doc sample1-solution nc

DESCRIPTION

adTRANSCRIPT

Exam Solution 1

London Business School

MIM2015 – Management Analysis & Systems Gah-Yi Vahn

SAMPLE FINAL EXAM 1

xxx 2015

Time: xxx

LBS Number__________________

Stream_________________

Total Points : 50

Question 1 : 25

Question 2 : 25

Duration: 2 hours

Instructions:

This is a closed-book exam.

The use of a hand-held calculator is allowed, but a graphics calculator is NOT allowed.

The exam paper consists of 2 questions; you are required to answer all questions. Allocate

your time optimally.

For your answers, please use the space provided. If you need more space, please use the

blank page opposite the question.

Make explicit any assumptions underlying your answers, interpret your results and justify

your answers, conclusions and recommendations.

In grading, importance will be attached to the clarity and conciseness of your answers.

Good luck!

EXAM SOLUTION

Exam Solution 2

Question 1 (25 points)

Maureen Laird is the chief financial officer for the Alva Electric Co., a major public utility in the UK. The

company has scheduled the construction of new hydroelectric plants 5, 10, and 20 years from now to meet

the needs of the growing population in the region served by the company.

To cover the construction costs, Maureen needs to invest some of the company’s money now to meet these

future cash-flow needs. Maureen may invest only in three different investment opportunities: A, B, and C. In

order to keep a diversified portfolio, Maureen can invest at most £800 million, £300 million, and £200

million in opportunity A, B, and C respectively. The investment opportunities produce income 5, 10, and 20

years from now, and that income is needed to cover the cash-flow requirements in those years. (Any excess

income above the minimum requirement for each time period will be used to increase dividend payments to

shareholders rather than saving it to help meet the minimum cash-flow requirement in the next time period.)

Table 1.1 shows both the amount of income generated by one million invested in each investment

opportunity and the minimum amount of income needed for each of the future time periods when a new

hydroelectric plant will be constructed.

Table 1.1 Investment income and cash flows required

Year

Income per £million invested Minimum Cash

Flow Required A B C

5 £2 million £2 million £1.8 million £450 million

10 £1.5 million £0.5 million £1 million £250 million

20 £0.3 million £0.5 million £2 million £200 million

Maureen wishes to determine the investment portfolio that will cover the cash-flow requirements while

minimising the total amount invested. For this purpose, she has developed a spreadsheet model. The decision

variables in the model are:

A: amount to be invested in opportunity A now (in £ million),

B: amount to be invested in opportunity B now (in £ million),

C: amount to be invested in opportunity C now (in £ million).

(i) (10 points) Write down an algebraic model for the problem described above (objective, decision

variables, and constraints in algebraic form).

Minimise A + B + C

Subject to

2A + 2B + 1.8C 450

1.5A + 0.5B + C 250

0.3A + 0.5B + 2C 200

A 800

B 300

C 200

A, B, C 0

Below, you will see:

Table 1.2: an Excel model with the optimal solution (obtained using Solver) and the same spreadsheet,

but with the formula’s made visible;

Exam Solution 3

Table 1.3: the Solver pop-up window (with some parts missing);

Table 1.4: the sensitivity analysis report.+

Table 1.2 Excel spreadsheet (in £million) with optimal solution

Exam Solution 4

Table 1.3 Solver pop-up window (with parts missing)

