authorities remain committed to achieving its program targets and address policy constraints with increasing its focus on building on the macroeconomic stability gains and to achieve higher, sustainable and inclusive growth.

3. GOVERNMENT’S PROGRAM

23. Upon taking office, the new administration introduced a comprehensive reform program. Under this program, the government committed to adopt stabilization measures to eliminate the country’s macroeconomic imbalances and initiate growth-oriented structural reforms needed for a more efficient economy (Box 1). In its first two years, the government has made promising inroads at implementing its reform agenda. On the one hand, it has issued holistic strategies and policies on its major reform areas: an energy policy on August 2013, a privatization strategy in October 2013, a tax reform strategy on February 2014, a 3-year plan for phasing out SROs-based tax exemptions policy on June 2014, a plan for improving the investment climate in October 2014, a national financial inclusion strategy in January 2015 and a Tariff Rationalization plan in March 2015. On the other hand, it has achieved some initial outcomes for reform implementation: it cleared pending powers arrears upon taking office; successfully completed the first equity and strategic sales of its privatization agenda; approved the first phase of the removal of the discriminatory SROs and Customs Rationalization Plan in the budget bill FY14/15; created the One Stop Shop for business registration; and prepared a set of draft bills on private credit bureaus, secured transactions and corporate restructuring that will change the landscape for financial inclusion in the country.

4. THE PROPOSED OPERATION

4.1. Link to Government Program and Operations Description

24. The proposed FSIG-II single-tranche credit has catalyzed the initial outcomes required for further consolidation and deepening of key inclusive growth-enhancing components of the government’s program described above. The first credit of the series addressed critical institutional and regulatory changes needed to jumpstart the reforms. The second credit brings continuity and sustainability to most actions of the first phase, while introducing new inclusion and governance actions. The policy program supported by FSIG-II is structured around two main pillars: (a) fostering private and financial sector development through privatization of SOEs, expanding access to finance, improving trade competitiveness, and enhancing the investment climate; and (b) mobilizing revenue and expanding priority social spending.

25. The pillars around which this FSIG series is organized are essential prerequisites and enablers for sustained poverty reduction and shared prosperity. As the growth elasticity of Pakistan’s poverty rate is among the highest in the world, by the expected impact on growth acceleration, the operation is also expected to contribute to poverty reduction and shared prosperity. And similarly, protecting the safety net and enhancing business-friendly conditions will contribute to inclusive growth and governance.

10

Box 1. Key Economic Priorities of the Government’s Program The government envisages stabilizing the economy, bringing inflation down to the 6–7 percent range, and achieving growth rate targets of 6–7 percent by 2017/18 or earlier. To do this, it has set the following goals and comprehensive policy agenda: Stabilization Moving to fiscal consolidation. Reducing the fiscal deficit from 8.3 percent of GDP in 2012/13 to 3.5-

4 percent in 2016/17 by increasing revenues by around 3 percent of GDP, eliminating tax exemptions; imposing austerity in other-than social expenditure outlays, cutting down power subsidies; raising the allocations to priority safety net (BISP); and carrying on active public debt management.

Rebuilding the external position to no less than 3 months of imports and tightening monetary policy. Scaling back monetary accommodation of fiscal deficits and setting up policy rates to keep positive real interest rates; strengthening the central bank’s independence; and protecting the external position by repurchasing reserves to cushion against major shocks.

Main growth-enhancing reforms Comprehensive power sector reform. Reducing power subsidies; restructuring boards of power distribution

and generation companies; making new investments; strengthening the power sector regulator; and expanding alternative sources of energy.

Reforming or privatizing SOEs. Privatizing by equity or strategic sales; or if restructuring, then requiring professional chief executives and board members and their compliance with Public Sector Companies (Corporate Governance) Rules 2013.

Improving trade competitiveness. Simplifying tariffs, with four slabs and 1–25 percent rates, and phasing out trade-distortive statutory regulatory orders (SROs) on some 4,000 products.

Normalizing trade relations with India. Extension of the most-favored nation status to it; shifting products to the “sensitive list” under the South Asian Free Trade Agreement to facilitate regional trade; and taking full advantage of trade preferences available from the European Union.