Table 1.4. Sensitivity Analysis Report

Variable Cells

Final Reduced Objective Allowable Allowable

Cell Name Value Cost Coefficient Increase Decrease

$B$10 Investments A 99.4 0 1 0.182 0.013

$C$10 Investments B 63.3 0 1 0.012 0.593

$D$10 Investments C 69.3 0 1 2.67 0.100

Constraints

Final Shadow Constraint Allowable Allowable

Cell Name Value Price R.H. Side Increase Decrease

$E$5 Cash Flows 450 0.482 450 291 77.8

$E$6 Cash Flows 250 0.012 250 60.7 106

$E$7 Cash Flows 200 0.060 200 217 115

Exam Solution 5

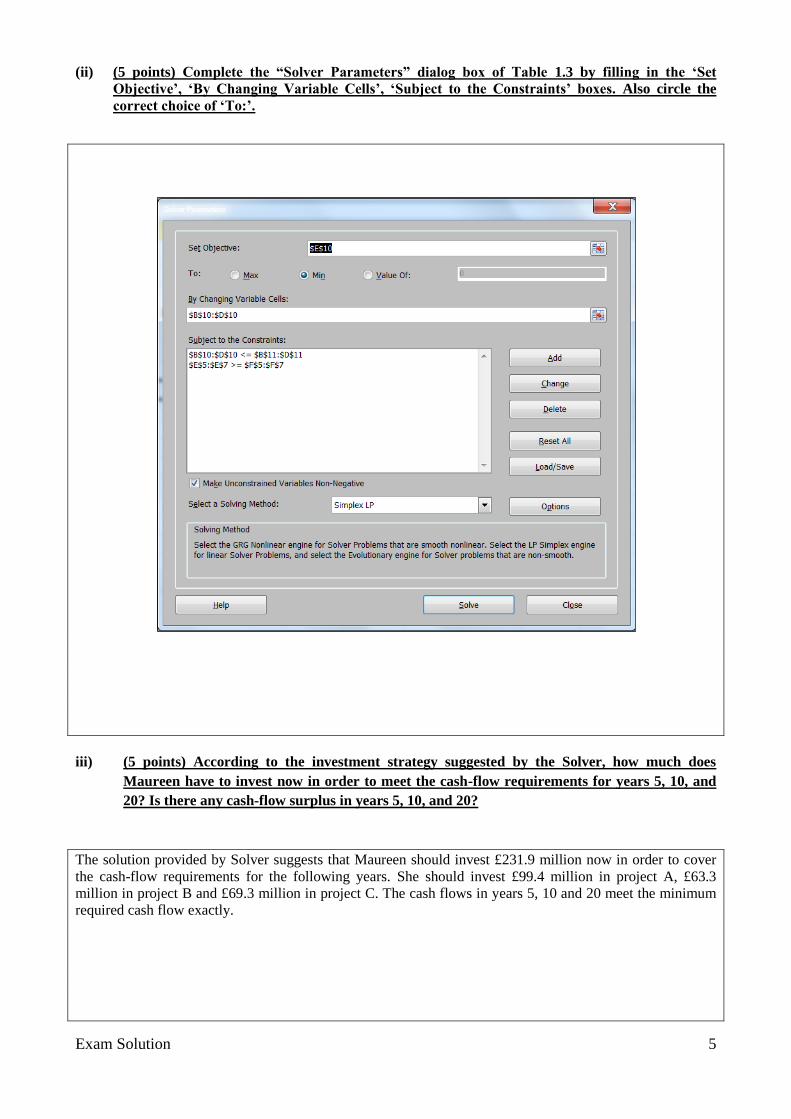

(ii) (5 points) Complete the “Solver Parameters” dialog box of Table 1.3 by filling in the ‘Set

Objective’, ‘By Changing Variable Cells’, ‘Subject to the Constraints’ boxes. Also circle the

correct choice of ‘To:’.

iii) (5 points) According to the investment strategy suggested by the Solver, how much does

Maureen have to invest now in order to meet the cash-flow requirements for years 5, 10, and

20? Is there any cash-flow surplus in years 5, 10, and 20?

The solution provided by Solver suggests that Maureen should invest £231.9 million now in order to cover

the cash-flow requirements for the following years. She should invest £99.4 million in project A, £63.3

million in project B and £69.3 million in project C. The cash flows in years 5, 10 and 20 meet the minimum

required cash flow exactly.

Exam Solution 6

iv) (5 points) In Table 1.4, the shadow price of the value in cell E5 is £0.482 million. Interpret this

value.

The shadow price of the E5 cell denotes the additional investment required now in order to have one more

million available in the 5th year (£451 million instead of £450 million), or alternatively, the reduced

investment needed upfront if in the 5th year, one million less were required (£449 million instead of £450

million).

In other words, if we wanted to have £451 million available in the 5th year, we would have to invest an

additional £0.482 million now. This shadow price holds up to an allowable increase of £291 million more

required in the 5th year. Likewise, if we could do with only £449 million in the 5

th year, we would not need to

invest £0.482 million now. This would be true up to an allowable decrease of £77.8 million.

Exam Solution 7

Question 2 (25 points)

Wildcat Dynamics Co. is an oil exploration company, founded in 1985. The company had been successful in

bringing in wildcat wells in various parts of the United States. By 1999 the company had reasonable

financial reserves of its own, but also occasionally entered into partnership with a group of investors in

Dallas. Hence, the firm usually did not have great difficulty in raising funds for a reasonably good wildcat

prospect.

It was Wildcat Dynamic’s policy to sell off the rights to produce the oil once a well was brought in.

Activities were confined to locating possible sites, arranging for appropriate leases, and contracting for

drilling operations.

In June of 2001, the company was trying to decide whether to drill on a parcel of offshore land in Louisiana.

The lease had been taken out in 1999 but the company had to decide whether or not to drill. The cost of

drilling at the site would be $70 million. This would be all lost if the well were dry. If the well were

successful, the value would depend upon the extent of the reserves uncovered. For simplicity, management

generally considered only two alternatives, described as either a “wet” well or a “soaking” well. The revenue

associated with selling the rights to a wet well is $220 million (i.e. $150 million in excess on the drilling

cost). For a soaking well, revenue is expected to be $670 million (i.e. $600 million above the drilling cost).

William Cooper, the company geologist, was consulted about the chances of actually finding oil. He said that

the chances depended upon whether or not a particular structure laid underneath the proposed drilling site. If

the underlying lime-shale formation rose into a flat dome shape where Wildcat proposed to drill then there

were substantially better chances of finding oil than if no such dome structure existed. Mr. Cooper said that

he estimated that there were roughly 6 chances in 10 of such a dome structure underneath the Wildcat site.

He based this estimate upon experiences of other drillers in the area and his own accumulated knowledge of

geology. Cooper also gave estimates of the probability of finding oil, given the existence of a dome (see also

Table 2.1): If there is a dome, there still is a 60% chance that there is no oil whatsoever. In 25% of the cases,

the well will be “wet”, while there is a 15% chance that it will be “soaking”. If there is no dome structure

underneath the site, chances are much bigger that there is no oil, namely 85%, and only 12.5% of a wet well

and 2.5% of a soaking well.

Dome Structure

Present

No Dome Structure Present

Dry Well 60% 85%

Wet Well 25% 12.5%

Soaking Well 15% 2.5%

Table 2.1 Probability of finding oil

Mr Cooper noted that these estimates represented his best judgement about the results of drilling. He

indicated that another expert might come up with a different set of estimates and that in fact, there were no

such things as “right” probability estimates in this business.

(i) (7 points) Given Cooper’s estimates about the probability of striking oil, should Wildcat go

ahead and drill for oil? (for all questions, ignore tax effects and the time value of money)

The decision tree below shows that the expected profit of this prospect equals $41 million, and that based on

this, Wildcat should go ahead and drill for oil. However, the risk profile below indicates that there is a 70%

chance that Wildcat will lose $70 million. Nevertheless, in oil exploration this is typically the situation that

you will face, i.e. high likelihood of losing money on a prospect, with a small change of making a lot of

profit, in this case up to $600 million (with a probability of 10%).

Exam Solution 8

Risk Profile

0%

20%

40%

60%

80%

100%

-200 -100 0 100 200 300 400 500 600 700

Value

Pro

bab

ilit

y

Drill

Do Not Drill

60% 36%

0 -70

60% Oil

0 85.5

25% 15%

220 150

15% 9%

670 600

TRUE Dome

-70 41

85% 34%

0 -70

40% Oil

0 -25.75

12.5% 5%

220 150

2.5% 1%

670 600

Drill

41

FALSE 0%

0 0

Wildcat

Yes

No

Yes

No

Dry

Wet

Soaking

Dry

Wet

Soaking

Exam Solution 9

Suppose that an oil-detector would be available that could detect whether the underground contained oil or

not (regardless of the presence of a dome structure) without drilling first, and that the detector would be able

to tell perfectly whether the well would be dry, wet or soaking.

(ii) (6 points) How valuable would this detector be for this project?

The expected value of the detector in this project would be $90 million (expected value of perfect

information about oil, EVPI-oil) - $41 million = $49 million.

Also, by using the detector, the risk profile would be radically changed, by completely eliminating the

downside. There is no chance that Wildcat would lose money on this prospect if they would have such a

detector (for free).

FALSE 0

-70 -70

70% Drill

0 0

TRUE 70%

0 0

Oil

90

TRUE 0.2

150 150

20% Drill

0 150

FALSE 0%

0 0

TRUE 0.1

600 600

10% Drill

0 600

FALSE 0%

0 0

Wildcat

Dry

Wet

Soaking

Yes

No

Yes

No

Yes

No

Risk Profile

0%

10%

20%

30%

40%

50%

60%

70%

80%

-100 0 100 200 300 400 500 600 700

Value

Pro

bab

ilit

y

Exam Solution 10

Unfortunately, such a detector does not (yet) exist. However, William Cooper suggested that Wildcat might

consider the possibility of taking a seismic test on the site before drilling. This test would cost $5 million.

The seismic test would give an estimate of the depth of the lime-shade formation, and hence give an

indication of the existence or non-existence of the dome structure.

(iii) (6 points) If you assume that the seismic test can detect the existence of a dome structure without

error, should Wildcat perform the seismic test first?