Enhancing the investment climate. Establishing a One Stop Shop for registering limited liability companies; and strengthening of the BOI in implementing a plan for improving the business environment and investment-friendly special economic zones.

Expanding access to finance. Developing the SBP’s Financial Inclusion Program to enhance access of SMEs to financial services through regulatory reforms, product innovation, financial literacy, and consumer protection.

26. The record of implementing reform-oriented operations in Pakistan has been mixed. Assessments of past operations therefore provide valuable country-specific lessons, and these have been borne in mind in designing and preparing this DPC series:

• The 2011 Country Partnership Strategy Progress Report notes that deep reform progress supported by development policy lending should be aware of the slow pace of structural reform, the permanent risk of an earlier than anticipated closing of the IMF program, and suggests that multi-sector operations tend to fail. As a result, this operation was deliberately split from the DPC on power and frontloaded on early achievements of the reform program. • The 2012 Tax Administration Reform Project Implementation Completion Report says that given the policy, legal, and institutional complexities involved in mobilizing revenue, an investment operation alone strictly focusing on improving tax administration is unlikely to increase the tax ratio on a sustained basis. It should be complemented by upfront tax-policy measures. As a result, this DPC complemented the following projects focused on tax administration at the federal level—the Project Preparation Facility on a Revenue Mobilization Disbursement-Linked Indicators Project (P128182) --and at the provincial level, the Sindh Public Sector Management Reform Project (P145617).

11

• The 2007 Poverty Reduction and Economic Support Operation underscores the importance of (a) aligning the program with the relevant levels of government, that is federal or provincial; (b) avoiding dispersion and being selective on the most critical areas of reform; (c) addressing capacity issues with timely technical assistance (TA); (d) undertaking robust and comprehensive prior analytical work; (e) being aware that institutional reforms take time and need multiyear support; and (f) having flexibility to respond to new developments. As a result, the design of this DPC matched the Government’s priorities, focused on just two areas, provided timely complementary TA, did prior relevant analytical efforts, and sequenced policy measures under flexible terms.

4.2. Prior Actions, Results and Analytical Underpinnings

27. The eleven FSIG-II prior actions and associated results indicators are set out in the Policy and Results Matrix (provided in Annex 1). The actions build on the achievements of FSIG-I. For most of the indicative triggers, the measures actually adopted by the government have been stronger than originally expected. The prior actions, while still supporting the original two pillars have been adjusted where necessary, following the principle of flexibility. Two new prior actions have been added to address inclusion and economic governance concerns and no trigger from FSIG-I was dropped. The policy matrix that appears in Annex A1.A in Annex 1 also includes an Annex A1.B showing the indicative triggers originally proposed for this second operation, the modified prior actions and the rationale for the change.

Fostering Private and Financial Sector Development

Advancing privatization. Action 2.1: As part of its privatization program, the GOP has completed one SOE strategic sale and three capital market SOE equity transactions.

28. The FSIG series supports a revival of Pakistan’s privatization program, which had been stalled for over eight years (Annex 5). FSIG-I recognized the steps taken by the Privatization Commission to launch the Privatization Program by issuing Requests for Proposals (RFP) and calling for Expressions of Interest (EOIs) in connection with the hiring of Financial Advisors (FA) to advise on the first SOE strategic sales, and the offering of equity in at least three SOEs in domestic and international markets. FSIG-II supports the completion of this first phase of the program.

29. The robust resumption of the privatization process in Pakistan is expected to provide both fiscal benefits and to further boost private sector job-creation. The aims of the privatization program are to both improve performance of SOEs that provide critical services to support private sector activity and to crowd in further private sector investment. In addition, privatization should facilitate the process of fiscal consolidation and create fiscal space for critical expenditures by reducing fiscal losses as well as providing one-time benefits from privatization proceeds.

Financial inclusion. Action 2.2: The National Assembly has approved the Credit Bureau Act; and the GOP has joined the Better than Cash Alliance Initiative.

30. The limited access to finance that Small and Medium Enterprises (SMEs), women and vulnerable groups in Pakistan have is a major constraint to inclusive growth in Pakistan. Less than 14 percent of the population has access to any financial service,

12

microfinance reaches less than 3 percent of the population, and less than 7 percent of SMEs use formal finance for working capital or investments. Though financial products and services are gradually becoming more widely available, access to credit continues to be particularly limited. Overall credit growth has been declining and rising NPL ratios have reinforced banks’ risk-aversion towards private sector lending.

31. To enhance access to finance, a National Financial Inclusion Strategy (NFIS) has been formulated, two critical components of which are supported by FSIG-II: improving credit information and the digitalization of financial payments (Annex 9). Well-functioning credit bureaus are an essential part of an economy’s financial infrastructure, which, with the proper legal framework, can reduce information asymmetries and potentially facilitate universal access to formal finance, particularly for small firms and households, improve borrower discipline, and support bank supervision and credit risk monitoring, thereby lowering interest rates. Public and private credit bureaus in Pakistan currently provide credit information on only 7 percent and 2 percent, respectively, of the population. Borrowers and third parties do not have access to their own credit information, and credit histories do not include information from nonfinancial institutions.5 The Credit Bureau Act, which was passed by the National Assembly (as recognized by FSIG-II) and is expected to be enacted after its review by the Senate by end-2015 will improve the regulatory framework (and cover private credit rating agencies); preserve consumer protection norms, increase the information available to consumers and SMEs, and expand the coverage and quality of credit information. In parallel, by joining the global Better than Cash Alliance Initiative (BTCA), GOP has signaled its commitment to the digitization of payment processes. Through membership in BTCA, GOP will become eligible for technical assistance support and access to toolkits and guidance on the best ways to digitize payments.

Improving trade competitiveness. Action 2.3: The Parliament has approved a budget law 2014/15 providing for the application of 6 statutory tariff slabs; and the MoF has approved a Plan to achieve 4 slabs in 3-years, within a range of 1 to 25 percent for all tariff lines, allowing very few exceptions and tariff peaks to address sensitive goods or special sectors only.

32. Pakistan’s trade competitiveness has been hurt by the increasing complexity of the tariff regime, further weakening an already poor investment climate. A decade ago Pakistan was among the most open economies worldwide, with four statutory tariff rates between 5 and 25 percent, and few exceptions. However, the number of standard statutory rates has doubled from only four (5, 10, 15, and 25 percent) in 2002/03 to eight (0, 5, 10, 15, 20, 25, 30 and 35 percent) in 2012/13 and the tariff regime has been further complicated with the introduction of new statutory duty rates, and the use of statutory regulatory orders (SROs) and additional duties. The increasing complexity of the tariff regime has made it more difficult for firms, including exporters, to import needed capital and intermediate goods, and that has contributed to the deterioration of Pakistan’s export growth performance since 2004. Tariff simplification and a reduction in the average duty rate, applied with priority to capital and intermediate goods, by reducing the administrative, menu and information costs associated with the current complex tariff structure should stimulate growth by boosting exports and increasing Pakistan’s ability to compete globally, while at the same time increasing consumer welfare.

5The State Bank of Pakistan has an electronic-Credit Information Bureau (e-CIB) system with mandatory membership for all banks and financial institutions but access to information from this database is restricted to members.