The decision tree below indicates that the test would increase the expected value of the prospect from $41 to

$46.3 million. The seismic test is therefore worth $10.3 million (expected value of perfect information about

the dome, EVPI-dome), $5.3 million more than its cost.

60% 36%

0 -75

TRUE Oil

-70 80.5

25% 15%

220 145

15% 9%

670 595

60% Drill

0 80.5

FALSE 0

0 -5

TRUE Dome

-5 46.3

85% 0%

0 -75

FALSE Oil

-70 -30.75

13% 0%

220 145

3% 0%

670 595

40% Drill

0 -5

TRUE 0.4

0 -5

Take Seismic Test

46.3

60% 0%

0 -70

60% Oil

0 85.5

25% 0%

220 150

15% 0%

670 600

TRUE Dome

-70 41

85% 0%

0 -70

40% Oil

0 -25.75

12.5% 0%

220 150

2.5% 0%

670 600

FALSE Drill

0 41

FALSE 0%

0 0

Wildcat

Yes

No

Yes

No

Yes

No

Dry

Wet

Soaking

Dry

Wet

Soaking

Yes

No

Yes

No

Dry

Wet

Soaking

Yes

No

Dry

Wet

Soaking

Exam Solution 11

Moreover, the test would also improve the risk profile. When taking the test, the probability of losing money

on the prospect is increased from 70% to 76%, but the probability of losing $70 million or more is reduced to

36%. Also, the upside is only slightly affected by the cost of the test. In conclusion, Wildcat should

definitely perform the seismic test first.

Unfortunately, the seismic test is not perfect. Sometimes intermediate layers of rock reflected the seismic

soundings sufficiently to give the impression of a dome when none is there, and sometimes soundings are

misinterpreted to say that no dome exists when in fact it does.

Cooper gave the following estimates of the reliability of the seismic test based on past experience:

When there was a dome present, the seismic test was positive (a dome was detected) in 90% of the

cases. However, in 10% of the cases the test mistakenly reported that there was no dome structure.

When there was not a dome present, the seismic test reported a dome structure to be present in 20%

of the cases while there was actually none (see Table 2.2).

Dome Structure Present No Dome Structure Present

Dome Detected 90% 20%

No Dome Detected 10% 80%

Table 2.2 Accuracy of seismic test

(iv) (6 points) Should Wildcat perform the seismic test at a cost of $5 million?

Using the Bayes rule (see below), we can derive the probability that the test would yield a positive result,

namely 62% (54% + 8%). Given a positive result, the probability that a dome will be present equals 87.1%

(54%/62%). Given a negative result, the probability that there indeed is no dome equals 84.2% (32%/38%).

Risk Profile

0%

10%

20%

30%

40%

50%

60%

70%

80%

-200 -100 0 100 200 300 400 500 600 700

Value

Pro

bab

ilit

y

1 : Yes

2 : No

Exam Solution 12

The decision tree shows that the expected profit of the prospect with the test (39.11 million) is less than

without it ($41 million). The value of the test is $3.11 million, substantially less than its cost ($5 million).

The risk profile does indicate, however, that the risk is reduced somewhat by the test, making the test more

interesting.

Dome (60%) No Dome (40%)

Positive (90%)

Negative (10%)

Negative (80%)

Positive (20%)

54%

32%

6%

8%

Dome (60%) No Dome (40%)Dome (60%) No Dome (40%)

Positive (90%)

Negative (10%)

Negative (80%)

Positive (20%)

54%

32%

6%

8%

Exam Solution 13

60% 0%

0 -75

87% Oil

0 80.5

25% 0%

220 145

15% 0%

670 595

TRUE Dome

-70 66.15

85% 0%

0 -75

13% Oil

0 -30.75

12.5% 0%

220 145

2.5% 0%

670 595

62% Drill

0 66.15

FALSE 0

0 -5

FALSE Test Results

-5 39.11

60% 0%

0 -75

16% Oil

0 80.5

25% 0%

220 145

15% 0%

670 595

FALSE Dome

-70 -13.18

85% 0%

0 -75

84% Oil

0 -30.75

12.5% 0%

220 145

2.5% 0%

670 595

38% Drill

0 -5.00

TRUE 0

0 -5.00

Take Seismic Test

41.0

Wildcat

Yes

Positive

Negative

Yes

No

Yes

No

Dry

Wet

Soaking

Dry

Wet

Soaking

Yes

No

Yes

No

Dry

Wet

Soaking

Dry

Wet

Soaking

Risk Profile

0%

10%

20%

30%

40%

50%

60%

70%

80%

-200 -100 0 100 200 300 400 500 600 700

Value

Pro

bab

ilit

y

Test

No Test