13

33. The actions under FSIG-II simplify the tariff regime and take the initial steps towards the reduction of average (and weighted) tariff rates and dispersion. Under the tariff-related provisions of the Finance Bill FY14/15, which were supported by FSIG-II, four main measures were adopted: (i) a reduction in the number of standard statutory (MFN) tariff slabs to 6 through the elimination of the 35 percent and 30 percent tariff slabs and the reduction in the customs duty for 341 tariff lines from 30 percent to 25 percent custom duty6; (ii) the interim designation, prior to a redesign of GOP policy towards the auto sector, of only the automobile sector as “special” with a 35 percent tariff slab for 267 tariff lines and a 30 percent tariff slab for 27 tariff lines; (iii) an increase, for fiscal reasons, in the “floor” customs paid for 440 products from zero to one percent, while about 70 “socially sensitive” items were left to be imported duty free as part of a newly created 5th Schedule of the Customs Tariff Act (see Annex 6); (iv) the elimination of the first set of SROs, which modified some Customs tariffs, under a 3-year phase out plan. These measures have initiated the simplification of the tariff regime but given the increase in the floor tariff rate have resulted in this initial round in only a slight reduction of the average tariff. The provisions of the Tariff Rationalization plan prepared and approved by Ministry of Finance (MoF) under FSIG-II are expected to be included in the next Finance Bills FY15/16 and FY16/17 and further reduce the simple average statutory tariff rate from its average of 14.4 percent in June 2013 to below 12 percent by June 2016. Enhancing the investment climate. Action 2.4: SECP, FBR and EOBI have established a virtual One-Stop-Shop (OSS) for business registration, and a physical OSS in Lahore.

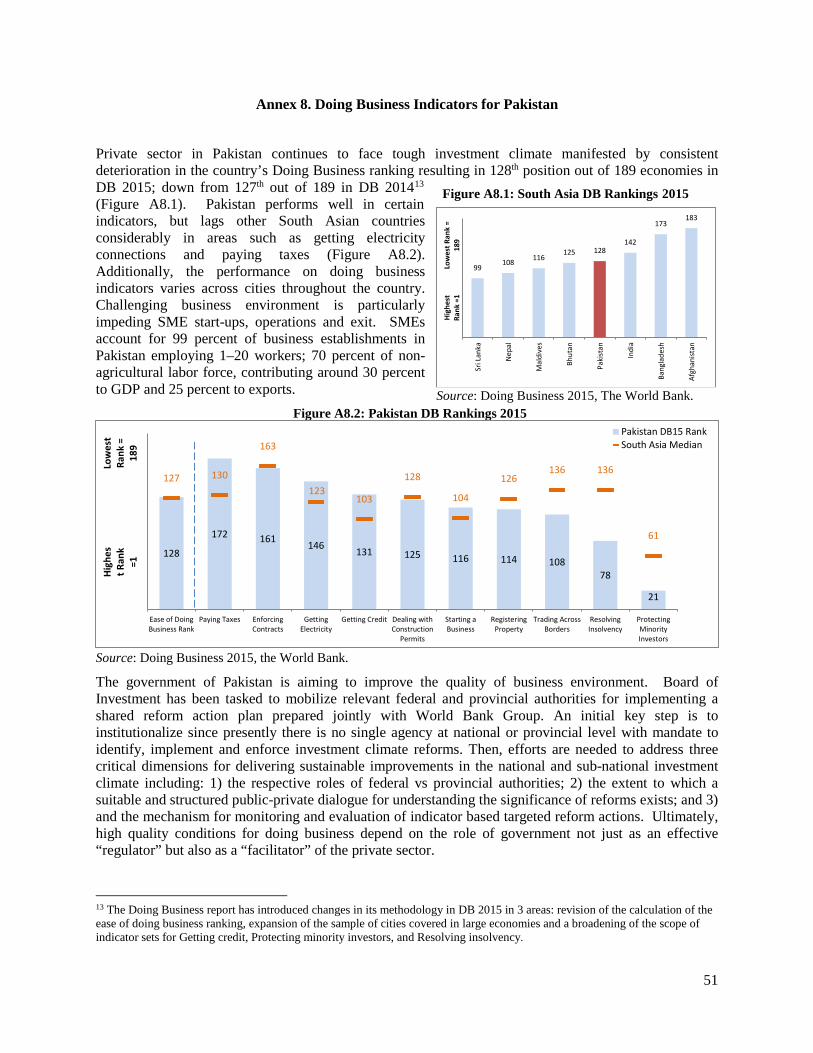

34. The business environment in Pakistan is exceptionally weak, and that has dampened economic growth and hindered private-sector led creation of better jobs. Pakistan is ranked 128 out of 189 economies on the overall ease of doing business rankings for the year 2015, having slipped in the rankings in the last five years across all Doing Business indicators. Supported by the World Bank’s Indicator-based Reform Advisory team, the Board of Investment (BOI), in October 2014, finalized a plan for improvement of the business environment, covering five federal indicators and one provincial including: paying taxes, registering property, enforcing contracts, business registration, trading across borders, and getting credit.

35. The FSIG series supports a critical component of GOP’s plan for improving the business environment—streamlining business registration. The process of registering a business in Pakistan is, as in many countries, cumbersome and opaque, involving many different public agencies and a range of different often unclear reporting obligations. That has deterred both starting a business and registering businesses, resulting in a large informal sector, with negative consequences for business activity and tax collection. In November 2014, the Federal Board of Revenue (FBR), Employees Old Age Benefits Institute (EOBI) and Securities and Exchange Commission of Pakistan (SECP) finalized a Memorandum of Understanding establishing a virtual OSS for limited liability companies (LLCs).

36. The expected result of these actions is to simplify business procedures and improve the investment climate in Pakistan. The opening of the OSSs should reduce the number of steps and days to register a business from 10 and 21 to at least 8 and 18 respectively.

6 We consider a standard tariff slab a tariff that applies to more than 30 tariff lines (products).

14

Expanding Social Protection and Revenue Mobilization Expanding social protection. Action 2.5: The Parliament has approved a budget law 2014/15 increasing the BISP allocation to PRs97.15 billion in order to raise the benefit amount to PRs1,500/month per beneficiary, well above inflation, and start activities to expand CCTs for primary education in no less than 27 districts with a benefit of PRs250 per month per child attending school; and the BISP has reached an implementation agreement with each provincial/regional government on a cost-sharing arrangement for CCTs. Improving the safety net. Action 2.6: In compliance with BISP Act 2010, the BISP Board has issued internal rules and regulations delineating the powers and functions of the BISP Management and the BISP Board.

37. FSIG-II supports the progressive expansion of Benazir Income Support Program (BISP) benefits, already expanded under FSIG-I. BISP is Pakistan’s largest income support program for the poor. In the federal budget for FY2014/15, the Government increased the allocation to BISP to PRs 97.15 billion. The Government is committed both to continue to expand the program coverage to 5.5 million by the end of the FY2015/16 and increased the benefit amount from PRs1,200 per month to PRs1,500 per month. The 25-percent increase in the benefit amount is above the inflation rate of around 8 percent. BISP has enrolled more than 500,000 CCT beneficiary children in all 27 of the extended-phase districts across provinces/regions. Enrollment campaigns will continue as 3.5 million potential beneficiaries have been reported in the 27 target districts. To support the enrollment of these children, BISP has signed an Implementation Agreement with each of the participating province/region in the CCT roll-out, as envisaged under the prior action. These actions constitute a significant expansion of the coverage of Pakistan’s main safety net program, and lay the foundations for mainstreaming a mechanism for supporting primary education enrollment nationwide.

38. FSIG-II also supports efforts to improve governance of BISP. Ambiguity in the BISP Act 2010 over a range of matters related to the powers and functions of the Board, the Chairperson and the Secretary (as the head of BISP Management and its Principal Accounting Officer), have prevented BISP from making key decisions on procurement or personnel matters such as, inter alia, filling of key senior positions. And this risks compromising BISP’s day-to-day management and effectiveness in serving the poor. To remedy the situation, the BISP Board has issued internal rules and regulations clarifying the division of roles, responsibilities and authorities between the Board and the management of BISP.

Mobilizing revenue Action 2.7: The Parliament has approved a budget 2014/15 which includes (i) a tax expenditure annex, (ii) the elimination of a set of tax exemptions and SROs, and (iii) provision of additional tax measures for a total revenue impact equivalent to at least 0.7 percent of GDP. Action 2.8: The Government (a) has issued a Presidential Ordinance containing all amendments of the corresponding tax laws to permanently eliminate the discretion of FBR to issue special tax exemptions, making any proposed tax exemption subject to parliamentary approval as part of the annual budget law and/or the corresponding tax legislation; and (b) has submitted to the Parliament such amendments as part of the Finance Bill for the budget 2015/16.

15

Action 2.9: FBR has (a) issued 171,000 notices to identified potential tax evaders to register and file tax payment, and taken administrative and/or legal actions on at least 25 percent of the potential taxpayers who received notices by 31 December 2014, but failed to respond to them; and (b) selected at least 7.5 percent of non-salary-including large taxpayers (filed for tax year 2013) through ballot- or risk-based audits, and completed audits for at least 10 percent of those selected cases. Action 2.10: (a) Two provinces have expanded the scope of their GST on services to increase their revenue; and (b) the Provinces have increased their 2014/15 budget allocations to non-salary education and health spending by no less than 26 percent.

39. The revenue mobilization actions under the FSIG series address well-known structural weaknesses in Pakistan’s tax system, thereby creating fiscal space for priority social and development expenditures without raising tax rates, and for lower domestic borrowing needs by the GOP, which helps reduce crowding out of private sector credit, two important prerequisite for inclusive growth. Weaknesses of the system include an inefficient tax administration; a narrow tax base (of 39.4 million employed persons, of whom fewer than 10 percent are registered), a skewed tax structure (68 percent of tax revenue is from indirect taxes); a complex and nontransparent tax system that favors numerous and generous ad hoc exemptions and concessions and corruption, and tax evasion; and low provincial revenue collection efforts (Annex 11). In response, the FSIG series focuses on broadening the tax base and on strengthening registration, enforcement, transparency and compliance. FSIG-II builds on the tax reform strategy formulated under the FSIG-I7, through direct measures to increase revenues (including those of the first stage of the three year plan for the elimination of tax exemptions supported by SROs), make tax expenditure transparent, reintroduce the tax audit function and large-scale registration of potential tax evaders, and eliminate FBR’s legal powers to issue special tax exemptions and concessions through SROs. The latest reform contributes to a major improvement in the fiscal position through two mechanisms: First, it eliminates the fundamental source of discriminatory, inequitable and corrupt-prone tax leakages and, coupled with the gradual phasing out of existing SROs, it brings additional resources into the tax net for a projected total revenue increase of no less than one percent of GDP (Annex 10).

40. The overall net fiscal space created by both DPCs series during FY13/14 and FY14/15 is projected to be 2.4 percent of GDP (Table 4). The revenue measures announced by the government in the 2014/15 budget have the potential of increasing tax revenue by about 0.9 percent of GDP.8 Tax measures contained in the tax strategy for the first two years of Government will raise federal revenue by about 1.4 percent of GDP. This does not include an increase of 0.2 percent of GDP from provinces essentially based in the expansion of the scope of GST taxed services and other tax adjustments. The startup of the tariff simplification process to six slabs inside 1-25 percent tariff bracket generated infra marginal losses due to the temporary compensatory regulatory duties adopted for fiscal reasons. There is also a modest gain projected from the tax administration measures adopted by FBR in Customs or in income or sales taxes, as

7Under FSIG-I, the government approved the medium-term reform strategy for FBR; estimated the fiscal cost of tax exemptions and concessions; issued over seventy thousand (70,000) notices to potential tax evaders to register and file tax payments; launched an information technology-based Taxpayers Audit Management System and selected five percent of total tax returns filed for tax year 2012 and enhanced the transparency of the tax system by publishing separate tax directories for the Parliamentarians and other taxpayers 8 These measures suffered legal challenges in approving a Gas cess and the fiscal effects of the drop in oil prices. To offset losses, the Government approved contingency tax measures for an equivalent gain of about 0.3 percent of GDP in February 2015.

16

tax administration reform outcomes materialize slowly. The power tariff reform (supported by a parallel DPC) has mainly contributed to create fiscal space--with lower budgeted Tariff Differential Subsidies (TDS) and savings-generation measures--by about 1 percent of GDP. The fiscal space freed up by these measures has been used to increase allocations to BISP individual beneficiaries (0.3 percent of GDP) and to increasing provincial non-salary education and health services expenditures by 27 percent (0.1 percent of GDP).